FEDERAL COURT OF AUSTRALIA

Wameja Limited, in the matter of Wameja Limited [2021] FCA 878

ORDERS

WAMEJA LIMITED ACN 052 947 743 Plaintiff | ||

DATE OF ORDER: | ||

THE COURT ORDERS THAT:

1. Pursuant to ss 411(1) and 1319 of the Corporations Act 2001 (Cth) (Act):

(a) the plaintiff convene a meeting (Scheme Meeting) of the holders of its fully paid ordinary shares (Shareholders) for the purpose of considering, and if thought fit, agreeing (with or without modification) to the proposed scheme of arrangement to be made between the plaintiff and Shareholders (Scheme), the terms of which are contained in Annexure A to the explanatory statement which is Exhibit 1 in these proceedings (Scheme Booklet);

(b) the Scheme Meeting be held at 3.00 pm (AEST) on Thursday, 2 September 2021 at Computershare, Level 3, 60 Carrington Street, Sydney, New South Wales 2000;

(c) subject to any public health restrictions, Scheme Shareholders be permitted to attend and vote at the Scheme Meeting:

(d) if public health restrictions prevent the holding of a physical meeting:

(e) provisions of the plaintiff’s Constitution as to quorum be taken to be satisfied provided that there is Online Attendance by two or more Eligible Voters (as that term is defined in the plaintiff’s Constitution);

(f) the time for determining eligibility to vote at the Scheme Meeting be fixed at 7.00 pm (AEST) on Tuesday, 31 August 2021;

(g) the chairperson of the Scheme Meeting be Stephen Baldwin or failing him, Tom Rowe;

(h) the chairperson appointed to the Scheme Meeting has the power to adjourn or postpone the Scheme Meeting in his absolute discretion for such time and to such date as the chairperson considers appropriate;

(i) at the Scheme Meeting, the resolution to approve the Scheme be decided by way of a poll.

2. The following documents be approved for distribution to Shareholders:

(a) the explanatory statement, substantially in the form of the Scheme Booklet at Exhibit 1 in these proceedings, being the Scheme Booklet approved for the purposes of section 411(1) of the Act; and

(b) a proxy form for the Scheme Meeting (substantially in the form of the pro forma copy which is at Annexure TDGR-22 to the Affidavit of Thomas David Germain Rowe affirmed 23 July 2021 in these proceedings) (Proxy Form);

3. The following documents be approved for distribution to holders of Depository Interests (as defined in the Scheme Booklet):

(a) the explanatory statement, substantially in the form of the Scheme Booklet at Exhibit 1 in these proceedings; and

(b) form of instruction for the Scheme Meeting (substantially in the form of the pro forma copy which is at Annexure TDGR-23 to the Affidavit of Thomas David Germain Rowe affirmed 23 July 2021 in these proceedings) (Form of Instruction).

4. Subject to registration of the Scheme Booklet with ASIC, on or before 2 August 2021, the plaintiff is to cause to be issued:

(a) to each Shareholder who, in accordance with the Act, has nominated an electronic address for the purposes of receiving notices of meeting from the plaintiff, at such address, an email substantially in the form of the document which is at Annexure TDGR-20 to the Affidavit of Thomas David Germain Rowe affirmed 23 July 2021 in these proceedings, including:

(i) electronic hyperlink to download the explanatory statement, substantially in the form of the Scheme Booklet at Exhibit 1 in these proceedings; and

(ii) electronic hyperlink to the webpage where that Shareholder can electronically lodge proxies for the Scheme Meeting.

(b) to each Shareholder (other than those referred to in 4(a) above) by pre-paid post, or in the case of a Shareholder whose registered address is outside Australia, by pre-paid air mail, addressed to that Shareholder's address set out in the register of members of the plaintiff:

(i) a copy of the explanatory statement, substantially in the form of the Scheme Booklet at Exhibit 1 in these proceedings;

(ii) a Proxy Form; and

(iii) a reply paid envelope addressed to the plaintiff, or in the case of a Shareholder whose registered address is outside Australia a return envelope addressed to the plaintiff.

(c) to each holder of Depository Interest in the plaintiff, by pre-paid post issued from the United Kingdom, addressed to that Depository Interest holder’s address set out in the register of Depository Interest holders held by the Depository Nominee:

(i) a copy of the explanatory statement, substantially in the form of the Scheme Booklet at Exhibit 1 in these proceedings;

(ii) a Form of Instruction; and

(iii) a reply paid envelope addressed to the Depository Nominee.

5. Rule 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) shall not apply to the Scheme Meeting, save in respect of the application of 75-15(2) of the Insolvency Practice Rules (Corporations) 2016 (Cth).

6. Notice of the hearing of the application pursuant to subsection 411(4)(b) of the Act for orders approving the Scheme be published once in “The Australian” newspaper, by advertisement substantially in the form of Annexure “B” to these orders, such advertisement to be published on or before 6 September 2021, and the plaintiff otherwise be exempted from compliance with the requirement to publish a notice of the hearing of the application pursuant to rule 3.4 of the Federal Court (Corporations) Rules 2000 (Cth).

7. The proceeding be stood over to 10.15 am on Thursday, 9 September 2021 for the hearing of any application to approve the Scheme.

8. There be liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE “A”

Wameja Limited (“Wameja”)

Scheme Meeting- Change to Virtual Meeting only.

[ ] August 2021

Wameja (LSE: WJA.L & ASX: WJA.AX), a joint venture partner with Mastercard in the HomeSend global payment hub, refers to the Notice of Scheme Meeting contained within the Scheme Booklet dated 27 July 2021 and advises that due to the New South Wales government’s extension of the public health orders preventing all non-essential physical gatherings of people in Sydney until [ ], the Scheme Meeting will now be held solely as a virtual meeting.

The Scheme Meeting of Wameja shareholders scheduled to commence at 3.00pm (Sydney time) on 2 September 2021 will be held online (internet) only through the https://web.lumiagm.com website or the Lumi AGM App.

Instructions on how to attend the virtual meeting are contained within the Scheme Booklet.

Authorised by:

Tom Rowe

Company Secretary

trowe@capitalcorporatelaw.com.au

For further information, please contact: Wameja Limited |

|

John Conoley, Non-Executive Chairman Tom Rowe, Company Secretary |

|

finnCap Limited (Nomad and Broker) Corporate Finance: Jonny Franklin-Adams / Charlie Beeson Corporate Broking: Tim Redfern / Richard Chambers |

|

About Wameja

Wameja and Mastercard are joint venture partners of the HomeSend global payment hub. HomeSend enables cross-border transfer between bank accounts, cards, mobile wallets, or cash outlets from anywhere in the world. As a founding partner in the HomeSend hub, Wameja helped conceive and bring the opportunity to market.

ANNEXURE “B”

Wameja Limited

ACN 052 947 743

Notice of hearing to approve scheme of arrangement

TO all the creditors and members of Wameja Limited (ACN 052 947 743) (Wameja).

TAKE NOTICE that at 10:15am (Sydney time) on 9 September 2021, the Federal Court of Australia at Law Courts Building, 184 Phillip Street, Queens Square, Sydney NSW 2000, Australia will hear an application by Wameja seeking the approval of a compromise or arrangement between Wameja and its ordinary shareholders (Shareholders) as proposed by a resolution passed at a meeting of Shareholders held on 2 September 2021.

If you wish to oppose the approval of the compromise or arrangement, you must file and serve on Wameja a notice of appearance, in the prescribed form, together with any affidavit on which you wish to rely at the hearing. The notice of appearance and affidavit must be served on Wameja at its address for service at least 1 day before the date fixed for the hearing of the application.

The address for service of Wameja is: c/- Simpsons Solicitors, Level 2, Pier 8/9, 23 Hickson Road, MILLERS POINT, New South Wales 2000 (Attention: Tom Rowe).

Tom Rowe, Capital Corporate Law

Solicitor for Wameja Limited

FARRELL J:

1 These are reasons for orders made on 27 July 2021.

INTRODUCTION

2 Wameja Limited ACN 052 947 743 is taken to be registered in New South Wales. Ordinary shares issued by Wameja (Wameja shares) are listed for quotation on the Australian Securities Exchange Limited (ASX) and depository interests over Wameja shares (Wameja DIs) are listed for quotation on the Alternative Investment Market of the London Stock Exchange (AIM).

3 As at 23 July 2021, there were 1,210,850,662 Wameja shares on issue. Wameja DIs are issued by Computershare Investor Services Plc, a company incorporated in the United Kingdom (Nominee). For each Wameja DI, there is one Wameja share which is registered in Wameja’s share register in the name of Computershare Clearing Pty Ltd (Custodian). A Wameja DI holder can swap their DI for an ordinary share at their choosing. Over the last two years, Wameja DIs have represented approximately 85% of Wameja shares on issue. Holders of Wameja DIs cannot vote in person or by proxy at shareholder meetings. However, they can direct the Custodian how to vote Wameja shares which their Wameja DIs represent.

4 Since the sale of Wameja’s previous core business to Seamless Distribution Systems AB on 25 July 2019, Wameja’s sole commercial activity has been the management of its investment in a financial payment hub operated through a joint venture vehicle incorporated in Belgium called HomeSend SCRL. Wameja holds 35.26% of the equity in HomeSend and the balance is held by Mastercard/Europay U.K. Limited, an indirectly wholly owned subsidiary of Mastercard Incorporated, which is listed on the New York Stock Exchange.

APPLICATION

5 By an originating process dated 8 October 2020, Wameja seeks orders pursuant to ss 411(1) and 1319 of the Corporations Act 2001 (Cth) (Act) convening a meeting of the holders of Wameja shares for the purpose of considering, and if thought fit, approving a scheme of arrangement between Wameja and its shareholders (scheme meeting) as explained in the scheme booklet which is Exhibit 1 in these proceedings.

Purpose of scheme

6 The purpose of the scheme is to effect the acquisition of all issued Wameja shares by Burst Acquisition Co. Pty Ltd ACN 644 142 834 (Bidder) for a consideration of £0.08 per Wameja share.

7 The Bidder’s ultimate holding company is Mastercard. The rationale for Mastercard is explained in the FAQs included in section 3 of the scheme booklet as follows:

Mastercard and Wameja are joint venture partners in the HomeSend JV with Wameja holding a 35.26% interest in HomeSend and Mastercard holding the remaining 64.74% interest in HomeSend. This transaction would result in Mastercard obtaining 100% of Wameja and therefore 100% of HomeSend. Mastercard believes that this transaction would resolve certain challenges faced by HomeSend by permitting Mastercard to fully integrate HomeSend with much larger related assets owned by Mastercard and incorporate HomeSend comprehensively under Mastercard’s treasury and operational capabilities, thereby creating synergies on an administrative and operational level necessary to compete effectively over the long term.

Delays

8 The fact that Wameja and the Bidder had entered into a Scheme Implementation Agreement on 10 September 2020 (SIA) in relation to the proposed scheme was announced on that date. There have been substantial delays in advancing the scheme proposal which has necessitated the execution of a number of deeds amending the SIA. The reason for the delays is explained in section 5.1 of the scheme booklet as follows

There was a significant delay to the Scheme due to notice of a potential claim pursuant to an indemnity granted by Wameja under the sale and purchase agreement for the sale of its core operating business to Seamless Distribution Systems AB on 25 July 2019. This delay necessitated three amendments to the Scheme Implementation Agreement with the last amendment being made on 18 June 2021. On 18 June 2021 the matters relating to the indemnity were resolved and Mastercard advised Wameja that it intended to proceed with the Scheme Implementation Agreement. Please refer to section 14.5 for further detail on the potential claims under the indemnity.

Conditions of scheme

9 The proposed scheme is subject to a number of conditions. Other than the usual conditions concerning shareholder and court approval of the scheme and filing of court orders with the Australian Securities and Investments Commission (ASIC), conditions precedent which are yet to be fulfilled include:

Wameja holding €1,500,000 in cash at completion of the scheme, less the amount of any capital contribution made by Wameja to HomeSend made between 24 May 2021 and 8.00 am on the date of the second court hearing. It is expected that Wameja will be required to hold €89,422 in cash at bank;

The cancellation of all employee and executive options (see [12]-[15] below);

The removal of all subsidiaries from Wameja. Section 14.4(c) of the scheme booklet makes the following disclosure:

It is expected to take until at least 3 months after the Implementation Date to wind up all the Subsidiaries. In anticipation of Subsidiaries remaining at the Effective Date, Wameja intends to transfer all remaining Subsidiaries to a new company holding company, New Hold Co, prior to the Effective Date. New Hold Co is yet to be incorporated and is expected to be controlled by Tom Rowe who will oversee the winding up of the Subsidiaries and ultimately the winding up of New Hold Co.

The Subsidiaries are currently dormant and will remain so until wound up. The Subsidiaries will have no value at the time of transfer to New Hold Co as they currently have negligible net assets and rely on the support of Wameja Limited for their solvency. After payment of all expenses related to the Scheme and outstanding liabilities and satisfying the Condition Precedent requiring Wameja to hold €89,422 cash at the Effective Date, Wameja Limited will transfer the balance of its cash to New Hold Co to cover the wind-up expenses and administrative costs of New Hold Co and the Subsidiaries.

Tom Rowe will charge New Hold Co his professional fees to manage the administration of New Hold Co and the winding up of the Subsidiaries and ultimately New Hold Co.

The Subsidiaries are not a substantial asset, within the meaning of ASX Listing Rule 10.2, and accordingly the transfer of the Subsidiaries to New Hold Co is not a transaction to which ASX Listing Rule 10.1 applies.

Wameja having no debt;

Regulatory approvals, including from the Foreign Investment Review Board and the National Bank of Belgium.

Directors and their interests

10 The directors of Wameja perform all executive and management functions; Wameja has no employees. If the scheme is implemented, they will all resign.

11 The directors and their share and option entitlements are discussed at sections 5.16, 6.4, 14.1 and 14.4 of the scheme booklet, and that information may be summarised as follows:

(a) John Conoley, chairman. Mr Conoley was appointed to the Board in May 2013. He was appointed as executive chairman of Wameja in April 2015. He ceased his executive role on 29 January 2020. He serves on the board of HomeSend. He holds 2,626,692 Wameja shares. He also holds 2 million executive options expiring on 8 August 2021 and 3.5 million executive options expiring on 13 March 2022 for which he will receive $37,350 and $79,800 respectively (an aggregate of $117,150) if the scheme is implemented;

(b) Stephen Baldwin, non-executive director. Mr Baldwin was appointed to the Board in November 2011. He holds 1,695,634 Wameja shares and no employee or executive options.

(c) Jamie Brook, non-executive director. Mr Brook was appointed to the Board in October 2018, having previously been on the Board between 2010 and 2013. He holds no Wameja shares or options;

(d) James Hume, non-executive director. Mr Hume was appointed to the Board in October 2019 and he is member of the HomeSend board. He holds 922,459 Wameja shares. He also holds 1.65 million employee options expiring on 8 August 2021 and 2.5 million employee options expiring on 24 November 2022 for which he will receive $30,813.75 and $64,125 respectively ($94,938.75) if the scheme is implemented;

(e) Tom Rowe, non-executive director and company secretary. Mr Rowe has been the company secretary since April 2011. He was appointed to the Board in March 2014. I note that his law firm, Capital Corporate Law, has acted for Wameja in relation to the scheme and Mr Rowe’s hourly rate is discussed in section 14.4(c). Mr Rowe’s role in the winding up of dormant subsidiaries of Wameja to satisfy a condition of the scheme is also disclosed in section 14.4(c). He holds no Wameja shares or options.

Executive and employee options.

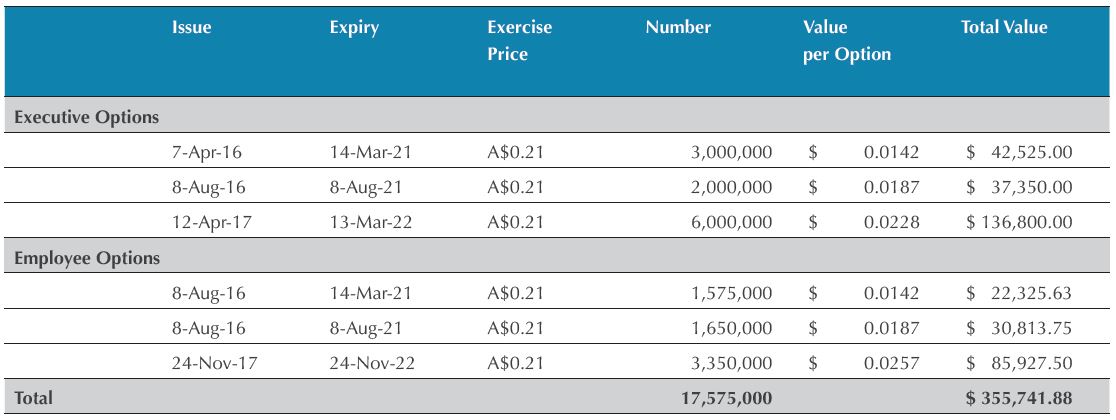

12 Although options are categorised as “executive” and “employee”, they were issued on the same terms save for the date on which tranches expire.

13 Section 5.16 of the scheme booklet discloses that, prior to entry into the SIA on 10 September 2020, Wameja entered into option cancellation deeds in respect of executive and employee options. Those deeds comprise annexure TDGR-16 (original cancellation deeds). The position under the original cancellation deeds is represented in the following table which appears in section 5.16 of the scheme booklet:

14 Section 5.16 also notes the expiry of three million executive options and 1,575,000 employee options on 14 March 2021 and that two million executive options and 1,650,000 employee options will expire on 8 August 2021 with the result that at the expected Implementation Date of the scheme, there will only be 6,000,000 executive options and 3,350,000 employee options at an exercise price of $0.21 on issue. It then goes on to explain that:

To obtain the agreement of each Optionholder for the cancellation of their Employee Options and Executive Options, Wameja agreed with each Optionholder (subject to specific agreements with Mr. John Conoley as disclosed in Section 14.4(c)) to pay the total consideration payable as agreed in the original option cancellation deed regardless of the fact that many of the Employee Options or Executive Options have expired or will expire prior to the Implementation Date.

The total consideration payable by Wameja for the cancellation of the Employee Options and Executive Options is $312,153.75.

Wameja has obtained a waiver of ASX Listing Rule 6.23.2 to permit the cancellation for consideration to occur without Wameja Shareholder approval.

15 In his affidavit affirmed on 23 July 2021, Mr Rowe deposed as follows:

(a) He managed negotiations with the individual option holders prior to 10 September 2020.

(b) An independent valuation was obtained from Hall Chadwick Corporate (NSW) Limited for the purpose of the negotiation (annexure TDGR-17). The valuation, dated 30 June 2020, found that:

(i) Options expiring on 14 March 2021 were valued at $0.0189;

(ii) Options expiring on 8 August 2021 were valued at $0.0249;

(iii) Options expiring on 13 March 2022 were valued at $0.0304;

(iv) Options expiring on 24 November 2022 were valued at $0.0342; and

(v) Performance options had no value.

(c) The consideration payable for cancellation of the options under the original cancellation deeds was approved by directors who did not hold options, being Messrs Rowe, Baldwin and Brooke. The involvement of Messrs Conoley and Hume was limited to agreeing to the cancellation of their options on the same terms as agreed by the other option holders.

(d) Due to the delays in progressing the scheme proposal, the original cancellation deeds expired on 31 March 2021 and Wameja was required to enter into new option cancellation deeds. Messrs Rowe, Baldwin and Brooke determined that Wameja would offer the same aggregate consideration to each option holder as was payable under the original cancellation deeds, regardless of whether any options had expired or would expire before the expected Implementation Date of the scheme, with one exception (see (e) below). Accordingly, new cancellation deeds were entered into as set out in annexure TDGR-18. Messrs Rowe, Baldwin and Brooke considered this appropriate because:

(i) The consideration offered under the original cancellation deeds was within the valuation range provided by Hall Chadwick;

(ii) The holders of those options had a financial expectation when they entered into the original cancellation deeds because it was intended that the scheme be implemented before 14 March 2021;

(iii) There was little scope for negotiation because of the condition precedent in the SIA; and

(iv) The cancellation of the options provided a commercial benefit to Wameja.

(e) The exception was Mr Conoley who agreed that he would not be paid for three million executive options which expired on 14 March 2021. I note that: The value foregone by Mr Conoley was $42,600. Mr Hume did not have any options which expired on 14 March 2021. Both of them will receive the same consideration as other option holders for their options which expire on 8 August 2021 as well as those options which expire after the proposed Implementation Date of the scheme.

Scheme consideration

16 The scheme consideration is £0.08 per Wameja share or its AUD equivalent. Wameja shareholders may make an election whether to receive GBP or AUD but Wameja DI holders may not. This is explained in the Chairman’s Letter in the scheme booklet at p 11 as follows:

What you will receive

Under the Scheme, you will be entitled to receive £0.08 for each Wameja Share or Wameja Depository Interest you hold at the Record Date.

If you are a Scheme Shareholder on the Australian Register but have a registered address in the United Kingdom, you will receive payment in Pounds Sterling unless you elect by the Record Date to receive payment by direct credit in Australian Dollars.

If you are a Scheme Shareholder on the Australian Register with a registered address outside of the United Kingdom, you will receive payment in Australian Dollars, unless you elect by the Record Date to receive payment by direct credit in Pounds Sterling.

I refer you to the section titled ‘Currency Election’ on page 13 for further details on how to elect the currency of payment.

If you are a Wameja DI Holder, you cannot elect to receive payment in Australian dollars. You will receive payment in Pounds Sterling via CREST.

If your payment is made in Australian Dollars, you will receive the Australian Dollar equivalent to £0.08 at the exchange rate that is received by Wameja and applied to the payment. This means that for anyone receiving their payment in Australian dollars, there is a risk:

• of an adverse movement in the exchange rate between when you make the election and when you receive payment; and

• that the exchange rate Wameja receives is not the exchange rate that you expect or could obtain yourself.

This risk rests with you.

Directors’ recommendation

17 The directors unanimously recommend a vote in favour of the scheme and say that they intend to vote their personal holdings in favour of the scheme. The Chairman’s letter sets out their reasons for the recommendation as follows:

The reasons for the Wameja Board’s recommendation that you vote in favour of the Scheme include:

• £0.08 per Wameja Share represents a 39.1 % premium to the closing price of Wameja Shares on AIM on 9 September 2020, being the day before the announcement of the proposed Scheme.

• The scheme provides a significant return of approximately 4 times Wameja’s cash investment in HomeSend over the life of the investment.

• The Scheme provides an implied enterprise value for HomeSend of approximately €290,000,000. This equates to a multiple of 39.7 times HomeSend’s FY2020 gross revenue. Comparable transactions over the last 26 months were conducted on an average multiple of 10.4 times gross revenue.

• The Scheme will provide liquidity for Wameja Shareholders, liquidity which is not otherwise available in a thinly traded stock.

• There is unlikely to be a superior offer in the short to medium term.

• If the Scheme does not proceed, Wameja expects to be called on to contribute further capital to the HomeSend JV in the short to medium term. In order to maintain its influence over HomeSend at the HomeSend JV board level and under the terms of the HomeSend JV, Wameja would need to participate in funding HomeSend and to do so would require further investment by Wameja Shareholders.

Independent expert’s recommendation

18 Hall Chadwick’s independent expert’s report is set out in section 12 of the scheme booklet. Hall Chadwick:

(a) Concluded that the scheme is fair and reasonable and in the best interests of Wameja shareholders in the absence of a superior proposal after taking into account the underlying value of Wameja shares, the value of the proposed consideration, the likely market price and liquidity of Wameja shares if the scheme is not implemented, and the likelihood of an emergence of an alternative proposal that could realise better value for shareholders;

(b) Noted that Wameja had a market capitalisation on AIM of £61.7 million prior to the announcement that Wameja and the Bidder had entered into the SIA on 10 September 2020. Subsequently, the market capitalisation has increased to £89 million as at the date of Hall Chadwick’s report;

(c) Determined that the indicative value of a Wameja share is between £0.062 and £0.074 per share, with a midpoint of £0.068 per share, inclusive of a 25% premium for control and that consideration within or above this value would be fair; and

(d) Determined that the scheme was reasonable. In forming that opinion Hall Chadwick considered the following factors:

(i) In the twelve months to the initial announcement of the scheme in September 2020, Wameja’s share price had ranged from £0.022 to £0.079. Subsequent to that announcement, the share price rose from £0.058 to £0.076 and Wameja shares are currently trading at £0.078. If the scheme is not approved by shareholders, it is possible that Wameja’s share price may return to the lower levels or continue to decrease depending upon future financial performance;

(ii) The scheme will provide an opportunity for Wameja shareholders to realise the value of their investment. HomeSend’s existing business model is still not profitable and Wameja has no activities outside of its investment in HomeSend. In Hall Chadwick’s view, the market value of Wameja shares significantly exceeds the value of the HomeSend investment based on a capitalisation of HomeSend’s revenue; and

(iii) The scheme will allow shareholders to realise the value of their investment in Wameja inclusive of a control premium to be paid by the Bidder.

PRINCIPLES

19 It is uncontentious that the proposed scheme is an “arrangement” for the purposes of s 411 of the Act.

20 Wameja relied on the summary of principles relevant to when a court will convene a scheme meeting which I set out in Capilano Honey Limited, in the matter of Capilano Honey Limited [2018] FCA 1568; (2018) 131 ACSR 9 at [32]-[34] as follows:

32 The Court will order that a scheme meeting be convened and approve a draft explanatory statement to be sent to shareholders if it is satisfied that:

(1) The plaintiff is a Pt 5.1 body;

(2) The proposed scheme is a compromise or (relevantly) an “arrangement” within the meaning of s 411. …;

(3) The scheme booklet will provide proper disclosure to shareholders;

(4) The scheme is bona fide and properly proposed;

(5) ASIC has had a reasonable opportunity to examine the terms of the scheme and the scheme booklet and make submissions and it has had at least 14 days’ notice of the proposed hearing date;

(6) The procedural requirements of the Federal Court (Corporations) Rules 2000 (Cth) have been met; and

(7) The scheme is of such a nature and cast in such terms that, if it receives a statutory majority at the meeting, the Court would be likely to approve it on the hearing of a petition which is unopposed.

33 The application for leave to summon a scheme meeting is in the nature of an interlocutory proceeding and is a preliminary to the final determination which is to be made when the matter comes back to the Court for approval after the holding of the meetings which have been directed: Australian Securities Commission v Marlborough Gold Mines Ltd (1993) 177 CLR 485 at 504-05. By granting leave, the Court does not give its imprimatur to the proposed scheme. At the stage of ordering a scheme meeting, the Court does not ordinarily go very far into the question of whether the arrangement is one that warrants the approval of the Court; that question is to be answered when the scheme returns to the Court for final approval. That is not to exclude the possibility that a scheme may appear on its face so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further: see Re Foundation Healthcare Limited (2002) 42 ACSR 252; [2002] FCA 742 at [36] and [44] per French J, cited with approval in Re CSR Limited (2010) 183 FCR 358; [2010] FCAFC 34 at [58] per Keane CJ and Jacobson J. Chief Justice Keane and Jacobson J went on to say (at [59] and [61]) that the adverb “blatantly” and the term “contrary to public policy” emphasise that the enquiry under s 411(1) is not intended to resolve difficult questions on which reasonable minds may differ, although it has long been recognised that a clear want of utility in putting in train the process of s 411(1) is a good reason to decline to order the convening of the first meeting.

34 At the first court hearing, the Court is concerned with whether the proposed scheme is one which is adequately explained to those who have a financial interest in it and whether there is any obvious flaw in the scheme, such that it would be inappropriate even for it to be submitted for consideration: see Re Abacus Funds Management Ltd (2006) 24 ACLC 211; [2005] NSWSC 1309 at [23]. The Court is not required to be satisfied that no better scheme could have been proposed. The question is whether it is reasonable to suppose that sensible business people might consider the arrangement proposed to be of benefit to members: see Centrebet International Limited [2011] FCA 870 at [29] per Emmett J.

EVIDENCE

21 The following affidavits were read on the application.

22 First, Mr Rowe’s affidavit affirmed on 23 July 2021 in which he gave evidence of:

(a) An ASIC search which establishes that Wameja is a Part 5.1 body;

(b) Wameja’s constitution. Among other things, the constitution permits the provision of notices by post and to an electronic address nominated by the recipient for that purpose. As at the date of Mr Rowe’s affidavit, there were 763 registered shareholders (including the Custodian) or which 345 had elected to receive electronic notification of meetings;

(c) Wameja DIs;

(d) The SIA and three unexecuted amending deeds; the executed amending deeds are annexed to Mr Rowe’s affidavit affirmed on 26 July 2021. I accept that the amended SIA is prima facie evidence that Wameja has committed itself to the scheme and accordingly the scheme is bona fide and properly proposed;

(e) A deed poll executed by the Bidder dated 10 September 2020;

(f) The negotiation of “deal protection clauses” included in the amended SIA. I note that the break fee of $500,000 represents less than 0.5% of the market value of Wameja shares as at 21 July 2021 calculated without a control premium (£66 million or AUD123 million). The SIA also contains “no shop”, “no talk” and “notification” obligations, subject to fiduciary carve outs in relation to the latter two obligations in conventional form. Mr Rowe deposes that the Wameja board approved these measures and considered them necessary to secure the SIA and that was in the best interest of Wameja shareholders;

(g) Provision of the draft scheme booklet to ASIC;

(h) The process employed for verification of the scheme booklet;

(i) The valuation of executive and employee options, the negotiation of the terms of original and new cancellation deeds, and the role of directors who do not hold options in setting the consideration to be paid to option holders;

(j) Instructions given to Hall Chadwick and correspondence with ASIC concerning the independent expert’s report;

(k) His consent to act as an alternate chairperson of the scheme meeting, including disclosure concerning payment he receives by way of director’s fees, an hourly rate for work done over and above what would normally be expected of a non-executive director and in his role as company secretary and in relation to legal advice in connection with the scheme;

(l) The proposed method of despatch of the scheme booklet and proxy form to shareholders;

(m) That the Nominee will send the scheme booklet and a form of instruction to the Custodian to Wameja DI holders;

(n) That he has arranged with Computershare the use of an internet based software program, Lumi, to allow remote access to the scheme meeting. That platform will allow attendees to remotely register for and view the scheme meeting in real time, and ask questions in writing, and allow shareholders to vote at the meeting; and

(o) A draft script for the Wameja Information Line to be managed by Computershare in the United Kingdom and Australia. It is appropriate that the Court have an opportunity to consider such communications at the time of the first court hearing so that it may be satisfied that the messages conveyed are consistent with the content of the scheme booklet which is approved for despatch to shareholders and deposit interest holders.

23 Second, Mr Rowe’s affidavit affirmed on 26 July 2021 in which he gave evidence of:

(a) The provision of ASIC’s “usual letter” dated 23 July 2021 in which an ASIC delegate confirmed that it had been given at least 14 days’ notice of the first court hearing, that it had a reasonable opportunity to examine the terms of the scheme booklet and to make submissions in relation to it, and that it does not intend to appear at the first court hearing;

(b) Executed deeds amending the SIA. The third amending deed was to expire on 2 July 2021 unless a written notice was delivered by the Bidder to Wameja of its intention to continue the implementation of the scheme. Annexure TDGR-28 is a copy of an email dated 18 June 2021 from Evan Michalovsky, Senior Managing Counsel at Mastercard to Mr Rowe indicating that the “sunset date” under the SIA is now 30 September 2021;

(c) A proposed amendment to cl 4.8 of the scheme of arrangement included as annexure A to the scheme booklet in the Court Book at Tab 4, correcting the description of the currency election; and

(d) Further information concerning the way the Lumi platform will allow Wameja shareholders and DI holders to participate in the scheme meeting.

24 Third, an affidavit affirmed by Drew Anthony Townsend on 22 July 2021. Mr Townsend is a director of Hall Chadwick and a partner in the accountancy practice that trades under that name. He gave evidence of his qualifications and experience, that he is the author of the draft independent expert’s report (annexure DAT-2) and he had overall responsibility for its preparation, that he holds the opinions expressed in it and that he is prepared to sign a report in that form for inclusion in the scheme booklet.

25 Fourth, Mr Michalovsky’s affidavit affirmed in New York on 20 July 2021 in relation to the verification of material related to the Bidder in the scheme booklet.

26 Fifth, Mr Baldwin’s affidavit affirmed on 21 July 2021 confirming his consent to act as chairperson of the scheme meeting.

DISCUSSION

27 I note that counsel specifically drew the following matters to the Court’s attention.

28 The first matter is the fact that, under the new cancellation deeds, Messrs Conoley and Hume (who are also shareholders of Wameja) will be paid the consideration agreed in the original cancellation deeds in respect of options that will have expired prior to the Implementation Date of the scheme as well as the consideration agreed in respect of the cancellation of options that expire after the Implementation Date. I understand this to raise two matters: first, the fact that Messrs Conoley and Hume joined with other members of the board in recommending the scheme to Wameja shareholders and DI holders; and second, whether there are any implications from a class perspective.

29 The appropriateness of a director’s decision to make a recommendation is always fact sensitive: Re MOD Resources Ltd; ex parte MOD Resources Ltd [2019] WASC 326 at [86] (Vaughan J). I am satisfied that the fact that Messrs Conoley and Hume joined in the directors’ recommendation in favour of the scheme should not weigh against making the orders now sought having regard to the facts that:

(a) The options issued to Messrs Conoley and Hume were on the same terms as other employee options and they were issued at the latest in November 2017, well before the proposed scheme was announced;

(b) It is a condition of the scheme that all options are cancelled and the satisfaction of that condition is necessary to achievement of the Bidder and Mastercard objective of being able to “incorporate HomeSend comprehensively under Mastercard’s treasury and operational capabilities”;

(c) The consideration to be paid does not exceed Hall Chadwick’s valuation and it was arrived at after negotiation to which neither of the two directors was a party;

(d) While some options will lapse before the scheme is implemented, that would not have been the case had the scheme progressed on its intended timetable and the overall benefit to the two directors is not large. Option holders who held options which lapsed in 2022 had leverage in ensuring that the agreement reached prior to 10 September 2020 was maintained and Messrs Conoley and Hume were not party to those negotiations. Mr Conoley has foregone consideration relating to options which lapsed in March 2021 (and Mr Hume had no such options); and

(e) The interests of Messrs Conoley and Hume in the outcome of the scheme on the basis of being parties to cancellation deeds is adequately disclosed in the scheme booklet at section 14.4(c) and that disclosure is generally cross-referenced where the directors’ recommendation is mentioned.

30 I am also satisfied that the interests of the two directors (or any other former employee option holder who might hold Wameja shares) arising out of the new cancellation deeds is not class-creating because I am satisfied that the interest is not one which will affect the ability of shareholders to consult together in a common interest. The relevant test was summarised by Barrett J in Re Hills Motorway [2002] NSWSC 897; (2002) 43 ACSR 101 at [12] as follows:

The test is thus not one of identical treatment. It is one of community of interest. The court must ask itself whether the rights and entitlements of the different groups, viewed in the totality of the scheme’s context, are so dissimilar as to make it impossible for them to consult together with a view to their common interest. The focus is not on the fact of differentiation but on its effects. The extent and nature of the differentiation must be measured in terms of the effect on the ability to consult together in a common interest or, in other words, the ability to come together in a single meeting and to debate the question of what is good or bad for the constituency as a whole and where the common good lies. Only if the differentiation destroys that ability – the word used by Bowen LJ is “impossible” – does class distinction come to prevail.

31 The second matter was performance risk which has been addressed in a way that has become conventional. Title to Wameja shares will not pass until consideration has been paid to Wameja under the terms of the scheme of arrangement set out in annexure A of the scheme booklet and the Bidder has entered into a deed poll. I note that a deed poll dated 10 September 2020 was executed by the Bidder. Since then, the SIA has been amended a number of times. Counsel for the Bidder confirmed to the Court that the Bidder’s position is and will be that those amendments have no impact on the undertakings contained in the deed poll. The written submissions observe that the Bidder has no assets from which it could meet any liabilities arising under the deed poll and I observe that Mastercard, a listed entity and holding entity for a group with global operations, is not a party to the deed poll. That is a common situation in member schemes. However, the deed poll is not a mere formality: the Bidder will hold all of the Wameja shares upon the scheme becoming effective and Mastercard has a commercial interest in that occurring as it wishes to integrate HomeSend into its group. Given the nature of its business, Mastercard also has an interest in being seen to observe promises made by its subsidiaries.

32 The submissions drew attention to the existence of a “deemed warranty” in cl 7.4 of the scheme of arrangement set out in annexure A to the scheme booklet. They also drew attention to the “break fee” and “deal protection” features of the SIA which I have discussed in the context of Mr Rowe’s affidavit affirmed on 23 July 2021. These matters are dealt with in a way which has become conventional in member schemes and their existence would not be a reason to refuse to make the orders sought.

33 I have also noted that: It is proposed that the scheme booklet will be despatched to shareholders who have provided email addresses by that means and otherwise by mail with a return addressed envelope. Wameja DI holders will receive the scheme booklet and voting instruction form through the Nominee. The scheme meeting is to be held at a physical location and on a virtual platform on which shareholders may vote and shareholders and DI holders may view and participate in the proceedings by written questions. DI holders will be able to instruct the Custodian to vote Wameja shares. I consider these arrangements to be appropriate and note that it may be necessary to hold the scheme meeting on a virtual platform without a physical gathering of shareholders having regard to current health orders imposing restrictions on gatherings and movement of people in Sydney designed to limit the spread of the SARS CoV-2 virus responsible for the COVID-19 disease and the orders make provision for an announcement to the ASX should such constraints be in effect at the time of the meeting. Further, approximately 85% of the issued shares are held by the Custodian on behalf of Wameja DI holders and those interests are traded on AIM in London so that it is likely that those holders will be better able to participate in the scheme meeting where it is held on a virtual platform.

34 The draft scheme booklet considered at the hearing was some 202 pages, inclusive of a copy of the SIA and the three amending deeds. I queried counsel for Wameja whether it was necessary to include those documents in the scheme booklet on the bases that: As Wameja is a listed company, copies of the SIA and amending deeds have been released on the ASX announcements platform shortly after they were executed. Material aspects of the amended SIA had been summarised in the scheme booklet. The notice of meeting was obscured in the scheme booklet since the copy of the SIA and the amending deeds fell after it. Without those copies, the scheme booklet was some eighty pages shorter, making the document less intimidating to readers. Wameja decided not to include the SIA and amending deeds in the scheme booklet, a decision which I endorse.

35 Wameja’s counsel’s submissions carefully set out how the scheme booklet and the evidence satisfies the relevant requirements of s 411(1) and (2) of the Act and the Corporations Regulations 2001 (Cth) and other matters discussed in Capilano Honey Limited at [32]-[34]. I was satisfied that those submissions should be accepted and the orders sought by Wameja at the first court hearing should be made.

I certify that the preceding thirty-five (35) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Farrell. |

Associate: