FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Commonwealth Bank of Australia [2022] FCA 1149

ORDERS

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | ||

AND: | COMMONWEALTH BANK OF AUSTRALIA (ACN 123 123 124) First Defendant COLONIAL FIRST STATE INVESTMENTS LTD (ACN 002 348 352) Second Defendant | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The proceeding be dismissed.

2. The Plaintiff will pay the First and Second Defendants’ costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REASONS FOR JUDGMENT

ANDERSON J:

1 This proceeding concerns the application of the “conflicted remuneration” provisions found in ss 963A, 963E, 963L and 963K of the Corporations Act 2001 (Cth) (Act) to certain alleged “benefits” provided by the Second Defendant, Colonial First State Investments Limited (CFSIL) to the First Defendant, Commonwealth Bank of Australia (CBA) relating to the distribution of CBA’s “MySuper” superannuation product, called Essential Super (Essential Super)..

2 In broad terms, the Plaintiff, Australian Securities and Investments Commission (ASIC) alleges that, during the period 1 July 2013 to 30 June 2019 (Relevant Period), CFSIL gave, and CBA accepted, monetary and/or non-monetary benefits which could reasonably be expected to influence financial product advice provided by CBA to its retail clients in relation to Essential Super. These benefits are said to comprise:

(a) choses in action pursuant to certain written agreements CBA and CFSIL entered into with respect to Essential Super distribution agreements (the Promises);

(b) cash transfers from CFSIL to CBA (the Cash Transfers);

(c) journal entries, totalling $55,723,946.65 in respect of Essential Super in the management accounts of the CBA Group (the Journal Entries);

(each an Impugned Benefit, and collectively, Impugned Benefits).

3 ASIC alleges that CBA contravened the prohibition against a financial services licensee accepting conflicted remuneration pursuant to s 963E of the Act. ASIC further alleges that CFSIL breached the prohibition on product issuers or sellers giving conflicted remuneration pursuant to s 963K of the Act.

4 CFSIL is a wholly owned subsidiary of CBA and is an entity within the Commonwealth Bank of Australia group (CBA Group).

5 ASIC relies on the same facts and circumstances to establish its case against CBA and CFSIL.

6 At trial, CFSIL relied upon the evidence tendered by CBA and adopted the submissions advanced by CBA, but made additional submissions on the proper construction of the conflicted remuneration provisions.

7 ASIC’s case may be summarised as follows.

8 CFSIL was the issuer of Essential Super, which was launched for distribution in the retail bank branches and online channels of CBA on 1 July 2013.

9 CBA and CFSIL entered into a written agreement on 27 June 2013 (2013 Distribution Agreement) with respect to Essential Super, for an initial five year term. Under the 2013 Distribution Agreement, CBA was obliged to provide services to CFSIL; and in return CBA was entitled to a payment of 30% of the total net revenue derived by CFSIL from Essential Super in each financial year. ASIC alleges that CBA and CFSIL subsequently entered into two further written agreements, one on 2 June 2015 (2015 Distribution Agreement) and another on 26 February 2018 (2018 Distribution Agreement) (collectively, Distribution Agreements). The Promises consisted of this arrangement to pay 30% of the total net revenue of the Essential Super Fund to CBA in consideration for the services CBA was providing under the Distribution Agreements.

10 ASIC alleges that from 1 July 2013 to 8 October 2017, Essential Super was sold in CBA retail branches to individuals and small business employers as a default fund for employees who did not choose a superannuation fund. CBA trained its retail branch staff to sell Essential Super in accordance with ASIC’s Regulatory Guide: “RG146 Licensing: Training of financial product advisers”. ASIC alleges that staff who had completed the training were authorised to provide general advice to customers about Essential Super. Staff who were not authorised to provide such advice were not permitted to sell Essential Super, but were trained to do a “warm handover” to authorised staff of customers that were potentially interested in Essential Super.

11 ASIC alleges that from 1 July 2013 to 3 July 2018, Essential Super was also available to individuals and small business employers via an online application process established by CBA. In addition, between September 2014 and August 2016, a number of individuals became members of Essential Super due to the transfer of “accrued default amounts” from the Colonial First State FirstChoice Superannuation Trust to Essential Super.

12 ASIC alleges that CFSIL derived revenue from Essential Super once an Essential Super account was opened and funds were placed in it (Funded Essential Super Accounts). The revenue comprised three elements:

(a) a fixed monthly member fee;

(b) a management/administration fee based on a percentage of funds under management; and

(c) an insurance administration fee calculated as 7.5% of premiums for insurance held by members through Essential Super.

13 ASIC alleges that the Cash Transfers, which comprised nine cash payments totalling $22,767,481.61, were made by CFSIL to CBA with respect to Essential Super, with the first payment being made on 31 July 2014 and the remainder in the 2019 financial year. In addition, the Journal Entries, which comprised 26 journal entries totalling $55,723,946.65, were posted in the CBA general ledger with respect to Essential Super in each of the 2014 to 2019 financial years.

14 ASIC alleges that, through these arrangements and resulting payments and journal entries, CFSIL gave, and CBA accepted, conflicted remuneration in contravention of the prohibitions within Division 4 of Part 7.7A of the Act.

15 CBA denies that it breached the conflicted remuneration prohibition in the Act. CBA’s defence to ASIC’s allegations may be summarised as follows.

16 CBA contends that the central issue in dispute in these proceedings is whether the nature of the alleged Impugned Benefits, and the circumstances in which they arose, could reasonably have been expected to influence either the choice of financial product recommended by CBA to its customers or the financial product advice that CBA gave to its customers.

17 CBA contends that the context and relevant circumstances in which the alleged Impugned Benefits arose are of critical importance, and include the following.

18 In 2000, CBA acquired Colonial Limited, the parent company of CFSIL, for substantial consideration in the order of $9.274 billion.

19 A significant purpose of that acquisition was to combine the capability, skill and strength of CFSIL in manufacturing and managing superannuation fund products and the ability of CBA to use its existing distribution network to distribute such products.

20 In 2012, the Commonwealth Parliament, through the introduction of “Stronger Super” legislative reforms (MySuper Reforms) created a market for a new, simple superannuation product in the form of MySuper that would apply with legislative force to around 60% of superannuation fund members.

21 CFSIL had the skill and capability to manufacture a MySuper product that would comply with the legislative requirements and be of benefit to the customers of CBA.

22 At all relevant times, Essential Super was the only CBA-branded MySuper Product that CFSIL manufactured and the only such product that CBA distributed.

23 Competitors of the CBA Group were also distributing MySuper products, including products those competitors had manufactured.

24 At all relevant times, the Impugned Benefits were not known to those who were distributing Essential Super.

25 When confronted with the legislative requirement and commercial opportunity to manufacture and distribute a MySuper product, CBA took the view that it was imperative that the CBA Group develop and produce such a product. The Retail Banking Services (RBS) and Wealth Management business units (Wealth Management) of CBA agreed to jointly develop the Essential Super product, which was to be manufactured by the entity within the CBA Group capable of doing so, being CFSIL. The Essential Super product was then distributed by the entity in the CBA Group best placed to do so, being CBA. Essential Super was endorsed by the Executive Committee of the CBA Group on 4 May 2012 on the basis that costs incurred and revenue earned would be shared between the two business units/legal entities on an appropriate basis.

26 CBA contends that against this background, the alleged “Impugned Benefits” were, in truth, no more than standard intragroup accounting allocations to support or reflect a sharing of costs and revenues between the two business units and the two associated legal entities that were responsible for the MySuper product.

27 CBA contends that from these circumstances alone, it follows that the nature of the Impugned Benefits and the circumstances in which they arose, when objectively assessed, do not amount to a benefit that could reasonably be expected to influence the choice of financial product or the content of financial advice for the purposes of the conflicted remuneration provisions.

28 CBA contends that from a financial and accounting perspective for the CBA Group, any purported transfer of value by virtue of the Impugned Benefits was irrelevant. This is because, upon consolidation of the accounts, those transfers “cancel out”. Further, due to the operation of the dividend distribution policy of the CBA Group, any value that would otherwise have been retained by CFSIL in respect of Essential Super, would have flowed through to CBA in any event through the distribution of dividends. Both of those factors, in CBA’s submission, demonstrate the illusory nature of the alleged “influence” of the Impugned Benefits as any value realised from the Essential Super product would have ultimately flowed to CBA in any event.

29 CBA contends that there are other aspects of the Impugned Benefits which are problematic for ASIC’s case:

(a) the quantum of those Impugned Benefits did not take into account all of the expenses incurred by CBA in developing and distributing the Essential Super product;

(b) the quantum of those Impugned Benefits was de minimis to CBA;

(c) the details of the Impugned Benefits were not known to staff authorised to sell the Essential Super product and therefore could not influence the financial product advice or choice of product; and

(d) the fact that the detail of the financial arrangements, including the way in which they changed over time, were overlooked for a significant period - demonstrates that these arrangements were incapable of influencing CBA to behave in any particular way.

30 In these circumstances, CBA submits that it is difficult to conceive how the Impugned Benefits and the circumstances in which they arose could have reasonably influenced any choice of financial product recommended by CBA’s authorised staff, or any financial product advice they gave for the purposes of s 963A of the Act.

31 CFSIL denies that it breached the conflicted remuneration prohibition in the Act.

32 CFSIL relies on the submissions of CBA, and in doing so, contends that the alleged Impugned Benefits relied upon by ASIC in this proceeding, are not “conflicted remuneration” for the purposes of s 963A of the Act and CFSIL has not contravened the prohibition in s 936K of the Act.

33 The critical issues in dispute in the proceeding are:

(1) the meaning of “conflicted remuneration” for the purposes of s 963A of the Act;

(2) whether the nature of the alleged Impugned Benefits, and the circumstances in which they were provided, could reasonably have been expected to influence either the choice of financial product recommended by CBA to its customers or the financial product advice that CBA gave its customers; and

(3) whether CBA and CFSIL can rely upon the “grandfathering exception” provided for by s 1528 of the Act.

34 The parties filed a joint statement of agreed facts and issues in dispute (SAFID) dated 29 October 2020.

35 The development of Essential Super is largely uncontested and is set out in the SAFID. It can be summarised as follows.

36 In or around April 2011, the CBA Group commenced developing a superannuation product (originally called Simple Super). This superannuation product would be compliant with the proposed MySuper Reforms, would capture superannuation guarantee contributions and would consolidate superannuation from other funds.

37 The CBA Group, comprising CBA and its wholly owned subsidiaries, is divided into legal entities and business units. Throughout the Relevant Period:

(a) RBS was a business unit that provided home loan, consumer finance and retail deposit products and services to all retail bank customers; and

(b) Wealth Management was a business unit that provided superannuation, investment, retirement and insurance products and services including financial planning.

38 At all material times, CBA was, and still is, the holder of Australian Financial Services Licence number 234945.

39 From in or around 2010, RBS and Wealth Management began work on a joint initiative to develop a superannuation product to be sold online and in branches, targeting personal and small business customers. The project was targeted to launch on 1 July 2013, in line with the MySuper regulations commencing on that date.

40 In 2012, the Australian Parliament passed the MySuper Reforms. MySuper products were designed to be a new, simple and cost-effective way of providing default superannuation products for the accumulation phase of superannuation which was designed for members who do not necessarily actively engage with their superannuation.

41 MySuper products are tightly regulated. They involve a requirement to obtain authorisation from APRA before a trustee of a superannuation fund can offer a MySuper product, restrictions on the types of fees that can be charged and investment options limited to either a single diversified option or a life cycle option. All MySuper products must contain life and total permanent disability insurance on an opt-out basis. No commission can be paid on MySuper products from funds in member accounts. Superannuation trustees are generally only permitted to offer one MySuper product in a fund.

42 From 1 January 2014, employers’ superannuation guarantee contributions for employees who had not made a choice of fund could only be directed to a fund that offered a MySuper product. Trustees of superannuation funds were required to transfer default amounts accrued prior to 1 January 2014 (“accrued default amounts” or “ADAs”) to a MySuper product before 30 June 2017.

43 On or around 3 June 2011, the CBA Group Executive Committee were presented with a paper entitled “Commonwealth Simple Superannuation – Business Case” (Business Case). The Business Case outlined the rationale for launching a MySuper compliant product on the basis that the CBA Group’s competitors had launched, or were expected to launch comparable simple superannuation products in late 2011 and 2012. The Business Case records that it is a joint initiative of Wealth Management and RBS and that the product will be sold online and in branch targeting personal and small business customers with simple needs.

44 By 2012, competitors in the market had developed, or were in the process of developing, MySuper compliant products to bring to market.

45 On or around 4 May 2012, the Business Case was presented to the CBA Group Executive Committee. As set out in the SAFID at [21], the Business Case recognised:

(a) the business need for the CBA Group to launch a MySuper product to remain competitive in the superannuation market and in time for the commencement of the MySuper regulations;

(b) that a joint initiative between Wealth Management and RBS was the most efficient and effective way for the CBA Group to develop a MySuper product. The plan leveraged the technical expertise in the field of superannuation that the CBA Group had acquired through its purchase of CFSIL in 2000, with RBS’s retail banking network;

(c) a division of responsibilities between RBS and CFSIL, with CFSIL to manufacture and administer the product, and RBS to distribute the product;

(d) a plan for “a 50% share of costs and benefits between RBS and CFS business units” so that revenue was allocated and attributed correctly in the CBA Group’s financial statements.

46 On 4 May 2012, the CBA Group Executive Committee endorsed the Business Case and requested that a methodology be developed for the sharing of costs and earnings between the relevant entities. Between 4 May 2012 and 1 July 2013, the joint development of the Simple Super product was undertaken. In October 2012, CBA and CFSIL chose “Essential Super” to be the name of the Simple Super product.

47 In late 2012, representatives of CBA and CFSIL commenced talks in relation to attribution of costs and revenue from Essential Super. On 27 June 2013, CBA and CFSIL entered into the 2013 Distribution Agreement for an initial 5 year term.

48 On 2 June 2015, representatives of CBA and CFSIL entered into the 2015 Distribution Agreement.

49 Between September and November 2017, representatives of CBA and CFSIL exchanged email correspondence concerning Essential Super. These emails dealt substantially with payments and deductions to be made between relevant business units within the CBA Group under the 2015 Distribution Agreement with respect to Essential Super.

50 On 23 February 2018, Linda Elkins, Executive General Manager, Colonial First State wrote a letter on behalf of CFSIL to Clive van Horen, Executive General Manager Retail Products, on behalf of CBA. That letter, titled “Letter of Variation” recorded the agreement between CBA and CFSIL to vary clauses of the 2015 Distribution Agreement.

51 On 28 February 2018, Clive van Horen executed the letter on behalf of CBA.

52 On 26 February 2018, Clive van Horen, on behalf of CBA and Linda Elkins, Director, and Bernadette Watts, Company Secretary, on behalf of CFSIL, executed the 2015 Distribution Agreement.

53 Clause 8(a) of the 2013 Distribution Agreement, 2015 Distribution Agreement and 2018 Distribution Agreement each provided that CFSIL was to pay CBA for services it performed with respect to Essential Super.

54 The invoicing procedure of the 2013 Distribution Agreement, 2015 Distribution Agreement and 2018 Distribution Agreement each provided that:

(a) at the end of each financial year, CFSIL was to determine the total net revenue for Essential Super for that financial year and advise CBA of the fee payable based on that total net revenue (Advice);

(b) on receipt of the Advice from CFSIL, CBA was to issue an invoice for the fees (Invoice).

55 Throughout the Relevant Period, CBA had over 1000 branches (Branches) throughout Australia that together formed its retail branch network (Branch Network).

56 Throughout the Relevant Period, CBA had digital assets including NetBank and CommBank, and after May 2016, CBA’s digital assets also included the CommBank App (Digital Channels). The Digital Channels were accessible online by the general public.

57 On and from 1 July 2013:

(a) until on or about 8 October 2017, CBA distributed Essential Super to individuals through its Branch Network (Branch Sales).

(b) until on or about 3 July 2018, CBA distributed Essential Super to individuals through its Digital Channels (Digital Sales).

(c) until on or about 3 July 2018, CBA distributed Essential Super to employers as a default fund for employees who did not make a choice of superannuation fund (Employer Sales).

58 As a result of Employer Sales, individuals became members of Essential Super (Employee Sales) when they:

(a) commenced employment with an Employer Sales member who had nominated Essential Super as the default fund for employees who did not make a choice of superannuation fund; and

(b) did not make a choice of superannuation fund for superannuation contributions by that employer.

59 During the Relevant Period, 390,400 individuals became members of Essential Super (excluding those members who never had funds in their Essential Super account), broken down by financial year as follows:

(a) 1 July 2013 to 30 June 2014: approximately 69,607;

(b) 1 July 2014 to 30 June 2015: approximately 70,141;

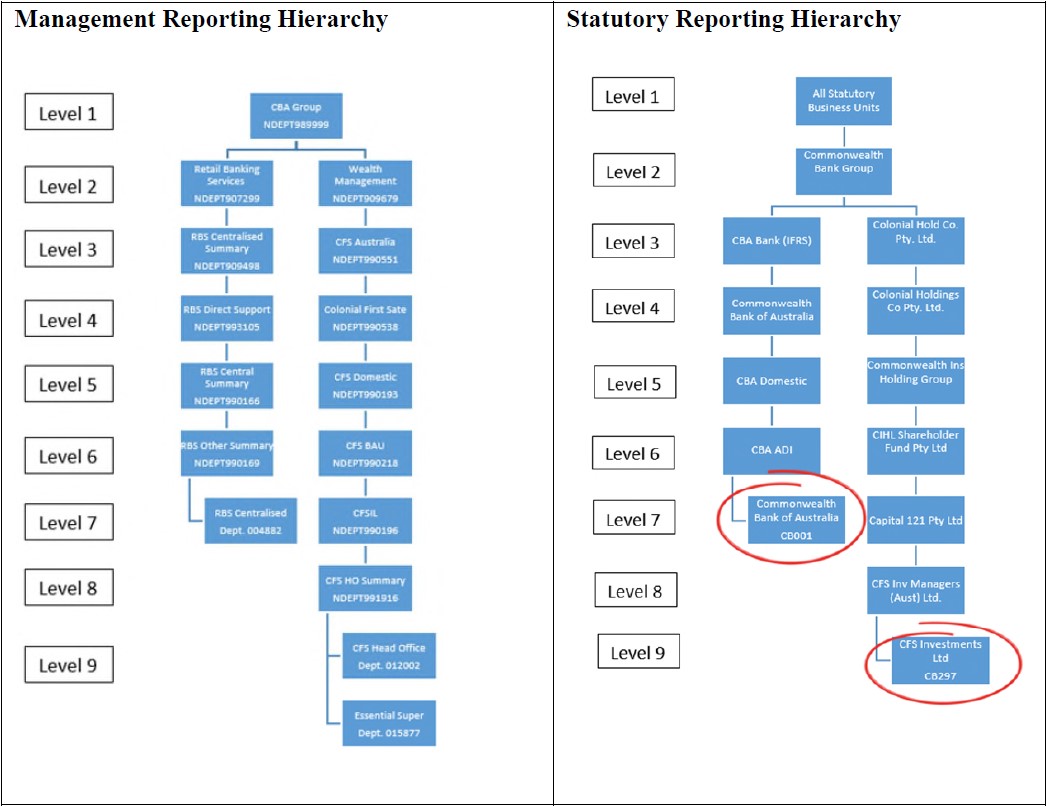

(c) 1 July 2015 to 30 June 2016: approximately 66,714;

(d) 1 July 2016 to 30 June 2017: approximately 112,617;

(e) 1 July 2017 to 30 June 2018: approximately 68,807; and

(f) 1 July 2018 to 30 June 2019: approximately 2,514.

60 Of the 390,400 individuals who became members of Essential Super during the Relevant Period:

(a) 191,364 individuals became members pursuant to Branch Sales;

(b) 135,499 individuals became members pursuant to Digital Sales;

(c) approximately 22,872 individuals became members pursuant to Employee Sales; and

(d) approximately 40,665 became members because they were members of the Colonial First State FirstChoice Superannuation Trust, had accrued default amounts in that fund and those accrued default amounts were transferred to the Commonwealth Essential Super fund between September 2014 and August 2016 (ADA Transfers).

61 Branch Sales involved a customer becoming a member of Essential Super as a result of:

(a) initiation of the Essential Super account opening process by a member (or members) of CBA’s staff in its “CommSee” system, within a Branch; and

(b) interactive completion of the application with the customer.

62 Where CommSee was unavailable a customer could lodge a paper application to become a member of Essential Super within a Branch.

63 During the Relevant Period, CBA staff who had completed the prescribed training and testing (Authorised Staff) were permitted to undertake the opening process of an Essential Super account for a customer.

64 During the Relevant Period, CBA staff who had not completed the prescribed training and testing (Non-Authorised Staff) could either perform a “warm handover” to Authorised Staff to assist a customer with opening an Essential Super account or could call the Essential Super call centre and assist a customer to become a member of Essential Super together with an Authorised Staff member in the call centre.

65 Between 1 July 2013 and 8 October 2017, CBA provided Non-Authorised Staff with approved scripts to use when discussing Essential Super with a customer or potential customer.

66 Between 1 July 2013 and 8 October 2017, the approved scripts could be accessed by branch staff. The scripts contained approved phrases including:

“Have you heard about Essential Super; it’s a superannuation fund, which can easily be viewed and managed in NetBank alongside a customer’s day to day banking”

“Essential Super is a simple superannuation fund, which can easily be viewed and managed in NetBank alongside a customer’s day to day banking.”

“Congratulations on your new job. If your employer pays super on your behalf, Essential Super issued by CFS is a simple and easy online account that accepts employer and personal contributions. I can't provide advice on this however let me introduce you to an accredited branch member who can help you?”

67 The text preceding the approved phrases provided that:

“Prepositioning Factual Information: I am not qualified to provide you advice about Essential Super, however let me introduce you to one of our Essential Super specialists (CSS) who can help you further.

…

Non-accredited staff should preposition Factual Information at the start of any interaction when discussing Essential Super.”

68 Between 1 July 2013 and 8 October 2017, branch staff were to follow standard operating procedures for Branch Sales.

69 From in or around June 2013 until 8 October 2017, Authorised Staff were trained by CBA to engage with a customer or potential customer, in respect of Essential Super, under a “general advice model”.

70 The training completed by Authorised Staff from in or around June 2013 until 8 October 2017 included various modules related to general advice pertaining to superannuation including:

(a) Superannuation fundamentals;

(b) Super investments;

(c) Employer contributions;

(d) Personal contributions; and

(e) Taxation and fees, among other things.

71 Between 1 July 2013 and 8 October 2017, CBA provided Authorised Staff with:

(a) a General Advice Warning approved script; and

(b) guides to use when introducing Essential Super to a customer or potential customer, including guides titled:

(i) “Start a Super Conversation”;

(ii) “Essential Super QRG”;

(iii) “How to discuss insurance or Essential Super with a customer”; and

(iv) “Essential Super Insurance: Common questions and suggested responses”.

72 On and from 1 July 2013 until on or around 3 July 2018, Employer Sales occurred:

(a) in Branches, where an employer was set up as a “standard employer sponsor” with respect to Essential Super in CBA’s “CommSee”; or

(b) digitally, where an employer set themselves up as a “standard employer sponsor” with respect to Essential Super by means of an online application via a Digital Channel.

73 Once an employer had been set up as a “standard employer sponsor” with respect to Essential Super, the employer was able to add employees as members of Essential Super:

(a) in a Branch; or

(b) by calling the Essential Super call centre; or

(c) via a Digital Channel.

74 With respect to Employer Sales in Branches, only Authorised Staff members were permitted to assist employer customers to be set up as a “sponsor” with respect to Essential Super in CBA’s “CommSee” system.

75 Throughout the Relevant Period, CBA provided an online application form for employers which stated:

Reasons for applying:

- To have a central depository for all your employees super details

- The ability to create a superannuation account for your employees.

Before you get started

- Please download and read the Essential Super Product Disclosure Statement (PDF 415KB) and Financial Services Guide (PDF 603.72KB).

Important information

- This application form provides general information only and is not financial advice

…

- This application form provides general information only and is not financial advice. It does not take into account your individual objectives, financial situation or needs.

... A Product Disclosure Statement (PDF 600KB) for Essential Super is available from commbank.com.au/super or by calling 13 40 74. You should read the PDS and assess whether the information is appropriate for you before making an investment decision.

76 On and from 1 July 2013 until on or about 3 July 2018, Digital Sales were completed by individuals completing an online application to open an Essential Super account via a Digital Channel.

77 The online application made available by CBA between 1 July 2013 and March 2015 contained details on how to apply for Essential Super, and required customers to update their personal details, select an investment option and select insurance options, among other things.

78 Further changes were made to the online application process until March 2018, but the key features were largely unchanged.

79 Individuals who became members of Essential Super as a result of ADA Transfers received a welcome pack from CBA which contained:

(a) a cover letter;

(b) an “Investment Confirmation” summarising the Essential Super account;

(c) a Product Disclosure Statement (PDS) for Essential Super;

(d) a “Super Choice” form to instruct the member’s employer to pay future contributions to Essential Super;

(e) a non-lapsing death benefit nomination form; and

(f) a booklet with information regarding NetBank and superannuation.

Essential Super transactions

80 RBS generated net profit after tax in the following amounts:

(a) $3,472 million in FY2013-14;

(b) $3,867 million in FY2014-15;

(c) $4,436 million in FY2015-16;

(d) $4,964 million in FY2016-17;

(e) $5,193 million in FY2017-18; and

(f) $4,234 million in FY2018-19.

81 The Cash Transfers, identified at [2] above, which CFSIL made to CBA are particularised as follows:

(a) $2,253,537.82 on or about 31 July 2014 for the 2014 financial year;

(b) $12,303,855.79 on or about 25 July 2018 for the 2018 financial year;

(c) $1,141,468.82 on or about 22 August 2018 for July 2018;

(d) $1,156,272.89 on or about 26 September 2018 for August 2018;

(e) $1,131,283.60 on or about 30 October 2018 for September 2018;

(f) $1,183,778.29 on or about 27 November 2018 for October 2018;

(g) $1,159,280.84 on or about 19 December 2018 for November 2018;

(h) $1,211,837.17 on or about 30 January 2019 for December 2018; and

(i) $1,226,166.87 on or about 29 March 2019 for January 2019;

82 The Cash Transfers made by CFSIL to CBA as outlined above, were in respect of Essential Super and were calculated in accordance with the methodology for calculating the fees in the 2018 Distribution Agreement.

83 The Journal Entries, identified at [2] above, which CFSIL and CBA made in respect of Essential Super were posted in the CBA general ledger (“CB001”) and can be particularised as follows:

(a) $2,253,537.82 on 30 June 2014 by journal entry #0002884878 for the 2014 financial year;

(b) $1,496,618.28 on 31 December 2014 by journal entry #0003107342 for the period from 1 July 2014 to 31 December 2014;

(c) $6,900,000 on 30 April 2016 by journal entry #0003717255 for the period from 1 July 2015 to 30 April 2016;

(d) $1,600,000 on 30 June 2016 by journal entry #0003806790 for the period 1 May to 30 June 2016;

(e) $841,981.57 on 31 July 2016 by journal entry #0003841311 for July 2016;

(f) $869,365.00 on 29 August 2016 by journal entry #0003874804 for August 2016;

(g) $1,026,926.59 on 30 September 2016 by journal entry #0003906361 for September 2016;

(h) $1,087,656.27 on 31 October 2016 by journal entry #0003958823 for October 2016;

(i) $1,096,550.90 on 30 November 2016 by journal entry #0003999590 for November 2016;

(j) $1,144,403.13 on 20 December 2016 by journal entry #0004027104 for December 2016;

(k) $879,960.58 on 31 January 2017 by journal entry #0004082645 for January 2017;

(l) $1,139,963.16 on 27 February 2017 by journal entry #0004112368 for February 2017;

(m) $1,295,850.01 on 30 March 2017 by journal entry #0004153297 for March 2017;

(n) $1,411,357.17 on 30 April 2017 by journal entry #0004185380 for April 2017;

(o) $1,468,285.55 on 19 May 2017 by journal entry #0004219522 for May 2017;

(p) $1,472,448.34 on 30 June 2017 by journal entry #0004274612 for June 2017;

(q) $1,472,448.34 on 31 July 2017 by journal entry #0004320320 for July 2017;

(r) $923,764.00 on 30 September 2017 by journal entry #0004400361 for August 2017;

(s) $1,028,352.00 on 22 September 2017 by journal entry #0004386160 for September 2017;

(t) $518,086.84 on 31 October 2017 by journal entry #0004437140 for October 2017;

(u) $1,047,901.63 on 30 November 2017 by journal entry #0004479319 for November 2017;

(v) $1,083,057.20 on 31 December 2017 by journal entry #0004517708 for December 2017;

(w) $1,116,922.93 on 31 January 2018 by journal entry #0004556462 for January 2018;

(x) $1,146,244.40 on 28 February 2018 by journal entry #0004592076 for February 2018;

(y) $1,184,953.45 on 31 March 2018 by journal entry #0004633395 for March 2018;

(z) $1,217,464.09 on 30 April 2018 by journal entry #0004669440 for April 2018;

(aa) $1,253,385.22 on 31 May 2018 by journal entry #0004709237 for May 2018;

(bb) $12,303,855.79 on 29 June 2018 by journal entry #0004745194 for the 2017/18 financial year;

(cc) $1,141,468.82 on 31 July 2018 by journal entry #0004799262 for July 2018;

(dd) $1,156,272.89 on 31 August 2018 by journal entry #0004834363 for August 2018;

(ee) $1,131,283.60 on 30 September 2018 by journal entry #0004873473 for September 2018;

(ff) $1,183,778.29 on 31 October 2018 by journal entry #0004913015 for October 2018;

(gg) $1,159,280.84 on 30 November 2018 by journal entry #0004955518 for November 2018;

(hh) $1,211,837.17 on 31 December 2018 by journal entry #0004995168 for December 2018; and

(ii) $1,226,166.87 on 11 February 2019 by journal entry #0005042639 for January 2019;

Revenue earned from funded accounts

84 CFSIL only earned revenue from Funded Essential Super Accounts, i.e. those accounts that had been opened and into which funds had been placed.

85 Between May 2013 and November 2013, in accordance with the PDS dated 17 May 2013, the net revenue earned by CFSIL from Funded Essential Super Accounts included:

(a) a “Member Fee” of $5 per month ($60 per annum) net of tax;

(b) a “Management Fee” of 0.80% per annum; and

(c) an “Insurance Administration Fee” of 7.5% of premiums for insurances held by members through Essential Super.

86 Between November 2013 and March 2015, in accordance with the PDS dated 2013, the net revenue earned by CFSIL from Funded Essential Super Accounts included:

(a) a “Member Fee” of $5 per month ($60 per annum) net of tax;

(b) an administration fee calculated at 0.40% per annum of funds under administration;

(c) an investment fee calculated at 0.40% per annum of funds under administration; and

(d) an “Insurance Administration Fee” of 7.5% of premiums for insurances held by members through Essential Super.

87 Between March 2015 and November 2018, in accordance with the PDS dated 28 March 2015, the net revenue earned by CFSIL from Funded Essential Super Accounts included:

(a) a “Member Fee” of $5.88 per month ($70.56 per annum) gross of tax;

(b) an administration fee calculated at 0.40% per annum of funds under administration;

(c) an investment fee calculated at 0.40% per annum of funds under administration; and

(d) an “Insurance Administration Fee” of 7.5% of premiums for insurances held by members through Essential Super.

88 Between November 2018 and the end of the Relevant Period, in accordance with the PDS dated November 2018, the net revenue earned by CFSIL from Funded Essential Super Accounts included:

(a) a “Member Fee” of $5.88 per month ($70.56 per annum) gross of tax;

(b) an administration fee calculated at 0.35% per annum of funds under administration

(c) an investment fee calculated at 0.40% per annum of funds under administration; and

(d) an “Insurance Administration Fee” of 7.5% of premiums for insurances held by members through Essential Super.

89 ASIC tendered at trial each of the documents identified in its Tender List dated 26 April 2022 and marked exhibit P-2. ASIC also tendered the redacted affidavit of Amanda Jean Jowett sworn 19 November 2020 (Jowett Affidavit), paragraphs [1]-[53], [74] and part of [76] and marked exhibit P-1. Ms Jowett, a senior lawyer with ASIC, deposed to the background of ASIC’s investigation and produced documents obtained by ASIC during the course of its investigation which had been tendered in evidence.

90 CBA tendered at trial each of the documents identified in its Tender List dated 4 May 2022 and marked exhibit MFI-2. In addition, CBA tendered three affidavits. The affidavit of Deirdre Langan, General Manager of Retail Products Finance, sworn 15 February 2021 (Langan Affidavit), marked exhibit D-1; the affidavit of David Huxtable, General Manager of CBA Group Treasury Finance, sworn on 15 February 2021 (Huxtable Affidavit), marked exhibit D-3; and the affidavit of Andrew Culleton, Executive General Manager Group People Services, sworn on 15 February 2021 (Culleton Affidavit), marked exhibit D-5.

91 CBA also tendered in evidence, as exhibit D-6, an expert report prepared by Mr Tony Samuel dated 12 March 2021 (Samuel Expert Report).

92 Ms Langan provided an affidavit sworn 15 February 2021. Ms Langan deposed to her experience working in various finance and accounting roles within the CBA Group.

93 Ms Langan is the General Manager, Retail Products Finance at CBA and has worked in various finance roles within the CBA Group for approximately 17 years.

94 Ms Langan has been involved in various capacities with Essential Super since July 2013.

95 Ms Langan was responsible for preparing financial statements and performance reporting (including journal posting), among other things.

96 Ms Langan gave evidence regarding the methodology applied to allocate the revenue and costs of Essential Super within the CBA Group by the relevant business units and finance departments at different times during the Relevant Period.

97 Ms Langan, in her affidavit, provided an overview of the finance processes within the CBA Group and set out:

(a) an overview of the general ledger of the CBA Group (General Ledger) and its various functions;

(b) an overview of the structure of the General Ledger;

(c) the procedure and process of journal postings to the General Ledger;

(d) how journal postings are “swept” across in the General Ledger each month; and

(e) General Ledger account and department IDs that are relevant to journal entries posted in relation to Essential Super.

Overview of the General Ledger

98 Ms Langan explained that the General Ledger is the master set of accounts that captures all transactions (including assets, liabilities, revenue and expenses), across the CBA Group business units and legal entities. The General Ledger contains a debit entry and a credit entry for every transaction recorded within it, therefore all debit balances should match the total of all credit balances.

99 Ms Langan deposed that, in her experience, the data contained within the General Ledger is the primary source material that is used by finance teams across the CBA Group to prepare:

(a) the management accounts of various CBA Group business units (for example RBS) and legal entities (for example CFSIL);

(b) the audited statutory accounts of each legal entity required to prepare such accounts (including CBA and CFSIL); and

(c) various financial statements for each entity including consolidated income statements, balance sheets, and statement of cash flows.

Structure of the General Ledger

100 Ms Langan explained how the General Ledger is arranged into two “hierarchies”. The management reporting hierarchy which is organised by business units and cost centres (Management Reporting Hierarchy) and the statutory reporting hierarchy which is organised by legal entities within the CBA Group (Statutory Reporting Hierarchy). The diagram below shows the structure during the Relevant Period.

101 The structure of the General Ledger therefore permits reporting at a level of business units, cost centres or products and separately, by a different class of entries, it also permits a recording of transactions that are going to impact legal entities.

102 Within this hierarchy:

(a) for RBS: all revenue and expenses are booked to the relevant RBS department code and also the legal entity code “CB001”; and

(b) for CFSIL: all revenue and expenses are booked to the relevant CFS department code and also the legal entity code “CB297”.

103 As shown above, the various CBA Group legal entities sit within and around this structure. Every CBA Group legal entity has its own subordinate ledger that sits within the General Ledger, to which journal entries can be posted. The mechanism through which transactional data is entered into the General Ledger is called a journal entry.

104 Journal entries are posted to the General Ledger by either:

(a) the relevant finance team populating the data necessary to create a journal entry; or

(b) automatically created by a CBA Group source platform (where no human input required).

As such, journal entries are primarily used by the CBA Group to attribute and track costs, revenue and expenses of different business units within the CBA Group.

105 In circumstances where CBA pays expenses on behalf of Colonial First State (CFS), being the wealth management and superannuation business of CFSIL, these entries are initially booked to the relevant CFS department and legal entity code “CB001” and are subsequently reallocated to legal entity code “CB297” via a journal entry process.

The monthly “sweep” process of expenses and resulting cash payments

106 Within the CBA Group it is common for one business unit (or legal entity) to incur expenses on behalf of another business unit (or legal entity) upfront.

107 Ms Langan deposed that it was only by means of a special “sweep” process that a journal entry would create a payable in the balance sheet, and the general practice was that all payables identified in that sweep process were thereafter settled by a cash payment between the relevant entities.

Journal entries posted in relation to Essential Super

108 In relation to Essential Super, CBA incurred expenses upfront on behalf of CFSIL. Ms Langan deposed that she was involved in posting one journal entry in financial year 2014, which was set up in such a way to “sweep” Essential Super costs borne by CBA (on behalf of CFSIL) to CFSIL. Ms Langan assumed that all subsequent journal entries posted in respect of Essential Super followed this model.

109 Ms Langan’s first interaction with Essential Super came during her time as Financial Controller of CFS and Wealth Management, which began in July 2013.

110 Ms Langan deposed that, in this role, she primarily received information about the finance processes that were in place for Essential Super from Mr Keith Wylie. Mr Wylie told Ms Langan that RBS and CFSIL had agreed to a 50:50 profit share, which the RBS and CFS finance teams were responsible for executing. Mr Wylie also told Ms Langan about the Business Case and the financial model underpinning it (Financial Model), both of which Mr Wylie had assisted in preparing.

111 The Business Case at section 6.2.4 provided:

6.2.4 Joint venture between CFS and RBS

The business case assumes a 50% share of costs and benefits between RBS and CFS business units. RBS and CFS Finance teams will be engaged following business case approval to agree to allocation methodology.

112 When Ms Langan first started as the Financial Controller, she received a briefing about the responsibilities she would be tasked with and the business teams that she would be supporting. Ms Langan worked across a number of different CBA products, but deposed that she did not recall having any specific conversations about Essential Super until approximately June or July 2014, when Andrew Strong (Executive Manager, Liability Products Finance, RBS) contacted her to discuss posting a journal entry to facilitate a 50:50 profit share with respect to Essential Super.

113 Ms Langan was never made aware of the fact that CBA and CFSIL had entered into the 2013 Distribution Agreement in respect of Essential Super.

114 As Financial Controller, Ms Langan was involved with posting one journal entry related to Essential Super, this took place at the end of the 2014 financial year and amounted to $2,253,537.82 (FY14 Cash Payment).

115 The FY14 Cash Payment was transferred from RBS to CFSIL.

116 On 7 July 2014, the FY14 Cash Payment was picked up in the CBA Group’s monthly sweep process, as was intended. The FY14 Cash Payment was transferred from CFSIL to the CBA legal entity on 31 July 2014.

117 The FY14 Cash Payment was calculated on the basis of operating expenses only and was based on a 50:50 profit share. Because Essential Super was loss-making in the 2014 financial year, this journal entry transferred expenses from RBS to CFSIL to reduce the loss position in RBS to create a 50% share of losses between RBS and CFS.

118 The figure transferred in this journal entry did not include any development costs incurred in the 2014 financial year in relation to Essential Super, which was approximately an additional $6,232,290 incurred by RBS. This figure also did not include or reflect any development costs incurred by CFSIL. If these total costs were included, Essential Super was a product which incurred a loss of $15,729,704 in the 2014 financial year.

119 In February 2016, Ms Langan commenced as the Executive Manager, Liability Products and was responsible for arranging the journal entries to be posted in relation to Essential Super.

120 Because it had been several years since she last worked with Essential Super due to an extended period of leave, Ms Langan had discussions with members of the RBS finance team to understand the correct processes that needed to be followed with respect to journal entries. Ms Langan was provided with a copy of a journal entry which was posted in December 2014 (December 2014 Journal).

121 Ms Langan deposed that the December 2014 Journal was comprised of:

(a) one credit entry in the amount of $-724,447.22 posted to account 58206 (Corporate Expense Accrual) and department 012002 (CFS “Head Office” cost centre);

(b) one debit entry in the amount of $724,447.22 posted to account 58149 (Other Operating Expenses) and department 004882 (RBS cost centre);

(c) one credit entry in the amount of $-2,221,065.50 posted to account 46205 (Other income) and department 016147 (RBS “Essential Super” - cost centre); and

(d) one debit entry in the amount of $2,221,065.50 posted to account 46388 (Sundry income - other) and department 012002 (CFS “Head Office” cost centre).

122 The December 2014 Journal therefore transferred a net total of $1,496,618.28 to CBA, to facilitate the profit share.

123 Ms Langan deposed that she reviewed the December 2014 Journal in order to learn what account and department codes should be used in future journal entries. In the course of that review, Ms Langan noticed that no journal entries were posted to effect a profit share for the January 2015 - June 2015 portion of the 2015 financial year and during the course of her work as part ASIC’s investigation into Essential Super, Ms Langan confirmed that in fact no journal entries were posted for the period January 2015 to June 2015.

124 On or around 29 April 2016, a journal entry was posted from CFSIL to RBS. The journal entry contained:

(a) one debit entry in the amount of $6,900,000.00, posted to account 46388 (Sundry Income - Other) and department 012002 (CFS cost centre); and

(b) one credit entry in the amount of $6,900,000.00, posted to account 46205 (Other income) and department 004882 (RBS cost centre).

125 The journal reflected a 50:50 split of profit earnt on Essential Super, in respect of the period July 2015 to April 2016.

Adoption of the Distribution Agreement allocation methodology

126 In early September 2017, Elizabeth Bennett (Senior Manager, Business Partnering of CFSIL) informed Ms Langan that she had discovered the 2015 Distribution Agreement executed between CBA and CFSIL. The 2015 Distribution Agreement provided for CBA and CFSIL to share the total net revenue of Essential Super on a 70:30 basis (with CFSIL receiving 70% and RBS receiving 30%), rather than the 50:50 profit share basis previously in place.

127 This was the first time Ms Langan became aware of the 2015 Distribution Agreement. Ms Langan deposed that she was not told about the 2015 Distribution Agreement during her role as Financial Controller for CFSIL and Wealth Management and was not told about the 2015 Distribution Agreement in her roles supporting RBS (until the conversation with Ms Bennett). To Ms Langan’s knowledge, no one in the RBS or CFS finance teams knew that the 2015 Distribution Agreement existed prior to 2017.

128 Because the net revenue share contemplated in the 2015 Distribution Agreement differed from the approach that was previously taken, Ms Langan spoke with her colleagues within the RBS finance team and the RBS business unit to understand more about the 2015 Distribution Agreement and obtained their views about what allocation methodology should be adopted from that point onward.

129 Ms Langan recalled that all of the colleagues that she spoke with were unaware of the 2015 Distribution Agreement.

130 After corresponding with Ms Bennett about this issue, it was agreed between CFSIL and RBS to adopt the allocation methodology set out in the 2015 Distribution Agreement, being a share of 30% of the net revenue earned on Essential Super from CFSIL to CBA.

131 Ms Langan deposed that after this agreement was reached, the RBS and CFS finance teams posted journal entries in accordance with the 30% net revenue share contemplated in the 2015 Distribution Agreement.

132 In order to correct the journal entries already posted within the 2018 financial year, the journal entry posted for October 2017 was in the amount of $518,086.84 in order to “true-up” the amounts on a year to date basis. This journal entry did not reverse the journal entries posted in respect of July, August and September 2017.

133 Throughout the balance of the 2018 financial year, journal entries were posted from CFSIL to RBS. This was only an allocation of revenue and did not include any cost allocations in relation to Essential Super for financial years 2018 and 2019.

134 In June 2018, further to the true-up process, the finance teams supporting CFSIL and RBS conferred about performing the 6-monthly true-up scheduled for June 2018.

Discovery that the journal entries were not resulting in cash payments

135 Ms Langan later learned that in June 2018, Ms Bennett discovered that no journal entry since the July 2014 journal had in fact resulted in a cash payment from CFSIL to CBA.

136 Ms Langan explained that the July 2014 journal entry resulted in a cash transfer.

137 However, in the ensuing 2015, 2016 and 2017 financial years, only management account journal entries were made; there were no sweep entries in those years which created a cash payable entry and nor were any cash payments made.

138 It was only in late 2017 when Ms Bennett discovered that no journal entry since July 2014 had in fact resulted in a cash payment from CFSIL to CBA.

139 Ms Langan deposed that, in order to ensure that an actual cash payment was transferred between legal entities, the CFS finance team proposed to modify the means by which journal entries were being posted, by posting from and to the “CB297” CFSIL legal entity ledger (as payer) and the “CB001” General Ledger (as receiver) (Cash Transfer Finance Process).

140 Because this issue was identified in June 2018 before the end of the 2018 financial year, the CFS finance team reversed the journal entries posted between July 2017 and May 2018 (Reversed Journal Entries) and posted a new journal entry which summed to the value of all of the Reversed Journal Entries (being $11,992,580.10) in accordance with the Cash Transfer Finance Process, to facilitate a cash settlement between CFSIL and CBA.

141 The CFS finance teams also posted a journal entry for the June 2018 true-up in the amount of $311,275.96. This figure was adjusted slightly down from the amount Ms Bennett had originally calculated.

Examination in chief of Ms Langan

142 Ms Langan was asked to explain the “sweep” process and the general process that she followed in July 2014, to make a journal entry that brought into effect the sweep process. Ms Langan explained that the sweep process is a standard monthly process to transfer costs from management accounts into financial accounts for the CFSIL legal entity, which occurs on work day five of each month. This is a manual process which is completed by a finance member.

143 Ms Langan explained the process with reference to an Essential Super RBS costs spreadsheet labelled as “D27” and marked for exhibit as MFI-1, an extract of which is below.

144 The codes that are listed under column “A”, being “CB297” and “CB001” pertain to CFSIL and CBA respectively. The sum of $14,881,010.84 were costs that were debited out of CBA and credited to the CFSIL legal entity’s account. Ms Langan gave evidence that this is the overall journal entry that would be posted for the month, and similar amounts would be posted each month, where costs were taken out of CB001 and placed into the CB297 and CFS entity.

145 Referring to the department column, Ms Langan explained that the code “011044” pertains to a department that sits within the CFSIL management. Ms Langan explained that this shows the sweep process that would happen each month wherein transfers for the sum of the expenses that had been paid on behalf of CFSIL by CBA, would be transferred into the CFSIL legal entity accounts.

146 Ms Langan gave evidence that under CBA’s processes, the use of the RBS and Wealth Management’s business codes in the management accounts triggers an intercompany payable from CFSIL to CBA. That intercompany payable then causes a monthly cash payment to settle the amounts that have been transferred between the legal entities. This mechanism for transitioning the business unit journal entry into a cash payment at the legal entity level is known as “sweeping”.

147 This process takes place at the end of every month.

Cross-examination of Ms Langan

148 Ms Langan gave the following evidence in cross-examination.

149 Ms Langan was cross-examined on the methodology applied to allocate the revenue and costs of Essential Super within the CBA Group during the Relevant Period.

150 Ms Langan was asked about the Distribution Agreements, which she discovered in the second half of 2017, and was questioned about her understanding of the annual fee equating to 30% net revenue. Ms Langan gave evidence that she reviewed the Distribution Agreements after becoming aware of them, but in terms of understanding the annual fee, she would have relied on her colleagues for this information.

151 Ms Langan gave evidence that prior to learning about the annual fee, she proceeded on the understanding that there was a 50:50 profit share arrangement. After coming to understand that net revenue did not include a deduction for operating costs, Ms Langan took the view that the calculation and journal entries needed to be organised in a different way. After adopting a new process for the calculation, Ms Langan gave evidence that this would have reduced the receipt of revenue by around $5 million.

152 Ms Langan was asked whether this realisation caused her to make any further checks. Ms Langan’s evidence was that she conferred with her colleagues and asked whether they were aware of the 2015 Distribution Agreement and the profit share arrangements; and also to advise her supervisors about the need to change the process to reflect the Distribution Agreements.

153 Ms Langan was asked about the arrangement with respect to statutory accounting that occurred each year. Ms Langan confirmed that both CFSIL and Capital 121 prepared separate statutory accounts in 2013 and 2014, and that, at least CFSIL lodged those separate statutory accounts with ASIC in the 2013 and 2014 financial years.

154 Ms Langan was then asked about CFSIL and the arrangement that it had in terms of functions and responsibilities within the CBA Group. Ms Langan gave evidence that CFSIL did not, and does not have any employees, rather, CBA would employ and pay staff to work on behalf of CFSIL. This employment arrangement would form part of the costs that were required to be transferred between the legal entities at the end of each month. CFSIL did not directly remunerate staff and there was no payroll function for CFSIL.

155 Ms Langan was questioned about her discovery of the revenue arrangement that existed within the Distribution Agreements and her subsequent understanding that costs were not being swept to CFSIL. Ms Langan was also asked whether this would have concerned CBA. Ms Langan gave evidence that, because CFSIL is a wholly owned subsidiary and the consolidated expenses sit within the CBA Group, this would not have affected CBA.

156 Ms Langan was asked to explain the difference between CFSIL and the CFS entities. Ms Langan explained that CFSIL is a distinct legal entity that has financial reporting requirements that need to be prepared and submitted with ASIC. CFS, on the other hand, is the overarching management arm. CFS managed the funds on behalf of CBA. CFSIL is wholly owned by CFS.

157 Ms Langan was asked about the management account journal entries. Ms Langan gave evidence that the 2014 management journals were subject to a sweep in July 2014. With respect to the 2015, 2016 and 2017 management journals, Ms Langan understood that there was no sweep which occurred, but Ms Langan gave evidence that she only came to learn this fact in 2019, during the evidence collection process as part of this proceeding.

158 Ms Langan, under cross examination conceded, with respect to the contention that the journal entries were management account entries that did not effect or constitute a payment between the two legal entities, that she was reliant on people within the CFS finance team for that conclusion as the sweep process sits within CFS and not RBS; and it would be necessary to adduce evidence from a person within CFS in order to satisfy the court that no cash payment was triggered in the 2015, 2016 and 2017 financial years.

159 Ms Langan was asked about the evidence deposed to in her affidavit with respect to the FY14 Cash Payment. Ms Langan gave evidence that this payment was in a different category to the payments in the 2015, 2016 and 2017 financial years, because, at the time of the 2014 financial year, Ms Langan was the financial controller of CFS and so had first-hand knowledge that a cash payment had been triggered and a sweep occurred.

160 In relation to the Distribution Agreements and the discovery of the profit share arrangement within these agreements, Ms Langan was asked what steps she was required to take going forward and what needed to occur. Ms Langan gave evidence that, from the perspective of RBS and within her financial expertise, she would not have needed to make any further investigations with respect to any restatements, because the amounts involved were not considered material to the management accounts.

161 Under cross examination, Ms Langan was directed to statements she made in her affidavit concerning the structure of the CBA Group and the different legal entities and business units that exist within it. Ms Langan gave evidence that CBA and CFSIL are legal entities and RBS and Wealth Management are business units.

162 Ms Langan was asked about the journal entries posted from CFSIL to RBS in the 2018 financial year. Ms Langan identified how the original journal postings from July through to May 2018 were posted as management entries. A modification to those entries was made in respect of those journal entries in June 2018 through the CFSIL legal entity. Insofar as there were amounts recorded in the management journal entries between CFSIL and RBS, Ms Langan gave evidence that these were recorded in the usual form without any corrections made; with the corrections to those entries in two separate entities in the June period. The first entry amounted to around $12 million and this entry was effectively the correction to the management entries to flow through the legal entities. The second entry, which was in the region of $300,000, was then a true-up to reflect the true revenue share for the year.

163 Ms Langan was asked to explain what the approximately $12 million sum represented. Ms Langan gave evidence that this sum represented the amounts from July 2017 through to May 2018 and were the amounts posted as management accounts in the business units only. This was then subject to the usual monthly sweep process.

164 With respect to the second entry in the region of $300,000, Ms Langan gave evidence that this figure reflected the management entries that would have been posted. This was an approximation of revenue that the team would have reviewed for the financial year and then would have adjusted the June amount, such that the full year transfer aligned to a 30% share of net revenue, there was then a sweep and a payment in respect of the true up by virtue of the legal entities.

165 Ms Langan impressed me as a person who was across the detail of the financial accounts of the CBA Group and its subsidiaries. Ms Langan was a forthright and compelling witness whose evidence I accept completely.

Evidence in chief

166 David Huxtable gave the following affidavit evidence.

167 Mr Huxtable has held various roles within the CBA Group and has advised on matters regarding accounting policy and reporting. Since September 2018, Mr Huxtable has held the role of General Manager, CBA Group Treasury Finance and since May 2021, the role of General Manager, Financial Reporting and Analysis.

168 Mr Huxtable gave evidence regarding the CBA Group structure (and the various business units within the CBA Group including RBS and Wealth Management) and the recording of financial performance, including with respect to Essential Super.

169 In his affidavit, Mr Huxtable outlined the CBA Group structure as at 2018. This reflects the structure of the CBA Group during the Relevant Period.

170 The CBA Group structure includes different business units such as RBS and Wealth Management. Mr Huxtable explained that CFSIL is a legal entity that sits within the CFS division of the Wealth Management business unit.

171 Mr Huxtable explained that, in its Annual Reports, the CBA Group provides information in respect of CBA as well as, on a consolidated basis, for its subsidiaries and that the financial results of all transactions that occur within the CBA Group structure are presented in the CBA Group’s financial statements for each reporting period. Mr Huxtable said that the CBA Group records its financial performance in the General Ledger and includes financial performance data for CBA Group entities such as CFSIL.

172 Mr Huxtable set out how Essential Super was presented in the CBA Group financial reporting in financial years 2014 and 2019.

173 Mr Huxtable said that in each financial year the revenue earned from the Essential Super product by CFSIL was recorded as “funds management income” which formed part of the CFS total recorded “funds management income” along with other subsidiaries. The CFS “funds management income” was recorded as part of the Wealth Management total “funds management income” and was recorded as part of CBA Group’s total “funds management income” in the CBA Group Annual Financial Statements.

174 Tables representing the flow of “funds management income” were set out in Mr Huxtable’s affidavit for the financial years 2014 to 2019. The figures presented in these tables were extracted from the CBA Group general ledger, profit announcements and annual reports (in particular financial statements included in the annual reports).

175 In relation to dividend payments, Mr Huxtable said that profits recognised in the CFSIL legal entity are distributed to the CBA legal entity (being CFSIL’s ultimate parent entity) through the CBA Group’s legal entity ownership structure as dividends. Dividends retained by CBA are retained as earnings or paid to its shareholders.

176 Mr Huxtable extracted the section of the CBA Group Capital Management of Subsidiaries and Branches Policy which sets out the mandatory requirements as to dividends, although he noted that exceptions in the policy allowed for dividends to be retained under specific circumstances:

Dividends

Subsidiaries must pay dividends to their parent companies, and branches must repatriate their earnings to CBA in Sydney, Australia, equal to their cash net profit after tax. Payments must be made at least semi-annually. The only exceptions to this are where the subsidiary or branch needs to retain profits:

a) to remain solvent;

b) to satisfy capital or regulatory requirements; or

c) Treasury Business Partnering confirms in advance that an adjustment to any required payment is in the best interest of the Group and does not have a negative capital impact on the Group. If there are constraints to the payment of dividends or profit repatriation (e.g. no foreign exchange liquidity), Treasury Business Partnering must be immediately informed.

177 For the years 2014 to 2019, Mr Huxtable set out:

(a) CFSIL’s dividend payments to its immediate parent company, Capital 121 Pty Limited (Capital 121);

(b) Capital 121’s dividend payments to its immediate parent company Commonwealth Insurance Holdings Limited (CIHL);

(c) CIHL’s dividend payments to its immediate parent entity Colonial Holding Company Limited (CHCL); and

(d) CHCL’s dividend payments to its immediate parent entity CBA.

178 These payments were recorded in the annual financial statements of each entity, which were audited and lodged with ASIC annually.

Cross-examination of Mr Huxtable

179 Mr Huxtable was cross-examined in relation to the dividend payment policy of the CBA Group and specifically, dividend payments made by CFSIL.

180 Mr Huxtable was first taken to the CBA Group’s capital management policies from 2012 through to 2020, which were exhibited to his affidavit. Mr Huxtable gave evidence that the group dividend policy, which had the CBA Group’s capital management policy appended to it, was updated annually from 2013 up until 2018 and this policy also covered the subsidiaries of the CBA Group.

181 Mr Huxtable explained that after 2018, there was a separate policy document that covered the subsidiaries; and the subsidiaries were no longer covered by the group policy. Mr Huxtable explained that the principles that applied to the subsidiary dividend did not change as part of this bifurcation process and that the only material difference was that there were two separate policy documents rather than one.

182 Mr Huxtable was taken through CFSIL’s annual financial statements and was asked to confirm CFSIL’s net profits (after tax) and dividends paid each financial year from June 2014 through to June 2019. Mr Huxtable accepted that, in the six financial years from 2013 to 2019, the actual percentage of net profit after tax distributed by CFSIL by way of dividend ranged from a low of 44% to a high of 98%.

183 Mr Huxtable also accepted that the dividend policy provided for capital requirements to take priority over the payment of dividends, and that, in the six years in question, the regulatory capital requirements for CFSIL were subject to change.

184 Mr Huxtable was taken to a paragraph of the CFSIL 2014 financial report which stated that:

In order to maintain or adjust the capital requirements, the company may adjust the amount of dividend paid to its shareholders.

185 Mr Huxtable agreed that it was apparent from this section of the 2014 financial report that CFSIL had to start transitioning to maintain its operation risk financial requirement (OPFR) as part of APRA’s requirement for Registrable Superannuation Entity (RSE) licensees. Mr Huxtable agreed that this had affected CFSIL’s capital requirements and, consequently, its dividends.

186 Mr Huxtable was taken to this same section within the 2015 financial report. Mr Huxtable confirmed that, for the year ended 30 June 2015, the company was also required to comply with ASIC Regulatory Guide 166, which imposed a net tangible asset requirement of 10% of average revenue on RSEs, on top of the APRA OPFR requirement.

187 Mr Huxtable confirmed that it was clear that CFSIL’s payment of dividends was subject to capital requirements.

188 Mr Huxtable explained, by reference to CFSIL’s principles of capital management, that regulatory capital requirements, which informed the level and quality of capital, were requirements imposed by different regulatory entities. Mr Huxtable said that for different entities there are different regulations, as there are different regulators who govern those entities. For example, ASIC will require a base level of capital to be retained within the entity so that it can maintain solvency. Mr Huxtable also said that a bank will have the regulatory capital requirement to maintain a certain level of capital to meet potential deposit outflows and to underwrite the going concern of the organisation.

189 Mr Huxtable then explained what is meant by economic capital requirements. Rather than being an external regulatory concept, he explained that economic capital is an internal measure of capital and is specifically designed to represent the amount of capital needed by reference to the risk that was being undertaken by a specific division. Further, it assists in determining the performance of a particular division based on the economic capital holds relative to the profit or revenue it was generating. Mr Huxtable clarified that while there are regulatory capital requirements for each subsidiary, when it comes to economic capital and assessing performance, it comes more from a management perspective as opposed to a “legal-entity level”.

190 Mr Huxtable confirmed that the primary capital requirement for CFSIL is the regulatory capital requirement, which can change over time.

191 I accept Mr Huxtable’s evidence. Mr Huxtable demonstrated a detailed knowledge of the CBA Group structure and the dividend policy adopted by the CBA Group. Mr Huxtable gave forthright evidence which I accept in its entirety.

Evidence in chief

192 Andrew Culleton gave the following evidence by affidavit.

193 Mr Culleton is the Executive General Manager, Group People Services at CBA and has held this position since April 2013. Mr Culleton gave evidence concerning the employment arrangements between employees and the CBA Group. Mr Culleton also gave evidence that CFSIL did not employ any personnel; and the personnel that did support CFSIL’s operations were employees of CBA or certain other related bodies corporate of CBA and CFSIL and did not make any payroll payments during the Relevant Period.

194 Mr Culleton outlined how CBA Group is comprised of a large number of corporate subsidiaries, all of which are ultimately owned by CBA. CBA Group subsidiaries are grouped and organised by business units. Between 1 July 2013 and 30 June 2019, CBA Group business units included amongst others, the RBS and Wealth Management business units.

195 Only a small number of CBA Group entities are employers of CBA Group personnel.

196 Based on his review of the CBA Group Enterprise Agreements, lodgments to the Australian Taxation Office (ATO) for payroll payments and the records of CBA Group’s HR systems, Mr Culleton formed the view that the CBA Group entities are the only entities that employed CBA Group staff. Mr Culleton deposed that, if there were other CBA Group entities who employed CBA Group staff then they would have been required to enter into an Enterprise Agreement, or otherwise have lodged payroll payments to the ATO or would have been identified in the CBA Group’s HR systems as an employer entity.

197 Mr Culleton identified the CBA Group employer entities as:

(a) the CBA legal entity (ACN 123 123 124);

(b) Colonial Services Pty Limited (ACN 075 733 023) (Colonial Services);

(c) Commonwealth Insurance Limited (ACN 067 524 216) (Commlnsure);

(d) Commonwealth Securities Limited (ACN 067 254 399) (CommSec);

(e) BWA Group Services Pty Ltd (ACN 111 209 440) (Bankwest Services); and

(f) Digital Wallet Pty Limited (ACN 624 272 475) (Digital Wallet) (noting that Digital Wallet made no payroll payments during the Relevant Period),

(collectively, the Employer Entities).

198 The CBA Group had various enterprise agreements and awards in place, which were approved by the Fair Work Commission. The enterprise agreements and the awards set out the minimum terms and conditions of employment of CBA Group personnel who are covered by the instrument.

199 Prior to 8 October 2014, the CBA Group had separate enterprise agreements and an award (Historical Industrial Instruments) in place which related to each of the Employer Entities, except for Bankwest and Bankwest Services. The Historical Industrial Instruments included various enterprise agreements relating to employee entitlements in the employment of CBA, CFSIL, Colonial Services and Commlnsure.

200 On, and from 9 October 2014, the Historical Industrial Instruments were replaced by a single enterprise agreement that covered all Employer Entities in the CBA Group, except for Bankwest and Bankwest Services.

201 The Commonwealth Bank Group Enterprise Agreement 2014, which was approved by the Fair Work Commission on 9 October 2014 and operated on and from 9 October 2014 (2014 Enterprise Agreement), applied to all relevant CBA Group personnel outside of the Bankwest division of the CBA Group.

202 The 2014 Enterprise Agreement was subsequently replaced by the Commonwealth Bank Group Enterprise Agreement 2016 (2016 Enterprise Agreement), which was approved by the Fair Work Commission on 25 November 2016 and which operated from 2 December 2016.

203 After the CBA Group acquired Bankwest, employees that had historically been employed by the Bankwest entity were transferred across so as to be employed by the BWA Services entity. This transfer was completed in or around March 2012.

Employees within Wealth Management and CFSIL

204 CFSIL is a wholly-owned subsidiary of CBA and sits within the Wealth Management business unit that provides investment, superannuation and retirement products to individuals as well as to corporate and superannuation fund investors.

205 The Employer Entities are the only CBA Group subsidiaries that employ CBA Group personnel. CBA Group personnel that support the Wealth Management business unit are typically employed by Colonial Services, however some are employed by CommInsure, and certain CBA Group personnel in Wealth Management are employed by CBA itself.

206 CFSIL does not employ any personnel.

207 CFSIL has made no payroll payments at any time. Mr Culleton deposed this to be within his knowledge and belief because:

(a) on 9 February 2021, he caused a search to be run on the ATO's Single Touch Payroll (STP) platform (which has records from 1 July 2016 onwards) for all payroll lodgments made by CFSIL. That search returned no results. The member of Mr Culleton’s team who ran that search, Steve Cottrell (Head of Governance and Assurance, CBA Group People Services), took a screenshot of the ATO Business Platform page that showed no results and the date and time of the search;

(b) also on 9 February 2021, Mr Culleton caused a search to be run on CBA's archived payroll software platform, known as “PeopleSoft”, for any payroll payments made by CFSIL. PeopleSoft was used between 2002 and 2018, the platform was then retired and its contents archived. Terry Spek (Senior Manager, Workforce analytics Supply and Enablement) queried the PeopleSoft archived data to determine whether CFSIL had ever made payroll payments, and that search returned no results.

208 In examination in chief, Mr Culleton identified that the companies listed as the Employer Entities in his affidavit were incomplete. Mr Culleton provided the names of four additional Employer Entities that he wished to add to the list. These were identified as:

(a) Avanteos;

(b) Arcadian;

(c) Aussie Home Loans; and

(d) CMLA.

Cross-examination of Mr Culleton

209 Mr Culleton was cross-examined and gave the following evidence.

210 Mr Culleton, in cross-examination, confirmed that the Employer Entities, including the four entities which he added to that list, employed CBA Group staff. Mr Culleton confirmed that CFSIL did not employ CBA Group staff.

211 Mr Culleton explained that CBA business units are supported by a combination of staff within the Employer Entities. Mr Culleton noted that CBA Group has an obligation to pay payroll tax for those employees to the relevant state agencies as well as withholding tax to the ATO and, for the purpose of payroll tax, each employee would be identified as working for the relevant Employer Entity. Mr Culleton confirmed that CFSIL is not, and has never been, an Employer Entity. Mr Culleton was made sure of this after undertaking extensive checks and reviews of the relevant financial records and payroll data.

212 Mr Culleton explained that his role is to apply the marginal or the withholding tax, and then the finance team account for the fringe benefits tax and the state-based payroll tax; and the withholding tax statement will identify the legal entity with whom the staff member is employed.

213 Mr Culleton was then asked in cross-examination, about the status of the employees that were supporting the operations of CFSIL.

214 Mr Culleton’s evidence was that, upon reviewing a number of different employees’ contracts, he could confirm that they were all employees of one of the Employer Entities, and many were employed by CBA. Those employees were subject to the direction of the team leader that runs the relevant department, which, Mr Culleton explained could be someone who is employed under the CBA entity.

215 Mr Culleton was asked about the minutes of a board meeting of CFSIL which took place on 29 May 2013. The board members and attendees of the meeting were listed on the first page of the minutes. Mr Culleton was asked whether he could recognise the names of any of the attendees that were listed. Mr Culleton could immediately recognise at least two of the names listed in the minutes, being Mr Michael Venter and Ms Annabel Spring. Mr Culleton stated that they were employees of the CBA Group. Mr Culleton recognised Ms Spring as a group executive. Mr Culleton was of the view that Ms Spring, as a group executive, would have been on a number of boards.