Federal Court of Australia

Quintis Ltd (Subject to Deed of Company Arrangement) v Certain Underwriters at Lloyd’s London Subscribing to Policy Number B0507N16FA15350 [2021] FCA 19

File number: | NSD 733 of 2020 |

Judgment of: | LEE J |

Date of judgment: | 28 January 2021 |

Catchwords: | INSURANCE – directors and officers’ liability insurance – four policies of insurance – amount of cover for “Entity Securities Liability Optional Extension” (“Side C cover”) – whether Side C cover sub-limited to primary policy – whether policies should be rectified – whether up to $50 million in Side C cover – Lloyd’s insurance market – no expert evidence – principles applicable to construction and rectification of insurance policies – policies represent bundle of contracts between insured and insurers CONTRACTS – construction of policies of insurance –interaction between primary and excess policies – distinction between construction and rectification – must not subconsciously allow evidence of parties’ actual intentions to affect questions of interpretation and construction – no ambiguity – no resort to extrinsic material EQUITY – rectification – consideration of relevant principles – standard of proof – policies represent bundle of contracts between the insured and insurer – impact of rectification on third party rights – inability to rectify primary policy to automatically affect excess policies – brokers – attribution of knowledge – common intention to be proved between broker and each insurer – volumes of contemporaneous material – common intention found between broker and some insurers – whether partial relief should be granted – equity should prevent unconscientious departure from true accord – form of rectification – focus on ascertaining the substance of intention EVIDENCE – circumstantial evidence – principles applicable to inferential reasoning – volumes of contemporaneous material – no witnesses called – adverse inferences – consideration of Blatch v Archer (1774) 1 Cowp 63 and Jones v Dunkel (1959) 101 CLR 298 REPRESENTATVE PROCEEDINGS – two class actions – settlement reached – policies of insurance only asset of value – settlement approval application – application adjourned – whether insured amount inadvertently incorrect – proceeding commenced against insurers |

Legislation: | Corporations Act 2001 (Cth) s 237 Evidence Act 1995 (Cth) ss 140, 144 Federal Court of Australia Act 1976 (Cth) s 33V |

Cases cited: | American Airlines Inc v Hope [1974] 2 Lloyd’s Rep 301 Australian Broadcasting Corporation v Chau Chak Wing [2019] FCAFC 125; (2019) 271 FCR 632 Australian Casualty Co Ltd v Federico (1985) 160 CLR 513 Australian Securities and Investments Commission v Hellicar [2012] HCA 17; (2012) 247 CLR 345 Australian Securities and Investments Commission v Rich [2009] NSWSC 1229; (2009) 236 FLR 1 Axon v Axon (1937) 59 CLR 395 Blatch v Archer (1774) 1 Cowp 63 Boyle v Wiseman (1855) 156 ER 598 Bradshaw v McEwans Pty Ltd (1951) 217 ALR 1 Briginshaw v Briginshaw (1938) 60 CLR 336 Brit UW Ltd v F & B Trenchless Solutions Ltd [2016] Lloyd’s Rep IR 68 Burke v LFOT Pty Limited [2002] HCA 17; (2002) 209 CLR 282 Chapmans Limited v Australian Stock Exchange Limited (1996) 67 FCR 402 CMG Equity Investments Pty Ltd v Australia and New Zealand Banking Group Ltd [2008] FCA 455; (2008) 65 ACSR 650 Codelfa Construction Pty Ltd v State Rail Authority of New South Wales (1982) 149 CLR 337 Commissioner of Stamp Duties (NSW) v Carlenka Pty Ltd (1995) 41 NSWLR 329 Con-Stan Industries of Australia Pty Ltd v Norwich Winterthur Insurance (Australia) Ltd (1986) 160 CLR 226 Craddock Brothers v Hunt [1923] 2 Ch 136 Crane v Hegeman-Harris Co Inc [1939] 1 All ER 662 Crane v Hegeman-Harris Co Inc [1939] 4 All ER 68 Drake Insurance Plc v McDonald [2005] EWHC 3287 (Ch) Dunlop Haywards (DHL) Ltd v Erinaceeous Insurance Services Ltd [2009] Lloyd’s Rep IR 149 Eagle Star Insurance Co Ltd v Spratt [1971] 2 Lloyd’s Rep 116 Electricity Generation Corporation v Woodside Energy Ltd [2014] HCA 14; (2014) 251 CLR 640 Equuscorp Pty Ltd v Glengallan Investments Pty Ltd [2004] HCA 55; (2004) 218 CLR 471 Fowler v Fowler (1859) 4 De G & J 250 Franklins Pty Ltd v Metcash Trading Pty Ltd [2009] NSWCA 407; (2009) 76 NSWLR 603 Galea v Bagtrans Pty Limited [2010] NSWCA 350 General Reinsurance Corporation v Forsakringsaktiebolaget Fennia Patria [1983] QB 856 Girlock (Sales) Pty Ltd v Hurrell (1982) 149 CLR 155 Halford v Price (1960) 105 CLR 23 Hall (Inspector of Taxes) v Lorimer [1992] 1 WLR 939 Harris v Smith [2008] NSWSC 545; (2008) 14 BPR 26,223 Hawksford Trustees Jersey Ltd v Stella Global UK Ltd [2012] EWCA Civ 55 Ho v Powell [2001] NSWCA 168; (2001) 51 NSWLR 572 Hung v Warner, in the matter of Bellpac Pty Ltd (Receivers and Managers Appointed) (In Liquidation) [2013] FCAFC 48 Icon Co (NSW) Pty Ltd v Liberty Mutual Insurance Company Australian Branch trading as Liberty Specialty Markets [2020] FCA 1493 Igloo Homes Pty Ltd v Sammut Constructions Pty Ltd [2005] NSWCA 280; (2005) ATC 4,986 Insurance Commissioner v Joyce (1948) 77 CLR 39 Jana Pty Ltd (atf Azizi Family Trust) v Ezistipdemo Pty Ltd [2017] NSWSC 1135 Jones v Dunkel (1959) 101 CLR 298 Joscelyne v Nissen [1970] 2 QB 86 Julian Praet et Cie S/A v HG Poland Ltd [1960] 1 Lloyds Rep 416 Kennedy v De Trafford [1897] AC 180 Kuhl v Zurich Financial Services Australia Ltd [2011] HCA 11; (2011) 243 CLR 361 Leibler v Air New Zealand Ltd (No 2) [1999] 1 VR 1 Maralinga Pty Ltd v Major Enterprises Pty Ltd (1973) 128 CLR 336 Marley v Rawlings [2015] AC 129 Marriner v Australian Super Developments Pty Ltd [2016] VSCA 141 Mayo v W & K Holdings (NSW) Pty Ltd (in liq) (No 2) [2015] NSWCA 119 McCann v Switzerland Insurance Australia Ltd [2000] HCA 65; (2000) 203 CLR 579 Morley v Australian Securities and Investments Commission [2010] NSWCA 331; (2010) 274 ALR 205 Mount Bruce Mining Pty Ltd v Wright Prospecting Pty Ltd [2015] HCA 37; (2015) 256 CLR 104 Muriti v Prendergast [2005] NSWSC 281 NIML Ltd v MAN Financial Australia Ltd [2006] VSCA 128; (2006) 15 VR 156 North & South Trust Co v Berkeley [1971] 1 All ER 980 O’Donnell v Reichard [1975] VR 916 Payne v Parker (1976) 1 NSWLR 191 Permanent Trustee Australia Ltd v FAI General Insurance Co Ltd (1998) 153 ALR 529 Perpetual Ltd v Myer Pty Ltd [2018] VSC 2 Perpetual Ltd v Myer Pty Ltd [2019] VSCA 98 Pukallus v Cameron (1982) 180 CLR 447 QBE Insurance Australia Ltd v Vasic [2010] NSWCA 166 Queenfield Pty Ltd v Gordon Finance Pty Ltd [2020] VSCA 282 Ryledar Pty Ltd v Euphoric Pty Ltd [2007] NSWCA 65; (2007) 69 NSWLR 603 Scott v Davis [2000] HCA 52; (2000) 204 CLR 333 Seymour Whyte Constructions Pty Ltd v Oswald Bros Pty Ltd (in liq) [2019] NSWCA 11; (2019) 99 NSWLR 317 Simic v New South Wales Land and Housing Corporation [2016] HCA 47; (2016) 260 CLR 85 Slee v Warke (1949) 86 CLR 271 Sprackling v Sprackling [2008] EWHC 2696 (Ch) Thomas Bates and Son Ltd v Wyndhams (Lingerie) Ltd [1981] 1 WLR 505 Touche Ross v Baker [1992] 2 Lloyd’s Law Rep 207 Transport Industries Insurance Co Ltd v Longmuir [1997] 1 VR 125 Weatherbeeta Limited v Hammersmith Nominees Pty Ltd [2019] VSC 559 WorkPac Pty Ltd v Rossato [2020] FCAFC 84; (2020) 378 ALR 585 XL Insurance Co SE v BNY Trust Company of Australia Limited [2019] NSWCA 215 |

Texts cited: | Birds J, Lynch B and Milnes S, MacGillivray on Insurance Law (Sweet & Maxwell, 14th ed, 2019) Dal Pont G E, Law of Agency (LexisNexis Butterworths, 3rd ed, 2014) Derrington D K and Ashton R S, The Law of Liability Insurance (LexisNexis Butterworths, 3rd ed, 2013) Henley C and Kemp S, The Law of Insurance Broking (Sweet & Maxwell, 3rd ed, 2016) Heydon J D, Cross on Evidence (LexisNexis Butterworths, 10th ed, 2015) Hodge D, Rectification: The Modern Law and Practice Governing Claims for Rectification for Mistake (Thomson Reuters, 2010) Lord Nicholls of Birkenhead, ‘My Kingdom for a Horse: The Meaning of Words’ (2005) 121 (Oct) Law Quarterly Review 577 |

Division: | General Division |

Registry: | New South Wales |

National Practice Area: | Commercial and Corporations |

Sub-area: | Commercial Contracts, Banking, Finance and Insurance |

404 | |

11 August 2020; 18 September 2020 | |

Counsel for the Applicants: | |

Solicitor for the Applicants: | Piper Alderman |

Counsel for the First and Third Respondent: | Mr M Jones SC with Mr E Ball |

Solicitor for the First and Third Respondent: | Wotton & Kearney |

Counsel for the Second Respondent: | Mr M R Elliott SC with Mr R J Pietriche |

Solicitor for the Second Respondent: | Colin Biggers & Paisley |

Solicitor for the Fourth Respondent: | The fourth respondents filed a submitting notice save as to costs |

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. By 3 February 2021, Quintis is file, serve and provide to the Associate to Justice Lee any written submissions limited to four pages in length on the issues of relief and costs.

2. By 10 February 2021, the Relevant Insurers are to file, serve and provide to the Associate to Justice Lee any written submissions limited to four pages in length on the issues of relief and costs.

3. By 12 February 2021, Quintis is to file, serve and provide to the Associate to Justice Lee any written submissions in reply limited to two pages in length.

4. If a party wishes to be heard orally on the issues of relief and costs, that party is to notify the Associate to Justice Lee no later than 4pm on 16 February 2021 (and if there is no such notification any outstanding issues as to relief and costs will be determined on the papers).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

[1] | |

[6] | |

[17] | |

[17] | |

[28] | |

[33] | |

[34] | |

[38] | |

[44] | |

[61] | |

[64] | |

[66] | |

[67] | |

[69] | |

[70] | |

[74] | |

[78] | |

[80] | |

[81] | |

[82] | |

[90] | |

F.3 The Evidence as a Whole and the Principles Applicable to Inferential Reasoning | [99] |

[100] | |

[104] | |

[108] | |

[109] | |

[124] | |

[131] | |

[138] | |

[208] | |

F.4.6 Subsequent events and evidence of post-contractual conduct | [220] |

[221] | |

[223] | |

F.5 The Principles Applicable to Inferential Reasoning Continued | [250] |

[251] | |

[258] | |

[262] | |

[264] | |

[270] | |

[273] | |

[282] | |

[309] | |

[310] | |

[310] | |

[320] | |

[328] | |

[337] | |

[337] | |

[349] | |

[355] | |

[356] | |

[357] | |

[366] | |

[371] | |

[384] | |

[388] | |

[391] | |

[393] |

LEE J:

1 The background to this proceeding is an unusual one. Its genesis is an application for approval of a conditional settlement of two class actions (NSD 1983 of 2017 and NSD 862 of 2018) brought on behalf of persons who acquired shares in a sandalwood plantation investment company, being the first applicant in this proceeding (Quintis). The class action applicants and group members alleged that Quintis, and others, engaged in conduct in contravention of various statutory norms causing loss and damage for which they seek compensation. For present purposes, further details of the class action claims are immaterial.

2 Quintis is subject to a deed of company arrangement, and it became evident to those acting for the applicants in the class actions that the only asset of any value held by Quintis was the proceeds of any responsive insurance policy. Following a mediation, an “in principle” settlement agreement was struck; however, prior to the hearing of the settlement approval application, it emerged that representations made during the course of the class actions by the solicitors for Quintis as to the relevant insured amount might have been inadvertently incorrect. When that became apparent to Mr Lawrance, counsel for Quintis in the class actions, he ensured that documents were disclosed, which illuminated the true position. That course, if I may say so, was in the best traditions of the Bar and prevented the settlement approval application proceeding on a false (or at least potentially false) basis.

3 In any event, following this revelation, compulsory process was issued seeking production of documents relating to the true position. Following production, this proceeding was commenced in July 2020, and leave was subsequently granted pursuant to s 237 of the Corporations Act 2001 (Cth) for relief to be sought on behalf of Quintis.

4 The assertion of the applicants in the class actions (and now Quintis) is that Quintis carried Investment Managers Insurance (IMI) policies for the period 30 September 2016 to 31 March 2018 and those policies provided up to $100 million in coverage for directors and officers’ (D&O) liability. It is contended that the common commercial intent when these policies came into existence was for Quintis to have up to $50 million in what is conventionally called “Side C” cover, by way of an “Entity Securities Liability optional extension” (so-called because the base coverage did not include such cover). That intention is now said to be reflected in the proper construction of those polices (Construction Claim), but in the event the mutual intention of the parties miscarried in the drafting of the instruments recording the paction, then it is said the policies need to be rectified to reflect the true accord (Rectification Claim). However, the position of Quintis’ underwriters is that Quintis’ Construction Claim is misconceived (and there is only $10 million in Side C cover) and the equity of rectification is unavailable. This is despite the fact that it is not in dispute, and the documentary record makes pellucid, that Quintis and its Australian broker intended to secure up to $50 million in Side C cover.

5 The following reasons are set out in the following structure:

Part B will outline the relevant actors and the policies;

Part C will deal with the procedural issues concerning Quintis’ amended originating application and the clarification of the relief sought;

Part D will outline a number of principles agreed by the parties applicable to the placement of insurance in the Lloyd’s of London (Lloyd’s) market;

Part E will address the Construction Claim;

Part F will, regrettably at some length, address the Rectification Claim, including setting out the evidentiary record and making findings in relation to any contested facts in issue; and

Part G will address the question of relief.

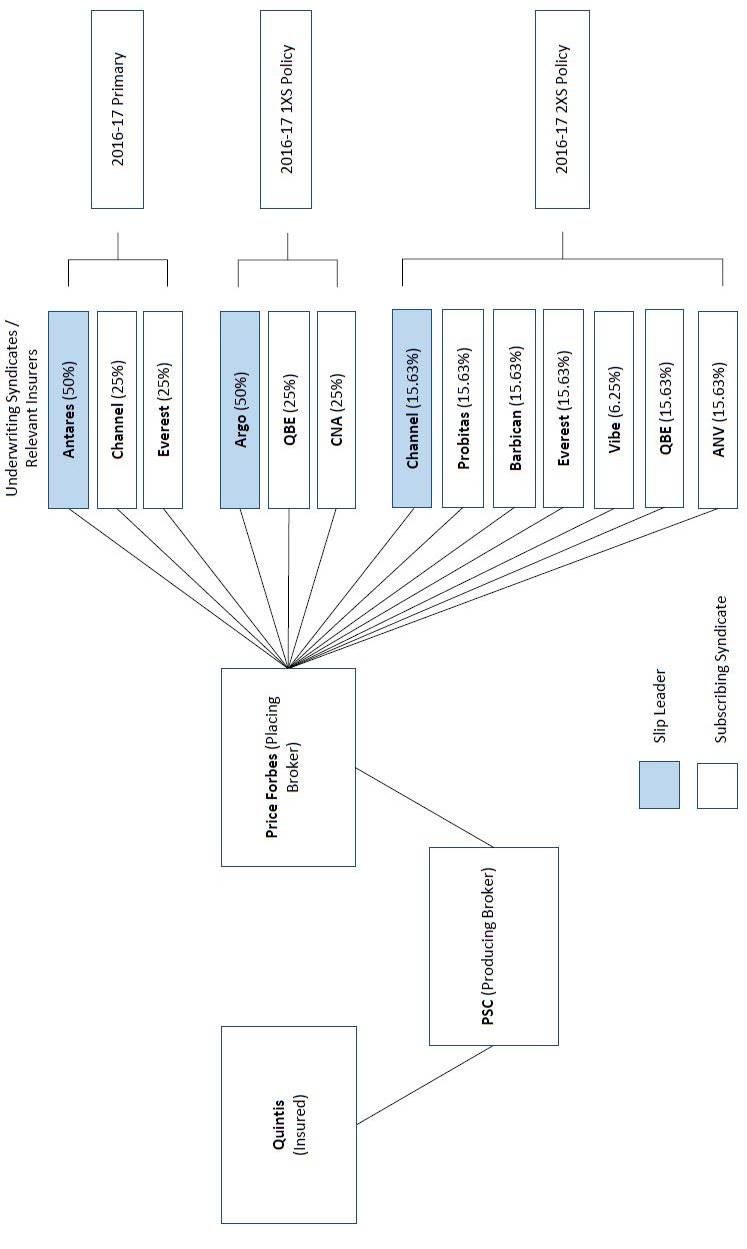

B THE RELEVANT ACTORS AND THE POLICIES

6 It is first convenient to set out the relevant actors and the policies.

7 Quintis was listed on the Australian Securities Exchange (ASX) and engaged in the business of cultivating and selling Indian sandalwood and products derived from Indian sandalwood.

8 AR (WA) Pty Ltd t/as PSC Insurance Brokers Perth (PSC) was Quintis’ Australian insurance broker. Ms Sarah Purdy was an Account Executive, and Ms Caroline Jackman was the Principal (Corporate and Agribusiness).

9 Price Forbes & Partners Ltd (Price Forbes) was a London-based insurance brokerage firm through which PSC arranged Quintis’ 2016-17 IMI in the Lloyd’s insurance market. Mr Shaun Butler was a Director and Mr Adrian Fox was Head of Financial Products.

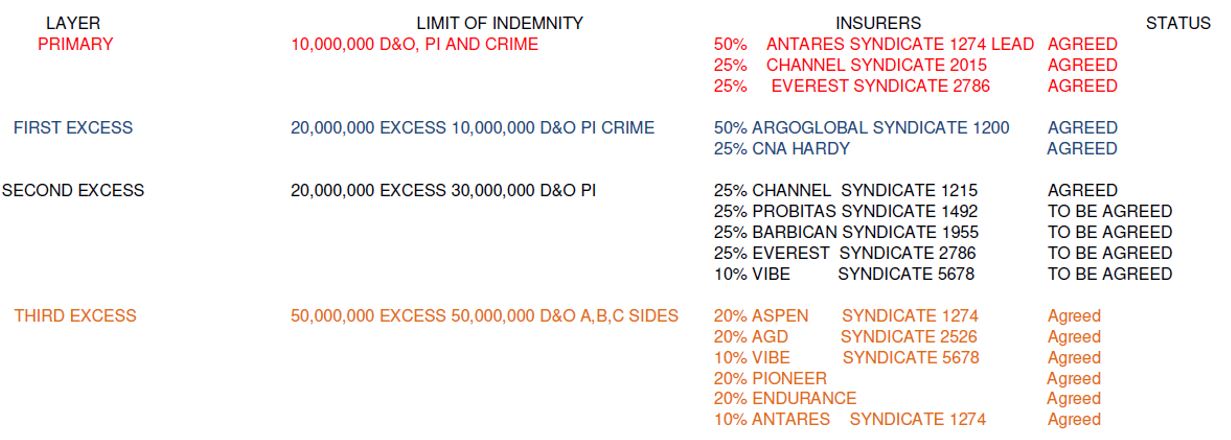

10 The present respondents comprise the various Lloyd’s underwriting syndicates subscribing to the following policies:

(1) a Policy Schedule identified as policy number B0507N16FA15350 and Munich Re Financial & Professional Risks Policy 09/14 policy wording (2016-17 Primary, the subscribing syndicates being the first respondent (Primary Insurers));

(2) a first excess layer policy identified as policy number B0507N16FA15360 (2016-17 1XS, the subscribing syndicates being the second respondent); and

(3) a second excess layer policy identified as policy number B0507N16FA15370 (2016-17 2XS, the subscribing syndicates being the third respondent).

(the policies collectively, 2016-17 Policies; the 2016-17 1XS and 2016-17 2XS collectively, Excess Policies; the respondents collectively, Relevant Insurers; the second and third respondents collectively, Excess Insurers).

11 There was also a third excess layer policy identified as policy number B0507N16FA15380 (2016-17 3XS). The underwriters of that policy have filed a submitting appearance in this proceeding; the reason being that in May 2017, those underwriters executed a retrospective endorsement excluding any liability for Side C cover (see [224]).

12 It is also convenient, for reasons that will become evident, to outline the policies comprising Quintis’ 2015-16 insurance programme as relevant to the current proceeding:

(1) a Policy Schedule identified as policy number PGLAUP1011178 and Munich Re Financial & Professional Risks Policy 09/14 policy wording (2015-16 Primary);

(2) a first excess layer policy identified as policy number FLD-368431 (2015-16 1XS);

(3) two second excess layer policies identified as policy number CFD212004A15 and policy number 50000/27/2015/0009 (2015-16 2XS);

(4) a third excess layer policy identified as policy number 05CH010390 (2015-16 3XS); and

(5) a fourth excess layer policy identified as policy number B0507N15T2300 (2015-16 4XS) (it appears that in the Court Book and some parts of the parties’ written submissions that this was referred to as a third excess layer policy – however, in oral submissions and as makes intuitive sense, this policy was referred to as a fourth excess layer policy in respect of the D&O component of the 2015-16 insurance tower).

(the policies collectively, 2015-16 Policies).

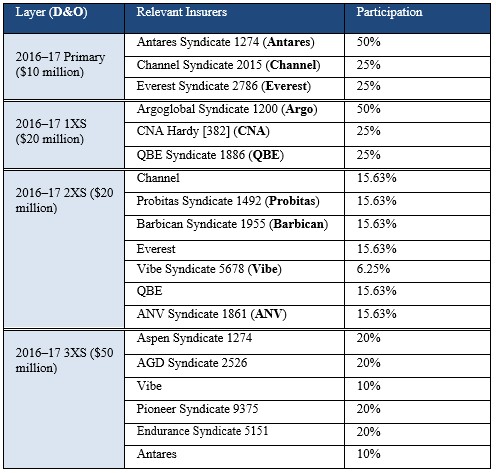

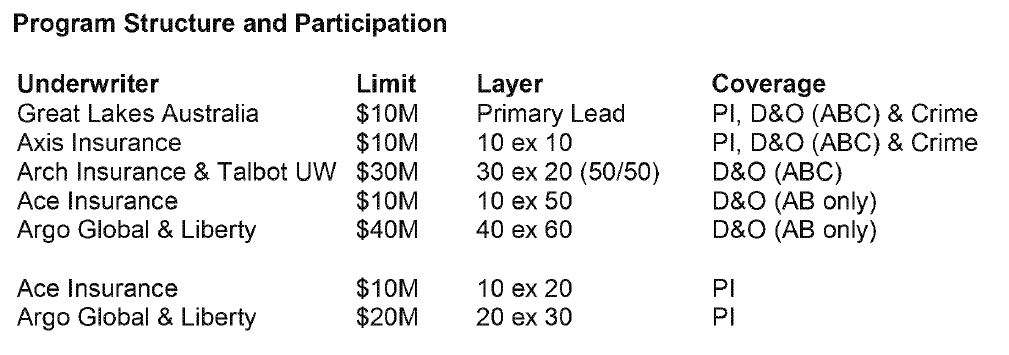

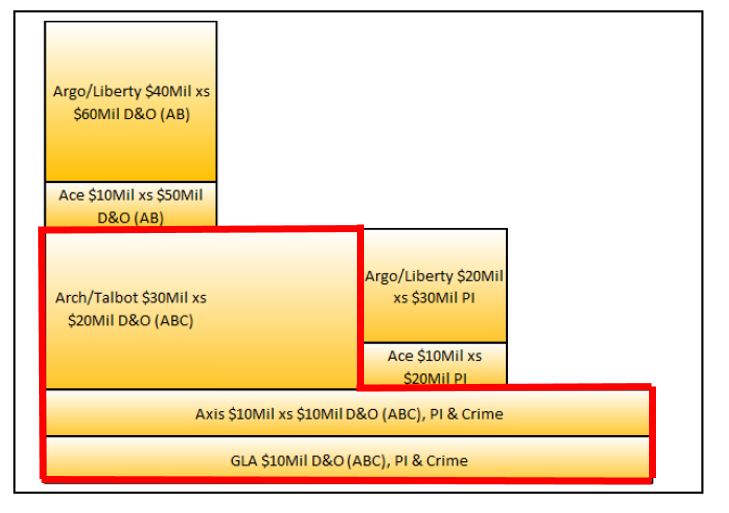

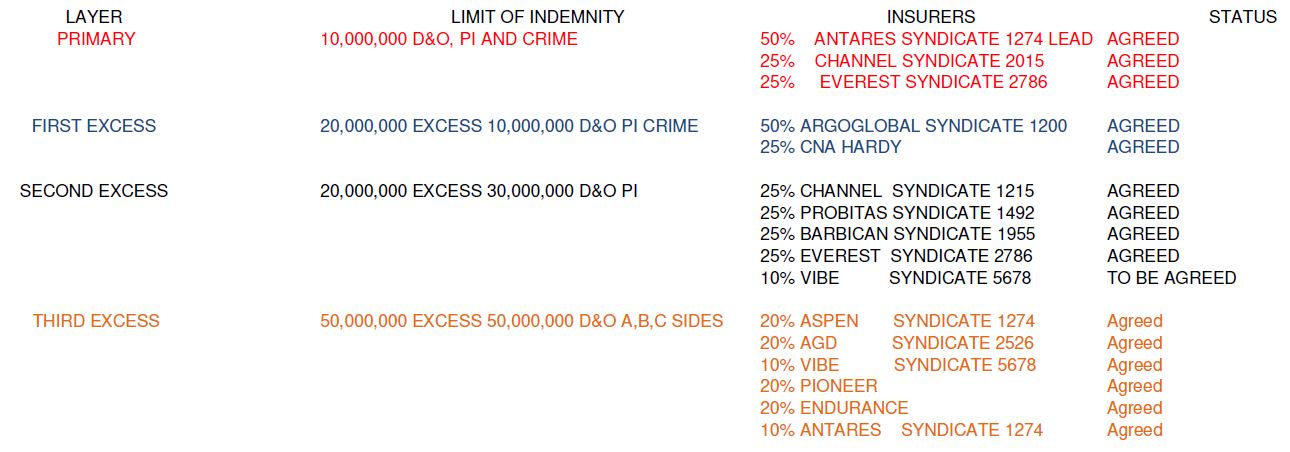

13 The syndicates comprising the Relevant Insurers to the 2016-17 Policies, and their level of participation at the D&O layer of each of the 2016-17 Policies, is summarised in the following table:

14 The participation levels for the 2016-17 2XS are not whole numbers because the policy was oversubscribed (i.e. over 100%) and the indicated participations were written down proportionately in accordance with the subscription terms.

15 The “slip leaders” for each of the policies were:

(1) Antares for the 2016-17 Primary;

(2) Argo for the 2016-17 1XS; and

(3) Channel for the 2016-17 2XS.

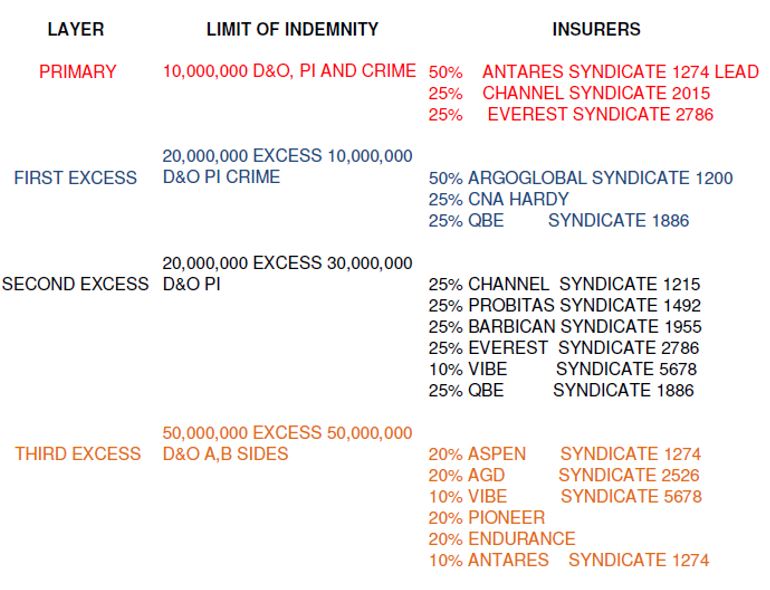

16 Diagrammatically, the relevant actors to the 2016-17 Primary, 2016-17 1XS and 2016-17 2XS can be identified as follows:

C.1 Amended Originating Application

17 On 10 August 2020, the day before the proceeding was listed for hearing, Quintis served on the Relevant Insurers a proposed amended originating application (Amended Application) to include the following (as underlined) in its claim for declarations and rectification relating to the 2016-17 Policies:

Details of claim

The Applicant claims:

1. A declaration that Quintis Ltd is entitled to rectification of policy number B0507N16FA15350 issued by the First Respondent for the period 30 September 2016 to 31 October 2017 (Policy) and, to the extent necessary, policy number B0507N16FA15360 issued by the Second Respondent (1st Excess) and policy number B0507N16FA15370 (2nd Excess) issued by the Third Respondent to the extent they incorporate the terms of the Policy, such that:

a. the words “4.9 Entity Securities Liability $10,000,000” are deleted, and in lieu thereof the words “4.9 Entity Securities Liability Included” or “4.9 Entity Securities Liability $50,000,000” are inserted at page 2 of the Policy Schedule; and

b. the words “4.9 Entity Securities Liability AUD $10,000,000” are deleted, and in lieu thereof the words “4.9 Entity Securities Liability Included” or “4.9 Entity Securities Liability AUD $50,000,000” are inserted at page 2 of the Market Reform Contract annexed to the Policy.

2. An order that the Policy and, to the extent necessary, the 1st Excess and 2nd Excess to the extent they incorporate the terms of the Policy, be rectified such that:

a. the words “4.9 Entity Securities Liability $10,000,000” are deleted, and in lieu thereof the words “4.9 Entity Securities Liability Included” or “4.9 Entity Securities Liability $50,000,000” are inserted at page 2 of the Policy Schedule; and

b. the words “4.9 Entity Securities Liability AUD $10,000,000” are deleted, and in lieu thereof the words “4.9 Entity Securities Liability Included” or “4.9 Entity Securities Liability AUD $50,000,000” are inserted at page 2 of the Market Reform Contract annexed to the Policy.

3. An order that a copy of Order 2 be endorsed on the Policy (including any copy of the Policy attached to the 1st Excess or 2nd Excess if such documents exist) and, to the extent necessary, the 1st Excess and 2nd Excess.

18 The reason for the proposed amendment arose out of arguments identified by the Relevant Insurers in their submissions served a few days earlier, being: (1) the assertion that rectification of the 2016-17 Primary has no effect on the “follow” Excess Polices; and (2) that the Excess Insurers sought to position themselves as strangers to the relief sought, such that they would be prejudiced by any extension of its consequences to them.

19 Leave to file the Amended Application was opposed by the Excess Insurers on the basis that the Excess Insurers had prepared their defence on the basis that their subjective intent was not in issue, they had not interviewed relevant witnesses, and the proposed amendment would therefore cause them prejudice.

20 The Excess Insures asserted that rectification of the Excess Policies was not sought on the basis of a “deliberate forensic choice” and pointed to the remarks of Mr Edwards, counsel for Quintis, in response to the following query I raised at a case management hearing on 13 July 2020 (at T5.5–12):

HIS HONOUR: … So rectification is only sought in respect of the policy issued by the first respondent …

MR EDWARDS: Yes. I mean, there’s a real question about whether all these other second layers and whatnot actually need to have active part because their policies follow form against that one. I mean, I understand they have an interest because they will get exposed quicker or slower, depending upon the answer. But, really, it’s not a case where we have to make out 30 rectification slips.

21 However, on the application to amend, an affidavit sworn by the solicitor on record for Quintis, Mr del Gallego, was read. He gave the following unchallenged evidence:

… During the course of the 13 July CMH, Mr Pietriche submitted in relation to the nature of the case, “we would expect that the applicants would need to demonstrate the case of rectification by having regard to documents visa-vis each of the syndicates involved. And where there at [sic] least 10 syndicates involved in the underwriting of this particular policy and where there are three separate parties, effectively, on the respondents side, we would expect that, in order for the applicants to make out their case as well as for each of the respondents to properly respond, that is a process that will necessarily take some time.” (T4:29-36)

I understood Mr Pietriche to be submitting that the Second Respondent’s position was that its characterisation of the forensic contest was that there was a factual dispute in contest as to the subjective intention of all the insurers. Mr Ball did not make any substantive submissions during the 13 July CMH, and I took from his silence and Mr Pietriche’s reference to that being a difficult exercise where [sic] “where there at least 10 syndicates involved in the underwriting of this particular policy” (T4:31) that this was the common position of the Respondents.

(Emphasis added, underline in original).

22 It was uncontroversial that at all times the case advanced by Quintis was that it had up to $50 million in Side C cover. Quintis did not initially consider that this would involve rectification of the Excess Policies as well as the 2016-17 Primary. However, given the unchallenged evidence of the solicitor with carriage of Quintis’ case, supported by the remarks of Mr Edwards both written and orally, I rejected the notion that some form of “deliberate forensic choice” was made. The reality is that despite the point taken by the Excess Insurers, at all times prior to the exchange of submissions in advance of the hearing, there was simply an asymmetry in the views taken by those advising the parties as to what was necessary in order to obtain utile relief. Given the requirement for the Court to facilitate the just resolution of disputes, I granted leave for Quintis to file and rely on the Amended Application.

23 This leave was granted notwithstanding I accept this course occasioned some prejudice to the Excess Insurers. To alleviate any prejudice, it seemed to me the appropriate course was for the hearing to be adjourned, for Quintis to file points of claim and thereafter there be a joinder of issue, particularly in relation to any equitable defences that may be called in aid by the Excess Insurers. Importantly, I also proposed a timetable for the filing of additional affidavit material and submissions, with the hearing to be reconvened on a date to be fixed.

24 Counsel for Quintis conceded that this course was, given the circumstances, the most suitable even though the vacation of the hearing would likely have adverse costs consequences. Notwithstanding this, the Relevant Insurers opposed any adjournment. The alternative proposed by Mr Jones SC, counsel for the first and third respondents, was that given there had been no opportunity to call witnesses and that the third respondent was prepared to run a defence on the documentary material filed to date, I should proceed to hear the case, with the express caveat that I would not make any adverse inferences against the Excess Insurers for their inability to call any witnesses. The second respondent endorsed this course. Indeed, counsel for both the second and third respondents, after I sought assurances, stated that they were in a position to meet the case advanced against them, that they wished to adduce no further evidence, that there were no additional documents to be discovered and despite the amendment, they were happy to proceed.

25 In those circumstances, and given that Quintis had only been given leave to file the Amended Application at the hearing, on balance it seemed to me consistent with the overarching purpose, and in particular with the need to facilitate the resolution of this dispute as quickly and inexpensively as possible, that the hearing proceed. No doubt if the evidence had concluded within the time initially allocated for the hearing, any inference that would otherwise have been available to be drawn by reason of the Excess Insurers not calling witnesses, would have been met with the response that there was a reasonable excuse not to call witnesses who, up until the time of the amendment, had not been considered material.

26 In any event, any discussion concerning prejudice or making limited enquires because of an alleged lack of understanding as to how Quintis was to run its case, ended up disappearing. That is because, when it became clear that the proceeding would run over the one day which had been allocated, I made orders to the effect that, inter alia, the Relevant Insurers file and serve any affidavit evidence upon which they proposed to rely in relation to the relief sought in the Amended Application (on the basis that given leave to amend was allowed, they were automatically entitled to reopen their evidence at the hearing, and read any further affidavit material they wished to read).

27 As it happened, the hearing was adjourned part heard to 18 September 2020. Although I deal below comprehensively with the evidential position, I should note here that apart from an affidavit relating to the verification of the list of documents produced by the first and third respondents, no additional affidavit material was relied upon, nor were any witnesses called. Given this, and the importance of inferences in this case to determining issues of intention, one might think it is unsurprising the Relevant Insurers did what they could to have the matter heard and resolved on the basis that no adverse inferences arising from the absence of witnesses could be drawn.

D Placing Insurance at Lloyd’s

28 With an understanding of the relevant actors, polices and the relief sought in mind, it is now appropriate to turn to the substance of Quintis’ claims. Before doing so, it is useful to canvass some largely uncontroversial aspects regarding the way in which Lloyd’s operates and how the current facts fit within that contemporary market practice. That is because such an understanding of the commercial context informs how a number of relevant issues should be approached.

29 No expert evidence was adduced in relation to the operation of the Lloyd’s market. Nor are such matters, to the extent they are factual, common knowledge allowing s 144 of the Evidence Act 1995 (Cth) (EA) to be engaged. As a consequence, and because it seemed to me the commercial context was of importance, prior to the second day of the hearing, my Associate sent the parties a document which (based on the submissions of the Relevant Insurers and my understanding of relevant cases), outlined the following principles applicable to placing insurance at Lloyd’s and how they apply in the present circumstances. The parties accepted the accuracy of this document. Although the initial list of principles sent to the parties included some additional matters, the following are those points which ended up being pertinent to the current proceeding:

(1) insurance placed with Lloyd’s must be undertaken through the agency of a broker who is registered to place business in the Lloyd’s market: see Julian Praet et Cie S/A v HG Poland Ltd [1960] 1 Lloyds Rep 416 (at 416–7 per Morris LJ); North & South Trust Co v Berkeley [1971] 1 All ER 980 (at 982 per Donaldson J); Brit UW Ltd v F & B Trenchless Solutions Ltd [2016] Lloyd’s Rep IR 68 (at [165] per Carr J); Birds J, Lynch B and Milnes S, MacGillivray on Insurance Law (Sweet & Maxwell, 14th ed, 2019) (at [37-008]–[37-009]); Henley C and Kemp S, The Law of Insurance Broking (Sweet & Maxwell, 3rd ed, 2016) (at [12-003]–[12-004]) (Henley and Kemp);

(2) there were two brokers intervening between the insured (Quintis) and the underwriters (the Relevant Insurers), being the “producing broker”, PSC (in direct contact with Quintis) and the “placing broker”, Price Forbes (in direct contact with the Relevant Insurers), who is the designated “Lloyd’s broker”;

(3) PSC and Price Forbes are both agents of the insured, however, it was Price Forbes as the placing broker who was the contracting agent (to use that term at a high level of generality) of Quintis at Lloyd’s: American Airlines Inc v Hope [1974] 2 Lloyd’s Rep 301 (at 304 per Lord Diplock, with whom Lord Wilberforce, Viscount Dilhorne, Lord Simon of Glaisdale and Lord Kilbrandon agreed);

(4) it is common that a placing broker will seek out a market “leader’” to endorse the “slip” as part of marketing efforts to attract other potential insurers and that although the traditional “slip” (as distinct from the separate policy document) is now a thing of the past (having been replaced by the Market Reform Contract (MRC)), the term “slip” is still widely used in the market to refer to an MRC (for example, a “quote slip”, as used in the present circumstances, commonly refers to a draft MRC used to negotiate the contract with underwriters (terms that I will use interchangeably in these reasons)): Henley & Kemp (at [12–008]) (I should note that this point was not expressly conceded by Quintis, but is clearly consistent with the entire documentary record);

(5) the slip method of placing insurance, by signing the MRC and stating the proportion of the risk that the underwriter is prepared to subscribe results in the conclusion of separate contracts between the insured and each subscriber of the slip: see General Reinsurance Corporation v Forsakringsaktiebolaget Fennia Patria [1983] QB 856 (at 864 per Kerr LJ, with whom Slade and Oliver LLJ agreed); Eagle Star Insurance Co Ltd v Spratt [1971] 2 Lloyd’s Rep 116 (at 124 per Lord Denning MR);

(6) the severability of each contract of insurance between the insured on the one hand and the individual subscribing underwriters is consistent with the autonomy of each underwriter: see Touche Ross v Baker [1992] 2 Lloyd’s Law Rep 207 (at 210 per Lord Mustill, with whom Lords Templeman, Jauncey of Tullichettle, Brown-Wilkinson and Slynn of Haldey agreed); and

(7) hence, while there may only be one primary policy and three excess polices, there are in fact nineteen separate contracts reflected by the 2016-17 Policies (although the 2016-17 3XS is not relevant to the Rectification Claim, and some underwriters subscribed at multiple levels of the tower).

30 It is worth noting that by the end of the case it was common ground that the 2016-17 Policies reflected a bundle of contracts and importantly, in response to a question posed by me, the parties accepted, as a matter of principle, that if common intention was proved in relation to only some underwriters, some relief may be available in relation to the separate contracts with the Relevant Insurers found to have held the relevant common intention.

31 It is convenient here to deal with the further issue as to when the contracts between Quintis and the Relevant Insurers were formed. It is apparent that a Firm Order Noted (FON) was sought and provided by email from all Relevant Insurers and an MRC in full form was also subsequently signed by each Relevant Insurer in days following. The first and third respondents stated in their written submissions that:

The reason as to why [Price Forbes] took the course of seeking an email ‘FON’ as well as obtaining signature on the complete MRC is a matter of speculation. It ultimately does not matter much what the reason was. Both the ‘FON’ confirmation and the signing of the complete MRC occurred relatively contemporaneously.

32 Quintis advanced its submissions on the basis that there was a continuum of intention culminating in the accord being reached at the time of the FON. This was presumably because, as will be discussed below, the excess policy terms were only attached to the complete MRC when it was signed. The second respondent submitted that it was preferable to treat the signing of the complete MRC as the time of formation, given that this is the instrument sought to be rectified. While the reasoning in Dunlop Haywards (DHL) Ltd v Erinaceeous Insurance Services Ltd [2009] Lloyd’s Rep IR 149 recognises that formation can occur at the time of the FON or the signing of a complete MRC, I do not think that an examination of the exact moment of formation is fruitful. That is because these actions occurred relatively contemporaneously and, while I accept that there is not in evidence any correspondence of the excess policy terms prior to the signing of the complete MRC, for reasons that will become evident, I do not think this materially alters any findings I am going to make. In any event, no party made any detailed submissions on the issue of formation to persuade me to conclude either way.

33 Contrary to the way in which Quintis framed its case, it is appropriate to the deal with the Construction Claim before the Rectification Claim. This is because the equity would be unnecessary if the legal position was determined in favour of Quintis. It might be thought telling as to the merits of Quintis’ Construction Claim that it was only addressed briefly at the end of their submissions and as an alternative to the Rectification Claim.

34 I recently set out the principles relating to the construction and rectification of insurance contracts in Icon Co (NSW) Pty Ltd v Liberty Mutual Insurance Company Australian Branch trading as Liberty Specialty Markets [2020] FCA 1493. I do not propose to repeat those principles at length here. It is only necessary to emphasise three important propositions.

35 First, it is trite that the process of construing insurance contracts is governed by ordinary principles of contractual interpretation: Australian Casualty Co Ltd v Federico (1985) 160 CLR 513 (at 520 per Gibbs CJ); McCann v Switzerland Insurance Australia Ltd [2000] HCA 65; (2000) 203 CLR 579 (at 589 [22] per Gleeson CJ). A clause in an insurance policy must be considered in the context of the policy as a whole, and the policy must be set in its surrounding circumstances or factual matrix, including, if excess policies are involved, the broad scheme of insurance cover intended to provide layers of insurance against the same risk: Derrington D K and Ashton R S, The Law of Liability Insurance (LexisNexis Butterworths, 3rd ed, 2013) (at 422 [3–64]); see also Mount Bruce Mining Pty Ltd v Wright Prospecting Pty Ltd [2015] HCA 37; (2015) 256 CLR 104 (at 116 [46] per French CJ, Nettle and Gordon JJ). This principle is not limited to instruments between the same parties: see McVeigh v National Australia Bank Ltd [2000] FCA 187; (2000) 278 ALR 429 (at 438–40 [30]–[34] per Finkelstein J, and at 447–51 [67]–[77] per Kenny J).

36 Secondly, as Mason ACJ, Murphy and Deane JJ notably remarked in Taylor v Johnson (1983) 151 CLR 422 (at 429) the objective theory of contract is “in command of the field”. As one would expect, the bulk of the evidence adduced by Quintis was directed to the subjective intention of the parties, and although this is central to the Rectification Claim, it must be put out of mind when having regard to the Construction Claim: see Simic v New South Wales Land and Housing Corporation [2016] HCA 47; (2016) 260 CLR 85 (at 95 [18] per French CJ); Ryledar Pty Ltd v Euphoric Pty Ltd [2007] NSWCA 65; (2007) 69 NSWLR 603 (at 655 [261] per Campbell JA, with whom Tobias JA relevantly agreed).

37 Thirdly, surrounding circumstances known to the parties is one of the elements required to be considered in the construction exercise. However, resort to evidence of those circumstances is confined. The classic authority for that proposition is the “true rule” as stated by Mason J (Stephen and Wilson JJ concurring) in Codelfa Construction Pty Ltd v State Rail Authority of New South Wales (1982) 149 CLR 337, which does not require further elaboration. Despite debate in the authorities, for the reasons I recently set out in Icon (at [55]–[60]), I adhere to the view that the “true rule” remains as Mason J stated it in Codelfa. I therefore proceed on the basis that it is only permissible for me to have regard to extrinsic material going to surrounding circumstances if, as Quintis contends, there exists ambiguity in the 2016-17 Policies.

38 Quintis’ Construction Claim can be summarised by reference to the following two contentions: (a) on its proper construction, the 2016-17 Primary does not impose a “sub-limit” on Entity Securities Liability, but the reference to “4.9 Entity Securities Liability AUD $10,000,000” is a reference to the corresponding Limit of Liability for Section 1B coverage taken on by the Primary Insurers (Construction Contention); and (b) alternatively, the 2016-17 Primary is ambiguous and ought be resolved against the Relevant Insurers in accordance with the contra proferentem rule (Ambiguity Contention). I deal with each of these contentions in turn below.

39 It is noteworthy that Quintis’ submissions on the Construction Claim were prefaced by the proposition that “all relevant participants in Quintis’ 2015-16 insurance program were of the view that Quintis was insured for $50m of Entity Securities Liability”. To paraphrase the words of Lord Nicholls of Birkenhead, and with no intended disrespect, I must be alive to the ploy of counsel placing evidence of the parties actual intentions before the Court on a rectification claim in the hope of consciously or subconsciously affecting the Court’s thinking on questions of interpretation and construction: see Lord Nicholls of Birkenhead, ‘My Kingdom for a Horse: The Meaning of Words’ (2005) 121 (Oct) Law Quarterly Review 577 (at 578).

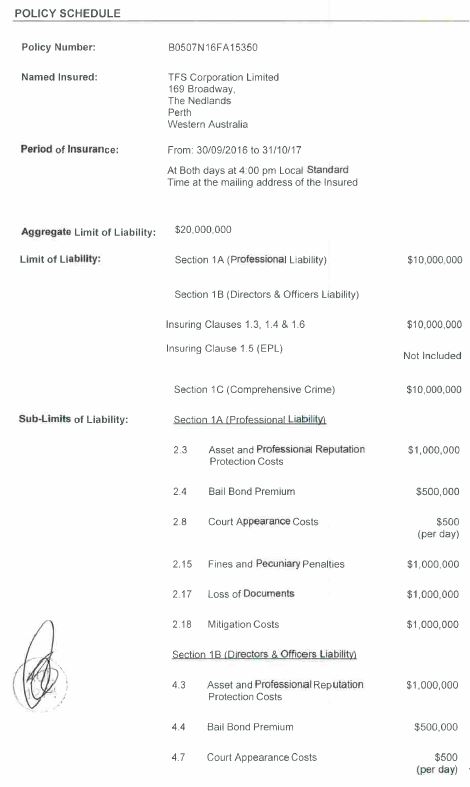

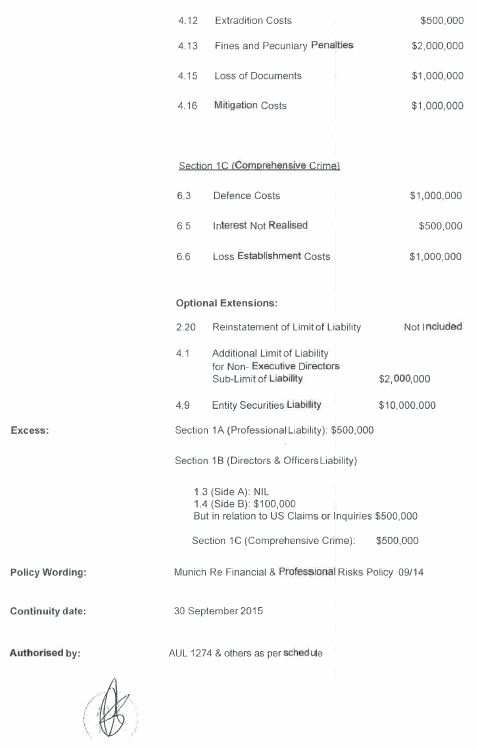

40 It is next convenient to set out the relevant terms of 2016-17 Primary Schedule:

41 It is also convenient to set out the provisions of the 2016-17 Primary relevant to the Construction Claim, which are as follows:

4 SECTION 4: EXTENSIONS TO SECTION 1B (DIRECTORS & OFFICERS LIABILITY)

Subject to all the terms, conditions and exclusions, including all definitions of the Policy, the Insurer further agrees to extend cover provided under Section 1B of the Policy as follows:

4.1 Additional Limit of Liability for Insured Persons

Notwithstanding subclauses 8.14(a) and (b) of this Policy, the Insurer will pay for any Insured Person under Insuring Clause 1.3, the Sub-Limit of Liability stated in the Schedule, in addition to the Limit of Liability applicable to Section 1B (Directors & Officers Liability), provided that each of:

(a) the Limit of Liability applicable to Section 1B (Directors & Officers Liability);

(b) any other directors and officers liability policy which covers the Insured Person; and

(c) all other indemnification available to the Insured Person

has been exhausted.

This extension is not automatic and will only apply if it is specifically included in the Schedule.

This extension does not provide any cover to the Insured Organisation.

…

4.9 Entity Securities Liability

The Insurer will pay on behalf of the Insured Organisation the liability and associated Defence Costs which the Insured Organisation is legally liable to pay as a result of a Securities Claim alleging a Wrongful Act first made the Insured Organisation, and notified to the Insurer, during the Period of Insurance.

This extension is not automatic and will only apply if it is specifically included in the Schedule.

The maximum amount payable by the Insurer under this extension is the applicable Sub-Limit of Liability specified in the Schedule. This sub-limit is part of and not in addition to the Limit of Liability.

…

8 SECTION 8: CONDITIONS APPLICABLE TO ALL COVER SECTIONS

…

8.14 Limit of Liability

(a) The maximum amount payable by the Insurer under each of Sections 1A, 1B and 1C of the Policy (and their associated Extensions) is the applicable Limit of Liability.

(b) The Limit of Liability is inclusive of any Defence Costs, Sub-Limits of Liability and any other amounts insured under each part of the Policy but does not include costs incurred by the Insurer in determining whether the relevant part of the Policy provides insurance to the Insured.

(c) Aggregate Limit of Liability

The total aggregate limit of the Insurers’ liability under all of Sections 1A, 1B and 1C of the Policy (and their associated extensions) is the Aggregate Limit of Liability. The Aggregate Limit of Liability is inclusive of any Defence Costs, Sub-Limits of Liability and any other amounts insured under the Policy.

(d) If any amounts insured under the Policy are covered under one or more parts of the Policy, then the maximum amount payable by the Insurer will be the highest of the applicable Limits of Liability or Sub-Limits of Liability and the Excess will be the applicable Excess for the Insuring Clause or Extension to which that Limit of Liability or Sub-Limit of Liability applies.

(Emphasis in original to signify defined terms).

42 The “Limit of Liability” is defined in the Definitions section of the 2016-17 Primary as:

Limit of Liability means the limit of liability stated in the Schedule and referred to in clause 8.14 of the Policy.

(Emphasis in original to signify defined terms).

43 Lastly, I should set out the following provisions contained in the Excess Policies (which for all relevant purposes are identical):

EXCESS LIABILITY INSURANCE

In consideration of the payment of premium and subject to the terms of this Policy, Insurers agree with the Insured that:

Section 1 - Insuring Section

1. Insurers shall provide the Insured with insurance coverage for claims first made against the Insured during the Policy Period in excess of the Primary Insurance and in excess of any Underlying Insurance. Insurance coverage hereunder will apply in conformance with the terms, conditions, endorsements, limitations and warranties of the Primary Insurance and any Underlying Insurance except as otherwise stated in this Policy.

…

Section 4 - Depletion of Primary Insurance and Underlying Insurance

…

4.4 In the event that the Primary Insurance or any Underlying Insurance specifically provides for a sub-limit of liability it is agreed that:

(a) where such sub-limit of liability is totally exhausted solely as a result of payment of losses under the Primary Insurance or any Underlying Insurance, then this Policy shall not provide any coverage in respect of such sub-limit of liability; or

(b) where such sub-limit of liability is partially exhausted solely as a result of payment of losses under the Primary Insurance or any Underlying Insurance, then this Policy shall continue for subsequent losses that would be subject to such sub-limit of liability provided that the amount payable hereunder shall not exceed the balance of the amount remaining under such sub-limit of liability and shall otherwise be part of and not in addition to the Limit of Liability.

(Emphasis in original to signify defined terms).

44 Quintis located its Construction Contention in the factual matrix culminating in the execution of the 2015-16 Policies. It was said this was a matter of significance to Quintis not only because of the level of cover available to it, but because it was an aspect of a comprehensive insurance review conducted by PSC in April 2015 in response to the “extremely low levels” of D&O insurance held by Quintis at that time. Indeed, Quintis asserted that it is clear that the 2016-17 Policies “just adopted the policy wording of the 2015-16 Policies without much particular thought”. For the reasons outlined above, this evidence of surrounding circumstances would only become relevant to the construction exercise if I were to find ambiguity in the 2016-17 Primary. Furthermore, before canvassing Quintis’ Construction Contention, it is necessary to address its submissions as to the purported formatting errors in the 2016-17 Primary, namely: (a) that the last paragraph under cl 4.9 is in fact a continuation of cl 4.9; and (b) that the sub-heading “Optional Extensions” should not be indented under the sub-heading “Sub-Limits of Liability”, but should sit as its own, separate sub-heading. I accept the former is a formatting error, but the same is not true of the latter.

45 As noted above, the core of Quintis’ construction contention was that, on its proper construction, the reference to “4.9 Entity Securities Liability AUD $10,000,000” is simply a reference to the corresponding Limit of Lability for Section 1B coverage taken on by the Primary Insurers. The argument proceeded along the following lines.

46 The significance of the distinction between the sub-headings “Sub-Limits of Liability” and “Optional Extensions” is that each of the clauses under “Sub-Limits of Liability” is automatic, in that they do not have to be specified as being included or not included. By contrast, each of the clauses under the heading “Optional Extensions” (cll 2.20 (which it was agreed should read cl 2.19), 4.1 and 4.9) are expressed to “only apply if ... specifically included in the Schedule”. One of those extensions – cl 2.19 – is not susceptible to a sub-limit at all. Hence, while cll 4.1 and 4.9 permit the identification of a sub-limit, a sub-limit is not required, as these are extensions to heads of primary cover under Section 1B, which, in any event, is subject to a Limit of Liability. This also formed the foundation for Quintis’ contention that those items contained under the heading “Optional Extensions” are not solely concerned with “Sub-Limits of Liability”, but rather noted the existence of any relevant Optional Extension.

47 Moreover, Quintis distinguished cl 4.1 from cl 4.9. In cl 4.1 there is a reference to “the sublimit of liability”, whereas in cl 4.9 reference is made to “the applicable sublimit of liability”. Quintis asserted that the term applicable is capable of being read as “if any”, reinforcing that cl 4.9 does not mandate that a sublimit must be specified, but that a sublimit may be specified, and if so specified, then that sublimit would be described as the “applicable” sublimit. Quintis argued that this is supported by the fact that the figure of $2 million attached to cl 4.1 includes, by express language, a “Sub-Limit of Liability” and the figure of $10 million attached to cl 4.9 does not. Hence viewing the Schedule as a whole, “[o]ne would think that if [cl 4.9] was intended to be sub-limited, it would say so expressly as is the case with the cl 4.1 extension”.

48 It was upon this foundation that Quintis argued the “unadorned figure” of $10 million attached to the term “Entity Securities Liability” could be regarded as doing no more than simply restating the Limit of Liability for Section 1B cover under the 2016-17 Primary, or at the least, there exists ambiguity in the 2016-17 Primary. Indeed, it was said looked at purely from the perspective of the Primary Insurer, it would be curious if the 2016-17 Primary expressed a “sub-limit” equal to its Limit of Liability for the very same Section of cover. That is, it would not be expected that the amount of $10 million would be specified in the 2016-17 Primary as a “sub-limit” of any Limit of Liability of the same amount. Quintis argued that this construction is supported by the commercial difficulty created by the alternative finding that a sub-limit must be specified. Quintis submitted that if it is true that: (a) cl 4.9 requires there to be a sub-limit applied to Entity Securities Liability; and (b) the effect of cl 8.14 is that the sub-limit must be an amount equal to or less than the Limit of Liability for Section 1B cover under the 2016-17 Primary, reading the 2016-17 Primary together with the Excess Policies would mean that no insurance arrangement involving the further term cl 4.4 could ever provide cover greater than $10 million in respect of Entity Securities Liability. Quintis asserted this was an “implausible construction … that would place considerable limits on the commercial freedom of the parties to make arrangements as to cover under what appear to be standard form terms”.

49 Despite Quintis saying everything it could, its Construction Contention cannot be sustained when the terms of the 2016-17 Primary and Excess Policies are properly considered.

50 Section 4 of the 2016-17 Primary (of which cl 4.9 forms part) recognises, by virtue of its chapeau, that the extensions set out in that section are “provided under Section 1B of the Policy”. Further, cl 4.9, after describing the nature of the cover available under the Entity Securities Liability Optional Extension, provides that “[t]he maximum amount payable by the Insurer under this extension is the applicable Sub-Limit of Liability specified in the Schedule” and “[t]his sub-limit is part of and not in addition to the Limit of Liability”. Hence, the nomination of a figure alongside “Entity Securities Liability” is a nomination for the purposes of being a sub-limited term, which is to be part of and not in addition to the Limit of Liability.

51 This is supported by the fact that the “Limit of Liability” is defined as the “limit stated in the Schedule and referred to in clause 8.14 of the policy”. The 2016-17 Primary Schedule provides that the Limit of Liability for Section 1B cover is $10 million in the aggregate and cl 8.14 states that “[t]he Limit of Liability is inclusive of any Defence Costs, Sub-Limits of Liability and any other amounts insured under each part of the Policy”. Hence, cl 8.14 underscores what cl 4.9 already makes plain, namely that the Entity Securities Liability sub-limit is part of and not in addition to the $10 million Limit of Liability for Section 1B cover. This conclusion is sound regardless of whether I found that the heading “Optional Extensions” is erroneously indented under the heading “Sub-Limits of Liability”.

52 Nor does an examination of the Excess Policies assist Quintis. It is a commonly accepted principle of contractual construction that a clause such as cl 1 of the Excess Policies has the effect of incorporating the relevant terms from the one contract into another, except as stated otherwise: Permanent Trustee Australia Ltd v FAI General Insurance Co Ltd (1998) 153 ALR 529 (at 560 per Hodgson CJ in Eq). Where this occurs, the incorporated terms become terms of the subject contract itself; the fact that those terms are not restated or reproduced in full in the contract is of no moment: see, eg, Weatherbeeta Limited v Hammersmith Nominees Pty Ltd [2019] VSC 559 (at [133] per Connock J); WorkPac Pty Ltd v Rossato [2020] FCAFC 84; (2020) 378 ALR 585 (at [363]–[364] per White J). It is noteworthy that while the term “Primary Insurance” is defined in cl 2.5 of the Excess Policies as the “policy identified as such in Item 4 of the Schedule”, there is in fact no Schedule attached to the Excess Policies. Instead, there is a document titled “Risk Details” as the first page of the MRC, which includes the condition “Full Follow Form As attached Primary Policy Number B0507N16FA15350”. It is clear (as Quintis accepted and as would make sense (D1, T49.37–44)), that the reference to “Primary Insurance” in cl 1 is a reference to the “Primary Policy Number” referred to in this condition, which is the 2016-17 Primary.

53 Thus, by virtue of cl 1, one of the terms incorporated into the Excess Policies from the 2016-17 Primary was cover in respect of Entity Securities Liability with a sub-limit of $10 million. Importantly, cl 4.4 further clarifies that incorporation, by limiting the cover extended by that term only to the uneroded portion of the $10 million Entity Securities Liability sub-limit and only on the basis that the sub-limit is part of and not in addition to the Limit of Liability of the Excess Policies. Hence, if it is the case that the sub-limit is not exhausted under the 2016-17 Primary because of, for instance, payment of defence costs or claims under cl 1.3, cover continues under the 2016-17 1XS, but only to that limited extent. Furthermore, while it is not entirely relevant to the Construction Claim, it is also clear that the reference to “Limit of Liability” in the Excess Policies, which is defined in cl 2.3 as the “amount stated in item 3 of the Schedule”, is the Limit of Liability stated on the first page of the MRC.

54 These reasons are sufficient to dispose of Quintis’ Construction Claim. However, for completeness, I will continue to deal four particular submissions advanced.

55 First, Quintis’ submission regarding the nomination of a figure contemplated by cl 4.9 being optional not mandatory, does not deal with the express words employed by the parties in a prudent businesslike way. The relevant sentence of cl 4.9 contains two elements: (a) it addresses a topic (the maximum amount payable); and (b) it identifies where to find that amount (the Schedule). In the commercial context of an insurance contract, where limitations on coverage are of key concern to the parties, the suggestion that the parties took the trouble to introduce a topic, but are taken to have agreed that they intended that the Schedule may not address such a topic, does not commend attraction. A more businesslike construction would be to read the sentence as requiring a mandatory nomination in the Schedule if the cover is taken up, so that the precise limits of that cover are expressly dealt with. That the parties, objectively, are to be taken as having intended such an outcome is further evident by reference to the final sentence of cl 4.9, which commences “This sub-limit” – a reference to the “sub-limit” described in the preceding sentence. Indeed, the clause does not state that if there is an applicable sub-limit specified in the Schedule, then the maximum amount the insurer is liable for is the amount there specified. Related to this, I am unpersuaded by Quintis’ submission that it is “implausible” to read the reference to $10 million as a sub-limit as this would mean that no insurance arrangement involving the excess term cl 4.4 could ever provide cover greater than $10 million in respect of Entity Securities Liability. While I do accept such a construction is limiting (in the sense that the Excess Polices only provide cover for the uneroded portion of the sub-limit), that does not mean that it is commercially unsound, let alone implausible.

56 Secondly, two reasons may explain the different terminology used in cll 4.1 and 4.9: (a) both clauses are in different forms, which may itself explains a choice of different words; and (b) the entry for cl 4.1 needed to achieve more than that required for cl 4.9. In the case of cl 4.9, all that was required was the nomination of a figure for the clause to operate on its terms. By way of contrast, the cl 4.1 entry not only dealt with nomination of a figure, but the modification of the scope of cover provided. This is evident when one has regard to the terms of cl 4.1, which describe an available extension for persons within the class of “Insured Person” for the purposes of cl 1.3. The definition of “Insured Person” is broader than “Non-Executive Directors”, which is referenced in the Schedule alongside cl 4.1. Functionally, the reference in the Schedule thus limits the scope of the persons to which the extension is to relate. By doing so, the Schedule also nominates the number as a sub-limit so that there is no confusion as to the coverage for that sub-class overall.

57 Indeed, even if one was to view this reference to a sub-limit as hard to reconcile with the fact that the same is not provided next to Entity Securities Liability, I do not think that such a reference creates ambiguity in the plain words of cll 4.9 and 8.14. That might have been the case if there were a number of nominations in the same form as cl 4.1, but this is simply one example, which in my view, can be justified. I am not of the view that Quintis’ comparative analysis of cl 4.1 introduces ambiguity into the terms of the 2016-17 Primary or supports the overall submission that Entity Securities Liability is not sub-limited.

58 Thirdly, Quintis’ construction of the 2016-17 Primary necessarily requires the Court to conclude that the parties intended to nominate a figure that was objectively unnecessary since the contract already provided for a Limit of Liability for Section 1B cover, which controlled that section and all extensions to it (including cl 4.9). As was noted in Chapmans Limited v Australian Stock Exchange Limited (1996) 67 FCR 402 (at 411 per Lockhart and Hill JJ), “[a] court will strain against interpreting a contract so that a particular clause is nugatory of ineffective, particularly if a meaning can be given to it consonant with the other provisions in a contract.” Nor is there any justification for the finding that the nomination of a figure in the Schedule is redundant: see XL Insurance Co SE v BNY Trust Company of Australia Limited [2019] NSWCA 215 (at [72] per Gleeson JA, with whom Bell P agreed). Indeed, such a submission neglects the words of cl 4.9, which refers to nomination of a sub-limit and does not refer to the nomination of a Limit of Liability.

59 Fourthly, I reject the submission that since the figure of $10 million for Entity Securities Liability is the same as the Limit of Liability for Section 1B cover, this is somehow suggestive of error which means one ought not treat the former figure as a sub-limit. Not only would this involve a construction of the 2016-17 Primary that is contrary to the express terms of cll 4.9 and 8.14, but there is nothing unusual about the sub-limit being the same as the limit for the section of cover (it would simply mean that the whole of the Limit of Liability could be applied to meeting a cl 4.9 liability). That position is even less surprising here, due to the existence of excess layer terms. Indeed, the operation of cl 4.4 of the Excess Policies proceeds on the existence of a sub-limit in the 2016-17 Primary: where the Section 1B cover Limit of Liability under the 2016-17 Primary is exhausted as a result of payments not made under cl 4.9, cl 4.4 of the Excess Policies provides that the unexhausted portion of the sub-limit continues into the Excess Policies, provided again that the remaining amount of the sub-limit shall be “part of and not in addition to the Limit of Liability” of the Excess Policies.

60 For the above reasons, the Construction Contention must be rejected.

61 Alternatively, Quintis argued that there exists ambiguity in the 2016-17 Primary, which ought be resolved by “recourse to events, circumstances and matters external to the terms of the 2016-17 [Primary], so as to identify the actual intentions of the parties”. For the above reasons, I do not accept that there is ambiguity in the 2016-17 Primary, making it unnecessary to look to extrinsic material, including the background of Quintis’ recent “comprehensive insurance review”.

62 Even if ambiguity were to be identified, I reject that it would lead to a different construction of the 2016-17 Policies. It is well established that if one is permitted to have resort to extrinsic material, evidence of surrounding circumstances is only admissible if it is known to the parties: Electricity Generation Corporation v Woodside Energy Ltd [2014] HCA 14; (2014) 251 CLR 640 (at 656–7 [35] per French CJ, Hayne, Crennan and Kiefel JJ); Codelfa (at 352 per Mason J), the rationale for which was explained by Allsop P (as the Chief Justice then was) in QBE Insurance Australia Ltd v Vasic [2010] NSWCA 166 (at [22], with whom Giles and Macfarlan JJA agreed). Such evidence is also not admissible to support the subjective intention or expectations of the parties: see Ryledar (at 655–6 [262]–[265] per Campbell JA, with whom Mason P and Tobias JA agreed).

63 The reason I emphasise these points is that it was Quintis’ submission that any ambiguity in the 2016-17 Policies ought be resolved by reference to the fact that Quintis had the commercial object of seeking to preserve its expiring amount of cover, that the 2016-17 Primary relevantly adopted the wording of the 2015-16 Primary, and importantly, that the policy wording was understood by Quintis, PSC and the expiring insurers to provide for up to $50 million is Side C cover. Furthermore, Quintis submitted that the evidence leading up to placement of the 2016-17 Policies demonstrates that such a “commercial object” was shared by Quintis and the Relevant Insurers. The difficulty with these submissions is twofold: (a) only four of the Relevant Insurers to the 2016-17 Polices provided insurance under the 2015-16 Policies, and even then, none of those insurers provided Side C cover (see [122])); and (b) this once again elides the distinction in the material sought to be relied upon by Quintis in its Construction Claim to that in its Rectification Claim. Quintis submitted in writing, in little more than a sentence, that the evidence relevant to its Rectification Claim was substitutable as extrinsic material in support of its Construction Claim. I shall not repeat the reasons for why that approach is misconceived. The fact is the evidence does not reveal that the parties objectively intended to provide Side C cover of up to $50 million and that this was not sub-limited. Hence, even if there was ambiguity in the 2016-17 Policies, I am not satisfied that the admission of the extrinsic material identified would alter the conclusion I have reached.

64 Quintis also submitted that in the event there was ambiguity, “it is an ambiguity in the real sense that ought to be resolved against [the Relevant Insurers] in accordance with the contra proferentem rule”.

65 Even if I was to accept that the Relevant Insurers were the proferens in the transaction (a questionable submission given that the insurance policies were drafted and presented by Price Forbes to the Relevant Insurers: cf Halford v Price (1960) 105 CLR 23 (at 30 per Dixon CJ with whom Menzies J agreed and at 34 per Fullagar J)), the contra proferentem rule is but one of a number of rules of contractual construction. Although it was traditionally the case that the contra proferentem rule applied strongly in insurance contracts, the rule is one of last resort, to apply only when ambiguity remains after all other avenues of construction have been exhausted. That view accords with the established position that the process of construing insurance contracts is governed by ordinary principles of contractual interpretation. Hence, even if there was ambiguity in the contract, I am not of the view that the contra proferentem rule assists Quintis.

66 It follows that on their proper construction, the instruments recording the 2016-17 Policies did not provide Side C cover of up to $50 million.

67 It is then necessary to wade into the brume of the Rectification Claim advanced by Quintis. Given the length of the reasons which are dedicated to resolving this claim, it is useful to first set out how this section of the judgment will be structured:

Part F.1 will first set out the general principles applicable to a claim for rectification and the standard of proof necessary to succeed in such a claim;

Part F.2 will articulate three preliminary issues, namely (a) the specific common intention to be established; (b) the documents that need to be rectified; and (c) whose intention is relevant to the rectification of those documents;

Part F.3 will make general comments about the evidentiary record and the principles applicable to inferential reasoning;

Part F.4 will detail the documentary record by way of chronology, including outlining how the parties intend to use each document in support of their case (by approaching the evidence in this way, one is able to understand and contextualise the inferences the Court is being asked to draw);

Part F.5 will expand upon the principles applicable to inferential reasoning by reference to the “rules” in Blatch v Archer (1774) 1 Cowp 63 and Jones v Dunkel (1959) 101 CLR 298;

Part F.6 will make findings as to the intention of Price Forbes and each of the Relevant Insurers, drawing on the evidentiary record outlined in Part F.4 and the submissions made by the parties; and

Part F.7 will examine whether the relevant intention was commonly held by any of the parties.

68 Prior to setting out the relevant legal principles, considering the evidence and making relevant findings, it is appropriate to commence the journey by setting out Quintis’ articulation of its alleged equity. Quintis seeks a declaration (along with an order giving effect to such a declaration to be endorsed on the 2016-17 Policies) that is entitled to rectification of the 2016-17 Primary, and to the extent that the Excess Policies incorporate the terms of the 2016-17 Primary, the Excess Policies, such that:

(1) the words “4.9 Entity Securities Liability $10,000,000” are deleted, and in lieu thereof the words “4.9 Entity Securities Liability Included” or “4.9 Entity Securities Liability $50,000,000” are inserted at page 2 of the 2016-17 Primary Schedule; and

(2) the words “4.9 Entity Securities Liability AUD $10,000,000” are deleted, and in lieu thereof the words “4.9 Entity Securities Liability Included” or “4.9 Entity Securities Liability AUD $50,000,000” are inserted at page two of the MRC annexed to the 2016-17 Primary.

69 The principles relevant to the equitable remedy of rectification were not in dispute. I recently set them out at length in Icon (at [111]–[118]). A summary follows.

F.1.1 General principles of rectification

70 The purpose of the equitable remedy is to make a contractual instrument “conform to the true agreement of the parties where the writing by common mistake fails to express that agreement accurately”: Maralinga Pty Ltd v Major Enterprises Pty Ltd (1973) 128 CLR 336 (at 350 per Mason J). Its rationale has been said to be the avoidance of an unconscientious departure from the common intention of the parties to an agreement: Franklins Pty Ltd v Metcash Trading Pty Ltd [2009] NSWCA 407; (2009) 76 NSWLR 603 (at 710 [444] per Campbell JA, with whom Allsop P and Giles JA agreed); Ryledar (at 667 [315] per Campbell JA, with whom Mason P and Tobias JA agreed); Mayo v W & K Holdings (NSW) Pty Ltd (in liq) (No 2) [2015] NSWCA 119 (at [57] per Gleeson JA, with whom Meagher JA and Sackville AJA agreed).

71 In Simic (at 117 [103]–[104]), Gageler, Nettle and Gordon JJ summarised the elements of rectification in the following way:

Rectification is an equitable remedy, the purpose of which is to make a written instrument “conform to the true agreement of the parties where the writing by common mistake fails to express that agreement accurately”. For relief by rectification, it must be demonstrated that, at the time of the execution of the written instrument sought to be rectified, there was an “agreement” between the parties in the sense that the parties had a “common intention”, and that the written instrument was to conform to that agreement. Critically, it must also be demonstrated that the written instrument does not reflect the “agreement” because of a common mistake. Unless those elements are established, the “hypothesis arising from execution of the written instrument, namely, that it is the true agreement of the parties” cannot be displaced.

The issue may be approached by asking – what was the actual or true common intention of the parties?

(Citations omitted).

72 As to the ascertainment of that common intention, it is useful to draw on the observations of Tobias JA in Ryledar (at 642 [182]–[186]), cited with approval in Simic (at 117 [104] n 113)):

First, the common intention which must be established by clear and convincing proof to justify rectification must be the actual or true common intention of the parties. Second, evidence of that intention may be ascertained not only from the external or outward expressions of the parties manifested by their objective words or conduct but also from evidence of their subjective states of mind.

Third, where, for instance, the correspondence between and/or conduct of the parties establishes a positive lack of an “objective” common intention, then that evidence must be taken in conjunction with the evidence (if any) of their subjective states of mind to determine whether the necessary common intention has been established. …

Fourth, in Westland Savings Bank v Hancock [1987] 2 NZLR 21 at 31, it was held by Tipping J that a party subsequently acting as if the instrument stood in the form into which it is sought to be rectified was strong evidence of that party’s intention at the time to execute the instrument in its rectified form. Such conduct is obviously of significance but, depending on other evidence, if any, is not necessarily conclusive although in the absence of any such evidence it may be.

Fifth, it follows that where the correspondence and/or conduct positively establishes the necessary common intention, then assertions by the party opposing rectification of his or her subjective state of mind which is inconsistent with that party’s outward manifestation of his or her intention, being unexpressed and uncommunicated, is unlikely to trump his or her expressed intention. But this is because that party is unlikely to be believed.

Sixth, where … the outward expression of the parties’ common intention is at best inconclusive, then establishing that the subjective states of mind of the parties evinces the relevant common intention becomes critical if the necessary standard of proof to support an order for rectification is to be achieved.

(Emphasis added).

73 Furthermore, in Ryledar, Campbell JA (with whom Tobias JA and Mason P agreed) discussed whether an “outward expression of accord” is necessary for the grant of relief by way of rectification (an issue considered, but not decided, by Kiefel J in Simic (at 103 [43]–[45], with whom French CJ agreed) and by Wilson J in Maralinga (at 452, with whom Gibbs CJ agreed)), concluding that an outward expression need not be by words that say in substance “this is my intention”, but rectification still requires disclosure of some form. This accords with what now appears to be a resolution of this issue by the High Court in Simic (at 117 [104] per Gageler, Nettle and Gordon JJ) that “[t]here is no requirement for communication of that common intention by express statement, but it must at least be the parties’ actual intentions, viewed objectively from their words or actions, and must be correspondingly held by each party”.

F.1.2 Proof necessary for rectification

74 As to the establishment of that common intention, the evidence necessary to discharge the onus needs to be convincing: see Fowler v Fowler (1859) 4 De G & J 250 (at 265 per Lord Chelmsford), cited with approval in Maralinga (at 449 per Mason J, with whom Menzies J agreed), Pukallus v Cameron (1982) 180 CLR 447 (at 457 per Brennan J) and Simic (at 102 [41] per Kiefel J, with whom French CJ agreed). Another formulation is that “clear and convincing proof” is necessary: Commissioner of Stamp Duties (NSW) v Carlenka Pty Ltd (1995) 41 NSWLR 329 (at 345 per McLelland AJA); Franklins (at 712 [451] per Campbell JA, with whom Allsop P and Giles JA agreed); Ryledar (at 638 [161] per Campbell JA, with whom Mason P and Tobias JA agreed); Joscelyne v Nissen [1970] 2 QB 86 (at 98 per Russell, Sachs and Phillimore LJJ). Elsewhere, it has been said that “it is not sufficient to show that the written instrument does not represent their common intention unless positively also one can show what their common intention was”: Perpetual Ltd v Myer Pty Ltd [2019] VSCA 98 (at [117] per Whelan, Niall and Hargrave JJA), citing with approval the remarks of Simonds J in Crane v Hegeman-Harris Co Inc [1939] 1 All ER 662 (at 665), which were themselves cited with approval in Slee v Warke (1949) 86 CLR 271 (at 281 per Rich, Dixon and Williams JJ). This insistence on clear proof reflects an ancient concern to not undermine the integrity of written agreements: Seymour Whyte Constructions Pty Ltd v Oswald Bros Pty Ltd (in liq) [2019] NSWCA 11; (2019) 99 NSWLR 317 (at 323 [13] per Leeming JA),

75 Furthermore, as I noted in Icon (at [116]–[118]), these observations must be viewed in the light of the mandatory considerations in s 140(2) of the EA, including the nature of the subject matter of the proceeding; namely, the unlikelihood that commercial persons would have formed a common intention which was not reflected in the agreement which they deliberately reduced to writing. Such inherent unlikelihood can be seen as a reflection of what Mason J termed the “hypothesis arising from execution of the written instrument, namely, that it is the true agreement of the parties”: Maralinga (at 350), quoted with approval in Simic (at 117 [103] per Gageler, Nettle and Gordon JJ); see also Equuscorp Pty Ltd v Glengallan Investments Pty Ltd [2004] HCA 55; (2004) 218 CLR 471 (at 483 [33] per Gleeson CJ, McHugh, Kirby, Hayne and Callinan JJ). Indeed, as Brightman LJ observed in Thomas Bates and Son Ltd v Wyndhams (Lingerie) Ltd [1981] 1 WLR 505 (at 521), “[i]t is not, I think, the standard of proof which is high, so differing from the normal civil standard, but the evidential requirement needed to counteract the inherent probability that the written instrument truly represents the parties’ intention because it is a document signed by the parties.”

76 In Franklins, Campbell JA echoed these considerations when he explained (at 713 [459]) that great care is required in making factual findings of common intention. The reasons include issues of policy, such as the practical importance and social institution of making contracts in writing, of people ordinarily being able to rely upon documents that are apparently regular, meaning what they say, and of the danger associated with imposing on a party a contract which they did not make.

77 The reason why I have dwelled so heavily on these statements of principle is because, as will become clear, the evidence adduced is largely circumstantial. That means that close attention needs to be paid to the question of onus and, in particular, the faithful application of s 140 of the EA.

78 As can be gleaned from these principles, three preliminary issues of central importance arise for determination in Quintis’ Rectification Claim:

(1) what is the specific common intention contended to have existed between the parties?;

(2) which documents need to be rectified to give effect to this common intention?; and

(3) who must it be proven held that common intention?

79 It is only once these preliminary questions have been addressed that one can turn to examine the evidence relating to intention.

F.2.1 What is the common intention alleged?

80 Quintis’ case is that the parties intended to execute the 2016-17 Policies on the basis that Side C cover was not subject to a sub-limit of $10 million, but was in fact equal to the Limit of Liability for Section 1B cover provided for by each of the 2016-17 Primary, the 2016-17 1XS and the 2016-17 2XS, meaning that the 2016-17 Policies collectively provided Side C cover of up to $50 million. I will refer to this purported intention as the Side C Coverage Intention.

F.2.2 Which documents need to be rectified?

81 Quintis submitted that its Rectification Claim could succeed in two alternative ways: (a) the primary argument advanced was that only the 2016-17 Primary needs to be rectified given that the Excess Policies contain the term “CONDITIONS: Full Follow Form As attached Primary Policy Number B0507N16FA15350” (Follow Form Argument); or (b) in the event that the primary submission is incorrect, each of the Excess Policies must also be rectified to the extent necessary.