FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v Forex Capital Trading Pty Limited, in the matter of Forex Capital Trading Pty Limited [2021] FCA 570

ORDERS

DATE OF ORDER: |

BY CONSENT, THE COURT DECLARES THAT:

AGAINST THE FIRST DEFENDANT:

Contraventions of s 961K(2) of the Corporations Act

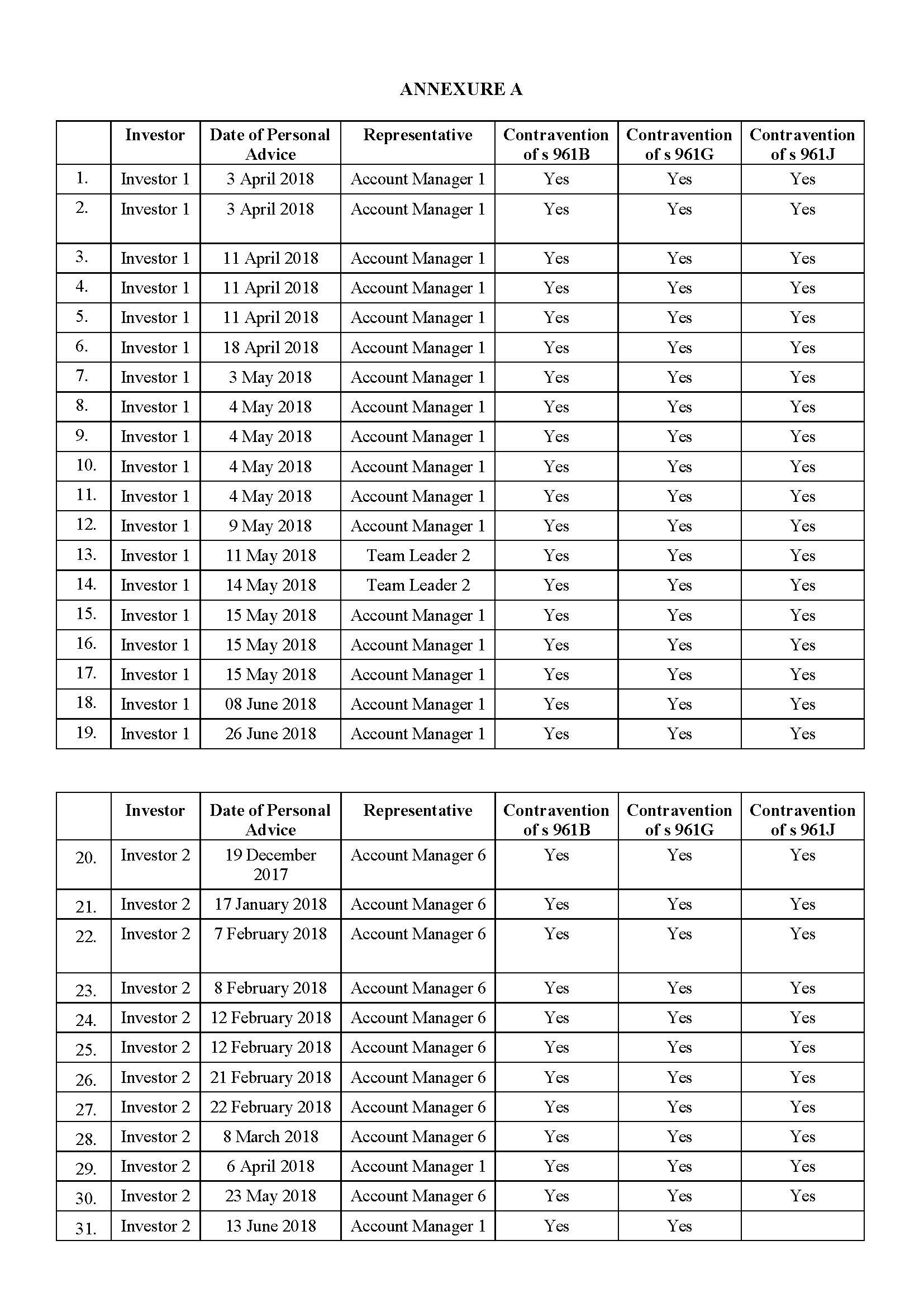

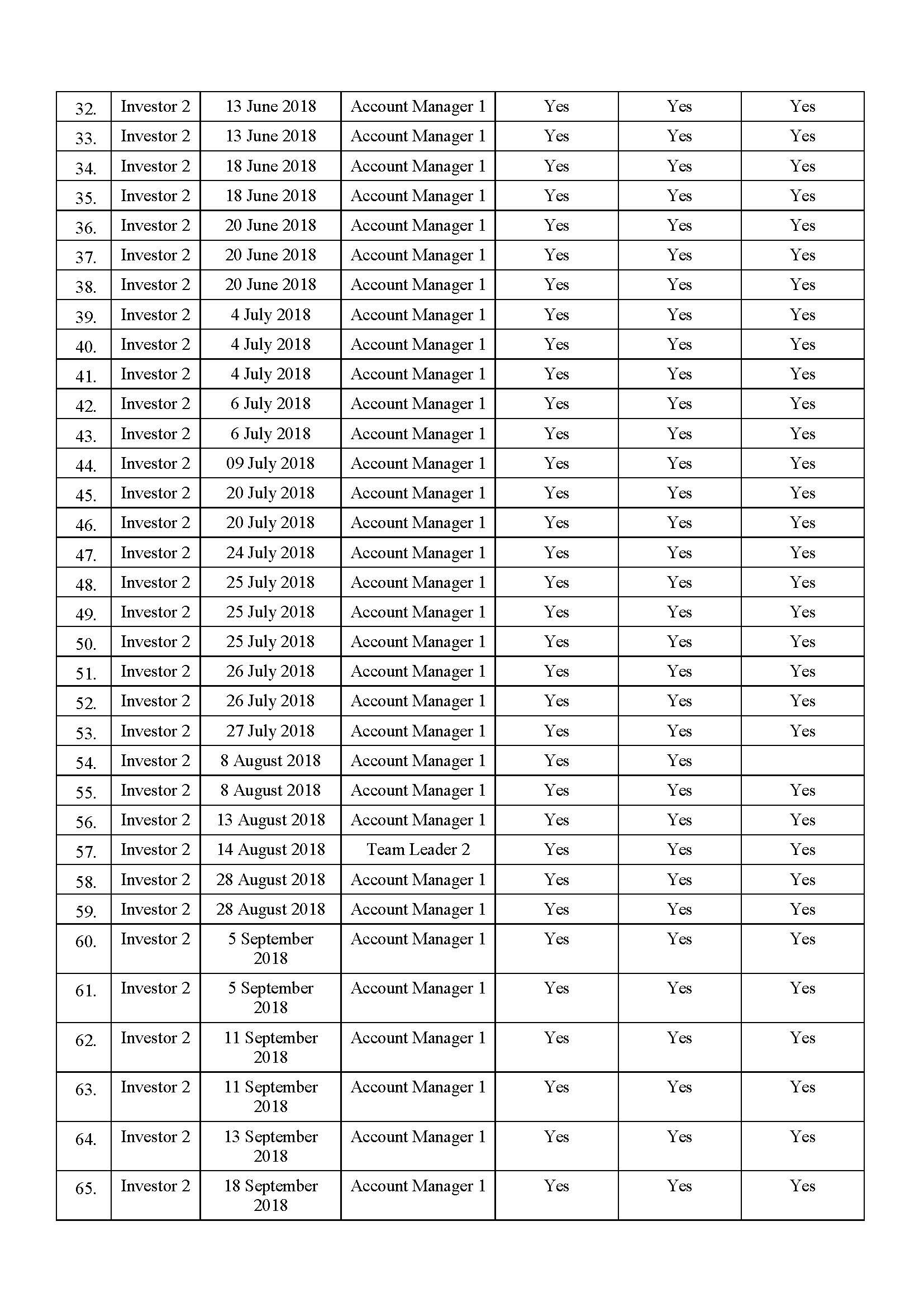

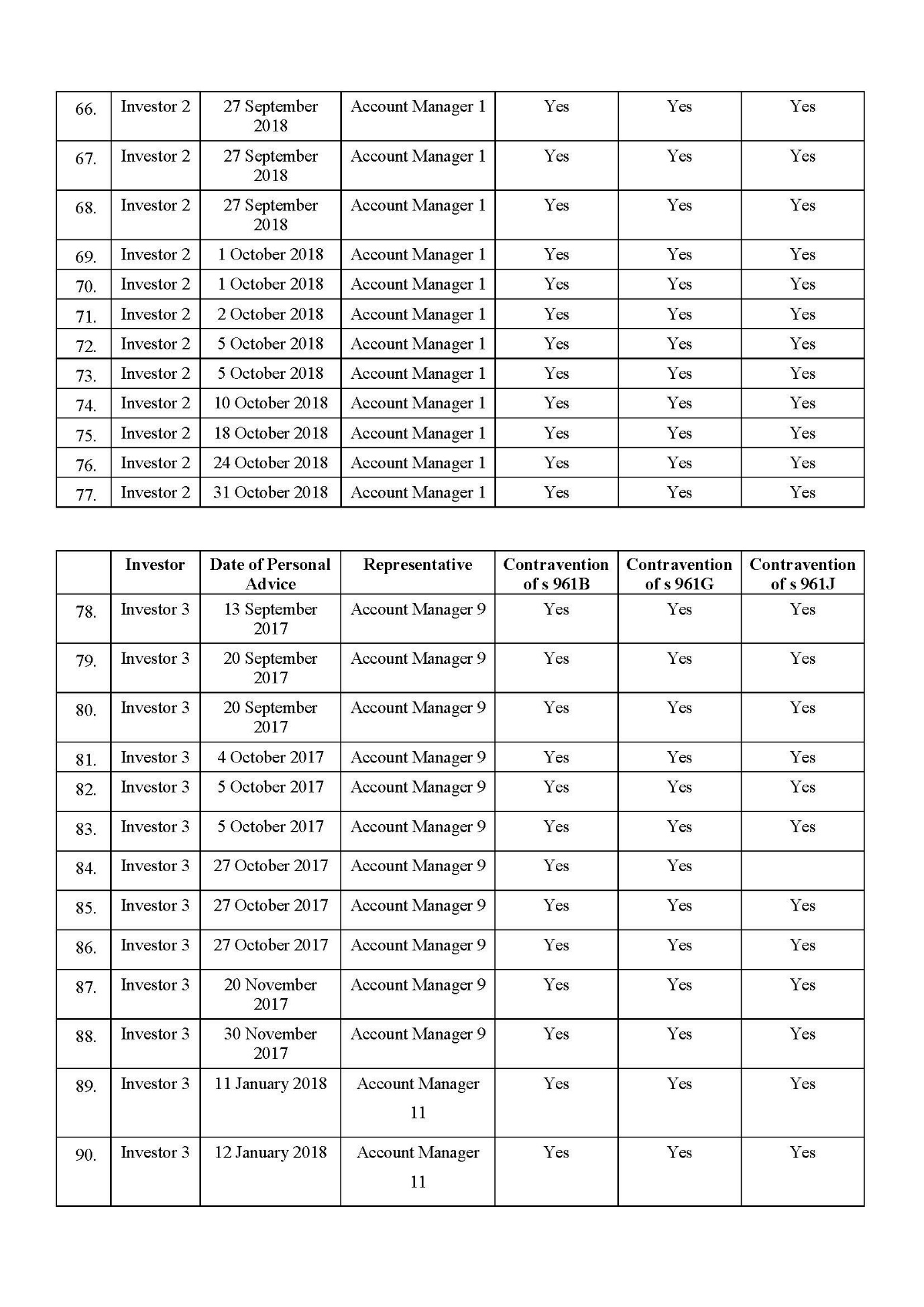

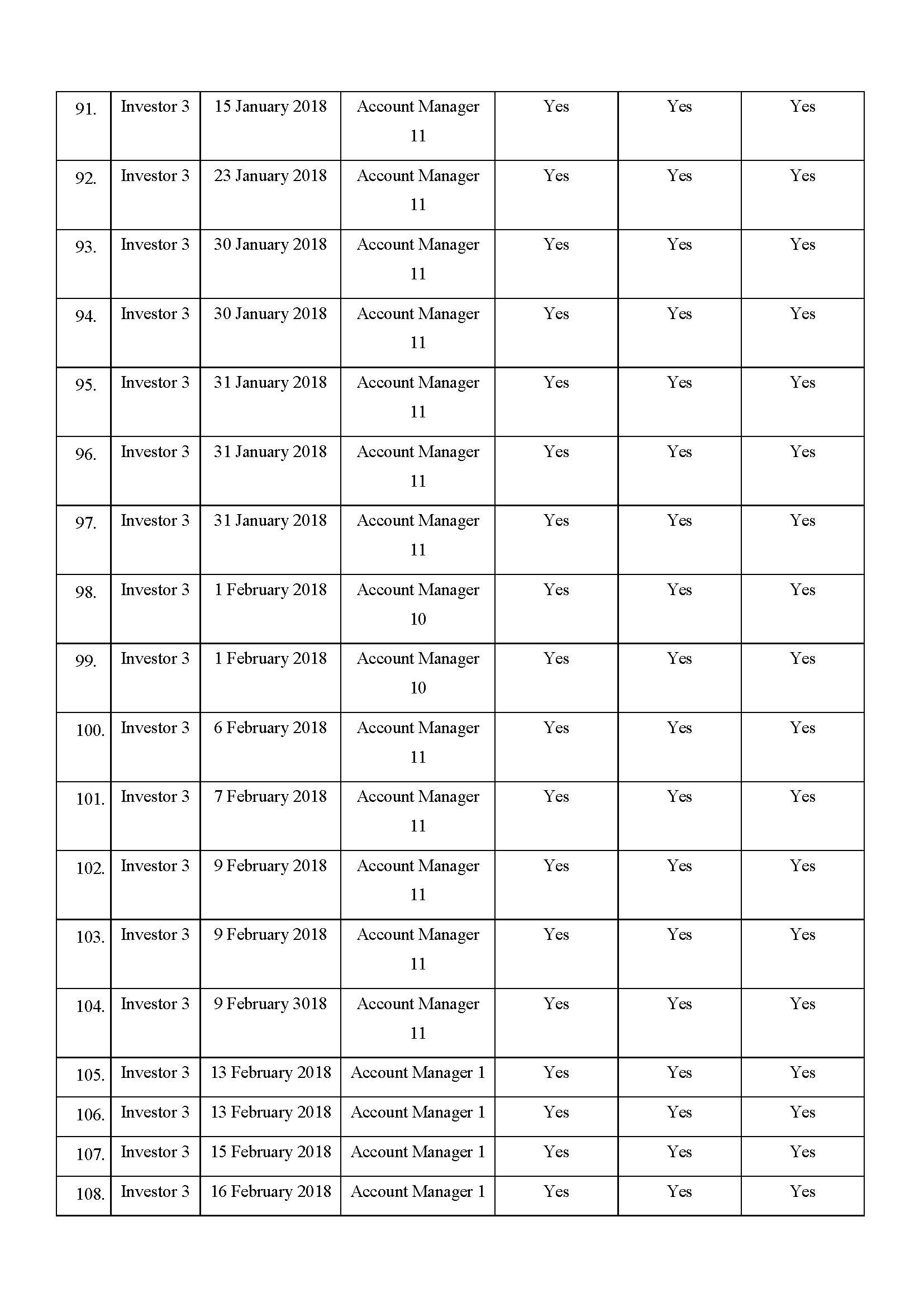

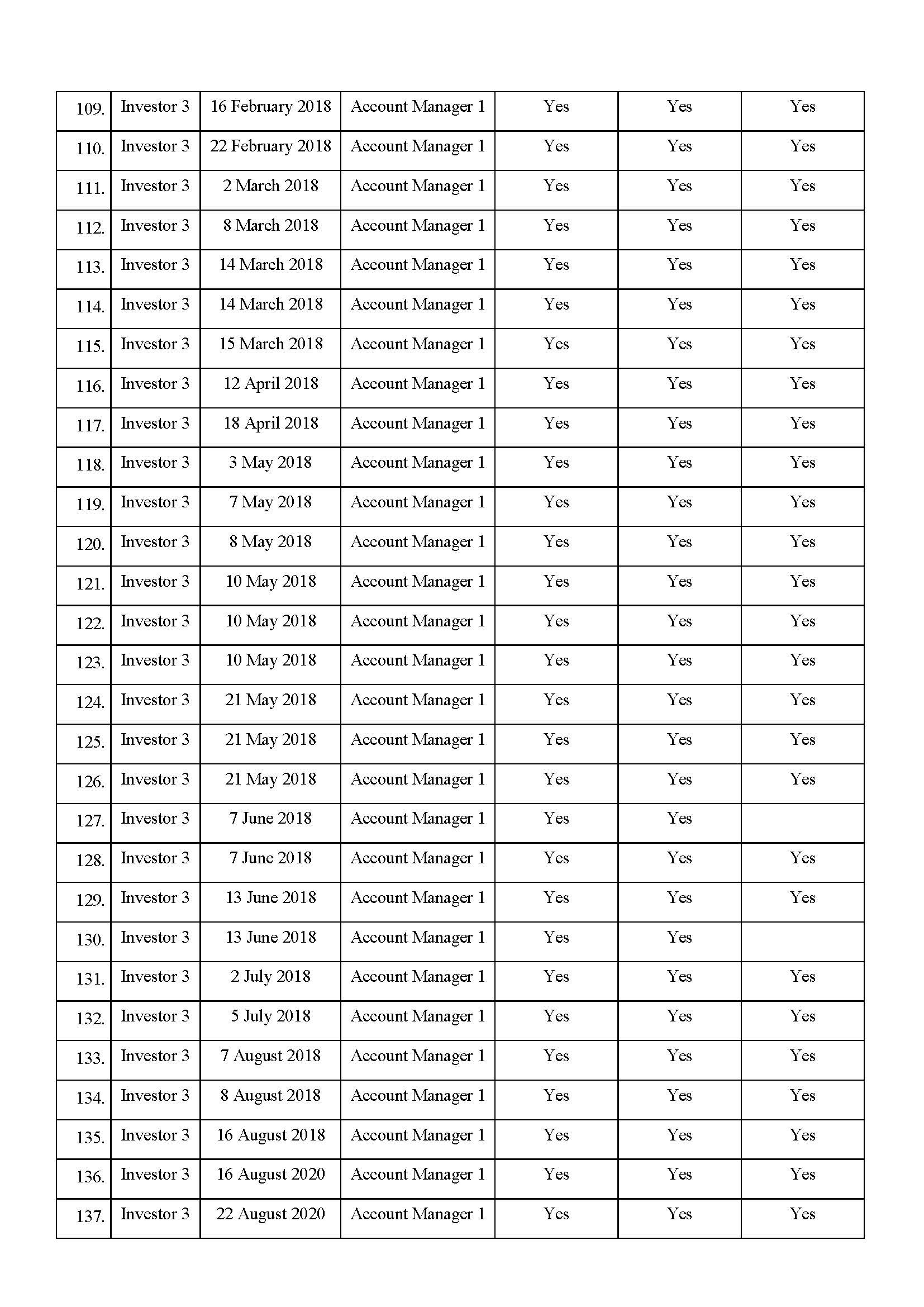

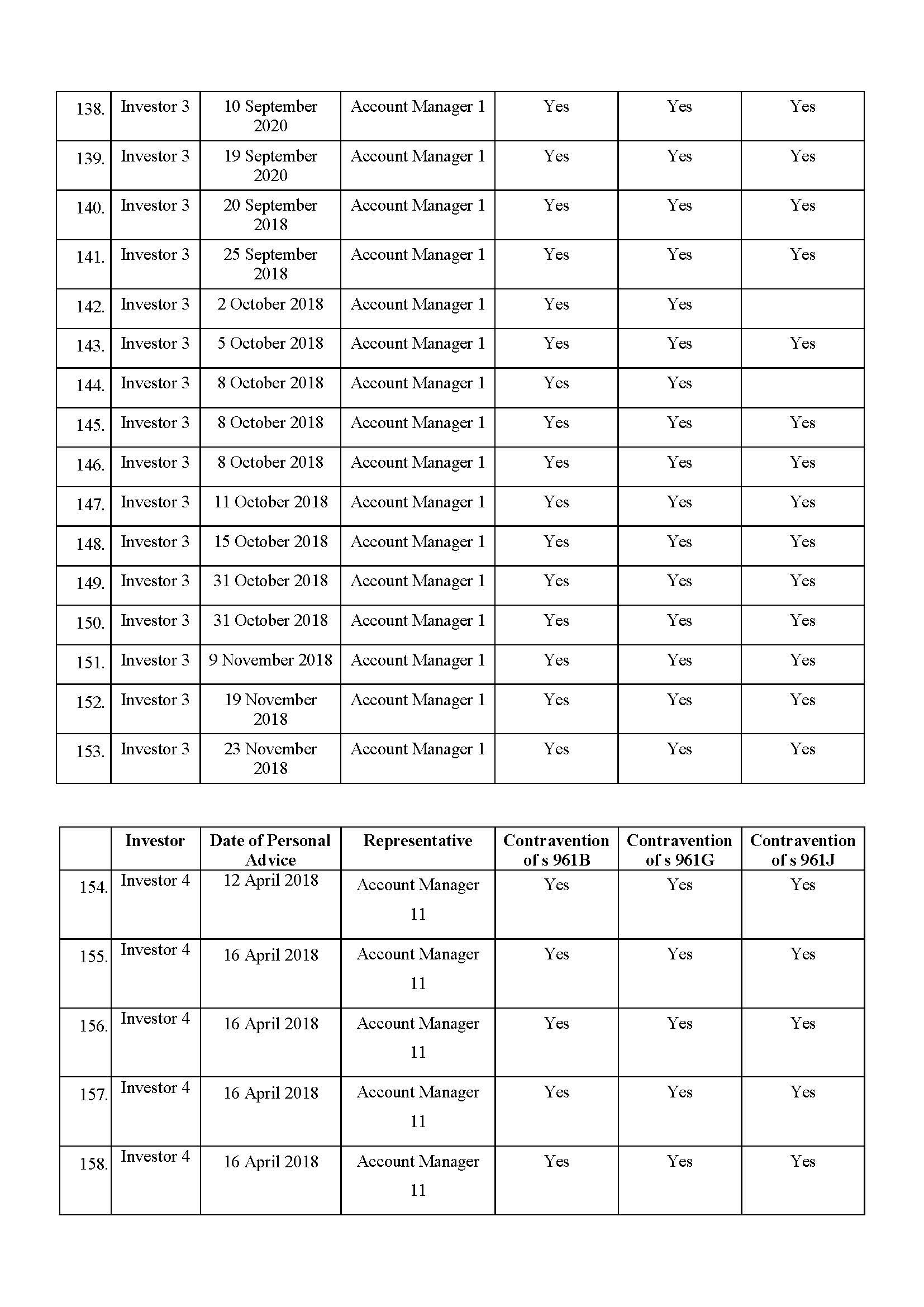

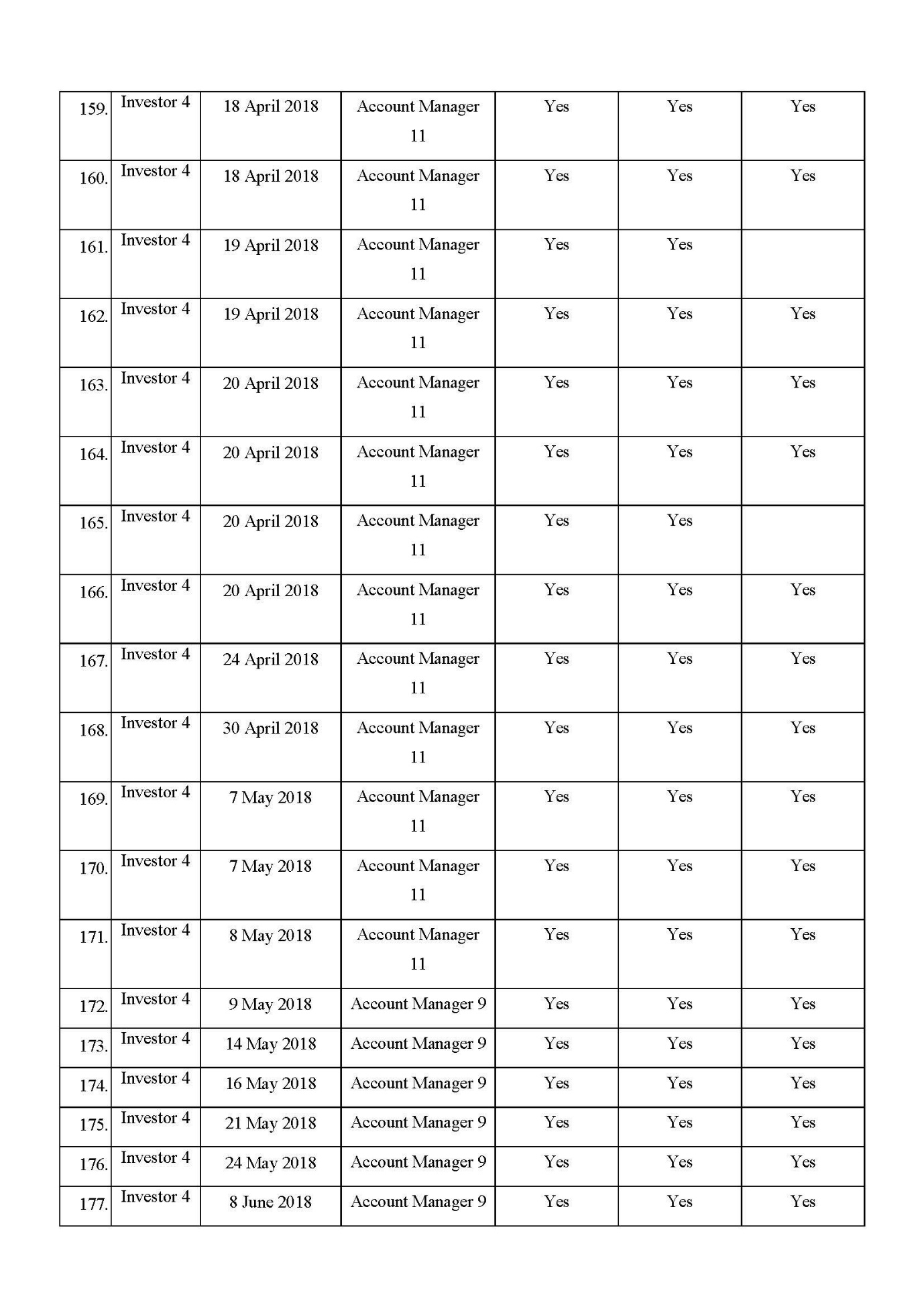

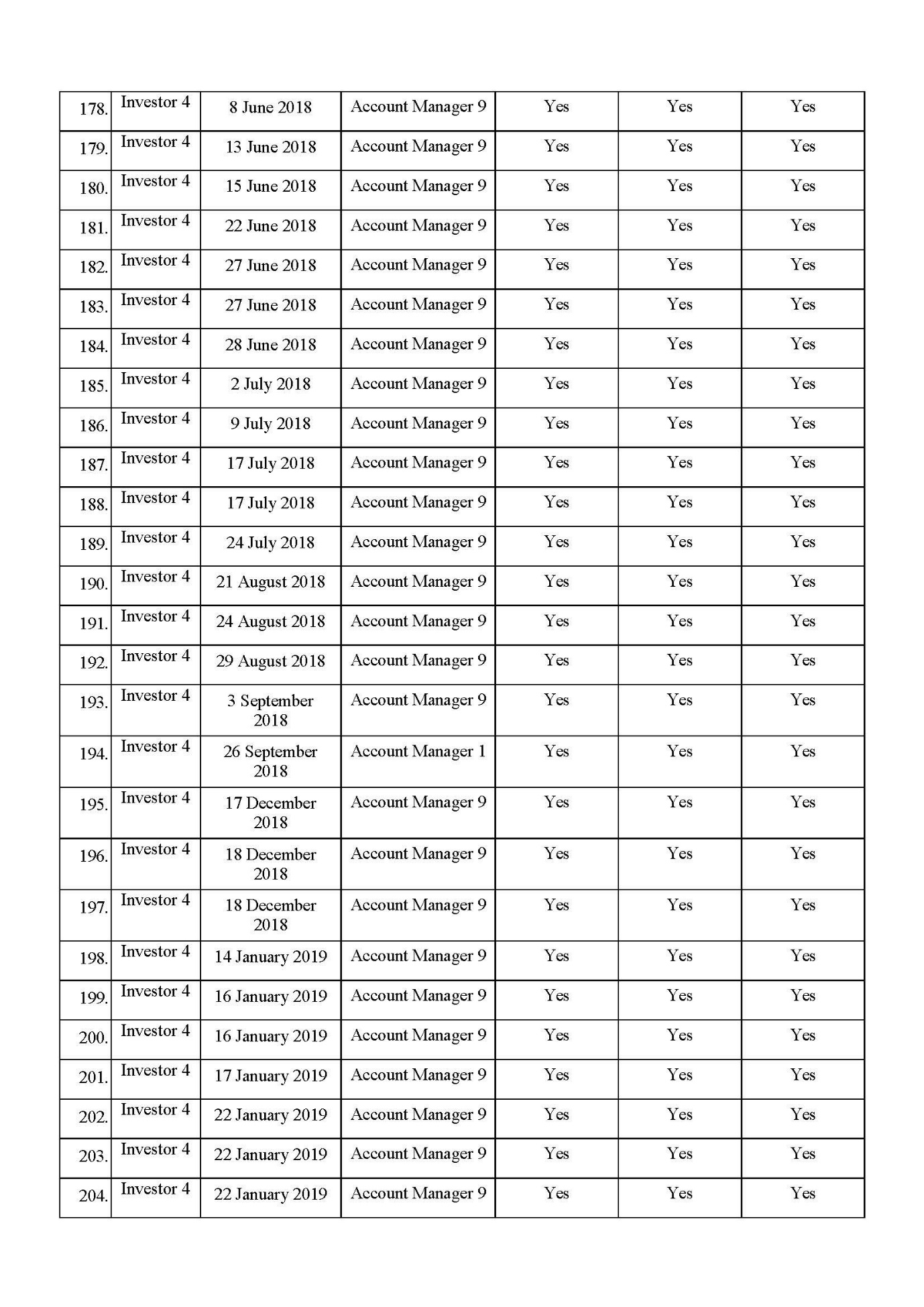

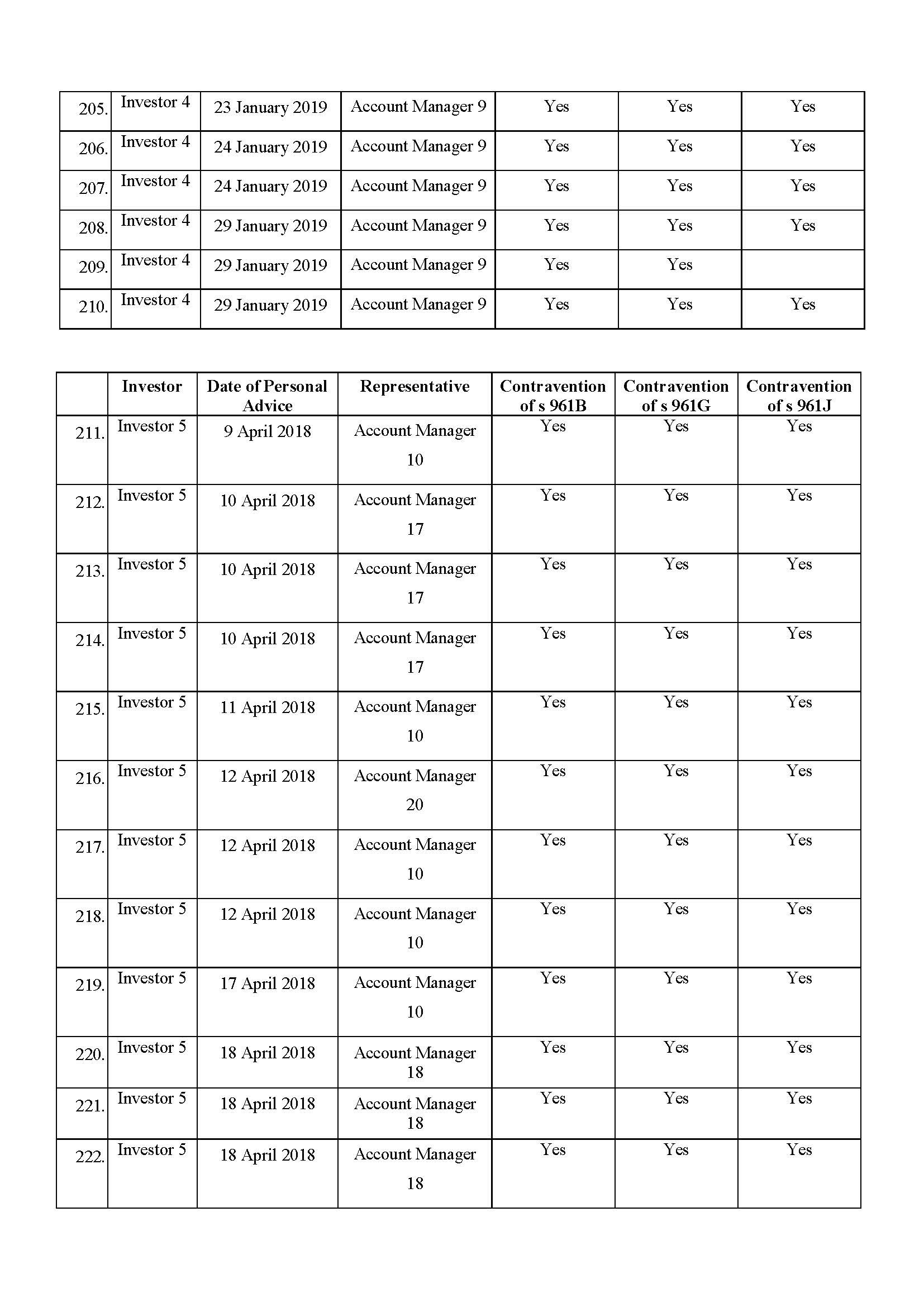

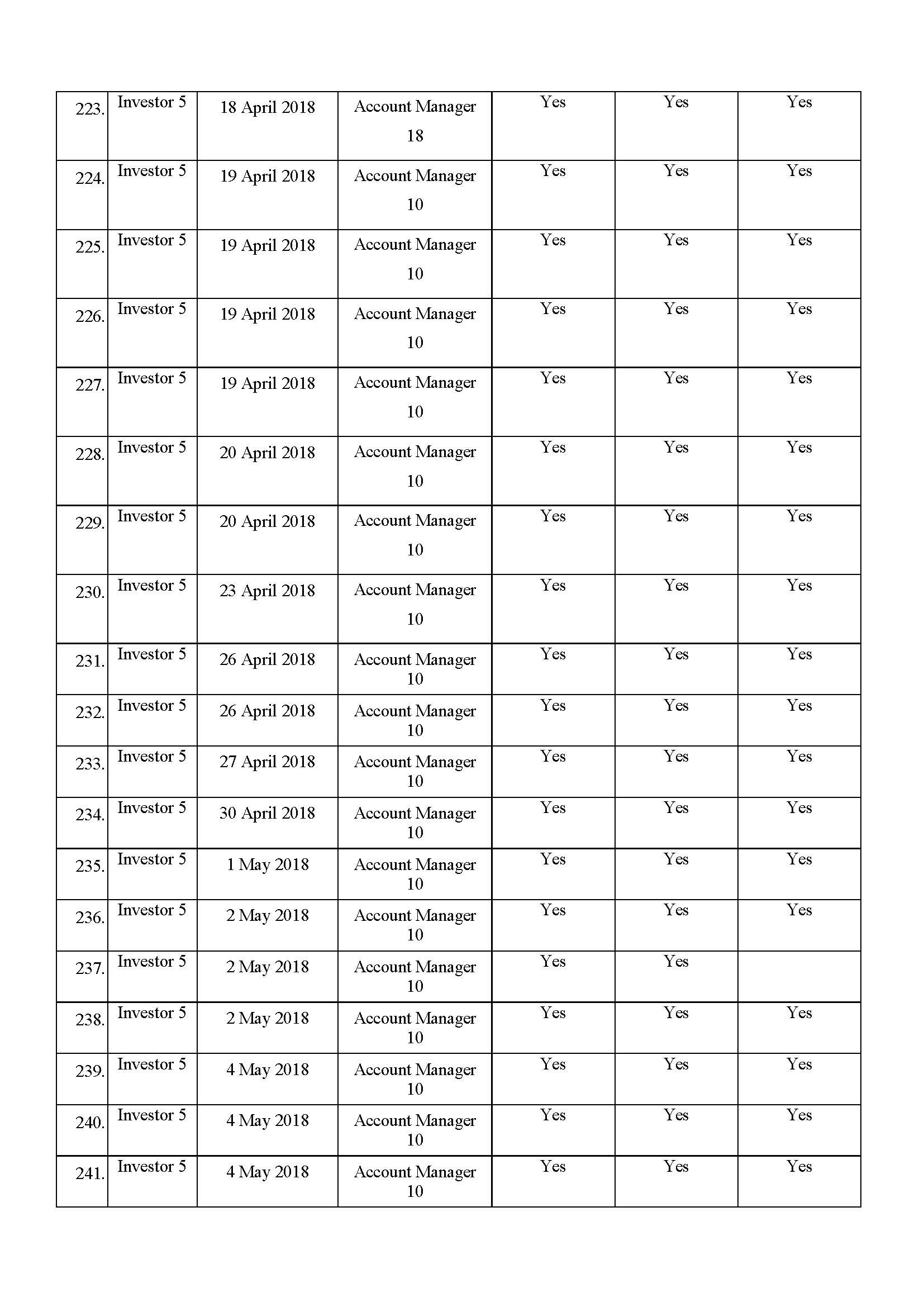

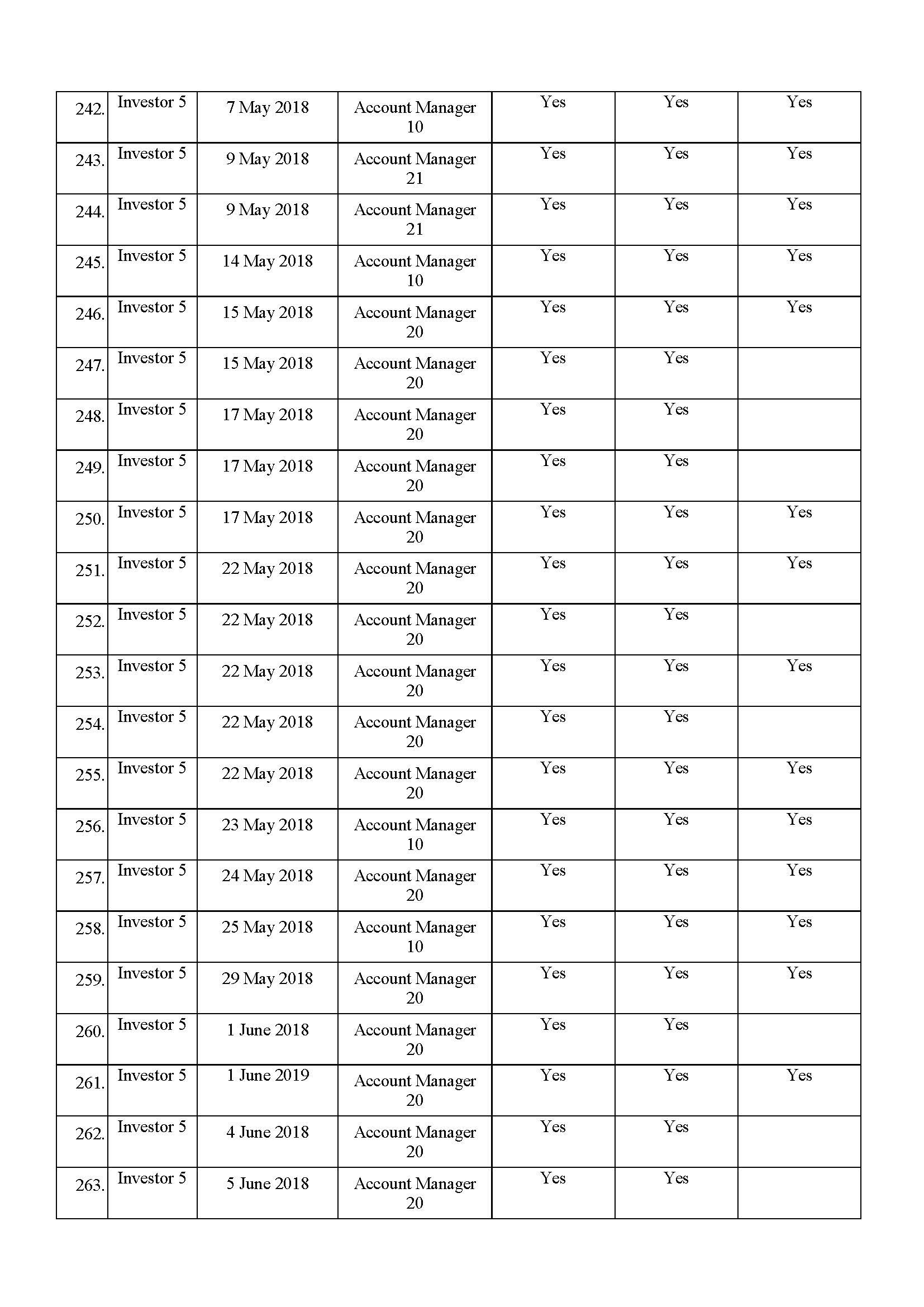

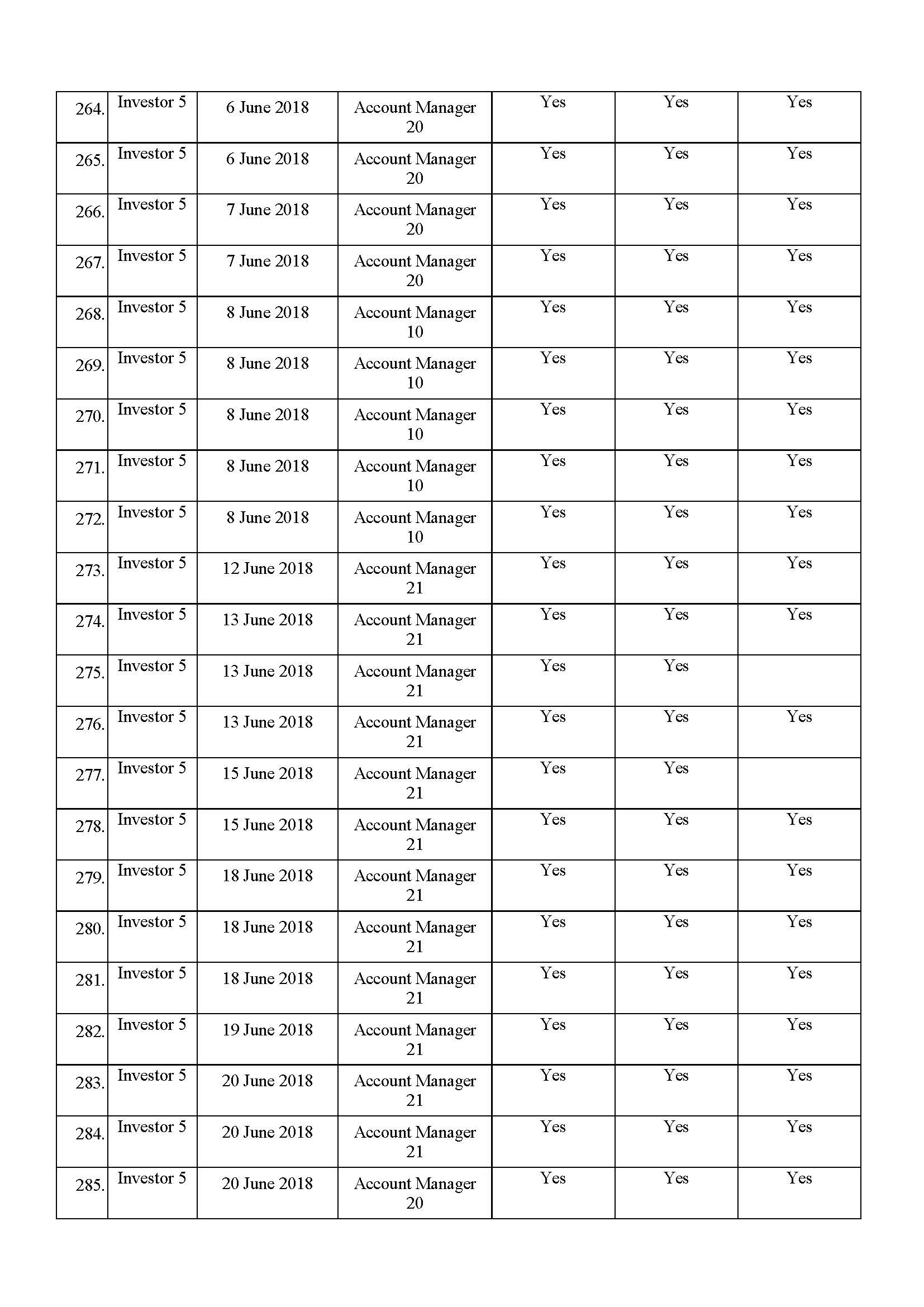

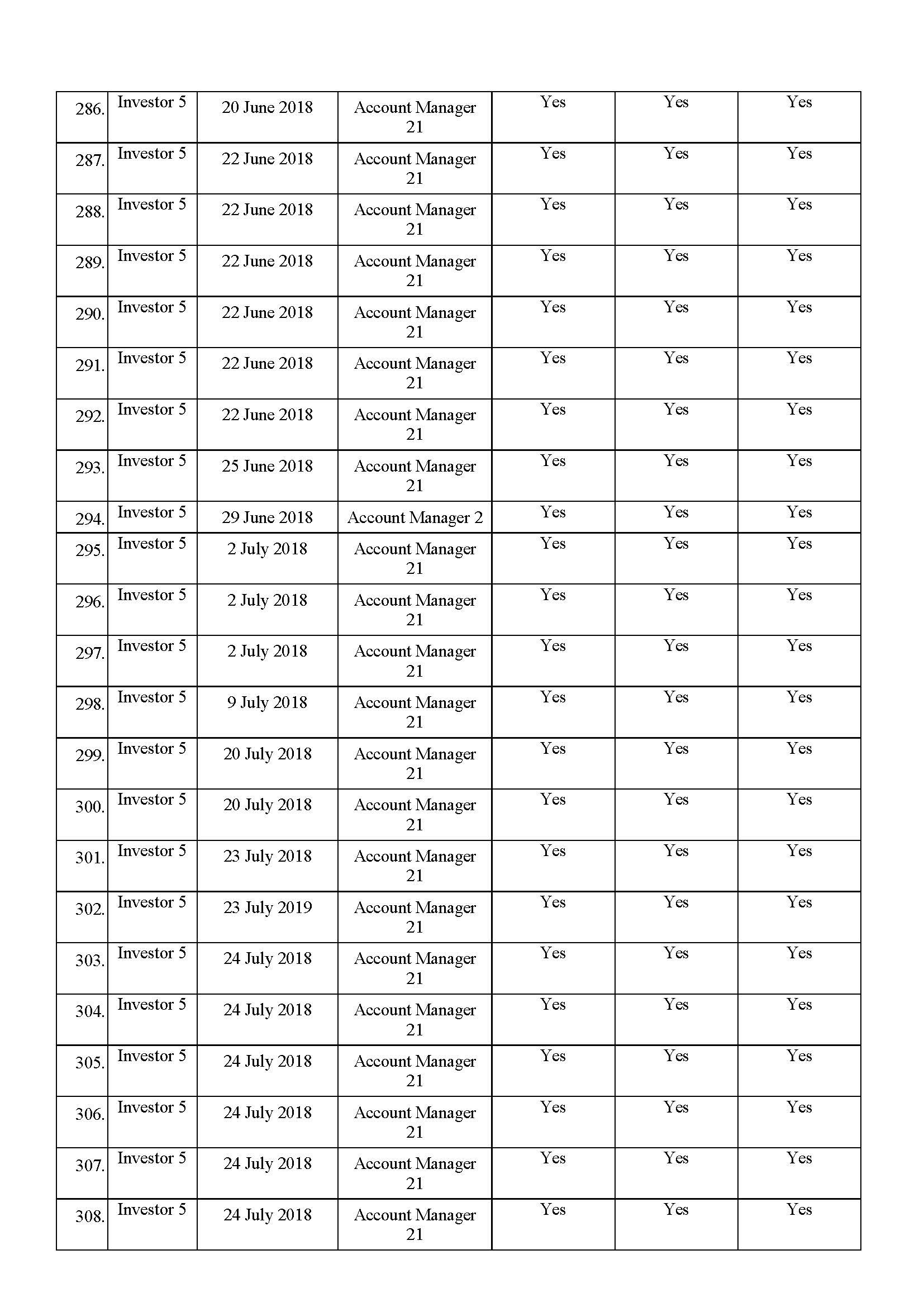

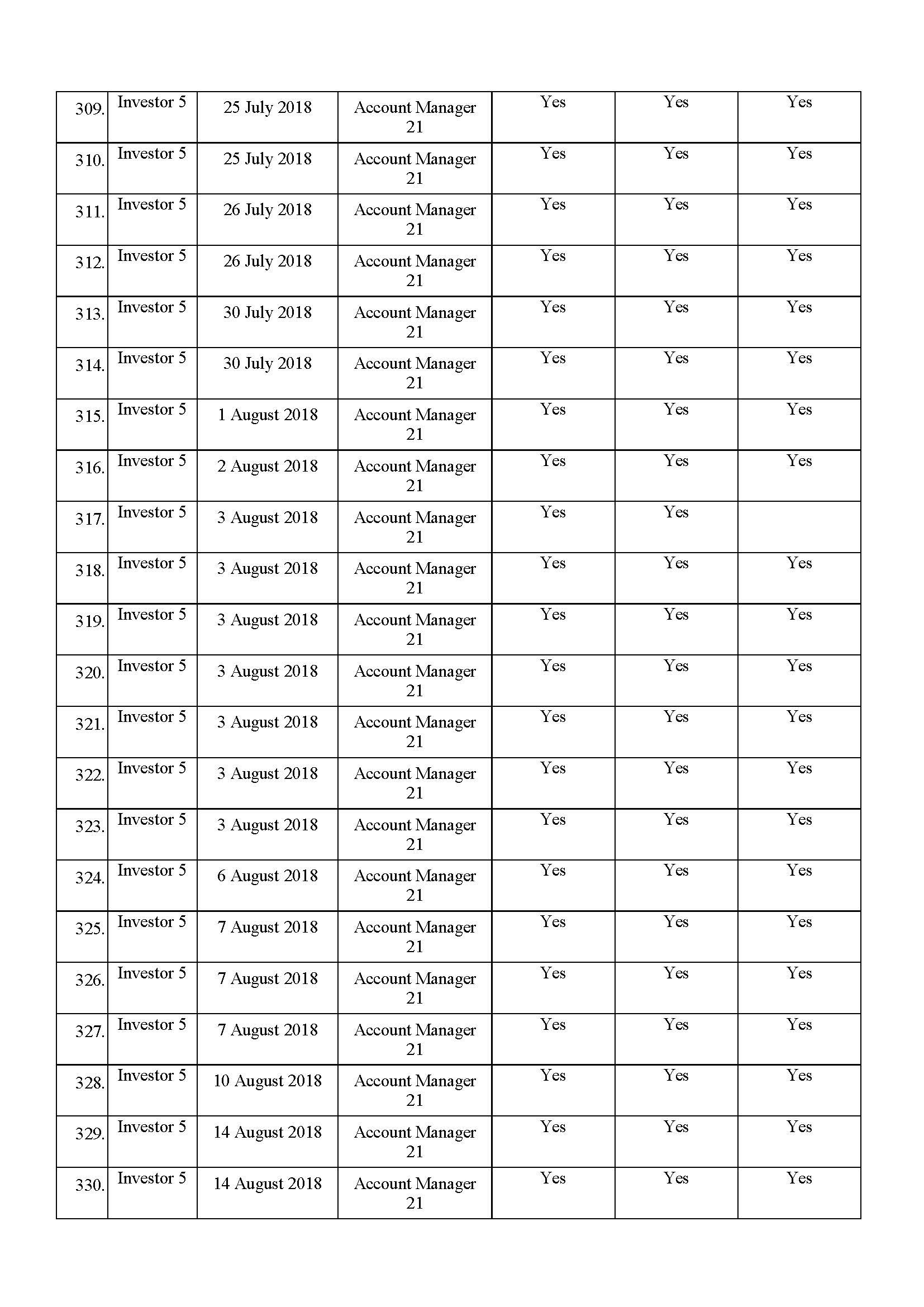

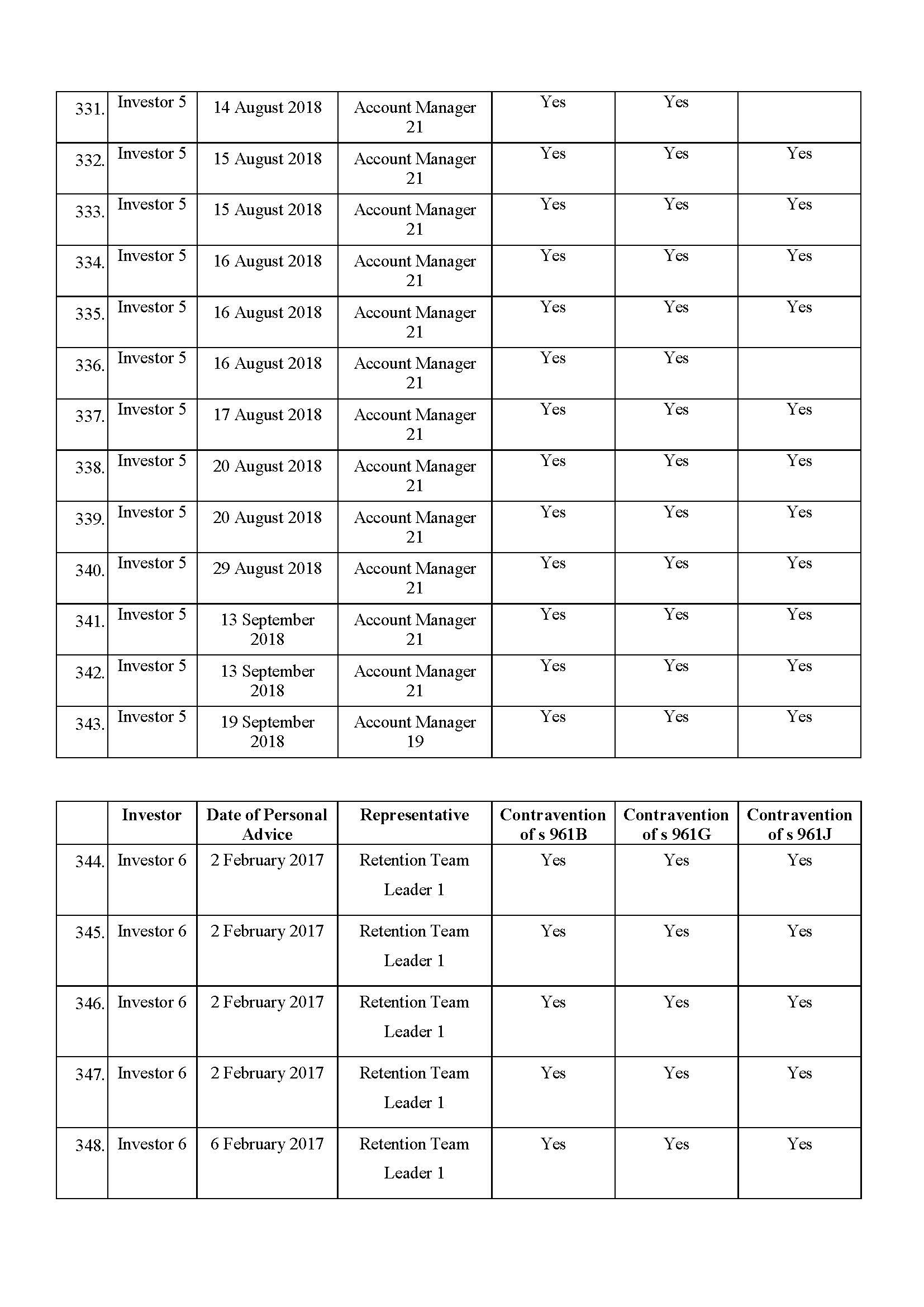

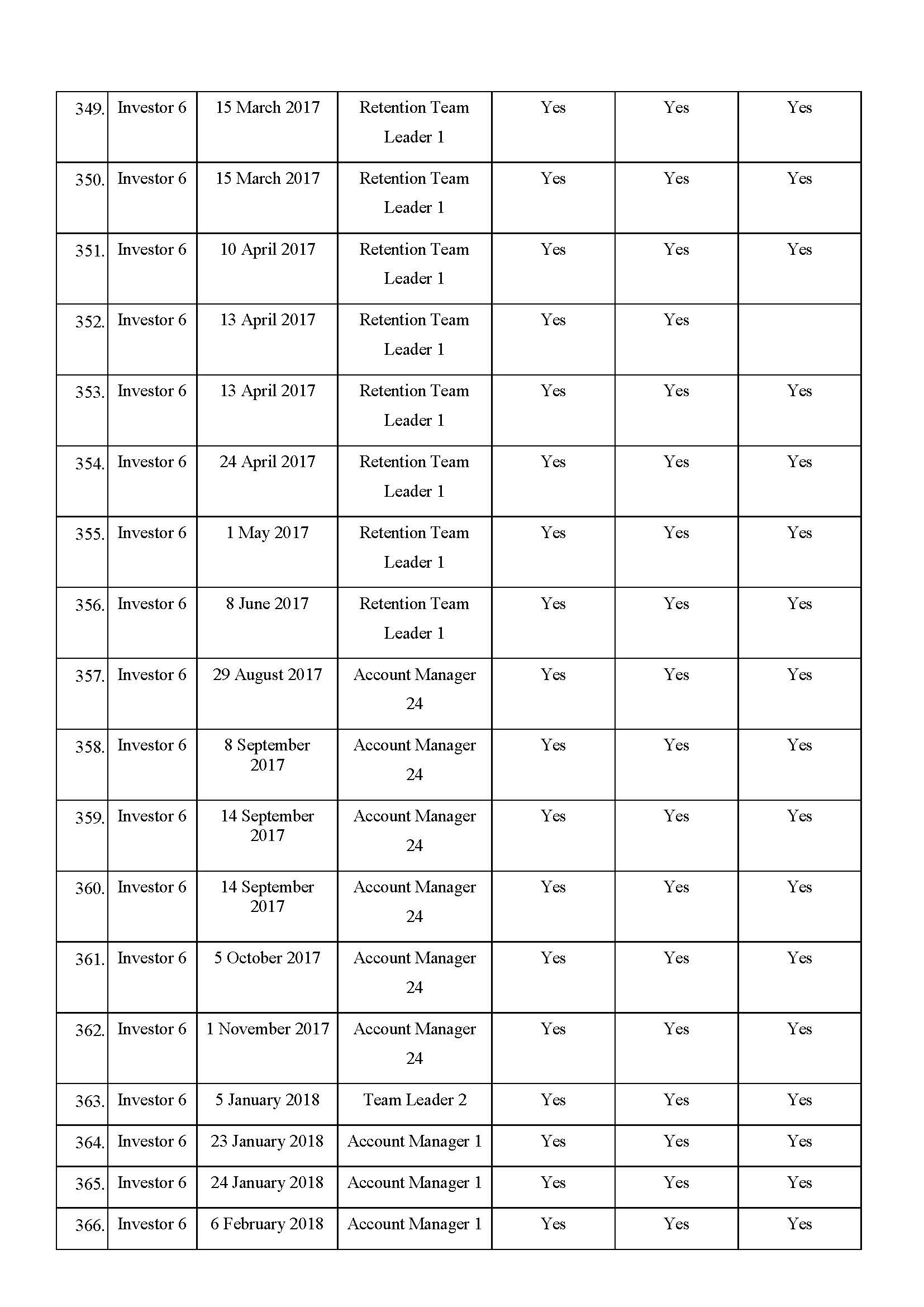

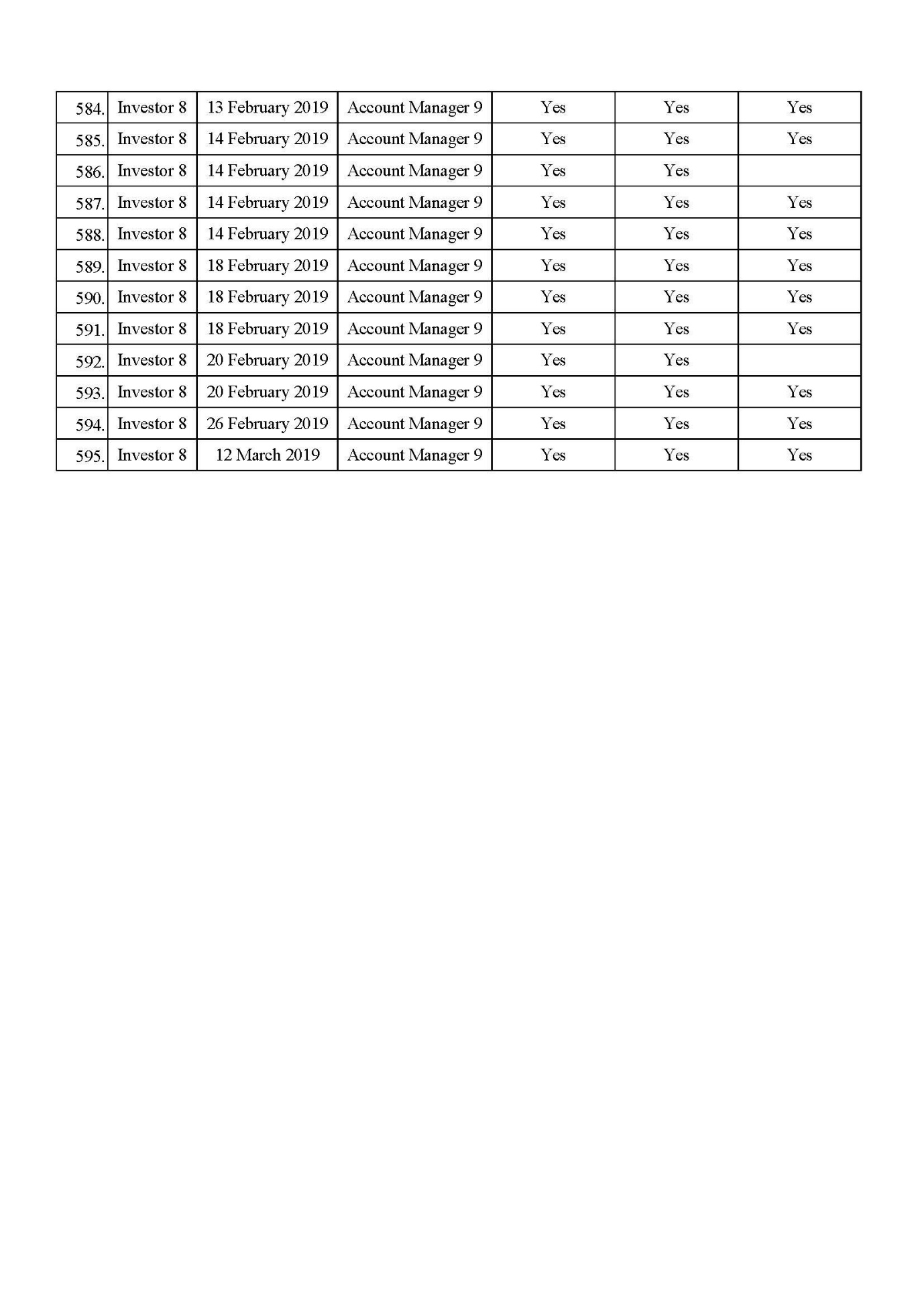

1. The First Defendant contravened s 961K(2) of the Corporations Act 2001 (Cth) (the Corporations Act) in 595 instances by reason of its representatives, other than an authorised representative, having contravened s 961B(1) of the Corporations Act by failing to act in the best interests of a client (who is identified in Annexure A, relevantly to each contravention, as Investor 1, Investor 2, Investor 3, Investor 4, Investor 5, Investor 6, Investor 7 or Investor 8) when providing personal advice to the relevant client on each of the dates identified in Annexure A.

2. The First Defendant contravened s 961K(2) of the Corporations Act in 595 instances by reason of its representatives, other than an authorised representative, having contravened s 961G of the Corporations Act by providing personal advice to a client (who is identified in Annexure A, relevantly to each contravention, as Investor 1, Investor 2, Investor 3, Investor 4, Investor 5, Investor 6, Investor 7 or Investor 8) on each of the dates identified in Annexure A when it would not have been reasonable to conclude that the advice was appropriate to the relevant client, had the representative satisfied the duty under s 961B to act in the best interests of the client.

3. The First Defendant contravened s 961K(2) of the Corporations Act in 556 instances by reason of its representatives, other than an authorised representative, having contravened s 961J(1) of the Corporations Act by providing personal advice to a client (who is identified in Annexure A, relevantly to each contravention, as Investor 1, Investor 2, Investor 3, Investor 4, Investor 5, Investor 6, Investor 7 or Investor 8) on each of the dates identified in Annexure A in circumstances where:

(a) there was a conflict between the interests of the relevant client and the interests of the representative and/or the First Defendant;

(b) the representative ought reasonably to have known of that conflict or those conflicts; and

(c) the representative failed to give priority to the interests of the relevant client when giving the advice.

Contravention of s 961L of the Corporations Act

4. During the period from 1 January 2017 to 1 April 2019 (the Relevant Period), the First Defendant contravened s 961L of the Corporations Act by failing to take reasonable steps to ensure that its representatives, referred to in orders 1 to 3 above, complied with ss 961B(1), 961G and 961J(1) of the Corporations Act in providing advice to Investor 1, Investor 2, Investor 3, Investor 4, Investor 5, Investor 6, Investor 7 or Investor 8 (as referred to in Annexure A) in each of the instances identified in Annexure A.

Contraventions of s 946A of the Corporations Act

5. The First Defendant contravened s 946A(1) of the Corporations Act in 595 instances by failing to provide a Statement of Advice in relation to the provision of personal advice to Investor 1, Investor 2, Investor 3, Investor 4, Investor 5, Investor 6, Investor 7 or Investor 8 (as referred to in Annexure A), each of whom was a retail client, in each of the instances identified in Annexure A as an instance that concerned that Investor.

Contraventions of s 1041H of the Corporations Act and s 12DA of the ASIC Act

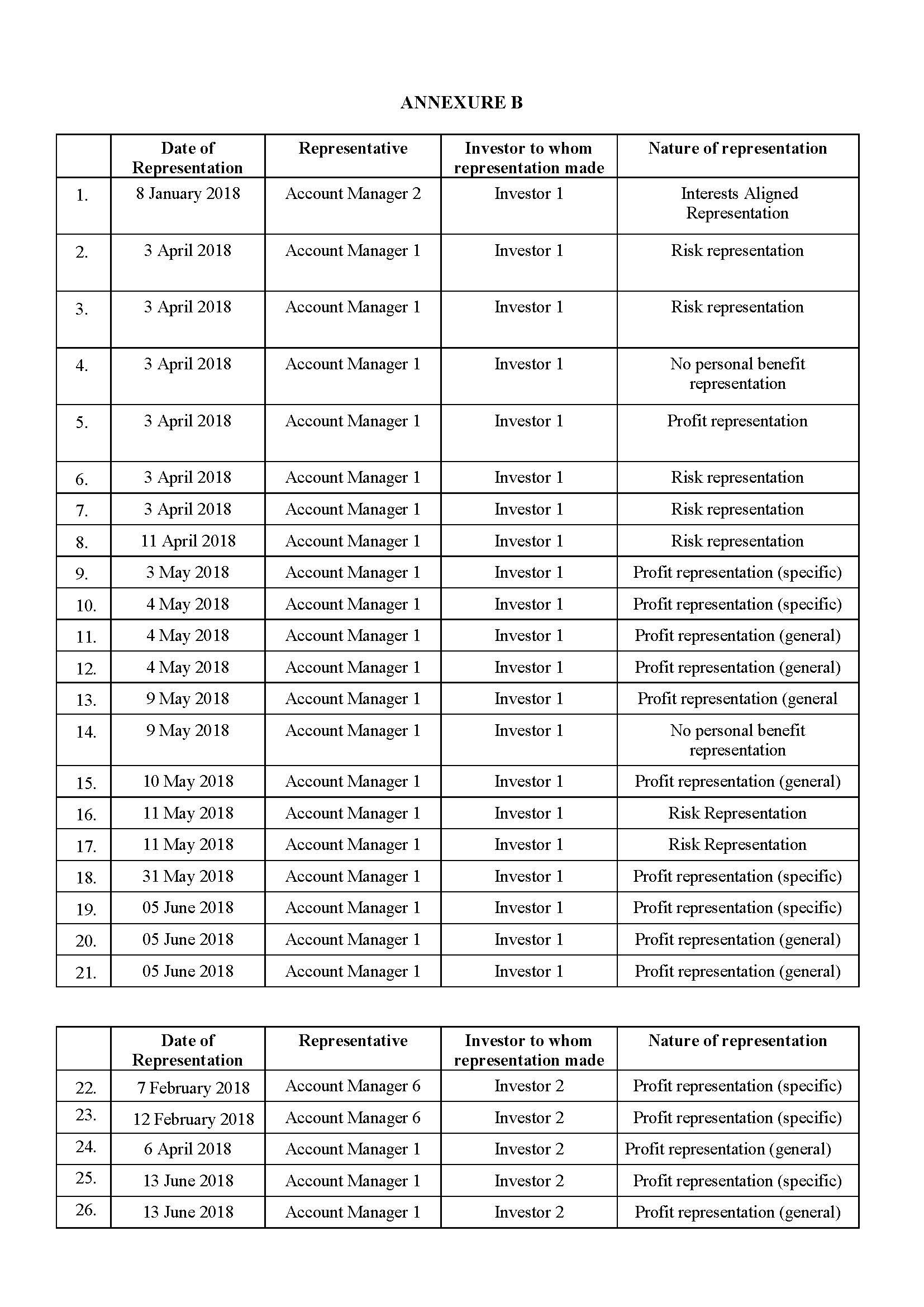

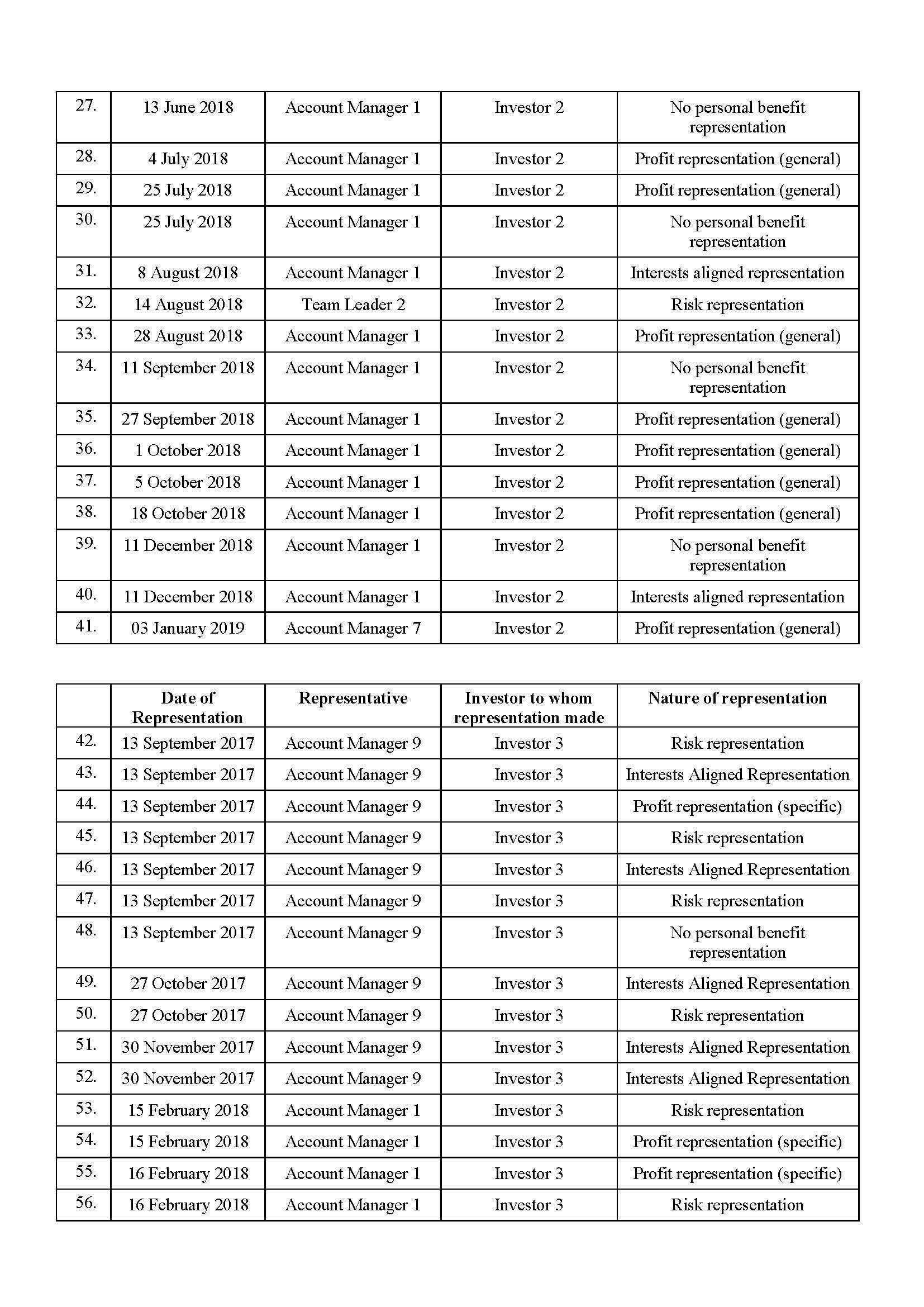

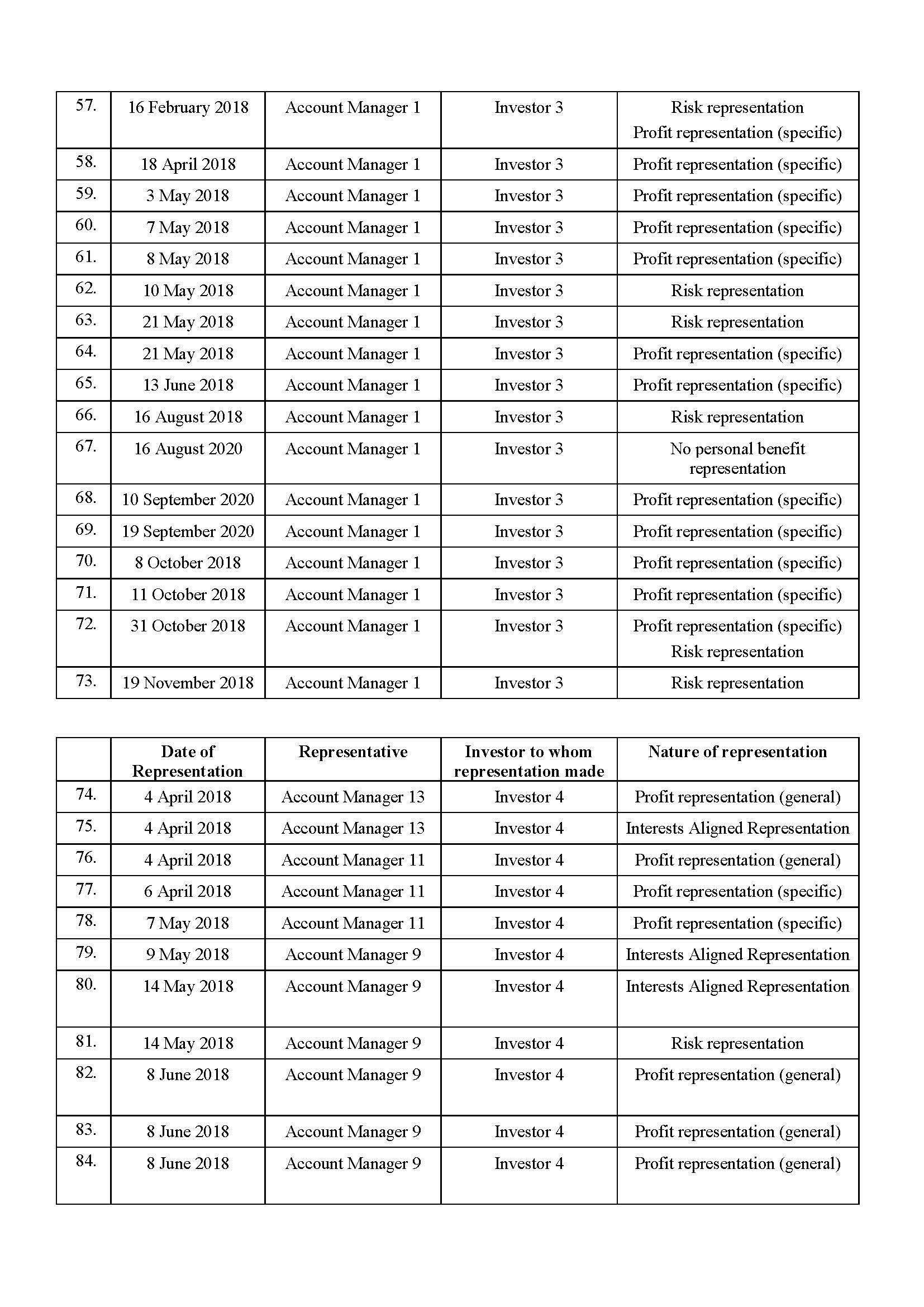

6. The First Defendant contravened s 1041H of the Corporations Act and s 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act) in 180 instances by making misleading or deceptive representations, or representations which are likely to mislead or deceive in relation to a financial service to a client (who is identified in Annexure B, relevantly to each contravention, as Investor 1, Investor 2, Investor 3, Investor 4, Investor 5, Investor 6, Investor 7 or Investor 8) in the instances identified in Annexure B to the effect that:

(a) the interests of the First Defendant or its Representatives were aligned with the interests of the client (Interests Aligned Representation);

(b) the Representative did not benefit from the deposit by the client of funds into the Investor’s trading account with the First Defendant (No Personal Benefit Representation);

(c) the risk of trading losses would be reduced if further funds were deposited in the client’s trading account with the First Defendant (Risk Representation);

(d) the client was likely to or might reasonably expect to generate profits by trading in margin foreign exchange instruments (Margin FX) and/or contracts for difference (CFDs) in the order of magnitude indicated by the Representative (Profit Representation (General)), and in some instances by reference to a particular trading position or strategies identified by the account manager (Profit Representation (Specific)); or

(e) it was in the best interests of the client to make a particular trade or to deposit additional funds (Implied Best Interests Representation),

and thereby, in trade or commerce, engaged in conduct, in relation to a financial service, that was misleading or deceptive or likely to mislead or deceive.

Contraventions of s 991A of the Corporations Act and s 12CB of the ASIC Act

7. During the Relevant Period, the First Defendant by providing financial product advice to, and dealing in financial products with each of Investor 1, Investor 2, Investor 3, Investor 4, Investor 5, Investor 6, Investor 7 or Investor 8, in circumstances where:

(a) each of the clients had no prior experience, or limited prior experience, in trading Margin FX and/or CFDs (together, the Products);

(b) it ought to have been reasonably apparent from the conversations between each of the clients and the First Defendant’s account managers that the client did not adequately understand the Products and the risks inherent in them, and was heavily reliant on the advice and recommendations of the account manager and therefore at a disadvantage in dealing with the First Defendant as the counterparty to each transaction in relation to the Products;

(c) the First Defendant’s representatives did not conduct a thorough assessment of the client’s objectives, financial situation and needs to determine whether the Products were appropriate for that person;

(d) each of the clients informed the First Defendant that they had limited financial resources;

(e) the First Defendant engaged in the contraventions in paragraph 6 above;

(f) the First Defendant employed unfair tactics by:

(i) providing advice to each client to place more trades or to place bigger trades, with the consequence of creating a “margin call” situation for the client that could then be used by the First Defendant to elicit a further deposit from the client to the client’s Forex CT trading account to avoid liquidation of the client’s account;

(ii) providing advice to each client to engage in trading strategies that exposed that client to a risk of loss that was materially greater than if the client had not adopted that strategy;

(iii) responding to requests by each client to withdraw funds from their Forex CT trading account in a way that was intended to delay or prevent the withdrawal;

(iv) using sales tactics such as offering incentives (credits and rebates) to encourage the client to transfer more money to their Forex CT trading account before a certain time, even after the client had told the account manager that they could not afford to invest more money, or were reluctant to do so;

(v) placing pressure on the client in lengthy and/or multiple telephone conversations to open additional CFD and/or Margin FX positions, or to deposit further funds to the client’s trading account;

(vi) receiving financial benefits when the client incurred financial losses on CFDs and/or Margin FX positions that the First Defendant had advised the client to open;

(vii) recommending strategies that were inappropriate to the client, such as placing more trades or trading with greater volume, leaving open trades that were in a loss, and using a credit card to fund further deposits to the client’s Forex CT trading account;

(viii) in respect of Investor 1, Investor 2, Investor 3 and Investor 6 only, advising those clients who had already incurred a loss to deposit further funds in the client’s trading account in order to be able to open further CFD and/or Margin FX positions and thereby recover some or all of the client’s losses;

(g) the First Defendant implemented an employee remuneration scheme that rewarded account managers according to, amongst other things, their clients’ net deposits, which created a conflict between the interests of the clients and the interests of account managers,

engaged in conduct in connection with the supply or possible supply of financial services that was in all of the circumstances unconscionable, in contravention of s 991A of the Corporations Act and s 12CB of the ASIC Act.

8. During the Relevant Period, the First Defendant engaged in an unconscionable system of conduct and/or pattern of behaviour in contravention of s 12CB of the ASIC Act by:

(a) engaging in, facilitating and/or encouraging the conduct referred to in paragraph 7

(b) facilitating trading in the Products:

(i) in circumstances where many of the clients of the First Defendant did not have a sufficient understanding of the nature of the Products and the risks inherent in them, and were reliant on the advice and recommendations of the account manager; and

(ii) without conducting a thorough assessment of the client’s objectives, financial situation and needs to determine whether the Products were appropriate for the client;

(c) providing inadequate or inappropriate training and guidance to account managers, including:

(i) training account managers to use the fact that a client was in a negative situation in relation to their trading of the Products (either in a “margin call” or liquidation) as an opportunity to persuade the client to deposit more funds into their trading account, without consideration of whether that was in the client’s best interests;

(ii) training account managers to follow scripts designed to persuade clients to cancel requests to withdraw funds from their trading account;

(d) implementing an employee remuneration scheme and key performance indicators that rewarded account managers according to, amongst other things, their clients’ net deposits and trading volume, which was likely to provide an incentive to account managers to encourage clients to deposit funds and to discourage them from withdrawing funds and to recommend trades or trading strategies that were not necessarily in the clients’ best interests;

(e) implementing and encouraging a trading floor culture that was directed towards maximising trading volume and client deposits rather than promoting a culture of compliance with applicable legal requirements; and

(f) failing to ensure compliance with financial services laws as identified in the statement of agreed facts.

Contravention of s 963F of the Corporations Act

9. During the Relevant Period, the First Defendant contravened s 963F of the Corporations Act by paying conflicted remuneration to account managers, comprising bonuses determined in accordance with the Retention Desk Bonus Structure (RD Bonus Structure) and Retention Desk Team Leader Bonus Structure (RD Team Leader Bonus Structure), being bonus payments calculated primarily by reference to the net deposits to the trading accounts of the account manager’s clients, thereby failing to take reasonable steps to ensure that representatives of the First Defendant did not accept conflicted remuneration.

Contravention of s 963J of the Corporations Act

10. The First Defendant contravened s 963J of the Corporations Act on 116 instances by giving: account managers conflicted remuneration for work carried out by the account manager as an employee of the First Defendant, being bonus payments calculated primarily by reference to the net deposits to the trading accounts of the account manager’s clients as provided by the RD Bonus Structure and RD Team Leader Bonus Structure.

Contraventions of s 912A of the Corporations Act

11. During the Relevant Period, the First Defendant, in the ways specified in these orders:

(a) failed to do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly in contravention of section 912A(1)(a) of the Corporations Act;

(b) failed to have in place adequate arrangements for the management of conflicts of interest that may arise wholly, or partially, in relation to activities undertaken by the First Defendant or its representatives in the provision of financial services as part of the financial services business of the First Defendant or its representatives in contravention of section 912A(1)(aa) of the Corporations Act;

(c) failed to comply with the financial services laws in contravention of section 912A(1)(c) of the Corporations Act;

(d) failed to take reasonable steps to ensure that its representatives complied with the financial services laws in contravention of section 912A(1)(ca) of the Corporations Act; and

(e) failed to ensure that its representatives were adequately trained and were competent to provide the financial services covered by the licence in contravention of section 912A(1)(f) of the Corporations Act.

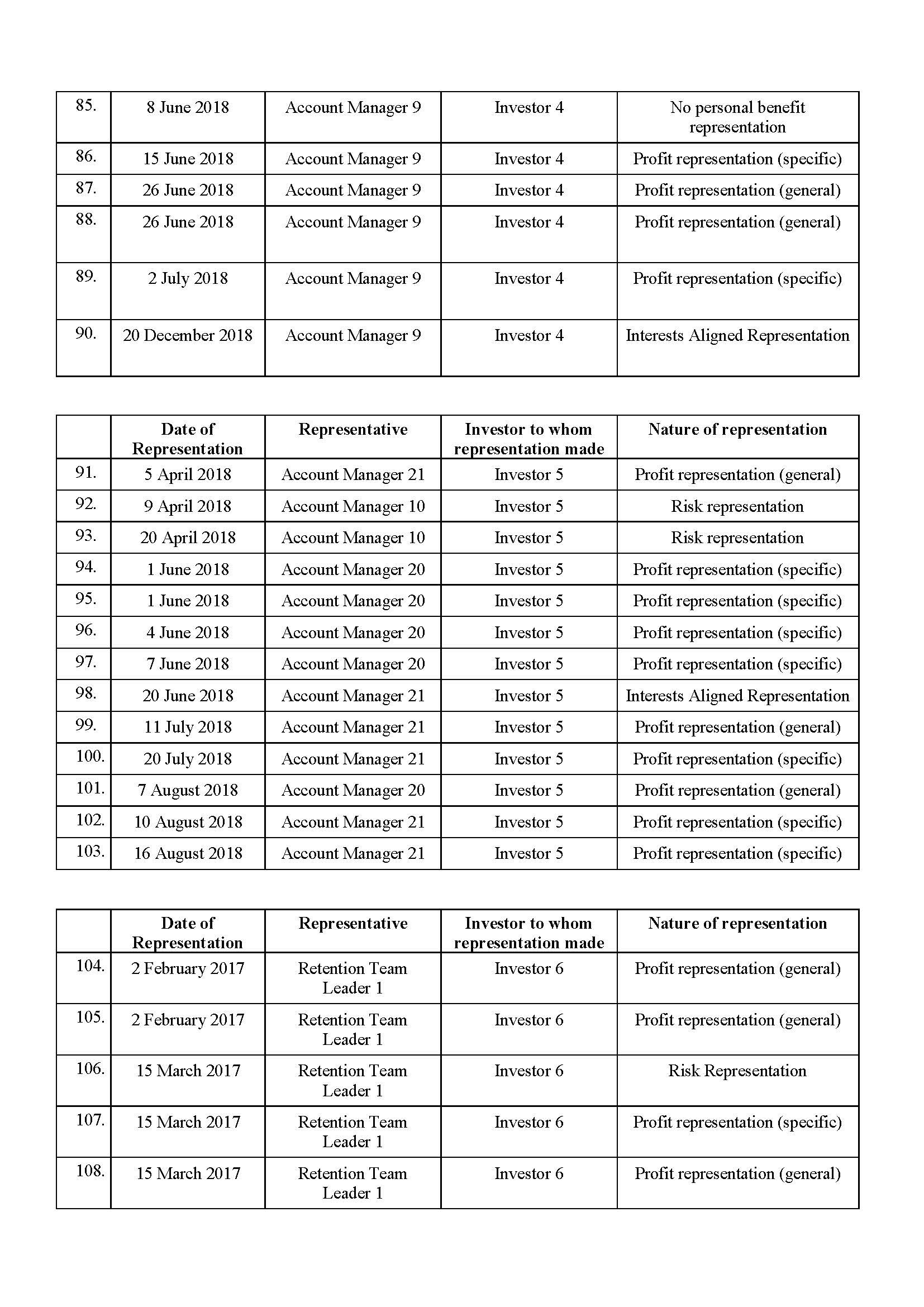

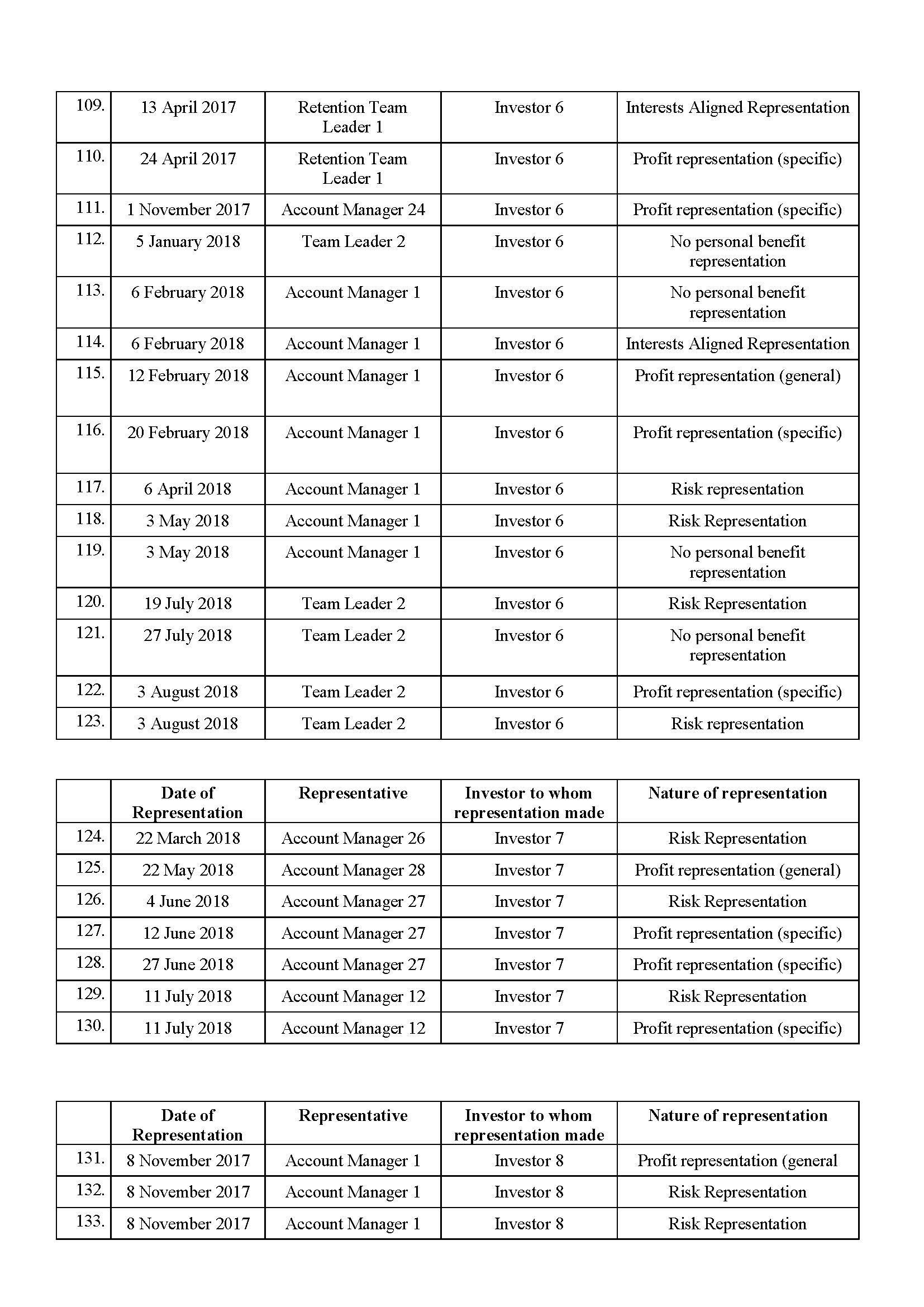

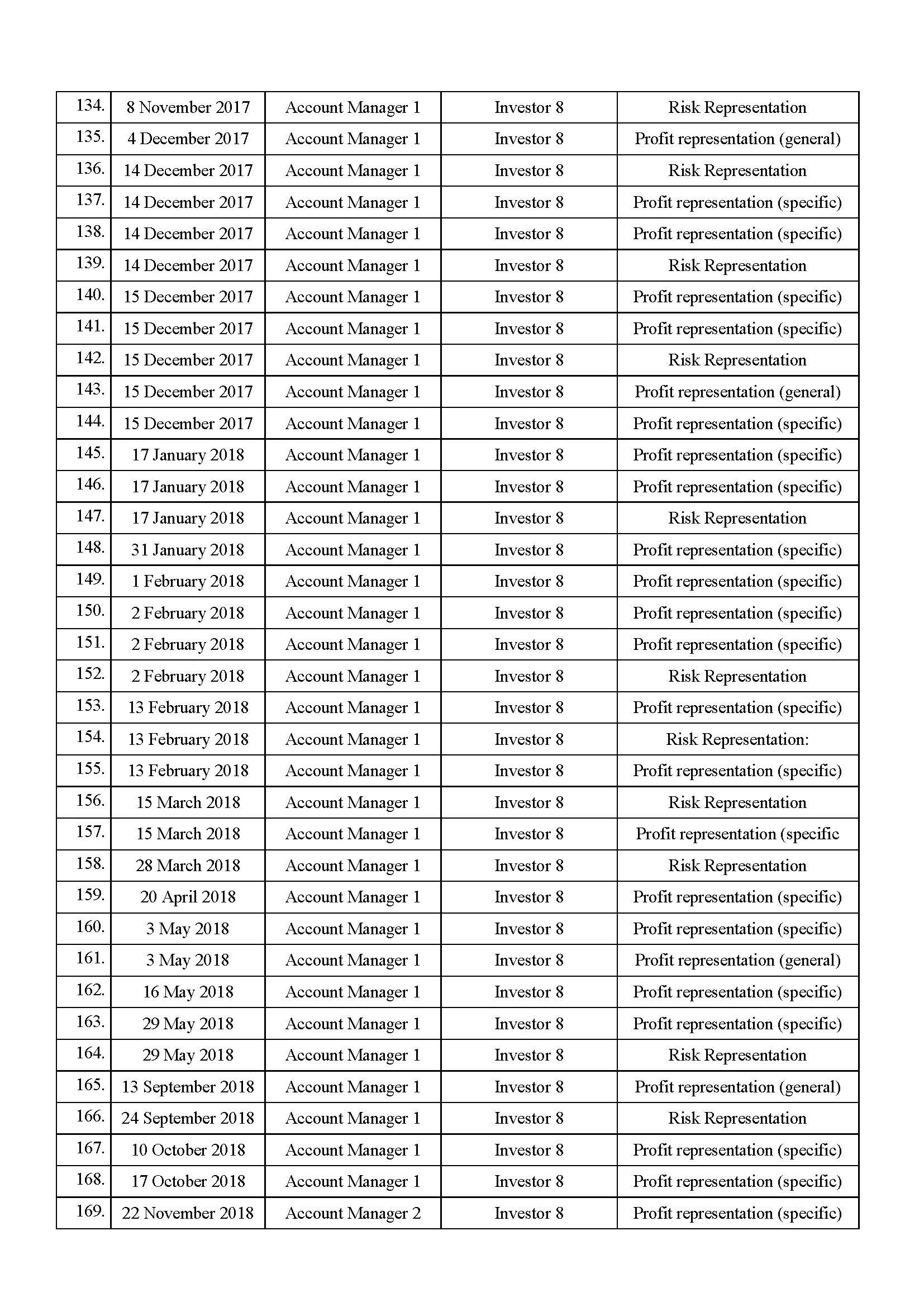

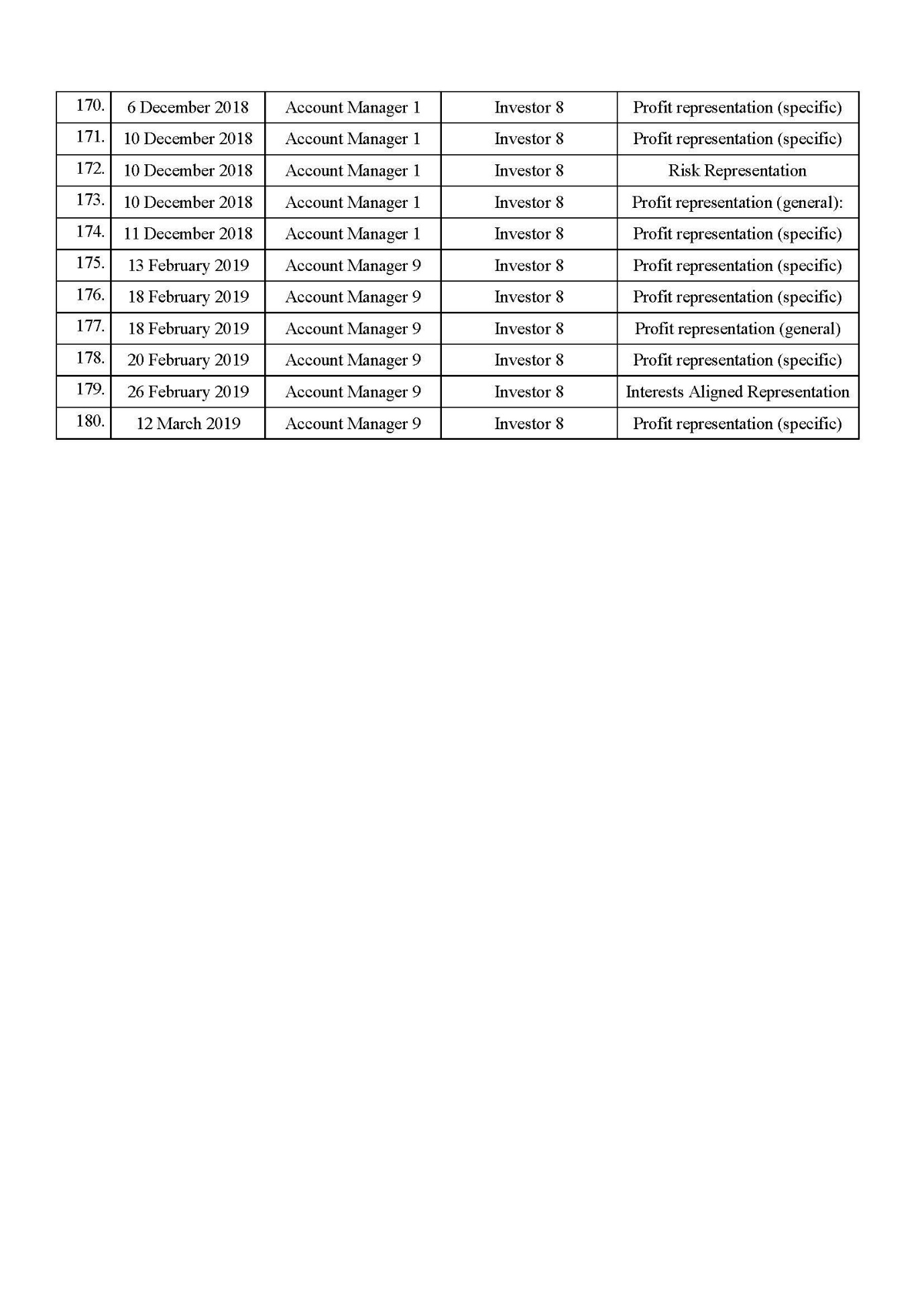

AGAINST THE SECOND DEFENDANT:

Contraventions of s 180 of the Corporations Act

12. During the Relevant Period, the Second Defendant contravened s 180(1) of the Corporations Act by failing to exercise a reasonable degree of care and diligence in the exercise of his powers and discharge of his duties as director and Chief Executive Officer of the First Defendant by authorising and applying remuneration structures (RD Bonus Structure and RD Team Leader Bonus Structure) and financial incentives for representatives of the First Defendant, which rewarded and encouraged the achievement of individual KPIs and targets in relation to account managers and Retention Desk Team Leaders primarily in relation to the quantum of net deposits by clients of the account manager to their trading account, and which created a significant risk of non-compliance by the First Defendant with its legal obligations (including those arising under Div 2 of Pt 7.7A of the Corporations Act and Div 2 of Pt 2 of the ASIC Act), and therefore jeopardised the First Defendant’s interests by exposing it to a risk of cancellation of its Australian Financial Services Licence (AFSL) and/or a civil penalty proceeding.

13. During the Relevant Period, the Second Defendant contravened s 180(1) of the Corporations Act by failing to exercise a reasonable degree of care and diligence in the exercise of his powers and discharge of his duties as director and Chief Executive Officer of the First Defendant by approving and/or authorising inadequate and inappropriate training materials for the First Defendant’s account managers and Team Leaders, which created a significant risk of non-compliance by the First Defendant with its legal obligations (including those arising under Div 2 of Pt 7.7A of the Corporations Act and Div 2 of Pt 2 of the ASIC Act), and therefore jeopardised the First Defendant’s interests by exposing it to a risk of cancellation of its AFSL and/or a civil penalty proceeding.

14. During the Relevant Period, the Second Defendant contravened s 180(1) of the Corporations Act by failing to exercise a reasonable degree of care and diligence in the exercise of his powers and discharge of his duties as director and Chief Executive Officer of the First Defendant by authorising a compliance monitoring program that was inadequate to ensure the First Defendant provided financial services in accordance with its legal obligations (including those arising under Div 2 of Pt 7.7A of the Corporations Act and Div 2 of Pt 2 of the ASIC Act), and therefore jeopardised the First Defendant’s interests by exposing it to a risk of cancellation of its AFSL and/or a civil penalty proceeding.

Aiding, abetting etc the First Defendant’s contravention of s 12CB of the ASIC Act

15. During the Relevant Period, the Second Defendant aided, abetted, counselled or procured the First Defendant to contravene s 12CB of the ASIC Act, as declared in paragraphs 8(b) to (f) above.

BY CONSENT, THE COURT ORDERS THAT:

16. The First Defendant pay, within 60 days of the date of this order, to the Commonwealth of Australia a pecuniary penalty of $20,000,000 in respect of the contraventions of ss 961K, 961L, 963F and 963J of the Corporations Act and s 12CB of the ASIC Act referred to in paragraphs 1 to 11 above.

17. The Second Defendant pay, within 60 days of the date of this order, to the Commonwealth of Australia a pecuniary penalty of $400,000 in respect of the contraventions of s 180(1) of the Corporations Act declared in paragraphs 12 to 14 above and the conduct in aiding, abetting, counselling and procuring the First Defendant to contravene s 12CB of the ASIC Act, as declared in paragraph 15 above.

18. The First Defendant and the Second Defendant pay, within 60 days of the date of this order, ASIC’s party/party costs of this proceeding fixed at $1,180,000.

THE COURT ORDERS THAT:

19. The Second Defendant be disqualified from managing corporations for a period of 8 years commencing 60 days from the date of this order.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MIDDLETON J:

INTRODUCTION

1 On 29 April 2021, I made orders in this proceeding. These are the reasons for those orders.

2 In the proceeding before me, the plaintiff, the Australian Securities and Investments Commission (‘ASIC’) claims that the first defendant, Forex Capital Trading Pty Limited (‘Forex CT’), contravened ss 912A(1), 946A, 961K(2), 961L, 963F, 963J, 991A and 1014H of the Corporations Act 2001 (Cth) (‘CA’), and ss 12CB and 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) (‘ASIC Act’).

3 ASIC also claims that the second defendant, Mr Shlomo Yoshai, who was the only Australian-based director and responsible manager, as well as the Chief Executive Officer (‘CEO’), of Forex CT throughout the Relevant Period, contravened s 180(1) of the CA and aided, abetted, counselled or procured Forex CT to contravene s 12CB of the ASIC Act.

4 The parties have now reached agreement as to the terms on which they seek to resolve this proceeding and, on 29 April 2021, jointly filed the following documents:

(1) a statement of agreed facts and admissions setting out the facts agreed between the parties and the admissions made by Forex CT and Mr Yoshai in respect of contraventions of the CA and the ASIC Act, a copy of which remains on the Court file for inspection by any person (subject to the observation in [6] hereof);

(2) an agreed minute of proposed declarations and orders setting out the relief (including as to penalty) which the parties submit is appropriate; and

(3) submissions jointly prepared by solicitors for the parties in support of the proposed declarations and orders.

5 For the purpose of this proceeding only, pursuant to s 191 of the Evidence Act 1995 (Cth) (‘Evidence Act’), Forex CT and Mr Yoshai have made the admissions set out in the statement of agreed facts. The statement of agreed facts is not signed by ASIC, Forex CT or Mr Yoshai, or their legal representatives, and so s 191(3)(a) of the Evidence Act — which provides that the benefits specified in s 191(2) will apply where the agreed facts are stated in an agreement in writing signed by the parties or their lawyers — is not engaged. However, the document was filed by consent and relied upon at the hearing in circumstances which likely engage s 191(3)(b) — which refers to facts being stated before the court with the agreement of all parties — and thereby attracts the operation of s 191(2) of the Evidence Act. I will proceed on the basis that, by operation of s 191(2), the parties are not required to prove the existence of any of the agreed facts.

6 As I have said, the statement of agreed facts is on the Court file. All of the schedules other than “Schedule Y” are available for inspection. “Schedule Y’ is a list of the names of Forex CT employees and the relevant pseudonyms used to refer to those employees in the statement of agreed facts, joint submissions and these reasons. On 29 April 2021, I made orders pursuant to s 37AF(1) of the Federal Court of Australia Act 1976 (Cth) to prohibit the publication or other disclosure of “Schedule Y”.

7 The parties’ joint submissions have informed the following reasons which explain why I was prepared to make declarations and orders for pecuniary penalties in the same form as that proposed by the parties.

8 The Court can receive and, if appropriate, accept joint submissions as to the quantum of penalty to be imposed in civil penalty proceedings: Commonwealth v Director, Fair Work Building Industry Inspectorate (2015) 258 CLR 482 (‘Commonwealth v DFWBII’) at [57]. However, it is ultimately a matter for the Court to determine whether the proposed pecuniary penalty is appropriate. While the Court’s role is not simply to “rubber stamp” a jointly proposed penalty (BlueScope Steel Limited v The Australian Worker’s Union [2019] FCA 182 at [3]), it is “highly desirable in practice” for the Court to accept the parties’ proposal, provided that the Court is persuaded as to the accuracy of the statement of agreed facts and that the proposed penalty is an appropriate remedy in the circumstances: Cth v FWBII at [58], noted in Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited (No 3) [2020] FCA 1421 at [78] (Allsop CJ); Australian Securities and Investments Commission v MLC Nominees Pty Ltd (11 September 2020) [2020] FCA 1306; 147 ACSR 266 at [114] (Yates J).

9 I consider that this principle is not confined to agreed submissions on pecuniary penalties but also applies to agreement on other forms of relief, including agreed positions on declarations.

10 There is one key issue where I disagree with the approach taken by the parties other than Mr Yoshai. It relates to the question of whether I am limited by the maximum penalty for a single contravention in determining the appropriate penalty for a contravention of s 12CB(1) of the ASIC Act in relation to a system of unconscionable conduct as pleaded. For the reasons I set out below, I consider that I am so limited, notwithstanding that the system of unconscionable conduct may have impacted thousands of Forex CT’s clients.

11 However, as I will explain, I have nonetheless arrived at the conclusion that the declarations and orders sought were appropriate to be made.

BACKGROUND TO THE ADMITTED CONTRAVENTIONS

12 The admitted contraventions occurred, for the most part, between 1 January 2017 to 1 April 2019 (‘Relevant Period’). There are a handful of contraventions that occurred outside of this period, the dates of which are set out in the statement of agreed facts and, where necessary, in the declarations and orders made.

13 Under its Australian Financial Services Licence (‘AFSL’), Forex CT was authorised to carry on a financial services business, including providing financial product advice in relation to derivative products and foreign exchange contracts (‘Margin FX’), dealing in those financial products, and making a market for those financial products to retail and wholesale clients. The AFSL permitted Forex CT to provide personal advice within the meaning of s 766B(3) of the CA. On 28 May 2020, ASIC cancelled Forex CT’s AFSL with effect from 31 July 2020.

14 Forex CT carried on a financial services business of providing advice to retail clients in relation to over-the-counter (‘OTC’) derivative products, including Margin FX and contracts-for-difference (‘CFDs’) (together, ‘Products’), which essentially allow a person to bet on whether the value of an underlying asset or instrument will increase or decrease over a defined period.

15 The high risk nature of OTC derivative products was recently outlined by Beach J in Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liquidation) (No 3) (2020) 275 FCR 57 (‘ASIC v AGM Markets (No 3)’) at [57]-[63], and Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liquidation) (No 4) [2020] FCA 1299 (‘ASIC v AGM Markets (No 4)’) at [13]-[29], wherein his Honour described OTC derivative products as “little more than gambling”: at [17].

16 In ASIC v AGM Markets (No 4), Beach J noted the following findings of ASIC in its Consultation Paper No 322, Product Intervention: OTC binary options and CFDs (August 2019) in relation to CFDs (at [20]):

(a) most retail clients who trade CFDs lose money;

(b) high leverage ratios carry inherent risk of significant losses, including losses which can exceed a retail client’s initial investment;

(c) fees and costs lack transparency, are magnified by leverage and can quickly and significantly deplete a retail client’s investment; and

(d) confusing and unclear pricing methodologies can lead to the sale to retail clients of CFDs that are misaligned with their needs, expectations and understanding.

17 Forex CT issued the Products by entering into a private contract with the retail client and, as issuer, was the counterparty to every transaction by which a client placed a trade or opened a position. Forex CT did not directly hedge trades placed by clients and so it benefited whenever a transaction was closed at a loss to the client and made a loss whenever a transaction was closed with a gain to the client. The Products were highly leveraged (up to 400:1 for certain Products) in that clients could open a position by depositing a relatively small percentage of the notional value of the underlying asset or instrument with their exposure to the fluctuations of the underlying asset or instrument being magnified.

18 The agreed facts disclose that Forex CT’s clients were unsophisticated retail investors with inadequate or incomplete understanding of the operation of the Products. The clients had no experience, or limited experience, of trading in the Products and were therefore reliant on the advice of Forex CT representatives.

19 Over the course of the Relevant Period, Forex CT employed 209 representatives in its call centre to provide financial services to clients, being:

(a) acquisition agents, or “sales”, whose role was to sell financial services to new clients;

(b) account managers, or “retention”, whose role was to engage with existing clients and drive trading activity and deposits; and

(c) retention team leaders, who had responsibility for the day-to-day operations of account managers,

(together, ‘representatives’).

20 Acquisition agents were required to take certain steps to register a potential client who was required to provide information as to their employment status and annual income, and if the person did not meet Forex CT’s minimum qualification requirements, was allowed three attempts to complete a quiz (‘qualification quiz’), with a further pathway for reassessment.

21 After registration, the client was provided with a trading account and assigned an account manager who thereafter became the client’s primary point of contact with Forex CT. Account managers communicated with clients over telephone or an online chat system, and were trained to call new clients every day during the first week after opening an account, tapering off to at least weekly calls from the fifth week onwards.

22 Through its employee remuneration scheme and use of key performance indicators, Forex CT rewarded its employees for, among other things, the size of clients’ net deposits and trading volume. There were different arrangements for different types of employees but, generally speaking, the scheme provided an incentive to representatives to encourage clients to deposit funds and to recommend trades or trading strategies that were not necessarily in the client’s best interests. I will outline the remuneration and reward scheme in more detail below.

23 The trading floor culture at Forex CT was also directed towards maximising client deposits and trading volume: for instance, a bell or gong was rung when clients deposited funds of certain amounts into their trading accounts, and account managers could participate in incentive games such as ‘wheel of fortune’ roulette tables and dice games to win cash if certain client deposit targets were met.

24 Broadly, Forex CT purported to provide financial services pursuant to a general advice model (rather than a personal advice model), and therefore did not provide any training to its representatives in relation to the obligations in Div 2 of Pt 7.7A of the CA which apply in relation to the provision of personal advice to retail clients: see s 961(1) of the CA.

25 It is agreed that, over the course of the Relevant Period:

(a) between 1203 and 4046 clients per month traded with Forex CT;

(b) Forex CT’s clients experienced total realised net losses of $77,619,916 which translated to a corresponding net gain to Forex CT; and

(c) after operating expenses, including tax and costs arising from the risk mitigation agreement (a matter to which I will return to below), Forex CT’s profit was $461,564.

ADMITTED CONTRAVENTIONS

26 Forex CT and Mr Yoshai have made the following admissions.

Contravention of s 961K(2) of the CA by Forex CT

27 Section 961K(2) of the CA provides:

A financial services licensee contravenes this section if:

(a) a representative, other than an authorised representative, of the licensee contravenes section 961B, 961G, 961H or 961J; and

(b) the licensee is the, or a, responsible licensee in relation to that contravention.

Note: this subsection is a civil penalty provision (see section 1317E).

28 Forex CT was a financial services licensee for the purpose of Pt 7.7A of the CA until 31 July 2020. As I indicated at [12] above, there were a handful of later contraventions, some of which occurred after this date, but I do not consider this materially affects the question for my determination, nor was it raised by any of the parties at the hearing.

29 The representatives were representatives of Forex CT for the purposes of s 961K(2)(a), and Forex CT was to be treated as a responsible licensee in relation to each of the representatives for the purpose of s 961K(2)(b).

30 Forex CT has admitted contravening ss 961B, 961G and 961J of the CA through its representatives, and thereby contravening s 961K(2) of the CA, in relation to eight identified clients. These provisions are in Div 2 of Pt 7.7A of the CA, which applies in relation to the provision of personal advice to retail clients: see s 961(1) of the CA.

The advice was personal advice

31 Personal advice is defined in s 766B(3) of the CA as:

financial product advice that is given or directed to a person (including by electronic means) in circumstances where…the provider of the advice has considered one or more of the person’s objectives, financial situations and needs…or…a reasonable person might expect the provider to have considered one or more of those matters.

32 Financial product advice is defined in s 766B(1) of the CA as:

a recommendation or a statement of opinion, or a report of either of those things, that:

(a) is intended to influence a person or persons in making a decision in relation to a particular financial product or class of financial products; or

(b) could reasonably be regarded as being intended to have such an influence.

33 The authorities have accepted that the expressions “recommendation” and “statement of opinion” in s 766B(1) of the CA are to be given a broad interpretation: Australian Securities and Investments Commission v Park Trent Properties Group Pty Ltd (No 3) [2015] NSWSC 1527 (‘ASIC v Park Trent Properties’) at [366] (Sackville AJA); Australian Securities and Investments Commission v Westpac Securities Administration Ltd (2019) 272 FCR 170 (‘ASIC v Westpac FCAFC’) at [16] (Allsop CJ), [217] (Jagot J); ASIC v AGM Markets (No 3) at [161] (Beach J). In particular, it is established that “a person may provide information or present material in a way that implicitly makes a recommendation or states an opinion in relation to a financial product”: ASIC v Park Trent Properties at [366] (Sackville AJA). See also ASIC v Westpac FCAFC at [18], [67] (Allsop CJ), [217] (Jagot J), [335] (O’Bryan J); Australian Securities and Investments Commission v Oxford Investments (Tasmania) Pty Ltd (2008) 169 FCR 522 at [17], [23] (Heerey J).

34 In respect of the definition of personal advice in s 766B(3) of the CA, in Westpac Securities Administration Ltd v Australian Securities and Investments Commission [2021] HCA 3; 95 ALJR 149 (‘Westpac v ASIC HCA’), the majority (Kiefel CJ, Bell, Gageler and Keane JJ) clarified that:

[15] In the context of the consumer protection provisions of Ch 7 of the Act, “considered” in s 766B(3) should be understood as meaning “took account of”…

[…]

[17] There is no basis in the text of s 766B(3), or the context in which it appears, to read the word “considered” as importing a requirement of an active and comprehensive process of evaluation. Such a gloss upon “considered” would impermissibly narrow the scope of a provision intended to protect consumers while at the same time adding a layer of uncertainty to its operation.

(Footnotes omitted.)

35 With regard to the phrase “one or more of the person’s objectives, financial situation and needs”, the majority went on to say (at [20]):

The primary judge and the Full Court rightly held that s 766B(3)(b) contemplates consideration of at least one aspect of the client’s objectives, financial situation or needs. The ordinary and natural meaning of the terms of s 766B(3) is readily applicable to a situation in which the issue for decision by the client is focused upon one aspect of his or her financial affairs. The scope of advice reasonably germane to the resolution of that issue may be expected by both adviser and client to encompass only so much of the client’s objectives, financial situation or needs as is relevant to its satisfactory resolution.

36 In Westpac v ASIC HCA, the High Court upheld the conclusion that an implied recommendation in relation to the rollover of superannuation funds that was given in the course of personal phone calls made to members with whom it had a pre-existing relationship constituted personal advice within the meaning of s 766B of the CA. This conclusion was reached notwithstanding that the phone calls had commenced with a disclaimer, that the advice was offered “free of charge”, and that the advisers did not have a complete knowledge of the member’s financial situation: see [7]-[10] (Kiefel CJ, Bell, Gageler and Keane JJ), [78]-[80] (Gordon J). The members were asked about their personal objectives, in circumstances in which it was reasonable to expect that the adviser might have taken account of those objectives in providing the advice: [11]-[13] (Kiefel CJ, Bell, Gageler and Keane JJ), [76]-[77] (Gordon J). The fact that the objectives and the advice were “generally applicable to all or most persons” did not prevent the advice from being regarded as personal advice (at [11] (Kiefel CJ, Bell, Gageler and Keane JJ)), and Gordon J noted that “where a provider of advice urges the recipient to follow a particular course of action, there is greater likelihood that a reasonable person might expect the adviser to have considered the recipient’s personal circumstances”: at [81].

37 I am satisfied that Forex CT was providing financial product advice to the eight identified clients in circumstances that satisfy the definition of personal advice in s 766B(3) of the CA. The Forex CT representatives sought information from clients regarding their objectives, financial position or needs, and had access to information about the client’s trading accounts which was expressly or implicitly apparent to the client. The advice was provided to clients by representatives in the context of an ongoing relationship, usually involving numerous one-on-one telephone calls with the same account manager. It was also explained to clients that the function of the account manager was to support or guide the client in his or her trading. A reasonable person would have expected the representative to have considered the client’s personal circumstances.

Contravention of s 961B(1) of the CA

38 Section 961B of the CA (the ‘best interests obligation’) relevantly provides:

(1) The provider must act in the best interests of the client in relation to the advice.

(2) The provider satisfies the duty in subsection (1), if the provider proves that the provider has done each of the following:

(a) identified the objectives, financial situation and needs of the client that were disclosed to the provider by the client through instructions;

(b) identified:

(i) the subject matter of the advice that has been sought by the client (whether explicitly or implicitly); and

(ii) the objectives, financial situation and needs of the client that would reasonably be considered as relevant to advice sought on that subject matter (the client’s relevant circumstances);

(c) where it was reasonably apparent that information relating to the client’s relevant circumstances was incomplete or inaccurate, made reasonable inquiries to obtain complete and accurate information;

(d) assessed whether the provider has the expertise required to provide the client advice on the subject matter sought and, if not, declined to provide the advice;

(e) if, in considering the subject matter of the advice sought, it would be reasonable to consider recommending a financial product:

(i) conducted a reasonable investigation into the financial products that might achieve those of the objectives and meet those of the needs of the client that would reasonably be considered as relevant to advice on that subject matter; and

(ii) assessed the information gathered in the investigation;

(f) based all judgements in advising the client on the client’s relevant circumstances;

(g) taken any other step that, at the time the advice is provided, would reasonably be regarded as being in the best interests of the client, given the client’s relevant circumstances.

(Note omitted.)

39 The best interests obligation under s 961B(1) of the CA was explained by Allsop CJ in ASIC v Westpac FCAFC in the following terms (at [151]):

…[t]he obligation of a financial advisor to act in the best interests of a client draws on the concepts of fiduciary loyalty commonly resting on persons in such a position: Daly v Sydney Stock Exchange Ltd (1986) 160 CLR 371 at 377 and 385. The circumstances that will lead to a conclusion that a provider of personal advice did not act in the best interests of his or her client may be drawn in part from the list of factors in s 961B(2), but the source of equitable faithfulness of the duty in s 961B(1) should also be recognised in the content of the phrase and the possible circumstances of its contravention.

40 Section 961C prescribes where a matter will be reasonably apparent for the purposes of s 961B(2)(c):

Something is reasonably apparent if it would be apparent to a person with a reasonable level of expertise in the subject matter of the advice that has been sought by the client, were that person exercising care and objectively assessing the information given to the provider by the client.

41 Section 961D in turn prescribes what would be a reasonable investigation for the purposes of s 961B(2)(e)(i):

(1) A reasonable investigation into the financial products that might achieve those of the objectives and meet those of the needs of the client that would reasonably be considered relevant to advice on the subject matter sought by the client does not require an investigation into every financial product available.

(2) However, if the client requests the provider to consider a specified financial product, a reasonable investigation into the financial products that might achieve those of the objectives and meet those of the needs of the client that would reasonably be considered relevant to advice on the subject matter sought by the client includes an investigation into that financial product.

42 Section 961E also prescribes what would reasonably be regarded as in the best interests of the client for the purpose of s 961B(2)(g):

It would reasonably be regarded as in the best interests of the client to take a step, if a person with a reasonable level of expertise in the subject matter of the advice that has been sought by the client, exercising care and objectively assessing the client’s relevant circumstances, would regard it as in the best interests of the client, given the client’s relevant circumstances, to take that step.

43 Forex CT admits that its representatives contravened s 961B of the CA on 595 instances when giving personal advice to the eight identified retail clients. In each of these instances, a representative failed to:

(a) identify and examine the client’s current financial situation, including income, savings, assets and debts;

(b) identify and understand the client’s objective and needs;

(c) ascertain the type of financial products that the client was interested in and that were appropriate for the client;

(d) inform the client whether the advice was based on incomplete information regarding the client’s financial situation, objectives or needs;

(e) educate the client about the financial products;

(f) advise the client that CFDs and Margin FX were leveraged and highly risky products; or

(g) provide a statement of advice at the time, or shortly after providing the advice (a matter to which I will return to below).

Contravention of s 961G of the CA

44 Section 961G of the CA (the ‘appropriate advice obligation’) relatedly provides:

The provider must only provide the advice to the client if it would be reasonable to conclude that the advice is appropriate to the client, had the provider satisfied the duty under section 961B to act in the best interests of the client.

Note: A responsible licensee or an authorised representative may contravene a civil penalty provision if a provider fails to comply with this section (see sections 961K and 961Q). The provider may be subject to a banning order (see section 920A).

45 Each of the instances of personal advice referred to at [43] above were recommendations for the client to do one or more of the following: deposit more funds into the client’s trading account, open a particular trade, adopt a particular trading strategy, increase volume of trades or leave a losing trade open.

46 Forex CT admits that these recommendations were made in circumstances where it was not reasonable to conclude that the advice was appropriate to the client had the duty under s 961B(1) of the CA been satisfied because, having regard to the nature of Margin FX and CFDs as high risk leveraged products, the recommendation would expose the clients to a higher risk of loss. Forex CT thereby admits that its representatives contravened s 961G of the CA on 595 instances when giving personal advice to the eight identified retail clients.

Contravention of s 961J(1) of the CA

47 Section 961J(1) of the CA (the ‘conflicts obligation’) provides:

If the provider knows, or reasonably ought to know, that there is a conflict between the interests of the client and the interests of:

(a) the provider; or

(b) an associate of the provider; or

(c) a financial services licensee of whom the provider is a representative; or

(d) an associate of a financial services licensee of whom the provider is a representative; or

(e) an authorised representative who has authorised the provider, under subsection 916B(3), to provide a specified financial service or financial services on behalf of a financial services licensee; or

(f) an associate of an authorised representative who has authorised the provider, under subsection 916B(3), to provide a specified financial service or financial services on behalf of a financial services licensee;

the provider must give priority to the client’s interests when giving the advice.

Note: A responsible licensee or an authorised representative may contravene a civil penalty provision if a provider fails to comply with this section (see sections 961K and 961Q). The provider may be subject to a banning order (see section 920A).

48 Within the instances of personal advice that contravened ss 961B and 961G of the CA, Forex CT also admit that there were 556 instances where an account manager gave personal advice which failed to give priority to the client’s interests in circumstances where the account manager ought reasonably to have known that there was a conflict between the interests of the relevant client and the interests of the account manager or Forex CT.

49 The conflict between the interests of the client and those of the account manager arises principally because of Forex CT’s remuneration and bonus arrangements, which I have referred to at [22] above. It was Forex CT’s policy to pay bonuses to account managers calculated by reference to:

(a) the amount of net deposits in the account manager’s ‘trading book’;

(b) the number of individual clients who have placed at least one trade per business day; and

(c) from 1 December 2017, the number of unique clients with a deposit amount greater than $1,000 at the end of the month.

50 This bonus structure meant that it was in the financial interests of account managers that clients in their ‘trading book’ maximised the amount of money deposited into their Forex CT trading account each month, minimised the amount of money withdrawn from the account, placed at least one trade per business day each month and deposited at least $1,000 into their Forex CT trading account each month.

51 Forex CT, as the counterparty to each trade, had an interest in the client accepting a recommendation to open a trade as it would receive a pecuniary benefit in the event that the trade closed with a negative outcome for the client. On the other hand, the client had an interest in receiving advice that was in their best interests, appropriate to them, and not affected by any incentive for the account manager to earn bonuses or interest on the part of Forex CT as the counterparty to the trades the subject of the advice.

52 Forex CT admits that its representatives contravened s 961J(1) of the CA on 556 instances when giving personal advice to the eight identified retail clients and failing to give priority to the interests of the client.

Contravention of s 961L of the CA by Forex CT

53 Section 961L of the CA provides:

A financial services licensee must take reasonable steps to ensure that representatives of the licensee comply with sections 961B, 961G, 961H and 961J.

Note: This section is a civil penalty provision (see section 1317E).

54 In Australian Securities and Investments Commission v AMP Financial Planning Pty Ltd (No 2) [2020] FCA 69; 377 ALR 55 (‘ASIC v AMP’), Lee J made the following observations about the construction of s 961L:

[105] First, the word “ensure” is forward-looking. It is directed to the taking of steps to achieve compliance with certain statutory norms (including the relevant best interest obligations) before any particular instance of non-compliance as arisen…

[106] Secondly, the text of s 961L makes it focus on the conduct of the licensee, not the representative, and whether the licensee has taken “reasonable steps”... Critically there is nothing in the text of s 961L that makes a contravention of the relevant best interests obligations a pre-requisite to a contravention of s 961L.

[107] Thirdly, the relevant best interests obligations to which s 961L refers fall under separate subdivision headings and each prescribe distinct statutory norms of conduct for the providers of financial advice, broadly summarised as: (a) acting in the best interests of the client (s 961B); (b) providing advice only where it is appropriate to the client (s 961G); (c) warning clients that advice is based on incomplete or inaccurate information (s 961H, not being an issue in this case); and (d) giving priority to the client’s interests when giving the advice (s 961J). Although the obligations relate to one another and breach of one may, depending upon the circumstances, amount to a breach of another, their particular content and focus differs.

55 It is agreed that Forex CT:

(a) purported to provide financial services pursuant to a general advice model (as I have already stated at [24] above), and therefore did not provide any training in relation to obligations under Div 2 of Pt 7.7A of the CA including how a representative was to discharge those obligations in the context of the financial services model deployed by Forex CT and in relation to the management of conflicts of interest;

(b) implemented remuneration arrangements and adopted key performance indicators that incentivised representatives to provide certain advice without ensuring that representatives were complying with ss 961B, 961G and 961J of the CA in providing that advice; and

(c) implemented a compliance framework that was inadequate to ensure that representatives complied with their obligations under Div 2 of Pt 7.7A of the CA.

56 Forex CT admits that it failed to take reasonable steps to ensure compliance by its representatives with ss 961B, 961G and 961J of the CA and thereby contravened s 961L of the CA.

Contravention of s 946A of the CA by Forex CT

57 Section 946A of the CA relevantly provides:

(1) The providing entity must give the client a Statement of Advice in accordance with this Subdivision and Subdivision D.

(2) The Statement of Advice may be:

(a) the means by which the advice is provided; or

(b) a separate record of the advice.

58 The main requirements for a “Statement of Advice” are set out in s 947B of the CA and include “a statement setting out the advice” and “information about the basis on which the advice is or was given”: see, eg, s 947B(2)(a), (c).

59 Forex CT admits that it failed to provide a Statement of Advice as required by s 946A(1) of the CA in each of the 595 instances that an account manager gave personal advice during the Relevant Period.

Contravention of s 1041H of the CA and s 12DA of the ASIC Act by Forex CT

60 Section 1041H(1) of the CA provides:

A person must not, in this jurisdiction, engage in conduct, in relation to a financial product or a financial service, that is misleading or deceptive or is likely to mislead or deceive.

(Notes omitted.)

61 Section 12DA(1) of the ASIC Act provides:

A person must not, in trade or commerce, engage in conduct in relation to financial services that is misleading or deceptive or is likely to mislead or deceive.

62 The statements made by Forex CT representatives to clients in relation to the Products were made “in relation to a financial product or a financial service” for the purpose of s 1041H(1) of the CA, and “in relation to financial services” for the purpose of s 12DA(1) of the ASIC Act.

63 Whether conduct is misleading or deceptive or likely to mislead or deceive is an objective question which is to be answered in the context of all the evidence and the surrounding circumstances. Relevant circumstances include “the nature of the parties, the character of the transaction contemplated, and the contents of [relevant documents]”: see Butcher v Lachlan Elder Realty Pty Ltd (2004) 218 CLR 592 at [40] (Gleeson CJ, Hayne and Heydon JJ).

64 Where a representation is made with respect to any future matter, one circumstance in which it will be misleading is if the person making the statement does not have reasonable grounds for making the representation: s 769C(1) of the CA, s 12BB(1) of the ASIC Act. A future matter means anything that is to occur in the future, a prediction or projection. Whether or not there were reasonable grounds is a question of facts, judged at the time the representations were made: Sykes v Reserve Bank of Australia (1998) 88 FCR 511 at 513 (Heerey J, Sundberg J agreeing). The person making the representation must have facts sufficient to induce in the mind of a reasonable person a basis for making the representation. Whether or not the identified facts amount to reasonable grounds is a question to be answered objectively, not by reference to the maker’s subjective state of mind: Australian Competition and Consumer Commission v Jones (No 5) [2011] FCA 49 at [32] (Logan J).

65 On 180 occasions, Forex CT representatives made false or misleading statements and representations to the effect that:

(a) the interests of Forex CT or its representatives were aligned with the interests of the client (‘Interests Aligned Representation’);

(b) the representative did not benefit from the deposit by the client of funds into the client’s trading account with Forex CT (‘No Personal Benefit Representation’);

(c) the risk of trading losses would be reduced if further funds were deposited in the client’s trading account with Forex CT (‘Risk Representation’);

(d) the client was likely to or might reasonably expect to generate profits by trading in Margin FX or CFDs in the order of magnitude indicated by the Representative (‘Profit Representation (General)’) and in some instances by reference to a particular trading position or strategies identified by the Representative (‘Profit Representation (Specific)’); or

(e) it was in the best interests of the client to make a particular trade or to deposit additional funds (‘Best Interests Representation’).

(a) Interests Aligned Representation: on 13 September 2017, Account Manager 9 said the following to Investor 3:

… So, you need to understand, obviously, when you’re doing well, all right, … we’re doing well. So, obviously, when you’re making money, the company makes money as well, all right, … and if you’re doing bad, obviously, we do bad too. So, you know, we don’t ever want to see our clients in the – obviously, in the negative, and it’s just – it’s – it’s …it’s real, real bad, mate.’

(b) No Personal Benefit Representation: on 3 April 2018, Account Manager 1 said the following to Investor 1:

…What you profit or what you deposit in your account has nothing to do with me. I get nothing from that. Not a single dollar, single cent. … Now, like I said to you before, we deposit money in your account, it goes to your own account, you can take it out whenever you like. Now, I don’t benefit nothing from that. All I'm saying to you is, be safer, give yourself a better opportunity, put on better, as in like bigger, bigger or better size positions and sit on a higher equity. Right? And you will see for yourself how much of a change it will do. From now or next week or the next two weeks …’

(c) Risk Representation: on 4 June 2018, Account Manager 27 had the following exchange with Investor 7:

[INVESTOR 7]: Yeah. Well, with, um, if you think I deposit, even in my account like if I was to deposit a grand and then you put in a grand, wouldn’t that get me over?

[ACCOUNT MANAGER 27]: Um, it would, it would definitely help, it would definitely help. But if you wanted to be on the safer side, um, you’d probably want to chuck in at five.

…

[ACCOUNT MANAGER 27]: Yeah, so, your, your margin percentage is under 1 per cent, um - - -

[INVESTOR 7]: Yep.

[ACCOUNT MANAGER 27]: So, yeah, I’d definitely look at increasing that, um, just even by a little bit, is going to help.

[INVESTOR 7]: Okay.

(d) Profit Representation (Specific): on 15 March 2017, Retention Team Leader 1 had the following conversation with Investor 6:

[RETENTION TEAM LEADER 1]: … Just 200 more and that’s only if you put the 10 in. Put 10 in and I’ll give you four and then no more than 300. So 200 more. But still, think of it this way right, so if it went down to even 1,150 right - - -

[INVESTOR 6]: Yep.

[RETENTION TEAM LEADER 1]: - - - and we had the 300. Just that is about 19 grand. It’s more than double your account in profit, that’s a very good trade…

(e) Profit Representation (General): on 26 June 2018, Account Manager 9 said the following to Investor 4:

I’m very, I’m very, very, very confident that you’re going to be able to, I’m very confident, I have no doubt, I believe that you’re going to hit quarter of a million dollars, all right. And I’m not, [Investor 4] …

(f) Best Interests Representation: on 7 February 2018, Account Manager 6 said the following to Investor 2:

What I'm saying is now you're at a level of over a 50K account. I mean, you – you're more than – it's better to – to look at trying to satisfy your volume requirement for your credit, make that withdrawable, and in combination with that, build your account up to a certain level and make a substantial withdrawal at that stage, as well. Do you know what I mean?

67 Further, on each instance that the representative gave personal advice to the clients, the representative made an implied representation to that client that it was in the best interests of the client to follow that advice (for example, by making a particular trade or by depositing funds): see ASIC v AGM Markets (No 3) at [318] (Beach J).

68 Forex CT admits that its representatives engaged in conduct in relation to financial services that was misleading or deceptive or was likely to mislead or deceive, and thereby breached s 1041H of the CA and s 12DA of the ASIC Act in 180 instances.

Contravention of s 991A of the CA and s 12CB(1) of the ASIC Act by Forex CT

69 Section 991A(1) of the CA provides:

A financial services licensee must not, in or in relation to the provision of a financial service, engage in conduct that is, in all the circumstances, unconscionable.

70 Section 12CB of the ASIC Act relevantly provides:

(1) A person must not, in trade or commerce, in connection with:

(a) the supply or possible supply of financial services to a person; or

(b) the acquisition or possible acquisition of financial services from a person; engage in conduct that is, in all the circumstances, unconscionable.

[…]

(4) It is the intention of the Parliament that:

(a) this section is not limited by the unwritten law of the States and Territories relating to unconscionable conduct; and

(b) this section is capable of applying to a system of conduct or pattern of behaviour, whether or not a particular individual is identified as having been disadvantaged by the conduct or behaviour…

71 Section 12CC(1) of the ASIC Act contains a non-exhaustive statement of matters to which the Court may have regard to for the purpose of determining whether a person has contravened s 12CB(1) of the ASIC Act. It provides:

(1) Without limiting the matters to which the court may have regard for the purpose of determining whether a person (the supplier) has contravened section 12CB in connection with the supply or possible supply of financial services to a person (the service recipient), the court may have regard to:

(a) the relative strengths of the bargaining positions of the supplier and the service recipient; and

(b) whether, as a result of conduct engaged in by the supplier, the service recipient was required to comply with conditions that were not reasonably necessary for the protection of the legitimate interests of the supplier; and

(c) whether the service recipient was able to understand any documents relating to the supply or possible supply of the financial services; and

(d) whether any undue influence or pressure was exerted on, or any unfair tactics were used against, the service recipient or a person acting on behalf of the service recipient by the supplier or a person acting on behalf of the supplier in relation to the supply or possible supply of the financial services; and

(e) the amount for which, and the circumstances under which, the service recipient could have acquired identical or equivalent financial services from a person other than the supplier; and

(f) the extent to which the supplier’s conduct towards the service recipient was consistent with the supplier’s conduct in similar transactions between the supplier and other like service recipients; and

(g) if the supplier is a corporation—the requirements of any applicable industry code (see subsection (3)); and

(h) the requirements of any other industry code (see subsection (3)), if the service recipient acted on the reasonable belief that the supplier would comply with that code;

(i) the extent to which the supplier unreasonably failed to disclose to the service recipient:

(i) any intended conduct of the supplier that might affect the interests of the service recipient; and

(ii) any risks to the service recipient arising from the supplier’s intended conduct (being risks that the supplier should have foreseen would not be apparent to the service recipient); and

(j) if there is a contract between the supplier and the service recipient for the supply of the financial services:

(i) the extent to which the supplier was willing to negotiate the terms and conditions of the contract with the service recipient; and

(ii) the terms and conditions of the contract; and

(iii) the conduct of the supplier and the service recipient in complying with the terms and conditions of the contract; and

(iv) any conduct that the supplier or the service recipient engaged in, in connection with their commercial relationship, after they entered into the contract; and

(k) without limiting paragraph (j), whether the supplier has a contractual right to vary unilaterally a term or condition of a contract between the supplier and the service recipient for the supply of the financial services; and

(l) the extent to which the supplier and the service recipient acted in good faith.

72 The meaning of ‘statutory unconscionability’ has been considered in a number of recent cases, including by the Full Court of this Court in Australian Competition and Consumer Commission v Quantum Housing Group Pty Ltd [2021] FCAFC 40 (‘ACCC v Quantum Housing Group’).

73 In ACCC v Quantum Housing Group, the Full Court (Allsop CJ, Besanko and McKerracher JJ) in considering s 12CB of the ASIC Act and the decision of the High Court in Australian Securities and Investments Commission v Kobelt (2019) 267 CLR 1, confirmed it was not an essential ingredient of statutory unconscionability that there is some form of pre-existing disadvantage, vulnerability or disability of which advantage is taken: at [78]-[85]. Rather, “unconscionable” has its ordinary or natural meaning of “doing what should not be done in good conscience”, as guided by the human values that inform an Australian business conscience: ACCC v Quantum Housing Group at [87]. See also Unique International College Pty Ltd v Australian Competition and Consumer Commission (2018) 266 FCR 631 (‘Unique International College v ACCC’) at [155] (Allsop CJ, Middleton and Mortimer JJ).

Contraventions in relation to each of the eight identified clients

74 Forex CT admits that it engaged in unconscionable conduct in relation to the eight identified clients in contravention of s 991A of the CA and s 12CB of the ASIC Act by reason of the following circumstances:

(a) each of the clients had an incomplete or inadequate understanding of the operation of the Products, which were complex and risky in nature;

(b) all of the clients had no experience, or limited experience, of trading in the Products and were therefore at a disadvantage vis-à-vis Forex CT as counterparty to the transaction;

(c) in relation to at least some of the clients, Forex CT failed to comply with guidelines published by ASIC for providers of CFDs and Margin FX. In particular, Forex CT failed to apply minimum qualification criteria when taking on new clients and, in some instances, the account manager effectively coached the client to pass the qualification quiz. For example, the following exchange occurred when Investor 4 was attempting to complete the quiz:

[ACCOUNT MANAGER 13]: We will – we will be trading CFDs which stands for contract for difference. When you are trading CFDs they are typically during volatile periods, leverage traded and trading as a short term investment.

[INVESTOR 4]: Yeah. Okay. That’s - - -

[ACCOUNT MANAGER 13]: Okay.

[INVESTOR 4]: - - - [01:29:24] that’s the - - - [ACCOUNT MANAGER 13]: If you think of the third one you click the third one. Okay.

[INVESTOR 4]: Okay.

[ACCOUNT MANAGER 13]: Okay. Beautiful.

(d) The explanation provided to each of the clients in relation to the risk of investing in the Products was inadequate. Given the inexperience of each of the clients, and the complexity and risk associated with leveraged products of the kind offered by Forex CT, much more was required by way of explanation of the risk of trading in the Products. For example:

[INVESTOR 1]: They're all in - - -

[ACCOUNT MANAGER 1]: Yeah. So - - -

[INVESTOR 1]: - - - red and I'm so scared to take [indistinct] - - -

[ACCOUNT MANAGER 1]: That’s okay. No, that’s, that’s okay. Don’t be afraid when you see red. Um, [Investor 1], like, when you see a red colour, obviously, it means that the market’s going against you, but you, you have to understand that the market does fluctuate, you know, in both directions, up and down. So - - -

[INVESTOR 1]: Yeah, okay.

[ACCOUNT MANAGER 1]: - - - um, even though it’s in red at the moment now, uh, I'm pretty sure, in the past, you’ve seen that you go onto a trade. It gets into a red. Next minute, two hours or three hours later or next day, it goes into a green colour and you’re in profit. Right?

[INVESTOR 1]: I know.

[ACCOUNT MANAGER 1]: Yeah. Now, [Investor 1], at the end of the day, what you want to, what you want to be careful of is, you know, you produce stuff. You can clearly see for yourself that you deposit a thousand, you produce close to 4,000 in your trades but, obviously, at the moment now it’s in the red, hence the reason why it’s gone in the other direction.

[INVESTOR 1]: Mmm.

[ACCOUNT MANAGER 1]: Um, but you need to understand one thing, [Investor 1]. Don’t think, and give yourself the opportunity, when I say give yourself the opportunity, what I mean by that is, when you place on a trade, um, don’t think that any money that you place in your account, that you’re going to lose it, because already you're thinking on a negative, negative pattern. You know what I mean? Like, why don’t you think if you had more money in there, you’ll be more safer. But a lot of clients are like this stock standardly. Um, you know, me, myself, here, I'm a, I'm a senior account manager. Acquisition Agent 1 is my junior here in ForexCT.

(e) The account managers failed to take any steps, or any adequate steps, to assess the client’s appetite for risk or the appropriateness of the Products to the client.

(f) The account managers employed high pressure sales tactics, such as offering credits and rebates to encourage the client to transfer more money to Forex CT, even after the client had told the account manager that they could not afford to invest more money, or were reluctant to do so.

(g) Forex CT implemented a remuneration structure (as I have already outlined at [22] and [49] above), which was likely to provide an incentive to account managers to encourage clients to deposit funds and to discourage them from withdrawing funds.

(h) The account managers made various misrepresentations to the clients (as I have already outlined at [65]-[66] above), and in particular as to the risk to the client of transferring further amounts to Forex CT and the prospect of the client profiting from particular trades.

(i) The account managers recommended strategies that were inappropriate to the clients, (as I have already outlined at [45]-[46] above), such as placing more trades or trading with greater volume, or leaving open trades that were in a loss (often with predictions made as to the likelihood that the trade would turn around, which the account manager could not have had reasonable grounds for making).

(j) The account managers delayed the processing of the client’s request to withdraw funds, and actively tried to dissuade the client from proceeding with the withdrawal.

Unconscionable system of conduct or pattern of behaviour

75 A system of conduct or pattern of behaviour can constitute unconscionable conduct for the purpose of s 12CB(1) of the ASIC Act without the necessity to identify the circumstances of, or the effect upon, any particular consumer: s 12CB(4)(b) of the ASIC Act.

76 Whether or not a corporation or an individual has engaged in conduct that reveals a system of conduct or pattern of behaviour will be context sensitive, as will the characterisation of conduct as unconscionable: Unique International College v ACCC at [150].

77 Forex CT admits that it engaged in a system of conduct or pattern of behaviour that amounted to unconscionable conduct in contravention of s 12CB of the ASIC Act by:

(a) engaging in, facilitating or encouraging the unconscionable conduct in relation to the eight identified clients, as discussed above;

(b) facilitating trading in Margin FX and CFDs:

(i) in circumstances where (as I have said at [18] above) many of the clients did not have a sufficient understanding of the nature of the financial products and the risks inherent in them, and were reliant on the advice and recommendations of the account manager;

(ii) without conducting a thorough assessment of the client’s objectives, financial situation and needs to determine whether such financial products were appropriate for the client;

(c) establishing and enforcing key performance indicators for retention team leaders, account managers and acquisition agents that resulted in a conflict between the interests of representatives and the interests of Forex CT clients;

(d) implementing an employee remuneration scheme and key performance indicators that (as I have said at [55 (b)] above), was likely to provide an incentive to account managers to encourage clients to deposit funds and to discourage them from withdrawing funds and to recommend trades or trading strategies that were not necessarily in the clients’ best interests;

(e) implementing a bonus structure that (as I have said at [49] above) incentivised acquisition agents to maximise the number of first time deposits that they obtained from new clients and therefore created a significant risk that acquisition agents would coach prospective new clients to assist them to pass the qualification quiz;

(f) implementing and encouraging a trading floor culture that was directed towards maximising trading volume and client deposits and not adequately promoting a culture of compliance with applicable legal requirements;

(g) establishing and implementing incentives for clients to deposit funds and disincentives for clients to withdraw funds from their trading accounts;

(h) providing inadequate or inappropriate training and guidance to representatives, including encouraging representatives to advise clients to trade more frequently and in higher volumes and training representatives to use a client in a negative situation in relation to their trading of the Products as an opportunity to persuade the client to deposit more funds into their trading account, without consideration of whether that was in the client’s best interests;

(i) training and encouraging representatives to deploy strategies to persuade clients to cancel requests to withdraw funds from their trading account; and

(j) failing to ensure compliance with financial services laws.

Contravention of ss 963F and 963J of the CA by Forex CT

78 Division 4 of Pt 7.7A of the CA bans the giving and acceptance of conflicted remuneration in certain circumstances. Section 963F of the CA provides:

A financial services licensee must take reasonable steps to ensure that representative of the licensee do not accept conflicted remuneration.

Note: This section is a civil penalty provision (see section 1317E).

79 Section 963J of the CA also provides:

An employer of a financial services licensee, or a representative of a financial services licensee, must not give the licensee or representative conflicted remuneration for work carried out, or to be carried out, by the licensee or representative as an employee of the employer.

Note: This section is a civil penalty provision (see section 1317E).

80 Section 963A of the CA defines conflicted remuneration as follows:

Conflicted remuneration means any benefit, whether monetary or non-monetary, given to a financial services licensee, or a representative of a financial services licensee, who provides financial product advice to persons as retail clients that, because of the nature of the benefit or the circumstances in which it is given:

(a) could reasonably be expected to influence the choice of financial product recommended by the licensee or representative to retail clients; or

(b) could reasonably be expected to influence the financial product advice given to retail clients by the licensee or representative.

(Note omitted.)

81 Forex CT paid monthly bonuses to its account managers based on a formula that was heavily weighted by reference to total net deposits to the trading accounts of clients of the relevant account manager. Under what is referred to by the parties as the “Retention Desk Bonus Structure”, the payment of a bonus was subject to the account manager meeting specified “prerequisites” or “gate openers” including a requirement that the account manager must meet an “average daily talk time target”. The payment of a bonus was also subject to meeting monthly targets in relation to the account manager’s ‘trading book’, which I have already outlined at [49] above.

82 Insofar as the financial product advice given by account managers involved recommendations that the client should deposit amounts into their trading account, or should not withdraw amounts from their trading account, it could reasonably be expected that the benefits paid in accordance with this bonus structure would influence that recommendation, regardless of whether or not it was in the client’s interests.

83 Forex CT admits that it contravened s 963F of the CA by failing to take reasonable steps to ensure that its account managers did not accept conflicted remuneration. Forex CT also admits that it contravened s 963J of the CA on 116 instances by giving bonuses and incentives to account managers that constituted conflicted remuneration for work carried out by that account manager as an employee.

Contravention of s 912A(1) of the CA by Forex CT

84 Section 912A(1) of the CA relevantly provides:

A financial services licensee must:

(a) do all things necessary to ensure that the financial services covered by the licence are provided efficiently, honestly and fairly…

85 In Australian Securities and Investments Commission v Camelot Derivatives Pty Ltd (in liq) [2012] FCA 414, Foster J accepted (at [69]-[70] citing Re Hres and Australian Securities and Investments Commission (2008) 105 ALD 124 at [237]) that the words “efficiently, honestly and fairly”:

connote an element not just of even handedness in dealing with clients but a less readily defined concept of sound ethical values and judgment in matters relevant to a client’s affairs.

86 In Australian Securities and Investments Commission v Cassimatis (No 8) [2016] FCA 1023, Edelman J stated:

[673] …the contraventions [of the CA] were sufficiently serious departures from reasonable standards of performance of advice that they involved a failure to ensure that the financial services covered by the licence were provided efficiently, honestly and fairly.

[674] This approach to “efficiently, honestly and fairly”, which treats the expression as including an assessment of reasonable expectations of performance and reasonable standards of performance, is consistent with the decision in Australian Securities and Investments Commission v Camelot Derivatives Pty Ltd (in liq) (2012) 88 ACSR 206; [2012] FCA 414…

87 Forex CT admits that it contravened s 912A(1) of the CA by engaging in the following actions in the Relevant Period:

(a) failing to take reasonable steps to ensure compliance by its representatives with financial services laws, in particular ss 961B, 961G, 961J, 991A and 1041H of the CA and ss 12CB(1) and 12DA of the ASIC Act;

(b) implementing recruitment practices that focused on recruiting people to perform the role of account manager who had a sales background, rather than a background in derivative financial products, or financial products more generally;

(c) failing to adequately train account managers and team leaders, including by providing ongoing training in relation to key legal requirements, including the distinction between general advice and personal advice;

(d) having inadequate or inappropriate training procedures for account managers allocated to clients, which failed to deter representatives from contravening applicable financial services laws;

(e) failing to implement an effective compliance monitoring process as, to the extent that compliance monitoring was conducted during the Relevant Period, it was inadequate in that Forex CT did not ensure:

(i) monitoring of a sufficient number of calls;

(ii) monitoring was conducted by compliance staff who were adequately trained in the requirements of the financial services laws and the compliance issues to look out for, and who themselves were subject to performance monitoring and review;

(iii) appropriate action was taken in relation to account managers found to be non-compliant;