Federal Court of Australia

Australian Securities and Investments Commission v GoGetta Equipment Funding Pty Ltd [2021] FCA 420

ORDERS

VID 532 of 2020 | ||

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Applicant | ||

AND: | GOGETTA EQUIPMENT FUNDING PTY LTD Respondent | |

DATE OF ORDER: | 26 April 2021 |

THE COURT ORDERS THAT:

1. Pursuant to s 166 of the National Consumer Credit Protection Act 2009 (Cth) (the National Credit Act), the Court declares that the Respondent contravened:

(a) section 29 of the National Credit Act on 10 occasions, on each occasion by engaging in the credit activity described in item 3(a) of s 6(1) of the National Credit Act, by being the lessor under the rental agreements (being consumer leases) (as particularised in Annexure A) (Agreement), when it did not hold a licence under the National Credit Act authorising it to engage in that credit activity; and

(b) section 32 of the National Credit Act on 295 occasions, on each occasion by demanding, receiving, and/or accepting fees, charges or other amounts from a consumer who was a party to an Agreement (as particularised in Annexure B) for engaging in the credit activity described in item 3(a) of s 6(1) of the National Credit Act, when it did not hold a licence under that Act authorising it to engage in that credit activity.

2. Pursuant to s 167(2) of the National Credit Act, the Court orders that the Respondent pay to the Commonwealth pecuniary penalties totalling $750,000 in respect of the declarations in Order 1 that the Respondent has contravened ss 29 and 32 of the National Credit Act.

3. The Respondent pay the Applicant’s costs in a sum that has been agreed between the parties.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

DAVIES J:

introduction

1 The applicant (ASIC) has applied to the Court for declarations and pecuniary penalties against the respondent (GoGetta) in respect of contraventions of ss 29 and 32 of the National Consumer Credit Protection Act 2009 (Cth) (National Credit Act). GoGetta has admitted the contraventions and the parties are agreed that a total penalty of $750,000 in respect of those contraventions would be just and appropriate. It is settled law that the task of the Court where parties have agreed on penalty is to consider whether the proposal can be accepted as fixing an appropriate amount and for that purpose the Court must satisfy itself that the submitted penalty is appropriate: Commonwealth of Australia v Director, Fair Work Building Industry Inspectorate (2015) 258 CLR 482; [2015] HCA 46 at [48] (Fair Work). For the reasons that follow I am satisfied that it is appropriate to make the declarations sought by ASIC and to impose a penalty of $750,000 for the contraventions.

relevant legislation

2 Section 29(1) of the National Credit Act provides that a person must not engage in a credit activity if the person does not hold a licence authorising the person to engage in the credit activity.

3 Section 32(1) of the National Credit Act provides that a person must not demand, receive or accept any fee, charge or other amount from a consumer for engaging in a credit activity if, by engaging in that credit activity, the person contravenes, or would contravene, s 29.

4 A person engages in a credit activity if:

(a) the person is a lessor under a consumer lease: s 6(1) item 3(a) of the National Credit Act; or

(b) the person performs the obligations, or exercises the rights, of a lessor in relation to a consumer lease or proposed consumer lease (whether the person does so as the lessor or on behalf of the lessor): s 6(1) item 3(c) of the National Credit Act;

5 A consumer lease is “a consumer lease to which Part 11 of the National Credit Code applies”: s 5 of the National Credit Act. The National Credit Code (the National Credit Code) is Schedule 1 to the National Credit Act.

6 Part 11 of the National Credit Code applies to a consumer lease if, when the lease is entered into:

(a) the goods are hired wholly or predominantly for personal, domestic or household purposes: s 170(1)(a) of the National Credit Code; and

(b) a charge is or may be made for hiring the goods and the charge together with any other amount payable under the consumer lease exceeds the cash price of the goods: s 170(1)(b) of the National Credit Code; and

(c) the lessor hires the goods in the course of a business of hiring goods carried on in this jurisdiction or as part of or incidentally to any other business of the lessor carried on in this jurisdiction: s 170(1)(c) of the National Credit Code.

7 If, in any proceeding, a party claims that a lease is a consumer lease to which Part 11 of the National Credit Code applies, it is presumed to be such unless the contrary is established: s 172(1) of the National Credit Code.

8 By s 172(2) of the National Credit Code, it is presumed for the purposes of the National Credit Code that goods hired under a lease are not hired wholly or predominantly for personal, domestic or household purposes if the lessee declares, before entering the lease, that the goods are hired wholly or predominantly for business purposes, unless the contrary is established.

the admitted contraventions

9 ASIC has alleged, and GoGetta has admitted, the following conduct:

(a) between 1 July 2014 and 23 February 2018 (the relevant period), GoGetta did not hold an Australian Credit Licence (an ACL) under the National Credit Act;

(b) between 30 April 2015 and 21 December 2016, GoGetta entered into 10 light passenger vehicle agreements (Rental Agreements) with customers;

(c) each Rental Agreement was a consumer lease to which Part 11 of the National Credit Code applied;

(d) GoGetta was the lessor and the customer was the lessee under each Rental Agreement;

(e) in making each Rental Agreement, GoGetta did not obtain from the customer a declaration under s 172(2) of the National Credit Code that the vehicle was, or vehicles were, hired wholly or predominantly for business purposes;

(f) GoGetta has not established that any Rental Agreement was not a consumer lease to which Part 11 of the National Credit Code applies;

(g) accordingly, each Rental Agreement was a consumer lease to which Part 11 of the National Credit Code applies;

(h) by each of the Rental Agreements:

(i) the customer authorised GoGetta to arrange for any amount GoGetta might debit or charge the customer to be debited through the bulk electronic clearing system account held at the customer’s financial institution; and

(ii) the customer agreed to pay weekly, from the Rental Agreement’s commencement date for the term of the Rental Agreement, rent of an expressed amount by direct debit to GoGetta;

(i) during the relevant period, GoGetta made automated demands to, and received and accepted payments from, customers under each Rental Agreement;

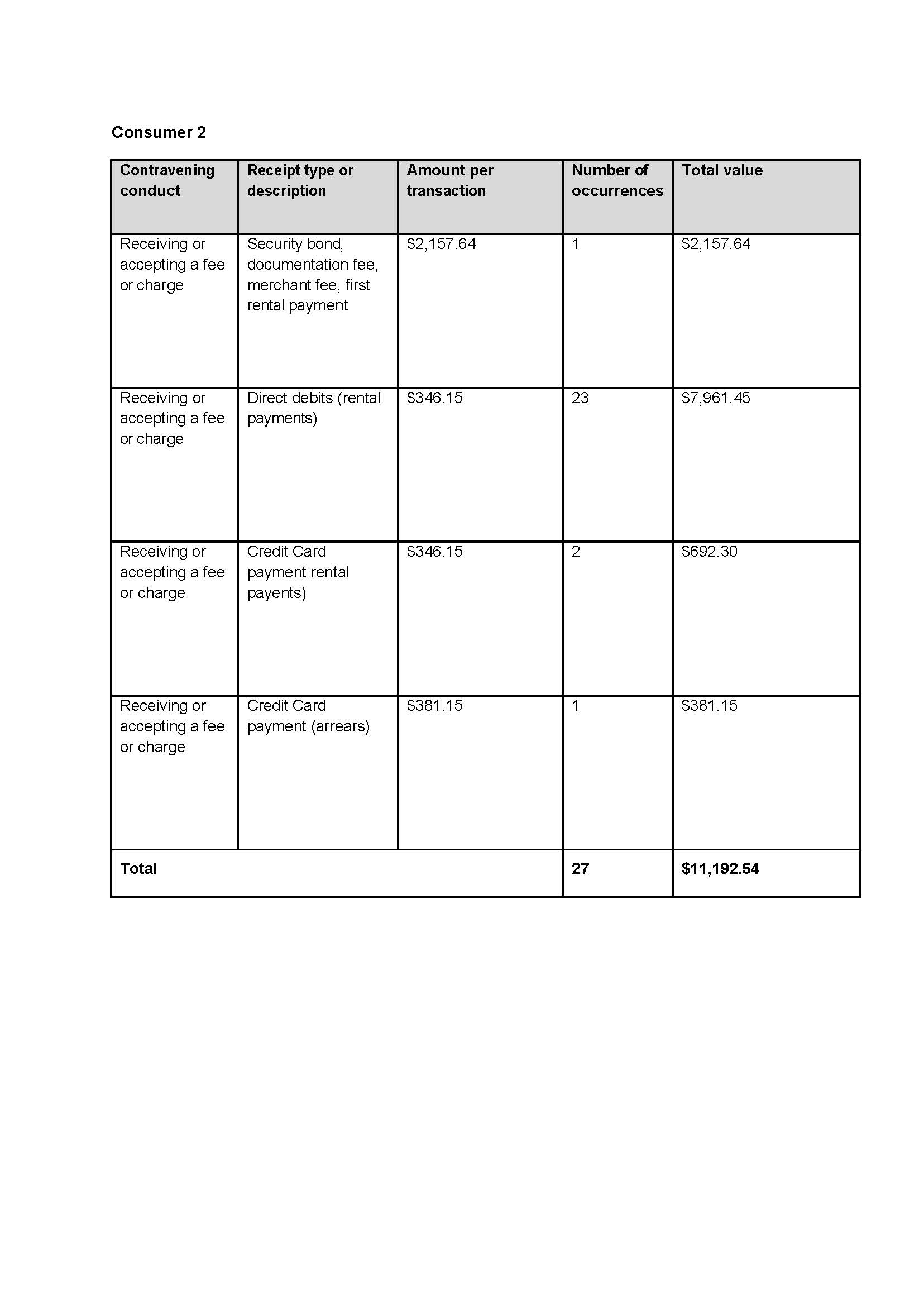

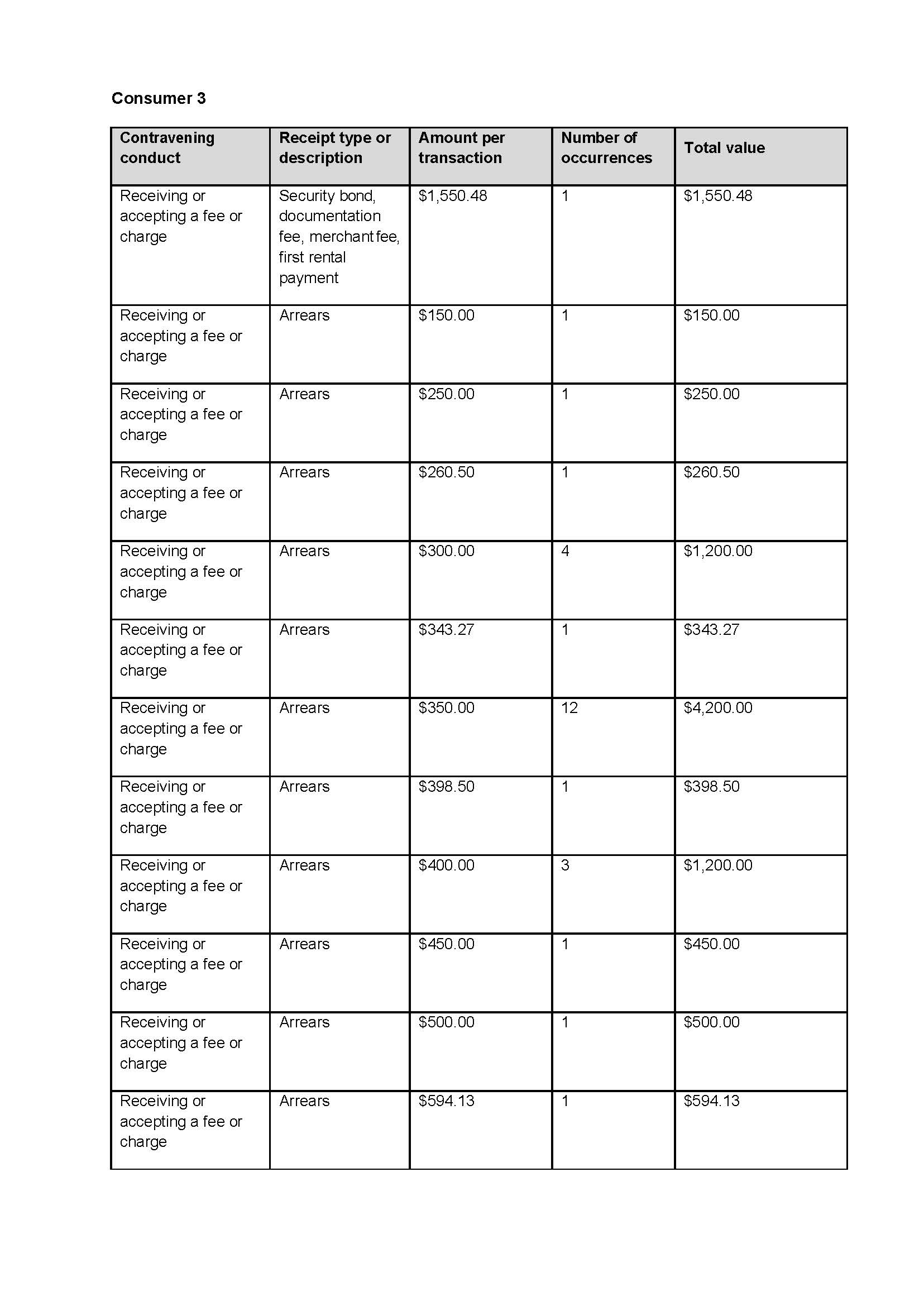

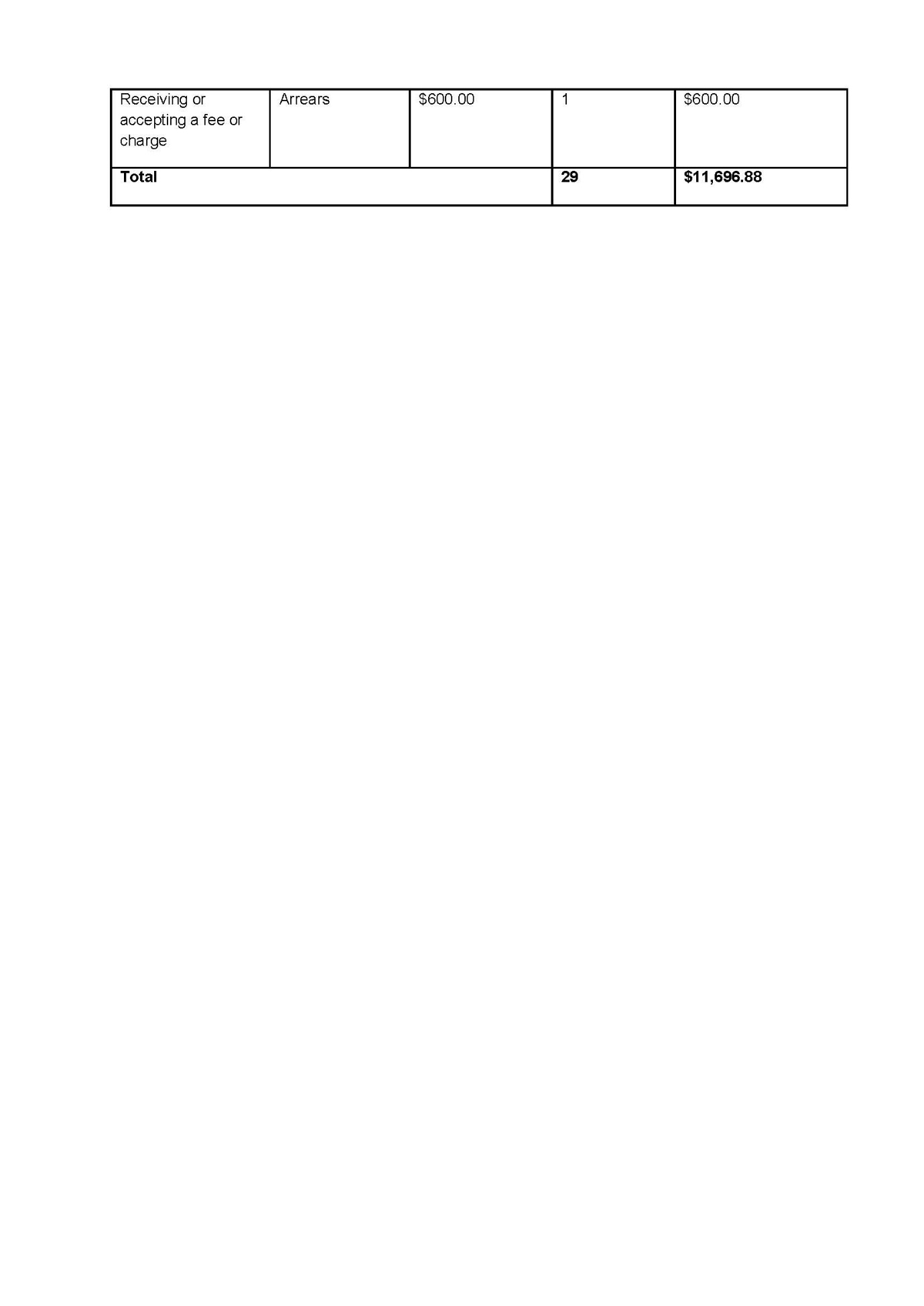

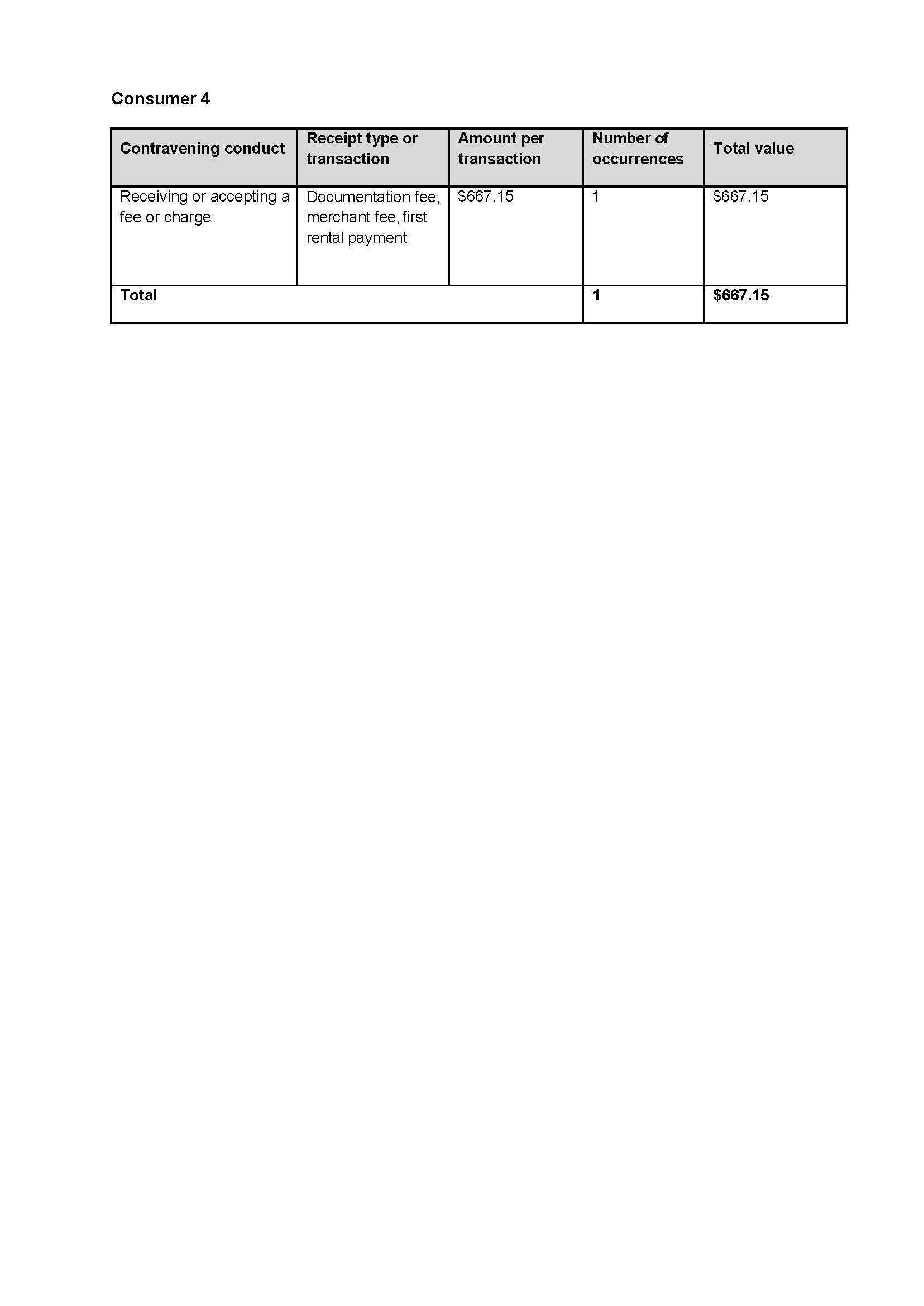

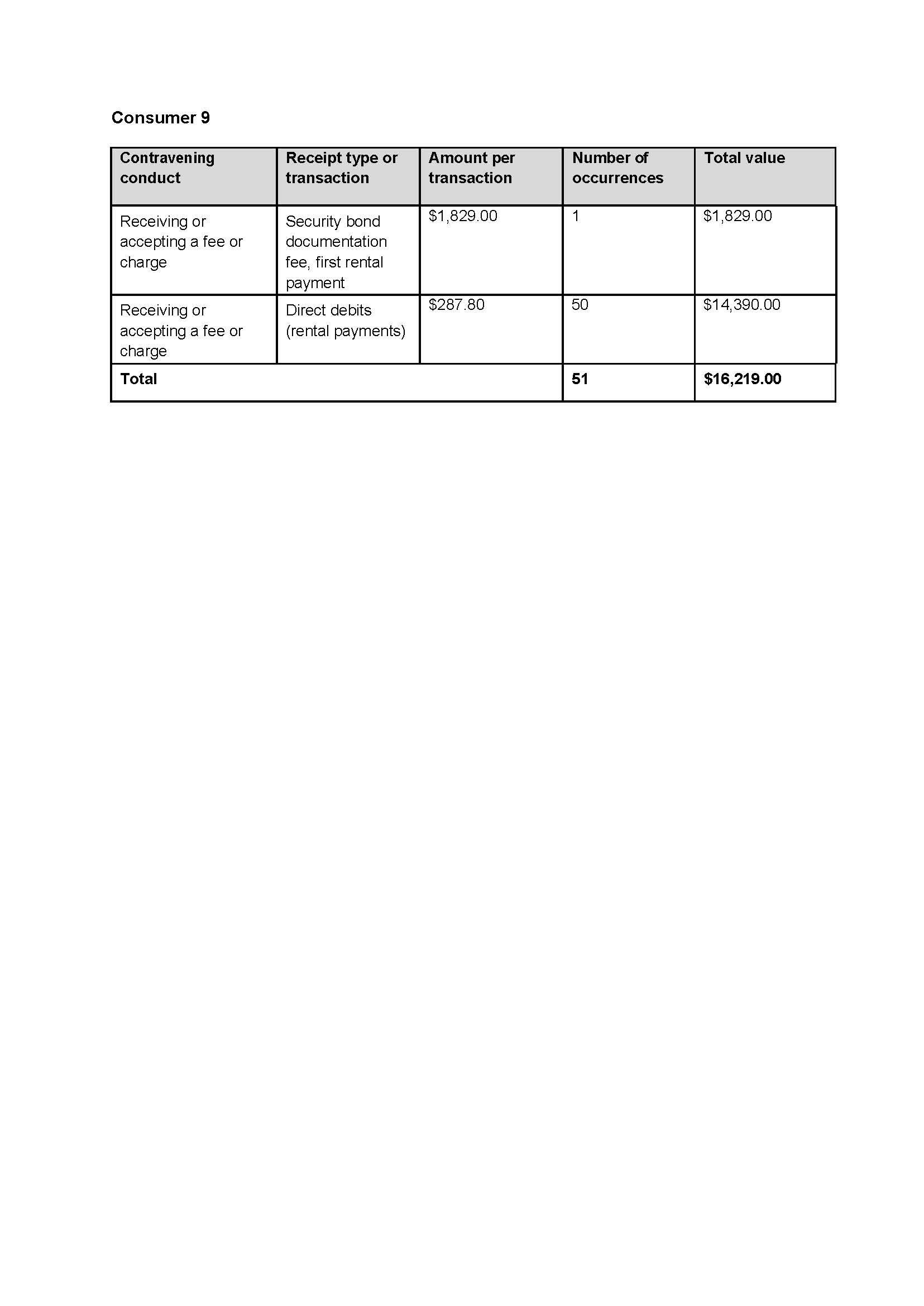

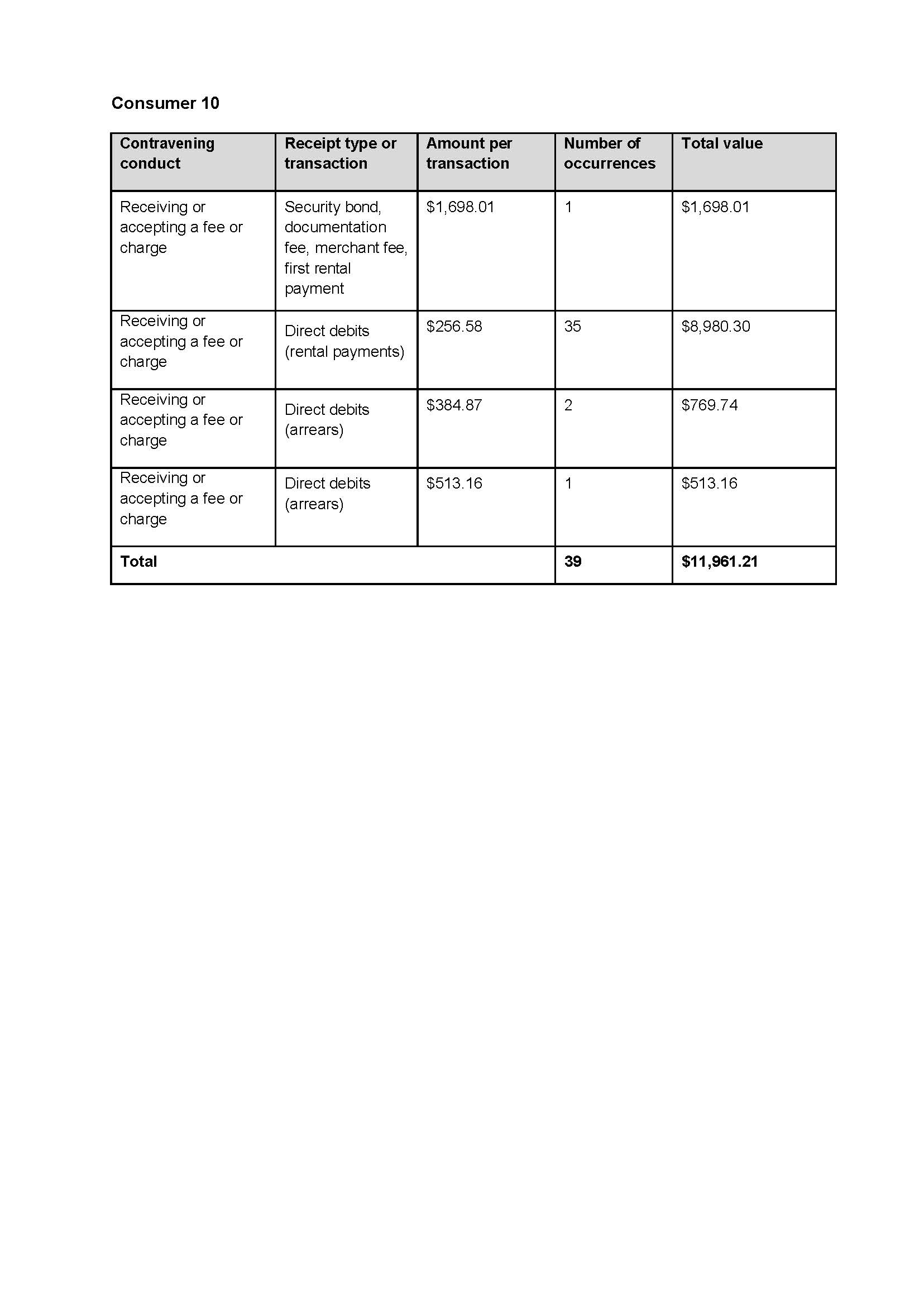

(j) the number of receipts for the 10 consumers was 295; and

(k) consequently, GoGetta contravened:

(i) section 29 of the National Credit Act in respect of the 10 Rental Agreements by engaging in a credit activity by being the lessor under each Rental Agreement without holding an ACL; and

(ii) section 32 of the National Credit Act 295 times by the conduct of accepting or receiving payments from the customer under each Rental Agreement for engaging in a credit activity.

underlying facts

10 The recitation of facts is taken from the agreed facts and documents submitted by the parties.

11 GoGetta is a wholly owned subsidiary of SIV Capital Limited (SIV Capital) which was founded in 1986 as a business to business equipment rental company. From 1986 to 2019 SIV Capital’s core business was equipment rental and financing to small and medium sized businesses in the hospitality sector. In 2007, SIV Capital established GoGetta, a wholly owned subsidiary, for the purposes of providing equipment rental and financing to commercial customers in sectors other than hospitality. GoGetta began operating in April 2008 to provide commercial equipment rental solutions to small and medium sized businesses in the broader commercial equipment market, operating primarily in the transport and construction sectors. From 1 July 2014, GoGetta expanded its asset leasing business to include the leasing of light passenger motor vehicles for use by businesses and during the relevant period, GoGetta entered into 5,544 rental agreements with 5,183 customers for light commercial vehicles.

12 GoGetta received rental applications for light passenger vehicles from third-party intermediaries (a finance broker or a used car dealership). GoGetta employees would primarily deal directly with the third-party intermediary, rather than the consumer, before entering into the rental agreement with the customer. The third-party intermediary would provide a standard-form rental agreement application to a potential customer wanting to enter into a rental agreement with GoGetta. The rental application form required the provision of business information, including the customer’s “trading name”, Australian Business Number, ACN if applicable, years of trading, industry type and whether the potential customer rented or owned their own business premises. If rented, the form required either confirmation from the landlord that the potential customer had a commercial lease or the provision of a copy of the commercial lease. The form also had a check box next to a “statement by applicant(s) for credit” which included the certification by the customer that the information provided was true and correct, and an acknowledgement that GoGetta was relying upon such information to assess the application.

13 The terms of the rental agreement were generally in a standard form. The rental agreement included terms to the following effect:

(a) the customer agreed to pay weekly rent of an expressed amount by direct debit to GoGetta from the rental agreement commencement date, for the term of the agreement;

(b) the term of the agreement was for a minimum of 12 months;

(c) the customer was responsible for paying any and all fees incurred throughout the rental term;

(d) the rental equipment remained the property of GoGetta at all times; and

(e) the customer could offer to purchase the equipment at any point in time or for an agreed price at the end of the initial 12 month period.

14 The rental agreement included a request and authority to debit (completed by the customer) authorising GoGetta to arrange for any amount to be debited or charged to the customer through the bulk electronic clearing system account held at the customer’s financial institution (the direct debit arrangement).

15 If the customer agreed to the terms of the rental agreement, the customer would sign the rental agreement and the direct debit arrangement. These documents would be returned to GoGetta, either by the applicant or via the third-party broker. GoGetta would then arrange a direct debit of an amount from the customer’s account for the security bond, the first rental payment and a documentation fee.

16 The GoGetta customer service team did not contact the applicant to verify that the application was being made for a business purpose or require an applicant to provide a business purpose declaration under the National Credit Code. GoGetta simply relied on the fact that applicants were required to provide an Australian Business Number as part of their application. GoGetta “did not contemplate the risk that a consumer may apply to enter into a rental agreement with [it]”.

17 On 20 July 2017, ASIC commenced an investigation into GoGetta regarding concerns that some of the motor vehicle leases GoGetta had entered into (from 1 July 2014) may have been consumer leases to which Part 11 of the National Credit Code applied. On 25 July 2017, ASIC issued a notice to GoGetta to produce documents in relation to the rental of motor vehicles to customers during the period 1 March 2015 to 30 June 2016. GoGetta complied with the notice, and shortly after submitting its response, GoGetta voluntarily ceased accepting applications for its light commercial vehicle rental business.

18 In December 2017, GoGetta engaged Ernst & Young to conduct an audit of its motor vehicle rental files to determine the risk of rental agreements being consumer leases, and to develop a framework for customer remediation. Ernst & Young provided an interim report (the EY Report) in February 2018. The EY Report identified 5,183 potentially impacted customers, of which:

(a) 207 customers (3.99%) had rental agreements that were at a high risk of being a consumer lease;

(b) 844 customers (16.28%) had rental agreements that were at a medium risk of being a consumer lease; and

(c) 4,132 customers (79.72%) had rental agreements that were at a low risk of being a consumer lease.

19 The EY Report also identified that:

(a) GoGetta’s operating model, systems, processes and controls were designed to deliver vehicle leasing to business customers for non-consumer purposes;

(b) GoGetta did not consider whether there was a risk that customers would seek a rental agreement for a consumer purpose, or whether any measures should be put in place to address such a risk;

(c) GoGetta relied on information from brokers and placed a high degree of trust in brokers;

(d) most customer files contained insufficient evidence to conclude whether the lease was for a business purpose or for a consumer purpose; and

(e) a number of the rental agreements had risk attributes that indicated there was a greater risk that they were obtained for a consumer purpose, rather than a business purpose.

20 The EY Report also identified a number of third-party intermediaries whom Ernst & Young considered were likely to have submitted a rental application to GoGetta in circumstances where there was a high risk that the customer would enter into a rental agreement for a consumer purpose.

21 On 7 August 2020, GoGetta and SIV Capital offered, and ASIC accepted, a court enforceable undertaking:

(a) to implement a remediation program to identify and remediate affected customers, being customers who were at high risk of having entered into a consumer lease, or who on the balance of probabilities, were more likely than not to have entered into a consumer lease;

(b) to appoint an independent remediation consultant to oversee the remediation program; and

(c) to pay:

(i) ASIC’s investigation costs;

(ii) the costs associated with the court enforceable undertaking and remediation program, including the cost of the independent remediation consultant; and

(iii) ASIC’s legal costs incurred in this proceeding.

22 The court enforceable undertaking included the following admissions by GoGetta and SIV Capital:

(a) GoGetta’s operating model, systems, processes and controls were not adequate to ensure that customers obtained motor vehicle leases for predominantly business purposes, and not for consumer purposes;

(b) when expanding its asset leasing business to include motor vehicle leases, GoGetta failed to contemplate or take any steps, alternatively adequate steps, to address the risk that customers were obtaining motor vehicle leases for consumer purposes;

(c) GoGetta did not obtain business purpose declarations from customers for the purpose of s 172(2) of the National Credit Code;

(d) the attributes of a number of customers suggest that there was considerable risk that they had obtained the motor vehicle leases for consumer purposes rather than for a predominantly business purpose; and

(e) notwithstanding that risk, GoGetta relied on limited information from its brokers and failed to carry out any independent inquiries, other than confirming the existence of the customer ABNs provided to it by brokers, to verify that customers entered into the motor vehicle leases for predominantly business purposes, and not for consumer purposes.

23 GoGetta and SIV Capital also admitted that GoGetta had contravened:

(a) section 29 of the National Credit Act by engaging in a credit activity whilst not holding an ACL, in respect of a number of motor vehicle leases entered into during the Relevant Period, which were in fact consumer leases; and

(b) section 32 of the National Credit Act by demanding and receiving a fee, charge or other amount pursuant to the motor vehicle leases which were consumer leases during the Relevant Period.

24 Under the remediation program, GoGetta and SIV Capital agreed, amongst other things:

(a) to make remediation payments to affected customers;

(b) not to profit, or retain any form of interest, or a fee or charge from an affected motor vehicle lease; and

(c) not seek to recover arrears or remaining payments from affected customers.

25 The following actions have been taken in compliance with the court enforceable undertaking and remediation program since its commencement on 7 August 2020:

(a) SIV Capital and GoGetta appointed David Carson of Compliance One as the independent remediation consultant on 3 September 2020;

(b) SIV Capital and GoGetta submitted to the independent remediation consultant for review, all non-remediation program settlements on 4 September 2020. Non-remediation program settlements are private settlements entered into between GoGetta and its customers (including 8 of the 10 consumers the subject of these proceedings) before the remediation program commenced. Pursuant to the court enforceable undertaking, the independent remediation consultant was to determine whether the compensation under the private settlements was no less than the compensation under the remediation program and assess any top up that might need to be paid by GoGetta;

(c) SIV Capital and GoGetta submitted to ASIC template customer communications on 16 September 2020, which were approved by ASIC on 9 November 2020;

(d) the independent remediation consultant submitted to ASIC a list of High-Risk Brokers on 9 October 2020, which was approved by ASIC on 27 October 2020; and

(e) the independent remediation consultant has submitted regular reports to SIV Capital, GoGetta and ASIC as to the status and progress of claims under the remediation program.

26 Prior to ASIC’s investigation, SIV Capital and its subsidiaries had not received any infringement notices, penalties or fines from ASIC in relation to any regulatory breaches. Further, GoGetta has not previously been found by any court, in any proceedings brought by ASIC, to have engaged in similar conduct to the conduct the subject of these proceedings.

COntraventions

27 GoGetta admitted a total of 305 contraventions of the National Credit Act, namely 10 contraventions of s 29 in respect of the 10 Rental Agreements the subject of the proceedings and 295 contraventions of s 32(1) – namely on each occasion it demanded, received or accepted a fee, charge or other amount under those Rental Agreements without an ACL. ASIC’s position was that the same 295 acts constituted separate further contraventions of s 29, namely the exercise of its rights as lessor under the Rental Agreements each time it accepted or received a payment. However, ASIC also acknowledged that these contraventions involved the same conduct that gave rise to the s 32 contraventions and that s 175 of the National Credit Act prevented the Court from imposing penalties in respect of contraventions both s 29 and s 32 relating to that same course of conduct. Accordingly, the total number of contraventions for which a penalty may be imposed is 305.

declaratory relief

28 By s 166(2) of the National Credit Act, the Court must make a declaration of contravention of a civil penalty provision if it is satisfied that the person has contravened the provision. Sections 29 and 32 are both civil penalty provisions. Having regard to the agreed facts and admissions, I am satisfied that GoGetta contravened s 29 on 10 occasions and s 32 on 295 occasions. The declarations sought by ASIC pursuant to s 166 of the National Credit Act are that GoGetta contravened:

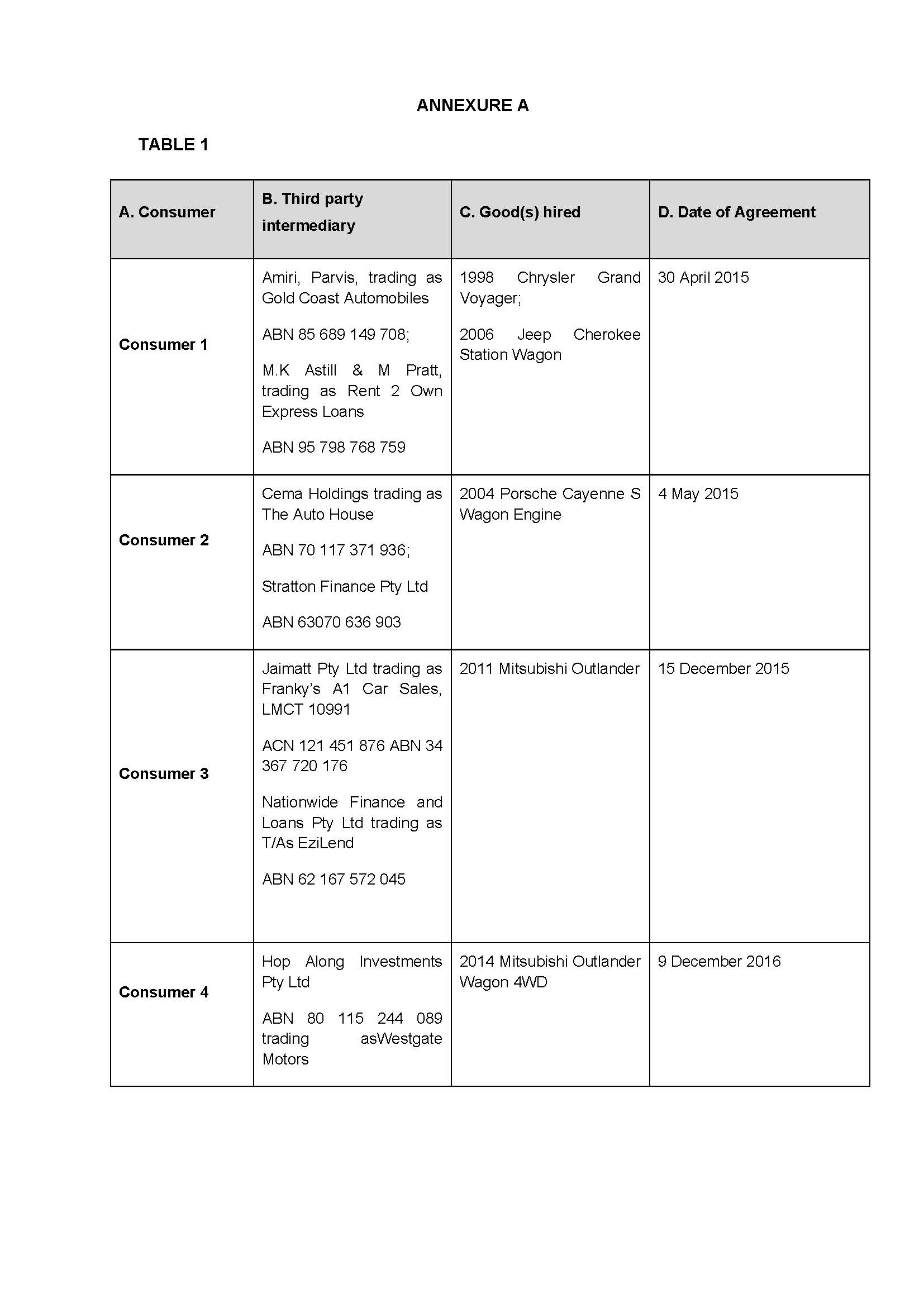

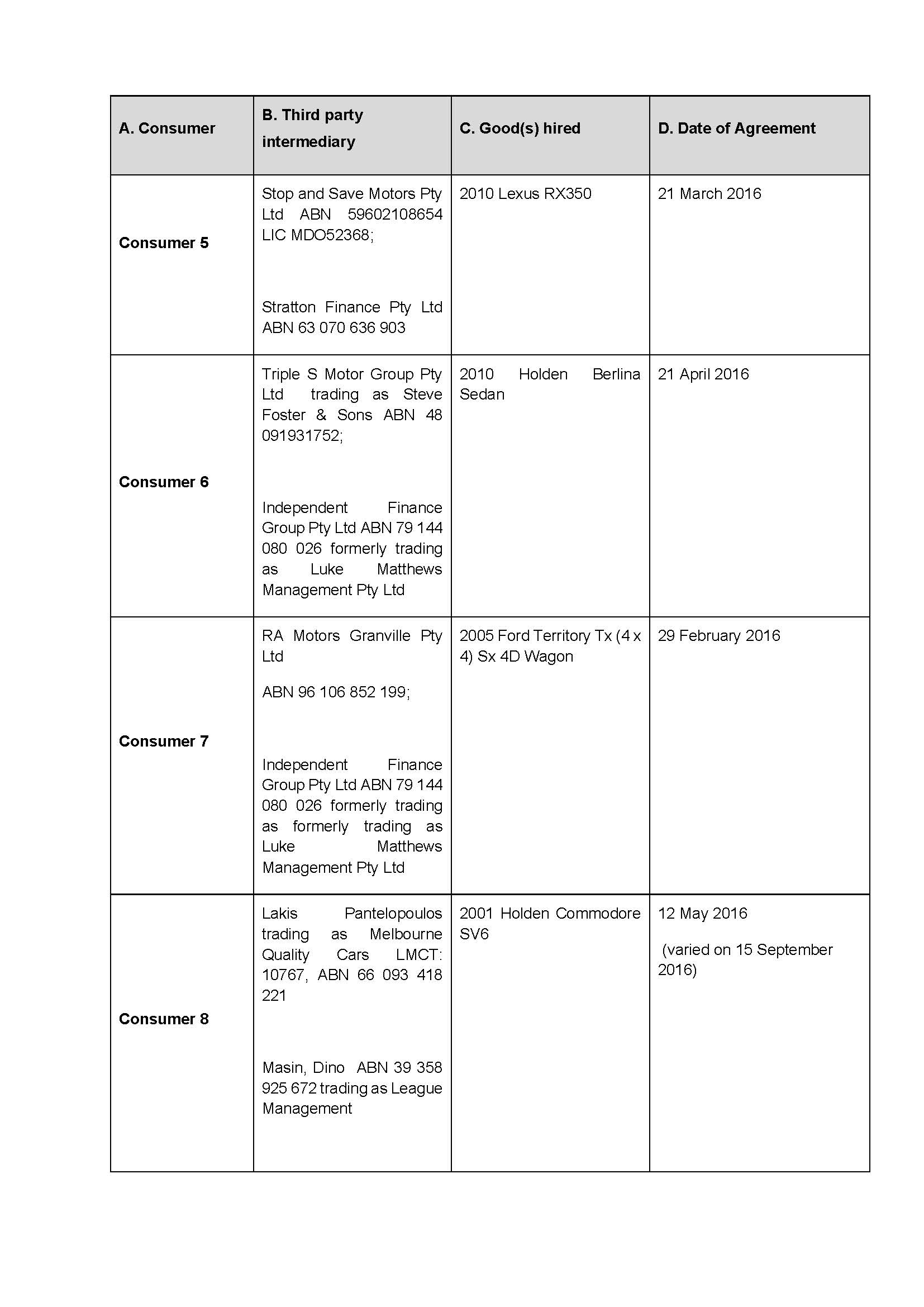

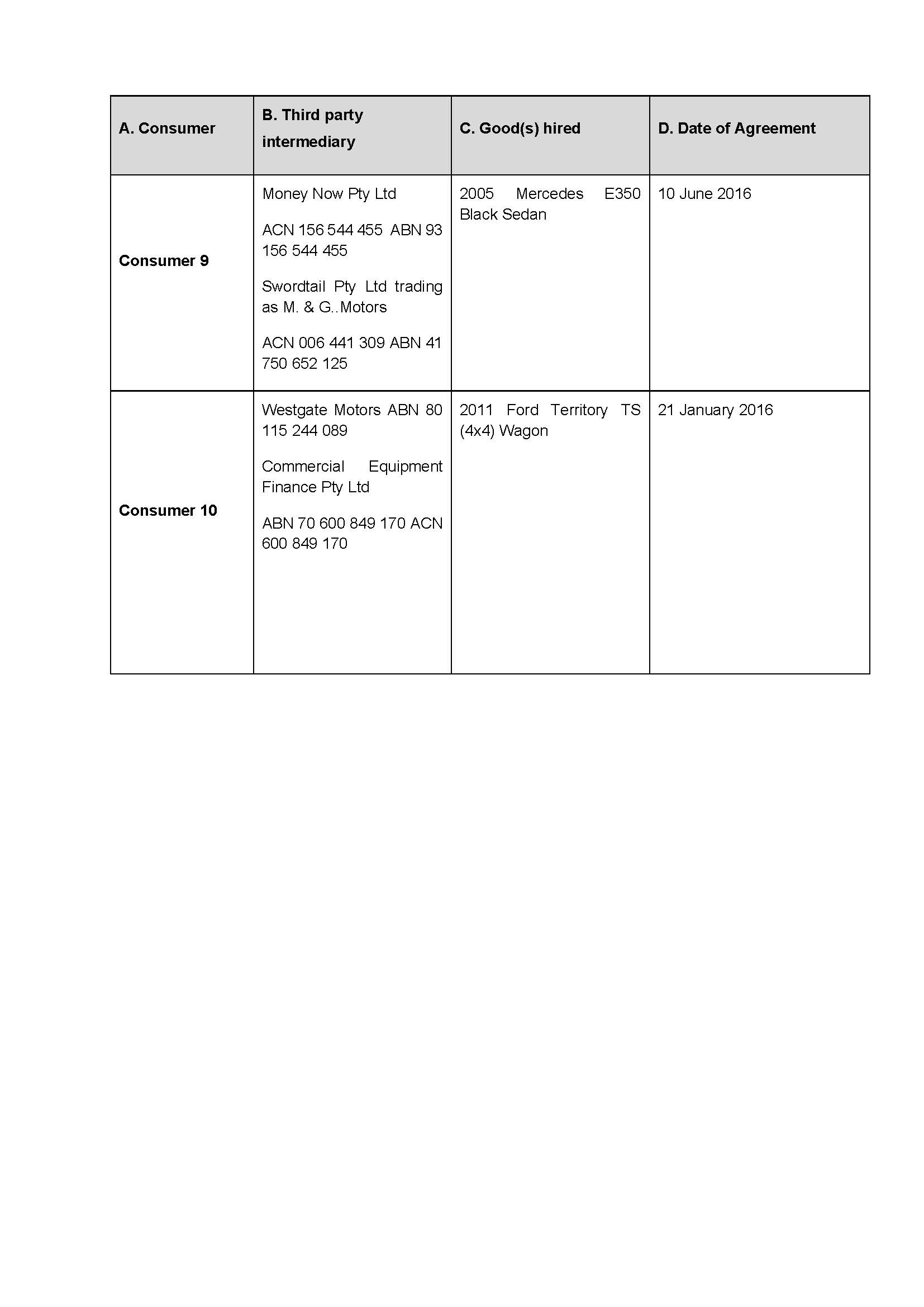

(a) section 29 of the National Credit Act on 10 occasions, on each occasion by engaging in the credit activity described in item 3(a) of s 6(1) of the National Credit Act, by being the lessor under a rental agreement (being a consumer lease) described in row A of Annexure A, Table 1 of the Amended Concise Statement filed in this proceeding (Agreement), when it did not hold a licence under the National Credit Act authorising it to engage in that credit activity; and

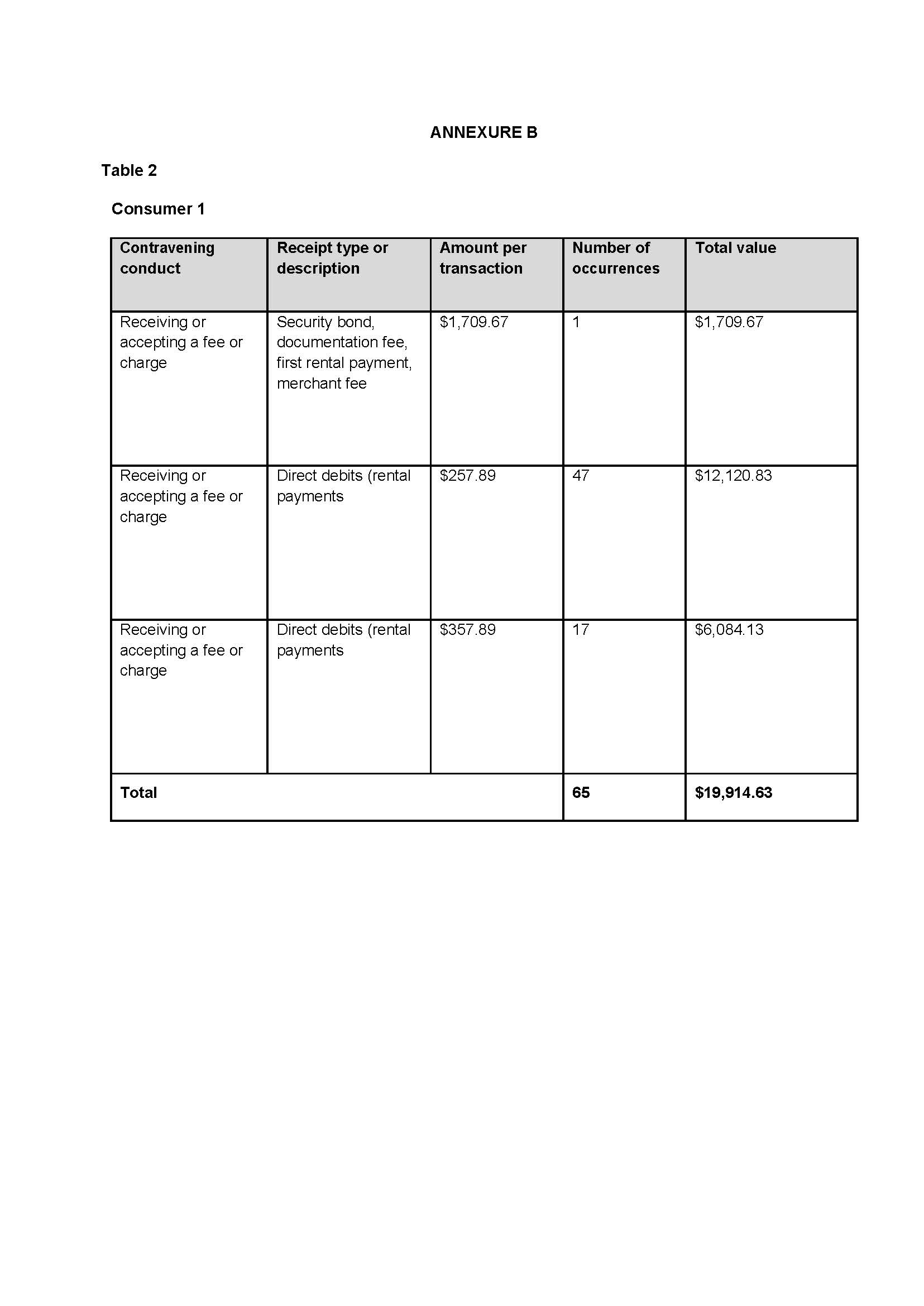

(b) section 32 of the National Credit Act on 295 occasions, on each occasion by demanding, receiving, and/or accepting fees, charges or other amounts from a consumer who was a party to an Agreement (as particularised in Annexure A, Table 2 of the Amended Concise Statement) for engaging in the credit activity described in item 3(a) of s 6(1) of the National Credit Act, when it did not hold a licence under that Act authorising it to engage in that credit activity.

29 As the form of the declaratory relief sought meets the requirements of s 166(3) of the National Credit Act, it is appropriate to make the declarations.

pecuniary relief

30 The making of the declaratory orders under s 166 of the National Credit Act founds the Court’s power to order GoGetta to pay a pecuniary penalty that the Court consider appropriate to the Commonwealth (s 167(2) of the National Credit Act). ASIC also seeks an order that GoGetta pay the Commonwealth pecuniary penalties for contravening ss 29 and 32 of that Act in the agreed amount of $750,000. The Court does not have to accept the agreed amount of the penalty, however as the High Court stated in Fair Work at [58], subject to the Court being sufficiently persuaded of the accuracy of the parties’ agreement as to facts and consequences, it is desirable that the Court accept the parties’ submissions on penalties, where it is satisfied that the penalty is appropriate in all the circumstances.

31 The relevant alleged contraventions occurred between 30 April 2015 and 21 December 2016. At the relevant times, a single contravention of either s 29 or s 32 of the National Credit Act attracted a maximum civil penalty of 2000 units. The penalty unit during that time was $170 until 30 July 2015 and $180 from 31 July 2015 to 30 June 2017. During the relevant period, s 167(3)(b) of the National Credit Act provided that the maximum penalty which may be imposed on a corporation for a contravention of a civil penalty provision is five times the maximum number of penalty units referred to in the relevant provision. Accordingly, the maximum civil penalties which may be imposed for GoGetta’s contraventions of ss 29 and 32 of the National Credit Act during the Relevant Period are:

(a) between 1 July 2014 and 30 July 2015, $1,700,000 (being 2000 x 5 x $170);

(b) between 31 July 2015 and 30 June 2017, $1,800,000 (being 2000 x 5 x $180).

32 Pursuant to s 167(3) of the National Credit Act, in determining pecuniary penalty, the Court must take into account all relevant matters, including:

(a) the nature and extent of the contravention;

(b) the nature and extent of any loss or damage suffered because of the contravention;

(c) the circumstances in which the contravention took place; and

(d) whether the person has previously been found by a court (including a court in a foreign country) to have engaged in similar conduct.

33 Other factors that are usually relevant include:

(a) the seriousness of the conduct and period over which it extended;

(b) the deliberateness of the conduct and whether the conduct was dishonest;

(c) the period of time over which the contraventions occurred;

(d) whether further contraventions are likely;

(e) whether the contravener has engaged in similar conduct in the past;

(f) whether the contravener has cooperated with ASIC in relation to the contravention;

(g) whether corrective measures have been taken by the contravener in response to an acknowledged contravention;

(h) whether the company had disgorged any profit or benefit received as a result of the contravention, or made reparation;

(i) the financial position of the contravener and its resources to pay a penalty

34 The list is not exhaustive nor a rigid catalogue or checklist of matters to be considered, however those factors may be taken to be relevant because they directly bear on the assessment of the penalty that is necessary to achieve general and specific deterrence: Volkswagen Aktiengesellschaft v Australian Competition and Consumer Commission [2021] FCAFC 49 at [150]. The overriding requirement is that the Court should weigh all relevant circumstances that bear on the assessment of an appropriate penalty in the circumstances of the case: Australian Securities and Investments Commission v GE Capital Finance Australia, in the matter of GE Capital Finance Australia [2014] FCA 701 (per Jacobsen J at [72]). In weighing and balancing the relevant factors, the Court must ensure that the penalty is just, bearing in mind the protective and deterrent purpose of a pecuniary penalty and the factors relevant to the contravention and the contravener: see Fair Work at [109].

35 The purpose for the imposition of a pecuniary penalty is to act as a specific deterrent to the contravener and as a general deterrent to others who might be tempted to contravene the law: Fair Work at 506 [55] per French CJ, Kiefel, Bell, Nettle and Gordon JJ (Gageler J agreeing at 511 [68], Keane J agreeing at 513 [79]); Australian Securities and Investments Commission v Australia and New Zealand Banking Group Ltd [2018] FCA 155 (ASIC v ANZ). The specific and general deterrent effect of pecuniary penalties is achieved by putting a price on a contravention that is “sufficiently high” to deter repetition by both the contravener and would-be contraveners: Fair Work at 506 [55] per French CJ, Kiefel, Bell, Nettle and Gordon JJ (Gageler J agreeing at 511 [68], Keane J agreeing at 513 [79]). In Singtel Optus Pty Ltd v Australian Competition and Consumer Commission (2012) 287 ALR 249; [2012] FCAFC 20 in a passage at p 265 at [62]–[63], approved by the High Court in Australian Competition and Consumer Commission v TPG Internet Pty Ltd (2013) 250 CLR 640; [2013] HCA 54 at [64] and [66], the Full Court explained the need to ensure that the penalty “is not such as to be regarded by that offender or others as an acceptable cost of doing business” and will deter those engaged in trade and commerce “from the cynical calculation involved in weighing up the risk of penalty against the profits to be made from contravention”. The penalty must also be proportionate to achieve the objective of specific and general deterrence, because the punishment should reflect what the offender has done: ASIC v ANZ at [7].

36 Ordinarily, where there are numerous contraventions arising from separate acts, each contravention should attract the imposition of a separate penalty. However it is also appropriate to consider whether, and the extent to which, the contravening conduct can be regarded as the same single course of conduct and penalised as one offence in relation to each category of contravention: ASIC v ANZ at [22]; Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union (2017) 254 FCR 68; [2017] FCAFC 113 at [145].

37 The contravening conduct in this case was serious. The contraventions are properly characterised as arising from a systemic failure by GoGetta from the outset to have an effective process for verifying business use in the conduct of its commercial rental business. Whilst GoGetta and SIV Capital were not subject to the obligations of Chapter 2 of the National Credit Act in respect of the rental and financing products they supplied to commercial customers, they did not have adequate processes and systems in place to ensure that the leases that GoGetta entered into were not consumer leases for the purposes of Chapter 3 of the National Credit Act. As a result, the 10 consumer leases the subject of this proceeding were entered into by GoGetta without the protection afforded to the consumers imposed by Part 3-4 of Chapter 3 of the National Credit Act. It is important to bear in mind that Part 3-4 of Chapter 3 of the National Credit Act imposes the obligation on a lessor to assess whether a consumer lease would be unsuitable for the consumer having regard to their ability to meet their financial obligations under the proposed lease or the consumer’s requirements and objectives and not to enter into the consumer lease if it would be unsuitable for the consumer. The failure to have adequate systems in place to ensure that leases were for business, not private or personal use, had the consequence of GoGetta providing consumer leasing services, albeit unintentionally. There was no suggestion that the contravening conduct was deliberate or the result of dishonest action, however it was submitted by ASIC that it was, or should have been, obvious to GoGetta that a business model providing leasing through intermediaries was open to use and abuse by intermediaries avoiding their obligations under Chapter 3 of the National Credit Act, because GoGetta was not required to comply with that regulatory regime. GoGetta may properly be criticised for its inattention and failure to consider whether customers would seek a rental agreement for a consumer purpose and its consequential failure to consider whether any measures should be put in place to address that risk. In mitigation, though, it would seem that such risk was relatively modest, as it is noted that there was no suggestion of systemic rorting or that endemic fraud existed. The more salient point is that the contraventions occurred because of GoGetta’s inattention to the adequacy of its own processes to ensure that none of the leases it entered into were consumer leases, including even after the possibility of contravention of s 29 of the National Credit Act was brought to its attention as far back as mid-2016. It was apparently only when ASIC took action and notified GoGetta of its investigation into the matter in mid July 2017, that GoGetta took steps to address the issue.

38 Significantly, however, since ASIC commenced its investigations and drew the contraventions to the attention of GoGetta, GoGetta has fully cooperated with ASIC, ceased this part of its business, admitted liability (save on the question of a number of contraventions which, initially, was the subject of dispute), acted swiftly to limit potential loss and damage to its customers, engaged Ernst & Young to conduct a review of its existing leasing and identify areas of concern, agreed to a court enforceable undertaking, agreed to (and implemented) a remediation program under which GoGetta and SIV Capital agreed to make remediation payments to affected customers, not to profit or retain any form of interest, or a fee or charge from an affected motor vehicle lease and not to seek to recover arrears or remaining payments from affected customers. GoGetta has, to date, complied with its obligations under the court enforceable undertaking and the remediation program. In its submissions to the Court, ASIC stated that it considered that “the level of cooperation by GoGetta since the commencement of ASIC’s investigation and during these proceedings has been exemplary”. Both parties submitted and I accept that these matters are significant mitigating factors that should be reflected in a significant discount to penalty. Another relevant consideration and mitigating circumstance in the assessment of penalty is that GoGetta has not been found to have engaged in similar conduct previously.

39 I am satisfied that a total pecuniary penalty of $750,000 is an appropriate penalty in the circumstances of the present case, taking all of these matters into consideration. In the overall circumstances, having regard to the mitigating factors, specific deterrence is not a significant factor and a weighty penalty is not necessary to achieve specific deterrence. In view of the fact that the contravening conduct was the result of system failures, rather than deliberate or dishonest conduct, and the significant mitigating factors of cooperation, admissions and remediation, it is also appropriate that there be a significant discount of the maximum penalty.

40 Both parties also submitted, and I accept that for the purpose of penalty, it is also appropriate that the 295 separate contraventions of s 32 (because GoGetta received multiple receipts in respect of each Rental Agreement) be treated as 10 courses of conduct, each constituting multiple receipts for a single Rental Agreement. It is also appropriate to treat the contraventions of ss 29 and 32 in respect of each Rental Agreement as a single course of conduct, given the close legal and factual relationships between the contraventions of s 29 and s 32 for each consumer and for the Court to determine a penalty on the basis of 10 courses of conduct. The contravening conduct under s 29 and s 32 was different, however the conduct was interrelated in that the contravening conduct under each provision was tied to GoGetta entering into, and being the lessor under the 10 Rental Agreements in question, without holding an ACL and exercising its rights as lessor under those rental agreements each time it accepted or received a payment without holding an ACL (s 32). The contraventions of s 32 are properly to be regarded as consequential to the primary contravention of entering into the Rental Agreements without an ACL in breach of s 29.

41 In my view, the agreed pecuniary penalty of $750,000 (or $75,000 per Rental Agreement) reflects the seriousness of the contravening conduct, is an amount that would not be regarded as an acceptable cost of doing business in relation to the 10 Rental Agreements and is sufficiently burdensome to act as general deterrence for others who engage in similar conduct, but which also makes appropriate allowance for the extensive mitigating factors. In the circumstances, it is appropriate to fix the pecuniary penalty in this amount.

I certify that the preceding forty-one (41) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Davies. |

Associate: