FEDERAL COURT OF AUSTRALIA

Star Entertainment Group Limited v Chubb Insurance Australia Ltd [2021] FCA 907

ORDERS

DATE OF ORDER: | 5 August 2021 |

THE COURT ORDERS THAT:

1. Order 1 of the orders made on 18 November 2020 be varied such that the issues raised in prayer 3A(a) and (b) of the Amended Originating Application as amended on the first day of the hearing on 28 April 2021, and set out in [12] of the reasons herein, be heard separately and before any other issue in the proceeding.

2. For the sake of clarification and good order the ruling made on 28 April 2021 under s 136 of the Evidence Act 1995 (Cth) that the evidence led by both parties is subject to the limitation that it shall not be used as evidence of the extent of any business interference or interruption, or the quantum of any loss, is confirmed.

3. Paragraphs 52 to 57 of the affidavit of John Martin Kaldor affirmed 23 February 2021 are rejected.

4. Paragraphs 95 to 97, and 113 to 120 of the affidavit of Ramon Zenel Shaban affirmed 22 February 2021 are allowed.

5. The claim for declaratory relief made in prayer 3A(a) of the Amended Originating Application be dismissed with costs, such costs to be agreed or assessed.

6. The parties file and serve any further brief submissions as to the spoilage claim in prayer 3A(b) of the Amended Originating Application, in the following order:

(a) the Insurers within 14 days file any further submissions of no more than five pages;

(b) Star within 14 days thereafter file any further submissions of no more than five pages;

(c) any submissions properly in reply by the Insurers to be filed and served within seven days thereafter and to be no more than two pages.

7. The resolution of the spoilage claim be thereafter completed on the papers unless the parties or either of them require a further hearing in which case the party should contend for such in its further written submissions.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ALLSOP CJ

1 The applicants are companies in The Star Entertainment Group. The first applicant is the ultimate holding company. Unless otherwise necessary, I will refer to the applicants as Star or the Star group. The second to ninth applicants are all subsidiary or related companies of the first applicant. All applicants are insureds under an Industrial Special Risks (ISR) Insurance Policy numbered 01FX534331 (the Policy) issued by the eleven respondents (the Insurers). The Insurers comprise Chubb Insurance Australia, the first respondent, which holds 20% of the risk, the balance being held by various Australian and international insurers, being the second to eleventh respondents. The terms of the insurance are found in the Policy which was propounded in the broking process by Star’s broker (a well-known and large international insurance broker, carrying on business in Australia) whose logo (Marsh) appears on each page of the Policy.

2 Through the various applicants the Star group conducts casinos in Sydney, Brisbane and the Gold Coast and conducts associated hotel, food and beverage, and retail businesses at various sites.

3 The claim for indemnity is for business interruption loss as a consequence of the governmental restrictions in 2020 in response to COVID-19 on travel into and within Australia and on movement and congregation of people in Australia, including the closure of the various premises of Star by governmental order.

4 For reasons more fully set out below, the claim for indemnity fails. The Policy, on its proper construction, does not respond to the claims as made.

My reasons in summary form

5 I accept that there is danger in bringing to the task of contractual interpretation a false paradigm of structure by reference to assumptions not borne out by the words agreed by the parties. The relevant parties to the broking and placing of the risk are an internationally recognised broker (Marsh) propounding (on behalf of a sophisticated business group, Star) a form of words to a group of underwriters. The type of Policy is well-known: an industrial special risks policy combining indemnity in one section for the physical loss, destruction or damage to property of the insured, and, in a second section, providing for indemnity for loss resulting from interruption of business from the physical loss, destruction or damage of the property of the insured brought about by insured perils.

6 The physical loss or destruction of or damage to revenue or turnover or profit generating property can be seen to be the core of the Policy. But, as shall be seen, physical interference with the insured’s profit generating property is not the only way an insured can suffer loss (whether of revenue, turnover, or profit). The Policy recognises this in the provisions to which I will come, which extend cover beyond this core of the Policy.

7 The case really turns on the proper construction of one of the memoranda to the second section of the Policy which extends coverage. The heading of the memorandum is “Civil Authority Extension”. That heading, however, is to be put to one side as not able to be used in the construction or interpretation of the Policy: cl 19 of conditions applicable to all sections. The terms of the memorandum 7 are as follows:

CIVIL AUTHORITY EXTENSION

The word “Damage” under Section 2 of this Policy is extended to include loss resulting from or caused by any lawfully constituted authority in connection with or for the purpose of retarding any conflagration or other catastrophe.

8 The indemnity clause of section 2 of the Policy is in the following terms:

THE INDEMNITY

In the event of any building or any other property or any part thereof used by the Insured at the Premises for the purpose of the Business being physically lost, destroyed or damaged by any cause or event not hereinafter excluded (loss, destruction or damage so caused being hereinafter termed ‘Damage’) and the Business carried on by the Insured being in consequence thereof interrupted or interfered with, the Insurer(s) will, subject to the provisions of this policy including the limitation on the Insurer(s) liability, pay to the Insured the amount of loss resulting from such interruption or interference in accordance with the applicable Basis of Settlement.

Provided that the Insurer(s) will not be liable for any loss under this Section unless the Insured’s property lost, destroyed or damaged is insured against such Damage and the Insurer or Insurers by which such property is insured shall have paid for, or admitted liability in respect of, such Damage unless no such payment shall have been made or liability shall not have been admitted therefor solely owing to the operation of a provision in such insurance excluding liability for loss below a specific amount.

9 Distilled to its essence Star submits that the Civil Authority Extension extends the word Damage from physical damage to damage by loss of use or custom or financial loss resulting from the many acts and orders of various governments in connection with, or for the purposes of retarding, the catastrophe of the COVID-19 pandemic.

10 The fundamental difficulty with that distilled simplicity is that it provides cover, without any sub-limit, and so up to $4 billion, for the consequences of government activity in connection with or to retard a catastrophe which itself is not an insured peril. This is not catastrophe insurance. No provision provides cover for the business consequences brought about by the spread of COVID-19 or by a catastrophe of the spread of any disease. Yet the construction propounded by Star provides full cover for the business interruption caused by government orders in connection with, or to retard, the catastrophic spread of the disease, notwithstanding that the pandemic, being the posited catastrophe, is not an insured peril.

11 The argument of Star should be rejected for two essential reasons that are related, but distinct. First, the better construction, and one conforming with the whole Policy, is to construe the words “conflagration or other catastrophe” in the Civil Authority Extension to refer to events or occurrences capable of or apt to cause physical loss or destruction of or damage to the property of the Insured at the Premises: that is, such events or occurrences as would be or are apt to be an insured peril. Secondly, the loss referred to in the Civil Authority Extension is the physical loss of property not the loss of use of the property or loss of custom or financial loss.

The scope of the hearing

12 The hearing before me on 28 and 29 April 2021 was to determine whether a declaration should be made in terms of prayer 3A of the Amended Originating Application dated 21 October 2020, as amended in oral submissions on 28 April. That declaration, with relevant amendments, was in the following terms:

3A. A declaration that the Respondents are obliged to indemnify the Applicants:

(a) under the Section 2 indemnity as extended by the Civil Authority Extension for any economic loss of the kind referred to in paragraph 14 of the Amended Concise Statement;

(b) under the Section 1 indemnity as extended by Section 1, Memoranda clause 14 for the loss referred to in paragraph 24E of the Amended Concise Statement.

13 Paragraph (b) of prayer 3A concerned a claim for spoilage of food and consumables. It was a confined claim and quite separate from the claim in para (a). The spoilage claim is dealt with at the end of the judgment.

14 Paragraph 14 of the Amended Concise Statement (ACS) referred to in prayer 3A(a) is set out below. It is to be understood by what precedes it in the ACS. These matters preceding were largely uncontentious.

15 The Star group own and operate casinos, hotels, food and beverage management businesses, convention centres, entertainment and parking facilities in Queensland and New South Wales: ACS [1].

16 The Policy insured all applicants (the first as a party to the Policy, and the second to ninth as third party beneficiaries under s 48 of the Insurance Contracts Act 1984 (Cth) (IC Act) against risks including business interruption from 4.00pm 1 November 2019 to 4.00pm 1 November 2020: ACS [2].

17 The ACS [4]–[10] described the outbreak of COVID-19 as follows:

4. By late December 2019 a novel viral disease was detected in the Chinese city of Wuhan. The virus was later named severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2) and the disease it caused in humans was later named COVID-19.

5. COVID-19 is capable of causing severe illness in humans and can be fatal. It is highly contagious. It can spread easily from person to person through, among other things, close contact, contact with respiratory droplets from an infected person and contact with contaminated objects or surfaces. COVID-19 can spread from an infected person even while they are pre-symptomatic (during the long incubation period) or asymptomatic. There is an absence of community immunity to COVID-19, no antiviral treatment and no vaccine.

6. By January 2020 cases of COVID-19 had been confirmed in other parts of China and the world, including the United States of America, United Kingdom and Japan. The first confirmed cases of COVID-19 in Australia were on 25 January 2020 in both Victoria and New South Wales, with the first confirmed case in Queensland being on 28 January 2020. The first confirmed death from COVID-19 in Australia was on 1 March 2020 in Western Australia, with the first confirmed death in New South Wales being on 4 March 2020 and the first confirmed death in Queensland being on 25 March 2020.

7. On 30 January 2020 the World Health Organisation declared COVID-19 a Public Health Emergency of International Concern. On 11 March 2020 it declared COVID-19 a pandemic.

8. By February 2020 (and thereafter) COVID-19 was spreading rapidly throughout the world, causing illness and death and threatening to overwhelm hospitals. By 1 February 2020 global confirmed cases of COVID-19 exceeded 12,000. By 18 March 2020 they exceeded 200,000, by 23 March 2020 they exceeded 380,000 and by 29 March 2020 they exceeded 700,000. By 2 April 2020 global confirmed cases exceeded 1 million, by 28 June 2020 global confirmed cases exceeded 10 million and by 11 August 2020 global confirmed cases exceeded 20 million. The actual prevalence of COVID-19 was much higher than confirmed cases due to limited testing and asymptomatic cases.

9. On 18 March 2020 the Commonwealth Governor General declared (Biosecurity (Human Biosecurity Emergency) (Human Coronavirus with Pandemic Potential) Declaration 2020):

“Human coronavirus with pandemic potential is an infectious disease:

(a) that has entered Australian territory; and

(b) that is fatal in some cases; and

(c) that there was no vaccine against, or antiviral treatment for, immediately before the commencement of this instrument; and

(d) that is posing a severe and immediate threat to human health on a nationally significant scale.”

10. The severe and immediate threat to human health posed by COVID-19 was not only national, but international.

18 The response of Australian authorities was described in ACS [11]–[12] as follows:

11. On and from February 2020, lawfully constituted authorities within Australia have put in place restrictions and given advice to the public in connection with COVID-19, and are likely to continue to do so during the Policy period, including:

(a) restrictions on foreign nationals entering Australia or persons entering a state;

(b) restrictions on the number of persons permitted to gather on or in premises;

(c) restrictions on opening premises or on opening them in certain ways or without certain procedures in place;

(d) restrictions on the circumstances in which persons could leave their residence;

(e) advice that persons stay home and avoid non-essential travel.

12. The instruments imposing or recording those restrictions and that advice which The Star has identified as at the date of commencing this proceeding are listed in Annexure A. It is likely that further restrictions and advice will be put in place/given during the Policy period.

19 It is unnecessary presently to refer in detail to the State, Territory and Commonwealth health orders. Their nature and effects are, in broad terms, well-known.

20 The effect on the Star group was described in ACS [13] and [14], as follows:

13. The effect of the restrictions/advice referred to at [11] above was and will continue to be that the First Applicant, its subsidiaries and related entities (including the Second to Ninth Applicants), lost the ability to access or use its premises to conduct its business as intended or as it ordinarily would and/or lost custom, including because:

(a) it could not allow more than a certain number of persons on its premises;

(b) it could not undertake certain activities on its premises that it intended to undertake or ordinarily undertook as part of its business or could not undertake them in the manner it intended to or ordinarily did;

(c) it could not open certain businesses or premises at all;

(d) patrons (including overseas and interstate patrons) and staff could not, and/or did not, access its premises for certain purposes of the business or at all.

14. The Star’s business was and continues to be thereby interrupted and/or interfered with, and The Star has and continues to suffer economic loss, including a reduction in turnover and gross revenue, and an increased cost of working.

21 The ACS thereafter described the dispute and the essential arguments under the Policy for indemnity.

The evidence

22 Conformably with the parties’ desire to derive utility from the hearing, in particular concerning the proper construction and operation of the Policy, the parties agreed that I should make an order under s 136 of the Evidence Act 1995 (Cth) limiting the use of the evidence. This led to much of the evidence that was filed and read not being crucial to the resolution of the issue that the Court was asked to resolve at this point. To the extent that it is necessary I will describe the evidence, make any necessary findings and resolve the residual question of admissibility in a later section of these reasons.

Introduction

23 For present purposes, it is sufficient to describe the factual background to the claim which is largely uncontentious, before turning to the Policy and the arguments of the parties. The following outline is taken from the evidence.

24 The virus that came to be named COVID-19 is a highly contagious viral infection capable of causing serious illness and death. The virus reached Australia by 25 January 2020 with four confirmed cases in New South Wales and two in Victoria. In the following week, further cases were confirmed in Queensland, South Australia and Victoria. By 1 March there was a fatality.

25 On 30 January 2020, the World Health Organisation (WHO) declared the outbreak of COVID-19 a public health emergency of international concern. On 11 March 2020, the WHO declared the outbreak a pandemic because of “alarming levels of spread and severity”. This announcement included the following:

In the past two weeks, the number of cases of COVID-19 outside China has increased 13-fold, and the number of affected countries has tripled.

There are now more than 118,000 cases in 114 countries, and 4,291 people have lost their lives.

Thousands more are fighting for their lives in hospital.

In the days and weeks ahead, we expect to see the number of cases, the number of deaths, and the number of affected countries climb even higher.

26 The applicant led a significant body of evidence in support of the proposition that the sudden and unexpected emergence, escape from China and rapid spread throughout the world of a highly infectious and potentially fatal novel pathogen was a catastrophic biological event with potential and actual drastic human and economic consequences. The notion of “catastrophe” and “catastrophic” is important given the language of the Civil Authority Extension.

27 In response to the growing threat, governments around the world, including Commonwealth, State and Territory governments in Australia, took steps to prevent the spread of the virus. As will be seen in the discussion of the Policy, such steps can be seen as attempts to prevent or retard or slow down the spread of the virus.

28 In Australia, the response of governments included the following:

(a) on 1 February 2020 the Commonwealth government placed a ban on Chinese foreign nationals entering Australia;

(b) on 16 March 2020 the New South Wales government placed a ban on public events at which there were, or were likely to be, 500 persons or more in attendance;

(c) on 18 March 2020 the Commonwealth Governor General declared:

Human coronavirus with pandemic potential is an infectious disease:

(a) that has entered Australian territory; and

(b) that is fatal in some cases; and

(c) that there was no vaccine against, or antiviral treatment for, immediately before the commencement of this instrument; and

(d) that is posing a severe and immediate threat to human health on a nationally significant scale.

(d) also on 18 March 2020 the NSW government placed limits on the number of persons permitted to gather at a venue. Queensland followed suit on 19 March 2020;

(e) on 23 March 2020 the NSW and Queensland governments directed that businesses, other than those providing essential services, not open. By that time there had been 292,142 cases of COVID-19 reported globally and 12,784 deaths, of which 1,765 cases and 7 deaths were in Australia (with virus genome sequencing indicating introduction to Australia from China, Iran, Europe and the USA). Those numbers were likely to be lower than real numbers due to limited testing and asymptomatic cases.

29 From mid to late March 2020 onwards, there were further public health directions designed to limit the spread of the virus including border closures between States and parts of States, stay at home orders, and limits on the number of people (including Australian citizens) who were permitted to enter Australia.

30 Notwithstanding the measures taken Australia was affected significantly. March 2020 saw the postponement of non-urgent elective surgery, the closure of schools and the suspension of jury trials. By 7 June 2020 confirmed cases in Australia reached 7,277 and there had been 102 deaths. A second wave of infections occurred between June and September 2020, in particular in Victoria, and a further outbreak occurred in December 2020 in New South Wales. By 27 September 2020 confirmed cases in Australia had grown to 27,095 and there had been 835 deaths.

31 The economic consequences in Australia by the middle of 2020 were significant: Real GDP fell 7% in the June 2020 quarter (the highest on record) and Australia entered its first recession in 28 years. Unemployment increased from about 5% in March to 7% by the end of June 2020, albeit inhibited or ameliorated by the Commonwealth government’s economic support measures.

32 Internationally, as at 21 February 2021, and subject to likely under-reporting of actual numbers due to limits on testing and asymptomatic cases, there were over 110 million cases reported globally (28,920 in Australia) and there had been 2.44 million deaths (909 in Australia).

33 The interference with or interruption to the businesses of the applicants was said to have been brought about by the various particular restrictions promulgated by governmental orders. A summary of the effects were as follows.

34 The restrictions on foreign nationals entering Australia meant a loss of custom from international patrons who made up a substantial part of Star’s business.

35 In March 2020, New South Wales and Queensland restricted the number of persons who could gather at Star’s Premises, required the division of Premises into separate areas and led to the cancellation or postponement of certain events. Later in March Star was prohibited from opening business other than for the provision of takeaway food and drink and for accommodation. From May 2020, in both New South Wales and Queensland Star’s businesses were progressively permitted to reopen, but that was subject to strict conditions including the numbers of people who could be present and the requirements that the business be operated in accordance with approved plans which involved limiting patron numbers and movements, restaurant settings and the numbers of players at gaming tables; and the closing of rooms for a period each day for cleaning and disinfection.

36 The restrictions in interstate movements by closure of borders or the requirement to quarantine affected the number of interstate visitors, who were a material part of Star’s ordinary custom.

37 From March 2020, restrictions on the circumstances in which persons could leave their residences and governmental advice to avoid non-essential travel prevented or discouraged people coming to Star’s business.

38 Star points to all these restrictions to explain the substantial drop in visitation numbers from February 2020 in Sydney and from March 2020 in Brisbane and the Gold Coast compared to the prior year.

39 Star’s business as a landlord is said to have been interfered with for the same reasons.

The Policy

40 The Policy is a carefully worded document. There were two sections to the Policy: section 1 “material loss or damage” and section 2 “consequential loss”. The claim is made under section 2, but it is important to understand the operation of section 1.

41 The Policy commenced with a note that it “does not insure against machinery breakdown, data processing/media failure breakdown and boiler & pressure vessel explosion, collapse etc”. Another policy covered such perils. The Policy then contained a statement of the structure of the Policy and of the indemnity:

This Policy incorporates the Schedule, Sections, Definitions, Conditions, Exclusions, Endorsements, Memoranda and Warranties (if any) and any other terms herein contained which are to be read together and any word or expression to which a specific meaning has been given in any part of this Policy shall bear this meaning wherever it may appear unless such meaning is inapplicable to the context in which the word or expression appears.

WHEREAS the Insured named in the Schedule has paid or agreed to pay to the Insurer(s) specified below the Premium shown on the Schedule, now the Insurer(s) agree(s), subject to the terms, Conditions, Exclusions, Memoranda, Warranties, limitations and other provisions contained herein or endorsed hereon, to indemnify the Insured as specified herein against loss arising from any insured events which occur during the Period of Insurance stated in the Schedule or any renewal thereof.

….

42 The Schedule set out the Insured and the Business. The Interest Insured for section 1 was real and personal property defined as:

All real and personal property of every kind and description (except as hereinafter excluded) belonging to the Insured or for which the Insured is responsible, or has assumed responsibility to insure prior to the occurrence of any damage, including all such property in which the Insured may acquire an insurable interest during the Period of Insurance.

43 The Interest Insured for section 2 was, relevantly:

(i) Business Interruption of Gross Profit and other Business Interruption as defined.

…

44 The period of insurance was from 4.00pm on 1 November 2019 to 4.00pm on 1 November 2020. The various Premises were identified. The declared values and items of consequential loss were set out. Limits of liability for sections 1 and 2 combined for different locations were set out: $4 billion for the Star Casino and hotel in Sydney, $1.75 billion for the Gold Coast and $1.43 billion for Brisbane with lower limits for other locations. The sub-limits for section 2 consequential loss included a $1 million limit in the annual aggregate for Memorandum 9 “Infectious Disease Murder Closure”.

45 Relevant to the spoilage claim in prayer 3A(b) were the various sub-limits of liability and the stated deductibles in respect of section 1.

46 Sub-limits to section 1 were as follows:

Section 1 – Material Damage

The liability of the Insurer(s) shall be further limited in respect of any one loss or series of losses at any one Situation arising out of any one original source or cause as set out hereunder and it is understood and agreed that such Sub Limit(s) shall not increase the liability of the Insurer(s) beyond the Limit(s) of Liability expressed above and also the undermentioned deductible(s) will apply in respect of such Sub-Limit(s) but shall not be cumulative.

Removal of Debris –The Indemnity-Clause (f) (i) to (ii) only | $ 30,000,000 |

Provision (iii) of Extra Cost of Reinstatement Memorandum no 6 | $25,000,000 |

Additional Extra Cost of Reinstatement-Memorandum no 7 | $ 20,000,000 |

Accounts Receivable | $ 10,000,000 |

Expediting Expenses -The Indemnity (k) | $ 10,000,000 |

Food Spoilage/Deterioration of Stock-Memorandum 14 | $ 250,000 |

Personal Effects of directors or employees or property of clubs-The Indemnity (g) | $ 20,000 per person per club |

Accidental Damage (as defined) | $ 20,000,000 |

Cash and Paper Money-Limited Cover- Memorandum no 16 | $ 25,000,000 |

Burglary & Theft of Property | $ 1,000,000 |

Rewriting of Records –Basis of Settlement (e) | $2,500,000 |

Art Works, antiques and curios –Basis of Settlement (k) | $5,000,000 |

Landscaping –The Indemnity (l) | $1,000,000 |

Cleaning and Decontamination of Property –The Indemnity (m) | $ 500,000 |

Statutory Inquiries-The Indemnity (n) | $ 500,000 |

Payment of Reward -The Indemnity (o) | $ 100,000 |

Exploratory Costs -The Indemnity (q) | $ 100,000 |

Loss of Land Value –Memorandum no 10 | $2,000,000 |

Additional Income Tax | $ 250,000 |

(Emphasis added)

47 Deductibles for sections 1 and 2 were (relevantly as to section 2) as follows:

The Insured shall bear the following amount(s) in respect of each claim or series of claims arising out of any one event.

Earth quake, Subterranean Fire or Volcanic Eruption - $20,000 or 1% of Declared Values at the site where the damage occurred, whichever is the lesser.

Section 1 – Material Damage

The Star Hotel and Casino Sydney including The Darling Hotel Sydney; The Star Hotel and Casino Gold Coast including The Darling Hotel Gold Coast; Treasury Casino and Hotel Brisbane and associated buildings - $750,000.

Cash and Paper Money –Limited Cover $750,000.

All Other including Head Office locations, Gold Coast Convention and Exhibition Centre - $50,000.

Personal Property of Directors, Employees, Clubs and Visitors - $1,000.

Section 2 – Consequential Loss

The Star Hotel and Casino including The Darling Hotel Sydney; The Star Hotel and Casino Gold Coast including The Darling Hotel Gold Coast; Treasury Casino and Hotel Brisbane and associated buildings – the first 5 Trading Days (Time Deductible) following loss or Damage to the Premises provided that where the quantum of the loss for the first 5 Trading Days exceeds $5,500,000, then the Deductible for the first 5 Trading Days following loss or Damage to the Premises will be capped at $5,500,000.

All Other including Head Office locations, Gold Coast Convention & Exhibition Centre - the first 2 Trading Days (Time Deductible) following loss or Damage to the Premises provided that where the quantum of the loss for the first 2 Trading Days exceeds $750,000 then the Deductible for the first 2 Trading Days following loss or Damage to the premises will be capped at $750,000.

...

48 The consequential loss indemnity period was set out in the Schedule. For the Sydney casino and hotel the periods are substantial and include 60 months for the main gaming floor and electronic gaming hall and 12 months for private gaming. For the “Infectious and Contagious Disease Clause” (memorandum 9) the indemnity period was three months. This latter clause, to which significant reference will be made, and to which I will refer as the Disease Extension appeared in the Policy near the Civil Authority Extension (memorandum 7) and is important to the resolution of the construction of the reach of the Civil Authority Extension.

49 The indemnity in section 1 for material loss and damage was as follows:

In the event of any physical loss, destruction or damage (hereinafter in Section 1 referred to as 'Damage' with 'Damaged' having a corresponding meaning) not otherwise excluded happening at the Situation to the Property Insured described in Section 1 the Insurer(s) will, subject to the provisions of this Policy including the limitation on the Insurer(s) liability, indemnify the Insured in accordance with the applicable Basis of Settlement.

50 Subject to limits of liability there was additional cover in section 1 for things such as professional fees, government or statutory authority fees, costs of fire extinguishment, debris removal, temporary protection costs, expediting expenses and other natural incidental expenses in dealing with major property damage. The indemnity for costs of extinguishing a fire was in the following terms:

Costs of Extinguishing a Fire

costs and expenses necessarily and reasonably incurred for the purpose of extinguishing fire at or in the vicinity of property hereby insured or threatening to involve such property or for the purpose of preventing or diminishing imminent Damage to property hereby insured by any other peril insured against by this Policy, including:

(i) damage to gain access and the cost of replenishment of fire fighting appliances;

(ii) charges incurred for the purpose of shutting off the supply of water or other substance following accidental discharge from any fire protective equipment or otherwise escaping from intended confines;

(iii) the cost of replacing any fire protective equipment with a different type of equipment, which has similar capabilities to the equipment being replaced, as a consequence of the discharge of any substance therefrom (such discharge being either accidental or malicious or for the purpose of extinguishing fire) and where replacement with such different type of equipment is required by law;

(iv) any liability incurred for fire brigade attendance fees solely because any part of the Insured's claim for Damage is within the amount of any Deductible applicable under this Policy

(v) all post fire extinguishment related costs not otherwise covered by this Policy.

This clause (c) applies whether or not Damage occurs to Property Insured in circumstances giving rise to indemnity under Section 1 of this Policy.

51 The property insured in section 1 was relevantly defined widely in terms substantially similar to the expression of the “interest insured” under section 1 in the Schedule ([42] above):

All real and personal property of every kind and description (except as hereinafter excluded) belonging to the Insured or for Damage to which the Insured is responsible, or has assumed responsibility to insure prior to the occurrence of any Damage, including all such property in which the Insured may acquire a pecuniary or economic interest, pending transfer of legal title to such property or for Damage to which the Insured becomes responsible or assumes responsibility to insure, after the commencement of the Period of Insurance.

…

52 The 16 memoranda to section 1 included two memoranda that dealt with government intervention. Memorandum 6 “Extra Cost of Reinstatement” included the following:

This Policy extends to include the extra cost of reinstatement (including demolition or dismantling) of Damaged Property Insured and/or undamaged Property Insured necessarily incurred to comply with the requirements of any Act of Parliament or Regulation made thereunder or any By-Law or Regulation of any Municipal or other Statutory Authority, subject to the following Provisions and subject also to the Terms, Conditions and Limit(s) or Sub Limit(s) of Liability of this Policy.

…

53 Memorandum 13 “Undamaged Foundations” contained the following:

For the purpose of the indemnity provided under the policy where property is destroyed but the foundations are not destroyed and due to the exercising of Statutory powers and/or authority by Government Department, Local Government or any other Statutory Authority reinstatement of the property has to be carried out upon another site then the abandoned foundations will be considered as being destroyed provided that if the presence of the abandoned foundations increases the resale value of the original property site then such increase in resale value shall be regarded as salvage and the amount thereof shall accordingly be payable to the Insurers by the Insured.

…

54 Memorandum 14 dealt with “Spoilage”:

Notwithstanding anything herein contained to the contrary it is agreed that the Policy under The Indemnity - Material Loss or Damage covers loss, destruction of or damage to stock and/or merchandise caused by deterioration, putrefaction, contamination or changes in temperature arising from any cause whatsoever other than work bans, shortage of fuel or the deliberate withholding of electricity supply.

55 The indemnity in section 2 is set out at [8] above.

56 There were five items in the Basis of Settlement. “Item No 1” was directed at loss of Gross Profit due to Reduction in Turnover, and Increase in Cost of Working, as follows:

The Insurance under this item is limited to loss of Gross Profit due to: (a) Reduction in Turnover and (b) Increase in Cost of Working and the amount payable as indemnity thereunder shall be:-

(a) In respect of Reduction in Turnover:

the sum produced by applying the Rate of Gross Profit to the amount by which the Turnover during the Indemnity Period shall, in consequence of the Damage, fall short of the Standard Turnover,

(b) In respect of Increase in Cost of Working:

the additional expenditure necessarily and reasonably incurred for the sole purpose of avoiding or diminishing the reduction in Turnover which, but for that expenditure, would have taken place during the Indemnity Period in consequence of the Damage, but not exceeding the sum produced by applying the Rate of Gross Profit to the amount of the reduction thereby avoided,

less any sum saved during the Indemnity Period in respect of such of the charges and expenses of the Business payable out of Gross Profit as may cease or be reduced in consequence of the Damage (excluding depreciation and amortisation).

57 Item No 2 gave the insured an election to have the amount of the loss calculated in accordance with the “Gross Revenue Basis of Settlement”, as follows:

The Insured may elect to have the amount of loss calculated in accordance with the Gross Revenue Basis of Settlement Item No. 2 set out hereunder in lieu of Item No. 1 Gross Profit subject to Gross Revenue being the basis upon which the Business Interruption values were declared for that Premises. Nothing contained herein will preclude the Insured from also claiming under Section 2 Item No’s. 4 and 5 where applicable.

Item no. 2

The Insurance under this Item is limited to loss of Gross Revenue due to (a) Reduction in Gross Revenue and (b) Increase in Cost of Working and the amount payable as indemnity thereunder shall be:

(a) In respect of reduction in Gross Revenue: The amount by which the Gross Revenue during the Indemnity Period shall, in consequence of the Damage, fall short of the Standard Gross Revenue,

(b) In respect of Increase in Cost of Working: The additional expenditure necessarily and reasonably incurred for the sole purpose of avoiding or diminishing the reduction in Gross Revenue which, but for that expenditure, would have taken place during the Indemnity Period in consequence of the Damage, but not exceeding the amount of the reduction in Gross Revenue thereby avoided,

less any sum saved during the Indemnity Period in respect of such charges and expenses of the Business as may cease or be reduced in consequence of the Damage (excluding depreciation and amortisation).

58 Item No 3 dealt with conduct of business in departments whose results were ascertainable as business units, and where income was from rental the insured could elect to use the Gross Rentals Basis of Settlement.

59 Item No 4 covered reasonable professional fees.

60 Item No 5 covered additional increased cost of working, as follows:

The insurance under this item is limited to any Additional Increased Cost of Working (not otherwise recoverable under Items 1,2 and/or 3 above) reasonably incurred during the Indemnity Period in consequence of the Damage for the purpose of avoiding or diminishing reduction in Turnover and/or Gross Revenue and/or Gross Rentals and/or resuming and/or maintaining normal operations and/or services of the Business.

61 Various terms were defined including (not all words and phrases in the Policy beginning with capital letters were defined):

GROSS PROFIT means the amount by which:-

(a) the sum of the Turnover and the amount of the Closing Stock and Work in Progress shall exceed

(b) the sum of the amount of the Opening Stock and Work in Progress and the amount of the Uninsured Working Expenses as set out in the Schedule.

…

TURNOVER means the money (less discounts, if any allowed) paid or payable to the Insured for goods sold and delivered and for services rendered in course of the Business at the Premises.

GROSS REVENUE means the money paid or payable to the Insured for services rendered (and goods, if any, sold) in the course of the Business at the Premises.

…

INDEMNITY PERIOD means the period beginning with the occurrence of the Damage and ending not later than the number of months specified in the Schedule thereafter during which the results of the Business shall be affected in consequence of the Damage.

…

SHORTAGE IN TURNOVER means the amount by which the Turnover during a period shall, in consequence of the Damage, fall short of the part of the Standard Turnover which relates to that period.

RATE OF GROSS PROFIT means the rate of Gross Profit earned on the Turnover during the financial year immediately before the date of the Damage.

STANDARD GROSS REVENUE means the Gross Revenue during that period in the twelve (12) months immediately before the date of the Damage which corresponds with the Indemnity Period (appropriately adjusted where the Indemnity Period exceeds twelve months).

STANDARD TURNOVER means the Turnover during that period in the twelve (12) months immediately before the date of the Damage which corresponds with the Indemnity Period (appropriately adjusted where the Indemnity Period exceeds twelve months).

62 After these definitions, there was a clause sometimes referred to as the “other circumstances clause”, see Roberts H, Riley on Business Interruption Insurance (Sweet & Maxwell, 10th ed, 2016) at 47–48 [3.25], as follows:

Adjustments shall be made to the Rate of Gross Profit, Standard Turnover, Standard Gross Revenue, and Standard Gross Rentals as may be necessary to provide for the trend of the Business and for variations in or other circumstances affecting the Business either before or after the date of the Damage or which would have affected the Business had the Damage not occurred, so that the figures as adjusted shall represent as nearly as may be reasonably practicable the results which but for the Damage would have been obtained during the relative period after the Damage occurred.

63 There then appeared 20 memoranda to section 2. They were introduced by the following qualification (identical to that which preceded the 16 memoranda to section 1):

Except to the extent this Policy is hereby modified under the following Memoranda the terms, Conditions and limitations of this Policy shall apply.

64 In written submissions, Star noted that “exclusions” were not referred to, though no reliance was placed on this omission in oral address. Notwithstanding the introduction to the structure of the Policy (see [41] above), there is a significance in the omission of the word “exclusions” in the preambles to the two sets of memoranda to sections 1 and 2 with which I will deal in due course.

65 The “Civil Authority Extension” is set out at [7] above.

66 Memorandum 8 “General Area Damage Extension” was as follows:

Loss as insured by Section 2 of the policy resulting from interruption or interference with the Business in consequence of Damage to property within a 10 kilometre radius of the Premises which results in cessation or diminution of Business due to temporary falling away of potential custom shall be deemed to be loss resulting from Damage to property used by the Insured at the premises. Property Exclusions 4, 9, 10, 14 shall not apply to the cover granted by this extension.

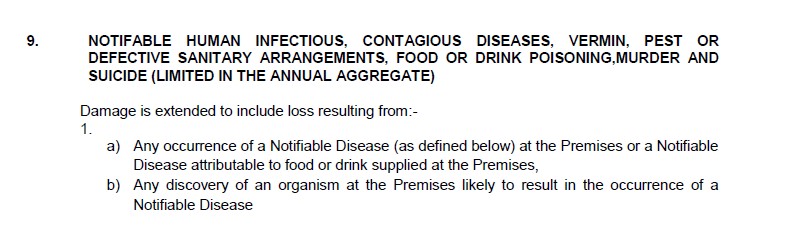

67 Memorandum 9 (the Disease Extension) is important as it deals with infectious disease and other matters, and was as follows:

Damage is extended to include loss resulting from:-

1.

a) Any occurrence of a Notifiable Disease (as defined below) at the Premises or a Notifiable Disease attributable to food or drink supplied at the Premises,

b) Any discovery of an organism at the Premises likely to result in the occurrence of a Notifiable Disease

2. The discovery of vermin or pests at the Premises,

3. Any accident causing defects in the drains or other sanitary arrangements at the Premises, which causes restrictions on the use of the Premises on the order or advice of the competent Local Authority

4. Any occurrence of murder or suicide at the Premises

Special Provisions

(a) Notifiable Disease shall mean illness sustained by any person resulting from

1. Food or drink poisoning or

2. An occurrence of a human infectious or human contagious disease which the competent Local Authority has stipulated shall be notified to them, with the exception of any occurrence, whether directly or indirectly, arising from Quarantinable disease listed in the Bio Security Act 2015, which are all specifically excluded hereunder.

(b) For the purpose of the extension Indemnity Period shall mean the period during which the results of the Business shall be affected in consequence of the Damage, beginning with the date from which the restrictions on the Premises are applied (or in the cast of 4, above, with the date of the occurrence) and ending not later than the maximum Indemnity Period thereafter.

Maximum Indemnity Period shall mean 3 months.

Premises shall mean only those locations stated in the Premises definition situate [sic] in Australia. In the event that the Material Damage or Business Interruption sections include an extension which deems Damage at other locations to be Damage at the Premises such extension shall not apply to the Extension.

(c) The Insurer shall not be liable under this extension for any costs incurred in the cleaning, repair, replacement and recall or checking of property

(d) The Insurer shall only be liable for loss arising at those premises which are directly subject to the Damage

(e) The liability of the Insurer shall not exceed the inner Limit of Liability stated in the specification

(f) Notwithstanding Special Provision (c), the insurance by this extension extends to include the costs and expenses necessarily incurred with the consent of the Insurer in

1. Cleaning and decontamination of property used by the Insured for the purpose of the Business (other than stock in trade)

2. Removal and disposal of contaminated stock in trade

At or from the Premises, the use of which has been restricted on the order or advice of the competent Local Authority solely in consequence of the Damage as defined above.

Notifiable Disease – AUD $1,000,000 in the aggregate any one period of Insurance

68 As will become clear, it is important to recognise that the typed form of the first part of the Disease Extension was as follows:

There is an issue of construction whether the words “which causes restrictions on the use of the Premises on the order or advice of the competent Local Authority” qualify 1, 2 and 3 or whether they are part of 3 and not qualifying of 1 and 2.

69 Memorandum 10 “Isolation by Landslip or Flood Extension” was as follows:

Loss as insured by Section 2 of the policy resulting from interruption of or interference with the Business in consequence of blockage of roads or railway links, bridges or tunnels caused by landslide or flood and which prevents or hinders the use of or access to the Premises shall be deemed to be loss resulting from Damage to property used by the Insured at the Premises. Property Exclusion 9 shall not apply to the cover granted by this extension.

70 Memorandum 11 “Public Utilities Extension” was as follows:

Loss as insured by Section 2 of the policy resulting from interruption of or interference with the Business in consequence of Damage to property, caused by a peril damage as a result of which is insured hereunder, at any communication link and/or any electric power station or sub-station, gasworks (including any land based premises of any gas supply undertaking or of any natural gas producer linked directly therewith) or water works including the distributive system from which the Insured obtains electric current, gas or water which is situated anywhere in Australia shall be deemed to be loss resulting from Damage to property used by the Insured at the Premises. Property Exclusions 16 and 17 shall not apply to this extension.

….

71 Memorandum 13 “Computer Extension” was as follows:

This Policy extends to include loss (not otherwise recoverable) resulting from interruption of or interference with the Business occasioned by Damage to computer installations, including ancillary equipment and data processing media utilised by the Insured anywhere in Australia.

72 Memorandum 15 “Premises in the Vicinity (Prevention of Access) Extension” was as follows:

Loss as Insured by this Policy resulting from interruption of or interference with the Business in consequence of Damage to property in the vicinity of the Premises caused by a peril, damage as a result of which is insured hereunder, which shall prevent or hinder the use thereof or access thereto, whether the Premises or property of the Insured therein shall be damaged or not, shall be deemed to be loss resulting from Damage to property used by the Insured at the Premises.

Loss as insured by this Policy resulting from interruption of or interference with the Business in consequence of Damage to property in the vicinity of and forming part of or contained in the complex of which the Premises forms part caused by a peril, damage as a result of which is insured hereunder, which results in a cessation or diminution of trade due to temporary falling away of potential custom, whether the Premises or property of the Insured therein shall be damaged or not, shall be deemed to be loss resulting from Damage to property used by the Insured at the Premises.

73 Memorandum 16 “Registered Vehicles and/or Trailer Extension” was as follows:

Notwithstanding the provisions of Property Exclusion 5, this Policy extends to include loss resulting from interruption of or interference with the Business occasioned by Damage to registered vehicles and/or trailers whilst such vehicles or trailers are at the Premises owned or occupied by the Insured; provided always that this Policy does not cover loss resulting from physical loss, destruction of or damage to such vehicles and/or trailers whilst they are being used on any public highway or thoroughfare.

74 Memorandum 18 “Suppliers and Customers Extension” was as follows:

Loss as insured by Section 2 of the Policy resulting from interruption of or interference with the Business in consequence of Damage to property at or in the vicinity of premises of the Insured's suppliers, manufacturers processors or storers of components, goods or materials or services or customers shall be deemed to be loss resulting from Damage to property used by the Insured at the premises.

75 Memorandum 19 “Violent Threat of Damage Extension” was as follows:

Loss as insured by Section 2 of the Policy resulting from interruption of or interference with the Business carried on by the Insured at the Premises in direct consequence of violent threat of damage to the premises and/or injury to persons therein. Provided that this necessitates the closure of the whole or part of the premises by order of competent Public Authority.

Provided always that the liability of the Insurers shall in no case under this memorandum of the policy exceed $5,000,000 any one loss and in the annual aggregate

76 The exclusions to the Policy were headed “Exclusions to All Sections”. There then appeared under the heading “Property Exclusions” 17 clauses identifying different types of property excluded, the chapeau to which enumeration was as follows:

This Policy does not cover physical loss, destruction of or damage to the following property or loss under Section 2 resulting therefrom:-

77 There then appeared under the heading “Perils Exclusions” 13 clauses, preceded by a chapeau which read:

The Insurer(s) shall not be liable under Sections 1 and 2 in respect of:-

78 Perils exclusion 1(b) was as follows:

1. physical loss, destruction of or damage to the Property Insured

…

(b) resulting from confiscation, nationalisation, requisition or damage to property by or under the order of any Government or Public or Local Authority

Notwithstanding the provisions of Perils Exclusion 1(b) the Insurer(s) shall be liable for loss, destruction of or damage to, or the cost of removal of, sound property at the Premises for the purpose of preventing or diminishing imminent damage by, or inhibiting the spread of, fire or any other peril insured against under this Policy.

79 Perils exclusion 3 was as follows:

3. physical loss, destruction or damage occasioned by or happening through water from or action by the sea, river, tidal wave or high water. Provided that this Exclusion shall not apply if loss, destruction or damage is caused by or arises out of an earthquake, named cyclone, storm and tempest, flood, volcanic eruption, seismological disturbance or any other clearly identifiable, sudden and unforeseen circumstance.

80 Perils exclusion 4(a) was as follows:

4. physical loss, destruction or damage occasioned by or happening through:-

(a) moths, termites or other insects, vermin, rust or oxidation, mildew, mould, wet or dry rot, corrosion, change of colour, dampness of atmosphere or other variations in temperature, evaporation, disease, inherent vice or latent defect, loss of weight, change in flavour texture or finish, smut or smoke from industrial operations (other than sudden and unforeseen damage resulting therefrom)

…

(emphasis added)

The arguments of the parties

Star’s written submissions

81 Star addressed in written submissions two constructional issues: the meaning of “loss” in memorandum 7 and the meaning of “catastrophe” in memorandum 7.

82 Star submitted that “loss” in the first line of the Civil Authority Extension should be given its ordinary meaning which includes loss of ability to use property and associated losses of loss of custom and financial loss. This would extend section 2 indemnity to cover business interruption losses of any kind caused by conduct of a lawfully constituted authority in connection with or for the purpose of retarding any conflagration or other catastrophe. The extension of the word “Damage”, which in the indemnity clause is restricted to physical loss, destruction or damage, to include “loss resulting from or caused by any lawfully constituted authority” extends the concept of loss to non-physical loss, including loss of ability to access or use Premises for the Business, a loss of custom and economic loss.

83 Star submitted that the COVID-19 pandemic is a “catastrophe” and the governmental orders were conduct of lawfully constituted authorities to retard it. It was submitted that a “catastrophe” is a sudden and widespread disaster, referring to available dictionary meanings and is not limited to physical events such as fire, flood or earthquake. Star referred to a document of Chubb (otherwise irrelevant to the Policy) being a document filed with the United States Securities and Exchange Commission in 2020 which referred to Chubb’s exposure to losses from “natural disasters, man-made catastrophes such as terrorism or cyber attack, and other catastrophic events, including pandemics”.

84 Star submitted that any restriction of the meaning of “catastrophe” by its association with “conflagration” to a physical event, such as a fire (from the word “conflagration”) was to misread the clause. “Other catastrophe” confines the meaning of “conflagration”: only conflagrations that are catastrophic are included. A genus containing physicality of property was not established.

85 Star submitted that memorandum 9 should not be treated as the only cover that the Policy provides for business interruption in connection with a human contagious disease. The two extensions: Civil Authority (memorandum 7) and Disease (memorandum 9) were intended to extend cover in their own respective spheres. The terms of one should not be used to cut down the cover of another. This was to meet the argument put by the Insurers that it was not logical for the Disease Extension to exclude quarantinable disease (see special provision (a)(2)) for the limited $1 million cover and yet give full cover (up to $4 billion) for steps to retard the spread of a quarantinable disease under the Civil Authority Extension. The two memoranda were said to be dealing with different subject matters: the Disease Extension dealt with a risk on the insured’s Premises and over which the insured has a measure of control both as to occurrence and consequences or continuation; the Civil Authority Extension dealt with a risk beyond the insured’s control (as to occurrence and continuation).

86 This separate construction of the two memoranda was assisted, it was submitted, by recognising that insurance policies may be constructed by “bolting on” clauses from different precedents at different times: Pickford & Black Ltd v Canadian General Insurance [1974] 53 DLR (3d) 277 at 280.

The Insurers’ written submissions

87 The Insurers’ written submissions were more intensely detailed and sought to emphasise the structure and purpose of the Policy. They began with the proposition that the fundamental object and purpose of the Policy was to provide indemnity for various perils that cause physical loss, destruction or damage (Damage) to real and personal property of the insured (in the relevant sense). That fundamental object or purpose, reflected in the two indemnity clauses in sections 1 and 2 meant that unless there was some extension the Policy simply did not cover loss of business caused by a disease or a pandemic affecting the patronage or turnover or gross profit of the businesses. The primary cover is for physical Damage in section 1 and the business consequences of such physical Damage in profit, turnover or rentals depending upon the Basis of Settlement applicable or chosen in section 2.

88 Extensions were provided under section 2 to that primary cover, including the Civil Authority Extension and the Disease Extension. The latter was submitted to be crucial: the parties specifically directed themselves to loss suffered by reason of diseases such as COVID-19: Such were to be excluded from the reach of the extension of cover in memorandum 9, COVID-19 being a “Quarantinable disease listed in the Biosecurity Act 2015”. The flaw or structural weakness in Star’s argument, it was submitted, was that it ignored the Policy as a whole and the other extensions and construed the contractual language acontextually in an attempt to engage cover.

89 Looking to the Civil Authority Extension, the Insurers submitted that it was only engaged in the following circumstances:

(a) The phrase “conflagration or other catastrophe” meant that the “other catastrophe” like “conflagration” was physical: the genus was physical property.

(b) The catastrophe must be occurring, as opposed to there being a risk or threat, and must have geographical proximity to the insured property.

(c) The civil authority takes action in connection with or for the purpose of retarding the catastrophe which is underway as opposed to taking action to prevent the catastrophe occurring. (In oral address this element was varied to the loss of the property in a physical sense, which would, as a matter of meaning, encompass destruction but not mere damage to the property.)

(d) In the course of such action physical loss, destruction or damage is done to insured property.

90 The Insurers submitted that these integers were not satisfied. The COVID-19 pandemic was not a catastrophe of the same genus as a fire or conflagration. It was not an occurrence, event or incident which causes or is capable of causing widespread property damage. The pandemic was not a catastrophe, nor one which had any geographical proximity to the property insured. Even if the pandemic could be seen as a catastrophe, the governmental actions were not to retard a catastrophe which had commenced and was unfolding, but rather to limit the risk or harm of a threat of a catastrophe. Further, the governmental action caused no physical loss, destruction or damage to insured property.

91 The Insurers broke down these submissions into five issues of construction and five factual issues. Before dealing with these, the Insurers stressed the architecture of the Policy, which informed the proper approach to construction.

92 From that architecture, the first step is to understand the indemnity clauses for both sections 1 and 2. In section 2, this involved the physical Damage to the building or other property used by the Insured at the Premises for the purpose of the Business “by any cause or event not hereinafter excluded”. Thus, to understand the perils insured against one needs to understand the perils exclusions to ascertain the scope of the primary cover. Only then are the memoranda that extend cover to be considered and understood.

93 As to the indemnities in sections 1 and 2 the Insurers noted that section 2 is narrower than section 1 as it requires the property physically lost, destroyed or damaged to be used by the insured at the Premises for the purpose of the Business. Such damage must be physical.

94 For section 2 attention must be paid to what perils: that is, what causes and events of the physical Damage (using “Damage” as a shorthand for loss, destruction or damage as does the Policy), were excluded. The Insurers submitted that two particular perils excluded were relevant: perils exclusions 1(b) (see [78] above) and 4(a) (see [80] above).

95 Perils exclusion 1(b) excluded Damage to property resulting from any order of any government. The relational prepositional phrase “resulting from” is wider than a proximate cause, requiring a common sense evaluation of a causal chain: Kooragang Cement Pty Ltd v Bates (1994) 35 NSWLR 452 at 463–464.

96 The writeback immediately after perils exclusion 1(b) was to be understood, it was submitted in the written submissions, by reference to cover available in section 1(c) “Costs of Extinguishing a Fire” (see [50] above). Perils exclusion 1(b), it was submitted, sought to complement and not restrict the cover available under section 1, for property in imminent danger of fire or other peril. Apart from the writeback liability for physical Damage which has a sensible causal connection to an order of a government is excluded from section 1 and 2.

97 Perils exclusion 1(b) and the writeback were put more simply in oral address. The perils exclusion 1(b) removed from cover the event and cause “the order of any Government or Public or Local Authority” under sections 1 and 2. The writeback, it was submitted, only provided in terms for liability for physical loss, destruction or damage of property: that is under section 1. This was important in attributing significant work to the Civil Authority Extension by reference to physical loss for the operation of, and cover to be provided under, section 2.

98 Perils exclusion 4(a) excluded physical Damage occasioned by or happening through, inter alia, “disease”. The relational prepositional phrases “occasioned by or happening through” denoted a wide scope of causal relationships: Switzerland General Insurance Co Ltd v Lebah Products Pty Ltd (1982) 2 ANZ Insurance Cases 60-498 at 77,826 and 77,827; Mercantile Mutual Insurance (Aust) Ltd v Rowprint Services (Victoria) Pty Ltd [1998] VSCA 147 at [24]; Prime Infrastructure (DBCT) Management Ltd v Vero Insurance Ltd [2005] QCA 369; 13 ANZ Insurance Cases 61-661 at [29] and [60].

99 Thus, it was submitted, there was no cover under either section 1 or 2 for physical Damage to property resulting from any government order (subject to the writeback for section 1) or occasioned by or happening through disease (for section 1) or for loss from interruption or interference with the Business in consequence of such physical Damage (section 2) (noting the refinement of the argument in oral address).

100 It was in this context that one now turned, the Insurers submitted, to the memoranda for section 2 which may be seen to extend cover.

101 The Insurers turned first to the Disease Extension. This provision emphasised the place specific occurrence of a Notifiable Disease at the Premises or attributable to supply at the Premises or an organism at the Premises. The Insurers referred to the notion of “occurrence” as an “event”: something which happens at a particular time, at a particular place, in a particular way: Axa Reinsurance (UK) plc v Field [1996] 1 WLR 1026 at 1035; Kuwait Airways Corporation v Kuwait Insurance Co SAK [1996] 1 Lloyd’s Rep 664 at 683–686; Mann v Lexington Insurance Co [2001] 1 Lloyd’s Rep 1 at 5–6.

102 Thus the memorandum was directed to the occurrence of a Notifiable Disease at the Premises and the resultant restrictions on the Premises, but not the occurrence of a Quarantinable disease listed in the Biosecurity Act 2015.

103 The Insurers recognised that the Biosecurity Act does not contain the phrase “Quarantinable disease”, which appeared in the repealed Quarantine Act 1908 (Cth). Under the Quarantine Act a “Quarantinable disease” was “any disease declared by the Governor-General, by proclamation to be a quarantinable disease”. Under the Biosecurity Act the Director of Human Biosecurity was authorised under s 42 to list human diseases that may be communicable and may cause significant harm to human health. The diseases are listed by way of determination and included in the Biosecurity (Listed Human Diseases) Determination 2016 as amended. The Insurers submitted that the infelicity of language of the use of “Quarantinable disease” would not prevent the exclusion of COVID-19 from the Disease Extension. Star did not take or contest that point.

104 At this point the Insurers directed their submissions to the first constructional issue:

Having regard to the terms of the insuring clause, the Perils Exclusions, the Civil Authority extension and the Disease Extension, is there any cover available in section 2 in respect of the COVID-19 pandemic?

105 The Insurers’ submissions emphasised that the Disease Extension directed itself not only to the question of disease, but also to the exclusion from cover of a type of disease of which COVID-19 was one. In that context of the specific words of the Disease Extension, the general words of the Civil Authority Extension should not be seen as affording cover. It would make no commercial sense, it was submitted, for an insurer to limit its exposure to a specific peril and agree to a much greater exposure to the same peril under general words.

106 The second constructional issue was posited by the Insurers as follows:

Does the word “loss” in the Civil Authority Extension include only physical loss, destruction or damage or does it also include loss of use and access, custom and potential custom?

107 The Civil Authority (7) and the Disease (9) Extensions commence in similar fashion:

7: The word “Damage” under section 2 of this Policy is extended to include loss resulting from or caused by …

9: Damage is extended to include loss resulting from…

108 The Insurers submitted that the two extensions of the meaning of Damage should be inserted at the end of the parenthetical definition of Damage in the insuring clause.

109 The Insurers submitted that “loss” was used in two distinct ways in the insuring clause: as part of the composite expression “physical loss, destruction or damage” and as the amount to be paid resulting from the interruption in accordance with the Basis of Settlement. It submitted that it was used in the former sense in the Civil Authority Extension. The Insurers noted that in memoranda 8, 10, 11, 15 and 18 the parties used a deeming technique to cover loss which was not physical in nature: Each such memorandum begins “Loss as insured by section 2 of the policy” or (in respect of memorandum 15) “Loss as insured by this Policy” resulting from interruption or interference with the Business as deemed to be loss resulting from Damage to property used by the Insured in the Business. In these clauses “loss” is clearly loss in the second sense. Memoranda 10 and 15 deal with the peril preventing or hindering access. If “loss” in the Civil Authority Extension was intended to be loss of use or custom such a technique would, it was submitted, be expected to be used.

110 Further, the Insurers submitted, memorandum 19 is also directed to closure of the whole or part of the Premises by order of a public authority.

111 These memoranda, it was submitted, recognised the availability of indemnity where the peril would not cause Damage to property of the Insured.

112 The Civil Authority Extension, on the other hand, did not use these drafting techniques. Rather, the word “Damage” being physical loss, destruction and damage is extended to include loss resulting from or caused by any lawfully constituted authority.

113 The Civil Authority Extension can be seen to be directed to physical loss and that it does work as an extension of cover was said by the Insurers to be made evident (in written submissions) by the relationship with the fire indemnity (“Cost of extinguishing a fire”): ([50] above). This clause in section 1 contemplated fire or some insured peril occurring at or near the Premises or the Premises being under threat of imminent damage. The writeback to perils exclusion 1(b) ([78] above) sought to ensure that perils exclusion 1(b) did not deprive the insured of cover under the fire indemnity where sound property is damaged or is affected by firefighting. The Civil Authority Extension extended this cover by allowing Damage for the purpose of the indemnity in section 2 to include actions by the authority where there is no imminent threat to insured property. In oral address, as I have said, a starker and clearer role for the Civil Authority Extension was submitted with the writeback in perils extension 1(b) only referable to section 1 of the Policy. Thus the word “Damage” in the indemnity in section 2 had to be extended because perils exclusion 1(b) had excluded governmental orders from the causes or events of the physical loss, destruction or damage “so caused” being the “Damage”. Damage does not just refer to the physical state or existence of property, it refers to something narrower: property lost, destroyed or damaged by any cause or event not excluded. What appears in parentheses makes this clear: “(loss, destruction, damage so caused being hereinafter termed ‘Damage’)”.

114 This approach was supported, it was submitted, by the recognition that the retardation of a conflagration is likely to have physical consequences. If insured property were damaged (say by fire retardant) or lost by being destroyed as a fire break and the conflagration was retarded and defeated, absent the Civil Authority Extension there would be doubt as to indemnity under the fire indemnity which is conditional on a fire at or in the vicinity of the Premises or by the operation of perils exclusion 1(b) even with the writeback read more widely, conditional as it was on damage to or removal of “sound property at the Premises”.

115 A conflagration or a physical catastrophe is likely to be retarded, it was submitted, by physical activity that affects the property. It is not likely to be retarded by closing or restricting access to the Premises.

116 Thus the extension is not to refer to any non-physical nature of the effect on the property, but rather to ensure that certain physical consequences of an authority’s actions are in general terms available to engage section 2 (even if physical damage recovery for section 1 is left to the interplay and operation of the fire indemnity, perils exclusion 1(b) and its writeback).

117 The third constructional issue was posited by the Insurers as follows:

On their proper construction, do the words “conflagration or other catastrophe” as they appear in the CAE:

(a) mean an event which has geographical proximity to the Premises and happens at a particular time, at a particular place, in a particular way?

(b) include any state of affairs anywhere in Australia or the world which is sufficiently adverse in terms of its effect and scale such as a global pandemic?

(c) include merely the risk or threat of a “conflagration or other catastrophe”?

118 The Insurers submitted that “conflagration or other catastrophe” meant an event which has geographical proximity to the property insured, and happens at a particular time, and place and in a particular way. The words suggest an identifiable and discrete event, not a state of affairs. Just as when the words “occurrence” or “event” are used in an insurance policy, they mean something which happens at a time, and place, and in a particular way: Financial Conduct Authority v Arch Insurance (UK) Ltd [2021] UKSC 1; 2 WLR 123 at [67]; and just as the word “incident” was given a similar meaning in Financial Conduct Authority v Arch Insurance (UK) Ltd [2020] EWHC 2448 (Comm) at 119 [404]. The word “catastrophe” is of similar character: something which happens at a time and place and in a way. Disease that spreads is not something that occurs at a particular time and place or in a particular way: Arch Insurance (UK) Ltd [2021] UKSC at [69]. Just as a conflagration is an event so is a “catastrophe” and in that respect the Insurers called in aid the causes of construction of noscitur a sociis and eiusdem generis: Lend Lease Real Estate Investments Ltd v GPT RE Ltd [2006] NSWCA 207 at [30]. “Conflagration” provides the genus. A “conflagration” is, it was submitted, a large fire which causes widespread destruction. The word “catastrophe” should take its meaning eiusdem generis because of the words “or other”: The Sun Fire Office v Hart (1889) 14 App Cas 98 at 103–104. The meaning should be taken from context. It can mean in the vernacular severe or adverse outcomes. It takes its meaning from “conflagration”, not as a fire but as a sudden, large scale event which causes widespread damage to property.

119 The language of the extension directed attention, it was submitted, to the retarding of a present not theoretical conflagration or catastrophe. Threat or risk is insufficient to engage the provision.

120 The fourth constructional issue was posited by the Insurers as follows:

On its proper construction, does the word “retarding” as it appears in the CAE mean to delay or impede the progress of a particular event or does it also include the prevention of a particular event from ever occurring?

121 This issue arises if “other catastrophe” includes the COVID-19 pandemic and, as a matter of fact, the arrival and spread of COVID-19 in Australia was not a catastrophe. In such circumstances for the Civil Authority Extension to be engaged the word “retarding” would have to reach beyond delaying or holding back in terms of progress or development and extend to preventing.

122 The Insurers submitted that as a matter of ordinary meaning that width of meaning was not available. The word “prevent” was used elsewhere, notably in the fire indemnity. The Insurers also pointed out that use of both “preventing” and “retarding” (along with minimising) in like clauses in other policies: see Allstate Explorations NL v QBE Insurance (Aust) Ltd [2007] VSC 380; 14 ANZ Insurance Cases 61-743 at [5].

123 The fifth constructional issue was posited by the Insurers as follows:

On their proper construction, do the words “interruption or interference” as they appear in the insuring clause of Section 2 include a loss of custom or potential custom by reason of government action where the operation of the Business is otherwise unaffected?

124 The issue is whether the phrase “interruption or interference” is limited, as the Insurers submitted, to the inability to conduct the Business on the Premises in the same way as prior to the Damage, or whether it extends to government regulation which does not affect the conduct of the Business but, instead, has the effect of reducing or potentially reducing custom of the Business.

125 The Insurers submitted that the Policy cannot be taken to insure against a decline in custom because of government regulation of the general human environment of the public.

Star’s oral address in answer to the Insurers’ written submissions

126 As to constructional issue 1, Star submitted that the pandemic was a catastrophe in the ordinary meaning of that word: in Australia and overseas. Measures taken in Australia were to retard it or were in connection with it. The emphasis on “retarding” by the Insurers ignored the width of “in connection with”: the global catastrophe and the incipient Australian catastrophe. The proper characterisation of the pandemic as a catastrophe can be taken from the extreme measures taken to deal with it in Australia.

127 As to noscitur a sociis and the eiusdem generis rule, Star submitted that the genus is catastrophe. In any event the rules are merely part of the construction process.

128 The two extensions: Civil Authority and Disease should be seen as separately operating.

129 As to the second construction issue and the meaning of “loss” in the Civil Authority Extension, Star drew attention to the similarity in introductory wording and the content of the Disease Extension. That extension operates without reference to physical loss, destruction or damage. Thus, it was submitted, the similar text introducing the Civil Authority extension shows that it was intended to operate without reference to physical loss.

130 Star submitted that the writeback to the perils exclusion 1(b) effectively meant that if the Civil Authority Extension was limited to physical loss it would be redundant. The Policy should be read so as to give work or operation to the Civil Authority Extension and not be given an empty lack of operation. Effect must be given to it if it possibly can be: Lewis v Barnett [1982] 2 EGLR 127 at 128. Star submitted that the writeback in perils exclusion 1(b) gave effect to cover under section 2, as well as section 1. Further, Star submitted that the argument in the written submissions as to the writeback and the provision concerning the costs of extinguishing a fire was artificial.

131 Star submitted that the language of the Civil Authority Extension (memorandum 7) is wide, it commenced with a form of words substantially in common with Disease Extension (memorandum 9) which is plainly not directed to physical loss, but is concerned with a field of operation distinct from the immediate Premises under the control of the insured with which memorandum 9 was concerned.

132 Star submitted that “loss” was non-physical loss, to include loss of use, or custom or financial loss caused by or resulting from the actions of the lawfully constituted authority.