Federal Court of Australia

Ippolito v Cesco, in the matter of Cesco [2021] FCA 656

ORDERS

IN THE MATTER OF MICHAEL CESCO | ||

Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. A sequestration order under the Bankruptcy Act 1966 (Cth) (Act) be made against the estate of Michael Cesco.

2. The applicant’s costs be taxed and paid from the bankrupt estate of Michael Cesco in accordance with the Act.

THE COURT NOTES THAT:

3. The date of bankruptcy is 6 February 2021.

4. A consent to act as trustee under s 156A of the Act has been signed by Bradley Tonks.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MARKOVIC J:

1 On 9 February 2021 the applicant, Steffan James Ippolito, presented a creditor’s petition seeking a sequestration order against the estate of the respondent, Michael Cesco. The creditor’s petition is founded upon Mr Cesco’s failure to comply with the requirements of Bankruptcy Notice BN 250223 issued on 30 July 2020 (Bankruptcy Notice) which claims the amount of $397,480.16. That amount is made up of an order made on 14 May 2020 by the Supreme Court of New South Wales (Supreme Court) in proceeding no 2018/00285545 between Mr Ippolito as plaintiff and Mr Cesco as first defendant (SC Proceeding), the effect of which was to require Mr Cesco to pay Mr Ippolito the sum of $380,509.03 (Judgment Debt), and post judgment interest accruing on the Judgment Debt from 15 May 2020 to 5 February 2021 in the sum of $17,543.46.

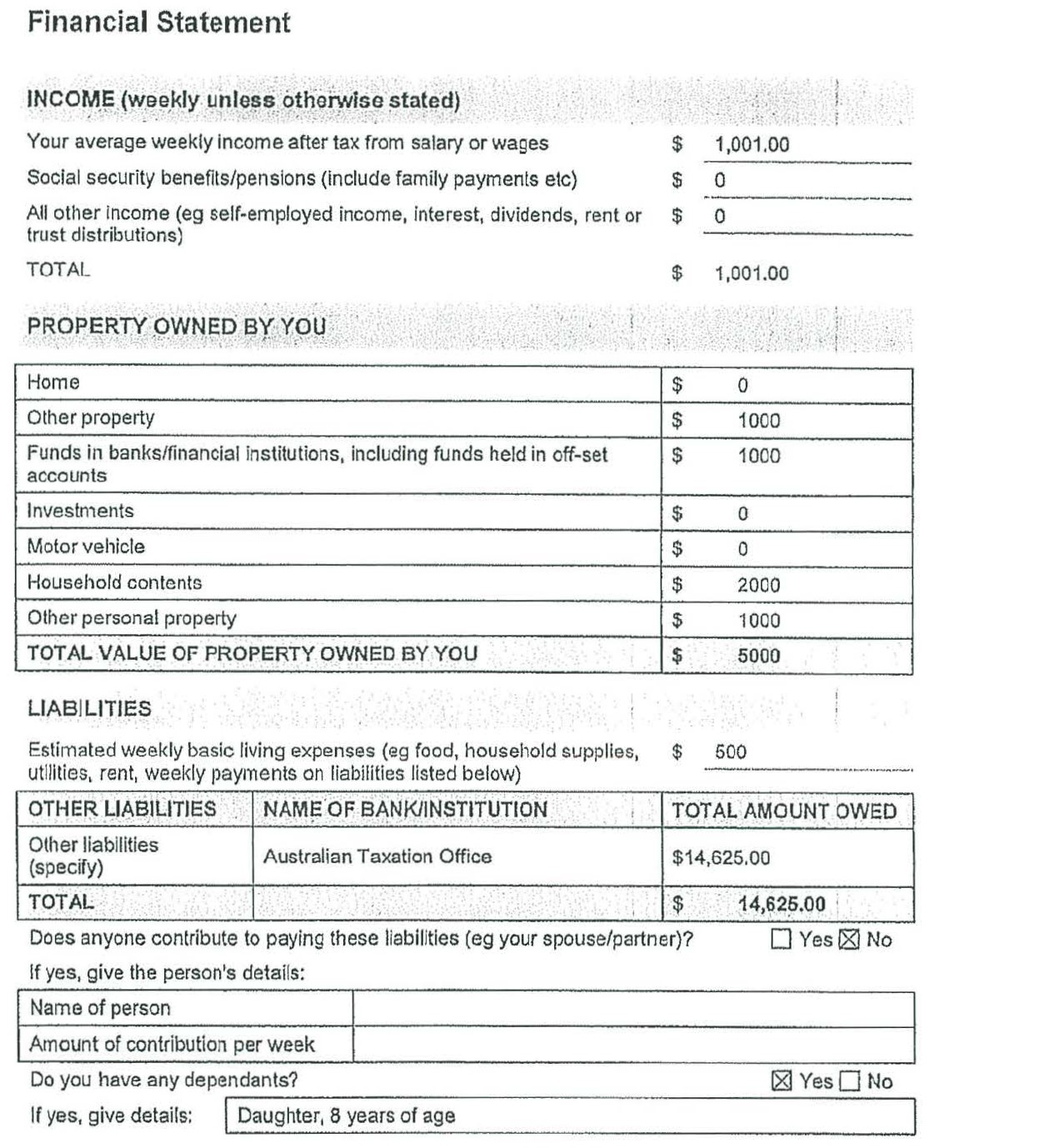

2 On 16 April 2021 Mr Cesco filed a notice stating grounds of opposition to the creditor’s petition raising two grounds. Mr Cesco says first, that he is solvent as a result of an order made in the Supreme Court that the Judgment Debt be payable in instalments and because his mother, Judith Hall, has agreed to pay or assist him to pay those instalments; and secondly, that Mr Ippolito has filed the creditor’s petition for the collateral purpose of enabling him to have recourse to home owners’ warranty insurance and, accordingly, it is an abuse of process.

3 Before turning to consider whether the order sought in the creditor’s petition should be made I set out the events which led to the Judgment Debt, the recent dealings between the parties and other evidence relevant to the issues raised by the parties.

background

Events leading up to commencement of this proceeding

4 On 13 July 2011 Messrs Ippolito and Cesco entered into a contract for the development of a dual occupancy residential property situated at 43A and 43B Robert St, Willoughby, New South Wales (Properties). The development was completed by 10 September 2014 and a final occupation certificate was issued on 23 February 2016.

5 Defects were identified at the Properties causing Mr Ippolito to commence a proceeding in the New South Wales Civil and Administrative Tribunal against Mr Cesco. That proceeding was subsequently transferred to the Supreme Court and became the SC Proceeding.

6 On 14 May 2020 an order was made in the SC Proceeding granting judgment for Mr Ippolito in the amount of the Judgment Debt: see Ippolito v Cesco [2020] NSWSC 561.

7 The Bankruptcy Notice was issued on 30 July 2020 and served on 6 August 2020. Mr Cesco had six months to comply with the Bankruptcy Notice: see s 5 of the Bankruptcy Act 1966 (Cth) (Bankruptcy Act) and Sch 12 of the Coronavirus Economic Response Package Omnibus Act 2020 (Cth).

8 Neither Mr Ippolito nor his solicitors received any correspondence or other communication from Mr Cesco in response to the Bankruptcy Notice. Having not complied with the Bankruptcy Notice within the six month period, on 6 February 2021 Mr Cesco committed an act of bankruptcy.

9 As set out above, on 9 February 2021 Mr Ippolito filed the creditor’s petition. On 14 February 2021 it was served on Mr Cesco together with an affidavit sworn by Alexander Harvey Frank Morton on 9 February 2021 deposing to searches undertaken of the records maintained by the registries of this Court and the Federal Circuit Court of Australia and the results of those searches; an affidavit sworn by Frank Hoare on 12 August 2020 deposing to service of the Bankruptcy Notice; and a Trustee Consent to Act Declaration dated 1 February 2021 signed by Bradley Tonks (Trustee Consent).

Mr Cesco’s application to pay the Judgment Debt by instalments

10 On 12 March 2021 Mr Cesco filed a Notice of Motion to Pay by Instalments – Individual (Instalment Application) in the SC Proceeding seeking an order that the Judgment Debt be paid by him to Mr Ippolito by monthly instalments of $12,187, with the first instalment to be paid on 12 April 2021. Affidavits sworn by Mr Cesco and Ms Hall on 12 March 2021 were filed in support of that application. The application was made on the basis that Ms Hall would provide Mr Cesco with the funds required on a monthly basis to enable him to make the instalment payments sought in the application and that Ms Hall would not require repayment of the amounts advanced at the conclusion of the instalment period.

11 In her affidavit, Ms Hall sets out her assets and liabilities. There is no dispute that she has significant assets. Ms Hall notes that she is a self-funded retiree, that she supports herself with income from her self-managed super fund and from income generated by her husband from his self-managed super fund and that her super fund consists of cash, Australian equities and real estate, the cash component is approximately $460,000 and it is from that component, which will be replenished by income generated by real estate assets in the fund, that she will draw to meet the monthly instalments. I address Mr Cesco’s affidavit below.

12 A Notice of Orders Made from the Supreme Court dated 12 March 2021 records, among other things, that on 12 March 2021 the following orders (Instalment Orders) were made in the SC Proceeding:

(1) The Court orders that pursuant to Rule 37.3 of the Uniform Civil Procedure Rules 2005 (NSW), the application by the First Defendant to pay by instalments is granted.

(2) The applicant is to pay $12,187.00 on a monthly instalment with the first payment to be made by 12 April 2021.

Correspondence between the parties

13 By email dated 16 March 2021 Tony Iuliano, Mr Cesco’s solicitor, informed Michael Lim, Mr Ippolito’s solicitor, that his client had filed the Instalment Application in the SC Proceeding. At that stage, Mr Iuliano was awaiting the Registrar’s determination.

14 On 8 April 2021 Mr Iuliano wrote to Mr Lim noting that he had not received a response to his email dated 6 April 2021 (which was not in evidence) and consequently had not been provided with Mr Ippolito’s bank details. Accordingly, a bank cheque for $12,187 made payable to Mr Ippolito was enclosed for the first instalment payable pursuant to the Instalment Orders.

15 On 9 April 2021 Messrs Lim and Iuliano exchanged emails:

(1) by email sent at 9.22 am Mr Lim acknowledged receipt of Mr Iuliano’s letter dated 8 April 2021 enclosing the bank cheque but noted that acceptance of it did not prejudice his client’s rights or position in any way and that Mr Ippolito would not be dismissing the creditor’s petition;

(2) by email sent at 9.40 am Mr Iuliano said, among other things, that (as written):

It would appear to our client that your client, as a creditor would in a far better position than if our client were to be declared bankrupt. The Instalment order will provide your client with a far better return than a sequestration order. In fact, the instalment arrangement would result in full payment of the judgment debt and interest; a sequestration order on the other would result I probably a nil return to your client. We are yet to understand the commercial utility of your client's desire to proceed with such process.

(3) by email sent at 10.40 am Mr Lim wrote (as written):

We refer to your email below.

We confirm that the bank details requested last week were not provided as we had not yet sought instructions and due to the public holidays had intended to seek same this week, noting that the first payment was not due til 12 April 2021.

We have already set out our client's commercial reasons and the prejudice suffered by our client in our earlier without prejudice email, which we do not propose to re-state, but, in short, our client would receive a better outcome in a bankruptcy.

To date, your client has not paid the principal debt in full, has not agreed to the quantum of our client's costs in respect of the costs order and your client's mother has not entered into any binding agreement with our client to guarantee the principal debt and the costs order payable by your client. Having regard to all the circumstances, it would take your client more than 4 years to pay the debts owed to our client, whereas upon bankruptcy our client would be entitled to rely on the home warranty insurance and the claim which has crystallised and in our client's view receive payment certainly before the instalment order is made. We certainly dispute the contention that our client would receive a nil return in a bankruptcy.

The above is the delay prejudice suffered by our client and the commercial prejudice suffered by our client is equally significant.

Evidence of Mr Cesco’s financial position.

16 As set out above Mr Cesco swore an affidavit in support of the Instalment Application. In Mr Cesco’s affidavit he deposed that he was separated from his wife and is currently paying maintenance for his eight year old daughter and that information about his present income, assets and liabilities set out in the annexed financial statement was true.

17 The annexed financial statement was in the following form:

18 By letter dated 14 April 2021 the Australian Taxation Office (ATO) confirmed Mr Cesco’s direct debit payment plan for his income tax balance of $14,625 requiring him to make an initial payment of $731 on 27 April 2021 and thereafter to pay $267.20 every fortnight.

Mr Ippolito’s purpose in filing and proceeding with the creditor’s petition

19 Mr Ippolito’s evidence is that as 7 June 2021 the Judgment Debt is still owing, but that he received two payments pursuant to the Instalment Orders on 8 April 2021 and 7 May 2021 respectively, leaving a balance owing of $379,535.53.

20 Mr Ippolito says that based on the Instalment Orders, and assuming the interest on the Judgment Debt remains the same, it would not be paid in full until 12 April 2024, which is 37 months from the date on which the Instalment Orders were made.

21 Mr Ippolito has not entered into any agreements with Ms Hall whereby she has guaranteed payment of the Judgment Debt and the obligations under the Instalment Orders. He says that Ms Hall does not proffer any valuable security for payment of the Judgment Debt and the interest associated with it.

22 The Judgment Debt relates to defects in the building work undertaken by Mr Cesco in relation to the Properties. Mr Ippolito is not in a position to rectify those defects until the Judgment Debt is satisfied and he has only been able to undertake limited rectification works to date. His intention is to undertake the balance of the works immediately after he receives payment of the Judgment Debt.

23 Mr Ippolito says that it has been more than six years since the first defect was identified at the Properties and, if it is necessary for him to wait until payment of the Judgment Debt pursuant to the Instalment Orders, the defects would have been present at the Properties for more than 10 years before they are rectified, the value of the Properties has decreased as a result of the defects which impacts on his options regarding the Properties and there is a real possibility and risk that by the time the Judgment Debt is paid in full the cost of the rectification works will have increased.

24 Mr Ippolito’s purpose in presenting the creditor’s petition is to obtain or realise what he can out of Mr Cesco’s estate in order to enable him to fund rectification of the defects.

Insurance

25 The works undertaken by Mr Cesco on each of the Properties are insured in accordance with the Home Building Act 1989 (NSW) (Home Building Act). The certificates of insurance showing Mr Ippolito as the building owner/beneficiary and Home Warranty Insurance Policy for Residential Building Works (Policy) were in evidence before me. Among other things, the Policy provides:

1.1 Residential building work

(a) Subject to the terms of the policy and in accordance with the Act and the Regulation, the policy will cover you if you suffer the following losses or damage in respect of the work:

(ii) loss or damage arising from a breach of a statutory warranty, being loss or damage in respect of which you cannot recover compensation from the builder or have the builder rectify because of the insolvency, death or disappearance of the builder.

(b) Subject to the terms of the policy, in accordance with the Act and the Regulation and without limiting paragraph (a), the policy will cover you for the following loss or damage, being loss or damage in respect of which you cannot recover compensation from the builder, or have the builder rectify, because of the insolvency, death or disappearance of the builder:

(i) loss or damage resulting from faulty design, where the design was provided by the builder;

(ii) loss or damage resulting from non-completion of the work because of early termination of the contract because of the builder's wrongful failure or refusal to complete the work;

(iii) the cost of alternative accommodation, removal and storage costs reasonably and necessarily incurred as a result of an event referred to in paragraph (a);

(iv) the loss of a deposit or progress payment due to an event referred to in paragraph (a); and

(v) any legal or other reasonable costs incurred by you in seeking to recover compensation from the builder for the loss or damage or in taking action to rectify the loss or damage.

(c) The policy will also cover you for any acts and omissions of all persons contracted by the builder to perform the work resulting in the loss or damage referred to in paragraph (a) or (b).

…

…

2.2 Structural defects

In respect of loss or damage arising from a structural defect, the policy provides cover for a period of six years after the completion of the work or the end of the contract, whichever is the later.

…

statutory framework

26 Section 43(1) of the Bankruptcy Act provides that where a debtor has committed an act of bankruptcy and at that time the debtor was relevantly, personally present or ordinarily resident in Australia or had a dwelling house or place of business in Australia; or was carrying on business in Australia, either personally or by means of an agent or manager the Court may, on a petition presented by a creditor, make a sequestration order against the estate of the debtor.

27 Section 40(1) of the Bankruptcy Act sets out when a debtor commits an act of bankruptcy including relevantly:

(g) if a creditor who has obtained against the debtor a final judgment or final order, being a judgment or order the execution of which has not been stayed, has served on the debtor in Australia or, by leave of the Court, elsewhere, a bankruptcy notice under this Act and the debtor does not:

(i) where the notice was served in Australia—within the time fixed for compliance with the notice; or

(ii) where the notice was served elsewhere—within the time specified by the order giving leave to effect the service;

comply with the requirements of the notice or satisfy the Court that he or she has a counter-claim, set-off or cross demand equal to or exceeding the amount of the judgment debt or sum payable under the final order, as the case may be, being a counter-claim, set-off or cross demand that he or she could not have set up in the action or proceeding in which the judgment or order was obtained;

28 Section 44 of the Bankruptcy Act sets out the conditions on which a creditor may petition and includes:

(1) A creditor's petition shall not be presented against a debtor unless:

(a) there is owing by the debtor to the petitioning creditor a debt that amounts to the statutory minimum or 2 or more debts that amount in the aggregate to the statutory minimum, or, where 2 or more creditors join in the petition, there is owing by the debtor to the several petitioning creditors debts that amount in the aggregate to the statutory minimum;

(b) that debt, or each of those debts, as the case may be:

(i) is a liquidated sum due at law or in equity or partly at law and partly in equity; and

(ii) is payable either immediately or at a certain future time; and

(c) the act of bankruptcy on which the petition is founded was committed within 6 months before the presentation of the petition.

29 Section 52 of the Bankruptcy Act relevantly provides:

(1) At the hearing of a creditor's petition, the Court shall require proof of:

(a) the matters stated in the petition (for which purpose the Court may accept the affidavit verifying the petition as sufficient);

(b) service of the petition; and

(c) the fact that the debt or debts on which the petitioning creditor relies is or are still owing;

and, if it is satisfied with the proof of those matters, may make a sequestration order against the estate of the debtor.

…

(2) If the Court is not satisfied with the proof of any of those matters, or is satisfied by the debtor:

(a) that he or she is able to pay his or her debts; or

(b) that for other sufficient cause a sequestration order ought not to be made;

it may dismiss the petition.

consideration

30 Mr Ippolito has provided proof of the matters required by s 52(1) of the Bankruptcy Act, namely: the matters stated in the creditor’s petition (by way of the affidavit verifying the petition); service of the creditor’s petition on Mr Cesco; and that the debt on which he relies is still owing. In addition Mr Ippolito relies on an affidavit deposing to the fact that the records of this Court and the Federal Circuit have been searched and that no application was made in relation to the Bankruptcy Notice and an affidavit of service of the Bankruptcy Notice, both of which have been served on Mr Cesco: see r 4.04 and r 4.05 of the Federal Court (Bankruptcy) Rules 2016 (Cth).

31 As I am satisfied of proof of the matters in s 52(1) of the Bankruptcy Act, subject to consideration of the grounds of opposition raised by Mr Cesco, I can exercise my discretion to make a sequestration order. I turn to consider those grounds.

A preliminary issue - the effect of the Instalment Orders on the creditor’s petition

32 As the Instalment Orders had prominence in both grounds of opposition it is convenient to consider, as a preliminary matter, how they affect the creditor’s petition and this proceeding.

33 The rules for the payment of judgment debts by instalments are found in Pt 37 of the Uniform Civil Procedure Rules 2005 (NSW) (UCPR). Relevantly:

(1) rule 37.2 enables a judgment debtor to apply to the court for an instalment order in relation to the amount owing under the judgment debt. Such an application must be supported by an affidavit setting out the judgment debtor’s financial circumstances;

(2) unless it is made during a hearing, the application is to be dealt with by the registrar under r 37.3;

(3) rule 37.3 provides that the registrar can deal with an application for an instalment order by either making an order, or refusing the application. As soon as practicable after making an instalment order the registrar must give notice of the order to the judgment creditor and the judgment debtor and must give the judgment creditor a copy of the affidavit of the judgment debtor’s financial circumstances relied on in support of the application. Either party may file an objection to, relevantly, an instalment order within 14 days after the order is made;

(4) rule 37.4A(1) requires the judgment debtor to pay the amounts under an instalment order to the judgment creditor unless the court for special reasons orders otherwise;

(5) rule 37.5(1) relevantly provides that execution of the judgment to which an application for an instalment order relates is stayed from the time the application is made until the time the application is determined;

(6) a judgment creditor may apply to the court for a variation or rescission of the instalment order upon proof of improvement in the judgment debtor’s circumstances: r 37.6; and

(7) an instalment order ceases to have effect if the judgment debtor fails to comply with it: see r 37.7.

34 Section 107 of the Civil Procedure Act 2005 (NSW) relevantly provides that a court in which judgment has been entered may, subject to and in accordance with the UCPR, make an order allowing for payment of the judgment debt by instalments and, subject to s 119, execution of the judgment for the payment of money is stayed while the judgment is the subject of an order in force under s 107.

35 While the Instalment Orders are in place there is a stay on execution of the Judgment Debt. However, the Instalment Application was filed and the Instalment Orders made after service of the Bankruptcy Notice, after Mr Cesco committed an act of bankruptcy by failing to comply with the requirements of the Bankruptcy Notice and after the creditor’s petition was presented.

36 It is established, and did not appear to be in dispute, that if an act of bankruptcy occurs before the grant of an order staying the judgment on which the act of bankruptcy is grounded, a subsequent stay will not prevent the presentation of a creditor’s petition or the making of a sequestration order in the discretion of the Court: see Re Padagas, Ex parte Carrier Air Conditioning Pty Ltd (1977) 30 FLR 170 (Ex parte Carrier) at 172; Re Schlekoff (1989) 22 FCR 407 at 408. The making of an instalment order converts a judgment debt into a debt payable at a certain future time within the meaning of s 44(1)(b)(ii) of the Bankruptcy Act: see Ex parte Carrier at 173.

Is Mr Cesco able to pay his debts?

37 The first ground relied on by Mr Cesco is that he is solvent because of the Instalment Order and Ms Hall’s agreement to pay or assist Mr Cesco in paying the instalments.

38 The relevant principles were not in dispute.

39 In Sandell v Porter (1966) 115 CLR 666 at 670 Barwick CJ (with whom McTiernan and Windeyer JJ agreed) said:

Insolvency is expressed in s. 95 as an inability to pay debts as they fall due out of the debtor's own money. But the debtor's own moneys are not limited to his cash resources immediately available. They extend to moneys which he can procure by realization by sale or by mortgage or pledge of his assets within a relatively short time – relative to the nature and amount of the debts and to the circumstances, including the nature of the business, of the debtor. The conclusion of insolvency ought to be clear from a consideration of the debtor's financial position in its entirety and generally speaking ought not to be drawn simply from evidence of a temporary lack of liquidity. It is the debtor's inability, utilizing such cash resources as he has or can command through the use of his assets, to meet his debts as they fall due which indicates insolvency. The question of solvency is to be assessed at the date of the hearing, but this does not mean that future events are to be ignored: see Leslie v Howship Holdings Pty Ltd [1997] FCA 133; (1997) 15 ACLC 459 at 466.

40 The debtor bears the onus of proving that that his or her assets are sufficient to pay his or her debts within the meaning of s 52(2)(a) of the Bankruptcy Act: see Re Sanders [2003] FCA 1079 at [22].

41 Mr Cesco accepts that the making of an instalment order after the issue of a bankruptcy notice does not prevent a debt from being owing and notes that there was no stay in place when the Bankruptcy Notice was issued, referring to McInerney, in the matter of Ghougassian v Ghougassian [2020] FCA 1230 at [95]-[96].

42 Mr Cesco submitted that Ms Hall has net assets in excess of $4.8 million which is sufficient to pay the Judgment Debt and any costs payable in the SC Proceeding. Mr Cesco relies on his evidence and that of Ms Hall of the agreement to provide him with funds sufficient to ensure that he complies with the Instalment Orders. He contended that he has a powerful incentive to comply with those orders because if he defaults in making an instalment payment they will be “automatically” vacated. He also referred to r 37.6 of the UCPR which permits a judgment creditor to apply for a variation or revision of an instalment order upon proof of an improvement in the judgment debtor’s circumstances. Mr Cesco submitted that there is evidence that he has entered into an arrangement with the ATO to pay his tax debt by instalments and that he has complied with that arrangement. He said that as far as Mr Ippolito’s costs in the SC Proceeding are concerned, it is common ground that they are yet to be assessed and, as such, they are a contingent or non-current liability and not yet a debt due and payable.

43 Mr Cesco submitted that having regard to his financial position “in its entirety”, it includes the financial support of Ms Hall and her willingness to lend or give him money in order to ensure that he remains able to meet his debts as and when they fall due.

44 The evidence relied on by Mr Cesco to demonstrate his solvency is comprised in his affidavit sworn on 12 March 2021 and the affidavit of Ms Hall also sworn on 12 March 2021, both filed in support of the Instalment Application, and the evidence of Mr Cesco’s instalment arrangement with the ATO for payment of his income tax liability.

45 The financial statement included in Mr Cesco’s affidavit sworn on 12 March 2021 records a weekly net income of $1,001 and estimated weekly living expenses of $500, leaving a balance of $500 per week. The instalment arrangement with the ATO, which was subsequently entered into, requires a fortnightly payment of $267 or $133.50 per week. When the latter amount is taken into account, Mr Cesco is left with a net balance of $366.50 per week. Mr Cesco says that he is currently paying maintenance for his eight year old daughter. It is not clear whether the maintenance paid is included in the estimate of weekly living expenses. Mr Cesco has assets valued at $5,000. Without more Mr Cesco would not be in a position to meet his obligations under the Instalment Orders and it would not be possible to conclude that he is solvent.

46 However, Mr Cesco relies on Ms Hall who is prepared to provide financial assistance to Mr Cesco and who will provide him with funds on a monthly basis in advance to enable him to meet his obligations under the Instalment Orders. Indeed that has already occurred, with the instalments which were due on 12 April 2021 and 12 May 2021 having been paid. Ms Hall’s evidence is that Mr Cesco is not required to repay Ms Hall the amounts provided to him at the conclusion of the instalment period. That evidence was not challenged. Putting to one side the costs order made in the SC Proceeding in favour of Mr Ippolito, based on the evidence and having regard to the support from Ms Hall, Mr Cesco is able to pay his debts.

47 The costs order made in the SC Proceeding has not yet been assessed. Mr Ippolito says that is because Mr Cesco has not yet paid the Judgment Debt, an assessment would require him to incur further legal costs and those costs could be avoided if Mr Cesco is made a bankrupt as the costs order would be dealt with under the Policy. A schedule of the costs Mr Ippolito incurred in the SC Proceeding shows total costs incurred of $250,453.21.

48 The question posed by s 52(2)(a) of the Bankruptcy Act is whether the debtor is able to pay his or her debts. The term “debt” is defined in s 5 of the Bankruptcy Act to mean a liability. The costs order is a liability, albeit a contingent liability given that it is yet to be quantified. Further, in considering Mr Cesco’s solvency, I can have regard to future events. That includes the fact that the costs order will at some point be quantified. The assessed amount of the costs order is not presently known, although it is likely to be an amount less than the total incurred by Mr Ippolito. Putting that to one side there is no evidence of how Mr Cesco would meet his liability for the costs order once assessed. There is no evidence of any source from which Mr Cesco could draw funds. I am not able to infer that Ms Hall would meet this liability. Based on the evidence of his current financial position, even assuming the costs once assessed were reduced by 50%, he could not satisfy the debt. When that matter is taken into account, I cannot be satisfied that Mr Cesco is able to pay his debts as required by s 52(2) of the Bankruptcy Act.

49 Even if I am wrong about the effect of the costs order made in the SC Proceeding and thus was to conclude that Mr Cesco is able to pay his debts, having regard to the matters set out at [22] and [23] above, I would not be satisfied that the creditor’s petition should be dismissed. Mr Ippolito should not be left in a position where he is unable to rectify defects in the Properties, which were identified over six years ago, while awaiting satisfaction of the Judgment Debt by way of payment in instalments.

Other sufficient cause

50 Mr Cesco’s second ground of opposition as set out in his notice of grounds of opposition is that the creditor’s petition has been filed for a collateral purpose, namely enabling Mr Ippolito to have recourse to the home owners’ warranty insurance, and accordingly it is an abuse of process. However, in his written submissions Mr Cesco contended that there are other collateral purposes in service of the Bankruptcy Notice and in maintaining this proceeding.

51 Mr Cesco relies on the email sent on 9 April 2021 by Mr Lim to Mr Iuliano (see [15(3)] above). He submitted that Mr Ippolito was entitled as of right to file an objection to the Instalment Orders within 14 days after the orders were made pursuant to r 37.3(3) UCPR and have the Supreme Court vary or rescind the Instalment Orders pursuant to r 37.4 UCPR. He contended that this would be the proper course for a creditor troubled by the extension in time for repayment of the debt occasioned by the making of the Instalment Orders. However, Mr Ippolito has not filed any such application nor sought leave to file such an application out of time.

52 Mr Cesco submitted that instead Mr Ippolito has continued with bankruptcy proceedings for the collateral purposes of:

(1) pressuring Mr Cesco to agree to the quantum of his costs in the SC Proceeding;

(2) pressuring Mr Cesco to procure from Ms Hall a binding agreement between Ms Hall and Mr Ippolito to guarantee repayment of the Judgment Debt and the costs order and thereby to place Mr Ippolito in the position of a secured creditor where ordinarily he would have no legal entitlement to such status;

(3) subverting the Instalment Orders by maintaining bankruptcy proceedings rather than applying to the Supreme Court to rescind or set aside the Instalment Orders with the object of expediting payment of the Judgment Debt;

(4) enabling Mr Ippolito to have recourse to the home owners’ warranty insurance so as to “receive payment certainly before the [Instalment Orders] is [sic] made”; and

(5) averting “delay prejudice” and “commercial prejudice”.

53 Mr Cesco submitted that the statement in Mr Lim’s email that “[w]e certainly dispute the contention that our client would receive a nil return in bankruptcy” should be taken in the context of the email in which it appears which sets out that that “return” includes collateral objects. Mr Cesco submitted that accordingly Mr Ippolito served the Bankruptcy Notice and has maintained this proceeding to achieve multiple collateral purposes, rendering the service of the Bankruptcy Notice and this proceeding an abuse of process.

54 The Court has an inherent power to set aside a bankruptcy notice that is an abuse of process: see Slack v Bottoms English Solicitors [2002] FCA 1445 (Slack) at [16]-[21]. The categories of abuse of process are not closed: see HWY Rent Pty Ltd v HWY Rentals (in liq) (No 2) [2014] FCA 449 at [74]. Abuse of process may be established where it can be concluded that a bankruptcy notice was issued simply to put pressure on a debtor rather than to genuinely invoke the Court’s bankruptcy jurisdiction: see Slack at [18] quoting from Killoran v Duncan [1999] FCA 1574.

55 In Mr Cesco’s notice of opposition to the creditor’s petition he says that the collateral purpose in bringing this proceeding is to enable recourse to the home owners’ warranty insurance. Section 92 of the Home Building Act required the building works undertaken at the Properties to be insured. Mr Ippolito accepts that a consequence of Mr Cesco becoming bankrupt is that he will be able to access the home owners’ warranty insurance taken out for his benefit (whether the Policy will respond is not an issue that needs to be resolved in the context of this proceeding). I accept, as submitted by Mr Ippolito, that the ability to access the insurance could not be a collateral purpose for the following reasons.

56 First, Mr Ippolito’s stated purpose in bringing the proceeding is to get the Judgment Debt paid. As things currently stand he is unable to undertake the rectification work required on the Properties for lack of funds. There is no evidence that Mr Ippolito served the Bankruptcy Notice, presented the creditor’s petition or is pursuing this proceeding simply to put pressure on Mr Cesco and not to invoke the bankruptcy jurisdiction of the Court.

57 Secondly, the contract of insurance and the Policy issued for the purpose of complying with s 92 of the Home Building Act contemplates that a person in Mr Ippolito’s position cannot access the insurance except in the circumstances specified in cl 1.1(a) of the Policy, namely where the owner cannot recover compensation from the builder because of his or her insolvency, death or disappearance. It would frustrate the statutory scheme underpinning insurance of this nature if the owner for whom the work had been done and who was named as the beneficiary on the insurance policy taken out for the purposes of the Home Building Act is unable to bring a proceeding to bankrupt a builder because to do so would be found to be a collateral purpose.

58 Thirdly, the legitimate purpose of a litigant may be to bring a proceeding to a successful conclusion so as to take advantage of an entitlement which the law gives the litigant in that event. The existence of the ultimate purpose or benefit cannot constitute an abuse of process when that purpose is to bring about a result for which the law provides in the event that the proceeding terminates in the prosecutor’s favour: see Williams v Spautz (1992) 174 CLR 509 at 526-527. Here, Mr Ippolito’s intention is to pursue this proceeding for the very purpose for which it is designed. That is, for a sequestration order to be made in relation to Mr Cesco’s estate. The existence of the ability to make a claim under the Policy does not constitute an abuse of process. It is a result for which the law provides in the event that the sequestration order is made.

59 I turn then to Mr Lim’s email and the other matters which are said to arise out of it and to constitute a collateral purpose. Before doing so, I note that Mr Lim’s email must be read in context. It was sent in response to Mr Iuliano’s email also sent on 9 April 2021 timed at 9.40 am (see [15(2)] above). Mr Lim responded to the proposition put by Mr Iuliano that Mr Ippolito would be in a better position under the Instalment Order than if Mr Cesco was declared a bankrupt. The former would result in full payment of the Judgment Debt while the latter would probably result in a nil return. Viewed in context Mr Lim’s email did no more than respond to that contention. It cannot be said to give rise to any of the asserted collateral purposes.

60 As to the remaining collateral purposes for which Mr Cesco contends, there is no evidence that Mr Ippolito’s purpose in continuing with this proceeding is to pressure Mr Cesco to agree to the quantum of his costs in the SC Proceeding, to place himself in the position of a secured creditor by procuring a binding agreement from Ms Hall to guarantee repayment of the Judgment Debt and the costs order or to subvert the Instalment Orders by proceeding to bankruptcy rather than applying to the Supreme Court to rescind or set aside those orders with the object of expediting payment. As to the latter, the evidence establishes that the creditor’s petition was presented both before the Instalment Application was filed and before the Instalment Orders were made and notified to Mr Ippolito. That Mr Ippolito took no steps to object to or vary the Instalment Orders does not mean that he had a collateral purpose in pursuing this proceeding. As I have already said, the Instalment Orders do not operate to stay this proceeding nor prevent the making of a sequestration order and there is no evidence that the continuation of this proceeding in the face of the Instalment Orders is to subvert them.

61 It is not clear what is intended by the alleged collateral purpose of averting “delay prejudice” and “commercial prejudice”. But, in any event, the evidence from Mr Ippolito is, as I have already observed, that he is pursuing this proceeding in order to achieve some return on the Judgment Debt. It was never put to Mr Ippolito that he had any of the collateral purposes alleged or that he served the Bankruptcy Notice and presented the creditor’s petition without the intention of invoking the Court’s jurisdiction.

62 The alleged collateral purposes are not established by Mr Lim’s email or any other evidence before the Court.

63 Mr Cesco also submitted at the hearing that the fact that payments of the Judgment Debt were being made, in accordance with the Instalment Orders, is a “sufficient cause” under s 52(2)(b) of the Bankruptcy Act for a sequestration order not to be made. He contended that there were other means available to Mr Ippolito to expedite the payment if he was unhappy with the Instalment Orders, namely by applying to the Supreme Court to set aside or vary those orders, rather than pressing on with the creditor’s petition.

64 Mr Cesco conceded that this ground was not raised in his notice of grounds of opposition. In any event, given my conclusions at [36] and [60] above, the mere fact that Mr Ippolito could apply to set aside or vary the Instalment Orders rather than proceed on his creditor’s petition does not in the circumstances of this case amount to a sufficient cause based on which I would dismiss the creditor’s petition.

conclusion

65 Mr Cesco has failed to make out either of his grounds of opposition. As set out at [31] above I am satisfied of proof of the matters required by s 52(1) of the Bankruptcy Act. In addition Mr Ippolito has served on Mr Cesco the Trustee Consent. In those circumstances I am satisfied that I should exercise my discretion to make a sequestration order against the estate of Mr Cesco.

66 I will make orders accordingly.

I certify that the preceding sixty-six (66) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Markovic. |