Federal Court of Australia

Woodhouse (Liquidator), in the matter of Forex Capital Trading Pty Ltd (in liq) [2022] FCA 600

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 90-15 of the Insolvency Practice Schedule (Corporations) (IPS) (being Schedule 2 to the Corporations Act 2001 (Cth)), the plaintiffs are deemed to have complied with reg 5.6.48(2)(b) and reg 5.6.48(3) of the Corporations Regulations 2001 (Cth) (Regulations) by taking the following steps:

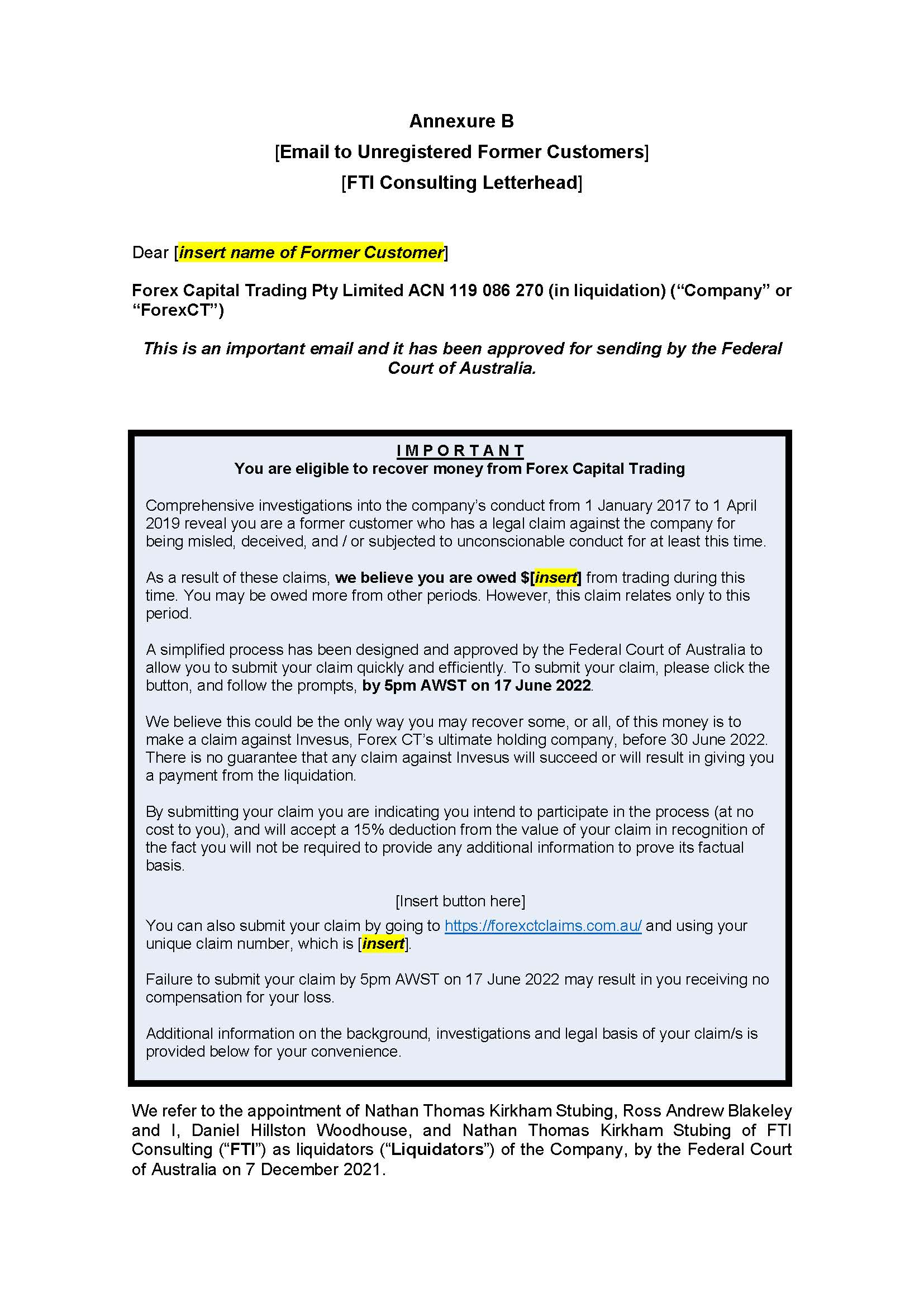

(a) distributing an email in substantially the same form as Annexure A to these orders to all former customers of the Company who have registered their potential claims against the Company and provided their email addresses (Registered Former Customers);

(b) distributing an email in substantially the same form as Annexure B to these orders to all the email addresses of all former customers of the Company who deposited money with the Company between 1 January 2017 and 1 April 2019 and who are not Registered Former Customers (Unregistered Former Customers), as those email addresses appear in the Company's books and records;

(c) distributing a letter in substantially the same form as Annexure C to these orders to all the postal addresses of all Registered Former Customers as those addresses appear in the Company's books and records;

(d) distributing a letter in substantially the same form as Annexure D to these orders to all the postal addresses of all Unregistered Former Customers as those addresses appear in the Company's books and records;

(e) publishing a notice in substantially the same form as Annexure E to these orders at the website maintained by the plaintiffs in respect of the Company;

(f) within seven days of sending the emails referred to in orders 1(a) and 1(b) above, publishing a notice in substantially the same form as Annexure F to these orders in the following newspapers:

(i) The Australian; and

(ii) The Australian Financial Review.

2. The notices set out in Annexures A to F are to provide a link to a copy of the Former Customer Claim Form in substantially the same form as Annexure G to these orders.

3. Pursuant to s 90-15 of the IPS the Liquidators are not required to take any further action if there is no response to a notice sent to a Former Customer, or if a Former Customer returns a notice to the plaintiffs unopened.

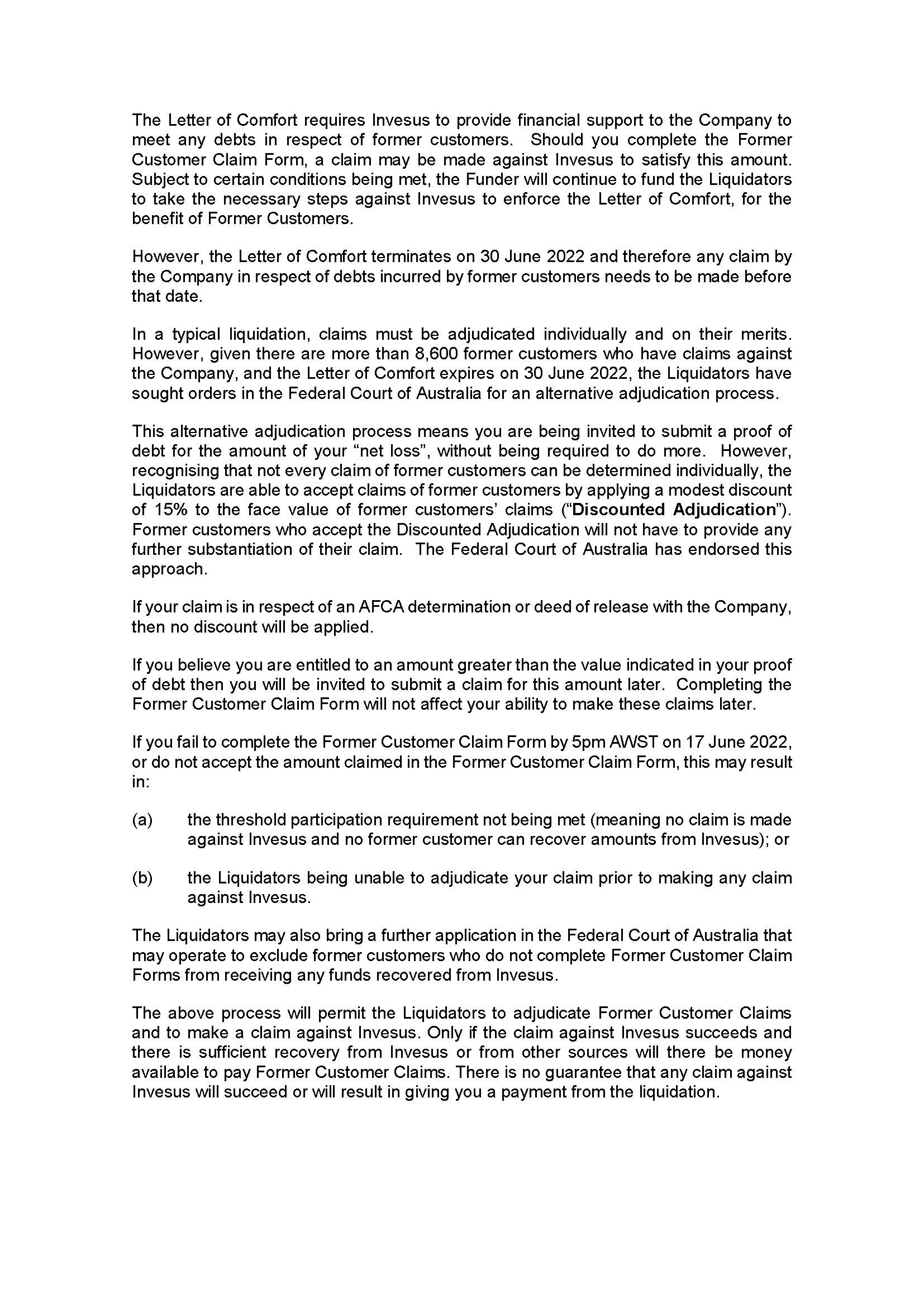

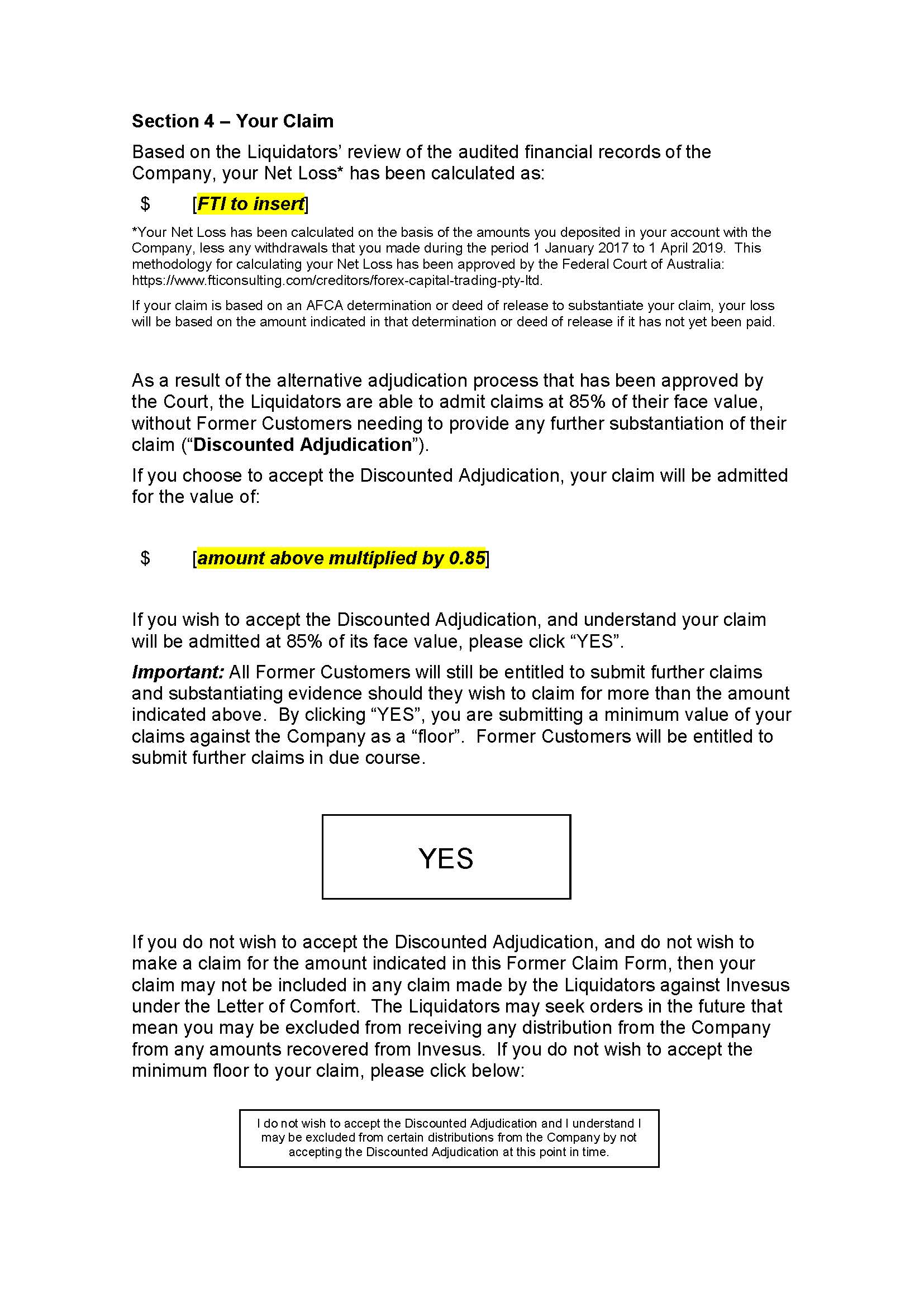

4. Pursuant to s 90-15 of the IPS the plaintiffs do not need to provide any response to Former Customers pursuant to reg 5.6.54 in respect of a proof of debt that is admitted at 85% of its face value in accordance with the Discounted Adjudication set out in Annexure G.

5. Pursuant to s 90-15 of the IPS each completion of the Former Customer Claim Form set out at Annexure G is deemed to comply with the requirements of reg 5.6.49(2)(b).

6. Pursuant to s 90-15 of the IPS, reg 5.6.48(4) of the Regulations does not apply to Former Customers who do not complete the Former Customer Claim Form by 5.00 pm AWST on 17 June 2022.

7. The plaintiffs have liberty to apply on two days' notice.

8. The costs of this application be costs in the liquidation.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BANKS-SMITH J:

Introduction

1 Forex Capital Trading Pty Limited (Forex) is in liquidation. The plaintiffs are its joint and several liquidators (Liquidators).

2 Forex formerly held an Australian Financial Services Licence (AFSL). It has many aggrieved former customers who suffered losses as a result of advice from Forex as to trading in high risk financial products.

3 Those products included over-the-counter derivative products, including margin foreign exchange and contracts-for-difference (Products). The high risk nature of such products is well-recognised. Indeed they have been described as 'little more than gambling': Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liquidation) (No 4) [2020] FCA 1499 at [17] (Beach J).

4 The Liquidators have found themselves in a position where they must deal with claims from some 8,600 former customers with a total claim value of approximately $69.5 million, and a potential source of funding to contribute towards any distribution to those customers that has a looming end date. That source is Forex's ultimate holding company, Invesus Group Limited (Invesus), which has provided a Letter of Comfort to Forex by which it undertakes that upon request it will provide financial support to meet any debts incurred by Forex, but the undertaking terminates on 30 June 2022.

5 The scope of the task faced by the Liquidators is readily apparent, particularly where the individual claims are in the nature of misleading or deceptive conduct and unconscionable conduct on the part of Forex.

6 In those circumstances the Liquidators approached the Court on an urgent basis for orders that will permit them to conduct an abridged process for the adjudication and admission of claims (in their capacity as liquidators) which offers former customers the option to accept a 15% discount on the value of their claims as calculated by the Liquidators by a certain deadline, in exchange for exempting them from providing further detailed evidence as to each element of their alleged claims and establishing causation (Expedited Process). The Liquidators contend that on a conservative view, even without a complete formal adjudication process, it is apparent that former customers have at least a claim for 85% of their face value.

7 Such an application, although rare, is not novel. A similar discounted election proof process was considered and endorsed by the Court in ION Limited, in the matter of ION Limited (Subject to Deed of Company Arrangement) [2010] FCA 1119 (ION Limited) (Dodds-Streeton J).

8 At the conclusion of the hearing on 17 May 2022, I considered it appropriate to grant the orders requested, subject to certain amendments suggested during the hearing. These are my reasons for doing so.

The evidence

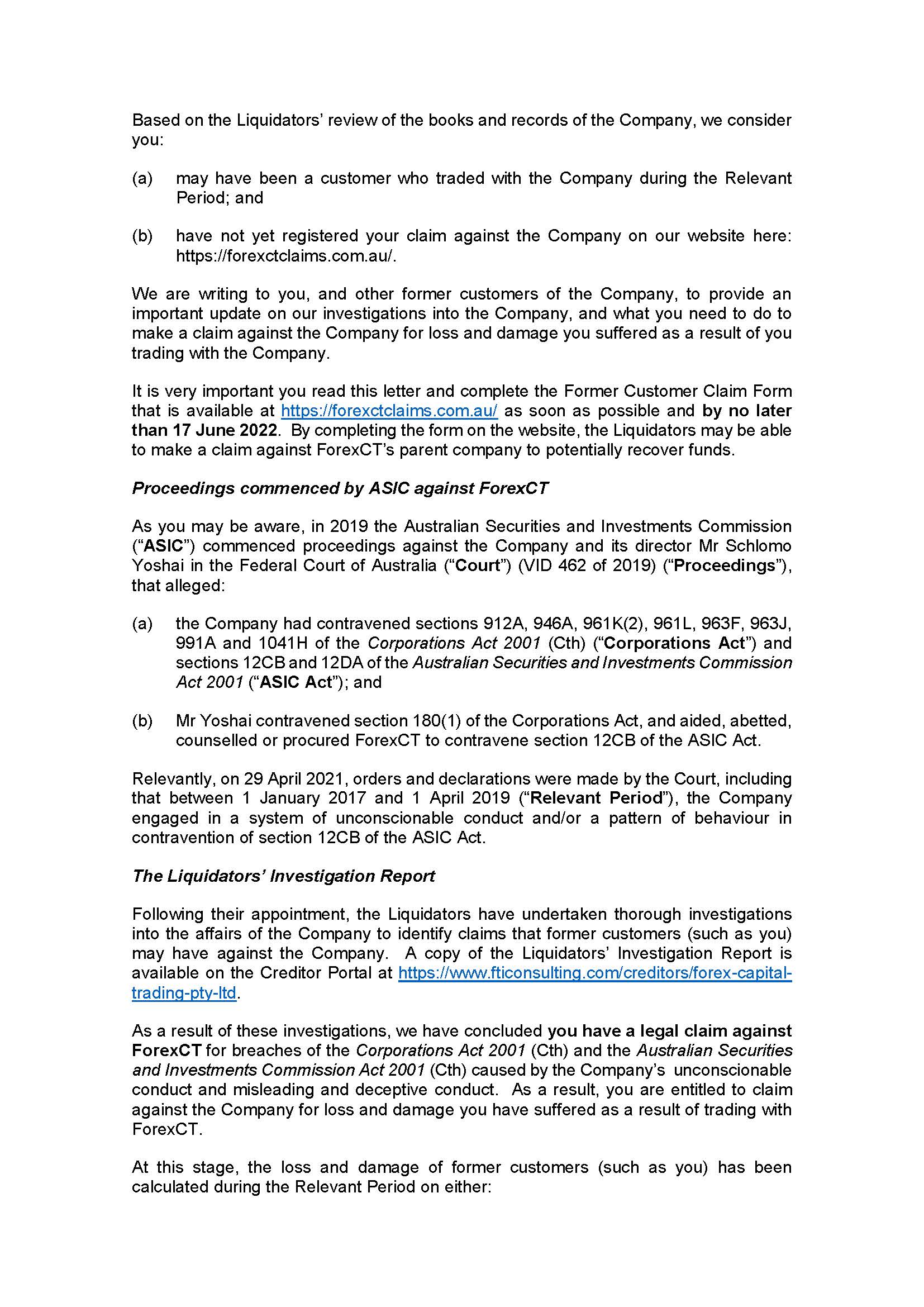

9 The Liquidators rely on evidence provided by way of two affidavits affirmed by the first-named plaintiff, Daniel Woodhouse. As detailed below, Mr Woodhouse explained that detailed investigations have already been undertaken into the nature and quantum of potential claims by former customers in the liquidation. A reference to 'former customers' is a reference to customers who had traded with Forex between 1 January 2017 and 1 April 2019 (Relevant Period). Importantly, the Liquidators also had the benefit of reasons arising out of proceedings issued by the Australian Securities and Investments Commission (ASIC).

The ASIC proceedings

10 In March 2019 ASIC commenced an investigation into the conduct of the business of Forex. It obtained certain asset restraining orders and, in July 2020, commenced proceedings against Forex. Ultimately those proceedings were determined on the basis of admitted contraventions of civil penalty provisions: Australian Securities and Investments Commission v Forex Capital Trading Pty Limited, in the matter of Forex Capital Trading Pty Limited [2021] FCA 570 (ASIC v Forex) (Middleton J).

11 The admitted contraventions were addressed in a statement of agreed facts filed on 29 April 2021, and received by the Court in accordance with s 191 of the Evidence Act 1995 (Cth). The statement of agreed facts is only admissible for the purposes of the ASIC proceedings.

12 On 29 April 2021 his Honour made declarations that Forex had contravened s 912A, s 946A, s 961K(2), s 961L, s 963F, s 963J, s 991A and s 1041H of the Corporations Act 2001 (Cth) and s 12CB and s 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act); made declarations that it had engaged in an unconscionable system of conduct or pattern of behaviour contrary to s 12CB of the ASIC Act; ordered the payment of pecuniary penalties; and made a disqualification order against the Australian-based director, Shlomo Yoshai.

13 The reasons in ASIC v Forex provide detailed background information as to the operations of Forex and these reasons assume some familiarity with those reasons. However, in summary, the admitted contraventions the subject of ASIC v Forex occurred for the most part during the Relevant Period. Middleton J accepted that the company's customers lost upwards of $77,619,916 during the Relevant Period. This translated into a net gain for Forex of a corresponding amount: ASIC v Forex at [25]. The company's customers were unsophisticated, had little understanding of or experience in the Products, and so they were reliant on the advice of its representatives: ASIC v Forex at [18].

The Letter of Comfort and the claim deadline

14 The Liquidators were originally appointed by way of a members' voluntary winding up on 26 June 2021, shortly after the orders were made by Middleton J. Mr Yoshai made a declaration of solvency for that purpose.

15 The Liquidators considered the basis of the solvency declaration, and in particular took into account that Forex had no means of meeting the claims of its customers as Invesus had withdrawn the profits from Forex. However, Invesus had provided the Letter of Comfort.

16 Following communications with Invesus seeking funding to further investigate the affairs of Forex, the Liquidators lost confidence in the Forex solvency declaration and sought and obtained orders from this Court on 7 December 2021 that Forex be wound up in insolvency.

17 Since their initial appointment on 27 June 2021 the Liquidators have conducted the usual inquiries required of liquidators and have kept the creditors informed by statutory reports. A committee of inspection was also formed following a resolution of creditors at a meeting of creditors.

18 Relevantly however, the Liquidators have expedited their investigations as to the nature and quantum of the claims of the former customers, having regard to the Letter of Comfort and the 30 June 2022 deadline.

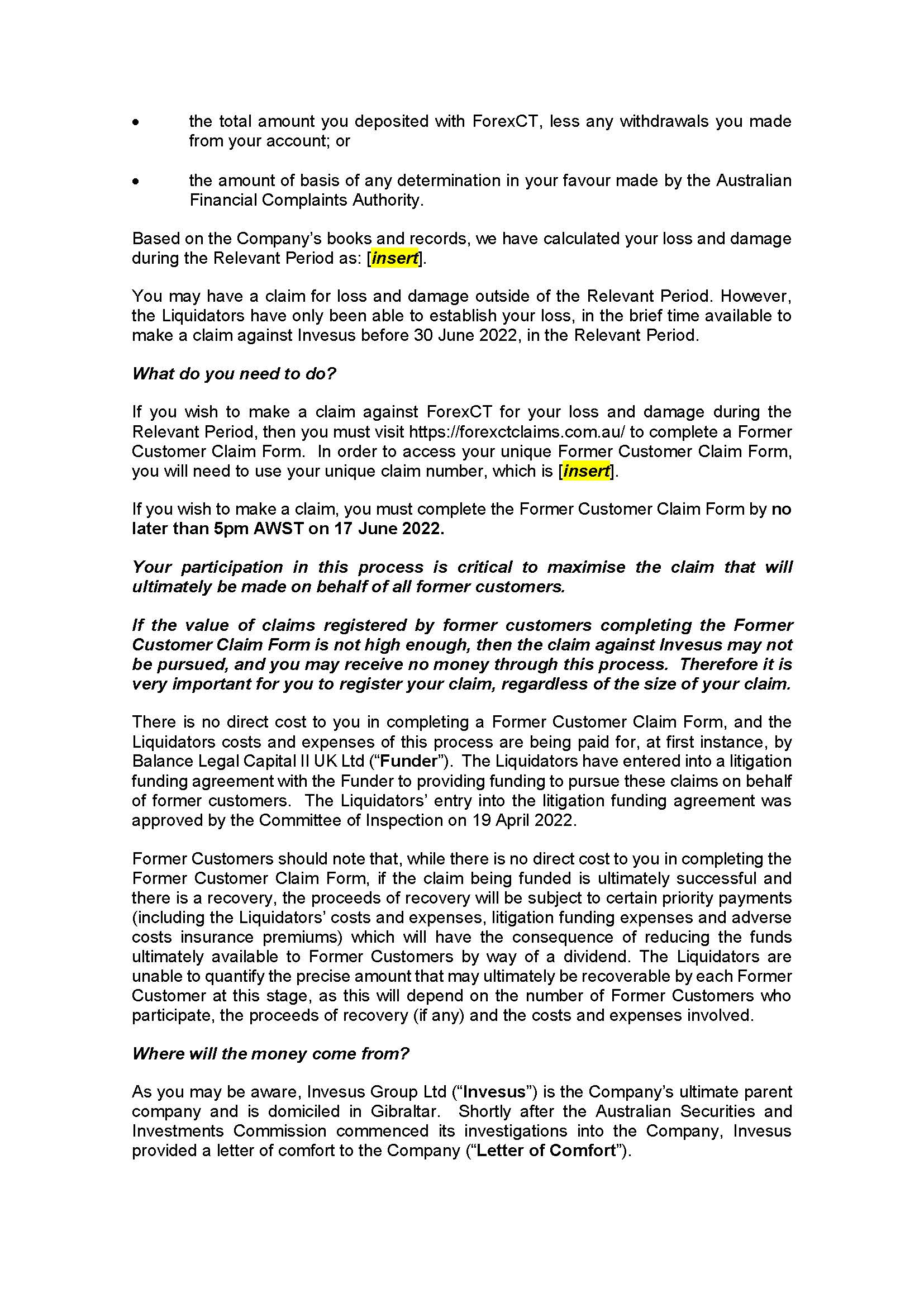

19 The usual regime for ruling on proofs of debt in a liquidation is well recognised. When liquidators admit or reject a proof of debt, they act in a quasi-judicial capacity according to standards no less than the standards of a court or judge: Tanning Research Laboratories Inc v O'Brien (1990) 169 CLR 332 at 338-339 (Brennan and Dawson JJ). The Corporations Regulations 2001 (Cth) provide that a liquidator must, within 28 days of receiving a request in writing from a creditor, admit or reject a proof of debt (reg 5.6.53(1)); and a dividend in the winding up of a company may be paid only to a creditor whose debt or claim has been admitted by the liquidator at the date of distribution of dividends (reg 5.6.63). That is, when creditors are paid a dividend, they are paid a sum certain, determined by reference to their admitted proof of debt.

20 The Liquidators are proceeding on the basis that admitted proofs of the former customers will be debts within the terms of the Letter of Comfort.

21 According to Mr Woodhouse, initial inquiries indicate that Invesus has access to sufficient assets in Gibraltar to allow it to meet a significant request under the Letter of Comfort. For example, it points to the fact that Invesus procured funds for Forex so that it could pay $21.8 million in pecuniary penalties pursuant to the orders of Middleton J. It perhaps goes without saying that the Liquidators are not in a position to give comfort to creditors that Invesus will in fact meet any obligations under the Letter of Comfort.

22 Regardless, it can be seen that the 30 June 2022 deadline is potentially of great importance in the liquidation. Given the time constraints and the large number of former customers with claims, it is not possible for the Liquidators to formally adjudicate on all of the potential claims of the former customers in order to identify each debt to which the Letter of Comfort should respond. Mr Woodhouse gave some evidence as to the scale of resourcing that would be required if a formal adjudication process for each claim were undertaken in that time frame. He said, for example, that it would be necessary to retain some 53 staff in the short term to assist and cost some $6.2 million, even assuming staff could be located and secured. By contrast, the Liquidators anticipate that under the Expedited Process, their costs for dealing with the claims of the former customers will be in the vicinity of $573,200 to $860,000.

The Expedited Process

23 The process that the Liquidators seek be endorsed by the orders is, in summary:

(a) the Liquidators will pre-populate claim forms to be provided to the former customers, with each former customers' net loss included, based upon the information in the company's books and records;

(b) the Liquidators will request the former customers to elect whether they want to participate by claiming their net loss based on the net loss figure provided by the Liquidators but with a 15% discount of value; and

(c) the Liquidators will admit claims where the former customer elects to accept the 15% discount on the specified net value without a further adjudication.

24 The Liquidators say that such a process can reasonably be completed in the limited time available before 30 June 2022, through streamlining the steps for example, by minimising the need for them to review substantial documentation from former customers and to request substantial further and better particulars. It will also avoid the need for the Liquidators to individually determine causation for each former customer's claim on a case-by-case basis, so avoiding, for example, the need for the Liquidators to review all communications and identify and listen to relevant audio recordings between Forex representatives and each former customer.

The investigations and considerations that support the proposal

25 The proposal is the culmination of a detailed investigation process undertaken by the Liquidators which has included a sampling of former customer claims.

Investigation Report

26 The Liquidators detailed that process in an Investigation Report that was provided to former customers and to Invesus on 5 May 2022. That report was detailed. It was verified by the first affidavit of Mr Woodhouse. The Liquidators' lawyers assisted in designing the parameters and content of their inquiries.

27 In summary:

(a) the Liquidators identified a randomised representative sample of former customers (defined as Selected Former Customers). They also took into account the claims of eight former customers whose claims were addressed in the ASIC proceedings (Judgment Customers);

(b) the methodology used to select the 58 Selected Former Customers involved identifying certain objective features of former customers based on information available to the Liquidators by way of 'suitability assessments' provided when a customer opened an account;

(c) having regard to that and other objective data, the Liquidators ascertained that former customers had the following characteristics:

a) Income: a weighted average income of approximately $92,270.

b) Age: an average age of 47.

c) Experience in trading Products: more than 75% of Former Customers had never or rarely traded in financial products similar to the Products offered by the Company.

d) Education about Products: only 28% of Former Customers had attended any sort of course relating to Products in the previous 2 years.

e) Relevant Work Experience: less than 20% of Former Customers had relevant experience from within the last 10 years that assisted them in understanding the Products.

f) Relevant Qualifications: nearly 75% of Former Customers did not have any relevant professional or academic qualifications to assist them in understanding Products.

(d) the Selected Former Customers were drawn from the pool of former customers who lost money trading with Forex in the Relevant Period, and were identified as having three objective characteristics which may have influenced the conduct of Forex towards them;

(e) those characteristics were the time period of their trading (divided into four periods), the amounts invested (divided into four categories) and trading frequency (four quartiles of total number of trades);

(f) those characteristics, when applied in combination, gave rise to 64 unique possible combinations, and the identification of the Selected Former Customers led to representation of most of those different combinations;

(g) the Liquidators reviewed over 680 individual phone calls between the company's representatives and some (but not all) of the Selected Former Customers;

(h) junior staff listened to the phone call recordings in order to identify potential instances of misleading or deceptive conduct or unconscionable conduct, and their comments were reviewed by senior staff who sought to confirm instances of wrongful conduct;

(i) in particular, the Liquidators and their staff sought to identify examples of Forex representatives misrepresenting the level of risk associated with the Products, examples of representatives misrepresenting their interests being aligned with those of the Selected Former Customers, examples of representatives delaying, deferring or discouraging withdrawals being made, and examples of representatives encouraging further investments in Products when such a course was clearly inappropriate; and

(j) the Liquidators also had access to the Court Book in the ASIC proceedings that included materials relevant to Forex's policies, processes and procedures.

28 Based on the investigations into the conduct directed towards the Selected Former Customers, including the telephone reviews, the review of the other general information available and the previous findings in the reasons in ASIC v Forex, the Liquidators considered whether claims might be made out by each of the Selected Former Customers and so, inferentially, by all of the former customers who incurred losses during the Relevant Period.

29 In doing so, they had regard to the elements of the relevant statutory provisions (which were included in the Investigation Report), informed by the relevant principles.

30 In the following paragraphs I will adopt (with some amendments) the summary of the provisions and authorities as set out in the Liquidators' written submissions, as I consider that they accurately and fairly record the legal position.

The statutory provisions and principles considered as part of the investigation

Misleading or deceptive conduct

31 Section 1041H(1) of the Corporations Act prohibits conduct, in relation to a financial product or service, that is misleading or deceptive, or is likely to mislead or deceive. It states:

A person must not, in this jurisdiction, engage in conduct, in relation to a financial product or a financial service, that is misleading or deceptive or is likely to mislead or deceive.

32 Similarly, s 12DA(1) of the ASIC Act prohibits conduct of the same kind, in trade or commerce, in relation to financial services. It states:

A person must not, in trade or commerce, engage in conduct in relation to financial services that is misleading or deceptive or is likely to mislead or deceive.

33 In order to establish a breach of these sections, an individual must satisfy each element of the above provisions. The relevant elements for misleading or deceptive conduct are that a person:

(a) engages in conduct;

(b) in relation to financial services (or, additionally, financial products under s 1041H of the Corporations Act); and

(c) that is misleading or deceptive or is likely to mislead or deceive.

34 A person will engage in conduct where, for example, that person makes representations as to a state of affairs: Campbell v Backoffice Investments Pty Ltd [2009] HCA 25; (2009) 238 CLR 304 at [34]-[36] (French CJ), [101]-[102] (Gummow, Hayne, Heydon and Kiefel JJ).

35 The term 'financial services' relevantly refers to providing financial product advice, or dealing in financial products: Corporations Act s 766A(1), 766B(1); ASIC Act s 12BAB(1).

36 As to whether conduct is misleading or deceptive or is likely to mislead or deceive, the question is whether the impugned conduct, viewed as a whole, has a sufficient tendency to lead a person exposed to the conduct into error by forming an erroneous assumption or conclusion about some fact or matter: Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd (1982) 149 CLR 191 at 198-199 (Gibbs CJ); Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640 at [39] (French CJ, Crennan, Bell and Keane JJ).

37 Whether conduct is misleading or deceptive or is likely to mislead or deceive is to be assessed objectively, and in the context of all the evidence and surrounding circumstances, including the nature of the parties, the character of the transaction contemplated and the contents of any relevant documents: Butcher v Lachlan Elder Realty Pty Ltd [2004] HCA 60; (2004) 218 CLR 592 at [40] (Gleeson CJ, Hayne and Heydon JJ).

Unconscionable conduct

38 Section 991A(1) of the Corporations Act and s 12CB(1) of the ASIC Act each prohibit engaging in conduct that is, in all the circumstances, unconscionable.

39 Section 991A(1) of the Corporations Act states:

A financial services licensee must not, in or in relation to the provision of a financial service, engage in conduct that is, in all the circumstances, unconscionable.

40 Section 12CB of the ASIC Act states:

(1) A person must not, in trade or commerce, in connection with:

(a) the supply or possible supply of financial services to a person; or

(b) the acquisition or possible acquisition of financial services from a person;

engage in conduct that is, in all the circumstances, unconscionable.

41 As to supplying or possibly supplying, this includes circumstances where the financial service was, in fact, supplied, and where the financial services were ultimately not supplied: Australian Securities and Investments Commission v Australian Lending Centre Pty Ltd (No 3) [2012] FCA 43; (2012) 213 FCR 380 at [176].

42 Whether conduct is unconscionable is assessed objectively, by asking whether what is being done is being done in good conscience, as guided by the human values that inform an Australian business conscience: Australian Competition and Consumer Commission v Quantum Housing Group Pty Ltd [2021] FCAFC 40; (2021) 285 FCR 133 at [87] (Allsop CJ, Besanko and McKerracher JJ). Relevant factors to be considered may include (ASIC Act s 12CC(1)):

(a) the relative strengths of the bargaining positions of the supplier and the customer;

(b) whether the customer was able to understand any documents or information provided to them;

(c) whether any undue influence or pressure was exerted on, or any unfair tactics were used against, the customer;

(d) the extent to which the supplier unreasonably failed to disclose to the customer any intended conduct of the supplier that might affect the interests of the service recipient;

(e) the extent to which the supplier acted in good faith; and

(f) the supplier's compliance with any applicable industry codes or guidelines.

Examples of application

43 The Liquidators in their Investigation Report refer to a number of examples disclosed by their investigations that they say demonstrate serious misleading, deceptive and unconscionable conduct towards the Selected Former Customers. They are as follows:

(a) a former customer was advised that it was in the best interests for the investor to do well as Forex's success was directly tied to the former customer's success. The former customer subsequently deposited money with the company and lost $17,200 over a four month period;

(b) a representative misrepresented the company's business model by stating that it acted as an intermediary between the buyer and seller to the trade. The former customer subsequently deposited $15,000 with the company the next day, and ultimately lost $33,900 over a three month period;

(c) a representative encouraged a former customer to invest $50,000 and place trades saying that it would be in the former customer's best interests, knowing that the former customer had no income and only had assets of $67,000. The former customer deposited $30,000 that day and lost $61,500 over the next six months;

(d) a representative encouraged a former customer to take out a credit card loan and draw the entire amount to deposit to and trade with Forex. The former customer subsequently deposited $3,000 later that day and lost $4,000 in one month;

(e) a representative contacted a former customer, aged in his 80s, more than 200 times in an 11-month period, and encouraged him to trade, despite the fact that the company's records made it plain that the former customer was 'bad with technology' and 'struggles to understand'. The former customer lost $22,000 over this 11-month period;

(f) a representative deterred a former customer from withdrawing their money, despite being advised the former customer required the money to pay their rent and that he was 'waiting for money - selling van'. This resulted in the former customer cancelling their withdrawal request, not withdrawing money to pay their rent and, instead, depositing an additional $1,000. Within one day, the former customer had lost the money they had sought to withdraw, and the additional money they had deposited.

Conclusions drawn from the investigations

44 Mr Woodhouse on behalf of the Liquidators, having undertaken the process described above concluded that:

68. Given the characteristics of the Selected Former Customers sampled, and the egregious nature of the conduct identified in the Investigation Report my fellow Liquidators and I have formed a view that each of the Former Customers would be able to satisfy the Liquidators, exercising their quasi-judicial function in adjudicating proofs of debt, that they have both Misleading or Deceptive Conduct Claims and Unconscionable Conduct Claims, should they choose to submit a proof of debt in the liquidation of the Company based on those claims.

69. I have formed this view in reliance of the materials that have been reviewed, and also the methodology adopted, which gives me confidence to extrapolate the findings in respect of Selected Former Customers to all Former Customers.

…

78. Based on the Investigations, I am satisfied each of the Selected Formed Customers would be able to establish the Misleading or Deceptive Conduct Claims, and the Unconscionable Conduct Claims against the Company should those claims be advanced in a proof of debt. I have formed this view for several reasons, including:

(a) the Company's records, and the targeted review of phone calls between Representatives and the Selected Former Customers, demonstrate the Company engaged and its Representatives engaged in conduct that would give rise to the Misleading or Deceptive Conduct Claims, by (among other things) making the following Misrepresentations to Former Customers, namely that:

(i) the interests of Forex CT or its Representatives were aligned with the interests of the customer;

(ii) a Representative did not benefit from the customer's deposit of funds into the customer's trading account with Forex CT;

(iii) the risk of trading losses would be reduced if further funds were deposited in the customer's trading account with Forex CT;

(iv) the Former Customer was likely to or might reasonably expect to generate profits by trading in [the Products] in the order of magnitude indicated by the Representative and in some instances by reference to a particular trading position or strategies identified by the Representative; and / or

(v) it was in the best interests of the customer to make a particular trade or to deposit additional funds;

(b) the Company's records, and the targeted review of phone calls between Representatives and the Selected Former Customers, demonstrate the Company engaged in conduct that would give rise to the Unconscionable Conduct Claims through (among other things):

(i) engaging in the misrepresentations set out above, and providing training and scripts to Representatives that would lead to them misrepresenting the level of risk associated with trading in the Products;

(ii) engaging in conduct intended to delay, defer or discourage Former Customers from withdrawing their funds; and

(iii) engaging in high-pressure sales tactics, including deliberately manufacturing a sense of urgency in order to pressure Former Customers into making further deposits with the Company

(c) the Company's records, and the targeted review of phone calls between Representatives and the Selected Former Customers, demonstrate the Company carried on an unconscionable system through (among other things):

(i) not taking adequate steps to ensure Former Customers had sufficient knowledge and understanding of the high-risk financial products offered by the Company;

(ii) encouraging Representatives to engage in conduct intended to delay, defer or discourage Former Customers from making withdrawals;

(iii) encouraging Representatives to engage in the high-pressure tactics described in the Investigation Report;

(iv) failing to implement a proper framework to ensure its Representatives complied with the relevant legal obligations imposed on the Company as a holder of an AFSL;

(v) implementing a conflicted remuneration policy which incentivised Representatives to maximise deposits from Former Customers, irrespective of the financial position of those customers; and

(vi) failing to disclose the remuneration structure and the conflicted remuneration of Representatives.

79. I am also satisfied on the basis of the Investigations undertaken that the Company's misleading or deceptive conduct and/or unconscionable conduct identified above caused Former Customers to (among other things) make deposits with the Company, to make particular trades with the Company, or to cancel withdrawal requests. That is to say, the wrongful conduct of the Company caused the Former Customers to lose money.

80. Further, given:

(a) the methodology chosen to select the Selected Former Customers;

(b) the egregious conduct of the Company and its Representatives towards the Selected Former Customers identified in the Targeted Telephone Review; and

(c) the extensive documents identified in the Document Review,

I verily believe each of the Former Customers would be able to satisfy me they had a valid Misleading or Deceptive Conduct Claim and/or Unconscionable Conduct Claim for loss or damage against the Company as at the Appointment Date, should the Former Customer choose to submit a proof of debt.

Calculation of loss

45 Mr Woodhouse stated that each former customer's net loss may be calculated on the books and records of Forex, using their respective account statements. Examples of how this may be undertaken were explained in his affidavit and it is not necessary to set out for current purposes the precise workings. It is apparent, however, that such an accounting exercise can be accurately undertaken, having regard to each former customer's deposits and bonuses, less trading loss and rollover fees, and taking into account manual adjustments (which were used for a variety of reasons, including where payments had been made to resolve a complaint or to reverse fees). Further, Mr Woodhouse notes that the company's books and records have been audited.

46 The state of Forex's books and records is such that for the purpose of the proof of debt process anticipated by the orders, information for individual former customers to be included in the proposed notices to be issued to them can be pre-populated, adding to the efficiency of the proposed course.

47 By his second affidavit, Mr Woodhouse deposed to some additional matters that had come to his attention when his staff prepared to populate the proposed notices. For example, whilst the net losses for the Relevant Period could be calculated as proposed, some former customers had traded in periods outside the Relevant Period and made profits that must to be taken into account in calculating the quantum of any overall claim. Similarly, some former customers did not record a net loss if trading only during the Relevant Period was taken into account, but did record a net loss when trading outside that period was accounted for. Mr Woodhouse's evidence indicates that the Liquidators accept that it is necessary to have regard to such examples when calculating net loss. Their current calculations indicate that having regard to such adjustments, the value of net loss that might be admitted to proof though the proposed Expedited Process and subject to the proposed discount will be approximately $69,563,089 (in contrast to the amount anticipated in Mr Woodhouse's first affidavit of between $77 million and $85 million).

Section 90-15 IPS

48 Against that backdrop it is appropriate to turn to the question of relief.

49 The Liquidators seek that the Court make orders pursuant to s 90-15(1) of Schedule 2 (Insolvency Practice Schedule (Corporations)) to the Corporations Act (IPS).

50 Section 90-15(1) of the IPS relevantly provides:

(1) The Court may make such orders as it thinks fit in relation to the external administration of a company.

51 The terms of this provision are broader than its two partial predecessor provisions, being s 479(3) and s 511(1)(a) of the Corporations Act. Despite this, courts have nonetheless been guided by the matters relevant to the exercise of the predecessor provisions: Walley, in the matter of Poles & Underground Pty Ltd (Administrators Appointed) [2017] FCA 486 at [41] (Gleeson J); Reidy, in the matter of eChoice Limited (Administrators Appointed) [2017] FCA 1582 at [27] (Yates J); In the matter of University Co-operative Bookshop Ltd (admins apptd) (No 2) [2020] NSWSC 97 at [13]-[14] (Gleeson J); and In the matter of Equiticorp Australia Ltd (in liq) [2020] NSWSC 143 at [43] (Gleeson J).

52 These notions include that the power should be exercised where it is just and beneficial to do so: Deputy Commissioner of Taxation, in the matter of ACN 154 520 199 Pty Ltd (in liq) v ACN 154 520 199 Pty Ltd (in liq) [2017] FCA 444 at [64] (Gleeson J).

53 Whilst a court generally refrains from making directions relating to a liquidator's or administrator's business or commercial decisions, it may give directions relating to issues such as a legal issue of substance or procedure, or an issue of power, propriety or reasonableness: In the matter of Ansett Australia Limited and Korda [2002] FCA 90; (2002) 115 FCR 409 at [44]-[46] (Goldberg J).

54 In In the matter of Polat Enterprises Pty Ltd (in liq) [2020] VSC 485 (Hetyey AsJ) the Court observed that s 90-15 is 'broad in its scope and contemplates not only the exercise of judicial discretion but also the determination of substantive rights' (at [31]): see also Joiner (Liquidator), in the matter of CuDeco Limited (Receivers and Managers Appointed) (in liq) [2020] FCA 1661 at [93]-[97] (Banks-Smith J); and Jahani, in the matter of Ralan Group Pty Ltd (in liquidation) [2022] FCA 107 at [158] (Farrell J).

55 Senior Counsel drew my attention to an example where relief under s 90-15 was refused: In the matter of DSHE Holdings Limited [2021] NSWSC 608 (Williams J). In that case the deed administrator relevantly sought an order that would permit them to exercise a statutory power granted to a liquidator under the Corporations Act to seek an order that ASIC de-register a company on a specified day. The Court declined to make such an order, noting that it would modify the operation of a provision of the Corporations Act in relation to a particular external administration, and in circumstances where the Court had received no assistance from the deed administrator as to whether s 90-15 of the IPS, construed in accordance with the principles of statutory interpretation, conferred such a power on the court. Her Honour noted that although the power under s 90-15 has been described as 'unconstrained', the matters relevant to the exercise of the predecessor provisions remain relevant.

56 The circumstances of In the matter of DSHE Holdings Limited are distinguishable from those before me. Here, the Liquidators are conducting the liquidation in accordance with Chapter 5 of the Corporations Act (which includes the provisions dealing with a winding up) but in that context seek orders relating to the method by which proofs of debt might be dealt with, having regard to the relevant regulations. The orders sought do not involve the modification of a provision of the Corporations Act, and, as ION Limited reflects, similar orders have previously been made under the predecessor provisions.

ION Limited

57 In ION Limited, following an invitation for proofs of debt, the deed administrators received roughly 3,300 proofs of debt from current and former shareholders of the company, making various allegations, but frequently based on claims for misleading and deceptive conduct and breaches of the continuous disclosure obligations imposed on the company as a publicly listed company: at [12]. The majority of shareholder claimants alleged that they had taken action (for example, acquired or sold their shares) based on the alleged contravening conduct: at [15]. As Dodds-Streeton J explained, 'The deed administrators were thus faced with a myriad of shareholder claims based on different allegations': at [18].

58 The deed administrators conducted investigations into the shareholders' claims, including by a process of electronic searches, interviews, compulsory discovery, public examinations and interviews in order to assess claims during a particular period: at [19]. Following these investigations, the deed administrators concluded there was contravening conduct by the company, however examination of causation would be required: at [21]-[22]. In recognition of the need to establish the causal link, the deed administrators proposed to admit the claims at 80% of their value, and sought relief under s 447D of the Corporations Act (the predecessor to s 90-15) to allow them to take this approach: at [22].

59 The proposed discount was offered as a 'quid pro quo of exemption from furnishing detailed evidence of causation': at [47].

60 Dodds-Streeton J granted the relief sought by the deed administrators, and observed:

[53] In the present case the deed administrators could, in my view, consistently with the obligations of a liquidator, properly take the proposed steps to invite proofs from the new shareholder claimants and could properly offer the discounted proof election.

61 The particular claim form provided to shareholders pursuant to the orders made in ION Limited required shareholders to tick a box if they wished to make a claim relating to share purchases on or after a specified date (10 September 2004), and if so, then to elect by ticking further boxes to either submit evidence and seek admission of 100% of their claim, or choosing the following:

In order to expedite the adjudication of my claim relating to shares purchased on or after 10 September 2004, I elect not to submit evidence of causation and agree to admission of my claim at 80% of its value (calculated in accordance with applicable legal principles).

62 The similarity with the basis of this application is apparent. As the Liquidators submitted, similarly to in ION Limited, in this case the Liquidators:

(a) received a number of claims against the company following their appointment;

(b) undertook further, detailed investigations into the affairs of the company in relation to these claims;

(c) concluded the former customers each have valid claims against the company; and

(d) propose to admit the claims of former customers with a modest discount.

63 In ION Limited, the deed administrators did not have sufficient direct evidence as to causation.

64 Here, the Liquidators do not have direct evidence as to liability with respect to each of the claims of the former customer claims but they have drawn a reasonable inference as to liability based on their investigations. They have been able to calculate net loss.

65 The Liquidators propose to admit the former customers' claims with a 15% discount, bearing in mind that the Liquidators have had to draw inferences from a representative sample and that under the Expedited Process the former shareholders who elect to participate need not submit further evidence of their losses. According to Mr Woodhouse:

The allowance proposed by the Liquidators is not to reflect that Former Customers may not have good claims. As previously stated, I believe that all Former Customers who traded with the Company during the Relevant Period have good claims against the Company for Misleading or Deceptive Conduct Claims, or Unconscionable Conduct Claims. The allowance is merely a concession to reflect the nature of the expedited adjudication process the Liquidators intend to follow, and [the] sampling process followed by the Liquidators.

66 Noting the importance of considering whether it would be just to exercise the discretion to make the orders, it is appropriate in the context of Mr Woodhouse's conclusions to say something more about the inferential reasoning of the Liquidators and the manner in which they have calculated net losses for the purpose of the claims that they propose to admit.

Inferences drawn by the Liquidators

67 I have referred to the fact that the Liquidators have drawn an inference as to liability in circumstances where it would not be practicable to undertake individual assessments of each claim of a former customer. Such inferential reasoning is permissible provided it is non-conjectural. As explained by Gageler J In Henderson v Queensland [2014] HCA 52; (2014) 255 CLR 1 at [87]-[91] (in dissent but not as a matter of principle), proof on a balance of probabilities can be demonstrated by evidence that invites a non-conjectural inference (at [88], citing Bradshaw v McEwans Pty Ltd (1951) 217 ALR 1 at 5); 'a party who bears the legal burden of proving the happening of an event or the existence of a state of affairs on the balance of probabilities can discharge that burden by adducing evidence of some fact the existence of which, in the absence of further evidence, is sufficient to justify the drawing of an inference that it is more likely than not that the event occurred or that the state of affairs exists' (at [89]); inferential reasoning cannot be described by formula and takes into account all relevant evidence including conventional perceptions about how people might behave (at [91]).

68 The Liquidators also referred to the more recent analysis of the authorities in Australian Securities and Investments Commission v GetSwift Limited (Liability Hearing) [2021] FCA 1384 at [1896]-[1900] (Lee J).

69 It is to be noted that Middleton J in ASIC v Forex drew inferences as to misconduct towards all former customers based on a system of unconscionable conduct:

[125] However, in respect of the contravention of s 12CB(1) of the ASIC Act by Forex CT in relation to the system of unconscionable conduct, and Mr Yoshai's involvement in that contravention, it is submitted by the parties (other than Mr Yoshai) that I am not limited by the maximum penalty for a single contravention of s 12CB(1). This is said to be because the systemic conduct towards the eight identified clients (being conduct that was pleaded as a single contravention) was representative of conduct towards all clients of Forex CT, of which there were more than 4,000.

…

[132] I am prepared to accept that the unconscionable system put in place by Forex CT was representative of the conduct towards all clients (not just the eight clients that have been identified).

(original emphasis)

70 The Liquidators have adopted a similar approach. They contended that there is a proper basis for drawing an inference that Forex adopted a course of business which was systematic, so supporting a conclusion that each of the former customers have claims against Forex based on misleading or deceptive conduct and, or in the alternative, unconscionable conduct. That basis is the methodology employed and reported upon in the Investigation Report, and featuring a process of randomly identifying the Selected Former Customers using objective characteristics to ensure they would be representative of all the different types of former customers who traded with the company, considering the circumstances and common themes of the substance of communications with them, in determining and finding that they each had claims. They formed the view that the results of their investigations of the sample group gave rise to a reasonable inference that the company deployed sales techniques across all of the former customers on a consistent and systematic basis. The Liquidators also had the benefit of the information relating to the Judgment Customers.

71 In those circumstances, I do not consider the approach of the Liquidators could properly be described as conjecture. The inferential reasoning and the objective basis for it is disclosed. On the information before me it appears that they have proceeded in a manner consistent with their duties as liquidators.

The net loss approach

72 Similarly, the Liquidators have exposed the basis upon which they propose to calculate net loss for each former customer for the purpose of their respective claims (and deal with other particular payments that affect some former customers. The proposed net loss methodology has the aim of effectively placing the former customer in the same position as though they had never traded with the company, an approach to the assessment of loss consistent with principle.

73 In AGM Markets, Beach J adopted a net loss methodology to determine the amount of refund that would be payable notwithstanding that neither ASIC, nor the company had sufficient records to complete the calculation of the net deposit for each client: AGM Markets at [154], [167]. In this case the Liquidators (and creditors) have the advantage that the books of the company have been audited.

74 In these circumstances, I consider that they have proceeded in a manner consistent with their duties as liquidators.

Other matters

Further substantiation of claims

75 The approach adopted by the Expedited Process creates a 'floor' on the claims of former customers. If a former customer wants to substantiate a claim for a larger amount, such as the balance 15% of the calculated net loss or otherwise, they will be able to do so at a later time (after 30 June 2022). It does not bar such a course.

Litigation funding

76 The Liquidators have entered into a third party litigation funding agreement, with the approval of the committee of inspection. Mr Woodhouse deposed to the fact that third party funding was the only means available to the Liquidators to ensure that there are sufficient funds available to bring this application, adjudicate claims, make the demand of Invesus, and ultimately take necessary steps to enforce the Letter of Comfort if Invesus does not comply with the demand.

77 Mr Woodhouse has disclosed that the funder may withdraw funding for the claim against Invesus should the responses of former customers not provide a sufficient quantum of claims that make the funding commercially viable for the funder. Further, should the company be successful in obtaining a pay-out from Invesus under the Letter of Comfort (whether voluntarily or by enforcement of a court order), the funder is entitled to a percentage share of the proceeds realised, which will be paid in priority to any distribution to the former customers and creditors.

78 The notices that are to be emailed to former customers pursuant to the orders as sought disclose information about the litigation funding agreement.

Notice to interested parties

79 I am satisfied that ASIC was given notice of this application by the solicitors for the Liquidators. It has not sought to participate.

80 I am satisfied that the former customers and Invesus were provided with copies of the Investigation Report, which expressly foreshadowed this application.

81 Each of the former customers was given notice of the time, date and subject of this application by email, and the Liquidators also published a 'frequently asked questions' document on the online Creditor Portal established for the Forex liquidation. I have read the FAQ document and consider it usefully explains the Expedited Process. Senior Counsel for the Liquidators took me to a sample of email responses received from former customers. Mr Woodhouse also deposed to phone calls received from three former customers. None of these communications indicated opposition to the Expedited Process. Some former customers provided further information about their dealings with Forex and about their claims, but such course was consistent with them wishing to have their claims determined. Three of the emails requested information as to how a claim for 100% of net loss could be made, a course still open to former customers as referred to above. I note that over 1500 former customers have registered as creditors via the Creditor Portal, but not all former customers have done so. The Liquidators by the orders intend to provide additional information to those former customers who have not registered as creditors, as they consider they may need additional explanation of some of the steps involved in the Expedited Process.

82 I am also satisfied that Invesus was given notice of this application by emails. On the morning of the hearing, its in-house general counsel provided an email to Mr Woodhouse relevantly stating:

Invesus is not a party to the Proceeding and cannot be bound by any orders sought in your originating process. For the avoidance of doubt, Invesus does not consider the Court has the power to make the orders sought.

83 The Liquidators were not obliged to serve Invesus and did not purport to do so, but they provided it with notice of the application and the opportunity to be heard if that had been its preferred course. Invesus did not provide any substance or basis for its contention that the Court does not have the power to make the orders sought. For completeness, however, I record its position. I do not accept its conclusion.

No contradictor

84 The absence of a contradictor in circumstances where interested parties have been duly informed ought not deprive the Liquidators of the opportunity to seek the aid of the Court. Senior Counsel properly raised a number of matters relevant to the application having regard to the fact that it ultimately proceeded ex parte and without any contradictor. Whilst it is generally undesirable to proceed without a contradictor, having regard to the significance of the proposed Expedited Process and the urgency of the relevant timeline, I consider it appropriate to determine the application regardless: Joiner at [12]; Lewis and Templeton and Warehouse Sales Pty Ltd (in liq) v LG Electronics Australia Pty Ltd (No 2) [2016] VSC 63; (2016) 48 VR 450 at [55]-[61]; and In the matter of Dalma No 1 Pty Ltd (in liquidation) [2013] NSWSC 1335 at [8]-[9].

Conclusion

85 The Expedited Process is a creative and efficient proposal, tailored to the particular circumstances which are faced by the former customers and the Liquidators, notably the pending 30 June 2022 deadline and the extraordinary costs that would be incurred if adjudication of claims proceeded in the usual way. The Liquidators also propose the discount on claims as a matter of fairness: in their view it provides a fair price for the ease of saving the former customers the need to collate evidence and formally prove their individual claims. On the evidence before me, it is apparent that considerable care and effort has been employed by the Liquidators in assessing the veracity of the Selected Former Customers' claims, the former customers' claims generally and the net losses. The orders sought are within the scope of the relief contemplated by s 90-15 and in my view it is open to the Liquidators to proceed in accordance with the Expedited Process. To do so is consistent with their obligations as liquidators.

Orders

86 It is useful to make some observations about the orders as drafted.

87 Order 1 addresses the requirements of reg 5.6.48(2)(b) of the Corporations Regulations. Regulation 5.6.48(2) requires notice to every person who to the knowledge of the Liquidators claims to be a creditor of the company and whose debt or claim has not been admitted. Given that the Liquidators have limited or incomplete contact details with respect to some former customers, order 1 adjusts the manner in which this requirement is met. I note that the proposed notices as annexed to the orders are comprehensive and appropriately disclose that the Expedited Process does not guarantee payment to former customers.

88 Order 2 provides for all former customers to be provided with a claim form inviting them to submit their claim through the Expedited Process.

89 Order 3 permits the Liquidators to not take any further steps if no response is received from former customers (a similar order was made in ION Limited).

90 Order 4 excuses the Liquidators from the obligations under reg 5.6.54 of the Corporations Regulations. Ordinarily, where a liquidator rejects a proof of debt, in whole or in part, they are obliged to provide notice to the creditor that their claim has been rejected. In this case the Liquidators propose to admit former customer claims as to 85% without any implication that they have rejected the remainder of such claims and without any need for the Liquidators to give notice as to any apparent rejection. This course leaves open the potential for the former customers to separately pursue claims above the 85% as calculated at a later date.

91 Order 5 excuses the Liquidators from reg 5.6.49(2)(b) of the Corporations Regulations which requires the proof of debt to be in the form of a Form 535. The claim form in this case (Annexure G to the orders) contains the equivalent information to a Form 535. I note that Section 4 of Annexure G clearly discloses to a reader the alternative 15% discounted adjudication process and the manner in which the relevant customer's net loss has been calculated.

92 Order 6 preserves the position that those former customers who do not submit a claim form under the Expedited Process may still submit a proof of debt in the future, to avoid the effect of reg 5.6.48(4) of the Corporations Regulations.

93 Orders were made on 17 May 2022 accordingly.

I certify that the preceding ninety-three (93) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Banks-Smith. |