FEDERAL COURT OF AUSTRALIA

Deputy Commissioner of Taxation v Williams [2022] FCA 263

ORDERS

QUD 78 OF 2022 | ||

BETWEEN: | DEPUTY COMMISSIONER OF TAXATION Applicant | |

AND: | SPENCER WILLIAMS First Respondent BRONWYN WILLIAMS Second Respondent REGISTRAR OF TITLES (QUEENSLAND) Third Respondent | |

order made by: | COLLIER J |

DATE OF ORDER: | 22 March 2022 |

1. The application for interlocutory relief be returnable instanter.

FREEZING AND ANCILLARY ORDERS:

2. Upon the Applicant giving the undertakings set out in Schedule A to each of the following annexures, freezing and ancillary orders be made:

(a) against the First Respondent in the form of Annexure A to these orders; and

(b) against the Second Respondent in the form of Annexure B to these orders.

3. Until 6.00pm on the date fixed for the next case management hearing of this matter or further order of the Court, the Third Respondent must not register any dealings which affect the property known as 44 Brittanic Crescent, Paradise Point, Queensland 4216, being Lot 70 on Registered Plan 222332 in the State of Queensland (Title Reference 17320088).

SERVICE:

4. Pursuant to rule 10.24 of the Federal Court Rules 2011 (Cth):

(i) personal service of the Application on the First and Second Respondents be dispensed with; and

(ii) the Applicant have leave to serve the Documents on the First and Second Respondents as follows:

A. by leaving a copy of the Documents at 44 Brittanic Crescent, Paradise Point, Queensland 4216;

B. by leaving a copy of the Documents at MKP Consulting & Co, Level 5, 219-223 Castlereagh St, Sydney NSW 2000;

C. by emailing the Documents to spencerpibworth@aol.com;

D. by emailing the Documents to spencerwilliams7@me.com.

5. In this order, "Documents" means:

(i) the originating application;

(ii) the interlocutory application;

(iii) the affidavit of Thomas Joseph Paino filed with the originating application and exhibit TJP-1;

(iv) the Applicant's outline of submissions in support of the interlocutory application;

(v) a transcript of the ex parte hearing, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court; and

(vi) a copy of these orders.

6. The time for service of the Documents is abridged and service is to be effected by 4.00pm on the third business day after the making of these orders.

7. A direction that, upon the undertaking of the Applicant to provide a paper copy of the exhibit to any supporting affidavit within three business days of a request by a Respondent to do so, service of any exhibit may be effected by:

(i) providing a copy on a USB drive; or

(ii) making it available for download by web link.

Other matters

8. The proceeding be listed for a case management hearing on a date to be fixed.

9. The costs of this application be reserved.

10. Liberty to apply on 24 hours’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

DEPUTY COMMISSIONER OF TAXATION Applicant | ||

AND: | First Respondent PENELOPE FARID Second Respondent RECORDER OF TITLES (TASMANIA) (and another named in the Schedule) Third Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The application for interlocutory relief be returnable instanter.

FREEZING AND ANCILLARY ORDERS:

2. Upon the Applicant giving the undertakings set out in Schedule A to each of the following annexures, freezing and ancillary orders be made:

(a) against the First Respondent in form of Annexure A to these orders.

(b) against the Second Respondent in the form of Annexure B to these orders.

3. Until 6.00pm on the date fixed for the next case management hearing of this matter, or further order of the Court, the Third Respondent must not register any dealings which affect the following properties:

(a) the property known as 5 Chessington Court, Sandy Bay, Tasmania 7005 being Lot 5 on Sealed Plan 62800 in the State of Tasmania (Volume 62800 Folio 5); and

(b) the property known as 3/479 Churchill Avenue, Sandy Bay, Tasmania 7005, being Lot 3 on Strata Plan 178426 in the State of Tasmania (Volume 178426 Folio 3).

4. Until 6.00pm on the date fixed for the next case management hearing of this matter or further order of the Court, the Fourth Respondent must not register any dealings which affect the property known as 1521/1 Lakeview Rise Noosa Heads, Queensland 4567, being Lot 3 on Strata Plan 178426 in the State of Queensland (Title Reference 51219278).

SERVICE:

5. Pursuant to rule 10.24 of the Federal Court Rules 2011 (Cth):

(a) Personal service of the Application on the First and Second Respondents be dispensed with; and

(b) The Applicant be granted leave to serve the Documents on the First and Second Respondent as follows:

(i) by leaving a copy of the Documents at 5 Chessington Court, Sandy Bay, Tasmania 7005;

(ii) by leaving a copy of the Documents at MKP Consulting & Co, Level 5, 219-223 Castlereagh St, Sydney NSW 2000;

(iii) by emailing the documents to yuliana.halim@mkpassociates.com.au;

(iv) by emailing the documents to simon@chessington.com.au.

6. In this order, "Documents" means:

(i) the originating application;

(ii) the interlocutory application;

(iii) the affidavit of Thomas Joseph Paino filed with the originating application and exhibit TJP-1;

(iv) the Applicant's outline of submissions in support of the interlocutory application;

(v) a transcript of the ex parte hearing, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court; and

(vi) a copy of these orders.

7. The time for service of the Documents is abridged and service is to be effected by 4.00pm on the third business day after the date of these orders.

8. A direction that, upon the undertaking of the Applicant to provide a paper copy of the exhibit to any supporting affidavit within three business days of a request by a Respondent to do so, service of any exhibit may be effected by:

(i) providing a copy on a USB drive; or

(ii) making it available for download by web link.

Other matters

9. The proceeding be listed for a case management hearing on a date to be fixed.

10. The costs of this application be reserved.

11. Liberty to apply on 24 hours’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Freezing Order

No. QUD 79 of 2022

Federal Court of Australia

District Registry: Queensland

Division: General

Deputy Commissioner of Taxation

Applicant

Simon Farid and others named in the schedule

Respondents

PENAL NOTICE

TO: Simon Farid IF YOU (BEING THE PERSON BOUND BY THIS ORDER): (A) REFUSE OR NEGLECT TO DO ANY ACT WITHIN THE TIME SPECIFIED IN THIS ORDER FOR THE DOING OF THE ACT; OR (B) DISOBEY THE ORDER BY DOING AN ACT WHICH THE ORDER REQUIRES YOU NOT TO DO, YOU WILL BE LIABLE TO IMPRISONMENT, SEQUESTRATION OF PROPERTY OR OTHER PUNISHMENT. ANY OTHER PERSON WHO KNOWS OF THIS ORDER AND DOES ANYTHING WHICH HELPS OR PERMITS YOU TO BREACH THE TERMS OF THIS ORDER MAY BE SIMILARLY PUNISHED. |

TO: Simon Farid

This is a 'freezing order' made against you on 22 March 2022 by Justice Collier at a hearing without notice to you after the Court was given the undertakings set out in Schedule A to this order and after the Court read the affidavits listed in Schedule B to this order.

THE COURT ORDERS:

INTRODUCTION

1.

(a) The application for this order is made returnable immediately.

(b) The time for service of the Documents is abridged and service is to be effected by 4.00pm on the third business day after the making of these orders.

2. Subject to the next paragraph, this order has effect up to and including a date to be fixed by order of the Court ("the Return Date"), at which time and date there will be a further hearing in respect of this order before a judge of this Court.

3. Anyone served with or notified of this order, including you, may apply to the Court at any time to vary or discharge this order or so much of it as affects the person served or notified.

4. In this order:

(a) 'applicant', if there is more than one applicant, includes all the applicants;

(b) 'you', where there is more than one of you, includes all of you and includes you if you are a corporation;

(c) 'third party' means a person other than you and the applicant;

(d) 'unencumbered value' means value free of mortgages, charges, liens or other encumbrances;

(e) 'Documents' means:

(i) the originating application;

(ii) the interlocutory application;

(iii) the affidavit of Thomas Joseph Paino filed with the originating application and exhibit TJP-1;

(iv) the applicant's outline of submissions in support of the interlocutory application;

(v) a transcript of the ex parte hearing, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court; and

(vi) orders made by the Court on return of the Applicant’s ex parte application.

5.

(a) If you are ordered to do something, you must do it by yourself or through directors, officers, partners, employees, agents or others acting on your behalf or on your instructions.

(b) If you are ordered not to do something, you must not do it yourself or through directors, officers, partners, employees, agents or others acting on your behalf or on your instructions or with your encouragement or in any other way.

FREEZING OF ASSETS

6.

(a) You must not remove from Australia or in any way dispose of, deal with or diminish the value of any of your assets in Australia ('Australian assets') up to the unencumbered value of $7,753,168 ('the Relevant Amount').

(b) If the unencumbered value of your Australian assets exceeds the Relevant Amount, you may remove any of those assets from Australia or dispose of or deal with them or diminish their value, so long as the total unencumbered value of your Australian assets still exceeds the Relevant Amount.

(c) If the unencumbered value of your Australian assets is less than the Relevant Amount, and you have assets outside Australia ('ex-Australian assets'):

(i) You must not dispose of, deal with or diminish the value of any of your Australian assets and ex-Australian assets up to the unencumbered value of your Australian and ex-Australian assets of the Relevant Amount; and

(ii) You may dispose of, deal with or diminish the value of any of your ex-Australian assets, so long as the unencumbered value of your Australian assets and ex-Australian assets still exceeds the Relevant Amount.

7. For the purposes of this order,

(a) your assets include:

(i) all your assets, whether or not they are in your name and whether they are solely or co-owned;

(ii) any asset which you have the power, directly or indirectly, to dispose of or deal with as if it were your own (you are to be regarded as having such power if a third party holds or controls the asset in accordance with your direct or indirect instructions); and

(iii) the following assets in particular (but your assets are not limited to these particular assets):

(A) the property known as 5 Chessington Court, Sandy Bay, Tasmania 7005 being Lot 5 on Sealed Plan 62800 in the State of Tasmania (Volume 62800 Folio 5) or, if it has been sold prior to the making of these orders, the net proceeds of the sale;

(B) the property known as 3/479 Churchill Avenue, Sandy Bay, Tasmania 7005, being Lot 3 on Strata Plan 178426 in the State of Tasmania (Volume 178426 Folio 3) or, if it has been sold prior to the making of these orders, the net proceeds of the sale;

(C) the property known as 1521/1 Lakeview Rise, Noosa Heads, Queensland 4567 being Lot 1521 on Survey Plan 290690 in the State of Queensland (Title Reference 51219278) or, if it has been sold prior to the making of these orders, the net proceeds of the sale;

(D) any money in the following bank accounts:

• Commonwealth Bank of Australia (CBA) account BSB 062-692 account number 36864667 in the name of Simon Farid;

• CBA account number 716722911184 in the name of Simon Karim Farid;

• CBA account BSB 062-692 account number 36864675 in the name of Simon Farid;

(E) the following motor vehicles:

• 2016 Aston Martin GT (VIN: SCFEJBAL0GGC20803);

• 2021 Land Rover Range Rover Sport (VIN: SALWA2AW3MA764150).

(b) the value of your assets is the value of the interest you have individually in your assets.

PROVISION OF INFORMATION

8. Subject to paragraph 9, you must:

(a) at or before the further hearing on the Return Date (or within such further time as the Court may allow) to the best of your ability inform the applicant in writing of all your assets in world-wide, giving their value, location and details (including any mortgages, charges or other encumbrances to which they are subject) and the extent of your interest in the assets;

(b) within 10 working days after being served with this order, swear and serve on the applicant an affidavit setting out the above information.

9.

(a) This paragraph (9) applies if you are not a corporation and you wish to object to complying with paragraph 8 on the grounds that some or all of the information required to be disclosed may tend to prove that you:

(i) have committed an offence against or arising under an Australian law or a law of a foreign country; or

(ii) are liable to a civil penalty.

(b) This paragraph (9) also applies if you are a corporation and all of the persons who are able to comply with paragraph 8 on your behalf and with whom you have been able to communicate, wish to object to your complying with paragraph 8 on the grounds that some or all of the information required to be disclosed may tend to prove that they respectively:

(i) (have committed an offence against or arising under an Australian law or a law of a foreign country; or

(ii) are liable to a civil penalty.

(c) You must:

(i) disclose so much of the information required to be disclosed to which no objection is taken; and

(ii) prepare an affidavit containing so much of the information required to be disclosed to which objection is taken, and deliver it to the Court in a sealed envelope; and

(iii) file and serve on each other party a separate affidavit setting out the basis of the objection.

EXCEPTIONS TO THIS ORDER

10. This order does not prohibit you from:

(a) paying up to $1,500 per week on your ordinary living expenses;

(b) paying up to $50,000 on your reasonable legal expenses;

(c) paying the Deputy Commissioner of Taxation;

(d) dealing with or disposing of any of your assets in the ordinary and proper course of your business, including paying business expenses bona fide and properly incurred; and

(e) in relation to matters not falling within (a), (b) (c) or (d), dealing with or disposing of any of your assets in discharging obligations bona fide and properly incurred under a contract entered into before this order was made, provided that before doing so you give the applicant, if possible, at least two working days written notice of the particulars of the obligation.

11. You and the applicant may agree in writing that the exceptions in the preceding paragraph are to be varied. In that case the applicant or you must as soon as practicable file with the Court and serve on the other a minute of a proposed consent order recording the variation signed by or on behalf of the applicant and you, and the Court may order that the exceptions are varied accordingly.

12.

(a) This order will cease to have effect if you:

(i) pay the sum of $7,753,168 into Court; or

(ii) pay that sum into a joint bank account in the name of your lawyer and the lawyer for the applicant as agreed in writing between them; or

(iii) provide security in that sum by a method agreed in writing with the applicant to be held subject to the order of the Court.

(b) Any such payment and any such security will not provide the applicant with any priority over your other creditors in the event of your insolvency.

(c) If this order ceases to have effect pursuant 12(a) above, you must as soon as practicable file with the Court and serve on the applicant notice of that fact.

COSTS

13. The costs of this application are reserved to the Court hearing the application on the Return Date.

PERSONS OTHER THAN THE APPLICANT AND RESPONDENT

14. Set off by banks

This order does not prevent any bank from exercising any right of set off it has in respect of any facility which it gave you before it was notified of this order.

15. Bank withdrawals by the respondent

No bank need inquire as to the application or proposed application of any money withdrawn by you if the withdrawal appears to be permitted by this order.

16. Persons outside Australia

(a) Except as provided in subparagraph (b) below, the terms of this order do not affect or concern anyone outside Australia.

(b) The terms of this order will affect the following persons outside Australia:

(i) you and your directors, officers, employees and agents (except banks and financial institutions);

(ii) any person (including a bank or financial institution) who:

(A) is subject to the jurisdiction of this Court; and

(B) has been given written notice of this order, or has actual knowledge of the substance of the order and of its requirements; and

(C) is able to prevent or impede acts or omissions outside Australia which constitute or assist in a disobedience of the terms of this order; and

(iii) any other person (including a bank of financial institution), only to the extent that this order is declared enforceable by or is enforced by a court in a country or state that has jurisdiction over that person or over any of that person's assets.

17. Assets located outside Australia

Nothing in this order shall, in respect of assets located outside Australia, prevent any third party from complying or acting in conformity with what it reasonably believes to be its bona fide and properly incurred legal obligations, whether contractual or pursuant to a court order or otherwise, under the law of the country or state in which those assets are situated or under the proper law of any contract between a third party and you, provided that in the case of any future order of a court of that country or state made on your or the third party's application, reasonable written notice of the making of the application is given to the applicant.

18. Notices under s 260-5 of Schedule 1 to the Taxation Administration Act 1953 (Cth)

Nothing in this order shall prevent any third party complying with the terms of a notice issued by the Commissioner of Taxation to the third party pursuant to section 260-5 of Schedule 1 to the Taxation Administration Act 1953 (Cth) in respect of any money which the third party may owe or may later owe to you.

SCHEDULE A

UNDERTAKINGS GIVEN TO THE COURT BY THE APPLICANT

(1) The applicant undertakes to submit to such order (if any) as the Court may consider to be just for the payment of compensation (to be assessed by the Court or as it may direct) to any person (whether or not a party) affected by the operation of the order.

(2) As soon as practicable, the applicant will file and serve upon the respondent copies of:

(a) this order;

(b) the application for this order for hearing on the return date;

(c) the following material in so far as it was relied on by the applicant at the hearing when the order was made:

(i) affidavits (or draft affidavits);

(ii) exhibits capable of being copied;

(iii) any written submission; and

(iv) any other document that was provided to the Court.

(d) a transcript, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court;

(e) the originating process, or, if none was filed, any draft originating process produced to the Court.

(3) As soon as practicable, the applicant will cause anyone notified of this order to be given a copy of it.

(4) The applicant will pay the reasonable costs of anyone other than the respondent which have been incurred as a result of this order, including the costs of finding out whether that person holds any of the respondent’s assets.

(5) If this order ceases to have effect the applicant will promptly take all reasonable steps to inform in writing anyone to who has been notified of this order, or who he has reasonable grounds for supposing may act upon this order, that it has ceased to have effect.

(6) The applicant will not, without leave of the Court, use any information obtained as a result of this order for the purpose of any civil or criminal proceedings, either in or outside Australia, other than this proceeding.

(7) The applicant will not, without leave of the Court, seek to enforce this order in any country outside Australia or seek in any country outside Australia an order of a similar nature or an order conferring a charge or other security against the respondent or the respondent’s assets.

SCHEDULE B

AFFIDAVITS RELIED ON

Name of deponent | Date affidavit made | |

(1) | Thomas Joseph Paino | 21 March 2022 |

(2) |

|

|

(3) |

|

|

NAME AND ADDRESS OF APPLICANT'S LAWYERS

The applicant's lawyers are: K&L Gates

Level 25 South Tower, 525 Collins Street, Melbourne VIC 3000,

Tel: +61 3 9205 2000 (during office hours)

Tel: +61 418 351 985 (after office hours)

Fax: +61 3 9205 2055

Email: Andrew.Chambers@klgates.com

Ref: TTRO.AJC.7390795.00132

Annexure B

Freezing Order

No. QUD 79 of 2022

Federal Court of Australia

District Registry: Queensland

Division: General

Deputy Commissioner of Taxation

Applicant

Simon Farid and others named in the schedule

Respondents

PENAL NOTICE

TO: Penelope Jane Farid IF YOU (BEING THE PERSON BOUND BY THIS ORDER): (A) REFUSE OR NEGLECT TO DO ANY ACT WITHIN THE TIME SPECIFIED IN THIS ORDER FOR THE DOING OF THE ACT; OR (B) DISOBEY THE ORDER BY DOING AN ACT WHICH THE ORDER REQUIRES YOU NOT TO DO, YOU WILL BE LIABLE TO IMPRISONMENT, SEQUESTRATION OF PROPERTY OR OTHER PUNISHMENT. ANY OTHER PERSON WHO KNOWS OF THIS ORDER AND DOES ANYTHING WHICH HELPS OR PERMITS YOU TO BREACH THE TERMS OF THIS ORDER MAY BE SIMILARLY PUNISHED. |

TO: Penelope Jane Farid

This is a 'freezing order' made against you on 22 March 2022 by Justice Collier at a hearing without notice to you after the Court was given the undertakings set out in Schedule A to this order and after the Court read the affidavits listed in Schedule B to this order.

THE COURT ORDERS:

INTRODUCTION

1.

(a) The application for this order is made returnable immediately.

(b) The time for service of the Documents is abridged and service is to be effected by 4.00pm on the third business day after the making of these orders.

2. Subject to the next paragraph, this order has effect up to and including a date to be fixed by order of the Court ("the Return Date"), at which time and date there will be a further hearing in respect of this order before a judge of this Court.

3. Anyone served with or notified of this order, including you, may apply to the Court at any time to vary or discharge this order or so much of it as affects the person served or notified.

4. In this order:

(a) 'applicant', if there is more than one applicant, includes all the applicants;

(b) 'you', where there is more than one of you, includes all of you and includes you if you are a corporation;

(c) 'third party' means a person other than you and the applicant;

(d) 'unencumbered value' means value free of mortgages, charges, liens or other encumbrances;

(e) 'Property' means the property known as 3/479 Churchill Avenue, Sandy Bay, Tasmania 7005, being Lot 3 on Strata Plan 178426 in the State of Tasmania (Volume 178426 Folio 3);

(f) 'Documents' means:

(i) the originating application;

(ii) the interlocutory application;

(iii) the affidavit of Thomas Joseph Paino filed with the originating application and exhibit TJP-1;

(iv) the applicant's outline of submissions in support of the interlocutory application;

(v) a transcript of the ex parte hearing, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court; and

(vi) orders made by the Court on the return of the Applicant’s ex parte application.

5.

(a) If you are ordered to do something, you must do it by yourself or through directors, officers, partners, employees, agents or others acting on your behalf or on your instructions.

(b) If you are ordered not to do something, you must not do it yourself or through directors, officers, partners, employees, agents or others acting on your behalf or on your instructions or with your encouragement or in any other way.

FREEZING OF ASSETS

6. You must not in any way dispose of, deal with or diminish the value of the Property (or if the Property has already been sold when these orders are made, you must not in any way dispose of, deal with, diminish the value of, or remove from Australia, the net proceeds of sale of the Property).

7.

(a) This order will cease to have effect if you:

(i) pay the sum of $7,753,168 into Court; or

(ii) pay that sum into a joint bank account in the name of your lawyer and the lawyer for the applicant as agreed in writing between them; or

(iii) provide security in that sum by a method agreed in writing with the applicant to be held subject to the order of the Court.

(b) Any such payment and any such security will not provide the applicant with any priority over your other creditors in the event of your insolvency.

(c) If this order ceases to have effect pursuant 7(a) above, you must as soon as practicable file with the Court and serve on the applicant notice of that fact.

COSTS

8. The costs of this application are reserved to the Court hearing the application on the Return Date.

PERSONS OTHER THAN THE APPLICANT AND RESPONDENT

9. Set off by banks

This order does not prevent any bank from exercising any right of set off it has in respect of any facility which it gave you before it was notified of this order.

10. Bank withdrawals by the respondent

No bank need inquire as to the application or proposed application of any money withdrawn by you if the withdrawal appears to be permitted by this order.

11. Notices under s 260-5 of Schedule 1 to the Taxation Administration Act 1953 (Cth)

Nothing in this order shall prevent any third party complying with the terms of a notice issued by the Commissioner of Taxation to the third party pursuant to section 260-5 of Schedule 1 to the Taxation Administration Act 1953 (Cth) in respect of any money which the third party may owe or may later owe to you.

SCHEDULE A

UNDERTAKINGS GIVEN TO THE COURT BY THE APPLICANT

(1) The applicant undertakes to submit to such order (if any) as the Court may consider to be just for the payment of compensation (to be assessed by the Court or as it may direct) to any person (whether or not a party) affected by the operation of the order.

(2) As soon as practicable, the applicant will file and serve upon the respondent copies of:

(a) this order;

(b) the application for this order for hearing on the return date;

(c) the following material in so far as it was relied on by the applicant at the hearing when the order was made:

(i) affidavits (or draft affidavits);

(ii) exhibits capable of being copied;

(iii) any written submission; and

(iv) any other document that was provided to the Court.

(d) a transcript, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court;

(e) the originating process, or, if none was filed, any draft originating process produced to the Court.

(3) As soon as practicable, the applicant will cause anyone notified of this order to be given a copy of it.

(4) The applicant will pay the reasonable costs of anyone other than the respondent which have been incurred as a result of this order, including the costs of finding out whether that person holds any of the respondent’s assets.

(5) If this order ceases to have effect the applicant will promptly take all reasonable steps to inform in writing anyone to who has been notified of this order, or who he has reasonable grounds for supposing may act upon this order, that it has ceased to have effect.

(6) The applicant will not, without leave of the Court, use any information obtained as a result of this order for the purpose of any civil or criminal proceedings, either in or outside Australia, other than this proceeding.

(7) The applicant will not, without leave of the Court, seek to enforce this order in any country outside Australia or seek in any country outside Australia an order of a similar nature or an order conferring a charge or other security against the respondent or the respondent’s assets.

SCHEDULE B

AFFIDAVITS RELIED ON

Name of deponent | Date affidavit made | |

(1) | Thomas Joseph Paino | 21 March 2022 |

(2) |

|

|

(3) |

|

|

NAME AND ADDRESS OF APPLICANT'S LAWYERS

The applicant's lawyers are: K&L Gates

Level 25 South Tower, 525 Collins Street, Melbourne VIC 3000,

Tel: +61 3 9205 2000 (during office hours)

Tel: +61 418 351 985 (after office hours)

Fax: +61 3 9205 2055

Email: Andrew.Chambers@klgates.com

Ref: TTRO.AJC.7390795.00132

Annexure A

Freezing Order

No. QUD 78 of 2022

Federal Court of Australia

District Registry: Queensland

Division: General

Deputy Commissioner of Taxation

Applicant

Spencer Williams and others named in the schedule

Respondents

PENAL NOTICE

TO: Spencer Williams IF YOU (BEING THE PERSON BOUND BY THIS ORDER): (A) REFUSE OR NEGLECT TO DO ANY ACT WITHIN THE TIME SPECIFIED IN THIS ORDER FOR THE DOING OF THE ACT; OR (B) DISOBEY THE ORDER BY DOING AN ACT WHICH THE ORDER REQUIRES YOU NOT TO DO, YOU WILL BE LIABLE TO IMPRISONMENT, SEQUESTRATION OF PROPERTY OR OTHER PUNISHMENT. ANY OTHER PERSON WHO KNOWS OF THIS ORDER AND DOES ANYTHING WHICH HELPS OR PERMITS YOU TO BREACH THE TERMS OF THIS ORDER MAY BE SIMILARLY PUNISHED. |

TO: Spencer Williams

This is a 'freezing order' made against you on 22 March 2022 by Justice Collier at a hearing without notice to you after the Court was given the undertakings set out in Schedule A to this order and after the Court read the affidavits listed in Schedule B to this order.

THE COURT ORDERS:

INTRODUCTION

1.

(a) The application for this order is made returnable immediately.

(b) The time for service of the Documents is abridged and service is to be effected by 4.00pm on the third business day after the making of these orders.

2. Subject to the next paragraph, this order has effect up to and including a date to be fixed by order of the Court ("the Return Date"), at which time and date there will be a further hearing in respect of this order before a judge of this Court.

3. Anyone served with or notified of this order, including you, may apply to the Court at any time to vary or discharge this order or so much of it as affects the person served or notified.

4. In this order:

(a) 'applicant', if there is more than one applicant, includes all the applicants;

(b) 'you', where there is more than one of you, includes all of you and includes you if you are a corporation;

(c) 'third party' means a person other than you and the applicant;

(d) 'unencumbered value' means value free of mortgages, charges, liens or other encumbrances;

(e) 'Documents' means:

(i) the originating application;

(ii) the interlocutory application;

(iii) the affidavit of Thomas Joseph Paino filed with the originating application and exhibit TJP-1;

(iv) the applicant's outline of submissions in support of the interlocutory application;

(v) a transcript of the ex parte hearing, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court; and

(vi) orders made by the Court on return of the Applicant’s ex parte application.

5.

(a) If you are ordered to do something, you must do it by yourself or through directors, officers, partners, employees, agents or others acting on your behalf or on your instructions.

(b) If you are ordered not to do something, you must not do it yourself or through directors, officers, partners, employees, agents or others acting on your behalf or on your instructions or with your encouragement or in any other way.

FREEZING OF ASSETS

6.

(a) You must not remove from Australia or in any way dispose of, deal with or diminish the value of any of your assets in Australia ('Australian assets') up to the unencumbered value of $3,907,935 ('the Relevant Amount').

(b) If the unencumbered value of your Australian assets exceeds the Relevant Amount, you may remove any of those assets from Australia or dispose of or deal with them or diminish their value, so long as the total unencumbered value of your Australian assets still exceeds the Relevant Amount.

(c) If the unencumbered value of your Australian assets is less than the Relevant Amount, and you have assets outside Australia ('ex-Australian assets'):

(i) You must not dispose of, deal with or diminish the value of any of your Australian assets and ex-Australian assets up to the unencumbered value of your Australian and ex-Australian assets of the Relevant Amount; and

(ii) You may dispose of, deal with or diminish the value of any of your ex-Australian assets, so long as the unencumbered value of your Australian assets and ex-Australian assets still exceeds the Relevant Amount.

7. For the purposes of this order,

(1) your assets include:

(i) all your assets, whether or not they are in your name and whether they are solely or co-owned;

(ii) any asset which you have the power, directly or indirectly, to dispose of or deal with as if it were your own (you are to be regarded as having such power if a third party holds or controls the asset in accordance with your direct or indirect instructions); and

(iii) the following assets in particular (but your assets are not limited to these particular assets):

(A) the property known as 44 Brittanic Crescent, Paradise Point, Queensland 4216, being Lot 70 on Registered Plan 222332 in the State of Queensland (Title Reference 17320088) or, if it has been sold prior to the making of these orders, the net proceeds of the sale;

(B) the following motor vehicles:

• 2020 Mercedes-Benz S450 Sedan (VIN: W1K2231612A018383);

• 2018 Landrover Range Rover Sport Wagon SDV6 (VIN: SALWA2AK1KA425459);

• 2016 Sea Doo GTX 155 Jetski (QLD Registration CF620Q);

• 2016 Sea Doo GTX 155 Jetski (QLD Registration CF621Q); and

• 2020 Brig Falcon Centre Console fibreglass boat (QLD Registration AAW18Q); and

(C) any money in Bendigo and Adelaide Bank account BSB 633-000 account number 167782168 in the name of S Williams.

(2) the value of your assets is the value of the interest you have individually in your assets.

PROVISION OF INFORMATION

8. Subject to paragraph 9, you must:

(a) at or before the further hearing on the Return Date (or within such further time as the Court may allow) to the best of your ability inform the applicant in writing of all your assets world-wide, giving their value, location and details (including any mortgages, charges or other encumbrances to which they are subject) and the extent of your interest in the assets;

(b) within 10 working days after being served with this order, swear and serve on the applicant an affidavit setting out the above information.

9.

(a) This paragraph (9) applies if you are not a corporation and you wish to object to complying with paragraph 8 on the grounds that some or all of the information required to be disclosed may tend to prove that you:

(i) have committed an offence against or arising under an Australian law or a law of a foreign country; or

(ii) are liable to a civil penalty.

(b) This paragraph (9) also applies if you are a corporation and all of the persons who are able to comply with paragraph 8 on your behalf and with whom you have been able to communicate, wish to object to your complying with paragraph 8 on the grounds that some or all of the information required to be disclosed may tend to prove that they respectively:

(i) (have committed an offence against or arising under an Australian law or a law of a foreign country; or

(ii) are liable to a civil penalty.

(c) You must:

(i) disclose so much of the information required to be disclosed to which no objection is taken; and

(ii) prepare an affidavit containing so much of the information required to be disclosed to which objection is taken, and deliver it to the Court in a sealed envelope; and

(iii) file and serve on each other party a separate affidavit setting out the basis of the objection.

EXCEPTIONS TO THIS ORDER

10. This order does not prohibit you from:

(a) paying up to $1,500 per week on your ordinary living expenses;

(b) paying up to $50,000 on your reasonable legal expenses;

(c) paying the Deputy Commissioner of Taxation;

(d) dealing with or disposing of any of your assets in the ordinary and proper course of your business, including paying business expenses bona fide and properly incurred; and

(e) in relation to matters not falling within (a), (b), (c) or (d), dealing with or disposing of any of your assets in discharging obligations bona fide and properly incurred under a contract entered into before this order was made, provided that before doing so you give the applicant, if possible, at least two working days written notice of the particulars of the obligation.

11. You and the applicant may agree in writing that the exceptions in the preceding paragraph are to be varied. In that case the applicant or you must as soon as practicable file with the Court and serve on the other a minute of a proposed consent order recording the variation signed by or on behalf of the applicant and you, and the Court may order that the exceptions are varied accordingly.

12.

(a) This order will cease to have effect if you:

(i) pay the sum of $3,907,935 into Court; or

(ii) pay that sum into a joint bank account in the name of your lawyer and the lawyer for the applicant as agreed in writing between them; or

(iii) provide security in that sum by a method agreed in writing with the applicant to be held subject to the order of the Court.

(b) Any such payment and any such security will not provide the applicant with any priority over your other creditors in the event of your insolvency.

(c) If this order ceases to have effect pursuant 12(a) above, you must as soon as practicable file with the Court and serve on the applicant notice of that fact.

COSTS

13. The costs of this application are reserved to the Court hearing the application on the Return Date.

PERSONS OTHER THAN THE APPLICANT AND RESPONDENT

14. Set off by banks

This order does not prevent any bank from exercising any right of set off it has in respect of any facility which it gave you before it was notified of this order.

15. Bank withdrawals by the respondent

No bank need inquire as to the application or proposed application of any money withdrawn by you if the withdrawal appears to be permitted by this order.

16. Persons outside Australia

(a) Except as provided in subparagraph (b) below, the terms of this order do not affect or concern anyone outside Australia.

(b) The terms of this order will affect the following persons outside Australia:

(i) you and your directors, officers, employees and agents (except banks and financial institutions);

(ii) any person (including a bank or financial institution) who:

(A) is subject to the jurisdiction of this Court; and

(B) has been given written notice of this order, or has actual knowledge of the substance of the order and of its requirements; and

(C) is able to prevent or impede acts or omissions outside Australia which constitute or assist in a disobedience of the terms of this order; and

(iii) any other person (including a bank of financial institution), only to the extent that this order is declared enforceable by or is enforced by a court in a country or state that has jurisdiction over that person or over any of that person's assets.

17. Assets located outside Australia

Nothing in this order shall, in respect of assets located outside Australia, prevent any third party from complying or acting in conformity with what it reasonably believes to be its bona fide and properly incurred legal obligations, whether contractual or pursuant to a court order or otherwise, under the law of the country or state in which those assets are situated or under the proper law of any contract between a third party and you, provided that in the case of any future order of a court of that country or state made on your or the third party's application, reasonable written notice of the making of the application is given to the applicant.

18. Notices under s 260-5 of Schedule 1 to the Taxation Administration Act 1953 (Cth)

Nothing in this order shall prevent any third party complying with the terms of a notice issued by the Commissioner of Taxation to the third party pursuant to section 260-5 of Schedule 1 to the Taxation Administration Act 1953 (Cth) in respect of any money which the third party may owe or may later owe to you.

SCHEDULE A

UNDERTAKINGS GIVEN TO THE COURT BY THE APPLICANT

(1) The applicant undertakes to submit to such order (if any) as the Court may consider to be just for the payment of compensation (to be assessed by the Court or as it may direct) to any person (whether or not a party) affected by the operation of the order.

(2) As soon as practicable, the applicant will file and serve upon the respondent copies of:

(a) this order;

(b) the application for this order for hearing on the return date;

(c) the following material in so far as it was relied on by the applicant at the hearing when the order was made:

(i) affidavits (or draft affidavits);

(ii) exhibits capable of being copied;

(iii) any written submission; and

(iv) any other document that was provided to the Court.

(d) a transcript, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court;

(e) the originating process, or, if none was filed, any draft originating process produced to the Court.

(3) As soon as practicable, the applicant will cause anyone notified of this order to be given a copy of it.

(4) The applicant will pay the reasonable costs of anyone other than the respondent which have been incurred as a result of this order, including the costs of finding out whether that person holds any of the respondent’s assets.

(5) If this order ceases to have effect the applicant will promptly take all reasonable steps to inform in writing anyone to who has been notified of this order, or who he has reasonable grounds for supposing may act upon this order, that it has ceased to have effect.

(6) The applicant will not, without leave of the Court, use any information obtained as a result of this order for the purpose of any civil or criminal proceedings, either in or outside Australia, other than this proceeding.

(7) The applicant will not, without leave of the Court, seek to enforce this order in any country outside Australia or seek in any country outside Australia an order of a similar nature or an order conferring a charge or other security against the respondent or the respondent’s assets.

SCHEDULE B

AFFIDAVITS RELIED ON

Name of deponent | Date affidavit made | |

(1) | Thomas Joseph Paino | 21 March 2022 |

(2) |

|

|

(3) |

|

|

NAME AND ADDRESS OF APPLICANT'S LAWYERS

The applicant's lawyers are: K&L Gates

Level 25 South Tower, 525 Collins Street, Melbourne VIC 3000,

Tel: +61 3 9205 2000 (during office hours)

Tel: +61 418 351 985 (after office hours)

Fax: +61 3 9205 2055

Email: Andrew.Chambers@klgates.com

Ref: TTRO.AJC.7390795.00131

Annexure B

Freezing Order

No. QUD 78 of 2022

Federal Court of Australia

District Registry: Queensland

Division: General

Deputy Commissioner of Taxation

Applicant

Spencer Williams and others named in the schedule

Respondents

PENAL NOTICE

TO: Bronwyn Williams IF YOU (BEING THE PERSON BOUND BY THIS ORDER): (A) REFUSE OR NEGLECT TO DO ANY ACT WITHIN THE TIME SPECIFIED IN THIS ORDER FOR THE DOING OF THE ACT; OR (B) DISOBEY THE ORDER BY DOING AN ACT WHICH THE ORDER REQUIRES YOU NOT TO DO, YOU WILL BE LIABLE TO IMPRISONMENT, SEQUESTRATION OF PROPERTY OR OTHER PUNISHMENT. ANY OTHER PERSON WHO KNOWS OF THIS ORDER AND DOES ANYTHING WHICH HELPS OR PERMITS YOU TO BREACH THE TERMS OF THIS ORDER MAY BE SIMILARLY PUNISHED. |

TO: Bronwyn Williams

This is a 'freezing order' made against you on 22 March 2022 by Justice Collier at a hearing without notice to you after the Court was given the undertakings set out in Schedule A to this order and after the Court read the affidavits listed in Schedule B to this order.

THE COURT ORDERS:

INTRODUCTION

1.

(a) The application for this order is made returnable immediately.

(b) The time for service of the Documents is abridged and service is to be effected by 4.00pm on the third business day after the making of these orders.

2. Subject to the next paragraph, this order has effect up to and including a date to be fixed by order of the Court ("the Return Date"), at which time and date there will be a further hearing in respect of this order before a judge of this Court.

3. Anyone served with or notified of this order, including you, may apply to the Court at any time to vary or discharge this order or so much of it as affects the person served or notified.

4. In this order:

(a) 'applicant', if there is more than one applicant, includes all the applicants;

(b) 'you', where there is more than one of you, includes all of you and includes you if you are a corporation;

(c) 'third party' means a person other than you and the applicant;

(d) 'unencumbered value' means value free of mortgages, charges, liens or other encumbrances;

(e) 'Property' means the property known as 44 Brittanic Crescent, Paradise Point, Queensland 4216, being Lot 70 on Registered Plan 222332 in the State of Queensland (Title Reference 17320088);

(f) 'Documents' means:

(i) the originating application;

(ii) the interlocutory application;

(iii) the affidavit of Thomas Joseph Paino filed with the originating application and exhibit TJP-1;

(iv) the applicant's outline of submissions in support of the interlocutory application;

(v) a transcript of the ex parte hearing, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court; and

(vi) orders made by the Court on the return of the Applicant’s ex parte application.

5.

(a) If you are ordered to do something, you must do it by yourself or through directors, officers, partners, employees, agents or others acting on your behalf or on your instructions.

(b) If you are ordered not to do something, you must not do it yourself or through directors, officers, partners, employees, agents or others acting on your behalf or on your instructions or with your encouragement or in any other way.

FREEZING OF ASSETS

6. You must not in any way dispose of, deal with or diminish the value of the Property (or if the Property has already been sold when these orders are made, you must not in any way dispose of, deal with, diminish the value of, or remove from Australia, the net proceeds of sale of the Property).

7.

(a) This order will cease to have effect if you:

(i) pay the sum of $3,907,935 into Court; or

(ii) pay that sum into a joint bank account in the name of your lawyer and the lawyer for the applicant as agreed in writing between them; or

(iii) provide security in that sum by a method agreed in writing with the applicant to be held subject to the order of the Court.

(b) Any such payment and any such security will not provide the applicant with any priority over your other creditors in the event of your insolvency.

(c) If this order ceases to have effect pursuant 7(a) above, you must as soon as practicable file with the Court and serve on the applicant notice of that fact.

COSTS

8. The costs of this application are reserved to the Court hearing the application on the Return Date.

PERSONS OTHER THAN THE APPLICANT AND RESPONDENT

9. Set off by banks

This order does not prevent any bank from exercising any right of set off it has in respect of any facility which it gave you before it was notified of this order.

10. Bank withdrawals by the respondent

No bank need inquire as to the application or proposed application of any money withdrawn by you if the withdrawal appears to be permitted by this order.

11. Notices under s 260-5 of Schedule 1 to the Taxation Administration Act 1953 (Cth)

Nothing in this order shall prevent any third party complying with the terms of a notice issued by the Commissioner of Taxation to the third party pursuant to section 260-5 of Schedule 1 to the Taxation Administration Act 1953 (Cth) in respect of any money which the third party may owe or may later owe to you.

SCHEDULE A

UNDERTAKINGS GIVEN TO THE COURT BY THE APPLICANT

(1) The applicant undertakes to submit to such order (if any) as the Court may consider to be just for the payment of compensation (to be assessed by the Court or as it may direct) to any person (whether or not a party) affected by the operation of the order.

(2) As soon as practicable, the applicant will file and serve upon the respondent copies of:

(a) this order;

(b) the application for this order for hearing on the return date;

(c) the following material in so far as it was relied on by the applicant at the hearing when the order was made:

(i) affidavits (or draft affidavits);

(ii) exhibits capable of being copied;

(iii) any written submission; and

(iv) any other document that was provided to the Court.

(d) a transcript, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court;

(e) the originating process, or, if none was filed, any draft originating process produced to the Court.

(3) As soon as practicable, the applicant will cause anyone notified of this order to be given a copy of it.

(4) The applicant will pay the reasonable costs of anyone other than the respondent which have been incurred as a result of this order, including the costs of finding out whether that person holds any of the respondent’s assets.

(5) If this order ceases to have effect the applicant will promptly take all reasonable steps to inform in writing anyone to who has been notified of this order, or who he has reasonable grounds for supposing may act upon this order, that it has ceased to have effect.

(6) The applicant will not, without leave of the Court, use any information obtained as a result of this order for the purpose of any civil or criminal proceedings, either in or outside Australia, other than this proceeding.

(7) The applicant will not, without leave of the Court, seek to enforce this order in any country outside Australia or seek in any country outside Australia an order of a similar nature or an order conferring a charge or other security against the respondent or the respondent’s assets.

SCHEDULE B

AFFIDAVITS RELIED ON

Name of deponent | Date affidavit made | |

(1) | Thomas Joseph Paino | 21 March 2022 |

(2) |

|

|

(3) |

|

|

NAME AND ADDRESS OF APPLICANT'S LAWYERS

The applicant's lawyers are: K&L Gates

Level 25 South Tower, 525 Collins Street, Melbourne VIC 3000,

Tel: +61 3 9205 2000 (during office hours)

Tel: +61 418 351 985 (after office hours)

Fax: +61 3 9205 2055

Email: Andrew.Chambers@klgates.com

Ref: TTRO.AJC.7390795.00131

REASONS FOR JUDGMENT

COLLIER J

1 These reasons for decision and orders concern two ex parte interlocutory applications brought by the Deputy Commissioner of Taxation (DCT) against different respondents. However the interlocutory applications raise similar legal issues, and involve certain common facts, suggesting that there is a business or other relationship between a number of the respondents. The interlocutory applications were heard together.

2 The relief sought by the DCT in each matter was as follows.

3 First, in QUD 79 of 2022 the DCT yesterday filed an originating application seeking relief against Mr Simon Farid, Ms Penelope Farid, the Recorder of Titles (Tasmania) and the Registrar of Titles (Queensland). In that originating application the DCT claimed as follows:

On the grounds stated in the statement of claim, accompanying affidavit or other document prescribed by the Rules, the Applicant claims:

1. Upon the following tax-related liabilities becoming due and payable, Judgment for the Applicant against the First Respondent in the sum of $7,753,168 plus any general interest charges thereon in respect of his liability for:

(a) income tax and shortfall interest charges for the year ended:

(i) 30 June 2017 as per notice of amended assessment issued 21 March 2022;

(ii) 30 June 2018 as per notice of amended assessment issued 21 March 2022;

(iii) 30 June 2019 as per notice of amended assessment issued 21 March 2022;

(iv) 30 June 2020 as per notice of amended assessment issued 21 March 2022;

(v) 30 June 2021 as per notice of amended assessment issued 21 March 2022;

(b) administrative penalties for the periods ended:

(i) 30 June 2017 as per notice of assessment issued 21 March 2022;

(ii) 30 June 2018 as per notice of assessment issued 21 March 2022;

(iii) 30 June 2019 as per notice of assessment issued 21 March 2022;

(iv) 30 June 2020 as per notice of assessment issued 21 March 2022;

(v) 30 June 2021 as per notice of assessment issued 21 March 2022; and

(c) any accrued general interest charges.

2. Costs.

3. Such further or other orders as the Court deems appropriate

Claim for interlocutory relief

The Applicant also claims interlocutory relief.

1. As set out in the Applicant's interlocutory process filed with this originating application.

4 By an interlocutory application also filed, ex parte, yesterday in QUD 79 of 2022, the DCT sought freezing and ancillary orders against the same respondents pursuant to Division 7.4 of the Federal Court Rules 2011 (Cth)(FCR) in the following terms:

1. An order that the application for interlocutory relief be returnable instanter.

Freezing and ancillary orders

2. Freezing and ancillary orders pursuant to Division 7.4 of the Federal Court Rules 2011 (Cth) (FCR) against the First Respondent in the terms specified in Annexure A to this application.

3. Freezing and ancillary orders against the Second Respondent pursuant to Division 7.4 of the FCR in the terms specified in Annexure B to this application.

4. An order that until the return date of the Applicant's application for freezing orders or further order of the Court:

(a) the Third Respondent must not register any dealings which affect the following properties:

(i) the property known as 5 Chessington Court, Sandy Bay, Tasmania 7005 being Lot 5 on Sealed Plan 62800 in the State of Tasmania (Volume 62800 Folio 5);

(ii) the property known as 3/479 Churchill Avenue, Sandy Bay, Tasmania 7005, being Lot 3 on Strata Plan 178426 in the State of Tasmania (Volume 178426 Folio 3);

(b) the Fourth Respondent must not register any dealings which affect the property known as 1521/1 Lakeview Rise Noosa Heads, Queensland 4567, being Lot 3 on Strata Plan 178426 in the State of Queensland (Title Reference 51219278).

Service

5. Pursuant to rule 10.24 of the FCR, orders that personal service of the Application on the First and Second Respondents be dispensed with and that the Applicant have leave to serve the Documents on the First and Second Respondents as follows:

(a) by leaving a copy of the Documents at 5 Chessington Court, Sandy Bay, TAS 7005;

(b) by leaving a copy of the Documents at MKP Consulting & Co, Level 5, 219-223 Castlereagh St, Sydney NSW 2000;

(c) by emailing the Documents to yuliana.halim@mkpassociates.com.au;

(d) by emailing the Documents to simon@chessington.com.au.

6. In this order, "Documents" means:

(a) the originating application;

(b) this interlocutory application;

(c) the affidavit of Thomas Joseph Paino filed with the originating application and exhibit TJP-1;

(d) the Applicant's outline of submissions in support of the interlocutory application;

(e) a transcript of the ex parte hearing, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court;

(f) orders made by the Court.

7. The time for service of the Documents is abridged and service is to be effected by 4.00pm on the third business day after the making of these orders.

8. A direction that, upon the undertaking of the Applicant to provide a paper copy of the exhibit to any supporting affidavit within three business days of a request by a Respondent to do so, service of any exhibit may be effected by:

(a) providing a copy on a USB drive; or

(b) making it available for download by web link.

Other

9. Costs of the interlocutory application be reserved.

10. Liberty to apply on 24 hours' notice.

11. Such further or other orders as the Court deems appropriate

5 Currently, in QUD 79 of 2022, it is only the ex parte interlocutory application which is before the Court.

6 Second, in QUD 78 of 2022 the DCT yesterday filed an originating application seeking relief against Mr Spencer Williams, Ms Bronwyn Williams, and the Registrar of Titles (Queensland). In that originating application the DCT claimed as follows:

1. Upon the following tax-related liabilities becoming due and payable, Judgment for the Applicant against the First Respondent in the sum of $3,907,935 plus any general interest charges thereon in respect of his liability for:

(a) income tax and shortfall interest charges for the year ended:

(i) 30 June 2017 as per notice of amended assessment issued 21 March 2022;

(ii) 30 June 2018 as per notice of amended assessment issued 21 March 2022;

(iii) 30 June 2019 as per notice of amended assessment issued 21 March 2022;

(iv) 30 June 2020 as per notice of amended assessment issued 21 March 2022;

(b) income tax for the year ended 30 June 2021 as per notice of assessment issued 21 March 2022;

(c) administrative penalties for the periods ended:

(i) 30 June 2017 as per notice of assessment issued 21 March 2022;

(ii) 30 June 2018 as per notice of assessment issued 21 March 2022;

(iii) 30 June 2019 as per notice of assessment issued 21 March 2022;

(iv) 30 June 2020 as per notice of assessment issued 21 March 2022; and

(d) any accrued general interest charges.

2. Costs.

3. Such further or other orders as the Court deems appropriate.

Claim for interlocutory relief

The Applicant also claims interlocutory relief.

1. As set out in the Applicant's interlocutory process filed with this originating application.

7 By an interlocutory application also filed, ex parte, yesterday in QUD 78 of 2022, the DCT sought freezing and ancillary orders against the same respondents pursuant to Division 7.4 of the FCRin the following terms:

Interlocutory orders sought

1. An order that the application for interlocutory relief be returnable instanter.

Freezing and ancillary orders

2. Freezing and ancillary orders pursuant to Division 7.4 of the Federal Court Rules 2011 (Cth) (FCR) against the First Respondent in the terms specified in Annexure A to this application.

3. Freezing and ancillary orders against the Second Respondent pursuant to Division 7.4 of the FCR in the terms specified in Annexure B to this application.

4. An order that until the return date of the Applicant's application for freezing orders or further order of the Court, the Third Respondent must not register any dealings which affect the property known as 44 Brittanic Crescent, Paradise Point, Queensland 4216, being Lot 70 on Registered Plan 222332 in the State of Queensland (Title Reference 17320088).

Service

5. Pursuant to rule 10.24 of the FCR, orders that personal service of the Application on the First and Second Respondents be dispensed with and that the Applicant have leave to serve the Documents on the First and Second Respondents as follows:

(a) by leaving a copy of the Documents at 44 Brittanic Crescent, Paradise Point, Queensland 4216;

(b) by leaving a copy of the Documents at MKP Consulting & Co, Level 5, 219-223 Castlereagh St, Sydney NSW 2000;

(c) by emailing the Documents to spencerpibworth@aol.com:

(d) by emailing the Documents to spencerwilliams7@me.com.

6. In this order, "Documents" means:

(a) the originating application;

(b) this interlocutory application;

(c) the affidavit of Thomas Joseph Paino filed with the originating application and exhibit TJP-1;

(d) the Applicant's outline of submissions in support of the interlocutory application;

(e) a transcript of the ex parte hearing, or, if none is available, a note, of any exclusively oral allegation of fact that was made and of any exclusively oral submission that was put, to the Court; and

(f) orders made by the Court.

7. The time for service of the Documents is abridged and service is to be effected by 4.00pm on the third business day after the making of these orders.

8. A direction that, upon the undertaking of the Applicant to provide a paper copy of the exhibit to any supporting affidavit within three business days of a request by a Respondent to do so, service of any exhibit may be effected by:

(a) providing a copy on a USB drive; or

(b) making it available for download by web link.

Other

9. Costs of the interlocutory application be reserved.

10. Liberty to apply on 24 hours' notice.

11. Such further or other orders as the Court deems appropriate

8 Currently, in QUD 78 of 2022 it is only the ex parte interlocutory application which is before the Court.

MATERIAL FACTUAL ALLEGATIONS BEFORE THE COURT

QUD 79 of 2022 Farid

9 Relevant factual material concerning Mr Farid was summarised in the affidavit of Mr Thomas Paino (the Technical Leader in the Lodge and Pay-Management-Resolutions, Service Delivery group at the Australian Taxation Office in Melbourne, sworn 21 March 2022 and filed in QUD 79 of 2022) and the submissions of the DCT.

10 Mr Farid migrated to Australia from the United Kingdom in 1995 and is an Australian resident for tax purposes. Mr Farid is not an Australian citizen. Ms Penelope Farid is Mr Farid’s spouse.

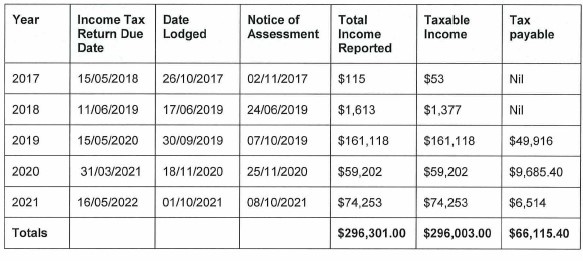

11 On the DCT’s case, Mr Farid has a history of poor compliance with income tax lodgement obligations. Mr Farid’s lodgement history for the income years 2017-21 is as follows:

12 The amounts declared by Mr Farid related to interest income, trust distributions over the 2020-2021 income years, and a large net capital gain in 2019. No salary or wages were declared.

13 On or about 13 May 2021, the DCT commenced a review of Mr Farid’s tax affairs. The review was conducted covertly given the DCT’s determination that there was a risk of Mr Farid dissipating assets were he put on notice of the review.

14 The DCT’s investigations revealed, in summary, that:

Significant unexplained deposits, which had not been disclosed in the assessable income of Mr Farid, had been made into Mr Farid’s bank accounts as follows:

2017 | 2018 | 2019 | 2020 | 2021 | Total | |

ANZ | $1,170,926 | $1,319,633 | $738,085 | Not applicable | Not applicable | |

CBA | Not applicable | Not applicable | $225,349 | $1,559,212 | $3,645,395 | |

Totals | $1,170,926 | $1,319,633 | $963,434 | $1,559,212 | $3,645,395 | $8,658,600 |

The unexplained deposits include large regular deposits from:

• Mr Spencer Williams;

• Brizo Group Pty Ltd; and

• Brizo Group Nominees Pty Ltd.

Mr Farid regularly used the unexplained deposits to support his and his family’s lifestyle;

Mr Farid has a history of receiving and transferring funds to bank accounts in foreign jurisdictions;

Mr Farid applied for an American Express Credit Card on 18 July 2017 in which application he stated that:

• Mr Farid was a Director of Chessington Nominees Pty Ltd;

• Mr Farid earned $900,000 per year before tax; and

• Mr Spencer Williams was a “business partner”.

There are four supplementary accounts attached to Mr Farid’s American Express account, namely:

• Mr Spencer Williams;

• Ms Bronwyn Williams;

• Ms Penelope Farid; and

• Mr Farid himself.

Mr Farid is the sole director, secretary and shareholder of Chessington Nominees Pty Ltd and Chessington Investments Pty Ltd;

Chessington Nominees Pty Ltd:

• was incorporated on 19 March 2015;

• has not lodged a tax return; and

• was likely the trustee of Chessington Trust ABN 35 523 653 955 (Chessington Trust).

Chessington Trust:

• was registered for income tax on 23 May 2015;

• had lodged tax returns for “consulting services” for the years 2015-16 and 2018-21.

Mr Farid was a Director of Heritage Fine Wines Pty Ltd between 26 March 2002 and 1 August 2004. Heritage Fine Wines Pty Ltd was placed into liquidation in May 2005.

Mr Farid was prohibited from performing any function in relation to regulated activities which correspond to investment businesses by the United Kingdom Financial Conduct Authority in 1996.

15 As a result of the review, the DCT determined that Mr Farid had significant undisclosed income and had engaged in tax evasion. On 21 March 2022, the DCT issued amended Notices of Assessment of taxable income and Notices of Assessment of shortfall penalty, for the income years 2017-21.

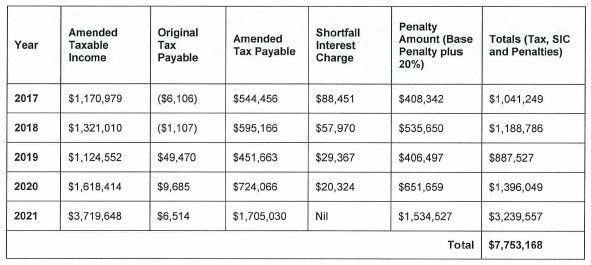

16 Mr Farid’s amended taxable income, administrative penalties and shortfall interest charge can be summarised as follows:

17 Assets allegedly owned by Mr Farid and Ms Farid, both individually and jointly, were identified by the DCT as follows:

Asset Type | Description | Interest | Encumbrances | Estimated Value | Document Page Reference |

Bank Account | CBA Name: Simon Farid BSB: 062692 Account: 36864667 | 100% | None | $63,712.53 (as at 18 January 2022) | Bank Statement: 406 INGOT Result: 680 |

CBA Name: Simon Karim Farid Account: 716722911184 | 100% | None | $1,000 (as at 20 January 2022) | INGOT Result: 681 | |

CBA Name: Simon Farid BSB: 062692 Account: 36864675 | 100% | None | $4,200,169.91 (as at 18 January 2022) | INGOT Result: 682 | |

Real Estate | 5 Chessington Court, Sandy Bay, Tasmania 7005 (Volume 62800 Folio 5) (the Chessington Tasmanian Property) | 100% | None | $1,180,000 | Title Search: 204 Equifax Property Summary: 683 |

3/479 Churchill Avenue, Sandy Bay, Tasmania 7005 (Volume 178426 Folio 3) (the Churchill Tasmanian Property) | 50% (joint tenants with Penelope Jane Farid) | None | $1,250,000 | Title Search: 684 Equifax Property Summary: 685 | |

1521/1 Lakeview Rise Noosa Heads, Queensland 4567 (Title Reference 51219278) (the Noosa Property) | 100% | None | $1,890,000 | Title Search: 686 Equifax Property Summary: 689 Transfer: 687 | |

Motor Vehicles | 2016 Aston Martin GT (Plate: AMV001) (VIN: SCFEJBAL0GGC20803) (Aston Martin) | 100% | PPSR Registration 201810220056225 (Secured Party: Metro Finance Pty Ltd ACN 600 674 093, Grantor: Chessington as trustee for the Chessington Trust) | $170,000 | Tasmanian Government Statement of Vehicles Operated Listing: 690 Motor Vehicle Registrations Listing: 691 PPSR Search: 699 |

2021 Land Rover Range Rover Sport (Plate: J65LI) (VIN: SALWA2AW3MA764150) (Range Rover) | 100% | None | $103,900 | Tasmanian Government Statement of Vehicles Operated Listing: 690 Motor Vehicle Registrations Listing: 691 PPSR Search: 695 |

18 The DCT identified that Mr Farid held the following directorships and shareholdings:

Company | Role |

Chessington Nominees Pty Ltd ACN 604 843 352 | Sole director and secretary (commenced 19 March 2015) Sole shareholder (100 ordinary shares @ $1.00 per share) |

Chessington Investments Pty Ltd ACN 604 843 343 | Sole director and secretary (commenced 19 March 2015) Sole shareholder (100 ordinary shares @ $1.00 per share) |

QUD 78 of 2022 Williams

19 Relevant factual material concerning Mr Williams was summarised in the affidavit of Mr Thomas Paino sworn 21 March 2022 and filed in QUD 78 of 2022, and the submissions of the DCT.

20 Mr Williams is a citizen of the United Kingdom having migrated to Australia in November 1997. The second respondent, Ms Bronwyn Williams, is his spouse. Mr and Ms Williams declared their taxable incomes in the 2017 to 2020 income years to be as follows:

Year | Taxpayer’s taxable income | Spouse’s taxable income |

2017 | $63,998 | $67,299 |

2018 | $59,715 | $0 |

2019 | $119,831 | $0 |

2020 | $119,079 | $0 |

TOTAL | $362,623.00 | $67,299 |

21 On the case of the DCT, Mr Williams did not declare any salary or wages income during the 2017 income year, rather only income resulting from partnership and trust distributions: $52,953 and $14,345 respectively.

22 Mr Williams was yet to lodge an income tax return for the 2021 income year. Nevertheless, the DCT submitted that, during the 2018, 2019 and 2020 income years, Mr Williams declared that he was employed as a sales consultant by the Trustee of the Australian Diamond Portfolio Trust. Mr Williams reported his income from this role in the amounts of $60,000, $120,000 and $120,000 in the 2018, 2019 and 2020 income years respectively.

23 On 24 May 2021 the DCT commenced a covert audit of Mr Williams’ tax affairs for the 2017 to 2020 income years. On 19 July 2021 the scope of the audit was widened to include the 2021 income year. This audit identified a number of large, unexplained deposits being made into three bank accounts belonging to Mr Williams that were not reflected in his income tax returns for the same period. These were as follows:

2017 | 2018 | 2019 | 2020 | 2021 | Total | |

ANZ VISA account ending 7166 | $965,000 | $870,000 | $225,000 | Not applicable | Not applicable | |

ANZ account ending 6253 | Not applicable | Not applicable | Not applicable | $175,000 | Not applicable | |

Bendigo Bank account ending 2168 | Not applicable | Not applicable | Not applicable | $339,267 | $3,280,000 | |

Totals | $965,000 | $870,000 | $225,000 | $514,267 | $3,280,000 | $5,854,267 |

24 In the context of this table, deposits occurring in the 2021 income year were included. Mr Williams is yet to file an income tax return for the current income year.

25 The audit also found that a number of these unexplained deposits were made with the description of a ‘Direct Credit’ from ‘Brizo Group Nomi’ (which appears to have been placed in voluntary liquidation), and uncovered large amounts of lifestyle expenditure. As a result of the audit, the DCT concluded that the deposits described in the table represented assessable income referable to Mr Williams in the 2017 to 2020 income years, that administrative penalties should be imposed, and that an increase of the base penalties of 20 per cent was appropriate in the circumstances.

26 Following the audit, the DCT yesterday issued the following assessments and amended assessments to Mr Williams:

Year | Amended Taxable Income (2017-2020) / Assessed Taxable Income (2021) | Original Tax Payable | Amended Tax Payable (2017 - 2020) / Tax Payable (2021) | Shortfall Interest Charge | Penalty Amount (Base Penalty plus 20%) | Totals |

2017 | $1,028,998 | Nil | $461,036 | $83,041 | $345,777 | $889,854 |

2018 | $870,000 | $10,954 | $399,032 | $38,795 | $359,129 | $796,956 |

2019 | $225,000 | $31,834 | $102,015 | $8,009 | $91,813 | $201,837 |

2020 | $514,267 | $31,556 | $237,964 | $5,690 | $214,167 | $457,821 |

2021 | $3,280,000 | N/A | $1,561,467 | Nil | Nil | $1,561,467 |

Total | $3,907,935 | |||||

RELEVANT LEGAL PRINCIPLES

27 Many of the legal principles arising in the present proceedings were recently summarised by me in Deputy Commissioner of Taxation v Raptis [2021] FCA 1192. It is convenient to repeat them:

46 The Court is empowered to make freezing orders by r 7.32 of the Federal Court Rules, which provides as follows:

7.32 Freezing order

(1) The Court may make an order (a freezing order), with or without notice to a respondent, for the purpose of preventing the frustration or inhibition of the Court’s process by seeking to meet a danger that a judgment or prospective judgment of the Court will be wholly or partly unsatisfied.

(2) A freezing order may be an order restraining a respondent from removing any assets located in or outside Australia or from disposing of, dealing with, or diminishing the value of, those assets.

Note: Without notice is defined in the Dictionary.

47 Orders ancillary to freezing orders are the subject of r 7.33, which provides:

7.33 Ancillary order

(1) The Court may make an order (an ancillary order) ancillary to a freezing order or prospective freezing order as the Court considers appropriate.

(2) Without limiting the generality of subrule (1), an ancillary order may be made for either or both of the following purposes:

(a) eliciting information relating to assets relevant to the freezing order or prospective freezing order;

(b) determining whether the freezing order should be made.

48 Rule 7.34 extends the powers of the Court in rules 7.32 and 7.33 to persons who are not otherwise parties to the substantive proceedings, namely third parties. For completeness I note that r 7.34 provides:

7.34 Order may be against person not a party to proceeding

The Court may make a freezing order or an ancillary order against a person even if the person is not a party in a proceeding in which substantive relief is sought against the respondent.

49 Rule 7.35 anticipates reezing orders against a judgment debtor, or prospective judgment debtor, or a third party. In particular r 7.35 (1)(b) states that:

(1) This rule applies if:

(a) ...

(b) an applicant has a good arguable case on an accrued or prospective cause of action that is justiciable in:

(i) the Court; or

(ii) ...

50 Further factors guiding the exercise of the Court’s discretion are set out in r 7.35 (4)-(6) as follows:

(4) The Court may make a freezing order or an ancillary order or both against a judgment debtor or prospective judgment debtor if the Court is satisfied, having regard to all the circumstances, that there is a danger that a judgment or prospective judgment will be wholly or partly unsatisfied because any of the following might occur:

(a) the judgment debtor, prospective judgment debtor or another person absconds;

(b) the assets of the judgment debtor, prospective judgment debtor or another person are:

(i) removed from Australia or from a place inside or outside Australia; or

(ii) disposed of, dealt with or diminished in value.

(5) The Court may make a freezing order or an ancillary order or both against a person other than a judgment debtor or prospective judgment debtor (a third party) if the Court is satisfied, having regard to all the circumstances, that:

(a) there is a danger that a judgment or prospective judgment will be wholly or partly unsatisfied because:

(i) the third party holds or is using, or has exercised or is exercising, a power of disposition over assets (including claims and expectancies) of the judgment debtor or prospective judgment debtor; or

(ii) the third party is in possession of, or in a position of control or influence concerning, assets (including claims and expectancies) of the judgment debtor or prospective judgment debtor; or

(b) a process in the Court is or may ultimately be available to the applicant as a result of a judgment or prospective judgment, under which process the third party may be obliged to disgorge assets or contribute toward satisfying the judgment or prospective judgment.

(6) Nothing in this rule affects the power of the Court to make a freezing order or ancillary order if the Court considers it is in the interests of justice to do so.

51 Having regard to these rules I note the following.