Federal Court of Australia

Hanwood Pastoral Co Pty Limited v Kelly (No 2) [2022] FCA 850

File number(s): | NSD 1053 of 2019 |

Judgment of: | HALLEY J |

Date of judgment: | 21 July 2022 |

Catchwords: | CORPORATIONS – application for declarations and compensation for alleged breach of directors’ duties by first defendant – application for reinstatement of director of plaintiff – whether first defendant caused detriment to plaintiff by causing it to enter into uncommercial consultancy agreement for sale of property in contravention of s 182(1)(b) of the Corporations Act 2001 (Cth) (Act) – whether director seeking reinstatement unlawfully removed as director of plaintiff in contravention of s 182(1)(a) of the Act – whether first defendant failed to discharge duties in good faith in best interests of plaintiff and for a proper purpose in causing plaintiff to make payments out of sale proceeds in contravention of s 181(1) of the Act – whether first defendant caused detriment to plaintiff by improperly using his position to cause payments to be made out of sale proceeds in contravention of s 182(1)(b) of the Act – where first defendant self-represented – where relative dearth of books and records relating to sale of property and disbursement of sale proceeds – where director seeking reinstatement and first defendant each maintain that the other holds the books and records – where first defendant bears evidentiary onus of proof – application dismissed |

Legislation: | |

Cases cited: | Bell Group Ltd (In liq) and Others v Westpac Banking Corporation and Others (No 9) (2008) 39 WAR 1; [2008] WASC 239 Crowe-Maxwell v Frost (2016) 91 NSWLR 414; [2016] NSWCA 46 Dinomyte Pty Ltd v Australian Securities & Investments Commission, in the matter of Hanwood Pastoral Co Pty Ltd [2019] FCA 1989 Hanwood Pastoral Co Pty Limited v Kelly [2020] FCA 1020 In the matters of Earth Civil Australia Pty Ltd, RCG CBD Pty Ltd, Bluemine Pty Ltd, Diamondwish Pty Ltd and Rackforce Pty Ltd (all in liq) [2021] NSWSC 966 Jones v Dunkel (1959) 101 CLR 298 Permanent Building Society (in liq) v Wheeler and Others (1994) 14 ACSR 109 R v Towey (1996) 21 ACSR 46 Re Colorado Products Pty Ltd (in prov liq) (2014) 101 ACSR 233; [2014] NSWSC 789 Re IW4U Pty Ltd (in liq) and Others (2021) 150 ACSR 146; [2021] NSWSC 40 Renton v Kelly [2018] NSWSC 1377 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Corporations and Corporate Insolvency |

Number of paragraphs: | |

Date of last submission/s: | 10 December 2021 (Plaintiff) |

25-27 October 2021, 3 December 2021 | |

Counsel for the First Defendant: | The First Defendant appeared in person |

Counsel for the Second Defendant: | The Second Defendant did not appear |

ORDERS

HANWOOD PASTORAL CO PTY LIMITED (ACN 003 985 797) Plaintiff | ||

AND: | First Defendant AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Second Defendant | |

DATE OF ORDER: | 21 July 2022 |

THE COURT ORDERS THAT:

1. The further amended originating process be dismissed.

2. If the parties are unable to agree orders by 18 August 2022 with respect to the payment by the first defendant of fixed sums in respect of the plaintiff’s costs of the case management hearings on 6 November 2020 and 19 November 2021, the costs thrown away by the vacation of the hearing of the strike out application on 11 June 2021, on an indemnity basis, and the first defendant’s application to reopen his case after the exchange of closing written submissions, each party should by no later than that date file and serve a copy of their proposed orders as to the payment of fixed sum costs, together with an outline of written submissions in support not exceeding four pages in length and any evidence by way of affidavit in support of the fixed sum orders sought.

3. Fixed sum costs orders will then be determined on the papers and without a further oral hearing.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

HALLEY J:

Introduction

1 By a further amended originating process filed on 25 October 2021, the plaintiff, Hanwood Pastoral Co Pty Limited ACN 003 985 797 (Hanwood) seeks declarations and compensation against the first defendant, Mr Frederick Norman Kelly, for alleged breaches of his duties as a director of Hanwood and an order for reinstatement of Mr Frederick William Renton as a director of Hanwood against the second defendant (formerly the sixth defendant), the Australian Securities and Investments Commission (ASIC), in relation to alleged acts done by Mr Kelly in contravention of the Corporations Act 2001 (Cth) (Corporations Act). The proceedings were dismissed by consent and without admissions as between Hanwood and the former second to fifth defendants on 14 May 2021.

2 Hanwood alleges that Mr Kelly caused Hanwood to suffer detriment by causing it to enter into an uncommercial and onerous property consultancy agreement (Consultancy Agreement) that provided for the payment of fees grossly in excess of the value of the services to be provided by Mr Kerry Nichols and Mr Matthew Somers (together, Consultants) in connection with the sale of an undeveloped property owned by Hanwood in the Hunter Valley (Property), unlawfully removed Mr Renton as a director of Hanwood and improperly caused Hanwood to make payments to his own company, Stintari Pty Limited (Stintari) and other associates out of the sale proceeds of the Property (Impugned Payments).

3 Mr Kelly contends that the entry by Hanwood into the Consultancy Agreement was justified and agreed by Mr Renton, Mr Renton resigned as a director of Hanwood on his own initiative and the Impugned Payments were made to discharge properly recorded and approved commercial liabilities of Hanwood.

4 Hanwood alleges that Mr Kelly:

(a) contravened s 182(1)(b) of the Corporations Act by causing or allowing Hanwood to enter into the Consultancy Agreement (Uncommercial Contract Contravention);

(b) contravened s 182(1)(a) of the Corporations Act by unlawfully removing Mr Renton as a director of Hanwood (Removal Contravention); and

(c) contravened ss 181(1) and 182(1)(b) of the Corporations Act by authorising or allowing payments totalling $2,425,350 to be made, causing detriment to Hanwood in an amount equal to the Impugned Payments (Payments Contravention).

5 The proceedings had a lengthy and acrimonious history in the period leading up to the final hearing of the claims advanced in the amended statement of claim and the relief sought in the further amended originating process.

6 Mr Kelly was not able to secure legal representation after 10 June 2021 and from that time appeared for himself. Mr Farrar of Farrar Lawyers appeared for Hanwood at all times in the proceedings from 10 June 2021.

7 The only relief sought against ASIC was an order for the reinstatement of Mr Renton as a director of Hanwood. ASIC informed the Court that it did not seek to be heard on that issue and it did not appear at the hearing of the proceedings.

8 The determination of the claims made by Hanwood in the proceedings was made significantly more difficult by three matters. First, an intractable dispute as to the location and existence of the historical financial and other corporate records of Hanwood that might evidence the specific liabilities of Hanwood the subject of the Impugned Payments and the basis on which funds might have been advanced by way of unsecured loans to Hanwood to enable such liabilities to be discharged. Second, Mr Kelly’s hearing difficulties and medical issues that presented formidable challenges to his effective participation in the proceedings as a self-represented litigant following the withdrawal of his legal representation in June 2021. Third, the extent to which Mr Renton left the development and realisation of the Property exclusively to Mr Kelly and, as the sole director of Hanwood’s only shareholder, refused to advance any funds to Hanwood to enable it to develop and realise the Property.

9 In the circumstances, it has been necessary to make factual findings by reference to an incomplete documentary record and to the apparent logic of events, particularly given the effluxion of time since most of the material events and the advanced age of both of the principal protagonists, Mr Renton and Mr Kelly.

10 For the reasons that follow I have concluded that:

(a) the evidence given by Mr Kelly can generally be accepted, notwithstanding the credit challenges made by Hanwood and Mr Kelly’s at times confrontational approach to the proceedings and giving evidence;

(b) Mr Kelly has produced all relevant books and records of Hanwood in his possession and he otherwise gave Mr Renton the historical books and records of Hanwood, including minute books evidencing, among other matters, the liabilities of Hanwood incurred with respect to the development and realisation of the Property and the means by which those liabilities were discharged;

(c) the payments made to the consultants under the Consultancy Agreement did not constitute a gross overpayment, and Mr Kelly’s conduct in causing Hanwood to enter into the Consultancy Agreement when viewed objectively and by reference to the standards of conduct expected from a person in Mr Kelly’s position did not confer significant benefits on the Consultants to the detriment of Hanwood;

(d) Mr Renton resigned as a director of Hanwood of his own volition and Mr Kelly did not unlawfully remove Mr Renton as a director of the company;

(e) Mr Renton left to Mr Kelly the exclusive responsibility of managing the development and realisation of the Property;

(f) Mr Renton had made it clear to Mr Kelly that he was not prepared to advance any funds to Hanwood to fund the development and realisation of the Property, notwithstanding he was the only shareholder in Hanwood through his private company Dinomyte Pty Ltd (Dinomyte);

(g) the discovery of critically endangered Persoonia pauciflora plants on the Property, the refusal of the Cessnock City Council to grant development approval, the proceedings in the Land and Environment Court, the length of time that Hanwood had sought to develop the Property and the time it took to find a purchaser inevitably led to the incurring of significant liabilities that Mr Kelly was obliged to make arrangements to discharge;

(h) the financial statements of Hanwood prepared by Mr Kelly, in the context of other financial records and bank statements admitted into evidence, can be relied upon, and are sufficiently probative of the facts asserted in them, to permit Mr Kelly to satisfy any evidential onus that he might have been under to establish that he was justified in making the Impugned Payments; and

(i) Hanwood has not succeeded in establishing the Uncommercial Contract Contravention, the Removal Contravention nor the Payment Contravention.

Factual Background

11 The following factual background is taken from documents tendered in evidence.

Hanwood

12 On 14 May 1990, Hanwood was incorporated as a proprietary company, initially as Redyoke Pty Limited, until it changed its name to “Hanwood Pastoral Co. Pty. Limited” on 31 August 1990.

13 In the period between 7 June 1990 and 14 February 1994, the directors and company secretaries of Hanwood were Mr John Holt and Mr Keith Holmes.

14 On 14 February 1994, Mr Renton and Mr Harry Terrett were appointed as directors and company secretaries of Hanwood.

15 On 3 December 1998, Mr Kelly was appointed as a director and company secretary of Hanwood.

16 On 16 October 2010, Mr Terrett ceased to be a director and company secretary of Hanwood.

17 On 20 May 2014, Mr Renton ceased to be a director and company secretary of Hanwood.

18 At all relevant times Dinomyte has been the sole shareholder of Hanwood. Mr Renton holds all the shares in Dinomyte.

The Property

19 During the early 1990s, Hanwood purchased the Property, located at Hanwood Road, North Rothbury New South Wales, being lots 3, 4 and 5 in DP1042140 in certificate of titles folio identifiers 3-5/1042140.

20 The Property was located in the Hunter Region of New South Wales. It was covered primarily in native vegetation.

September 2008 Consultancy Agreement Letter

21 By letter dated 3 September 2008, Hanwood wrote to Mr Nichols confirming that they wished his company, Hunter Developments Brokerage Limited (HDB), to act as a consultant on the proposed sale of the Property (September 2008 Consultancy Agreement Letter).

22 The September 2008 Consultancy Agreement Letter was signed by Mr Kelly, Mr Renton and Mr Terrett in their capacities as directors of Hanwood. The letter provided for the following consulting fee to be paid (as written):

On settlement of sale ( Hanwood Stage 5 ), ( Hanwood ) will pay ( HDB. ) and or ( HDB’S ) nominee a consulting fee equal to 4% of a sale price up to and including $5,000,000.00 and any sale price in excess of $5,000,000.00 an amount equal to 50% of the excess over $5,000,000.00.

23 The September 2008 Consultancy Agreement Letter also provided that HDB would not charge any other fee for services provided after 15 June 2008 in relation to the Stage 5 development of the Property unless mutually agreed in writing between Hanwood and HDB.

Heads of Agreement

24 The documents discovered by Mr Kelly, as part of what I have referred to below as the Late Discovered Documents, included a document entitled “HEADS OF AGREEMENT FOR THE FORMULATION OF A BIO-BANKING/ENVIROMENTAL OFFSETTING STRATEGY AND ON SALE OF LAND AT NORTH ROTHBURY” dated April 2013 (Heads of Agreement).

25 The parties to the Heads of Agreement were stated to be Hanwood as the owner of the Property and the Consultants (Mr Somers and Mr Nichols). The Consultants were described as “recognised and experienced experts in the development field” with “extensive industry contacts” which gave them the “opportunity to maximise the economic return to owner of the site”. The Heads of Agreement provided that it would expire if a sales contract had not been exchanged within 24 months of execution of the agreement. It also provided that upon a sale of the Property the sale proceeds were to be first allocated to the payment of the costs incurred by the Consultants during the term of the agreement, then a payment of the “base value” of $1.2 million to Hanwood and finally the balance was then to be split between Hanwood (as to 60%) and the Consultants (as to 40%).

Consultancy Agreement

26 On 22 April 2013, Mr Kelly sent an email to Mr Nichols concerning a foreshadowed entry by Hanwood into the Consultancy Agreement (22 April 2013 Email), which included the following confirmation and explanation:

We, Fred Renton and myself have resolved to enter into an agreement with your group.

I have delayed making contact as Hanwood was deregistered due to non payment of fees, however I have made application with ASIC for reinstatement which I am advised will take between 3 - 4 weeks.

27 On 2 July 2013, Mr Nichols sent an email to Mr Kelly attaching a draft of the Consultancy Agreement.

28 On 12 July 2013, Mr Kelly sent an email to Mr Renton and Mrs Renton (12 July 2013 Kelly Email) while they were in Hawaii in these terms (as written):

Many thanks for your contact.

Fred I would like to see you Vi re Hanwood ASAP after you return, and before the scalpel falls AM on the 17th.

I also need time to, in necessary go to Maitland, no later than early pm on the 16th.

It would be appreciated if you would advise ETA Sydney and where I can conveniently meet up with you thereafter?

Your advice is greatly appreciated.

Enjoy the remainder of your so journ and safe and pleasant flight home.

29 Later on 12 July 2013, Mrs Renton responded to the 12 July 2013 Kelly Email in these terms (as written):

Fred will be at Rosé Bay on Tuesday after 9 am 16 th . He will be happy to speak or meet with you then. Maybe you could go to Maitland together- is that the idea?- on that day,as long as you are happy to drive.!!!

Fred intends to be in Sydney til the Thursday 18 th

We are enjoying the sunshine, thanks.

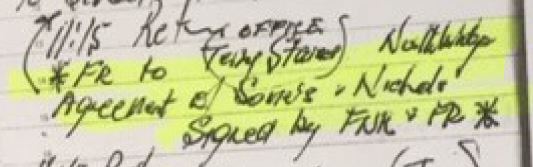

30 On 16 July 2013, Mr Renton’s handwritten diary includes the following entry (Renton 16 July 2013 Diary Note):

11:15 Return

(OFFICE)

* FR to (Terry Staines) Northbridge

Agreement of Somers + Nichols

Signed by FNK + FR *

There is an arrow between the words “* FR” and “Agreement” which points to above “11:15”, as follows:

31 The Consultancy Agreement was executed by both Mr Kelly and Mr Renton for Hanwood. It was dated 17 July 2013. I will return to the specific dates on which the Consultancy Agreement was in fact signed later in these reasons.

32 The Consultancy Agreement provided that Mr Nichols and Mr Somers were to provide the following services to Hanwood:

(a) undertaking and updating flora and fauna studies to identify any endangered species, to secure the optimum biodiversity value of the Property;

(b) consulting with the Office of Environment and Heritage to determine the environmental credits available for the Property;

(c) liaising and consulting with New South Wales National Parks to attempt to have land included as part of an adjacent national park;

(d) obtaining such consents or approvals as necessary for the subdivision of the Property, to optimise the aggregate sale price;

(e) liaising with and seeking the assistance of the Federal Environmental Department under the Environment Protection and Biodiversity Conservation Act 1999 (Cth) to ensure compliance with the relevant federal legislation; and

(f) formulating a marketing strategy for the sale of the Property, or parts thereof, to maximise the value of the Property.

33 The Consultancy Agreement further provided that Mr Nichols and Mr Somers would contribute their “skill and expertise” to secure the highest and best use of the Property.

34 Under the Consultancy Agreement, Hanwood was obliged to pay Mr Nichols and Mr Somers for the services they provided:

(a) all of the expenses incurred by them in relation to those services, in priority to the payment to Hanwood of the original land value; and

(b) 40% of the net sale proceeds plus additional GST.

35 In October 2013, Niche Environment and Heritage Pty Ltd completed a BioBank assessment of the potential offsets available on the Property and another site in the Hunter Valley (Niche Report). The Niche Report confirmed that an estimated 337 ecosystem credits might be generated on the Property and 228 species credits were calculated for 155 individual Persoonia pauciflora plants.

36 Mr Nichols and Mr Somers retained HDB to provide project management and consulting services, including providing a planner and senior planner.

Sale of the Property

37 On 7 January 2015, Hanwood entered into a contract with Warkworth Mining Limited (Warkworth) pursuant to which it agreed to sell the Property to Warkworth for $3.63 million (including GST) (Sale Contract).

38 On 13 March 2015, the Sale Contract completed and Hanwood received the amount of $3,267,154.95 (Settlement Proceeds).This amount was the balance of the purchase price outstanding after settlement adjustments and the earlier payment of the deposit of $363,000 (including GST) (Deposit). The Sale Proceeds were initially paid into the trust account of Patey & Murphy, the solicitors acting for Hanwood on the sale of the Property.

39 By an authority dated 18 March 2015, Mr Kelly directed Patey & Murphy to pay:

(a) $452,150.18 to each of Mr Nichols and Mr Somers (in aggregate $904,300.36) by payments to their companies PBN Property Investments Pty Ltd and AAJS Pty Limited;

(b) $43,183.17 to HDB for its services;

(c) $6,518.76 to Patey & Murphy for its tax invoice dated 13 March 2015; and

(d) $2,673,555.52, being the balance of the Settlement Proceeds and the Deposit (Net Sale Proceeds), to Hanwood.

40 Mr Kelly then caused Hanwood to make the Impugned Payments, in an aggregate amount of $1,925,341.64. Inexplicably, Hanwood alleges in its amended statement of claim and its closing submissions that the aggregate amount of the Impugned Payments was $2,425,350. It appears that Hanwood overlooked that the payments made by Mr Kelly from the Net Sale Proceeds included a $500,000 payment to Mr Renton. If the payment to Mr Renton is added to the alleged Impugned Payments identified below, the aggregate figure of the amounts disbursed by Mr Kelly from the Net Sale Proceeds increases to $2,425,341.64 (or, given the rounding in the figures in the amended statement of claim, the amount of $2,425,350, the precise amount alleged to be the aggregate of the Impugned Payments).

41 The Impugned Payments were alleged to comprise the following specific payments (noting that the $700,000 term deposit that ultimately found its way to Stintari has been included in the payments to the Stintari category rather than in the other payments category):

(a) $1,789,991.64 to Stintari in various tranches between 19 March 2015 and 15 June 2015 (Stintari Payments);

(b) $135,350 in other payments, comprising:

(i) a payment to TW Staines & Co on 25 March 2015 of $25,000 (Staines Payment);

(ii) two payments of $30,033 by cheque on 5 June 2015 to Mr Keith Hainsworth and Ms Phyllis Hainsworth, respectively (Hainsworth Payments); and

(iii) a payment to Ms Biba Zupan on 5 June 2015 of $50,284 (Zupan Payment);

(together, Other Payments).

42 At all material times, Mr Kelly was the sole director, secretary and sole shareholder of Stintari.

Procedural History

43 This matter has a long and complex procedural history. The proceeding as it relates to Mr Kelly, Mr Renton and Hanwood is set out below.

Application for preliminary discovery

44 By summons filed on 20 October 2017, Mr Renton and Dinomyte sought orders in the Supreme Court of New South Wales in the nature of preliminary discovery against Mr Kelly (Supreme Court proceedings). Mr Renton alleged that the orders were necessary due to “an inability to obtain relevant documents/information” from Mr Kelly and “the continued assertion by [Mr Kelly] that Renton was in possession of [Hanwood’s] books and records”: Renton v Kelly [2018] NSWSC 1377 (Renton) at [3] (Ward CJ in Eq, as her Honour then was). By the time the matter came before her Honour for determination, the documents sought under the summons had apparently been produced and the proceedings were dismissed by consent on 17 July 2018, save as to the question of costs: Renton at [13].

Application for reinstatement of Hanwood and commencement of derivative action

45 On 3 July 2019, Dinomyte and Mr Renton commenced proceedings by originating process in this Court against ASIC, seeking an order that ASIC reinstate Hanwood and for leave to commence proceedings in the name and on behalf of Hanwood against Mr Kelly, Stintari, Mr Nichols, HDB, Mr Somers, and his company, AAJS Pty Limited (proposed derivative action).

46 On 1 August 2019, Gleeson J ordered that ASIC reinstate Hanwood and on 29 August 2019 listed the application to commence the proposed derivative action for hearing on 6 September 2019. The hearing was initially stood over to 20 September 2019 and then subsequently to 27 September 2019.

47 At the hearing on 27 September 2019, Gleeson J granted leave for Mr Kelly to be heard in the proceeding without becoming a party and made orders that Hanwood be joined as the second defendant to the proceeding.

48 On 26 November 2019, Gleeson J delivered judgment in Dinomyte Pty Ltd v Australian Securities & Investments Commission, in the matter of Hanwood Pastoral Co Pty Ltd [2019] FCA 1989. Her Honour found that the evidence suggested that there may be a serious question to be tried, and granted leave to the plaintiffs to file further evidence in support of the application and a further draft statement of claim.

49 On 17 February 2020, Mr Kelly’s solicitors, Makinson d’Apice Lawyers, filed a notice of ceasing to act, which had been preceded by a notice of intention to cease to act filed on 5 February 2020.

50 The matter was listed for hearing before Gleeson J on 2 March 2020. There was no appearance by Mr Kelly. Justice Gleeson noted that Mr Renton and Dinomyte would indemnify Hanwood in respect of its costs of the proceeding and any adverse costs order, and ordered, inter alia, that leave be granted pursuant to s 237 of the Corporations Act to the plaintiffs to file the statement of claim and an amended originating process, and to serve a copy of the orders, the amended originating process and statement of claim on each of the defendants. Hanwood become the plaintiff, and the defendants now became, in order, Mr Kelly, Mr Somers, the Trustee for the MJS Trust, Mr Nichols, K G Nichols Holdings Pty Ltd and ASIC.

51 The second to fifth defendants filed a notice of appearance on 2 April 2020.

52 Mr Kelly did not file an appearance and orders were made on 6 April 2020 for substituted service on Mr Kelly.

Application for default judgment

53 Mr Kelly did not appear at a case management hearing on 28 May 2020. On that date Gleeson J made orders, inter alia, that Hanwood file and serve any application for judgment in default of any appearance by Mr Kelly, together with affidavits in support, by 18 June 2020.

54 On 18 June 2020, Hanwood filed an application for default judgment, seeking declarations that Mr Kelly had contravened a number of civil penalty provisions in the Corporations Act and orders that he compensate Hanwood for his alleged improper actions as a director in causing it to dispose of the sale proceeds of the sale of the Property.

55 On 7 July 2020, the application for a default judgment was heard by Rares J. There was no appearance by Mr Kelly.

56 Justice Rares delivered an ex tempore judgment: Hanwood Pastoral Co Pty Limited v Kelly [2020] FCA 1020 (default judgment).

57 Justice Rares found (at [18]) that a medical certificate dated 23 March 2020 from a general practitioner, Dr Chiew, which Mr Kelly had provided to the Court prior to the hearing on 7 July 2020, was out of date. Further, his Honour found that there was no evidence of any kind to support the granting of an adjournment, and Mr Kelly was well aware that the hearing had been set down for 7 July 2020.

58 Justice Rares found that Mr Kelly was in default of doing an act required to be done by the Federal Court Rules 2011 (Cth) (Rules), namely failing to file a defence, by not attending to hearing on 7 July 2020 or the case management hearing on 28 May 2020 after his solicitors had ceased to act, and in failing to defend the proceeding with due diligence.

59 His Honour ordered, inter alia, that Mr Kelly pay to Hanwood a sum of $1,398,967.62 inclusive of interest up to 7 July 2020 and that Mr Kelly pay Hanwood’s costs of the application for the default judgment. His Honour declared that Mr Kelly had improperly used his position as a director of Hanwood to gain an advantage for himself in contravention of s 182(1)(a) of the Corporations Act by removing Mr Renton as a director of Hanwood and causing ASIC to register on or about 20 May 2014 that Mr Renton had resigned as a director of Hanwood when, in fact, he had not resigned that office.

60 On 22 July 2020, Mr Kelly filed a notice of acting which appointed Mr Phillip Beazley of Beazley Lawyers to represent him.

Application to stay default judgment

61 On 24 July 2020, Mr Kelly filed an interlocutory application seeking an order that the default judgment be stayed, an order that the default judgment be set aside, an order that Mr Kelly be permitted to file a defence in the form annexed to the application and an order that Mr Renton pay the costs of the application.

62 The application was listed for hearing on 21 August 2020. Much of the argument was directed at who was in possession of the books and records the subject of the Supreme Court proceedings, Mr Kelly’s alleged difficulties in attending remote hearings, and alleged deficiencies in and the lateness of Mr Kelly’s defence.

63 At the conclusion of the hearing, Rares J made orders upon the undertaking of Mr Kelly by his solicitor not to reduce the current equity in, or otherwise dispose of, his real or personal property or other assets otherwise than by incurring reasonable medical, legal or usual and living expenses, without the leave of the Court until further order. His Honour ordered that the order of 7 July 2020 requiring payment by Mr Kelly to Hanwood of $1,398,967.62 be vacated and that Mr Kelly file his defence by 31 August 2020. His Honour further ordered that Hanwood prepare a statement on its recoverable costs, with those costs to be fixed on the papers. Finally, his Honour ordered that Mr Kelly provide Hanwood with the current bank or mortgage statements relating to the mortgage over his home and any other indebtedness (current financial records), also by 31 August, and a monthly list of his previous month’s expenses exceeding $1000.

64 On 26 August 2020, Mr Kelly filed a defence.

65 On 25 September 2020, Hanwood’s costs of the hearing on 21 August 2020 were fixed in the sum of $27,500. Justice Rares also made orders for Mr Kelly to give standard discovery on or before 9 October 2020.

66 On 16 October 2020, a case management hearing was held before Rares J, in which Mr Farrar appeared for Hanwood and Mr Beazley appeared for Mr Kelly. Mr Farrar informed Rares J that Mr Kelly had not produced the current financial records, the costs associated with setting aside the default judgment had not been paid, Mr Kelly had not complied with the order for discovery, and Stintari had not complied with a subpoena. Mr Beazley informed Rares J that Mr Kelly was in hospital.

67 On 6 November 2020, Justice Rares made orders for the filing and service of evidence of lay witnesses and expert evidence, and referred the matter to mediation before a Registrar.

Strike Out Application

68 On 12 May 2021, Hanwood filed an interlocutory application (Strike Out Application) seeking the following orders:

(a) Mr Kelly’s defence filed in August 2020 be struck out;

(b) Mr Kelly pay Hanwood the sum of $1,436,830.63 inclusive of interest up to 6 May 2021;

(c) Mr Kelly pay Hanwood’s costs of the proceedings; and

(d) in the alternative, an order that Order 3 made on 21 August 2020 (being that Mr Kelly was to pay Hanwood’s costs of the interlocutory application for default judgment) be varied so that the payment be made to Mr Renton and Dinomyte.

69 On 7 May 2021, orders were made by Rares J listing the Strike Out Application for hearing on 11 June 2021 and providing for the filing and service of evidence and written submissions.

70 On 14 May 2021, Rares J noted that the second to fifth defendants had entered into a confidential settlement agreement, and the proceeding as between Hanwood and those defendants were dismissed. The only two remaining defendants were Mr Kelly, the first defendant, and ASIC, the sixth defendant.

71 On 28 May 2021, the proceedings were transferred to my docket.

72 At 4.38 pm on 10 June 2021, Mr Beazley lodged a notice of ceasing to act with the Registry. Mr Beazley emailed my chambers at 5.07 pm on the same day, copying Mr Kelly and Mr Farrar, advising that the notice had been lodged but a filed copy had not yet been returned by the Registry. Mr Beazley stated that Mr Kelly had been advised of the hearing details (being the hearing of the Strike Out Application), but that Mr Kelly did not have new representation and Mr Beazley anticipated Mr Kelly would seek an adjournment of the hearing.

73 Mr Kelly did not file any submissions or evidence in opposition to the Strike Out Application.

74 At the hearing of the Strike Out Application on 11 June 2021, I granted leave for Mr Brett Kelly, Mr Kelly’s son, to appear on his behalf by Microsoft Teams for the purposes of making an adjournment application.

75 Mr Kelly was unable to tell me why he had not provided the current financial records, as ordered by Rares J on 21 August 2020. When asked about the utility of granting a three to four week adjournment, Mr Kelly informed me that he would do his best to comply with the Court orders, and that he would attempt to obtain alternative representation. Further, he alleged that Mr Beazley was in possession of the evidence that he wished to rely upon and he had been preparing subpoenas, and that he needed to recover that material. He further submitted that he was restricted by lack of funds and that he had asked Mr Beazley a number of times to apply to the Court to give him permission to borrow additional funds.

76 Mr Farrar, appearing for Hanwood, opposed the adjournment, citing the numerous previous extensions granted to Mr Kelly to comply with orders, and Mr Kelly’s non-compliance with orders, in particular the order that Mr Kelly provide monthly financial records for payments over $1000.

77 In part due to Mr Beazley’s late notice of ceasing to act, I ordered that the hearing of the Strike Out Application be stood over to 21 July 2021 to enable Mr Kelly to obtain legal representation and address his alleged defaults. I also made orders on that date for the parties to file and serve any affidavit evidence on which they sought to rely and that the costs of and incidental to the vacated hearing on 11 June 2021 be paid by Mr Kelly on an indemnity basis.

78 On 21 July 2021, Mr Kelly did not appear. Mr Alexander of counsel appeared for Mr Beazley to explain why more notice had not been given of his decision to cease acting for Mr Kelly on the evening before the date fixed for the hearing of the Strike Out Application. Mr Farrar appeared for Hanwood. Immediately prior to the hearing on 21 July 2021 the Court was provided with a facsimile from Mr Kelly containing financial information in purported compliance with the order made by Rares J on 21 August 2020 to produce the current financial records.

79 During the interlocutory hearing, I formed the view that, rather than proceeding with the Strike Out Application, the interests of justice would be better served by permitting the matter to proceed to a final hearing and for Hanwood’s claims to be determined on their merits. I formed that view principally for the following reasons:

(a) the lengthy and complex procedural history of the matter;

(b) Mr Kelly’s hearing difficulties that made it difficult for him to participate in electronic hearings;

(c) Mr Kelly’s inability at the time to access legal aid due to Mr Beazley remaining on the record;

(d) Mr Kelly being a self-represented litigant; and

(e) Mr Kelly appearing to have produced at least some of the sought-after financial records to address his alleged defaults.

80 I therefore listed the matter for a final hearing on 25 October 2021 with an estimate of two days. I further granted leave to Mr Beazley to file a notice of ceasing to act, dispensing with r 4.05(1) of the Rules, ordered that the determination of any personal liability of Mr Beazley for the costs thrown away by reason of the adjournment on 11 June 2021 be reserved, and further that the costs of the hearing set down for 21 July 2021 be reserved.

Pre-hearing case management

81 Mr Beazley’s notice of ceasing to act was eventually filed on 10 August 2021.

82 I conducted case management hearings in the proceedings on 18 August 2021, 1 September 2021, 24 September 2021, 7 October 2021 and 22 October 2021. Mr Kelly did not appear at the case management hearings held on 18 August 2021 and 1 September 2021 because they were conducted by Microsoft Teams. As COVID-19 restrictions eased I was able to make arrangements for the case management hearings on 24 September 2021, 7 October 2021 and 22 October 2021 to be “in person” hearings and Mr Kelly attended each of those case management hearings.

83 The case management hearings were principally concerned with Mr Kelly’s explanations of his unsuccessful applications for legal aid and pro bono assistance, his subsequent unsuccessful attempts to refinance his mortgage to obtain funds to secure legal representation and his ongoing medical conditions.

84 Mr Kelly made an application on 22 October 2021, being one business day before the hearing was to commence, for the hearing to be adjourned. Hanwood strongly opposed any application for adjournment.

85 I permitted Mr Kelly to make an oral application because he was a litigant in person but I had earlier explained to him that any application that he might make to adjourn the hearing needed to be supported by evidence.

86 I refused Mr Kelly’s application for an adjournment of the hearing as the only evidence provided in support of his application was evidence regarding his refinancing attempts, but this did not rise higher than preliminary approaches to financial institutions.

Further application for an adjournment

87 At the commencement of the hearing on 25 October 2021, Mr Kelly renewed his application for an adjournment. The application was again opposed by Hanwood.

88 I refused the renewed application by Mr Kelly.

89 The medical evidence on which Mr Kelly sought to rely was the medical certificate from Dr Chiew dated 23 March 2020 that had been provided to Rares J prior to the hearing of the Strike Out Application on 7 July 2020 and a further certificate from Dr Chiew dated 28 June 2021. The 28 June 2021 certificate stated that:

Mr Frederick Kelly suffers from diabetes, ischaemia heart disease, prostate cancer, previous operation for bowel cancer, hearing loss and a Whipple resection. All these conditions make it very hard for him to prepare for court and to provide evidence in a timely manner.

90 Also annexed to Mr Kelly’s affidavit was a health summary sheet dated 28 June 2021, which outlined the medications Mr Kelly was currently taking, his current medical conditions and past medical history. This evidence did not shed light on whether Mr Kelly was able to hear, or hear sufficiently well to be able to participate in a court proceeding in person. Given his lack of progress to date, I was not confident that finance would become available to Mr Kelly in the foreseeable future to allow him to instruct someone to represent him. Mr Kelly also pointed to documents he was trying to obtain from the Hunter Valley. I was not persuaded that those documents were critical, and the timeframe for obtaining those documents was indeterminate. Finally, I considered Mr Kelly’s demonstrated ability to communicate effectively, at least in writing, and the fact that it is not uncommon for parties to represent themselves at the hearing of commercial matters and that pro bono assistance is very unlikely in a commercial context, particularly where an asset could have been leveraged to obtain funding.

91 The original estimate of two days for the hearing to be conducted proved unduly optimistic. The initial stage of the hearing ultimately took place over three days, 25 to 27 October 2021, and an additional day, 3 December 2021, was set aside for closing submissions.

Application by Mr Kelly to reopen his case to adduce new evidence

92 On 9 November 2021, Mr Kelly sent an email to the Court which appeared to be an application to adduce further evidence from himself and Mr Nichols. Mr Kelly stated in his email (as written):

The Federal Court, through Justice Halley is requested to consider, in a reasonable and proper way, in the interest of “Natural Justice and Procedural Fairness” taking into account the unprecedented and extraordinary circumstances due to the enforced and restricted COVID 19 environment and make provision for the appearance and examination of [Mr Nichols] prior to any final determination of matter NSD 1053/2019.

93 In the email, Mr Kelly alleged that he had asked Mr Nichols to attend the hearing on 27 October 2021 at the “last minute”, and that Mr Nichols had not been able to attend due to appointments that he could not reschedule and the lockdown provisions in Maitland due to COVID-19 restrictions.

94 Mr Kelly also sought a deferral of the continuation of the hearing on 3 December 2021.

95 Hanwood opposed the application.

96 In the light of this communication from Mr Kelly, I listed the matter for a case management hearing on 19 November 2021. I granted leave to Mr Kelly to file his application in Court. Mr Kelly stated that the relevance of Mr Nichols’ evidence was that he had been involved as a consultant to Hanwood going back to the late 1990s and that his company provided details of contractors that were utilised on the site of the subdivisions. Further, he could verify payments made on behalf of Hanwood.

97 I rejected Mr Kelly’s application to defer the final hearing day due to the administration of justice requiring that the matter be dealt with expeditiously in the circumstances of Mr Renton’s ill-health. However, after taking into account that Mr Kelly was a self-represented litigant, his ability to conduct the hearing so far, difficulties imposed by the COVID-19 restrictions, and the apparent relevance of the evidence that Mr Kelly sought to adduce, I granted leave to Mr Kelly to reopen on the condition that the evidence be served in affidavit form prior to 3 December 2021, Mr Kelly make himself available for further cross-examination, and the costs thrown away by the application and the costs of and incidental to the case management hearing be paid by Mr Kelly, to be determined on a fixed sum basis shortly after delivery of this judgment.

98 Mr Kelly relied on an affidavit of Mr Nichols sworn on 29 November 2021 at the continuation of the hearing on 3 December 2021.

99 Mr Kelly also sought and was given leave to rely on a further affidavit from Ms Zupan (Mr Kelly’s carer) and affidavits from Mr Staines and Ms Louise Ellen Creighton (a former receptionist and personal assistant to Mr Nichols). At the same time Hanwood sought and was given leave to rely on an affidavit from Mr Renton’s wife, Mrs Isabel Vivienne Renton.

100 Mr Kelly did not seek to adduce any further evidence from himself.

101 On 3 December 2021, Mr Nichols and Ms Zupan were cross-examined. Mrs Renton was called as a witness by Mr Farrar but Mr Kelly stated he was not in a position to cross-examine her. Neither Ms Creighton nor Mr Staines were available to be cross-examined. Mr Farrar indicated that he did not wish to cross-examine Mr Staines and although he initially indicated that he wished to cross-examine Ms Creighton, he ultimately did not press for her to be cross-examined.

Supplementary submissions

102 At the conclusion of the hearing on 3 December 2021, I ordered that any supplementary submissions of Hanwood relating to issues that arose in the cross-examination of Mr Nichols and Ms Zupan, and the affidavits that were read of Mr Nichols, Ms Zupan, Ms Creighton and Mr Staines, be filed and served by 10 December 2021.

103 I also ordered that Mr Kelly file any supplementary submissions in response to Hanwood’s supplementary submissions, and any submissions addressing any issues that arose in the course of the cross-examination of Mrs Renton or in her affidavit, by 17 December 2021.

104 Hanwood filed its supplementary submissions on 10 December 2021.

105 On 17 December 2021, Mr Kelly sent an email to the Court outlining his various health issues and asking for an extension to file his supplementary submissions to 21 December 2021.

106 On the same day, I made orders that Mr Kelly file and serve his supplementary submissions by 21 December 2021.

107 On 21 December 2021, Mr Kelly sent the following email to the Court (as written):

The (1stD) advises due to ongoing problems, both ongoing uncontrollable medical and other matters associated with current covid restrictions, and the inability to obtain assistance as expected, The (1stD) is unable to comply with the established dead line and is endeavour to have the response available for submission by 4.30 tomorrow the 22nd December 2021 together with details that have contributed to they delasy.

108 On 22 December 2021, Mr Kelly sent an email to the Court which appeared to be a combination of submissions and further evidence.

109 On 24 December 2021, Mr Kelly sent a further email to the Court stating that he was preparing his supplementary submissions and requested “allowances” to be made by the Court. A further, similar, email was sent on 29 December 2021, stating that the final submissions would be submitted by no later than 7 January 2022.

110 On 1 February 2022, Mr Kelly sent another email to the Court, giving a relatively detailed summary of his current health issues, and health issues faced by Ms Zupan and requesting a further extension for filing his supplementary submissions until 9 February 2022.

111 I directed my chambers to advise Mr Kelly that any application for a further extension of time to file submissions pursuant to the orders made on 3 December 2021 must be made by way of interlocutory application and accompanied by affidavit evidence.

112 On 28 February 2022, the Registry received a facsimile from Mr Kelly attaching a medical certificate dated 26 February 2022 from St George Hospital, stating that (as written):

Mr Kelly is currently admitted as an inpatient at St George Hospital from the 18th of February requiring intravenous antibiotics for [a medical condition]. His estimate date of discharge is Monday 1st March.

113 The handwritten covering letter to the facsimile, signed by Mr Kelly on 26 February 2022, stated that on discharge from St George Hospital he would not be returning to “the Turramurra residence” for three to four days in case readmission to hospital was necessary. He further stated that the Court would be advised on his return to Turramurra. He also noted that he would not have access to email until his return to Turramurra.

114 Mr Kelly has not filed any interlocutory application for an extension to file his supplementary submissions and the Court has not received any further communication from Mr Kelly since 26 February 2022.

Evidence and credit findings

115 Hanwood relied on affidavit evidence from Mr Renton, Ms Sherwyn Lee, a solicitor employed by Mr Farrar, and an expert report from Mr Adam Blundell dated 26 March 2021 and filed on 6 April 2021. Hanwood also relied on an affidavit from Mrs Renton after Mr Kelly was given leave to reopen his case.

116 Mr Kelly initially relied on a statement that he verified when giving evidence and a statement from Ms Zupan. After he was given leave to reopen his case, Mr Kelly also relied on affidavits from Ms Zupan, Ms Creighton, Mr Staines and Mr Nichols.

Mr Renton

117 Mr Renton provided four signed but unsworn affidavits dated 18 June 2020, 12 August 2020, 17 August 2020 and 21 October 2021 that he verified when giving evidence at the hearing and an affidavit sworn on 9 October 2020. Mr Renton’s evidence was directed at Hanwood’s entry into the Consultancy Agreement, the circumstances in which he ceased to be a director of Hanwood, the extent of his knowledge of the sale of the Property, the disbursement of the Net Sale Proceeds by Mr Kelly and the steps taken by Mr Renton’s lawyers to obtain Hanwood documents from Mr Kelly. Mr Renton annexed to his affidavits most of the documents that were produced by Mr Kelly in response to orders for production or discovery. Mr Renton also gave evidence of the limited involvement he had in the development of the Property and the extent of his reliance on Mr Kelly to conduct the affairs of Hanwood.

118 Mr Renton is 89 years old and suffering from significant medical conditions. At the time he was being cross-examined he was recovering from femoral neck fracture and was taking nine separate medications, including two medications for pain relief. Perhaps understandably in the circumstances, his oral evidence was of limited assistance.

119 It was readily apparent from his demeanour in Court that Mr Renton had a deep antipathy towards Mr Kelly and that he found it difficult to focus on the questions that were being put to him. In the course of seeking to clarify some of his oral evidence, I had the following exchange with Mr Renton:

So Mr Kelly advised you that Hanwood should retain Mr Nichols, is that the case?---Yes. I – I think he actually did it and told us about it later.

Okay. He told you that he had retained Mr Nichols - - -?---Yes.

- - - for Hanwood?---Yes.

Did he tell you why he had retained Mr Nichols?---He said - - -

Sorry?---I beg your pardon?

Did he tell you why he had retained Mr Nichols?---To give him – not really, no.

Was it a matter of any interest to you as to why Mr Nichols had been retained?---Not particularly. It was, yes.

Well, did you think that it would involve the payment of any money by Hanwood to Mr Nichols?---Yes, well we left all that to Mr Kelly, you know, and he was handling it so our involvement was always after the events. So yes, if Mr Kelly - - -

Sorry? Sorry, did you just say if Mr Kelly told you that the company needed some money, you would pay the money?---Yes. We would pay, yes. I’ve forgotten the details but we always paid our bills.

When you say we paid our bills, is that Hanwood paying its bills?---That was – yes, it was personal debts or, like, it’s not personal debt. Yes, it’s just – yes. I can’t – can’t recall that. It’s all a bit vague. I spent, I’ve recently – recently spent six weeks in hospital and all of this is all a bit vague. So I’ve had most of my stomach removed, I’m – I’m just – just not up with it, I don’t think. Sorry.

120 Mr Renton’s difficulties in focusing on the issues on which he was being cross-examined was similarly evident when he was pressed about the circumstances in which he ceased to be a director of Hanwood:

MR KELLY: In relation to your resignation, Mr Renton, do you recall having a meeting whereby you produced your written resignation and explained to me the reason why?---Resignation for where? Resignation for where? From what?

You tabled your resignation and we had discussions as to why you wanted to resign at that time?---I can’t recall - - -

..... - - -?--- - - - any of this. I – I cannot recall any of this.

HIS HONOUR: Mr Kelly is asking you about your resignation as a director from Hanwood?---Of Hanwood. Of Hanwood.

And he’s asking you, do you recall producing a letter of resignation - - -?---I – I don’t recall what - - -

- - - from Hanwood and giving it to - - -?---I – I - - -

- - - Mr Kelly?---I – I don’t recall. What’s the relevance?

Don’t worry about the relevance. Just answer the questions that Mr Kelly - - -?---Yes. Thank you.

- - - is asking you.

MR KELLY: Your Honour, I – I think that it has got to a point where I’ve asked all the questions that I – are reasonable. There’s a lot of things that went on. I will just finally ask Mr Renton, do you recall the many times that we had discussions about the length of time I spent on – not just onsite and – and making decisions in relation to the development and kept you updated over a lengthy period of time, do you recall that I never got paid for that?---I – I – I – I actually do not recall that you never got paid. Every bill that you ever put in you were paid promptly onto – almost on the dot. I think that’s a complete furphy.

121 A matter that Mr Renton was at pains to stress throughout his cross-examination was that he left all matters affecting Hanwood to Mr Kelly. This was emphasised in the following exchange, when I was again seeking to clarify the evidence that Mr Renton had given about the proceedings that Hanwood had brought in the Land and Environment Court challenging the decision of the Cessnock City Council to revoke approval of the proposed sub-division of the Property:

So what did you leave to Mr Kelly, then?---We left it all to him.

When you say, “all”, what do you mean by, “all”?---Well, Harry [Terrett] and I didn’t have anything to – we left him in charge of it, you know what I mean?

Left in charge of what?---Yes. The – the whole – the whole purchase, the whole of the – the – the – we didn’t – Mr Kelly - - -

So the purchase of - - -?---Mr Kelly was handling - - -

Yes?--- - - - everything.

Well, when you say, “everything”, do you mean by that he was making all the decisions - - -?---Yes.

- - - for the company, for Hanwood?---Basically, yes.

And did that include obtaining finance to fund Hanwood’s operations?---Well, I’m not sure of that.

Well, when you said you left everything to him, did that include obtaining money to enable Hanwood to continue to operate?---Yes. He could have done.

So is it your evidence that you don’t know what money was obtained by Mr Kelly for the purpose of conducting the business of Hanwood?---That’s correct. That’s correct. I don’t know.

You left it entirely to Mr - - -?---Kelly, yes.

- - - Kelly?---Yes. Yes. Yes. We did.

Did Mr Kelly tell you from time to time what he was doing with Hanwood?---He did. But after – he did, yes.

122 In his affidavit, sworn on 21 October 2021, Mr Renton gave evidence of his current health conditions, the steps that he has taken to seek to understand what Mr Kelly had done with the proceeds of the sale of the Property and the financial impact to him of pursuing the proceedings against Mr Kelly.

Ms Lee

123 Hanwood also relied on an affidavit of Ms Lee sworn 15 October 2020. She was not cross-examined.

124 Ms Lee gave evidence of communications with Mr Kelly’s former solicitor, Mr Beazley, concerning the adequacy of Mr Kelly’s provision of financial records in compliance with the orders made by Rares J on 21 August 2020 for the production of financial records.

Mrs Renton

125 Mrs Renton is Mr Renton’s wife. She gave evidence, in her statement signed on 1 December 2021 and verified in the witness box on 3 December 2021, that she was with Mr Renton in Hawaii between 27 June 2013 and 14 July 2013 and annexed email communications that she had with Mr Kelly while she was in Hawaii about a meeting that Mr Kelly wished to have with Mr Renton on his return from Hawaii. Mrs Renton was not cross-examined.

Mr Kelly

126 Mr Kelly relied on a statement dated 5 February 2021, which he verified in the witness box on 26 October 2021. Mr Kelly gave evidence principally directed at the entry by Hanwood into the Consultancy Agreement, the resignation of Mr Renton as a director of Hanwood, the provision of funding by Stintari to Hanwood and the sale of the Property and the subsequent disbursement of the Net Sale Proceeds. At times, as I explain further below, Mr Kelly as a self-represented litigant found it difficult to appreciate the difference between submissions and evidence. In making findings of fact in these proceedings, I have only had regard to evidence given by Mr Kelly, either in his statement or in the course of his cross-examination, and I have not had regard to submissions that he has made that are not supported by any evidence.

127 Mr Kelly adopted a combative and belligerent stance throughout much of his cross-examination, as illustrated in the following exchanges with his cross-examiner, Mr Farrar:

MR FARRAR: Since Stintari was incorporated, have you been the sole director?---I – look, I would have to look. I may not have been for the first couple of years. I can’t remember that offhand.

Have you been the sole secretary?---Back when I was an accountant, I had clients. I had – there were hundreds of companies. I would have to do a search to find out exactly when I became a director and shareholder.

I’m not asking you about other companies. I’m asking you about Stintari, your company?---What I’m saying to you, I would have to go back and check to have the dates. No – if Stintari was incorporated, I think in about 1990. I can’t remember exactly.

128 Hanwood submits that the Court should have grave reservations regarding Mr Kelly’s credibility and the reliability of his evidence given the self-serving nature of his answers, his exaggerated difficulties in giving evidence, his overall capability to articulate himself in written form, the passage of time and his ill-health, and the fact that in the absence of a diary his evidence was based solely upon memory.

129 I accept that aspects of Mr Kelly’s evidence, including his explanations of when he commenced and ceased to practice as an accountant, his reluctance to answer questions directly, his tendency to become argumentative and his explanations for the delays in discovering documents, particularly in relation to the initial preliminary discovery orders, reflected adversely on his credit.

130 Nevertheless, I am satisfied that Mr Kelly was seeking to be truthful in his responses in the course of his cross-examination. At times, however, his stubbornness and understandable lapses in memory on questions of detail led him to give evidence that was implausible or to refuse to make concessions that otherwise appeared to be objectively compelling and appropriate. This was particularly evident in his evidence concerning the timing of the execution of the Consultancy Agreement by Mr Renton.

131 On balance, after taking into account the challenges faced by any self-represented litigant and Mr Kelly’s hearing difficulties and other medical issues, I am satisfied that Mr Kelly was generally seeking to give honest and truthful evidence, but his memory of relevant events was at times inconsistent with objective documentary evidence.

132 Moreover, Mr Kelly had an unfortunate tendency to be combative and make serious allegations of dishonest conduct on the part of others, including Mr John Holt, a former director, company secretary and shareholder of Hanwood and, even more concerning, against Mr Farrar. In many ways Mr Kelly was his own worst enemy and often did his cause no favours in his approach to the proceedings.

Ms Zupan

133 Ms Biba Zupan, described as Mr Kelly’s carer, gave a statement dated 5 February 2021 explaining the circumstances in which she came to lend Mr Kelly money. She was not cross-examined on this statement.

134 Ms Zupan gave evidence in her affidavit sworn on 29 November 2021 that Mr Kelly had left her house at Lugarno in Sydney for Maitland at approximately 6.00 am on 16 July 2021, contacted her at about 1.00 pm to inform her that his son was undergoing emergency surgery at Royal North Shore Hospital following a workplace accident and that Mr Kelly returned to her house at approximately 7.00 pm that evening. Ms Zupan was briefly cross-examined on this affidavit. Ms Zupan answered all questions directly and succinctly. I am satisfied that her answers were given truthfully to the best of her recollection.

Ms Creighton

135 Ms Creighton gave evidence in her affidavit sworn on 29 November 2021 that Mr Kelly had attended HDB’s offices in Maitland during the morning on 16 July 2013 to attend a meeting with Mr Nichols and Mr Somers but neither was present at that time. She stated that Mr Nichols returned to the office mid-morning and met with Mr Kelly. She recalled Mr Kelly then telling her that his son had had an accident and he had to leave. She otherwise confirmed that a contract was signed by Mr Somers and Mr Nichols on 17 July 2021 and that she then sent the signed contract to Mr Kelly. She was not available for cross-examination but her evidence was largely non-controversial except to the specific arrival time of Mr Kelly at HDB’s offices in Maitland on 16 July 2013. Hanwood contends that it was more likely, based on Mr Renton’s diary entries, to be early afternoon rather than in the morning.

Mr Staines

136 Mr Staines gave evidence, in his affidavit sworn on 30 November 2021, that Mr Kelly told him on or about 13 July 2013 that he was about to undergo urgent surgery on 17 July 2013 for the removal of his pancreas and that he would be recovering from the operation for at least three months. He also gave evidence that he had no record nor recollection of a visit from Mr Renton on behalf of Hanwood on 16 July 2013. Mr Staines was not cross-examined. The evidence was not controversial. Mr Renton did not suggest that he had any meeting with Mr Staines on 16 July 2013, only that he had met Mr Kelly at the offices of Mr Staines’ firm.

Mr Nichols

137 Mr Nichols is a director of HDB and a party to the Consultancy Agreement. He swore an affidavit on 29 November 2021 addressing the scope of the services provided by HDB in relation to the development of the Property and more specifically the consulting services that he and Mr Somers performed pursuant to the Consultancy Agreement. He was cross-examined.

138 Mr Nichols was an impressive witness. He answered questions that were put to him directly and succinctly and I was satisfied that he was telling the truth and not seeking to embellish his answers or otherwise act as an advocate for Mr Kelly.

Legal Principles

139 The relevant legal principles and statutory provisions were not in dispute.

Section 181(1) of the Corporations Act

140 Section 181(1) of the Corporations Act relevantly provides as follows:

181 Good faith—civil obligations

Good faith—directors and other officers

(1) A director or other officer of a corporation must exercise their powers and discharge their duties:

(a) in good faith in the best interests of the corporation; and

(b) for a proper purpose.

Note 1: This subsection is a civil penalty provision (see section 1317E).

141 The duty to act in good faith in the best interests of a corporation and for a proper purpose are conceptually separate duties, even if at times it is difficult to separate considerations relevant to each duty: Bell Group Ltd (In liq) and Others v Westpac Banking Corporation and Others (No 9) (2008) 39 WAR 1; [2008] WASC 239 at [4456] (Owen J).

142 Whether the duty to act in the best interests of the company is determined objectively or subjectively remains unsettled. Justice Black summarised the position in Re Colorado Products Pty Ltd (in prov liq) (2014) 101 ACSR 233; [2014] NSWSC 789 (Re Colorado Products) (at [420]) in the following terms:

The case law is divided as to whether a contravention of s 181(1)(a) of the Corporations Act requires that it be established that a director engaged deliberately in conduct which he or she knew was not in the company’s best interests: for example, Forge v Australian Securities and Investments Commission (2004) 213 ALR 574; 52 ASCR 1; [2004] NSWCA 448 at [245] per McColl JA (with whom Handley and Santow JJA agreed); Holyoake Industries [(Vic) Pty Ltd v V-Flow Pty Ltd] at [150], varied on appeal on another point in V-Flow [Pty Ltd v Holyoake Industries (Vic) Pty Ltd]. In Westpac Banking Corporation v Bell Group Ltd (in liq) (No 3) (2012) 44 WAR 1; [2012] WASCA 157 (Westpac Banking Corporation), the Court of Appeal of the Supreme Court of Western Australia unanimously held that the corresponding general law duty to act in good faith in the company’s best interests was subjective and would be complied with if directors honestly believed they acted in the company’s best interests: at [923] per Lee AJA at [1988] per Drummond AJA at [2027], [2772] and [2795] per Carr AJA. The alternative view is that a contravention of that limb of s 181 can be established if the law objectively considers that what the director did was improper, even if the director subjectively believed that he or she was acting in the company’s best interests: see, for example, Australian Growth Resources Corporation Pty Ltd v Van Reesema (1988) 13 ACLR 261 at 270–1; 6 ACLC 529 per King CJ; Mernda Developments Pty Ltd (in liq) v Alamanda Property Investments No 2 Pty Ltd (2011) 86 ACSR 277; [2011] VSCA 392 at [32]–[33]. The difference in those approaches does not seem to me to be material for the purposes of this case. The section may be contravened if a director promotes his or her personal interest in a situation where there is a conflict or real or substantial possibility of a conflict between those interests and the company’s interests: [Australian Securities and Investments Commission v] Adler at [735]; Parker at [72].

143 It is not necessary in the present case to express any definitive view on the differences in approach on this issue. I am satisfied for the reasons that I explain later in these reasons that Hanwood has not established that Mr Kelly has contravened s 181(1)(a) on either an objective or subjective basis.

144 The weight of authority indicates that the question of whether a director has acted for a proper purpose is to be determined objectively: In the matters of Earth Civil Australia Pty Ltd, RCG CBD Pty Ltd, Bluemine Pty Ltd, Diamondwish Pty Ltd and Rackforce Pty Ltd (all in liq) [2021] NSWSC 966 (Earth Civil) at [967] (Ward CJ in Eq, as her Honour then was); citing by way of example, Re Colorado Products at [421]; In the matter of HIH Insurance Limited and HIH Casualty and General Insurance Limited; Australian Securities and Investments Commission v Adler [2002] NSWSC 171 at [738]-[740] (Santow J); Australian Securities and Investments Commission v Somerville (2009) 77 NSWLR 110; [2009] NSWSC 934 at [38] (Windeyer AJ). Her Honour also referred to the distillation of the relevant principles by Ipp J, as his Honour then was, (with whom Seaman J and Malcolm CJ agreed) in Permanent Building Society (in liq) v Wheeler and Others (1994) 14 ACSR 109 at 137 as follows:

The principles applicable in determining whether directors of a company have acted for an improper purpose and in abuse of their powers are well settled. Relevantly, as regards the issues that arise in this case, it may be said that those principles are:

(a) Fiduciary powers and duties of directors may be exercised only for the purposes for which they were conferred and not for any collateral, or improper purpose.

(b) It must be shown that the substantial purpose of the directors was improper or collateral to their duties as directors of the company. The issue is not whether a management decision was good or bad; it is whether the directors acted in breach of their fiduciary duties.

(c) Honest or altruistic behaviour by directors will not prevent a finding of improper conduct on their part if that conduct was carried out for an improper or collateral purpose. Whether acts were performed in good faith and in the interest of the company is to be objectively determined, although statements by directors about their subjective intentions or beliefs will be relevant to that inquiry.

(d) The court must determine whether but for the improper or collateral purpose the directors would have performed the act impugned.

Section 182(1) of the Corporations Act

145 Section 182(1) of the Corporations Act relevantly provides:

182 Use of position—civil obligations

Use of position—directors, other officers and employees

(1) A director, secretary, other officer or employee of a corporation must not improperly use their position to:

(a) gain an advantage for themselves or someone else; or

(b) cause detriment to the corporation.

Note 1: This subsection is a civil penalty provision (see section 1317E).

146 The question of whether a director has used their position improperly to gain an advantage for themselves or another or to cause detriment to the corporation is to be assessed objectively: Earth Civil at [969] (Ward CJ in Eq, as her Honour then was) citing Re Colorado Products at [432]-[433]; Taxa Australia Pty Ltd v Wang (2018) 130 ACSR 531; [2018] NSWSC 1412 at [33] (Black J) and the following statement by Gleeson CJ (with whom Allen and James JJ agreed) in R v Towey (1996) 21 ACSR 46 at 57 that impropriety is established by:

a breach of the standards of conduct that would be expected of a person in the position of the alleged offender by reasonable persons with knowledge of the duties powers and authority of the position and the circumstances of the case.

147 It is not necessary for the relevant advantage or detriment sought be achieved in order to establish a contravention of s 182(1): Re Colorado Products at [433] (Black J).

Section 1317E of the Corporations Act

148 Section 1317E of the Corporations Act relevantly provides:

1317E Declaration of contravention of a civil penalty provision

Declaration of contravention

(1) If a Court is satisfied that a person has contravened a civil penalty provision, the Court must make a declaration of contravention.

(2) The declaration must specify the following:

(a) the Court that made the declaration;

(b) the civil penalty provision that was contravened;

(c) the person who contravened the provision;

(d) the conduct that constituted the contravention;

(e) if the contravention is of a corporation/scheme civil penalty provision—the corporation, registered scheme or notified foreign passport fund to which the conduct related;

149 Section 1317E(3) relevantly provides that ss 181(1) and 182(1) are corporation/scheme civil penalty provisions.

Section 1317H of the Corporations Act

150 Section 1317H relevantly provides as follows:

1317H Compensation orders—corporation/scheme civil penalty provisions

Compensation for damage suffered

(1) A Court may order a person to compensate a corporation, registered scheme or notified foreign passport fund for damage suffered by the corporation, scheme or fund if:

(a) the person has contravened a corporation/scheme civil penalty provision in relation to the corporation, scheme or fund; and

(b) the damage resulted from the contravention.

The order must specify the amount of the compensation.

Note: An order may be made under this subsection whether or not a declaration of contravention has been made under section 1317E.

Damage includes profits

(2) In determining the damage suffered by the corporation, scheme or fund for the purposes of making a compensation order, include profits made by any person resulting from the contravention or the offence.

…

151 As Gleeson J explained in Re IW4U Pty Ltd (in liq) and Others (2021) 150 ACSR 146; [2021] NSWSC 40 at [47]:

The words “resulted from” require a causal connection between the damage and the impugned conduct and do not import the more stringent test in equity for breach of fiduciary duty: Adler v Australian Securities and Investments Commission (2003) 46 ACSR 504; [2003] NSWCA 131 at [707]–[710]. It has been said that the common sense test of causation from March v E & M H Stramare Pty Ltd (1991) 171 CLR 506; 99 ALR 423; 12 MVR 353 whether loss would have occurred had there been no breach of duty, is applicable to s 1317H: Hydrocool Pty Ltd v Hepburn (No 4) (2011) 279 ALR 646; 83 ACSR 652; [2011] FCA 495 at [476]. Such an assessment may involve the positing of counterfactuals: see the remarks of Beach J in Australian Securities and Investments Commission v Mitchell (No 2) (2020) 382 ALR 425; 146 ACSR 328; [2020] FCA 1098 at [1778]–[1780], in the similar context of s 1317G.

Uncommercial Contracts Contravention

Submissions

152 Hanwood submits that the maximum amount that would have been appropriate to be paid for the services provided by the Consultants pursuant to the Consultancy Agreement was $50,000. It relies on the expert evidence of Mr Blundell.

153 Hanwood submits that Mr Renton’s knowledge of the Consultancy Agreement was limited to what he had been told by Mr Kelly, which was only that it was a standard document, Mr Kelly had reviewed it and Mr Renton did not need to seek any advice about it.

154 Mr Kelly gave the following evidence in his statement about the impact of the discovery of the critically endangered plants on the saleability of the Property and the proposed entry into the Consultancy Agreement:

64. When we put the road in off Hanwood Road, plants started to shoot up right in the roadway. What had happened was that by digging them up, it raised the seeds. Once that happened they said you can’t do any more roadwork for at least seven years and the rest of the seeds in the soil probably have a 15 year life. That was the only access you could get. You couldn’t sell the land. The development was dead in the water. The land was unsalable as a commercial site.

65. I went to real estate agents and said can we sell and they said we won’t waste our time because the first thing we have to tell people is that you can’t get a road and you can’t get access, so who’s going to buy it so that’s what commenced the discussions with Kerry Nichols, so if you read his write-up, also gives details of his history and experience. He had worked for two or three councils. He said the only thing, and the State government had changed the laws and made biodiversity credits available for certain circumstances. He said that the only possibility. If we can find somebody who needs credits then there’s a chance they might buy the land. That was the basis of going into the consultancy agreement.

66. They turned at a consultancy agreement. If you look at the details, it’s more like a joint-venture agreement, in other words they paid expenses. Their solicitor said consultancy agreement. I discussed as number of times with Renton, and he got the draft in April, and eventually we got the final agreement.

155 Hanwood submits in response to this evidence of Mr Kelly that there was no evidence that Mr Kelly approached anyone other than the Consultants to provide the “services” in connection with the sale of the Property, no evidence of any competitive tendering process nor any evaluation as to whether the services could be provided by anyone other than the Consultants, and Hanwood was deprived of the opportunity of obtaining the services from other providers, such as Mr Blundell, on “more competitive terms”.

The Consultancy Agreement

156 The scope of the services to be provided under the Consultancy Agreement was specified in the following clauses of the agreement:

2.1 In consideration of Hanwood entering into this Agreement the Consultants undertake to Hanwood to:-

2.1.1 observe and perform all and any of the Consultants’ obligations under this Agreement;

2.1.2 do all things reasonably necessary (including all studies) to meet the requirements of Government Authority to procure the recognition of the Land (or substantial parts thereof) as Environmental Land.

2.2 The Consultants aim to achieve each of the following objectives which are acknowledged by Hanwood:-

2.2.1 to undertake and to update flora and fauna studies for the Land to identify the full extent of Endangered Flora and Fauna so as to secure the Optimum Biodiversity Value;

2.2.2 consult with the Office of Environment and Heritage in order to have determined by the Office the environmental credits attributable to the Land so as to maximise the value of such environmental credits;

2.2.3 liaise and consult with the New South Wales National Parks to secure the inclusion or opportunity for inclusion of the Environmental Land as part of the adjacent National Park;

2.2.4 obtain such consents or approvals as may be necessary to subdivide the Land where the subdivision of the Land will permit separation (by way of separate lots) of:-

(i) Environmental Land;

(ii) rural residential land;

(iii) any other land classification;

where the aggregate value of the Land upon sale is optimised.

2.2.5 liaise with and seek the assistance of the Federal Environmental Department under the Environment Protection and Biodiversity Conservation Act to ensure compliance with relevant Federal Legislation;

2.2.6 formulate marketing strategy for the sale of the Land, or the parts thereof so as to maximise the value of the Land.

2.3 The Consultants will contribute each of the following:-

2.3.1 the funding of all costs necessary to identify and have recognised by Government Authorities the Environmental Land upon the basis they will recover those costs under clause 5;

2.3.2 their skill and expertise to secure the highest and best use of the Land, in terms of its final value, in accordance with this Agreement;

2.3.3 their expertise in environmental matters including securing the necessary reports and liaising with appropriate Government Authorities.

2.3.4 together with all necessary costs to achieve the objectives outlines in Clause 2.2.4

157 Further, cl 3.1 of the Consultancy Agreement provided that:

3.1 During the Environmental Assessment Phase, the Consultants must at their own cost:- ·

3.1.1 undertake all necessary studies and seek all necessary approvals and otherwise do all things necessary to achieve the environmental recognition;

3.1.2 at the time of lodging the document with the Government Authority to effect the environmental changes, notify Hanwood and provide particulars to Hanwood.

3.2 The Environmental Planning Phase commences on the date of this Agreement and concludes on the date upon which the Office of Heritage and Environment, in conjunction with the Consultants, determine the Optimum Biodiversity Value, including the concurrence of the New South Wales National Parks if required.

158 The allocation of the proceeds of the sale of the Property was addressed in cl 5 of the Consultancy Agreement in the following terms:

5.1 Hanwood, upon completion of the Land Sale Agreement, shall deposit the sale proceeds into a joint account in the names of Hanwood and the Consultants.

5.2 The parties shall cause the sale proceeds to be applied as follows:-

5.2.1 firstly, to pay any costs incurred on the sale of the lot;

5.2.2 secondly, to the Australian Taxation Office that amount as represents any GST received on the sale; in accordance with under the Income Tax Assessment Act

5.2.3 thirdly, to the Consultants to reimburse the Consultants the Consultants’ Expenses;

5.2.4 fourthly, to pay the Base Landholder Sum to Hanwood;

5.2.5 thereafter, the remaining funds shall be paid as follows:-

(i) as to an amount as represents 40% of the balance to the Consultants jointly as Consultancy Fees together with the GST applicable thereto;

(ii) as to any balance to Hanwood.

5.3 At the completion of the Project a reconciliation is to be made of the distribution of the sale proceeds with the intention that:-

5.3.1 all GST will be correctly accounted for;