Federal Court of Australia

Shafston Avenue Construction Pty Ltd, in the matter of CRCG-Rimfire Pty Ltd (subject to deed of company arrangement) v McCann (No 3) [2021] FCA 938

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. By close of business on 20 August 2021, the parties are to prepare and submit to my Chambers a draft set of orders to reflect the contents of these reasons and to address the question of costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

REEVES J:

INTRODUCTION

1 This matter concerns three construction projects undertaken in Brisbane by CRCG-Rimfire Pty Ltd (CRCG), a building and construction company. The plaintiffs, Shafston Avenue Construction Pty Ltd (Shafston), 28 Baxter Street Construction Pty Ltd (Baxter) and Lincoln Street Construction Pty Ltd (Lincoln), are three related special purpose companies that was each incorporated to undertake one of these projects. The three companies are, in part, related because each possesses the same sole director, Mr Murray Thornton. He is also the Managing Director of Devcorp Pty Limited (Devcorp), another related company which acted as the management entity for all of the projects. Each of the plaintiffs entered into an agreement, or agreements, with CRCG between May 2016 and early 2017 related to the particular development project in which it was involved. In due course the agreement relating to each project was terminated.

2 CRCG entered voluntary administration on 16 November 2017, when Mr Said Jahani and Mr Michael McCann, the first and second defendants, were appointed its joint and several administrators (the Administrators). Subsequently, Shafston, Baxter and Lincoln each lodged an original and two amended Proofs of Debt in the administration claiming monies due under its agreement with CRCG. The final amended version of each of those Proofs of Debt was subsequently rejected by the Administrators.

3 In this proceeding, Shafston, Baxter and Lincoln have applied for orders that their Proofs of Debt be allowed in full under s 90-15 of Schedule 2 to the Corporations Act 2001 (Cth) (the Insolvency Practice Schedule).

FACTUAL BACKGROUND

4 As may be expected, each of the projects has a separate and unique history, the pertinent details of which are set out hereunder.

Shafston

5 On or about 17 May 2016, Mr Thornton, on behalf of Shafston, and Mr Adam Moore, CRCG’s Construction Director, on behalf of CRCG, signed a Letter of Intent relating to the design and construction of the Lume Project, a residential apartment complex situated at 25 Shafston Avenue, Kangaroo Point, in inner city Brisbane, intended to comprise 119 apartments. That Letter of Intent recorded, among other things: that Shafston and CRCG had “discussed entering into a contract” for the design and construction of the Lume Project “for the target lump sum price of $48,400,000 plus GST” (cl 1.1); that the purpose of the Letter of Intent was “to confirm the mutual intent of [Shafston] and [CRCG] to negotiate in good faith and use reasonable endeavours to agree” that contract (cl 1.2); that CRCG was authorised “to commence preliminary works which consist primarily of design and reasonable preliminary costs” (cl 1.4); and that the works “shall be designed and further detailed but that the Contract Sum shall not vary” (cl 2.1).

6 Clause 3.1 of the Letter of Intent provided that, “[i]n the event that [CRCG] and [Shafston] proceed to contract, the form of contract that will be entered into will be a Design and Construct Contract”. Further, cl 3.3 of the Letter of Intent provided that the parties would “use all reasonable endeavours to negotiate in good faith the terms of the Contract and agree its terms by 31 May 2016[.] If the contract is not executed by 30 June 2016, then [CRCG] may claim for design costs incurred on a monthly basis until the execution of the contract takes place”. Relatedly, cl 11.2 of the Letter of Intent provided that, if the parties had not entered into a contract by the date nominated in cl 3.3, then the Letter of Intent would “automatically terminate unless an extension is agreed in writing by both parties”. In that event, cl 11.4 of the Letter of Intent provided that:

Upon termination or expiry of this Letter, the Contractor will provide to the Principal all materials, designs, models, drawings, prints, samples, specifications, reports, documentation, manuals, software, or any other similar items produced by the Contractor or obtained from others pursuant to this Letter …

7 Following the signing of the Letter of Intent, CRCG undertook preliminary design works and other preparatory design and construction works in connection with the Lume Project. Shafston paid CRCG the total sum of $1,468,656.02 for those works.

8 Between 29 June 2016 and 31 May 2017, Mr John Petrie, Shafston’s Project Manager, sent letters to Mr Moore of CRCG on 14 occasions in the same format giving notice “[i]n accordance with Clause 11.2, we are extending the letter of intent automatic termination date to … [a particular date]”. Each letter went on to request a response in writing to confirm acceptance of the extension concerned. There is no evidence that CRCG responded to any of these letters so the parties seem to have proceeded on the footing that this process met the requirement of cl 11.2 for any extension of the Letter of Intent to be agreed in writing by both parties. The last of these extensions was from 31 May 2017 to 31 July 2017.

9 In the meantime, during November 2016, three meetings were held (on 10, 23 and 29 November) between representatives of Shafston and CRCG to conduct further negotiations to finalise the contract for the Lume Project. Thereafter, a Heads of Agreement (HOA) document was prepared by CRCG and executed by Mr Moore of CRCG. That document was then delivered to Shafston on 10 January 2017. In cl A of the introductory Background section, it contained a statement that CRCG “has or intends to enter into a Building Contract with [Shafston]” and, in cl D, that the parties “have agreed to be bound by this agreement and to execute all such other agreements or documents as reasonably required to give effect to this agreement”. However, it later emerged that this HOA document had not been properly executed as required by s 127 of the Corporations Act 2001 (Cth) (the Act), as it was said to have been. The deficiency was that it had only been signed by one director of CRCG, namely Mr Moore. Consequently, on 24 January 2017, Mr Thornton of Devcorp sent an email to Mr Moore requesting that one of CRCG’s other directors also sign the document. This was never done.

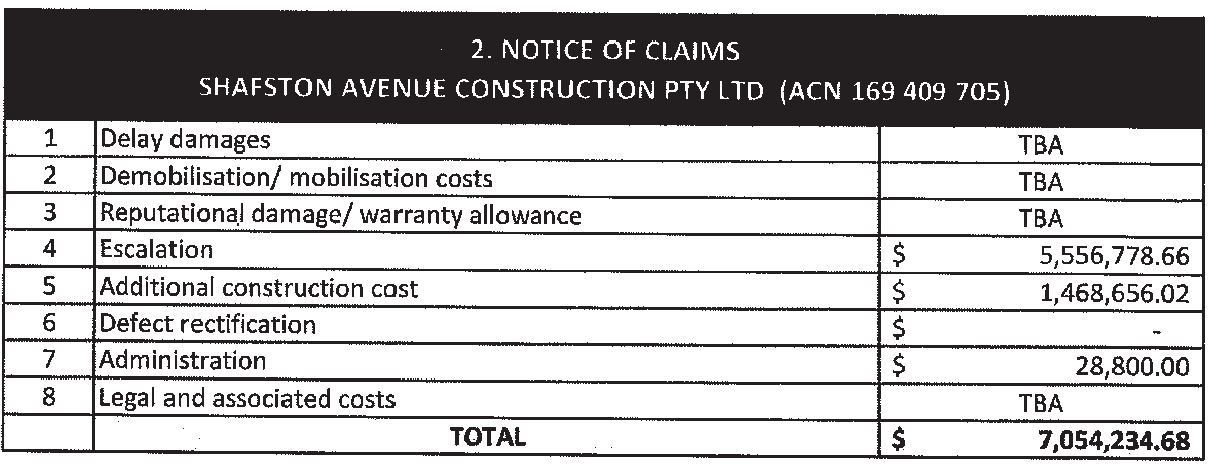

10 Between early January 2017 and early March 2017, a series of letters or emails passed between representatives of CRCG and Mr Petrie of Devcorp concerning different aspects of the Lume Project. They included: warnings about “cost creep” associated with design changes to the Project (letter dated 9 January 2017); a requirement that the balconies on the Project have flush thresholds (letter dated 16 January 2017); proposed amendments to the Principal Project Requests (letter dated 16 January 2017); a requirement for smoke exhausts to be installed in the lobbies of the building (letter dated 19 January 2017); clarification being sought as to whether air-conditioning had to be installed in the building’s foyers (letter dated 23 January 2017); and revised pricings being provided for the basement plans (letter dated 3 February 2017).

11 Soon after the last letter above, Mr Moore sent a letter (on 22 February 2017) to Mr Thornton enclosing a tender submission for the design and construction of the Lume Project. Among other things, Mr Moore stated in that letter: “Our offer is a conforming tender based on the Design Development to date … for a total lump sum price of $50,499,463 (ex GST), for a nominated build duration of 25 months from commencement on site to handover of site” (bold in original).

12 Apparently unaware of that letter, on 2 March 2017, Mr Cameron Kirkwood of CRCG sent a letter to Mr Petrie headed “LUME DEVELOPMENT – Design and Construct Contract – Outstanding Contract Terms and Conditions Reminder” (bold in original) which concluded with the statement “[w]e again request a meeting between Devcorp & [CRCG] to agree the final terms”.

13 On 6 March 2017, Shafston and CRCG entered into a Construction Management Agreement, under which CRCG was engaged as “Construction Manager” to “review the design and manage and control the construction and completion of the building” (cl 2). Under cl 3 of that agreement, CRCG’s duties were described as:

(a) In conjunction with [Shafston] produce a builder’s estimate of cost for construction of the project.

(b) In conjunction with [Shafston] produce a builder’s budget for the project.

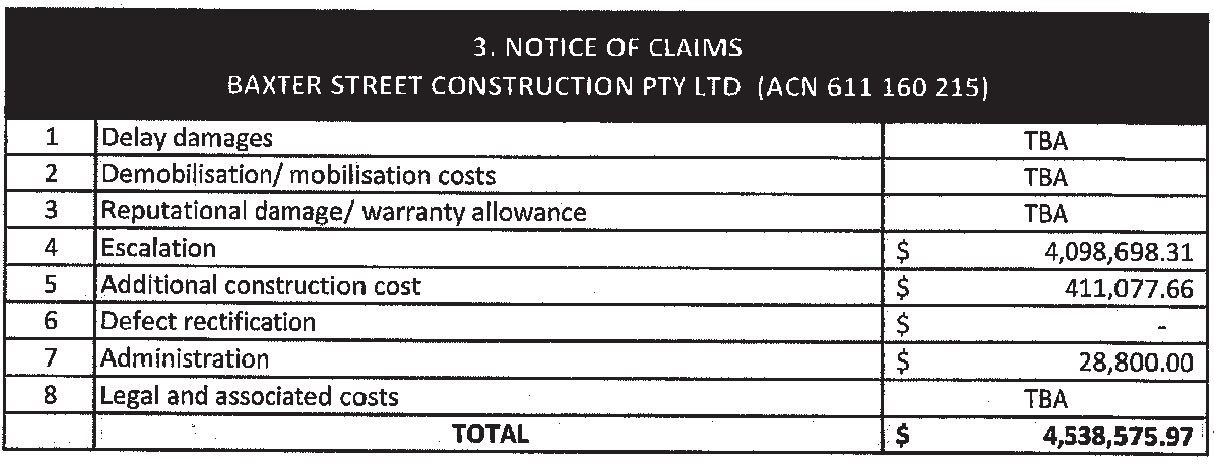

(c) In conjunction with [Shafston] produce a building methodology for the project which will include site staffing, materials handling, craneage and programming to completion.

…

Further, cl 6(a) of that agreement provided: “[CRCG] shall commence construction of the building as soon as practicable after execution of the building contract”. The expression “Building Contract” was defined in cl 1.1 as follows: “The building contract to be made between [CRCG] and [Shafston] for the construction of the Building as varied from time to time”. Finally, under cl 8 and Item 4 of the Schedule to that agreement, CRCG was entitled to be paid a construction management fee of $1,755,000 as follows:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 On 14 March 2017, an employee of St.George Bank Limited advised Mr Thornton of Shafston by email that St.George Bank was not willing to support CRCG as the builder for the proposed development. Among the reasons given were that:

1. Proposed project is very large and [CRCG] have no consistent track record for projects of this size or nature;

2. [CRCG] has only been in operation for 2 years and therefore has a relatively short term track record in the building industry;

3. [CRCG’s] rapid growth into large scale projects in such a short period of time;

4. Wider Westpac Group’s exposure to [CRCG] on other projects currently being funded by the Banking Group[.]

15 Similarly, on 26 April 2017, an employee of National Australia Bank Limited (NAB) advised Mr Thornton by email that: “Our discussion internally indicate that [CRCG] would not be considered acceptable for the project of this scale and as such we could not proceed on that basis”.

16 In early June 2017, through his involvement in the Lincoln on the Park Project, Mr Thornton became aware that one of CRCG’s “related entities [e.g. Rimfire Constructions (Qld) Pty Ltd] has experienced financial difficulty, and as a result, Subcontractors that are working on the Lincoln on the Park Project are owed money outside of payment terms”.

17 On 13 June 2017, a meeting was held between representatives of Devcorp (including Mr Thornton and Mr Petrie) and representatives of CRCG (including Mr Li Gangnan, its Managing Director, and Mr Zhao Dapeng, its Vice-Chairman). At that meeting, among many other things, the resignation of Mr Moore as General Manager of CRCG was discussed along with a number of items connected with the Lume Project. After that meeting, Mr Petrie sent an email to Mr Li and Mr Zhao in which he stated, among other things:

…

o 30 May 2017 was the first time CRCG was advised about the financial difficulty of Rimfire Construction Qld Pty Ltd (RCQ)

o There will be an announcement tomorrow regarding Adam’s [Moore] resignation to all staff

…

Lume

o Alex [Mr Zhao] and Charlie [Mr Li] have not reviewed the contract sum amount for Lume yet

o Murray [Thornton] proposed to change the approved 10% performance guarantee to be 5% and lower the pre-sales guarantee (Heads of Agreement) from 20% to 10%. The 5% removed from the performance to then be assigned to the pre-sales guarantee. So performance guarantee to be 5% and pre-sales guarantee 15%.

o [Mr Zhao] advised that as these numbers are now lower the approval is not as high level and so will seek an approval to this within 2 weeks from today

Lume Action Items

1. [Mr Zhao] will speak to Mr Lin regarding the 20% heads of agreement and have Mr Lin get it approved by the relevant party

2. If the 20% guarantee as approved by [Mr Moore] is not acceptable, then the reviewed 5% building contract performance guarantee and 15% heads of agreement will be proposed and seek approval to ensure construction of Lume can proceed shortly

3. [Mr Li] will speak to lawyer regarding security requirements from Devcorp.

…

(Bold and underlining in original)

18 On 16 June 2017, Mr Thornton sent a letter to Mr Li giving notice of the termination of the Letter of Intent in the following terms:

…

In accordance with Clause 11.1, we are terminating the letter of intent effective today, 16 June 2017. [CRCG] is to provide all information and documents in accordance with Clause 11.4.

[CRCG] is to cease with the early (civil connections) works and also retract the operational works and construction management plan approvals from Brisbane City Council. [CRCG] is to remove all site sheds and other equipment from the Site within two weeks.

(Emphasis added)

Part of the present dispute concerns the emphasised part of the first paragraph above and the operation of cl 11.4.

19 Soon after the termination of the Letter of Intent, Shafston circulated an Invitation to Tender with respect to the Lume Project. In response to that Invitation, on 28 August 2017, J Hutchinson Pty Ltd trading as Hutchinson Builders (Hutchinson) submitted a tender to Shafston. Shafston accepted that tender and subsequently entered into a contract with Hutchinson on 20 October 2017 to design and construct the Lume Project.

20 As already mentioned, CRCG entered voluntary administration and the Administrators were appointed on 16 November 2017. On 19 March 2018, the company entered into a Deed of Company Arrangement and the Administrators were appointed Deed Administrators.

21 Shafston lodged its original Proof of Debt on 24 November 2017 in the sum of $7,054,234.68, particularised as follows:

22 After the Deed of Company Arrangement was entered into, Shafston lodged two amended Proofs of Debt – one on 23 April 2018 in the sum of $8,483,086.32 and the other on 24 August 2018 in the sum of $9,273,771.28. The details of these amended claims were set out in two letters from Macpherson Kelley, lawyers for the plaintiffs, to Clayton Utz, lawyers for the Administrators, one on 23 April 2018 and the other on 7 August 2018.

23 The Administrators initially allowed Shafston’s original Proof of Debt in the sum of $1 for voting purposes only. Ultimately, Shafston’s second amended Proof of Debt was wholly rejected by the Administrators on 17 September 2018. The Notice of Rejection document listed the correspondence passing between the lawyers for the parties in the period from 11 January 2018 to 7 September 2018 and noted that, in the last of these letters, Shafston indicated that it would “not be providing further information in support of its proof of debt” (italics in original). That Notice then summarised Shafston’s claims in support of its final amended Proof of Debt as follows:

(i) [CRCG] repudiated the [Letter of Intent]. That repudiation gives rise to:

A. a damages claim against [CRCG] for the additional costs to be incurred by Shafston to complete the construction of the development in the amount of $5,556,778 (Escalation Damages); and

B. a damages claim against [CRCG] arising from the delay of the completion of the development, being the cost of additional finance, in the amount of $2,248,337 (Delay Damages).

(ii) it was unable to obtain permission to use the Shafston Documents and it suffered loss as a result of a need to have new material prepared in the amount of $1,468,656 (Construction Costs).

24 Lastly, the Notice provided the following reasons for rejecting Shafston’s claim and disallowing the Proof of Debt:

…

Escalation Damages ($5,556,778) and Delay Damages ($2,248,337)

(g) Shafston’s proof of debt is based on an allegation that [CRCG] breached or otherwise repudiated the [Letter of Intent]. The [Letter of Intent] was terminated by Shafston in accordance with its terms, as outlined in the letter of termination dated 16 June 2017.

(h) The [Letter of Intent] was not a legally binding contract between Shafston and [CRCG] for the construction of the project. The obligations imposed by the [Letter of Intent] were largely limited to:

(i) an obligation on the parties to use all reasonable endeavours to negotiate and agree on the terms of a contract for the construction of the project; and

(ii) an obligation on [CRCG] to perform the preliminary works.

(i) Given the [Letter of Intent] did not give rise to an obligation to construct the project, the alleged escalation and delay damages are rejected.

(j) Even if a repudiation had occurred, which is denied, it would not have entitled Shafston to the amounts claimed in its proof of debt.

Construction Costs ($1,468,656)

(k) Shafston asserts that it has been unable to use the Shafston Documents as it could not be satisfied that it had authority to use the intellectual property existing in those documents.

(l) Given the terms of the [Letter of Intent] (clause 9.1), all intellectual property existing in the Shafston Documents was owned by Shafston. It did not require [CRCG’s] authority or permission to use the Shafston Documents.

(m) [CRCG] had no contractual obligation to satisfy Shafston as to its rights in respect of the intellectual property existing in the Shafston Documents. In any event, [CRCG] was permitted to, and did, transfer all intellectual property rights existing in the Shafston Documents to Shafston.

(n) Shafston had (and continues to have) the authority to use the Shafston Documents.

(o) [CRCG] has received no evidence that:

(i) Shafston did not, in fact, use the Shafston Documents;

(ii) new material was recommissioned and paid for to replace the Shafston Documents; and

(iii) requests were made to [CRCG] for permission to use the Shafston Documents.

Set-Off

(p) In addition to the above and assuming [CRCG] was indebted to Shafston, Shafston remains indebted to [CRCG] in the amount of $262,927.56 for work performed by [CRCG] pursuant to the [Letter of Intent]. The Deed Administrators are entitled to set off that amount against any debt or claim of Shafston.

…

(Italics and underlining in original)

Baxter

25 At the same time as CRCG signed the Letter of Intent for the Lume Project (17 May 2016), it signed a similar Letter of Intent with Baxter for the design and construction of a residential apartment complex situated at 28 Baxter Street, Fortitude Valley in Brisbane. The pertinent terms of that Letter of Intent mirrored those of the Shafston Letter of Intent set out above (at [5]). The Baxter Letter of Intent was also extended in the same manner as the Shafston Letter of Intent (see at [8] above), but only on four occasions, with the last being to 28 October 2016. On that date, it automatically terminated under cl 11.2 of the Letter of Intent, rather than being terminated by a notice under cl 11.1 as the Shafston Letter of Intent was.

26 Following the signing of the Letter of Intent, CRCG undertook preliminary works primarily related to the design of the apartment building. Baxter paid it $411,077.66 for those works.

27 Baxter lodged its original Proof of Debt with the Administrators on 24 November 2017 in the sum of $4,538,575.97, particularised as follows:

28 As with the Shafston Proof of Debt, the Administrators initially allowed Baxter’s Proof of Debt at $1 for voting purposes only. Further, as occurred with Shafston’s Proof of Debt, Baxter lodged two amended Proofs of Debt – one on 23 April 2018 and the other on 24 August 2018. Both were in the sum of $411,077.66 corresponding to item 5 “Additional construction cost” above.

29 The Notice of Rejection of the Baxter Final Proof of Debt followed the same format as the Shafston Notice of Rejection. First, the same chain of correspondence was referenced; secondly, the same refusal to provide further information was cited; and, thirdly, Baxter’s claim was summarised as follows:

Baxter asserts that it has been unable to use any of the Baxter Documents as it does not have authority to use the intellectual property existing in them. As a result, it claims damages of $411,077.66.

30 Finally, the Notice provided the following reasons for wholly rejecting that Proof of Debt:

…

(g) The Deed Administrators have:

(i) provided Baxter with a copy of all Baxter Documents held by the Deed Administrators; and

(ii) confirmed that Baxter has authority to use the intellectual property in the Baxter Documents.

(h) The Deed Administrators have received no evidence from Baxter in relation to:

(i) whether it made requests to [CRCG] for permission to use the Baxter Documents;

(ii) whether Baxter proposes to advance the works the subject of the [Letter of Intent]; or

(iii) if the works are proposed to be advanced, whether it proposes to utilise the Baxter Documents (ie. whether it proposes to construct a development with the same or similar specifications).

(i) It is the Deed Administrators’ view that:

(i) Given the terms of the [Letter of Intent] (clause 9.1), all intellectual property existing in the Baxter Documents was owned by Baxter.

(ii) [CRCG] had no contractual obligation to satisfy Baxter as to its rights in respect of the intellectual property existing in the Baxter Documents. Even if it did have such an obligation, [CRCG] was permitted to, and did, transfer all intellectual property rights existing in the Baxter Documents to Baxter.

(iii) Baxter has authority to use the Baxter Documents.

Set-Off

(j) In addition to the above and assuming [CRCG] was indebted to Baxter, Baxter remains indebted to [CRCG] in the amount of $7,557.11 for work performed by [CRCG] pursuant to the [Letter of Intent]. The Deed Administrators are entitled to set off that amount against any debt or claim of Baxter.

Lincoln

31 On 27 May 2016, Lincoln entered into a contract with Rimfire Constructions (Qld) Pty Ltd, a company related to CRCG, for the design and construction of a residential high rise apartment complex called “Lincoln on the Park” located at 48-54 Lincoln Street, Greenslopes in Brisbane (the Lincoln contract).

32 On 13 March 2017, the Lincoln contract was novated to CRCG and thereafter CRCG took over the role of contractor. As required by the novated Lincoln contract, on 10 April 2017, CRCG provided two bank guarantees to Lincoln totalling $2,150,000.

33 In the meantime, CRCG, and, before it, Rimfire Constructions, proceeded with the constructions of the Lincoln on the Park Project. As mentioned earlier, in early June 2017, Mr Thornton became aware that some of the subcontractors on that Project were not being paid (see at [16]) above. The primary concern at that time was to ensure that the construction works on the Lincoln on the Project were completed. That concern was reflected in the following passages in the email Mr Petrie sent to Mr Li and Mr Zhao on 13 June 2017 (see at [17] above)

Lincoln on the Park

o Murray advised that with Progress Claim 14 unless confirmation is given on payment of debt before payment due date, Devcorp will hold money to pay subcontractors directly

o Minter Ellison has advised CRCG that they are not obligated for the outstanding debt from [Rimfire Constructions]

o Adam [Moore] has shares and Adam [Moore] has proposed to sell shares to pay subcontractors, however, legal advice is that cannot be done

o CRCG priority is to keep site ongoing to finish on time

o CRCG board members have not approved to pay out the debts owed to the creditors

o CRCG (Alex [Mr Li] and Charlie [Mr Zhao]) advised that they will tomorrow start communication with creditors

o Charlie [Mr Zhao] advised that the plan is for CRCG to not pay the outstanding debts but speak to all of the creditors face to face

o Murray advised he believes [Rimfire Constructions] has deadline of June 22 for voluntary administration and so resolution of the creditors needs to happen immediately

Lincoln on the Park Action Items

1. CRCG to provide tomorrow signed letter advising of the General Manager position and also the action CRCG will take to ensure the Lincoln project will continue unaffected

2. CRCG to provide tomorrow written resolution nominating Charlie [Mr Zhao] as the General Manager

3. CRCG to provide tomorrow revised organisation chart nominated Charlie [Mr Zhao] as General Manager/Director

4. CRCG to provide tomorrow [CRCG] aged creditors report for the Lincoln project

(Bold and underlining in original)

34 On 24 August 2017, CRCG served a Notice of Anticipated Practical Completion of the Lincoln on the Park Project. In response, Mr Thornton, as Managing Director of Lincoln, sent a letter dated 4 September 2017 to Mr Kirkwood as CRCG’s Contractor’s Representative notifying him that “in accordance with clause 44.6(b) the Principal’s Representative will be inspecting Site 8am Tue 5 Sep 2017 to further inspect the works, to which the Contractor’s Representative is requested to attend” (underlining in original). It appears from Mr Thornton’s letter that the process of attending to defects in the building had commenced by agreement between the parties with onsite inspections from 29 June 2017. This puts in context the following paragraph of the letter:

Please be advised the defect reports issued to date & moving forward will continue to be considered Punchlists for the specific areas inspected. To date, the majority of items within the Units being inspected are minor in nature, however the items below are considered Punchlist A items that are required to be completed prior to Practical Completion on or before 5 October 2017.

(Underlining in original)

35 Under the heading “Punchlist A items - as at 4 Sep 2017 (all previously raised under separate cover)” (bold in original), the letter went on to list the following eight items:

- Eastern façade rectification (re; jointing, render, workmanship, windows)

- Automatic irrigation installation to all garden beds

- Basement storage cages installation

- Roof Top Pergola – workmanship, finishing & sagging issues

- Roof Top Pool – sharp step edges, compliance & safety concerns

- Kitchen sink scratches requiring rectification or sink replacement

- Unit 102 – Rectification of exposed plumbing drain through façade of building

- Lift – Compliance re weather protection (warranties, longevity, maintenance)

36 On 19 October 2017, CRCG made a formal request that a Certificate of Practical Completion be issued for the Project. In response, on 24 October 2017, Mr Thornton, as Principal’s Representative and Managing Director of Lincoln, sent a letter to Mr Kirkwood which stated, in part:

…

In accordance with clause 44.6(c)(ii) of the Contract, the Principal’s Representative advises that Practical Completion has not been achieved in accordance with the requirements of the Contract.

Accordingly, the Principal’s Representative gives the Contractor a Punchlist identifying the Punchlist A Items that must be completed and Punchlist B Items that the Principal’s Representative considers require rectification or completion by the Contractor (see Annexure [A] for Punchlist A Items and Punchlist B Items).

The Principal’s Representative further advises that Practical Completion has not been achieved for the following reasons:

1 all Units are not fully complete with no defects remaining to be rectified which could in any way affect the ability of the Principal to complete the Sales Contracts;

2 the Contractor has not complied with clause 36 of the Contract;

3 the Contractor has not provided to the Principal all Completion Documents which, in the opinion of the Principal’s Representative, are essential for the immediate use, operation, occupation and maintenance of the Works (see Annexure B for outstanding Completion Documents), and

4 all rubbish, debris, wrappings, containers and residual materials resulting from the Works have not been removed from the Site;

Further, the Principal’s Representative refers to its Notice – Defects Inspection & Punchlist – Clause 44.6(b) dated 4 September 2017 which sets out a number of Punchlist A Items which required rectification by the Contractor and which remain outstanding.

Punchlist A items (all previously raised under separate cover):

- Eastern façade rectification (re; jointing, render, workmanship, windows)

- Automatic irrigation installation to all garden beds

- Basement storage cages installation

- Roof Top Pergola – workmanship, finishing & sagging issues

- Roof Top Pool – sharp step edges, compliance & safety concerns

- Lift – Compliance re weather protection (warranties, longevity, maintenance)

In accordance with clause 44.6(d), the Contactor is required to rectify all Punchlist A items and complete all outstanding works detailed in this letter for the purposes of achieving Practical Completion under the Contract.

Terms capitalised but not otherwise defined in this letter have the same meaning as set out in the Contract.

The Principal reserves all its rights under the Contract and at law.

…

It is to be noted that the list of Punchlist A items above does not include the sixth (kitchen sink) and seventh (unit 102) items in the similar list in the 4 September 2017 letter above at [35].

37 Attached to this letter at Annexure A was a document headed “Punchlist A items & Punchlist B items” (bold in original) as follows:

Notes:

- Attached documents are noted as ‘A’ or ‘B’ to reflect the above Punch list category

- Punchlist A items are reasonably requested for completion by 14 Nov 2017

- Punch list B items are reasonably requested for completion by 28 Nov 2017

- In addition to the attached Punchlist items;

o the Landscaping has significant areas in poor condition, dying &/or in need of immediate maintenance. Given the living nature of this item, immediate repair is required by 31 Oct 2017 to avoid replacement of large areas of the Works.

…

38 There followed two reports by Better Building Group Qld Pty Ltd (BBG) – one prepared on 5 October 2017 listing 203 items and the other prepared on 19 October 2017 listing 250 items. The top of each of those reports contained the handwritten notation “A – Entire report Punchlist A due to the volume of defects impacting occupation”. As well, there were attached an email dated 15 October 2017 and several lists variously dated 25 August 2017, 15 September 2017, 5 October 2017, 9 October 2017, 15 October 2017 and 20 October 2017, some of which were marked “A” and others “B”.

39 Notwithstanding the contents of the letter above, two days later, on 26 October 2017, Mr Thornton, as Principal’s Representative and Managing Director of Lincoln, sent a letter to Mr Kirkwood notifying him that he had decided to issue the Certificate of Practical Completion as follows:

We refer to the following correspondence:

o letter from the Principal’s Representative to the Contractor dated 4 September 2017 (ref Notice – Defects Inspection & Punchlist);

o letter from the Contractor to the Principal’s Representative dated 19 October 2017 (ref Lincoln on the Park – Design and Construct Contract – Certificate of Practical Completion – Formal Request); and

o letter from the Principal’s Representative to the Contractor dated 24 October 2017 (ref Certificate of Practical Completion – Rejection of Formal Request).

In accordance with clause 44.6(f)(i) of the Contract and notwithstanding that Practical Completion has not been achieved by the Contractor under the Contract, the Principal’s Representative in its absolute discretion hereby issues to the Contractor the Certificate of Practical Completion. The Date of Practical Completion is 26 October 2017.

In accordance with clause 44.6(f)(i), the Principal’s Representative advises the Contractor that there are a number of Defects (including Punchlist A Items) which the Con tractor is required to rectify. These Defects are set out in Annexure A and include the incomplete and defective works that were notified by the Principal’s Representative to the Contractor on 24 October 2017 and 4 September 2017.

The Contractor is required to rectify the Defects within the corresponding time frames specified in Annexure A. In the event that the Contractor is either unwilling or unable to rectify the relevant Defects in the time required by this Certificate of Practical Completion, the Principal reserves all its rights under the Contract and at law, including its rights under clause 44.6(f)(i) to rectify such Defects itself and to reduce the Contract Sum by the cost of rectifying those Defects.

…

40 With one insignificant exception, the documents annexed to this letter were identical to those annexed to the 24 October 2017 letter above at [36]. The exception was that the notes at the beginning of the annexures included the six Punchlist A Items whereas they had been listed in the body of the earlier letter.

41 On 8 November 2017, Mr Wentao Gao of CRCG sent an email to Mr Mark Gaskin-Harris of Devcorp in which he agreed to undertake certain defects in the Lincoln on the Park building, but disputed CRCG’s liability for others as follows:

…

Please find attached an update on our internal tracking sheet for internal defects in the apartments and lobbies. Please also find attached our Basement defect tracking sheet. As mentioned yesterday we are working to close out any defects outstanding (that we do not dispute). We are also working through the basement defects provided by BBG and will notify of any defects we dispute In the coming days.

We have sufficient site resources to manage the defects that are not in dispute. We currently have 1 site manager , 1 foreman, 1 site engineer, 1 administrator and any required labour to complete defects not in dispute.

In response to the Defects raised in the Practical Completion dated the 26 October 2017 we dispute pursuant to clause 56.1. Consider this correspondence a Notice of Dispute.

In reference to the alleged Defects in your correspondence of the of the 24 October 2017 – “Certificate of Practical Completion – Rejection of Formal Request”.

We have marked up your correspondence with paragraph numbers “Mark-up of Correspondence dated 24 October” and provide the following details as to why we dispute these Defects:

Para 3 – Refer items 16 to 19 below which relates to the Principal’s Annexure A;

Para 4 – We dispute this statement – we have closed out all 3rd party defects by A Plus Property Inspections as at the 24 October 2017 which are representing the Principal for defect inspections of the

Internals of each unit as documented at this date other than minor items that are contained in the attached Outstanding Defects – Lincoln on the Park tracking register. We note that 26 units have settled successfully on the 27 October 2017. These

items are not affecting the ability for the Principal to settle units. Further have settled since this date;

Para 5 – We dispute this statement - we have issued all warranties that we are reasonably aware via drop box, USB and hardcopy as at COB 25/10. (drop box link attached)

…

Para 6 – We dispute this statement - As per paragraph 5 above;

Para 7 – We dispute this statement – The Site was cleaned and all rubbish removed by 27th October 2017;

Para 8 – Refer to our dispute of the item 9 to 14 below;

Para 9 – We dispute this statement - Eastern Façade is within tolerances and any rectification works are purely cosmetic and has no effect on the functionality of the building;

Para 10 – We dispute this statement - We previously responded via letter dated 11/9/17 disputing this item and have had no response to date;

Para 11 – We dispute this statement - We previously responded via letter dated 12/9/17 disputing this item and have had no response to date;

Para 12 – We dispute this statement – The Workmanship, Finishing & Sagging issues have now been rectified to within tolerances and have no effect on the functionality of the building;

Para 13 – We dispute this statement - We have form 16 and form 11 for the pool so it has been deemed safe and has been installed strictly in accordance with Devcorps design;

Para 14 – We dispute this statement - We have form 16 and form 11 for the Lift and the Lift contractor has inspected the final product and installation and the Lift contractor

Has provided all warranties;

Para 15 – We dispute this statement as per the reasons stated above and below;

Para 16 – These documents have never been provided nominated as punch list category ‘A’ or ‘B’. Notwithstanding we have attended to any defects that

were provided in these documents that we consider are defective and have not disputed.

Para 17 – All Punchlist ‘A’ items that are not disputed above and below will be completed by this date;

Para 18 – All Punchlist ‘B’ items that are not disputed above and below will be completed by this date;

Para 19 – We dispute this statement - the Principal has taken over these works – refer attached email 26 September 2017.

In summary we dispute the statements as set out above we do class the items disputed as defects.

A copy of this Notice will be hand delivered to the Principal’s Office.

(Errors and typography in original)

42 Four days after CRCG was placed into voluntary administration, Lincoln terminated the Lincoln contract by letter dated 20 November 2017 under cll 52.11(a)(v)(A) and 52.3(a)(vi), reserving its rights under cl 52.10. On the same day, Lincoln called on the bank guarantees mentioned earlier (at [32]) and subsequently received the sum of $2,150,000.

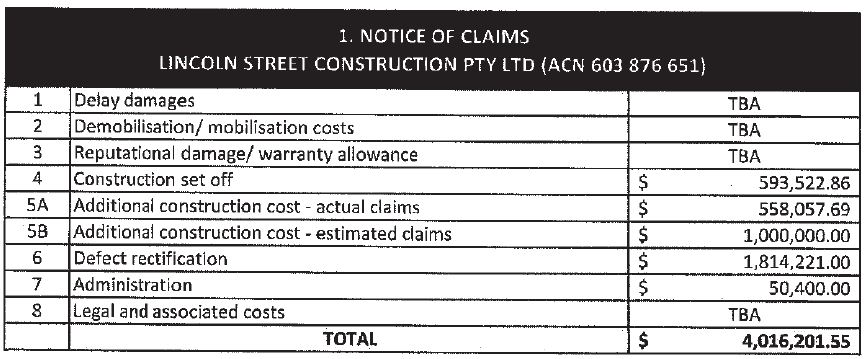

43 In lodging its Proofs of Debt in the administration, Lincoln followed the same pattern as that described for the other two projects above. Its original Proof of Debt was lodged on 24 November 2017. That was followed by two amended Proofs of Debt – one on 23 April 2018 and the other on 24 August 2018. Its original claim was for $4,016,201.55, particularised as follows:

44 In the period before Lincoln’s first amended Proof of Debt was lodged, it obtained two assessments relating to the estimated costs of rectifying the defects in the Lincoln on the Park Project – one by Gleeds Australia (East) Pty Ltd (Gleeds) on 20 November 2017 and the other by BBG on 29 March and 4 April 2018. A later report was prepared by Mitchell Brandtman on 19 April 2020 estimating the value of the trade warranties that were not provided for the Project.

45 The first amended Proof of Debt on 23 April 2018 was in the sum of $2,627,116.44. This claim took into account the $2,150,000 that Lincoln had received from calling on the guarantees provided by CRCG, as the following letter from Macpherson Kelley to Clayton Utz of the same date explained:

Defects report claim: $1,276,721.00

In or about late August or early September 2017, as the scaffolding for the Lincoln on the Park building works was being removed, it became apparent that several critical defects were present in the Lincoln on the Park works. On 4 September 2017, Murray Thornton of Lincoln sent a letter to [CRCG] outlining these defects and calling for their immediate rectification. A copy of that letter is attached.

On 26 October 2017, in accordance with 44.6(f)(i) of the Lincoln Agreement, Lincoln:

(a) Issued [CRCG] with a certificate of practical completion (PC Certificate); and

(b) Notified the Company, by way of a comprehensive defect report compiled by [BBG] (BBG Report), of a large number of Punchlist A and B defective items present in the building.

A copy of the certificate of practical completion and the BBG Report is attached.

On 20 November 2017, on the basis of the BBG Report and a further inspection of the defects by [Gleeds], Lincoln received a preliminary defects rectification estimate from Gleeds (Gleeds Report). The Gleeds Report calculated the cost of rectification in respect of the defects identified in the works to be $1,276,721.00. A copy of the Gleeds Report is attached.

In the premises, Lincoln has a claim against [CRCG] for the cost of rectification of the defects identified in the BBG Report and the Gleeds report in the sum of $1,276.271.00 (Lincoln Defects).

Further defects: $1,295,260.00

Subsequent to the receipt of the Gleeds Report, the following further defects have been identified in the works:

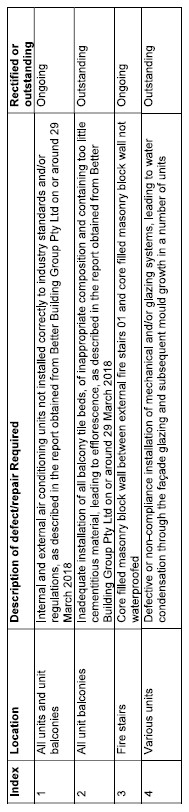

1. Air Conditioning installation defects; and

2. Defective balcony tiling; and

3. Water ingress into fire stairs.

Please find attached:

1. A report from [BBG] … dated 29 March 2018 estimating that the cost to rectify the Air conditioning installation defects and defective balcony tiling amounts to $1,260,260.00 (excluding GST); and

2. A further report from BBG dated 4 April 2018 estimating that the cost to rectify the water ingress into the fire stairs amounts to $35,000.00 (excluding GST).

The total cost to rectify the above defects therefore amounts to $1,295,260.00.

Warranties: $2,205,135.44

Clause 44.8 of the Lincoln Agreement relevantly required that upon practical completion being reached, [CRCG] was to provide to Lincoln all Completion Documents, being “those operation and maintenance manuals, as built design documents, warranties and other documents described as such in the Principal’s Project Requirements …” (emphasis added).

Clause 15.8 of the Principal’s Project Requirements for Lincoln on the Park relevantly required that the Contractor provide to the Principal warranties for the works to be performed as set out in the below table.

Item | Warranty period |

Glazing | Manufacturer’s warranty |

Roof sheeting | 7 years workmanship, materials to manufacturer’s warranty |

Waterproofing | 7 years workmanship, materials to manufacturer’s warranty |

Carpet | Manufacturer’s warranty |

Landscaping | 12 weeks maintenance, weeding and watering |

Electrical | 7 years workmanship, materials to manufacturer’s warranty |

Mechanical | 7 years workmanship, materials to manufacturer’s warranty |

Fire systems | 7 years workmanship, materials to manufacturer’s warranty |

Hydraulics | 7 years workmanship, materials to manufacturer’s warranty |

Lift services | 7 years workmanship, materials to manufacturer’s warranty 12 months’ maintenance included |

Pool | 7 years workmanship, materials to manufacturer’s warranty |

Other | Manufacturer’s warranty |

(together, the Warranties)

Subsequent to the issue of the PC Certificate, [CRCG] has refused or otherwise failed to provide Lincoln with all of the Warranties to the satisfaction of Lincoln in accordance with the Principal’s Project Requirements.

After Lincoln received the BBG Report, Gleeds Report, and the builder’s handover package, the Development Manager of Devcorp, Mark Gaskin-Harris identified that [CRCG] had failed to provide satisfactory warranties in accordance with the Principal’s Project Requirements.

Lincoln has since received a report dated 19 April 2018 from Mitchell Brandtman estimating the cost to provide the Warranties which have not been provided by [CRCG] to be $2,205,135.44.

Security: ($2,150,000.00)

Pursuant to Clause 5.2 of the Lincoln Agreement, as amended by Clause 4(g) of the Novation Deed, [CRCG] was required to supply bank guarantees in favour of Lincoln the sum of $2,150,000.00 as security for performance of [CRCG’s] obligations under the Lincoln Agreement (the Guarantees).

On 20 November 2017, in accordance with Clause 5.7 of the Lincoln Agreement, Lincoln instructed the Bank of China to make payment to Lincoln pursuant to the terms of the Guarantees. Lincoln received such payment on or about 8 December 2017.

Lincoln asserts claims against [CRCG] in the sum of $4,777,116.44 and acknowledges an offset in the sum of $2,150,000.00.

In the premises, Lincoln’s total claim against the company in the sum of $2,627,116.44 is calculated as follows:

Lincoln Defects: | $1,276,271.00 |

Further defects: | $1,295,260.00 |

Warranties: | $2,205,135.44 |

LESS Security: | ($2,150,000.00) |

Total Claim: | $2,627,116.44 |

…

46 The second amended Proof of Debt lodged on 24 August 2018 was in the same amount as above. It referred to the letter from Macpherson Kelley dated 23 April 2018 above and a further letter from that firm dated 7 August 2018. The latter letter contained further details about the defects and warranties claims as follows:

RECTIFICATION DEFECTS

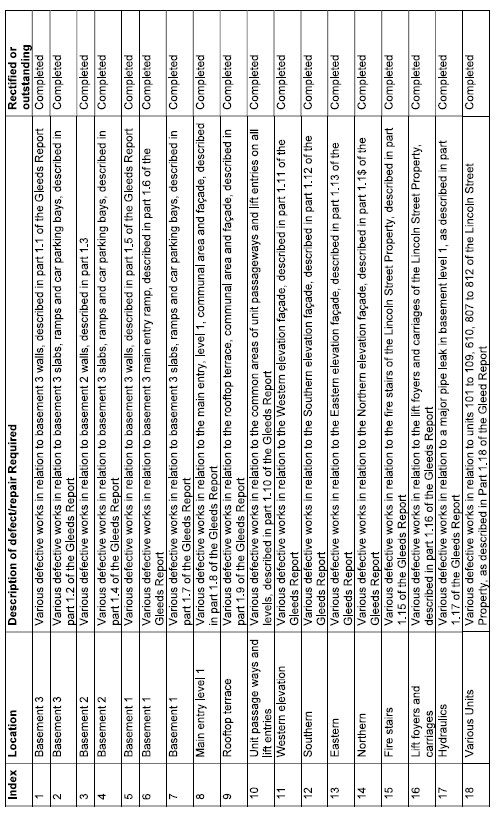

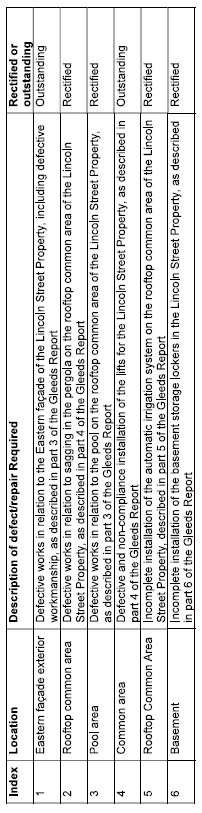

4. Please find enclosed a defects matrix prepared by our client as at 20 July 2018. On 9 July 2018, we provided your office with a copy of all relevant invoices for rectification works completed to date. The defects matrix shows the entirety of construction defects identified and not rectified.

5. To the extent the defects have not yet been rectified, Lincoln is taking steps to rectify those defects and continues to receive requests from occupants to rectify same. We reserve our client’s rights to enlarge its claim should more defects be identified such that our client’s estimate of further defects is insufficient.

6. However, as an indicative sum in order to enable the Administrators to adjudicate our client’s proof of debt, the costs of the defects as at April 2018 have been independently assessed by a third party, that being [Gleeds] and [BBG], whose reports in relation thereto have been provided to you on 23 April 2018.

7. We note that our client has had extreme difficulty in seeking assistance from subcontractors of [CRCG] in rectifying construction defects. For example, we are instructed that our client has contacted [CRCG’s] air conditioning subcontractor, with such subcontractor refusing to provide assistance on the basis that it remained a creditor of [CRCG].

WARRANTIES

8. The warranties were required to be provided pursuant to the terms of the Construction Contract between Lincoln and Rimfire Constructions (Qld) Pty Ltd dated 27 May 2016. Being that [CRCG] is unable to provide warranties as required, Lincoln must source alternative warranty arrangements.

9. The value of such warranties has been independently verified by way of report completed by Darryl Bird of [Mitchell Brandtman] dated 19 April 2018. A copy of that report together with various instructions and documents referred to was provided to your office on 9 July 2018.

10. At this stage, it is not our client’s intention to utilise further resources in obtaining a further report from [Mitchell Brandtman].

11. Lincoln’s basis for asserting that the Lift installation is non-compliant is as identified in the Gleeds report dated 20 November 2017, which was provided to your office on 23 April 2018 (Gleeds Report).

12. We disagree with your observation in respect of the double counting of the cost of the Lift replacement and the costs of repairing the water penetration into the fire stairs. To that end, please see the attached email communication from Darryl Bird of Mitchell Brandtman clarifying this part of his report. We are instructed that our client continues to press the entirety of its claim in this regard on that basis.

13. The rectification work required to the east façade, existing pergola and pool tiling are all as identified and verified in the Gleeds Report.

14. In respect of the automatic irrigation and basement locker installation, we note that the requirement for [CRCG] to provide these items is as follows:

(a) section 10.4 of the Principal’s Project Requirements at Annexure C of the Design and Construct Contract between Lincoln and Rimfire Constructions Pty Ltd and later novated to [CRCG] (the Principal’s Requirements) required [CRCG] to install an automatic irrigation system; and

(b) section 6.11 of the Principal’s Requirements required [CRCG] to install a basement locker.

To assist your client in properly adjudicating Lincoln’s proof of debt, please find enclosed a spreadsheet setting out the calculations used in calculating Lincoln’s claims.

…

(Bold and underlining in original)

47 As with the other two projects, the Administrators initially allowed Lincoln’s original Proof of Debt at $1.00 for voting purposes only. The Administrators then wholly rejected Lincoln’s Proof of Debt on 13 December 2018. The Notice of Rejection of the Proof of Debt was in similar, but not identical, terms to that for the other two projects. It listed a different chain of correspondence passing between the lawyers for the parties, but referred to the same indication in Macpherson Kelley’s letter dated 7 September 2018 that Lincoln would “not be providing further information in support of its proof of debt” (italics in original). The Notice then summarised the claims Lincoln made as follows:

h) Lincoln claims the following amounts as against [CRCG]:

I. damages for the rectification of alleged defects in the amount of $2,571,981.00; and

II. damages for an alleged failure by [CRCG] to provide it with warranties in the amount of $2,205,135.44.

i) The above claim has been reduced by the amount of the guarantee called and paid to Lincoln resulting in a total claim of $2,627,116.44.

48 Lastly, the Notice contained the following reasoning for wholly rejecting Lincoln’s Proof of Debt:

Rectification of Defects

j) Lincoln relies on the following in order to establish the alleged defective works and the costs required to remedy those defects:

o report prepared by [Gleeds] dated 20 November 2017 identifying defects totalling $1,276,721.00;

o report from [BBG] dated 29 March 2018 identifying air-conditioning and balcony tiling defects which were estimated to cost $1,260,260.00 to complete; and

o report from [BBG] dated 4 April 2018 identifying water ingress defects which were estimated to cost $35,000.00 to complete.

k) The Deed Administrators have requested access to Lincoln on the Park in order to inspect the alleged defects and obtain an independent assessment of the costs to remedy those defects. Lincoln has not responded to those requests for access. As a result, the Deed Administrators have not been able to verify the defects and they cannot be accepted.

l) Further, the Deed Administrators have no evidence (with the exception of that set out below) that the alleged defects have been rectified, noting that Lincoln holds the funds paid to it as a result of its call on the bank guarantees. In addition, a number of the alleged defects listed in the Gleeds Report indicated that they are “closed”. Despite request, Lincoln has not confirmed whether it maintains those defect claims.

m) The Deed Administrators have been provided with the following identifying the costs incurred by Lincoln it alleges is associated with defects or incomplete works:

o Retention Tracking Summary from October to December 2017 (with relevant invoices) totalling $5,188.03 (excluding GST);

o Retention Tracking Summary from January 2018 (with relevant invoices) totalling $4,585.85 (excluding GST);

o Retention Tracking Summary from February 2018 (with relevant invoices) totalling [$]25,860.42 (excluding GST);

o Retention Tracking Summary from March 2018 (with relevant invoices) totalling $71,816.29 (excluding GST);

o Retention Tracking Summary from April 2018 (with relevant invoices) totalling $90,444.00;

o Retention Tracking Summary from May 2018 (with relevant invoices) totalling $175,542.11;

o Further Retention Tracking Summary from May 2018 (with relevant invoices) totalling $139,676.24.

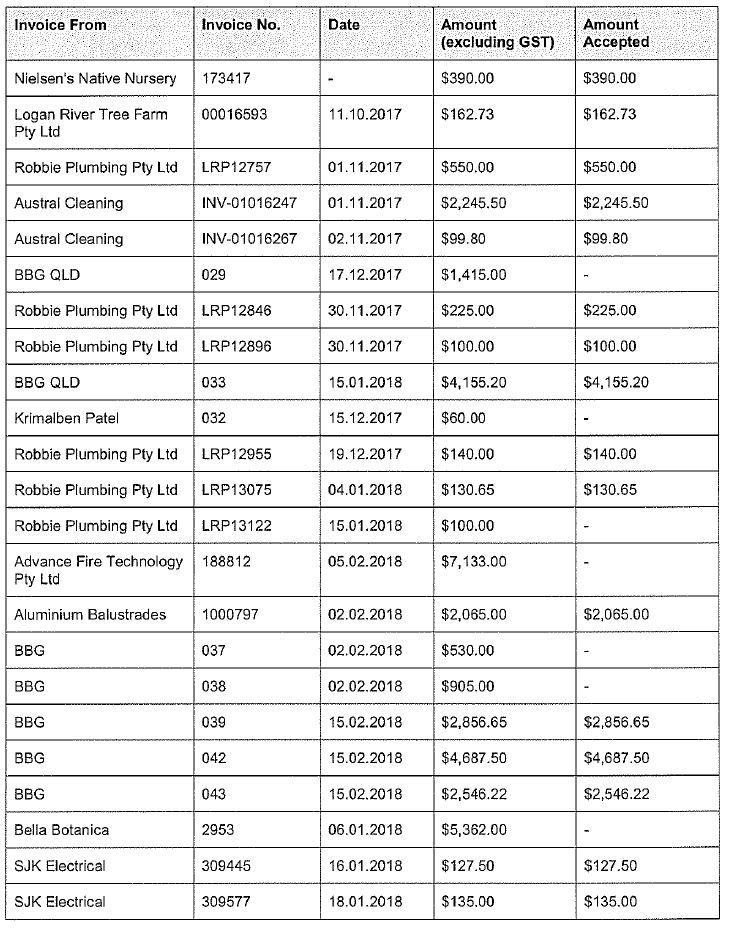

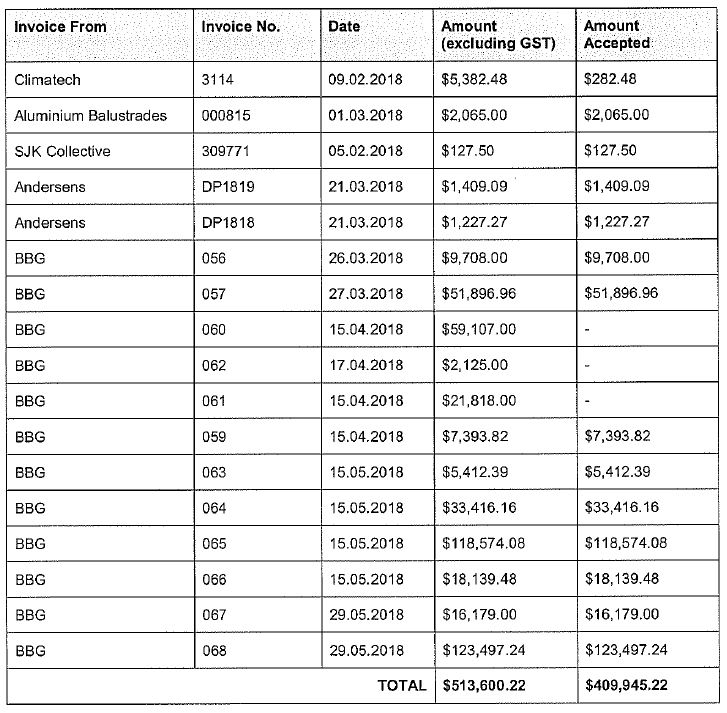

n) We set out in Annexure 1 the invoices accepted as being payable by [CRCG] in the amount of $409,945.22.

o) The Deed Administrators do not have sufficient information to accept any of the further defect claims and they are hereby rejected.

p) The value of the defects accepted by the Deed Administrators does not exceed the security held by Lincoln, which security has been applied to remedy the defects as outlined in the Retention Tracking Summary.

Warranty Claims

q) Lincoln alleges that [CRCG] did not provide warranties to Lincoln as required by clause 15.8 of the Principal’s Project Requirements forming Attachment 1 to the Novation Deed.

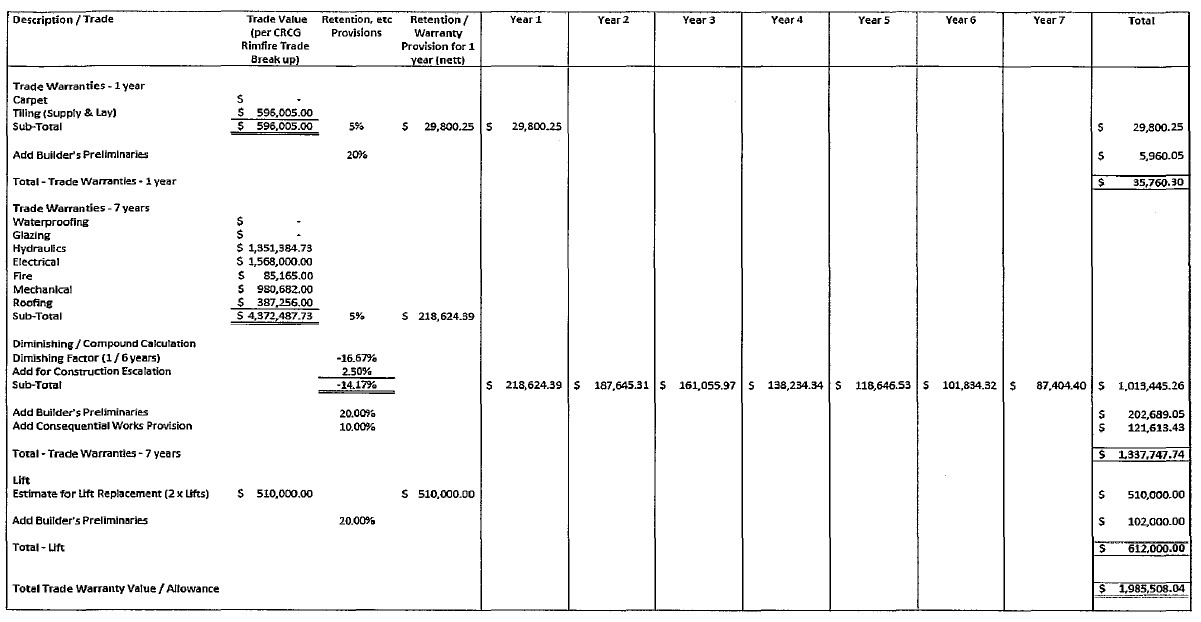

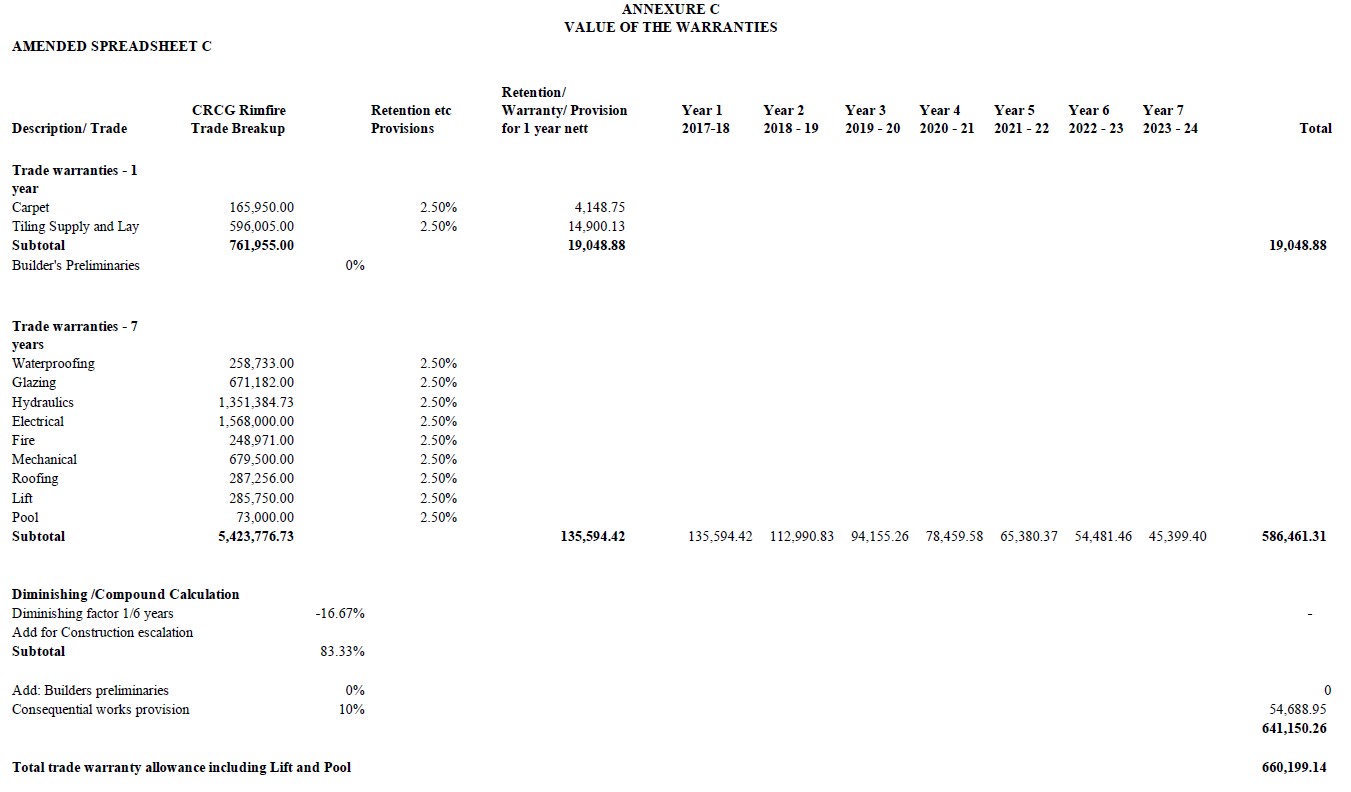

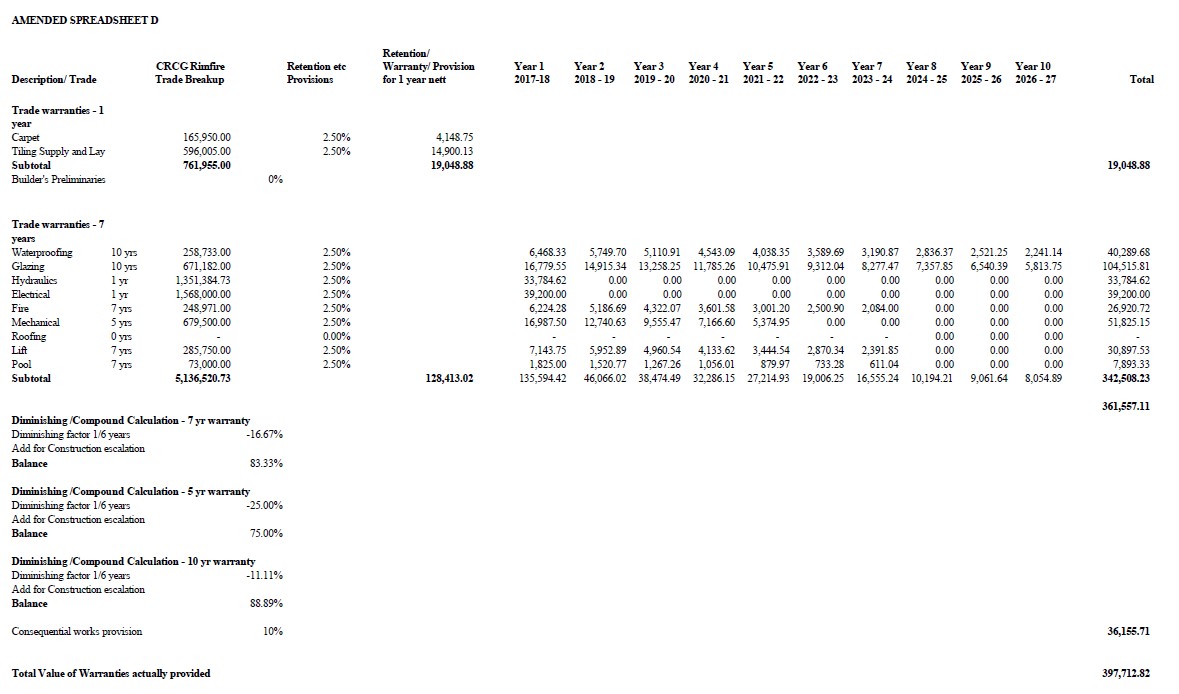

r) Lincoln has obtained a report of Mitchell Brandtman dated 19 April 2018 on which it seeks to rely in order to quantify its loss as a result of the alleged failure of [CRCG] to provide the stated warranties. The report quantifies the value of the work provided under the contract with respect to each trade and values the failure to provide the warranty for the first year as 5% of the total value of work performed. The value of the warranty then diminishes over the course of 7 years.

s) The Deed Administrators do not accept that this is the correct methodology for determining any loss suffered by Lincoln as a result of any failure to provide a warranty.

t) In any event, the Deed Administrators’ investigations indicate that:

o warranties were obtained and provided to Lincoln;

o on 8 November 2018 Wentao Gao of [CRCG] sent an email to Mark Gaskin-Harris for Lincoln indicating that [CRCG] had provided all warranties of which it was reasonably aware via USB, hard copy and drop box; and

o Lincoln was listed a Beneficiary under each Subcontract Agreement entered into with Subcontractors of [CRCG] and Rimfire. As a Beneficiary, Lincoln is entitled to enforce the warranties contained in those Subcontractor Agreements;

u) An officer of Lincoln, Murry [sic] Thornton, has signed an affidavit in which he stated “Lincoln has been required to source alternative warranty arrangements”. Despite request, Lincoln has not provided details of those alternative warranty arrangements of the cost to Lincoln of sourcing those arrangements.

v) On the information available to the Deed Administrators, they are not able to accept this claim.

Set-Off

w) In addition to the above Lincoln remains indebted to [CRCG] in the amount of $36,543.69 for work performed by [CRCG] pursuant to the Contract and Novation Deed but not paid. The Deed Administrators are entitled to set off that amount against any debt or claim of Lincoln.

(Italics in original)

49 Annexure 1 to this Notice was in the following form:

PROCEDURAL HISTORY

50 The plaintiffs’ originating application in this proceeding was filed on 18 September 2018. On 31 October 2018, the plaintiffs obtained leave to amend that document to seek an order to terminate the Deed of Company Arrangement that CRCG entered into on 19 March 2018. From that point, that application became the plaintiffs’ primary focus in this proceeding. It proceeded to hearing on 1 April 2019 and judgment was delivered on 30 August 2019 dismissing the plaintiffs’ application (Shafston Avenue Construction Pty Ltd, in the matter of CRCG-Rimfire Pty Ltd (subject to deed of company arrangement) v McCann [2019] FCA 1426]). The plaintiffs then filed an appeal against that judgment, which was heard by the Full Court on 14 February 2020 and dismissed on 22 May 2020 (Shafston Avenue Construction Pty Ltd v McCann [2020] FCAFC 85).

51 In the meantime, on 8 October 2019, the balance of the proceeding, namely the plaintiffs’ present challenges to the rejection of their Proofs of Debt, was tentatively set down for hearing for three days commencing 24 March 2020 and trial programming orders were made directed to achieving those trial dates. On 17 December 2019, because the plaintiffs had failed to comply with various aspects of those orders, they were amended, but the tentative trial dates were retained. Under that amended trial program, the plaintiffs were to file any expert evidence upon which they intended to rely by close of business on 9 January 2020. No such material was filed. Instead, on 15 January 2020, Macpherson Kelley sent a letter to Clayton Utz stating, in part:

We refer to the above matter and note that our clients’ expert reports were due to be filed on 9 January 2020.

As previously advised, it was our clients’ initial intention to simply put in the reports contained in the affidavit of Murray Thornton (that being [BBG], Gleeds, and Mitchell Brandtman) formally in as expert evidence.

Whilst we made attempts with our client’s experts at the end of last year to convert the reports into a format that they can be filed as expert evidence, we have been contacted by two of those experts, namely Gleeds and [BBG], who have advised that they no longer wish to be involved in any litigation against [CRCG]. Despite asking for further information from those experts, they will not provide us with any further details. We are still waiting to hear back from Mitchell Brandtman.

In the circumstances we are making enquires in relation to alternative experts for the purposes of obtaining reports to the same matters to those reports initially obtained by our clients. However, as you would appreciate, this will take some time. In the circumstances, we will be likely be seeking an adjournment of the hearing date which is currently set for March 2020 …

52 Approximately seven weeks later, on 2 March 2020, the plaintiffs’ lawyers filed an interlocutory application seeking to vacate the March trial dates, as foreshadowed in the final paragraph of their 15 January 2020 letter above. In his affidavit in support of that application, Mr Benjamin Rooks, the plaintiffs’ solicitor, set out two reasons for that course. The first was that he had attempted to obtain reports from the persons who had assisted Lincoln to prepare its Proofs of Debt in respect of the Lincoln on the Park project, namely Gleeds, Mitchell Brandtman and BBG, but had been informed by Gleeds and BBG that “they are now conflicted out of the matter and can no longer be part of the proceedings”. Accordingly, Mr Rooks said that Lincoln needed additional time “in which to engage new experts, to prepare expert reports on items which they had previously already had reports prepared” and that those new experts “will be briefed within the next seven days”. It will be noted that these statements are to substantially the same effect as those contained in the plaintiffs’ lawyers’ 15 January 2020 letter above (at [51]).

53 The second reason Mr Rooks provided for the adjournment was that 30 boxes of documents had recently been discovered in a property formerly occupied by CRCG which appeared to be relevant to the Lume and Lincoln on the Park Projects. In view of the steps both parties needed to take to examine and analyse those documents, Mr Rooks said that it would be “unlikely that the Plaintiffs will be in a position to proceed with the hearing on 24 March 2020”.

54 Because of the latter development and somewhat fortuitously for the plaintiffs given their dilatory approach to obtaining their replacement expert evidence, the March trial dates were vacated by consent and new trial dates were fixed for three days commencing on 7 July 2020. As a part of the amended trial program, Lincoln was ordered to file the expert evidence upon which it intended to rely by the close of business on 31 March 2020. No materials were filed by that time.

55 During April/May 2020, following the onset of the Corona Virus Disease 2019 (COVID-19) pandemic, the July hearing dates were initially treated as provisional and eventually vacated. Subsequently, new trial dates were proposed for early October 2020, but eventually they were fixed for the three days commencing 31 August 2020.

56 On 25 June 2020, the matter was listed for a pre-trial case management hearing because of concerns about the plaintiffs’ continuing non-compliance with the trial programming orders. At that hearing, the defendants relied on an affidavit by their solicitor, Mr Scott Sharry, which outlined in some detail the history of that non-compliance. It included:

not responding to the defendants’ objections to the plaintiffs’ affidavit materials;

not filing their opening submissions;

not providing a draft Index to the Court Book;

prevaricating in respect of the expert evidence they intended to rely upon.

57 As to the last of these items, during that case management hearing, the defendants’ counsel said that he had recently been informed by the plaintiffs’ lawyers that they intended to revert to their original proposal of relying upon the reports annexed to the affidavit of Mr Thornton dated 18 September 2018 (see the letter of 15 January 2020 at [51] above) and to seek the issue of subpoenas to those three persons. In response, the plaintiffs’ counsel confirmed that they had adopted that course to avoid incurring the additional expense associated with obtaining replacement expert evidence. Because this issue was likely to have an adverse effect on the preparations for trial, the parties were ordered to exchange materials outlining their positions with respect to it and a hearing date was fixed to resolve the issue. On the day before that hearing, the parties filed consent orders. The resulting orders made on 9 July 2020 provided that the plaintiffs could apply to issue subpoenas to the three persons concerned, namely: Mr Andrew King (Gleeds); Mr Steve Franklin-Bull (BBG) and Mr Darryl Bird (Mitchell Brandtman). Those orders also confined the evidence-in-chief which the plaintiffs could seek to adduce from those witnesses to the contents of the following reports:

(a) Mr King (being document 13 of Annexure MT-1 to the Affidavit of Murray John Thornton sworn 5 September 2018 and filed 18 September 2018 (the Thornton Affidavit);

(b) Mr Franklin-Bull (being documents 14 and 15 of Annexure MT-1 to the Thornton Affidavit); and

(c) Mr Bird (being document 16 of Annexure MT-1 to the Thornton Affidavit).

58 As well, Order 8 of those Orders also gave the plaintiffs leave to, by close of business on 17 July 2020:

… file and serve further lay evidence given by a suitable officer of the third plaintiff concerning the ongoing defects in the property at 54 Lincoln Street, Stones Corner in the State of Queensland and limited to the matters identified in [11] of the Affidavit of Mark Gaskin-Harris (unsworn) served on 6 July 2020.

The identified matters in question were:

(a) the nature of the particular Remediation Works which have been completed to date;

(b) the actual costs which Lincoln has incurred to date in performing the Remediation Works;

(c) the expenditure and depletion of the Guarantee Funds; and

(d) the nature of the Defects which have not yet been remediated to date, and which Lincoln is still required to remediate.

Finally, on 20 July 2020 (three days late, but an unsworn copy was filed on 17 July 2020), the plaintiffs filed an affidavit by Mr Gaskin-Harris as provided for in the order above. I will return to this affidavit later in these reasons when I come to consider the Lincoln defects issue (see below at [100]).

THE ISSUES

59 At the conclusion of the evidence at the trial and before they prepared their closing submissions, the parties agreed that some, or all, of the following issues fell to be determined in this matter, noting that issue 1(b) was ultimately not pressed:

Admissibility issue

1. Are the following admissible such that they should be received in evidence in the proceeding:

(a) the email from Matthew Molony to Mark Gaskin-Harris dated 2 August 2017; and

(b) the section headed “Rectification works” in the letter from Climatech to Steven Franklin-Bull dated 8 February 2017 (being an attachment to the Report of Steven Franklin-Bull dated 29 March 2018)?

Shafston construction contract claim

2. Did CRCG and Shafston enter into a binding contract for the construction of the Lume development, by way of:

(a) a partly written and partly oral agreement arising out of the Letter of Intent, three meetings on 10 November 2016, 23 November 2016 and 29 November 2016, and the Heads of Agreement?

(b) an agreement partly in writing and partly by conduct, consisting of the Letter of Intent, the Heads of Agreement and a course of conduct by CRCG performing works?

3. As to either alleged binding contract:

(a) Did CRCG and Shafston agree on a price of $48.4 million for the construction of the Lume development?

(b) Did CRCG and Shafston agree on the scope of works for the construction of the Lume development?

(c) Was the Heads of Agreement binding and enforceable against CRCG requiring it to provide bank guarantees to Shafston in connection with the Lume development?

(d) Did CRCG perform works in connection with the Lume development which were outside of the scope of works in the Letter of Intent, and if so, what were those works?

4. Has Shafston suffered any actual loss and damage in the sums alleged by reason of CRCG’s alleged non-completion of any binding construction contract in respect of the Lume development? As to these matters:

(a) Had Shafston secured funding for construction of the Lume development to proceed in accordance with a contract for the construction of that development with CRCG by the time of the purported termination in June 2017?

(b) Was the price for the construction of the Lume development under the contract which Shafston (or its related entity) entered into with Hutchinson Builders $53.9m?

(c) Was there a completion date for construction of the Lume development?

Shafston and Baxter intellectual property claims

5. On the proper construction of clause 11.4 of the Shafston and Baxter Letters of Intent, was CRCG required to provide Shafston and Baxter with confirmation that Shafston and Baxter could use the intellectual property in work undertaken by or on behalf of CRCG under the Letters of Intent?

6. Should a term be implied into the Shafston and Baxter Letters of Intent which required CRCG to provide permission to Shafston and Baxter to use and have the benefit of the intellectual property in the work undertaken by or on behalf of CRCG under the Letters of Intent (the Implied Term)?

7. Did CRCG fail to comply with clause 11.4 of the Shafston and Baxter Letters of Intent on its proper construction?

8. Did CRCG fail to comply with the Implied Term?

9. As to [7] and [8], if any obligation of CRCG arose:

(a) on what date did each of Shafston and Baxter request the provision of the intellectual property?

(b) on what date was the intellectual property provided?

10. Is the effect of clauses 9.1 and 9.2 of the Shafston and Baxter Letters of Intent that CRCG in fact complied with its obligations under clause 11.4 of Letter of Intent and the Implied Term?

11. Did any breach of contract on the part of CRCG cause either Shafston or Baxter to suffer loss? As to this, had either of Shafston or Baxter already incurred expense in relation to the intellectual property by the time it was provided?

12. What is the value (if any) of the loss or damage suffered by Shafston and Baxter?

Lincoln defects claim

13. What is the proper construction of the Lincoln contract in respect of the rectification of defects? As to this:

(a) Are subclauses 44.6(b) and (c) of the Lincoln Contract applicable to the claim made by Lincoln for the costs of rectifying defects in the Lincoln development?

(b) If subclauses 44.6(b) and (c) are applicable, on their proper construction, do they operate so that if they apply and have been complied with, Lincoln need not prove that defects identified in the Punchlist schedules are Defects within the meaning of the Lincoln contract?

(c) Is subclause 44.6(f) applicable to the claim made by Lincoln for the costs of rectifying defects in the Lincoln development?

(d) If subclause 44.6(f) is applicable, on its proper construction, does it operate so as to require CRCG only to rectify those identified defects in the Lincoln development which are Defects within the meaning of the Lincoln contract?

14. Has Lincoln proved that it has suffered loss and damage by reason of defects in the Lincoln development? In particular:

(a) Has Lincoln proved that there are defects in the Lincoln development?

(b) Has Lincoln proved that those defects are Defects within the meaning of the Lincoln contract?

(c) Has Lincoln proved what work is required to rectify the defects in the Lincoln development which are outstanding and the value of that work?

(d) Has Lincoln proved that there is work which has been undertaken by it or on its behalf to rectify defects in the Lincoln development and the value of that work?

(e) What is the total value of the work done or work required to be done to rectify defects in the Lincoln development which Lincoln can prove?

Lincoln warranties claim

15. What warranties was CRCG obliged to procure for Lincoln under clause 44.8 of the Lincoln contract and clause 15.8 of the Principal’s Project Requirements (Annexure C to the Lincoln contract)?

16. What warranties did CRCG in fact procure for Lincoln under clause 44.8 of the Lincoln contract and clause 15.8 of the Principal’s Project Requirements?

17. What is the appropriate methodology for valuing warranties which ought to have been procured under clause 44.8 of the Lincoln contract and clause 15.8 of the Principal’s Project Requirements? In particular, is it appropriate to:

(a) Take as a starting point the subcontract price for the value of the works the subject of the required warranties?

(b) Apply as a percentage for the value of the required warranties in their first year the retention amount stipulated in the Lincoln contract as required to be held by the principal for the first year after practical completion?

(c) Value the warranties in the years after their first year on the basis that only a warranty for workmanship would be provided and not a manufacturer’s warranty?

(d) Apply as a percentage for the value of the warranties in the years after the first year following practical completion, a diminishing compound factor with or without an increase for cost escalation?

(e) Add a component to the total value of the required warranties for builder’s preliminaries?

(f) Take into account when valuing the warranties which ought to have been, but have not been, procured for Lincoln, the benefit which Lincoln has received from warranties which have been procured on more favourable terms than those required by the Lincoln contract?

18. What is the value (if any) of the warranties which have not been procured by CRCG to Lincoln?

(Bold and error in original; underlining added)

60 Since the admissibility issue is connected with the Lincoln defects claim, that matter will be considered in conjunction with that issue. With that exception, these issues will be considered in turn below. However, first, it is convenient to say something about the nature of this proceeding and the plaintiffs’ onus of proof.

THE NATURE OF THIS PROCEEDING AND THE PLAINTIFFS’ ONUS OF PROOF

61 The principles bearing on the nature of this proceeding were helpfully summarised recently by Rees J in In the matter of Azmac Pty Limited (2020) 146 ACSR 113; [2020] NSWSC 204 (Azmac) at [41]-[44] where her Honour explained that this proceeding is properly brought under s 90-15 of the Insolvency Practice Schedule; that it proceeds as a hearing de novo; and that the critical question is whether the debt concerned is a true liability of the company, as follows:

41 An appeal to the Court challenging the decision of a liquidator with respect to a proof of debt was previously brought under section 1321 of the Corporations Act 2001 (Cth), now repealed, and, as explained by Gleeson JA in Hill v Esplanade Wollongong Pty Limited (subject to a deed of company arrangement), appeals are now made under section 90-15 of Schedule 2 Insolvency Practice Schedule (Corporations), Corporations Act: at [21]. The case law in respect of the earlier provision is, however, of continuing relevance: Re ACN 096 281 542 Limited (in liq) per Randall AsJ at [6]; El-Saafin v Franek (No 3) per Lyons J at [63]; see, for example, Hill v Esplanade Wollongong Pty Limited.

42 An appeal against a liquidator’s rejection of a proof of debt is a hearing de novo and thus the Court may make its decision on evidence that was not before the liquidator: Tanning Research Laboratories Inc v O’Brien at 340-1 per Brennan and Dawson JJ. As their Honours explained, when the liquidator is called upon to consider a proof of debt, the relevant consideration is whether the alleged debt is a “true liability of the company” or “is not legally enforceable” (at 339, 341) but, on an appeal, at 341: (emphasis added)

The liquidator may defend [the company’s] assets against the creditor’s claim on any ground on which the company may have defended the claim had it been sued by the creditor. … The issue in the proceeding is whether the liability referred to in the proof of debt is a true liability of the company enforceable against it.

43 As further explained in Tanning Research Laboratories v O’Brien at 339-341, in determining whether the debt is “a true liability of the company enforceable against it”, ordinarily the general law applies including statutes of limitation and equitable principles. There are some exceptions, however, where the liability, though enforceable against the company, is founded merely on some act or omission on the part of the company which unjustly prejudices the interests of the creditors or contributories in the assets available for distribution. For example, there may be a judgment debt against the company but there is some good reason why there ought not be such a judgment; the circumstances may tend to show that the judgment was obtained by collusion or an absurd compromise. In such circumstances, the liquidator is armed with grounds for rejecting the proof of debt additional to grounds available under the general law: at 340. Likewise, on an appeal, the liquidator is entitled to rely on this special defence which allows him, for example, to go behind a judgment in order to ascertain the true liability of the company: at 341. There is no suggestion that any of these additional grounds arise here.

44 Nor is the creditor, on such an appeal, strictly confined to each allegation and proposition by which it originally sought to advance the proof of debt, “As long as the claim remains the original claim, some change in the explanation of the way in which it is said to be a true liability of the company enforceable against it is permitted”: Johnston v McGrath at [26] per Barrett J citing Re Jay-O-Bees Pty Limited; Rosseau Pty Limited v Jay-O-Bees Pty Limited per Campbell J; Re St Gregory's Armenian School Inc per Black J at [34]-[35].

(Citations omitted)

62 As well as the matters mentioned by Rees J above, in Tanning Research Laboratories Inc v O’Brien (1990) 169 CLR 332 at 340, Brennan and Dawson JJ emphasised that “[t]he occasions when it is right to reject a proof of debt in respect of what is not a true liability of the company may not be susceptible of exhaustive definition”. However, their Honours did suggest that some guidance may be obtained from the observations of Barwick CJ in Wren v Mahony (1972) 126 CLR 212 as follows:

“Circumstances tending to show fraud or collusion or miscarriage of justice or that a compromise was not a fair and reasonable one, in the sense that even if not fraudulent it was foolish, absurd and improper, or resulted from an unequal position of the parties (see In re Hawkins; Ex parte Troup) offer occasions for the exercise by the Court of Bankruptcy of its power to inquire into the consideration for the judgment.”

(Footnote omitted)

63 As for the onus of proof, in Re Galaxy Media Pty Ltd (In Liq) [2001] NSWSC 917 (Galaxy Media), Santow J explained, by reference to several authorities, how it remained firmly on the plaintiffs and that a liquidator’s (Administrators in this matter) rejection of a proof of debt should not be upset unless the Court is properly satisfied that they have discharged that onus. In particular, his Honour said (at [25]-[26]):

25 Thus the notion of “appeal” is not so much directed at the nature of the review but to the onus lying upon the “appellant” who challenges the liquidator’s decision. Thus in Westpac Banking Corporation v Totterdell (at 154), Ipp J concluded:

“Although the issue before the court on the appeal is whether the liability referred to in the proof of a debt is a true liability of the company, enforceable against it (Tanning Research Laboratories Incorporated v O’Brien (at 341)), it remains incumbent on an appellant to show that the liquidator was wrong in admitting the proof of the debt. As Kennedy J said in Bradshaw v Medical Board (WA) at 328:

‘An appeal in the nature of a re-hearing under the [Medical Act 1984] remains an appeal and the court “must recognise the onus of the appellant to satisfy it that the decision below is wrong”: Powell v Streatham Manor Nursing Home at 255 per Lord Atkin.

Although Bradshaw v Medical Board (WA) concerned different legislation, the nature of an appeal under s 1321 is the same as that considered in that case and the rule mentioned by Kennedy J is equally applicable.”

26 More recently, in Lewis v Notrex Pty Ltd, Young CJ in Equity affirmed that the applicant has the onus “to establish the facts that would enable the proof of debt to be allowed” and “when one is trying a separate issue of fact, the same person bears the onus of proof as would have borne it had the question been tried with the rest of the questions at the final trial”: see at [15].

(Citations omitted, bold added)