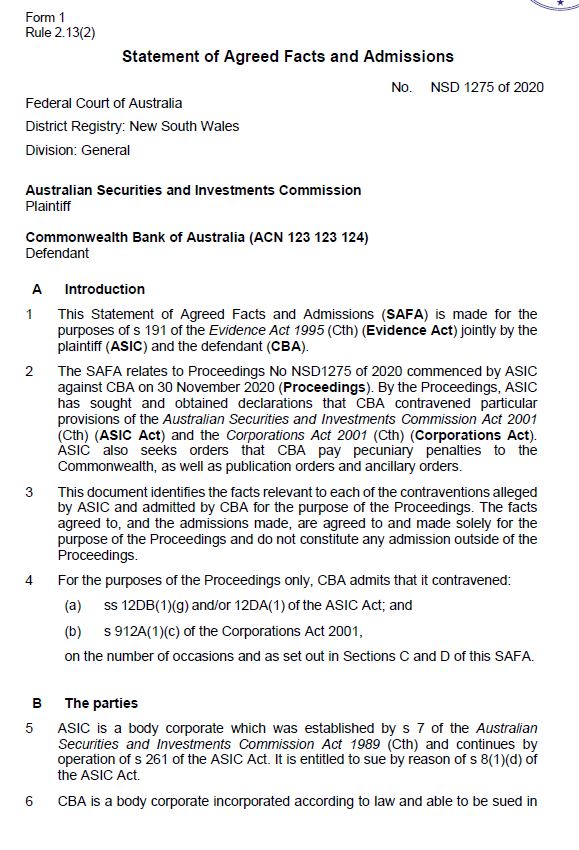

Federal Court of Australia

Australian Securities and Investments Commission v Commonwealth Bank of Australia [2021] FCA 423

ORDERS

AUSTRALIAN SECURITIES & INVESTMENTS COMMISSION Applicant | ||

AND: | COMMONWEALTH BANK OF AUSTRALIA ACN 123 123 124 Respondent | |

DATE OF ORDER: | 6 March 2021 |

THE COURT ORDERS THAT:

1. Pursuant to s 12GBA(1) of the Australian Securities and Investments Commission Act 2001 (Cth), within 30 days, CBA is to pay to the Commonwealth of Australia a pecuniary penalty of $7 million.

2. The proceeding be listed for a further case management hearing at 9.30am on 28 April 2021.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

(Revised from the Transcript)

LEE J:

A Introduction

1 This is a proceeding brought for the imposition of a pecuniary penalty by the Australian Securities and Investments Commission (ASIC). More particularly, ASIC seeks declarations of contraventions of the Australian Securities and Investments Commission Act 2001 (Cth) and the Corporations Act 2001 (Cth), pecuniary penalty orders and ancillary orders, including costs.

2 In a manner which has characterised its constructive and helpful approach to the conduct of this litigation, at the first case management hearing, the respondent (CBA) informed the Court that it admitted the facts and allegations contained in ASIC’s concise statement (subject to an irrelevancy that need not detain us) and did not oppose the making of declarations on 12 February 2021 to the following effect:

THE COURT DECLARES THAT:

1. By provision of a periodic account statement with an Interest Summary Error, and in all the circumstances, on 12,119 occasions during the period 1 December 2014 to 31 March 2018 inclusive, CBA represented to a customer in trade or commerce that the interest rate that had been applied upon overdraft facility borrowings over the date range referred to in the statement was the interest rate shown in a notation to the statement (Representations), which representations were each:

a. a false or misleading representation with respect to the price of services, in contravention of s 12DB(1)(g) of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act); and

b. misleading or deceptive conduct, or conduct that was likely to mislead or deceive, in relation to financial services, in contravention of s 12DA(1) of the ASIC Act,

in that the interest rate actually charged was greater than that referred to in the applicable Representation.

2. On each occasion that CBA contravened ss 12DA(1) and 12DB(1)(g) as referred to above, CBA breached its general obligation as a financial service licensee to comply with financial services laws in contravention of s 912A(1)(c) of the Corporations Act 2001 (Cth).

3 I was prepared to make those declarations, and it was a licit exercise of Chapter III judicial power to do so, because I was satisfied on the basis of the matters specified in the concise statement and facts agreed that there was a proper factual and legal basis for the granting of that remedy. Accordingly, these reasons deal with the balance of the relief sought by ASIC concerning the applicable penalty and related orders.

4 The principal object of a pecuniary penalty is to attempt to put a price on a contravention that is sufficiently high enough to deter repetition by the malefactor and by others who might be tempted to contravene. Given this, it might be thought in a case such as the present, that there is a degree of tension between two well-established principles.

5 The first of these principles is that the size of a corporation alone does not justify a higher penalty than might otherwise be imposed: see Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2015] FCA 330; (2015) 327 ALR 540 (at 559–60 [89]–[92] per Allsop CJ).

6 The second of these principles is that where the penalty does not impose a sting or burden on the contravener, it is less likely to achieve the deterrent effect that is the raison d’être of its imposition: see Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2018] HCA 3; (2018) 262 CLR 157 (at 195–6 [116] per Keane, Nettle and Gordon JJ).

7 Although not part of this tension, there is a further important principle that arises squarely in the circumstances of this case. That is, there is an important public policy involved in promoting the predictability of outcomes in civil penalty proceedings, which encourages corporations to acknowledge contraventions: see Australian Competition and Consumer Commission v Apple Pty Ltd (No 4) [2018] FCA 953 (at [6] per Lee J). Such acknowledgements assist in avoiding lengthy and complex litigation and hence diminish demand on the public resources constituted by both the Court and the regulator. Although in the circumstances of this case we are not dealing with an agreed penalty, it is this underlying principle which was the foundation of the High Court’s comments in Commonwealth of Australia v Director, Fair Work Building Industry Inspectorate [2015] HCA 16; (2015) 258 CLR 482 (at 507 [57] per French CJ, Kiefel, Bell, Nettle and Gordon JJ) that in civil proceedings there is generally very considerable scope for the parties to agree on the facts and upon the consequences, and there is also very considerable scope for them to agree upon the appropriate remedy and for the Court to be persuaded of the appropriate remedy.

8 Prior to the hearing, I was assisted by comprehensive and thoughtful submissions filed on behalf of both ASIC and the CBA. The thoroughness of those submissions, the exchange today at the oral hearing, and the high degree of cooperation in agreeing upon relevant facts, has allowed me to proceed immediately to the delivery of judgment.

B The Relevant Facts

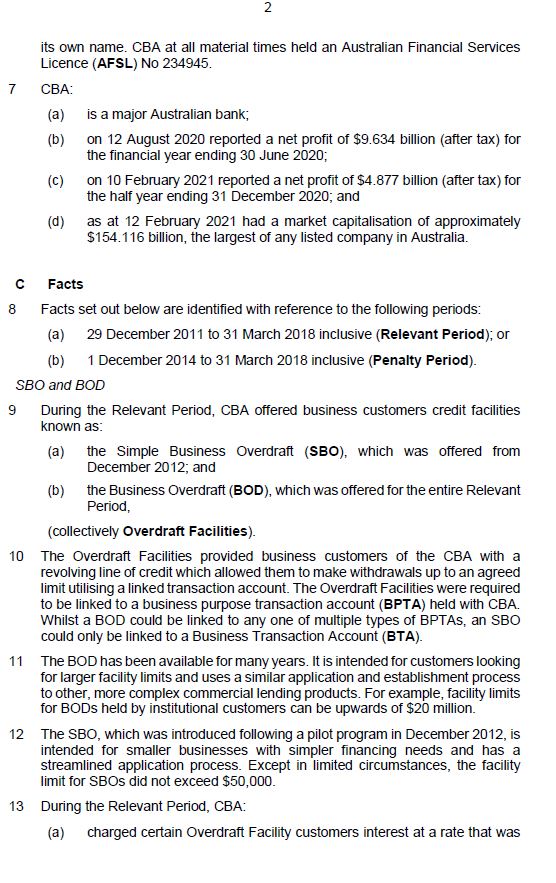

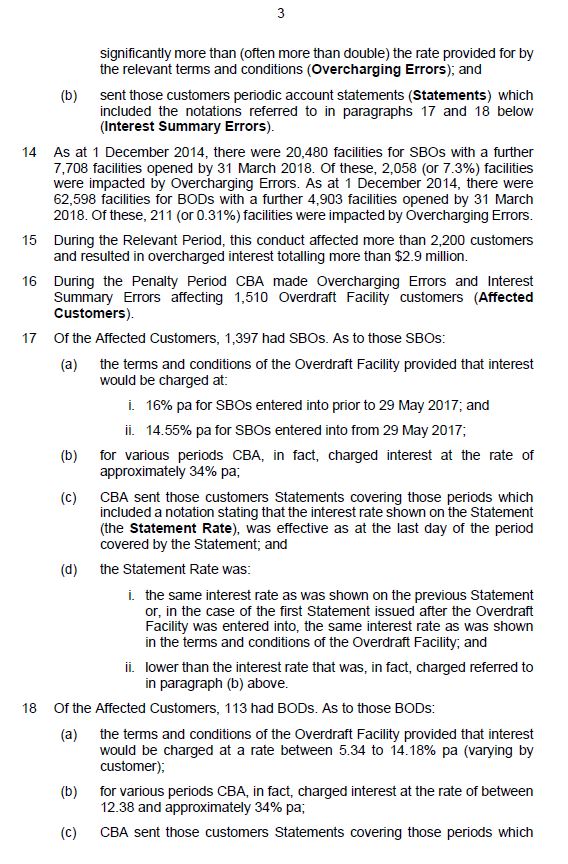

9 Admitted pursuant to s 191 of the Evidence Act 1995 (Cth) was a statement of agreed facts and admissions. This document was marked Exhibit A in the proceeding and is reproduced at Annexure A to these reasons. I find for the purposes of this proceeding the facts identified at [5]–[59] of Exhibit A.

10 Without any criticism, one aspect of what has occurred that seems to me to be of great significance, being the chronology of events, does not emerge with great clarity from Exhibit A. It is worth focusing on an aspect of that chronology.

Month | Description |

December 2011 | Due to a coding defect, the CBA started charging certain overdraft facilities customers interest at a rate that was significantly more than (often more than double) the rate provided for by the relevant terms and conditions (Overcharging Errors) and sent those customers statements which did not reflect the correct position concerning interest. The overdraft facilities to which Exhibit A makes reference were managed by different business units within the CBA and involved two products, namely: (a) the Simple Business Overdraft (SBO); and (b) the Business Overdraft (BOD). |

August 2013 | The Overcharging Errors in relation to the SBOs were first identified by the CBA at this time after the CBA had received an enquiry from an SBO customer regarding the amount of monthly debit interest that had been charged on the customer’s account the previous month. During this month, the CBA conducted investigations which indicated that two separate interest rates had been applied to the SBO account. Further, manual checking of randomly selected accounts identified that the same issue had occurred in relation to one other account. At this stage, there was evidence that there was a problem. |

October 2013 | At this time, the CBA implemented a monthly manual process aimed at identifying and removing incorrect pricing before it affected any SBO or BOD account, and it was assumed by the CBA that this process was sufficient. |

November 2013 | What was described as a CBA “internal incident management team” identified that not only SBOs but also BODs were impacted by the coding defect and that this had been occurring since late 2011 in relation to certain BODs. Hence, by November 2013 it appears that the broad scope of the difficulty had been identified. |

May 2015 | By this time a coding change to the system had been implemented which was directed at ensuring that the correct interest would be charged, and there was certain testing undertaken. |

January 2016 | It became apparent through the receipt of customer complaints that the Overcharging Errors were apparently still occurring, and a couple of months later further changes were made. Subjectively, the CBA considered that the changes made by this time had resolved the issues causing the Overcharging Errors. |

June – July 2016 | A complaint was made by a customer to the Financial Ombudsman Service (FOS) that interest had been overcharged on her SBO account, and the following month the issue was “escalated” to Mr Clive Van Horen, Executive General Manager Retail Products in the Retail Banking Services business unit of the CBA. This, it appears, was the first time that the Overcharging Errors and the bank’s receipt of amounts representing interest to which it was not entitled had been made apparent to an officer within the CBA of some seniority. |

September 2016 | For reasons that are not apparent on the evidence, it was not until September 2016 that the investigation was managed as “a high priority” with regular reviews being held, and the CBA became aware that there were ongoing difficulties, with a consequence that the matter was escalated to the CBA’s Executive Committee. |

November 2016 | During a long period of further investigation, as set out in Exhibit A (at [49]), the CBA belatedly commenced a customer remediation programme which, at the request of the FOS, was the subject of regular reporting, and which ultimately involved the payment of $3.74 million (including interest on the overcharged amount) being paid to the customers that had been overcharged until it was completed in March 2019. |

March – May 2018 | It was only in March 2018 that a revised table identifying matters of misconduct was provided to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. Following this, in May 2018, the CBA submitted a breach report to ASIC in relation to the Overcharging Errors. The CBA had not taken this step prior to this time as it had considered that it was not in breach of s 912D of the Corporations Act, because, inter alia, the BODs and SBOs were apparently considered not to be “financial products”, the Overcharging Errors did not amount to any breach of the financial services laws, and the CBA personnel who had reviewed the decision five years previously had formed the view that it was “not sufficiently significant to warrant reporting”. |

11 In my view, a few conclusions should be drawn from this chronology.

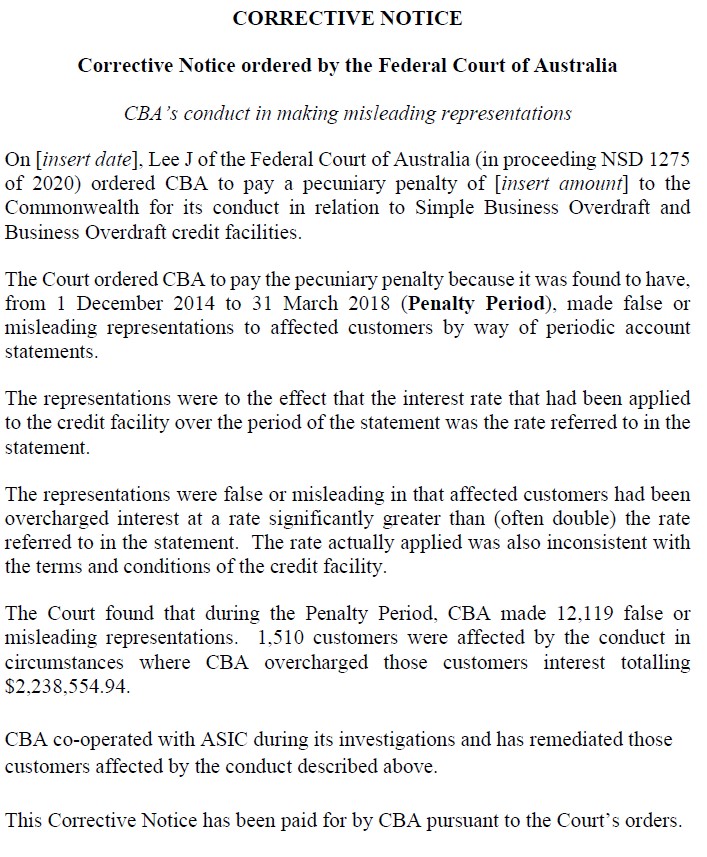

12 First, the overcharging originally occurred not as a result of any sort of deliberate decision to procure the payment of moneys to which the CBA was not entitled, but, rather, due to an unfortunate systems error.

13 Secondly, when the problems first became apparent, and for a very considerable period thereafter, persons within the CBA were content to not take steps to notify customers that had been affected and, notwithstanding that they were aware the CBA was holding onto money to which it was not entitled, were content to let the matter rest. The matter was not further addressed until a customer had actually taken the step of making a complaint.

14 Thirdly, even when the complaint was raised, the reaction of the CBA remained tardy and wholly inappropriate, until the matter had been escalated by a further complaint to the FOS, at which time finally someone with a degree of seniority became involved.

15 Fourthly, after a further period of time elapsed, a remediation programme was finally put in place.

16 Given the way that I have drawn these threads out of the chronology, no doubt, it would already be evident that I regard this conduct, which I will describe as the CBA delay, as both serious and reflecting poorly upon those that were aware the bank was holding onto money to which it was not entitled. Indeed, this was not a case of any complexity – even the most junior member of the bank apprised of all the relevant details would be aware of the fundamental relationship between a bank and its customer and the premise that a customer is likely to take a statement given to them by the bank at face value. Further, the customer is likely to be influenced by matters such as the Banking Code of Practice, which is supposed to provide for protections (or at least assurances) addressing the imbalances between a bank and customer.

C The ambit of the dispute

17 As it turned out, through the exchange of submissions, the residuum of the dispute between ASIC and the CBA related to the quantum of the penalty. ASIC submits that it is appropriate to impose a penalty of $7 million. The CBA submits that the penalty should be somewhere within the range of $4 million to $5 million and, as it was put in oral submissions today, the imposition of a penalty of $7 million would represent this case being an “outlier”: T22.43–4.

18 The point of departure between the parties seemed to revolve around two propositions:

(1) first, it is not appropriate to describe (or at least is potentially inaccurate to describe) the contraventions as “numerous” or “extensive”; and

(2) secondly, the penalty sought by ASIC is “materially inconsistent” with the application of the parity principle and principles of general deterrence.

19 Needless to say, in the course of fixing a penalty, I engage with both of these propositions or areas of disagreement.

D THE Relevant principles

20 The world does not need yet a further penalty judgment which canvasses at great length the principles that are well-known and not in dispute. I have identified above the principles that have real resonance or importance in resolving the nature of the dispute between the parties. Needless to say, faithful to the statutory mandate in s 12GBA(2) of the ASIC Act (as relevantly in force until 12 March 2019), I have had regard to all relevant matters, including: (a) the nature and extent of the act or omission and of any loss or damage suffered as a result of the act or omission; (b) the circumstances in which the act or omission took place; and (c) whether the person has previously been found by the Court in proceedings to have engaged in similar conduct. I have also had regard to the general principles usefully summarised, if I may respectfully say so, by Yates J in Australian Securities and Investments Commission v MLC Nominees Pty Ltd [2020] FCA 1306; (2020) 147 ACSR 266 (at 285–9 [115]–[132]).

21 In addition to the principles I have explained above, the only additional point I would make is to reinforce what Beach J explained in a recent proceeding between the same litigants (see Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790), when his Honour considered the approach to what is sometimes described as the so-called “parity principle”. As his Honour noted (at [77]):

… in all but the co-offender scenario or analogues thereof it is conceptually problematic to look at penalties in other cases to calibrate a figure in the present case when all that one has from the other cases are single point determinations produced by opaque intuitive synthesis. Deconvolution analysis of the single point determinations in order to work out the causative contribution of any particular factor is unrealistic. No juridical style Fourier transformation is possible. But unless that can be done, comparisons outside the co-offender or like scenario have little value. Moreover, the comparative value of other single point determinations is even further reduced in cases where they have been substantially influenced by the parties’ identification of and then consensus to the relevant figure or range.

22 It is trite to remark that no two cases are alike. It necessarily follows that no bespoke operation of the principles (which leads to an instinctive synthesis) operates in the same way. Further, judgments, particularly agreed judgments on penalty, do not necessarily reflect all of the evidence before the judge called upon to undertake such a process. Although in this area of the law generalisations are seldom helpful or even appropriate, one thing can be said for cases such as the present. That is, the apparent difficulty of reconciling, as I indicated in the introduction, the notion that the size of a corporation does not justify a higher penalty, with the need for the penalty to impose a sufficient sting or burden (such that the penalty should not be regarded by either the contravener or those sought to be deterred as a cost of doing business).

E CONSIDERATION

23 During the course of his helpful oral submissions, Mr Kulevski gave particular emphasis to the issue of parity and stressed the important public policy involved in promoting predictability of outcomes. These submissions were said to have a particular resonance when they were illustrated by reference to two cases: (1) the decision of Allsop CJ in Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited (No 3) [2020] FCA 1421; and (2) the decision of Beach J in ASIC v CBA. I will consider each of these decisions in turn.

24 First, in relation to ASIC v ANZ, counsel for the CBA stressed that I should obtain some assistance from the way in which the Chief Justice approached what was described in that case as the “two remediation contraventions”. I will resist the temptation of detailing at any length the facts giving rise to that case. It suffices to note that the Chief Justice found that since July 2011, ANZ knew that there was a risk that it was not entitled to charge what were described as the “same-name fees” to the affected customers: see [51]. It also knew or ought to have known that during the period between February 2014 and September 2015, there was a risk that not all affected customers would repaid all the fees that it was continuing to charge and, at all times during the period between 2014 and 2015, knew or ought to have known that in relation to a portion of the same-name fees that it was continuing to charge, the affected customers would not be repaid because it had a practice of not remediating customers who no longer had an ANZ account and who only had a low amount of remediation payable: see [56]. Further, ANZ admitted that it had engaged in two contraventions by not making remediation payments to certain customers, being affected customers who had been charged the relevant fees during the period between 2005 and 2007: see [10]. The decision made by ANZ, apparently, was that the start of the remediation programme would be at the beginning of 2008. As his Honour noted, this meant that there were a number of customers entitled to remediation who did not receive a payment: see [66].

25 The parties to that case agreed that, in respect of these two remediation contraventions, a total penalty of $2 million was appropriate. The Chief Justice noted that if he had been required to come to a figure it was likely he would have considered the appropriate figure to be slightly lower than $2 million. However, in respect of the contraventions related to charging the fees, an agreed penalty of $8 million was imposed, notwithstanding that the Chief Justice stated he would likely have imposed a penalty somewhat more than $8 million if he was approaching it in circumstances where there had not been a joint position presented by the parties: see [75].

26 The point made on behalf of the CBA was that given $2 million was charged for the remediation contraventions in that case, how could it possibly be consistent for a penalty in the region sought by ASIC to be imposed (or some higher figure) when, albeit belatedly, and unlike the position in ASIC v ANZ, full remediation was eventually given. Further, it was said that although ASIC v ANZ involved contraventions of different provisions of the ASIC Act, this only serves to emphasise the lack of parity between an $8 million penalty imposed in that case for the charging conduct and the penalty sought by ASIC in this case. It was said that the impugned conducted considered in ASIC v ANZ was simply a different species of conduct (in the sense of being more egregious) to the conduct in this case.

27 Secondly, the CBA drew attention to Beach J’s judgment in ASIC v CBA, in which his Honour imposed a pecuniary penalty of $5 million on the CBA for conduct in relation to the AgriAdvantage Packages offered by the CBA between May 2005 and November 2015. In that case, it was found that in a penalty period spanning from March 2014 to December 2015, the CBA made false and misleading representations to customers that it had adequate systems and processes to be able to provide customers with the benefits offered by the packages and would apply those benefits in accordance with its terms and conditions: see [3] and [26]–[27]. Further, during the broader period from 2005 to 2015, the CBA accepted payments in exchange for the CBA applying the benefits when there were reasonable grounds for believing the CBA would not be able to provide the benefits: see [4]. As a consequence of this conduct, a large number (8,659) of customers were harmed on a multitude (131,542) of occasions: see [84]. The CBA remediated the full amount of over $8 million, including interest. Again, commendably in the circumstances of that case, the CBA cooperated with ASIC during its investigations.

28 At the outset of his Honour’s judgment, Beach J observed (at [11]) that “a penalty of $5 million may be seen to be on the light side”. His Honour stressed that it must be appreciated that the CBA took early self-generated steps to remedy the deficiencies and remediate its customers and also “reported the deficiencies to ASIC at an early stage”. It was for these two reasons that his Honour considered there was little need for a substantial penalty to serve the objective of specific deterrence. His Honour also found that general deterrence would, in the circumstances of that case, be sufficiently served by a $5 million penalty.

29 These cases need to be approached through the correct lens (which I have already identified). There is a real, significant and important public interest in predictability of outcomes in civil penalty proceedings. It is only if parties are assured that there will not be idiosyncratic and capricious results that matters will be litigated in a way that reduces the demand on public resources. But that does not mean that one must lose sight of the inherent difficulties that accompany some supposed ideal of comparability. This is why Beach J’s comments extracted above (at [21]) have such resonance.

30 As I indicated during the course of oral argument, the imposition of a penalty does not just serve the notion of deterrence but also represents a condign curial response to what has occurred. As in the case with criminal sentencing, what may have been an appropriate sentence at one time for a particular offence may, through developments unrelated to the particular case at hand (but reflecting broader societal developments), be considered inadequate or manifestly excessive at another time. Similarly, in the context of pecuniary penalties for wrongful corporate conduct, what may have been regarded as an appropriate penalty at one time, may not reflect an appropriate penalty at another time (so as to give effect to the notion of deterrence both specific and general).

31 Although both cases which were suggested to be of particular importance do provide some assistance, that assistance cannot result in me looking at the facts of those cases and then adding and subtracting the differences and then determining an appropriate figure. That is not the way an instinctive synthesis works.

32 Without losing sight of the factors identified by French J in Trade Practices Commission v CSR Limited (1991) 13 ATPR 41–076 (at 52,152–3) and Burchett and Kiefel JJ in NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission (1996) 71 FCR 285 (at 292–4), one of the factors which is relevant in this case is the important role of an organisation such as the CBA in Australian society. The Chief Justice touched upon this consideration in ASIC v ANZ when his Honour noted the following (at [13]–[14]):

The importance of the banking system in Australian social and commercial life need only be stated. Reliance by customers on the integrity and good faith of their bank is at the heart of social and commercial life in this country. It is highlighted in general life from advertising by banks and by community expectations. Despite all other features, the banker and customer relationship is at the heart of the economic system. It is a relationship based on contract, but, as the Code of Banking Practice reveals, it is founded on trust and good faith in a commercial sense.

It would shock any customer to know that his or her bank took and was continuing to take his or her money in fees when it knew that there was a risk that it had no authority to do so, and without thereafter coming to a view that it did have that authority. This would be especially the case if the customer knew that, upon a view that the terms would be changed in the ordinary course of business, no decision would be made to stop taking the fees because that was difficult and would lead to other fees about which there was no risk not being charged. The customer might well consider that he or she had not been treated fairly and in good faith in those circumstances. But, of course, in their position the customers were not privy to that knowledge, especially in relation to terms and conditions that reflect contracts of adhesion (or standard form contracts) in the ordinary course of business.

33 Indeed, large organisations who adopt a public position of adhering to norms such as is reflected in the Banking Code of Practice and which hold themselves out as having persons whose titles include terms such as “governance” and “compliance” must do more than simply declaim platitudes. What matters is the corporate will to do the right thing. As I noted in Australian Securities and Investments Commission v AMP Financial Planning Pty Ltd (No 2) [2020] FCA 69; (2020) 377 ALR 55 (at 59 [2]):

For generations, many successful financial institutions did not need “value statements” setting out bromides; nor was it thought necessary to have an array of compliance executives with highfalutin titles; those responsible simply ensured that their employees or representatives dealt with customers in a manner reflecting an instinctive institutional commitment to playing with a straight bat.

34 Although the conduct in this case does not reflect the seriously wrongful conduct of the representatives in ASIC v AMP, the CBA delay is particularly troubling given the nature of the commercial relationship between the bank and its customers. One would expect an organisation such as the CBA to do the right thing without having to be activated by customer complaints.

35 ASIC pointed to the fact that in ASIC v CBA, in contradistinction to the current case, the steps taken by the CBA once it had identified the problem were timely and thorough, including in relation to remediation, and it had brought ASIC “into the loop” at the earliest opportunity: see [100] and [119]. This has a significance in distinguishing between these two cases, but also points to the real problem in the present case – the failure of the CBA to act without prompting, deal with ASIC straightaway, or put in place a remediation programme with celerity.

36 Like in ACCC v Apple (No 4) (at [56]–[60]), there does seem to me to be a high degree of artificiality in reconciling the notion that a penalty of $7 million (which represents profit earned in a little over six hours of the bank’s operations during the course of the year when the remediation programme was finally completed) would operate in a way to deter repetition of this conduct by an organisation as large as the CBA and by others who might be tempted to contravene.

37 Uninstructed by the parity principle (such as it is) and the views of the regulator, I would have thought an appropriate sum to give effect to deterrence and to impose a sting or burden on an organisation such as the CBA (and having full account of the other considerations to which I must have regard by reference to the statute and the authorities), would be higher than that proposed by ASIC. Indeed, during the course of oral submissions, counsel for the CBA did accept that the contravening conduct could be described appropriately as “serious”: T14.16–7.

38 It follows I do not consider the penalty sought by ASIC to be materially inconsistent with the application of the parity principle and principles of general deterrence. In fact, I think any lower figure would insufficiently have regard to the principles of deterrence, both specific and general. In this regard, it is important to recall that specific deterrence is not simply served by reason of the fact that the systemic breach has been rectified, but rather makes plain that conduct of this type or nature must be prevented and the business be conducted in a way which is consistent with statutory norms.

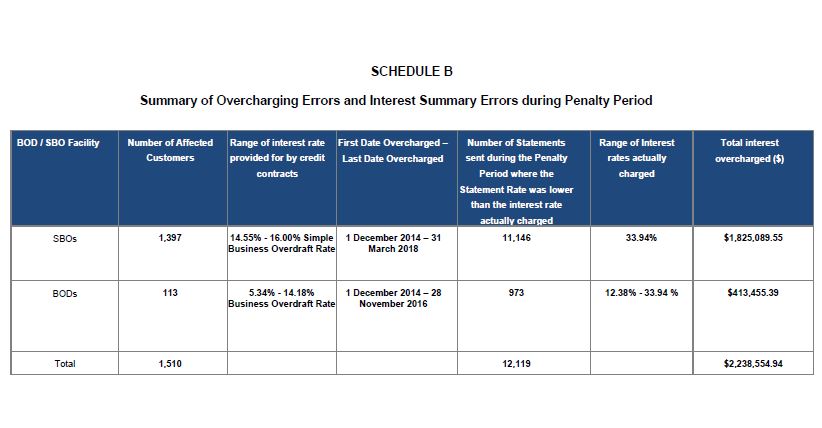

39 The contravening conduct is serious without being egregious. It is possible to imagine far worse cases. However, I specifically reject the submission made by the CBA that it acted expeditiously in relation to the rectification of the problem once it was identified. As I have said, the delay reflects very poorly on the CBA. At the end of the day, one must remember that a large number of customers were misled as to the interest charged on their accounts on 12,119 occasions, and the false and misleading representations were significant with the result that customers were overcharged interest totalling $2,238,554.94. This does call for a response that goes well beyond a sum which could be conceptualised as a mere cost of doing business.

40 Lastly, I should note that although it is rightly accepted that the contraventions were serious, terms such as “numerous” and “extensive” need to be approached with some degree of care. In a financial institution the scale of the CBA, many financial services are delivered on a continual basis. It must be recognised, as the CBA correctly submits, that even within the cohort of the CBA customers that transacted on the overdraft facilities affected by the contravening conduct, 0.31 per cent of customers with BODs were affected and 7.3 per cent of those with SBOs were affected, and that a significant number of contraventions resulting from the coding error caused repetition of the conduct in respect of those customers. Again, when it comes to the notion of “extensive”, there is merit in the CBA’s submission that while it must ensure that it establishes and maintains appropriate systems and processes to deliver the financial services it delivers, it cannot really be said that the conduct here was extensive, given the extent of the transactions it has with its customers.

41 Accordingly, I intend to impose a pecuniary penalty of $7 million. In reaching this view, I have also had regard to the cooperative way in which the CBA has conducted itself since ASIC became aware of the contraventions and, in particular, the way in which the CBA has approached the litigation consistently with the overarching purpose.

F Other Relief

42 Part of the relief sought by ASIC was for a corrective notice, which is reproduced at Annexure B to these reasons. As I indicated to the parties, I do not think that I should make such an order.

43 When I asked Mr Luxton, counsel for ASIC, as to the purpose of such an order, he noted, unsurprisingly, “the point is to draw it to the attention of the public”: T3.10. If this is the purpose, then I think a notice in the terms of Annexure B is unlikely to assist in achieving this purpose.

44 While I express no criticism of either party for agreeing the terms of such a notice, which is in a form similar to those that have been ordered in a number of cases in the past, in my view, the time has come to rethink the form in which this information is communicated to the public.

45 Section 12GLB of the ASIC Act is in the following terms:

12GLB Punitive orders requiring adverse publicity

(1) The Court may, on application by ASIC, make an adverse publicity order in relation to a person who:

(a) has been ordered to pay a pecuniary penalty under section 12GBB; or

(b) is guilty of an offence under section 12GB.

(2) In this section, an adverse publicity order, in relation to a person, means an order that:

(a) requires the person to disclose, in the way and to third parties specified in the order, such information as is so specified, being information that the person has possession of or access to; and

(b) requires the person to publish, at the person’s expense and in the way specified in the order, an advertisement in the terms specified in, or determined in accordance with, the order.

(3) This section does not limit the Court’s powers under any other provision of this Act.

46 As the heading makes clear, it is a punitive order which seeks to publicise relevant information. In relation to a notice issued pursuant to this section, like those issued in other areas of the law, regard must be had to the audience to which that information is proposed to be communicated.

47 I dealt with a similar issue in Lenthall v Westpac Banking Corporation (No 2) [2020] FCA 423; (2020) 144 ACSR 573, where I considered the content of opt-out notices issued pursuant to s 33X of the Federal Court of Australia Act 1976 (Cth) (FCA Act). In a regime where no consent is required for people to become group members in a class action, Pt IVA of the FCA Act provides a mechanism by which the Court is required to set a date for opt-out and approve a notice to be communicated to members of the public: ss 33J(1) and 33X(1)(a). That notice is to apprise the public of information upon which the group member relies to make a decision as to his or her rights.

48 Although the issue of effective communication by the Court to group members in a class action may be somewhat different than the present context, the underlying purpose of the communication is the same: it is to provide members of the public with information the Court considers to be significant.

49 In Lenthall v Westpac, I noted (at [45]) that, like here, the audience is likely to include highly sophisticated persons and persons who are unsophisticated in financial and legal matters, including those who may have either literacy problems or at the least some difficulty in taking in complex information in written form. In that case, I noted that I did not consider it was unduly stretching the bounds of s 144(1) of the Evidence Act to remark that:

… it is not reasonably open to question that advanced Western societies have reached a stage where significant parts of the community, and, in particular, younger members of the community, more readily digest information conveyed to them in audio-visual rather than written form.

50 I then went onto say (at [46]–[50]) that:

Connected to this phenomenon, a number of studies in the United States have suggested that both the quantity and quality of adult reading abilities are in decline: see, for example, Alice Horning, “Reading, Writing and Digitizing: A Meta-Analysis of Reading Research”, (2010) 10(2) Reading Matrix 243. Further, although there is scant readily accessible recent data, according to a 2012 report of the OECD, some 12.6% of Australian adults attained only Level 1 (of 5) or below in literacy proficiency. At that level of literacy, adults can read brief texts on familiar topics and locate a single piece of specific information identical in form to information in the question or directive, but otherwise experience difficulty: Organisation for Economic Cooperation and Development, Australia - Country Note: Survey of Adult Skills First Results (OECD, 2012) at 3. An Australian Bureau of Statistics commentary of that OECD Survey noted that:

[a]round 3.7% (620,000) of Australians aged 15 to 74 years had literacy skills at Below Level 1, a further 10% (1.7 million) at Level 1, 30% (5.0 million) at Level 2, 38% (6.3 million) at Level 3, 14% (2.4 million) at Level 4, and 1.2% (200,000) at Level 5.

Australian Bureau of Statistics, 4228.0 - Programme for the International Assessment of Adult Competencies, Australia, 2011-12 (https://www.abs.gov.au/AUSSTATS/ abs@.nsf/productsbyCatalogue/A7F52A484135C822CA257BFE00257DD5?OpenDocument).

It seems to me quite obvious that in large scale consumer class actions, the Court is communicating to a number of people who are within cohorts who have attained only basic levels of literacy.

The concept of “readability” has spawned various tests which have been used to measure the readability of certain texts, providing quantitative estimates of the style difficulty of different writing examples. “Readability” has been variously defined, but in essence consists of three aspects: “comprehension, fluency (reading speed), and interest”: see Grant Richardson and David Smith, “The Readability of Australia's Goods and Services Tax Legislation: An Empirical Investigation”, (2002) 30(3) Federal Law Review 475 at 478. If information must be conveyed in writing, there is a need to adopt a form of language, structure and design, which maximises the chance of all the intended audience readily understanding the information sought to be communicated.

Leaving aside the adoption of plain language, I consider the time has come for those proposing notices to consider new modes of communicating complex information. This need will only become more acute as we progress (if that is the right word) further into the age of social media.

Put more directly, it is simply complacent to continue to make the assumption that sending complex information in written form is the best way of communicating information to group members in some types of class actions, and consideration should be given as to whether supplementary or substitute modes of conveying information should be adopted.

51 Likewise, in the present context, it might be thought less than satisfactory to continue to just assume that notices of the type set out in Annexure B are an appropriate means to communicate punitive orders requiring adverse publicity – just because this is the way it has always been done.

52 Both parties, commendably, have indicated that they have no difficulties with the information being prepared and being communicated in a different form. Given the high degree of cooperation that has been reflected in the conduct of this litigation to date, I propose to stand the matter over to a convenient date in order for the parties to confer as to an appropriate form of the punitive order requiring adverse publicity.

53 Such an adjournment would also allow the parties to confer in relation to the issue of costs. It is proposed that I make an order that the CBA pay ASIC’s costs of and incidental to the proceeding. My preference would be to make an order in a lump sum, if that can be agreed, and failing any agreement, for me then to make directions as to the quantification of the lump sum costs amount.

G CONCLUSION AND ORDERS

54 For the above reasons, at present, I will make the following orders:

(1) Pursuant to s 12GBA(1) of the Australian Securities and Investments Commission Act 2001 (Cth), within 30 days, CBA is to pay to the Commonwealth of Australia a pecuniary penalty of $7 million.

(2) The proceeding be listed for a further case management hearing at 9.30am on 28 April 2021.

I certify that the preceding fifty-four (54) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Lee. |

Dated: 26 April 2021

Annexure A

Annexure B