Federal Court of Australia

Huon Aquaculture Group Limited, in the matter of Huon Aquaculture Group Limited [2021] FCA 1170

ORDERS

HUON AQUACULTURE GROUP LIMITED Plaintiff | ||

DATE OF ORDER: | 22 September 2021 |

THE COURT ORDERS THAT:

1. Pursuant to section 411(1) of the Corporations Act 2001 (Cth) (Act), the plaintiff, Huon Aquaculture Group Limited (ACN 114 456 781) (Huon), convene and hold:

(a) a meeting of its ordinary shareholders (Huon Shareholders) other than Surveyors Investments Pty Ltd (ACN 602 004 179) (the Excluded Shareholder):

(i) for the purposes of considering and, if thought fit, agreeing (with or without any alterations or conditions) to a scheme of arrangement (Structure A Scheme), being the scheme substantially in the form contained at Annexure A to these orders proposed to be made between Huon and its ordinary shareholders (other than the Excluded Shareholder); and

(ii) to be held at 10:00 am (Hobart time) on Friday, 29 October 2021 and be conducted electronically through an online platform (which is to be accessed in accordance with the instructions included in the Notice of Primary Scheme Meeting which is set out in Appendix F to the Transaction Booklet (Notice of Structure A Scheme Meeting) and is to be sent to Huon shareholders in accordance with Order 2 below),

(Structure A Scheme Meeting); and

(b) a meeting of its ordinary shareholders:

(i) for the purposes of considering and, if thought fit, agreeing (with or without any alterations or conditions) to a scheme of arrangement (Structure B Scheme), being the scheme substantially in the form contained at Annexure B to these orders proposed to be made between Huon and its ordinary shareholders; and

(ii) to be held at 10:00 am (Hobart time), or as soon as reasonably practicable after the conclusion or adjournment of the Structure A Scheme Meeting (whichever time is later) on Friday, 29 October 2021 and be conducted electronically through an online platform (which is to be accessed in accordance with the instructions included in the Notice of Secondary Scheme Meeting which is set out in Appendix G to the Transaction Booklet (Notice of Structure B Scheme Meeting) and is to be sent to Huon shareholders in accordance with Order 2 below),

(Structure B Scheme Meeting),

(each a Scheme Meeting and together, the Scheme Meetings).

2. The Scheme Meetings be convened by sending on or before 29 September 2021:

(a) in the case of Huon Shareholders who have elected to receive electronic shareholder communications (Email Shareholders), an email substantially in the form at Tab 21 of Exhibit “TCH-1” to the affidavit of Thomas Cleveland Haselgrove dated 21 September 2021 (Haselgrove Affidavit), which includes access by embedded links to the following:

(i) an electronic copy of a document substantially in the form of the Transaction Booklet, a draft of which is at Tab 32 of Exhibit “JRB-2” to the affidavit of John Richard Brewster dated 22 September 2021 (Second Brewster Affidavit) (save for the reference to “Thursday, 23 September 2021” on page 25 of that draft being amended to “Tuesday, 28 September 2021”, the references to “23 September 2021” on page 116 of that draft being amended to “28 September 2021”, the deletion of paragraph (iv) in section 12.12(a) on page 152, and the reference to “clause 5.5(b)(a)” on page 281 of that draft being amended to “clause 5.5(a)”), which contains, among other things, the Notice of Structure A Scheme Meeting and the Notice of Structure B Scheme Meeting;

(ii) a proxy form substantially in the form at Tab 14 of Exhibit “TCH-1” to the Haselgrove Affidavit (Proxy Form); and

(iii) an online portal or website that is accessible by Email Shareholders and which enables Email Shareholders to lodge their proxy for the Scheme Meetings and voting instructions online; and

(b) in the case of Email Shareholders a Proxy Form and a reply paid envelope for the return of the Proxy Form by post; and

(c) in the case of Huon Shareholders who are not Email Shareholders (Postal Shareholders) the following documents by post:

(i) a document substantially in the form of the Transaction Booklet, a draft of which is at Tab 32 of Exhibit “JRB-2” to the Second Brewster Affidavit (save for the reference to “Thursday, 23 September 2021” on page 25 of that draft being amended to “Tuesday, 28 September 2021”, the references to “23 September 2021” on page 116 of that draft being amended to “28 September 2021”, the deletion of paragraph (iv) in section 12.12(a) on page 152, and the reference to “clause 5.5(b)(a)” on page 281 of that draft being amended to “clause 5.5(a)”), which contains, among other things, the Notice of Structure A Scheme Meeting and the Notice of Structure B Scheme Meeting; and

(ii) a Proxy Form and a reply paid envelope for the return of the Proxy Form.

3. If it comes to the attention of the Plaintiff that any email dispatched to Email Shareholders in accordance with Order 2(a) above has returned an undeliverable or undelivered receipt for an Email Shareholder’s nominated email address, then the Plaintiff shall dispatch to that Email Shareholder within a reasonable time thereafter the specified documents in accordance with Order 2(b) above.

4. Subject to these Orders and pursuant to sections 411(1) and 1319 of the Act:

(a) the Scheme Meetings are to be convened using the notices of meeting substantially in the form of the Notice of Structure A Scheme Meeting and substantially in the form of the Notice of Structure B Scheme Meeting without specifying a physical location for the meetings;

(b) the Scheme Meetings are to be held and conducted electronically, without any physical meeting of Huon Shareholders being held, pursuant to the arrangements for attending, participating and voting described in the Notice of Structure A Scheme Meeting and the Notice of Structure B Scheme Meeting respectively relating to the appointment and revocation of proxy and attorney appointments and in respect of the effect of a Huon Shareholder’s attendance at a Scheme Meeting on a proxy or attorney appointment by that Huon Shareholder;

(c) at the Structure A Scheme Meeting, Huon Shareholders other than the Excluded Shareholder are to be permitted to submit questions, and at the Structure B Scheme Meeting, Huon Shareholders are to be permitted to submit questions, in the manner provided on the website, subject to the functions and powers of the Chair under the Plaintiff’s Constitution as applicable and the general law;

(d) notwithstanding clause 39(b) of the Plaintiff’s Constitution and section 249Y(3) of the Act, the appointment of a proxy in respect of the Structure A Scheme Meeting shall not be revoked or suspended by the appointing Huon Shareholder attending and taking part in the Structure A Scheme Meeting, but if the appointing Huon Shareholder votes on a resolution at the Structure A Scheme Meeting, the proxy is not entitled to vote as the appointing Huon Shareholder’s proxy on that resolution and any such vote by the proxy must not be counted in the results of the relevant poll;

(e) notwithstanding clause 39(b) of the Plaintiff’s Constitution and section 249Y(3) of the Act, the appointment of a proxy in respect of the Structure B Scheme Meeting shall not be revoked or suspended by the appointing Huon Shareholder attending and taking part in the Structure B Scheme Meeting, but if the appointing Huon Shareholder votes on a resolution at the Structure B Scheme Meeting, the proxy is not entitled to vote as the appointing Huon Shareholder’s proxy on that resolution and any such vote by the proxy must not be counted in the results of the relevant poll;

5. Except to the extent addressed by these Orders, the Scheme Meetings be:

(a) convened, held and conducted in accordance with the provisions of Part 2G.2 of the Act that apply to members of the company, and the provisions of the Plaintiff’s Constitution as applicable that are not inconsistent with these Orders and Part 2G.2; and

(b) convened, held and conducted as if rule 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) (Rules) does not apply.

6. Voting on the resolutions to approve the Structure A Scheme and Structure B Scheme is to be conducted by way of a poll.

7. The Proxy Form will be valid and effective if, and only if, it is completed and delivered in accordance with its terms by is 10.00am (Hobart time) on 27 October 2021.

8. Mr Neil Alexander Kearney, or failing him, Mr Kevin Anthony Dynon be the Chairperson of the Scheme Meetings.

9. The Chairperson of the Scheme Meetings shall have the power to adjourn the Scheme Meetings to such time, date and place as he considers appropriate.

10. Compliance with rule 3.4 and Form 6 of the Rules is dispensed with.

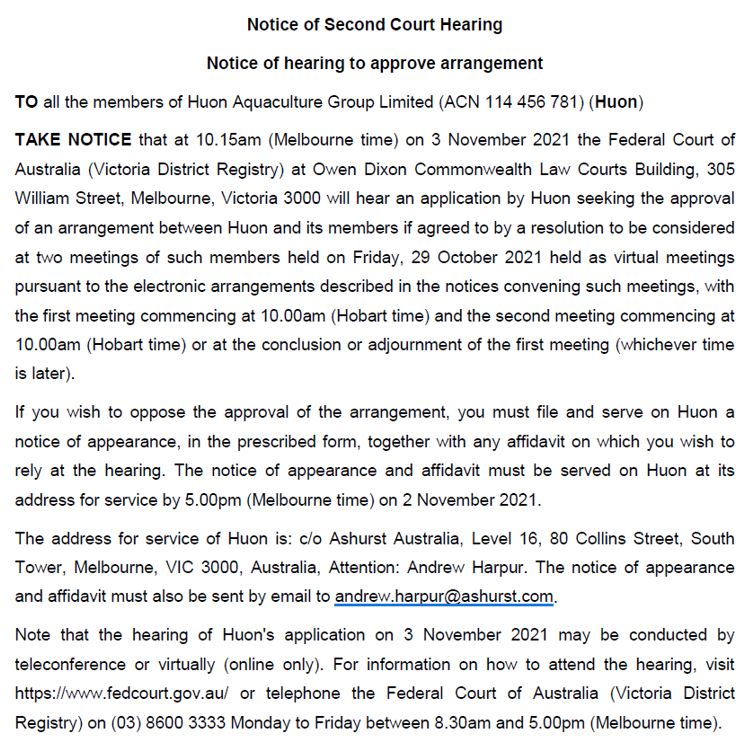

11. The Plaintiffs publish in The Australian newspaper once on or before 28 October 2021 a notice of hearing substantially in the form of Annexure C to these Orders.

12. The further hearing of the Originating Process in respect of the Plaintiff’s application is adjourned to a hearing before the Honourable Justice O’Callaghan on 3 November 2021 at 10.15am (Melbourne time) or as soon thereafter as the business of the Court allows.

13. There be liberty to apply.

14. Pursuant to rule 39.34 of the Federal Court Rules 2011 (Cth), these orders be entered forthwith.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Annexure A

Structure A Scheme

Annexure B

Structure B Scheme

Annexure C

O’CALLAGHAN J:

1 I made the orders set out above at the hearing held on 22 September 2021. These are my reasons.

2 Huon Aquaculture Group Limited (Huon) is a publicly listed company which operates a vertically integrated salmon production business. Its operations span all aspects of the supply chain from hatcheries and marine farming to harvesting and processing, as well as sales and marketing. Huon’s marine farms, and its registered office, are located in Tasmania.

3 By an application dated 6 September 2021, Huon sought orders pursuant to s 411(1) of the Corporations Act 2001 (Cth) (Act) convening two separate meetings of Huon shareholders concerning two alternative schemes of arrangement that are proposed concurrently.

4 The implementation of either of the two alternative schemes of arrangement will result in the acquisition by JBS Aquaculture Pty Ltd (JBS) of all of the ordinary shares in Huon (Huon Shares) for $3.85 per Huon Share (less the amount of any special dividend declared and paid by Huon). JBS is the entity that has been nominated by JBS Australia Pty Ltd (JBS Australia) under the share acquisition implementation deed (referred to below) to acquire the Huon Shares.

5 The reasons why two alternative and concurrent schemes of arrangement and a simultaneous takeover bid are being proposed are set out in the 21 September affidavit of Mr Thomas Haselgrove, the Company Secretary and CFO of Huon.

6 As Mr Haselgrove deposed, in February 2021 the Huon board announced a strategic review to assess potential transactions in light of unsolicited approaches it had received. Huon approached a number of parties as part of that review, including JBS Australia, Tattarang Agrifood Pty Ltd (Tattarang), and others, to explore the possibility of a range of alternative transactions. Indicative offers were received, including a non-binding and conditional offer from Tattarang. The final offer by JBS Australia of $3.85 per Huon Share was considered by the board to be the most attractive proposal.

7 Huon’s managing director and CEO (Mr Peter Bender) and his family own or control some 52.68% of the issued shares in Huon. This shareholding is held as to 40.53% by Surveyors Investments Pty Ltd (Surveyors), of which Mr Bender is the sole director and shareholder, with the remaining (rounded up) 12.15% of Huon Shares also controlled by the Bender family as follows:

(a) 12.07% held by Mr Bender in a personal capacity;

(b) 0.005% held by Mrs Frances Bender, Huon’s Executive Director, in a personal capacity;

(c) 0.05% held by Mr and Mrs Bender as custodians for the PJ and FR Bender Family Trust; and

(d) 0.02% held by P & F Bender Super Pty Ltd as custodian for the P & F Bender Family Super Fund.

8 Accordingly, a change of control transaction via a scheme of arrangement cannot proceed without the support of Mr Bender.

9 The draft acquisition booklet exhibited to Mr Haselgrove’s affidavit summarised the three proposed transactions as follows:

Under the Implementation Deed, Huon has agreed to propose a:

Primary Scheme, under which JBS would acquire the Huon Shares held by Huon Shareholders (other than the Huon Shares held by Surveyors) under the Primary Scheme for the $3.85 Scheme Consideration. Under the associated Surveyors acquisition, JBS would acquire all Surveyors Shares in Surveyors pursuant to the Share Sale Agreement. Surveyors hold approximately 40.53% of the Huon Shares. It is a condition of the Primary Scheme that the Surveyors Acquisition Resolution is passed at the Annual General Meeting[.]

… Secondary Scheme, under which JBS would acquire all Huon Shares held by Huon Shareholders (including the Huon Shares held by Surveyors) under the Secondary Scheme for the $3.85 Scheme Consideration.

… Takeover Bid, under which JBS has agreed to make Takeover Offers for the $3.85 Takeover Offer Consideration Price subject to a 50.1% minimum acceptance condition and other conditions similar to the conditions of the Schemes, in parallel but not in substitution to the Schemes.

10 The draft booklet also explained the background to these proposed transactions:

The proposal received from JBS Australia was to acquire all Huon shares at $3.85 per share on the basis that the Bender family sign a non-compete undertaking in favour of JBS. The Bender family confirmed they were prepared to provide these undertakings if the Primary Scheme structure involving the separate Surveyors Acquisition was put forward. Structuring the transaction in this way provides financial advantages to Mr Bender. Under the Primary Scheme transaction which involves the separate but related Surveyors Acquisition, Mr Bender will receive the proceeds from the sale of his shares in Surveyors personally [through] the sale of his shares in Surveyors to JBS under the Surveyors Acquisition. Conversely, under the Secondary Scheme, Surveyors will receive the proceeds from the sale of its Huon Shares as the Huon Shares held by Surveyors will be acquired by JBS under the terms of the Secondary Scheme. Mr Bender has determined that the flexibility of receiving the proceeds personally is preferable to him from a long term estate planning perspective.

Further, different capital gains consequences arise from the two alternatives. If Mr Bender receives proceeds personally from the sale of shares in Surveyors he will be entitled to a capital gains discount through the first 50% of capital gains being disregarded and will be subject to capital gains on the balance at the personal marginal rate. If Surveyors receives the proceeds from the sale of its Huon Shares it will be subject to capital gains on the full amount but at the corporate rate.

Negotiations with JBS Australia took place after Tattarang had acquired an approximate 7.33% interest in Huon but had not made a proposal to acquire Huon. In these circumstances, JBS Australia was only willing to agree to the Primary Scheme if the Board also proposed and supported a Scheme that would permit all Huon Shareholders to vote on the transaction. The Secondary Scheme provided this security. The Bender family agreed to the Secondary Scheme as an alternative even though Mr Bender would not receive the financial advantages referred to above in order to secure the offer price of $3.85 for Huon Shareholders.

On 10 August 2021, shortly after an implementation deed relating to the Schemes had been executed, Tattarang announced that it had increased its voting power in Huon to approximately 18.5%. This means Tattarang and a relatively small number of other shareholders might be able to block both of the Schemes. Given the offers received following the extensive strategic review process, the Huon Directors were concerned that this outcome might deprive Huon Shareholders of the opportunity to receive $3.85 for each Huon Share.

It was in this context that JBS proposed the Takeover Offers to Huon. JBS was prepared to make the Takeover Offers if the Bender family provided an unconditional commitment in relation to 19.9% of Huon’s Shares (Pre-Bid Acceptance) and an expanded non-compete undertaking. The Bender family accepted the terms of the pre-bid acceptance in order that all Huon Shareholders can receive a more flexible proposal, even though they risk financial detriment as compared to other Huon shareholders if there is a superior proposal.

Peter and Frances Bender have also made statements as Huon Directors that they will vote in favour of each Scheme resolution on which they are entitled to vote and will accept the Takeover Offers in relation to all of the Huon Shares they control. Unlike the Pre-Bid Acceptance, these statements are subject to the qualifications in Section 5.4.

Although the Primary Scheme and the associated Surveyors Acquisition is the preferred outcome for the Bender family, the dollar amount payable to Mr Bender for the sale by him of his shares in Surveyors to JBS is based on the same amount per Huon Share as other Huon Shareholders will receive (including Mr and Mrs Bender in respect of the 12.075% parcel of Huon Shares held by them personally) from JBS under the Primary Scheme. For Huon Shareholders other than the Bender family and their associated interests (including Surveyors) there is no difference in treatment between the Primary Scheme and Secondary Scheme, in that they will receive the same amount per Huon Share under either Scheme. Neither the Primary Scheme nor the Secondary Scheme could have proceeded without the support of the Bender family in view of their majority shareholding in Huon.

In announcing the Proposed Transactions with JBS Australia, Huon has entered into customary deal protection restrictions in the Implementation Deed, including restrictions that it will not solicit Competing Proposals. However there is nothing that prevents a third party from making an unsolicited Competing Proposal. As at the date of this Booklet, no Superior Proposal has emerged.

…

The consideration that Huon Shareholders will receive if they are paid in accordance with any of the Proposed Transactions is the same - $3.85 per Huon Share.

The Scheme Consideration payable under both the Primary Scheme and the Secondary Scheme is $3.85 per Huon Share.

The Huon Board currently intends to pay a fully franked Special Dividend of $0.125 per Huon Share prior to implementation of the Schemes, if either of the Schemes are approved by Huon Shareholders and the Court and subject to receiving a favourable tax ruling from the ATO before the Implementation Date.

If either of the Schemes becomes Effective, Huon Shareholders registered as such on the Scheme Record Date will receive the Scheme Consideration of $3.85 per Huon Share, less the amount per Huon Share of the Special Dividend (if any) paid by Huon.

If the Takeover Offers becomes unconditional Huon Shareholders who accept the Takeover Offer made to them will also receive $3.85 per Huon Share. As stated in this Booklet, the Takeover Bid is an alternative to the Schemes. Accordingly, the Takeover Offers will only proceed if neither of the Schemes becomes Effective and the conditions of the Takeover Offers are otherwise satisfied or waived. The Special Dividend will not be payable if the Proposed Transaction proceeds via the Takeover Offers.

(Emphasis in original.)

11 As is apparent from the form of the orders made on 22 September, Huon sought orders that the following two scheme meetings be convened:

(a) a meeting of the ordinary shareholders of Huon other than Surveyors (the Excluded Shareholder) for the purposes of considering a scheme of arrangement (Structure A Scheme) proposed to be made between Huon and its ordinary shareholders (other than the Excluded Shareholder) (Structure A Scheme Meeting); and

(b) a meeting of the ordinary shareholders of Huon for the purposes of considering a scheme of arrangement (Structure B Scheme) proposed to be made between Huon and its ordinary shareholders (Structure B Scheme Meeting).

12 While the two alternative and concurrent schemes of arrangement are referred to in the originating process (and in the transaction documents) as the “Structure A Scheme” and the “Structure B Scheme”, they are referred to in the draft acquisition booklet as the “Primary Scheme” and the “Secondary Scheme” respectively. The acquisition booklet also uses the terms “Primary Scheme Meeting” and “Secondary Scheme Meeting”. For clarity, I adopt the Primary Scheme and Secondary Scheme terminology used in the acquisition booklet.

13 Both the Primary Scheme Meeting and the Secondary Scheme Meeting are proposed to be held as virtual meetings on Friday, 29 October 2021. It is also proposed that Huon’s Annual General Meeting will be held on the same day, at which Huon shareholders will consider, among other matters, JBS’s proposed acquisition of Surveyors. Each of the notices of meeting provide that the relevant meeting will commence at 10.00am (Hobart time). It is proposed that the three meetings will all be opened at 10.00am and then each of the Secondary Scheme Meeting and the Annual General Meeting will be adjourned respectively to the conclusion of the Primary Scheme Meeting and the Secondary Scheme Meeting.

14 It is proposed that Mr Neil Kearney (Huon’s Chairman) will chair the Scheme Meetings and the Annual General Meeting unless he is unable to do so, in which case Mr Kevin Dynon (a non-executive director of Huon) will chair the meetings.

15 On 3 September 2021, a draft acquisition booklet (which included the explanatory statement for the Schemes required by s 412(1) of the Act) was lodged with ASIC. On 7 September 2021, a copy of the application filed 6 September 2021 and an affidavit of the same date of Mr John Brewster, a partner at Ashurst (the solicitors for Huon), were sent to ASIC.

16 The author of the draft independent expert’s report, which is to be annexed to the acquisition booklet, has opined that:

(a) the Primary Scheme is fair and reasonable and hence in the best interests of Huon shareholders in the absence of a superior alternative proposal emerging, and the advantages of the Surveyors acquisition outweigh the disadvantages;

(b) the Secondary Scheme is fair and reasonable and hence in the best interests of Huon shareholders in the absence of a superior alternative proposal emerging; and

(c) the takeover offer is fair and reasonable to Huon shareholders in the absence of a superior alternative proposal emerging.

17 The statutory framework under the Act relating to schemes of arrangement involves a three stage process:

(a) the hearing of an application to the court for orders to convene a meeting or meetings (s 411(1));

(b) the holding of the meeting or meetings (s 411(4)(a)); and

(c) the hearing of an application to the court for an order to approve the scheme (ss 411(4)(b) and 411(6)).

18 Section 411 confers a discretion on the court to make appropriate orders if:

(a) a compromise or arrangement is proposed between a Part 5.1 body and its members (or any class of them);

(b) application for the order is made in a summary way by the body;

(c) 14 days’ notice of the hearing of the application has been given to ASIC (or such lesser period as the court or ASIC permits); and

(d) the court is satisfied that ASIC has had a reasonable opportunity to:

(i) examine the terms of the proposed compromise or arrangement to which the application relates and a draft explanatory statement relating to the proposed compromise or arrangement; and

(ii) make submissions to the court in relation to the proposed compromise or arrangement and the draft explanatory booklet.

19 These requirements were met in this case and the court’s discretion to make the orders sought is thus enlivened.

20 In exercising its discretion whether or not to convene a scheme meeting, the court needs to be satisfied of two matters: first, that the scheme is fit for consideration, in that it is of such a nature and cast in such terms that, if it achieved the statutory majority at the meeting, the court would likely approve it on a petition which was unopposed; and secondly, that the members are to be properly informed as to the nature of the scheme before the scheme meeting.

21 As Finkelstein J explained in an oft cited passage in Re CSR Ltd (2010) 183 FCR 358 at [74]-[76], at the first court hearing the court should generally confine itself to ensuring that certain procedural and substantive requirements are met (for example, that there will be adequate disclosure), with limited consideration of issues of fairness. And the court should only consider the merits or fairness of a proposed scheme at the convening hearing if the issue is such as would “unquestionably” lead to a refusal to approve the scheme at the approval hearing; that is, the scheme may “appear on its face so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further” (quoting Re T & N Ltd [2007] 1 All ER 851 and Re Foundation Healthcare Ltd (2002) 42 ACSR 252; [2002] FCA 742).

22 At the 22 September hearing, Huon’s counsel raised the following features of the Schemes:

(a) the terms of the Schemes;

(b) performance risk;

(c) the exclusivity provisions;

(d) the break fee;

(e) the deemed warranty provision;

(f) the question of class in terms of benefits to Mr Bender;

(g) the unanimous recommendation of the directors for the Secondary Scheme and the associated question of director benefits in the form of performance rights for Mr Bender;

(h) the special dividend and the associated question of financial assistance; and

(i) section 411(17) of the Act.

23 The terms of the Schemes are set out above, and need no elaboration.

24 On applications of this type, the court wishes to ensure that the relevant party (here JBS) is bound to perform the role assigned to it and that its obligations are able to be enforced. I am satisfied, for the reasons advanced by counsel for Huon, that no relevant performance risk exists.

25 Likewise, no issue arises with respect to the exclusivity provisions, the break fee, or the deemed warranty provision.

26 It is necessary to say something about the class question.

27 Section 411(1) of the Act provides that where an arrangement is proposed between a company and its members or any class of them, the court may order a meeting of the members of the company or a class of them to consider that arrangement.

28 The test for what constitutes a separate class of creditors dates back to the late 19th century. See Sovereign Life Assurance Co v Dodd [1892] 2 QB 573 at 583 (Bowen LJ). Essentially, the test is whether the interests of the persons in question are so different as to make it impossible for them to consult together with the other shareholders. And see generally the useful review of the authorities in First Pacific Advisors LLC v Boart Longyear Ltd (2017) 121 ACSR 136; [2017] NSWCA 116 at [77]–[81] (Bathurst CJ, Beazley P and Leeming JA agreeing).

29 As is apparent from the extract of the draft acquisition booklet set out at paragraphs 8 and 9 above, the Primary Scheme is a scheme between Huon and all Huon shareholders other than Surveyors. The scheme meeting for the Primary Scheme is a meeting of a class of Huon shareholders, being all Huon shareholders other than Surveyors. As the shares in Huon held by Surveyors (being 40.53% of Huon’s issued shares) are not proposed to be acquired under the Primary Scheme, Surveyors is an “excluded shareholder” for the purposes of the Primary Scheme and is not entitled to vote on the Primary Scheme. As to the 12.15% of shares described in paragraph 7 above, it is proposed that they will be acquired by JBS under the terms of the Primary Scheme, and that they will be voted on the Primary Scheme resolution. It is also proposed that the votes in respect of those shares cast at the Primary Scheme Meeting will be tagged.

30 ASIC’s s 411(17)(b) letter dated 22 September 2021, which was tendered into evidence, makes a point about tax consequences. As the draft acquisition booklet explains, different capital gains consequences arise from the two transaction alternatives. If Mr Bender receives proceeds personally from the sale of shares in Surveyors he will be entitled to a capital gains tax discount through the first 50% of capital gains being disregarded, and will be subject to capital gains on the balance at the personal marginal rate. If Surveyors receives the proceeds from the sale of its Huon Shares it will be subject to capital gains on the full amount but at the corporate rate.

31 ASIC’s letter, which is set out below, proceeds on a slight, although understandable enough, misunderstanding in its contention that Mr Bender should vote in a different class to other shareholders under the Primary Scheme. The letter refers to “the 12.15% shares Mr Bender holds directly”. As explained above, Mr Bender holds 12.07% of the shares in his personal capacity, and the balance of the difference between 12.07% and 12.15% is held in separate amounts by Mrs Bender, a family trust, and the Bender family super fund. (No separate class question is said to arise with respect to the Secondary Scheme.)

32 ASIC’s letter contended as follows:

ASIC’s position on class composition in respect of the Primary Scheme

ASIC understands that it is proposed that Mr Bender will vote shares held by him directly, comprising an interest of 12.15% in the Company, on the Primary Scheme in the same class as other shareholders of the Company. This is proposed to occur in circumstances where Company shares held by Surveyors Investments Pty Ltd ACN 602 004 179 (Surveyors) (comprising a 40.53% interest in the Company) will be acquired by JBS Australia Pty Ltd ACN 011 062 338 (JBS) through the acquisition of Surveyors (Surveyors Acquisition), subject to shareholder approval pursuant to an item 7, section 611 resolution, rather than under the Primary Scheme.

We understand that the Surveyors Acquisition is structured to provide Mr Bender with significant benefits flowing from the different taxation treatment applicable to the acquisition of Surveyors compared to an acquisition of the Company shares held by Surveyors pursuant to the Primary Scheme. We understand that this structure was requested by, and is preferred by, Mr Bender. While we acknowledge that the rights attached to the 12.15% shares Mr Bender holds directly may not be different to that of rights attaching to shares held by other shareholders and may be treated in the same manner under the Primary Scheme, the tax benefit that would flow to Mr Bender under the Primary Scheme in respect of the 40.53% of Company shares held through Surveyors is an advantage that is not available to other shareholders. Further, we understand that the Company is unable to confirm whether there are other shareholders in the Company who would likewise receive similar taxation benefits from their shares being acquired directly, rather than under the Primary Scheme.

As a consequence of the significant commercial benefits that may be available to Mr Bender that are not available to other shareholders, we consider that it would be appropriate for Mr Bender to vote in a different class to other shareholders.

The Company has not provided shareholders with an independent expert’s report on the valuation of the benefit flowing to Mr Bender from the Surveyors Acquisition. No valuation is disclosed in the draft explanatory statement provided to ASIC. ASIC is therefore unable to assess whether the benefit is provided on “arms-length” terms or whether there is a “net benefit”.

We understand that the Company also submits that the benefit offered to Mr Bender should be viewed in the context of the “burden” that he has agreed to accept by virtue of entering into a non-compete agreement with JBS. However, we note that the Company has not established that entry into the non-compete agreement is connected to the structuring of the Primary Scheme including the Surveyors Acquisition, noting that the non-compete agreement also applies where the Secondary Scheme is implemented and no taxation benefit is available to Mr Bender.

We understand that the Company also submits that the issue of whether Mr Bender should vote in a separate class is addressed by the fact that it has proposed both the Primary Scheme and Secondary Scheme with the same offered consideration, and thus that shareholders other than Mr Bender may choose to vote against the Primary Scheme and vote in favour of the Secondary Scheme, where there is no separate acquisition of Surveyors, should they wish to do so. Although shareholders other than Mr Bender may choose to do so, ASIC does not agree that this in any way addresses the effect of Mr Bender voting in favour of the Primary Scheme in the same class as the other shareholders. ASIC submits that it is for precisely the reason that other shareholders may choose to vote against the Primary Scheme and vote in favour of the Secondary Scheme where there is no separate acquisition of Surveyors that Mr Bender should not vote in the same class as other shareholders in respect of the Primary Scheme. Further, we consider that should the Primary Scheme be voted down in circumstances where Mr Bender was required to vote in a separate class to other shareholders, the Secondary Scheme, where all holders including Mr Bender vote in the same class, mitigates any risk that separate classes will give rise to the transaction as a whole being vetoed.

ASIC notes that the question of classes is properly to be addressed by the Court at the first court hearing. Nevertheless, ASIC understand that the Company will tag the votes of Mr Bender in respect of the 12.15% of shares he holds directly in respect of voting on the Primary Scheme. ASIC has requested that relevant material on the voting of the Schemes be provided to the Court and ASIC as soon as reasonably practicable after the Scheme Meeting.

We consider that, should Mr Bender vote in favour of the Primary Scheme in the same class as other shareholders and should his votes unduly influence the outcome of voting on the Primary Scheme, the additional commercial benefits that are offered to Mr Bender and the impact on voting may also warrant further consideration for the purposes of fairness at the approval court hearing.

33 The contention that there should be a separate class as ASIC suggests seems to me improbable. First, whatever financial consequence may exist for Mr Bender arises as a consequence of taxation law, and are not rights which are relevantly affected by the Primary Scheme, because a tax benefit is not a benefit that the shareholder receives in consideration for voting in favour of a scheme. Secondly, and relatedly, it is difficult to see how different tax consequences that may arise between different shareholders would mean that it is impossible for them to consider the scheme as one class. Such consequences may create divergent commercial interests, but they are extrinsic to share membership, so ordinarily, such interests are not a factor which should differentiate classes. Thirdly, although the ASIC letter proceeded on the assumption that Mr Bender holds 12.15% of the shares in Huon, as I explained above, there is in fact 0.07% of the shares held by the family trust and the super fund. Tax consequences for them will inevitably differ. Fourthly, the courts have made it clear that judges should not be “too assiduous in identifying classes” lest one “end[s] up with any number of classes”. See Re Opes Prime Stockbroking Ltd (No 2) (2009) 179 FCR 20 at [66] (Finkelstein J). Creating different classes of shareholders based on the different tax consequences that a scheme may produce seems to me, with respect, to be a recipe to do just that.

34 In any event, I am satisfied that it is reasonably arguable that separate classes are not required and there is insufficient merit in ASIC’s contention that the Primary Scheme Meeting proceed by way of any separate class.

35 No issue arises in respect of the unanimous recommendation of the directors for the Secondary Scheme and the associated question of director benefits in the form of performance rights for Mr Bender or the special dividend. Shareholders would ordinarily expect directors to make a recommendation, even when that stand to gain a substantial financial benefit. As Robson J said in Re SMS Management & Technology Ltd [2017] VSC 257 (at [26]), “I think it is important that the managing director, who in this case is the main moving force behind the company, give his reasons for putting forward the scheme”. See generally Re Kidman Resources Limited [2019] FCA 1226; (2019) 375 ALR 760 at 778-782 [99]-[115]; Re Villa World Limited [2019] NSWSC 1207; (2019) 139 ACSR 550 at [38]-[40]; Re GBST Holdings Limited [2019] NSWSC 1280 at [24]-[30]; and Re ERM Power Limited [2019] NSWSC 1502 at [16]-[18]. The question is, rather, one of disclosure. Here, the relevant performance rights and the special dividend are fully disclosed in the acquisition booklet.

36 And no issue arises about whether the payment of a special dividend breaches the implied prohibition against financial assistance in s 260A of the Act. See, by way of example only, Re Legend Corporation Limited [2019] FCA 1249 at [73]-[75].

37 I was also satisfied that the Schemes are of such a nature and cast in such terms that, if they achieve the statutory majorities at the separate Scheme Meetings, the court would be likely to approve them (noting that court approval would be sought in respect of the Secondary Scheme only if approval was not obtained for the Primary Scheme) and that it is therefore appropriate that orders be made convening the Scheme Meetings.

38 I was also satisfied that the information to be provided to shareholders is adequate, for the reasons advanced by counsel for Huon.

39 For those reasons, I made the orders sought by Huon.

I certify that the preceding thirty-nine (39) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice O'Callaghan. |

VID 512 of 2021 | |

JBS AQUACULTURE PTY LTD | |

JBS AUSTRALIA PTY LTD | |

INDUSTRY PARK PTY LTD |