Federal Court of Australia

Commissioner of Taxation v Zou (No 2) [2021] FCA 633

Table of Corrections | |

In Order 7, the orders referred to have been changed from “orders 3 to 7” to “orders 2 to 6” |

ORDERS

COMMISSIONER OF TAXATION OF THE COMMONWEALTH OF AUSTRALIA Applicant | ||

AND: | First Respondent REGISTRAR OF TITLES (VICTORIA) Second Respondent | |

DATE OF ORDER: |

THE COURT DECLARES THAT:

The First Respondent has failed to comply with the requirement to give security to the Applicant under section 255-100 of schedule 1 to the Taxation Administration Act 1953 (TAA53) pursuant to the notice dated 4 December 2020 (the Security Notice) given to the First Respondent by the Applicant pursuant to section 255-105 of schedule 1 to the TAA53.

THE COURT ORDERS THAT:

1. Within 7 days of this order, the First Respondent must comply with the requirement to give security to the Applicant as set out in the Security Notice, including that the First Respondent must give to the Applicant security by way of a first mortgage in registrable form (the Security) in respect of the property described as Lot 2608E on Plan of Subdivision 723350Q of Parent Title Volume 11825 Folio 364 being the property known as Unit 2608E, Level 26, 888 Collins Street, Docklands, in the State of Victoria.

2. The Applicant must serve a copy of these orders (the Orders) on the First Respondent by 5.00pm on 7 June 2021.

3. Pursuant to Rule 10.44(2) of the Federal Court Rules 2011, the Applicant has leave to serve the Orders on the First Respondent in the People’s Republic of China in accordance with the Hague Convention on the Service Abroad of Judicial and Extrajudicial Documents in Civil or Commercial Proceedings 1965.

4. Personal service and service in accordance with the Hague Convention on the Service Abroad of Judicial and Extrajudicial Documents in Civil or Commercial Proceedings 1965 of the Orders on the First Respondent be dispensed with.

5. Pursuant to Rule 10.24 of the Federal Court Rules 2011, the Applicant has leave to serve the Orders on the First Respondent by way of substituted service as follows:

(a) By leaving a copy of the Documents at Electronic Taxation & Accounting Pty Ltd, Suite 5, 42a Hercules Street Ashfield NSW 2131, marked with attention to Charles Shi;

(b) By leaving a copy of the Documents at Unit 102, 8 Murrell Street, Ashfield NSW 2131, marked with attention to Shuming Zou;

(c) By emailing a copy of the Documents to newage8@hotmail.com; and

(d) By emailing a copy of the Documents to 22859988@163.com.

6. Service of the Orders be deemed to have been effected on the First Respondent immediately once all the steps set out in the preceding order have been undertaken.

7. For the avoidance of doubt, orders 2 to 6 of the Orders are made to ensure compliance with the requirements of subsection 255-115(4) of schedule 1 to the TAA53, that is, as the Orders were not given orally by the Court to the First Respondent, the Court has caused a copy of the Orders to be served on the First Respondent in the manner set out in orders 2 to 6.

8. Order 1 of the orders made on 5 May 2021 be extended until the earlier of:

(a) 14 days after the First Respondent gives the Security to the Applicant; or

(b) Until further order.

9. Order 2 of the orders made on 5 May 2021 be extended until the earlier of:

(a) 14 days after the First Respondent gives the Security to the Applicant; or

(b) Until further order.

10. Liberty to apply in respect of the freezing orders made on 26 April 2021 be granted on 24 hours’ notice.

11. The First Respondent is to pay the Applicant’s costs of the proceedings, including the costs of the interlocutory application made on 26 April 2021, with such costs to be taxed in the absence of agreement.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

(Revised from transcript)

DAVIES J:

1 By s 255-100 of sch 1 to the Taxation Administration Act 1953 (Cth) (TAA53), the Commissioner of Taxation (the Commissioner) may require a taxpayer to give security for the payment of an existing or future tax related liability if, amongst other things, the Commissioner reasonably believes that the requirement is appropriate, having regard to all relevant circumstances. Section 255-100 of sch 1 to the TAA53 provides:

255-100 Commissioner may require security deposit

(1) The Commissioner may require you to give security for the due payment of an existing or future *tax related liability of yours if:

(a) the Commissioner has reason to believe that:

(i) you are establishing or *carrying on an *enterprise in Australia; and

(ii) you intend to carry on that enterprise for a limited time only; or

(b) the Commissioner reasonably believes that the requirement is otherwise appropriate, having regard to all relevant circumstances.

Note: A requirement to give security under this section is not a tax related liability. As such, the collection and recovery provisions in this Part do not apply to it.

(2) The Commissioner may require you to give the security:

(a) by way of a bond or deposit (including by way of payments in instalments); or

(b) by any other means that the Commissioner reasonably believes is appropriate.

(3) The Commissioner may require you to give security under this section:

(a) at any time the Commissioner reasonably believes is appropriate; and

(b) as often as the Commissioner reasonably believes is appropriate.

Example: The Commissioner may require additional security if he or she reasonably believes that the original security requirement underestimated the amount of the likely tax related liability.

2 If the Commissioner requires security to be given, a written notice of that requirement must be given: s 255-105 of sch 1 to the TAA53. Section 255-105 of sch 1 to the TAA53 provides:

255-105 Notice of requirement to give security

Commissioner must give notice of requirement to give security

(1) If the Commissioner requires you to give security under section 255-100, he or she must give you written notice of the requirement.

Content of notice

(2) The notice must:

(a) state that you are required to give the security to the Commissioner; and

(b) explain why the Commissioner requires the security; and

(c) set out the amount of the security; and

(d) describe the means by which you are required to give the security under subsection 255-100(2); and

(e) specify the time by which you are required to give the security; and

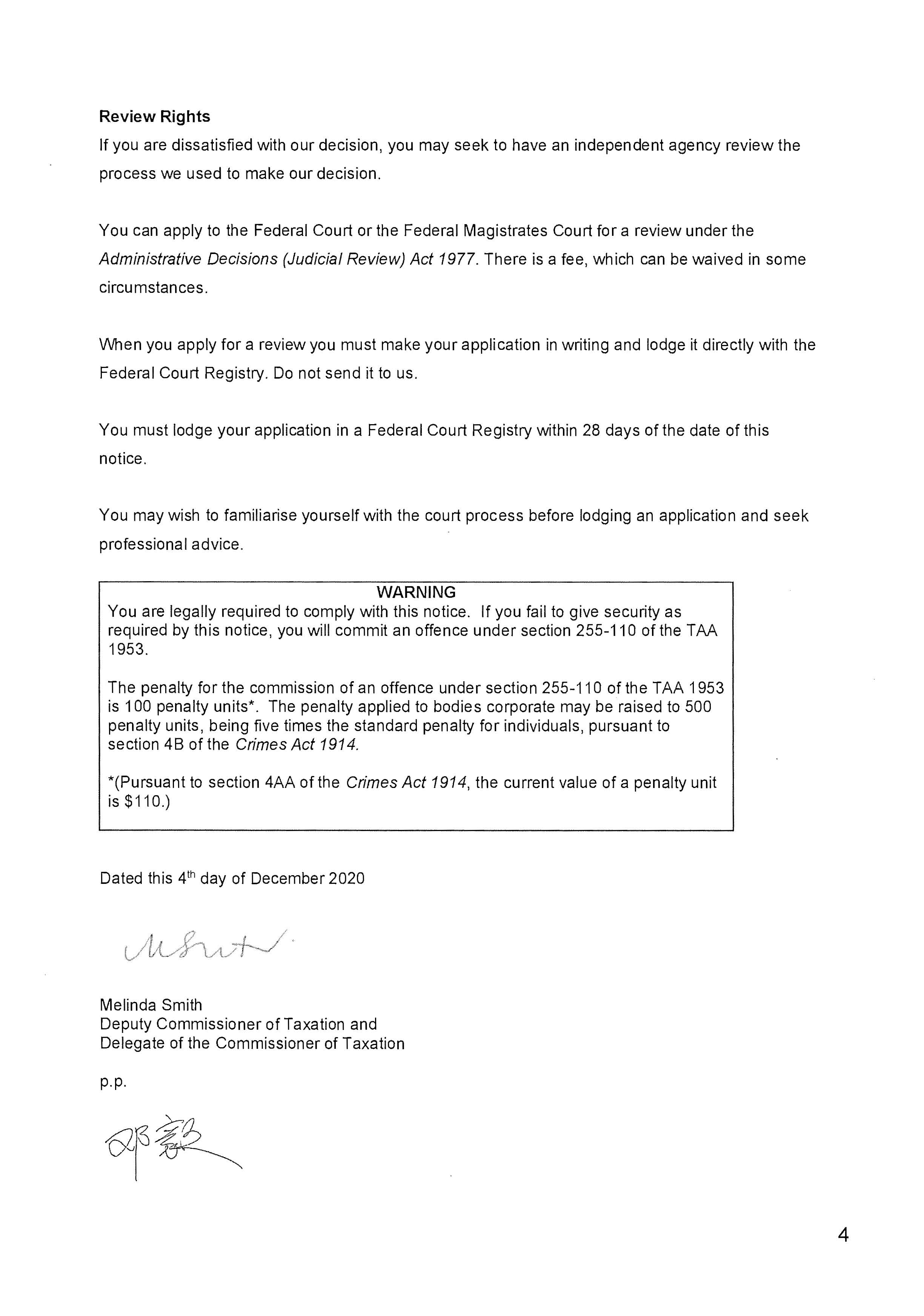

(f) explain how you may have the Commissioner's decision to require you to give the security reviewed.

(3) To avoid doubt, a single notice may relate to security for the payment of 2 or more existing or future *tax-related liabilities, but must comply with subsection (2) in relation to each of them.

When notice is given

(4) Despite section 29 of the Acts Interpretation Act 1901, a notice under subsection (1) is taken to be given at the time the Commissioner leaves or posts it.

Note: Section 28A of the Acts Interpretation Act 1901 may be relevant to giving a notice under subsection (1).

Miscellaneous

(5) A failure to comply with this section does not affect the validity of the requirement to give the security under section 255-100.

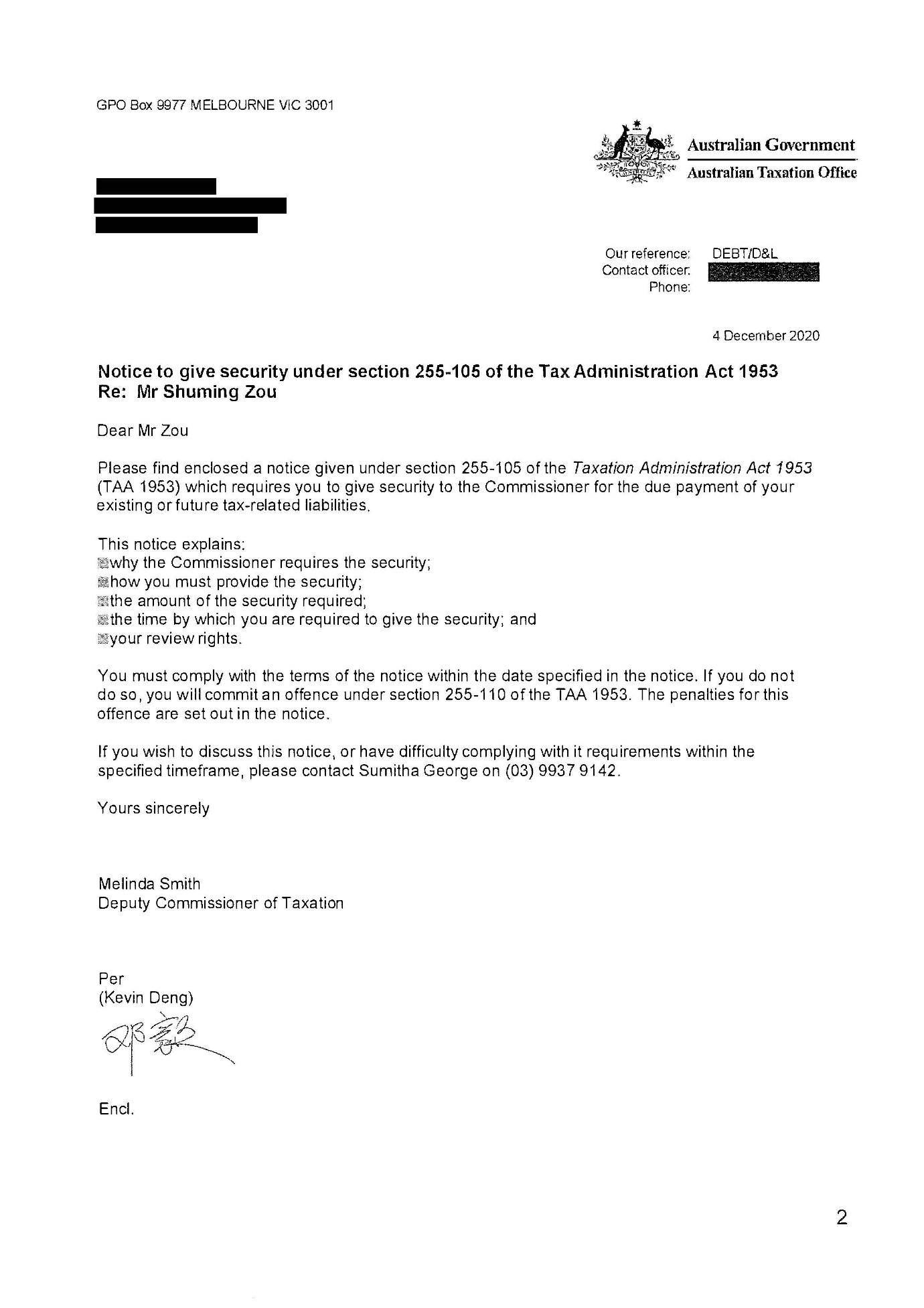

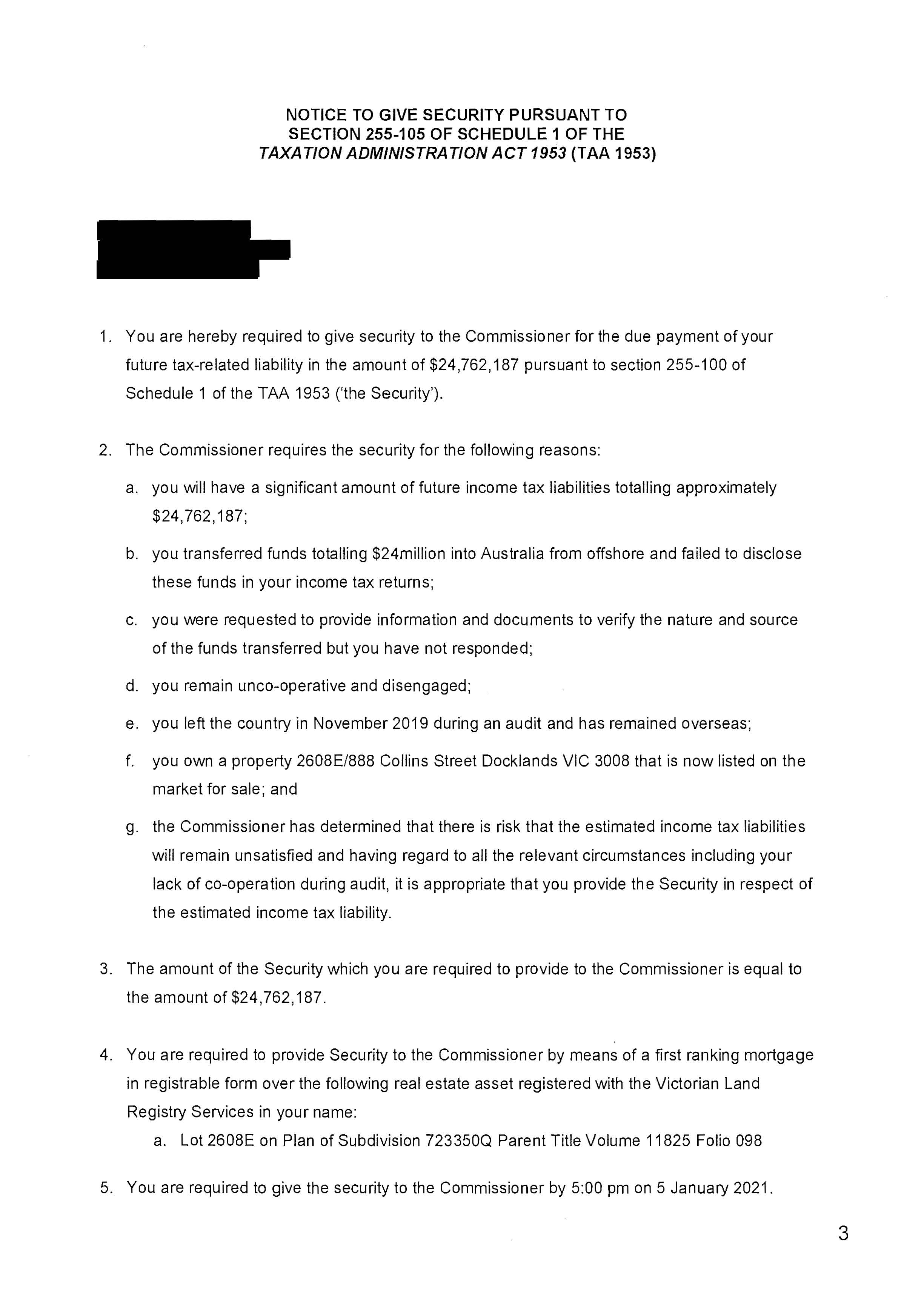

3 By a notice given on 4 December 2020 by the Commissioner to the first respondent (Mr Zou) pursuant to s 255-105, Mr Zou was required to give security to the Commissioner in the amount of $24,762,187 by 5:00 pm on 5 January 2021 for the due payment of a future tax related liability of Mr Zou. The security was required to be given by means of a first ranking mortgage in registrable form over the real estate registered with the Victorian Land Registry Services in his name, described as being Lot 2608E on Plan of Subdivision 723350Q, Parent Title Volume 11825 Folio 098. The evidence before the Court is that Mr Zou did not comply with the security notice or seek to have the decision of the Commissioner to give the security notice reviewed.

4 The Commissioner seeks a declaration that Mr Zou has failed to comply with the requirement to give security and an order under s 255-115 that Mr Zou comply with the requirement to give security. Section 255-115 provides:

255-115 Order to comply with requirement

(1) The Federal Court of Australia may, on the application of the Commissioner, order you to comply with a requirement to give security under section 255-100, if the Commissioner has given you notice of the requirement under subsection 255-105(1).

(2) If the Court makes an order under subsection (1), the Court may also order you to comply with such other requirements made, or that could be made, in relation to you under the taxation law as the Court considers necessary to ensure the effectiveness of the requirement referred to in that subsection.

(3) An order under subsection (1) or (2) may require you to comply with the requirement on or before a day specified in the order.

(4) If an order under subsection (1) or (2) is not given to you orally by the court, the proper officer of the court must cause a copy of the order to be served on you in the prescribed manner, or otherwise as may be ordered by the court.

5 Service of the originating application and supporting affidavits was effected on Mr Zou in accordance with an order for substituted service made on 26 April 2021: Commissioner of Taxation v Zou [2021] FCA 433. Service of the order made on 5 May 2021 setting the matter down for hearing on 2 June 2021 was effected by the order being emailed to the same two email addresses used to effect service of the originating application and supporting affidavits in accordance with the substituted service order. There has been no response from Mr Zou and Mr Zou has not attended the hearing, however there is nothing to indicate that the methods of service would not have brought the application and hearing to Mr Zou’s attention.

6 I am satisfied that the declaration and order under s 255-115 sought by the Commissioner should be made for the following reasons.

7 First, I am satisfied that the power to require Mr Zou to give security was enlivened in that:

(a) at the time of service of the security notice, Mr Zou had a future tax related liability for primary tax and penalties totalling $24,762,187 (s 255-100(1)). That future tax liability has since crystallised into an actual liability by the issue by the Australian Taxation Office of notices of amended assessment of income tax and penalties in March 2021 with due dates for payments variously of 22 March 2021, 29 March 2021 and 1 April 2021. Copies of the notices of assessment are evidence in these proceedings and the evidence is that none of the tax, as assessed, has been paid; and

(b) the security notice given to Mr Zou under s 255-105 evidences that the Commissioner reasonably believed that the requirement for Mr Zou to give security was appropriate, having regard to all relevant circumstances: s 255-100(1)(b). As required by s 255-105, the Commissioner gave the following explanation as to why he requires the security:

(a) you will have a significant amount of future income tax liabilities totalling approximately $24,762,187;

(b) you transferred funds totalling $24,000,000 into Australia from offshore and failed to disclose these funds in your income tax returns;

(c) you were requested to provide information and documents to verify the nature and source of the funds transferred but you have not responded;

(d) you remain unco-operative and disengaged;

(e) you left the country in November 2019 during an audit and has (sic) remained overseas;

(f) you own a property 2608E/888 Collins Street, Docklands, VIC, 3008 that is now listed on the market for sale; and

(g) the Commissioner has determined that there is a risk that the estimated income tax liabilities will remain unsatisfied and having regard to all the relevant circumstances including your lack of co-operation during audit, it is appropriate that you provide the Security in respect of the estimated income tax liability

That explanation is consistent with the evident purpose for which a security notice may be given, namely to facilitate the recovery of tax where there is a risk, arising from the nature of the business being undertaken or proposed to be undertaken, or by reason of other circumstances, that the liability to pay tax will not be met: Keris Pty Ltd (Trustee) v Deputy Commissioner of Taxation [2015] FCA 1381 at [30]–[31]; the Explanatory Memorandum, Tax Laws Amendment (Transfer of Provisions) Bill 2010 (Cth), 2.41-2.42.

8 Secondly, the security notice served on Mr Zou on 4 December 2020 (see Annexure 1) meets the requirements of s 255-105(2). As required by s 255-105(2), the security notice stated that Mr Zou was required to give security, explained why the Commissioner requires the security, set out the amount of the security to be given, described the means by which Mr Zou was required to give the security, specified the time by which the security was to be provided and explained how the Commissioner’s decision may be reviewed.

9 Thirdly, the Commissioner’s evidence is that Mr Zou did not comply with the security notice by 5 January 2021 or at any time thereafter by giving the first ranking mortgage as specified or other security in any other form.

10 Accordingly it is appropriate to grant the declaration sought and make orders under s 255-115, including an order under s 255-115(4), as Mr Zou did not attend the hearing and there was no appearance on his behalf. As there is no reason to doubt that the methods of substituted service adopted for the purposes of serving the application and supporting material did not bring those documents to the attention of Mr Zou, the same methods of substituted service (outlined in Commissioner of Taxation v Zou [2021] FCA 433) should apply. I note that there is an error in the land description at para 4(a) of the security notice, which gives a folio number of “098” when it should read “364”. That error duplicates the error in the land description contained in the certificate of title itself. Hence, for accuracy, the correct folio number of “364” will appear in order 1.

11 Additionally, the Commissioner seeks an order that the freezing orders against Mr Zou and the second respondent, the Registrar of Titles be extended until the earlier of either 14 days after the security is given or until further order: Commissioner of Taxation v Zou [2021] FCA 433 at [10]. It is appropriate to grant that extension. Given that Mr Zou has not participated in the proceeding, given his substantial tax liability and his failure to comply with the security notice and given his absence from Australia, there is a high risk that he may not comply with any order of the Court in respect of the required security and there remains the same risk of asset dissipation that justified the making of the freezing order against him in the first place. Secondly, even if security was given the Commissioner would still need some time to register the mortgage. A 14 day time period seems appropriate for that purpose and the freezing order would then automatically be discharged after security was given.

I certify that the preceding eleven (11) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Davies. |

Associate:

ANNEXURE 1