FEDERAL COURT OF AUSTRALIA

Kelly (Liquidator), in the matter of Halifax Investment Services Pty Ltd (in liquidation) v Loo [2021] FCA 531

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

In these orders the following terms mean:

Distribution Process means the process for undertaking a cash distribution, as set out in Order 19 below.

Gain Suspense Account means a bank account of the third plaintiff (Halifax AU) called GAIN SUSP with Bankwest and with account number 302100 9049132.

Halifax Pro Suspense Account means a bank account of Halifax AU called HLFX PRO SUS with Bankwest and with account number 302100 9066457.

IB AU platform means the Trader Workstation platform for Halifax AU.

IB AU Prop Account means a bank account of Halifax AU called IB AU Prop Account with Interactive Brokers LLC and with account number U1430547.

IB NZ platform means the Trader Workstation platform for Halifax New Zealand Ltd (in liquidation) (Halifax NZ).

IB Suspense Account means a bank account of Halifax AU called IB SUSPENSE with Bankwest and with account number 302100 9023952.

Interactive Brokers means Interactive Brokers LLC.

MT4 platform means the MetaTrader4 trading platform licensed by Halifax AU from MetaQuotes Software Corp (MetaQuotes) and also known as “Halifax Pro”.

MT5 platform means the MetaTrader5 trading platform licensed by Halifax Capital Markets, a related entity of Halifax AU, from MetaQuotes and also known as “Halifax Plus”.

NAB GBP Account means a bank account of Halifax AU with the National Australia Bank (NAB) and with account number HAFAXGBP01.

NAB USD Account means a bank account of Halifax AU with the NAB and with account number HAFAXUSD01.

Post-Appointment Deposits means the funds totalling (as at 30 November 2020) AUD125,733 deposited on or after 23 November 2018 into the IB Suspense Account, the Halifax Pro Suspense Account, the Saxo Suspense Account, the Gain Suspense Account, the NAB USD Account, the NAB GBP Account and (by use of a credit card) account number 5353109291777640.

Pre-Appointment Deposits means the funds totalling (as at 30 November 2020) AUD25,000 deposited on 22 November 2018 into the Saxo Suspense Account, the IB Suspense Account and the Halifax Pro Suspense Account.

Saxo Suspense Account means a bank account of Halifax AU called SAXO SUSP with Bankwest and with account number 302100 9001247.

AMENDMENT OF ORDERS MADE ON 3 APRIL 2020

1. Pursuant to r 2.13(3) and (5) of the Federal Court (Corporations) Rules 2000 (Rules) and/or s 90-15(1) of the Insolvency Practice Schedule (Corporations), being Schedule 2 to the Corporations Act 2001 (Cth) (IPS), Fiona McMullin be added as the fifth defendant and appointed:

(a) to represent all clients of Halifax Investment Services Pty Ltd (in liquidation) (Halifax Australia) and all clients of Halifax NZ who invested before 1 January 2016 in order to propound the argument that investments made before there was a deficient mixed fund are traceable;

(b) to represent all clients of Halifax NZ who acquired shares before 1 November 2013 and who have not traded in those shares; and

(c) to represent all clients of Halifax Australia and Halifax NZ who transferred shares into the Saxo trading platform from another stockbroker and have not traded in those shares, which shares were transferred from the Saxo trading platform to the IB AU platform or the IB NZ platform and were recorded in a client account on the MT5 platform, the IB AU platform or the IB NZ platform.

CATEGORY 3 INVESTORS

2. The plaintiffs are justified in organising for the shares of clients of the third plaintiff, Halifax AU, and Halifax NZ that were transferred from another broker to the IB AU platform or the IB NZ platform, and were never traded (Category 3 Shares), to be transferred to a person nominated in writing (including by email) by the client in respect of whom the entitlement to those shares is recorded by Halifax AU or Halifax NZ (as the case may be).

3. The plaintiffs are justified in conclusively identifying clients of Halifax AU and Halifax NZ as those with an entitlement to Category 3 Shares by:

(a) sending a written communication (which may include an email) to all clients of Halifax AU and Halifax NZ with accounts on the IB AU platform or the IB NZ platform, which have open share positions recorded, asking them to confirm in writing within 21 days whether they contend that they have an entitlement to Category 3 Shares (Category 3 Communication); and

(b) proceeding on the basis that only affirmative responses of clients to the Category 3 Communication are to be further considered as to whether the clients responding hold an entitlement to Category 3 Shares.

4. If, within 35 days, the plaintiffs do not receive a written response to the Category 3 Communication they are justified in treating those who have not responded as having no entitlement to Category 3 Shares.

5. The plaintiffs are justified in requiring that all clients of Halifax AU and Halifax NZ from whom they receive an affirmative response to the Category 3 Communication pay to the first and second plaintiffs (Liquidators) a fee of AUD1,500 within 21 days of the plaintiffs’ request for such a fee together with a proportionate share of all additional fees and expenses of the Liquidators concerning their work in relation to the Category 3 Shares as approved by the Court.

6. If the Liquidators do not receive the fee of AUD1,500 requested pursuant to Order 5 above within 35 days of their request, the plaintiffs are justified in treating the shares the subject of the Category 3 Communication as not being Category 3 Shares.

CATEGORY 5 INVESTORS

7. The plaintiffs are justified in organising for the shares of clients of Halifax AU or Halifax NZ who:

(a) transferred shares from another broker to the Saxo platform and never traded in those shares, which shares were transferred from the Saxo platform to the IB AU platform or the IB NZ platform and were recorded in a client account on the MT5 platform, the IB AU platform or the IB NZ platform; or

(b) purchased shares through the IB NZ platform prior to 1 July 2013 and never traded in those shares; or

(c) purchased shares through the IB AU platform prior to 1 May 2012 and never traded in those shares,

(collectively, Category 5 Shares) to be transferred to a person nominated in writing (including by email) by the client in respect of whom the entitlement to those shares is recorded by Halifax AU or Halifax NZ (as the case may be).

8. The plaintiffs are justified in conclusively identifying clients of Halifax AU and Halifax NZ as those with an entitlement to Category 5 Shares by:

(a) sending a written communication (which may include an email) to all clients of Halifax AU and Halifax NZ with accounts on the IB AU platform or the IB NZ platform, which have open share positions recorded, asking them to confirm in writing within 21 days whether they contend that they have an entitlement to Category 5 Shares (Category 5 Communication); and

(b) proceeding on the basis that only affirmative responses of clients to the Category 5 Communication are to be further considered as to whether the clients responding hold an entitlement to Category 5 Shares.

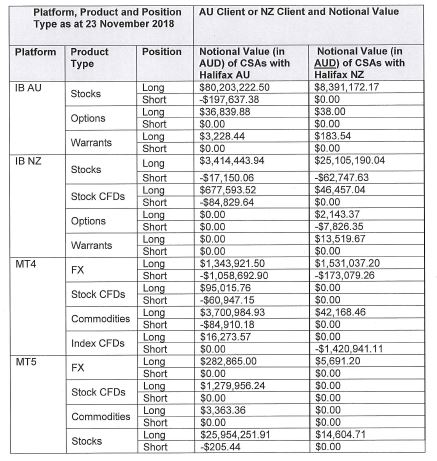

9. If, within 35 days, the plaintiffs do not receive a written response to the Category 5 Communication they are justified in treating those who have not responded as having no entitlement to Category 5 Shares.

10. The plaintiffs are justified in requiring that all clients of Halifax AU and Halifax NZ from whom they receive an affirmative response to the Category 5 Communication pay to the Liquidators a fee of AUD1,500 within 21 days of the plaintiffs’ request for such a fee together with a proportionate share of all additional fees and expenses of the Liquidators concerning their work in relation to the Category 5 Shares as approved by the Court.

11. If the Liquidators do not receive the fee of AUD1,500 requested pursuant to Order 10 above within 35 days of their request, the plaintiffs are justified in treating the shares the subject of the Category 5 Communication as not being Category 5 Shares.

PRE-APPOINTMENT DEPOSITS

12. The plaintiffs are justified in organising for the Pre-Appointment Deposits to be returned to the client(s) who made those deposits and in returning those deposits.

POST-APPOINTMENT DEPOSITS

13. The plaintiffs are justified in organising for the Post-Appointment Deposits to be returned to the client(s) who made those deposits and in returning those deposits.

DATE OF CALCULATION OF VALUE OF CLIENTS’ ENTITLEMENTS

14. Subject to Orders 2, 7, 12 and 13 above, the plaintiffs are justified in adopting 27 November 2018 as the date at which the proportionate entitlements of clients are to be calculated.

E. POOLING AND DISTRIBUTION

15. Subject to Orders 2, 7, 12 and 13 above, the plaintiffs are justified in calculating client entitlements using the pari passu approach.

16. Subject to Orders 2, 7, 12 and 13 above, as soon as reasonably practicable, the plaintiffs are justified in closing out, or directing the closing out of:

(a) open positions of clients of Halifax AU recorded in accounts on the IB AU platform and the IB NZ platform;

(b) open positions of Halifax AU recorded in the IB AU Prop Account; and

(c) open positions of clients of Halifax AU and Halifax NZ recorded in client accounts on the MT4 and MT5 platforms.

17. Subject to Orders 2, 7, 12 and 13 above, the plaintiffs are justified in pooling the funds in the bank accounts listed in Annexure A to these Orders.

18. For the purpose of calculating each client’s proportionate entitlement in accordance with Orders 14 and 15 above and/or for the purpose of making a distribution to clients in accordance with Order 19 below, the plaintiffs are, prior to making the calculation and/or distribution, justified in converting into Australian dollars or New Zealand dollars any foreign currency in the Liquidators’ or Halifax AU’s control.

F. DISTRIBUTION PROCESS

19. The plaintiffs are justified in adopting the following process to distribute client entitlements:

(a) the Liquidators are to email each client (or, if email is not, in the Liquidators' opinion, the most appropriate means of communication with an individual client, post to the client’s last known address) a notification providing them with unique login details to a secure, web-based client portal (Investor Portal) and instructing them that, upon logging into the Investor Portal, they will be notified of the value of their entitlement for the purpose of any distribution (Distribution Notice);

(b) in the Investor Portal, the Liquidators are:

(i) to ask clients to verify their identity and to confirm the value of their entitlement;

(ii) if a client disputes the value of their entitlement, to ask the client to notify the plaintiffs of this and provide reasons and supporting documentation (if any) in support of their position; and

(iii) to ask clients to provide their bank account details (Nominated Bank Account) for the distribution of an entitlement;

(c) clients are to be given 21 days to respond to the Distribution Notice by logging into the Investor Portal and completing the steps identified in Order 19(b) above;

(d) if, in response to the Distribution Notice, a client affirmatively disputes the value of their entitlement then, on the condition that their response is accompanied by both reasons and any necessary supporting documents:

(i) the Liquidators are to assess whether the dispute is well-founded;

(ii) if the dispute is well-founded, the Liquidators are to notify the client that the Liquidators agree with the issues raised in the dispute and have agreed to amend the value of the entitlement; and

(iii) if the dispute is not well-founded, the Liquidators are to notify the client that they may apply to the Court (in this proceeding) if the client considers that their dispute is well-founded and that otherwise the Liquidators may proceed to distribution on the basis of the value of the entitlement as set out in the Distribution Notice;

(e) the Liquidators are to proceed to distribution on the basis of the value of the entitlement of each client as recorded in the Investor Portal if:

(i) within 35 days of the Distribution Notice, the client confirms the value of their entitlement on the Investor Portal; or

(ii) the client does not log into the Investor Portal to confirm or dispute their entitlement within 35 days of the Distribution Notice; or

(iii) the client logs into the Investor Portal and disputes their claim but provides no particularity as to the basis of their dispute within 21 days of notification that the client must provide further particularity or else the distribution will proceed on the basis of the client’s entitlement as set out in the Distribution Notice; or

(iv) the Liquidators notify the client that their dispute is not well-founded in accordance with the process in Order 19(d)(iii) above and the client does not apply to the Court (in this proceeding) within 21 days of that notification.

SET-OFF

20. The plaintiffs are justified in proceeding on the following basis in respect of the calculation of entitlements of clients:

(a) where a client has multiple accounts on the IB AU platform and/or the IB NZ platform and/or the MT4 platform and/or the MT5 platform, the plaintiffs are entitled to combine the balances of those accounts to calculate the net position of a client; and

(b) setting off positive account balances credited to a particular client against negative account balances incurred by the same client.

LOW ACCOUNT BALANCES

21. The plaintiffs are justified in treating clients who have a credit balance of AUD100 or less as having no right to participate in the distribution of funds by the Liquidators.

ELECTRONIC COMMUNICATIONS

22. Subject to Order 19(a) above, the plaintiffs are justified in publishing or sending any notices, correspondence or other relevant material to clients as part of the distribution process set out in Order 19 by:

(a) sending copies of any notices, correspondence or other relevant materials to the email address of each client for whom the Liquidators, Halifax AU or Halifax NZ holds an email address; and

(b) by notice or link on https://home.kpmg/au/en/home/creditors/halifax-investment-services.html and https://home.kpmg/au/en/home/creditors/halifax-nz-limited.html.

COSTS

23. The eighth and ninth defendants are to pay the plaintiffs’ costs and expenses incurred by reason of their joinder to this proceeding, including in responding to the contentions raised by those defendants in the letter dated 3 July 2020 from their solicitors at the time, on an indemnity basis and in a lump sum in the amount of AUD351,810.05 (exclusive of 88.99% of GST).

24. On or before 2 June 2021 the plaintiffs (and any other party wishing to make a claim) are to file and serve their submissions, not exceeding three pages in length, in relation to any claim for costs as against the sixth and seventh defendants.

25. On or before 16 June 2021 the sixth and seventh defendants are to file and serve their submissions in response, not exceeding three pages in length.

26. If submissions are filed and served in accordance with Orders 24 and 25 above, any claim for costs against the sixth and seventh defendants will be determined on the papers.

NOTICE

27. The requirement to provide notice for the purpose of s 63(8) of the Trustee Act 1925 (NSW) (Trustee Act) is dispensed with.

28. The time fixed for making an application under s 63(10) of the Trustee Act is 14 days after the date of these Orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

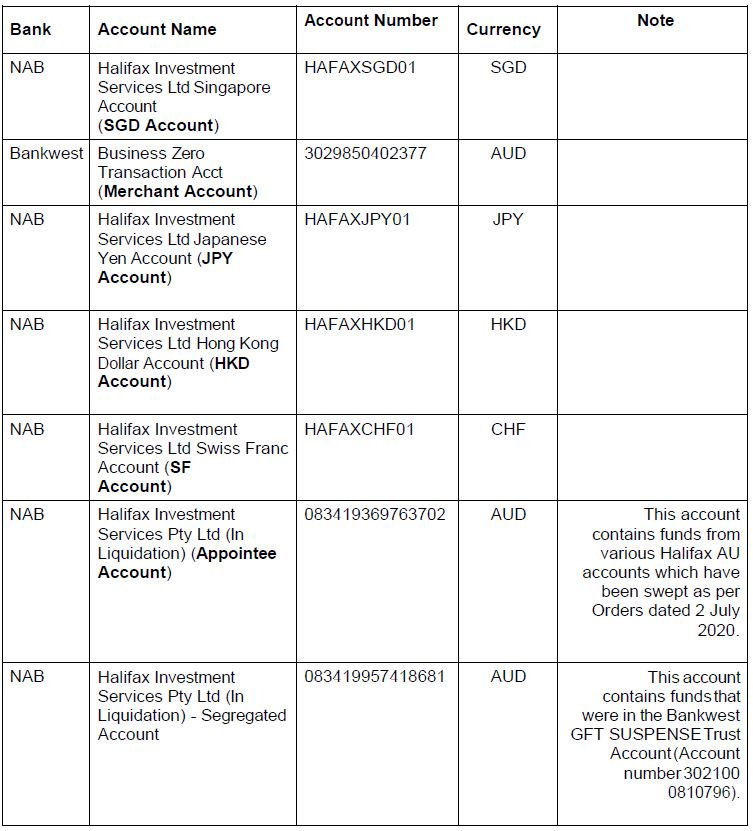

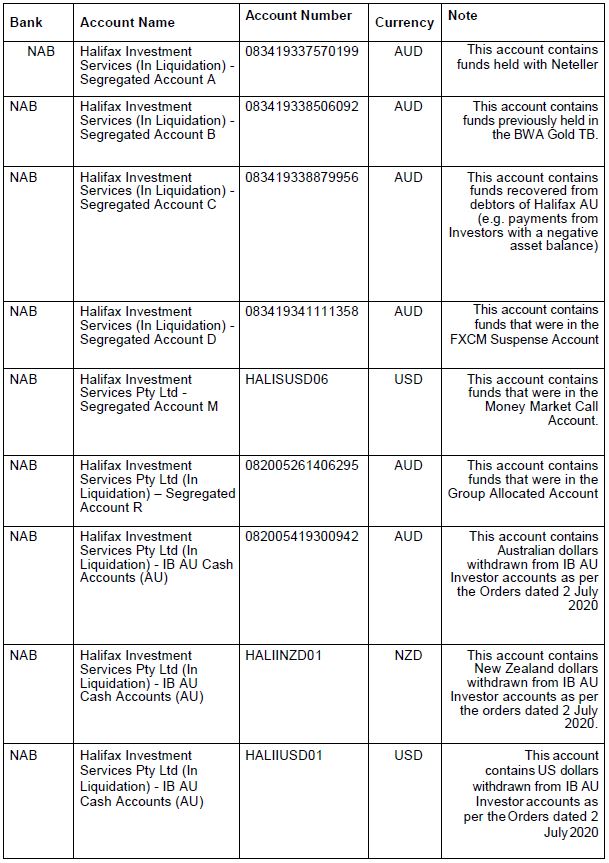

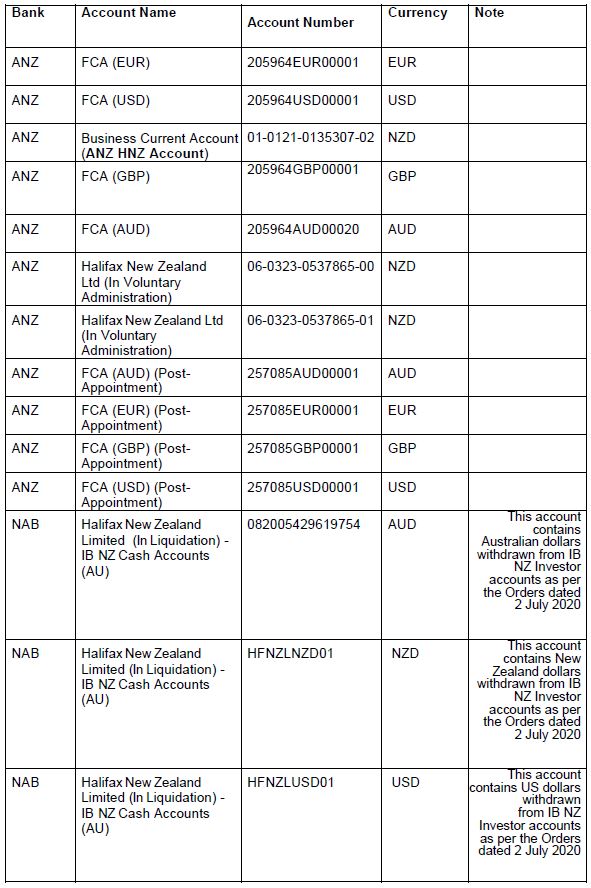

Annexure A

Bank accounts of Halifax AU

Bank accounts of Halifax NZ

[11] | |

[14] | |

2.1 An application for judicial advice and directions – legal principles | [14] |

[21] | |

[31] | |

[32] | |

[36] | |

[40] | |

[44] | |

[45] | |

[55] | |

[73] | |

[76] | |

[79] | |

[81] | |

[93] | |

3.10 Distribution of funds held by Halifax AU and Halifax NZ | [97] |

[97] | |

[98] | |

[105] | |

[109] | |

[118] | |

4.1 Moneys held by Halifax AU and Halifax NZ – legislative framework | [118] |

[134] | |

[147] | |

6.1 Did the funds held on trust by Halifax AU and Halifax NZ become commingled? | [149] |

6.2 Was there a deficiency in the funds held by Halifax AU and Halifax NZ? | [160] |

[165] | |

[166] | |

[167] | |

[172] | |

[181] | |

[197] | |

[198] | |

[210] | |

[216] | |

[231] | |

[253] | |

[254] | |

[258] | |

[267] | |

[283] | |

[283] | |

[288] | |

[298] | |

[312] | |

[325] | |

[329] | |

[340] | |

[366] | |

9.1 Correspondence between the Liquidators and the Shareholders | [366] |

[371] | |

[392] | |

[393] | |

[399] | |

[408] | |

[410] |

REASONS FOR JUDGMENT

MARKOVIC J:

1 Halifax Investments Services Pty Ltd (in liquidation) (Halifax AU) was incorporated on 30 May 2001. It is an Australian company. Its current ordinary shareholders are:

(1) Hong Kong Capital Holdings Pty Ltd (HK Capital) which holds 40.97% of the ordinary shares;

(2) Jeffrey Worboys who holds 40.97% of the ordinary shares; and

(3) Blunsdon Management Pty Ltd which holds 18.06% of the ordinary shares.

2 Halifax New Zealand Limited (in liquidation) (Halifax NZ) was incorporated on 21 May 2008. It is a New Zealand company. Prior to 9 October 2013 Halifax NZ was called Strategic Capital Management Limited (Strategic Capital). In 2013 Halifax AU purchased a controlling interest in Halifax NZ. Its current shareholders are:

(1) Halifax AU as to 70%;

(2) Kay Williams and Andrew Gibbs (Andrew Gibbs Family Trust) as to 29.5%; and

(3) Andrew Gibbs, the director of Halifax NZ, as to 5%.

3 Halifax AU and Halifax NZ were financial service providers dealing in financial products on behalf of their respective clients. Their operations are described in more detail below.

4 On 23 November 2018 Morgan John Kelly, Philip Alexander Quinlan and Stewart McCallum were appointed as joint and several voluntary administrators of Halifax AU pursuant to s 436A(1) of the Corporations Act 2001 (Cth) (Corporations Act). On 27 November 2018 Messrs Kelly, Quinlan and McCallum were appointed as joint and several voluntary administrators of Halifax NZ pursuant to s 239(1) of the Companies Act 1993 (NZ) (Companies Act (NZ)).

5 On 20 March 2019 Messrs Kelly, Quinlan and McCallum were appointed as liquidators of Halifax AU pursuant to s 439C(c) and s 446A of the Corporations Act and, on 22 March 2019, they were appointed as liquidators of Halifax NZ pursuant to s 241(2)(d) of the Companies Act (NZ).

6 On 9 and 13 May 2019 respectively Mr McCallum resigned from his appointment as a liquidator of Halifax NZ and of Halifax AU. I will refer to the remaining liquidators of those companies, Messrs Kelly and Quinlan, as the Liquidators in these reasons.

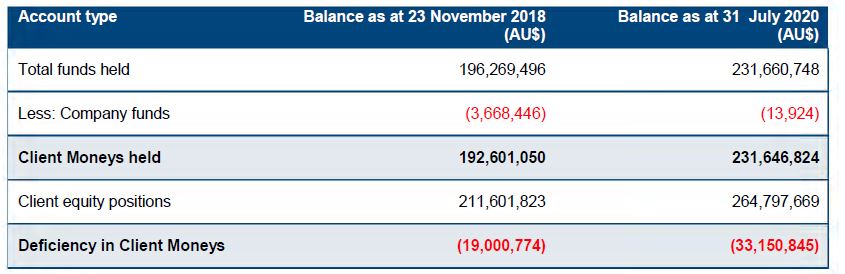

7 By way of interlocutory process dated 2 July 2019, the Liquidators and Halifax AU bring an application for directions and judicial advice regarding a number of questions that arise in relation to the distribution of funds held on trust by Halifax AU for its investor clients, including whether the Liquidators and Halifax AU would be justified in: pooling all or some of the funds held by each of Halifax AU and Halifax NZ in various accounts; paying each client their entitlement to the funds in the pool on a pari passu or on some other basis; converting funds held in foreign currency to Australian dollars and funds held in Australian dollars to New Zealand dollars for the purpose of distribution to clients of Halifax AU and Halifax NZ respectively; calculating the value of investments by each client for the purposes of distribution as at 23 November 2018, 27 November 2018, the date of realisation of each investment or some other date; setting off positive net account balances against negative net account balances for the same client; and excluding those clients who have a credit balance of AUD100 or less from participating in a distribution of funds.

8 By originating application for directions filed in proceeding CIV-2019-404-2049 (NZ Proceeding) in the High Court of New Zealand (High Court NZ) on 25 September 2019, the Liquidators and Halifax NZ seek judicial advice and directions in respect of the same questions.

9 This Court and the High Court (NZ) each determined to hear the interlocutory process filed in this Court and the originating application for directions filed in the High Court (NZ) concurrently: see Re Kelly; Halifax Investment Services Pty Ltd (in liq) (No 5) [2019] FCA 1341; (2019) 139 ACSR 56 (Kelly (No 5)) and Minute No (4) issued on 12 December 2019 in the NZ Proceeding.

10 Accordingly, since December 2019, this proceeding and the NZ Proceeding have proceeded in parallel with the two courts sitting concurrently to hear applications and conduct case management hearings and, ultimately, to conduct the hearings of the interlocutory application and the originating application in which, in each case, the Liquidators and either Halifax AU or Halifax NZ, as applicable, seek judicial advice and directions.

11 By orders made on 19 February 2020 in this proceeding and 3 April 2020 in the NZ Proceeding the following parties were appointed, for the purposes of this proceeding under r 2.13(3) and (5) of the Federal Court (Corporations) Rules 2000 (Cth) (Corporations Rules) and/or s 15(1) of the Insolvency Practice Schedule (Corporations) being Schedule 2 to the Corporations Act (IPS), to represent certain bodies of clients of Halifax AU and/or Halifax NZ:

(1) Choo Boon Loo as first defendant to represent all clients/investors of Halifax AU and of Halifax NZ whose proportionate entitlement to or share of funds from the “deficient mixed fund” (as that phrase is defined in [189] of the affidavit of Mr Kelly sworn 26 June 2019 in this proceeding (Kelly June 2019 Affidavit)) will be higher after the realisation of all extant investments than it was on the date administrators were appointed to Halifax AU and Halifax NZ (category 1 investors);

(2) Elysium Business Systems Pty Ltd (Elysium) as second defendant to represent all clients/investors of Halifax AU and of Halifax NZ whose proportionate entitlement to and share of funds from the “deficient mixed fund” (as that phrase is defined in [189] of the Kelly June 2019 Affidavit) will be lower after the realisation of all extant investments than it was on the date administrators were appointed to Halifax AU and Halifax NZ (category 2 investors);

(3) Jason Hingston as third defendant to represent all clients/investors of Halifax AU and of Halifax NZ who transferred shares into the Trader Workstation (also known as Halifax AU’s IB Platform or Halifax NZ’s IB Platform) from another stockbroker and have not traded in those shares (category 3 investors);

(4) Atlas Assets Management Pty Ltd as trustee for the Atlas Management Trust (Atlas) as fourth defendant to represent all clients/investors of Halifax AU and of Halifax NZ whose investments are not traceable and who wish to contend that all clients should share in any deficiency regardless of whether investments are traceable or not (category 4 investors); and

(5) Fiona McMullin as fifth defendant to represent all clients/investors of Halifax AU and of Halifax NZ who invested before 1 January 2016 in order to propound the argument that investments made before there was a deficient mixed fund are traceable (category 5 investors).

12 On 3 April 2020 Andrew Phillip Whitehead and Marlene Whitehead, in their capacity as trustees of the Beeline Trust and Andrew Phillip Whitehead (collectively, Whitehead Interests), were added as sixth and seventh defendants to this proceeding pursuant to r 2.13(3) and (5) of the Corporations Rules and/or s 90-15(1) of the IPS and to the NZ Proceeding to propound certain arguments in their own interest.

13 On 13 August 2020 and 21 September 2020 respectively Mr Worboys and HK Capital (collectively, Shareholders) were joined as eighth and ninth defendants to this proceeding and to the NZ Proceeding to propound particular claims relating to Halifax AU. On 12 November 2020 the solicitors for Mr Worboys and HK Capital filed a notice of ceasing to act. Thereafter Mr Worboys and HK Capital each notified the Court of their respective addresses for service. However, there was no appearance by them or on their behalf at the hearing of the interlocutory process.

2. The nature of the proceeding

2.1 An application for judicial advice and directions – legal principles

14 The application before this Court is, on the part of the Liquidators, for directions pursuant to s 90-15 of the IPS and, on the part of Halifax AU in its capacity as a trustee, for judicial advice. Before proceeding further it is convenient to set out the principles that guide the Court on such applications.

15 Section 90-15(1) of the IPS provides that the Court may make such orders as it thinks fit in relation to the external administration of a company which may include an order determining any question arising in the external administration of the company: see s 90-15(3)(a).

16 In Re Kelly, in the matter of Halifax Investments Services Pty Ltd (in liq) (No 8) [2020] FCA 533; (2020) 144 ACSR 292 at [50]-[59] Gleeson J set out the principles applicable to the exercise of the power in s 90-15 of the IPS including relevantly:

52 In Ample Source International Limited v Bonython Metals Group Pty Limited (in liquidation), in the matter of Bonython Metals Group Pty Limited (in liquidation) (No 8) [2018] FCA 1614 at [88]-[92], I set out the following matters concerning s 90-15:

[88] By s 90–20(1)(d) of the Insolvency Practice Schedule and the definition of “officer” in s 9 of the Act, a liquidator is a person who may apply for an order under s 90–15.

[89] The Court’s supervisory powers under s 90–15 of the Insolvency Practice Schedule are arguably as broad, or broader than, its powers under the previous provision, being the former s 479(3) of the Act.

[90] Section 479(3) allowed a court-appointed liquidator to apply to the Court for directions in relation to a matter arising under a winding up. The function of a liquidator’s application for directions under s 479(3) was to give the liquidator advice as to the proper course of action for him or her to take in the liquidation: Re MF Global Australia Ltd (in liq) [2012] NSWSC 994; (2012) 267 FLR 27 at [7].

[91] In Re Ansett Australia Ltd and Korda [2002] FCA 90; (2002) 115 FCR 409, Goldberg J explained at [44]:

When liquidators and administrators seek directions from the Court in relation to any decision they have made, or propose to make, or in relation to any conduct they have undertaken, or propose to undertake, they are not seeking to determine rights and liabilities arising out of particular transactions, but are rather seeking protection against claims that they have acted unreasonably or inappropriately or in breach of their duty in making the decision or undertaking the conduct. They can obtain that protection if they make full and fair disclosure of all relevant facts and circumstances to the Court. In Re G B Nathan & Co Pty Ltd (1991) 24 NSWLR 674, McLelland J said at 679–680:

The historical antecedents of s 479(3) …, the terms of that subsection and the provisions of s 479 as a whole combine to lead to the conclusion that the only proper subject of a liquidator’s application for directions is the manner in which the liquidator should act in carrying out his functions as such, and that the only binding effect of, or arising from, a direction given in pursuance of such an application (other than rendering the liquidator liable to appropriate sanctions if a direction in mandatory or prohibitory form is disobeyed) is that the liquidator, if he has made full and fair disclosure to the court of the material facts, will be protected from liability for any alleged breach of duty as liquidator to a creditor or contributory or to the company in respect of anything done by him in accordance with the direction.

…

Modern Australian authority confirms the view that s 479(3) ‘does not enable the court to make binding orders in the nature of judgments’ and that the function of a liquidator’s application for directions ‘is to give him advice as to his proper course of action in the liquidation; it is not to determine the rights and liabilities arising from the company’s transactions before the liquidation’: [cases cited omitted].

[92] At [65], Goldberg J concluded:

[T]he prevailing principle adopted by the courts, when asked by liquidators and administrators to give directions, is to refrain from doing so where the direction sought relates to the making and implementation of a business or commercial decision, either committed specifically to the liquidator or administrator or well within his or her discretion, in circumstances where there is no particular legal issue raised for consideration or attack on the propriety or reasonableness of the decision in respect of which the directions are sought. There must be something more than the making of a business or commercial decision before a court will give directions in relation to, or approving of, the decision. It may be a legal issue of substance or procedure, it may be an issue of power, propriety or reasonableness, but some issue of this nature is required to be raised. It is insufficient to attract an order giving directions that the liquidator or administrator has a feeling of apprehension or unease about the business decision made and wants reassurance. There must be some issue which arises in relation to the decision. A court should not give its imprimatur to a business decision simply to alleviate a liquidator’s or administrator’s unease. There must be an issue calling for the exercise of legal judgment.

53 In S & D International & Anor v MIG Property Services & Ors [2010] VSC 336; (2010) 79 ACSR 373, Warren CJ approved the liquidator’s compromise of legal proceedings involving competing claims over a property held on trust, exercising the power then conferred by s 511 of the Corporations Act. At [17], her Honour described the case as one that “dealt with the risk attendant upon a conscientious liquidator in an acrimonious liquidation environment” and considered that s 511 orders may have utility to protect liquidators “where such protection would be just and beneficial to advancing the liquidation process as a whole”.

…

56 In Re One.Tel Ltd and Ors [2014] NSWSC 457; (2014) 99 ACSR 247 at [35], Brereton J noted the need for caution in making a direction, saying:

But the fact that a direction under s 511 — unlike an approval under s 477(2A) or (2B) — exonerates the liquidator from personal liability, means that a closer examination of the liquidator’s decision is required than under s 477. In short, the court should not make a direction the effect of which is to exonerate the liquidator from personal liability in respect of a commercial judgment that the liquidator is concerned may prove contentious, unless satisfied that the liquidator’s decision is, in all the circumstances, a proper one.

…

58 In Re KSK Holdings (Australia) Pty Ltd (in liquidation) [2019] NSWSC 1463 at [18], Rees J explained:

The Court may give directions where it will be “of advantage in the liquidation”: Dean-Wilcox v Soluble Solution Hydroponics Pty Limited (1997) 42 NSWLR 209 at 212; (1997) 24 ACSR 79 at 81. The Court will not generally give a direction where the matter relates to the making or implementation of a business or commercial decision or when no legal issue is raised, or where there is no attack on the propriety or reasonableness of the liquidator’s decision, but it may do so where there is the prospect of such an attack: In the matter of Steel Distribution Pty Limited (in liquidation) (receivers and managers appointed) [2013] NSWSC 669 at [20] per Black J; In the matter of Dungowan Manly Pty Limited (in liq) [2018] NSWSC 1083 at [17].

17 Section 63(1) of the Trustee Act 1925 (NSW) (Trustee Act) enables a trustee to apply to the Court for an opinion, advice or direction on any question in relation to the management or administration of the trust property or the interpretation of the trust instrument.

18 The principles in respect of judicial advice to trustees were considered in Macedonian Orthodox Community Church St Petka Inc v His Eminence Petar The Diocesan Bishop of Macedonian Orthodox Diocese of Australia and New Zealand (2008) 237 CLR 66 (Macedonian Orthodox Church). There, the plurality (Gummow ACJ, Kirby, Hayne and Heydon JJ) observed at [56]-[60] that there is no limitation on the power of the Court to give judicial advice pursuant to s 63 of the Trustee Act but there is one jurisdictional bar to relief under the section. That is that an applicant “must point to the existence of a question respecting the management or administration of the trust property or a question respecting the interpretation of the trust instrument”: see Macedonian Orthodox Church at [58].

19 At [64] of Macedonian Orthodox Church, the plurality observed that s 63 of the Trustee Act operates as an exception to a court’s ordinary function of deciding disputes between competing litigants and affords a facility for providing private advice to a trustee, noting that it is private advice because, as is evident from the operation of s 63(2) of the Trustee Act, its function is to give personal protection to the trustee. Section 63(2) of the Trustee Act provides that, if the trustee acts in accordance with the opinion advice or direction, the trustee shall be deemed, so far as regards the trustee’s own responsibility, to have discharged its duty as trustee in the subject matter of the application provided that the trustee has not been guilty of any fraud, wilful concealment or misrepresentation in obtaining the opinion, advice or direction.

20 Given the nature of the relief sought, save in relation to the Shareholders, the Liquidators have quite properly taken a neutral approach in relation to controversial issues raised for resolution, while providing submissions to assist the Court. This is consistent with the approach to be taken where a dispute has arisen between beneficiaries of a trust as to their rights in the trust estate: see Re MF Global Australia (in liq) (2012) FLR 27 (MF Global) at [2].

21 Given its somewhat unique nature, it is appropriate to say something about the conduct of the hearing.

22 In Kelly (No 5) at [32], in considering the Liquidators’ application for the issue of a letter of request to the High Court NZ seeking for that Court to act in aid of and auxiliary to this Court in respect of the interlocutory process filed in this Court, to enable it and the proposed originating application (yet to be filed in the High Court NZ) to be resolved in an effective way, Gleeson J relevantly said:

More specifically, the request, if issued, would be that the NZHC agree to hear and determine the proposed NZ application by sitting jointly with the FCA whilst the FCA hears and determines the application in this proceeding, with a view to each court hearing all of the evidence and all of the submissions in both proceedings together (including evidence adduced by, and submissions by, those who may be joined to either proceeding or who may be given leave in either proceeding to be heard). This could be done in a manner to be jointly determined by the courts,... The letter of request, if issued by this Court as sought by the plaintiffs, would contemplate that the NZHC would deliberate together with the FCA so as to seek to achieve, so far as possible, an outcome in which inconsistency between the judicial advice or directions given by each Court in respect of the same commingled pool of funds is effectively eliminated.

23 At [60] her Honour also observed that:

… Further, it can be readily appreciated that, if the liquidators’ applications are not coordinated, there is a real and obvious prospect of inconsistent findings, inconsistent directions or advice and consequent additional litigation, all potentially to the detriment of creditors of Halifax AU. One means by which the NZHC might act in aid of and be auxiliary to this Court in connection with the application for the pooling order might be to participate in a concurrent hearing of the proposed NZ application with the hearing of the interlocutory process.

24 As set out above, this proceeding and the NZ Proceeding were case managed concurrently and the interlocutory application filed in this Court and the originating application filed in the High Court NZ were heard concurrently. The hearing was facilitated by the use of video conferencing technology with each Court sitting in its own jurisdiction over a period of seven days.

25 The parties were represented by the same solicitors and counsel in each proceeding (save that there was an additional member of the Liquidators’ counsel team who only appeared in the NZ Proceeding) and relied on the same evidence and submissions in each proceeding. Where a witness was cross-examined, he gave an oath or affirmation in each proceeding. Rulings on objections were made by each Court depending on the location of cross-examining counsel. For example, if there was an objection to a question asked in cross-examination by counsel physically situated in the High Court NZ, Venning J sitting in that Court ruled on the objection and the ruling was, in effect, adopted by this Court. No party opposed this approach.

26 The Liquidators submit that it is important to all parties to avoid, so far as possible, inconsistency in the directions and/or judicial advice to be given by this Court and the High Court NZ and that the Courts have recognised this to be the case. They say that an “obvious tool” available for avoiding inconsistency is for the Courts to deliberate together and urged that to occur. In their oral closing submissions, the Liquidators went so far as to suggest that this Court and the High Court NZ might produce or adopt a joint or common set of reasons, drawing an analogy to judges delivering the reasons of an appellate court.

27 The defendants each supported the notion that the two Courts would deliberate together to achieve, so far as possible, consistency in the judicial advice and/or directions to be given.

28 Given what has occurred in the operation of Halifax AU and Halifax NZ (which is described below), including the uncontroversial fact that there is a deficiency in moneys held on trust for the benefit of clients of those companies and a commingling of funds, it is of some importance to the administration of Halifax AU and Halifax NZ, and to their creditors, that there be consistency in the approach of this Court and the High Court NZ.

29 In Westpac Banking Corporation v Lenthall (2019) 265 FCR 21, an application for leave to appeal and appeal were heard concurrently by a Full Court of this Court (Allsop CJ, Middleton and Robertson JJ) with a matter before the New South Wales Court of Appeal, BMW Australia Ltd v Brewster (2019) 343 FLR 176, at the same time and in the same court room. At [2] the Full Court said:

… The issues in the two matters overlapped considerably; and, given the importance of the questions, in particular of the Constitutional questions, it was thought convenient for the administration of justice that both Courts have the advantage of written and oral argument of counsel on the same occasion. Each Court would, of course, decide the matter before it according to the views of the judges constituting the Court. One party, BMW, raised concerns about the procedure and, in particular, objected to any discussion among or between judges from the two Courts about the issues. In light of this, a protocol was announced at the commencement of the hearing of the two matters that dealt with such matters as judges from either Court asking any counsel questions in argument. Each Court had the written submissions relied on in both matters. To the extent that evidence was relevant it was read by affidavit in each proceeding. The Courts informed the parties that, without the consent of the parties, the members of the Courts would not discuss the substance of the arguments or their views thereon with the judges from the other Court, or exchange drafts. No argument was heard on this question and whether this was a necessary or proper precaution. It is appropriate to say, however, that (subject to being persuaded to the contrary) we would not have considered that the kinds of considerations discussed in Re JRL; Ex parte CJL [1986] HCA 39; 161 CLR 342 (see especially the judgment of Mason J at 350–352) would have made such communications in any way inappropriate. As Mason J said at 351, a judge may consult another judge of his or her court who has no interest in the matter or other court personnel whose function is to aid him or her in carrying out his or her judicial responsibilities. In an integrated federal judicature, with two benches hearing two matters with overlapping issues in federal jurisdiction, it would be passing strange if a principle underpinning the fair, impartial and due administration of justice prevented discussions between the members of the Courts involved in deciding the cases, having just heard all the arguments in the same courtroom, as if the members of the bench of the other Court were strangers or third parties having private communications with the Court. It would go without saying that if any issue raised in such discussions had not been adequately ventilated, natural justice might require that some step be taken (just as it would if judges of the same court were to consider such a new issue to be relevant).

(Emphasis added.)

30 In this case no objection was taken to deliberation between the Courts. Indeed, as I have already observed, the parties consented to that course and, in the circumstances of this case and in light of the nature of this proceeding and the NZ Proceeding, it was an appropriate course to adopt. Accordingly Venning J of the High Court NZ and I engaged in discussions about the issues before each of the Courts for resolution and the arguments raised by the parties. However, in my opinion, it is not appropriate that the two Courts adopt or deliver one set of reasons. Unlike an appellate court, this Court and the High Court NZ are each exercising their own jurisdiction, according to the applicable legislative framework and law. It is necessary for each Court to reach its own conclusions and to express its reasons for doing so.

31 I turn then to consider the factual background against which the issues arise for resolution.

32 From 19 February 2003 to 7 January 2019 Halifax AU held an Australian Financial Services License (AFSL). Halifax AU’s AFSL authorised it to provide financial product advice on a range of financial products, deal in financial products and make a market for foreign exchange contracts and derivatives.

33 Halifax AU was not a licensed broker but facilitated the acquisition of shares by clients through an online broker and made a range of financial products available to clients. It had 16 employees prior to going into administration and provided administrative and treasury functions for its own operations and those of Halifax NZ.

34 Halifax AU conducted its business by way of the following trading platforms:

(1) an Interactive Brokers LLC (IB) trading platform known as Trader Workstation, referred to as Halifax AU IB platform or IB AU;

(2) MetaTrader4 (MT4) trading platform also known as Halifax Pro which was licenced by MetaQuotes Software Corp (MetaQuotes);

(3) from about 8 August 2016 MetaTrader5 (MT5) trading platform also known as Halifax Plus and which was also licenced by MetaQuotes; and

(4) from about 2009 to about July or August 2016 the Saxo trading platform.

35 As Halifax AU was not a market participant on the Australian Securities Exchange (ASX), its clients with accounts on the various trading platforms could access those platforms and place trades at their own discretion.

36 Halifax NZ held a Financial Service Provider’s Licence (FSPL) granted by the Financial Markets Authority (New Zealand) which authorised it to sell derivatives, including contracts for difference (CFDs), options, futures, margin foreign exchange contracts and non-derivative products including warrants and margin foreign exchange, equities and exchange-traded funds. Halifax NZ also acted as a broker for its clients in respect of various exchange-traded products including shares and warrants. Halifax AU was an authorised body under Halifax NZ’s FSPL.

37 Halifax NZ was not a market participant on any exchange. It was an introducing broker and, in that capacity, introduced prospective clients to Halifax AU for the purpose of financial products trading. Prior to Halifax NZ going into administration it had four employees who were principally involved in sales.

38 Halifax NZ conducted its business by:

(1) providing access for its clients and for clients of Halifax AU to the IB trading platform referred to as the Halifax NZ IB platform or IB NZ; and

(2) facilitating access for its clients to Halifax AU’s IB AU, MT4 and MT5 platforms.

39 Halifax NZ’s revenue was principally derived from commissions earned from trades placed by its clients, either on the IB NZ platform or as a result of the introduction of clients to the platforms operated by Halifax AU referred to in the preceding paragraph.

3.3 Products offered by Halifax AU and Halifax NZ

40 Clients of Halifax AU and Halifax NZ were able to trade in the following financial products:

(1) shares;

(2) warrants;

(3) CFDs;

(4) equity and index options;

(5) options on futures;

(6) futures; and

(7) foreign exchange.

41 In addition, clients of Halifax NZ could trade in mutual funds.

42 The financial products in which clients of Halifax AU and Halifax NZ could trade were either:

(1) exchange-traded financial products. That is, investments which are traded on a regulated exchange such as the ASX, New York Stock Exchange (NYSE) or London Stock Exchange (LSE), including shares, warrants, futures and options; or

(2) over the counter (OTC) financial products comprising derivatives which were not listed on a regulated exchange such as the ASX but traded via private contracts between two parties, in this case the client and either Halifax AU or Halifax NZ. The value of the contracts is derived from the price of the assets or products such as shares, precious metals and commodities.

43 Exchange-traded financial products were available for trading through the IB AU, IB NZ and MT5 platforms and OTC financial products were available for trading through the MT4, MT5 and IB NZ platforms.

3.4 The trading platforms explained

44 The MT4, MT5, IB AU and IB NZ platforms were operated in Australia by Halifax AU. Clients of Halifax AU and clients of Halifax NZ were able to trade on all of the platforms regardless of whether they had executed a client service agreement (CSA) with Halifax AU or Halifax NZ although, in order to trade on a particular platform, it was necessary for a client first to have set up and funded an account in connection with the relevant platform.

45 IB operates an online trading platform across a range of jurisdictions and provides access to multiple markets in approximately 24 different countries. The Trader Workstation is one of the platforms offered by IB. IB provided that platform to Halifax AU and Halifax NZ and, in turn, each of those entities provided their clients with access to the platform for trading.

46 The Trader Workstation or IB platform is a single trading platform. Each of Halifax AU and Halifax NZ separately contracted with IB to access and utilise it. These contracts remain in place although the platforms are now in “close only” mode; investors can close positions but cannot place new trades.

47 The IB AU platform enabled clients to trade in shares, warrants, equity and index options, futures and options on futures. The IB NZ platform enabled clients to trade in shares, warrants, foreign exchange, equity and index options, futures, options on futures, mutual funds and CFDs on shares.

48 Halifax AU and Halifax NZ operated a white label system with IB. This meant that all trades and data in relation to the IB AU and the IB NZ platforms were recorded as being held by IB for Halifax AU or Halifax NZ and not for the individual clients.

49 In relation to trades undertaken through the IB AU and the IB NZ platforms:

(1) IB charged a commission to Halifax AU or Halifax NZ, as applicable, which Halifax AU or Halifax NZ then on-charged with a mark-up or commission to the client undertaking the trade. The commission was automatically deducted for each trade. Some clients also paid for live data through subscriptions with IB which deducted a fee for that service;

(2) IB provided a range of reports to Halifax AU, Halifax NZ and their clients;

(3) IB used custodians and clearing brokers for trading stocks, options and futures in different countries; and

(4) the platform was not a virtual platform. All positions were exchange-traded, with the purchase of stocks or other financial products supported on a 1:1 basis by cash, stocks or other financial products.

50 Under their respective contracts with IB, Halifax AU and Halifax NZ each hold a consolidated account with IB, which I will refer to respectively in these reasons as the IB AU Consolidated Account and the IB NZ Consolidated Account. Each of the IB AU Consolidated Account and the IB NZ Consolidated Account is comprised of three types of accounts:

(1) IB AU Master Account (in the IB AU Consolidated Account) and IB NZ Master Account (in the IB NZ Consolidated Account) which each held a pool of funds from which amounts were paid into individual client sub-accounts (IB Client Sub-Accounts);

(2) IB Client Sub-Accounts in connection with each of the IB AU Consolidated Account and the IB NZ Consolidated Account which record the investments (cash, shares and other securities) held on behalf of clients on the IB AU and IB NZ platforms. Clients could log into their respective IB Client Sub-Account and execute a trade on the IB platform or they could instruct Halifax AU or Halifax NZ to access their IB Client Sub-Account and execute a trade on their behalf; and

(3) IB AU Prop Account and IB NZ Prop Account which purport to hold:

(a) revenue derived by Halifax AU and Halifax NZ from commissions and interest;

(b) in the case of the IB AU Prop Account:

(i) shares as hedges against MT5 client positions as well as dividend income generated from these shares; and

(ii) a cash balance (which may result from the realisation of assets held as hedges, or cash that was transferred into the IB AU Prop Account from the IB AU Master Account to ensure there was sufficient collateral to open new hedge positions as required).

However, as Mr Kelly explains, the IB AU Prop Account and IB NZ Prop Account were just accounting records which did not hold any shares or cash.

51 Until about late 2015 Halifax AU offered three types of IB Client Sub-Accounts to clients on IB AU: a cash account, a margin account and a portfolio margin account. These accounts were maintained by IB and recorded the transactions entered into by the client and the balance of the account. After late 2015, IB AU no longer offered margin or portfolio margin accounts for individuals applying for a new IB Client Sub-Account but individuals who already held such an account could continue to use them. After this change, individuals residing in Australia who wished to trade in stock CFDs had to do so on the MT4 or MT5 platforms.

52 Joseph Lum is a technical support officer employed by Halifax AU. From September 2008 to April 2015, and from January 2016 to November 2018, he worked in the online trading support team. Mr Lum describes each type of IB Client Sub-Account as follows:

(1) cash accounts – clients with cash accounts could trade in shares and certain types of options. They did not trade in CFDs. If a client with a cash account wanted to execute a trade, the client had to have sufficient cash in the account to cover the cost of the trade. Where the account balance approached a negative value positions automatically closed out, i.e. the shares were sold, to prevent the account balance going into negative. IB decided which open positions to close out automatically and, according to Mr Lum, usually closed out the most liquid shares or positions recorded in an account. Clients could set up their accounts to direct IB to sell certain shares last in the event of an automatic close out; and

(2) margin or portfolio margin accounts – these accounts had to satisfy margin requirements, set by IB, in order for the client to conduct trades. That is, they had to record a net asset value equivalent to a certain percentage of the total value of the trade. Clients with margin accounts on IB AU could trade in shares, options, futures, futures options and US bonds. Clients with margin accounts on IB NZ could trade in shares, options, stock CFDs, futures, futures options, foreign currency and US bonds. If the making of a new investment or a change in value of an existing investment would otherwise have caused the overall balance of a margin account or a portfolio account on IB AU to fail to meet IB’s margin requirements, sufficient open positions recorded in that account would automatically close out to remedy the margin violation. IB decided which open positions to close out automatically and, as was the case with cash accounts, clients could set up their accounts to direct IB what it should sell last in any automatic close out. The principal difference between a margin account and a portfolio margin account was that, for a portfolio margin account, a client was required to have a higher balance in the account, at least around USD100,000, before IB would approve the enabling of the portfolio margin setting.

53 Notwithstanding that assets were recorded in individual IB Client Sub-Accounts, the assets in the IB Client Sub-Accounts were, as set out at [50(2)] above, held by IB on behalf of Halifax AU or Halifax NZ. In turn, Halifax AU or Halifax NZ held their interest in the assets on behalf of their clients. Clients of Halifax AU and Halifax NZ did not have a contractual relationship with IB. They had a contractual relationship with either Halifax AU or Halifax NZ.

54 The investments currently held by IB on behalf of Halifax AU and Halifax NZ are largely shares and cash. Shares are held by IB on behalf of Halifax AU and Halifax NZ in the Client Sub-Accounts.

55 As set out above, the MT4 and MT5 software is owned by MetaQuotes which licences the trading platforms to Halifax Capital Markets, a related entity of Halifax AU. At the time the administrators were appointed, Halifax AU was the licensee of the MT4 and MT5 software. The licence was transferred to Halifax Capital Markets shortly thereafter in line with a transfer agreement signed prior to the administrators’ appointment. Notwithstanding the transfer, Halifax AU continues to pay the ongoing licence fees to MetaQuotes.

56 The software for the MT4 and MT5 platforms consists of a client and server component. The server component was run by Halifax AU and the client software was made available to clients who used it to see live streamed prices and charts, place orders and manage their accounts. The servers for the MT4 and MT5 platforms are hosted by oneZero, which also provides IT infrastructure to connect the MT4 and MT5 platforms to the IB AU Prop Account and to lnvast Financial Services Pty Ltd (lnvast) and Gain Capital (Gain), which are both hedging counterparties. Halifax AU pays a service fee to oneZero.

57 The MT4 platform has been operational within the Halifax group since at least April 2016 and the MT5 platform has been operational within the Halifax group since about 8 August 2016, following termination of the Saxo platform. The majority of Halifax AU clients on the Saxo platform were migrated to the MT5 platform.

58 The MT4 and MT5 platforms are described as “virtual” trading platforms. The MT4 platform enabled clients to engage in virtual trading in foreign exchange derivatives and CFDs on indexes, metals and commodities and the MT5 platform enabled clients to engage in virtual trading in the same products as well as shares.

59 When a trade was placed Halifax AU did not buy the asset but, rather, held the moneys paid by the client and recorded the profit or loss in the client’s account based on the movement in value of the asset. In relation to the MT5 platform the only assets acquired by way of trading on that platform, shares, were in fact acquired on the IB AU platform and any assets acquired by Halifax AU for the purpose of its hedging activities (as described below) were acquired on another platform, IB AU, Invast or Gain. That is, there was no cash movement in or out of the MT4 or MT5 platforms; the funds were, or should have been, held by Halifax AU in statutory trust accounts in accordance with its obligations under s 981B of the Corporations Act (see [124] below). This was a procedure which Halifax AU did not always follow. Moneys paid by New Zealand clients for trading on the MT4 or MT5 platforms could be transferred into a New Zealand statutory trust account maintained by Halifax NZ or a statutory trust account maintained by Halifax AU.

60 The values of the virtual positions on the MT4 and MT5 platforms were, depending on the nature of the position, referable to the price of an underlying product listed on an exchange (e.g. the ASX) or the price of an underlying currency on a currency market. When a client decided to close out his or her position, the client’s account balance would either increase or decrease depending on the difference in the price of the underlying asset when the position was opened and the price when the position was closed (resulting in debits or credits to each party depending on the profit or loss of each trade).

61 Mr Lum explains that once the MT5 platform became available to clients of Halifax AU and Halifax NZ (whose access to the MT5 platform was facilitated by Halifax NZ through Halifax AU), clients with accounts on the MT5 platform (MT5 Client Accounts) could invest in shares as well as other financial products. When shares were traded by a client on the MT5 platform they were recorded in that client’s MT5 Client Account (with a special code indicating the trade was in shares) as well as in the IB AU Prop Account; there was a “bridge” between the MT5 platform and the IB AU Prop Account which facilitated automatic acquisition or sale of the shares on IB AU. Because Halifax NZ facilitated investment by its clients on the MT5 platform (in shares and stock CFDs) through Halifax AU, the shares that were acquired by clients and recorded in the IB AU Prop Account related both to Halifax AU and Halifax NZ clients.

62 Clients could also trade stock CFDs on the MT5 platform. Halifax AU hedged all client trades in stock CFDs on the MT5 platform by acquiring on IB AU the shares the subject of a CFD position on the MT5 platform. This was done through the “bridge” noted above. The shares which were acquired to hedge stock CFD trades executed by clients were recorded in the IB AU Prop Account. The client’s MT5 Client Account recorded the acquisition of a share CFD. The shares which were acquired on IB AU when a client traded in shares on the MT5 platform or as a hedged trade when a client traded in stock CFDs on the MT5 platform were not recorded in the IB AU Prop Account as relating to a particular client. However, according to Mr Lum, trades recorded in the IB AU Prop Account either corresponding to a share trade or relating to a stock CFD trade on the MT5 platform could be identified by a manual process which would require matching up client positions on the MT5 platform with corresponding positions in the IB AU Prop Account.

63 Clients who used the MT4 or MT5 platforms were divided into two categories: A-Book clients and B-Book clients. Mr Lum explains that all clients were initially treated as B-Book clients but those who traded in shares and stock CFDs were considered to be A-Book clients for the purpose of those trades. Clients who engaged in FOREX trading or trading in index CFDs and had a history of making significant profits or were considered to be “risky”, because they traded in large volumes, were also classified as A-Book clients.

64 If an A-Book client placed a FOREX trade on the MT4 or MT5 platforms, Halifax would automatically place the same trade through a bridge maintained by oneZero on lnvast or Gain (see [61] above). If the A-Book client made money on the FOREX trade, Halifax also made money on the corresponding trade that it had placed on lnvast or Gain. Conversely, if the A-Book client lost money on the FOREX trade, Halifax also lost money on its corresponding trade.

65 Halifax AU hedged trades made by A-Book clients and virtual trades made through the MT5 platform in shares and stock CFDs so that it was not exposed to profits or losses for those trades.

66 Both the shares acquired by Halifax AU to hedge stock CFDs in respect of which clients transacted with it and also, as explained above, the shares acquired by clients by trading on the MT5 platform were acquired immediately on the IB AU platform because the MT5 platform linked automatically to the IB AU platform.

67 Halifax did not hedge the virtual trades entered into by B-Book clients. Those clients only made trades in foreign exchange, index CFDs, metals and commodities.

68 For all trades made on the MT4 or MT5 platforms, Halifax AU earned revenue through either commissions or margin spreads. For B-Book clients Halifax AU also earned profits when clients made losses on trades.

69 The assets acquired by Halifax AU in hedging trades as described in [66] above were held in Halifax AU’s name and recorded in the IB AU Prop Account (which, as noted at [50(3)] above, was just an accounting record and did not hold any shares or cash) without differentiating between trades by clients in shares and CFDs in shares. They were not recorded in the name of any specific Halifax AU client but as part of a pool of stocks and were assets held by IB on behalf of Halifax AU.

70 In the same way as set out at [64] above for FOREX trades, when Halifax AU hedged trades made by A-Book clients on the MT5 platform it simultaneously acquired the same position as the client trade. For example, if a client entered into a virtual position of 50 shares in company A on 1 January 2018, Halifax AU bought 50 shares in company A on the same date. The shares had a value referable to a price listed on an exchange e.g. the ASX. If the client decided to close his or her position on 30 June 2019, Halifax AU would also sell the shares referable to that position on that date. If the value of the shares had increased, the balance of the client’s account on the MT5 platform would record the price increase and the client could elect to redeem that amount in cash.

71 As set out at [50(3)] above, Halifax NZ also had an IB NZ Prop Account with IB. Like the IB AU Prop Account, the IB NZ Prop Account was just an accounting record and did not hold any shares or cash. Moneys for rebates received, which were commissions that Halifax NZ was entitled to be paid by its clients, and interest earned from IB were held in Halifax NZ’s name and recorded in the IB NZ Prop Account.

72 lnvast and Gain held a pool of money as collateral for the hedged trades made by Halifax AU, comprising funds transferred by Halifax AU to Invast or Gain and funds realised from Halifax AU’s positions on its hedged trades. At various points in time, depending on the movement of the trades, funds were transferred to or from Halifax AU to maintain an appropriate collateral level.

73 Each of Halifax AU and Halifax NZ had a form of CSA. The most recent versions of the Halifax AU CSA and the Halifax NZ CSA (for individuals) are dated 3 September 2018 and 8 July 2018 respectively.

74 The Halifax AU CSA is between Halifax AU, referred to as “we” or “us”, the client, referred to as the “Client” or “you”, and the guarantor. It sets out the basis on which Halifax AU will enter into transactions with the client and governs each transaction entered into or outstanding between the client and Halifax AU on or after the CSA comes into effect. Among other things, it:

(1) includes the following definitions in cl 1 “definitions and interpretation”:

Agency Transaction means a Transaction under which Halifax facilitates the Client’s instruction of an acquisition or disposal of a Quoted Financial Product through a third party broker. For clarity, Halifax will not be a party to such a Transaction and will not hold any legal or beneficial interest in any Financial Product in respect of such Transaction on trust for the Client.

…

Financial Product includes securities, derivatives, deposit and payment products, foreign exchange, government securities and other financial investment products whether traded on an eligible exchange or over-the-counter, as those terms are defined in the applicable legislation or as used by market convention.

…

Quoted in respect of a Financial Product means quoted for trading on a stock exchange.

…

Transaction means each transaction entered into, or proposed to be entered into, by the Client under this Agreement.

…

(2) under the heading “Agency Transactions” provides:

(a) The Client acknowledges that Halifax is not an ASX participant nor is it a participant of any other stock exchange. Any Agency Transaction entered into by the Client will be arranged by Halifax as agent for the Client, through a third party Broker. Halifax takes no responsibility for the performance by the Broker of the Broker’s obligations in respect of any Transaction. Halifax will not hold any financial products on trust for the Client. Halifax’s Australian financial services licence does not authorise it to provide custodial or depository financial services. Financial Products acquired on behalf of the Client will be held either in the Client’s name, or in the name of the relevant Broker (or its custodian), on behalf of the Client. The terms of the agreement with a relevant Broker is available from Halifax by request. The Client should carefully review their terms as they will govern the Client’s rights and obligations in respect of Agency Transactions made through the Broker. Halifax will have no responsibility for the Client’s obligations to settle any Agency Transaction.

(b) For each Agency Transaction, the Client appoints Halifax as the Client’s agent to:

(i) arrange, through the relevant Broker, a transaction in the Financial Products on behalf of the Client pursuant to the instructions of the Client, or otherwise in accordance with the terms of this Agreement; and

(ii) do all things reasonably necessary to perform this function and all things reasonably incidental to the performance of this function.

(3) under the heading “CFD Transactions, FX Transactions and FX Option Transactions” provides:

CFD Transactions, FX Transactions and FX Option Transactions will be governed by the provisions in Schedule 1, in addition to the other provisions of this Agreement. To the extent of any inconsistency between the provisions of Schedule 1 and the other provisions of this Agreement, Schedule 1 prevails in respect of CFD Transactions, FX Transactions and FX Option Transactions.

(4) provides for the payment of commissions, fees and expenses by the client to Halifax AU;

(5) sets out the circumstances in which a “Default Event” will occur. These include if “it becomes or may become unlawful for [Halifax AU] to maintain or give effect to all or any of the obligations under this [CSA] or otherwise to carry on its business or if [Halifax AU] or the Client is requested not to perform or to Close Out a Transaction (or any part thereof) by any Governmental Agency whether or not that request is legally binding”;

(6) provides for the steps that Halifax AU can take after a Default Event occurs. These include closing out or reducing the notional amount in respect of any or all of the client’s Transactions or closing out, exercising or abandoning any option not yet exercised; and

(7) includes in Schedule 1, which governs “CFD Transactions, FX Transactions and FX Option Transactions” (see (3) above):

(a) the following definition of “Termination Amount”:

Termination Amount means the amount calculated by Halifax in relation to all Open Transactions as the amount of Halifax’s exposure to the Client if those Transactions were Closed Out at the specified termination time, based on the then current market value for those Transactions as determined by Halifax. If the amount so calculated is an amount that would be owing to:

(a) the Client, then the Termination Amount is that amount expressed as a negative number; or

(b) Halifax, then the Termination Amount is that amount expressed as a positive number.

(b) clause 11.2 which concerns “net termination sum” and which provides that:

If Halifax has given notice of termination to the Client, neither Halifax nor the Client need make further payments or perform the obligations required of it under the terminated Relevant Transactions or the Account. Instead, this paragraph 11.2 governs the payments to be made and the obligations to be performed.

On the specified termination date, Halifax must calculate in the Account Currency for the Client for the relevant Platform(s) the value of the Termination Amount and the Account as at the termination date.

Halifax then determines a single net sum payable between the parties in respect of the terminated obligations by subtracting the value of the Account from the Termination Amount.

If the resulting net amount is positive then the Client must pay this to Halifax on the date on which Halifax notifies the Client of the amount payable. The other provisions of this Agreement (including Halifax’s right to set off under paragraph 11.1(c)) apply to this amount.

If the resulting net amount is negative then Halifax agrees to pay this amount to the Client.

Halifax agrees to notify the Client of the result of those calculations as soon as practicable after making those calculations. The Client’s obligation to make any payment is not conditional on receiving any further information in relation to those calculations, or being satisfied with those calculations. Payments due under this paragraph must be made not later than 2 Business Days after Halifax gives this notice.

75 The Halifax NZ CSA is between Halifax NZ, the nominated client, referred to as Client, and each person named as a guarantor. Among other things, it:

(1) includes the following definitions:

Financial Product includes securities, derivatives, deposit and payment products, foreign exchange, government securities and other financial investment products whether traded on an Exchange or over-the- counter, as each of those terms are defined in the applicable legislation or as used by market convention.

…

Transaction means trading in the Financial Products described in the Client Details Form and such other Financial Products as may be agreed between Halifax NZ and the Client from time to time.

(2) under the heading “Appointment” provides:

a. The Client appoints Halifax NZ as its agent to:

i. enter into the Transactions on behalf of the Client;

ii. do all things reasonably necessary to perform the Transactions; and

iii. do all things reasonably incidental to the performance of the Transactions.

(3) under the heading “Other governance considerations” provides:

The Client and Halifax NZ agree that the terms of their relationship in respect of derivatives contracts, and any dealings between them concerning derivatives contracts, are subject to, and that they are bound by, the Financial Markets Conduct Act 2013, the Derivatives Issuer Licence, the NZX Operating Rules and the procedures, customs, usages and practices of NZX and its related entities, as amended from time to time, in so far as they apply to derivatives contracts.

(4) under the heading “Trusts and Segregated Accounts” provides, among other things:

The Client agrees and acknowledges the following:

a. All money and property deposited by the Client with Halifax NZ, or received by Halifax NZ on behalf of the Client, will, if required by law, be deposited in a trust account or client segregated account by Halifax NZ and held in accordance with applicable legal requirements.

(5) provides for the Client to pay to Halifax NZ commission, fees and certain taxes, costs and expenses.

3.6 Product disclosure statements

76 There were a number of product disclosure statements (PDS) issued by Halifax AU in the period January 2008 to April 2018 and by Halifax NZ in 2015 and 2016 in evidence. With the exception of the PDS issued on 30 January 2008 by Halifax AU, they relate to derivative products.

77 The most recent Halifax AU PDS in evidence was issued by Halifax AU with effect from 4 April 2018 for CFDs and foreign exchange (FX) products. It describes Halifax AU as the issuer of the CFD and FX products referred to in the PDS and as an entity which carries on a financial services business in accordance with its AFSL authorised to provide advice, dealing and making a market to retail and wholesale clients in derivatives which include CFDs and FX products.

78 The PDS sets out the key features of the financial products it covers namely CFDs, and FX products, which are OTC products including:

(1) a description and the key features of a CFD including that:

A CFD is an agreement by which you can make a profit or loss from changes in the market price, value or level of the relevant Underlying Product. The Underlying Product is usually an exchange-traded share or other security or a market index, commodity, bond or interest rate. The holder of a CFD does not own, or have any indirect interest in or right to, the Underlying Product. Because the value of the CFD is (in part) derived from the value of the Underlying Product, a CFD is a derivative financial product.

And:

A CFD offered by us is a financial product in the form of an agreement between you and us to trade the difference arising from movements in the price, value or level of an Underlying Product.

(2) a description and the key features of margin FX products including:

A Margin FX product is an agreement by which you can make a loss or a profit from movements in the level of an Exchange Rate for different currencies and/or precious metals (referred to as the Underlying Exchange Rate).

And:

A Margin FX product offered by us is a financial product in the form of an agreement between you and us to trade the difference arising from movements in the level of an Underlying Exchange Rate.

Margin FX transactions can either be FX transactions or metal transactions. The differences between the two are explained in the PDS;

(3) a description and the key features of FX options including:

Option contracts traded over Margin FX are referred to as FX Options. The buyer of an FX Option pays a Premium in exchange for the right, but not the obligation, to enter into a Margin FX Transaction with the seller at a predetermined Exchange Rate (called the Exercise Rate) on the Expiry Date.

And:

The key features of an FX Option are as follows.

(a) Call and Put Options: An FX Option is either a Call Option or a Put Option. From the buyer’s viewpoint, an FX Option that is:

(i) a Call Option gives the buyer the right, but not the obligation, to buy or enter long a Margin FX Transaction at the prescribed Exercise Rate in return for payment of a Premium; and

(ii) a Put Option gives the buyer the right, but not the obligation, to sell or enter short a Margin FX Transaction at the prescribed Exercise Rate in return for payment of a Premium.

The seller only has a right to a premium in return for which it accepts an obligation to sell or enter short, in the case of a call option, or to buy or enter long, in the case of a put option, a margin FX transaction at the exercise rate of the FX option if the FX option is validly exercised by the buyer;

(4) the risks of trading in the CFDs and FX products offered by Halifax AU. Among other things, it provides that the client will have a counterparty risk and thus an exposure to Halifax AU in relation to each transaction and that, while Halifax AU relies to a significant extent on hedging to manage its exposure, to the extent it does so it acts as principal and not as the client’s agent. It also notes that if Halifax AU becomes insolvent it may not be able to meet its obligations to the client in full or at all and that there may be considerable delays before the client is able to access the amount, if any, that it is able to recover;

(5) margin requirements noting that because CFD and FX products are subject to margin obligations, clients must have a sufficient balance in their account for security/margining purposes. Details of the two components of the margin requirement that a client is required to pay, the initial margin and the variation margin, are described;

(6) in relation to dealing with a client’s money that moneys paid in connection with any CFDs or FX products offered by Halifax AU will generally be subject to the Clients’ Money Rules which provide that clients’ money held by Halifax AU is taken to be held in trust by it for the benefit of its client and is required to be paid into an account maintained with an Australian bank or other authorised deposit taking institution. Relevantly, the PDS also provides: