FEDERAL COURT OF AUSTRALIA

Australian Securities and Investments Commission v M101 Nominees Pty Ltd (No 3) [2021] FCA 354

ORDERS

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Plaintiff | ||

AND: | First Defendant JAMES PETER MAWHINNEY Second Defendant SUNSEEKER HOLDINGS PTY LTD Third Defendant | |

THE COURT NOTES THAT:

For the purpose of this order, the “Mawhinney Entities” means:

1. the Second Defendant in his personal capacity;

2. any superannuation fund of which the Second Defendant or any of his immediate family members is a member; and

3. any trust or company outside of the Mayfair 101 Group through which Mr Mawhinney holds personal investments or shares.

THE COURT ORDERS THAT:

1. For a period of 20 years from the date of these Orders, the Second Defendant, by himself, his servants, agents, employees and any company of which he is an officer or member, be restrained from:

(a) soliciting funds in connection with any financial product (as defined in Division 3 of Chapter 7 and s 9 of the Corporations Act 2001 (Cth)) (Financial Product)), including but not limited to products known as the M Core Fixed Income Notes, M+ Fixed Income Notes and Australian Property Bonds;

(b) receiving funds in connection with any Financial Product, including but not limited to products known as the M Core Fixed Income Notes, M+ Fixed Income Notes and Australian Property Bonds, other than financial products held by or issued to the Mawhinney Entities;

(c) advertising, promoting or marketing any Financial Product, including but not limited to products known as the M Core Fixed Income Notes, M+ Fixed Income Notes and Australian Property Bonds; and

(d) without a Court order, removing or transferring from Australia any assets acquired directly or indirectly with funds received in connection with any Financial Product, including but not limited to products known as the M Core Fixed Income Notes, M+ Fixed Income Notes and Australian Property Bonds, other than Financial Products held by or issued to the Mawhinney Entities.

2. Paragraphs 5, 6 and 7 of the orders dated 13 August 2020 be vacated.

3. The interlocutory application filed by the Second Defendant on 10 September 2020 be dismissed.

4. The Second Defendant pay the Plaintiff’s costs of the application for the injunction.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

[1] | |

[8] | |

[13] | |

[15] | |

[27] | |

[30] | |

[49] | |

[67] | |

[68] | |

[74] | |

[77] | |

[80] | |

[97] | |

[113] | |

[122] | |

[126] | |

[127] | |

[132] | |

[135] | |

[146] | |

[153] | |

[160] | |

[167] | |

[167] | |

[182] | |

Other evidence relied on by ASIC in respect of the various funds | [192] |

[194] | |

[195] | |

[208] | |

[209] | |

[232] | |

[233] | |

[245] | |

[247] | |

[249] | |

[255] | |

[257] | |

[258] | |

[268] | |

[276] | |

[277] | |

[279] | |

[287] | |

[288] | |

[289] | |

[289] | |

[297] | |

[300] | |

[301] | |

[303] | |

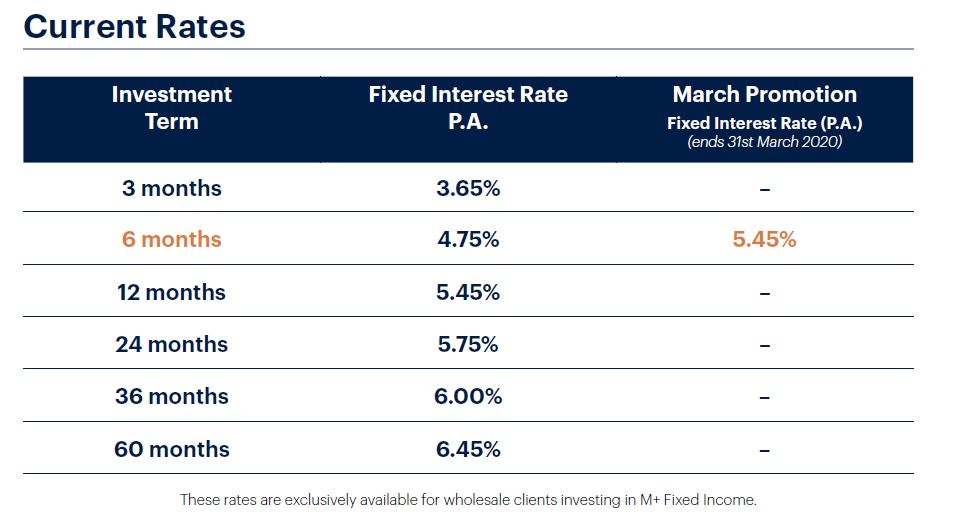

[304] | |

[315] | |

[317] | |

[320] | |

[323] | |

[324] | |

[325] | |

[328] | |

[334] | |

CONSIDERATION: PRINCIPLES RELATING TO MISLEADING AND DECEPTIVE CONDUCT | [335] |

CONSIDERATION: SUMMARY OF FINDINGS ON THE EVIDENCE AND OTHER MATTERS | [349] |

[350] | |

[351] | |

[352] | |

[365] | |

[369] | |

[380] | |

[381] | |

Section 79 of the Corporations Act and s 12GBCL of the ASIC Act | [388] |

[392] | |

[396] | |

[397] | |

[398] | |

[398] | |

[399] | |

[402] | |

[403] | |

[408] | |

[409] | |

Principles concerning s 1101B and s 1324 of the Corporations Act | [409] |

[415] | |

[427] | |

[428] | |

[433] | |

[433] | |

High propensity that the defendant may engage in similar activities or conduct | [437] |

[443] | |

[449] | |

Disregard for the law and compliance with corporate regulations | [451] |

[453] | |

[456] | |

[459] | |

[471] | |

[472] |

REASONS FOR JUDGMENT

ANDERSON J:

1 The Plaintiff (ASIC), by its Originating Process dated 7 August 2020, sought orders for the winding up of the First Defendant, M101 Nominees Pty Ltd (M101 Nominees), pursuant to s 461(1)(k) of the Corporations Act 2001 (Cth) (Corporations Act) on the ground that it is just and equitable. ASIC also sought injunctions pursuant to ss 1101B(1) and 1324(1) of the Corporations Act or s 23 of the Federal Court of Australia Act 1976 (Cth) (FCA Act) restraining the Second Defendant (Mr Mawhinney) from:

(a) receiving or soliciting funds in connection with any financial product, including but not limited to products known as the “M Core Fixed Income Notes” (Core Notes), the “M+ Fixed Income Notes” (M+ Notes) and the “Australian Property Bonds”;

(b) advertising, promoting or marketing any financial product, including but not limited to the Core Notes, the M+ Notes and the Australian Property Bonds; and

(c) removing or transferring from Australia any assets acquired directly or indirectly with funds received in connection with any financial product, including but not limited to the Core Notes, the M+ Notes and the Australian Property Bonds (together, the Injunction).

2 On 13 August 2020, I granted ASIC’s application for ex parte interim orders appointing Mr Said Jahani and Mr Philip Campbell-Wilson as joint and several provisional liquidators of M101 Nominees and granted the Injunction on an interim basis and made other orders (until further order) against Mr Mawhinney.

3 On 29 January 2021, I granted ASIC’s application seeking final orders that the provisional liquidators of M101 Nominees be appointed as liquidators of that company on the ground that it was just and equitable to do so: see Australian Securities and Investments Commissions v M101 Nominees Pty Ltd [2021] FCA 62.

4 This judgment concerns ASIC’s application that the Injunction which I granted on 13 August 2020 be made on a permanent basis. That application is opposed by Mr Mawhinney.

5 At the trial, Ms Caryn van Proctor of counsel appeared on behalf of ASIC. Mr William Newland of counsel appeared on behalf of Mr Mawhinney.

6 The First Defendant and Third Defendant did not make submissions in relation to the relief sought by ASIC in relation to Mr Mawhinney.

7 For the reasons that follow, I will make orders which, in short, restrain Mr Mawhinney from engaging in certain activities in relation to certain financial products for a period of 20 years.

SUMMARY OF THE EVIDENCE TENDERED

8 At trial, ASIC tendered in evidence, without objection from Mr Mawhinney’s counsel, a Court Book (CB) which included the following affidavits:

(a) an affidavit of an ASIC solicitor, Ms Dayle Buckley, affirmed 5 August 2020 (CB, Tab 2) (First Buckley Affidavit) (providing details of ASIC’s investigation) and 27 November 2020 (CB, Tab 9) (Third Buckley Affidavit) (providing information in relation to companies controlled by Mr Mawhinney, including IPO Wealth Holdings Pty Ltd and related entities (IPO Wealth Group) and IPO Capital Pty Ltd (IPO Capital));

(b) an affidavit of Jason Tracy affirmed 24 November 2020 (CB, Tab 6) (providing an independent expert opinion in relation to the security held over investments made by M101 Nominees);

(c) an affidavit of Hamish Mackinnon sworn 23 November 2020 (CB, Tab 4) (in relation to the IPO Wealth Group);

(d) an affidavit of an ASIC solicitor, Ms Lisa Saunders, sworn 6 November 2020 (in relation to service and advertising);

(e) an affidavit of Mr Peter Hui affirmed 15 January 2021 (CB, Tab 5) (an investor in the M+ Notes, who has not been able to redeem his investment);

(f) an affidavit of Mr Richard Rouse affirmed 19 November 2020 (CB, Tab 3) (an investor in the Australian Property Bonds, who has not received any interest payments or confirmation of his investment);

(g) an affidavit of Mr Kieran Egan sworn 25 November 2020 (CB, Tab 7) (an investor in IPO Capital, who has not been able to redeem his investment);

(h) an affidavit of Mr Jordan Hicks affirmed 15 January 2021 (CB, Tab 8) (an investor in IPO Capital, who has not been able to redeem his investment);

(i) the report of the provisional liquidators of M101 Nominees dated 24 September 2020 (CB, Tab 10).

9 On 29 January 2021, the solicitors acting for Mr Mawhinney in this proceeding advised the Court about certain matters which relate to this proceeding and proceeding VID 228 of 2020, being ASIC v Mayfair Wealth Partners Pty Ltd and others (Mayfair Proceeding). M101 Nominees is a party to both this proceeding and the Mayfair Proceeding. The solicitors for Mr Mawhinney in this proceeding advised the Court of the following:

The parties have conferred in relation to how the contest about the permanent injunctions might conveniently be dealt with and have reached the following agreement (subject to the convenience of the Court):

• The hearing of ASIC’s application for permanent injunctions against Mr Mawhinney be adjourned to 15-17 February 2021, when a hearing is already set down in the proceeding ASIC v Mayfair Wealth Pty Ltd (VID 228/2020) (Mayfair Proceeding) (the Mayfair Proceeding to be dealt with first, however, before this proceeding). The defendants in the Mayfair Proceeding are currently unrepresented, and on the basis that that matter will proceed undefended, ASIC’s estimate is that the Mayfair Proceeding will occupy 1 day;

• Evidence in the Mayfair Proceeding be evidence in this proceeding in relation to the permanent injunctions sought against Mr Mawhinney …

10 On 2 February 2021, I made the following order (among others) in this proceeding:

Evidence filed in proceeding VID228 of 2020 (ASIC v Mayfair Wealth Partners Pty Ltd & Others) is evidence in this proceeding in relation to the [ASIC’s] application for injunctions against [Mr Mawhinney] pursuant to paragraphs 4 and 5 of the Originating Process.

11 ASIC, pursuant to that order, relies upon the evidence in the Mayfair Proceeding as evidence in this proceeding, in relation to its application for permanent injunctions against Mr Mawhinney.

12 By reason of the correspondence to the Court dated 29 January 2021 from Mr Mawhinney’s solicitors, I am satisfied that Mr Mawhinney and his solicitors were on notice that evidence in the Mayfair Proceeding would be treated as evidence in this proceeding and that Mr Mawhinney had the opportunity to be heard in respect to the evidence tendered in the Mayfair Proceeding (to the extent it relates to this proceeding), but determined that the Defendants in the Mayfair Proceeding would be unrepresented and that the Mayfair Proceeding would proceed before the Court as an undefended matter. I am satisfied that, to the extent ASIC referred to evidence in the Mayfair Proceeding at the trial of this proceeding, Mr Mawhinney had a fair opportunity to confront and test that evidence.

EVIDENCE TENDERED BY MR MAWHINNEY

13 At the outset, it should be noted that, at trial, Mr Mawhinney did not tender any lay or expert evidence. Mr Mawhinney’s counsel cross-examined ASIC’s expert witness, Mr Tracy, with respect to the opinions he expressed in his expert report (to which I will come).

14 Significantly, Mr Mawhinney has not challenged the evidence of the liquidators relied upon by ASIC. Mr Mawhinney only sought to cross-examine the expert opinion of Mr Tracy. No other challenge was made to the evidence relied upon by ASIC.

TENDENCY EVIDENCE AND THE EVIDENCE RELIED ON BY ASIC

15 Before setting out the evidence relied on by ASIC, reference should be made to Part 3.6 (titled “Tendency and coincidence”) of the Evidence Act 1995 (Cth) (Evidence Act). Section 94(3) in that Part provides:

94 Application

…

(3) [Part 3.6] does not apply to evidence of:

(a) the character, reputation or conduct of a person; or

(b) a tendency that a person has or had;

if that character, reputation, conduct or tendency is a fact in issue.

16 Section 97 in Part 3.6 then provides:

97 The tendency rule

(1) Evidence of the character, reputation or conduct of a person, or a tendency that a person has or had, is not admissible to prove that a person has or had a tendency (whether because of the person’s character or otherwise) to act in a particular way, or to have a particular state of mind unless:

(a) the party seeking to adduce the evidence gave reasonable notice in writing to each other party of the party’s intention to adduce the evidence; and

(b) the court thinks that the evidence will, either by itself or having regard to other evidence adduced or to be adduced by the party seeking to adduce the evidence, have significant probative value.

(2) Paragraph (1)(a) does not apply if:

(a) the evidence is adduced in accordance with any directions made by the court under section 100; or

(b) the evidence is adduced to explain or contradict tendency evidence adduced by another party.

17 Section 99 provides that “[n]otices given under section 97 … are to be given in accordance with any regulations or rules of court made for the purposes of this section”. Regulation 7(2) of the Evidence Regulations 2018 (Cth) sets out the requirements for a notice under s 97(1).

18 In Aristocrat Technologies Australia Pty Ltd v Global Gaming Supplies Pty Ltd; Aristocrat Technologies Australia Pty Ltd v Allam [2013] HCA 21; 297 ALR 406, French CJ, Crennan, Kiefel, Gageler and Keane JJ stated that s 97 “must be read with s 94(1)” (at [30]).

19 In Allam v Aristocrat Technologies Australia Pty Ltd (No 2) [2012] FCAFC 75, Bennett, Middleton and Yates JJ stated that “[a] “fact in issue”, for the purposes of s 94(3), should be understood to mean “ultimate fact in issue” …” (at [33]). In Smith v The Queen [2001] HCA 50, 206 CLR 650, Gleeson CJ, Gaudron, Gumrnow and Hayne JJ stated at [7]:

In determining relevance, it is fundamentally important to identify what are the issues at the trial. On a criminal trial the ultimate issues will be expressed in terms of the elements of the offence with which the accused stands charged. They will, therefore, be issues about the facts which constitute those elements. Behind those ultimate issues there will often be many issues about facts relevant to facts in issue.

20 In Hughes v The Queen [2017] HCA 20, 263 CLR 338, Gageler J described the nature of tendency reasoning at [70]:

Applied to evidence of past conduct, tendency reasoning is no more sophisticated than: he did it before; he has a propensity to do this sort of thing; the likelihood is that he did it again on the occasion in issue.

21 Having regard to those principles, it will become apparent later in these reasons that much of the evidence ASIC relied upon was used as a basis for tendency reasoning. Broadly, ASIC relied on much of the evidence to submit that Mr Mawhinney has engaged in instances of certain past conduct, and, as a result, the likelihood is that Mr Mawhinney will engage in such conduct in the future.

22 Without more, that type of reasoning would be problematic because it would need to confront the tendency rule in s 97 of the Evidence Act in circumstances where ASIC has not complied with s 97(1)(a).

23 However, as stated above, Part 3.6 of the Evidence Act “does not apply to evidence of … the character, reputation or conduct of a person[,] or a tendency that a person has or had[,] if that character, reputation, conduct or tendency is a fact in issue”: Evidence Act, s 94(3).

24 In this proceeding, there are certain “ultimate facts in issue” which can be broadly stated as follows. First, has there been conduct which enlivens jurisdiction under s 23 of the FCA Act or ss 1101B or 1324 of the Corporations Act? Second, if there is such jurisdiction, does Mr Mawhinney have a tendency to engage in such conduct and is there accordingly a likelihood that Mr Mawhinney will engage in that conduct in the future? If there is an affirmative answer to that second issue, a legal issue arises as to what orders should be made (if any) to enjoin such conduct in the future in order to serve a relevant purpose within the contemplation of the Corporations Act.

25 In these circumstances, by reason of s 94(3) of the Evidence Act, Part 3.6 (including s 97(1)) “does not apply” to evidence which ASIC sought to use to prove the proposition that Mr Mawhinney has engaged in certain conduct and there is accordingly a likelihood that Mr Mawhinney will engage in that conduct in the future. As a consequence, I am satisfied that s 97 of the Evidence Act does not make inadmissible the tendency evidence which was the basis of a number of ASIC’s submissions. I should also observe that Mr Mawhinney’s counsel did not object to any evidence including tendency evidence being admitted into evidence.

26 I turn now to set out the evidence tendered by ASIC.

27 ASIC relies upon the following evidence to support the grant of permanent injunctions against Mr Mawhinney. That evidence largely concerned five products which ASIC contends were formulated and issued by entities controlled by Mr Mawhinney. Those five products or funds were:

(a) IPO Capital. I refer to the evidence relied on by ASIC in respect of IPO Capital below;

(b) the IPO Wealth Group. Evidence in respect of the IPO Wealth Group is referred to in more detail below;

(c) the Core Notes. By way of background, M101 Nominees received significant funds (approximately $65.6 million) from investors in the Core Notes, based on representations that there would be security for the full amount invested. Since 11 March 2020, M101 Nominees has been unable to repay funds invested in the Core Notes. The payment of interest to investors has also ceased. Evidence concerning the Core Notes is referred to in more detail below;

(d) the “M+ Notes”. The M+ Notes were unsecured promissory notes issued by M101 Holdings Pty Ltd (M101 Holdings). Evidence concerning the M+ Notes is referred to in more detail below;

(e) the “Australian Property Bonds”. Evidence relied on by ASIC concerning the Australian Property Bonds is referred to in more detail below. ASIC contends in respect of the Australian Property Bonds that Mr Mawhinney sought to raise funds from investors through this product. ASIC submits that investors in that product have not received interest payments due to them. ASIC submits that the Australian Property Bonds appear to be secured by properties at Mission Beach – that is, the same assets that are owned by various trusts that the relevant security trustee holds security over for the benefit of Core Notes investors. ASIC contends that Mr Mawhinney was seeking to raise funds for his stated purpose of improving “the Group’s liquidity position”: Rouse Affidavit [9]-22], [42] (CB Tab 3); First Buckley Affidavit [6.8], [132] (CB Tab 2).

28 In this proceeding there were various references to the “Mayfair 101 Group” of companies in various submissions and affidavits. That group of companies was not always precisely defined. This judgment will refer to the Mayfair 101 Group as comprising IPO Capital, the IPO Wealth Group, M101 Nominees, M101 Holdings and Mayfair Wealth Partners Pty Ltd (Mayfair 101 Group).

29 I turn to consider each of these aspects of ASIC’s evidence in more detail.

30 ASIC relied on a scheme which was referred to as IPO Capital. Set out below is the evidence referred to by ASIC in this regard.

31 Mr Mawhinney was the sole director of IPO Capital. The sole shareholder of IPO Capital was Online Investments Pty Ltd, and Mr Mawhinney was the sole shareholder in Online Investments Pty Ltd.

32 On 8 September 2016, Terry Marks of ASIC emailed a letter addressed to Mr Mawhinney, regarding IPO Capital. The letter stated (among other things):

ASIC is writing to you as the proprietor and director of [IPO Capital].

It has come to our attention that [IPO Capital], via the website http://www.120dayreturns.com/ (the Website), may be operating as a provider of Marketplace lending (peer-to-peer lending) products or otherwise providing financial services that require an Australian Financial Services (AFS) licence.

ASIC’s records indicate that neither [IPO Capital] nor yourself hold an AFS licence or authorisation as a representative of an AFS licence holder.

ASIC is also concerned that the Website may include content that is misleading, false or deceptive in relation to the provision of financial services, including but not limited to the stated returns and security of the investment offer.

…

ASIC is seeking further information to ensure that [IPO Capital] and you are complying with your obligations under the Act and ASIC Act.

33 ASIC sought various information from Mr Mawhinney. Mr Mawhinney provided certain materials in relation to ASIC’s request.

34 On 5 December 2016, Mr Don Christie of Astute Lawyers sent an email to ASIC attaching a letter dated 5 December 2016. The letter stated in part:

We advise that we act on behalf of [IPO Capital].

We have been provided with a copy of your letter to our client dated … 8 September 2016 …

We believe that there are a number of issues that are raised in your letter that our client needs to address.

We would like to discuss with you how the product might be “regularised” in order to move forward.

35 On 7 December 2016, ASIC emailed to Mr Christie a letter dated 7 December 2016. The letter states (among other things):

ASIC has serious concerns in relation to your client’s website www.120dayreturns.com (the First Website). Those concerns may be summarised as follows:

• IPO Capital may be issuing debentures, and it may need an AFS licence if it provides financial advice.

• If IPO Capital is issuing debentures, it is required to comply with Chapters 2L and 6D of the Corporations Act2001 [sic] (the Act).

• Alternatively, if IPO Capital is not issuing debentures then it may be issuing interests in an unregistered managed investment scheme; or miscellaneous financial products. These issues require a product disclosure statement (PDS) to be given.

• Additionally, ASIC takes the view that IPO Capital may be carrying on unauthorised banking business for the purposes of the Banking Act 1959 (Banking Act), legislation administered by APRA.

• IPO Capital’s claim that it works with Bell Potter is potentially misleading or deceptive.

Whilst we note that the content of the First Website appears to have been removed recently, ASIC notes that another website, www.ipocapital.com.au (the Second Website), a website associated with IPO Capital, remains current. ASIC is currently undertaking a review of the Second Website, and whilst it is evident that reference to Bell Potter has been removed, a preliminary view is that most of the concerns raised in relation to the First Website are still significant in relation to the Second Website.

36 On 9 December 2016, Mr Christie sent an email to ASIC, stating: “I was instructed last night that the IPO capital website will be down today and the Google adwords directions to it will be deleted”.

37 Mr Christie sent a letter to ASIC dated 4 January 2017. The letter stated (among other things):

… Since July 2016 funds have been raised by placing advertisements on Google adwords directing the potential investor to one of the websites for either Eleuthera [Group Pty Ltd], or IPO Capital from where they are invited to contact Mr Mawhinney.

Rates offered have varied.

…

Mr Mawhinney’s initial clients were sourced locally and from overseas.

While his initial contact was over the web each client was personally contacted.

His understanding was that he was able to raise up to $2m up to 12 months from up to 20 investors excluding sophisticated and foreign investors.

…

A number of investments have been in excess of $500,000 which we believe would automatically make them sophisticated investors under S708.

A number of investments have been made by overseas investors which would exclude them as investors under S708(5).

Use of the phrase “Term Deposits” was initially used on the 28 September 2016 iteration of the website however no traffic/marketing was directed to the website until 17 October 2016. Use of the phrase was deleted as at 15 November 2016 …

The website sought investments from sophisticated investors and while appropriate certificates were not obtained at the time of investment Mr Mawhinney has taken steps across December to rectify that issue by seeking the appropriate certificates or repaying smaller investors early with the return to date.

…

As stated above the google adwords and websites were shut down on 9 December 2016.

In the interim we have made inquiries with a view to ensuring the product is structured with appropriate licences, support services and provides a compliant Information Memorandum.

Discussion [sic] are underway (delayed by the Christmas break) with two parties, one which is prepared to appoint IPO Capital as an authorised representative for the purposes of issuing interests to sophisticated investors.

38 Attached to this letter was a list of investors in IPO Capital (presumably as at 4 January 2017). That attachment indicates that approximately 50 investors had invested.

39 On 11 January 2017, by email, Mr Christie informed ASIC that:

… IPO Capital has engaged Vasco Fund Managers (Vasco FM) to prepare in conjunction with IPO Capital: a wholesale unit trust based on classes of units and terms to match those currently offered to investors; and an information memorandum and application form suitable for sophisticated investors.

Once the Unit trust is formed Vasco FM will offer, subject to their final approval, a new entity and nominated personnel or contractors an authorisation or sub authorisation under their AFSL to act as fund manager.

40 On 19 January 2017, Mr Christie sent an email to ASIC attaching a draft Information Memorandum for the “IPO Wealth Fund” as well as a proposal from Vasco Investment Managers to establish a fund to invest in certain investments. The implication was that any investors in the non-compliant IPO Capital fund would be transferred to the compliant “IPO Wealth Fund”.

41 Pausing there, in relation to IPO Capital, ASIC relevantly referred to the affidavit of Mr Keiran Egan sworn 25 November 2020. Mr Egan is 67 years of age. Mr Egan deposes that:

… in approximately November 2016 I received a telephone call from the Managing Director, James Mawhinney. I cannot recall our exact conversation[.] [H]owever[,] I remember that James told me that the government’s bank guarantee was worthless …

42 On 8 November 2016, Mr Mawhinney sent the following email to Mr Egan:

Hi Kieran,

Good to speak with you a few minutes ago. I have just arranged for our Information Pack to be emailed over to you.

I can confirm that IPO Capital is Self-Managed Super Fund compatible. We have quite a number of Australian investors we work with who invest with us via their SMSF.

Term Deposit Rates

Our current term deposit rates are as follows -

• 3 months – 3. 40% p.a.

• 6 months – 3.65% p.a.

• 12 months – 3.95% p.a .

• 24 months – 4.25% p.a.

• 60 months – 5.25% p.a.

November Bonus Interest

Investors that come on board this month are entitled to a bonus 0.25% per annum on top of the rates above for the term of their deposit.

Next Steps

To proceed we just need the following –

• Deposit Agreement completed and returned by email or fax (see attached – I have amended it to include the bonus 0.25%)

• A copy of your driver’s licence or passport (please advise if you don’t have either of these)

• A copy of the transfer remittance advice

Feel free to contact me on the details below should you have any questions.

We look forward to welcoming you on board.

(Bold text in the original.)

43 Mr Egan’s affidavit records that, in July 2017 and September 2017, Mr Egan made investments of $100,000 and $200,000 respectively with IPO Capital. The “Investment Agreement” dated 12 July 2017 entered into by Mr Egan is branded as “IPO Capital”, while the agreement was with Eleuthera Group Pty Ltd (Eleuthera). In the Third Buckley Affidavit, Ms Buckley deposes that Eleuthera does not have a relevant Australian financial services licence. Mr Egan also received an “Account Statement” from IPO Capital dated 30 September 2020 in respect of Mr Egan’s investment.

44 In these circumstances, the unchallenged evidence is that, in 2017, Mr Mawhinney, by way of IPO Capital or Eleuthera, continued to raise funds from Mr Egan without an Australian financial services licence, despite ASIC putting Mr Mawhinney on notice of this non-compliance in September 2016. The evidence before the Court is that Mr Egan has still not received the return of his second investment, being an investment of $200,000, which had a maturity date of September 2019.

45 ASIC also referred to the affidavit of Mr Jordan Hicks affirmed 15 January 2021. Mr Hicks is 29 years of age. In July 2017, Mr Hicks invested $295,000 with “IPO Capital”. The majority of the funds for Mr Hicks’ investment were sourced from a compensation payment made to Mr Hicks following an injury he sustained at work. The “Investment Agreement” entered into by Mr Hicks is branded “IPO Capital” and is an agreement between Mr Hicks and Eleuthera. To recall, the evidence is that Eleuthera does not have an Australian financial services licence. Again, this unchallenged evidence shows that, in 2017, Mr Mawhinney, by way of IPO Capital or Eleuthera, was raising funds from investors after Mr Mawhinney was put on notice of the serious non-compliance issues raised by ASIC in September 2016. Mr Hicks deposes that, as at the date of his affidavit, he has “not received the return of [his] investment with IPO Capital”.

46 There are several other “IPO Capital”-branded “investment agreements” entered into between investors and Eleuthera which were dated in or around July 2017. These were exhibited to the Third Buckley Affidavit.

47 In short, the unchallenged evidence is that Mr Mawhinney, by way of IPO Capital or Eleuthera, continued to raise funds from investors after ASIC had raised concerns with Mr Mawhinney that an Australian financial services licence may be required and, in response, Mr Mawhinney arranged for the IPO Wealth Fund to be established under a third party’s licence. I refer to the IPO Wealth Fund below.

48 I find that such conduct as referred to above is a contravention of s 911A(1) of the Corporations Act. Section 911A(1) provides that “a person who carries on a financial services business in this jurisdiction must hold an Australian financial services licence covering the provision of the financial services”. There are exemptions to s 911A(1) in other subsections of s 911A, but none of these exemptions obviously apply and Mr Mawhinney has not filed any evidence which would indicate that the relevant entities could obtain the benefit of those exemptions.

49 As to the “IPO Wealth Group”, ASIC relied on an affidavit of Mr Hamish MacKinnon sworn 23 November 2020. Mr MacKinnon is a registered liquidator practising at Dye & Co Pty Ltd, Insolvency Practitioners and Chartered Accountants. Mr MacKinnon’s affidavit deposes to the following matters.

50 On 22 May 2020, Vasco Trustees Limited as trustee of the IPO Wealth Fund (Vasco) appointed Mr MacKinnon and Mr Nicholas Giasoumi as joint and several receivers and managers of the assets and undertaking of IPO Wealth Holdings Pty Ltd (IPO Wealth) and several other entities, which I will refer to collectively as the “IPO Wealth Subsidiaries”. IPO Wealth and the IPO Wealth Subsidiaries were generally referred to in this proceeding as the “IPO Wealth Group”.

51 On 2 July 2020, the Supreme Court of Victoria appointed Mr Giasoumi and Mr MacKinnon as joint and several provisional liquidators of IPO Wealth and the IPO Wealth Subsidiaries.

52 On 17 September 2020, the Supreme Court of Victoria appointed Mr Giasoumi and Mr MacKinnon as joint and several liquidators of IPO Wealth and the IPO Wealth Subsidiaries.

53 Mr MacKinnon and Mr Giasoumi have prepared a range of reports in relation to these entities. These reports were exhibits to Mr MacKinnon’s affidavit in this proceeding.

54 One of those reports is dated 27 August 2020. That report records the following matters.

55 Mr Mawhinney is the sole director of IPO Wealth and the IPO Wealth Subsidiaries. The sole shareholder of IPO Wealth is Online Investments Pty Ltd, and Mr Mawhinney is the sole director and shareholder of Online Investments Pty Ltd. The sole shareholder of the IPO Wealth Subsidiaries is IPO Wealth.

56 The report provided the following overview of the “IPO Wealth Fund”, IPO Wealth and the IPO Wealth Subsidiaries:

The IPO Wealth Fund

The IPO Wealth Fund is an unregistered unit trust governed by a Constitution dated 17 March 2017. Its trustee is Vasco Investment Managers Limited (Trustee). Investment in the IPO Wealth Fund was promoted by Information Memoranda. Investors are entitled to fixed “target” rates of return on their investments. Since its establishment, members of the public have invested more than $80 million in the IPO Wealth Fund. Some investments have been redeemed. There are currently 181 investors in the IPO Wealth Fund.

Loans by the Trustee to [IPO Wealth]

[IPO Wealth] borrowed moneys from the Trustee. The loan agreement between the Trustee and [IPO Wealth] provides that [IPO Wealth] agrees to pay to the Trustee an amount equal to 10 per cent per annum calculated and accruing daily on the outstanding balance of the loan. The loan is secured over the assets of [IPO Wealth] under a General Security Agreement.

Loans by [IPO Wealth] to the [IPO Wealth Subsidiaries]

In his recent public examination, Mr Mawhinney asserted that the funds borrowed by [IPO Wealth] from the Trustee were applied by [IPO Wealth] in acquiring shares in the [IPO Wealth Subsidiaries]. This is not consistent with the results of our investigations, which have led us to conclude that the funds were lent variously by [IPO Wealth] to the [IPO Wealth Subsidiaries] pursuant to executed loan agreements, one for each [IPO Wealth Subsidiary]. [IPO Wealth]’s loans to the [IPO Wealth Subsidiaries] are unsecured.

Investments by the [IPO Wealth Subsidiaries]

The [IPO Wealth Subsidiaries] invested the money they borrowed from [IPO Wealth] in various debt and equity investments. These investments were generally illiquid in nature and might not mature for a period of at least … three (3) years. During this period, the investments generally did not provide a return. This ultimately resulted in the IPO Wealth Group encountering significant cash flow issues, as the investments were not generating sufficient income or capital returns to enable [IPO Wealth] to pay the required interest to the Trustee. As a result, the Trustee was unable to meet investor redemptions and interest payments.

Further, as the investments were somewhat speculative in nature, there would inevitably be successes and failures. Losses encountered in failed investments would need to be covered by gains in successful investments in order to enable [IPO Wealth] to meet its obligations to the Trustee and the investors.

On 3 June 2020, the Trustee issued a Notice of Default and Demand to [IPO Wealth] for a total amount of $79,062,394.02 including unpaid interest, which [IPO Wealth] did not and does not have the capacity to pay when due.

It is of particular concern that some … investments [by the IPO Wealth Subsidiaries] … have been transferred out of the IPO Wealth Group to other entities within the broader Mayfair 101 group.

57 As to the management of IPO Wealth and the IPO Wealth Subsidiaries, the report states:

Mr Mawhinney is the sole director of all companies in the IPO Wealth Group. Mr Mawhinney gave evidence during the examination … that the [IPO Wealth Subsidiaries] largely operated off the one bank account of [IPO Wealth] and therefore any proceeds that were collected from the investments made by the [IPO Wealth Subsidiaries] would go directly into [IPO Wealth]. Accordingly, transactions between [IPO Wealth] and the [IPO Wealth Subsidiaries] can only be reconciled by reference to journal entries. The only financial statements for [IPO Wealth] that were completed and signed off by Mr Mawhinney were for the year ended 30 June 2017 at which stage [IPO Wealth] had only operated for a period of a little over 2 months. We have some concerns as to the accuracy of those financial statements with respect to:

• the reporting of management fees as income; and

• the investments held as at 30 June 2017.

It appears that potentially both the income received and the assets held may have been overstated as at 30 June 2017. The [IPO Wealth Subsidiaries] have never completed any financial statements and all of their accounts are still in draft.

The IPO Wealth Group has failed to produce any signed financial statements for the years ended 30 June 2018 and 30 June 2019. As a consequence, it has been difficult to come to a concluded view of any particular transaction recorded in the accounts as they are all effectively still in draft.

In his recent public examination, Mr Mawhinney gave evidence that the accounts are only in draft form and should not be relied upon in determining a true and correct position regarding transactions. He gave evidence that the primary accounting document was the Quarterly Investment Portfolio Summary which the IPO Wealth Group provided to [a certain] Trustee and that the accounts of [IPO Wealth] and the [IPO Wealth Subsidiaries] should be based on this report. One of the problems with this approach is that the Quarterly Investment Portfolio Summary has few working papers and does not appear to have been produced from a properly maintained set of books of account.

58 The report states:

During his public examination, Mr Mawhinney mentioned other persons involved in the administration of the affairs of the IPO Wealth Group, however, he acknowledged that he was the ultimate decision-maker in the group.

59 The report states:

… we have sufficient evidence to justify concerns with respect to: …

• poor documentation surrounding the acquisition of investments;

• agreements that have not been fully executed and security interests which were not registered on an appropriate securities register;

• investments that are, on the whole, illiquid in that their future realisation is likely to extend over many years;

• the acquisition of investments, the documented terms of which required interest

• payments, in circumstances where there was never any realistic prospect that such interest payments could be made;

• non-receipt of interest income on loans;

• a failure to attempt to collect interest payments which were overdue;

• documentation that suggested the ownership of shares in companies that did not reconcile with the share registers of those companies;

• inconsistent information as to whether convertible notes have been converted to equity;

• a lack of up-to-date information regarding a number of investments; and

• a lack of consistent information as to when investments were actually made.

60 The report further states:

Having regard to the [analysis set out in the report], we consider it uncontroversial that the [IPO Wealth] is presently insolvent. It is not able to pay the amount which it currently owes to the Trustee and it is unlikely to be able to do so in the future. Mr Mawhinney conceded in the examination that [IPO Wealth] was insolvent.

…

We are of the view that [IPO Wealth] had inherent problems in funding the interest and redemption requirements of the loan facility. This was not a matter of mere temporary illiquidity. The requirement that interest would be paid quarterly, and the entitlement of investors to redeem their investment at short notice, was at odds with the investment strategy of the IPO Wealth Group. The investments made by the Group were largely speculative, long-term in nature and generally did not provide any short-term return to the IPO Wealth Group. We note that only two of the investments … have provided cash income to [IPO Wealth] and [the IPO Wealth Subsidiaries] in the 2020 calendar year.

The first payment of a redemption to the Trustee by [IPO Wealth] was made on 3 October 2019. Within four months thereafter, [IPO Wealth] was in default of its loan obligations and it appears that subsequent interest and the repayment of redemptions were funded from director-related entities paying back funds which had been advanced to them by [IPO Wealth] up to July 2019.

This is a structural issue and pre-dated any effect of COVID-19.

We are also extremely concerned that Mr Mawhinney has:

• advanced significant monies to entities with which he was associated up until approximately July 2019;

• attempted to sell shares in Accloud PLC out of the IPO Wealth Group without proper care and diligence;

• altered the intended investment in the shares in the companies that owned Isola San Spirito to a long-term loan with an entity registered in the United Kingdom of which he is a director; and

• caused [IPO Wealth] to advance significant funds to 101 Investments Ltd and M101 Holdings Pty Ltd so that these entities could make their own investments with no benefit to the IPO Wealth Group from future income streams which might be generated by those investments.

As noted above, the first redemption from the Fund was made on 3 October 2019, only a day prior to [one of the IPO Wealth Subsidiaries] entering into an agreement to sell the Accloud PLC shares to [101 Investments Ltd] on 4 October 2019.

…

In summary, our preliminary investigations support a view that the insolvency of the IPO Wealth Group did not arise through temporary illiquidity, but came about through a structural liquidity issue connected to the performance of the underlying investments, and perhaps the design of the investment strategy.

61 As to the likely return to creditors, the report states:

Having regard to:

• the fact that all debt investments have ‘observable data’ of credit impairment; and

• none of the equity investments are particularly liquid,

it is presently our view that a full return to creditors is unlikely.

We have engaged corporate finance specialist to value and consider options for the realisation of the interest held [in a certain] investment. Of all the interests, this one is the most marketable (it is the only one generating cash income).

… However, depending on the recoveries from:

• realisation of 21,250,000 shares in Accloud PLC;

• the loan of $12,368,3210.25 from 101 IL;

• the loan of $3,266,204 against M101 Holdings Ltd; and

• the claim to the sale proceeds in the island of Venice,

we hold the view there will be a substantial shortfall to the Trustee.

62 As to potential claims which may arise out of the IPO Wealth Group, the report states:

We have formed the preliminary view that the claims set out below (among others) would be available to liquidators appointed to [IPO Wealth] and the [IPO Wealth Subsidiaries].

1. Recovery action in relation to:

(a) the loan of $12,368,3210.25 from [101 Investments Limited]; and

(b) the loan of $3,266,204 against M101 Holdings Ltd.

2. A claim to any sale proceeds arising out of [a certain] island in Venice.

3. Claims against Mr Mawhinney under Part 5.7B of the Corporations Act in relation to:

(a) the transfer of the Accloud shares to 101 Investments (on the basis that that transfer constituted an uncommercial transaction or an unreasonable director-related transaction);

(b) [transactions referred to as] the Poveglia and Retta share transfers to Okto Holdings (on the basis that those transfers constituted uncommercial transactions or unreasonable director-related transactions); and

(c) insolvent trading (in relation to [IPO Wealth] and each of the [IPO Wealth Subsidiaries]).

4. Claims against Mr Mawhinney for breaches of his directors’ duties and/or misleading or deceptive conduct in relation to:

(a) causing the Poveglia and Retta shares to be transferred to Okto Holdings, rather than [a certain IPO Wealth Subsidiary];

(b) causing the transfer of the Accloud shares to 101 Investments Ltd;

(c) capitalising expenses across the [IPO Wealth Subsidiaries] and inaccurately increasing their value (which arguably caused the companies to be put into provisional liquidation and/or wound up …).

Any claims based upon breaches of Mr Mawhinney’s duties as a director may be accompanied by applications for pecuniary penalties, relinquishment orders and/or compensation orders pursuant to Part 9.4B of the Corporations Act.

The above is a limited summary of the claims that may be brought by us if we were appointed liquidators of [IPO Wealth] and the [IPO Wealth Subsidiaries] …

63 ASIC relied on these matters to submit that Mr Mawhinney’s conduct, in relation to the IPO Wealth Group, was indicative of several instances of conduct which entailed an inherently risky and fatally flawed investment scheme formulated and implemented by Mr Mawhinney. In light of the evidence concerning the Core Notes, the M+ Notes and the Australian Property Bonds (to which I will come), I agree.

64 On the basis of this evidence, ASIC submits that the IPO Wealth Group, and its demise, had similar features to the Core Notes, M+ Notes and the “Australian Property Bonds” products (to which I will come). I agree. In particular, the report of the liquidators of the IPO Wealth Group stated that “[t]he investments made by the Group were largely speculative, long-term in nature and generally did not provide any short-term return to the IPO Wealth Group”. The report stated that there were “agreements that have not been fully executed and security interests which were not registered on an appropriate securities register”, and investments had been made which were, “on the whole, illiquid in that their future realisation is likely to extend over many years”. Those are features which are wholly consistent with the problems associated with the Core Notes and the M+ Notes products (to which I will come).

65 Mr Mawhinney did not tender any evidence which responded to the issues raised in the report of the liquidators of the IPO Wealth Group.

66 I turn now to set out the evidence concerning the Core Notes, M+ Notes and the Australian Property Bonds.

67 As indicated above, the First Defendant, M101 Nominees, was the issuer of a product which has been referred to in this proceeding as the “Core Notes”. Set out below is evidence relied on by ASIC in relation to the Core Notes.

Representations made to Core Notes investors

68 A brochure in respect of the Core Notes dated 12 December 2019 was annexed to the First Buckley Affidavit. The title page of that brochure included the following:

M Core Fixed Income

A secured, asset-backed, term-based investment opportunity exclusively available to wholesale investors[.]

(Bold text in the original.)

69 The brochure continued:

Tired of term deposits?

Activate your idle money and earn monthly distributions from a secured, asset-backed, term-based investment product.

Investing in our [Core Notes] product is a smart and effective way of earning competitive rates of return and monthly income whilst interest rates are at record lows. We invite you to invest in [the Core Notes], a secured, asset-backed term-based investment product offered by a forward-thinking group that is working to drive positive change in the financial services and investment industry.

(Bold text in the original.)

70 The brochure then included the following table:

71 The following text appeared below this table:

Mayfair Platinum is the manager of our [Core Notes] product, which is issued by M101 Nominees Pty Ltd (the Issuer). Investment funds raised under our [Core Notes] product are used for ongoing investment and capital management purposes across the Mayfair 101 group of companies, a regulated international investment and corporate advisory group with offices in Melbourne, Sydney and London.

(Bold text in the original.)

72 The following “Key Features” of the Cores Notes were listed:

• Supported by first-ranking, unencumbered asset security (see FAQs)

• A$250k minimum investment

• Fixed interest rates

• Monthly interest payments

• No setup or maintenance fees

• Dedicated Client Relationship Manager

• Individual, Company, Trust & Self-Managed Superannuation Fund (SMSF) compatible

• Available exclusively to wholesale investors

• Early redemption available (subject to liquidity and other applicable terms)[.]

73 The brochure contained a section titled “Frequently Asked Questions”, which stated (among other things) the following:

How is the [Core Notes] product secured?

The [Core Notes] product is secured by a pool of assets in respect of which first-ranking, registered security interests have been granted. The assets are otherwise unencumbered, and are made up of Australian real estate, assets held by Mayfair 101 Group entities, and cash from investors held in the Issuer’s dedicated M Core Fixed Income bank account. Such cash will only be used where there is dollar-for-dollar secured asset support.

A third party security trustee, PAG Holdings Australia Pty Ltd, (ACN 636 870 963, AFSL Auth. Rep. No. 001278649) of Perpetuity Capital Pty Ltd (ABN 60 149 630 973, AFSL 405364), as trustee of the Mayfair Platinum Secured Notes Security Trust, administers the secured pool of collateral assets on behalf of investors, and the assets are revalued at least yearly to ensure dollar-for-dollar secured asset support for each dollar of [the Core Notes].

Why should I choose Mayfair Platinum?

The Mayfair 101 group was established in 2009 and has assets spanning 10+ countries across a diverse range of sectors, including financial services, wealth management, technology, property and emerging markets. Our capital management strategy provides considerable geographic, industry & sector, business maturity, and currency diversification, which is a key reason why investors entrust their funds with us.

Is Mayfair Platinum regulated?

Yes. Mayfair Wealth Partners Pty Ltd (t/a Mayfair Platinum) is a corporate authorised representative (#00176207) of Quattro Capital Pty Ltd, which holds an Australian Financial Services Licence (#334653).

How can you pay fixed interest rates higher than the banks?

The interest rates we offer our investors are facilitated by the Mayfair 101 group’s capital management strategy. The group carefully selects opportunities to invest in that provide strong yields, capital growth, and refinancing opportunities that enable us to support principle [sic] and interest repayments to our investors.

Are my returns tied to the Issuer’s investment performance?

No. The Issuer is obligated to pay the quoted rates of interest and principal on the [Core Notes] product, regardless of the performance of its investments.

Is the Issuer a bank?

No. However, many [Core Notes] investors have chosen to move away from the banks due to historically low interest rates on term deposits and savings accounts. We operate by accessing capital from third parties (our investors), paying our investors for access to that capital, and utilising that capital to grow the Mayfair 101 group.

…

What are the risks?

Investors should be mindful that, like all investments, there are risks associated with investing in our [Core Notes] product. Risks to take into consideration include general investment, lending, liquidity, asset, interest rate, cyber, related party transactions and currency risks.

…

Can I withdraw my money out early if I need to?

Yes, although redemptions are subject to liquidity and other applicable terms. Please note this may be subject to a 1.5% early withdrawal and liquidity fee. Please provide 30 days’ notice in writing for amounts up to A$1m. For amounts above A$1m simply email your Client Relationship Manager and they will advise a repayment schedule within 2 business days.

Is the [Core Notes] product covered by the Australian Government’s Financial Claims Scheme (FCS)?

The Australian Government’s Financial Claims Scheme (FCS) (or ‘Government Guarantee’) doesn’t cover investments made in our [Core Notes] product. The Financial Claims Scheme has a limit of A$250k for each account holder per bank, and the banks have a bailout limit of just A$20b per bank. Be mindful that bank investments above A$250k aren’t covered by the Financial Claims Scheme, which is a reason why [the Core Notes] is worth considering for larger investment amounts.

(Bold text in the original; italicised text added.)

74 The terms of the Core Notes are set out in a “Secured Promissory Note Deed Poll” (Deed Poll) entered into by M101 Nominees on 24 October 2019. The Deed Poll was annexed to the First Buckley Affidavit and has the following relevant terms:

(a) M101 Nominees “decided to issue secured redeemable promissory notes, in accordance with, on the terms of, and subject to the conditions set out in, [the Deed Poll]”;

(b) the Deed Poll “binds [M101 Nominees] for the benefit of each Noteholder as if each such person were a party to [the Deed Poll], whether or not the person is in existence at the time of execution of this deed”: cl 2.1;

(c) M101 Nominees “may, in its discretion, agree to the issue of a Note or a number of Notes, as determined by [M101 Nominees] from time to time”: cl 3.1. The term “Notes” was defined as “secured redeemable promissory notes issued or to be issued by [M101 Nominees] under, and on and subject to the terms of, [the Deed Poll], which may be designated by [M101 Nominees] from time to time with a particular label or name, such as the “Mayfair Platinum Secured Notes” …”: cl 1.1;

(d) the Notes were “debt obligations of [M101 Nominees] owing under [the Deed Poll], take the form of entries in [a certain] Register and are evidenced by Note Certificates”: cl 3.5(a). “Each entry in the [relevant] Register constitutes a separate and individual acknowledgement to the relevant Noteholder of the indebtedness of [M101 Nominees] to that Noteholder”: cl 3.5(a);

(e) M101 Nominees could, “from time to time, determine to create a Note Class” which would “provide for all Notes issued under that Note Class to have the same: … (i) name; (ii) Face Value; (iii) Note Term …; (iv) Maturity Date; and (v) Interest Rate”: cl 3.2(a). The “Maturity Date” was defined as: “with respect to a Note, the last day of the Note Term”. The “Interest Rate” was defined as “the interest rate which applies to the debt obligation arising under a Note, which is determined by its Note Class”: cl 1.1. The “Note Term” was defined as “the period of the loan conferred by the Note which is specified by its Note Class, and which begins on and from the date the Note is issued”: cl 1.1;

(f) M101 Nominees was required to “calculate interest on the Monies Owing in respect of each Note daily on the balance of the Monies Owing, on the basis of a yearly interest rate equal to the Interest Rate, and a year of three hundred and sixty-five (365) days”: cl 4.1;

(g) M101 Nominees was required to “pay interest which accrue[d] … to the Noteholder, on a calendar monthly basis, with payment due within five (5) Business Days following the end of the relevant calendar month”: cl 4.3(a);

(h) a “Noteholder [could] notify [M101 Nominees] in writing that it require[d] all or a number of the Noteholder’s Notes to be redeemed on the Maturity Date, by submitting a Withdrawal Notice”: cl 5.1(a). If “a Withdrawal Notice [was] not received by [M101 Nominees] by thirty (30) days before the Maturity Date”, the Notes “automatically roll[ed] over at the end of the Note Term, for a further period equal to the Note Term”: cl 5.1(b);

(i) a “Noteholder [could] request that [M101 Nominees] redeem all or a number of the Noteholder’s Notes on a date which [was] before the Maturity Date … by submitting a Withdrawal Notice”: cl 5.1(a). However, the “Noteholder acknowledge[d] that [M101 Nominees was] under no obligation to agree to an Early Withdrawal Request, and [could] refuse to do so for any reason in [M101 Nominees’] sole and absolute discretion, with or without stating its reasons”: cl 5.2(b);

(j) “[u]pon redemption of any Notes”, M101 Nominees was required to “pay the Noteholder the total amount of the Monies Owing on those Notes calculated as at the Withdrawal Date”: cl 5.5(a). There was “no priority of payments between Noteholders”: cl 5.5(d). M101 Nominees could “in its absolute and sole discretion … pay any one … Noteholder in priority to any other Noteholder”: cl 5.5(d);

(k) M101 Nominees could, “at any time, extend the Payment Date”, if M101 Nominees:

(i) “in its reasonable opinion, consider[ed] that it [did] not have sufficient Liquidity to fund the redemption”;

(ii) “received multiple Withdrawal Notices in a short period which will have a negative impact on its Liquidity”;

(iii) “consider[ed] that if the redemption [was] paid on the Payment Date, it may [have] affect[ed] [M101 Nominees’] Liquidity to pay future anticipated redemptions of other Noteholders’ Notes”: cl 5.6(a).

75 Clause 3.6 of the Deed Poll provides:

3.6 Notes secured

(a) Secured – The Notes are secured redeemable promissory notes.

(b) STD - Certain parties will from time to time provide security for the payment by [M101 Nominees] of amounts due in respect of the Notes, to be held by a security trustee on behalf of the Noteholders, under the terms of the Security Trust Deed.

(c) Attorney - Each Noteholder, for consideration received, appoints the security trustee under the Security Trust Deed and each officer for the time being and from time to time of that security trustee severally its attorney, in its name and on its behalf, to do all things and execute, sign, seal and deliver (conditionally or unconditionally in the attorney’s discretion) all documents, deeds and instruments necessary or desirable in respect of the Security Trust Deed.

(Underlining and bold text in the original.)

76 The “Security Trust Deed” was defined as:

“Security Trust Deed” means the Security Trust Deed dated on or about the date of [the Deed Poll] entered into by [M101 Nominees] and other parties, under which certain parties provide security for the payment by [M101 Nominees] of amounts due in respect of the Notes, to be held by a security trustee on behalf of the Noteholders …”

77 M101 Nominees and PAG Holdings (Australia) Pty Ltd (PAG Holdings) entered into a “Security Trust Deed” on 24 October 2019 (Security Trust Deed). For present purposes, relevant terms of the Security Trust Deed were as follows:

(a) PAG Holdings declared “that it holds the sum of ten dollars (A$10) … and will hold the Trust Fund on trust for the Security Beneficiaries from time to time on the terms of this deed”: cl 4.1. The “Trust Fund” included (among other things) “all money paid to” PAG Holdings under the Security Trust Deed: cl 1.1. The “Security Beneficiaries” referred to “all and each of the Noteholders from time to time” and “the Security Trustee in its personal capacity as Security Trustee”: cl 1.1. The Trust was to be known as the “Mayfair Platinum Secured Notes Security Trust”: Schedule 1;

(b) subject to the Security Trust Deed, PAG Holdings was “entitled to exercise all Powers under the Securities (including those Powers conferred on trustees generally by statute and those conferred on trustees generally by law or equity in respect of the Securities) as if [PAG Holdings was] the sole beneficial owner of the Securities …”: cl 8.1(a);

(c) PAG Holdings was “irrevocably appointed and authorised by the Security Beneficiaries to enter into the Securities and other Finance Documents to which it is expressed to be a party and act as trustee for the Security Beneficiaries and to enforce the rights under or in relation to the Securities and those other Finance Documents on behalf of the Security Beneficiaries in accordance with the Finance Documents”: cl 8.1(c);

(d) “[d]espite anything else in” the Security Trust Deed “or any other Finance Document”, M101 Nominees was required to “procure that at all times the Over-arching Obligations [were] complied with”: cl 10.6. Those “Over-arching Obligations” included the following:

Security - There are sufficient Security Providers providing sufficient Security in connection with this deed, to comply with any statements contained in the Information Memorandum regarding the nature, amount or sufficiency of Security Interests supporting the making of payments due in respect of the Notes. [The “Information Memorandum” was defined as “the information memorandum, by whatever name called (such as brochure, disclosure or offer document), issued from time to time by the Grantor to prospective or actual Noteholders regarding the details of arrangements relating to the Notes”: cl 1.1];

Use – [M101 Nominees] uses all or any part of any Security Property from time to time only and solely for ongoing investment and capital management purposes across the corporate group of which [M101 Nominees] is a member (the “Company Group”).

Security Interests – [PAG Holdings] holds the benefit of first (1st) ranking Security Interest(s) in assets, registered in the relevant statutory register, in favour of [PAG Holdings] under the terms of, and covered as Security Property by, this deed, of a value which is at least equal to all amounts due in respect of all Notes outstanding, where such assets must be either:

(a) cash – the account of the Grantor with the financial institution, and with the details, referred to in the Specific Security Deed Poll (Bank Account) dated on or about the date of this deed and entered into by [M101 Nominees] in favour of [PAG Holdings] and all moneys from time to time in that account, in respect of which a first (1st) ranking Security Interest granted under that deed in favour of [PAG Holdings] is registered in the Personal Property Securities Register established under section 147 (Personal Property Securities Register) of the Personal Property Securities Act 2009 (Cth) (the “PPS Register”);

(b) real estate – Australian real estate, owned by a member of the Company Group, in respect of which a first (1st) ranking mortgage in favour of [PAG Holdings] is registered in the Land Registry of the relevant Australian State or Territory;

(c) specific assets – specific, identifiable, tangible assets, with or without a serial number, owned by a member of the Company Group, in respect of which a first (1st) ranking Security Interest granted under a specific security agreement or deed in favour of [PAG Holdings] is registered in the PPS Register; or

(d) general assets – all or other present and after-acquired property owned by a member of the Company Group, in respect of which a first (1st) ranking Security Interest granted under a general security agreement or deed in favour of [PAG Holdings] is registered in the PPS Register …

(Emphasis added.)

78 In a letter to ASIC from PAG Holdings’ solicitors dated 29 June 2020, PAG Holdings’ solicitors stated that the “primary purpose of the [Mayfair Platinum Secured Notes Security Trust] is for [PAG Holdings] to hold security in relation to redeemable promissory notes issued by [M101 Nominees] to noteholders”.

79 There was expert evidence about the security arrangements which were in fact implemented in relation to the Core Notes. I turn to set out that evidence.

The Expert Opinion of Mr Tracy

80 ASIC tendered and relied on an affidavit of Mr Jason Tracy of Deloitte affirmed 24 November 2020. Mr Tracy’s affidavit annexed five documents, namely:

(a) a letter of instruction to Mr Tracy from ASIC dated 25 May 2020 (which was annexure “JMT-2”);

(b) a letter of instruction to Mr Tracy from ASIC dated 1 June 2020 (which was annexure “JMT-3”);

(c) an expert opinion dated 12 June 2020 (which was annexure “JMT-1”);

(d) a supplementary expert opinion dated 12 August 2020 (which was annexure “JMT-4”);

(e) a second supplementary expert opinion dated 14 September 2020 (which was annexure “JMT-5”) (collectively, Expert Opinion): see Tracy Affidavit, Annexures “JMT1”, “JMT4” and “JMT5” at CB, Tab 6.1, 6.4 and 6.5.

81 Mr Tracy is a Chartered Accountant, having been admitted as a member of Chartered Accountants Australia and New Zealand. Mr Tracy is also a Registered Liquidator. He has in excess of twenty years’ experience in the external administration of corporate entities and the assessment of entities on behalf of financial institutions and other debt providers. Mr Tracy also has experience in providing expert evidence in matters concerning the financial performance and position of corporate and other entities, as well as insolvency-related matters.

82 Mr Tracy was asked for his opinion on (among other things) whether the debts owed to Core Notes investors were secured and, if so, “[w]hat form does that security take”, “[o]ver what assets is there security”, and “[w]hat is the value of that security?”

83 At [3.4]-[3.6] of the expert opinion dated 12 June 2020, Mr Tracy described the Core Notes as follows:

Core Notes are secured promissory notes issued by M101 Nominees. Core Notes were promoted as only available to wholesale investors with a minimum investment threshold of $250,000, for an investment term of six to 60 months. Interest was to be paid monthly at a fixed rate dependent on the investment term regardless of investment performance.

Core notes were promoted as a “secured, asset backed, term-based investment”, with a key feature being that they were supported by “first ranking, unencumbered asset security”. Secured assets for Core Note investors comprise of cash in a bank account held in the name of M101 Nominees, real property assets in the Mission Beach region, Queensland, deposits paid for the purchase of real properties and loans made to related parties.

The real property assets are held in trusts which Sunseeker Holdings is the unit holder. Security over the trust assets is generally established through a suite of security documents, whereby a third-party security trustee, PAG Holdings Australia Pty Ltd (PAG) which represents the interest of investors, is the secured party. As at 20 March 2020 a total of $59,208,332 was invested in Core Notes.

84 At [3.9], Mr Tracy’s 12 June 2020 expert opinion notes:

The Core Note investment brochure outlines the ability of M101 Nominees to freeze redemptions in the event of liquidity constraints. On 11 March 2020, M101 Nominees froze all redemptions due to liquidity concerns.

85 In relation to whether the debts owed to Core Notes investors were secured, Mr Tracy stated the following in his 12 June 2020 expert opinion:

(a) in relation to cash held in M101 Nominees’ bank account, Mr Tracy noted that, as at 31 December 2019, M101 Nominees held cash at bank of $5,274,908. However, as at 20 March 2020, M101 Nominees’ cash at bank was $572,561. Mr Tracy stated that, “[g]iven the security was in place prior to 31 December 2019 and 20 March 2020, it appears to me that this asset is secured”. However, Mr Tracy noted that he did “not have bank statements to verify the bank account balances at those dates”;

(b) in relation to a loan made to Eleuthera by M101 Nominees, Mr Tracy stated:

The loan agreement between M101 Nominees and Eleuthera (a related party) is titled Facility Agreement. The facility agreement does not detail any information relating to proposed security arrangement in respect to the loan, nor does it detail the purpose of the loan. The loan commenced on 18 October 2019, has a limit of $250m, attracts an interest rate of 8.0% per annum and is for an initial term of 10 year with an option to extend. Full repayment is due before the expiry date, unless otherwise agreed in writing between the lender and the borrower.

(c) in respect of “[r]eal properties and deposits paid on properties but not settled”, Mr Tracy stated:

In respect to assets held in Mainland Property Holdings Pty Ltd (MPH) ATF Mission Beach Property Trust (MBPT) (82 properties, 30 deposits paid on properties not settled at 20 March 2020), I comment as follows: … Except for one real property at 999 Seaview Street, Mission Beach, [the security trustee] did not have direct first mortgage security over the other properties held in MBPT at 31 December 2019 or 20 March 2020. In fact, it appears that a third party lender, Naplend Pty Ltd (Naplend)[,] has first registered mortgages on all titles except for one title, where it appears Australia and New Zealand Banking Group Ltd (ANZ) is first registered at 31 December 2019 and 20 March 2020.

…

In respect to assets held in Mainland Property Holdings No 2 Pty Ltd (MPH2) ATF Mission Beach Property Trust No 2 (MBPT2) (24 properties, 54 deposits paid on properties not settled at 20 March 2020), I comment as follows: … [the security trustee] does not have direct first mortgage security over any of the properties held in MBPT2 at 31 December 2019 or 20 March 2020. In fact, it appears that a third party lender, Naplend[,] has first registered mortgages on all titles.

…

In respect to assets held in Mainland Property Holdings No 3 Pty Ltd (MPH3) ATF Mission Beach Property Trust No 3 (MBPT3) (11 properties and 19 deposits paid on properties not settled at 20 March 2020), … [the security trustee] does not have direct first mortgage security over any of the properties held by MBPT3 at 31 December 2019 or 20 March 2020. In fact, it appears that a third party lender, Naplend[,] has first registered mortgages on all titles.

…

In respect to assets held in Mainland Property Holdings No 8 Pty Ltd ATF Mission Beach Property Trust No 8 (MBPT8) (1 property at 20 March 2020), … [the security trustee] does not appear to have first registered security at 31 December 2019 or 20 March 2020. According to the PPSR it appears [the security trustee]’s security was registered on 23 April 2020 and 15 May 2020 respectively, being after the date the property appears to have been acquired and after AllPAAP security was registered by Naplend and the Trustee for Naplend No 13. In the absence of a priority deed or other instrument giving priority it would appear the security interests of Naplend are ahead of Core Note investors.

…

In respect to the asset held in Mayfair Asset Holdings Pty Ltd (MAH) ATF Mayfair Island Trust (MIT) (1 property at 20 March 2020), … [the security trustee] does not have direct first mortgage security over the property held by MIT at 31 December 2019 or 20 March 2020. In fact, it appears that a third party, Family Islands Group Pty Ltd (Family Group) has registered mortgages on all titles.

…

In respect to the assets held [by various other relevant trusts], I comment as follows:

(a) According to the PPSRs it appears in all instances that [the security trustee]’s security was registered on 23 April 2020 and 15 May 2020 being after the date the deposits appear to have been paid in respect to properties not settled.

(b) Based on the information made available to me there is a significant risk that [the security trustee] did not have first security at 31 December 2019 and 20 March 2020 despite deposits on properties not settled having been paid.

(c) In respect to the deposits paid on properties not settled, I am concerned that these may be at risk of forfeiture for failure to complete on the real property transactions.

…

In respect to assets held in Jarrah Lodge Holdings Pty Ltd ATF Jarrah Lodge Unit Trust No 1 (JLUT), … [the security trustee] does not appear to have first registered security. According to the PPSR it appears [the security trustee’s] security was registered on 16 April 2020, 23 April 2020 and 15 May 2020, all being after the date the loan appears to have been made and after AllPAAP security was registered by Naplend … on 23 December 2019 over JLUT.

…

(Emphasis added.)

86 At [2.11] – [2.16], Mr Tracy’s expert opinion dated 12 June 2020 concludes as follows concerning the security in place:

While various security arrangements have been entered into between [the Security Trustee] as security trustee, M101 Nominees and the various trustees, it would appear, with one exception, that [the security trustee] does not have direct first mortgage security over the real properties held in the various trusts at 31 December 2019 and 20 March 2020.

It also appears that deposits were paid on properties in instances where there was no security registered on the PPSR in favour of [the Security Trustee] at the time of the deposit being paid, including at 31 December 2019 and 20 March 2020.

Further, in relation to the two related party loans, one of the loans appears to have had no security registered on the PPSR at 31 December 2019 and 20 March 2020, while the other appears to have a prior registered third party security at 20 March 2020.

… [I]n my opinion, there are a significant number of instances where Core Note investor security was not first ranking and the assets were not otherwise unencumbered at 31 December 2019 and 20 March 2020.

…

In respect to the loan to [Eleuthera by M101 Nominees], it appears that the loan is not secured. There is no security interest registered by [the security trustee] against Eleuthera on the PPSR and the documents made available to me make no reference to security being provided in respect to that loan at 31 December 2019 or 20 March 2020.

(Emphasis added.)

87 At [2.24], Mr Tracy’s expert opinion dated 12 June 2020 states:

In summary, it would appear that Core Note investor funds were not and are not generally supported by first-ranking, unencumbered asset security at 31 December 2019 and 20 March 2020.

(Emphasis added.)

88 Mr Tracy’s expert opinion dated 12 June 2020 also sets out further concerns regarding the asset security value, at [2.25] and [2.26]:

In the absence of a funds flow showing the receipt of Core Note investor funds and payment from the M101 Nominees bank account, it is unclear whether all the funds from Core Note investors have flowed to secured assets.

I have a number of concerns regarding the asset security values for Core Note investors:

(a) There is a risk that prior registered security holders may be able to escalate their facilities and appoint receivers. In the event this happens, asset values and the recovery of funds to Core Note investors could be negatively impacted.

(b) There is a risk given [Mayfair] was active in acquiring a large number of properties from October 2019 to April 2020 that these entities established a market price in an otherwise illiquid and small property market at Mission Beach. Consequently, there is a risk that the contract price in each sale contract is above market price in today’s terms, negatively impacting the asset security values and recovery of funds to Core Note investors.

(c) The deposits paid on the properties not settled totalling $5,852,387 at 20 March 2020 may be at risk of forfeiture due to failure to complete, especially if significant additional funds of $86,483,036 cannot be sourced to settle these transactions. It is unclear to me where these additional funds would come from.

(d) The financial capacity of the related entities to repay the loans received from M101 Nominees is unclear in the absence of financial information outlining their financial position, historical and forecast performance.

(e) The basis of the 4% uplift totalling $2,983,400 at 20 March 2020 applied by M101 Nominees to the carrying value of the 119 real property assets, including Dunk Island is not well supported by the documents made available to me. If this amount is excluded, there would appear to be a deficiency of $2,732,540 to Core Note investors, assuming full recovery of all other secured assets in line with M101 Nominees report to [the Security Trustee] at 20 March 2020.

89 Mr Tracy provided a further expert opinion dated 12 August 2020 which stated at [2.5]-[2.8]:

The new documents [provided to Mr Tracy and] listed in Appendix 2 do not cause me to change my opinion outlined in my First Report, that [the security trustee] does not have direct first mortgage security (with one exception noted in my First Report) over the real properties held in the various trusts at 31 December 2019 and 20 March 2020.

…

The new documents listed in Appendix 2 do not cause me to change my opinion outlined in my First Report, that it appears there were deposits paid in instances where there was no security registered on the PPSR in favour of [the security trustee] at the time the deposit was paid, including at 31 December 2019 and 20 March 2020.

…

The new documents listed in Appendix 2 do not cause me to change my opinion in respect to the security position of the loan to Eleuthera as outlined in my First Report at 31 December 2019 and 20 March 2020, that is, that the loan is not secured.

The new documents listed in Appendix 2 do not change my opinion in respect to the loan to [Jarrah Lodge Holdings Pty Ltd as trustee for the Jarrah lodge Unit Trust No 1 (JLUT)] as outlined in my First Report that [the security trustee] does not hold first ranking unencumbered asset security at 31 December 2019 and 20 March 2020 …

In summary, I confirm my opinion in my First Report that it would appear that Core Note investor funds were not and are not generally supported by first-ranking, unencumbered asset security at 31 December 2019 and 20 March 2020.

(Emphasis added.)

90 As to the value of the security held by the relevant security trustee, Mr Tracy’s expert opinion dated 12 August 2020 stated at [2.9]: