Federal Court of Australia

Reeves v Nulis Nominees (Australia) Limited (Trustee) [2022] FCA 627

ORDERS

DATE OF ORDER: | 1 June 2022 |

THE COURT ORDERS THAT:

1. The appeal be dismissed.

2. The applicant pay the third and fourth respondents’ costs of the appeal.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

NICHOLAS J:

Background

1 The applicant brings this appeal under s 1057(1) of the Corporations Act 2001 (Cth) (“Corporations Act”) against the decision of the second respondent (“the Authority”) dated 16 February 2021 (“the Authority’s decision”) affirming the decision of the first respondent (“the Trustee”) to distribute a death benefit of approximately $400,000 to the parents of the late Trent James Seary (“the deceased”). Pursuant to orders made on 21 April 2021 the deceased’s parents, Paul and Marie Seary (“Mr and Ms Seary”) were joined as the third and fourth respondents to this proceeding.

2 Section 1057(1) of the Corporations Act provides that a party to a superannuation complaint may appeal to the Federal Court, on a question of law, from the Authority’s determination of the complaint. By the Authority’s decision in this case it rejected the applicant’s complaint concerning the decision of the Trustee to distribute the death benefit to Mr and Ms Seary.

3 The deceased died on 25 December 2017 while holidaying on Norfolk Island with the applicant. He was, at that time, a member of the MLC Superannuation Fund of which the first respondent was the Trustee. The Trustee was obliged to determine who would receive the death benefit payable as a result of the death of the deceased in accordance with the terms of the relevant Trust Deed (“the Deed”).

The Trust Deed

4 It is common ground that the deceased did not nominate a dependant beneficiary or legal personal representative and that, consequently, the Trustee was required to pay the death benefit in accordance with cl 13.6(h) of the Deed. Clause 13.6(h) provides:

If the Trustee is required to pay or has decided to pay a Death Benefit, or a portion of a Death Benefit, to a Legal Personal Representative of a Member and a Legal Personal Representative is not appointed, or the Trustee is unable to identify the Legal Personal Representative, within 90 days of the date of death or any later date the Trustee considers reasonable, the Trustee must pay the whole or the part of the Death Benefit:

(1) to such one or more of the Dependants of the Member; or

(2) if none, to any other person or persons in accordance with the Relevant Law, as the Trustee determines.

5 The expression “Relevant Law” is defined in the Deed to include:

any present or future law of Australia, a State or Territory of Australia or a foreign jurisdiction which the Trustee determines to be a Relevant Law for the purpose of this deed.

Relevant Legislative Provisions

SIS Act

6 The Deed provides that the word “dependant” is to be given the same meaning as in the Superannuation Industry (Supervision) Act 1993 (Cth) (“the SIS Act”).

7 Section 10 of the SIS Act defines “dependant” as follows:

dependant, in relation to a person, includes the spouse of the person, any child of the person and any person with whom the person has an interdependency relationship.

8 The word “spouse” is defined by s 10 of the SIS Act to mean:

spouse of a person includes:

(a) another person (whether of the same sex or a different sex) with whom the person is in a relationship that is registered under a law of a State or Territory prescribed for the purposes of section 2E of the Acts Interpretation Act 1901 as a kind of relationship prescribed for the purposes of that section; and

(b) another person who, although not legally married to the person, lives with the person on a genuine domestic basis in a relationship as a couple.

9 The term “interdependency relationship” is defined in s 10A of the SIS Act as follows:

10A Interdependency relationship

(1) Subject to subsection (3), for the purposes of this Act, 2 persons (whether or not related by family) have an interdependency relationship if:

(a) they have a close personal relationship; and

(b) they live together; and

(c) one or each of them provides the other with financial support; and

(d) one or each of them provides the other with domestic support and personal care.

(2) Subject to subsection (3), for the purposes of this Act, if:

(a) 2 persons (whether or not related by family) satisfy the requirement of paragraph (1)(a); and

(b) they do not satisfy the other requirements of an interdependency relationship under subsection (1); and

(c) the reason they do not satisfy the other requirements is that either or both of them suffer from a physical, intellectual or psychiatric disability;

they have an interdependency relationship.

(3) The regulations may specify:

(a) matters that are, or are not, to be taken into account in determining under subsection (1) or (2) whether 2 persons have an interdependency relationship; and

(b) circumstances in which 2 persons have, or do not have, an interdependency relationship.

10 Regulation 1.04AAAA of the Superannuation Industry (Supervision) Regulations 1994 (Cth) (“the SIS Regulations”) provides:

1.04AAAA Interdependency relationships (Act s 10A)

(1) For paragraph 10A(3)(a) of the Act, the following matters are to be taken into account in determining whether 2 persons have an interdependency relationship, or had an interdependency relationship immediately before the death of 1 of the persons:

(a) all of the circumstances of the relationship between the persons, including (where relevant):

(i) the duration of the relationship; and

(ii) whether or not a sexual relationship exists; and

(iii) the ownership, use and acquisition of property; and

(iv) the degree of mutual commitment to a shared life; and

(v) the care and support of children; and

(vi) the reputation and public aspects of the relationship; and

(vii) the degree of emotional support; and

(viii) the extent to which the relationship is one of mere convenience; and

(ix) any evidence suggesting that the parties intend the relationship to be permanent;

(b) the existence of a statutory declaration signed by one of the persons to the effect that the person is, or (in the case of a statutory declaration made after the end of the relationship) was, in an interdependency relationship with the other person.

(2) For paragraph 10A(3)(b) of the Act, 2 persons have an interdependency relationship if:

(a) they satisfy the requirements of paragraphs 10A(1)(a) to (c) of the Act; and

(b) one or each of them provides the other with support and care of a type and quality normally provided in a close personal relationship, rather than by a mere friend or flatmate.

Examples of care normally provided in a close personal relationship rather than by a friend or flatmate:

1. Significant care provided for the other person when he or she is unwell.

2. Significant care provided for the other person when he or she is suffering emotionally.

(3) For paragraph 10A(3)(b) of the Act, 2 persons have an interdependency relationship if:

(a) they have a close personal relationship; and

(b) they do not satisfy the other requirements set out in subsection 10A(1) of the Act; and

(c) the reason they do not satisfy the other requirements is that they are temporarily living apart.

Example for paragraph (3)(c): One of the persons is temporarily working overseas or is in gaol.

(4) For paragraph 10A(3)(b) of the Act, 2 persons have an interdependency relationship if:

(a) they have a close personal relationship; and

(b) they do not satisfy the other requirements set out in subsection 10A(1) of the Act; and

(c) the reason they do not satisfy the other requirements is that either or both of them suffer from a disability.

(5) For paragraph 10A(3)(b) of the Act, 2 persons do not have an interdependency relationship if 1 of them provides domestic support and personal care to the other:

(a) under an employment contract or a contract for services; or

(b) on behalf of another person or organisation such as a government agency, a body corporate or a benevolent or charitable organisation.

These provisions were reproduced by the Authority in a section of its reasons for decision entitled “Relevant Law”.

Corporations Act

11 The Corporations Act provides that a person may make a complaint to the Authority relating to superannuation under the Australian Financial Complaints Authority scheme, established under Pt 7.10A (see the definitions in s 761A). Relevantly, if the complaint is that the trustee of a regulated superannuation fund (such as the trustee here) has made a decision relating to a particular member or former member of the fund that is or was unfair or unreasonable (s 1053(1)(a)), the Authority has, subject to s 1055, all of the powers, obligations and discretions conferred on the trustee who made the decision to which a complaint relates.

12 Section 1055 of the Corporations Act authorises the Authority (referred to in the legislation as AFCA) to make a determination in relation to a superannuation complaint. Section 1055 of the Corporations Act provides:

(1) In making a determination of a superannuation complaint, AFCA has, subject to this section, all the powers, obligations and discretions that are conferred on the trustee, insurer, RSA provider or other person who:

(a) made a decision to which the complaint relates; or

(b) engaged in conduct (including any act, omission or representation) to which the complaint relates.

Affirming decisions or conduct

(2) AFCA must affirm a decision or conduct (except a decision relating to the payment of a death benefit) if AFCA is satisfied that:

(a) the decision, in its operation in relation to the complainant; or

(b) the conduct;

was fair and reasonable in all the circumstances.

(3) AFCA must affirm a decision relating to the payment of a death benefit if AFCA is satisfied that the decision, in its operation in relation to:

(a) the complainant; and

(b) any other person joined under subsection 1056A(3) as a party to the complaint;

was fair and reasonable in all the circumstances.

Varying etc. decisions or conduct

(4) If AFCA is satisfied that:

(a) a decision (except a decision relating to the payment of a death benefit), in its operation in relation to the complainant; or

(b) conduct;

is unfair or unreasonable, or both, AFCA may take any one or more of the actions mentioned in subsection (6), but only for the purpose of placing the complainant, as nearly as practicable, in such a position that the unfairness, unreasonableness, or both, no longer exists.

(5) If AFCA is satisfied that a decision relating to the payment of a death benefit, in its operation in relation to:

(a) the complainant; and

(b) any other person joined under subsection 1056A(3) as a party to the complaint;

is unfair or unreasonable, or both, AFCA may take any one or more of the actions mentioned in subsection (6), but only for the purpose of placing the complainant (and any other person so joined as a party), as nearly as practicable, in such a position that the unfairness, unreasonableness, or both, no longer exists.

(6) AFCA may, under subsection (4) or (5), do any of the following:

(a) vary the decision;

(b) set aside the decision and:

(i) substitute a decision for the decision so set aside; or

(ii) remit the decision to the person who made it for reconsideration in accordance with any directions or recommendations of AFCA;

…

Limitations on determinations

(7) AFCA must not make a determination of a superannuation complaint that would be contrary to:

(a) law; or

(b) subject to paragraph (6)(c), the governing rules of a regulated superannuation fund or an approved deposit fund to which the complaint relates; or

(c) subject to paragraph (6)(d), the terms and conditions of an annuity policy, contract of insurance or RSA to which the complaint relates.

13 The Authority has power under s 1055(6) to vary, set aside and substitute a decision or remit the matter to the decision-makers, but must not make a determination that would be contrary to law (s 1055(7)). The Authority must give reasons for its decision (s 1055A).

14 This Court’s jurisdiction in relation to a determination under s 1055 arises under s 1057 which relevantly provides:

1057 Appeals to the Federal Court from determination of superannuation complaint

(1) A party to a superannuation complaint may appeal to the Federal Court, on a question of law, from AFCA’s determination of the complaint.

…

(3) The Federal Court is to hear and determine the appeal and may make such order as it thinks appropriate.

(4) Without limiting subsection (3), the orders that may be made by the Federal Court on an appeal include:

(a) an order affirming or setting aside the determination of AFCA; and

(b) an order remitting the matter to be determined again by AFCA in accordance with the directions of the Court.

(5) The Federal Court must not make an order awarding costs against a complainant if the complainant does not defend an appeal instituted by another party to the complaint.

Other Provisions

15 In submissions, counsel for the applicant made repeated references to s 2CA, 2D and 2F of the Acts Interpretation Act 1901 (Cth) (“Acts Interpretation Act”). In circumstances where it is common ground that the applicant was not legally married to the deceased, s 2CA of that Act has no application. Nor does s 2D or 2F have any application in circumstances where the term “de facto partner” is not used in any statutory provision relevant to the appeal.

The Trustee’s Decision

16 The Trustee’s decision is recorded in a document dated 17 October 2018 which determined that 50% of the deceased’s superannuation balance of $401,117.34 (representing the proceeds of the death benefit) should be paid to each of Mr and Ms Seary. The documentation produced by the Trustee notes the material that was relied on by its officers in arriving at that decision but does not include any detailed statement of reasons.

17 On 26 November 2018 the applicant’s solicitors notified the Trustee that she objected to the Trustee’s decision. Officers of the Trustee conducted an internal review. The Trustee’s decision was affirmed following that internal review. The applicant lodged a complaint with the Authority on 30 May 2019 in respect of the Trustee’s decision.

The Authority’s decision

18 The Authority identified the issues and its key findings at para 1.2 of its reasons. The first issue identified (the dependency issue) was whether the applicant was a dependant of the deceased at the date of his death. The Authority found that the applicant was not a dependant. The second issue identified by the Authority (the reasonableness issue) was whether the Trustee’s decision was fair and reasonable. The Authority found that the Trustee’s decision was fair and reasonable.

The dependency issue

19 The Authority noted that the applicant claimed to be the deceased’s “de facto spouse and interdependent [sic]”. In addressing the dependency issue the Authority’s reasons show that it noted cl 13.6(g) of the Deed and the definition of “dependant”. It should be observed that the Authority plainly recognised that the definition of “dependant” is not exclusive and that “… it also includes someone who was financially dependent on the person”.

20 The Authority observed:

In order to be considered for payment of the death benefit of the benefit as a dependant, the complainant had to satisfy the relevant definition of spouse, be in an interdependency relationship with the deceased member at the date of his death or be a financial dependent of the deceased member at the date of his death.

21 It is therefore apparent that the Authority considered that there were three possibilities in play:

the applicant was a dependant because she was the deceased’s de facto spouse (see definition of “dependant” and “spouse”);

the applicant was a dependant of the deceased because of their “interdependency relationship” (see definition of “dependant”, definition of “interdependency relationship” and reg 1.04AAAA); and

the applicant was a dependant of the deceased because she was financially dependent on him (see definition of “dependant”).

22 The Authority referred to what it characterised as “conflicting evidence about the nature and status of the relationship”. Its reasons include a detailed summary of evidence relied on by the applicant and Mr and Ms Seary. These included statutory declarations made by them together with declarations made, or letters written, by various relatives and friends. That material included five statutory declarations made by the applicant which provided her account of her relationship with the deceased, including details of their social, emotional and financial relationship. Amongst other things the applicant claimed in her statutory declarations that she was the spouse of the deceased and financially dependent on him. She produced various financial records which were relied upon by her to show that the deceased provided her with financial support and that he promised to continue to do so after she was made redundant on 21 December 2017.

23 The Authority noted that the applicant claimed that she and the deceased both had a mutual commitment to a shared life and that the deceased had committed to support her financially, that he had plans to marry her and have children, and to purchase a home to live in together.

24 The Authority went on to observe that the evidence given by Mr and Ms Seary demonstrated that the relationship was volatile and that the deceased was not necessarily committed to it. The Authority noted that the deceased was said by friends and family to have intended to end the relationship when he returned from his holiday with the applicant and that he was not interested in a committed relationship which involved them living together. The Authority referred to evidence which showed that the applicant and the deceased kept separate residences as their dogs did not get along, spent time together during the week which ranged from between two and four nights a week, and were known to one another’s family. The evidence also showed that the deceased also made some transfers to the applicant’s bank account during their relationship.

25 The Authority went on to refer to the various factors which “should be present to establish a relationship as a spousal relationship”. These factors were said by the Authority to include the duration of the relationship; the nature and extent of a common residence; whether or not a sexual relationship existed; the degree of financial dependence or interdependence; ownership, use and acquisition of property; the degree of mutual commitment to a shared life; the care and support of children; and the reputation and public aspects of the relationship. In reaching its decision the Authority dealt with each of the eight factors to which it referred and concluded that “the evidence does not support a spousal relationship”.

26 The Authority then considered whether the complainant was in an interdependency relationship with the deceased. The Authority noted that the factors to be considered are “very similar to the factors for a de facto relationship with the addition of whether the relationship was intended to be permanent and whether the relationship was one of mere convenience”. For reasons already considered in relation to a spousal relationship, the Authority concluded that the requirements for an interdependency relationship were not met. The Authority also found that none of the statutory exceptions to the applicant and deceased living together were met. The Authority also concluded that the applicant was not a financial dependant of the deceased for reasons considered in relation to the spousal relationship.

The reasonableness issue

27 The Authority considered whether the Trustee’s decision was fair and reasonable. At para 2.3 of its reasons the Authority said:

2.3 Was the decision of the trustee fair and reasonable?

Trustee based its distribution on rules of intestacy

If there are no dependants and no LPR, the trustee is permitted to pay the death benefit to such individuals as it determines. As the trustee did not consider the deceased member had any dependants and he did not have an LPR, it determined to pay the death benefit equally to both parents.· The trustee has explained that it was guided by the rules of intestacy in the Succession Act 1981.

I note the death certificate is a NSW death certificate and the death occurred on Norfolk Island. I accept that similar reasoning in relation to the rules of intestacy would apply in NSW also.

While it was open to the trustee to consider the complainant in its distribution to nondependent individuals, as the deceased member’s girlfriend, I accept that it was within the range of what is fair and reasonable for the trustee not to make an apportionment to her on the basis of intestacy provisions. If the parents had applied for letters of administration, the trustee would have had to pay the death benefit to them as LPRs and they would have shared in the benefit equally, so a direct distribution to them was consistent with this outcome.

I am satisfied on the evidence before AFCA that the proposed distribution of the death benefit to the parents was open to the trustee.

The trustee’s decision was fair and reasonable

Where a trustee has a discretion in the distribution of a death benefit, there can be a range of decisions that might be considered fair and reasonable in the circumstances. Under section 1055(3) of the Corporations Act 2001, AFCA must by law affirm a decision if it determines it is within the range of what is fair and reasonable in the circumstances.

While I accept there was a relationship between the complainant and deceased member, I do not consider it was more than that of boyfriend and girlfriend. I acknowledge that they may have been working toward a spousal relationship, but the objective evidence as a whole does not indicate that it had reached that point at the date of the deceased member’s death. I am not satisfied the complainant met the definition of dependant at the date of the deceased member’s death.

The trustee’s decision to pay the death benefit to the deceased member’s parents in equal shares was fair and reasonable in its operation in relation to the complainant and the joined parties, in all the circumstances.

Questions of Law

28 The subject matter of the applicant’s appeal, and its scope, are confined to a question or questions of law. For that reason it is important that the question or questions of law be stated with precision. Further, the notice of appeal, either in the questions of law postulated, or in any accompanying grounds of appeal, should indicate why it is that, if the question of law is answered in the way for which the applicant contends, the appeal should be allowed and other consequential orders sought by the applicant made. The authorities recognise that it may sometimes be appropriate, particularly in appeals brought by self-represented litigants, to afford some latitude in relation to the precision with which the relevant question of law is identified. It may even be appropriate in some cases for the Court to formulate the question in appropriate terms when it is apparent from either the notice of appeal or the applicant’s submissions that a question of law does arise. See generally Haritos v Federal Commissioner of Taxation (2015) 233 FCR 315 (Haritos).

29 The applicant purports to identify in her amended notice of appeal 16 questions of law said to arise from the Authority’s decision. There are difficulties with the way in which the questions of law have been framed in this case. For example, ground 1 implicitly asserts that a question of law arises out of the Authority’s decision because a relevant definition appearing in the Deed was misinterpreted or misapplied by the Authority. The difficulty with ground 1 is that it does not identify the alleged error nor does it disclose any link between the alleged error and the Authority’s decision.

30 Other questions of law relied on by the applicant suffer from the same vice. In the circumstances, I have looked beyond the notice of appeal to the applicant’s written and oral submissions for the purpose of identifying any particular error of law that the applicant can rely on. That task has been made more difficult than it need have been due to the failure on the part of the applicant to clearly identify the provisions said to have been misinterpreted or misapplied and those parts of the Authority’s decision in which the postulated error is said to be disclosed. I propose to work through the postulated questions sequentially. Before doing so it is necessary to refer to some important principles.

31 First, of course a pure question of fact does not involve or raise any question of law. However, a mixed question of fact and law may do so if the question is whether the facts as found are within the scope of a statutory provision. However, special considerations apply when the relevant statute uses words according to their common understanding and the question is whether the facts as found fall within those words: see Hope v Bathurst City Council (1980) 144 CLR 1 at 7 per Mason J. In that situation the question that arises is likely to be one of fact rather than law. Whether or not the words used should be given some different meaning may itself constitute a question of law.

32 Secondly, the jurisdiction arising under s 1057 of the Corporations Act is limited to the question or questions of law arising out of the Authority’s decision: see Haritos at [85]. In that case the Full Court referred with approval to the following passage in the judgment of the Full Court in Brown v Repatriation Commission (1985) 7 FCR 302 at 304:

The existence of a question of law is not merely a qualifying condition to ground an appeal from a decision of the Tribunal; rather, it and it alone is the subject matter of the appeal, and the ambit of the appeal is confined to it. Although it is necessary in some appeals pursuant to s 107VZZH for this Court to consider the evidence before the Tribunal (for example, where the alleged question of law is that there is no evidence upon which the Tribunal could reasonably support its finding) the court should be cautious before embarking on its own analysis of the evidence where the task of assessing facts has been placed by the legislature in the hands of specialist bodies such as the Tribunal and the Commission which are equipped to deal with them.

33 As the High Court observed in Repatriation Commission v Owens (1996) 70 ALJR 904 (Brennan CJ, Gaudron and Gummow JJ) at 904 when refusing special leave to appeal in a case involving administrative review by the Administrative Appeals Tribunal:

The purpose of limiting an appeal to a question of law is to ensure that the merits of the case are dealt with not by Federal Court but by the Administrative Appeals Tribunal. This distribution of function is critical to the correct operation of the administrative review process.

34 Thirdly, merely to assert that a question of law arises is not to state a question of law: Haritos at [92]-[93]. Whether the appeal raises a question of law is a matter that must be addressed as a matter of substance. As the Full Court said in Haritos at [94]:

In our opinion, the issue must be approached as one of substance. In cases of doubt, the Court should consider the notice of appeal, the alleged question or questions of law, the grounds raised, the statutory context, and the Tribunal’s reasons for its decision, and having considered all those matters, satisfy itself that there is in fact a question of law.

As I will explain, most of the questions that the applicant describes as questions of law either do not in fact arise or are properly characterised as questions of fact.

35 Fourthly, a finding of fact may be affected by an error of law if the Authority has failed to take into account a relevant matter, or had regard to an irrelevant matter, or if the decision is unreasonable in the legal sense of that word: Sharp Corporation of Australia Pty Ltd v Collector of Customs (1995) 59 FCR 6 at 12-13 per Davies and Beazley JJ (with whom Hill J agreed). In a passage approved by the Full Court in Haritos, Davies and Beazley JJ said at 12-13:

Thus, it is primarily a question of fact, not of law, as to what is the meaning of an ordinary English word or phrase as used in a statute in its ordinary sense and so also is the question whether, there being different conclusions reasonably open, a particular set of facts comes within the description of such a word or phrase. This principle was enunciated in detail and explained by Jordan CJ in Australian Gas Light Co v Valuer-General (1940) 40 SR (NSW) 126 at 137-138 and by Mason J in Hope v Bathurst City Council (1980) 144 CLR 1 at 7-8. The principle was followed by Beaumont and Burchett JJ in Jedko Game Co Pty Ltd v Collector of Customs (NSW) (unreported, Federal Court, 10 March 1987); noted 12 ALD 491.

Even so, in any particular decision, although the decision may be a factual one, all the usual grounds of review will apply for they are regarded as being illustrative of questions of law. Thus a decision-maker may have failed to provide procedural fairness or may have failed to take into account a relevant fact, or may have had regard to an irrelevant matter or the decision may have been so unreasonable that no reasonable decision-maker could have come to it. Examples where Courts have inquired under these principles into the facts found by administrative decision-makers are Commissioner of Taxation (Cth) v McCabe (1990) 26 FCR 431; Bushell v Repatriation Commission (1992) 175 CLR 408.

If the decision-maker adopts a wrong approach to the task, the decision may be set aside and the matter remitted for reconsideration. See Times Consultants Pty Ltd v Collector of Customs (Qld) (1987) 16 FCR 449 and Waterscheid Australia Pty Ltd v Collector of Customs [sc. Walterscheid Aust Pty Ltd v Collector of Customs (1988) 14 ALD 785; (1988) 7 AAR 555]. This may occur if the decision-maker has not applied the well-understood ordinary meaning of a term but has given to it a meaning or qualification of his or her own or if, in the application of terms such as “income”, “capital” and “incurred” which appear in the Income Tax Assessment Act 1936 (Cth) and the term with which we are now concerned, “essential character”, all of which have been the subject of exposition in reasons of courts, the decision-maker adopts a meaning contrary to that which has been established by legal decisions.

In Commissioner of Taxation v Roberts (1992) 37 FCR 246, the issue fell within the fifth proposition enunciated in Pozzolanic. In Minister for Industry and Commerce v Zyfert (1983) 77 FLR 471, the words of the Tariff which were in question took on a meaning from the context in which they appeared and therefore the construction of the Tariff was in issue. In cases of the latter type, which may involve mixed questions of fact and law, it is necessary to identify whether the administrative decision-maker is alleged to have made an error of law or an error of fact.

(Emphasis added in Haritos at [126])

Those paragraphs illustrate the breadth of the jurisdiction based on the existence of a question of law. For present purposes it is important to note that no question of law arises if on analysis what is alleged to be an error in deciding a mixed question of fact and law involves merely an error of fact not affected by any related error of law. For this reason what might appear to be a question of mixed fact and law (and therefore a question of law) may not give rise to a question of law if on analysis it is apparent that the alleged error was essentially an error in fact finding.

Question 1

Whether the definitions in the trust deed were applied when determining if the applicant was the deceased’s de facto partner or in an “interdependency” relationship with him at the date of his death and therefore his dependant.

36 Question 1 does not identify the error said to give rise to the question of law. It does not identify any definition said to have been misinterpreted or misapplied and does not explain why it was that the Authority was required to determine “… if the applicant was the deceased’s de facto partner”.

37 The applicant drew attention to the definitions in the Acts Interpretation Act of “de facto partner” in s 2D and “de facto relationship” in s 2F. However, neither of those terms is used in the Deed or any of the relevant statutory provisions referred to in it. In those circumstances the Authority was not required to apply those definitions for the purpose of determining whether the applicant was a spouse of the deceased. To the extent the applicant says that the Authority erred in failing to apply or have regard to those definitions, I do not accept that the Authority made any error.

38 The applicant drew attention in her written submissions to the definition of “spouse” in s 10 of the SIS Act which includes “another person who, although not legally married to the person, lives with the person on a genuine domestic basis in a relationship as a couple”. However, it is clear that the Authority had regard to those words and considered whether they described the relevant living arrangements and relationship. Having explicitly identified and considered factors that may support a conclusion that “two people live with each other on a genuine domestic basis in a relationship as a couple” the Authority concluded that the evidence did not support such a conclusion in this case.

Question 2

Whether, in order for the applicant to come within the definition of “dependent” [sic] in the trust deed it was necessary for her to be financially dependent on the deceased and living with him continuously at the same residence at the date of his death.

39 This question appears to be founded on a misinterpretation of the Authority’s reasons.

40 The Authority did not hold that in order to come within the definition of “dependant” as used in cl 13.6(h) of the Deed, it was necessary for the applicant to show that she was financially dependent on the deceased or living with him continuously at the same residential residence at the date of his death.

41 The Authority found that the evidence did not show that either the applicant or the deceased considered either of their homes to be a shared, common residence. What the Authority said was this:

The complainant’s legal representative has provided a number of cases, which he says indicate a couple can maintain separate residences and still be considered to be in a de facto relationship.

While I acknowledge the complainant and deceased member stayed at one another’s home and that this could have extended to storing belongings at the respective homes, the evidence provided to AFCA does not support the complainant or deceased member considered either of their homes to be a shared, common residence.

42 I do not think the Authority’s reasons can be understood as suggesting that it was necessary for the purposes of determining whether the applicant and the deceased lived together, that they lived continuously at the same residence. Rather, I understand the Authority to have accepted that, though a couple may live together in more than one residence, that would not be an accurate characterisation of the applicant’s and the deceased’s living arrangements in this case. Consistent with its broader conclusion, I understand the Authority to have concluded that the applicant and the deceased spent time at each other’s houses, but did not live together. Indeed this seems to be the principal basis on which, based on the Authority’s findings, no “interdependency relationship” existed.

43 As to financial dependence, the Authority properly directed itself to the meaning of dependant, but focused on the matter of financial dependence because this was the form of dependency upon which the applicant’s claims and evidence focused. This was relevant to both the question of whether the applicant was financially dependent on the deceased and also whether there was an interdependency relationship between them.

44 The Authority’s reasons set out the definition of “dependant” and include a note which states that “because the definition is not exclusive and therefore takes its natural meaning, it also includes someone who was financially dependent on the person”. It was not suggested that note is incorrect or otherwise discloses error. The Authority’s interpretation of the word dependant, as is evident from the note, explains why it was necessary for the Authority to consider whether the applicant was financially dependent on the deceased.

45 With regard to financial dependence, the Authority said:

The complainant has submitted bank statements, which show transfers from the deceased member between October 2016 until December 2017. A number of the transfers are for repayment in relation to holiday bookings and hotels, concert tickets and a sporting event. The deceased member also made a number of loans to the complainant and there is one transfer that relates to a ‘Bill’. There are two transfers relating to ‘shopping’ in October and December and two small transfers for ‘stuff’ in December 2017.

The complainant’s legal representative has taken exception to the transfers for the holiday bookings and entertainment not being included in the assessment of the complainant's financial dependence. However, the concept of financial dependence generally requires the provision of regular financial contributions of specified amounts for everyday living expenses, even if the amounts are small. Further, the purpose of a superannuation death benefit is to provide for a deceased member’s dependants who were receiving financial support and might reasonably have expected to continue to receive financial support from the deceased member, had they not died. In this complaint, the majority of the transfers related to discretionary expenses and were not related to the living expenses of the complainant. The small transfers, which related to ‘shopping’ and ‘stuff’, occurred in late 2017 and were not regular in nature.

The complainant says she was made redundant on 21 December 2017 and that the deceased member promised to look after her financially. He said in a text message ‘we will get through this’. Whether the deceased member’s text message referred to financial support is not conclusive, as he passed away a few days later and there is no other evidence the deceased member provided or planned to provide for the complainant financially after her redundancy.

On the evidence provided, I am not satisfied there was a level of regular financial support being provided by the deceased member at the date of his death or that the complainant was financially dependent upon the deceased member in the required sense.

46 With regard to the statement that “…the concept of financial dependence generally requires the provision of regular financial contributions of specified amounts for everyday living expenses, even if the amounts are small”, the applicant’s written submissions suggested that this statement was wrong as a matter of law. I do not agree.

47 First, the significance of the word “generally” is not to be overlooked. The Authority was not purporting to apply an inflexible or absolute test as to what might constitute financial support. Secondly, the statement must be read in the context of the claims made by the applicant. The evidence submitted by the applicant included bank transfers from the deceased relating to what was described as “shopping” and “stuff” in late 2017 (the deceased died in December 2017), which the Authority noted were small and not regular in nature. The fact that the transfers were small, not regular in nature, and not related to living expenses, was a matter relevant to the question of whether the applicant was financially dependent on the deceased.

48 In any event, the applicant’s submissions in relation to what was said to be the evidence of her financial dependence, clearly involved a challenge to the Authority’s factual conclusion. Whether the applicant was financially dependent on the deceased was primarily a question of fact involving the meaning of an ordinary English word (“dependant”) as used in the relevant definition.

49 While it may be accepted that a question of law may arise out of what is properly characterised as a mixed question of fact and law, there is no basis to conclude that the Authority committed any legal error in its approach to the question of whether the applicant was financially dependent on the deceased which could be said to have affected its appraisal of the relevant evidence.

50 The question whether a person is financially dependent on another will usually involve factual questions involving matters of context and degree including, as in this case, the nature and frequency of financial contributions made. That the deceased did not contribute regularly to the applicant’s day to day living expenses (rather than expenses such as concerts or holidays) was a matter that the Authority was entitled to give some weight in determining whether the applicant was financially dependent on the deceased.

Question 3

Whether in order to come within the definition of “dependent” [sic] in the trust deed it was necessary for the applicant to be financially dependent on the deceased at the date of his death and ‘financially dependent’ in the sense that he was providing her with ‘regular financial contributions of specified amounts of everyday living expenses, even if the amounts [were] small.’

51 This question also appears to be founded on a misinterpretation of the Authority’s reasons. The Authority did not decide the matter on the basis that financial dependence could only arise if there were “regular financial contributions of specified amounts of everyday living expenses” made by the deceased to the applicant. As explained above, the nature and frequency of the expenditure was relevant to the question of whether the applicant was financially dependent on the deceased.

52 The form of question 3 implicitly acknowledges that the Authority considered the nature of the financial contributions of the deceased, and therefore the question should be regarded as whether the Authority weighed that evidence properly. This is not a question of law.

Question 4

Whether the deceased’s payment of the couple’s holiday and entertainment expenses was irrelevant to the question of whether the applicant was the deceased’s “dependent” [sic] because such expenditure was unrelated to her living expenses.

53 This question also appears to be founded on a misinterpretation of the Authority’s reasons. The Authority did not find that the payment of holiday and entertainment expenses was irrelevant to the question of whether the applicant was financially dependent on the deceased. The Authority considered the payments made in respect of holiday and entertainment expenses but was not persuaded that the evidence was sufficient to establish that the applicant was financially dependent on the deceased. The Authority did not make the error which the applicant seeks to attribute to it in question 4.

Question 5

Whether the definition of dependent [sic] in the trust deed required that two people live together continuously at the one residence or consideration of the nature and extent of their common residence.

54 This question also appears to be founded on a misinterpretation of the Authority’s reasons. It suggests that the Authority approached the definition of “dependant” on the basis that the applicant and the deceased must have lived together continuously in one residence. I have already considered this in relation to question 2 and it is clear that the Authority did not approach the definition of dependant in that way. Its reasons recognise that a person may be financially dependent on another person even though they do not continuously live together.

55 If this question is to be understood as suggesting that the Authority did not consider the nature and extent of common residence it is clear that the Authority did consider this matter, although it did so primarily in the context of the applicant’s claim that the applicant and the deceased were in a spousal relationship. The nature and extent of their common residence was the second of the eight factors identified and considered by the Authority as relevant to the question whether the applicant was the deceased’s spouse. It was a matter for the authority to determine what weight it would give to the applicant and the deceased’s residential arrangements in determining whether or not the applicant was his dependant.

Question 6

Whether in determining if the applicant was in a de facto relationship with the deceased at the date of his death the following circumstances regarding their relationship should have been taken into account pursuant to section 2F subsection (2) of the Acts Interpretation Act 1901(AIA): the nature and extent of their common residence; the degree of financial dependence or interdependence and any arrangements for financial support between them in addition to the other circumstances listed in subs (2) and without any of the circumstances being regarded as requirements of a de facto relationship.

56 As previously explained, s 2F of the Acts Interpretation Act defines the term “de facto relationship” for the purposes of s 2D(b) of that Act. Neither s 2F nor s 2D of the Acts Interpretation Act has any application in this case. Nevertheless, it may be observed that reg 1.04AAAA, in specifying the matters to be taken into account in determining whether there is an interdependency relationship, refers in para 1(a) to some (but not all) of the matters referred to in s 2F(2) and some others that are not referred to. The argument that s 2F of the Acts Interpretation Act applied or that the Authority was required to determine whether the applicant and the deceased were in a “de facto relationship” as defined by s 2F is untenable.

Question 7

Whether in determining if the applicant was in an “interdependent relationship” with the deceased at the date of his death within the meaning of the trust deed matters that should have been taken into account were not taken into account including the applicant’s statutory declaration to the effect that she was in such a relationship and her evidence that the reason why she and the deceased did not live together continuously at the same residence was their dogs (Superannuation Industry (Supervision) Regulations 1994 see Reg 1.04 AAA[sic]).

57 The suggestion here seems to be that in determining whether the applicant was in an interdependent relationship with the deceased the Authority failed to take the applicant’s evidence into account. The only matters identified in question 7 which it is alleged the Authority failed to take into account is the applicant’s statutory declaration in which she asserted that they were in such a relationship and her explanation as to why she and the deceased did not live together continuously at the same place of residence.

58 There is no doubt that the Authority had regard to the applicant’s statutory declarations, the applicant’s and the deceased’s living arrangements, and the explanation she proffered as to why they did not occupy one residence. Both the applicant’s statutory declaration and her explanation with regard to the relevant living arrangements were expressly referred to in the Authority’s reasons. The Authority did not make the error which the applicant seeks to attribute to it in question 7.

Question 7A

Whether in determining if the applicant was in an “interdependency relationship” with the deceased at the date of death the first respondent/ombudsman failed to consider the requirements of an interdependency relationship, stating the requirements were the same or similar to the requirements for a de facto relationship – that he had already considered them when determining if there was a spousal relationship and determined they had not been met. It was therefore unnecessary to consider them again (determination at p.9).

59 In considering whether the applicant and the deceased were in an “interdependency relationship” the Authority drew specific attention to s 10A of the SIS Act and reg 1.04AAAA of the SIS Regulations. It noted that the regulation specifies the various factors to be taken into account in determining whether there is an interdependency relationship. It also noted that those “… factors are very similar to the factors for a de facto relationship, with the addition of whether the relationship intended to be permanent and whether the relationship was one of mere convenience”. In referring here to “a de facto relationship”, it is possible that the Authority was referring to the definition of “de facto relationship” in s 2F of the Acts Interpretation Act which applies if (inter alia) a couple “have a relationship as a couple living together on a genuine domestic basis”. In any event, that appears to be very much in the nature of an incidental remark. Importantly, the Authority also said (at p 9):

I am not satisfied that the complainant was in an interdependency relationship such that it would satisfy the criteria necessary as outlined in the regulations. The requirements are similar to those for a spousal relationship and, as I have outlined above, I am not satisfied that they were met. In addition, the complainant and the deceased member were not living together and none of the statutory exceptions to this requirement are met.

60 The suggestion seems to be that because the Authority referred to its earlier findings in relation to whether or not there was a spousal relationship, it was necessary for the Authority to further explain why it did not consider that the deceased and the applicant were not living together or that she was not financially dependent on the deceased. The Authority’s findings in relation to both of those matters were fatal to the applicant’s claim based on the existence of an interdependency relationship: see s 10A(1). With regard to living arrangements, the Authority correctly noted that none of the statutory exceptions to s 10A(1) in s 10A(2) applied. The Authority therefore concluded that it was not satisfied the applicant and the deceased were in an interdependency relationship such as would make her a dependant under the “SIS regulations”. I think it is clear that the latter reference is a slip and should instead refer to s 10 of the SIS Act. This error is immaterial and of no consequence. In any case, there is no substance to the criticism of the Authority’s reasons implicit in question 7A.

61 There was considerable attention given in the applicant’s submissions to what was said to be the Authority’s failure to determine whether the applicant and the deceased were in a “close personal relationship” as required by s 10A(1)(a) of the SIS Act. It is clear that the Authority had regard to the nature of the relationship between the applicant and the deceased which it characterised as no more than that of boyfriend and girlfriend. Although it did not make any express determination as to whether the applicant and deceased were in a “close personal relationship” it was not necessary for the Authority to do so given its other findings.

Question 8

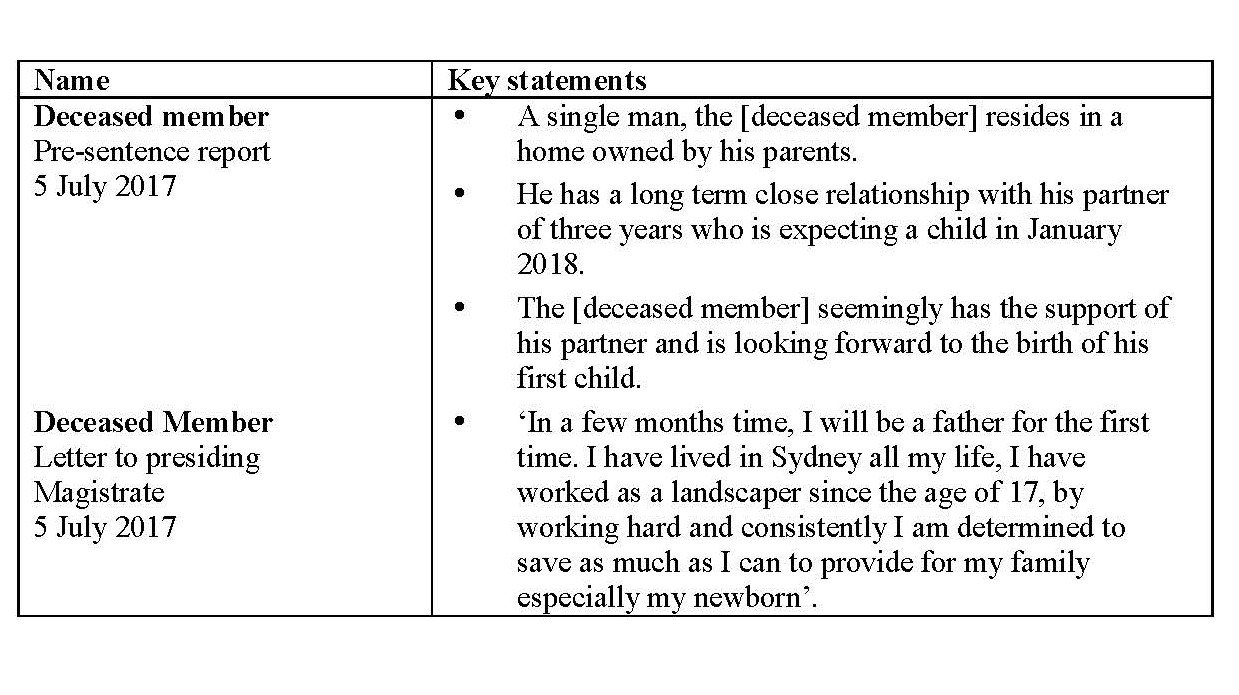

Whether it can be inferred that AFCA’s determination of the applicant’s complaint was unfair or unreasonable or both given the information the deceased provided about their relationship in text messages and in July, 2017 (which was five months before his death) when he was charged with mid-range PCA. He told authorities that his address and “home” was the property the applicant leased and lived in at Greenfield Park – that he had been “driving home following a phone call from his partner who was concerned for her health” – that he had “a long term close relationship and his partner of three years was expecting a child in January 2018” ... – that he had “the support of his partner and [was] looking forward to the birth of his first child.” In his signed written statement addressed to the Liverpool Local Court dated 6 July, 2017 the deceased said: “In a few months time, I will be a father for the first time. By working hard and consistently I am determined to save as much as can [sic] to provide for my family especially my newborn.” (see documents obtained from Liverpool Local Court).

62 The Authority’s reasons include a summary of what it described as “key statements”. Relevant to question 8 is the following account of the material that was before Liverpool Local Court in July 2017 when the deceased was dealt with for a drink driving offence:

63 The Authority referred to the applicant’s evidence extensively including material presented to the Local Court in July 2017. Its reasons show that it was aware that the applicant suffered a miscarriage sometime thereafter and that the applicant claimed that she and the deceased wanted to have a child. However, the Authority also had before it other material which it also had to consider. The Authority said (at p 7):

However, the statutory declarations and statements provided by the deceased member’s father indicates the relationship was volatile and the deceased member was unsure of its future. The deceased member’s commitment has also been put into question by some of the statements from his friends, which indicate he was in fact seeing other women and the [sic] he did not want to commit or have a live-in partner. Statements from the deceased member’s friends indicate the relationship changed significantly after the miscarriage.

Although the complainant believes that she was the deceased member’s de facto spouse and it may have been that the couple were working toward a shared life, I am not satisfied at the date of the deceased member’s death there was in fact a mutual commitment to a shared life.

64 The Authority was required to determine whether the Trustee’s decision was fair and reasonable. It is important to note that these words are not to be understood in this context as postulating that the decision be fair and reasonable in the sense those terms are used in the context of a challenge to an administrative decision based on the concept of legal unreasonableness: cf Minister for Immigration and Citizenship v Li (2013) 249 CLR 332. The Authority was instead required to determine whether the Trustee’s decision was fair and reasonable in accordance with the ordinary meaning of those words.

65 It is not the role of the Court to embark on any consideration of whether the decision was fair and reasonable except in so far as the Authority’s decision might be characterised as legally unreasonable and therefore beyond power. Question 8 does not appear to me to do more than seek to contest the correctness of the Authority’s decision by way of impermissible merits review. As the Authority noted in its reasons (at p 10) “there can be a range of decisions that might be considered fair and reasonable in the circumstances”. I do not consider that its conclusion with respect to what was fair and reasonable in the circumstances of this case was affected by an error of law or that question 8 raises a question of law in the relevant sense.

Question 9

Whether the information provided by the deceased to Liverpool Local Court in July 2017 and the failure to apply the provisions in the deed demonstrate that the trustee and AFCA were clearly wrong in concluding the [sic] that the applicant was not the deceased’s dependent and that she did not have a “fair and valid claim to the benefit”.

66 Implicit in this question is the suggestion that the Authority failed to apply the provisions of the Deed. I do not think there is any substance to that complaint. Further, as discussed in the context of question 8, there was a considerable body of evidence before the Authority besides the information provided at Liverpool Local Court which indicated that the applicant was not a dependant of the deceased. In light of the additional material, the Authority’s decision cannot be said to be “clearly wrong” or, more importantly, affected by error of a kind giving rise to a question of law in the relevant sense.

Questions 10, 11, 12, 13 and 15

The trustee determined that because the deceased had no dependent and no legal representative it was entitled to pay the death benefit to any person who had a fair and valid claim to the benefit and that the parents had [sic] fair and valid claim because under the law of intestacy they would be entitled to the benefit as next of kin.

The decision to pay the benefit to the deceased’s parents was not fair and reasonable because it was not possible to conclude that they would be entitled to the benefit as next of kin.

Under the law of intestacy in NSW the deceased’s de facto spouse (which was what the applicant claimed to be) would be entitled to the whole of his estate and his parents entitled as next of kin only if he left no de facto spouse and whether the applicant came within the definition of de facto spouse under NSW law had not been determined, the trustee having applied a different meaning of de facto spouse under the deed to that which applied in NSW where in order for a person to be the de facto spouse of another person it is not necessary for the person to be financially dependent on the other person or to reside full time with the other person at the same residence.

Whether it was fair and reasonable not to consider the applicant when determining who had a fair and valid claim to the benefit.

Whether it would be an error of law to treat the law of intestacy as determinative of how the superannuation death benefit should be distributed.

67 It is convenient to deal with these questions together because they all appear to relate to the final step in the Authority’s reasoning. For the purposes of addressing the substance of the complaints made by the applicant it is necessary to refer to some additional legislative provisions not previously referred to in these reasons or in the Authority’s reasons.

68 It is apparent that the Authority reasoned that because there was no legal personnel or representative the Trustee was obliged to pay the Death Benefit to one or more of the deceased’s dependants, or if there were no dependants, to any other person or persons in accordance with the “Relevant Law”. It is also apparent that the Authority was satisfied that the deceased did not have any dependants.

69 The Trustee reasoned that since the deceased died intestate, if Mr and Ms Seary had applied for letters of administration, the Trustee would have been obliged to pay the death benefit to them, that in those circumstances they would have shared in the benefit equally, and that a direct distribution to them was consistent with this outcome. The Authority considered that the Trustee’s approach was open to it and that the decision to distribute the death benefit in that manner was fair and reasonable.

70 The relevant intestacy provisions are found in the Succession Act 2006 (NSW) (“the Succession Act”). Section 128(1) of the Succession Act states that the parents of an intestate are entitled to the whole of the intestate estate if the intestate leaves no spouse and no issue. It is apparent that the Authority considered that this provision would apply in this case with the consequence that Mr and Ms Seary, as the deceased’s parents, would be entitled to the whole of the estate.

71 The term “spouse” as used in s 128 is defined in s 104. Section 104 refers to “domestic partnership” which is itself defined in s 105. Sections 104 and 105 provide:

104 Spouse

A spouse of an intestate is a person—

(a) who was married to the intestate immediately before the intestate’s death, or

(b) who was a party to a domestic partnership with the intestate immediately before the intestate’s death.

105 Domestic partnership

A domestic partnership is a relationship between the intestate and another person that is a registered relationship, or interstate registered relationship, within the meaning of the Relationships Register Act 2010, or a de facto relationship that—

(a) has been in existence for a continuous period of 2 years, or

(b) has resulted in the birth of a child.

72 Relevant to the facts of the present case, the question is whether the applicant and the deceased were in a de facto relationship at the date of his death that had been in existence for a continuous period of two years.

73 The expression “de facto relationship” is defined in s 21C of the Interpretation Act 1987 (NSW) to mean as follows:

…

(2) Meaning of “de facto relationship” For the purposes of any Act or instrument, a person is in a de facto relationship with another person if—

(a) they have a relationship as a couple living together, and

(b) they are not married to one another or related by family.

A de facto relationship can exist even if one of the persons is legally married to someone else or in a registered relationship or interstate registered relationship with someone else.

(3) Determination of “relationship as a couple” In determining whether 2 persons have a relationship as a couple for the purposes of subsection (2), all the circumstances of the relationship are to be taken into account, including any of the following matters that are relevant in a particular case—

(a) the duration of the relationship,

(b) the nature and extent of their common residence,

(c) whether a sexual relationship exists,

(d) the degree of financial dependence or interdependence, and any arrangements for financial support, between them,

(e) the ownership, use and acquisition of property,

(f) the degree of mutual commitment to a shared life,

(g) the care and support of children,

(h) the performance of household duties,

(i) the reputation and public aspects of the relationship.

No particular finding in relation to any of those matters is necessary in determining whether 2 persons have a relationship as a couple.

…

74 For the applicant to be in a “de facto partnership” with the deceased, it was necessary for her to show that they had “a relationship as a couple living together”. The nine matters referred to in paras (a)-(i) of s 21C(3) to be considered in determining whether the persons concerned have “a relationship as a couple” include the eight matters that were considered by the Authority when determining whether they lived together on a genuine domestic basis in a relationship as a couple.

75 As previously discussed, the Authority observed that the evidence did not support the conclusion that either the applicant or the deceased considered either of their homes to be a shared common residence and that they were not living together. It necessarily follows that the applicant and the deceased were not, in the opinion of the Authority, in a relationship as a couple living together. That being so, I do not consider that the Authority can be said to have made any error of law in concluding that if Mr and Ms Seary had obtained letters of administration, the Trustee would have had to pay the death benefit to them and they would have shared in the benefit equally.

76 For completeness I should note that the applicant contended in submissions that the Authority’s decision involved an error of law because the Authority considered that a couple could only live together if they did so in one residence. It is clear from the Authority’s reasons that it did not approach this issue in that way. The Authority expressly averted to the possibility (at p 5) that there could be a “spousal relationship” despite the fact that the applicant and the deceased lived apart on those nights that they did not spend together.

Question 14

Whether AFCA erred at law in concluding there was no evidence the applicant had an expectation of future financial support from the deceased because she was not financially dependent on him and his text messages to her when she was made redundant (stating “we will get through this together”) were not evidence he promised or planned to look after her financially (at p.9).

77 This is another question that appears to be based on a misunderstanding of the Authority’s reasons. The Authority made express reference to the text message in which the deceased said to the applicant that “we will get through this together”. The Authority said of this text message that it was not conclusive, as the deceased passed away a few days later, and there is no other evidence that he provided or planned to provide for the applicant financially after her redundancy. The proposition that there was such other evidence was not developed in either the applicant’s written or oral submissions. It was for the Authority to evaluate the text message, and consider whether or not it evinced an intention on the deceased’s part to provide the applicant with financial support. Neither the question itself nor the applicant’s submissions identify any question of law arising out of the Authority’s consideration of the text message or any other evidence relevant to the matter of financial support.

Disposition

78 In my opinion the applicant has failed to identify any error of law capable of giving rise to a question of law which, if answered in the applicant’s favour, would entitle the Court to make any order under s 1057 of the Corporations Act. This is because the Authority did not make any of the legal errors that the applicant sought to attribute to it. The appeal will be dismissed. The applicant must pay Mr and Ms Seary’s costs.

I certify that the preceding seventy-eight (78) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Nicholas. |