Federal Court of Australia

Star Entertainment Group Limited v Chubb Insurance Australia Ltd (No 2) [2022] FCA 16

ORDERS

DATE OF ORDER: | 19 january 2022 |

THE COURT ORDERS THAT:

1. The claim for declaratory relief in prayer 3A(b) be dismissed with costs.

2. The Amended Originating Application otherwise be dismissed with costs.

3. The costs in Orders 1 and 2 to be agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ALLSOP CJ:

1 On 5 August 2021, I made orders and delivered reasons in this matter on what might be called the main issues in the proceeding: Star Entertainment Group Limited v Chubb Insurance Australia Ltd [2021] FCA 907. I did not decide on an issue concerned with spoilage as can be seen from Order 6 made on 5 August 2021 for reasons set out in [219] of the earlier judgment.

2 The parties provided the submissions contemplated by the orders. I anticipated a decision of the Full Court by the end of 2021 within the context of which to finalise these reasons. I considered that such decision might conceivably affect the reasoning for the spoilage claim. In the light of the Full Court’s decision not being handed down in December 2021, I think it is appropriate that I finalise the claims in this proceeding by dealing with this last part of the proceeding. I set out the extension for spoilage in memorandum 14 to section 1 of the Policy in [54] of my earlier reasons. For convenience I repeat it:

Notwithstanding anything herein contained to the contrary it is agreed that the Policy under The Indemnity - Material Loss or Damage covers loss, destruction of or damage to stock and/or merchandise caused by deterioration, putrefaction, contamination or changes in temperature arising from any cause whatsoever other than work bans, shortage of fuel or the deliberate withholding of electricity supply. (Emphasis added.)

3 No deductible is expressed within the memorandum, as there is in memorandum 16 to section 1.

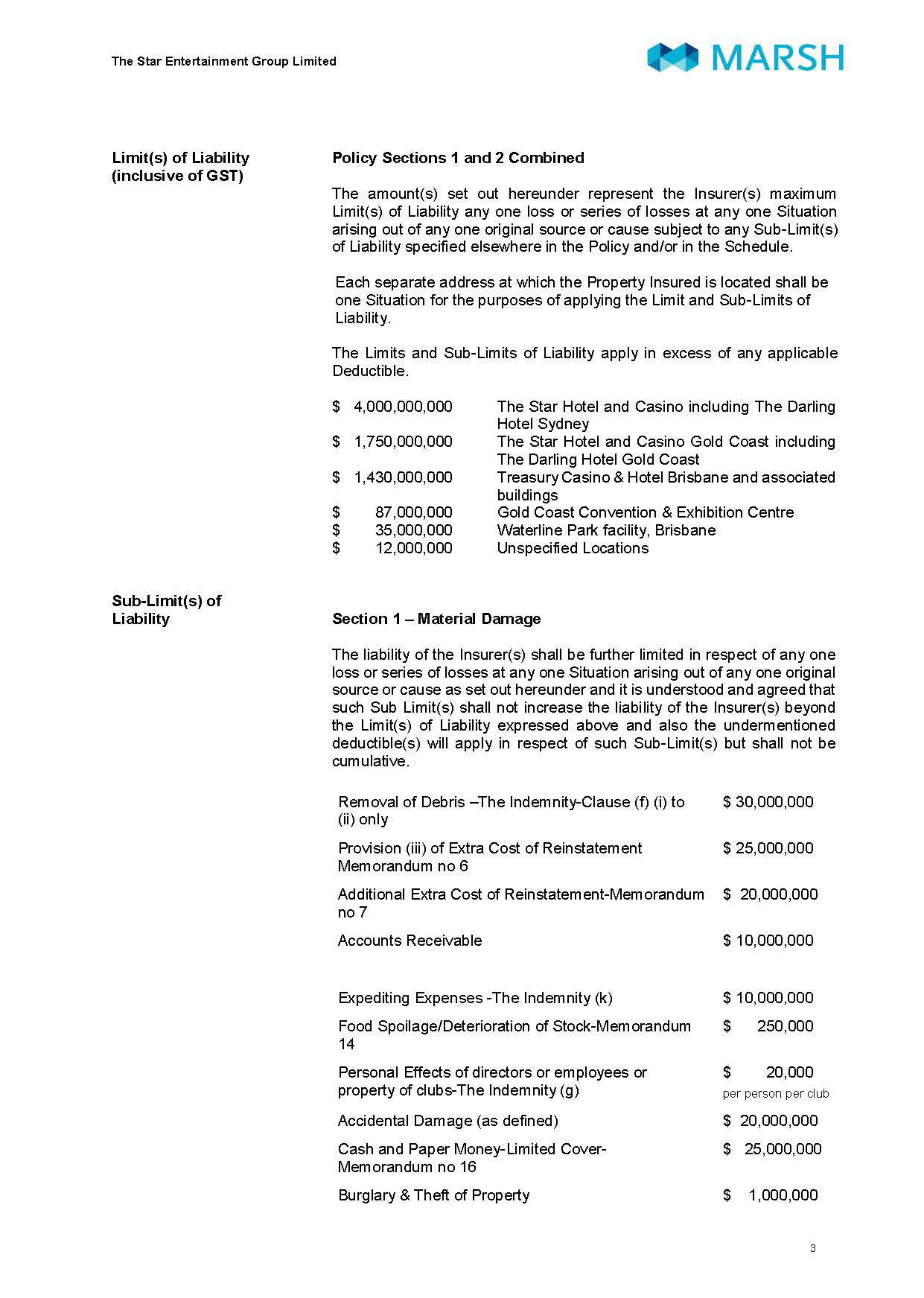

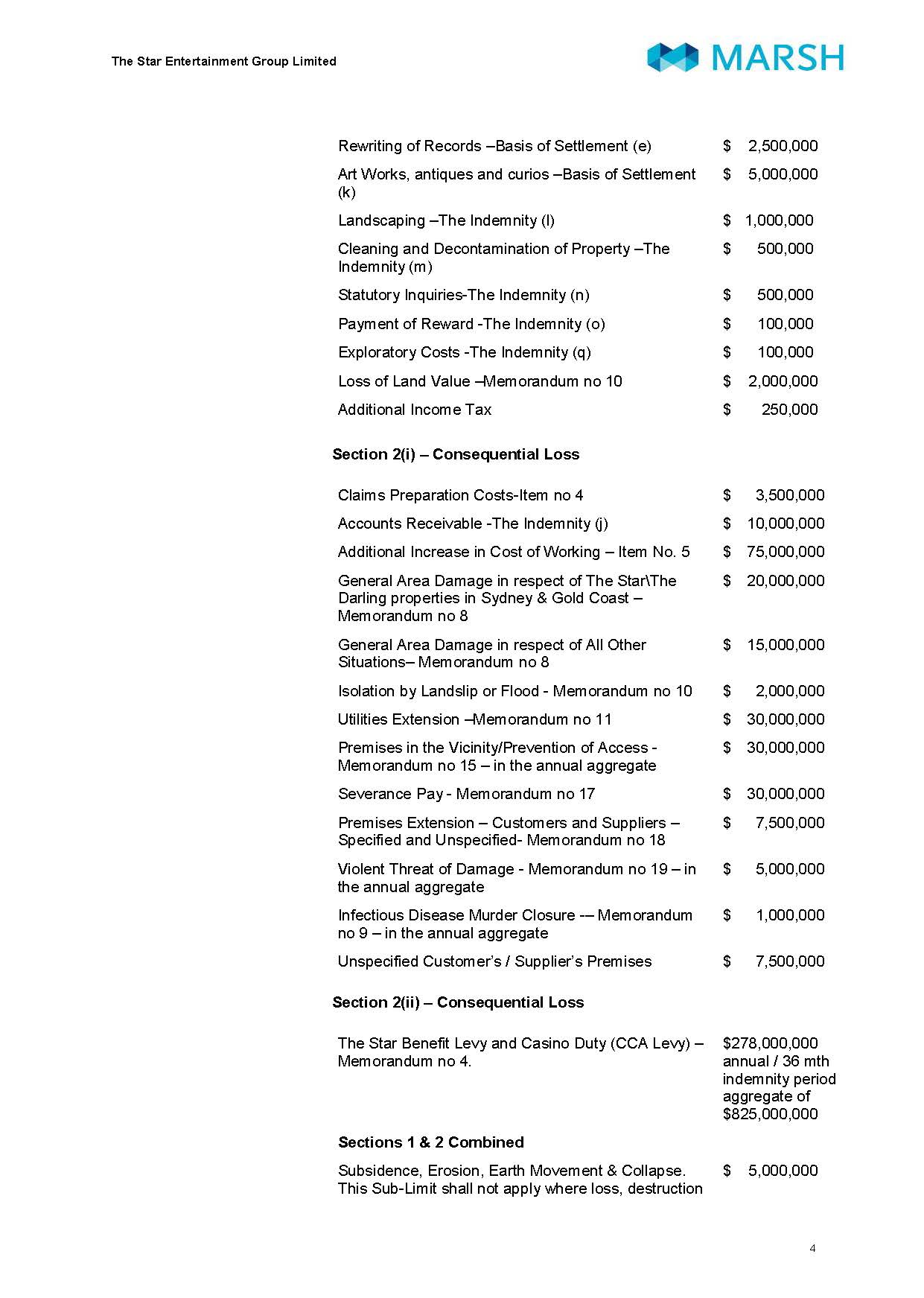

4 The sub-limits to section 1 are set out at [46] of my reasons. For spoilage it is $250,000.

5 There is no express deductible identified specifically for spoilage.

6 At [216]–[218] of my earlier reasons I expressed preliminary views as follows:

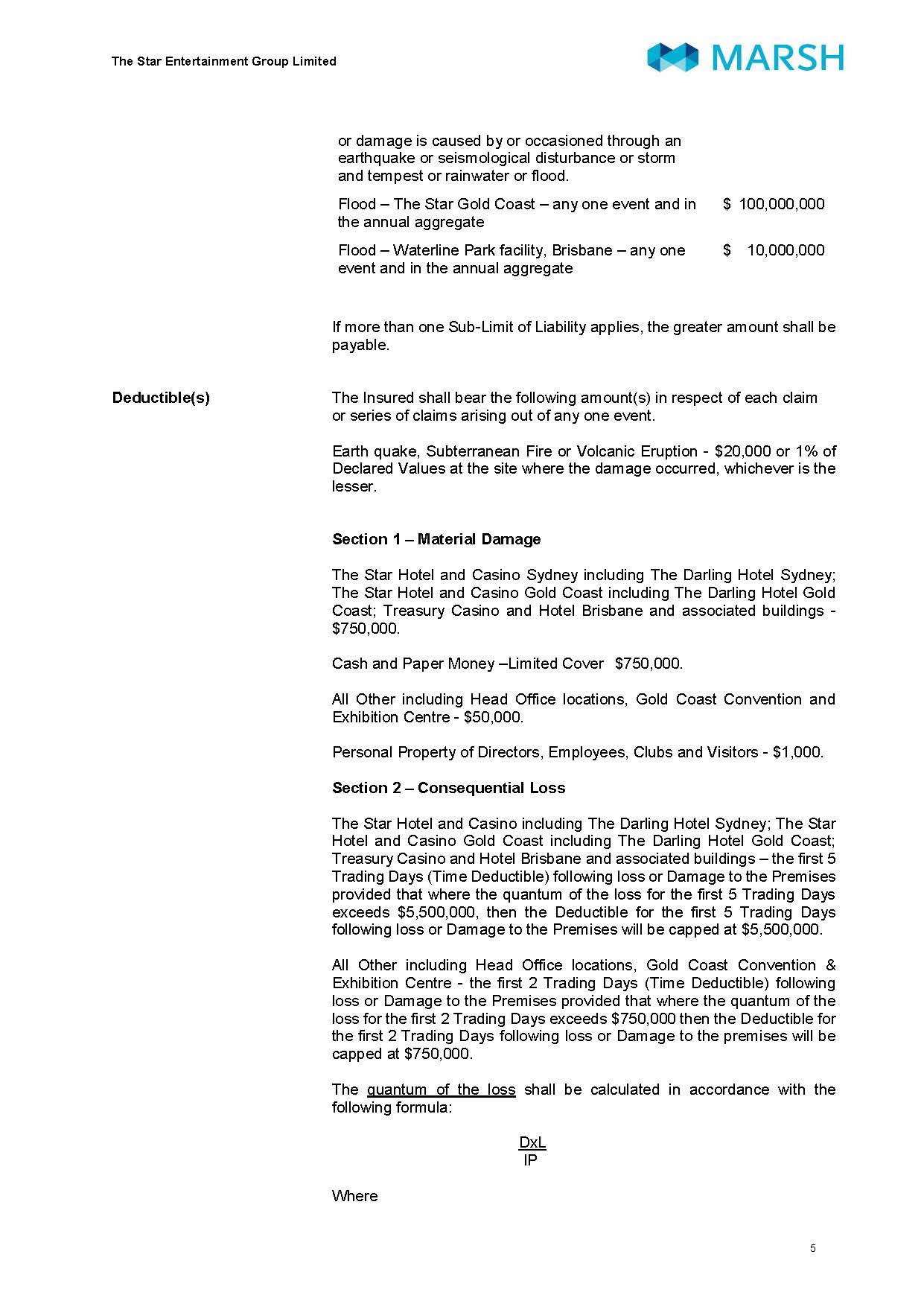

216 The Spoilage Extension, memorandum 14 to section 1 is in wide terms. No deductible is identified within it, as it is in memorandum 16 in section 1 headed “Cash and Paper Money - Limited Cover”, and in memorandum 9 in section 2 (the Disease Extension).

217 The sub-limit for cash and paper money was $25 million and a stated deductible was $750,000. The sub-limit for spoilage is $250,000. There is no stated individual deductible for spoilage. It was submitted by the Insurers that the relevant deductible is $750,000 for each of the claims at the three premises by force of the first paragraph under the heading “Section 1 – Material Damage” under “Deductible”.

218 I am inclined to reject the Insurers’ submission. The $750,000 appears to be a deductible for material damage to property at, in the sense of being part of, the sites falling within the section 1 indemnity under an applicable Basis of Settlement. The presence of named deductibles for one of the extensions in memorandum 16 tends to indicate that if a deductible is to apply to an extension under a memorandum it will be separately identified. It is clear that, as here, spoilage is subject to indemnity irrespective of whether the section 1 indemnity is engaged, absent the effect of memorandum 14. A small limit of $250,000 and a deductible of three times that is not readily explicable. One does not explain that disconformity by assuming that if there is a spoilage claim there will always be a likely large material damage claim under the section 1 indemnity to absorb the deductible.

7 The claims for spoilage are at 3 locations: the Treasury Casino and Hotel at Brisbane: $154,183, the Star Hotel and Casino on the Gold Coast: $227,109, and the Star Hotel and Casino at Sydney: $230,380.

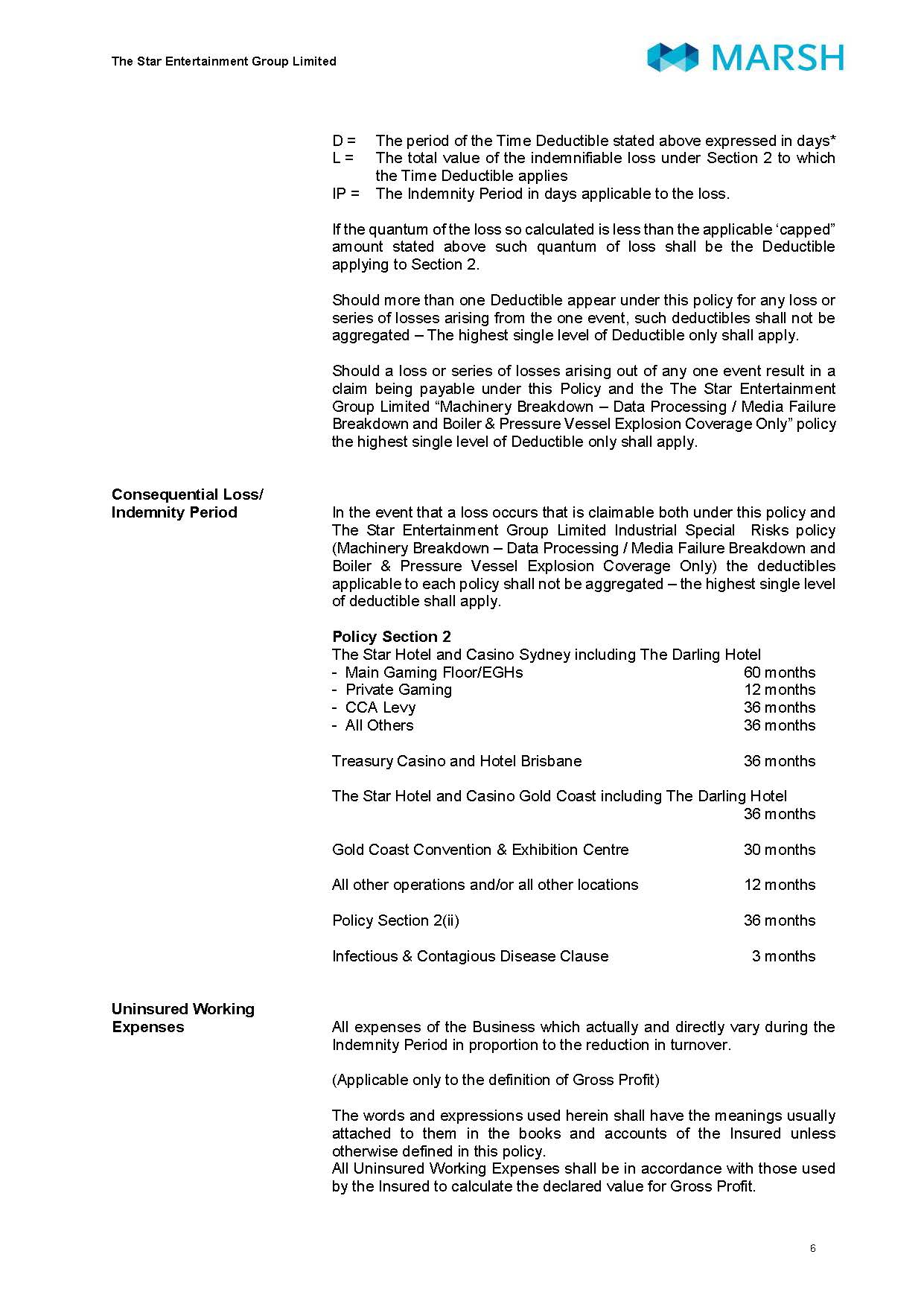

8 The “Limit(s) of Liability” for “Policy Sections 1 & 2 Combined”; the “Sub-Limit(s) of Liability” for “Section 1 – Material Damage”, “Section 2(i) – Consequential Loss”, “Section 2(ii) – Consequential Loss” and “Sections 1 & 2 Combined”; and the “Deductible(s)” for “Section 1 – Material Damage” and “Section 2 – Consequential Loss” were set out on pages 3–6 of the Policy. For convenience I attach these sections of the Policy to these reasons as Annexure A.

9 The Insurers submitted that there was a clear intention for a deductible of $750,000 to the spoilage claim. This conclusion was said to be drawn from six propositions.

10 First, the chapeau to the part of the Policy on deductibles makes it clear that the Policy does not contemplate cover for any claim without a deductible. This was said to flow from the following words:

The Insured shall bear the following amount(s) in respect of each claim or series of claims arising out of any one event.

11 Secondly, in the chapeau to the sub-limit(s) clause the words “and also the undermentioned deductible(s) will apply in respect of such Sub-Limit(s)” reinforced the proposition that a deductible applies to every claim.

12 Thirdly, the third introductory paragraph to the limits clause: “The Limits and Sub-Limits of Liability apply in excess of any applicable Deductible” makes clear that the cover for spoilage (with a sub-limit of $250,000) shall “apply in excess of any applicable Deductible”.

13 Fourthly, the chapeaux to both the limits and sub-limits clauses make clear that the limits and sub-limits apply to “any one loss or series of losses at any one Situation arising out of any one original source or cause”. This ties the claim or loss or series of losses to one Situation.

14 Fifthly, the second introductory paragraph to the limits clause makes clear that the casino locations at Sydney and Melbourne, and on the Gold Coast are each one Situation: each is a “separate address at which the Property Insured is located”.

15 Sixthly, the wording of the deductibles clause reflects a conscious allocation of different deductibles to different Situations and types of claim.

16 Taken together, the above provisions reveal an intention that there are no claims without a deductible set out, so it was submitted.

17 The policy cannot be intended, it was submitted, to cover every piece of spoiled food, however small. Rather, cover for spoilage in such an insurance context is directed to significant losses that are out of the ordinary run of things to which an industrial special risks policy of this kind might respond.

18 There is nothing to be taken, it was submitted, from the lack of a deductible in memorandum 14, but the presence of a deductible in memorandum 16. The other memoranda to section 1 do not specify a deductible, but it was submitted one must apply: see in particular memoranda 5 and 6. Further, memorandum 16 refers to “each and every loss or series of losses” modifying the wording of the deductible provision “each claim or series of claims”. There is no mention of a deductible in memorandum 9 to section 2 (contrary to that which I erroneously stated in [216] of my earlier reasons). There is an aggregate sub-limit there.

19 There is nothing odd, it was submitted, about a large deductible ($750,000) and a small sub-limit ($250,000). It reflects the nature of the policy as one for major physical disruptions and not attaching cover for “every basket of prawns that ‘goes bad’ or every carton of milk that goes ‘off’”.

20 The applicants stressed the opening words of the memorandum 14 “notwithstanding anything herein contained to the contrary”. This width, combined with the lack of a specific deductible for spoilage, makes plain, it was submitted, that no deductible is to apply. The introductory words are not just directed to exclusions 4(a) and (b) (in the way memorandum 16 commences “[n]otwithstanding Property Exclusion 2”). Rather they are wider. The extension operates according to its terms.

21 The limits and sub-limits clauses refer to application in excess of any applicable deduction. The limits and sub-limits clauses do not provide necessarily for a deductible for all memoranda.

22 The Policy would not, the applicants submitted, apply to every “basket of prawns or a carton of milk”. General condition 13 requiring the insured to take all reasonable precautions to prevent loss or destruction of or damage to the Property Insured serves a purpose similar to a deductible: guarding against events that give rise to a claim for indemnity.

23 It is unlikely, it was submitted, that only spoilage claims of $1 million are covered (for the $250,000 sub-limit above the deductible of $750,000).

Consideration and disposition

24 To a degree the arguments have developed in the light of my views as to the principal claim.

25 The extension is in wide terms. Its introduction makes clear its breadth. But its operation is to make clear that “the Policy under The Indemnity – Material Loss or Damage covers loss, destruction of, or damage to stock and/or merchandise” from spoilage as described.

26 The deductible for the three Situations: Sydney, Brisbane and the Gold Coast, was $750,000. That was a deductible for each claim or series of claims arising out of any one event. Memorandum 14 made clear that spoilage for any cause other than the three identified causes was within the indemnity for material loss or damage. I consider that I was in error in [218] of my earlier reasons in limiting the $750,000 deductible for material damage to property, in the sense of being part of, the Situations. There was no textual basis for that conclusion. The $750,000 deductible is for the material damage to Insured Property at the Situations. Memorandum 14 makes plain that spoilage is to fall within that indemnity for material damage. No separate deductible is provided for, as it is with cash and paper money.

27 Thus, if a claim were made for material damage for $2 million which included $75,000 for spoilage the deductible for the $2 million claim would be $750,000. There would be no separate deductible for spoilage. If the spoilage element of the claim were $300,000 the sub-limit would confine that part of the claim to $250,000. Whereas, if the claim was for $2 million material damage including $1 million for cash and paper money, the claim for the latter would be reduced to $250,000 by its separate deductible of $750,000. How that would affect the balance of the claim being $1 million or $1.25 million depending on how one deals with the claim for cash and paper money of $250,000 and whether the $1 million or $1.25 million bears an additional $750,000 material damage deductible otherwise may be open to debate. But it is clear that cash and paper money has a separate deductible. Spoilage does not, though it has a sub-limit.

28 The problem arises here in the context that there has been no material damage, other, of course, than spoilage. Thus the only material damage claim “under The Indemnity – Material Loss or Damage” arises under memorandum 14. The material damage deductible under the indemnity is stated to be $750,000.

29 Thus there is a deductible for spoilage in this case. This is not because spoilage has a separate deductible, but because the spoilage claim is taken to be under the Policy “under The Indemnity – Material Loss or Damage” and is subject to the material damage deductible in the first paragraph under the heading “Section 1 – Material Damage” adjacent to the heading “Deductible(s)”.

30 Thus, given the totality of the spoilage claim is under $750,000 and there is no other material damage claim, the claim for indemnity fails.

31 In these circumstances, it is unnecessary to consider the question whether one or multiple deductibles applies or apply to the claim for each Situation.

32 Therefore the appropriate orders are that the claim for declaratory relief made in prayer 3A(b) be dismissed with costs, such costs to be agreed or assessed; and the Amended Originating Application otherwise be dismissed with costs, such costs to be agreed or assessed.

I certify that the preceding thirty-two (32) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Allsop. |

Associate:

NSD 928 of 2020 | |

THE STAR PTY LIMITED ACN 060 510 410 | |

Fifth Applicant: | THE STAR ENTERTAINMENT SYDNEY PROPERTIES PTY LTD ACN 050 045 120 |

Sixth Applicant: | THE STAR ENTERTAINMENT SYDNEY APARTMENTS PTY LTD ACN 075 423 666 |

Seventh Applicant: | THE STAR ENTERTAINMENT QLD CUSTODIAN PTY LTD ACN 067 888 680 |

Eighth Applicant: | THE START BRISBANE CAR PARK HOLDINGS PTY LTD ACN 610 776 184 |

Ninth Applicant: | THE STAR ENTERTAINMENT GC INVESTMENTS PTY LTD ACN 615 401 164 |

ZURICH AUSTRALIAN INSURANCE LIMITED ABN 13 000 296 640 | |

Fifth Respondent: | ALLIANZ AUSTRALIA INSURANCE LIMITED ABN 15 000 122 850 |

Sixth Respondent: | SWISS RE INTERNATINAL SE AUSTRALIA BRANCH ABN 38 138 873 211 |

Seventh Respondent: | ASSICURAZIONI GENERALI S.P.A (HONG KONG) |

Eighth Respondent: | LIBERTY MUTUAL INSURANCE COMPANY ABN 61 086 083 605 |

Ninth Respondent: | HDI GLOBAL SE AUSTRALIA ABN 55 490 279 016 |

Tenth Respondent: | ALLIED WORLD ASSURANCE COMPANY, LTD (SINGAPORE BRANCH) |

Eleventh Respondent: | PICC PROPERTY AND CASUALTY COMPANY LIMITED |

Annexure A