Federal Court of Australia

Tax Practitioners Board v Van Stroe [2022] FCA 482

Table of Corrections | |

The citation of the judgment has been amended to correctly state the respondent's correct surname 'Van Stroe'. |

ORDERS

Applicant | ||

AND: | JESSA VAN STROE (ALSO KNOWN AS JESSA LAYOLA) Respondent | |

DATE OF ORDER: |

TO: JESSA VAN STROE (ALSO KNOWN AS JESSA LAYOLA)

TAKE NOTICE THAT, PURSUANT TO ORDER 41.06 OF THE FEDERAL COURT RULES 2011 (CTH):

You are liable to imprisonment, sequestration of property or other punishment for contempt if you:

(a) refuse or neglect to do the things that this order requires you to do; or

(b) do the things that this order requires you to abstain from doing, or you otherwise disobey this order.

THE COURT DECLARES THAT:

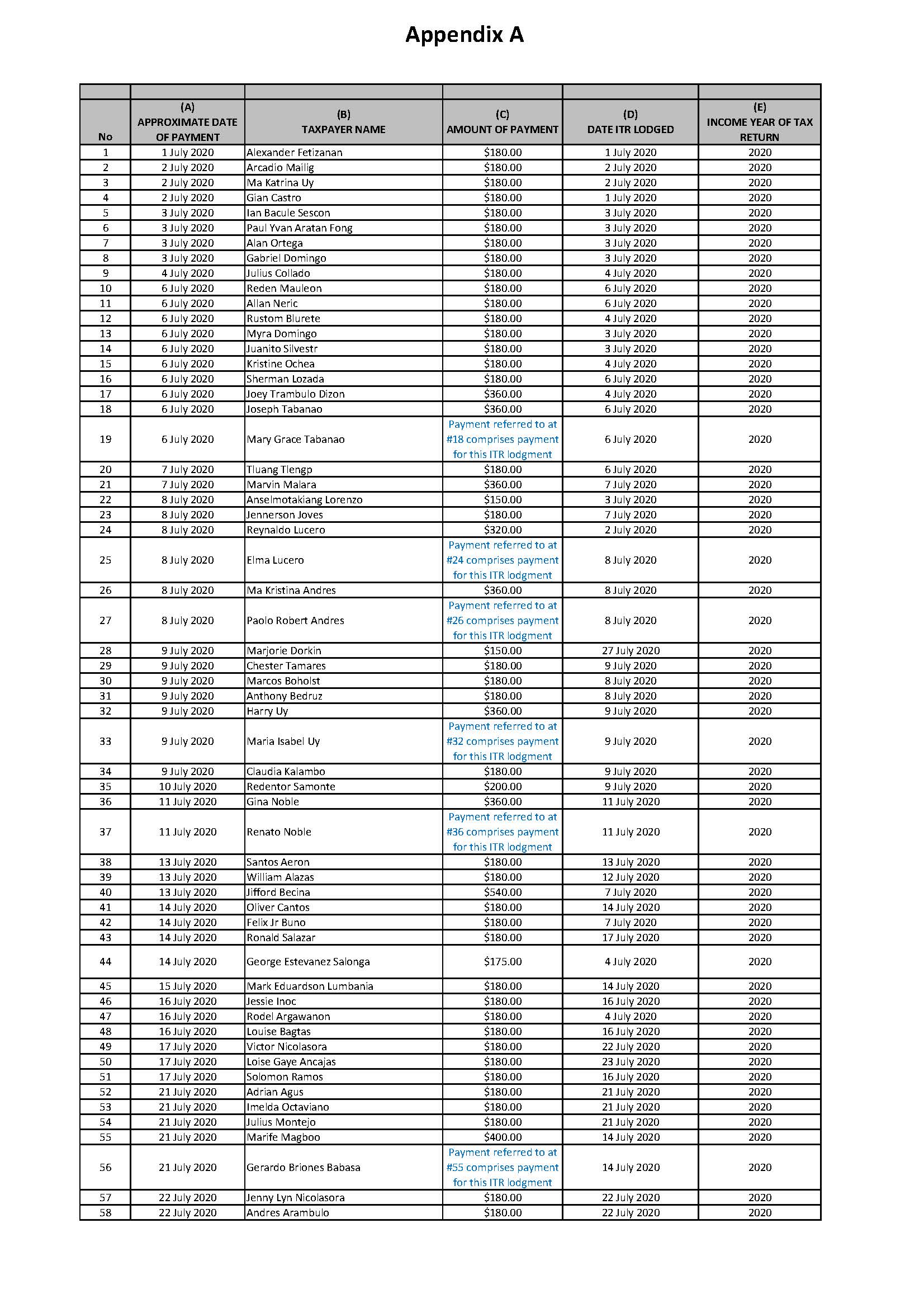

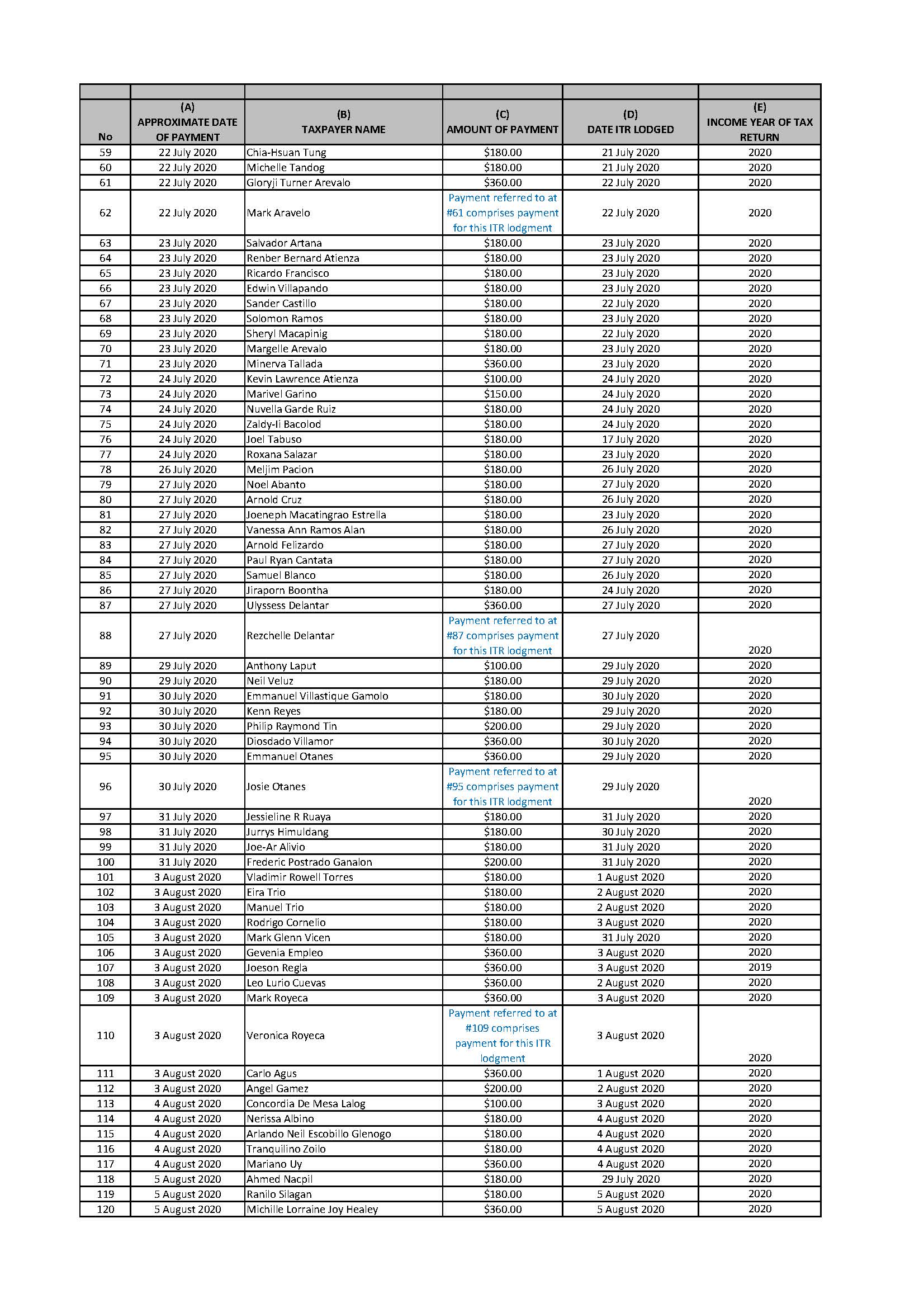

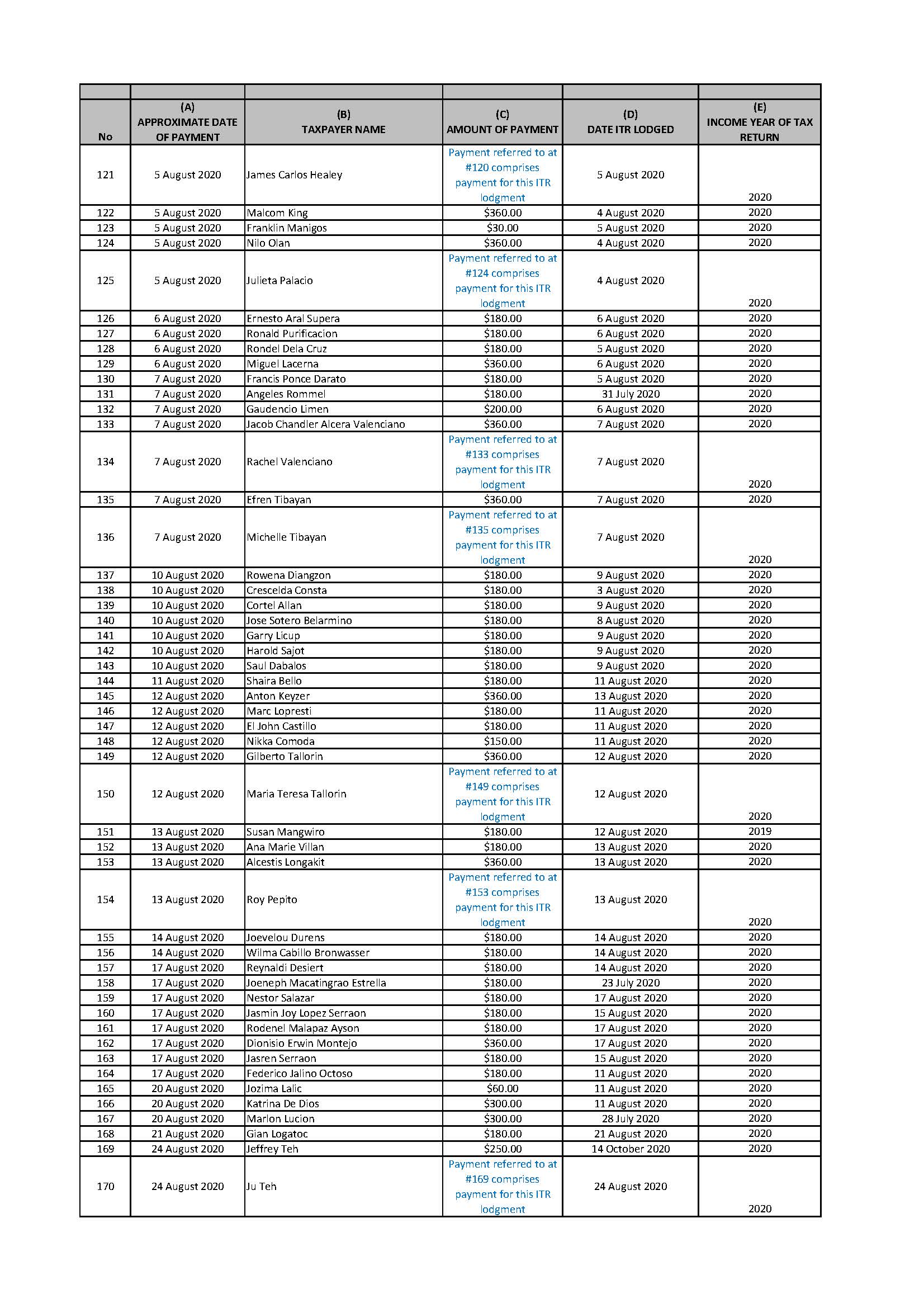

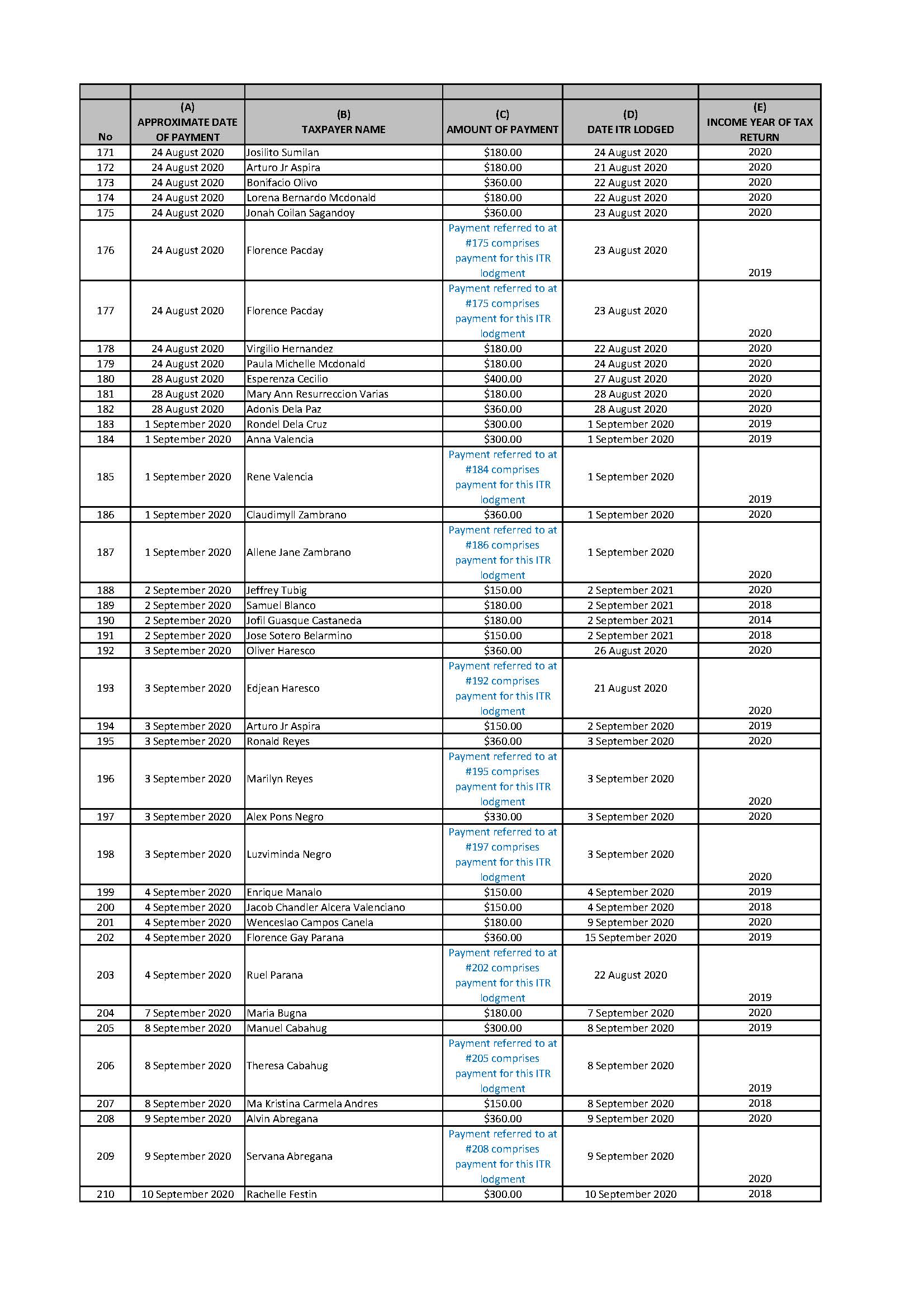

1. Upon admissions which the respondent is taken to have made consequent upon defaults under the Federal Court Rules 2011 (Cth), on each occasion specified in Appendix A to these orders, the respondent contravened s 50-5(1) of the Tax Agent Services Act 2009 (Cth) (TAS Act) by preparing and lodging income tax returns for taxpayers, being the provision of a tax agent service, for a fee or other reward, whilst not a registered tax agent within the meaning of the TAS Act.

THE COURT ORDERS THAT:

2. Pursuant to s 47B of the Federal Court of Australia Act 1976 (Cth), counsel be permitted to deliver oral submissions at the hearing by way of internet connection.

3. Pursuant to s 70-5(1) of the TAS Act, the respondent be permanently restrained from providing tax agent services (as defined in the TAS Act) for a fee or other reward, whilst not a registered tax agent within the meaning of the TAS Act.

4. The matter be listed for hearing on a date to be fixed for the purposes of determining the quantum of any pecuniary penalties to be imposed upon the respondent in respect of her declared contraventions of the TAS Act.

5. Costs reserved.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BANKS-SMITH J:

1 The applicant, the Tax Practitioners Board, alleges that the respondent contravened s 50-5 of the Tax Agent Services Act 2009 (Cth) (TAS Act) on some 531 occasions by providing tax agent services for a fee or reward while not registered to provide those services.

2 This is an application for default judgment and certain relief. The Board seeks relevantly declaratory relief and a permanent injunction. It also seeks pecuniary penalties, but the consideration of penalties is deferred, pending the outcome of this application.

The statutory context

3 The Board is a statutory authority established by s 60-5 of the TAS Act. It is charged with a statutory duty to, amongst other things, administer and regulate the conduct of tax agents, administer the system of registration for registered tax agents and investigate conduct in breach of the TAS Act.

4 Section 2-10 of the TAS Act provides:

General guide to each Part

(1) You need to be registered to provide *tax agent services for a fee or to engage in other conduct connected with providing such services. Part 2 sets out the requirements for registration.

…

(in accordance with the convention in some Commonwealth legislation, the asterisk indicates a defined term)

5 Section 50-5 of the TAS Act provides:

Providing tax agent services if unregistered

(1) You contravene this subsection if:

(a) you provide a service that you know, or ought reasonably to know, is a *tax agent service; and

(b) the tax agent service is not a *BAS service or a *tax (financial) advice service; and

(c) you charge or receive a fee or other reward for providing the tax agent service; and

(d) you are not a *registered tax agent; and

(e) if you provide the tax agent service as a legal service - either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that tax agent service; or

(ii) subject to subsection (3), the service consists of preparing, or lodging, a return or a statement in the nature of a return.

Civil penalty:

(a) for an individual - 250 penalty units; and

(b) for a body corporate - 1,250 penalty units.

…

6 Section 90-5 of the TAS Act provides:

Meaning of tax agent service

(1) A tax agent service is any service:

(a) that relates to:

(i) ascertaining liabilities, obligations or entitlements of an entity that arise, or could arise, under a *taxation law; or

(ii) advising an entity about liabilities, obligations or entitlements of the entity or another entity that arise, or could arise, under a taxation law; or

(iii) representing an entity in their dealings with the Commissioner; and

(b) that is provided in circumstances where the entity can reasonably be expected to rely on the service for either or both of the following purposes:

(i) to satisfy liabilities or obligations that arise, or could arise, under a taxation law;

(ii) to claim entitlements that arise, or could arise, under a taxation law.

7 Section 50-35(2) of the TAS Act provides:

Federal Court may order you to pay a pecuniary penalty for contravening a civil penalty provision

…

Court may order you to pay pecuniary penalty

(2) If the *Federal Court is satisfied that you have contravened a civil penalty provision, the Federal Court may order you to pay to the Commonwealth, for each contravention, the pecuniary penalty that the Federal Court determines is appropriate (but not more than the maximum amount specified for the provision).

8 Section 70-5(1) provides:

Injunction to restrain or require certain conduct

(1) If, on the application of the Board, the *Federal Court is satisfied that you have engaged, or are proposing to engage, in conduct that would constitute a contravention of a civil penalty provision, the Federal Court may grant an injunction:

(a) restraining you from engaging in the conduct; or

(b) if in the Federal Court's opinion it is desirable to do so, requiring you to do something.

(2) Before deciding the application, the *Federal Court may grant an interim injunction:

(a) restraining you from engaging in conduct; or

(b) requiring you to do something.

The pleaded case

9 The Board alleges that the respondent prepared and lodged with the Commissioner of Taxation income tax returns for persons who were required to give those returns under s 161(1) of the Income Tax Assessment Act 1936 (Cth).

10 It alleges that the respondent was not, however, at any relevant time registered under the TAS Act as a 'registered tax agent'.

11 The Board pleads that the services that the respondent provided constituted a 'tax agent service' within the meaning of the TAS Act. It pleads that is so because each of the services provided by the respondent:

(a) was not a 'BAS Service' as defined in the TAS Act;

(b) was not a 'tax (financial) advice service' as defined in the TAS Act;

(c) was not provided as, or as part of, a legal service;

(d) related to ascertaining liabilities, obligations or entitlements of the taxpayers that arose, or could arise, under a taxation law;

(e) related to representing the taxpayers in their dealings with the Commissioner of Taxation; and

(f) was provided in circumstances where the taxpayers could reasonably be expected to rely on the [services] to:

(i) satisfy liabilities or obligations that arose, or could arise, under a taxation law; and/or

(ii) claim entitlements that arose, or could arise, under a taxation law.

12 It is apparent that the pleading was prepared having regard to the elements of the statutory definition of 'tax agent service'.

13 Further, it is pleaded that the respondent knew or ought to have known that the services she provided were characterised as tax agent services. It says that such knowledge is to be inferred from all of the circumstances, including her repetitive provision of such services, her interactions with the Australian Taxation Office (ATO) and MyGov, and correspondence that was issued to her on 8 March 2018 from the Board, informing her that the Board had received information alleging that she may be providing tax agent services for a fee or reward, whilst unregistered.

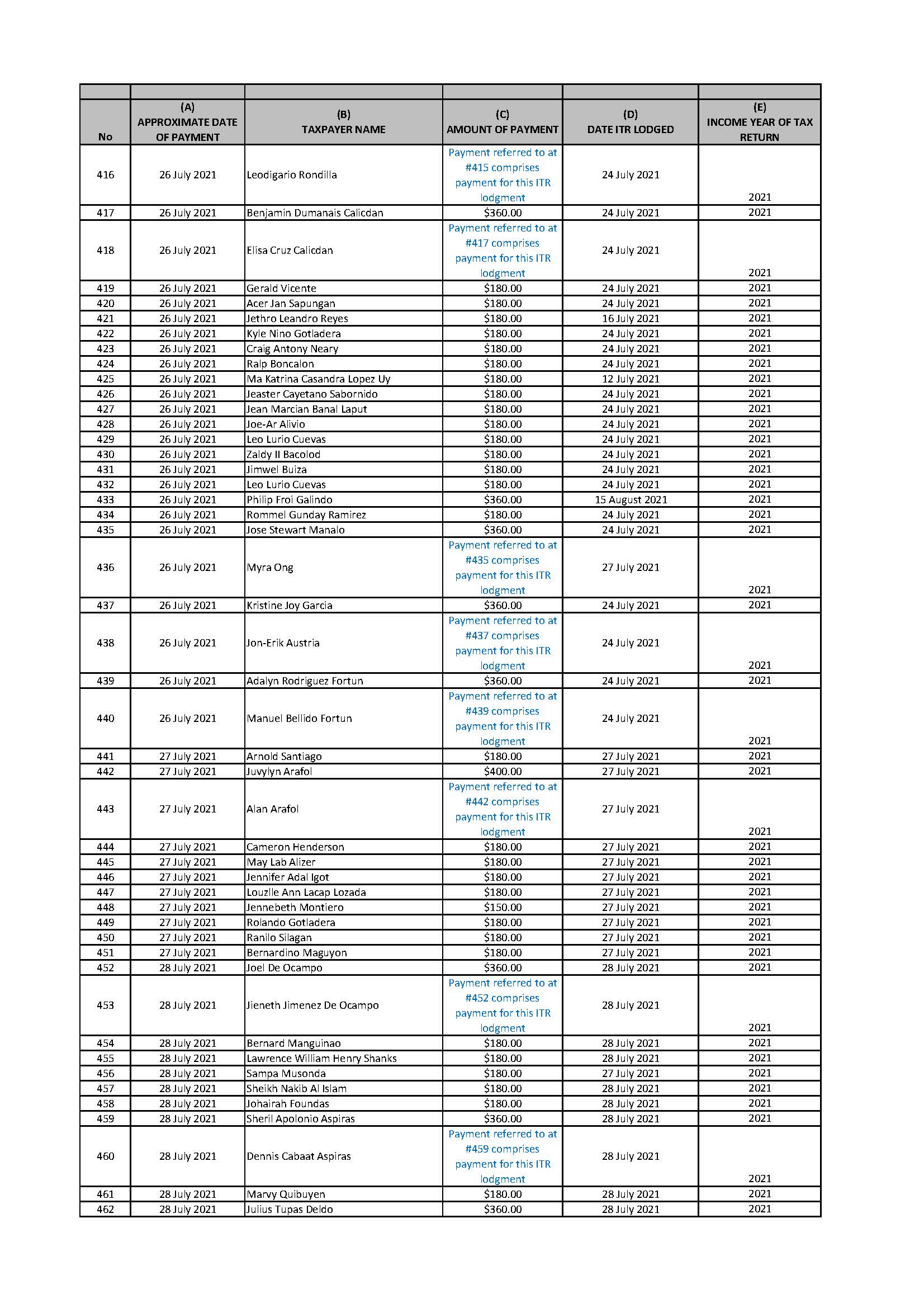

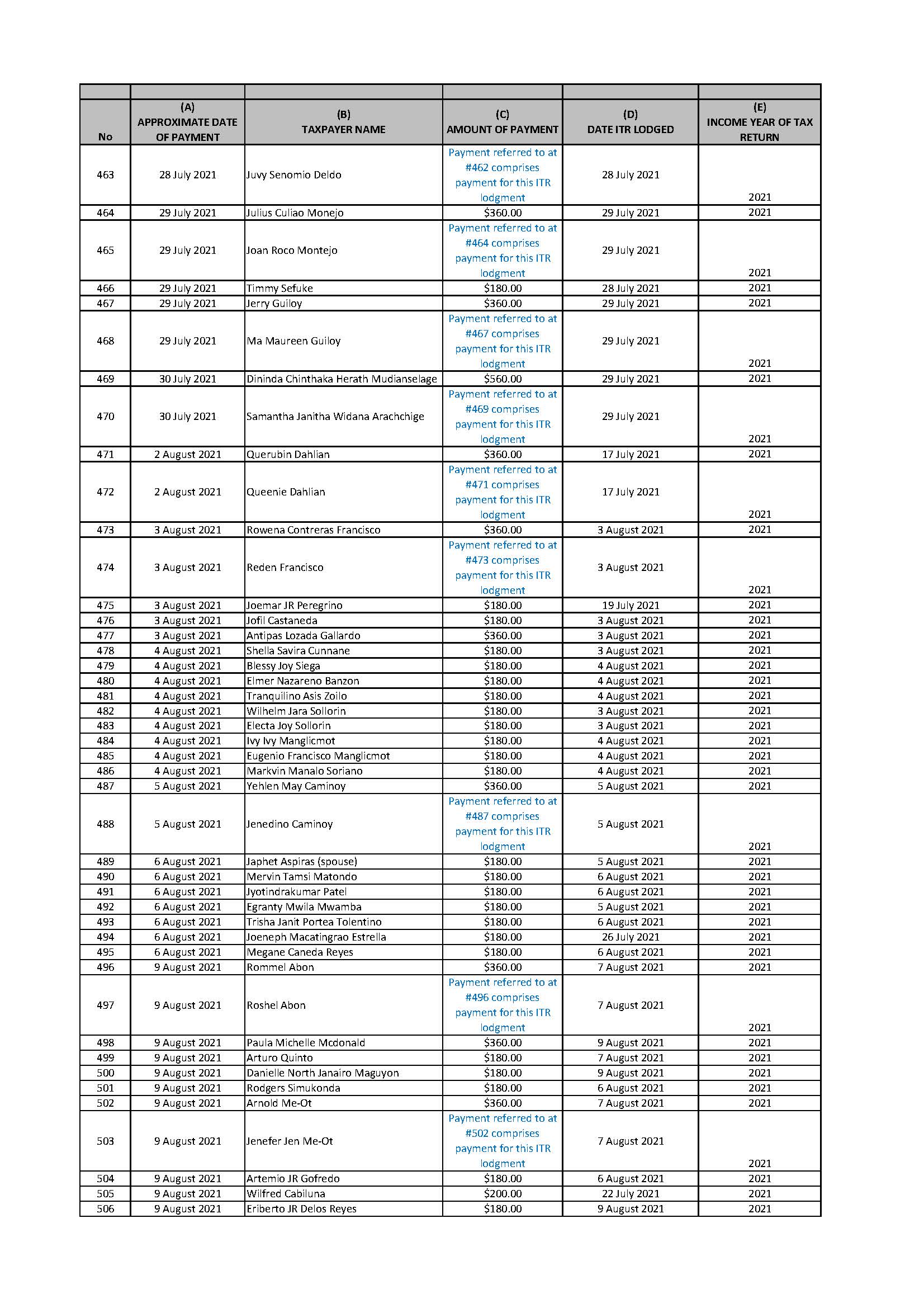

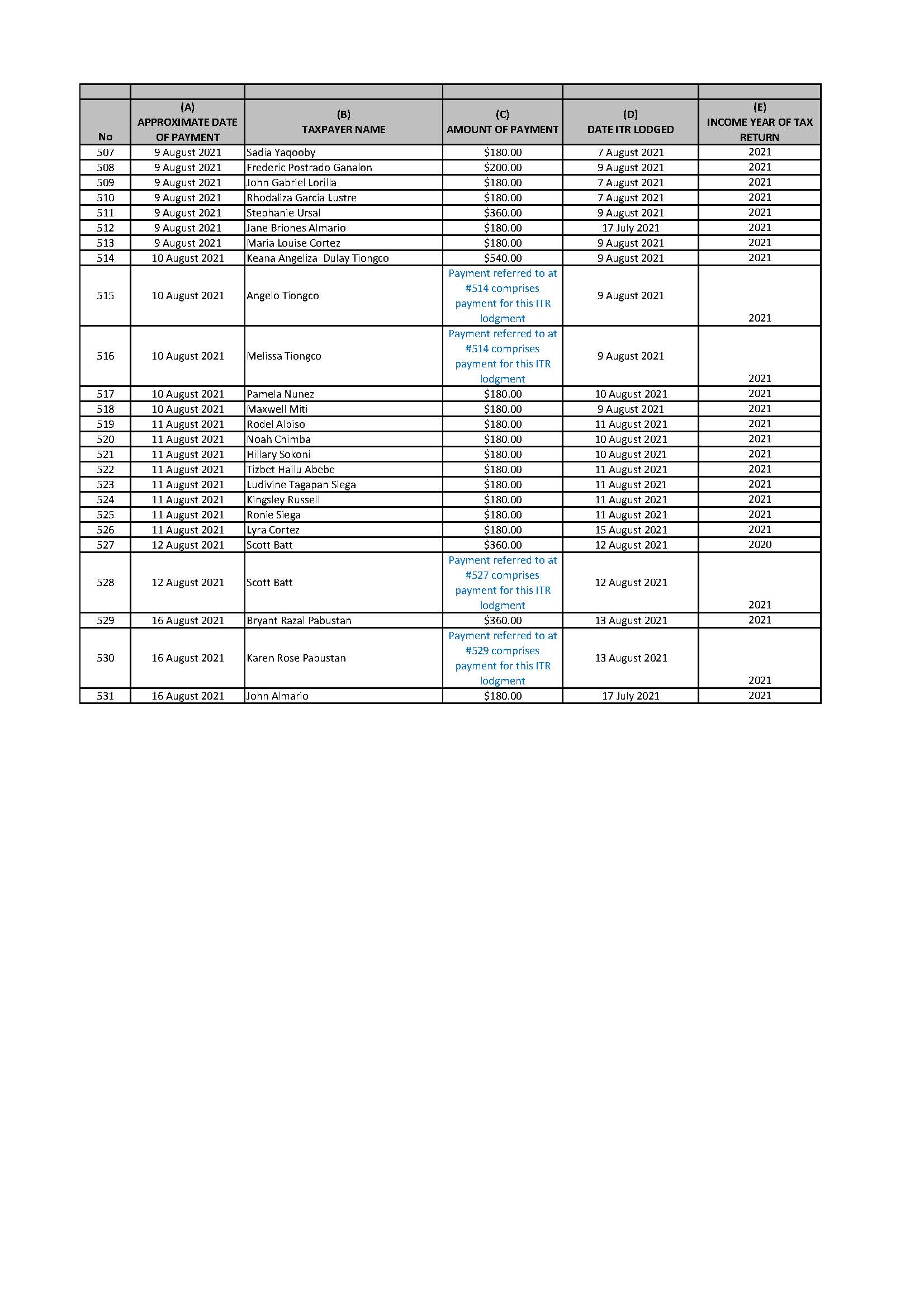

14 The Board pleads that the respondent lodged the 531 returns during the period 1 July 2020 to 15 August 2021, and charged a fee (which appears to have been consistently $180) for each return lodged.

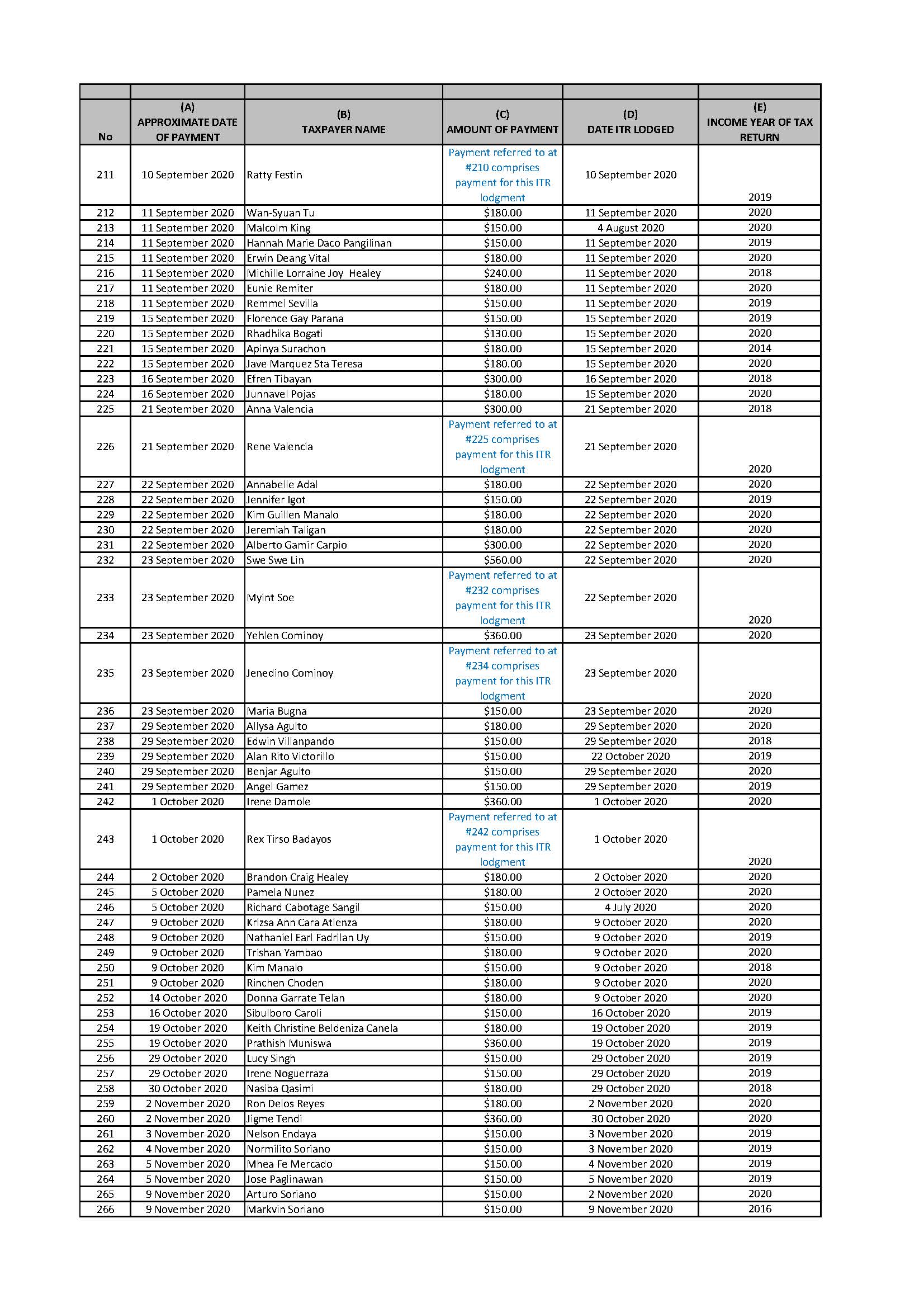

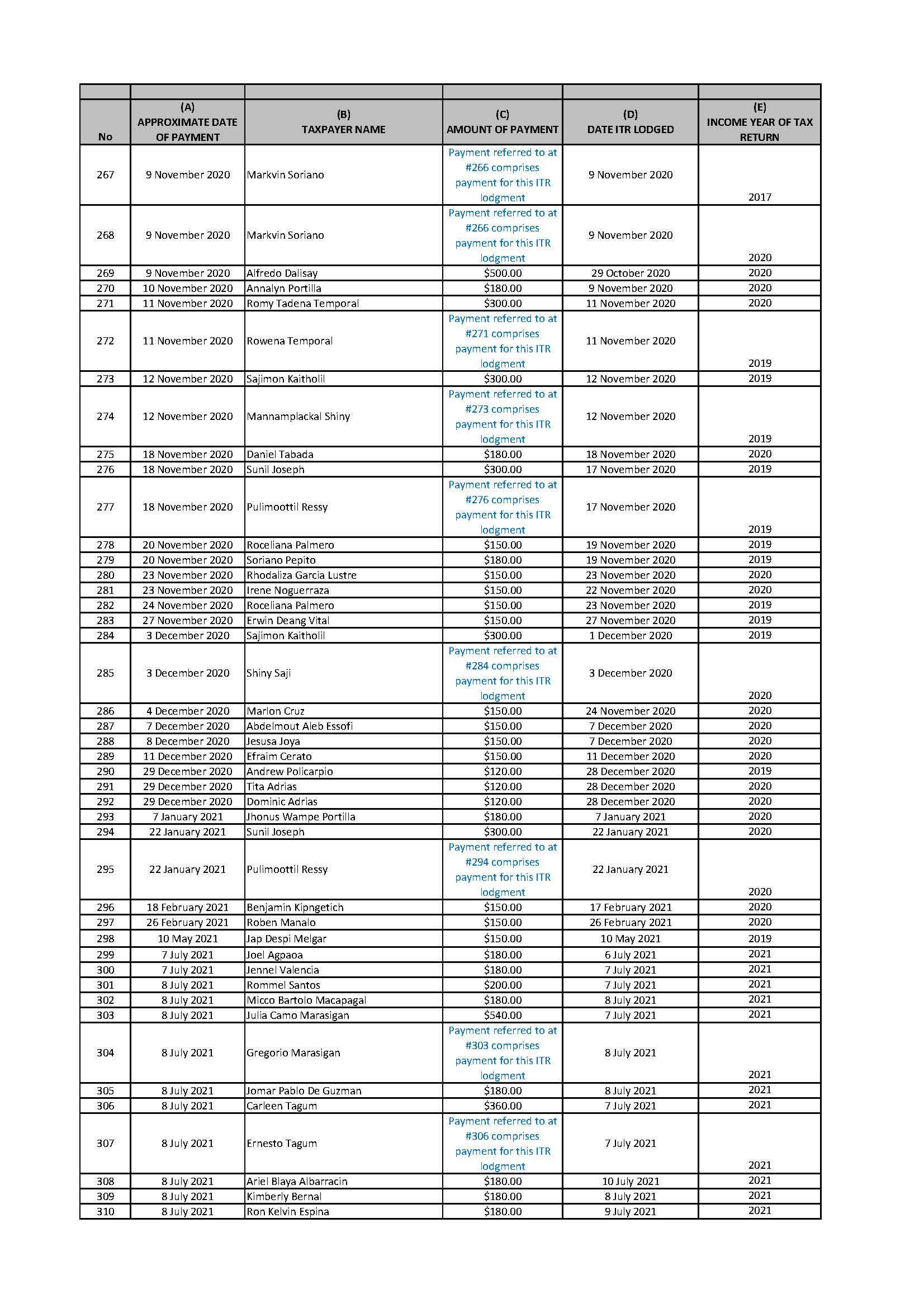

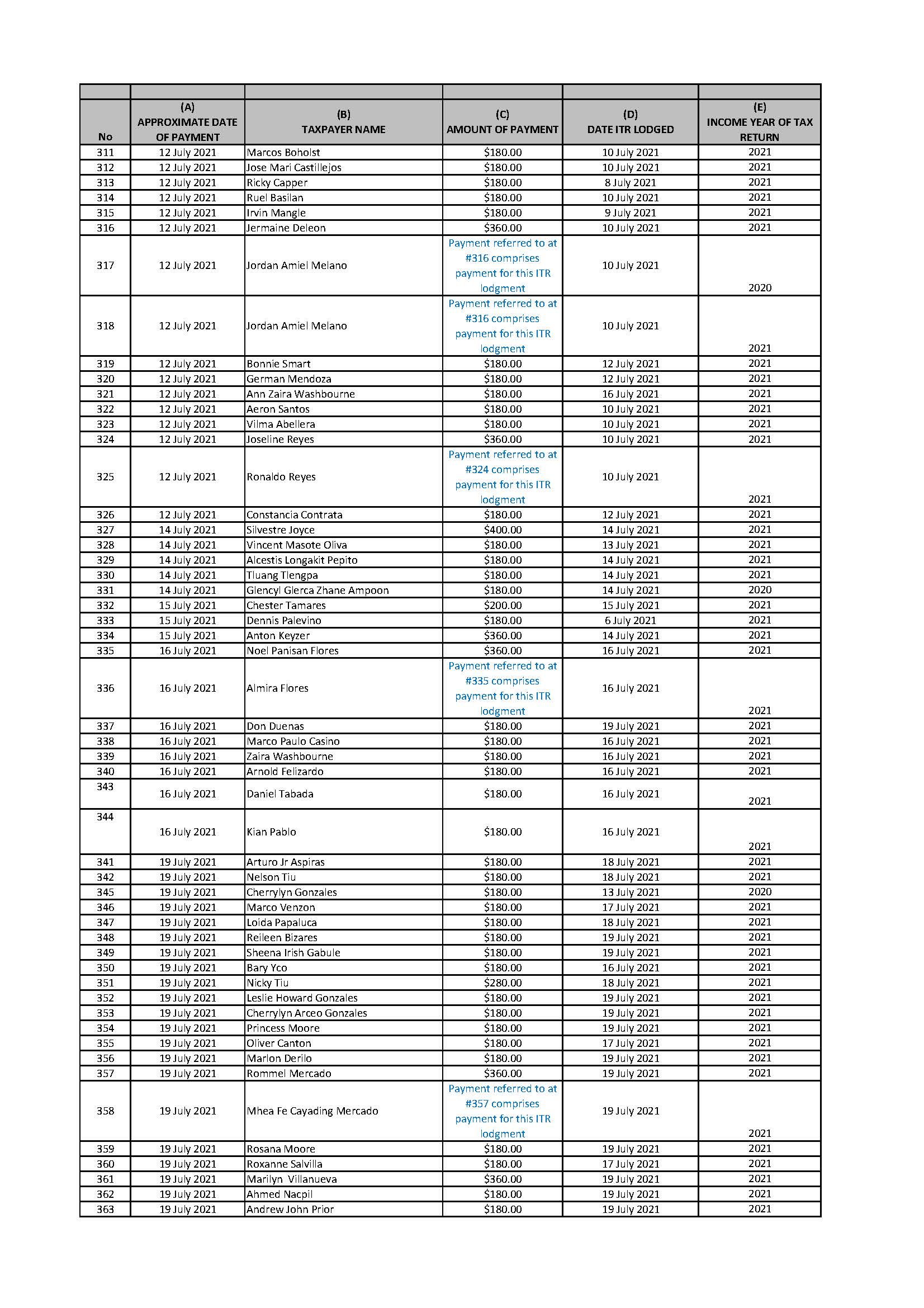

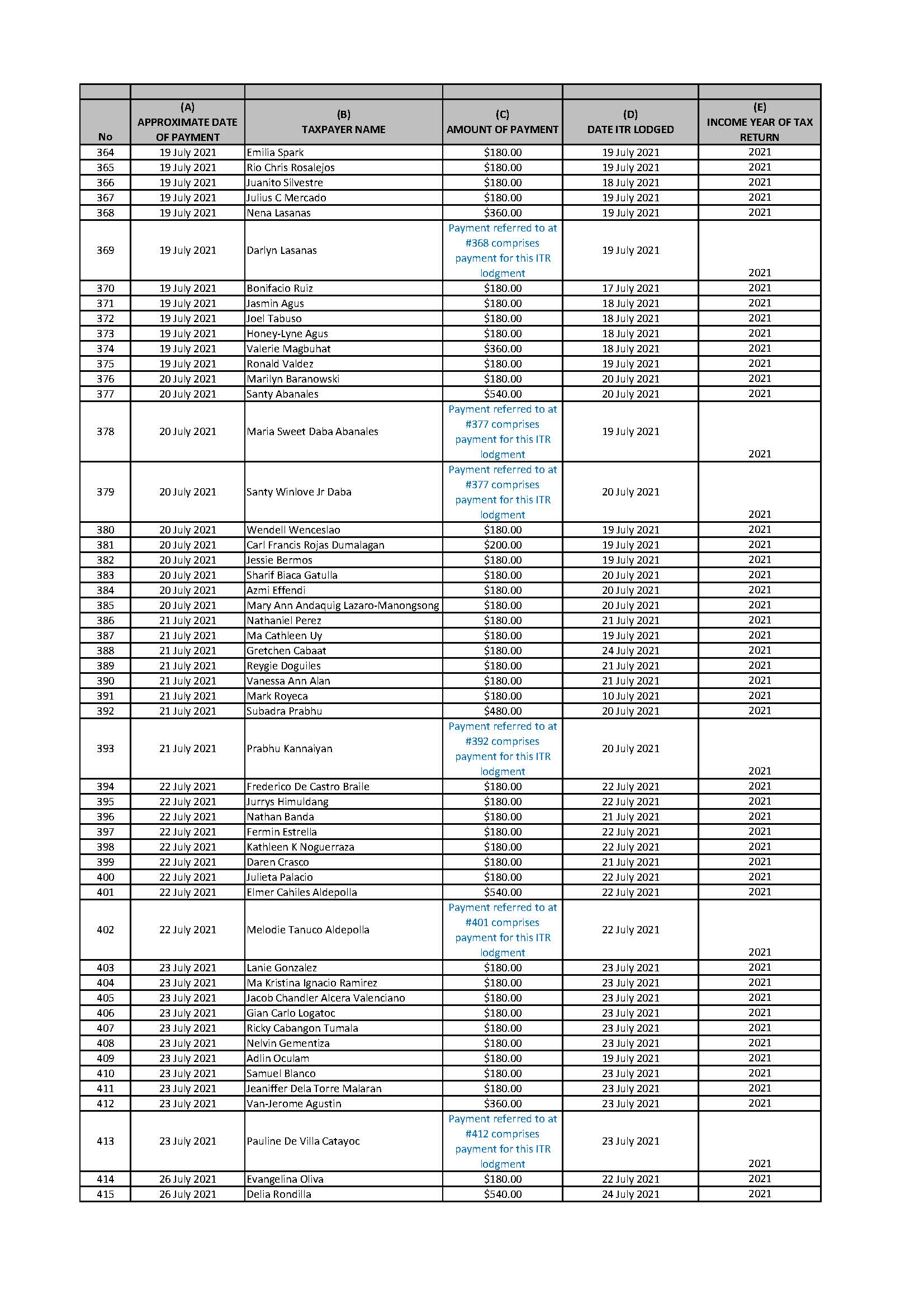

15 The statement of claim annexes a schedule which particularises each of the 531 alleged contraventions of the TAS Act by the respondent. The schedule provides the following information with respect to each alleged contravention:

(a) the taxpayer name, being the person for whom the respondent is alleged to have provided a tax agent service;

(b) the approximate date of payment to the respondent;

(c) the amount of payment to the respondent; and

(d) the date the taxpayer's income tax return (ITR) was lodged with the ATO.

16 Accordingly, the Board alleges, the respondent contravened s 50-5(1) of the TAS Act.

Procedural background

17 This proceeding was commenced by originating application on 12 August 2021.

18 On 23 August 2021 McKerracher J ordered that until the hearing and determination of the originating application or further order, the respondent be restrained from preparing and lodging income tax returns for taxpayers, for a fee or other reward, whilst not a registered tax agent within the meaning of the TAS Act.

19 The Board evinced affidavit evidence as to personal service on the respondent of the originating application and supporting affidavits filed for the purpose of the hearing before McKerracher J. The respondent did not appear at the hearing.

20 The Board's solicitor (relevantly Patrick Long of MinterEllison) has affirmed a number of affidavits that depose to his communications and attempted communications with the respondent.

21 On 30 August 2021 the respondent sent an email to MinterEllison which attached a signed standard form Federal Circuit Court of Australia 'Notice of Address for Service', which disclosed a physical address for service, a mobile phone number and an email address, and identified that the respondent was acting in person.

22 The respondent did not file a notice of address for service in this Court, despite Mr Long emailing her to inform her that she was required to file such notice, and providing the contact details of the Western Australian Registry of the Court.

23 On 3 September 2021 Mr Long emailed the respondent at the email address she had identified for service with respect to an interlocutory application that the Board filed relating to the redaction of confidential information in an affidavit that had been filed on the Boards' behalf. No response was received. On 28 September 2021 I made orders providing for a redacted version of the relevant affidavit to be filed, with the unredacted version to be removed from the Court file. On the same day Mr Long emailed the respondent providing a copy of the orders and the redacted affidavit.

24 On 30 September 2021 the respondent emailed Mr Long apologising for the failure to respond to communications, indicating she had been sick with the flu and due to pregnancy, and stating that she would respond to emails as soon as she became well.

25 On 1 November 2021 I conducted a case management hearing. The Board's counsel participated by Microsoft Teams link but it was open to the respondent to appear in person or by Microsoft Teams link. The respondent was called at the hearing but did not appear. I am satisfied that she had notice of the hearing by way of communications from my chambers to the email address that had been identified and used to communicate with Mr Long. Orders were made at the hearing programming the filing of a notice of address for service, pleadings and submission for the purpose of a hearing. I am satisfied on the basis of Mr Long's evidence that the respondent was served with a copy of the orders.

26 Neither Mr Long nor my chambers received any communication from the respondent with respect to the case management hearing or orders.

27 The Board then sought to amend its application. I am satisfied that the Board by its solicitors sought to confer with the respondent about those amendments. Mr Long provided evidence as to his email communications with the respondent that were unanswered and his phone messages that were unanswered. On 23 November 2021 I granted leave to the Board to file an amended originating application. I am satisfied on the basis of Mr Long's evidence that the respondent was served with the papers filed in support of the application to amend and a copy of the orders of 23 November 2021.

28 On 29 November 2021 the Board filed the amended originating application and a statement of claim.

29 I am satisfied that those documents were provided to the respondent by email and were also served on her (together with a covering letter) by being placed in an envelope which was sent by registered post to the physical address that the respondent had indicated was her physical address for service. Australia Post records indicated that the envelope was delivered on 6 December 2021.

30 Despite the 1 November orders, the respondent did not file a notice of address for service or a defence.

31 On 27 January 2022 Mr Long wrote to the respondent by letter attached to an email, informing her that the Board intended to make an application for default judgment in these proceedings.

32 I am satisfied on the basis of Mr Long's evidence that the letter was also sent separately by Express Post to the respondent and that Australia Post records indicate the relevant envelope was delivered on 31 January 2022.

33 On 11 February 2022 Mr Long relevantly emailed copies of three affidavits upon which the Board relies in this proceeding together with a notice of intention to adduce coincidence evidence.

34 On 14 February 2022 Mr Long emailed the respondent attaching a copy of an affidavit that he had affirmed together with a copy of the Board's interlocutory application seeking default judgement and a covering letter.

35 I am satisfied on the basis of Mr Long's evidence that the documents attached to the 14 February 2022 email were also sent separately by Express Post to the respondent and that Australia Post records indicate the relevant envelope was delivered on 21 February 2022.

36 I conducted a further case management hearing to address the programming of the interlocutory application on 17 March 2022. Mr Long emailed the respondent about programming orders prior to the hearing, but did not receive any response. I am satisfied on the basis of communications from my chambers that the respondent was informed of the case management hearing and accorded the opportunity to appear. Due to COVID-19 guidelines and restrictions then in place, the hearing proceeded by Microsoft Teams link. The respondent was informed of such arrangements and did not seek to appear either by Microsoft Teams link or in person.

37 At the 17 March 2022 case management hearing I fixed the hearing as to all aspects of liability and relief save for the question of penalty for 28 April 2022 and directed that it be conducted by Microsoft Teams link, having regard to uncertainty as to the potential to conduct a hearing in person at the time. Programming orders were made for the filing of submissions by the Board and the respondent. The respondent was ordered to file her submissions by 12 April 2022.

38 I am satisfied on the basis of Mr Long's evidence that a covering letter and the 17 March 2022 orders (which include notice of the hearing date) were served by the Board on the respondent by email (dated 21 March 2022) and by Express Post, and that Australia Post records indicate the relevant envelope was delivered to the respondent's address on 28 March 2022.

39 The Board filed its submissions on 30 March 2022. I am satisfied on the basis of Mr Long's evidence that a covering letter and the Board's submissions and list of authorities were served by the Board on the respondent by email (dated 30 March 2022) and by Express Post, and that Australia Post records indicate the relevant envelope was delivered to the respondent's address on 6 April 2022.

40 Mr Long has affirmed six affidavits in this matter addressing his attempts to communicate with the respondent and the manner in which the Board has provided filed documents and relevant information to the respondent. Mr Long has deposed to the fact that apart from the communications that are referred to at [21] and [24] above, he has received no replies or communications from the respondent.

41 My chambers also took a number of steps to inform the respondent about the hearing. In particular, my associate emailed the respondent at her identified email address on 17 March 2022 attaching the 17 March 2022 orders and noting the hearing date of 28 April 2022. On 21 April 2022 my associate emailed the respondent at the same email address providing a copy of the Microsoft Teams hearing link for the 28 April 2022 hearing. There is no record of any response received from the respondent to those emails.

42 The respondent was called at the hearing but did not appear.

Default judgment

Principles

43 In order to be satisfied that an applicant is entitled to the relief sought in r 5.23(2)(c) of the Federal Court Rules 2011 (Cth), the Court must be satisfied that a respondent has been served with the relevant documents and that the Court has jurisdiction to grant the relief: Speedo Holdings B.V. v Evans (No 2) [2011] FCA 1227 at [18] (Flick J).

44 The principles applicable to the power to enter default judgment were usefully collected by Yates J in Chamberlain Group Inc v Giant Alarm System Co Ltd (No 2) [2019] FCA 1606 as follows:

[13] The power to give judgment against a defaulting party is undoubtedly discretionary. The discretion must be exercised cautiously. Where the defaulting party is a respondent to a pleaded claim, the giving of judgment for final relief on the application will deliver complete success to the applicant without investigation of the merits of the pleaded claim: ACOHS Pty Ltd v Ucorp Pty Ltd [2009] FCA 577 at [27]. There is no requirement that the act or acts of default be intentional or amount to contumelious conduct. There is no requirement that the act or acts of default result in inordinate or inexcusable delay. That said, such features, if present, will be relevant to the exercise of the Court's discretion. So too will conduct that persuades the Court that the defaulting party is manifesting an inability or unwillingness to cooperate with the Court and the other party or parties to the proceeding.

[14] Rule 5.23(2)(c) requires the Court to be satisfied that the applicant is entitled to the relief claimed in the statement of claim. This requirement has been interpreted as meaning that the Court must be satisfied that 'on the face of the statement of claim' the applicant is entitled to the relief that is claimed. It is not a requirement that the applicant prove its claim by way of evidence. Put another way, the facts alleged in the statement of claim are taken to have been admitted: Australian Competition and Consumer Commission v Dataline.Net.Au Pty Ltd [2007] FCAFC 146; 161 FCR 513 at [42]. If, on inspection of the statement of claim, the Court is satisfied that the applicant would be entitled to the relief sought then this requirement of r 5.23(2)(c) will be met: CNIP Pty Ltd v Chan & Naylor Norwest Pty Ltd (No 2) [2011] FCA 1170 at [18] - [19]; Speedo Holdings B.V. v Evans (No 2) [2011] FCA 1227 at [23]. The Court may permit further evidence to be adduced, but not evidence that would alter the pleaded case: Australian Competition and Consumer Commission v Dataline.Net.Au Pty Ltd [2006] FCA 1427; 236 ALR 665 at [45], [48] - [50]; United Broadcasting International Pty Ltd v Turkplus Pty Ltd (No 2) [2010] FCA 1413 at [42] - [44]; Australian Competition and Consumer Commission v Yellow Page Marketing BV (No 2) [2011] FCA 352; 195 FCR 1 at [62] - [63].

45 There are a number of authorities where the Court has entered default judgment in circumstances where the applicant has sought civil penalties and declarations: for example, Australian Competition and Consumer Commission v EDirect Pty Ltd (in liq) [2012] FCA 976; (2012) 206 FCR 160 (Reeves J); Australian Communications and Media Authority v Getaway Escapes Pty Ltd [2016] FCA 795 (Rangiah J); Geneva Laboratories Ltd v Prestige Premium Deals Pty Ltd (No 4) [2016] FCA 867 (Bromwich J); Fair Work Ombudsman v IE Enterprises Pty Ltd [2020] FCA 848 (Anderson J); and Nasib Baik Pty Ltd v Sydney Ridelender Pty Ltd [2022] FCA 301 (Markovic J).

46 The Full Court in Professional Administration Service Centres Pty Ltd v Commissioner of Taxation [2012] FCAFC 180 (Edmonds, McKerracher and Nicholas JJ) noted that an overriding consideration in the exercise of the discretion to dismiss proceedings under r 5.23 is whether any injustice would flow from such an order. However, it stated at [44] that a number of matters fall under the umbrella of that overriding consideration, although they are not intended to be exhaustive:

(i) the nature of the default involved;

(ii) the duration of the default and whether it is continuing;

(iii) the circumstances in which the orders, in respect of which default has occurred, were made including whether the orders made accorded with the practice of the court in making orders of that kind;

(iv) the circumstances which occurred between the time of making the orders and the order for the dismissal of the proceeding, including whether any attempt was made by the defaulting party to amend or set aside the orders to accommodate or deal with these intervening circumstances;

(v) whether the continuing default is occasioning unnecessary delay, expense or other prejudice or unacceptable burden on the respondent;

(vi) the attitude of the applicant to the default and the court's judgment as to whether or not the applicant genuinely wishes the matter to go to trial within a reasonable period;

(vii) the stage that the proceeding has reached - whether they have only recently been commenced; whether it has been commenced for some time but not advanced due, in whole or in part, to the default; or whether the proceeding is in an advanced state ready or nearly ready for hearing;

(viii) the likely disruption to hearing dates or, if not fixed, to setting the matter down for hearing at an early date; and

(ix) the consequences to the applicant of dismissing the proceeding.

47 Whilst acknowledging that those matters were referred to in the context of summary dismissal under r 5.23, their potential relevance in the context of default judgment under the same rule is readily apparent.

Consideration

48 I am satisfied that the respondent was personally served in accordance with the Rules with the originating process and affidavits in support. The respondent was obliged to file a notice of address for service as required by r 5.02 of the Rules, and failed to do so, despite the Board informing her of her obligation. The respondent is in continuing default pursuant to r 5.22(b) of the Rules.

49 I am satisfied that the respondent was on notice of each of the first return of the originating application before McKerracher J on 23 August 2021, the case management hearing before me on 1 November 2021, and the case management hearing before me on 17 March 2022. The respondent failed to attend the hearings and is accordingly in default pursuant to r 5.22(c) of the Rules.

50 Order 4 of the 1 November 2021 orders required the respondent to file a defence. She has not done so. The respondent is accordingly in default pursuant to r 5.22(b) of the Rules.

51 Given those defaults, the Court is empowered to make orders pursuant to r 5.23(2)(c) of the Rules, but there remains a discretion as to whether or not that power should be exercised.

52 It is apparent from the chronology relayed above that the respondent has not engaged in these proceedings. She has evinced no intention to defend the proceedings or proffered any explanation for the various defaults. Apart from the two occasions identified, she has not responded to communications from the Board's solicitors.

53 I note that: the respondent's defaults have been ongoing since the proceedings were commenced; the Board's solicitors have continued to make diligent attempts to contact the respondent and ensure she is on notice of her obligations and the orders of the Court; the respondent has given the appearance of an absence of interest in the proceedings; and the Board has undertaken all reasonable preliminary steps so that the proceeding is otherwise ready for hearing and determination. I am satisfied that on the face of the statement of claim the Board is entitled to the relief that is claimed. The elements of the claimed contraventions are pleaded. Whilst noting that default judgment should not be entered lightly, in the circumstances of this case I am satisfied that it is appropriate to enter judgment in default under r 5.23(2)(c).

Relief sought by the Board

Declaratory relief

54 By her failure to file a defence, and pursuant to the principles cited at [43] and [44] above, the respondent is taken to have admitted the facts pleaded against her in the statement of claim, but not the entitlement to relief flowing from those facts. Accordingly, the respondent is taken to have admitted that she provided tax agent services within the meaning of the legislation on 531 occasions for fee or reward, whilst not a registered tax agent. She is also taken to have admitted that on each occasion when she provided those services she knew or ought to have known that they bore the characteristics of tax agent services as defined. It follows that the Board has established the respondent's contraventions.

55 The Court has a wide discretionary power to grant declaratory relief pursuant to s 21 of the Federal Court of Australia Act 1976 (Cth).

56 The principles with respect to the grant of declaratory relief, and this Court's jurisdiction to make declarations, are well recognised. The question must be a real and not hypothetical one; the applicant must have a real interest in raising it; and there must be a proper contradictor: Forster v Jododex Australia Pty Ltd (1972) 127 CLR 421 at 437-438 (Gibbs J). The principles were extensively analysed and addressed by the Full Court in Clarence City Council v Commonwealth of Australia [2020] FCAFC 134; (2020) 280 FCR 265 at [57]-[75] (not impugned by the appeal to the High Court: Hobart International Airport Pty Ltd v Clarence City Council [2022] HCA 5).

57 Insofar as there is a requirement for there to be a proper contradictor, Bromwich J considered and applied the principles in Geneva Laboratories v Prestige Premium Deals (No 4), stating:

[80] The Full Court considered the requirement of a contradictor in Australian Competition and Consumer Commission v MSY Technology Pty Ltd [2012] FCAFC 56; (2012) 201 FCR 378 in the context of the grant of power in s 21of the Federal Court of Australia Act 1976 (Cth) (the Federal Court Act). Their Honours noted at 382 [14] that '[t]here is a difference between having an interest to oppose the granting of declaratory relief and, having that interest, choosing whether or not to oppose the granting of that relief'.

[81] The Full Court in MSY Technology held at 387 [30] that the requirement for a contradictor was met if there is a party who had an interest to oppose the declaratory relief sought. This was necessary as well because it went to the existence of federal jurisdiction to exercise the power under s 21 of the Federal Court Act, due to the jurisdictional need for a controversy between the parties, even if resolved after commencement of proceedings: MSY Technology at 385 [20].

[82] I interpret the requirement for no more than a joined party having an interest to oppose declaratory relief as encompassing a range of responses from a respondent, from outright opposition, to not turning up despite knowing that a declaration was to be sought, especially if there was precise knowledge of the date of the hearing of the application. It cannot be that a choice made not to participate puts a respondent in a better position than one who attends and presents arguments against relief being granted. Fortunately, that was not a question that I had to resolve as both parties were represented at the hearing of the application for default judgment by solicitors and counsel.

58 In this case the respondent is a person who has a true interest to oppose the declaration. She has chosen not to, despite being served and having all due notice of each relevant filed document, application and hearing.

59 I am also satisfied that there is utility in making the declaration sought. The Court has generally accepted that in proceedings brought by a regulator involving contraventions of civil penalty provisions, a declaration is an available remedy to formally record the basis upon which the proceeding has been resolved, even where penalties are to be imposed.

60 The issue is not hypothetical: it relates to the characterisation of conduct that affects a large number of persons identified as having paid money to the respondent for her services.

61 There will be a declaration in the terms sought by the Board.

Injunctive relief

62 Having regard to the terms of s 70-5(1) of the TAS Act, I am satisfied that the respondent has contravened a civil penalty provision, being s 50-5(1), and having regard to the repetitive nature of the conduct I consider it appropriate that the interim injunction granted by McKerracher J be made permanent.

63 I have referred above to the principle that default judgement is to be entered according to the terms of the pleading alone: Australian Competition and Consumer Commission v Dataline.Net.Au Pty Ltd [2006] FCA 1427 (Kiefel J) as cited by Yates J in Chamberlain Group v Giant Alarm System. ACCC v Dataline.Net.Au concerned resale price maintenance and contraventions of a number of provisions of the Trade Practices Act 1974 (Cth), and the relief sought included declarations, injunctions and pecuniary penalties. Kiefel J cited with approval the decision in Phonographic Performance Ltd v Maitra [1998] 2 All ER 638 at 644 where Lord Woolf MR confirmed the general rule that 'judgment in default is given upon the facts pleaded in the statement of claim and that affidavit evidence to supplement or support those facts is not appropriate as the pleaded facts are deemed to be admitted'. His Lordship went on to say (also at 644):

… However, that cannot be rigidly applied where the judge has to exercise a discretion whether to grant the relief sought. Where an injunction is sought facts relevant to the grant of that injunction, which are not deemed to be admitted, should be brought to the attention of the judge by way of affidavit or otherwise. Further, if the judge is aware of matters relevant to the exercise of his discretion, he can seek an appropriate explanation before coming to any decision …

64 It follows that where the relief is discretionary (including declarations, injunctions, pecuniary penalties), the Court is entitled, if not obliged, to receive materials relevant to the exercise of that discretion so long as that evidence does not contain evidence of additional facts which should have been pleaded in the claim: ACCC v Dataline.Net.Au at [49]-[51].

65 The Board in this case relied upon a number of affidavits sworn or affirmed by taxpayers who had utilised the services of the respondent. It is apparent from the affidavit evidence that the respondent did not take steps to confirm that information included in tax returns was supported or substantiated by reliable documentary evidence. This conduct, together with the apparent failure to respond to the Board's letter of 8 March 2018 referred to in the particulars, the repetitive nature of the contraventions and the matters deemed to be admitted, persuade me that it is appropriate to exercise the Court's discretion to grant an injunction.

66 In coming to this view I have taken into account the potential prejudice to the respondent, but note that the terms of the injunction provide a mechanism for her to provide tax agent services in the future if she becomes a registered tax agent.

67 The terms of the injunction sought by the Board are sufficiently clear, and there will be an order in the terms sought.

Other

68 There will be a separate hearing in due course to address pecuniary penalties sought by the Board. Costs of this hearing will be addressed at that time.

I certify that the preceding sixty-eight (68) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Banks-Smith. |

Associate: