Federal Court of Australia

Mastronardo v Commonwealth Bank of Australia [2021] FCA 443

ORDERS

Appellant | ||

AND: | COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 TRADING AS BANKWEST Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The appeal be dismissed.

2. The appellant pay the respondent’s costs, as agreed or taxed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GRIFFITHS J:

1 This appeal is from a judgment and orders of the Federal Circuit Court of Australia (FCCA), which are reported as Commonwealth Bank of Australia trading as Bankwest v Mastronardo [2020] FCCA 2614 (primary judgment). The FCCA declined to adjourn the hearing of a creditor’s petition concerning the appellant and it proceeded to make an order under the Bankruptcy Act 1966 (Cth) that his estate be sequestrated.

2 There is a long history in the dispute between the appellant, some of his family members and the respondent Bank, which I will broadly outline below.

3 In the present proceeding, by a further amended notice of appeal dated 12 March 2021, the appellant abandoned some of his previous grounds of appeal. He confined the appeal to the finding of the primary judge at [90]-[91] of the primary judgment that parts of an unfiled Proposed Cross-Claim in separate proceedings in the Supreme Court of New South Wales relating to the appellant’s guarantee of certain loans were not reasonably arguable. It will be necessary to summarise those parts of the Proposed Cross-Claim which relate to certain guarantees, but it is sufficient to note at this point that they could fairly be described as secondary to the primary thrust of the Proposed Cross-Claim, which concerned claims that the respondent had engaged in unconscionable conduct. The Proposed Cross-Claim was substantially similar to a proposed amended cross-claim which the appellant’s father (Antonio Mastronardo) intended to file in the same NSW Supreme Court proceeding, save that Antonio sought damages for trespass/conversion relating to the sale of his mortgaged properties by receivers.

4 The grounds of appeal which have been abandoned by the appellant (Adrian Mastronardo) in the present proceeding all related to those claims of unconscionability. The appellant has now confined his appeal to the primary judge’s finding, and reasons for finding, that the proposed claims based on the discharge of loan guarantees were not reasonably arguable.

Broad summary of background matters

5 As mentioned, the appeal forms part of a long running dispute between members of the Mastronardo family, companies which were related to the family and the respondent Bank. That history includes my judgment in Via Sanantonio Pty Ltd v Commonwealth Bank of Australia [2019] FCA 58, where I declined to set aside bankruptcy notices against the appellant’s father (Antonio) and Adrian’s wife (Claudia Mastronardo). The Full Court dismissed an appeal from that judgment in Mastronardo v Commonwealth Bank of Australia [2019] FCAFC 127.

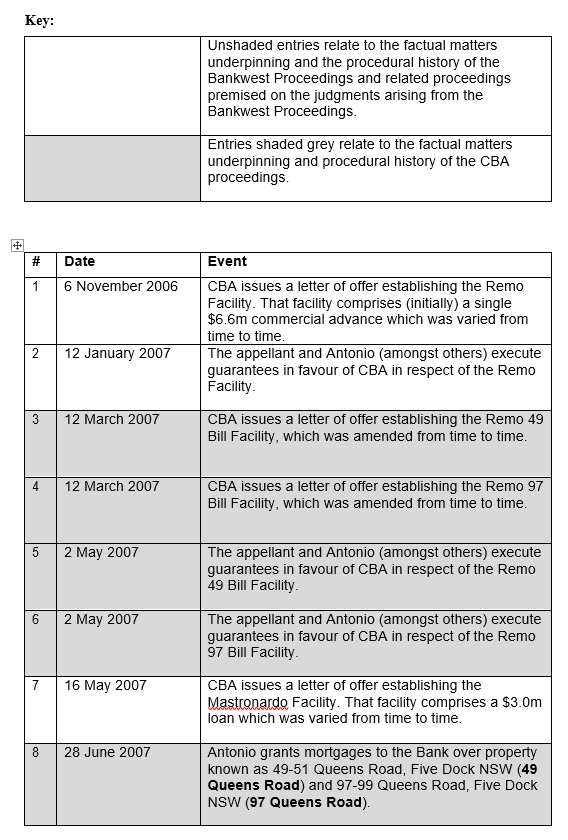

6 On 28 March 2013, the Bank commenced proceedings in the NSW Supreme Court against Antonio and Adrian and a company called Remo 97-99 Queens Road Pty Ltd (deregistered) in which it sought to recover damages under guarantees given by Antonio and Adrian. Those proceedings had the file number 2013/95636 (CBA Proceedings).

7 On 21 March 2014, Adrian and Claudia (and a related company) commenced separate proceedings in the NSW Supreme Court against the Bank. These proceedings were given the file number 2014/86502 (Bankwest Proceedings). The plaintiffs’ primary claims were for damages in contract for the Bank’s alleged repudiation of a provision for the release from its security of certain real property and damages based on a claim that the Bank’s conduct was unconscionable. The Bank cross-claimed seeking money judgments and for orders for possession of real properties held as security in respect of certain facilities.

8 On 21 December 2015, Antonio filed a cross-claim in the CBA Proceedings. No cross-claim was filed by Adrian (see [12] below). Antonio’s cross-claim alleged that the Bank purported to execute the mortgages to which his guarantees applied without first having made any demand upon him and at a time when he was not in default. Antonio contended that the Bank’s premature actions constituted a breach of various express and implied terms of his two guarantees and resulted in him being discharged from those guarantees. He sought damages in trespass/conversion relating to the sale of his properties by the Receivers.

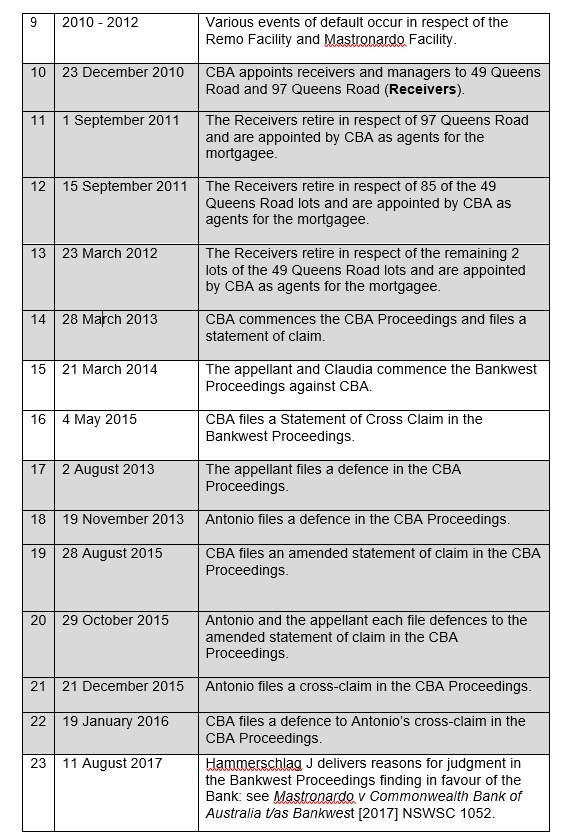

9 On 11 August 2017, Hammerschlag J delivered reasons for judgment in the Bankwest Proceedings. The plaintiffs’ claims were dismissed and the Bank’s cross-claim was upheld (see Mastronardo v Commonwealth Bank of Australia Trading as Bankwest [2017] NSWSC 1052). Money judgments against Adrian and Claudia were entered in the Bank’s favour as guarantors of the obligations to the Bank of Remo Corporation Pty Ltd (in liq) under a series of facilities. On 14 September 2017, Adrian and Claudia sought leave to appeal Hammerschlag J’s judgment. That application was unsuccessful (Mastronardo v Commonwealth Bank of Australia Ltd [2018] NSWCA 136). An application by Adrian and Claudia for special leave to appeal that judgment of the NSW Court of Appeal was unsuccessful (Mastronardo v Commonwealth Bank of Australia [2018] HCASL 361).

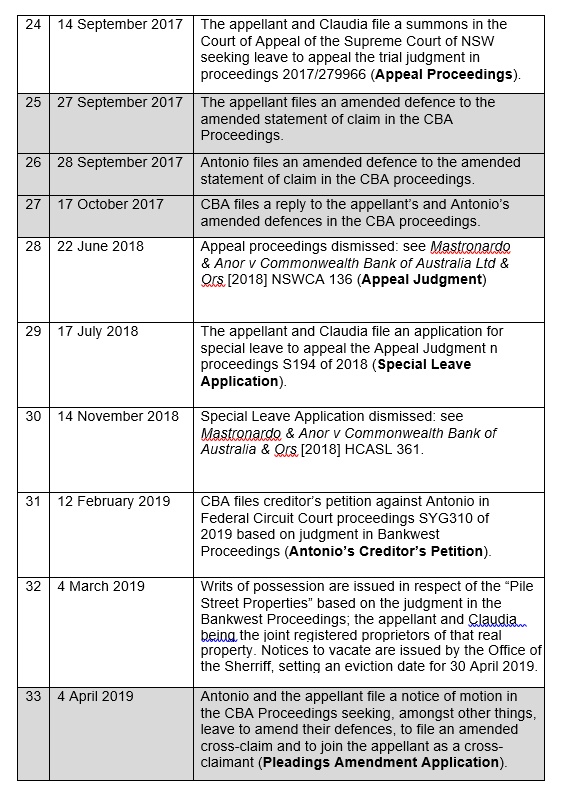

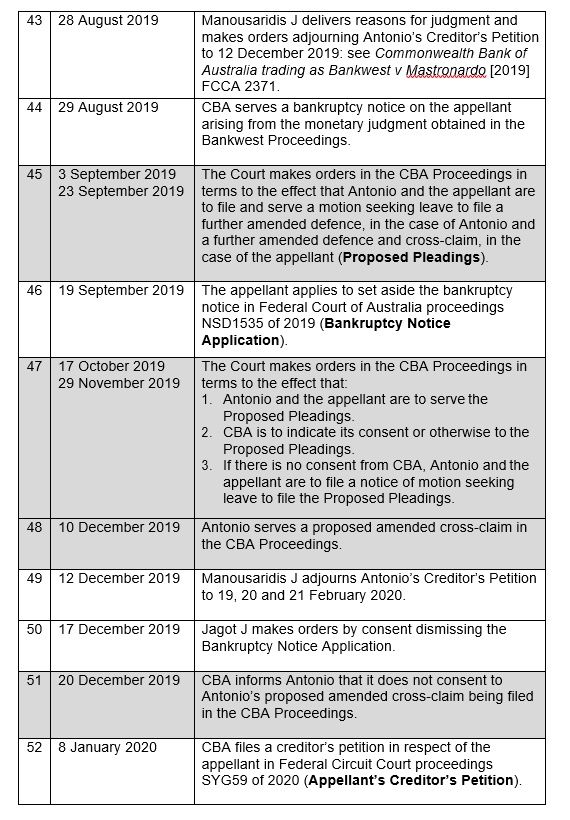

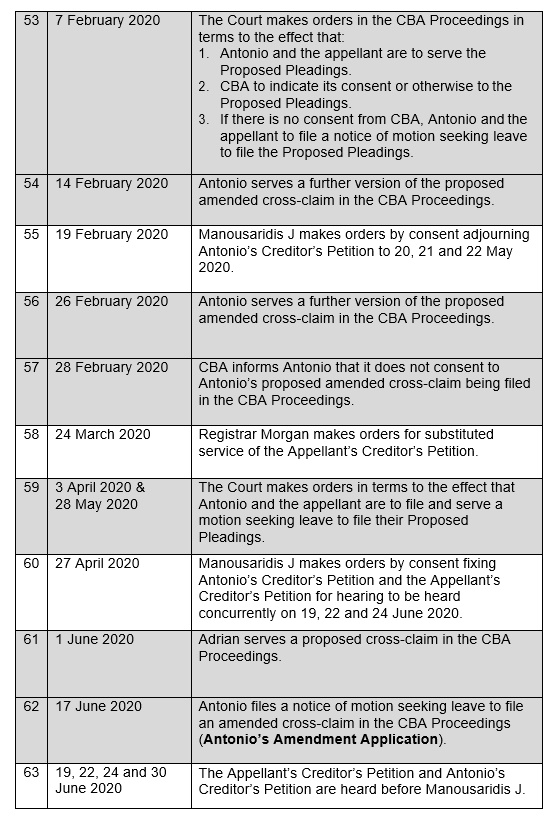

10 During the period from early January 2016 to mid-February 2021, the parties to the CBA Proceedings filed or sought to file multiple amended pleadings. The parties were also involved in numerous interlocutory applications (see the annexed Chronology prepared by the Bank for more details). On 4 April 2019, Adrian and Antonio filed a notice of motion in the CBA Proceedings seeking leave to file an amended cross-claim and to join Adrian as a cross-claimant (Pleadings Amendment Application). The Pleadings Amendment Application was dismissed by Fagan J on 7 May 2019 (Commonwealth Bank of Australia v Remo 97-99 Queens Road Pty Ltd [2019] NSWSC 510). As Fagan J observed at [2], this was the first occasion on which Adrian had sought to raise a cross-claim notwithstanding that the proceedings had been on foot for over six years. The Pleadings Amendment Application included a proposed amended cross-claim which included, for the first time, claims by Adrian for damages based upon alleged breach of implied terms of guarantee, misrepresentation, misleading or deceptive conduct and unconscionable conduct (see [19] at Fagan J’s reasons for judgment). Justice Fagan gave detailed reasons why he would not permit the cross-claim to be amended to raise Adrian’s claim. They included a finding that Adrian had failed to articulate a viable case on breach of an implied obligation of good faith (at [22]); other deficiencies in the pleadings relating to implied terms (at [23]-[25]); failure to plead a viable misrepresentation case (at [27]); the proposed misrepresentation case was founded upon a misrepresentation which was alleged in terms of “profound uncertainty” (at [28]); and the same defect affected the proposed case concerning unconscionability (at [29]). Justice Fagan added at [32] that the Proposed Cross-Claim did not particularise the damages claimed by either Antonio or Adrian.

11 In rejecting an application by Antonio and Adrian to file affidavits which would outline the case the Bank would have to meet under the Pleadings Amendment Application, Fagan J said at [33] that this was unacceptable having regard to all the deficiencies in the draft pleadings, which deficiencies went beyond “a mere lack of particularity”. His Honour described the amendments as failing to allege viable cross-claim causes of action, however particularised. Further, at [34], his Honour said that it was incumbent on Antonio and Adrian clearly to articulate any additional cross-claim causes of action having regard to the belated raising of those matters. His Honour noted the lengthy procedural chronology of the litigation, which dated back to 2013.

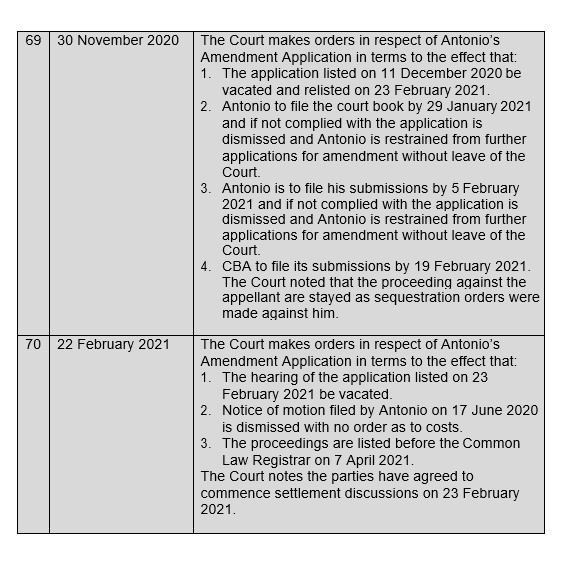

12 Adrian failed to file a cross-claim in the CBA Proceedings notwithstanding that there were multiple consent orders made in those proceedings during the period 29 July 2019 to 28 May 2020 providing him with an opportunity to do so.

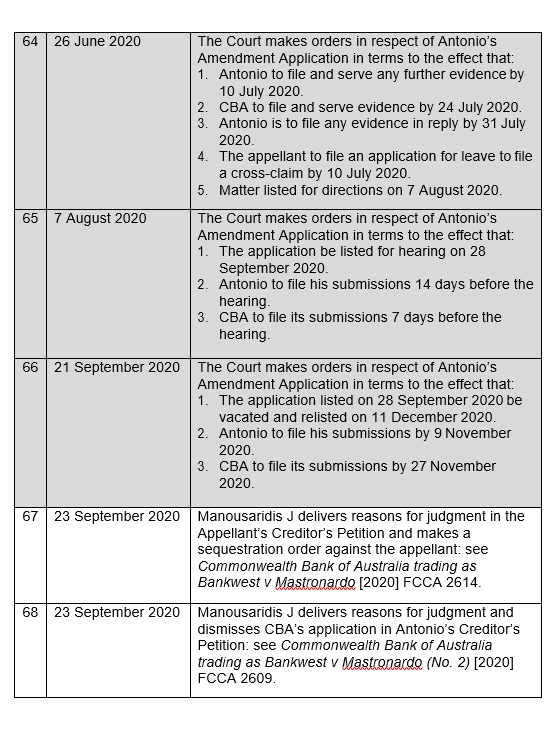

13 On 20 August 2019, the FCCA heard the creditor’s petitions against Antonio and Claudia. On 28 August 2019, the primary judge delivered his reasons for judgment in Commonwealth Bank of Australia Trading as Bankwest v Mastronardo [2019] FCCA 2371. The primary judge found that Antonio had a reasonably arguable case that his liabilities under two guarantees had been discharged and that he had a reasonably arguable claim against the Bank for money had and received in relation to an amount of approximately $24.5m (which is the amount obtained by the Receivers on the sale of two properties). Although the primary judge found that he could not find that it was likely that Antonio would succeed in his cross-claim, he considered that the cross-claim was of sufficient substance to warrant it being litigated in the ordinary course in the NSW Supreme Court. Accordingly, his Honour adjourned the hearing of the creditor’s petition in relation to Antonio to 12 December 2019, on condition that Antonio prosecute his cross-claim in the NSW Supreme Court with reasonable dispatch.

14 The primary judge declined to adjourn the hearing of the creditor’s petition relating to Claudia. His Honour made an order of sequestration of Claudia’s estate under the Bankruptcy Act.

15 Later, in December 2019, the FCCA noted that Antonio had not progressed in any substantial way his Proposed Cross-Claim in the CBA Proceedings. Accordingly, the FCCA proceeded to hear the creditor’s petitions against both Antonio and Adrian at a four day hearing commencing on 19 June 2020. At the commencement of the hearing below, each of Antonio and Adrian tendered a Proposed Cross-Claim, which were in substantially identical terms. Both Antonio and Adrian said that they intended to file the Proposed Cross-Claims in the CBA Proceedings.

16 The bankruptcy notice relating to Adrian was in the amount of approximately $12.5m, which represented the difference between the judgment debt obtained by the Bank against Adrian in the Bankwest Proceedings, less an amount recovered by the Bank after the judgment was entered. The creditor’s petition in the present proceeding arises from the Bankwest Proceedings. The bankruptcy notice relating to him was issued on 29 August 2019 and the date of Adrian’s act of bankruptcy is 15 October 2019. The creditor’s petition relating to Adrian was filed on 8 January 2020.

17 On 23 September 2020, the FCCA published separate reasons for judgment (Commonwealth Bank of Australia Trading as Bankwest v Mastronardo (No 2) [2020] FCCA 2609) for its conclusion that, having regard to Antonio’s Proposed Cross-Claim and other material in the CBA Proceedings, Antonio was likely to succeed in his proposed trespass claim. Accordingly, it was likely to be held that he was entitled, if he so elected, to recover an amount of approximately $24.5m representing the proceeds of sale of the properties sold by the Receivers, less just expenses of sale. Accordingly, the primary judge decided to exercise his discretion under s 52(2)(b) of the Bankruptcy Act in favour of not making a sequestration order. The FCCA declined to dismiss the creditor’s petition against Antonio.

18 In his reasons for judgment relating to Antonio, the primary judge explained why he concluded that it was likely that at the trial of Antonio’s Proposed Cross-Claim, he would be held to be entitled to elect to claim as to his remedy for the invalid appointment of the Receivers an order that the Bank account to him for the proceeds of sale of the two mortgaged properties (see at [127]-[129]). This conclusion related to that part of Antonio’s Proposed Cross-Claim which raised a claim in trespass based upon implied terms in Antonio’s guarantees, the invalid appointment of the Receivers and the Receivers being in wrongful possession of the two properties. No reliance was placed on Antonio’s unconscionability case.

19 On the same day as the FCCA published those reasons for judgment relating to Antonio, it published separate reasons for judgment in respect of Adrian (see Commonwealth of Bank of Australia Trading as Bankwest v Mastronardo [2020] FCCA 2614). This is the primary judgment for the purposes of the present appeal. As noted above, Adrian relied upon an unfiled Proposed Cross-Claim in the CBA proceeding which was in substantially similar terms to Antonio’s, except that it did not make any claim for charges for trespass/conversion, presumably because Adrian did not own the mortgaged properties. The primary judge held that the claims made by Adrian in his unfiled Proposed Cross-Claim did not constitute a “sufficient cause” to warrant either adjourning the hearing or dismissing the creditor’s petition relating to Adrian. I will summarise below the primary judge’s reasons for taking a different view concerning the prospects of Adrian’s Proposed Cross-Claim, as opposed to Antonio’s.

Summary of key features of dispute between Mastronardo family and the Bank

20 It is desirable to now provide a broad outline of the relevant features of the commercial dispute between the Mastronardo family and the Bank. This summary of the background facts, which are not in dispute, draws heavily on the primary judge’s description of them both below at [16]-[52] and in other proceedings in the FCCA, as referred to above.

21 In around 2005 Adrian and Antonio became partners in a property development business which they carried on through Remo Corporation Pty Ltd (Remo).

22 From 2005, Remo, through subsidiary companies, was involved in the development of two sites, one at 49 Queens Road, Five Dock, and the other at 97-99 Queens Road, Five Dock. Remo 49 Pty Ltd undertook the development of 49 Queens Road (49 Queens Road Property), and Remo 97 Pty Ltd undertook the development of 97-99 Queens Road (together, Queens Road Properties). Antonio was the registered proprietor of the Queens Road Properties.

23 By letter dated 12 March 2007, the Bank offered Remo 49 a bill line facility of up to $26 million (Remo 49 Facility).

24 By a separate letter dated 12 March 2007, the Bank offered Remo 97 a bill line facility of up to $9 million (Remo 97 Facility).

25 On 2 May 2007, Adrian executed two deeds of guarantee in favour of the Bank, under which he guaranteed the obligations of Remo 49 and Remo 97 respectively. Antonio also gave similar guarantees.

26 By letter dated 29 June 2007 (shortly after Antonio granted mortgages to the Bank over the Queens Road Properties) the Bank offered to increase the amount of the Remo 49 Facility to $27.6 million. Remo 49 accepted the variation on 16 July 2009.

27 In around August 2007, another company, Ashe Morgan Capital No. 2 Pty Limited (AMW), agreed to lend $5 million to Remo 49 and Remo 97. That led to AMW, Remo 49, Remo 97, and the Bank entering into a deed of priority and subordination.

28 In around October 2008, in response to the global financial crisis, Adrian and Antonio formulated a new strategy for the 49 Queens Road Property which consisted of redesigning the four level office block into small strata title office suites or units, and increasing the building’s gross floor area. Antonio estimated that these changes would increase the costs of the development by around $4.3 million.

29 By letter dated 19 December 2008, the Bank offered to increase the Remo 49 Facility from $27.6 million to $31.9 million. By letter dated 25 June 2009, the Bank offered to increase the Remo 49 Facility to $34.7 million.

30 In July 2009, there was an exchange of correspondence as to the implications of the $2.8m increase in the Remo 49 Facility for the deed of priority. It is unnecessary to detail that correspondence.

31 By letter dated 17 July 2009, the Bank offered to increase the Remo 49 Facility from $31.9 million to $34.7 million.

32 By 14 October 2010, the Bank and AMW entered into a dispute regarding priority.

33 By two letters dated 10 December 2010, one addressed to Remo 49 and the other addressed to Remo 97, the Bank claimed that Remo 49 and Remo 97 were in default of the Remo 49 Facility and the Remo 97 Facility. The Bank claimed that Remo 49 and Remo 97 owed it $32,863,492.40 and $9,834,482.50 respectively, and demanded that Remo 49 and Remo 97 pay these amounts by 17 December 2010.

34 Both Antonio and Adrian contended that neither received any formal demand to enforce the guarantees for the debts of Remo 49 and Remo 97.

35 Neither Remo 49 nor Remo 97 met the demands.

36 On 29 December 2010, Adrian was told that the Bank had appointed Receivers to the Queens Road Properties.

Relevant parts of the primary judgment summarised

37 As noted above, Adrian contended at the commencement of the hearing before the FCCA on 19 June 2020 that he intended to file the Proposed Cross-Claim in the CBA Proceedings. Although the primary judge found that there was sufficient cause in Antonio’s case to adjourn the hearing of the creditor’s petition against him, the primary judge declined to do so in Adrian’s case.

38 In circumstances where Adrian has confined his appeal to those parts of the primary judgment which relate to the discharge of his obligations under the guarantees, it is sufficient to set out [90] and [91] of the primary judgment, which relate to that matter:

90. The Proposed Cross Claim alleges that because of the appointment of the Receivers Adrian was discharged from his obligations under the guarantees he had given. That is not reasonably arguable. The appointment of Receivers was directed to property owned by Antonio and could not reasonably be characterised as the purported enforcement of the guarantees Adrian had granted. On the evidence before me, it is not reasonably arguable that the Bank took, or purported to take, any action under the guarantees Adrian granted before the Bank made a demand under the guarantees by letter dated 13 January 2013.

91. In any event, even if the appointment of the Receivers discharged Adrian from his obligations under the guarantees he granted, that would not have given rise to any claim for damages against the Bank; and if it did, there is no evidence that is reasonably capable of proving that Adrian suffered the damages the Propose (sic) Cross Claim alleges he suffered.

39 The primary judge’s reference at the end of [91] to there being no evidence reasonably capable of proving that Adrian suffered the damages claimed by him in the Proposed Cross-Claim implicitly refers to the primary judge’s reasons at [85]-[89] where his Honour explained why he concluded that there was no evidence which was reasonably capable of supporting the damages assuming that the Bank had engaged in unconscionable conduct. In brief, the primary judge concluded that Adrian had not established that there were reasonably arguable prospects of recovering damages in an amount that would equal or exceed the debt relied upon by the Bank in the creditor’s petition. The primary judge summarised the relevant parts of the Proposed Cross-Claim relating to damages. Particular reference was made to the claim that Adrian had suffered a loss in the amount of $7.5m because the effect of the appointment of the Receivers was that it prevented companies associated with Adrian from obtaining finance to complete two projects (namely developments at West Ryde and North Strathfield). The primary judge concluded at [88] that there was simply no evidence which was reasonably capable of supporting these claims in the Proposed Cross-Claim. His Honour referred to Adrian’s affidavit dated 1 June 2020, which purported to proffer some evidence in support of the claim for damages, but the primary judge concluded that the affidavit simply asserted matters without any supporting evidence. He described Adrian’s claim for damages as being “based on nothing more than bare assertions”.

The further amended notice of appeal

40 As noted above, Adrian did not press any grounds in the further amended notice of appeal relating to his claim that the Bank engaged in unconscionable conduct. Thus, grounds 1, 2, 8 and 9 were not pressed. In addition, Mr McDonald (who appeared for Adrian) said that ground 4 is to be read as being limited to Adrian’s case relating to the guarantees (i.e. only paragraph 4(a) was pressed). It is convenient to set out grounds 3, 4, 6 and 7 of the further amended notice of appeal (tracked to show amendments):

3. His Honour erred in finding, in paragraph 56 of the decision below, that it was not enough for a debtor to produce a pleading in another proceedings, without evidence or other material sufficient to show that it is reasonably arguable or of substance, to and constitute an "other sufficient cause" for not making a Sequestration Order.

4. His Honour erred in finding that the appellant's applicant's unconscionable conduct claims made in the proposed Cross-Claim did not have any substance or any sufficient substance to warrant either adjourning the proceedings until such time as the Cross-Claim is determined in the ordinary course or the proceedings be dismissed and did not give adequate or due consideration to, or sufficient substantial consideration to the following matters of fact or law in the Decision:

a. that the Guarantee provided by the appellant in the Supreme Court proceedings had been discharged because the bank had sought to enforce the guarantees without first making a demand on the appellant applicant;

b. that the Bank engaged in conduct in relation to financial services within the meaning of the law;

c. that the appointment of the Receivers without a demand was not a breach of contract, and further that the bank's but whose conduct in doing so was unconscionable in which the bank took advantage of the appellant's vulnerable position and there was enough evidence to support a claim of unconscionable behaviour by the bank;

d. that the appointment of the Receivers “was contrary to the Hold Safe Representations” referred to in paragraph 69 of the Decision and there was enough evidence to support a claim of unconscionable behaviour by the bank;

e. that the purported exercise of its rights by the Bank, when where it was not entitled to do so, was not a breach of contract and could support a claim for unconscionable conduct;

f. that the conduct of the Bank of “repeatedly” extending the date of repayment by increasing the amount of the loan under the facilities with less time to pay and build a larger development led to was an expectation being held by the Appellant and his father and related entities, sufficient to constitute unconscionable conduct. This expectation would be reasonably capable of supporting a finding that it rendered the appoint of receivers as unconscionable conduct by the Bank;

g. that it the appointment of the Receivers was contrary to the “common intention” referred to in paragraphs 79-81 of the Decision; and

h. that the conduct of the Bank to extricate itself from the dispute between the Bank and the second mortgagee (Ashe Morgan) supports the claim that the appointment of the Receivers constituted unconscionable conduct as referred to in paragraph 82 of the Decision and his Honour erred in rejecting this argument.

5. His Honour erred in finding that the proposed Cross-Claim did not have any substance, or any sufficient substance at paragraph 89 of the Decision or did not disclose a reasonably arguable case at paragraph 90 of the Decision. that by appointing the Receivers the Bank engaged in unconscionable conduct in the circumstances supported by the evidence filed in the Supreme Court Proceedings and the evidence in support of the proceedings in the same court of SYG310/2019. It was an order of the court that the evidence in one matter would be evidence in the other case.

6. His Honour erred in rejecting the Appellant's claim for damages was based on nothing more than bare assertions referred to in paragraphs 85-89 of the Decision.

7. His Honour erred in rejecting the proposition that the appointment of the Receivers discharged the appellant's Applicant's obligations under the Guarantee which he granted and which would give rise to a claim for damages against the bank referred to in paragraphs 90-91 of the Decision.

The appellant’s contentions summarised

41 In brief, Adrian contended that the primary judge erred in not being satisfied for the purposes of s 52(2)(b) of the Bankruptcy Act that his claim relating to the guarantees was of sufficient substance such that the creditor’s petition in relation to him should have been adjourned until such time as the validity of the cross-claim was determined or, alternatively, the creditor’s petition should have been dismissed. He contended that the primary judge devoted insufficient consideration to the “release of guarantee” grounds and failed to give proper or due consideration to that part of Adrian’s case. Adrian did not dispute the correctness of the principles identified by the primary judge, but contended that those principles had been misapplied.

42 In his outline of written submissions, Adrian identified the following components of his Proposed Cross-Claim as being relevant to the appeal (footnotes omitted):

33. The Appellant submits that, in respect of the issues on this appeal, they are best addressed collectively, on the basis of that the relevant components of the Proposed Cross Claim, are:

a. The Appellant and his father carried on business as property developers and would make the profits from one project available to the next.

b. The Queens Road project, being the Remo 49 and Remo 97 projects, (which are the subject of the loans guaranteed by the Appellant and his father) was one of the projects of the above business.

c. The “Third Guarantee”, given by the Appellant related to the Remo 49 project

d. The “Fifth Guarantee”, given by the Appellant related to the Remo 97 project

e. The ability of the Appellant and his father to continue the property development business was dependent on the successful completion of the Queens Road project.

f. The purpose of the Appellant entering into the above guarantees was to facilitate the above successful completion.

g. It was an implied and essential term of the above guarantees that the Bank had a duty to respect the terms of the Mortgage (from Antonio) and not exercise any powers under it, unless it was entitled to do so.

h. Further, was an implied and essential term of the above guarantees that the Bank had a duty of good faith to act, inter alia, with regard to the Appellant’s interests.

i. Further, was an implied and essential term of the above guarantees that the Code of Banking Practice would apply and the Bank would follow that Code.

j. The Bank appointed Receivers under the Mortgages and at the time, inter alia, Antonio had not been given any demand and was not in default under the Mortgages.

k. The Receivers were not validly appointed and were not entitled to possession of the properties which made up the Queens Road project.

l. By appointing the Receivers in the above circumstances, the Bank breached the “duty to respect the terms of the Mortgage” terms, the “duty of good faith with regard to the Appellant interests” term and the Code of Banking Practice.

m. As a result of the above breaches, the Bank discharged the Appellant from the guarantees, or repudiated the guarantees.

n. Further, as a result of the above breaches (and those pleaded by Antonio in his Statement of Claim), the Bank was not entitled to sell the properties of Antonio which made up the Queens Road Project, nor enter into subsequent Appointment Deeds.

43 With reference to the primary judge’s finding at [91], namely that even if Adrian had been released from his guarantees this would not have given rise to any claim for damages against the Bank and, even if it did, there was no evidence which was reasonably capable of proving that Adrian suffered the damages alleged in the Proposed Cross-Claim, Adrian contended that the primary judge did not require further evidence of loss or damage. This was because there was a finding in the reasons for judgment published on 23 September 2020 concerning Antonio at [127] that it was likely that Antonio would be held to be entitled to an order that the Bank account to him for the proceeds of sale of the mortgaged properties by the Receivers, being an amount of approximately $24,400,000 less just expenses of sale.

44 Alternatively, Adrian contended that there was evidence below to support his claim for damages, as set out in [205]-[251] of the Proposed Cross-Claim. This evidence was said to include Adrian’s affidavit of 1 June 2020 and evidence including third party feasibility studies.

45 In his written Reply, Adrian acknowledged that he had not filed the Proposed Cross-Claim in the CBA Proceedings. But he added that his evidence was that a notice of motion had been filed in the CBA Proceedings seeking leave to file the Proposed Cross-Claim and the notice of motion was due to be heard in the NSW Supreme Court during the period of the four day hearing in the FCCA. He said that he never abandoned his Proposed Cross-Claim.

46 Adrian also contended that the primary judge failed to appreciate the business relationship which he had with his father, which gave rise to “a conflation of their dealings with the bank”. He pointed to the pleaded implied terms within the guarantees as set out in the Proposed Cross-Claim, including that it was an implied term of the guarantees that the Bank had a duty to respect the terms of the mortgages from Antonio and not exercise any powers unless it was entitled to do so. Adrian pointed to the primary judge’s findings at [88] and [127] in the reasons for judgment relating to Antonio, that it was likely that Antonio was not in default within the meaning of the mortgages. Consequently, there was no entitlement to appoint the Receivers and it was likely that Antonio might obtain an order that the Bank account to him for the proceeds of the sale of the two properties, less just expenses of sale. Adrian contended that only “very small steps” were required for the primary judge in these circumstances to hold that, being partners in a property development business, Adrian also had a bona fide claim that the Bank was liable to account to him as a partner of Antonio and for the same amount, which would exceed the balance of the Bankwest Proceeding debt due to the Bank.

47 Adrian indicated that he was willing to be subject to strict conditions regarding the prompt prosecution of his Proposed Cross-Claim.

48 In oral address, Mr McDonald described the essence of the appeal as being that Adrian wished to “piggyback” on Antonio’s success. He said that the primary judge erred in not finding that, because of the close business relationship between Adrian and Antonio and their involvement in property developments as joint venturers or business partners, Adrian would be entitled to a share of the $24.5m to which Antonio was entitled in the circumstances as outlined at [18] above.

The respondent’s submissions summarised

49 To avoid adding unnecessarily to the length of these reasons for judgment, I will not summarise the Bank’s contentions. They are substantially reflected in my reasons for dismissing the appeal.

Consideration and resolution of the appeal

50 I accept the Bank’s submission that Adrian’s argument on the appeal essentially distils to the following propositions: because Antonio was successful in his arguments, which are not available to Adrian, and because Antonio had a separate and distinct claim for damages in the CBA Proceedings, and despite the unassailable judgment debt owed by Adrian to the Bank, the Court should have adjourned the creditor’s petition to allow Adrian to progress his Proposed Cross-Claim, which he had not done for several years and which, even if successful, would not satisfy his liability to the Bank arising from the Bankwest Proceedings.

51 The primary judge was exercising a discretion in both refusing to adjourn the hearing of the creditor’s petition and in making the sequestration order (Barton v Malcolm Johns Legal Pty Ltd (No 2) [2015] FCA 166 at [34] per Gleeson J). Mr McDonald accepted that this meant that, for Adrian’s appeal to succeed, he needed to establish an error on the part of the primary judge within the ambit of the principles in House v R (1936) 55 CLR 499 at 504-505. This requires him to demonstrate that the primary judge acted upon a wrong principle, or allowed extraneous or irrelevant matters to guide or affect him, or took a mistaken view of the facts, or did not take into account some material consideration. If it does not appear how the primary judge reached the result embodied in the Court’s orders, Adrian needs to establish that, on the facts, the primary judge’s decision is unreasonable or plainly unjust, such that the appeal Court may infer that in some way there has been a failure by the primary judge to exercise his discretion properly.

52 As Beach J concluded in Liang v LV Property Investments Pty Ltd [2015] FCA 1057 at [59], there is an important distinction between a cross-claim which is likely to succeed and a cross-claim which is bona fide and reasonably arguable, but where it is not established by the judgment debtor that it is likely to succeed. Where it is established that a cross-claim is likely to succeed, such a claim may warrant the refusal of a sequestration order whereas, in the latter case, the appropriate course may be to adjourn the creditor’s petition and not refuse a sequestration order at that time.

53 A similar distinction was drawn by Lehane J in Re Ling; Ex parte Enrobook Pty Ltd (1996) 142 ALR 87 and, more recently, by Jackson J in Williams (formerly Turco) v Mortgage Ezy Australia Pty Ltd [2020] FCA 1567 at [28].

54 It is also relevant to note what Beach J said in Liang at [61] and [62]:

61. It is important to emphasise that a judgment debtor does not establish a bona fide and reasonably arguable claim by merely producing a statement of claim in a separate proceeding or by pointing to such litigation or indeed by bare assertion; Ms Liang’s position falls into that last category. There must be sufficient evidence or other material to show that it is reasonably arguable or of substance. This may require prima facie verification of the key factual elements as well as demonstrating legal tenability.

62. Finally and separately, a decision to adjourn a hearing constitutes an exercise of a court’s discretion. An appellant bears a heavy onus in establishing that the exercise of such a discretion has miscarried. A court will be reluctant to interfere with the exercise of such a discretion.

55 Mr McDonald did not contend that the primary judge had erred in his identification and understanding of the relevant principles. The appeal was said to relate to the application of those principles. For the following reasons, the appeal should be dismissed.

56 First, no error has been demonstrated in relation to the primary judge taking a different view as to the strength of Adrian’s Proposed Cross-Claim as opposed to that of Antonio. The primary judge’s favourable assessment of the strength of Antonio’s trespass/conversion claim under his Proposed Cross-Claim ultimately related to the two mortgages which Antonio had given to the Bank over the Queens Road Properties and the implied terms of the guarantees Antonio had given. The primary judge found that, upon the proper construction of those mortgages and two guarantees given by Antonio, there was an implied term that the Bank had to make a demand before it could appoint receivers under either mortgage. In the absence of any demand, the appointment of the Receivers would be invalid, Antonio would be discharged from his obligations under the guarantees and the Receivers would not have been entitled to sell the Queens Road Properties. In these circumstances, the primary judge said that it was likely that Antonio would be entitled to an order that the Bank account to him for the proceeds of the sale of the mortgaged properties, less just expenses of sale. Antonio’s legal rights as mortgagor were critical to the primary judge’s reasoning in respect of his case.

57 As the primary judge made clear at [90] of the primary judgment relating to Adrian, his position was very different. That is because Adrian’s contention that he was discharged from his obligations under the guarantees he had given was not reasonably arguable in circumstances where the appointment of the Receivers was directed not to any property owned by Adrian, but to properties owned and mortgaged by Antonio.

58 Moreover, his Honour correctly found at [90] that the appointment of the Receivers could not reasonably be viewed as the purported enforcement of the guarantees Adrian had granted. This was so because, even on Adrian’s own case as pleaded in the Proposed Cross-Claim, no demand had ever been given to him in respect of the guarantees. No error has been identified in respect of the primary judge’s finding at [90] that, on the evidence before the FCCA, it was not reasonably arguable that the Bank took any action under Adrian’s guarantees.

59 Secondly, I do not accept that the primary judge fell into appealable error within the House principles by not applying the same reasoning to Adrian as he did to Antonio regarding the alleged implied terms. Mr McDonald spent some time in oral address taking the Court to various parts of Adrian’s Proposed Cross-Claim which pleaded implied terms in the guarantees Adrian had given. He submitted that the primary judge’s error was to not take into account relevant parts of the Proposed Cross-Claim relating to Adrian’s implied terms argument. After drawing the Court’s attention to the implied pleaded terms at [70] and [72] of the Proposed Cross-Claim, Mr McDonald took the Court to [162] in which it was pleaded that when the Bank appointed the Receivers, it did so without making any demand upon either Antonio or Adrian and that the mortgages had not become enforceable. It was claimed in [163] that this involved the Bank breaching the Conditions Precedent as referred to in [60] and [61]. At [164] it was pleaded that, in the circumstances referred to in [162] and [163], the Receivers were not validly appointed or entitled to take possession of the Queens Road Properties. Paragraph 165 of the Proposed Cross-Claim addressed the alleged breach of the implied terms in the mortgages. It is in the following terms:

Adrian repeats the facts and matters referred to in paragraphs 162 and 163 above and says further that, in the circumstances there referred to, the Bank breached the Implied Terms of the Mortgages referred to in paragraph 69 above.

Particulars

Adrian repeats and relies upon the particulars referred to in paragraph 162 and 163 above.

60 As the Bank pointed out, it is difficult to see any sound legal basis for the pleading in [165], which relates to mortgages involving Antonio and the Bank and not Adrian.

61 When asked by the Court to point to any material which indicated that the implied terms argument now advanced by Mr McDonald had been put to the primary judge in Adrian’s case, Mr McDonald frankly acknowledged that there was no such material and he was not in a position to say that the point had been run below. The outline of written submissions which had been filed in the proceeding below on behalf of both Antonio and Adrian (a copy of which was in evidence in the appeal) contains no reference to any such argument having been put to the primary judge in Adrian’s case. In the events that occurred, Adrian represented himself at the hearing before the primary judge commencing on 19 June 2020. A transcript of any closing oral submissions made by him was not included in the appeal papers. Accordingly, there is no evidence to suggest that the implied terms argument was ever put to the primary judge in Adrian’s case.

62 It is not easy to understand how the primary judge could commit a House error in not addressing a case which evidently was never put. Ground 4 is rejected.

63 Thirdly, ground 3 of the further amended notice of appeal must be dismissed. As Beach J pointed out in Liang at [61] (see [54] above), a judgment debtor does not establish a reasonably arguable claim merely by producing a pleading in a separate proceeding and, in order to show that a claim is reasonably arguable and is one of substance, verification of the key factual elements may be required. It was plainly open to the primary judge to adopt a similar approach.

64 Fourthly, I reject grounds 6 and 7 of the further amended notice of appeal, which focuses upon the issue of damages. As to ground 6, which contends that the primary judge erred in concluding at [85]-[89] of the primary judgment that Adrian’s claim for damages was based on nothing more that bare assertions, Mr McDonald frankly and correctly acknowledged that this indeed was the case. He then added, however, that there was no need for Adrian to adduce evidence of his loss or damages because it was open to him simply to rely on his entitlement to share in any damages obtained by Antonio because of their business relationship. That contention must be rejected. Nothing in the evidence indicated that Adrian had a legal right to any part of damages which Antonio might obtain as a result of his claim in trespass. A document dated 8 August 2009 and entitled “Separation – Term Sheet” fell far short of providing such evidence. In particular, the statement in paragraph 5 of that document that Adrian and Antonio had agreed that “profits and or loss incurred from [the Queens Road Projects] and the group of Remo Corporation to be shared 50% /50% between Adrian and Antonio” could scarcely apply to any damages Antonio obtained under his Proposed Cross-Claim.

65 Moreover, the primary judge did not err when he found at [91] of the primary judgment that if the appointment of Receivers had the effect of discharging Adrian from his obligations under the two guarantees he had granted, this would not give rise to any claim for damages by him against the Bank. Even if it did, as Mr McDonald frankly acknowledged, there was simply no evidence which established any damages on Adrian’s part.

Conclusions

66 For these reasons, the appeal will be dismissed, with costs.

I certify that the preceding sixty-six (66) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Griffiths. |

Associate:

ANNEXURE: BANK’s Chronology

Dramatis personae and defined terms | |

Adrian | means Carmelo Adriano Mastronardo, the appellant |

Antonio | means proceedings commenced by Adrian and Claudia against CBA trading as Bankwest in Supreme Court of New South Wales proceedings number 2014/86502. |

CBA | means Commonwealth Bank of Australia ACN 123 123 124, the respondent. |

CBA Proceedings | means proceedings commenced by the CBA against Remo 97-99 Queens Road Pty Ltd (deregistered), Antonio and Adrian being Supreme Court of NSW proceedings 2013/95636. |

Claudia | means Claudia Alejandra Mastronardo, the wife of Adrian (now a bankrupt). |

Mastronardo Facility | means the loan facility established pursuant to a letter of offer dated 16 May 2007 issued by CBA (accepted in writing on 21 May 2007), as varied from time to time, pursuant to which Adrian and Claudia were borrowers, with Antonio and Remo (amongst others) guarantors. |

Remo | means Remo Corporation Pty Ltd (ACN 117 341 796) (deregistered), the borrower in respect of the Remo Facility. |

Remo 49 Bill Facility | means the loan facility established pursuant to the Better Business Bill Facility – Variable Rate No. 134 292 between the Commonwealth Bank of Australia ACN 123 123 124 and Remo 49 Queens Road Pty Ltd (deregistered) and dated 12 March 2007. |

Remo 97 Bill Facility | means the loan facility established pursuant to the Better Business Bill Facility – Variable Rate No. 134 171 between the Commonwealth Bank of Australia ACN 123 123 124 and Remo 97- 99 Queens Road Pty Ltd (deregistered) and dated 12 March 2007. |