Federal Court of Australia

Quintis Ltd (Subject to Deed of Company Arrangement) v Certain Underwriters at Lloyd’s London Subscribing to Policy Number B0507N16FA15350 (No 2) [2021] FCA 327

File number: | NSD 733 of 2020 |

Judgment of: | LEE J |

Date of judgment: | 6 April 2021 |

Catchwords: | EQUITY – rectification – policies of insurance – policies represent bundle of contracts between insured and insurer – consideration of intention of ten insurers – where common intention found between insured and some insurers – form of relief – whether relief can be calibrated to give effect to common intention found – whether relief impermissibly transforms bargain struck – consideration of rationale of rectification and limits on equity’s intervention – exact form of words in which common intention framed immaterial as long as in substance parties’ intention can be ascertained – consideration of contractual structure – common intention as to bilateral rights and obligations of insured and each insurer – equity available – simply bringing policies to a form consistent with common intention of parties – relief granted |

Legislation: | Federal Court of Australia Act 1976 (Cth) s 43 |

Bush v National Australia Bank Ltd (1992) 35 NSWLR 390 Club Cape Schanck Resort Co Ltd v Cape Country Club Pty Ltd [2001] VSCA 2; (2001) 3 VR 526 Crane v Hegeman-Harris Co Inc [1939] 1 All ER 662 Crane v Hegeman-Harris Co Inc [1939] 4 All ER 68 EMI Songs Australia Pty Ltd v Larrikin Music Publishing Pty Ltd [2011] FCAFC 92 Fowler v Fowler (1859) 4 De G & J 250 Franklins Pty Ltd v Metcash Trading Pty Ltd [2009] NSWCA 407; (2009) 76 NSWLR 603 General Reinsurance Corporation v Forsakringsaktiebolaget Fennia Patria [1983] QB 856 Kilcarne Holdings Ltd v Targetfollow (Birmingham) Ltd [2004] EWHC 2547 (Ch); [2005] 2 P&CR 8 KPMG v Network Rail Infrastructure Ltd [2007] EWCA Civ 363; [2008] P&CR 11 Leibler v Air New Zealand Ltd (No 2) [1999] 1 VR 1 Lloyds TBS Bank plc v Crowborough Properties Ltd [2013] EWCA Civ 107 Maralinga Pty Ltd v Major Enterprises Pty Ltd (1973) 128 CLR 336 Maynard v Mosely (1676) 3 Swans 651; (1976) 36 ER 1009 Mosely v Virgin (1796) 3 Ves Jun 184; (1796) 30 ER 959 Mount Bruce Mining Pty Ltd v Wright Prospecting Pty Ltd [2015] HCA 37; (2015) 256 CLR 104 Muriti v Prendergast [2005] NSWSC 281 Queenfield Pty Ltd v Gordon Finance Pty Ltd [2020] VSCA 282 Quintis Ltd (Subject to Deed of Company Arrangement) v Certain Underwriters at Lloyd’s London Subscribing to Policy Number B0507N16FA15350 [2021] FCA 19 Ryledar Pty Ltd v Euphoric Pty Ltd [2007] NSWCA 65; (2007) 69 NSWLR 603 Simic v New South Wales Land and Housing Corporation [2016] HCA 47; (2016) 260 CLR 85 Swainland Builders Ltd v Freehold Properties Ltd [2002] EWCA Civ 560; [2002] 2 EGLR 71 Towry Law plc v Chubb Insurance Co of Europe SA [2008] NSWSC 1352 W G Mitchell (Gleneagles) Ltd v Jemstock One Ltd [2006] EWHC 3644 (Ch) | |

Derrington D K and Ashton R S, The Law of Liability Insurance (LexisNexis Butterworths, 3rd ed, 2013) Hodge D, Rectification: The Modern Law and Practice Governing Claims for Rectification for Mistake (Thomson Reuters, 2nd ed, 2016) MacMillan C, Mistakes in Contract Law (Hart Publishing, 2010) Story J, Commentaries on Equity Jurisprudence as Administered in England and America (13th ed, 1886) | |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

106 | |

Date of last submissions: | 24 February 2021 |

Determined on the papers | |

Counsel for the Applicants: | |

Solicitor for the Applicants: | Piper Alderman |

Counsel for the First and Third Respondent: | Mr M Jones SC with Mr E Ball |

Solicitor for the First and Third Respondent: | Wotton & Kearney |

Counsel for the Second Respondent: | Mr M R Elliott SC with Mr R J Pietriche |

Solicitor for the Second Respondent: | Colin Biggers & Paisley |

Solicitor for the Fourth Respondent: | The fourth respondents filed a submitting notice save as to costs |

ORDERS

DATE OF ORDER: | 6 April 2021 |

THE COURT ORDERS THAT:

1. The policies of insurance identified as policy number B0507N16FA15360 (2016-17 1XS) and policy number B0507N16FA15370 (2016-17 2XS) for the policy period 30 September 2016 to 31 October 2017 be rectified in accordance with the Annexure to these orders.

2. A copy of the Court’s judgments dated 28 January 2021 and 6 April 2021, and this order is to be indorsed upon the 2016-17 1XS and 2016-17 2XS.

3. Quintis pay 25% of the second and third respondent’s costs.

4. There be no order as to costs as between Quintis and the first and fourth respondents.

5. Leave be granted for any party to apply for a lump sum costs order by notification to the Associate to Justice Lee within 14 days (in which case directions will be made on the papers as to the process of quantification of costs).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Annexure

ITEM | RECTIFIED INSTRUMENT |

Policy B0507N16FA15360 (to the extent it records a contract with Argo) | |

I | The 2016-17 1XS (A79) is amended to include the following clause in the MRC Risk Details schedule following “Conditions” (at A80): “First Additional Entity Securities Sub-Limit of Liability:

|

II | The 2016-17 1XS (A79) is further amended to include the following clause in the Risk Details schedule under the heading “Conditions” (at A80): “In relation to any claim in respect of the provisions of SECTION 4: EXTENSIONS TO SECTION 1B (DIRECTORS & OFFICERS LIABILITY) 4.9 Entity Securities Liability of the Primary Insurance in respect of the First Additional Entity Securities Sub-Limit, such claim will be paid only by Argoglobal Syndicate 1200 in proportion to its written line [of 50%], and only to the extent that written line would not be exceeded. Further, and for the avoidance of doubt:

|

Policy B0507N16FA15370 (to the extent it records a contract with Vibe) | |

III | The 2016-17 2XS (A100) is amended to include the following clause in the MRC Risk Details schedule following “Conditions” (at A101): “Second Additional Entity Securities Sub-Limit of Liability:

|

IV | The 2016-17 2XS (A100) is further amended to include the following clause in the Risk Details schedule under the heading “Conditions” (at A101): “In relation to any claim in respect of the provisions of SECTION 4: EXTENSIONS TO SECTION 1B (DIRECTORS & OFFICERS LIABILITY) 4.9 Entity Securities Liability of the Primary Insurance in respect of the Second Additional Entity Securities Sub-Limit, such claim will be paid only by Vibe Syndicate 5678 in proportion to its written line [of 10% (as reduced to 6.25% in accordance with the Signing Provisions)], and only to the extent that written line would not be exceeded. Further, and for the avoidance of doubt:

|

LEE J:

1 In Quintis Ltd (Subject to Deed of Company Arrangement) v Certain Underwriters at Lloyd’s London Subscribing to Policy Number B0507N16FA15350 [2021] FCA 19; (2021) 385 ALR 639 (principal judgment or J), I made findings as to whether Quintis’ IMI insurance policies should be rectified on the basis that they did not reflect the true accord reached. These reasons assume a familiarity with that judgment and will adopt its abbreviations.

2 In the principal judgment, it was accepted (J[268]) that Quintis and PSC, Quintis’ Australian broker, held the relevant intention, defined (at J[80]) as the Side C Coverage Intention. Quintis also succeeded in establishing that Price Forbes (J[303]), Quintis London broker, Argo (J[348]) (being one of the subscribing insurers forming part of the second respondent) and Vibe (J[383]) (being one of the subscribing insurers forming part of the third respondent), held the Side C Coverage Intention. Informed by the caution as to making findings as to common intention in rectification suits, I was not satisfied to the requisite standard that the eight other insurers held the Side C Coverage Intention: see J[319], [327], [336], [354], [356], [365], [370] and [387].

3 Given these mixed findings, I directed each party to provide submissions on the specific question of relief and costs in the light of the judgment. I also gave each party the opportunity to address the Court on the questions of relief and costs orally. No party took the opportunity to address the Court orally and, on 22 March 2021, my Associate wrote to the parties to inform them that given no communication had been received by the Court requesting an oral hearing, judgment had been reserved and reasons would be delivered as soon as practicable. Hence, the questions of relief and costs will be determined on the bases of the findings in the principal judgment, the evidence before the Court at the hearing, and the written submissions filed by the parties.

4 I have reached the conclusion that Quintis is entitled to relief against Argo and Vibe. In explaining why this is so, and what form the relief should take, the balance of my reasons will be divided into the following headings:

B Concessions at the initial trial;

C The proposed form of relief;

D The availability of the equity;

E Considering the relief proposed;

F The practical operation of the relief;

G Costs; and

H Conclusion and orders.

B Concessions at the initial trial

5 At [395], I observed that two issues arose in relation to the question of relief given the conclusions reached in the principal judgment, namely: (a) whether the Rectification Claim can succeed given my findings; and (b) if so, how should equity respond. I then noted at [396]:

The answer to the former of these questions is simple. Both parties accepted that consistently with each of the 2016-17 Policies in fact representing a bundle of separate contracts between the insured and each Relevant Insurer, it was possible for the Rectification Claim to succeed against some of the Relevant Insurers but not others. However, the answer to the latter of these question is more complex. While both parties accepted that the Rectification Claim could succeed in theory, given the case was presented in a binary fashion, no detailed submissions were provided as to the calibration of relief in the present circumstances.

(Emphasis added).

6 However, despite this common position at the hearing and my intention that the supplementary written submissions be directed to the form of relief that would give effect to the common intention as found, the Relevant Insurers’ submissions have focussed on why relief is not available at all. It is therefore necessary for me to first explain why I made the bolded comment extracted above.

7 As noted above, unsurprisingly, the case was presented initially in a binary fashion: that is, Quintis argued that it was entitled to relief on the Rectification Claim including because Quintis and each of the Relevant Insurers all had the Side C Coverage Intention; while the Relevant Insurers asserted that none of the Relevant Insurers had the Side C Coverage Intention.

8 After receiving the evidence and the updated submissions of the parties provided after the first day of the hearing, it became apparent to me that it was possible the picture was somewhat more nuanced than the polarities adopted by the parties.

9 In its submissions filed after the first day of the hearing (at [2(b)]), the first and third respondents submitted that:

As will become apparent, [Quintis] will only succeed in this claim if it is able to establish that:

…

(b) each of the underwriters of the primary policy, first excess policy and second excess policy (a total of ten separate underwriters) all had a common intention that was the same as the placing broker and inconsistent with the form of the documents presented to them over the same 5-6 week period.

10 Partly because of forming the preliminary view that the evidence may not sustain the proposition that all Relevant Insurers held the Side C Coverage Intention (or none of them did), at the commencement of the second day of the hearing, all counsel were provided by my Associate with a document entitled “Questions for Counsel”. That document formed the basis of the summary of the principles applicable to the Lloyd’s insurance market, accepted by the parties and recorded at J[29]. Further, in that document, I posed the following question to counsel with respect to the issue of common intention:

Common Intention:

6. If common intention is required as between the insured and each of the Relevant Insurers as to each of the “separate contracts with the subscribers of the slip” (General Reinsurance Corporation v Forsakringsaktiebolaget Fennia Patria [1983] QB 856 (CA) (at 864, per Kerr LJ with whom Slade and Oliver LLJ agreed)) such as to allow rectification of each of these separate contracts, can some relief still be granted if the common intention of only some of the [Relevant] Insurers to the 2016-17 Policies can be proven? For example, on the hypothesis it was proved:

a. it was the common intention of Quintis and Antares and Quintis and Channel that the 2016-17 Primary provided for $50 million by way of an “Entities Securities Liability Optional Extension” (“Side C” cover), but the evidence does not allow for the same conclusion to be reached that this was the intention of Everest, can rectification still be granted as to the relevant separate contracts as between Quintis and Antares and Quintis and Channel to reflect this position?

b. the common intention of Quintis, Antares, Argo, CNA, Probitas, Barbican, Vibe and ANV was that the 2016-17 Primary provided “Side C” cover of $50 million and that the “Follow Form” provision in Risk Details Schedule of the MRC’s attached to the Excess Policies meant the Excess Policies incorporated the terms of the 2016-17 Primary, but the evidence does not allow for the same conclusions to be reached that this was the relevant intention of QBE, can rectification still be granted as to all the relevant separate contracts as between Quintis and the Relevant Insurers other than QBE?

11 It should also be noted that in closing submissions filed on the morning of the second day of the hearing, Quintis acknowledged the potential of a mixed result and essentially submitted that, given the contractual structure at play, in circumstances where some insurers were found to hold the common intention but not others, there is no reason why equity could not fashion relief accordingly and, further, that it would be against conscience not to: see J[397].

12 The transcript of the second day of the hearing records the following (D2, T41.12–30):

MR JONES: Now, the second key player is the relevant underwriters. Now, something tells me, your Honour is shortly going to know, that is not quite the way we put the case. We don’t put the case that it is necessary to establish that every single underwriter had to have had a common intention for this or any aspect of these contracts to be rectified. All we were making is that they – that each underwriter has a separate contract and therefore if there is to be a rectification suit, it has to be specifically directed at that particular underwriter.

HIS HONOUR: So if you look at paragraph 2(b) of your written submissions [extracted above at [9]], I should take what you say in 2(b) in that way?

MR JONES: You should, your Honour.

HIS HONOUR: Yes. Okay.

MR JONES: Now, there is an authority in the bundle which I won’t take your Honour to, but it’s General Reinsurance Corporation v Fennia Patria. There is a reference in that that goes to the question of separate contracts, which I won’t take your Honour to because I think we may be on common ground there anyway.

13 To obtain further clarity, towards the end of final submissions, the relevant questions I posed were addressed more directly (D2, T79.38–T80.21):

MR JONES: … I’ve had a look at your Honour’s document. I think I went into question 6 and 7 in my submissions to date …

HIS HONOUR: Well, what are your answers to 6 and 7, in summary?

MR JONES: The – the answer to 6 and 7 – in relation to 6, we accept that each contract – there is a separate contract for each underwriter.

HIS HONOUR: Yes.

MR JONES: And that’s what we said before, however, as I said before, you can take into account any clear proof of understanding to inform the question of common intention. In terms of 7, again - - -

HIS HONOUR: No, what about (b). What about 6(b)? I was asking you to deal with a hypothesis. If it was proved that – if you proved – and this isn’t supposed to be done on the basis of the – of any [descent into] the detail as to relevant strengths of the evidence. It’s merely me just testing the legal proposition. There would – in the event that I was satisfied that all the [Relevant Insurers], save for one – the relevant common intention of Quintis had been proved. The mere fact that one of the [10 insurers] cannot prove it in respect of one of them could not deny relief in respect of the balance.

MR JONES: We would agree with that.

HIS HONOUR: Yes. Yes, okay.

MR JONES: That logically follows from the fact they’re separate contracts, your Honour.

HIS HONOUR: Yes, yes. Okay...

14 In relation to the second respondent, the following exchange occurred (D2, T90.1–15):

MR ELLIOT: … I should formally indicate the position in relation to your Honour’s questions.

HIS HONOUR: Yes. I was just thinking [that] – yes.

MR ELLIOT: Your Honour, we think that we essentially [take the] same position as Mr Jones.

HIS HONOUR: Right. Okay.

MR ELLIOT: The only thing that I would say is that in relation to question 6, we agree with what Mr Jones says. Whether or not that would translate into an obligation to indemnify, in a hypothetical world in which some policies were rectified and others not, it would obviously depend on the terms of the policy as rectified.

15 There is somewhat of a tension between this considered approach taken by senior counsel for the Relevant Insurers at the hearing and the position now advanced. Indeed, the second respondent in their written submissions on relief now say that:

… the analysis now required involves a deeper consideration of matters beyond the mere absence of the common intention of an insurer. On that deeper consideration, and having regard to the particular facts and circumstances arising as set out above, rectification of the Argo contract in the terms now sought is not available.

Even if the above was not the case, and Argo was in some respect changing its position (which is denied), it ought be permitted to do so. The ‘mixed outcome’ issue was only raised in the course of closing submissions, was at that point a broad conceptual one really focussing on the fact of separate contracts, is an issue which the Court has not yet determined but instead reserved for further debate, and is a substantial issue in respect of which the parties ought be permitted to address more fully now that the underlying findings of fact have been made.

(Emphasis added).

16 Despite this marking a departure from what I had understood to be the common position, the second respondent has not taken the opportunity to be heard orally on the question of relief. Nor has there been any application to re-open. It is also important to recall that the Relevant Insurers did not call any witnesses at the initial trial as to their subjective intention. Nor was any evidence adduced in relation to the market practice of the operation of the 2016-17 Policies or the commercial motivations of the insurers entering into these contracts of insurance with Quintis. In these circumstances, it would be unfair to Quintis to, in effect, accept evidence from the bar table as to commercial motivations or subjective intentions of those that entered into the contracts underlying the 2016-17 Policies in respect of which relief is sought. The only evidence to which regard can be had is that which was adduced at the initial trial, and the inferences available to be drawn from that evidence.

17 In any event, notwithstanding the submissions now made represent a change of position, I consider I ought to deal with them on their merits (to the extent the submissions made are open on the evidence adduced at the hearing).

18 In their written submissions, Quintis included the following annexure which outlines the changes it contends are necessary to bring the 2016-17 Policies into line with the common intention as found between the parties:

ITEM | RECTIFIED INSTRUMENT |

Policy B0507N16FA15360 (to the extent it records a contract with Argo) | |

I | The 2016-17 1XS (A79) is amended to include the following clause in the MRC Risk Details schedule following “Conditions” (at A80): “First Additional Entity Securities Sub-Limit of Liability:

|

II | The 2016-17 1XS (A79) is further amended to include the following clause in the Risk Details schedule under the heading “Conditions” (at A80): “In relation to any claim under the provisions of SECTION 4: EXTENSIONS TO SECTION 1B (DIRECTORS & OFFICERS LIABILITY) 4.9 Entity Securities Liability of the Primary Insurance under the First Additional Entity Securities Sub-Limit, such claim will be paid only by Argoglobal Syndicate 1200 in proportion to its written line [of 50%], and only to the extent that written line would not be exceeded. Further, and for the avoidance of doubt:

|

Policy B0507N16FA15370 (to the extent it records a contract with Vibe) | |

III | The 2016-17 2XS (A100) is amended to include the following clause in the MRC Risk Details schedule following “Conditions” (at A101): “Second Additional Entity Securities Sub-Limit of Liability:

|

IV | The 2016-17 2XS (A100) is further amended to include the following clause in the Risk Details schedule under the heading “Conditions” (at A101): “In relation to any claim under the provisions of SECTION 4: EXTENSIONS TO SECTION 1B (DIRECTORS & OFFICERS LIABILITY) 4.9 Entity Securities Liability of the Primary Insurance under the Second Additional Entity Securities Sub-Limit, such claim will be paid only by Vibe Syndicate 5678 in proportion to its written line [of 10% (as reduced to 6.25% in accordance with the Signing Provisions)], and only to the extent that written line would not be exceeded. Further, and for the avoidance of doubt:

|

19 While it will be necessary to engage with the form of relief below specifically, it is necessary to deal initially with the overarching submissions as to why no relief ought to be granted.

D THE AVAILABILITY OF THE EQUITY

20 The submissions as to why relief ought not to be awarded can be broadly summarised by reference to the following three propositions:

(1) the relief now sought goes beyond the Amended Application;

(2) the findings as to common intention are inconsistent; and

(3) the relief now sought lies beyond the ambit of equity’s reach.

21 I will deal with each of these in turn.

D.1 Beyond the Amended Application

22 As summarised at J[17]–[27], Quintis was granted leave to file an amended originating application (the Amended Application (J[17])) on the morning of the first day of hearing. The effect of this amendment was to allow Quintis to seek rectification of the 2016-17 Primary and, “to the extent they incorporate the terms of the [2016-17 Primary]”, the 2016-17 1XS and the 2016-17 2XS (i.e. not simply the 2016-17 Primary). It is now argued that given the Court’s finding that only Argo and Vibe held the Side C Coverage Intention (neither of whom were participating at the 2016-17 Primary layer), the relief now contended for falls beyond that sought in the Amended Application. In other words, Quintis’ claim must fail because rectification of the Excess Policies was never sought independently of the 2016-17 Primary.

23 This submission, apparently based on notions of procedural fairness, was developed in the following way. It was said that cl 4.4 of the Excess Policies (extracted at J[43]), absent any rectification, governs the field in relation to the Excess Insurers’ indemnity obligations in respect of Side C cover; this cover being sub-limited to the “Primary Insurance” (found to mean the 2016-17 Primary (J[52])). It was said that no other policy term purports to regulate the obligation in respect of sub-limited cover and that this clause, in substance, imposes an obligation on the Excess Insurers to indemnify, but only where the $10 million sub-limit (being the sub-limit in the 2016-17 Primary that is not to be rectified) has not been exhausted, and even then, only for the uneroded balance of the sub-limit.

24 Argo and Vibe argued that despite clear reference to this clause in opening submissions prior to amendment, Quintis opted to make minimal changes to the relief it sought in the Amended Application, including: (a) only seeking rectification of the 2016-17 Primary “and to the extent they incorporate the terms of the [2016-17 Primary]”, the Excess Policies; and (b) confining its proposed form of relief to the terms of the 2016-17 Primary Schedule. Further, it was said that the Relevant Insurers ran their case and made forensic decisions on the basis that cl 4.4 of the Excess Policies was not under direct or indirect attack, and that they could take comfort in the view that, should the case against all Primary Insurers fail, no relief would be available against the Excess Insurers. It was asserted that this is not a case of refinement of the precise terms of the relief presented in the Amended Application in a manner consistent with the case advanced, but rather a case where the conceptual premise and terms upon which the claim for rectification was sought, as disclosed by the Amended Application, differ substantively to the relief now sought in the post-judgment submissions. Such a substantial amendment, it was said, ought not to be allowed in circumstances where the case cannot be re-run by the Relevant Insurers.

25 While these submissions might appear superficially to be attractive, they do not withstand scrutiny.

26 First, while I accept that in an attempt to reduce costs and speed up what has become a long and drawn out class action, I dispensed with the need for the parties to file pleadings, the Relevant Insurers were on notice of the substance of the case put against them. The purpose of the Amended Application was to seek rectification of the contracts between Quintis and all Relevant Insurers (as opposed to the Primary Insurers only). This is consistent with the underlying premise, on which the case proceeded, that the 2016-17 Polices reflected a bundle of contracts between Quintis and each Relevant Insurer and that it was therefore necessary to assess the subjective intention of each Relevant Insurer.

27 In this regard, it should be recalled that (at J[23]) I accepted that granting leave to Quintis to file and rely upon the Amended Application caused the Excess Insurers prejudice. My proposal to adjourn the proceeding, for Quintis to file points of claim and thereafter there be a joinder of issue and to allow the Excess Insurers to file additional affidavit material and submissions, was met with resistance. Instead, the Excess Insurers confirmed that they knew and were in a position to meet the case against them, wished to adduce no further evidence, and submitted that I should proceed to hear the matter that day. It is somewhat surprising to assert after a debate on the Amended Application spanning 16 pages of the transcript, in which it was made plain that Quintis was seeking rectification of all contracts comprising the 2016-17 Policies and that the subjective intention of all Relevant Insurers was in issue, that the Relevant Insurers did not understand the case put against them. Indeed, the whole purposes of the amendment was to do away with the technical argument that the Excess Policies were not sought to be rectified.

28 Secondly, while I will address the form of relief below, the reliance by Argo and Vibe on the fact that rectification of cl 4.4 was not explicitly sought, or that rectification was only sought in respect of the 2016-17 Primary, elides the equity with the relief. While I appreciate that the Amended Application sought that rectification be effected by a simple amendment to the 2016-17 Primary, consistent with a binary approach to the case (i.e. that all the Relevant Insurers held the Side C Coverage Intention), this did not “lock down” the form to which the document ought to be brought. As I stated at J[399], the authorities have moved away from the need to show precisely the form to which the document sought to be rectified ought to be brought: cf Fowler v Fowler (1859) 4 De G & J 250 (at 265 per Lord Chelmsford). Indeed, while one must find that which was specifically intended, the exact form of words in which the common intention is to be framed is immaterial as long as in substance and in detail the parties’ intention is to be ascertained: Crane v Hegeman-Harris Co Inc [1939] 1 All ER 662 (at 669 per Simonds J), approved on appeal in Crane v Hegeman-Harris Co Inc [1939] 4 All ER 68 (at 72 per Sir Wilfrid Greene MR, with whom Clauson and Goddard LJJ agreed).

29 As the Court stated in Queenfield Pty Ltd v Gordon Finance Pty Ltd [2020] VSCA 282 (at [80] per McLeish, Niall and Sifris JJA), a case in which the parties to a sale of units deed omitted a term transferring intercompany loans on the books of a cooperate trustee to a related entity borrower:

The fact that the evidence did not go so far as to show that a term in that specific form was intended by the parties is not a bar to the rectification claim. What is required is a common intention as to what was agreed. While that might be articulated in legal language or in the form of a draft contractual term, that is not essential. Conversely, the fact that different ways might be found of formulating the intention in legal terms does not deny that the intention exists.

(Emphasis added).

30 Further, after affirming that there was no error in the primary judge amending the relief ultimately proposed by the respondents, their Honours noted (at [87]):

… the making of a finding about common intention did not depend on establishing a form of words upon which the parties were agreed. It sufficed to show a clear common intention that could be reduced to a legal form which could take its place in the contract between the parties by way of [a] remedy so as to give that intention legal effect.

(Emphasis added).

31 See also Leibler v Air New Zealand Ltd (No 2) [1999] 1 VR 1 (at 27–8 [71]–[73] per Kenny JA, with whom Winneke P and Phillips JA substantially agreed at 5 [11]); Muriti v Prendergast [2005] NSWSC 281 (at [132]–[137] per White J); Franklins Pty Ltd v Metcash Trading Pty Ltd [2009] NSWCA 407; (2009) 76 NSWLR 603 (at 711 [450] per Campbell JA, with whom Allsop P and Giles JA agreed).

32 It was clear as the case developed and from the acceptance by all parties that some but not all of the Relevant Insurers may be found to have held the Side C Coverage Intention, that the simple form of relief which Quintis had proposed in its Amended Application was insufficient. It would have also been evident that, in the event an intermediate position was accepted as reflecting the position proved on the evidence, the relief would need to be calibrated accordingly.

33 Thirdly, in the absence of sworn evidence, I do not accept the submission that the Relevant Insurers would have run their case any differently even if they did have the understanding for which they now contend or if they had of been aware of the specific relief now sought. This is because the Relevant Insurers made written and oral submissions on the intention of each Relevant Insurer. I am fortified in this view by recalling what occurred with respect to the Amended Application on the first day of the initial trial. In relation to the amendment, the Relevant Insurers submitted that the contention that the subjective intention of all Relevant Insurers was in issue and that all contracts underlying the 2016-17 Policies were potentially subject to rectification was “obviously not the basis upon which [the Relevant Insurers had] run the case”: D1, T10.35. It was suggested that the Relevant Insurers made forensic decisions based on the approach adopted by Quintis and would suffer real prejudice if the amendment was allowed, including being prejudiced by having previously made a decision not to interview witnesses. Despite this, when the amendment was allowed, the insurers changed tack entirely and took an approach which reflected the fact that they were not sufficiently prejudiced so as to accept an adjournment of the hearing to meet the prejudice they had identified: see J[24]. Rather, they insisted that the case be heard that day.

34 I therefore reject any submission that the Relevant Insurers were not on notice of the case put against them and, in the absence of evidence, I do not accept that they would have proceeded differently if their understanding of the case had of been different (in that they were aware the relief now sought would have been advocated by Quintis if a mixed result had been obtained).

D.2 A purported tension in the findings as to common intention

35 The second overarching submission made as to why the equity is unavailable was advanced in relation to Vibe only and can be dealt with relatively shortly. Vibe submitted that given: (a) the market practice of a slip being presented to the subscription market on the basis that it had been endorsed by the market leader; and (b) its intention to support the terms agreed by the 2016-17 2XS market leader Channel (evident by it offering “support” of 10% on the second excess layer (J[182], considered at J[376])), it cannot be said that Vibe intended to accept more onerous terms than the market leader. It was argued that the Court’s findings therefore stand in conflict: on the one hand Vibe held the Side C Coverage Intention, and, on the other, it intended to support the terms of the market leader who “did not have the Side C Coverage Intention”.

36 The most obvious issue with this submission is that, as Quintis rightly points out, it is an appeal point masquerading as a matter relevant to relief. In any event, the submission is without merit for the following reasons.

37 First, this submission mischaracterises the finding made at J[327], which was that “[i]t has not been satisfactorily established that Channel held the Side C Coverage Intention”, not that Channel “did not have the Side C Coverage Intention”. These words, needless to say, were deliberately chosen. Hence, any submission as to a logical inconsistency is incorrect.

38 Secondly, the fact that Vibe offered to “support” 10% of the 2016-17 2XS, or the market practice of brokers presenting a slip on the basis that it has been endorsed by a market leader, is of no moment. Counsel representing Vibe made pellucid in writing at the initial trial that this was a case in which the “placing broker [was required] to separately approach each underwriter” and “the relevant ‘common intention’ that needs to be established is not just with the slip leader for each policy, but separately with each of the subscribing underwriters, as each has entered into separate contractual relations”. To rely on any subjective intention of Channel to inform the intention of Vibe, or to assert an issue with any purported inconsistency of intention, is plainly contrary to this position.

39 Thirdly, and in any event, this submission takes Mr Wren’s reference to “support” out of context. Once the email extracted at J[182] is considered as a whole, it is clear that Mr Wren is offering to support the structure conveyed to him by Mr Butler via “updates”. Even if it was found that Channel “did not have the Side C Coverage Intention”, such a finding has no bearing on the evidence upon which I was satisfied that Vibe held the Side C Coverage Intention; namely, its communications with Price Forbes.

D.3 Beyond the ambit of equity’s reach

40 Turning now to the core and more forceful submission advanced by Argo and Vibe in counter to the award of relief. It was suggested that this is not a case in which equity’s remedial flexibility is limited or stultified by a lack of precision in the form of relief reflecting the conclusions reached in the judgment, but rather, that the contracts between Quintis and Argo and Quintis and Vibe cannot be rectified to capture the intention found without transforming the bargain into one that was not intended by the parties. As counsel for the second respondent put it, the rectification sought will result in the Court “fashioning a bargain that was not struck”, thereby “creat[ing] a patchwork tower” that no party intended and which is contrary to equity’s role in rectification. Before turning to the substance of this submission, it is necessary to revisit some aspects of principle.

41 The general principles applicable to rectification were outlined at J[70]–[76]. As I stated at J[70], the purpose of the equitable remedy of rectification is to make a contractual instrument conform to the true agreement of the parties where the writing by common mistake fails to express that agreement accurately: Maralinga Pty Ltd v Major Enterprises Pty Ltd (1973) 128 CLR 336 (at 350 per Mason J). The rationale of the remedy is the avoidance of an unconscientious departure from the common intention of the parties to an agreement: Franklins (at 710 [444] per Campbell JA, with whom Allsop P and Giles JA agreed); Ryledar Pty Ltd v Euphoric Pty Ltd [2007] NSWCA 65; (2007) 69 NSWLR 603 (at 655–7 [305]–[315], with whom Mason P agreed). Indeed, in ordering rectification, courts operate to relieve the conscience of the respondent, and thereby to assist the applicant, by seeking to hold the parties to their actual intentions: Hodge D, Rectification: The Modern Law and Practice Governing Claims for Rectification for Mistake (Thomson Reuters, 2nd ed, 2016) (at 7 [1–10]). As Story J explained in Commentaries on Equity Jurisprudence as Administered in England and America (13th ed, 1886) (at 168–9 [155]):

A Court of Equity would be of little value if it could suppress only positive frauds, and leave mutual mistakes, innocently made, to work intolerable mischiefs contrary to the intention of parties. It would be to allow an act originating in innocence to operate ultimately as a fraud, by enabling the party who receives the benefit of the mistake to resist the claims of justice under the shelter of a rule framed to promote it. In a practical view there would be as much mischief done by refusing relief in such cases as there would be introduced by allowing parol evidence in all cases to vary written contracts.

(Citation omitted).

See also the helpful summary of early commentary on the rationale underpinning the equity of rectification in MacMillan C, Mistakes in Contract Law (Hart Publishing, 2010) (at 45–6).

42 However, it has also long been accepted that there are limits to equity’s intervention. As the Relevant Insurers correctly submitted, it is no place of equity to relieve a mistake in a document where this would amount to writing a new agreement for the parties: see Mosely v Virgin (1796) 3 Ves Jun 184; (1796) 30 ER 959 (at 961 per Lord Chancellor Loughborough). This limitation is commonly reflected in the maxim that equity “mends no man’s bargain”: Maynard v Mosely (1676) 3 Swans 651; (1976) 36 ER 1009 (at 1011 per Lord Nottingham). In the case of rectification, equity “does not alter the bargain itself; it merely alters the written record of the bargain”: Kilcarne Holdings Ltd v Targetfollow (Birmingham) Ltd [2004] EWHC 2547 (Ch); [2005] 2 P&CR 8 (at 162–3 [231] per Lewison J). This is because the equity of rectification is concerned with defects in the recording, not the making, of an agreement.

43 Whether relief ought to be granted in the current circumstances involves consideration of an apparent tension between these two core principles underlying the equitable remedy of rectification.

D.3.2 The contentions of Argo and Vibe

44 The argument that rectification in the current circumstances would transform the transaction into something neither Argo nor Vibe intended (in the absence of any direct evidence as to their intention) was expressed in two ways.

45 First, is that Argo and Vibe intended to be co-insurers at the 2016-17 1XS and 2016-17 2XS layers, respectively. It was said that these insurers had underwritten Quintis’ risk on the basis that: (a) they had the benefits and advantages of co-insurance (such as pooling funds towards the disposal of a claim and the opportunity to seek to buy out a risk where the quantum was uncertain); and (b) all underwriters were on the same page. It was said that the hypothetical situation in which rectification is ordered in respect of the contracts between Quintis and Argo and Quintis and Vibe is not the context in which Argo and Vibe approached the underwriting task. The second respondent submitted that in these circumstances, rectification “does not bring about a result which reflects the common intention [of the parties], but instead produces a different outcome that is beneficial to [Quintis] and harmful to Argo … in effect rewarding one party for its mistake and harming another party for that very same mistake”. It was said that the result may have been different if Quintis had argued, and the Court had found, that the common intention of Quintis, Argo and Vibe was that the Relevant Insurers would provide Side C cover in accordance with the Side C Coverage Intention irrespective of the position of the other insurance contracts, but that is not the case.

46 Secondly, and specific to Vibe, is that Vibe intended to be an excess insurer to the 2016-17 2XS. It was said that the Court’s finding that Vibe intended for the 2016-17 Policies to “collectively provide up to $50 million in Side C cover” (J[80]) was on the basis that prior to the 2016-17 2XS attaching, there would be exhaustion of the layers below (which, on its intention, included up to $30 million of Side C cover). It was said that this is not the case where (as here) two of the three 2016-17 1XS insurers do not provide cover that would enable such an intention to come to pass. It was argued that this is commercially significant as it means that now only up to $20 million of capacity to deal with a Side C claim is available below the 2016-17 2XS, and not $30 million as understood by Vibe according to the Side C Coverage Intention. It was submitted that the risk profile and pricing for an excess insurer is a function of the insurance capacity below it to deal with claims irrespective of the excess insurer’s attachment point.

47 Quintis’ simple answer to these submissions is that its proposed form of relief is calibrated to respond to these nuances and does not place Argo or Vibe in any worse position than they would have been in if all the Relevant Insurers had been found to hold the Side C Coverage Intention. However, the critical question, perhaps not fully grappled with by Quintis in their written submissions, is whether calibrating relief to provide for these nuances is available by way of the equity of rectification.

48 It is necessary to recall four important findings made in the principal judgment:

(1) the Side C Coverage Intention is defined at J[80] in the following terms:

… the parties intended to execute the 2016-17 Policies on the basis that Side C cover was not subject to a sub-limit of $10 million, but was in fact equal to the Limit of Liability for Section 1B cover provided for by each of the 2016-17 Primary, the 2016-17 1XS and the 2016-17 2XS, meaning that the 2016-17 Policies collectively provided Side C cover of up to $50 million.

(2) all parties accepted, consistent with what is revealed in the authorities, that the slip method of placing insurance, by signing the MRC and stating the proportion of the risk that the underwriter is prepared to subscribe, results in the conclusion of separate contracts between the insured and each subscriber of the slip (J[29(5)]);

(3) hence, while there may only be one primary policy and three excess polices, there are in fact nineteen separate contracts reflected by the 2016-17 Policies (J[29(7)]); and

(4) in light of these findings, it was necessary to assess the intention of each individual insurer: cf Towry Law plc v Chubb Insurance Co of Europe SA [2008] NSWSC 1352 (at [66] and [138] per McDougall J).

49 These findings are integral to the question of relief. That is because the common intention as defined must be understood in the context of how it applies to the specific contract between Quintis and each Relevant Insurer and the rights and obligations created by that contract. As was made clear in General Reinsurance Corporation v Forsakringsaktiebolaget Fennia Patria [1983] QB 856 (at 864 per Kerr LJ, with whom Slade and Oliver LLJ agreed), each subscribing insurer becomes bound to the extent of its proportion of the risk when it accepts its individual contract. Hence, while I have found that Argo and Vibe were operating with the intention that the layers to which they were subscribing provided Side C cover up to the Limit of Liability for Section 1B cover, and that Quintis’ overall insurance programme provided for $50 million in Side C Cover, the manifestation of that intention as it applied to their contract with Quintis was to provide a set proportion of cover at a specific layer.

50 While no party referred at length to these provisions, what I have said is consistent with what appears under in the MRC under the Security Details heading:

SECURITY DETAILS

INSURER’S LIABILITY:

(Re)insurer’s liability several not joint

The liability of a (re)insurer under this contract is several and not joint with other (re)insurers party to this contract. A (re)insurer is liable only for the proportion of liability it has underwritten. A (re)insurer is not jointly liable for the proportion of liability underwritten by any other (re)insurer. Nor is a (re)insurer otherwise responsible for any liability of any other (re)insurer that may underwrite this contract.

The proportion of liability under this contract underwritten by a (re)insurer (or, in the case of a Lloyd’s syndicate, the total of the proportions underwritten by all the members of the syndicate taken together) is shown next to its stamp. This is subject always to the provision concerning “signing” below.

…

Proportion of liability

Unless there is “signing” (see below) the proportion of liability under this contract underwritten by each (re)insurer (or, in the case of a Lloyd’s syndicate, the total of the proportions underwritten by all the members of the syndicate taken together) is shown next to its stamp and is referred to as its “written line”.

Where this contract permits, written lines, or certain written lines, may be adjusted (“signed”). In that case a schedule is to be appended to this contract to show the definitive proportion of liability under this contract underwritten by each (re)insurer (or, in the case of a Lloyd’s syndicate, the total of the proportions underwritten by all the members of the syndicate taken together). A definitive proportion (or, in the case of a Lloyd’s syndicate, the total of the proportions underwritten by all the members of a Lloyd’s syndicate taken together) is referred to as a “signed line”. The signed lines shown in the schedule will prevail over the written lines unless a proven error in calculation has occurred.

Although reference is made at various points in this clause to “this contract” in the singular where the circumstances so require this should be read as a reference to contracts in the plural.

51 Indeed, I do not think that it is a precondition to the award of relief, as the second respondent suggests, to find that Argo and Vibe intended to provide Side C cover irrespective of the position of the other insurance contracts (although there is no direct evidence bearing on this question one way or another). To refuse relief on the basis that it has not been found that the other insurers to the 2016-17 Policies held the Side C Coverage Intention is to confuse the 2016-17 Policies, which record the bundle of contracts, with the individual contracts themselves, and the bilateral rights and obligations created under these contracts.

52 Two factors have caused me pause before coming to the conclusion that rectification is available in the current circumstances.

53 First, is the reality in which Argo and Vibe now find themselves (unsupported by co-insurers and, in the case of Vibe, by a complete underlying first excess layer) and the need to insert terms into the 2016-17 Policies which are inconsistent with the Side C Coverage Intention being commonly held by all parties. In this respect, the first and third respondents sought to draw support from the following passage of Campbell JA’s reasons in Franklins (at 711 [450]):

It is the document as a whole that is rectified, and the point of the exercise is that, once rectified, the document will not be contrary to the common intention of the parties to the document. Thus if a particular change to some words will result in some other words of the document operating in a different way, rectification will be justified only if that different operation of those other words is shown to be in accordance with the common intention of the parties.

(Emphasis added).

54 However, upon examination, I do not think these remarks assist Argo or Vibe’s case. Any suggestion that the form of relief cannot be reconciled with the Side C Coverage Intention not being commonly held by all parties must acknowledge the contractual structure at play. This is because, although the proposed terms do isolate Argo and Vibe, they do so consistently with the Side C Coverage Intention found, as it applies to the contracts between Quintis and these insurers. That is, these terms simply bring the 2016-17 Policies to a form that reflects the contractual intention of these insurers to indemnify a set proportion of risk at a certain layer (but militates against the intention being held by others).

55 In my view, and applying what was said by McLeish, Niall and Sifris JJA in Queenfield (at [87]), I do not see how giving effect to the “clear common intention” of Quintis and these insurers rewards one party for its mistake and harms the other party for that very same mistake. What matters is that the intention is given effect (see [28]–[31] above) and that the order for rectification, “once made, relates back so that the rights of the parties are treated as having always been in accordance with the contract as so rectified” (emphasis added): Franklins (at 750 [644] per Campbell JA, with whom Allsop P and Giles JA agreed); see also Simic v New South Wales Land and Housing Corporation [2016] HCA 47; (2016) 260 CLR 85 (at 117 [103]–[104] per Gageler, Nettle and Gordon JJ) and Lloyds TBS Bank plc v Crowborough Properties Ltd [2013] EWCA Civ 107 (at [62]–[64] per Lewison LJ, with whom Rimer and Mummery LJJ agreed).

56 Secondly, is the submission that the availability of funds from co-insurers on the same layer would give these insurers the opportunity to seek to buy out a risk where the quantum was uncertain (i.e. a claim against an insured that could produce a range of results) at a higher price than they would wish to if they were using their funds alone. If this were true, placing Argo and Vibe in a position where they no longer have such an opportunity would be to alter the bargain entered into. These submissions may have had force at the initial trial, but the fact is that these insurers led no evidence whatsoever in support of this proposition even when it became apparent that there may be mixed findings as to the holding of the Side C Coverage Intention as it applies to the contracts between Quintis and the various insurers. Further, as I have outlined above, Argo and Vibe expressed no desire to apply to reopen or to be heard orally on the question of relief. In making this remark, I am not reversing the onus of proof, but highlighting that the concept of the “comfort of co-insurance”, without any supporting lay or expert evidentiary foundation, is a somewhat nebulous and speculative one.

57 In these circumstances, I am not of the view that to order rectification in the circumstances would, on the evidence, be fashioning a bargain that the parties did not strike or giving effect to an agreement that goes beyond that which the parties intended: see Muriti (at [137] per White J). Nor is there a danger, to adopt the words of Campbell JA in Franklins (at [459]), of “imposing on a party a contract which he did not make”. All that rectification is doing in these circumstances is bringing the policy, as the document recording the contracts of insurance, into line with the common intention of the parties. Indeed, this is not a situation where there was in fact no common intention between the parties, a common misunderstanding, or an oversight of a particular matter: see, eg, Club Cape Schanck Resort Co Ltd v Cape Country Club Pty Ltd [2001] VSCA 2; (2001) 3 VR 526 (at [12] per Tadgell JA). Nor is this a case in which the Court would be supporting a doctrine of rectification pro tanto: cf KPMG v Network Rail Infrastructure Ltd [2007] EWCA Civ 363; [2008] P&CR 11 (at 199 [31]–[33] per Carnwath LJ). It is a situation in which parties entered into bilateral contracts with a common intention to provide a specific proportion of cover at a specific layer.

58 Indeed, consistent with the rationale articulated above, it would be against conscience to allow the 2016-17 Policies to stand in their current form. As Campbell JA noted in Franklins (at 710 [444], with whom Allsop P and Giles JA agreed):

… equity focuses on what it is unconscientious for a party to assert about the contract. The rationale is that it is unconscientious for a party to a contract to seek to apply the contract inconsistently with what he or she knows to be the common intention of the parties at the time that the written contract was entered. In other words, when a plaintiff succeeds in a claim for rectification, the plaintiff is found to have been justified in effect saying to the defendant “you and I both knew, when we entered this contract, what our intention was concerning it, and you cannot in conscience now try to enforce the contract in accordance with its terms in a way that is inconsistent with our common intention.”

(Emphasis added).

59 Therefore, despite the novel aspects of the way in which the claim for rectification has played out, given that the 2016-17 Policies represent distinct contracts between Quintis and Argo and Quintis and Vibe, the equity should run.

60 With these issues now clarified, it is necessary to turn to the precise form of relief.

E CONSIDERING THE RELIEF PROPOSED

61 The relief proposed by Quintis is extracted above (at [18]). In order to determine whether the proposed relief is suitable, it is necessary to consider:

(1) what the relief must achieve to give effect to the common intention found;

(2) whether the relief proposed gives effect to the common intention found;

(3) the issues raised by Argo and Vibe in relation to the relief proposed; and

(4) the practical operation of the relief.

E.1 What the relief must achieve to give effect to the common intention found

62 In order to assess whether the relief proposed by Quintis gives effect to the common intention as found, it is first necessary to understand what the relief must achieve. In doing so, one must ensure that the contracts between Quintis and the Relevant Insurers other than Argo and Vibe are not affected by the relief. Broadly summarised, the relief must be faithful to the following four subject matters.

63 First, the amount of Side C cover provided for by each of the 2016-17 1XS and 2016-17 2XS must equal the Limits of Liability for Section 1B cover for each of those policies. This is because each of Argo and Vibe intended their respective layer to provide full Side C coverage.

64 Secondly, Argo and Vibe did not intend to provide Side C cover until the insurance below them was exhausted. This is evident by cl 3.2 of the Excess Policies, which outlines:

Insurers shall only be liable for that proportion of loss which exceeds the limit of liability of the Primary Insurance and any Underlying Insurance. Insurers shall have no liability under this Policy unless and until all limits of liability of the Primary Insurance and any Underlying Insurance have been exhausted by the payment of losses under the Primary Insurance and any Underlying Insurance.

65 Argo intended to cover Side C claims once $10 million of insurance had been paid out (whether in respect of Side C claims or non-Side C claims). Vibe intended to cover Side C claims once $30 million of insurance had been paid out (whether in respect of Side C claims or non-Side C claims). In effect, neither Argo nor Vibe can pay earlier than they would have if all the Relevant Insurers had been found to have held the Side C Coverage Intention.

66 Thirdly, and as outlined above, Argo and Vibe intended to provide Side C cover in proportion to their participation in their respective layers. Argo intended to cover 50% of the claims within its layer, following the subscription of the other insurers to the 2016-17 1XS. Vibe intended to cover 10% of the claims within its layer, reduced to 6.25% following oversubscription for the 2016-17 2XS. Neither Argo nor Vibe can pay more for a Side C claim than they would have if all the Relevant Insurers were found to have held the Side C Coverage Intention.

67 Fourthly, the other Relevant Insurers’ position in relation to Side C cover ought not change given that I was not satisfied to the requisite standard that these insures held the Side C Coverage Intention. Instead, on the evidence, these insurers still believed that they were exposed to Side C claims to the extent the (unrectified) sub-limit of $10 million “travelled up the tower” (e.g. if a large non-Side C claim were to be paid out first, it was possible that from their perspective, the entire Side C sub-limit might sit within the 2016-17 2XS).

E.2 Whether the relief proposed gives effect to the common intention found

68 Subject to one minor issue that I will address below, I am satisfied that the form of relief proposed by Quintis gives effect to the common intention as found. Before turning to deal with the arguments of Argo and Vibe as to why this is not the case, it is convenient to outline (by reference to the subject matters discussed immediately above) why I am satisfied that the relief is appropriate. The form of relief adopts the logical process of first considering what changes to the 2016-17 Policies would be required to reflect a position where all Relevant Insurers held the Side C Coverage Intention and, secondly, confines these amendments so as to ensure they hold true for Argo and Vibe only.

69 Items I and III address the first subject matter. This is because the introduction of the “First Additional Entity Securities Sub-Limit of Liability” (First Additional Sub-Limit) and the “Second Additional Entity Securities Sub-Limit of Liability” (Second Additional Sub-Limit) (collectively, Additional Excess Sub-Limits) allow the amount of Side C cover provided for by each of the 2016-17 1XS and 2016-17 2XS to equal the Limit of Liability for Section 1B cover for these policies. I accept, as Quintis submitted, that there is no practical difference between specifying one Side C sublimit of $50 million, and specifying three cumulative sub-limits of $10 million, $20 million and $20 million.

70 Items II and IV address the second to fourth subject matters. The first paragraph in item II and IV provides that Argo and Vibe are only liable to pay claims proportionately to their participation for Side C claims on the Additional Excess Sub-Limits. Clause (a) ensures that the Additional Excess Sub-Limits will not attach until the existing 2016-17 Primary sub-limit travels up the insurance tower (for which all insurers are liable by cl 4.4(b) of the Excess Policies). While this is immaterial from Argo and Vibe’s perspective (as they intended Side C cover to be co-extensive with the Limit of Liability for Section 1B cover at their respective layer), it matters to preserve the intention of the other insurers to be liable for Side C liability in accordance with the 2016-17 Primary sub-limit. Clause (b) ensures that no insurer other than Argo or Vibe is liable to pay in respect of the Additional Excess Sub-Limits, but preserves their liability to pay on the 2016-17 Primary sub-limit if it travels up the insurance tower. Clause (c) ensures that the Additional Excess Sub-Limits are taken to be exhausted once Argo and Vibe have paid or admitted the full amount of their liability in respect of these sub-limits, which resolves the fact that proportionate payment would not exhaust the total applicable sub-limit, and functionally gives effect to the uninsured component of any Side C claim.

E.3 Purported issues with the form of relief

71 Argo and Vibe raised a number of issues with the form of relief proposed by Quintis. Beyond the objections already addressed by reference to the overarching considerations above, these issues can be broadly summarised by reference to the following five propositions:

(1) the introduction of new sub-limit terms is impermissible;

(2) the relief circumvents, or otherwise does not cohere with, the operation of cl 4.4 of the Excess Policies;

(3) the relief leaves an insurance “gap”;

(4) the relief leads to incoherence generally; and

(5) aspects of the relief are superfluous.

72 I will deal with each of these propositions in turn.

E.3.1 Whether the introduction of new sub-limit terms is impermissible

73 Both Argo and Vibe argued that the introduction of new sub-limit terms in the 2016-17 1XS and 2016-17 2XS is impermissible. I reject this submission for the following two reasons.

74 First, as Quintis submitted, the combination of the adoption of the terms of the 2016-17 Primary in the Excess Policies (by virtue of the “Follow Form” Condition) and cl 1 of the Excess Policies (see J[43]), which incorporates such terms unless otherwise stated, can be reconciled with the provision of sub-limits of liability in the 2016-17 1XS and 2016-17 2XS. Indeed, while cl 8.14 of the 2016-17 Primary and Section 3 of the Excess Policies deal with the same subject matter, the Excess wording is apt to capture sub-limits expressed in the Excess Policies. This is evident by the terms of cl 3.1 of the Excess Policies, which commences:

The Limit of Liability is the aggregate limit of Insurers liability and the maximum amount payable by Insurers under this Policy …

75 Further, the adoption of the 2016-17 Primary terms with respect to Sections 1A, 1B and 1C (not dealt with in the Excess Policies) is sufficient to ensure that any sub-limit for Entity Securities Liability is payable only under the Section 1B cover available.

76 Secondly, the provision of sub-limits in the Excess Policies is supported by the terms of cl 4.4 of the Excess Policies, which contemplates that both the “Primary Insurance” and “Underlying Insurance” may specifically provide for a sub-limit of liability. This is evident by the opening terms of cl 4.4, which provides that:

4.4 In the event that the Primary Insurance or Underlying Insurance specifically provides for a sub-limit of liability it is agreed that ...

(Emphasis added).

77 It is noteworthy that in its written submissions, Argo replaced the emphasised portion of cl 4.4 with an ellipsis. While I accept that, in line with the finding made at J[52], the reference to “Underlying Insurance” in the 2016-17 1XS should be taken to be synonymous with “Primary Insurance” (given it is the only insurance underlying the 2016-17 1XS), it is clear that the reference to “Underlying Insurance” in the 2016-17 2XS is a reference to the 2016-17 1XS. This is consistent with the ordinary process of construction with respect to insurance policies, in which the terms must be considered in the context of the policy as a whole, including, if excess policies are involved, the broad scheme of insurance cover intended to provide layers of insurance against the same risk: Derrington D K and Ashton R S, The Law of Liability Insurance (LexisNexis Butterworths, 3rd ed, 2013) (at 422 [3–64]); see also Mount Bruce Mining Pty Ltd v Wright Prospecting Pty Ltd [2015] HCA 37; (2015) 256 CLR 104 (at 116 [46] per French CJ, Nettle and Gordon JJ). Hence, along with finding that the interaction of the 2016-17 Primary and Excess Policies allows for the provision of sub-limits of liability in the Excess Policies, cl 4.4 specifically anticipates a sub-limit being provided for in the Excess Policies.

E.3.2 Whether the relief proposed circumvents, or otherwise does not cohere, with the operation of cl 4.4 of the Excess Polices

78 Both Argo and Vibe took issue with the way in which the proposed amendments interact with cl 4.4 of the Excess Policies. I will deal with each of these contentions individually.

79 Argo sought to rely on the terms of cl 4.4 to assert that, in the policy landscape in which cl 4.4 sits, absent any rectification, that clause governs the field of the Excess Insurers’ indemnity obligations in respect of Side C cover; that cover being sub-limited to the “Primary Insurance” (the 2016-17 Primary (see J[52])) in the amount of $10 million. It was said that rather than confronting this reality directly, and recognising that, as a matter of substance, cl 4.4 is sought to be varied by way of rectification such that it no longer covers the field in relation to Argo’s obligation to indemnify in respect of Side C cover, Quintis has set about creating entirely new terms and provisions so as to leave cl 4.4 physically unaltered, but with a substantially different and lesser role to play. For example, it was said that the introduction of the First Additional Sub-Limit seeks to craft a way around Argo’s obligation by reference to the 2016-17 Primary sub-limit alone. It was submitted that this drafting device cannot conceal from equity’s eyes that which is sought to be achieved as a matter of substance; namely, the practical modification of cl 4.4 of the 2016-17 1XS, such that it no longer governs Argo’s obligation to indemnify for sub-limited cover.

80 This submission is misguided. Nothing is being “imposed” on Argo; the policy is simply being brought to a state that reflects the contractual relationship between Quintis and Argo. Nor do I see merit in the argument that the relief is “side-stepping” cl 4.4 or “concealing” the practical modification of cl 4.4, such that it no longer governs Argo’s obligations as to sub-limited cover. This is because, as Quintis rightly points out, cl 4.4 could be rectified if that was a convenient way of effecting the common intention of the parties. It is no bar to an order for rectification that the mistake could be put right in more than one way: W G Mitchell (Gleneagles) Ltd v Jemstock One Ltd [2006] EWHC 3644 (Ch) (at [19] per Sir Andrew Morritt C); see also Swainland Builders Ltd v Freehold Properties Ltd [2002] EWCA Civ 560; [2002] 2 EGLR 71 (at 74 [38] and 75 [43] per Peter Gibson LJ, with whom Jonathan Parker LJ agreed). What is required is that words or expressions or other text inserted into or deleted from the document give effect to the common intention found to have existed: Cape Schanck (at 531 [14] per Tadgell JA). In one sense it is clear that the relief is having an effect on the existing provisions relevant to sub-limited cover, that is the whole purpose of granting relief. Once again, it must be emphasised that the equity of rectification is concerned with the intention of the parties and giving that intention legal effect: see Queenfield (at [87] per McLeish, Niall and Sifris JJA).

81 Further, Vibe contended that the proposed rectification does not cohere with the operation of cl 4.4 of the Excess Polices. It was said that with the introduction of another sub-limit, there will now be three sub-limits that bear relevance to the 2016-17 2XS: (a) the Second Additional Sub-Limit; (b) the First Additional Sub-Limit (picked up by the reference to “Underlying Insurance” in cl 4.4 of the 2016-17 2XS); and (c) the sub-limit referred to in the Schedule to the 2016-17 Primary, which is also picked up by cl 4.4. It was said that this creates confusion in the operation of the 2016-17 Policies, particularly where the new words bear no relationship to the sub-limit references upon which cl 4.4 operates. Moreover, Vibe argued that the Second Additional Sub-Limit contains within it two excess references, which makes no sense, having regard to the functional relevance of a sub-limit, which is to identify the maximum amount payable by an insurer, not to create coverage.

82 I do not accept these submissions. There is no confusion in the operation of the 2016-17 Policies, where cl 4.4 on its terms is a generic provision that contemplates there being multiple sub-limits: see [76]–[77] above. Indeed, the reference to subsisting sub-limits is coherent with the terms of cl 4.4, which provides that the sub-limits below float up the tower until exhausted. Further, any reliance by Vibe on market practice and the “functional relevance of a sub-limit” again rings hollow in the absence of any sworn evidence.

E.3.3 Whether the relief proposed leaves an insurance “gap”

83 Vibe contended that the use of excess terminology interferes with any seamless interrelationship between the 2016-17 2XS and 2016-17 1XS. It was said that if the wording is to be interpreted as meaning there is no Side C cover at the 2016-17 2XS layer until payments of $30 million for Side C cover are made (since the 2016-17 1XS exhausts on payments to the Limit of Liability for Section 1B cover), this would leave a potential gap if any payments are made towards other items falling within Section 1B (e.g. D&O cover). I reject this submission. There will be liability in accordance with the Second Additional Sub-Limit if the 2016-17 1XS Limit of Liability for Section 1B cover is reached, because the First Additional Sub-Limit will be exhausted in accordance with the rectified language in item IV (i.e. there is no insurance “gap” that interferes with the seamless operation of the 2016-17 2XS and 2016-17 1XS): see, eg, Annexure E.

E.3.4 Whether the relief proposed leads to incoherence generally

84 Vibe submitted that in the ordinary operation of excess cover, the excess insurer drops down to act as the primary insurer when the limits of the underlying layers exhaust: see cl 3.2 of the 2016-17 2XS. It was said that the proposed relief defeats this operation by tying attachment to a different event; namely, the “exhaustion” of a sub-limit. In this respect, it was submitted that once half of the 2016-17 1XS operates in providing Side C cover in accordance with cl 4.4, then the nominated sub-limit of $20 million will never exhaust, since those 2016-17 1XS insurers will never pay a full $10 million towards a Side C claim. It was said that the terms of item IV(a) do not address this issue, as instead of an attachment point, they deal with a quantum payable; the words direct attention to a reduction in the sub-limit by reference to the “remaining amount”. It was said that this immediately raises for consideration what is meant by the “remaining amount”, and, for the “Underlying Insurance”, which is the sub-limit that is to be used (the First Additional Sub-Limit or the 2016-17 Primary sub-limit). It was said that even if this selection is resolved in favour of the former by a means not apparent on the words, it seems that the “remaining amount” is the part of the below sub-limits not paid. Vibe submitted that a reduction by an unpaid amount is illogical and that even if this was changed to an amount paid (to reflect the wording of cl 4.4(b)), it would still make no sense if the object of rectification is to fix Vibe with an obligation not sub-limited in extent by the payments below.

85 These submissions overcomplicate the form of relief. I have outlined above (at [70]) what items II(a)–(c) and IV(a)–(c) achieve. In the present circumstances, I see no practical issue with tying the attachment point of the Additional Excess Sub-Limits to the exhaustion of an underlying sub-limit, given the relevant sub-limits are, in any event, part of, and not in addition to, the respective Limits of Liability for Section 1B cover. Indeed, this does not defeat the operation of cl 3.2 (which prevents liability attaching until the limit of liability in the underlying insurance has been exhausted), but merely supplements and interacts with it. There is also no risk of the 2016-17 1XS not being exhausted, as the First Additional Sub-Limit exhausts once Argo has paid its full contribution: see item II(c). Further, it is clear that what is meant by the “remaining amount” in item IV(a) is the amount that remains in respect of the 2016-17 Primary sub-limit and the First Additional Sub-Limit after these sub-limits are applied at the below layers. It is also clear that the sub-limit to apply to “Underlying Insurance” is the First Additional Sub-Limit; this is expressly stated in item IV(a). I also see no issue in the present circumstances with calculating the reduction by reference to a “remaining amount” as opposed to an “amount paid”. Nor does the relief fix Vibe with an obligation inconsistent with its intention. As I have stated above, the way in which the Side C Coverage Intention applied to Vibe was to provide a set proportion of cover at the 2016-17 2XS layer.

E.3.5 Whether there are aspects of the relief that are superfluous

86 Vibe submitted that it is unclear what the inclusion of Item IV(c) is intended to add. It was said that if Vibe pays the amount it is obligated to pay under an aspect of coverage (whether sub-limited or otherwise), then that necessarily exhausts its obligation to pay for that coverage. Quintis submitted that this clause was included for consistency with Item II(c), but did, in their reply submissions, accept that this provision need not be included if considered unnecessary. I am inclined to include this provision in the relief I will grant, as it leaves no doubt as to the way in which the instrument should operate.

87 Lastly, Vibe submitted that “an insurer does not pay ‘under’ a sub-limit”. This is a semantic point of little substantive import. However, for the sake of consistency with the terms previously used by the parties, I am willing to amend the references to “under” in Quintis’ proposed relief to “in respect of” (as is used in the endorsement, recorded at J[246]). The power for me to amend the form of relief in this respect is consistent with reasoning of the Court of Appeal in Queenfield (at [87] per McLeish, Niall and Sifris JJA). Indeed, it is for the Court to determine with appropriate clarity both the substance and detail of the precise variation: Bush v National Australia Bank Ltd (1992) 35 NSWLR 390 (at 407 per Hodgson J).

88 I therefore find that Quintis is entitled to the relief set out in Annexure A to these reasons, which is amended to reflect the changes identified above (at [87]).

F THE PRACTICAL OPERATION OF THE RELIEF

89 Given the novel and somewhat complex nature of the rectified 2016-17 Policies, it is illustrative to demonstrate how the wording, as rectified, is to operate in practice. This is best done by reference to a series of hypothetical examples, represented diagrammatically.

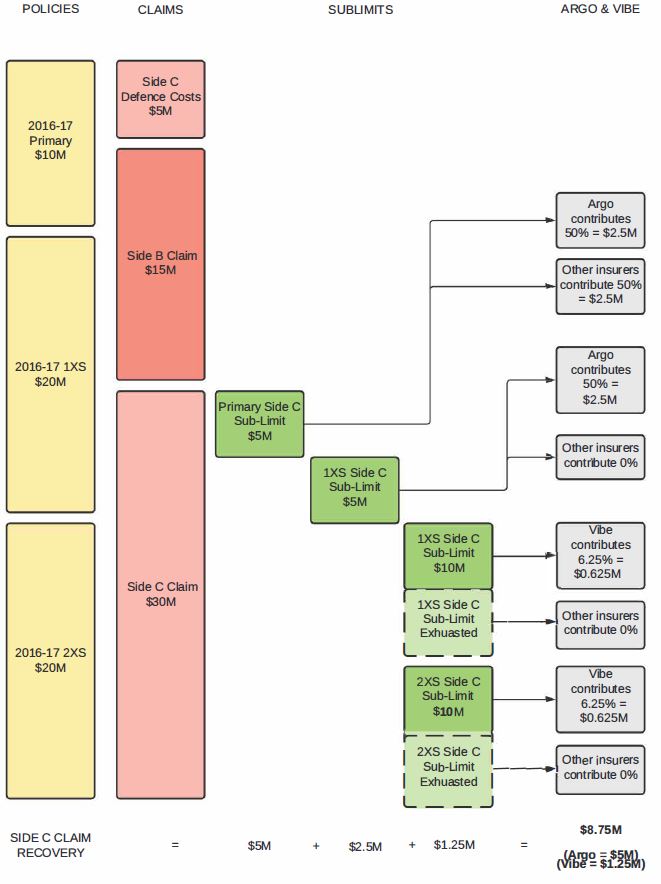

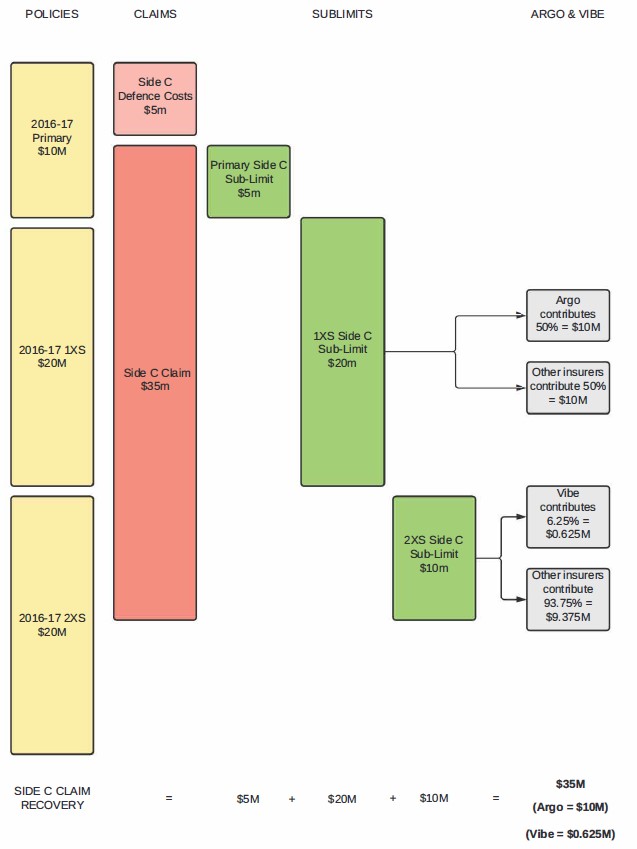

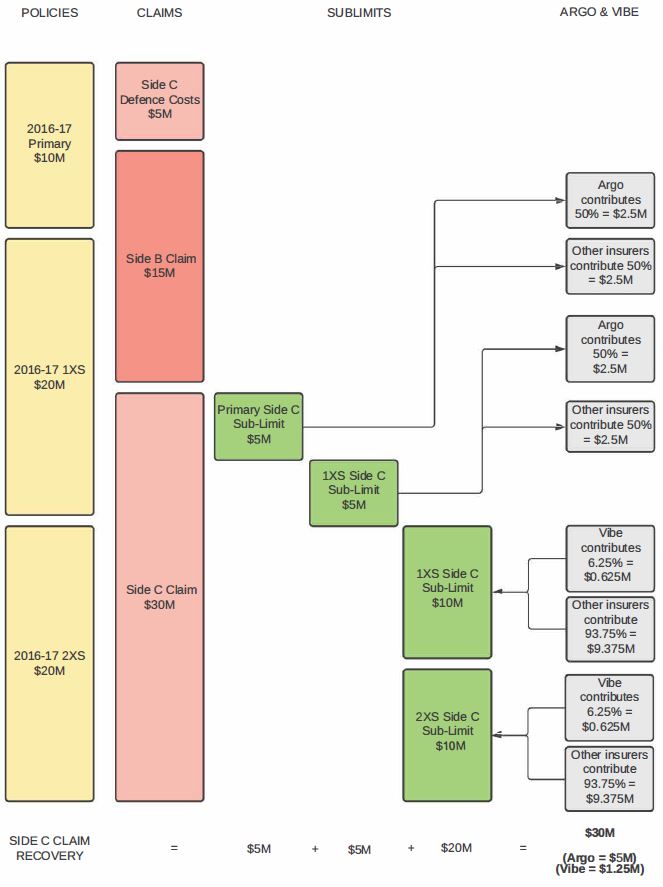

90 In testing the application of the rectified polices, is convenient to demonstrate not only how the policies are to operate in the event of a Side C Claim, but also by reference to a situation in which all parties held the Side C Coverage Intention. To this end, annexed to these reasons are diagrammatical representations of the following counterfactual scenarios:

(1) Annexure B: All Relevant Insurers to the 2016-17 Policies held the Side C Coverage Intention (aggregate $50 million Side C sub-limit). Assumed facts: $35 million Side C claim.

(2) Annexure C: All Relevant Insurers to the 2016-17 Policies held the Side C Coverage Intention (aggregate $50 million Side C sub-limit). Assumed facts: prior $15 million Side B claim and later $30 million Side C claim.

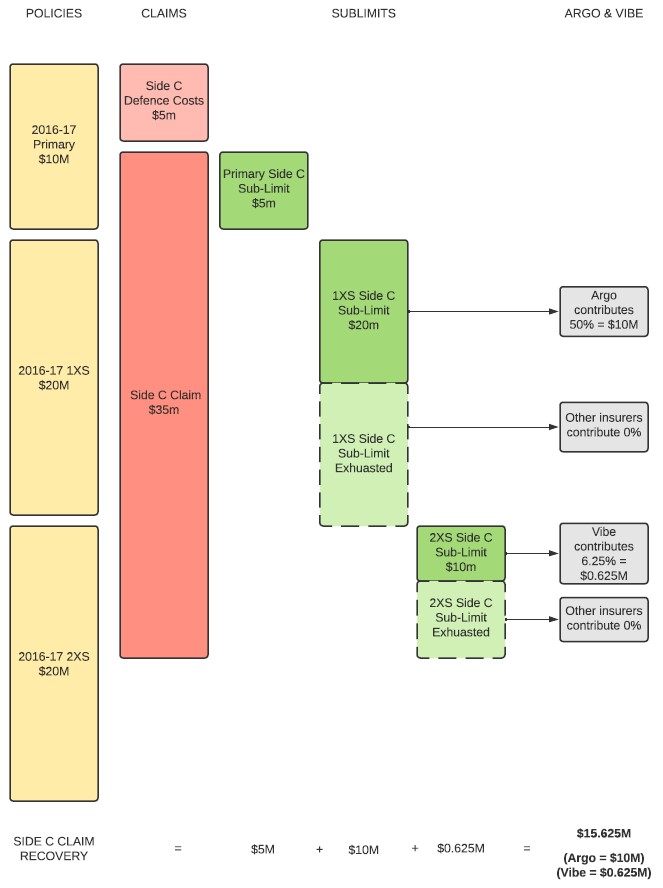

(3) Annexure D: The 2016-17 Policies as rectified (i.e. Argo and Vibe held the Side C Coverage Intention). Assumed facts: $35 million Side C claim.

(4) Annexure E: The 2016-17 Policies as rectified (i.e. Argo and Vibe held the Side C Coverage Intention). Assumed facts: prior $15 million Side B claim and later $30 million Side C claim.

91 I have been assisted by the submissions of Quintis in the construction of these diagrams.

92 Further, and although not the subject of any submissions, I should note one change (beyond fixing calculation errors) that I have made to these diagrams to reflect what, in my view, is the way in which the relief is to operate on its terms. In Annexure C and E, Quintis originally noted that the amount payable at the 2016-17 2XS layer in accordance with the First Additional Sub-Limit was $15 million, with $5 million to then be paid in accordance with the Second Additional Sub-Limit (I note that in Annexure E, reference was actually made to $5 million being payable in respect of the First Additional Sub-Limit not $15 million, although, when one takes into account the calculation of Vibe’s liability, this must have been a typographical error).

93 I presume the thinking behind these figures was as follows:

(1) in accordance with the counterfactual, there would be $15 million remaining in respect of the First Additional Sub-Limit ($5 million already having been exhausted at the 2016-17 1XS layer); and

(2) given the Second Additional Sub-Limit is to be reduced by the amount remaining in respect of the First Additional Sub-Limit (see item IV(a)), liability in accordance with the Second Additional Sub-Limit would be $5 million.

94 The difficulty I have with this breakdown is that I do not think it accounts for the operation of item II(a), which dictates that if the 2016-17 Primary sub-limit rolls into the 2016-17 1XS, then the First Additional Sub-Limit is to be reduced by the remaining amount of the 2016-17 Primary sub-limit. Indeed, in light of this provision, I am of the view the following operation is correct: