Federal Court of Australia

Brady v NULIS Nominees (Australia) Limited in its capacity as trustee of the MLC Super Fund (No 3) [2022] FCA 224

ORDERS

Applicant | ||

AND: | NULIS NOMINEES (AUSTRALIA) LIMITED (ACN 008 515 633) IN ITS CAPACITY AS TRUSTEE OF THE MLC SUPER FUND Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. By 25 March 2022:

(a) the parties are to confer and, to the extent necessary, provide draft orders to the Associate to Markovic J giving effect to these reasons; or

(b) if the parties are unable to agree on a form of proposed orders they are:

(i) each to notify the Associate to Markovic J of the proposed orders for which they contend; and

(ii) have the proceeding listed for case management hearing for the purpose of determining the orders to be made.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MARKOVIC J:

1 This proceeding is a representative proceeding under Pt IVA of the Federal Court of Australia Act 1976 (Cth) (Federal Court Act). It is brought by Mervyn Lawrence Brady as applicant on his own behalf and as representative party for and on behalf of members of the MLC Super Fund whose benefits were transferred on 1 July 2016 by successor fund transfer from The Universal Superannuation Scheme Fund (TUSS) to the MLC Super Fund. NULIS Nominees (Australia) Limited in its capacity as trustee of the MLC Super Fund is the respondent.

2 The background to the proceeding is described at Brady v NULIS Nominees in its capacity as trustee of the MLC Super Fund [2021] FCA 999 (Brady (No 1)) at [5]-[9] and, in particular at [5]-[6] where the nature of Mr Brady’s claim is described as follows:

5. … In summary, the applicant impugns two resolutions made by the NULIS board in connection with the preparation and consideration of the successor fund transfer: the decision made on 10 June 2016 “to approve to maintain the current grandfathered commission arrangements pertaining to the products which form part of TUSS following the proposed [successor fund transfer] to the MLC Super Fund” (Grandfathering Decision); and the decision made on 16 June 2016 to approve certain contractual documents pursuant to which the grandfathered commissions were paid prior to the successor fund transfer. The applicant alleges that each of those decisions were made by NULIS in breach of the statutory covenants implied into the governing rules of the MLC Super Fund by subs 52(2)(b), (c) and (d) of the Superannuation Industry (Supervision) Act 1993 (Cth) (SIS Act).

6. The applicant also alleges that NULIS breached those covenants during the period from 1 July 2016 to 23 September 2020 (Relevant Period) by implementing the decision to maintain the grandfathered commission arrangements, by paying the commissions to financial services licensees and by obtaining the commissions from the members of the MLC Super Fund.

3 On 23 August 2021, among others, orders were made requiring Mr Brady to notify NULIS of a proposed sample group member who did not in the period from 1 July 2016 to 23 September 2020, satisfy a condition of release or have unrestricted non-preserved benefits (as that term is used in the Superannuation Industry (Supervision) Regulations 1994 (Cth) (SIS Regulations)) in the TUSS Division of the MLC Super Fund and for Mr Brady to file and serve a points of claim in respect of the sample group member and NULIS to file and serve a points of defence: see Brady (No 1).

4 These reasons are the third in a series concerning case management and related questions which have arisen in the conduct of the proceeding. They concern the proposed common questions of fact and law to be determined at the initial trial. To that end on 8 December 2021:

(1) an order was made that the question of whether any loss or damage suffered by Mr Brady and group members as alleged can be awarded in an aggregate amount pursuant to s 33Z(1)(f) of the Federal Court Act is not to form part of the initial trial: see Brady v NULIS Nominees (Australia) Limited in its capacity as trustee of the MLC Super Fund (No 2) [2021] FCA 1517 (Brady (No 2)); and

(2) as a consequence of the resolution of that question further orders were made requiring the parties to confer to finalise the list of common questions of fact and law to be determined at the initial trial and, in the event that the parties could not agree on the list of common questions, they were each to provide a copy of their proposed orders together with a short outline of submissions in relation to the outstanding issues that arose between them.

5 The parties agreed that, unless the Court otherwise ordered, any unresolved issues in relation to the common questions could be determined on the papers. I am satisfied that I can proceed in that manner and that an oral hearing is not required.

proposed common questions

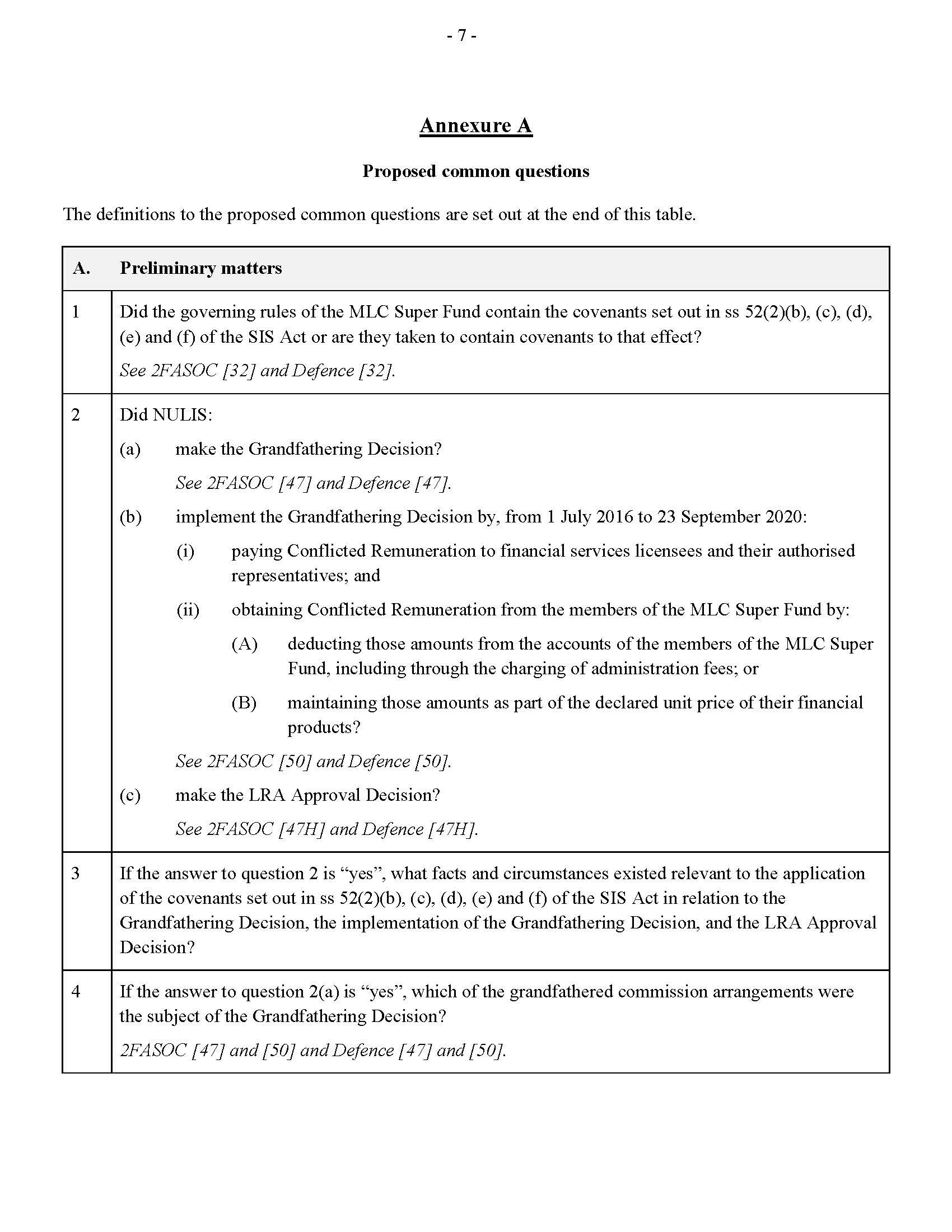

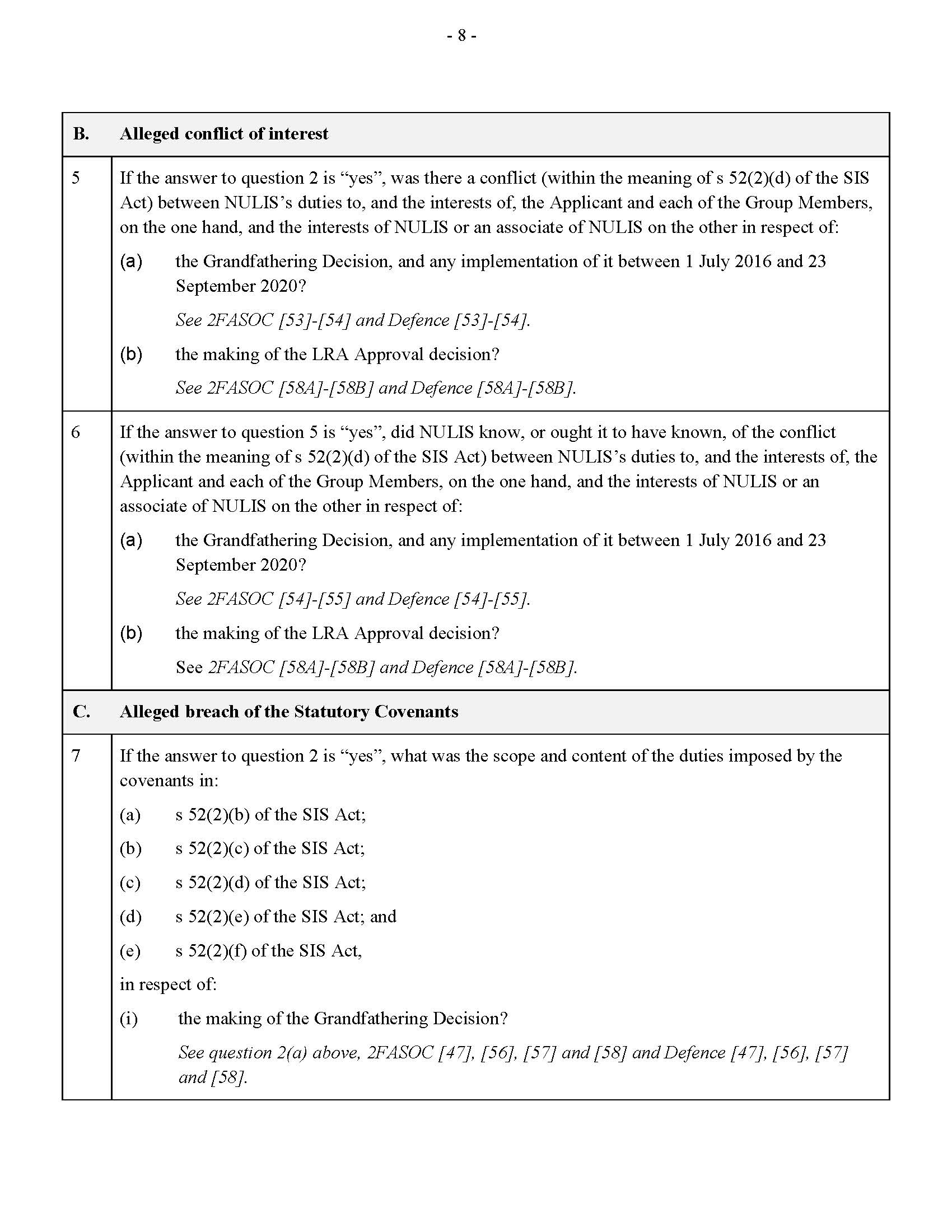

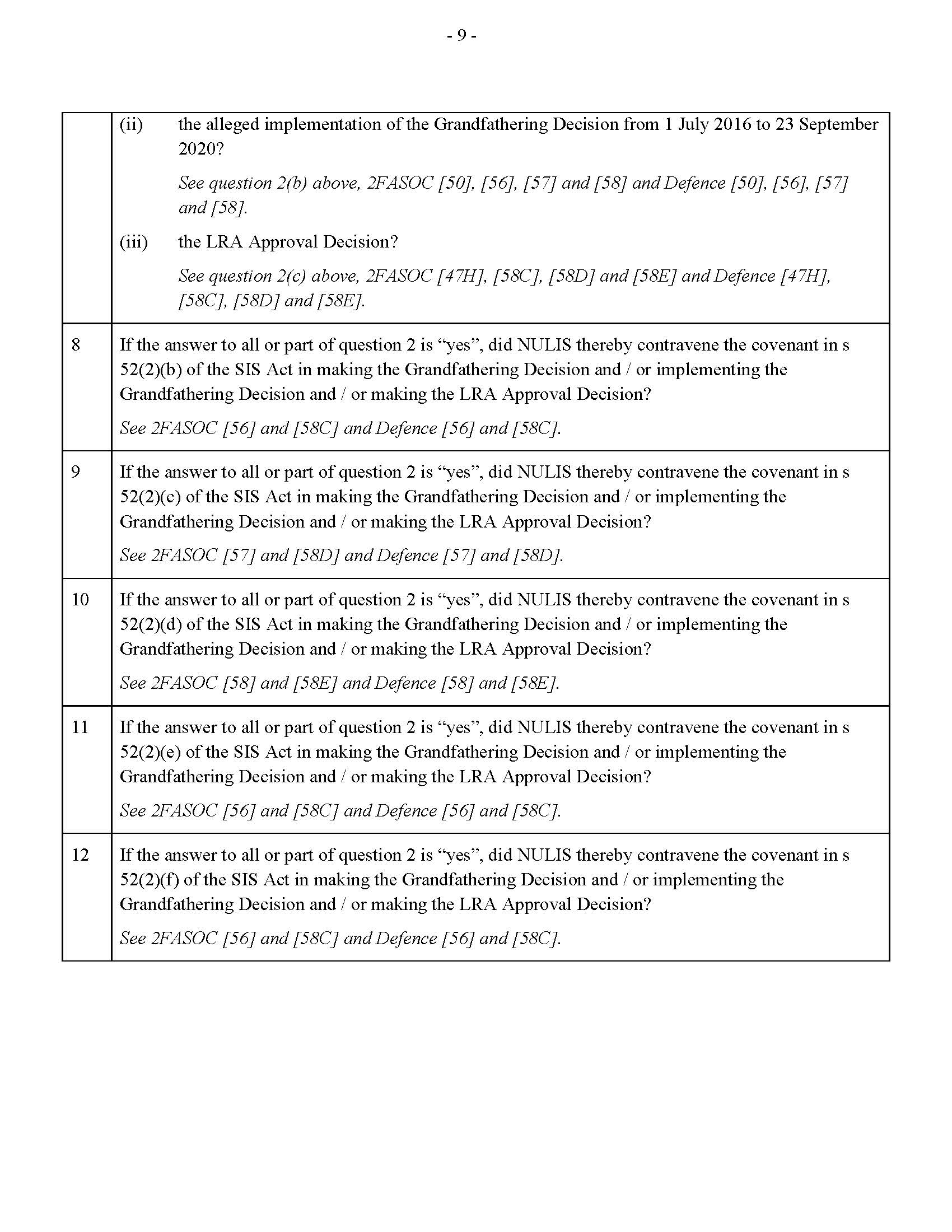

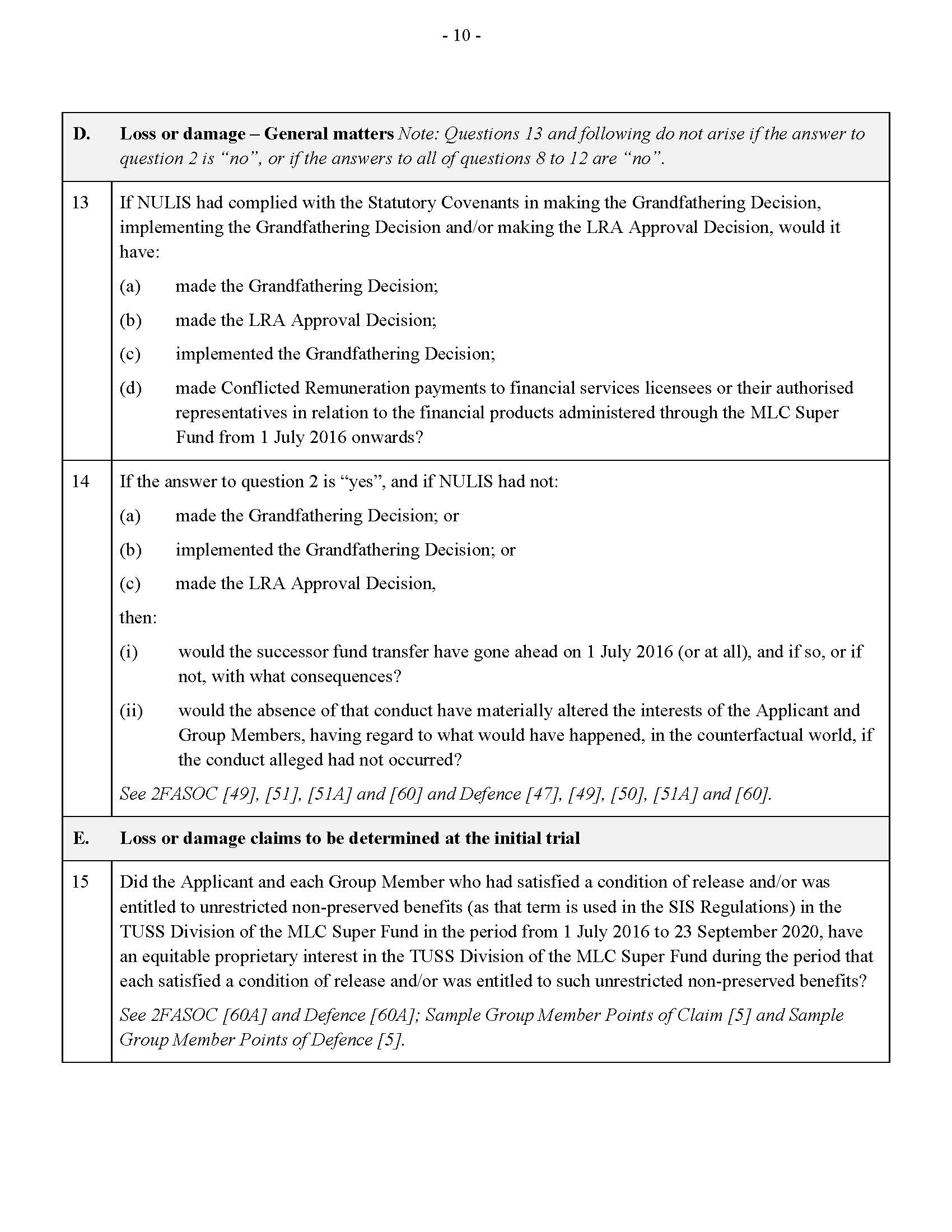

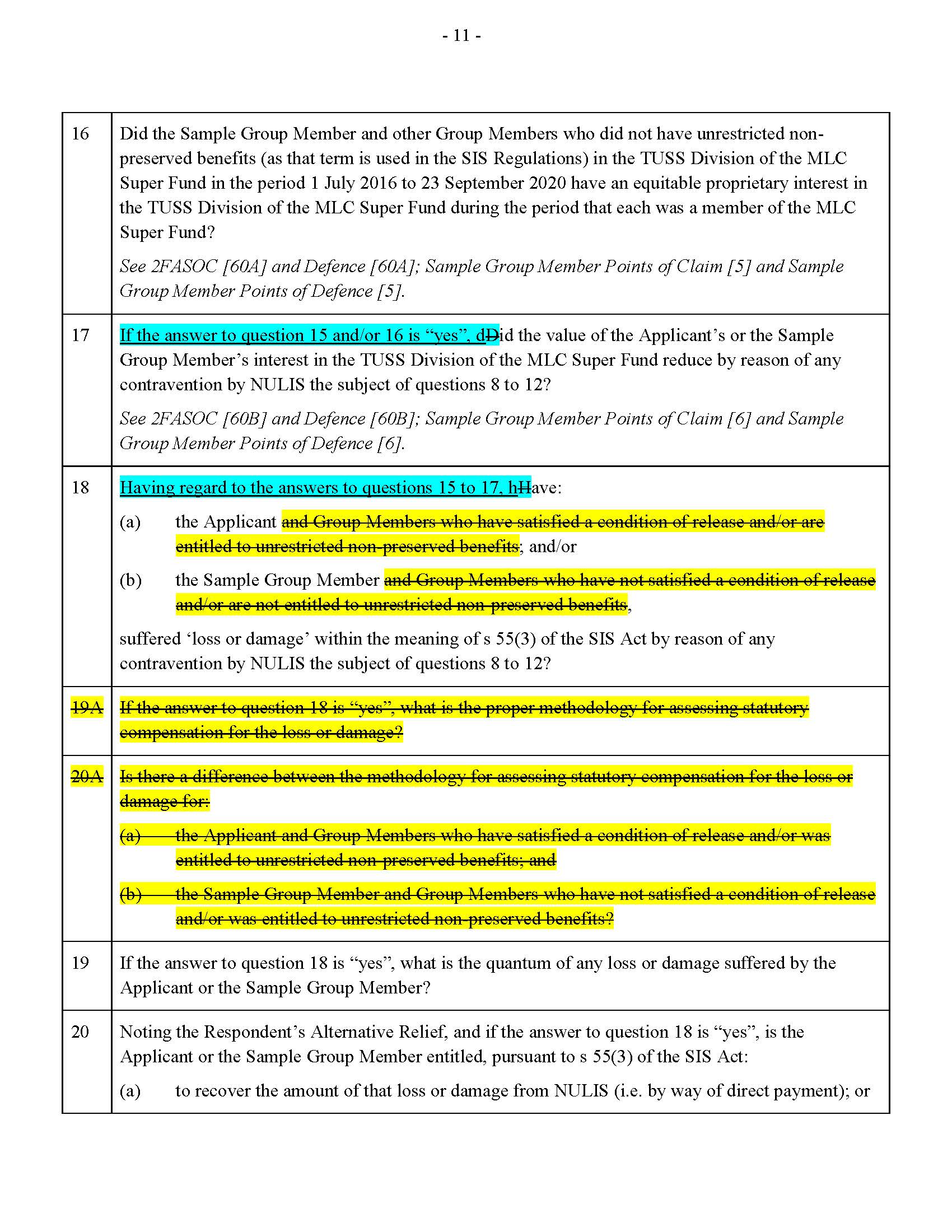

6 Annexed to these reasons is a copy of a document titled “Annexure A Proposed common questions” which sets out the proposed common questions and which are, for the most part, agreed. There are four points of difference between the parties: the form of questions 17 and 18 and whether questions in the form of proposed questions 19A and 20A should be included as common questions for the initial trial. Each of the questions that remain in issue concern loss, as opposed to liability.

7 By way of explanation of the annexure:

(1) Mr Brady seeks to have the text highlighted in yellow included in the common questions. To the extent he does, NULIS rejects its inclusion and, in the case of proposed questions 19A and 20A, rejects the entirety of the questions; and

(2) NULIS seeks to have the underlined text, highlighted in blue included in the questions. To the extent it does, Mr Brady opposes its inclusion.

8 I deal with each of the questions in issue below.

Proposed question 17

9 NULIS proposes that the words “[i]f the answer to question 15 and/or 16 is ‘yes’” be included as the opening words to question 17. It does so because it says that on Mr Brady’s pleaded case question 17 only arises for consideration if the Court answers questions 15 or 16 in his favour. NULIS contends that its proposed additional words make that position clear and tie the question of reduction in value to Mr Brady’s pleaded case.

10 Question 17 concerns the alleged loss pleaded at [60B] of the second further amended statement of claim (SFASOC). The pleading of loss and damage commences at [60] of the SFASOC. In order to understand [60B] in context it is necessary to have regard to [60]-[60B] of the SFASOC which provide:

60 Had NULIS complied with its statutory covenants in making the Grandfathering Decision and in implementing the Grandfathering Decision, and making the LRA Approval Decision, NULIS would not have:

(a) made the Grandfathering Decision or implemented the Grandfathering Decision or made the LRA Approval Decision; or

(b) continued to make the Conflicted Remuneration Payments.

60A By reason of the matters pleaded in paragraphs 17(a) and (b) above, the Applicant and each Group Member during the period each of them was a Member of the Fund had an equitable proprietary interest in the TUSS Division of the MLC Super Fund.

Particulars

(i) The Applicant was a Member of the TUSS Division of the MLC Super Fund from 1 July 2016 to 23 February 2021 and the benefits in his account no 8301190 were “unrestricted and non-preserved” during that period; 2016 annual statement MLB.001.001.0085 at page 1; 2017 annual statement MLB.001.001.0087 at page 1; 2018 annual statement MLB.001.001.0089 at page 1; and 2019 annual statement MLB.001.001.0090 at page 1;

(ii) SIS Regulations 1994 (Cth) reg 6.20;

(iii) Particulars of the period in which each of the Group Members was a Member of the TUSS Division of the MLC Super Fund and the benefits in their accounts shall be provided following the Initial Trial.

60B The value of the interests referred to in paragraph 60A was reduced by reason of NULIS obtaining the Conflicted Remuneration from the Applicant and each Group Member.

Particulars

(i) The value of the Applicant’s interest is that recorded in the 2016 annual statement MLB.001.001.0085 at page 1; 2017 annual statement MLB.001.001.0087 at page 1; 2018 annual statement MLB.001.001.0089 at page 1; and 2019 annual statement MLB.001.001.0090 at page 1 for account no 8301190;

(ii) In the case of the Applicant, the Conflicted Remuneration was deducted by NULIS from account no 8301190 by including it in the calculation of the unit price for each investment option with the consequence that the balance in the account was reduced by the amount of the deduction; 2016 annual statement MLB.001.001.0085 at pp 3-4; 2017 annual statement MLB.001.001.0087 at pp 3-4; 2018 annual statement MLB.001.001.0089 at pp 3-4; and 2019 annual statement MLB.001.001.0090 at pp 3-4;

(iii) Further particulars will be provided in conjunction with the Applicant’s expert evidence;

(iv) Particulars in respect of the Group Members shall be provided following the Initial Trial.

11 Relevantly [17(a)] and [17(b)] of the SFASOC provide:

17 The MLC Super Fund was established by a trust deed dated 9 May 2016 and amended from time to time (MLC Super Fund Trust Deed). The trust deed relevantly provided in respect of members of the TUSS Division:

(a) The following defined terms:

(i) a ‘Beneficiary’ includes:

(A) a Member; or

(B) any other person who is entitled to be paid a benefit from the Fund;

(ii) a ‘Member’ is a person admitted as a member of the Fund and who has not ceased to be a member;

(iii) an ‘Account’ is an account maintained by the Trustee for a Beneficiary.

Particulars

MLC Super Fund Trust Deed, cl 1.1.

(b) The Trustee must hold the Fund assets on trust for the Beneficiaries subject to the terms of this deed.

Particulars

MLC Super Fund Trust Deed, cl 1.1.

12 The sample group member’s points of claim repeats the matters pleaded in [60], [60A] and [60B] of the SFASOC.

13 In its defence to the SFASOC, NULIS denies para [60] and at [60A] and [60B] responds to [60A] and [60B] of the SFASOC as follows:

60A In response to paragraph 60A of the 2FASOC, NULIS:

(a) refers to and repeats paragraph 17 above;

(b) in respect of the Applicant:

(i) admits that, from 1 July 2016, the Applicant had unrestricted non-preserved benefits (as that term is used in the SIS Regulations) in the TUSS Division of the MLC Super Fund;

(ii) says that the quantum of those benefits at any given time was subject, inter alia, to the charging of costs against such benefits pursuant to reg 5.02 of the SIS Regulations;

(iii) admits that, from 1 July 2016, the Applicant was entitled to payment of those benefits in accordance with ss 31 - 34 of the SIS Act and Part 6 of the SIS Regulations and subject, inter alia, to the charging of costs against such benefits pursuant to reg 5.02 of the SIS Regulations; and

(iv) admits that, from 1 July 2016 to the date of this Defence, the Applicant's interest in the MLC Super Fund was an equitable proprietary interest in a share of the assets of the TUSS Division of the MLC Super Fund, such share to be determined in accordance with the governing rules of the MLC Super Fund, the SIS Act and the SIS Regulations;

(c) in respect of the Group Members:

(i) refers to and repeats paragraph 3 above;

(ii) admits that members of the TUSS Division of the MLC Fund from time to time have had a beneficial interest in the MLC Super Fund, but that the precise form and quantum of such interest is contingent on particular events and circumstances personal to individual members and which NULIS cannot plead to in global terms;

(iii) denies that any member of the TUSS Division of the MLC Fund had any interest (including any proprietary interest) in any individual piece of trust property, or any identifiable portion of the MLC Super Fund, or any immediate right to payment in respect of preserved or restricted non-preserved benefits; and

(iv) says further that any interest in respect of any benefits was subject to the governing rules of the MLC Super Fund, the SIS Act and the SIS Regulations; and

(d) otherwise denies the paragraph.

60B In response to paragraph 60B of the 2FASOC, NULIS:

(a) denies that it obtained Conflicted Remuneration from the Applicant and each Group Member and therefore denies the paragraph; and

(b) further or in the alternative:

(i) refers to and repeats paragraphs 24 and 50 and subparagraph 60A(a) above; and

(ii) denies that the payment of Grandfathered Remuneration to financial services licensees in respect of certain products as described in paragraph 50 above reduced the value of any interests of Group Members who, at the time, had not satisfied a condition of release or were not entitled to access unrestricted non-preserved benefits.

14 NULIS’ points of defence to the sample group member’s points of claim relevantly repeats [60], [60A] and [60B] of its defence to the SFASOC as well as expressly pleading in relation to matters unique to the characteristics of the sample group member.

15 Mr Brady submitted that the effect of the addition of the words sought by NULIS is to limit question 17 to a consideration of the equitable proprietary interests in questions 15 and 16. Mr Brady’s case is that the contraventions in questions 15 and 16 caused the value of his (or the sample group member’s) interest or amount in the TUSS Division of the MLC Super Fund to reduce. One way he says that this arises is by characterising his interest as an equitable proprietary interest.

16 Mr Brady submitted that the critical question for the Court at the initial trial is whether the conduct the subject of questions 8 to 12 of the common questions, if proved, caused the value of a relevant interest or amount to reduce and whether that reduction sounds in damages under s 55(3) of the Superannuation Industry (Supervision) Act 1993 (Cth) (SIS Act). He said that his formulation of proposed question 17 is consistent with the issue as framed in Shimshon v MLC Nominees Pty Ltd [2021] VSCA 363.

17 Mr Brady understands that NULIS’ concern about question 17 is not that it cannot be asked as a matter of substance but that it does not arise on the pleading. He submitted that if the Court was to accept that argument, the appropriate course is for him to be given leave to amend the proceeding to resolve any uncertainty.

18 The matters in issue between the parties to this proceeding are framed by the pleadings. That each party should be confined to his or its pleaded case is neither novel nor surprising. To proceed otherwise would make the preparation for and conduct of the trial difficult, if not unworkable, particularly given the nature and relative complexity of the issues. Similarly, the scope of the common questions for initial trial must depend on the issues that arise on the pleadings.

19 On a review of the relevant part of the SFASOC it is apparent that Mr Brady contends that he and the group members had an equitable proprietary interest in the TUSS Division of the MLC Super Fund. At [60B] of the SFASOC that interest is referred to and its value is alleged to have been reduced by reason of NULIS’ conduct.

20 Mr Brady relies on Shimshon in support of his submission that the way in which he has framed question 17 is consistent with the way the issue was framed in that case. In Shimson the Victorian Court of Appeal considered whether the proceeding was, as the primary judge had found to be the case, a “proceeding …. concerning property subject to a trust” within the meaning of s 33B(2)(b)(ii) of the Supreme Court Act 1986 (VIC). The consequence of finding that it was such a proceeding meant that it could not continue as a group proceeding under Pt 4A of the Supreme Court Act because such a proceeding is excluded from Pt 4A by s 33B(2)(b)(ii). The Court of Appeal granted leave to appeal and the appeal was allowed.

21 At [2] Sifris and Walker JJA (who agreed with Whelan JA in the result but departed from his Honour’s reasoning in some respects) summarised the claim brought by the applicant, Shimshon. The respondents to the proceeding were MLC Nominees Pty Ltd and NULIS. Shimshon alleged that, as a result of the respondents’ breaches of their duties as trustee of a superannuation fund, additional fees and commissions were charged to the accounts of the members of the funds thus reducing the amount recorded in each member’s account and causing a consequent reduction in investment returns. In turn this was alleged to have led to a reduction in the amount which members received, or could expect to receive upon the occurrence of an event permitting them to receive payments from the fund, and resulted in members having, prior to any such payments, incorrect account balances.

22 There were three proposed grounds of appeal but Sifris and Walker JJA divided proposed ground 1 into two parts, 1(a) and 1(b). Their Honours held that proposed ground 1(a), which was directed towards the primary judge’s conclusion that the beneficiaries of the funds had only a contingent interest in the funds, and proposed ground 2, which concerned the proposition that the claims made in the proceeding were causes of action directed toward restoration of trust property, were both made out. Their Honours concluded that the proceeding was not one to which s 33B(2)(b)(ii) of the Supreme Court Act applied for the reasons given by Whelan JA. That was because the proceeding sought statutory and equitable compensation payable to individual beneficiaries for breach of statutory and general law duties by a trustee. The proceeding was about whether the trustee breached its general law and statutory duties to the beneficiaries of the funds.

23 At [12]-[14] Sifris and Walker JJA explained:

[12] Having discerned error in the judge’s reasons, the critical question is whether the proceeding is one to which s 33B(2)(b)(ii) applies. We have concluded that it is not, for the reasons given by Whelan JA. As his Honour explains, this is a proceeding seeking statutory and equitable compensation payable to individual beneficiaries for breach of statutory and general law duties by a trustee. A proceeding of that kind is not a proceeding ‘concerning … property subject to a trust’. It is not ‘about’ such property, it is ‘about’ whether the trustee breached its general law and statutory duties to the beneficiaries. The fact that an alternative remedy, of restoration of the trust property, is sought does not convert the proceeding into one concerning property subject to a trust.

…

[14] The nature, extent and characterisation of any loss suffered by the members as a consequence of breach, should breach be established, and the appropriate remedy, are matters for trial and do not control the proper characterisation of the claim. …

24 Having upheld those aspects of the appeal, it was not strictly necessary for their Honours to determine ground 1(b). By that ground Shimshon alleged that the primary judge erred in finding that members of the fund had not suffered “loss or damage” under s 55(3) of the SIS Act, such that those members did not have a statutory cause of action against the trustee. However, they proceeded to do so as they considered it was appropriate, given the significance of s 55(3) to the proceeding, to explain why in their view the primary judge erred in his consideration of that section.

25 Relevantly, the primary judge held that Shimshon had not suffered loss or damage notwithstanding that his expectation, that he may suffer loss or damage in the future, could be legitimate. As a result the primary judge considered that Shimshon could not bring a claim under s 55(3) of the SIS Act: see Shimshon at [56]. On his application for leave to appeal Shimshon contended that the primary judge erred in his construction of s 55(3) of the SIS Act and that the section was specifically intended to confer upon any person who had suffered loss or damage the right to seek compensation, unconstrained by general law principles, and that “loss or damage” was to be construed broadly. Their Honours concluded that proposed ground 1(b) was made out and that the primary judge had erred in relying on a finding of the kind described in ground 1(b) as the basis for concluding that the claim pursuant to s 55(3) of the SIS Act was not a claim “concerning property subject to a trust”: at [58]-[59].

26 Again, although not strictly necessary, Sifris and Walker JJA considered it appropriate to make some observations about the primary judge’s finding that Mr Shimshon had not suffered loss or damage within the meaning of s 55(3) of the SIS Act and as a consequence had no statutory cause of action against the trustee. At [62]-[63] Sifris and Walker JJA said:

[62] The question of when a person ‘suffers loss or damage’ under s 55(3) is a question of statutory construction. Thus it is necessary to have regard to the text, context and purpose of the section. It is also appropriate to have regard to the principle of construction that beneficial legislation should be accorded a ‘fair, large and liberal interpretation’, rather than one which is literal or technical, because we consider that the SIS Act generally, and s 55(3) in particular, is beneficial legislation.

[63] The judge held that the meaning of that phrase is its ordinary meaning as a matter of general law. His Honour placed particular emphasis on the word ‘suffers’, indicating a requirement for present loss or damage. But even accepting as much, in our view attention must be given to the scope of the phrase ‘loss or damage’. And, in so doing, it is vital to have regard to the statutory context and the purpose of s 55. That statutory context includes the following matters.

(rr) A superannuation fund, while established as a trust, receives contributions from workers and their employers that are directly related to the workers’ work. As noted above, employer contributions have been described by the High Court as ‘deferred pay’.

(ss) As the judge observed, the SIS Regulations describe the individual members as having ‘benefits in the fund’, and a trustee of a superannuation fund is required to maintain minimum benefits for members.

(tt) Further, and as the judge again observed, under the SIS Regulations, trustees of regulated superannuation funds are obliged to allocate contributions to members. That is, superannuation trustees are required to keep individual accounts for members, which correspond to their own and their employers’ contributions, plus the returns (or minus the losses), and less the expenses, of the fund. The scheme requires that it is possible to identify within the fund an amount to which the worker is entitled at a particular time, should a relevant event occur, even though the worker is not entitled to particular assets of the fund.

(uu) Superannuation is portable; that is, the identified amount can be moved from one fund to another at any time and, as noted in Whelan JA’s judgment, can be dealt with as an asset of the worker for the purposes of a division of assets under family law.

(Footnotes omitted.)

27 At [64] their Honours concluded that each of those matters supported a reading of “loss or damage” in s 55(3) of the SIS Act “as sufficiently broad as to include a diminution in the member’s individual account within the fund, even where the member’s entitlement to payment out of the fund has not crystallised”.

28 Mr Brady’s intent is to frame proposed question 17 so that it is consistent with the issue as framed in Shimshon. While he does not say so, I assume by that he intends to refer to the conclusion at [64]1 (see [27] above). That may be so but the inclusion of the words proposed by NULIS are to ensure that the question reflects the pleaded case. If those words were removed the question would go beyond the effect of Mr Brady’s pleading at [60A]–[60B]. Accordingly, I am satisfied that the opening words proposed by NULIS should be included so that proposed question 17 is in the following terms:

If the answer to question 15 and/or 16 is “yes”, did the value of the Applicant’s or the Sample Group Member’s interest in the TUSS Division of the MLC Super Fund reduce by reason of any contravention by NULIS the subject of questions 8 to12?

29 If it is Mr Brady’s intent that there should be a common question which is not so confined, then he may wish to seek leave to amend his pleading. However, I am not inclined to grant him leave to do so, without him first providing a copy of any proposed amendment to NULIS. If there is no objection to such an amendment, it can be made by consent and any proposed consequential amendment to the common questions could then be considered.

Proposed question 18

30 Two issues arise in relation to proposed question 18: first, NULIS seeks the inclusion of the words “[h]aving regard to the answers to questions 15-17” at the commencement of the question; and secondly, Mr Brady seeks the addition of words such that the question of whether loss or damage has been suffered within the meaning of s 55(3) of the SIS Act by reason of any contravention by NULIS should be answered both in relation to, on the one hand, the applicant and the sample group member, and on the other, the group members more generally.

31 I turn first to consideration of the inclusion of the additional words sought by NULIS. The addition of those words is not required. The terms of proposed question 18, absent the additional words proposed by NULIS, are consistent with Mr Brady’s pleading.

32 At [61] of the SFASOC Mr Brady alleges that:

By reason of the matters pleaded in paragraphs 53 to 60B above, the Applicant and each Group Member have suffered, and continue to suffer, loss or damage.

Particulars

(i) The contraventions have caused, and continue to cause, a reduction in the amount which the Applicant and each of the Group Members have received from the MLC Super Fund;

(ii) The contraventions have caused, and continue to cause, a reduction in the amount which the Applicant and each of the Group Members can expect to receive from the MLC Super Fund;

(iii) The contraventions have caused, and continue to cause, a reduction in the value of the interests referred to in paragraph 60A above;

(iv) The particulars to paragraphs 60A and 60B above are repeated.

33 That is by [61] of the SFASOC Mr Brady refers back to the matters pleaded at [53]-[60B] inclusive. It is thus difficult to see how that part of the pleading is limited by reference to or contingent upon the claim in [60A]-[60B] and the establishment of an equitable proprietary interest in the TUSS Division of the MLC Super Fund. The additional words proposed by NULIS should not be included.

34 I turn then to the second matter, namely the proposed inclusion by Mr Brady of a reference to group members such that the Court would be asked to consider whether the alleged contraventions caused loss or damage within the meaning of s 55(3) of the SIS Act for group members, as well as for Mr Brady and the sample group member.

35 Mr Brady submitted that there is already (in proposed question 14) an agreed common question about causation which is relevantly framed to include a consideration of the effect of NULIS’ conduct on the interests of group members. Mr Brady contended that it logically flows from that question for the Court to consider the question of whether the “material…alter[ation of] the interests of the Applicant and Group Members” is loss or damage.

36 I do not agree that the additional words proposed by Mr Brady should be included. The question of whether the initial trial should be limited to a determination of whether Mr Brady and the sample group member have suffered loss or damage or whether all group members have suffered loss or damage by reason of NULIS’ alleged contraventions was determined in Brady (No 2).

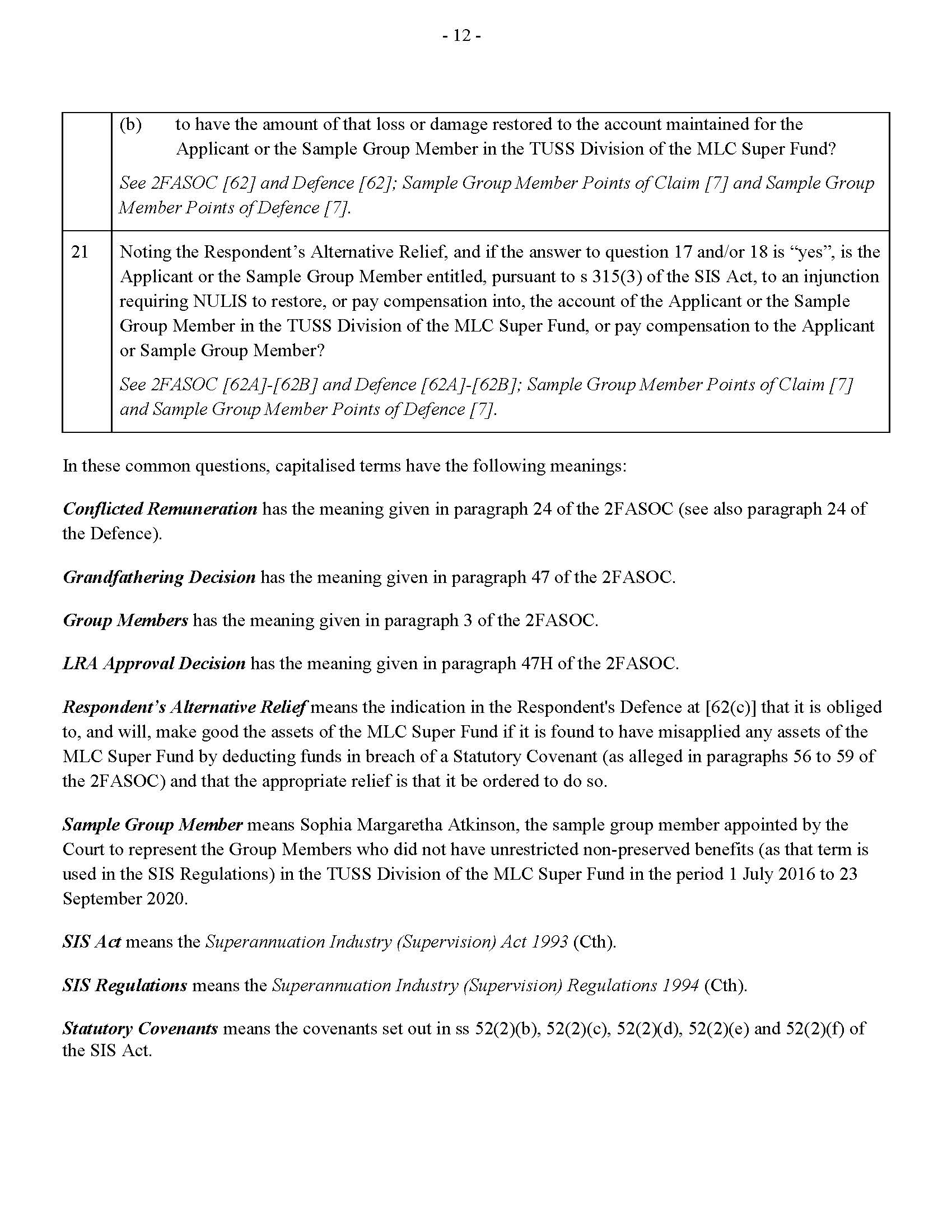

37 At [22] of Brady (No 2) I referred to [62(c)] of NULIS’ defence where it pleads that: if it has misapplied any assets, which it denies, then as trustee of the MLC Super Fund it is “obliged to (and will) make good the assets of the MLC Super Fund, and the appropriate relief is an order that it do so”; and that, upon the assets being made good, no loss or damage will have been suffered by Mr Brady or any group member who remains a member of the MLC Super Fund. In those circumstances NULIS contended that there was thus no loss or damage to be recovered under s 55 of the SIS Act. NULIS relied on this as a powerful reason why the initial trial should be confined to questions of breach and determination of Mr Brady’s own claim. At [23] I referred to Mr Brady’s submission as to why NULIS’ contention was wrong.

38 At [24] of Brady (No 2) I concluded that the initial trial should be confined to “questions of breach, determination of [Mr Brady’s] individual claim” and “issues such as whether the offer made by [NULIS] at [62(c)] of its defence is available, to whom, and whether it can supplant a claim for damages under s 55(3) of the SIS Act”. I noted that all of those issues could be determined in the context of Mr Brady’s claim.

39 I accept NULIS’ submission that the additional words proposed by Mr Brady would put questions of loss and damage at large and bring into consideration individualised questions not appropriate for the initial trial. Such questions could include the nature of the advice received by individual group members about product selection for their superannuation investments, fee and cost structures applicable to those products and the nature of any arrangements group members had reached with their advisors to reduce the fees payable and choices they might have made if the products’ fees and costs structures had been different.

40 Thus proposed question 18 should be as follows:

Have:

(a) the Applicant; and/or

(b) the Sample Group Member,

suffered loss or damage within the meaning of s 55(3) of the SIS Act by reason of any contravention by NULIS the subject of questions 8 to 12?

Proposed questions 19A and 20A

41 Mr Brady seeks the inclusion of these questions in the common questions for trial. They go to the methodology for assessing statutory compensation.

42 Mr Brady submitted that the inclusion of questions of this nature is an entirely orthodox approach to representative proceedings and that he intends to lead expert evidence in relation to the question of methodology which will be to the effect that there is a common methodology for the quantification of loss. However, Mr Brady accepts that the exact amount of damages suffered by group members will not be matters for determination at the initial trial.

43 Mr Brady observed that given NULIS’ opposition to the inclusion of these questions it is apparent that it will seek to lead evidence or make submissions about the individual nature of loss and damage. He submitted that the appropriate course is to include these questions in the form proposed so that the issue can be decided at trial. Mr Brady said that the Court can reassess the appropriateness of the common questions after the evidence is before the Court and can, after the trial, decline to answer the question because, having heard the evidence, it is satisfied that the question is not common. Mr Brady submitted that this approach is consistent with Brady (No 2).

44 Mr Brady accepts that it will not be possible to determine aggregate damages at the initial trial and does not seek to do so. He said that he only seeks to have dealt with the proper methodology of assessing statutory compensation for the loss or damage suffered by him and other group members who have satisfied a condition of release and/or are entitled to non-preserved benefits and those who have not. He does not seek to have the question of the methodology for the assessment of aggregate damages determined at the initial trial.

45 Mr Brady submitted that proposed questions 19 and 20 will only answer the process and methodology for assessing individual losses. He contended that the questions will allow the Court to answer the issues raised in Brady (No 2) at: [25] (whether NULIS can elect which remedy is available to Mr Brady and whether that affects the methodology for assessing statutory compensation); [26] (the determination of any “prior issues” that might affect the calculation of loss and damage); and [27] (whether there is a distinction between vested and non-vested members of the MLC Super Fund and whether a member who does not have a vested interest in a superannuation fund can suffer loss or damage for the purposes of the SIS Act).

46 Mr Brady relied on Jarra Creek Central Packing Shed Pty Ltd v Amcor Ltd [2007] FCA 1559 which concerned an application for further discovery in a representative proceeding. One of the questions that arose for consideration was whether there should be further discovery of “documents relating to market structure or behaviour” see Jarra at [15]. The respondents argued that such documents only went to questions of causation and damage and thus it was not necessary to make them available until after liability had been determined. However, Tamberlin J accepted the evidence of a witness relied on by the applicant and found that documents as to market structure were relevant to causation and damages as well as liability. In that context at [18] his Honour said:

Although the final precise assessment of damages in respect of an individual group member must be determined having regard to its individual circumstances, there are often more general questions arising (such as causation, remoteness, and types of damage) which can be determined as common questions. In the present case, the application specifically states in paragraph [4(h)] that one of the common questions is the “correct measure of any damages which the Respondents may be liable … to pay to the Applicant and any Group Member”. This does not mean that the exact amount of damages which may depend on individual circumstances is to be determined as a common question, but rather that there are common or overarching questions concerning damages more generally.

(Emphasis in original.)

47 So much can be readily accepted. The question that arises is whether proposed questions 19A and 20A are of that nature and apt to be determined at the initial trial, particularly given the earlier ruling that the question of whether there can be an award of aggregate damages pursuant to s 33Z(1)(f) of the Federal Court Act is not to form part of the initial trial.

48 In Brady (No 2) I determined that the exercise of calculating loss and damage ought only be undertaken after determination of any anterior issues that might affect that calculation: at [26]. At [29] I said:

Thirdly, the question of aggregate damages will of course only arise if the applicant succeeds on his liability case. That anterior issue (and the amount payable to the applicant for any loss or damage he has suffered) ought to be determined prior to the parties embarking on the preparation of complex evidence in relation to aggregate damages. That is particularly so in circumstances where the applicant no longer claims that his liability case necessarily depends upon his damages case and where he has not yet identified the methodology he proposes for the assessment of aggregate damages, a matter which could, subject to the approach taken, impact on the ambit of the controversy between the parties and therefore the conduct of the trial. That being so, it is not appropriate to bring forward questions of aggregate damages until questions of liability are determined. To do so would not be in the interests of the efficient conduct of the proceeding having regard to the purpose of Part IVA and s 37M of the Federal Court Act.

49 The questions of aggregate damages that are to be deferred until after the initial trial include determination of the methodology to be applied for the purpose of calculating such damages. Evidence in relation to methodology and a determination of the appropriate methodology will only become relevant if Mr Brady succeeds in establishing liability and NULIS is not successful in establishing [62(c)] of its defence. The preparation of what is likely to be complex evidence in relation to the appropriate methodology to adopt would be premature and, as is apparent from Brady (No 2), ought not to form part of the initial trial.

50 The invitation to include proposed questions 19A and 20A and thus necessitate the preparation of evidence to allow the Court to determine them, but with the option of declining to do so on the basis that I would form the view that the questions are not common, is unattractive in the circumstances of this case. First, a determination has already been made that the question of aggregate damages is not to be part of the initial trial; and secondly, such an approach would not be in the interests of the efficient conduct of the proceeding. The parties ought not to be put to the expense and effort of preparing such evidence in the circumstances of this case and of adopting the two staged approach which now seems to be suggested by Mr Brady.

51 In the circumstances of this case and having regard to its history, proposed questions 19A and 20A are not general questions that can be determined at the initial trial and ought not to be included in the common questions for the initial trial.

conclusion

52 To the extent necessary, the parties should provide my Associate with draft orders reflecting these reasons within 10 days of the date of their publication, including any proposed order in relation to costs. If the parties cannot agree on the form of orders they should provide my Associate with their respective versions of their proposed daft orders within that time together with a request that the proceeding be listed for case management hearing at which time the form of orders to be made will be resolved.

I certify that the preceding fifty-two (52) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Markovic. |