FEDERAL COURT OF AUSTRALIA

Quality Medical Innovations Pty Ltd v Keogh [2021] FCA 154

ORDERS

QUALITY MEDICAL INNOVATIONS PTY LTD ACN 101 586 476 First Plaintiff MR KIM LEONARD GAUL Second Plaintiff | ||

AND: | First Defendant MAJAC MEDICAL PRODUCTS PTY LIMITED ACN 086 942 421 Second Defendant | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Paragraphs 2 to 6 of the plaintiffs’ interlocutory application filed on 4 December 2020 be dismissed.

2. Each party pay their own costs of this application.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MARKOVIC J:

1 On 27 October 2020, Kim Leonard Gaul as plaintiff commenced this proceeding against Quality Medical Innovations Pty Limited (QMI), Michael Phillip Keogh and Majac Medical Products Pty Limited (Majac) as first, second and third defendants respectively. Dr Gaul and Mr Keogh are both directors of and equal shareholders in QMI. Mr Keogh is the sole director of and shareholder in Majac.

2 At the time of commencement of the proceeding Dr Gaul sought relief under s 232 and s 233 of the Corporations Act 2001 (Cth) (Corporations Act) and orders requiring QMI to commence proceedings against Mr Keogh and Majac for, among other things, alleged breaches by Mr Keogh of his director’s duties and passing off. On 4 December 2020, Dr Gaul filed an interlocutory process (IP) seeking leave to commence proceedings in the name of QMI against Mr Keogh and Majac in respect of causes of action pleaded in a draft statement of claim (which has been subsequently filed) and for interim injunctive relief pursuant to s 1324 of the Corporations Act.

3 On 14 December 2020, orders were made by consent including an order granting Dr Gaul leave to join QMI as a plaintiff to the proceeding and otherwise dismissing Dr Gaul’s application for leave to commence a proceeding in the name of QMI as sought in para 1 of the IP. As a result, the parties to this proceeding now comprise QMI and Dr Gaul as first and second plaintiffs respectively and Mr Keogh and Majac as first and second defendants respectively.

4 QMI and Dr Gaul press their application for interim injunctive relief included at paras 2 and 3 of the IP. They seek the following orders:

2. An order that [Mr Keogh and Majac], by themselves, their employees, or agents, be restrained until further order from:

(a) making representations in trade or commerce about or relating to any products of [QMI], or any brand or trademark associated with [QMI];

(b) offering for sale, under any trading name, brand or trademark, any product created or derived from chemical formulae being the property of [QMI];

(c) offering for sale, under any trading name, brand or trademark, any product created or derived from formulae for the products offered for sale by [QMI] under any of the trademarks set out in the schedule attached hereto in the column headed "QMI Trademark";

(d) offering for sale any product under the trademarks or brands set out in the schedule attached hereto in the column headed "Majac mark".

3. In the alternative to prayer 2, an order that until further order:

(a) [Majac] pay all proceeds from the sale of any product sold under any of the brands set out in the schedule attached hereto in the column headed "Majac mark" into a bank account dedicated for that purpose (Escrow Account);

(b) [Majac] be restrained from withdrawing any funds from the Escrow Account save for any account-keeping or other administrative fees relating to the maintenance of the Escrow Account;

(c) [Majac] is to provide to the plaintiff a monthly statement for the Escrow Account;

(d) [Majac] is to facilitate inspection of its books and records by qualified professionals engaged on behalf of the plaintiff for the purpose of confirming [Majac’s] compliance with these orders.

5 In the course of the hearing of QMI and Dr Gaul’s application for the relief set out in the preceding paragraph, Mr Keogh proffered an undertaking (Undertaking) to the Court until determination or settlement of the proceeding or further order in the terms of para 2(a) of the IP which has been noted. The Undertaking is a complete answer to the claim for relief in para 2(a) of the IP.

6 Mr Keogh and Majac oppose the balance of the relief sought by Dr Gaul and QMI in paras 2 and 3 of the IP.

EVIDENCE

7 Dr Gaul and QMI relied on three affidavits sworn by Dr Gaul on 23 October 2020, 4 December 2020 and 11 February 2021. Mr Keogh and Majac relied on two affidavits affirmed by Jessica Louise Carroll, a solicitor in the employ of Thynne + Macartney, their solicitors, on 1 February 2021 and 15 February 2021. I set out below a summary of the evidence relevant to the application now before me.

QMI is established

8 In 2000, Dr Gaul, Mr Keogh and Linley Lochead formed a partnership to produce and market infection control products for the healthcare industry. They called the partnership business Quality Medical Innovations and referred to it as QMI. The partnership business was conducted on the basis that Dr Gaul, Mr Keogh and Ms Lochead were equal partners. As far as Dr Gaul can recall, there was no formal partnership agreement.

9 At about the same time as the formation of the partnership, there was also an agreement between Dr Gaul, Mr Keogh and Ms Lochead that Majac sell QMI products. Majac subsequently became the sole distributor of those products.

10 On 5 August 2002 QMI was registered as a company. Upon its registration, Dr Gaul, Mr Keogh and Ms Lochead were appointed directors of, and were equal shareholders in, the company, each holding ten shares. QMI continued to sell and distribute its products solely through Majac.

11 On 30 October 2003 Ms Lochead resigned as a director of QMI and in March 2014 she sold her shares in QMI to Dr Gaul. Subsequently Dr Gaul transferred five of the shares he acquired from Ms Lochead to Mr Keogh at the same price that he had paid per share to Ms Lochead.

Trade marks used by QMI

12 QMI uses trade marks, which are registered in the names of Dr Gaul and Mr Keogh, for its products. According to Dr Gaul the following trade marks (QMI Trade Marks), in each case registered in his and Mr Keogh’s names, are used by QMI:

Trade mark | Date Registered | Registration costs paid for by |

Clinidet | 9 October 2000 | The Partners |

Clinicol | 20 July 2001 | The Partners |

CliniZyme | 2 February 2004 | QMI |

CliniVac | 2 February 2004 | QMI |

Clini-Sorb and Clinisorb | 7 January 2006 | QMI |

Vibactum | 3 February 2010 | QMI |

CliniGuard | 27 June 2012 | QMI |

Clinisoak and Clini-soak | 23 December 2016 | QMI |

Clinijet | 23 December 2016 | QMI |

QMI has paid for all registration renewal fees for the QMI Trade Marks.

13 Dr Gaul had originally intended for the Clinidet trade mark to be registered in the joint names of all of the partners. However, he recalls that at the time of its registration a conversation to the following effect took place:

Ms Lochead: I don't want to have any trademarks in my name. I think it would compromise my consulting work because of the potential conflict of interest.

Dr Gaul: That is understandable. It doesn't matter who holds the trademarks, since they belong to the partnership anyway.

Mr Keogh: I agree. Kim and I can hold the trademarks in our names on behalf of the partnership.

14 Dr Gaul has always regarded all of the QMI Trade Marks as the property of QMI.

15 Despite that, on 20 September 2006, Dr Gaul, Mr Keogh and QMI entered into a trade mark licence (TM Licence). While Dr Gaul cannot now remember precisely why that was so, he recalls that it related to ensuring that QMI had a legal right to the use of some of the QMI Trade Marks. At the time there was a dispute relating to those trade marks and Dr Gaul opines that it may be that dispute that led to the entry into of the TM Licence.

16 The TM Licence:

(1) defines:

(a) “Licensed Trade Marks” to mean the trade marks set out in schedule 1 which are the Clinidet, Clinicol and CliniZyme trade marks;

(b) “Term” to mean a period of 10 years commencing on the date of the TM Licence or, in relation to any particular individual trade mark, the date of the lapsing of registration of that trade mark included in schedule 1, whichever is the earlier;

(c) “Licence Fee” to mean 2.5% of the gross revenue from sales of goods and/or services (net of GST) by QMI displaying or in any way using any of the Licenced Trade Marks;

(2) provides at:

(a) cl 2.1 for the grant by Dr Gaul and Mr Keogh to QMI of a non-exclusive non-assignable licence for the Term and in Australia to use the Licensed Trade Marks only upon or in relation to the goods and/or services for which they are registered;

(b) cl 2.2 that QMI will pay the License Fee to Dr Gaul and Mr Keogh; and

(c) cl 3.1 that:

QMI acknowledges Gaul and Keogh’s title to the Licensed Trade Marks in Australia and the validity of Gaul and Keogh as the registered owners under the [Trade Marks Act 1995 (Cth)] and undertakes not to take any action which would or might:

(a) invalidate or put in dispute Gaul and Keogh’s title;

(b) oppose any application for registration of the Licensed Trade Marks or invalidate any registration of the Licensed Trade Marks in due course;

(c) support an application to remove the Licensed Trade Marks as a registered trade mark,

nor will QMI assist any other person directly or indirectly in any of these acts.

17 According to Dr Gaul, he and Mr Keogh never discussed taking a licence fee and no licence fee was ever paid to either of them but a fee was included in the TM Licence on the advice of the lawyer who prepared it in order to ensure that QMI’s right to use the trade marks was legally binding.

18 The term of the TM Licence has expired and a new licence has not been entered into. However, Dr Gaul says that he and Mr Keogh have permitted QMI to continue to use the QMI Trade Marks.

19 Dr Gaul considered that following Ms Lochead’s departure from QMI there was no longer any need for trade marks to be held separately from its other assets. While Ms Lochead was with QMI, the ownership of the trade marks had apparently been in conflict with her consulting business. Accordingly, in 2017 QMI registered the following trade marks in its name: Plasdet in March 2017, Alpha 10 in August 2017; and Aquadet in September 2017 (2017 Trade Marks).

The operations of QMI and its relationship with Majac

20 Dr Gaul describes himself as QMI’s managing director. He says that he has the technical expertise in relation to product formulation whereas Mr Keogh’s role was limited to sales which were undertaken through Majac. While there was no formal resolution of directors to appoint Dr Gaul to the role of managing director, he conducted its banking, carried out negotiations in relation to pricing, manufacturing and supply chains, caused the company to enter into production contracts and arranged for payments to manufacturers. These tasks were undertaken without any objection from Mr Keogh.

21 According to Dr Gaul he did not require Mr Keogh’s approval to conduct the business of QMI and Mr Keogh did not seek to constrain or limit the powers he exercised but was happy for Dr Gaul to do so as he saw fit. Dr Gaul relies on an email dated 21 February 2019 from Mr Keogh titled “general business matter”, in which Mr Keogh refers to Dr Gaul as “head clerk”, as an acknowledgement by Mr Keogh of his role as managing director.

22 According to Dr Gaul, he and Mr Keogh were generally on good terms and communicated regularly about the operation of the businesses of QMI and Majac.

23 Dr Gaul describes the procedure which was adopted for the sale of QMI products through Majac as follows:

(1) Mr Keogh would email Dr Gaul orders of QMI products;

(2) Dr Gaul would arrange for the production of the product ordered by Majac and pay third party manufacturers for their manufacture and delivery of those products to Majac;

(3) QMI invoiced Majac for the goods ordered and delivered, and Majac was required to pay QMI for the product supplied to it. QMI kept the funds paid to it by Majac and, apart from a small salary paid to Dr Gaul, all of its profit was reinvested into QMI; and

(4) Majac would then sell the QMI products at a mark up and derive profit from selling those goods. Majac kept all funds it derived from selling the QMI products.

24 Dr Gaul’s evidence is that over the years Majac was often unable to pay QMI’s invoices. From time to time he would forgive a debt owed by Majac to QMI and, on other occasions, he would provide Majac with free product to assist it. Until recently, Dr Gaul spent a significant amount of time and QMI’s resources assisting Mr Keogh to market and sell QMI products included in the Majac product list. Dr Gaul felt that it was in QMI’s best interest to keep Majac solvent and strong because Majac could then put more effort into selling QMI’s products.

25 Whilst QMI forgave or wrote off some debts owed by Majac, Dr Gaul also kept a record of those invoices that were not forgiven or written off and for which Majac remains indebted to QMI. Those invoices cover the period 28 December 2017 to 27 August 2020 and are for a total amount of $166,614.24.

26 Ms Carroll has been informed by Mr Keogh that Majac is ready, willing and able to pay QMI for all products supplied and properly invoiced but that it has been unable to substantiate the amount which QMI says remains owing to it.

Mr Keogh contacts Symbio Australia

27 Symbio Australia is one of the major manufacturers of QMI products.

28 Dr Gaul’s evidence is that on 16 April 2020 Guy Warner, a shareholder and the CEO of Symbio Australia, telephoned Dr Gaul and reported on conversations he said he had with Mr Keogh the previous day and over the previous few months. According to Dr Gaul, Mr Warner said words to the following effect to Dr Gaul:

Mike was abusive and belligerent towards me. He threatened legal action against Symbio Australia, and demanded that Symbio Australia hand over to him all price lists and pricing for QMI products along with formulations and technical information regarding QMI products. Throughout the conversation Mike insisted that I was to keep the call confidential and not to tell you about the call.

And:

I felt compromised and bullied into the actions. I don't think this was right.

And:

I'm of the opinion that Mike wishes to create a copy of QMI products for Majac branding.

And:

I have supplied Mike with a test formulation for hand sanitiser, however, QMI has the formulation for Clinisan and that would be a competing sanitiser to that being proposed by Mike.

And:

The conversations with Mike has placed the business relationship between QMI and Symbio Australia at risk

And:

I will refuse to continue to manufacture QMI products if Mike continues to contact me.

29 Dr Gaul says that Mr Keogh had no reason to contact Symbio Australia because he had no role in the technical, purchasing or logistic aspects of QMI, although occasionally he would liaise with Symbio Australia in order to coordinate delivery times of product.

Correspondence between the parties

30 There followed, commencing in late April 2020 and up to mid May 2020, an exchange of correspondence between:

(1) the solicitors for Mr Keogh and the solicitors for QMI in which the solicitors for Mr Keogh requested copies of QMI’s constitution, share certificates, minutes of each annual general meeting since the registration of QMI and the resolution authorising set up of QMI’s bank account. To the extent they existed, those documents were provided;

(2) the solicitors for QMI and Mr Keogh concerning the conversation reported by Mr Warner of Symbio Australia and alleging that Mr Keogh was acting in breach of his duties owed to QMI as a director; and

(3) Mr Keogh, on behalf of Majac, and Dr Gaul in relation to two QMI products, Clinicol and Vibactum, and whether those products should be listed on the Australia Register of Therapeutic Goods (ARTG).

I do not propose to set out any of this correspondence in detail. Suffice to say it demonstrates a deterioration in the relationship between Dr Gaul and Mr Keogh.

Directors’ Meeting 19 June 2020

31 On 19 June 2020 a meeting of the directors of QMI was held. Dr Gaul and Mr Keogh attended and Chen Gaul, Dr Gaul’s wife who was also the accountant for QMI, attended as an observer. Dr Gaul’s description of the nature of that meeting manifests the deterioration of the relationship between him and Mr Keogh. In the course of the meeting a suggestion was made by Dr Gaul that he sell his shares in QMI to Mr Keogh.

Mr Keogh’s correspondence

32 On 25 June 2020, Mr Keogh in his capacity as a director of QMI sent a letter to Mr Warner of Symbio Australia which was marked confidential and included:

Due to changes that are to occur with the ownership of Quality Medical Innovations Pty Ltd (QMI) I am obliged to audit all outstanding accounts and the general business of QMI.

We require your assistance with business matters relating to Symbio Chemicals.

1. A Statement and copies of all outstanding invoices on QMI.

2. Current Price Lists to include a display of what components QMI contributes and the costs to Symbio Chemicals e.g. labels, chemicals. After perusal we will discuss any options that may be more functional and profitable, for the future.

3. Do not dispose of any Clinidet or Vibactum until we have a discussion next week. The reason for the return of these two disinfectants is that QMI (Kim Gaul) has a conflict of claims with the TGA regarding the ability of the two products and the claims actually made. Kim Gaul had given literature that implied that Clinicol was a Virucide and as you are aware it will kill a virus but if the Disinfectant is not listed on the ARTG (Australian Register of Therapeutic Goods) then no claim is to be made. He has submitted test results that were authentic alright but removed from the TGA register and quite old. It was after counsel with a representative of the TGA who suggested that we return the goods to the Sponsor/Manufacturer pending an acceptable explanation. As you are aware the TGA has issued specific Directives regarding Disinfectant Claims as a result a Pandemic (COVID-19) Situation being declared.

…

I appreciate your assistance and will discuss future forecasts and requirements next week after we achieve a resolution to the outstanding financial obligations.

33 Dr Gaul does not accept any of the allegations made by Mr Keogh in point 3 of his letter to Symbio Australia. It is not necessary, in the context of the current application, to set out his explanation for why that is so.

34 On 25 June 2020 Mr Keogh in his capacity as director of QMI sent a letter to Roger White, director of Australian Chemical Services Pty Ltd (ACS), which was marked confidential and which included:

Due to changes that are to occur with the ownership of Quality Medical Innovations Pty Ltd (QMI). We are obliged to audit all outstanding accounts and the general business of Australian Chemical Services Pty Ltd (ACS) relating to QMI.

We require your assistance with the business matters concerning ACS Chemicals.

1. A Statement and copies of all outstanding invoices on QMI/ACS.

2. Any current projects e.g. I have been advised that QMI, Symbio and ACS are reformulating Clinidet.

3. After perusal we will discuss any options that may be more functional and profitable, for the future.

4. We require copies of all Chemical formulae that are the property of QMI.

…

I appreciate your assistance and will discuss future requirements next week after we achieve a resolution to any outstanding QMI outstanding finances.

Majac is no longer the distributor of QMI products

35 Dr Gaul explains that Majac no longer sources its cleaning and disinfectant products from QMI. So much can be inferred from the joint letter sent by Dr Gaul, on behalf of QMI, and Mr Warner, on behalf of Symbio Australia, to “Quality Medical Innovations Customers” in which QMI announced the “new sole National Distribution Partnership” with its Australian manufacturer, Symbio Australia. Neither the circumstances in which the sole distribution arrangement between QMI and Majac came to an end or the date of despatch of the joint letter is disclosed by Dr Gaul in his evidence. I infer in relation to the latter, from surrounding correspondence, that it was prior to 9 September 2020.

36 Ms Carroll gives evidence about the arrangements between QMI and Majac. She says that she has been informed by Mr Keogh that since about 2003 Majac has been the sole distributor of QMI’s products “pursuant to an arrangement agreed between the parties” and that, in or about August 2020, QMI ceased supply of its products to Majac contrary to that arrangement as a result of an alleged debt owed by Majac to QMI.

37 There is no evidence about the terms of the arrangement said to be struck between QMI and Majac. However, the evidence given through Ms Carroll that Majac was the sole distributor of QMI products accords with Dr Gaul’s evidence to that effect (see [9] above).

Majac develops new products

38 Ms Carroll has been informed by Mr Keogh of the following matters:

(1) Majac has been distributing QMI’s products for 17 years and in that time has developed a reputation in the medical and dental equipment industry as a distributor of those products and built relationships with customers;

(2) the arrangement with QMI to distribute its products represented approximately 60% of Majac’s income;

(3) as a result of the cessation of its arrangement with QMI to distribute its products Majac has suffered, and will continue to suffer, significant financial and reputational loss and loss of long term retailer arrangements;

(4) in order to offset that loss Mr Keogh and Majac, in conjunction with third parties, developed chemical cleaning products to replace the products no longer supplied by QMI. Those products are PreDet, DetVac, DentiVac and PlasClean (Majac Products);

(5) the Majac Products currently represent approximately 5% of Majac’s income. The other 95% of Majac’s income derives from sales of sterilising tests and eye protection equipment. Prior to cessation of its arrangement with QMI to distribute its products sales from this equipment represented approximately 40% of Majac’s income;

(6) as the Majac Products were only introduced to the market in about October 2020, Mr Keogh and Majac are in the process of developing their brand and reputation, with sales figures slowly increasing each month;

(7) since 20 October 2020 Majac’s sales figures for the Majac Products have been approximately $4,300 for DentiVac, DenJet and PlasClean and $6,000 for ProDet; and

(8) Mr Keogh and Majac intend that the Majac Products will eventually produce comparable sales to the products previously supplied by QMI under Majac’s arrangement with it for distribution of QMI’s products.

Mr Keogh’s application for registration of “Clinidet” as a trade mark

39 On 17 November 2020, Dr Gaul conducted a search of IP Australia and located a filing for Clinidet which was under examination and the owner of which is recorded as Mr Keogh. Dr Gaul did not authorise the filing.

Majac’s website

40 Dr Gaul gave the following evidence about statements published by Majac on its website on 23 and 24 September 2020:

(1) on 23 September Majac published the following statement:

CUSTOMERS PLEASE NOTE

All the products sponsored by Quality Medical Innovations (QMI) of Port Macquarie NSW and contract manufactured by Symbio Australia of Heathwood Qld are no longer available. Majac Healthcare is rebuilding this website and an exciting range of “NEW” Clinical Detergents. Once we have advised our customers and distributors of the situation.

(2) on 24 September at 12.16 pm Majac published the following statement:

Kim Gaul a Direction (sic) of our former supply partner Quality Medical Innovations Pty Ltd (QMI) advises that the Disinfectant Vibactum and Clinicol are not on the ARTG or Listed with the TGA. The Disinfectants cannot mek (sic) any claim as being effective against Bacteria or any virus. In the interest of our distributors clinics and their patients we have discontinued being the Distributor.

(3) Dr Gaul instructed QMI’s solicitors to write to Majac’s solicitor demanding the removal of the statement set out above; and

(4) on 24 September 2020 at 2.17 pm Majac published the following statement:

Majac Healthcare has been instructed to remove all of the other brand Cleaning Products and Disinfectants previously distributed by Majac Healthcare from our website.

Our apologies t6o (sic) Kim Gaul and Mike Keogh the Directors of Quality Medical Innovations Pty Ltd (QMI). Majac Healthcare was not aware the information was defamatory or misleading.

We say ‘thank you’ to our loyal customers that are supporting us through this difficult period.

Our website is being changed over the next few weeks as we modify our product range.

41 On 3 December 2020 Dr Gaul logged onto the website at www.majacmedical.com.au and located a page with the heading “Cleaning Products for Infection Control” which offered for sale the following products:

(1) ProDet described as a medical and dental instrument and equipment detergent;

(2) PlasClean described as a medical and dental equipment cleaner for sensitive materials;

(3) DenJet described as a dental aspiration unit sanitizer and cleaner; and

(4) DentiVac described as a foam free daily sanitiser/cleaner.

42 According to Dr Gaul those products correspond with QMI products Clinidet, Plasdet, Clinijet and Clinivac respectively.

Other websites

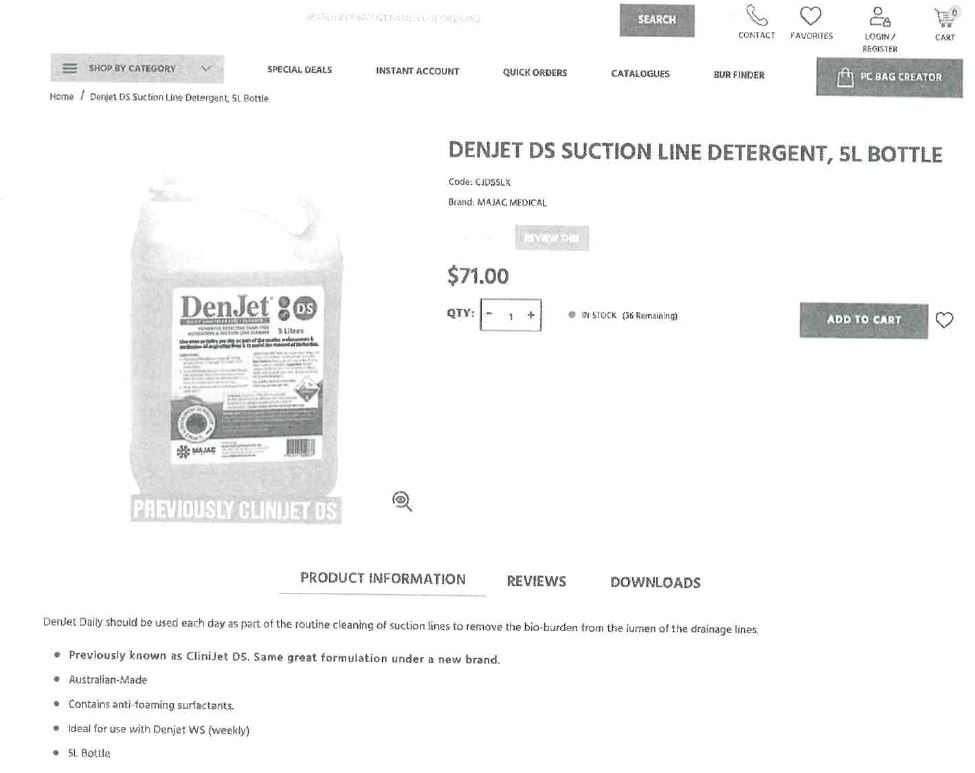

43 On 3 December 2020, Dr Gaul went to web address oriendentalsupplies.com.au/shop/ cleaning-disinfectant/suction-cleaning-solutions.html, a webpage on a website operated by a company trading as Orien Dental Supplies (Orien Webpages). Screenshots taken of the Orien Webpages by Dr Gaul display the Majac Products DenJet, ProDet and DentiVac for sale. The following text is included on those webpages:

(1) in the case of DenJet that it is “previously known as CliniJet DS. Same great formulation under a new brand”;

(2) in the case of ProDet that it is “previously known as CliniDet. Same great formulation under a new brand”; and

(3) in the case of DentiVac that it is “previously known as CliniVac. Same great formulation under a new brand”.

44 By way of example a copy of one of the screenshots taken by Dr Gaul at the time from the Orien Webpages for DenJet appears as follows:

45 Ms Carroll says that on 15 February 2021 she accessed the Orien Dental Supplies website. She puts into evidence images of the DenJet and DentiVac product pages from that website. Those images show that there is no reference to the QMI products.

DBS Medical website

46 On 11 February 2021, Dr Gaul received an email from Louis Gravestein of Symbio Australia which, in turn, attached an email from Luis Merkyll. There is no evidence about Mr Merkyll’s role, where he works or why he came to send the email. Dr Gaul puts into evidence two images which he said were embedded in Mr Merkyll’s email. Those images appear to be screenshots from a website of DBS Medical Supplies and concern the Majac Products PlasClean and ProDet. By way of example, a copy of one of the images is reproduced below:

47 According to Ms Carroll, Mr Keogh has no control over or interest in the business of or website maintained by DBS Medical Supplies. However, she says that, in response to Dr Gaul’s affidavit sworn 11 February 2021 annexing the screenshots from that website, Mr Keogh contacted a representative of DBS Medical Supplies and asked that there be no reference to QMI PlasDet or CliniDet products in relation to Majac’s products. Insofar as Mr Keogh is aware there are now no such references included on the DBS Medical Supplies site. Screenshots from the DBS Medical Supplies website provided to Mr Keogh by DBS Medical Supplies at 8.47 am on 15 February 2021 were in evidence before me and confirm that to be so. According to Ms Carroll, Mr Keogh never asked or caused the DBS Medical Supplies business to make comparisons between Majac’s products and those of any other company.

THE PLAINTIFFS’ CLAIM

48 In their statement of claim QMI and Dr Gaul seek the following relief:

(1) as against Mr Keogh and Majac:

(a) general damages for breach of confidentiality, copyright infringement, passing off, misleading and deceptive conduct and/or injurious falsehood;

(b) further or in the alternative an account of profits;

(c) a declaration that each of the QMI Trade Marks is held on trust for QMI by Dr Gaul and Mr Keogh;

(d) an order requiring Dr Gaul and Mr Keogh to cause each of the QMI Trade Marks to be registered in QMI’s name; and

(e) permanent injunctions restraining them from making certain representations, offering products created or derived from chemical formulae which are the property of QMI for sale and offering for sale any product under the trade marks or brands ProDet, DentiVac, DenJet and PasClean;

(2) as against Mr Keogh:

(a) a declaration under s 1317E of the Corporations Act that he acted in contravention of ss 181, 182 and/or 183 of that Act;

(b) compensation under s 1317H of the Corporations Act;

(c) a declaration that the affairs of QMI, to the extent they are being conducted by Mr Keogh, are being conducted against the interests of QMI and/or Dr Gaul;

(d) removal of Mr Keogh as a director of QMI;

(e) at the election of Dr Gaul that Mr Keogh be required to sell his shares in QMI at their fair value or, alternatively, that the sale price of those shares be set off against any damages or other sum ordered against Mr Keogh and related relief in relation to the valuation of those shares; and

(f) in the event that Dr Gaul does not elect to acquire Mr Keogh’s shares, an order that QMI be wound up; and

(3) as against Majac:

(a) damages for debt in the sum of $166,614.24; and

(b) further, or in the alternative, an account of profits.

49 QMI and Dr Gaul make claims in relation to the QMI Trade Marks; allege that Mr Keogh breached his duties of good faith and fidelity owed to QMI as a director of QMI in providing information which it is alleged he obtained in his capacity as a director of QMI to enable Majac to produce its products which compete with QMI products; allege that Majac is indebted to QMI for goods delivered to it in the sum of $166,614.24; allege that Mr Keogh and Majac infringed QMI’s copyright; allege that Majac has engaged in passing off by representing that its products and marks are products and marks of QMI; allege that Majac has engaged in misleading or deceptive conduct contrary to s 18 of the Australian Consumer Law being Schedule 2 to the Competition and Consumer Act 2010 (Cth) by making certain representations about QMI products and Majac products; and allege that Mr Keogh and Majac made representations that were false and were published maliciously.

50 Given that QMI and Dr Gaul make their application for interim relief pursuant to s 1324 of the Corporations Act, I do not propose to set out any of these claims in detail. Most relevantly for this application, QMI and Dr Gaul also allege that Mr Keogh has breached his duties under ss 181, 182 and 183 of the Corporations Act, which he owes as a director to QMI, by:

(1) producing and offering for sale the Majac Products;

(2) using information that was confidential to QMI to produce the Majac Products;

(3) creating or procuring and publishing the “ProDet Photograph” and the “ProDet Brochure”. QMI and Dr Gaul allege that the ProDet Photograph was created by digitally altering the photographic depiction of CliniDet products and superimposing labels for ProDet thereon, and that the ProDet Brochure was creating by substantially copying the text and layout of QMI’s promotional brochure for CliniDet, and that in doing so, in each case, Mr Keogh (and Majac) infringed QMI’s copyright;

(4) making representations that the ProDet Photograph and ProDet Brochure were original works of Majac (Copyright Representations);

(5) making representations that DentiVac products are the same products that were previously branded and produced by QMI as CliniVac (Previously Clinivac Representations);

(6) making representations that DenJet products are the same products that were previously branded and produced by QMI as Clinijet (Previously Clinijet Representations);

(7) making representations to Symbio Australia that QMI was acting contrary to its obligations in respect of the requirements of the Therapeutic Goods Administration and the ARTG (TGA Representations);

(8) making representations on or about 23 September 2020 that all QMI products are no longer available (Availability Representations);

(9) making representations on about 24 September 2020 that the QMI products Vibactum and Clinicol were not fit for purpose and had been discontinued by Majac in the interests of Majac’s distributors and customers (FFP Representations); and

(10) causing Majac to undertake each of the matters referred to subparagraphs (1) to (9).

STATUTORY FRAMEWORK AND LEGAL PRINCIPLES

51 In making their application for interim relief the plaintiffs rely on s 1324 of the Corporations Act. That section relevantly provides:

(1) Where a person has engaged, is engaging or is proposing to engage in conduct that constituted, constitutes or would constitute:

(a) a contravention of this Act; or

(b) attempting to contravene this Act; or

(c) aiding, abetting, counselling or procuring a person to contravene this Act; or

(d) inducing or attempting to induce, whether by threats, promises or otherwise, a person to contravene this Act; or

(e) being in any way, directly or indirectly, knowingly concerned in, or party to, the contravention by a person of this Act; or

(f) conspiring with others to contravene this Act;

the Court may, on the application of ASIC, or of a person whose interests have been, are or would be affected by the conduct, grant an injunction, on such terms as the Court thinks appropriate, restraining the first‑mentioned person from engaging in the conduct and, if in the opinion of the Court it is desirable to do so, requiring that person to do any act or thing.

…

(4) Where in the opinion of the Court it is desirable to do so, the Court may grant an interim injunction pending determination of an application under subsection (1).

…

(6) The power of the Court to grant an injunction restraining a person from engaging in conduct may be exercised:

(a) whether or not it appears to the Court that the person intends to engage again, or to continue to engage, in conduct of that kind; and

(b) whether or not the person has previously engaged in conduct of that kind; and

(c) whether or not there is an imminent danger of substantial damage to any person if the first‑mentioned person engages in conduct of that kind.

52 As set out above the plaintiffs allege that Mr Keogh has breached his duties owed to the company under ss 181, 182 and/or 183 of the Corporations Act which relevantly provide:

181 Good faith—civil obligations

Good faith—directors and other officers

(1) A director or other officer of a corporation must exercise their powers and discharge their duties:

(a) in good faith in the best interests of the corporation; and

(b) for a proper purpose.

182 Use of position—civil obligations

Use of position—directors, other officers and employees

(1) A director, secretary, other officer or employee of a corporation must not improperly use their position to:

(a) gain an advantage for themselves or someone else; or

(b) cause detriment to the corporation.

183 Use of information—civil obligations

Use of information—directors, other officers and employees

(1) A person who obtains information because they are, or have been, a director or other officer or employee of a corporation must not improperly use the information to:

(a) gain an advantage for themselves or someone else; or

(b) cause detriment to the corporation.

53 In Armstrong World Industries (Australia) Pty Limited v Parma (2014) 101 ACSR 150; [2014] FCA 743 at [21]-[22] Beach J observed that the statutory test for the grant of an injunction under s 1324(4) of the Corporations Act is in form, and partly in substance, different to the equitable basis and that the jurisdiction exercised by the Court under the former differs from the traditional equitable jurisdiction in at least one type of factor to be taken into account. His Honour identified the additional factor to be whether the injunction would have some utility or would serve some purpose within the contemplation of the Corporations Act such as preventing or ameliorating a threat or contravention of that Act, referring to the discussion in Australian Securities and Investments Commission v Mauer-Swisse Securities Limited (2002) 42 ACSR 605 at 613-614; [2002] NSWSC 741 at [34]-[36].

54 In In the matter of Ikon Group Limited (2015) 107 ACSR 146; [2015] NSWSC 980 Brereton J observed at [22] that the touchstone of s 1324 of the Corporations Act is a past or threatened contravention of the Corporations Act and that the power to grant an injunction under the section is conferred in respect of conduct that constituted, or would constitute, a contravention of that Act. At [26] his Honour said that where interim relief is sought under s 1324 of the Corporations Act, the relevant considerations are usually whether there is a sufficient seriously arguable case of an actual or threatened contravention of the Act, the balance of convenience and whether there are any other discretionary considerations informing the grant of interlocutory relief.

55 In Samsung Electronics Co Ltd v Apple Inc (2011) 217 FCR 238 (Samsung) at [55] a Full Court of this Court (Dowsett, Foster and Yates JJ), in considering the grant of an interlocutory injunction in the context of a patent case, identified that the two questions to be considered by the Court are: first, whether the plaintiffs have made out a prima facie case, “in the sense that if the evidence remains as it is there is a probability that at the trial of the action the plaintiff will be held entitled to relief”; and secondly, “whether the inconvenience or injury which the plaintiff would be likely to suffer if an injunction were refused outweighs or is outweighed by the injury which the defendant would suffer if an injunction were granted”, quoting from Beecham Group Ltd v Bristol Laboratories Pty Ltd (1968) 118 CLR 618.

56 At [67]-[68] their Honours observed that the two questions are interrelated, noting that the questions of whether there is a serious question or prima facie case should not be considered in isolation from the balance of convenience. Their Honours observed that the apparent strength of the parties’ substantive cases can be an important consideration to be weighed in the balance and that it may also be necessary to consider and evaluate the impact that the grant or refusal of an injunction will have or is likely to have on third persons and the public generally.

CONSIDERATION

Is there a serious question to be tried?

57 QMI and Dr Gaul submit that, in relation to the claims based upon Mr Keogh’s breaches of his duties as a director of QMI and upon the representations by Mr Keogh and Majac in respect of, and misappropriation of, QMI’s products, there is a considerable weight of evidence that Mr Keogh and Majac have not sought to challenge on this application. They submit that Mr Keogh has represented to the market in which QMI trades, to QMI’s manufacturer, Symbio Australia, and to ACS, its quality assurance provider, that QMI’s products are not compliant with TGA requirements, assertions for which there is no support. They say that even if those assertions had substance, as a director of QMI it would be incumbent upon Mr Keogh to act in QMI’s interest and seek to resolve any such issues internally.

58 QMI and Dr Gaul observe that the defendants attempt to excuse Mr Keogh competing directly with QMI as a reaction to QMI denying supply to Majac in August 2020 but contend that the difficulties with that assertion include that Mr Keogh was attempting to obtain QMI formulations and price lists from Symbio Australia from as early as August 2020; Mr Keogh began making unsupported allegations about QMI being non-compliant with TGA requirements no later than May 2020; Majac’s return of stock to Symbio Australia without prior warning appears to be based upon the unsupported TGA claims and the escalation of Mr Keogh’s and Majac’s moves against QMI appears to coincide with Dr Gaul raising historical debts owned by Majac to QMI in response to the return of stock by Majac to Symbio Australia.

59 QMI and Dr Gaul submit that, in any event, so long as Mr Keogh remains a fiduciary of QMI he is and at all times has been bound to act in the interests of QMI and he was thus prohibited from competing with QMI through Majac. QMI and Dr Gaul say that the fact that Mr Keogh placed himself and Majac in a position of conflict with QMI is no answer to that charge but is rather an independent and overlapping example of Mr Keogh’s breaches of duty to QMI. They contend that there is a serious question to be tried on QMI’s claim in respect of breaches of fiduciary duty by Mr Koegh, through Majac.

60 These submissions were supplemented by detailed oral submissions.

61 Mr Keogh and Majac submit that the plaintiffs’ case reduces to the say-so of Dr Gaul about alleged oral agreements and understandings, which are denied, and brought in the face of Dr Gaul’s own conduct of excluding a co-director and 50% owner of QMI and the QMI Trade Marks from information and participation in management to which Mr Keogh is entitled; termination of a distribution arrangement with Majac without board or shareholder approval; entering into a new distribution partnership with Symbio Australia without notifying, and in the face of express disapproval by, Mr Keogh; and holding himself out as “managing director” when he knows no such authorisation or delegation has been made.

62 Mr Keogh and Majac contend that, on the materials before it, the Court cannot be satisfied that there is a serious question or prima facie case which warrants injunctive relief. If the evidence remains as it is the Court cannot be satisfied that there is a probability that at the trial of the action QMI and Dr Gaul will be held entitled to relief.

63 The question of whether there is a serious question to be tried, or perhaps put more precisely in the context of s 1324(4) of the Corporations Act whether there is a sufficiently seriously arguable case of an actual or threatened contravention of the Corporations Act, must be considered through the lens of the claims made by QMI and Dr Gaul against Mr Keogh for breach of the Corporations Act and the nature of the interim relief sought.

64 In terms of the pleaded claim, first Mr Keogh is alleged to have breached his duties owed under ss 181, 182 and/or 183 of the Corporations Act by making the Copyright Representations, the Previously Clinivac Representations, the Previously Clinijet Representations, the TGA Representations, the Availability Representations and the FFP Representations. Much of the oral argument before me and evidence relied on by QMI and Dr Gaul focussed on Mr Keogh’s conduct in making these representations. The interim relief sought in para 2(a) of the IP seeks to restrain conduct of this nature.

65 The Undertaking which has been given by Mr Keogh to the Court and which is in terms of para 2(a) of the IP, in effect, provides the relief sought. Subject to the impact on the question of costs, which I address below, no more need be said about the alleged breaches by Mr Keogh arising out of this conduct.

66 Secondly, Mr Keogh is alleged to have breached his duties owed under ss 181, 182 and/or 183 of the Corporations Act by using information that was confidential to QMI to produce the Majac Products. By the relief sought in paras 2(b) and (c) of the IP, QMI and Dr Gaul seek to restrain the sale of any of the Majac Products that were created or derived from chemical formulae which are the property of QMI or from formulae for the products offered for sale under the QMI Trade Marks or the 2017 Trade Marks.

67 I accept that if there is evidence to establish or ultimately prove, on the balance of probabilities, that Mr Keogh used information that was confidential to, or the property of, QMI to produce the Majac Products, that would amount to a sufficiently arguable case that Mr Keogh breached his duties owed to QMI under ss 181, 182 and/or 183 of the Corporations Act. The issue that arises is whether there is sufficient evidence before me for the plaintiffs to establish that is so.

68 The evidence relied on by QMI and Dr Gaul establishes that, in April 2020, Mr Keogh asked Mr Warner of Symbio Australia for “formulations and technical information” for QMI products and that, on 25 June 2020, he requested ACS to provide “copies of all Chemical formulae that are the property of QMI”. It is apparent that Mr Keogh sought to obtain this information in a somewhat clandestine manner to the exclusion of Dr Gaul. However, based on the evidence before me, it is also apparent that the information sought was not provided to Mr Keogh.

69 The plaintiffs submit that I should infer, in light of the enquiries made by Mr Keogh and the subsequent production of the Majac Products in competition with the QMI products, that the Majac products were produced based on or using the formulae for QMI products. However, there is nothing in the evidence relied on by QMI and Dr Gaul that would permit me to draw that inference.

70 QMI and Dr Gaul also rely on “safety data sheets” which are published in relation to each QMI product, and submit that it is possible, based on those documents, to discern the composition of products. Those documents include, at part 3, “composition/information on ingredients”. However, there was no evidence before me about how the material included there, which did not on my review seem to include a complete list of the ingredients in any of the products, might be used, in effect, to reverse engineer the formula for a particular product.

71 In my view, QMI and Dr Gaul have not established a sufficiently arguable case that Mr Keogh breached his duties owed to QMI under ss 181, 182 and/or 183 of the Corporations Act by using QMI’s confidential information to produce the Majac Products.

72 Thirdly, Mr Keogh is alleged to have breached his duties owed under ss 181, 182 and/or 183 of the Corporations Act by producing and offering for sale the Majac Products. By the relief sought in para 2(d) of the IP, QMI and Dr Gaul seek to restrain Mr Keogh and Majac from offering for sale any product under the trade marks or brand names ProDet, DentiVac, DenJet and PlasClean.

73 As I understand it, QMI and Dr Gaul submit that as a director of Majac, which competes with QMI, Mr Keogh has placed himself in a position of conflict in breach of his duties owed to QMI or, alternatively, by producing and selling the Majac Products Mr Keogh is diverting business opportunities from QMI to Majac.

74 In support of those propositions, QMI and Dr Gaul rely on Fitzpatrick v Cheal (2012) 264 FLR 313; [2012] NSWSC 261. The facts of that case are complicated but, relevantly, there was an allegation of breach of ss 180, 181 and 182 of the Corporations Act and an allegation of breach of fiduciary duty owed by the defendant, Mr Cheal. In the context of considering whether that was so, Ward J (as her Honour then was) considered the authorities relating to the obligations of a fiduciary. QMI and Dr Gaul rely on [117] and [122] where her Honour said:

117 As to the equitable duties alleged to have been breached, Mr Evans notes that the essential obligation imposed on a fiduciary is that stated by Lord Hershell in Bray v Ford [1896] AC 44 at 51-2:

It is an inflexible rule of a Court of Equity that a person in a fiduciary position, such as the respondent's, is not, unless otherwise expressly provided, entitled to make a profit; he is not allowed to put himself in a position where his interest and duty conflict. It does not appear to me that this rule is, as has been said, founded upon principles of morality. I regard it rather as based on the consideration that, human nature being what it is, there is danger, in such circumstances, of the person holding a fiduciary position being swayed by interest rather than by duty, and thus prejudicing those whom he was bound to protect. It has, therefore, been deemed expedient to lay down this positive rule.

…

122 In Canadian Aero Service v O'Malley [1974] SCR 592; 40 DLR (3d) 371, Laskin J said:

An examination of the case law in this Court and in the Courts of other like jurisdictions on the fiduciary duties of directors and senior officers shows the pervasiveness of a strict ethic in this area of the law. In my opinion, this ethic disqualifies a director or senior officer from usurping for himself or diverting to another person or company with whom or with which he is associated a maturing business opportunity which his company is actively pursuing; he is also precluded from so acting even after his resignation where the resignation may fairly be said to have been prompted or influenced by a wish to acquire for himself the opportunity sought by the company, or where it was his position with the company rather than a fresh initiative that led him to the opportunity which he later acquired.

(Emphasis added.)

(Original Emphasis.)

75 Ultimately, Ward J found, in the circumstances of the case before her Honour, that Mr Cheal had breached his statutory and fiduciary duties as a director in a number of ways.

76 There are a number of other cases in which the issue of conflict in the context of the personal interests of a director and those owed by the director to the company have been considered. One such case is Links Golf Tasmania Pty Ltd v Sattler (2012) 213 FCR 1 (Links Golf). In that case the plaintiff, who I will refer to as LGT, operated a golf course on land which it leased from the defendant, Mr Sattler. Mr Sattler also owned an adjoining piece of land on which he developed a second golf course. At the time of establishment of the second golf course, Mr Sattler was a director of LGT but, by the time the second golf course was operating as a business, he had resigned from that position. One argument advanced by LGT was that Mr Sattler’s decision to carry on a competing business necessarily involved a conflict of interest and duty. This argument was distinct from any argument that Mr Sattler had breached his duties owed as a director to LGT by taking for himself an opportunity to develop the second golf course that should have been offered to LGT: Links Golf at [539].

77 Following a comprehensive review of the authorities Jessup J observed at [562] that “[i]t is … a striking feature of the authorities referred to above how rare have been the circumstances in which a court has been called on to deal with the pure case of a director’s involvement in a competing business, without any additional or complicating factor”. His Honour continued at [562]-[564]:

562 … I must accept that, in Australia, Bell v Lever Bros is good law to the extent that it stands for the proposition that merely by acting as a director of a competing company, or carrying on a competitive business on his or her own behalf, a company director will not be regarded as being in breach of his or her fiduciary obligations. …

563 Although nowhere so stated in terms, the principle with which the authorities are consistent is that carrying on business — including doing so by working as an executive director of a company — in competition with the company of which he or she is a non-executive director will not necessarily be regarded as involving a conflict of interest or duty. It cannot be assumed, as a matter of fact, that a situation of this kind will inescapably involve “a real or substantial possibility of a conflict between [the director’s] personal interests and those of the persons whom he [or she] is bound to protect” (Hospital Products at 103 per Mason J). So understood, the principle is a very high-level one that could be used only as the broadest of starting points for the resolution of issues arising in a particular case.

564 Notwithstanding the heavily qualified nature of the legal principle on which LGT relies, to the extent that the defendants’ case is to be understood as involving the proposition that Lord Blanesburgh’s dictum in Bell v Lever Bros opens up as legitimate any and all kinds of competitive business to the director of a company, that proposition must be rejected. The question whether, in the light of the nature of the competitive business, the director’s role in it and other relevant circumstances, the director’s conduct would give rise to the sensible possibility of conflict, is not foreclosed by the dictum. At most, the dictum means that the mere fact of being the director of a company will not preclude the director from engaging in a competing business on his or her own account. But it leaves open any issues of actual conflict, or of conflict reasonably perceived to be within the range of sensible possibilities, arising on the facts of a particular case.

(Emphasis added.)

78 At [574] Jessup J observed that “[t]he question which equity requires the fiduciary to ask of himself or herself is not ‘will my establishment of a second business deliver a benefit to the first?’, but ‘in the conduct of a second business, is it a substantial possibility that I will be required to make decisions, and to conduct myself generally, in circumstances where I will be confronted with a conflict?’”. At [575] his Honour said:

In the nature of things, the prospect that Sattler, operating his own business at Lost Farm, would, from time to time if not regularly, be obliged to make decisions that might work to the relative advantage of Lost Farm over Barnbougle Dunes, or vice versa, could not be dismissed as insubstantial. Nothing in the evidence suggests otherwise. The situations in which Sattler might find himself facing a conflict may be of such subtlety that he himself would not recognise the fact of conflict. Even an attempt at even-handedness may not achieve the result which equity would require, which is that of undivided loyalty to the company of which the fiduciary is a director. …

79 In Australian Careers Institute Pty Ltd v Australian Institute of Fitness Pty Ltd (2016) 340 ALR 580; [2016] NSWCA 347 the New South Wales Court of Appeal upheld a finding that Mr Hornsey, a director of the respondent, had breached his duties as director by setting up and promoting a fitness education business known as the Sage Institute of Fitness which competed with the business conducted by the respondent. In the course of doing so, Sackville AJA (with whom Meagher JA agreed) referred to Links Golf at [563] and, at [135], observed that the conclusion reached there “appeared to be sound as a matter of principle”. At [136]-[137] his Honour described the nature of the enquiry to be undertaken when determining whether a conflict arose:

136 In determining whether there is a conflict between the personal interests of a director of a company, and the director’s duties to the company, it is necessary to identify the functions or responsibilities the director has undertaken in that capacity. As was said by the Full Federal Court in Grimaldi v Chameleon Mining NL (No 2), the actual functions or responsibilities assumed by the fiduciary determine the subject matter over which his or her obligations extend, at least for the purposes of deciding whether there is a conflict of interest and duty or a conflict between duties. While the functions or responsibilities of a director are generally framed in broad terms, the precise scope of the functions or responsibilities in a particular case is a question of fact. Thus, the content of fiduciary duties are moulded to the character of the particular relationship between the director and the company.

137 In assessing the circumstances of a case, it is important to bear in mind the protective rationale for the imposition of fiduciary duties. In Chan v Zacharia, Deane J discerned two distinct themes in the “fundamental rule” that a fiduciary is not permitted to put himself or herself in a position where duty and interest conflict:

“The first [theme] is that which appropriates for the benefit of the person to whom the fiduciary duty is owed any benefit or gain obtained or received by the fiduciary in circumstances where there existed a conflict of personal interest and fiduciary duty or significant possibility of such conflict: the objective is to preclude the fiduciary from being swayed by considerations of personal interest. The second is that which requires the fiduciary to account for any benefit or gain obtained or received by reason of or by use of his fiduciary position or of opportunity or knowledge resulting from it: the objective is to preclude the fiduciary from actually misusing his position for his personal advantage.”

(Footnotes omitted.)

80 These cases all included an alleged breach by a director of their fiduciary duties. No such allegation is made in this case. QMI and Dr Gaul only contend a breach by Mr Keogh of his statutory duties. However, it is well settled that a director who promotes his or her own personal interest by making or pursuing a gain in circumstances where there is a conflict, or real or substantial possibility of conflict, between their personal interests and those of the company will breach his or her statutory duty under s 181 of the Corporations Act (and, if that conduct involves misuse of information or their position, s 182 and s 183 of the Corporations Act): Australian Securities and Investments Commission v Adler (2002) 168 FLR 253 at [735]; Parker v Tucker (2010) 77 ACSR 525; [2010] FCA 263 at [72].

81 The question of whether Mr Keogh has breached those duties by placing himself in a position of conflict as between his personal interests and those owed by him as a director to QMI, by enabling Majac to offer the Majac Products for sale, is to be determined by reference to the facts. The apparent competition between QMI and Majac, who it seems operate in the same or similar markets selling similar products, is not of itself sufficient to make the claim good. There must be something more. In particular, it is necessary to identify Mr Keogh’s functions or responsibilities as a director of QMI as they determine the subject matter over which his obligations extend, at least for the purposes of deciding whether there is a conflict of interest and duty or a conflict between duties.

82 The only evidence of Mr Keogh’s responsibilities as a director of QMI is given by Dr Gaul who says that his role was limited to sales and marketing and that he had no input into QMI’s management. How that role was undertaken vis a vis QMI is not the subject of evidence before me. However, Dr Gaul also says that the sales role was undertaken by Majac. According to Ms Carroll, Mr Keogh never received a salary or any dividends from QMI. It thus seems, on the evidence before me, that Mr Keogh’s responsibilities were limited to sales and marketing which, with Dr Gaul’s consent, he apparently undertook in a dual capacity: as a director of QMI; and as a director of Majac. Mr Keogh has now caused Majac to develop and sell the Majac Products. Arguably in doing so he has put himself in a position of conflict of duty to QMI in the sales and marketing of QMI products, albeit through Majac, and his own interests in promoting the sale of the Majac Products.

83 However, I am not satisfied that the evidence supports a seriously arguable case that Mr Keogh has breached his duties owed to QMI by diverting business opportunities from QMI to Majac. Dr Gaul says that Mr Keogh returned a large quantity of stock to Symbio Australia on 13 May 2020 without warning or explanation and points to correspondence, sent from Dr Gaul to Mr Keogh, which inquires about “a number of Pallets of Clinicol and Vibactum” received by Symbio Australia. In an earlier email, however, Dr Gaul approves the return of those products by Majac and says “[u]nsold Clinicol and Vibactum currently at MAJAC can be returned to Symbio for disposal and a credit will be issued for the returns”. Dr Gaul’s evidence deals only with the return of Clinicol and Vibactum products and makes no mention of any other QMI products. In contrast, as noted at [36] above, Ms Carroll’s evidence is that QMI ceased supply of its products to Majac contrary to a distribution arrangement as a result of an alleged debt owed by Majac to QMI.

84 QMI and Dr Gaul submitted that I should put no weight on Ms Carroll’s evidence, relying on Blatch v Archer (1774) 1 Cowp 63; 98 ER 969 and Jones v Dunkel (1959) 101 CLR 298. However, given that this is an interlocutory application I decline to adopt that approach: see s 75 Evidence Act 1995 (Cth). Ms Carroll’s evidence can be given some weight. Considered in its totality, the evidence is equivocal. On the one hand, Dr Gaul’s evidence is not sufficient to permit me to make the finding that QMI and Dr Gaul urge and, on the other, based on Ms Carroll’s evidence an available inference is that Mr Keogh developed the Majac Products because QMI stopped supply of its products to Majac. Based on the evidence it is not sufficiently clear that, at the time Majac began producing and selling the Majac Products, there still existed a relevant business opportunity of QMI to be diverted.

85 On balance, I am satisfied that there is a prima facie or sufficiently arguable case of contravention by Mr Keogh of s 181 of the Corporations Act insofar as he has enabled or caused Majac to offer the Majac Products for sale and, in doing so, placed himself in a position of conflict. I am accordingly satisfied that there is a serious question to be tried.

Balance of convenience

86 I turn then to consider where the balance of convenience lies.

87 QMI and Dr Gaul submit that they have provided clear objective evidence of Mr Keogh’s breaches of duty to QMI which are calculated to destroy QMI’s reputation in the market and to allow Majac to fill the resulting gap. They contend that Majac’s answers, that its actions were reactive to QMI’s refusal to supply it and to grant injunctive relief will cause it financial harm, in the case of the first assertion, have been shown to be false and, in the case of the second, lack objective evidentiary support. QMI and Dr Gaul submit that, on the material available to the Court, the balance of convenience clearly favours Mr Keogh and Majac being restrained from further harming QMI’s position in the market. They contend that the nature of Mr Keogh’s and Majac’s interference with QMI’s goodwill and property rights means that damages are not an adequate remedy and will be unable to compensate QMI’s loss.

88 In my opinion, having regard to the evidence before me, the balance of convenience does not favour a grant of interlocutory relief restraining Mr Keogh and Majac from offering any of the Majac Products for sale or the alternative relief sought in para 3 of the IP. That is so for the following reasons.

89 First, as identified in Samsung, the question of whether there is a serious question to be tried is not to be considered in isolation from a consideration of the balance of convenience and the apparent strength of the substantive case can be an important consideration to be weighed in the balance. The evidence based on which I have concluded that QMI and Dr Gaul have established a prima facie case of breach of s 181 is not detailed and is only just sufficient to enable me to reach the necessary state of satisfaction. That is, the strength of the case is at the lower end. Further, I have concluded at [71] and [83] above that there is insufficient evidence before me to support a sufficiently arguable case that Mr Keogh used QMI’s confidential information to produce the Majac Products or that he has diverted QMI’s business opportunities to Majac. In those circumstances it seems that, on the state of the authorities, a breach only subsists while Mr Keogh remains a director of both QMI and Majac. The consequences of a director’s resignation, where that director would otherwise have been in a position of conflict between competing interests or duties, were discussed by Jessup J in Links Golf at [581]:

… During the course of the final address of counsel for LGT, I pressed them to deal with the general question whether, aside from any issue as to the appropriation of an opportunity which arose as the result of a director’s fiduciary position, the resignation of the director from his or her fiduciary office would leave him or her free to engage in competing business activities, they being activities in which he or she had commenced to engage whilst still a fiduciary. After what was, according to counsel, a thorough examination of the authorities, counsel were unable to put it any higher than that a director who had resigned would breach his or her fiduciary obligation to his or her former company if he or she made available to his or her later company — or, presumably, used in his or her own business — any information that was confidential to the former company, or if he or she sought to exploit, either for his or her own benefit or for that of the later company, any maturing business opportunity of the former company. … That being the case, there appears to be no suggestion in the authorities that a director who has, in breach of his or her fiduciary duty, commenced to compete with his or her company, and who, upon realising the mistake, procures his or her own removal from the office of director, cannot thereafter continue his or her involvement in those very activities…

(Emphasis added.)

90 Secondly, as set out at [83] above, the evidence before me is equivocal and does not lead me to conclude that Mr Keogh’s actions are calculated to destroy QMI’s reputation in the market.

91 Thirdly, as Mr Keogh and Majac submit, there is no evidence as to why damages are an inadequate remedy, should QMI and Dr Gaul succeed at trial. To the extent they allege that there has been an interference with QMI’s goodwill and property rights, evidence could have been adduced, for example, of any reduction in sales of QMI products, reduced revenue or profits or of confusion on the part of consumers.

92 Fourthly, there is some evidence of the prejudice which Mr Keogh and Majac would suffer should the relief sought be granted such as loss of income (and its effect) and the potential for redundancies.

CONCLUSION

93 For those reasons I decline to grant the relief sought in paras 2 and 3 of the IP. As the relief sought in para 1 of the IP was dealt with by consent on another occasion, the appropriate order is to dismiss the balance of the IP.

94 That leaves the question of costs. Subject to one matter, QMI and Dr Gaul have been unsuccessful in their application. That one matter concerns the Undertaking. While that was proffered by Mr Keogh without the need for me to resolve the issue, that occurred in the course of the hearing of the IP and after QMI and Dr Gaul had made their submissions and developed their case, much of which focussed on the relief sought in para 2(a) which is the subject of the Undertaking. On one view the Undertaking represents some success for QMI and Dr Gaul on their IP.

95 In those circumstances, the appropriate order is that each party should pay their own costs of this application.

96 I will make orders accordingly.

I certify that the preceding ninety-six (96) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Markovic. |

Associate: