Federal Court of Australia

PM Capital Asian Opportunities Fund Limited, in the matter of PM Capital Asian Opportunities Fund Limited [2021] FCA 1380

ORDERS

IN THE MATTER OF PM CAPITAL ASIAN OPPORTUNITIES FUND LIMITED (ACN 168 666 171) | ||

PM CAPITAL ASIAN OPPORTUNITIES FUND LIMITED (ACN 168 666 171) Plaintiff | ||

DATE OF ORDER: |

OTHER MATTERS:

A. The Court notes that ASIC was provided with at least 14 days’ notice of the hearing of this application.

B. The Court is satisfied that ASIC has had a reasonable opportunity to:

(i) examine the terms of the proposed scheme of arrangement to which the application relates and a draft explanatory statement relating to that arrangement; and

(ii) make submissions to the Court in relation to the proposed scheme of arrangement and the draft explanatory statement.

C. The Court notes the letter from ASIC to the directors of the plaintiff, PM Capital Asian Opportunities Fund Limited (PAF) dated 4 November 2021 produced at the hearing.

THE COURT ORDERS THAT:

1. Pursuant to subsection 411(1) and section 1319 of the Corporations Act 2001 (Cth) (Act), PAF convene and hold a meeting of its shareholders (Scheme Meeting):

(a) for the purpose of considering and, if thought fit, agreeing (with or without modification) to the scheme of arrangement (Scheme) proposed to be made between PAF and its shareholders (PAF Shareholders), the terms of which are set out in Annexure A to these orders; and

(b) to be held on Monday, 13 December 2021 at 11.00 am (Melbourne time) and to be conducted electronically through an online platform, which is to be accessed in accordance with the instructions included in the Notice of Meeting to be sent to shareholders in accordance with order 2.

2. Pursuant to subsection 411(1) and section 1319 of the Act, the Scheme Meeting be convened by sending on or before 12 November 2021:

(a) an email to each PAF Shareholder who has nominated an electronic address for the purpose of receiving notices from PAF (Email Shareholder) (or, in the case of joint holders, to the holder whose name appears first in PAF’s register), such email to be substantially in the form of Annexure AM-9 to the affidavit of Andrew Stuart McGill affirmed on 3 November 2021 (McGill Affidavit), and which contains hyperlinks to:

(i) an electronic copy of a document substantially in the form of the document which is annexure RAL-7 to the third affidavit of Richard Anthony Lustig dated 4 November 2021 (Scheme Booklet) (which contains, among other things, the proposed Scheme of Arrangement at annexure B and Notice of Scheme Meeting at annexure D);

(ii) an online portal or website that is accessible by the Email Shareholder and which enables the Email Shareholder to lodge proxy voting instructions for the Scheme Meeting online; and

(iii) an online portal or website that is accessible by the Email Shareholder to view, listen to and participate in the Scheme Meeting online;

(b) to each PAF Shareholder who is not an Email Shareholder (or, in the case of joint holders, to the holder whose name appears first in the plaintiff’s register) (Postal Shareholder):

(i) a hard-copy document substantially in the form of the notice and access form at annexure AM-10 to the McGill affidavit (Notice and Access Form) setting out a URL which provides access to a website from which the Postal Shareholder:

(A) can download an electronic copy of the Scheme Booklet; and

(B) is directed to an online portal or website that is accessible by the Postal Shareholder to view, listen to and participate in the Scheme Meeting online; and

(ii) a hard copy proxy form substantially in the form of the proxy form at annexure AM-10 to the McGill Affidavit (Proxy Form) and a reply paid envelope for the Postal Shareholder to lodge their Proxy Form and voting instructions for the Scheme Meeting.

3. The documents referred to in order 2(b) be sent:

(a) in the case of Postal Shareholders whose registered address is within Australia, by prepaid ordinary post addressed to the relevant addresses recorded in PAF’s register; and

(b) in the case of Postal Shareholders whose registered address is outside Australia, by airmail or international courier service addressed to the relevant addresses recorded in PAF’s register.

4. Compliance with r 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) (Rules) be dispensed with, except in so far as that rule applies rule 75-15(2) of the Insolvency Practice Rules (Corporations) 2016 (Cth).

5. Voting on the resolution to agree to the Scheme is to be conducted by way of a poll.

6. A proxy in respect of the Scheme Meeting will be valid and effective if, and only if, it is completed and delivered in accordance with its terms or a proxy is lodged online in accordance with the instructions on the online portal or website referred to in order 2(a)(ii) and received by PAF by 11.00 am (Melbourne time) on Saturday, 11 December 2021.

7. Mr Andrew Stuart McGill or, failing him, Mr Benjamin Everard Skilbeck, be Chairperson of the Scheme Meeting.

8. The Chairperson of the Scheme Meeting has the power to adjourn the Scheme Meeting to such time, date and at such place (including electronically) as the Chairperson considers appropriate.

9. PAF publish a notice of hearing in The Australian newspaper, in substantially the form that appears at Annexure B to these orders, not later than 5 days prior to the date fixed for the hearing of any application to approve the Scheme, and PAF be relieved from compliance with Rule 3.4 and Form 6 of the Rules to the extent necessary.

10. The further hearing of the originating process is adjourned to the Honourable Justice Beach at 10.15 am (Melbourne time) on Wednesday, 17 December 2021 or as soon thereafter as the business of the Court allows.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A

Scheme of Arrangement

[The order entered is available on the Commonwealth Courts Portal, which attaches the Scheme]

Notice of hearing to approve scheme of arrangement

TO all the members of PM Capital Asian Opportunities Fund Limited (ACN 168 666 171) (PAF):

TAKE NOTICE that at 10:15am on 17 December 2021, the Federal Court of Australia will hear an application by PAF seeking the approval of a scheme of arrangement between PAF and its members (the Scheme) if agreed to by a resolution to be considered and, if thought fit, passed by the members of PAF at the meeting to be held on 13 December 2021.

If you wish to oppose the approval of the compromise or arrangement, you must file and serve on PAF a notice of appearance, in the prescribed form, together with any affidavit on which you wish to rely at the hearing. The notice of appearance and affidavit must be served on PAF at its address for service at least 1 day before the date fixed for the hearing of the application.

The address for service of PAF is c/- Baker McKenzie, Level 19, 181 William Street, Melbourne VIC 3000, Australia (Attention: Helen Joyce) (Email: helen.joyce@bakermckenzie.com).

REASONS FOR JUDGMENT

BEACH J:

1 PM Capital Asian Opportunities Fund Limited (PAF) has applied for orders under ss 411(1) and 1319 of the Corporations Act 2001 (Cth) to convene and hold a meeting of its shareholders to consider a proposed scheme of arrangement, the purpose of which is to effect a merger of PAF and PM Capital Global Opportunities Fund Limited (PGF). It is proposed that PGF will acquire all of PAF’s shares that it does not already own in exchange for issuing new shares in PGF. PGF presently owns 19.93% of the shares in PAF.

2 The PAF directors have unanimously recommended that PAF shareholders vote in favour of the scheme. This voting recommendation and the reasons for it are set out in the scheme booklet. In addition, all directors of PAF intend to vote any PAF shares held or controlled by them at the time of the scheme meeting in favour of the scheme. The directors’ voting intention is disclosed in the scheme booklet. The scheme booklet includes the explanatory statement required by s 412(1)(a).

3 Further, the PAF directors have also given consideration to a conditional off-market takeover offer for all of the ordinary shares in PAF which has been made by WAM Capital Limited (WAM) subsequent to the announcement of the scheme. But the PAF directors have not considered that the offer by WAM is superior to the scheme.

4 Further, an independent expert report has been prepared that concludes that the scheme is fair and reasonable and in the best interests of PAF shareholders. The basis for this conclusion is that the value of the scheme consideration is consistent with the assessed valuation range for PAF shares. The independent expert has also considered the offer from WAM in the context of assessing whether the scheme is in the best interests of PAF shareholders, and has concluded that the WAM offer is less attractive than the scheme. The independent expert’s conclusions and analysis in respect of the WAM offer are summarised in the scheme booklet and a copy of the independent expert’s report is to be annexed to the scheme booklet.

5 Now at the hearing I granted WAM leave to be heard on the basis that WAM is an interested person. But WAM is not a shareholder of PAF, and its interests are limited to its status as a competing bidder for PAF who as I say has proposed an alternative and conditional offer.

6 Let me begin with some contextual matters.

Some background facts

7 PAF and PGF are both public companies limited by shares, which are listed on the Australian Securities Exchange. PAF specialises in providing investors with an opportunity to invest in the Asian region. PGF is an investment company, whose objectives are to provide long term capital growth through investment in a concentrated portfolio of global equities and other investment securities.

8 The investment manager of both PAF and PGF is PM Capital Limited (PM Manager). Mr Paul Moore owns and controls 89% of the issued capital of PM Manager by himself and through associates. Further, he owns or controls by himself and through associates 19% of PGF and 13.09% of PAF. He is not, however, a director of PAF or PGF. I will return to Mr Moore’s position later.

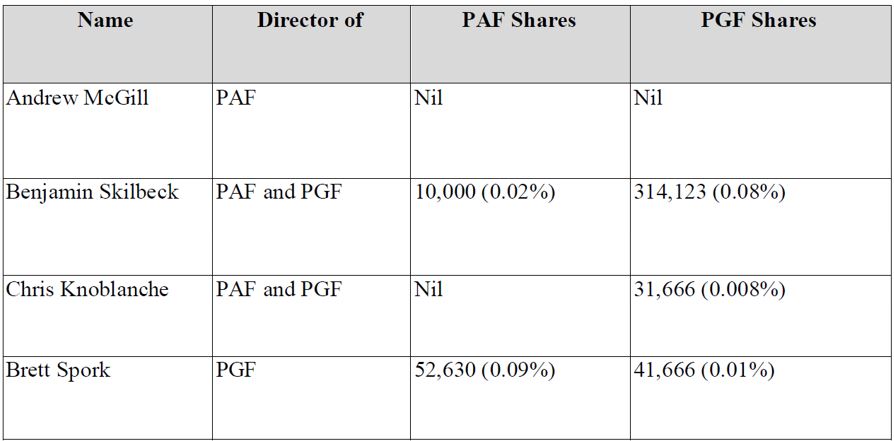

9 PAF has 57,330,012 ordinary shares on issue. PAF does not have any options or performance rights.

10 PGF currently holds 19.93% of the shares in PAF. PGF will not vote these shares at the scheme meeting, and these shares will not participate in the scheme.

11 The directors of PAF are:

(a) Mr Andrew McGill, chairman;

(b) Mr Ben Skilbeck, executive director; and

(c) Mr Chris Knoblanche, non-executive director.

12 Mr Skilbeck and Mr Knoblanche are also directors of PGF. In addition, Mr Brett Spork is a director of PGF.

13 The directors of PAF and PGF and their associates hold the following relevant interests in PGF and PAF:

14 On 15 September 2021, PAF and PGF jointly announced that PGF and PAF had entered into a scheme implementation deed. Under the deed, PAF and PGF agreed to implement a transaction to merge the two entities by way of a scheme of arrangement.

15 Prior to PGF proposing the merger to PAF, the boards of both PAF and PGF were comprised of the same directors, being Mr Skilbeck, Mr Knoblanche and Mr Spork. Accordingly, PAF and PGF established governance protocols to ensure independent consideration of the transaction by PAF and PGF. In particular, pursuant to the PAF governance protocol, PAF formed an independent board committee to consider the scheme comprised of Mr McGill and Mr Skilbeck, and pursuant to the PGF governance protocol PGF formed an independent board committee to consider the scheme, comprised of Mr Knoblanche and Mr Spork.

16 The governance protocols operated in the following fashion.

17 Mr Skilbeck was involved in the PAF board’s consideration of the scheme as a member of the PAF board committee but not the PGF board’s consideration of the scheme. In particular, from the date on which PGF proposed the transaction to PAF, Mr Skilbeck has not been involved as a director of PGF in decision-making concerning the transaction, and will not be involved for the duration of the transaction.

18 Mr Knoblanche was involved in the PGF board’s consideration of the scheme as a member of the PGF board committee but not the PAF board’s consideration of the scheme. In particular, from the date on which PGF proposed the transaction to PAF, Mr Knoblanche has not been involved as a director of PAF in decision-making concerning the transaction, and will not be involved for the duration of the transaction.

19 Mr Spork is involved in the PGF board’s consideration of the scheme as a member of the PGF board committee but not the PAF board’s consideration of the scheme. Mr Spork resigned as a director of PAF shortly prior to entry into of the scheme implementation deed.

20 Mr McGill was appointed as a new director of PAF shortly prior to entry into of the scheme implementation deed, and is a member of the PAF board committee. Mr McGill is independent of PGF and will not assist PGF for the duration of the transaction. From the time that the PAF governance protocol was entered into until his appointment as a director of PAF, Mr McGill was a consultant to PAF and he assisted PAF in the negotiation of the scheme implementation deed and as a member of the PAF board committee.

21 The following matters are also relevant.

22 Each of PAF and PGF has separately appointed PM Manager as its investment manager under separate investment management agreements. The Chief Investment Officer and Chairman of PM Manager is Mr Moore. PM Manager is responsible for the implementation of the investment strategy of each of PGF and PAF, and for the day-to-day administration of each company’s affairs.

23 As I have said, the shares in PM Manager are owned as to 89% by Mr Moore and entities he controls. The board of PM Manager is comprised of Mr Moore, Mr Jarod Dawson and Mr Skilbeck. Mr Moore was appointed by PM Manager to be the portfolio manager for PGF.

24 Further, as I have said, Mr Moore through entities he controls presently holds approximately 19% of the shares in PGF and 13.09% of the shares in PAF.

25 Further, as already noted, PGF holds 19.93% of the shares in PAF. Now under the PGF management agreement, PM Manager was authorised to sell or vote the PAF shares held by PGF. Further, as a consequence of the PGF management agreement, and prior to the revocation of authority referred to below, PM Manager had voting power in respect of approximately 27% of the total issued share capital of PAF, being the aggregate of the approximately 8% holding of Mr Moore and entities he controls and the approximately 19% holding of PGF.

26 But the governance protocols provided that at the time of entry into of the scheme implementation deed and the announcement of the proposed transaction, PGF would remove the PAF shares held in its portfolio from the PGF management agreement by giving notice to PM Manager. The governance protocols noted that the effect of this would be that neither PM Manager nor Mr Moore would control the buy/sell or voting decisions relating to PGF’s shareholding in PAF.

27 Pursuant to the governance protocols, on 14 September 2021 PGF formally revoked the authorisation for PM Manager to sell or vote the PAF shares that were held by PGF as at the date of announcement of the scheme implementation deed. Pursuant to this revocation of authority, those securities were subsequently moved out of the prime broking custodial account, which was administered on a day-to-day basis by the investment manager, and moved into self-custody and so controlled directly by the PGF board.

Key aspects of the scheme

28 If the scheme is implemented:

(a) PGF will acquire all of the PAF shares on issue at the scheme record date, other than the PAF shares held by PGF (scheme shares);

(b) the holders of scheme shares will be issued with new PGF shares as consideration for the transfer of their scheme shares to PGF;

(c) the number of new PGF shares proposed to be exchanged for each scheme share will be equal to PAF’s after-tax net tangible assets (before deferred tax assets) per share (PAF NTA) divided by PGF’s after-tax net tangible assets (before deferred tax assets) per share (PGF NTA), calculated in a manner consistent with that published by those companies in monthly ASX NTA announcements (the exchange ratio); and

(d) the date for determining the exchange ratio will be the date of court approval of the scheme, which will have the effect that any changes to the PAF NTA or PGF NTA prior to court approval will be taken into account in the exchange ratio.

29 The exchange ratio is expected to result in after-tax NTA per share neutrality for both PGF and PAF when comparing the after-tax NTAs immediately before and after the calculation date, and therefore not to be to the benefit or detriment of shareholders of either company on an after-tax NTA basis.

30 As a result of the scheme and PGF’s existing shareholding in PAF, PGF will own 100% of the issued shares in PAF.

31 Let me elaborate further on some aspects concerning the scheme consideration.

32 The scheme provides that on the implementation date, subject to the provision of the scheme consideration in the manner contemplated by the scheme, all of the scheme shares will be transferred to PGF without the need for any further act by any scheme shareholder by PAF effecting a valid transfer or transfers of the scheme shares to PGF. The scheme provides that, on the implementation date, as consideration for the transfer to PGF of each scheme share PGF will issue to each scheme shareholder other than an ineligible foreign PAF shareholder, for each scheme share, that number of new PGF shares determined by the exchange ratio.

33 Up until the calculation date, the PAF NTA and PGF NTA are subject to change, including as a result of investment and market performance pursuant to the usual business operations of PAF and PGF. Any relative change between these two NTAs will have the effect of changing the value of the scheme consideration. Accordingly, the exact number of new PGF shares to be issued to each scheme shareholder will not be known until the scheme consideration is calculated.

34 Under the scheme implementation deed, PAF must procure that the PAF NTA is calculated and delivered to PGF within two business days of the calculation date with sufficient supporting information to permit PGF and its auditor to review and confirm the calculation. PGF has agreed to confirm in writing the PAF NTA within one business day of receipt of PAF’s calculation of the PAF NTA. Further, PGF must procure that the PGF NTA is calculated and delivered to PAF within two business days of the calculation date with sufficient supporting information to permit PAF and its auditor to review and confirm the calculation. PAF has agreed to confirm in writing the PGF NTA within one business day of receipt of PGF’s calculation of the PGF NTA. Further, if PGF and PAF cannot agree to the calculation of the PAF NTA and/or the PGF NTA within three business days, then the calculation of the relevant NTA must be referred immediately to the auditor of the party whose NTA is the subject of the calculation, to provide certification of the relevant NTA amount.

35 Following the NTA review and confirmation process outlined above, PAF will announce the scheme consideration, being based on the exchange ratio for each new PGF share, to the ASX. The new PGF shares are expected to commence trading on the ASX, initially on a deferred settlement basis from the business day after the effective date and, by the business day after the implementation date, on a normal settlement basis.

36 Let me say something further concerning ineligible foreign shareholders. The scheme provides that on the implementation date, as consideration for the transfer to PGF of each scheme share by an ineligible foreign PAF shareholder, PGF will issue to the nominee such number of new PGF shares to which the ineligible foreign PAF shareholder would have been entitled as scheme consideration if they were an eligible scheme shareholder. The scheme provides that no more than 20 business days after the implementation date, the nominee will sell on the ASX the new PGF shares issued to it in respect of ineligible foreign PAF shareholders, and remit the proceeds of the sale to PGF. Further, after the last sale of new PGF shares, PGF will pay to each ineligible foreign PAF shareholder their entitlement from the net proceeds of sale. The sale proceeds net of proportional fees and costs such as brokerage, taxes and charges will be paid to each ineligible foreign PAF shareholder by either sending, or procuring the dispatch, to that ineligible foreign PAFs shareholder by prepaid post to that ineligible foreign PAF shareholder’s registered address at the record date, a cheque in the name of that ineligible foreign PAF shareholder or making a deposit in an account with any authorised deposit taking institution in Australia notified by that ineligible foreign PAF shareholder to PGF or the PAF share registry and recorded in or for the purposes of the PAF register at the record date.

37 Let me say something about performance risk. Although the scheme provides that PGF is to issue or procure the issue of the scheme consideration, PGF is not a party to the scheme. But relevant provisions of the scheme implementation deed and the scheme protect against performance risk. Further, PGF has executed a deed poll under which it covenants in favour of scheme shareholders, subject to the scheme becoming effective, to perform the actions attributable to PGF under the proposed scheme as if it was a party to the scheme, including the obligation of PGF to issue the scheme consideration to eligible scheme shareholders (or to the sale agent in respect of ineligible foreign PAF shareholders) on the implementation date. This is, in my view, adequate to address any such perceived risk.

38 Finally, there are a number of conditions precedent to the scheme implementation deed and to the scheme, but I need not elaborate on these.

Should the scheme meeting be convened?

39 The principles which apply at this first stage of the scheme of arrangement procedure are well-known. As I have said on more than one occasion, my function on an application to order the convening of a meeting is supervisory. At this stage I should generally confine myself to ensuring that certain procedural and substantive requirements have been met including dealing with adequate disclosure, but with limited consideration of issues of fairness. But having said that, it is appropriate to consider the merits or fairness of a proposed scheme at the convening hearing if the issue is such as would unquestionably lead to a refusal to approve a proposed scheme at the approval hearing, that is, the proposed scheme appears now to be on its face “so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further” (Re Foundation Healthcare Ltd (2002) 42 ACSR 252 at [44] per French J).

40 Clearly, my role is not to usurp the shareholders’ decision whether to agree to a scheme by attempting to intrude my own commercial judgment. The question whether to accept particular consideration for shares is a commercial matter for the members to assess, and they ought not to be prevented from having the opportunity to do so provided that I am satisfied that they are acting on sufficient information and with time to consider what they are voting on. If the arrangement is one that seems fit for consideration by the meeting of members and is a commercial proposition likely to gain my approval if passed by the requisite majorities, then orders should be made to convene the meeting.

41 In summary, my task is to assess, first, whether the statutory prerequisites to the making of orders convening a meeting have been met and, second, whether it is appropriate for me to exercise my discretion in favour of making those orders.

42 Now I am satisfied that all relevant statutory prerequisites have been satisfied in this case. Accordingly my discretion to make the convening orders is therefore enlivened.

43 The relevant discretionary considerations involve two main questions being, first, whether the scheme is fit for consideration by the members, that is, whether the scheme is of such a nature and cast in such terms that, if agreed to at the scheme meeting, I would be likely to approve the scheme at the second court hearing and, second, whether the members are to be properly informed as to the nature of the scheme.

44 In my view the scheme is fit for consideration by PAF’s members. In particular, there is no issue arising from the scheme which would unquestionably lead to a refusal by me to approve the scheme at the approval hearing. Furthermore, it cannot be said that the scheme is on its face unfair or otherwise inappropriate such that I should not order the convening of the scheme meeting.

45 Let me now in the context of addressing this first question address some specific matters.

46 First, I should say something concerning the scheme consideration.

47 As I have said, the calculation date for determining the exchange ratio will be the date the Court approves the scheme. This will have the effect that any changes to the PAF NTA or PGF NTA prior to my approval will be taken into account in the determination of the exchange ratio. It will also have the effect that PAF shareholders will not know the value of the scheme consideration at the time of the scheme meeting. But PAF shareholders will know the formula for the calculation of the exchange ratio at the date of the scheme meeting. Moreover, the fact that the value of the scheme consideration will not be known at the time of the scheme meeting has been disclosed in the scheme booklet. For example, in the Chairman’s letter on page 9, the following statement appears:

The value of the Scheme Consideration will not be known at the time of the Scheme Meeting on 13 December 2021. The value of the Scheme Consideration will be calculated as at the Calculation Date (expected to be 17 December 2021) and is expected to be announced to the ASX around 21 December 2021. The Scheme Consideration will be calculated using the formulas disclosed in this Explanatory Memorandum, and illustrative worked examples have been provided (see section 3.4.3) to assist PAF Shareholders. PAF will keep PAF Shareholders fully informed of the NTA of each of PAF and PGF via weekly Monday ASX announcements through to the Calculation Date. PAF will ensure that an ASX announcement of the NTA of each of PAF and PGF is made on the morning of and prior to the Scheme Meeting on 13 December 2021.

48 Now variable consideration mechanisms of this type have been accepted in previous schemes involving listed investment companies. Let me elaborate on one example.

49 In Re Templeton Global Growth Fund Limited [2021] NSWSC 1169, the plaintiff (TGG), a listed investment company, proposed a scheme pursuant to which all of the shares in TGG would be acquired by WAM Global Ltd, a listed investment company. The scheme provided that WAM Global would acquire the TGG shares in consideration for the issue of ordinary shares and options in WAM Global based on the relative NTA per share of TGG and WAM Global before deferred taxes. In parallel, TGG would undertake an equal access buy-back of TGG shares which would enable TGG shareholders to elect to sell into the buy-back for cash equal to the NTA per TGG share after current and deferred taxes and transaction costs. TGG shareholders could therefore either accept the buy-back offer and receive cash from TGG for their TGG shares or they could elect not to accept the buy-back offer and receive the scrip consideration under the proposed scheme. The NTA backings of TGG and WAM Global used to determine the scrip consideration and cash consideration were to be calculated as at the day after the scheme meeting. TGG shareholders would therefore not know the exact amount of the scrip consideration or cash consideration they would receive under the scheme and buy-back as at the date of the scheme meeting, although they would know the means by which it was calculated.

50 Further, in Re Templeton, the reasons for adopting the variable consideration formula included: first, WAM Global and TGG were listed investment companies whose assets comprised liquid securities traded on stock exchanges; second, their respective NTA varied daily with the listed prices of the securities held in their respective investment portfolios; and third, setting the valuation and exchange parameters in proximity to implementation of the transaction provided fair recognition of the current value of TGG and WAM Global shares at implementation and avoided the prospect that TGG shareholders would be disadvantaged by a favourable movement in the value of TGG’s investment portfolio relative to the performance of WAM Global’s portfolio between a historical date and implementation of the scheme.

51 Now the reasons for adopting the variable consideration formula in the scheme before me mirror those just noted. As I have said, PAF and PGF are listed investment companies whose assets comprise liquid securities traded on stock exchanges, and their respective NTA varies daily with the listed prices of the securities held in their respective investment portfolios. Further, setting the valuation and exchange parameters in close proximity to the implementation of the transaction provides fair recognition of the current value of PAF and PFG shares at implementation and avoids the prospect that PAF shareholders would be disadvantaged by a relevant movement in the value of PAF’s investment portfolio relative to the performance of PGF’s portfolio between an historical date and the date of approval of the scheme. Further, if the exchange ratio was to be fixed at an earlier date and PGF’s NTA was to relevantly change prior to implementation, this may expose PAF shareholders to a risk of being disadvantaged.

52 Now after considering the reasons for adopting the variable consideration formula in Re Templeton, Black J made various observations (at [18]) and then accepted that disclosure was sufficient to address the issue. His Honour noted that (at [19]):

It seems to me that TGG shareholders are properly informed in the explanatory memorandum of the methodology by which the amount they will receive by shares or options in WAM Global under the scheme, or cash under the buy-back is determined, and its relationship with the NTA of TGG and WAM Global as applicable, and as to the range of possible outcomes by the illustrations in the explanatory memorandum. If any issue then arises as to the implementation of that formula, including by any unexpected market developments which particularly affect either TGG or WAM Global, that is properly addressed at the second scheme hearing.

53 I have adopted the same approach in the present case. In particular, there is nothing inherently unfair in the consideration being determined based on the most up-to-date NTA of both PAF and PFG, and PAF shareholders will have little difficulty in comprehending the conceptual basis for the determination of the scheme consideration. Further, there is prominent disclosure of this matter in the scheme booklet.

54 Second, I have no difficulty with the exclusivity provisions, the break fee or the shareholder warranties. Now I note that WAM has raised the question of the break fee with the Takeovers Panel. That is a matter for it. I need say nothing further.

55 Third, let me say something about class issues and the tagging of votes.

56 As I have noted, one of the directors of PAF, Mr Skilbeck, holds 10,000 shares in PAF, representing approximately 0.02% of the total issued share capital of PAF. Mr Skilbeck is also a director of PGF, however he is not involved in PGF’s decision-making concerning the scheme and is on a leave of absence from the PGF Board for the duration of the transaction. Mr Skilbeck holds 314,123 PGF shares, representing approximately 0.08% of the total issued share capital of PGF. In addition, one of the directors of PGF, Mr Spork, holds 52,630 PAF shares, representing approximately 0.09% of the total issued share capital of PAF. Mr Spork is not a director of PAF. Mr Spork holds 41,666 PGF shares, representing approximately 0.01% of the total issued share capital of PGF.

57 Now in this context, although the Act does not prohibit scheme proponents or their associates who hold target shares from voting in relation to an acquisition, it is appropriate to consider whether it is necessary for Mr Skilbeck or Mr Spork to be placed in a separate class for the purposes of voting their PAF shares at the scheme meeting. It is also appropriate to consider whether, if there are no separate classes, the votes of any directors should be tagged.

58 In my view, no separate class meetings are appropriate or necessary in respect of Mr Skilbeck or Mr Spork and their votes do not need to be tagged.

59 Even where certain members may have extraneous interests in the outcome of a scheme of arrangement, this in itself is not a reason for placing those members in a separate class for voting purposes. However, the Court is entitled to take the existence of any such interests into account in the exercise of its general fairness discretion in deciding whether to approve a scheme. And in a clear case where the Court is of the view that the existence of such extraneous interests means that the outcome of the vote does not fairly represent the views of the class, the Court will be entitled to discount or even disregard those votes.

60 In the present case, no such concerns arise in relation to Mr Skilbeck or Mr Spork. Neither Mr Skilbeck nor Mr Spork could properly be said to have extraneous or divergent interests in the outcome of the scheme, including that neither of them is to receive a material collateral benefit from the bidder if the scheme proceeds.

61 Further and generally speaking, a person should not be excluded from a class merely because they hold equity securities in both the bidder and the target. So, where a director of a bidder holds shares in the target, provided that the director is to be treated the same as every other target member under the scheme, which is the case here in respect of Mr Skilbeck and Mr Spork, that director is not required to be placed in a separate class for voting purposes.

62 Further, the fact that the relevant member is a director of the bidder and therefore an associate of the bidder does not make it appropriate or necessary for that member to vote in a separate class.

63 In my view no separate class should be constituted for Mr Skilbeck and Mr Spork. Further, particularly in light of Mr Skilbeck’s and Mr Spork’s small holdings of PAF shares, it is not necessary to tag their votes at the scheme meeting.

64 Let me now deal with the position of Mr Moore and his associates. But before doing so I need to elaborate on some arguments of WAM and some further background.

65 WAM says that it appears that PAF and PGF have organised their affairs in a way designed to affect voting on the proposed scheme in a manner potentially adverse to the interests of ordinary PAF shareholders. The following matters are pointed to.

66 On 15 September 2021, PAF and PGF announced that they had entered into a scheme implementation deed. As I have indicated, PAF and PGF are both managed by PM Manager. At that time PAF and PGF each lodged an ASX substantial holding notice purporting to have split their voting power by removing both PM Manager’s relevant interest in PGF’s PAF shares, as well as the association between PGF and PM Manager. This was said to be achieved by PGF revoking PM Manager’s control over PGF’s PAF shares by the revocation of authority I have referred to earlier.

67 On 28 September 2021, WAM announced its intention to make an off market takeover bid for all of the shares in PAF.

68 On 1 October 2021, PGF lodged an updated substantial holding notice which provided additional disclosure.

69 On 29 September and 13 October 2021, PM Manager’s substantial holding notices disclosed acquisitions of PAF shares. Currently, PGF holds 19.93% and it is said that PM Manager holds 13.09% “voting power” in PAF, with, so it is said, combined voting power of approximately 33%. It is said that this is about a 6% increase in their combined voting power of 26.86% held six months previously.

70 On 14 October 2021, WAM lodged its bidder’s statement relating to its bid.

71 WAM says that it is at least arguable, particularly given the timing of the revocation and the September notices, that the revocation was undertaken to allow PM Manager to acquire more PAF shares, as well as to potentially allow PM Manager to vote in the scheme in the same class as other shareholders.

72 WAM says that despite the revocation, PGF and PM Manager continue to be associates for the purposes of the scheme. Indeed, WAM says that the scheme makes PGF’s and PM Manager’s association even more apparent.

73 WAM says that the building up of 26.86% voting power in a target, then artificially splitting that holding between the company and the manager to allow further acquisitions, is a matter that ought be of concern. It is said that the interests of PM Manager and its associates in the scheme’s outcome should be properly disclosed to shareholders.

74 More particularly, WAM says that I should be concerned to ensure that assent to the scheme should come from each distinct class within PAF’s members in circumstances where it is unlikely that PGF and PM Manager could be said to have a community of interest with ordinary shareholders in relation to the scheme.

75 WAM has also drawn my attention to s 411(17), particularly in the context of the on-market acquisitions by PM Manager and its associates as disclosed to the market on 28 September 2021 and 13 October 2021 and the deal protection mechanism afforded by the scheme’s break fee.

76 Now I should note that the concerns identified by WAM relate to alleged voting power, relevant interests and associations, which only arise as a consequence of various provisions in the Act which apply to determining whether an entity has contravened the 20% rule. In this context, in its application to the Takeovers Panel WAM alleges a contravention of s 606 by PGF and PM Manager in having acquired more PAF shares, as well as alleging that the basis for the revocation of authority was to allow such further acquisitions. Of course, the Panel is the appropriate forum for raising these matters.

77 But for my context, WAM’s submissions conflate voting power calculated in accordance with ss 608 and 610 of the Act for the purposes of assessing compliance with the 20% rule in s 606, with votes to be cast at the scheme meeting. WAM says that PM Manager holds 13.09% voting power in PAF. But PM Manager’s direct holding in PAF shares is only approximately 0.13%, which has been unchanged since June this year. The reference to 13.09% voting power by WAM is a reference to voting power calculated in accordance with ss 11, 12, 608 and 610 of the Act. But on the evidence before me there is no basis to conclude that PM Manager has or will have the ability to vote shares in PAF at the scheme meeting other than the 0.13% it directly holds.

78 In any event, the key consideration relevant to class and voting issues in the present context is proper disclosure. In that context the following matters should be noted:

(a) PGF’s 19.93% holding in PAF is disclosed in the scheme booklet, where it is also said that PAF will not vote on the scheme at the scheme meeting. Further, PGF’s PAF shares are not scheme shares, and will not participate in the scheme.

(b) Further, the voting power of PAF’s substantial shareholders is disclosed. In this respect the scheme booklet discloses PGF’s voting power in 19.93% of PAF shares and discloses voting power in 13.09% of PAF shares held by Mr Moore, PM Manager and other entities who are associated with Mr Moore. The shares of Mr Moore, PM Manager and other entities who are associated with Mr Moore are scheme shares and will participate in the scheme. Further, the holding of shares in PAF by Mr Moore and entities associated with him is disclosed.

(c) Further, the relevant terms of the PGF investment management agreement are summarised. Moreover the revocation of authority is disclosed. It is stated that:

On 14 September 2021, PGF wrote to PM Capital Limited (in its capacity as Investment Manager of PGF) to formally revoke the authorisation for PM Capital to sell, or vote the PAF Shares that were beneficially held by PGF as at the date of announcement of the Scheme Implementation Deed. Those securities were subsequently moved out of the prime broking custodial account (which is administered on a day-to-day basis by the Investment Manager), and moved into self-custody (which is controlled directly by the PGF Board).

79 It is apparent from this disclosure that PGF’s 19.93% holding in PAF will not be voted by PM Manager. It is also apparent that this holding is controlled directly by the PGF board and PGF has undertaken not to vote this holding at the scheme meeting.

80 So, there is no basis to consider that PM Manager has any right to vote any PAF shares at the scheme meeting other than the 0.13% it holds. Accordingly, WAM’s reference to PM Manager’s 13.09% voting power and its concerns about whether PM Manager proposes to vote on the scheme and on what basis are misplaced.

81 But apart from PM Manager’s 0.13%, the remainder of the 13.09% voting power in PAF disclosed in the most recent substantial holder notice relates to shares held by Horizon Investments Australia Pty Ltd and Roaring Lion Pty Ltd, which are companies that Mr Moore has voting power above 20% or that he controls.

82 Now in relation to Mr Moore and his associates and their holdings in PAF, in my view no separate class needs to be constituted. But it is appropriate to consider whether the votes of any person should be tagged. Should I require tagging of the relevant votes at the present time?

83 Now PAF says that WAM has not made out a case for the tagging of any votes at the scheme meeting. PAF also says that a requirement to tag votes would also mean a delay in shareholders receiving the scheme booklet. In addition, disclosures as to vote tagging in the scheme booklet are likely to create some doubt and uncertainty in the minds of shareholders with respect to the scheme. PAF submits that in the context of a contested takeover and competing offers for PAF, it would not be appropriate to require vote tagging and its consequent disclosure in the scheme booklet without clear justification.

84 Now I note that ASIC has been provided with a copy of WAM’s submissions and its supporting evidence. Subsequently, ASIC sent PAF a letter on the morning of the hearing before me where it stated that it did not propose to appear to make submissions or intervene to oppose the scheme at the first hearing. But ASIC noted:

…pending the outcome of WAM’s application to the Takeovers Panel, ASIC may withhold its statement of ‘no objection’ under s411(17)(b) and make submissions at the second court hearing. ASIC may also seek for the Company to have the votes of relevant parties ‘tagged’ prior to the scheme meeting and a voting report provided to ASIC.

85 In my view, the shares of Mr Moore and his associates, if voted, should be tagged. These shares should be tagged so that if issues arise as to the circumstances of voting of these shares, the effect of the voting of these shares can be assessed by me at the second court hearing. I should direct tagging now, rather than leave the question up in the air to await any later direction by ASIC. Moreover, there is no downside to PAF, particularly as I will not require any alteration to the scheme booklet in this respect.

86 Fourth, the proposed treatment of ineligible foreign shareholders is unremarkable. The proposed treatment of such shareholders under the scheme accords with common practice adopted in schemes where scrip comprises or is a component of the proposed scheme consideration. In particular, the issuing to a sale agent under a scheme of scrip that would otherwise have been issued to ineligible foreign shareholders does not require those shareholders to meet together as a separate class for the purposes of considering the proposed scheme of arrangement. Accordingly, no separate class arises as regards the ineligible foreign shareholders.

87 Fifth, let me say something further about the WAM offer and the disclosures that have been made to PAF’s shareholders.

88 As I have said, on 28 September 2021 WAM announced an intention to make a conditional off-market takeover offer for all of the fully paid ordinary shares in PAF. The WAM offer is subject to a number of defeating conditions. For example, one of those conditions is that the merger of PAF and PGF by way of the scheme does not progress. Another condition is that the pre-tax NTA of PAF not decline by 5% or more below the pre-tax net NTA of PAF of $1.10 per share, announced to the ASX on 27 September 2021. It is also a condition of the WAM offer that if a PAF shareholder accepts the WAM offer, they appoint WAM as their attorney to vote at any PAF shareholder meeting, including the scheme meeting. WAM has also made it clear that should the scheme progress and if WAM is entitled to vote at PAF’s scheme meeting, WAM will vote against any PAF shareholder resolution agreeing to the scheme.

89 Now in the present context, the key consideration with respect to the WAM offer for my purposes is whether PAF shareholders are properly informed as to the comparative advantages and disadvantages of the scheme and the WAM offer so that they can make an informed decision on the scheme. Now in this respect PAF shareholders will have received or will receive the following information at the following times:

(a) On 28 October 2021, WAM sent the bidder’s statement to PAF shareholders which included details in respect of the WAM offer.

(b) On or before 12 November 2021, PAF proposes to send PAF shareholders the scheme booklet. The scheme booklet contains a detailed consideration of the advantages and disadvantages of the scheme, and also sets out information about the WAM offer. Further, the scheme booklet sets out the PAF directors’ recommendation that shareholders vote in favour of the scheme. In addition, the scheme booklet annexes a copy of the independent expert’s report which provides an opinion on whether the scheme is fair and reasonable and in the best interests of PAF shareholders and also considers the WAM offer and compares it to the scheme.

(c) Further, by 12 November 2021 PAF must send a target statement to its shareholders in relation to the WAM offer. Section 633(1) item 11 requires PAF to send its target statement to its shareholders no later than 15 days after it received notice from WAM that WAM had sent offers to all PAF shareholders, which notice PAF received on 28 October 2021. The target statement must include all of the information that PAF shareholders and their professional advisers would reasonably require to make an informed assessment whether to accept the offer under the bid, and a statement by each director of PAF recommending that offers under the WAM offer be accepted or not accepted, and giving reasons for the recommendation, or giving reasons why a recommendation is not made (see ss 638(1) and (3)).

90 Now the WAM offer opened for acceptance on 28 October 2021, and is scheduled to close at 7pm on 29 November 2021. Under the terms of the WAM offer, PAF shareholders who accept the offer will receive the consideration under the offer within one month of the later of the date they accept the offer and the date the offer becomes unconditional. In any event, accepting shareholders will receive the bid consideration within 21 days after the end of the offer period, assuming that all defeating conditions are satisfied or waived, that is, by 20 December 2021.

91 Now the scheme meeting is to be held on 13 December 2021, and proxies are to be returned by 11 December 2021. And implementation of the scheme and the issue of the scheme consideration is to take place on 30 December 2021.

92 Accordingly, at the times at which PAF shareholders must make a decision whether or not to accept the WAM bid or to agree to the scheme, such shareholders will be in receipt of all material information and recommendations from the PAF directors in relation to each proposal, as well as a comparative evaluation by an independent expert. So, the circumstances of the WAM offer do not provide a reason for me to decline to make an order that PAF convene the scheme meeting. Indeed, to the contrary. PAF shareholders ought to be given the opportunity to exercise an informed choice between the competing offers, including by voting at the scheme meeting.

93 Now I should also say at this point that the proceedings in the Takeovers Panel as a result of WAM’s application do not alter this analysis. The final orders sought by WAM in those administrative proceedings are that the scheme implementation deed be amended to remove the break fee and that all PAF shares acquired by PM Manager and its associates on or after 29 September 2021 be vested in ASIC. Similarly, the application made to the Takeovers Panel by PGF does not alter my analysis; the relief sought by PGF before the panel is an order that WAM provide a replacement bidder’s statement to correct various deficiencies.

94 Let me deal with one other matter relevant to the scheme implementation deed. In its market announcements, WAM has stated that the WAM offer is a superior proposal to the scheme. However, the PAF directors and the independent expert have expressed the contrary view, namely, that the WAM offer is not a “Superior Proposal” as defined in the scheme implementation deed and is less attractive than the scheme.

95 Now WAM’s stated view that the WAM offer is a superior proposal to the scheme was based upon the implied value of the scheme consideration if the exchange ratio were calculated on 24 September 2021 and the PGF share price on 27 September 2021. But the calculation date for determining the exchange ratio will be the date I approve the scheme, which will have the effect that any changes to the PAF NTA or PGF NTA prior to court approval will be taken into account in the determination of the exchange ratio. Further, WAM’s stated view was based on the implied value of the offer having regard to WAM’s share price as at 27 September 2021. But the implied value of the WAM offer will depend upon the WAM share price at the date the bid consideration is provided. Further, the future share price of WAM as well as the respective future NTAs of PGF and PAF will each have a bearing on the relativities of the competing proposals.

96 Now the PAF board committee has considered the WAM offer and its potential advantages to PAF shareholders, in the context of the existing agreement with PGF to propose the scheme to PAF shareholders and to implement the scheme subject to certain conditions. The result of this evaluation is that the PAF directors do not believe that the WAM offer as matters presently stand is a better offer or superior proposal than the scheme.

97 I need say nothing further for the moment.

98 Let me now deal with other aspects concerning the adequacy of the information to be provided to shareholders. I am satisfied concerning compliance with section 412(1) of the Act and relevant provisions of the Corporations Regulations 2001 (Cth). Further, the information in the scheme booklet has been subject to thorough verification processes.

99 Further, it is necessary that the scheme booklet be registered by ASIC before being sent to PAF shareholders. Before registering the scheme booklet, ASIC must conclude that it appears to comply with the requirements of the Act, and must form the opinion that the scheme booklet does not contain any matter that is false in a material particular or materially misleading in the form and context where it appears. This provides further assurance as to the satisfaction of the relevant disclosure requirements. Further, ASIC’s comments have been addressed in the draft scheme booklet, and ASIC has stated that it has no further comments. In this context and given the registration requirement, I do not propose to separately approve the explanatory statement in the scheme booklet.

100 Further, PAF proposes to provide the scheme booklet to shareholders electronically, and to conduct the scheme meeting via an online platform. This is justified and appropriate.

101 Finally, ASIC’s letter of intent dated 4 November 2021 concerning s 411(17)(b) is in a satisfactory form.

Conclusion

102 I am satisfied that the scheme is of such a nature and cast in such terms that, if it achieves the statutory majorities at the scheme meeting, I would be likely to approve it. It is therefore appropriate to make the orders sought convening the scheme meeting.

103 For the foregoing reasons I have made the orders sought.

I certify that the preceding one hundred and three (103) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Beach. |