Federal Court of Australia

Australian Securities and Investments Commission v Westpac Banking Corporation (The Consumer Credit Insurance Case) [2022] FCA 359

ORDERS

AUSTRALIAN SECURITIES & INVESTMENTS COMMISSION Plaintiff | ||

AND: | WESTPAC BANKING CORPORATION ACN 007 457 141 Defendant | |

THE COURT DECLARES THAT:

1. During the period 7 April 2015 to 28 February 2017, the defendant (Westpac) in trade or commerce asserted to 99 customers, to whom a consumer credit insurance policy (CCI Policy) called Credit Card Repayment Protection had been supplied, a right to payment from the customer for the CCI Policy, and by each such assertion contravened s 12DM(1) of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) in that:

(a) Westpac had arranged for the CCI Policy to be supplied to each customer without a request from, or on behalf of, the customer;

(b) for that reason and by virtue of s 12DMA of the ASIC Act, the customer was not liable to make any payment for the CCI Policy; and

(c) Westpac issued a “Welcome Letter” which:

(i) referred to the details of the CCI Policy including policy number, policy commencement date, the credit card to which the policy related and the name of the insured person; and

(ii) stated:

Credit Card Repayment Protection costs 52 cents for every $100 owing on your credit card. Your monthly premium is calculated on the balance owing on your credit card at the end of each statement cycle, and interest may be payable on the premium.

2. During the period 7 April 2015 to 28 February 2017, Westpac in trade or commerce asserted to 42 customers, to whom a CCI Policy called Flexi Loan Repayment Protection had been supplied, a right to payment from the customer for the CCI Policy, and by each such assertion contravened s 12DM(1) of the ASIC Act in that:

(a) Westpac had arranged for the CCI Policy to be supplied to each customer with a request from, or on behalf of, the customer;

(b) for that reason and by virtue of s 12DMA of the ASIC Act, the customer was not liable to make any payment for the CCI Policy; and

(c) Westpac issued a “Welcome Letter” which:

(i) referred to the details of the CCI Policy including policy number, policy commencement date, the Flexi Loan to which the policy related and the name of the insured person; and

(ii) stated

Flexi Loan Repayment Protection costs 30 cents for every $100 owing on your Flexi Loan. Your monthly premium is calculated on the balance owing on your Flexi Loan at the end of each statement cycle, and interest may be payable on the premium.

3. By reason of the above matters, Westpac failed to comply with the financial services law and thereby contravened s 912A(1)(c) of the Corporations Act 2001 (Cth).

THE COURT ORDERS THAT:

4. Westpac pay a pecuniary penalty to the Commonwealth of Australia in respect of each declared civil penalty contravention in the total amount of $1.5 million.

5. Westpac pay the plaintiff’s costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

KATZMANN J:

Introduction

1 The Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) prohibits a person, in trade or commerce, from asserting a right to payment for unsolicited financial services or unsolicited financial products (s 12DM(1)). A financial services licensee who does so also contravenes s 912A(1)(c) of the Corporations Act 2001 (Cth).

2 Westpac Banking Corporation (Westpac) is a financial services licensee and a provider of financial services within the meaning of the ASIC Act. It is commonly known as one of the big four Australian banks because of its dominant place in the market.

3 In this proceeding, instituted by ASIC on 7 April 2021, Westpac has admitted to 141 contraventions of s 12DM(1) over a period of nearly two years, from 7 April 2015 to 28 February 2017 (penalty period). Each of the contraventions relates to the issue of a consumer credit insurance (CCI) policy to a customer of the bank who did not seek it and who did not agree to its acquisition. While Westpac has since cancelled the policies and refunded the premiums paid by these customers, it is common ground that, but for their complaints, it would not have done so.

4 ASIC seeks declaratory relief and pecuniary penalties as well as orders for adverse publicity. The parties have agreed on the facts necessary to support declarations they now jointly invite the Court to make. They also jointly invite the Court to make a pecuniary penalty order in the amount of $1.5 million and to order Westpac to pay ASIC’s costs. Orders for adverse publicity, which were originally sought, are not pressed. The parties provided joint, helpful submissions.

General principles

5 In a case such as this, where a regulator and a contravener seek declarations and orders by consent, the principles are well-established. First, there is a public interest in settlement but the Court must satisfy itself that it has the power to make the orders and that the orders are appropriate. There must be evidence to support the relief sought and the Court’s satisfaction must be based on that evidence. Second, the proposed orders must not be contrary to the public interest and at least be consistent with it. Third, the Court should exercise some restraint when scrutinising proposed terms of settlement especially where both parties are legally represented. Fourth, in deciding whether agreed orders conform to legal principle, the Court is entitled to treat the consent of the defendant as an admission of all facts necessary or appropriate for the grant of the relief sought. See Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2014] FCA 1405 at [70]–[73] (Gordon J).

The statutory framework

6 Section 12DM is one of the suite of provisions outlawing reprehensible business practices of various kinds conducted in connection with the supply of financial services and products. Despite the use of the present tense all the references in this judgment to the provisions of the legislation are references to those provisions during the penalty period.

7 Section 12DM falls within Pt 2 Div 2 Subdiv D of the ASIC Act. Division 2 deals with unconscionable conduct and consumer protection in relation to financial services and products, Subd C with unconscionable conduct in relation to financial services, Subdiv D with consumer protection in relation to financial services and/or products.

8 In the present case, while the contraventions are of s 12DM, s 12DMA is also relevant.

9 Section 12DMA provides that:

If a person, in trade or commerce, supplies unsolicited financial services or unsolicited financial products to another person, the other person:

(a) is not liable to make any payment for the services or products; and

(b) is not liable for loss or damage as a result of the supply of the services or products.

10 As the parties submitted, ss 12DM and 12DMA were and remain, albeit in their amended forms, a statutory couplet with analogues in ss 40 and 41 of the Australian Consumer Law (in Sch 2 to the Competition and Consumer Act 2010 (Cth)), formerly ss 64 and 65 of the Trade Practices Act 1974 (Cth) (TPA).

11 Section 12BEA(1) of the ASIC Act relevantly provides:

For the purposes of this Division, a person is taken to assert a right to payment from another person if the person:

(a) makes a demand for the payment or asserts a present or prospective right to the payment; or

…

(e) sends any invoice or other document that:

(i) states the amount of the payment; or

(ii) sets out the price of unsolicited financial services; or

(iii) sets out the charge for an advertisement, for financial services or financial products, that has been published;

and does not contain a statement, to the effect that the document is not an assertion of a right to a payment, that complies with any requirements prescribed by the regulations.

12 Section 2E of the Australian Securities and Investments Commission Regulations 2001 (Cth) prescribes that the statement had to say, in text that was the most prominent text in the document:

This is not a bill. You are not required to pay any money.

13 Each of the terms “unsolicited financial services” and “unsolicited financial products” is a defined term. “Unsolicited financial products” means “financial products supplied to a person without any request made by the person or on the person’s behalf” and “unsolicited financial services” has a corresponding meaning (s 12BA). “Supply” and “supplied” are also defined in s 12BA. “Supply” includes to “provide, grant or confer when used as a verb in relation to services” and “supplied” has a corresponding meaning.

14 “Financial product” for the purposes of Pt 2 Div 2 expressly included, with certain exceptions presently irrelevant, contracts of insurance (s 12BAA(7)(d)) and also “a life policy, or a sinking fund policy, within the meaning of the Life Insurance Act 1995, that is not a contract of insurance” (s 12BAA(7)(e)). A person provides a financial service for the purposes of Pt 2 Div 2 if the person “deal[t] in a financial product” (s 12BAB(1)(b)). “Issuing a financial product” constitutes “dealing in a financial product” (s 12BAB(7)(b)). And “arranging for a person to engage in conduct referred to in [s 12BAB(7)] is also dealing in a financial product, unless the actions concerned amount[ed] to providing financial product advice” (s 12BAB(8)).

15 It follows that, where one party arranges for another to issue an insurance policy, the first party supplies a financial service and the other party supplies a financial product.

16 Section 912A(1)(c) of the Corporations Act relevantly provides that a financial services licensee must comply with the financial services laws, which relevantly includes a provision of Pt 2 Div 2 of the ASIC Act, like s 12DM.

The facts

17 A statement of agreed facts and admissions was tendered in evidence. On the basis of the agreed facts and admissions I make the following findings.

Westpac and consumer credit insurance policies

18 During the penalty period Westpac held, and continues to hold, an Australian Financial Services Licence. During the same period and continuing, Westpac has been a provider of financial services within the meaning of the ASIC Act. One of the financial services it has provided is arranging for CCI policies to be issued to customers. Those CCI policies related to Westpac credit cards and a line of credit known as Westpac “Flexi Loans” (the Credit Products). This case is concerned with two types of CCI policies:

(1) “Credit card replacement protection” (CCRP), formerly known as “credit card insurance” and later “credit card protection”, which was linked to a Westpac credit card account; and

(2) Flexi-Loan Repayment Protection (FLRP), which was linked to a Flexi Loan account.

19 I was informed at the hearing that there is no material difference between the two products.

20 During the penalty period 35,822 CCRP and 30,140 FLRP policies were sold. From now on, when it is unnecessary to distinguish between the two types of policies, I will refer to them as “the CCI Policies”.

21 Subject to the terms of the relevant CCI Policy, certain benefits were payable if the customer lost his or her job, became unfit for work or died.

22 The CCI Policies were issued by Westpac General Insurance Limited and Westpac Life Insurance Services Limited (Westpac insurance companies), both wholly owned subsidiaries of Westpac. Each was a financial product within the meaning of s 12BAA(7)(d) and/or (e) of the ASIC Act.

23 Each time Westpac arranged for a CCI Policy to be issued, Westpac arranged for the two Westpac insurance companies to deal in a financial product within the meaning of s 12BAB(7)(b). Westpac thereby dealt in the financial product for the purposes of s 12BAB(8). By so dealing, Westpac provided, and therefore supplied, a financial service within the meaning of s 12BAB(1)(b).

24 All the relevant conduct was in trade or commerce.

The operation of the CCI Policies

25 Under the terms of each of the CCI Policies, the Westpac insurance companies had a right to payment of a monthly premium. In accordance with the terms of each of those policies, Westpac debited the amount of the monthly premiums to the Credit Product account of each customer who held a CCI Policy and who had accrued a debit balance on his or her Credit Product account. In the case of CCRP, each month the amount of the premium was calculated on the debit balance of the underlying credit card at the end of the monthly statement cycle and charged as a debit to the credit card account. In the case of FLRP, each month the amount of the premium was calculated on the debit balance at the end of the monthly statement cycle and charged as a debit to the Flexi Loan account.

26 Each month Westpac paid the Westpac insurance companies an amount corresponding to the premium due by customers calculated in this way and Westpac debited the credit card or Flexi Loan account of each of those customers in an amount equal to the premium paid or to be paid by Westpac to the Westpac insurance companies. Westpac retained part of the sum due to the Westpac insurance companies as commission in accordance with the arrangements between Westpac and each of those companies respectively.

27 All the accounts to which Westpac debited amounts for the monthly premiums were credit accounts. In accordance with the terms and conditions of the Credit Products, Westpac had a right to payment from the customer of amounts debited to their account (including the amount of any premium charged in respect of a CCI Policy), and, subject to the debit balance being repaid each month, a right to payment of interest by the customer.

28 The amount debited for premiums due under the CCI Policies varied from customer to customer and, in relation to each customer, from month to month, depending upon the amount of the customer’s debit balance on the last day of that customer’s monthly statement cycle.

29 If there was no balance owing on the related Credit Product account at the end of the customer’s monthly statement cycle, no CCI premium was charged to the customer that month.

Westpac’s sales practices

30 During the penalty period, Westpac sold its Credit Products in bank branches, over the telephone or online.

31 CCI is “add on” insurance which means that it is not usually actively sought out by the customer but was usually sold when a customer applied for another product (such as a Credit Product) and sometimes sold when a customer contacted the bank for another purpose (such as to request an increase in the credit limit of the related Credit Product).

32 Westpac offered staff performance incentives (variable awards) for selling financial products. But at all material times, including during the penalty period, the revenue generated by the sale of a single CCI Policy was not “overly significant”. That is to say, it was not high in comparison to other lines of credit. But anecdotes from Westpac’s frontline staff, reported to certain members of Westpac’s senior management, including the Chief Executive of Australian Financial Services, indicated to Westpac that CCI Policies could take less incremental (or additional) effort to sell than other products because it was “add on” insurance, as explained above at [31]. In addition, in order to be eligible for a variable reward, branch and call centre staff were required to satisfy criteria (known as “gate openers”). The criteria included: achieving expected behavioural standards (in line with Westpac’s values); complying with the risk and compliance requirements outlined for the role (such as completing all requisite training and accreditation in the role); and demonstrating effective performance in the role. If these minimum requirements were not met, an employee would not be eligible for any variable reward, regardless of their performance against any financial and non-financial key performance indicators.

33 A sale of a Credit Product in a branch or over the telephone was made by Westpac staff using Relationship Builder. This was a software application that guided branch staff through customer conversations. Westpac staff accessed Relationship Builder and completed the steps in the system by which the Credit Product was sold. Relationship Builder also permitted Westpac staff to arrange for the issue of a CCI Policy related to the Credit Product being sold, by completing further steps in the system. The further steps included requiring bankers to click a box recording that the customer consented to purchasing the CCI Policy. If this box was not clicked, the CCI Policy could not be issued.

34 The customer interacted with the Westpac staff but had no access to Relationship Builder.

35 At all material times, including during the penalty period, Westpac conducted training for its branch staff and call centre staff. During the training, amongst other things Westpac instructed the banker selling a CCI Policy to obtain the consent of the customer to discuss CCI; obtain the consent of the customer to purchase a CCI Policy; and inform the customer that CCI was optional. But during the penalty period a customer who was sold a CCI Policy in a branch or over the telephone was not required to complete a written application form stating that he or she consented to purchase the CCI Policy. And, while telephone calls were recorded, Westpac’s internal policies did not require recordings of telephone calls to be kept for more than 45 days.

ASIC regulatory action and Westpac’s response

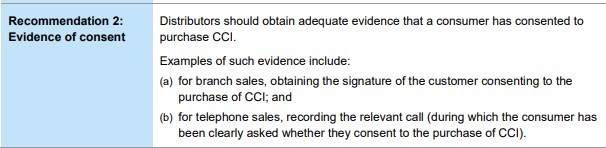

36 In 2010 and 2011 ASIC conducted a review into the CCI sales practices of the banks generally. That review resulted in the publication of Report 256: Consumer Credit Insurance: A Review of Sales Practices by Authorised Deposit Taking Institutions (Report 256). Report 256 included the following recommendation:

37 At the time that ASIC released Report 256, Westpac did not have in place a process for obtaining the signature of the customer consenting to purchase a CCI Policy and did not retain a recording of telephone sales for more than 45 days.

38 During the period 2012 to March 2017, Westpac had processes in place to obtain the following evidence that a customer had consented to purchase CCI:

(1) in respect of branch and telephone sales, the electronic record made by Westpac staff but not the customer; and

(2) in respect of telephone sales, by Westpac recording those conversations and keeping those recordings for 45 days.

Westpac did not implement a process to obtain the signature of the customer consenting to purchase a CCI Policy or to retain a recording of telephone sales for more than 45 days.

39 On 1 April 2014, more than a year before the start of the penalty period, Westpac’s Chief Executive of Australian Financial Services commissioned an internal review into the controls on the sale of CCRP Policies (Deep Dive).

40 On 5 June 2014 a report of findings and recommendations from the Deep Dive was provided to the Chief Executive of Australian Financial Services.

41 Amongst other things, the report found that despite an upgraded control environment, the following remained as key areas of concern:

(a) the lack of robust preventative or detective controls to evidence customer consent for CCRP within credit card application forms; and

(b) the fact that verbal consent in branches was recorded on systems by branch staff.

42 The report contained a number of core recommendations to bring about an appropriate control environment, including the development of controls to evidence customer consent. One of the proposed controls was a consent document to be signed by both the banker and the customer.

43 Between 5 June 2014 and 23 July 2014 the Chief Executive of Australian Financial Services endorsed the Deep Dive report. On 23 July 2014 the report was presented in a meeting to the AFS Leadership Team, including the Group Executive of Westpac Retail and Business Banking and the Chief Executive Officer of BT Financial Group, Westpac’s wealth business which included Westpac General Insurance Services and Westpac Life Insurance Services Limited.

44 In response to the issues raised in the Deep Dive report, which included those referred to in [41] above as well as other unrelated issues in connection with concerns about CCI sales, Westpac suspended sales of CCI in its branch network from on or around 20 October 2014 to on or around the end of November 2014 to allow Westpac time to implement measures addressing certain findings made in the report. Westpac took steps to implement a number of the recommendations made in the Deep Dive report including by:

(a) providing additional staff training (including mandatory refresher training), to be completed annually, that addressed the key requirements for a compliant sale; and

(b) developing a reporting model to identify sales of CCI made by bankers who were not accredited (according to Westpac’s internal policies) to sell CCI.

45 But it was not until after the penalty period (in March 2017) that Westpac implemented the recommendation for the development of a consent document to be signed by both the banker and the customer.

Customer complaints

46 Between 1 December 2014 and 31 December 2017, Westpac received approximately 3,730 complaints from customers to whom a CCI Policy had been supplied. These complaints were initially recorded by Westpac as consent related although not all of them were in fact consent related. In the same period Westpac arranged for approximately 92,609 new CCI policies and had a total of approximately 190,000 CCI policies on issue at any time.

47 Westpac’s practice was to refund any customer who made a consent related complaint unless a signed application form recording the customer consent or a sales call recording could be found. In accordance with that practice, Westpac refunded premiums to many of the 3,730 customers who made complaints. A total amount of approximately $1.7 million was refunded.

Unsolicited CCI Policies and the affected customers

48 During the penalty period, Westpac sold one or more Credit Products, either in a branch or over the telephone, to each of the customers with which the 141 contraventions are concerned (the affected customers). None of them requested Westpac to arrange a CCI Policy to be issued to him or her or the Westpac insurance companies to supply him or her with a CCI Policy. Yet Westpac arranged for one or more CCI Policies to be issued to each of them, and the Westpac insurance companies supplied the CCI Policy or CCI Policies to them. A total of 99 CCRP policies related to a credit card were supplied to 99 affected customers and a total of 42 FLRP policies related to a Flexi Loan were supplied to 42 affected customers.

49 Since none of the affected customers had asked to acquire the CCI Policy that was issued to them:

(1) Westpac’s arrangement for the issuance of the relevant CCI Policy was an unsolicited financial service under s 12BA of the ASIC Act;

(2) the subsequent issue of the CCI Policy was the supply of an unsolicited financial product under s 12BA of the ASIC Act;

(3) none of the affected customers was liable to make any payment for the relevant CCI Policy under s 12DMA(a) of the ASIC Act; and

(4) Westpac was prohibited from asserting a right to payment from the affected customer for the relevant CCI Policy under s 12DM(1) of the ASIC Act.

The Welcome Letters and the assertion of the right to payment

50 During the penalty period, shortly after arranging for a CCI Policy to be issued to him or her, Westpac sent, or caused to be sent, to each affected customer a letter entitled “Policy Schedule” (Welcome Letter).

51 For CCRP, for the whole of the penalty period each Welcome Letter:

(1) referred to the details of the relevant CCI Policy, including the policy number, policy commencement date, the credit card to which the policy related and the name of the insured person; and

(2) stated:

Credit Card Repayment Protection costs 52 cents for every $100 owing on your credit card. Your monthly premium is calculated on the balance owing on your credit card at the end of each statement cycle, and interest may be payable on the premium.

52 For FLRP, for the whole of the penalty period each Welcome Letter:

(1) referred to the details of the relevant CCI Policy, including the policy number, policy commencement date, the Flexi Loan to which the policy related and the name of the insured person; and

(2) stated:

Flexi Loan Repayment Protection costs 30 cents for every $100 owing on your Flexi Loan. Your monthly premium is calculated on the balance owing on your Flexi Loan at the end of each statement cycle, and interest may be payable on the premium.

53 Each Welcome Letter was sent in trade and commerce and constituted an assertion by Westpac of a right to payment from the affected customer for the relevant CCI Policy.

Complaints by the affected customers

54 Each of the affected customers contacted Westpac about their CCI Policy within three months of the date on which it was issued. During the course of those interactions, each of those customers made a positive statement to the effect that they had not agreed to acquire a CCI Policy.

55 In order to complain, the affected customers were generally required to telephone a Westpac call centre, which could be a time-consuming process, and provide their identification information and speak to multiple Westpac staff. Certain affected customers were required to explain their complaint more than once and some of them contacted Westpac more than once in relation to their complaint.

56 Following each complaint, the CCI Policy of each affected customer was cancelled.

57 Westpac also provided refunds of premiums paid by affected customers in relation to their CCI Policies shortly after the making of the complaint. Of the affected customers, 125 were given a full refund; 14 did not pay a premium; and two (whose premiums totalled $19.65) did not receive a refund at the time of their complaints but later received full refunds.

58 In circumstances where each of the affected customers had in fact been issued with an unsolicited CCI Policy, in the ordinary course, had any of the affected customers not complained, Westpac would not have cancelled his or her CCI Policy or provided a refund of the premiums.

59 The affected customers paid a total of $10,999.49 in premiums for their CCI Policies. The total amount of refunds of the premiums paid for the CCI Policies issued to the affected customers in the penalty period (excluding over-refunds) was $10,999.39 (including refunds of $19.65 paid to two customers made after the commencement of this proceeding). The slight discrepancy in the total amount paid and the total amount refunded was due to inadvertence in the payment of a refund in one case.

60 During the period between the CCI Policy being issued and cancelled, each affected customer had the benefit of the insurance cover provided by the policy, but none made any claims under their respective CCI Policies and therefore received no financial return.

61 On each of the 141 occasions it sent a Welcome Letter to one of the affected customers, Westpac contravened s 12DM(1) of the ASIC Act.

62 By reason of the contraventions Westpac contravened s 912A(1)(c) of the Corporations Act.

63 In order to avoid unnecessary repetition, additional facts relating to some of the matters relevant to penalty I set out below in the context in which they arise for consideration.

Should the declarations be made?

64 The Court has power to grant declaratory relief. See Federal Court of Australia Act 1976 (Cth), s 21. In the case of a contraventions of s 912A of the Corporations Act, s 1101B(1)(a)(i) of the Corporations Act is an additional source of power. These are broad discretionary powers. In general, the power is properly exercised where the question raised is real and not theoretical, where the person who raises it has a real interest in doing so, and where there is a proper contradictor: Russian Commercial and Industrial Bank v British Bank for Foreign Trade Ltd. [1921] 2 AC 438 at 448 (Lord Dunedin); Forster v Jododex Australia Pty Ltd (1972) 127 CLR 421 at 437-438 (Gibbs J).

65 Each of these circumstances is present here. The questions here are not theoretical. They were raised by the regulator in the performance of its statutory powers and functions and in pursuance of its statutory obligations (see ASIC Act, s 1(2)(g)). Westpac is a proper contradictor, despite the fact that it consents to the making of the declarations, as it has a true interest in the action: Oil Basins Limited v Commonwealth of Australia (1993) 178 CLR 643 at 648–9 (Dawson J); IMF (Australia) Ltd v Sons Of Gwalia Ltd (Administrator Appointed) [2004] FCA 1390; 211 ALR 231; 22 ACLC 1554; 51 ACSR 111 at [47] (French J); Australian Competition and Consumer Commission v MSY Technology Pty Ltd (2012) 201 FCR 378 at [30] (Greenwood, Logan and Yates JJ).

66 There is utility in granting declaratory relief and declarations in the proposed form or to the same effect are appropriate. The agreed facts and admissions are sufficient to support them. The declarations will serve to mark the Court’s disapproval of the contravening conduct, vindicate the regulator’s claim, act at least to some extent as a deterrent, and help the regulator to carry out its duties. See, for example, Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union (2017) 254 FCR 68 at [91], [93] (Dowsett, Greenwood and Wigney JJ) (ABCC v CFMEU).

Should a pecuniary be imposed and, if so, in what amount?

The power to impose penalties

67 The power to impose a civil penalty for a contravention of this kind is contained in s 12GBA(1) of the ASIC Act. During the penalty period, s 12GBA(1) relevantly provided that:

If the Court is satisfied that a person:

(a) has contravened a provision of Subdivision C, D or GC (other than section 12DA);

…

the Court may order the person to pay to the Commonwealth such pecuniary penalty, in respect of each act or omission by the person to which this section applies, as the Court determines to be appropriate.

The parties’ agreement

68 ASIC and Westpac agree that $1.5 million is an appropriate pecuniary penalty for the 141 contraventions of s 12DM(1). No penalty may be imposed for a contravention of s 912A(1) of the Corporations Act as it is not and was not during the penalty period a civil penalty provision.

The statutory maximum

69 The maximum penalty for a contravention of s 12DM(1) by a body corporate was 10,000 penalty units: s 12GBA(3) item 2. The maximum penalty provides a “yardstick” to be taken into account with all other relevant factors: Australian Competition and Consumer Commission v Reckitt Benckiser (Australia) Pty Ltd [2016] FCAFC 181; 340 ALR 25 at [154]-[156] (Jagot, Yates and Bromwich JJ).

70 The value of a penalty unit is fixed by s 4AA(1) of the Crimes Act 1914 (Cth). The value changed during the penalty period. Until 30 July 2015 it was $170 and thereafter $180. Thus, the maximum penalty for each contravention increased on 30 July 2015 from $1,700,000 to $1,800,000. I was informed that approximately 80% of the contraventions occurred in the latter period. It follows that the theoretical maximum for the sum total of the contraventions is in excess of $240 million.

The relevant principles

71 The public interest in giving effect in appropriate cases to consent orders in civil penalty matters was affirmed by the High Court in Commonwealth v Director, Fair Work Building Industry Inspectorate (2015) 258 CLR 482 (Agreed Penalties Case). The imposition of a civil penalty serves to promote predictable outcomes, encouraging corporations to acknowledge their contraventions, thereby avoiding lengthy and complex litigation, freeing the Court to deal with other matters and the regulator to turn its attention to other areas of investigation: Agreed Penalties Case at [46]. Thus,

Subject to the court being sufficiently persuaded of the accuracy of the parties’ agreement as to facts and consequences, and that the penalty which the parties propose is an appropriate remedy in the circumstances thus revealed, it is consistent with principle and … highly desirable in practice for the court to accept the parties’ proposal and therefore impose the proposed penalty. To do so is no different in principle or practice from approving an infant’s compromise, a custody or property compromise, a group proceeding settlement or a scheme of arrangement.

Agreed Penalties Case at [58].

72 Nevertheless, the Court is not bound by the figure agreed upon by the parties: Agreed Penalties Case at [48]–[49]. As the Full Court recently emphasised in Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission (2021) 284 FCR 24 (Wigney, Beach and O’Bryan JJ) (Volkswagen), the above public policy considerations cannot override the statutory directive to the Court to impose a penalty it considers to be appropriate in the circumstances. Whether or not the agreed penalty is appropriate depends on whether it is within the permissible range within which no particular figure can necessarily be said to be more appropriate than another: Volkswagen at [127].

73 Civil penalties, like sentences for criminal offences, are determined by a process of “instinctive synthesis”, that is, by taking into account all relevant factors and arriving at a result which takes “due account” of them: Wong v The Queen (2001) 207 CLR 584 at [75] (Gaudron, Gummow and Hayne JJ); Makarian v The Queen (2005) 228 CLR 357 at [37] (Gleeson CJ, Gummow, Hayne and Callinan JJ); Pattinson v Australian Building and Construction Commissioner (2020) 282 FCR 580 (Pattinson) at [112] (Allsop CJ, White and Wigney JJ).

74 In determining the appropriate penalty for the contraventions in the present case, the Court is required to take into account all relevant matters including:

(a) the nature and extent of the act or omission and of any loss or damage suffered as a result of the act or omission; and

(b) the circumstances in which the act or omission took place; and

(c) whether the person has previously been found by the Court in proceedings under this Subdivision to have engaged in any similar conduct.

See ASIC Act, s 12GBA(2).

75 A convenient summary of the relevant matters appears in Australian Securities and Investments Commission v Westpac Banking Corporation [2019] FCA 2147 at [256]–[260] (Wigney J). The following two paragraphs are taken from that summary. To the extent that they are relevant to this case, they were addressed by the parties in their joint submissions.

76 Other matters relevant to the objective seriousness of the contravention include whether the conduct was deliberate, covert or reckless rather than negligent or careless; whether the contravention was isolated, systematic, or prolonged; where the contravenor is a body corporate, the extent to which senior officers of the company were involved or responsible; the existence or otherwise of compliance systems and a culture of compliance; the impact or consequences of the contravention on the market or innocent third parties; and the extent of any profit or benefit derived from the contravention.

77 In the case of a corporate contravenor, other relevant matters generally include the size and financial position of the company; whether the company has been found to have engaged in similar conduct in the past; any improvements to compliance systems since the contravention; whether the company (through its senior officers) has demonstrated contrition and remorse; whether the company had disgorged any profit or benefit received as a result of the contravention, or made reparation; whether the company has cooperated with and assisted the relevant regulatory authority in the investigation and prosecution of the contravention; and whether the company has suffered any extra-curial punishment or detriment arising from the finding that it had contravened the law.

78 In weighing the relevant matters, however, it is important to bear in mind that the purpose of a civil penalty is primarily, if not wholly protective; it is to promote the public interest in compliance: Agreed Penalties Case at [55]. The object is “to attempt to put a price on contravention that is sufficiently high to deter repetition by the contravenor and by others who might be tempted to contravene …”: Trade Practices Commission v CSR Limited [1990] FCA 762; [1991] ATPR ¶41-076 at 52, 152; (French J). The penalty must be fixed with a view to ensuring that it is not regarded by the contravenor or others as an acceptable cost of doing business: Singtel Optus Pty Ltd v Australian Competition and Consumer Commission [2012] FCAFC 20; 287 ALR 249; [2012] ATPR ¶42–387 at [62], [68] (Keane CJ, Finn and Gilmour JJ). It follows that deterrence, both general and specific, is a primary consideration: Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640 at [64]–[65] (French CJ, Crennan, Bell and Keane JJ); at [72] (Gageler J).

79 That said and while the objects of a criminal sentence are broader, just as the punishment must fit the crime, a civil penalty must be proportionate to the particular contravention or contraventions: Pattinson esp. at [108] (Allsop CJ, White and Wigney JJ), that is to say the penalty must bear an appropriate relationship to the nature and severity of the contravention or contraventions.

80 It is neither appropriate nor permissible to treat multiple contraventions as one contravention for the purposes of determining the statutory limit: Australian Competition and Consumer Commission v Yazaki Corporation (2018) 262 FCR 243 (Yazaki) at [227] (Allsop CJ, Middleton and Robertson JJ). But in an appropriate case a single penalty may be imposed for multiple contraventions where that course is agreed or accepted by the parties as appropriate: ABCC v CFMEU at [149] (Dowsett, Greenwood and Wigney JJ). One such case is where there is an interrelationship between the legal and factual elements of a number of contraventions, it is necessary to take care to ensure that the contravenor is not penalised twice for what amounts to the same wrongdoing. This principle, originally developed in the context of the sentencing discretion, is commonly known as the “course of conduct” or “one transaction” principle. See, for example, Construction, Forestry, Mining and Energy Union v Cahill [2010] FCAFC 39; 269 ALR 1; 194 IR 461 (Cahill) at [39] (Middleton and Gordon JJ). The principle requires that in such a case consideration should be given to whether the contraventions arise out of the same course of conduct or the one transaction in order to determine whether it is appropriate that a “concurrent” or single penalty should be impose for the multiple contraventions: Yazaki at [234]. Even if the course of conduct principle is applicable, however, a judge is not obliged to apply the principle if the resulting penalty does not reflect the seriousness of the contraventions: Cahill at [39]; Yazaki at [235]. It may also be appropriate for the Court to fix a single penalty where the precise number of contraventions cannot be ascertained; where the number is so large that the fixing of separate penalties is not feasible; or where there is such a large number of relatively minor related contraventions such that the contraventions “are most sensibly considered compendiously”: ABCC v CFMEU at [149].

81 Finally, where multiple contraventions are imposed, the Court is required to aggregate the total sums and review the aggregate amount in order to consider whether it reflects what is “just and appropriate” and if not to adjust the penalties accordingly. This is known as the “totality principle” and was also developed in the context of criminal sentencing. See, for example, ABCC v CFMEU at [116]–[120], [140].

82 The joint submissions also referred to the so-called “parity principle”, which the parties asserted “contemplates consideration of the penalties imposed in analogous cases”. This principle is said to be directed to the objective of equal treatment in similar cases so as to meet the principle of equal justice. The parties cited the judgment of Murphy J in Australian Competition and Consumer Commission v Optus Mobile [2019] FCA 106 at [40] but there are earlier references, such as Australian Competition & Consumer Commission v Ithaca Ice Works Pty Ltd [2001] FCA 1716; (2002) ATPR ¶41–851 (Wilcox, Hill and Carr JJ) and Schneider Electric (Australia) Pty Ltd v Australian Competition and Consumer Commission [2003] FCAFC 2 at [10]–[11] (Sackville J). NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission (1996) 71 FCR 285 at 295 (NW Frozen Foods) is often cited in support of the principle. There, Burchett and Kiefel JJ observed that equality before the law is “a hallmark of justice” and, “other things being equal, corporations guilty of similar contraventions should incur similar penalties …”. But their Honours did not use the expression “the parity principle”.

83 In NW Frozen Foods also at 295 Burchett and Kiefel JJ were also quick to point out that “other things are rarely equal where contraventions of the Trade Practices Act are concerned”. Their Honours observed that in that case, “differing circumstances, size, market power and responsibility for the contraventions, as well as other factors, complicate any attempt to compare the penalties imposed on the appellant with those imposed on the other corporations”. The same can be said of the ASIC Act and the present case. Importantly, their Honours went on to counsel against another form of comparison.

Another form of comparison is not appropriate. The facts of the instant case should not be compared with a particular reported case in order to derive therefrom the amount of the penalty to be fixed. Cases are authorities for matters of principle; but the penalty found to be appropriate, as a matter of fact, in the circumstances of one case cannot dictate the appropriate penalty in the different circumstances of another case. The point was well made by Spender J in Trade Practices Commission v Annand and Thompson Pty Ltd (at 48,394) when he said:

“Each case must, of course, be viewed on its own facts and facts may be infinite in their variety.”

It follows, as his Honour also said, that “[t]he quantum of penalties imposed in other cases can seldom be of very much direct assistance”.

84 I accept, of course, that the Court should have regard to analogous cases for they may assist in determining the appropriate range for a contravention of the kind with which the instant case is concerned.

85 With the greatest respect, however, it is potentially confusing to describe this as the “parity principle”. In criminal sentencing, at least, parity is only relevant in sentencing co-offenders, that is, offenders charged with the same offence and extends to those engaged in the same criminal enterprise. It is described in the following way in the Sentencing Bench Book published by the Judicial Commission of NSW:

The parity principle is an aspect of the systemic objectives of consistency and equality before the law – the treatment of like cases alike, and different cases differently: Green v The Queen (2011) 244 CLR 462 at [28]. The avoidance of unjustifiable disparity between the sentences imposed upon offenders involved in the same criminal conduct or a common criminal enterprise is a matter that is “required or permitted to be taken into account by the court” under s 21A(1): Green v The Queen at [19]. The principle is applied at first instance and on appeal (see below). An assertion by an offender of unjustified disparity can be a separate ground of appeal: Green v The Queen at [32].

86 In Green v The Queen at [28]–[29] French CJ, Crennan and Kiefel JJ explained the principle:

“Equal justice” embodies the norm expressed in the term “equality before the law” … It applies to the interpretation of statutes and thereby to the exercise of statutory powers. It requires, so far as the law permits, that like cases be treated alike. Equal justice according to law also requires, where the law permits, differential treatment of persons according to differences between them relevant to the scope, purpose and subject matter of the law. As Gaudron, Gummow and Hayne JJ said in Wong v The Queen:

“Equal justice requires identity of outcome in cases that are relevantly identical. It requires different outcomes in cases that are different in some relevant respect.” (emphasis in original)

Consistency in the punishment of offences against the criminal law is “a reflection of the notion of equal justice” and “is a fundamental element in any rational and fair system of criminal justice”. It finds expression in the “parity principle” which requires that like offenders should be treated in a like manner. As with the norm of “equal justice”, which is its foundation, the parity principle allows for different sentences to be imposed upon like offenders to reflect different degrees of culpability and/or different circumstances.

…

The consistency required by the parity principle is focussed on the particular case. It applies to the punishment of “co-offenders”, albeit the limits of that term have not been defined with precision.

(Emphasis added.)

Applying the principles

87 I now turn to the application of the principles in the present case.

The nature and extent of the contravening conduct

88 The details are set out in the statement of agreed facts and admissions and are summarised above. There is no need to repeat them. It suffices to say this.

89 The conduct the subject of the contraventions involved asserting a right to charge fees for unsolicited financial products. While the ASIC Act does not outlaw the supply of unsolicited products or services, it prohibits the supplier from asserting a right to payment and relieves the consumer of any obligation to pay for them. In oral argument ASIC emphasised this feature of the legislation. He characterised the making of the sale as “essential background”, “intimately connected” to the contravention, emphasising that the Act penalises the assertion of the right rather than the unsolicited supply. In determining an appropriate penalty “through the prism of the object of deterrence”, however, it is a significant matter that the products were unsolicited and that none of the affected customers consented to receiving the insurance cover: Australian Securities and Investments Commission v BT Funds Management Limited [2021] FCA 844 at [48] (Wheelahan J).

90 In any event, it is common ground that it is a serious matter for a financial institution to assert to its customers that it has a right to payment for services rendered when there is no such right. As the parties submitted, customers generally rely on their bank to provide accurate information. Indeed, they are entitled to expect nothing less. That is particularly so, as the parties also submitted, where the matters to which the services or products relate are complex, subject to statutory regulation, and over which the bank has control. Fees payable to a bank or its subsidiaries is a prime example. The customer is in a vulnerable position. While the relationship between banker and customer is a contractual one, “it is founded on trust and good faith in a commercial sense” and “[r]eliance by customers on the integrity and good faith of their bank is at the heart of social and commercial life in this country”: Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited (No 3) [2020] FCA 1421 at [13] (Allsop CJ). Westpac’s conduct in this case involved a breach of trust. For this reason alone it is serious.

91 ASIC does not allege that Westpac’s admitted contraventions were deliberate or reckless. And the parties agreed that it was not systemic. Nevertheless, the conduct was not isolated. And it occurred over a prolonged period.

The nature and extent of the loss or damage suffered

92 These matters, too, are set out above (at [1]–[60]). In summary, the affected customers paid a total of $10,999.49 in premiums for the CCI Policies. Each of them had sought private credit from Westpac and would only have been charged a premium if he or she had used the credit and failed to pay off the entire balance of debt at the end of the monthly payment cycle. Fourteen of the 141 were not charged a premium. Some were charged miniscule amounts. Many were charged less than $100. Only two was charged more than $500. The highest figure was $2,115.30. There was no evidence about the financial circumstances of the affected customers. But the parties agreed and I accept that, while each of those affected customers who were charged paid a modest amount in premiums, the amount in any particular case may well have been a significant amount to the customer concerned.

93 Each of the policies was cancelled following the making of a complaint and, where premiums had been paid (in 127 of the 141 cases) premiums were refunded shortly thereafter.

94 As the parties submitted, however, while “the smallness of the premium may contain the extent of harm which may be caused [to] any particular customer in any particular month”, “the prohibited demand for payment of a small sum from many potential customers is still serious”. As they pointed out, the very fact that the fee was small, increased the risk that the customers might not notice or pay attention to the demand for payment or might not trouble themselves to complain about or inquire into it. Further, the CCI Policies related to lines of credit which would ordinarily operate indefinitely and over an indefinite period the payments required of each customer could be substantial. As the parties put it, the wrongful demand for payment exposed each of the affected customers to the risk of such a loss, contained only by each customer’s willingness to pursue a complaint.

The circumstances in which the contraventions took place

95 These circumstances are also described above. They include aspects of Westpac’s sales practices, staff training and internal review in the years leading up to the penalty period and regulatory action by ASIC in 2010 and 2011 directed to the incidence of unsolicited supply of CCI policies by banks.

Previous findings by the Court of findings similar conduct

96 It will be recalled that one of the mandatory considerations mentioned in s 12GBA(2) is whether the contravenor has previously been found by the Court in proceedings under Subdiv G to have engaged in any similar conduct.

97 Westpac has not previously been found by the Court to have contravened s 12DM(1). But on two recent occasions it has been found by the Court in proceedings under Subdiv D to have engaged in similar conduct.

98 The first was in 2018 when Beach J ordered Westpac to pay a pecuniary penalty of $3.3 million for three contraventions of s 12CC of the Corporations Act (as then in force) relating to manipulative trading in the bank bill market: Australian Securities and Investments Commission v Westpac Banking Corporation (No 3) [2018] FCA 1701; 131 ACSR 585 (Beach J). While the conduct in that case was different in nature from the conduct in the present case, as the parties acknowledged it was similar in the sense that it also contravened a provision of the Act enacted for the purpose of consumer protection. It was also similar in that it involved conduct in which the bank took advantage of consumers, although the conduct in that case was much more serious in that, unlike the present case, it was deliberate, premeditated, and engaged in with the intention of achieving a proscribed outcome.

99 In 2021, in BT Funds Management, Wheelahan J ordered two wholly owned subsidiaries of Westpac to pay pecuniary penalties of $3 million ($1.5 million each) for falsely representing that adviser fees were not being charged to clients and therefore contravening s 12DB(1)(g) of the ASIC Act. This conduct was similar to the conduct in the present case in that both involved the provision of inaccurate information to many customers about the payment of monthly sums, in that case fees, in this case premiums.

Course of conduct

100 The parties submitted that this is an appropriate case for the application of the course of conduct principle. They point to the fact that the Welcome Letters for each of the two types of CCI Policy were in a standard form and that the standard form for each type of CCI Policy was substantially the same as the other. They also cited Australian Securities and Investments Commission v MLC Nominees Pty Ltd [2020] FCA 1306; 147 ACSR 266 (MLC Nominees) at [207]–[208] in which, despite ASIC’s submission to the contrary, Yates J held that a contravenor should be penalised on this basis. MLC Nominees was in a case involving 220,000 contraventions of s 12DB(1)(g) and (i) (making false or misleading representations with respect to the price of financial services and making false or misleading representations concerning the existence of a right). In holding that it was appropriate to penalise the company under the course of conduct principle, his Honour noted that letters, “welcome kits” and annual statements sent to “no-adviser” fund members, though personalised to the member’s individual account, were otherwise standard form documents and were sent to the members in standardised circumstances.

101 I accept the parties’ submission. I have no doubt that this is a proper case for the application of the principle. I would have come to this conclusion even if my attention had not been drawn to the decision in MLC Nominees. In the present case the legal and factual elements of Westpac’s conduct are so closely interrelated as to make it applicable. Were it not applied, Westpac would be penalised over and over again for what is essentially the same wrongdoing. As the underlying conduct is the same with respect to the two types of CCI Policy, I conclude that there is one course of conduct, not two.

Responsibility of senior officers

102 There was no suggestion that senior management knew of the 141 contraventions. Nor, for that matter, was there any suggestion that senior management participated in, or authorised, them.

103 During the penalty period, however, certain members of Westpac’s senior management, including the Chief Executive of Australian Financial Services, were aware that most of the complaints from customers for whom a CCI Policy had been arranged were consent related. They also knew that Westpac had not implemented ASIC’s recommendation (in Report 256) to obtain adequate evidence that a consumer has consented to purchase CCI by taking up ASIC’s suggestion, in the case of branch sales, that the signature of the customer consenting to the purchase be obtained. Furthermore, in the case of telephone sales, they knew that they did not have a policy which required recordings of a call in which customers were clearly asked whether they consented to the purchase to be retained for more than 45 days.

104 As the parties submitted, it may therefore be inferred that members of Westpac’s senior management were aware of the potential for improvement in obtaining customer consent to acquire CCI Policies.

Size and resources of Westpac

105 This is an important consideration as the size and resources of the corporate contravenor affects the amount necessary to operate as an effective deterrent. The larger the company and its resources, the greater the penalty required. See Westpac at [260]. In that case, Wigney J observed at [286]:

Westpac is undoubtedly a very large company. Its profits in the years preceding the contravening conduct exceeded $6 billion. Westpac’s size and financial position suggests that the objective of deterrence may require the imposition of higher penalties than would be required for smaller and less well-resourced companies.

106 The agreed facts in the present case show that Westpac is still a very large company making substantial profits. They reveal that Westpac had a market capitalisation as at 30 September 2020 of $61 billion, with $912 billion of total assets. In the 2019–2020 financial year, Westpac reported a net profit after tax of $2,290 million and its net profit before operating expenses and impairment charges was $7,444 million. From 1 October 2015 (FY 2015-2016) to 30 September 2020 (FY 2019-2020) (the most recent available published information), the statutory profit of Westpac was reported as:

Financial year | Reported net profit after tax |

FY2016 | $7,445 million |

FY2017 | $7,990 million |

FY2018 | $8,095 million |

FY2019 | $6,784 million |

FY2020 | $2,290 million |

Compliance systems and culture

107 Westpac trained branch and call centre staff throughout the penalty period and, as part of that training instructed the banker selling a CCI Policy to obtain the customer’s consent to discuss CCI; to obtain the customer’s consent to purchase a CCI Policy; and to inform the customer that CCI was optional.

108 From 2012 until March 2017 Westpac had processes in place to obtain evidence of customer consent to the purchase of CCI but they were inadequate. Westpac’s internal review, conducted in the wake of the ASIC review and the publication of Report 256 revealed their weaknesses, and made a number of recommendations designed to address them. Those recommendations, made in early June 2014, included the development of controls to evidence customer consent, including a consent document to be signed by both banker and customer. But it took nearly three years before that system was put in place.

109 Thus, Westpac did not ignore ASIC’s recommendation as to obtaining evidence of customer consent in Report 256 but ASIC’s suggestions were not fully implemented until more than five years after Report 256 was published.

Modifications to the compliance systems

110 In March 2017, the month following the end of the penalty period, Westpac implemented ASIC’s recommendation for the development of a consent document to be signed by both the banker and the customer.

The extent to which Westpac profited from its conduct and has otherwise made reparation

111 The affected customers were charged premiums for the CCI Policies and received insurance cover in return but none of them claimed on the relevant policy. It follows that the company which received the premiums derived a profit. That company was not Westpac but the two Westpac insurance companies. For this reason any profit Westpac might have derived from its conduct would be indirect. In any case there is no evidence that Westpac did profit. In any case, reparations were made by the refund of the premiums.

Contrition

112 It is an agreed fact that Westpac deeply regrets the impact of its conduct on the affected customers and apologises to the affected customers for their experiences. While it might be thought that an expression of remorse in an affidavit from a senior executive might be more powerful, there is no reason why I should not accept the agreed fact and I do.

Cooperation with the regulator

113 During its investigation into Westpac’s conduct before the proceeding was instituted, ASIC issued a number of compulsory notices to Westpac. ASIC and Westpac spent significant time meeting and liaising to determine why documents, data and recordings could not be produced and to identify potential repositories of documents.

114 The parties agreed on liability and penalty after the institution of the proceeding but before the formal exchange of evidence. I accept the parties’ submission that this circumstance is a mitigating factor and is reflected in the amount of the agreed penalty. It was common ground that the admission of liability was made at the earliest reasonable opportunity, after ASIC had refined its case. Westpac’s cooperation with the regulator and its early admission of liability in particular have significant utilitarian value. As the Full Court remarked in ABCC v CFMEU at [163]:

From a public policy perspective, it is important to encourage such cooperation by reflecting it in the penalties imposed. It also shows a willingness on the part of the [contravenor] to accept responsibility for its actions and to facilitate the course of justice. The fact that the proceeding was not defended saved the community the expense of a potentially lengthy contested hearing.

Comparable cases

115 No civil penalties have previously been ordered for a contravention of s 12DM. The parties drew the Court’s attention, however, to two cases under the equivalent provisions of the TPA and the ACL. The first was Australian Competition and Consumer Commission v Adepto Publications Pty Ltd [2013] FCA 247 (Adepto) (Cowdroy J), the second Australian Competition and Consumer Commission v Artorios Ink Co Pty Ltd (No 2) [2013] FCA 1292 (Mortimer J).

116 The second is of no use at all, since the respondent company was in liquidation at the time of the judgment. Pecuniary penalties were only imposed on the individual respondents who were accessories to the company’s contraventions.

117 The first relevantly involved a contravention of s 64 of the TPA. The contravening conduct consisted of the company sending business invoices and making other demands for payment for placing unsolicited advertisements in magazines published by the company when it had no reasonable cause to believe it had a right to payment. The Court ordered the corporate defendant to pay a penalty of $500,000 for what it inferred were “many hundreds’ of contraventions over a three and a half year period”. But the decision is of no value. Findings were also made of contraventions of other sections of the TPA (all essentially involving misleading or deceptive conduct and false representations) and the penalty, which was agreed, was for all the contraventions. In any event, the circumstances were very different. In contrast to the present case, the wrongdoing in Adepto was found to be “blatantly and knowingly deceitful” (it was repeatedly described as a “scam”), perpetrated by senior officers for personal gain and which, but for the intervention of the regulator, would probably have continued (at [52]). It involved swindling more than twice the number of consumers (312) ([55]) and there is no suggestion in the judgment that they were recompensed for their losses. While there was some cooperation with the regulator ([57]), agreement was only reached two years into the proceedings commencing and there was no evidence of contrition. On the other side of the ledger, the company had stopped trading before the judgment and had no assets (at [36]).

118 The parties also referred to three recent cases involving contraventions of other provisions of Pt 2 Div 2 of the ASIC Act. Two of them concerned the Commonwealth Bank. They were Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790 in which Beach J imposed a single penalty of $5 million for contraventions of ss 12DB(1)(e) and 12DB(1)(g) of the ASIC Act and Australian Securities and Investments Commission v Commonwealth Bank of Australia [2021] FCA 423 in which Lee J imposed a single penalty of $7 million for 12,119 contraventions of s 12DB(1)(g). In the former the conduct related to selling customers a package of benefits which were not ultimately provided. In the latter the conduct concerned overcharging interest in excess of $2.2 million to 2,269 bank customers. The third concerned two subsidiaries of Westpac. That was BT FundsManagement. In that case, two wholly owned subsidiaries of Westpac admitted to “at least” 487 contraventions of s 12DB(1)(g) and s 1041 of the Corporations Act (both concerned with misleading or deceptive conduct) involving customers who were incorrectly charged approximately $130,000. Wheelahan J imposed a penalty of $1.5 million on each of the defendants

119 The parties acknowledged that each of these cases turned on its own facts and were likely to be “of limited assistance to the Court” but submitted that they were capable of assisting in that they suggested that a single penalty of $1.5 million in the present case may be regarded by the Court as within the range of appropriate penalties.

Conclusion

120 I am acutely conscious of the need to impose a penalty that is sufficient to act as a deterrent both to Westpac and to other financial institutions. The contraventions were admittedly serious. While this is the first time Westpac has been found to have contravened s 12DM(1), it is not the first time it has been found to have contravened the consumer protection provisions of the Act. I was initially concerned about whether a penalty of $1.5 million could possibly operate as a deterrent for a large, profitable, asset-rich banking institution like Westpac. While deterrence is the primary consideration, however, it is not the only one.

121 For the following reasons Westpac’s conduct, though serious, does not warrant a penalty anywhere near the upper end of the scale.

122 First, the contraventions were not deliberate or reckless. And it was common ground that, although there was a lack of care, Westpac’s conduct did not amount to negligence. Second, the contraventions were not systemic. Throughout the penalty period staff were directed during training to ensure that customer consent was obtained. Although staff were incentivised to sell the products, they were also obliged to ensure that they complied with risk and other requirements and no direct commission was paid for the sale of CCI Polices. Third, in some cases the customers lost no money, in most cases the losses were small. Fourth, Westpac did not profit from the contraventions and, save for one customer who is 10 cents out of pocket, made full and prompt reparation. Fifth, Westpac has since modified its compliance systems, putting in place ASIC’s recommendations, albeit later than it should have. It is unclear why it took so long. Nevertheless, in view of the modifications, the risk of Westpac reoffending, so to speak, is substantially reduced. Five years have passed since the end of the penalty period. Sixth, Westpac admitted liability relatively early in the proceeding and cooperated with ASIC, a level of cooperation ASIC described as “very constructive”. Seventh, Westpac is contrite. Finally, I take heed of, and give weight to, the public policy considerations.

123 In all these circumstances, while minds might differ as to the appropriate penalty or penalties for the contraventions, I am persuaded that the agreed penalty is an appropriate one. The limited guidance offered by the authorities suggests that it is within the range; it certainly does not indicate otherwise. There is no reason to reduce the amount on account of the totality principle.

I certify that the preceding one hundred and twenty-three (123) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Katzmann. |

Associate: