FEDERAL COURT OF AUSTRALIA

Controlled Thermal Resources Limited, in the matter of Controlled Thermal Resources Limited [2022] FCA 1292

ORDERS

IN THE MATTER OF CONTROLLED THERMAL RESOURCES LIMITED (ACN 166 638 142) | ||

CONTROLLED THERMAL RESOURCES LIMITED (ACN 166 638 142) Plaintiff | ||

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 411(1) of the Corporations Act 2001 (Cth) (Act), the Plaintiff convene a meeting (Scheme Meeting) of the holders of fully paid ordinary shares in the Plaintiff (Shareholders) for the purpose of considering and, if thought fit, agreeing (with or without modification) to a scheme of arrangement between the Plaintiff and the Shareholders in the terms set out in Tab 4 of Exhibit AJR1 to the Affidavit of Ashley Julian Rose sworn on 24 October 2022 (Scheme).

2. Pursuant to s 1319 of the Act:

(a) the Scheme Meeting be held on Tuesday, 22 November 2022 commencing at 9.00am (Brisbane time) in person at Tattersalls Club, 215 Queen Street, Brisbane City QLD 4000 and virtually through the online meeting platform at https://meetings.linkgroup.com/CTR22 (as to virtual access, the meeting to be accessed substantially in accordance with the instructions contained in the Notice of Scheme Meeting set out in Annexure E of the Scheme Booklet); and

(b) the Scheme Meeting be convened, held and conducted in accordance with the provisions of Part 2G.2 of the Act that apply to members of a company, and the provisions of the Plaintiff's constitution that are not inconsistent with the Act and these orders.

3. Pursuant to ss 411(1) and 1319 of the Act, the Scheme Meeting be convened by sending the following documents on or before Monday, 31 October 2022 to each Shareholder whose name is recorded in the Plaintiff's register of members as being a Shareholder as at 7.00pm (Brisbane time) on 27 October 2022:

(a) those Shareholders who have provided an email address to the Plaintiff for shareholder communications (Email Shareholders) are to be sent an email broadcast substantially in the form of Annexure A to these orders (Email Broadcast) providing electronic links by email to their nominated email address of the following:

(i) the Scheme Booklet (substantially in the form of Exhibit 2 tendered on 28 October 2022); and

(ii) a proxy form substantially in the form appearing in annexure DEA-2 to the Affidavit of Deborah Elsie Austin sworn on 26 October 2022 (Proxy Form);

(b) those Shareholders who have not provided an email address to the Plaintiff for shareholder communications, who have a postal address shown on the register of members of the Plaintiff as being within Australia are to be sent, by prepaid ordinary post to their postal address, a letter substantially in the form of Annexure B to these orders (Letter Notification) providing instructions on how to access the Scheme Booklet electronically, a Proxy Form and a reply-paid envelope;

(c) those Shareholders who have not provided an email address to the Plaintiff for shareholder communications and whose postal address is shown on the register of members of the Plaintiff as being outside Australia are to be sent the Letter Notification, a Proxy Form and an unstamped envelope return addressed to the Plaintiff's company registry by prepaid airmail to their postal address; and

(d) if the Plaintiff, through its share registry services provider, receives a notification that the Email Broadcast was unable to be delivered to the nominated email address of any of the Shareholders (Undelivered Email Recipients), the following are to be sent to the Undelivered Email Recipients' respective postal addresses:

(i) the Letter Notification, the Proxy Form and a reply-paid envelope are to be sent by pre-paid ordinary post (in the case of Shareholders within Australia); or

(ii) the Letter Notification, the Proxy Form and an unstamped envelope return addressed to the Plaintiff's company registry by pre-paid airmail (in the case of Shareholders outside Australia);

4. The Plaintiff cause a copy of the Scheme Booklet to be provided to any Shareholder if requested by that Shareholder.

5. Despatch of the Scheme Booklet be subject to the document's registration with the Australian Securities and Investments Commission (ASIC) pursuant to s 412(6) of the Act.

6. Pursuant to s 1319 of the Act:

(a) the Plaintiff may determine that, for the purposes of the Scheme Meeting, all of the shares in the Plaintiff be taken to be held by the person, persons or bodies corporate who held them as at 7:00pm (Brisbane time) on Sunday, 20 November 2022;

(b) the Plaintiff may determine that only the proxy forms in relation to the Scheme Meeting received by the Plaintiff by no later than 9:00am (Brisbane time) on Sunday, 20 November 2022 are valid;

(c) the Chairperson of the Scheme Meeting be David Douglas Jackson or in his absence, Kemsley John Cross;

(d) the Chairperson of the Scheme Meeting shall have the power to adjourn the meeting in their absolute discretion to such time, date and place as they consider appropriate; and

(e) a poll must be taken to decide the resolutions put to the vote at the Scheme Meeting, except for procedural motions.

7. The Plaintiff publish a Notice of Hearing in The Australian newspaper, in substantially the form that appears at Annexure C hereto, not later than 5 days prior to the date fixed for the hearing of any application to approve the Scheme, and the Plaintiff be relieved from compliance with rule 3.4 and Form 6 of the Federal Court (Corporations) Rules 2000 (Cth) to the extent necessary.

8. Rule 2.15 of the Rules shall not apply to the Scheme Meeting.

9. The proceedings be adjourned to 10:15am on Monday, 12 December 2022 before Justice Cheeseman for the hearing of any application to approve the Scheme.

10. The Plaintiff has liberty to apply.

11. These orders be entered forthwith.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A – EMAIL BROADCAST

Shareholder Number: [●]

Dear CTR Shareholder

On Friday, 28 October 2022, the Federal Court of Australia ordered that Controlled Thermal Resources Limited (CTR) convene a meeting (Scheme Meeting) of all its shareholders (CTR Shareholders) to consider and vote on a scheme of arrangement (Scheme) between CTR and CTR Shareholders in relation to the proposed re- domiciliation of CTR and each of its related bodies corporate, other than Controlled Thermal Resources Holdings Inc. (CTR US HoldCo), (CTR Group) from Australia to the United States.

Scheme Booklet

CTR would be pleased to provide you with a copy of the scheme booklet in connection with the Scheme (Scheme Booklet), which contains important information for your consideration about the Scheme and contains the Notice of Scheme Meeting.

To obtain a copy, you can telephone 1300 794 935 (within Australia) or +61 1300 794 935 (outside Australia) or click on the following link to view and download the Scheme Booklet (which includes the Notice of Meeting):

https://events.miraqle.com/CTRScheme

You should read the Scheme Booklet in full before you decide whether or not to vote in favour of the Scheme.

Details of the Scheme Meeting

You are invited to participate in the Scheme Meeting to be held at 9:00am (Brisbane time) on Tuesday, 22 November 2022.

The Scheme Meeting will be held as a hybrid meeting, providing an opportunity for CTR Shareholders to either attend in-person at Tattersalls Club, 215 Queen Street, Brisbane City QLD 4000 or participate virtually via the online platform at: https://meetings.linkgroup.com/CTR22

All CTR Shareholders registered on the CTR share register as at 7:00pm (Brisbane time) on Sunday, 20 November 2022 will be eligible to vote at the Scheme Meeting.

Further details on how to participate and vote in the Scheme Meeting, including how to access the online platform and attend the Scheme Meeting, are set out in the Notice of Scheme Meeting attached to the Scheme Booklet at Annexure E.

Lodge a proxy

If you would like to lodge your proxy online, please click on the link below and follow the instructions provided:

https://investorcentre.linkgroup.com/voting/ctr

Please note that proxies submitted online must be received no later than 9:00am (Brisbane time) on Sunday, 20 November 2022.

Further queries and support

For more information, please refer to the Scheme Booklet.

If you experience any issues accessing your voting screen(s), please contact Link Market Services on 1300 794 935 (within Australia) or +61 1300 794 935 (outside Australia).

David Jackson

Chair of Controlled Thermal Resources Limited

Do not reply to this email, as this email address is not monitored.

ANNEXURE B – LETTER NOTIFICATION

Shareholder Number: [●]

Dear CTR Shareholder

On Friday, 28 October 2022, the Federal Court of Australia ordered that Controlled Thermal Resources Limited (CTR) convene a meeting (Scheme Meeting) of all its shareholders (CTR Shareholders) to consider and vote on a scheme of arrangement (Scheme) between CTR and CTR Shareholders in relation to the proposed re- domiciliation of CTR and each of its related bodies corporate, other than Controlled Thermal Resources Holdings Inc. (CTR US HoldCo), (CTR Group) from Australia to the United States.

Scheme Booklet

CTR would be pleased to provide you with a copy of the scheme booklet in connection with the Scheme (Scheme Booklet), which contains important information for your consideration about the Scheme and contains the Notice of Scheme Meeting.

To obtain a copy, you can telephone 1300 794 935 (within Australia) or +61 1300 794 935 (outside Australia), or view and download the Scheme Booklet (which includes the Notice of Meeting):

https://events.miraqle.com/CTRScheme

You should read the Scheme Booklet in full before you decide whether or not to vote in favour of the Scheme.

Details of the Scheme Meeting

You are invited to participate in the Scheme Meeting to be held at 9:00am (Brisbane time) on Tuesday, 22 November 2022.

The Scheme Meeting will be held as a hybrid meeting, providing an opportunity for CTR Shareholders to either attend in-person at Tattersalls Club, 215 Queen Street, Brisbane City QLD 4000 or participate virtually via the online platform at: https://meetings.linkgroup.com/CTR22

All CTR Shareholders registered on the CTR share register as at 7:00pm (Brisbane time) on Sunday, 20 November 2022 will be eligible to vote at the Scheme Meeting.

Further details on how to participate and vote in the Scheme Meeting, including how to access the online platform and attend the Scheme Meeting, are set out in the Notice of Scheme Meeting attached to the Scheme Booklet at Annexure E.

Lodge a proxy

You can appoint a proxy by voting online or by completing and returning to Link Market Services the enclosed Proxy Form for the Scheme Meeting by one of the following methods:

1. Online at:

https://investorcentre.linkgroup.com/voting/ctr and following the instructions provided.

2. Mail:

(a) In Australia, using the reply-paid envelope (only for use in Australia) to: Link Market Services Limited

Locked Bag A14, Sydney South NSW 1235

(b) From outside of Australia, to:

C/- Link Market Services Limited

Locked Bag A14, Sydney South NSW 1235

Please note that proxies submitted online must be received no later than 9:00am (Brisbane time) on Sunday, 20 November 2022.

Further queries and support

For more information, please refer to the Scheme Booklet.

If you experience any issues accessing your voting screen(s), please contact Link Market Services on 1300 794 935 (within Australia) or +61 1300 794 935 (outside Australia).

David Jackson

Chair of Controlled Thermal Resources Limited

Do not reply to this email, as this email address is not monitored

ANNEXURE C – NOTICE OF HEARING TO APPROVE SCHEME OF ARRANGEMENT

To all the members of Controlled Thermal Resources Ltd ACN 166 638 142 (CTR).

Take notice that at 10:15am (AEDT) on Monday, 12 December 2022, the Federal Court of Australia at Law Courts Building, Queens Square Sydney, New South Wales 2000, will hear an application by CTR seeking approval of a scheme of arrangement between CTR and its members as proposed by a resolution to be considered and, if thought fit, passed by the meeting of the members of CTR to be held on Tuesday, 22 November 2022.

If you wish to oppose the approval of the scheme of arrangement, you must file and serve on CTR a notice of appearance, in the prescribed form, together with any affidavit on which you wish to rely at the hearing. The notice of appearance and affidavit must be served on CTR at its address for service at least one day before the date fixed for the hearing of the application.

CHEESEMAN J

INTRODUCTION

1 The plaintiff (CTR) has applied for orders under s 411(1) of the Corporations Act 2001 (Cth) for, inter alia, convening a meeting of its shareholders to consider a proposed Scheme of arrangement. CTR is an unlisted Australian public company and is the ultimate holding company of a group of companies (CTR Group) engaged in power and mineral production with a focus on lithium.

2 On 30 September 2022, CTR entered into a Scheme Implementation Deed (SID) with Controlled Thermal Resources Holdings Inc (CTR US HoldCo). CTR US HoldCo is a newly formed company, incorporated in Delaware, United Stated of America (USA), on or around 30 August 2022 for the specific purpose of becoming the United States holding company of the CTR Group. The Scheme is an arrangement under Part 5.1 of the Act by which it is proposed that CTR US HoldCo will acquire all of the issued shares in CTR in consideration of the shareholders of CTR being provided with all of the issued shares in CTR US HoldCo. In that way, it is proposed that CTR US HoldCo will become the parent entity of the CTR Group and CTR will become a wholly owned subsidiary of CTR US HoldCo, the new parent entity of the CTR Group.

3 The effect of the proposed Scheme, if implemented, will be to redomicile the CTR Group from Australia to the USA. The proposed scheme is a “tophatting” scheme where a new company, (CTR US HoldCo) is superimposed or tophatted over the scheme company (CTR) so that the scheme company becomes a subsidiary of the new company and the shareholders of the scheme company are divested of their shares in the scheme company and become shareholders in the new company.

BACKGROUND

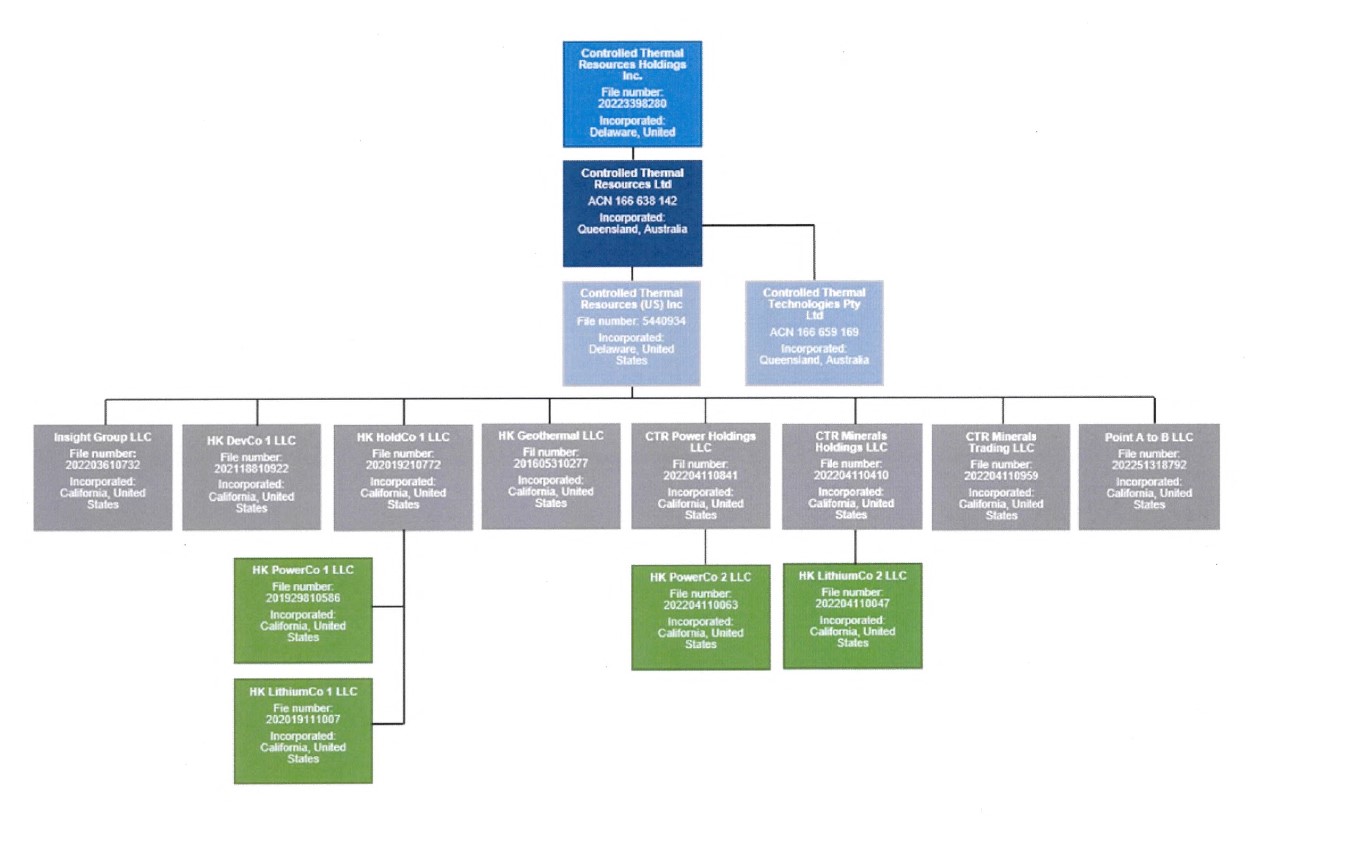

4 CTR is an Australian public company incorporated under the Act. CTR is the ultimate holding company of: 12 corporate entities incorporated under the laws of California; one entity incorporated under the laws of Delaware; and one Australian proprietary limited company incorporated in Queensland. Save for the one Australian proprietary limited company, all of the corporate entities ultimately controlled by CTR in the CTR Group are governed by the laws of the USA. Schedule 1 to these reasons is a diagram depicting the present structure of the CTR Group.

5 Under the existing structure, CTR is domiciled in Australia, with operations in California. Through its subsidiaries, CTR has interests in geothermal resource rights which are situated in California. Controlled Thermal Resources (US) Inc (incorporated in Delaware) (CTR US Inc) is a wholly owned subsidiary of CTR. CTR US Inc in turn owns all of the issued shares in HK Geothermal LLC (incorporated in the State of California, USA). HK Geothermal LLC holds leasehold rights in defined portions of the Salton Sea, California, which arise from a lease agreement between Imperial Irrigation District (as lessor) and HK Geothermal LLC (as lessee) dated 15 March 2016. In January 2020, CTR, through one of its wholly-owned subsidiaries, entered into a 25-year power purchase agreement with Imperial Irrigation District, the largest irrigation district in North America. Under that agreement, CTR is to supply the Imperial Irrigation District with geothermal energy from September 2023.

DESCRIPTION OF SCHEME

Top-hatting arrangement

6 As mentioned above, the Scheme has been developed for the purpose of redomiciling the CTR Group to Delaware. Schedule 2 to these reasons is a diagram depicting the structure of the CTR Group post implementation of the proposed scheme.

7 The reasons advanced by CTR for seeking to redomicile the CTR Group include:

(1) to align CTR Group's corporate structure with its business operations, given the majority of its assets, operational headquarters, management, staff, strategic partners and customer base are situated in North America;

(2) to better position CTR Group in a more appropriate capital market for continuing international growth, allowing existing CTR shareholders to benefit to the maximum extent possible from that growth and to be in a position to more clearly evaluate the performance and future prospects of CTR Group;

(3) in the event of an initial public offering (IPO) on a US securities exchange, to potentially increase demand for CTR Group's shares due to the possible inclusion of CTR Group in important US stock market indices such as the Russell 2000, Nasdaq Composite and the S&P Total Market;

(4) to provide access to a broader US investor pool that previously could not, or were unlikely to, invest in non-US securities; and

(5) to draw upon a securities market which is familiar with, and has a stronger interest in, early to mid-stage lithium exploration and development companies, which may lead to a stronger valuation of CTR Group over time and improve liquidity in CTR share trading.

8 The evidence of Mr Colwell, CTR Chief Executive Officer and Executive Director, demonstrates that:

(1) the majority of the CTR Group's assets, headquarters, management, staff, strategic partners and customer base are situated in North America;

(2) a majority of the CTR’s employees reside in the USA;

(3) the CTR’s key assets are situated in California; and

(4) the CTR’s key off-takers of lithium (respectively, Stellantis N.V. and General Motors Company) have substantial operations in the USA.

9 In their Independent Expert Report, the independent experts, Mr Adam Myers and Mr Sherif Andrawes, of BDO Corporate Finance (WA) Pty Ltd conclude that to redomicile the CTR Group to the USA is in the best interest of shareholders for the reasons substantially the same as those advanced by CTR. First, that implementation of the Scheme could potentially allow CTR access to new funds. Secondly, that political and economic conditions in the USA are favourable for lithium and renewable energy production. Thirdly, that redomiciling in the USA could increase the profile of CTR, better align its corporate structure with CTR’s key stakeholders and operating model, and make it generally easier to conduct business in the USA. Fourthly, the prospect of an IPO on a US securities exchange may result in a more favourable liquidation event for shareholders as compared to an Australian securities exchange. Against this, the experts weighed the implementations costs, potential exposure to increased litigation risk, changes to shareholder protections in Delaware as compared to under Australian law, and that any ineligible foreign holders would be cashed out and not receive shares in CTR US HoldCo as factors weighing against the Scheme. However, the experts concluded that the implementation of the Scheme is, on balance, in the interests of shareholders and that the advantages of the Scheme outweigh its disadvantages.

Scrip consideration

10 The Scheme is a scrip for scrip swap at an exchange rate of 1:1. Save for Ineligible Foreign Holders, CTR shareholders will be issued one common stock in CTR US HoldCo for each ordinary share they hold in CTR in consideration for the transfer of their ordinary shares to CTR US HoldCo. Ineligible Foreign Holders will receive monetary consideration for the transfer of their ordinary shares to CTR US HoldCo and not scrip consideration.

11 The reason for the different treatment of Ineligible Foreign Holders is that legal restrictions in some foreign countries may make it impractical or unlawful for CTR US HoldCo shares to be issued to the CTR shareholders in those countries. Scheme Participants whose address is shown in the CTR share register on the relevant date as being in a jurisdiction outside Australia, the United States, New Zealand, Switzerland and the United Kingdom, or from within a jurisdiction which CTR US HoldCo has determined, acting reasonably, is a place that it is unlawful or unduly onerous to issue the CTR US HoldCo Shares, or who are otherwise determined to be an Ineligible Foreign Holder, will be regarded as Ineligible Foreign Holders for the purposes of the Scheme, unless CTR US HoldCo determines that it is lawful and not duly onerous or impracticable to issue CTR US HoldCo Shares in that jurisdiction if the Scheme becomes effective.

12 The SID provides in relation to Ineligible Foreign Holders that CTR US HoldCo will:

(1) issue shares that Ineligible Foreign Holders would otherwise be entitled to (but for their status as Ineligible Foreign Holders) to a Sale Agent appointed by CTR US HoldCo;

(2) instruct the Sale Agent to act on behalf of all Ineligible Foreign Holders, and to sell all CTR US HoldCo shares issued to the Sale Agent as soon as reasonably practicable after the implementation date of the Scheme at such price and on such terms as the Sale Agent determines in good faith; and

(3) remit to the Ineligible Foreign Holders the proceeds from the sale of the Sale Agent's CTR US HoldCo shares in Australian dollars pari passu on the basis of each Ineligible Foreign Holders' proportionate entitlement.

13 In the present case, there may not be any Ineligible Foreign Holders in any event. As at close of business on 24 October 2022, of the 117 shareholders noted on CTR’s share registry as being outside Australia, they were all noted in the share registry to be situated in the USA, New Zealand, Switzerland or the United Kingdom and accordingly, they are not Ineligible Foreign Holders. The Scheme Booklet includes a statement that as at the date of the Scheme Booklet, there are no Ineligible Foreign Holders.

Cancellation of CTR Performance Rights and CTR Indeterminate Rights

14 CTR has on issue to Isdell Pty Ltd as trustee for the JIB Trust:

(1) 50,000 Performance Rights; and

(2) an indeterminate number of Indeterminate Rights,

(collectively, the CTR Rights).

15 The CTR Rights arise from two offer letters dated 28 April 2020. The Performance Rights have not been exercised. At the first court hearing, CTR tendered an undertaking on behalf of the holder of the Performance Rights that the Performance Rights would not be exercised prior to the implementation date. Prior to the exercise of the Performance Rights, persons eligible to exercise Performance Rights are not entitled to vote or attend any meeting of shareholders or receive dividends declared by CTR. The Indeterminate Rights have not vested.

16 In order to deal with the CTR Rights in the Scheme, CTR has negotiated the following arrangements:

(1) CTR, CTR US HoldCo and Isdell have executed the Rights Exchange Agreement;

(2) Isdell has executed the Performance-Based Stock Option Award Agreement with CTR US HoldCo; and

(3) Isdell has executed an Indeterminate Stock Option Award Agreement with CTR US HoldCo,

(collectively, the CTR Rights US Agreements).

17 The CTR Rights US Agreements collectively have the effect that any rights of Isdell with respect to CTR will roll over to become rights against CTR US HoldCo if the Scheme is implemented.

CTR’s directors interests

18 Direct and indirect shareholdings of the CTR’s directors in the CTR are disclosed in the Scheme Booklet as a numerical value and as a percentage of total issued share capital in CTR. Mr Colwell holds 248,707,983 CTR Shares (47.7%) indirectly through L & A Management Services Pty Ltd. Mr James Turner holds 216,429 CTR Shares (0.04%) jointly with Ms Turner. Mr David Jackson holds 876,355 CTR Shares (0.17%) indirectly through KPSF Pty Ltd ATF The Jackson Family Super Fund and Keystone Private Wealth Pty Ltd. Mr Kemsley Cross holds 20,710,784 CTR Shares (3.97%) indirectly through KJ & M Cross Pty Ltd ATF the Cross Family Super Fund. Finally, Mr Nicholas Cavanagh holds 41,595,218 CTR Shares (7.98%) indirectly through Cavanagh Bros Project Management Pty Ltd ATF the Cavanagh Bros Directors Trust and Bashley Pty Ltd as trustee for Cav's Superannuation Fund. This accounts for 312,106,769 shares, being 59.86% of total issued share capital in CTR.

19 L & A Management has pre-emptive rights under rule 26 of CTR’s constitution. However, L&A Management has agreed to waive those rights in return for equivalent rights being granted to L & A Management in CTR US HoldCo.

20 The Australian Securities and Investments Commission (ASIC) is aware of L & A Management’s percentage of proportional shareholding in CTR and the waiver of pre-emptive rights and has not raised any concerns or queries during the process of reviewing the Scheme Booklet that has occurred in advance of the first court hearing.

21 CTR submits that L & A Management, Rodney Colwell, and Nicole Colwell will not receive any other benefits from the approval of the Scheme.

Scheme is recommended by CTR directors

22 The CTR directors have unanimously recommended that, in the absence of a superior proposal, CTR shareholders vote in favour of the proposed scheme at the Scheme meeting.

Independent experts’ conclusion that the proposed scheme is in the bests interests of CTR’s shareholders

23 As noted above, the independent experts appointed by the CTR’s board to assess the Scheme have concluded that on balance and considering the Shareholders’ interests as a whole, the advantages of the Scheme outweigh its disadvantages and accordingly the Scheme is in the best interests of shareholders as a whole in the absence of an alternative proposal or any further information. Mr Colwell provides evidence of the steps taken by CTR to verify that the factual statements provided to BDO, and contained in the Independent Expert Report, are factually correct and not misleading or deceptive. A copy of the Independent Expert Report is annexed to the Scheme Booklet.

APPLICABLE PRINCIPLES

24 Part 5.1 of the Act provides a procedure whereby an arrangement between a company and its members can be made binding on all members. Section 411 is the principal provision. The procedure involves three main steps:

(1) an application to the Court for an order to convene a scheme meeting;

(2) if such an order is made, the convening of a meeting at which a resolution to agree to the scheme is considered, and perhaps passed; and

(3) if the resolution is passed by the necessary majorities, an application to the Court for approval of the scheme.

25 This application concerns the first stage, being an application to the Court for an order to convene the Scheme meeting.

26 Courts have commonly applied the approach described by Street J (with whom Hutley and Samuels JJA agreed) in FT Eastment & Sons Pty Ltd v Metal Roof Decking Supplies Pty Ltd (1977) 3 ACLR 69 at 72 in deciding whether to convene a scheme meeting (including in respect of a scheme between a company and its members):

…The approach taken upon a summons is that the court will not ordinarily summon a meeting unless the scheme is of such a nature and cast in such terms that, if it achieves the statutory majority at the creditors’ meeting the court would be likely to approve it on the hearing of a petition which is unopposed…

27 Section 411 of the Act does not state the criteria that must be satisfied before a scheme meeting is ordered, but it is clear that, if certain statutory pre-requisites are met, s 411(1) confers a discretion on the court in relation to whether the scheme meeting should be ordered: see, for example, Re Healthscope Limited [2019] FCA 542; 139 ACSR 608 at [43]; Re Amcor Limited [2019] FCA 346 at [45]; Re DuluxGroup Limited [2019] FCA 961; 136 ACSR 546 at [15]; Re Legend Corporation Limited [2019] FCA 1249 at [17]; Re Wellcom Group Limited [2019] FCA 1655 at [24]; Re Verdant Minerals Limited [2019] FCA 556 at [28], citing Re CSR Limited [2010] FCAFC 34; 183 FCR 358 at [8]; and Re Sienna Cancer Diagnostics Limited [2020] FCA 899 at [43].

28 The principles which apply at this first stage of the scheme of arrangement procedure are well-known and have recently been summarised by Beach J in a number of decisions including Re PM Capital Asian Opportunities Fund Limited [2021] FCA 1380 at [39] to [40]:

39 …my function on an application to order the convening of a meeting is supervisory. At this stage I should generally confine myself to ensuring that certain procedural and substantive requirements have been met including dealing with adequate disclosure, but with limited consideration of issues of fairness. But having said that, it is appropriate to consider the merits or fairness of a proposed scheme at the convening hearing if the issue is such as would unquestionably lead to a refusal to approve a proposed scheme at the approval hearing, that is, the proposed scheme appears now to be on its face “so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further” (Re Foundation Healthcare Ltd (2002) 42 ACSR 252 at [44] per French J).

40 Clearly, my role is not to usurp the shareholders’ decision whether to agree to a scheme by attempting to intrude my own commercial judgment. The question whether to accept particular consideration for shares is a commercial matter for the members to assess, and they ought not to be prevented from having the opportunity to do so provided that I am satisfied that they are acting on sufficient information and with time to consider what they are voting on. If the arrangement is one that seems fit for consideration by the meeting of members and is a commercial proposition likely to gain my approval if passed by the requisite majorities, then orders should be made to convene the meeting.

29 The relevant discretionary considerations are primarily whether the scheme is fit for consideration by the members (such that if agreed to at the scheme meeting, it would be likely to be approved if unopposed at the second court hearing) and whether the members are properly informed of the nature of the scheme: Re PM Capital at [43].

30 In considering whether the Scheme is fit for consideration by shareholders, it is not necessary for the Court to be satisfied that no better scheme could have been proposed: Re Foundation Healthcare Ltd [2002] FCA 742; 42 ACSR 252 at [44]. By granting leave, the Court does not give its imprimatur to the proposed scheme: Re Capilano Honey Ltd [2018] FCA 1568; 131 ACSR 9 at [33].

CONSIDERATION

Statutory conditions

31 I turn first to consider whether CTR has met the statutory conditions necessary to enliven the discretion under s 411(1) of the Act.

32 On the evidence before me, I am satisfied that each of the necessary statutory conditions has been met by CTR.

33 First, the proposed Scheme is an arrangement in respect of which the Court may order a meeting of the members pursuant to s 411(1) of the Act. I am satisfied that the Scheme is an arrangement – it is well accepted that the use of a members’ scheme of arrangement to effect redomiciliation is within the scope of an ‘arrangement’ within the meaning of s 411 of the Act: Re Avita Medical Limited, in the matter of Avita Medical Limited (No 2) [2020] FCA 674 at [7]. CTR is a company registered under the Act and is within the definition of a Part 5.1 body. The Scheme participants are members of CTR. Details of CTR’s corporate constitution, and its issued share capital, number of shareholders and location of shareholders are in evidence. In accordance with r 2.4(2) of the Federal Court (Corporations) Rules 2000 (Cth) (Corporations Rules), CTR has in its evidence included an ASIC company extract recording search results carried out no earlier than 7 days before the originating process was filed.

34 Secondly, ASIC has had a reasonable opportunity to examine the terms of the Scheme and the Scheme Booklet and make submissions to the Court in relation to those matters as required by s 411(2)(b) of the Act. A draft of the Scheme Booklet was lodged with ASIC on 30 September 2022. On 13 October 2022, ASIC advised that it had no further comments in relation to the Scheme Booklet, but requested that CTR provide further information in relation to material to be relied upon at the first court hearing before it would be in a position to consider issuing a preliminary letter as to its intention under s 411(17)(b) of the Act. At the first hearing, counsel for CTR tendered a letter from ASIC dated 27 October 2022 in which ASIC confirmed that it does not propose to appear at the first court hearing. On the basis of the evidence before me, I am satisfied that ss 411(2)(a) and (b) of the Act have been met.

35 Thirdly, the Scheme Booklet provides disclosure in accordance with s 412(1)(a)(i) of the Act and contains the prescribed information in s 412(1)(a)(ii) of the Act, regulation 5.1.01 and clauses 8301 to 8310 of Schedule 8 to the Corporations Regulations 2001 (Cth). I am satisfied that the Scheme Booklet is presented in a form that is intelligible to reasonable shareholders to whom it is directed, and contains information that is realistically useful relative to the complexity of the proposal: Re HIH Casualty and General Insurance Ltd [2006] NSWSC 485; 200 FLR 243 at [81] to[83].

36 The Scheme Booklet explains the effect of, relevantly, the arrangement, and in particular states the material interests of the directors, and the effect on those interests of the Scheme so far as it is different from the effect on the like interests of other persons. The effect of the Scheme on CTR shareholders is addressed in section 2.6, and the interest of CTR’s directors is addressed in section 13.1 of the Scheme Booklet.

37 The process by which the statements in the Scheme Booklet have been verified by CTR’s due diligence committee indicates that reasonable steps have been taken to confirm that the statements in the Scheme Booklet are accurate, not misleading or deceptive, and that material information has not been omitted, see regulation 5.1.01 and Schedule 8 of the Regulations. The Scheme Booklet includes information relevant to deciding whether or not to agree to, relevantly, the arrangement in sections 3, 4, 7, 10, 11, and Annexure A (being the Independent Expert Report).

38 It is necessary for the Scheme Booklet to be registered by ASIC before being sent to CTR shareholders: s 412(6) of the Act. Before registering the Scheme Booklet, ASIC must conclude that it appears to comply with the requirements of the Act, and must form the opinion that the Scheme Booklet does not contain any matter that is false in a material particular or materially misleading in the form and context where it appears: ss 412(7) and 412(8) of the Act. These requirements in relation to registration of the Scheme Booklet provide protection in relation to the adequacy of disclosure contained therein.

39 The procedural requirements of the Corporations Rules have been met. In accordance with r 3.2 of the Corporations Rules, evidence about the proposed chair and alternate chair has been provided. The proposed chair is David Jackson, the current chairperson and an independent non-executive director of CTR. The alternate chair is Kemsley John Cross, the chief executive officer and an executive director of CTR.

40 On the evidence before me on this application, there is no apparent reason why the Scheme should not receive the Court’s approval at the second court hearing, if unopposed and subject to the necessary majorities being achieved at the shareholders’ meeting.

41 At the first court hearing, a submission was made that the assets supporting the value of CTR shares are the same assets that will support the value of the shares in CTR US HoldCo and the value of the original shares and the replacement shares is constant before and after the Scheme implementation. However, if any capital or debt raising is undertaken before the Implementation Date which impacts on the correspondence of value in the scrip for scrip consideration, that is a matter which will be addressed at the second court hearing.

Discretion

42 Being satisfied that the statutory conditions are met, I now move to consider the relevant discretionary considerations. First, whether the Scheme is fit for consideration by the shareholders, and secondly, whether the members are to be properly informed as to the nature of the scheme.

The Scheme is fit for consideration

43 I am satisfied that the proposed Scheme is bona fide and properly proposed. That CTR has committed itself to propounding the Scheme and that the Scheme is unanimously recommended by CTR’s directors are indicia of the Scheme being bona fide. Moreover, the conclusion of the independent experts is that the advantages of the Scheme outweigh the disadvantages, and that the Scheme is in the best interests of shareholders as a whole in the absence of any alternative proposal.

44 Consistently with the duty of disclosure which falls on CTR, there are a number of matters which CTR brought to the Court’s attention: Re Permanent Trustee Company Limited [2002] NSWSC 1177; 43 ACSR 601 at [7]. None of the matters raised are such that the discretion should not be exercised in favour of convening the Scheme meeting so that CTR’s shareholders can consider and vote on the Scheme.

The CTR shareholders form a single class

45 The first issue raised is whether the CTR shareholders form a single class for the purpose of convening and holding the Scheme meeting to consider the Scheme. The particular issue that CTR raises is whether the CTR Rights give rise to a separate class of CTR shareholders for the purpose of the Scheme meeting.

46 CTR proposes orders for the convening of a single meeting of CTR shareholders.

47 In URB Investments Limited, in the matter of URB Investments Limited [2019] FCA 1977 at [44] to [46], Markovic J summarised the applicable principles in relation to the identification of separate classes as follows:

44 In David Jones (No 2) at [33] Farrell J noted that the second court hearing is the time for the court to determine whether or not a collateral benefit has been received and, if so, its relevance to the court’s discretion to approve the scheme, having regard to the voting at the scheme meeting and the disclosure provided. However, where one or more members of a target receive a net benefit, in addition to full and frank disclosure of the benefit, a related issue arises as to whether it is appropriate for those members to be placed into a separate class. That is an issue properly addressed at the first court hearing: see First Pacific Advisors LLC v Boart Longyear Ltd (2017) 320 FCR 78; [2017] NSWCA 116 at [40]-[41].

45 In Sovereign Life Assurance Company v Dodd [1892] 2 QB 573 at 583 Bowen LJ set out the test for identifying a class for scheme of arrangement purposes as follows:

It seems plain that we must give such a meaning to the term ‘class’ as will prevent the section being so worked as to result in confiscation and injustice, and that it must be confined to those persons whose rights are not so dissimilar as to make it impossible for them to consult together with a view to their common interest.

46 In Perpetual Custodians Ltd (as custodian for Tamoran Pty Ltd as trustee for Crivelli) v IOOF Investment Management Ltd (2013) 304 ALR 436; [2013] NSWCA 231 at [51], Leeming JA (with whom McColl and Gleeson JJA agreed) said:

Fourth, the legislation has long contemplated meetings of classes of members. The point of requiring members to vote in separate classes is to ensure that members can consult so as to determine their common interest. That is what drives class definition. Where the interests of members are so different as to make it impossible for them to consult with other shareholders, separate classes may be required: Sovereign Life Assurance Co v Dodd [1892] 2 QB 573 at 583 (Sovereign Life Assurance) per Bowen LJ; Re NRMA Ltd (2000) 33 ACSR 595 ; [2000] NSWSC 82 at [76] per Santow J; Re Cashcard Australia Ltd (2004) 48 ACSR 738 ; [2004] FCA 223 at [5] per Jacobson J; Re Sino Gold Mining Ltd (2009) 74 ACSR 647 ; [2009] FCA 1277 at [52]–[57] per Lindgren J. As Barrett J said in Hills Motorway at [12] after referring to the statements by Lord Esher MR and Bowen LJ in Sovereign Life Assurance:

[12] The test is thus not one of identical treatment. It is one of community of interest. The court must ask itself whether the rights and entitlements of the different groups, viewed in the totality of the scheme’s context, are so dissimilar as to make it impossible for them to consult together with a view to their common interest. The focus is not on the fact of differentiation but on its effects. The extent and nature of the differentiation must be measured in terms of the effect on the ability to consult together in a common interest or, in other words, the ability to come together in a single meeting and to debate the question of what is good or bad for the constituency as a whole and where the common good lies. Only if the differentiation destroys that ability — the word used by Bowen LJ is “impossible” — does class distinction come to prevail.

48 The test must be applied with some rigour to avoid too readily identifying separate classes and thereby creating unfairness by giving one group an effective veto: Re Opes Prime Stockbroking Ltd (No 2) [2009] FCA 813; 179 FCR 20 at [66]. As Santow J observed in Re NRMA Ltd (No 1)[2000] NSWSC 82; 33 ACSR 595 at [80]:

The ‘shifting’ or ‘fracturing’ of classes into smaller groups can undermine the objective of obtaining decision by a large majority, by giving one group an effective veto over the wishes of the majority. That itself can be oppressive…

49 CTR submits that it is appropriate to treat all CTR shareholders as one class for the Scheme meeting and voting purposes, and there is no reason for the Court to intervene in respect of the contractual arrangements that have been made in respect of the CTR Rights. The holders of CTR Rights have entered into contractual arrangements contingent on implementation of the Scheme, which have the effect of transferring those rights to the new environment produced by redomiciling the ultimate holding company of the CTR Group. The holders of the CTR Rights do not seek any orders in respect of those rights. An undertaking has been given not to exercise the Performance Rights prior to the implementation of the Scheme. The Indeterminate Rights have not vested. The holders of the Performance Rights and the Indeterminate Rights do not presently have rights as members of CTR as a result of the CTR Rights. The contractual arrangements put in place to, in effect, roll-over the CTR Rights to CTR US HoldCo are subject to the Scheme being implemented and are disclosed in the Scheme Booklet. In circumstances where the holders of CTR Rights do not exercise any voting rights in respect of those rights and their pre-existing contractual rights are being rolled over to the new environment if, and only if, the Scheme is implemented, I do not see that there is any need for the creation of a separate class in respect of such rights holders to the extent that they may also be shareholders.

Provisions of the Scheme

50 The Scheme is annexed to the Scheme Booklet and is in evidence.

Ineligible Foreign Shareholders

51 The sale mechanism and consequent treatment of Ineligible Foreign Holders is adequately disclosed. It is similar to that considered to be appropriate in a number of cases: Re Hills Motorway Ltd [2002] NSWSC 897; 43 ACSR 101 at [9] to [13]; Re Orica Ltd [2010] VSC 231 at [14]; and Re Amcor Limited [2019] FCA 346 at [41].

Conditions Precedent

52 The Scheme is subject to the conditions precedent in clause 3.1, including Court approval and lodgement of the Court orders with ASIC. These conditions precedent need to be satisfied or waived prior to 8:00 am AEDT, 12 December 2022, being the second court hearing date, so that the Scheme will be self-executing upon the making of orders at the second court hearing and the registration of those orders with ASIC.

Completion Risk

53 CTR US HoldCo is not a party to the Scheme but has executed a Deed Poll in favour of the Scheme participants. The executed Deed Poll dated 30 September 2022 is in evidence on this application. The Deed Poll enables the Scheme participants to directly enforce the obligations in respect of the provision of the consideration for the transfer of their ordinary shares in CTR. The Deed Poll is governed by the laws of New South Wales. CTR submits, and I accept, that the performance risk has been adequately mitigated by the Deed Poll.

Securities Act 1933 (US)

54 CTR and CTR US Inc intend to rely on the Court’s approval of the Scheme (if given at the second hearing) for the purposes of qualifying for the exemption under s 3(a)(10) of the Securities Act of 1933 (US) (US Securities Act) from US registration/prospectus requirements in connection with the implementation of the Scheme. This issue is addressed in the Scheme Booklet as follows:

The CTR US HoldCo Shares have not been registered under the US Securities Act or the securities laws of any state or other jurisdiction of the United States. Instead, CTR US HoldCo intends to rely on an exemption from the registration requirements of the US Securities Act provided by Section 3(a)(10) of the US Securities Act in connection with the consummation of the Scheme and the issuance of CTR US HoldCo Shares. Section 3(a)(10) exempts securities issued in exchange for other securities from the general requirement of registration where the terms and conditions of the issuance and exchange have been approved by any court of competent jurisdiction, after a hearing upon the fairness of the terms and conditions of the issuance at which all persons to whom the securities will be issued have the right to appear. Approval of the Scheme by the Court will be relied upon by the Company and CTR US HoldCo for purposes of qualifying for the section 3(a)(10) exemption.

55 An issue along similar lines was considered by Beach J in Re Amcor Limited (No 2) [2019] FCA 842 at [32] to [38] and described (at [33]) as “common practice in schemes of arrangement”. It is an issue which the Court will consider at the second court hearing.

56 For present purposes, it is sufficient to note that CTR and CTR US HoldCo intend to rely on the second court hearing as the relevant hearing at which the fairness and reasonableness of the Scheme was considered by a court for the purposes of applying for an exemption under s 3(a)(10) of the US Securities Act and that this has been disclosed in the Scheme Booklet. At the second court hearing, the Court must be sufficiently informed of the manner in which the scheme consideration will be calculated in order to determine the value of the securities to be offered and surrendered. The second court hearing will be open to everyone to whom the securities would be issued so that those to whom the new securities are to be issued have had opportunity to oppose or otherwise raise any objection to the Scheme. The matter, having been raised, will be deferred for consideration at the second court hearing.

Absence of any deal protection provisions

57 For completeness, I note that, as a tophatting scheme, the Scheme does not involve a real change of control. The proposed recipient of the CTR shares is an entity created for the purpose of receiving those shares and issuing new shares in itself to the CTR shareholders. In this way, although there will be a formal change of control of the CTR Group from CTR to CTR US HoldCo, the transaction is essentially the replacement of the current Australian holding company owned by the CTR shareholders with a US holding company substantially owned by the same shareholders (except for any Ineligible Foreign Holders, who will be cashed out). Accordingly, there are no deal protections, such as break fees or exclusivity provisions, included in the SID.

Court approval of the Scheme Booklet

58 At the first court hearing CTR originally sought an order that the Court approve the Scheme Booklet. In supplementary written submissions, CTR highlighted a divergence in the practice of courts as to whether, when making an order to convene a meeting under s 411(1), the Court will also make an order approving the explanatory statement: Re Duluxgroup Ltd [2019] FCA 961 at [63]; Re Sienna Cancer Diagnostics Limited [2020] FCA 899 at [98]; and Re Redflex Holdings Ltd [2021] FCA 417 at [50]. While I am satisfied that s 411(1) authorises the making of such an order, having regard to the fact that ASIC has not yet registered the Scheme Booklet under s 411(6) and before it does so, is obliged under s 411(8) to satisfy itself that the statement complies with the Act and the Regulations and is not misleading, I indicated that I was not inclined to make an order approving the explanatory statement given the registration process mandated by s 411 of the Act. In the circumstances, CTR did not press for an order that the Court approve the Scheme Booklet.

Proposed orders for convening Scheme meeting

59 CTR proposed ancillary orders under s 1319, including for the convening and conduct of the Scheme meeting, for the appointment of a chair and alternate chair and for publication of a notice of the second court hearing in The Australian newspaper. I made orders substantially in the form sought.

60 The orders distinguished between shareholders who (1) have provided an email address to CTR for shareholder communications, and (2) shareholders who have not provided an email address to the company for that purpose. As regards the former group, CTR proposes to provide an email broadcast giving notice of the Scheme meeting, with links to access the Scheme Booklet and the proxy form electronically, and explaining how to participate in the meeting. In relation to the latter group, CTR proposes to send a letter by post that provides notice of the meeting, includes the details of how to participate in the meeting (either by registering to join the meeting through a third party online platform, or in person), explains how to lodge a proxy vote, and encloses a physical proxy form. In both cases, the communication to shareholders will inform the shareholder that a physical copy of the Scheme Booklet is available and will be sent to the shareholder upon request.

CONCLUSION

61 For these reasons, at the first court hearing I made orders substantially in the form sought by CTR.

I certify that the preceding sixty-one (61) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Cheeseman. |

Associate:

SCHEDULE 1

SCHEDULE 2