FEDERAL COURT OF AUSTRALIA

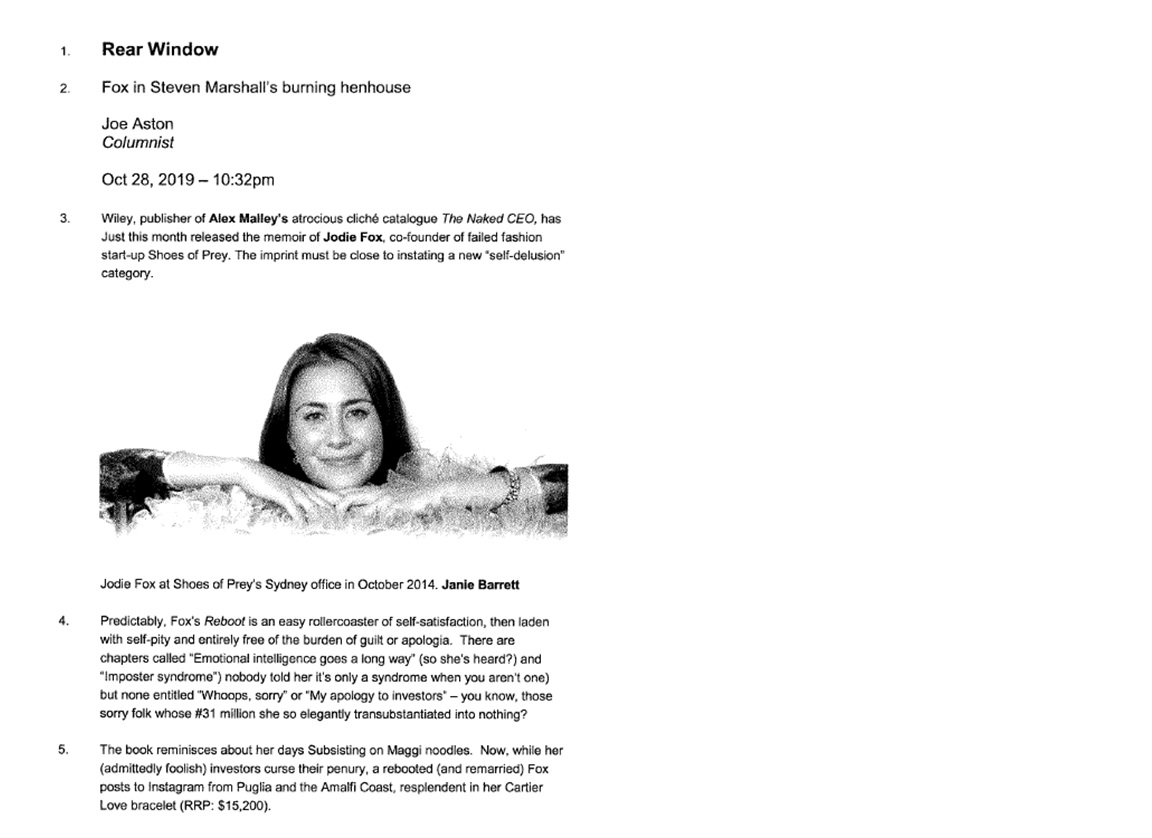

Stead v Fairfax Media Publications Pty Ltd [2021] FCA 15

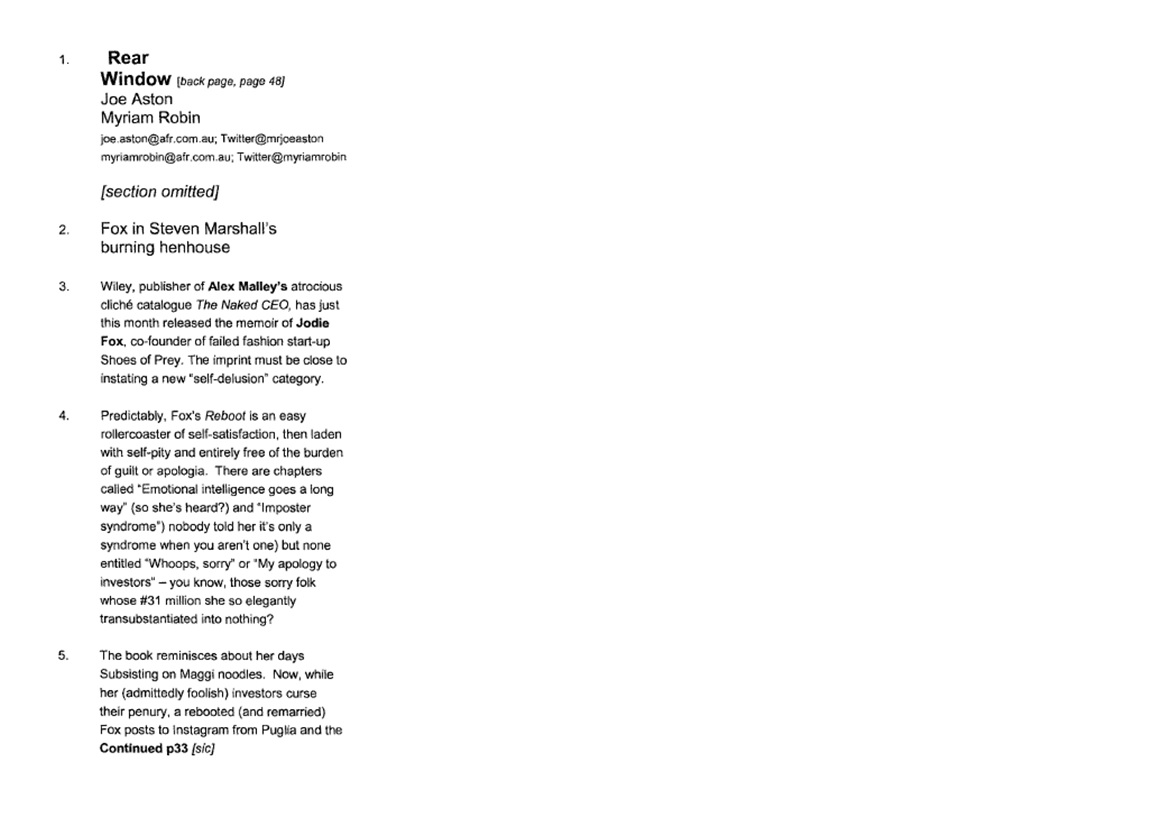

ORDERS

Applicant | ||

AND: | FAIRFAX MEDIA PUBLICATIONS PTY LTD (ACN 003 357 720) First Respondent JOE ASTON Second Respondent | |

DATE OF ORDER: | 27 Janaury 2021 |

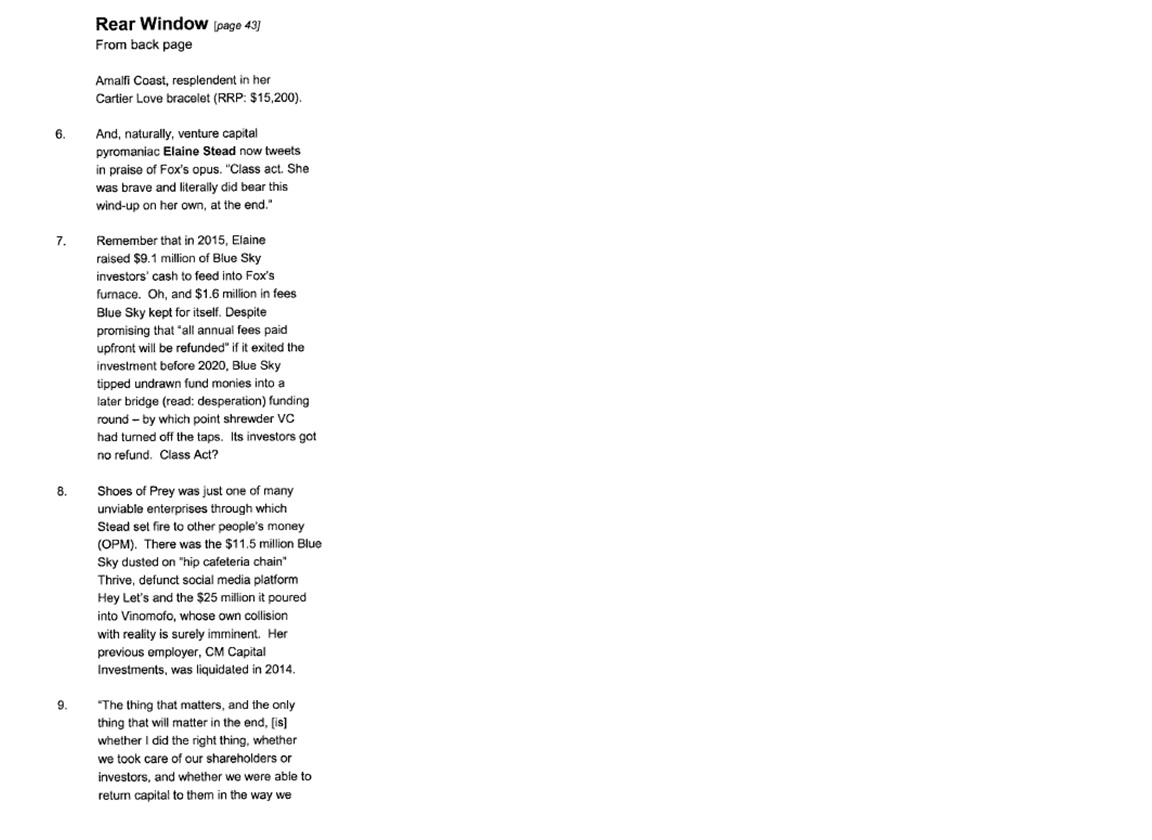

THE COURT ORDERS THAT:

1. The proceeding be adjourned to 9am on 3 February 2021 for the making of final orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

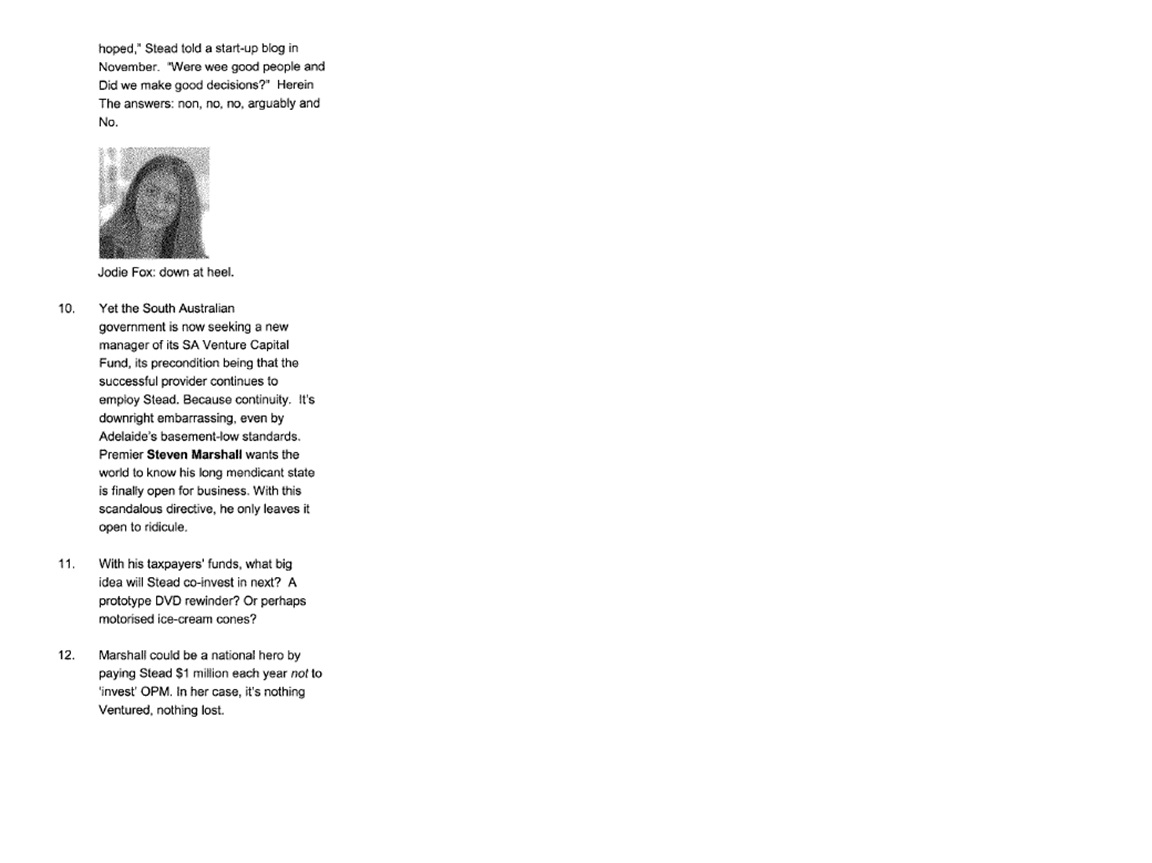

LEE J:

A INTRODUCTION AND OVERVIEW

1 Mr Joe Aston, together with a colleague, writes a column entitled “Rear Window” for The Australian Financial Review (AFR) published by Fairfax Media Publications Pty Ltd (Fairfax).

2 It is common ground Mr Aston is a talented and oftentimes highly entertaining wordsmith. He is no respecter of persons. He gave evidence he has a “blank canvass” to “target and address” hypocrisy, cant, farce and misfeasance in the corporate and political world. From the perspective of readers who inhabit those worlds, Mr Aston’s work, with its characteristic acerbity, is no doubt often amusing; but one suspects the mirth of some readers might be mixed with a vague sense of disquiet that their behaviour might someday become the subject of his mocking focus. It was perhaps for this reason that Mr Aston blithely (but self-revealingly) gave evidence that he was “not a very popular” columnist.

3 But a writer targeting and addressing the perceived folly or sins of others walks a fine line. It is a line which reflects the tension between two important rights which the law of defamation seeks to balance: the right to freedom of expression and the right to reputation. Consistently with protecting the right to expression, which is fundamental to the exchange of ideas, is that liberty is given to express ideas provocatively. As Sir Fredrick Jordan observed in Gardiner v John Fairfax & Sons Pty Ltd (1942) 42 SR (NSW) 171 (at 174), “a critic is entitled to dip his pen in gall for the purpose of legitimate criticism; and no one need be mealy-mouthed in denouncing what he regards as twaddle, daub or discord”. But the counterbalance is that for a writer’s opinion to attract protection it must, in truth, be an opinion, be related to a matter of public interest, and be properly based – these requirements mean a freedom to express one’s views, however foolish or malignant, does not become a licence to defame without lawful excuse. In essence this case is about whether this line the law draws was crossed.

4 In 2018 and 2019, Mr Aston directed his focus to Blue Sky Alternative Investments Limited (Blue Sky), a listed asset manager, of which Dr Elaine Stead was a director and the Head of Venture Capital. For reasons I will explain, given the focus of his column, it is unsurprising that Blue Sky came into his ken.

5 Dr Stead asserts that she was singled out from the others associated with Blue Sky and that in doing so, not only did Mr Aston cross the line the law draws, but that he pole vaulted it. As a consequence, she brings this proceeding in relation to five publications reproduced in the schedules to these reasons, being:

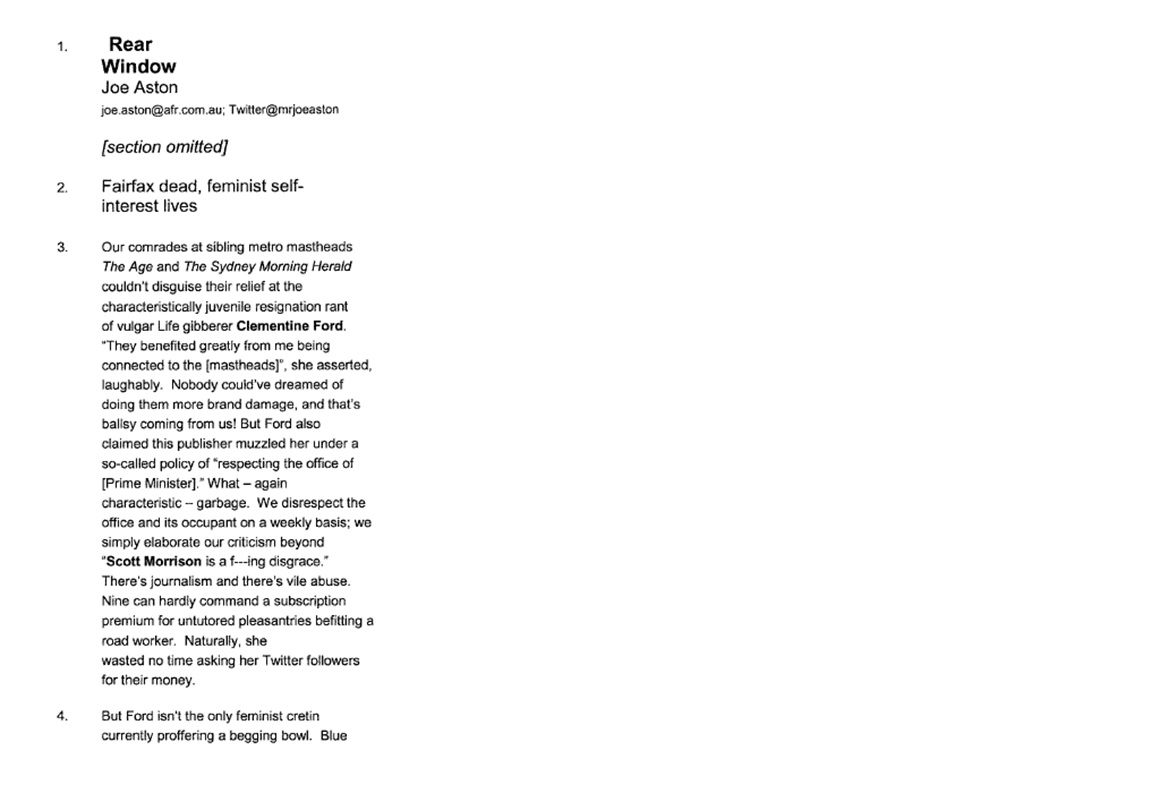

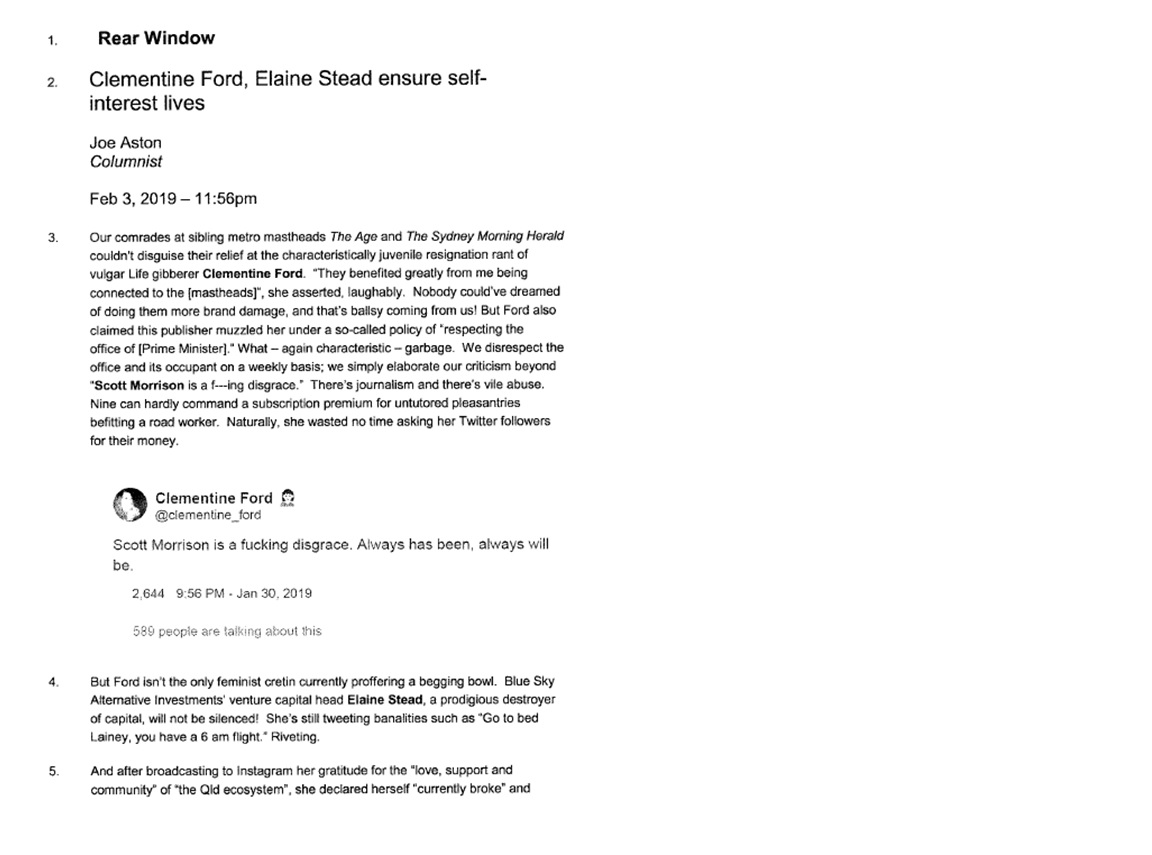

(1) a column entitled “Fairfax dead, feminist self-interest lives” published in the AFR newspaper on 4 February 2019 (First Article);

(2) a column entitled “Clementine Ford, Elaine Stead ensure self-interest lives” published on the AFR website from 3 February 2019 (First Internet Matter);

(3) a column entitled “Fox in Steven Marshall’s burning henhouse” published in the AFR newspaper on 29 October 2019 (Second Article);

(4) a column entitled “Fox in Steven Marshall’s burning henhouse” published on the AFR website from 28 October 2019 (Second Internet Matter); and

(5) a Twitter post published by Mr Aston on 28 October 2019 (Third Matter).

6 Dr Stead alleges that the matters conveyed various imputations detailed below, each of which she alleges is defamatory. Issue has been joined by Fairfax and Mr Aston denying that the pleaded (or substantively similar) meanings were conveyed. Further, Fairfax and Mr Aston relied upon, and only relied upon, the defence of honest opinion pursuant to s 31 of the Defamation Act 2005 (NSW) (Act), being the opinion of Fairfax’s employee, Mr Aston.

7 For the reasons that follow, Dr Stead has established that some of the imputations pleaded (or imputations substantially similar to them) have been conveyed, and that they are defamatory. The pleaded defence of honest opinion has not been made out by Fairfax or Mr Aston and, as a consequence, Dr Stead is entitled to relief.

8 In explaining these conclusions, the balance of these reasons will be divided into the following headings:

Part B: The Imputations Conveyed and the Defamation

Part C: The Evidence of Dr Stead and Mr Aston Generally

Part D: Honest Opinion

Part E: Relief

Part F: Conclusion and Orders.

B THE IMPUTATIONS CONVEYED AND THE DEFAMATION

B.1 The Pleaded Imputations and the Separate Determination

9 Dr Stead pleaded the following defamatory imputations:

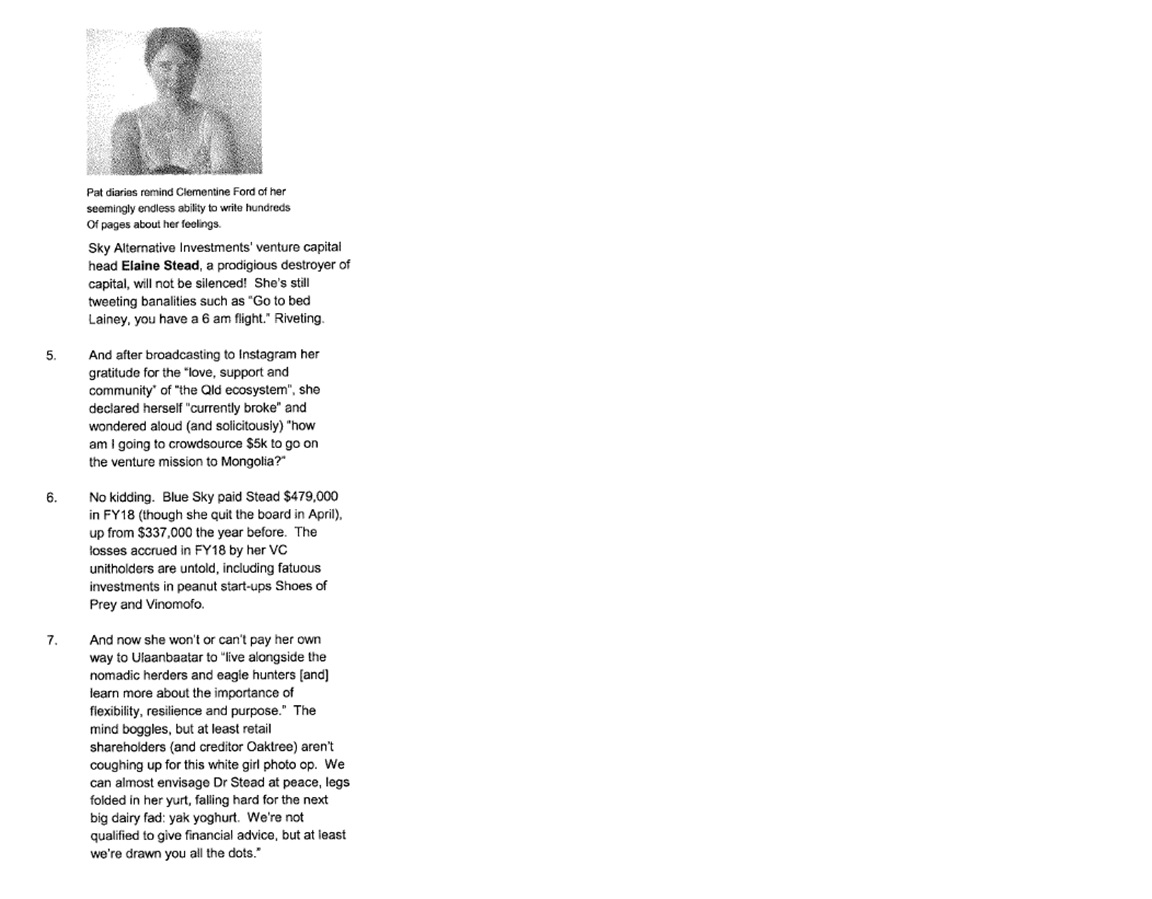

(1) as to the First Article and the First Internet Matter (First Matter), that:

(a) the applicant is a cretinously stupid person (First Alleged Imputation);

(b) the applicant wilfully destroyed the capital of business ventures with which she was associated causing enormous losses to unitholders (Second Alleged Imputation);

(c) alternatively to (b), the applicant recklessly destroyed the capital of business ventures with which she was associated causing enormous losses to unitholders (Third Alleged Imputation);

(d) the applicant is a venture capitalist, who made stupid investments in two worthless companies, Shoes of Prey and Vinomofo, which had no business and no prospects of success (Fourth Alleged Imputation);

(2) as to the Second Article and the Second Internet Matter (Second Matter), that:

(a) the applicant deliberately destroyed the capital of business ventures with which she was associated causing enormous losses to investors (Fifth Alleged Imputation);

(b) the applicant, a venture capitalist, wantonly lost millions of dollars entrusted to her by unsuspecting investors by channelling their funds into a string of hopeless investments (Sixth Alleged Imputation);

(c) the applicant is an untrustworthy venture capitalist who fails to deliver on her promises to shareholders and investors (Seventh Alleged Imputation); and

(3) as to the Third Matter, that the applicant is not competent to hold the position of VC fund manager for South Australia because she deliberately and shamelessly lost other people’s money (Eighth Alleged Imputation).

10 There was no issue Dr Stead was identified in the publications and despite initially adopting a different approach, by the time of the filing of their opening submissions, Fairfax and Mr Aston did not contest that the pleaded imputations are defamatory of Dr Stead, allowing the Court to move directly to considering the issue of meaning.

11 The parties agreed that it would be expedient to determine the issue of meaning at the conclusion of Dr Stead’s case. This course was embraced as it would mean, consistently with the overarching purpose of civil litigation in this Court, that any defence case and any final submissions were directed only to the meanings actually conveyed, and not to irrelevancies.

12 Accordingly, on 4 December 2020, an order was made by consent and pursuant to s 37P(2) of the Federal Court of Australia Act 1976 (Cth), that the issues joined by paragraphs 5, 8 and 10 of the statement of claim and the second further amended defence be determined separately and before any other issue in the proceeding. It may be obvious, but it is worth stressing, that the task upon which the Court was engaged in deciding this separate question was not the legal issue as to whether the matters were reasonably capable of bearing the defamatory meaning or meanings alleged, but rather the final determination of whether the publications did in fact convey the meanings for which Dr Stead contends.

13 Argument took place immediately, and on the following hearing day, prior to the opening of the defence case, I determined the separate question. To avoid any bifurcation of the proceeding but preserve the rights of the parties, I made orders granting leave to appeal (to the extent it is necessary), and extending time to allow any separate question appeal to be filed contemporaneously with any appeal from the orders made at the conclusion of this proceeding. Set out in the balance of this section are my reasons for my determination of meaning.

B.2 The Relevant Law

14 The three matters were pored over repeatedly during the hearing, but it is erroneous to approach the question of meaning by scrutinising the publications with the intensity of deconstructing a haiku. The principles to apply were not in dispute, and I explained them in Oliver v Nine Network Australia Pty Ltd [2019] FCA 583 (at [19]–[20]) as follows:

The relevant principles … are summarised, with respect helpfully and comprehensively, by White J in Hockey v Fairfax Media Publications Pty Limited [2015] FCA 652; (2015) 237 FCR 33 at 49-51 [63]-[73]. More recently, as the High Court (Kiefel CJ, Bell, Keane, Nettle and Gordon JJ) relevantly explained in Trkulja v Google LLC [2018] HCA 25; (2018) 92 ALJR 619 at 627 [31]-[32]:

The test for whether a published matter is capable of being defamatory is what ordinary reasonable people would understand by the matter complained of. In making that assessment, it is necessary to bear in mind that ordinary men and women have different temperaments and outlooks, degrees of education and life experience. As Lord Reid observed in Lewis v Daily Telegraph Ltd, “[s]ome are unusually suspicious and some are unusually naïve”. So also are some unusually well educated and sophisticated while others are deprived of the benefits of those advantages. The exercise is, therefore, one of attempting to envisage a mean or midpoint of temperaments and abilities and on that basis to decide the most damaging meaning that ordinary reasonable people at the midpoint could put on the impugned words or images considering the publication as a whole.

… it is often a matter of first impression. The ordinary reasonable person is not a lawyer who examines the impugned publication over-zealously but someone who views the publication casually and is prone to a degree of loose thinking. He or she may be taken to “read between the lines in the light of his general knowledge and experience of worldly affairs”, but such a person also draws implications much more freely than a lawyer, especially derogatory implications, and takes into account emphasis given by conspicuous headlines or captions. Hence, as Kirby J observed in Chakravarti v Advertiser Newspapers Ltd, “[w]here words have been used which are imprecise, ambiguous or loose, a very wide latitude will be ascribed to the ordinary person to draw imputations adverse to the subject”.

(Citations and footnotes omitted)

Hence my task, as the tribunal of fact, is addressing the question as to whether the ordinary reasonable viewer would have understood the matters complained of in the defamatory sense pleaded: Favell v Queensland Newspapers Pty Ltd [2005] HCA 52; (2005) 79 ALJR 1716 at 1720 [11], 1721 [17]. Meaning is to be determined objectively, by reference to the hypothetical construct of the ordinary reasonable viewer, who is taken to glean the ordinary meaning conveyed … It necessarily follows that the meaning the respondents intended to convey is irrelevant, as is any evidence as to how the publication was actually understood: Wagner v Harbour Radio Pty Ltd [2018] QSC 201 at [33] (Flanagan J).

15 It is worth summarising some further principles relevant to meaning because during argument, there was extensive debate as to reformulations and whether they differed in substance to the pleaded imputations. There was also debate as to the distinct question as to whether it was possible for Dr Stead to depart from the pleading. To ensure there was no misunderstanding as to how these issues were to be resolved, I prepared (and the parties eventually agreed) a summary of the relevant principles, largely but not exclusively drawn from Australian Broadcasting Corporation v Chau Chak Wing [2019] FCAFC 125; (2019) 271 FCR 632. It was as follows:

(1) procedural fairness requires that a respondent is entitled to know what defamatory imputations are relied upon by an applicant, thus requiring the imputations to be pleaded specifically: see Federal Court Rules 2001 (Cth) (FCR) 16.02, 16.08 and 16.41;

(2) an applicant may allege that a published matter conveys distinct defamatory imputations, and may allege imputations in the alternative: see FCR 16.06;

(3) it is open to an applicant to choose the imputations relied upon, which will generally confine the questions of meaning and will determine the metes and bounds of the contest at trial;

(4) these boundaries extend to meanings that are not substantively different in that they are comprehended in, or are a shade or nuance of, the pleaded meaning;

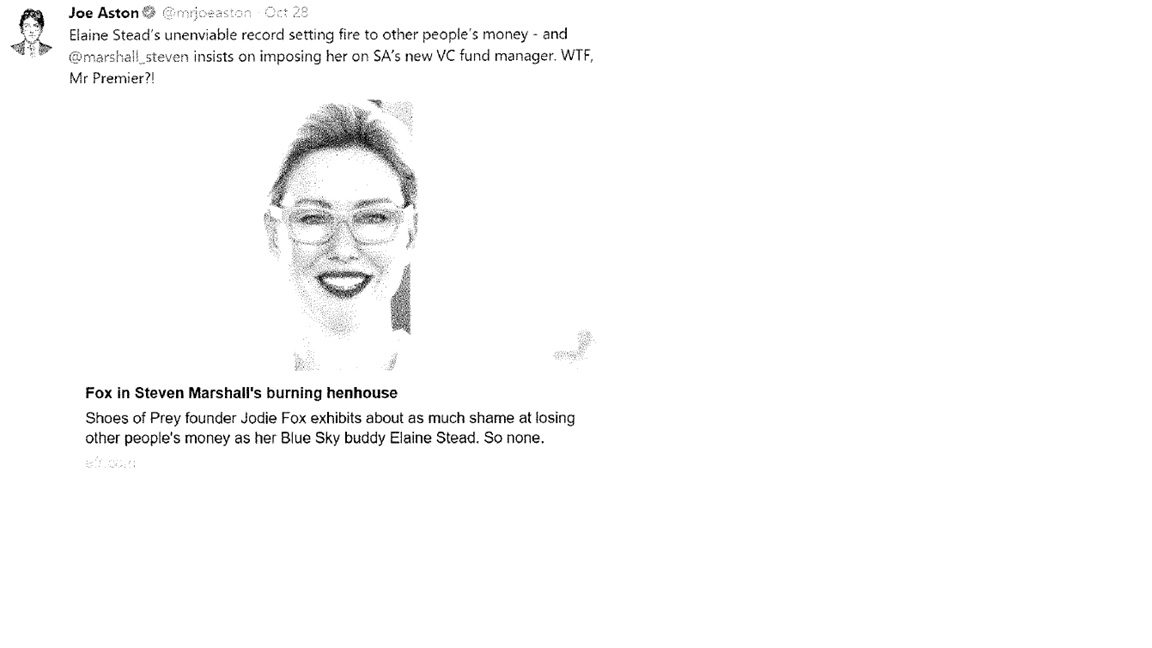

(5) if a variant imputation is proposed to be relied upon, whether, and to what extent, a departure from the pleaded meanings is permitted is to be resolved by considerations of fairness and practical justice;

(6) if a respondent is, or might reasonably be thought to be, prejudiced, embarrassed or unfairly disadvantaged by the proposed departure to a variant meaning, the applicant will be held to the meaning pleaded;

(7) in considering the question of prejudice or fairness as between the parties, it is relevant to bear in mind that when an applicant makes a forensic choice to plead a more serious or “higher” meaning than others that are available, a consequence of this forensic choice is to render more difficult the task of a respondent in proving the imputation is substantially true (it necessarily follows that allowing a less serious meaning to be relied upon by an applicant at trial could, depending upon the circumstances, visit an unfairness upon a respondent);

(8) the Court at trial is required to determine the meaning which the matter conveyed to an audience or readership composed of ordinary decent persons, being reasonable people of ordinary intelligence, experience and education who bring to the question their general knowledge and experience of worldly affairs;

(9) given that meaning is to be determined objectively, the audience is taken to have a uniform view of meaning and although different people might in fact have understood the meanings conveyed in different ways, the Court must arrive at a single objective meaning; and

(10) in considering the defences that may have been run, the statutory defence of truth under s 25 of the Act requires the respondent to prove that the imputations carried are substantially true and hence a respondent is limited to justifying a meaning upon which the applicant might have succeeded.

16 With all these principles in mind, it is appropriate to deal with each pleaded imputation in turn.

B.3 Were the Imputations Conveyed?

First Alleged Imputation

17 Although formally put in issue, at trial there was no contest that the First Alleged Imputation was conveyed in a substantially similar form (but removing the tautology). It became common ground that the imputation that Dr Stead is a cretin was conveyed.

Second Alleged Imputation

18 The imputation that “Dr Stead wilfully destroyed the capital of business ventures with which she was associated causing enormous losses to unitholders” was said to arise from the phrase “a prodigious destroyer of capital” in [4] (emphasis added), and the sentence commencing “[t]he losses accrued in FY18” in [6], and what was said to be the overall tone of the First Matter. In addition, in the First Internet Matter, this meaning is said to be further advanced by the by-line “a tax loss specialist” in [8].

19 This contention is unpersuasive. The hypothetical referee would not understand the First Matter to convey that Dr Stead wilfully, that is, deliberately, destroyed capital causing enormous losses to unitholders. As set out above, a meaning that the ordinary reasonable reader would understand from the First Matter is that Dr Stead is a cretin. The ordinary reasonable reader would also understand Mr Aston to be saying that she had made silly or maladroit decisions, such as investing in the companies known as Shoes of Prey and Vinomofo (at [6]). The impression conveyed is one of stupidity and want of care and skill, and this is inconsistent with the notion that she was engaging in the wilful destruction of property. Although the focus is always on what was conveyed to the ordinary reasonable reader, it is noteworthy that in her final submissions (at [232]) Dr Stead agreed that destroying capital, causing enormous losses to investors, amounted to an allegation of “criminal conduct”. Although the correctness of that characterisation would depend upon the circumstances, it points to the seriousness of an assertion in the terms of the Second Alleged Imputation, which I do not consider was conveyed.

Third Alleged Imputation

20 Necessarily, given it eschews deliberate conduct, the imputation that Dr Stead “recklessly destroyed the capital of business ventures with which she was associated causing enormous losses to unitholders”, is a true alternative to the Second Alleged Imputation. Dr Stead asserts that it arises from the same content. The primary submission of Fairfax and Mr Aston is that given the notion that Dr Stead made silly or pointless decisions is conveyed, this impression is contrary to the suggestion that her conduct is reckless. This submission should be rejected. Given the ordinary meaning of the relevant adverb is the action of taking steps “[w]ithout regard to consequences or risk, rashly, imprudently” (Oxford English Dictionary, 3rd ed, 2009 (OED)), this captures accurately what was conveyed to the ordinary reasonable reader. Having said this, recklessness is a somewhat nebulous concept: it can mean subjective recklessness (being conduct engaged in without any regard to the consequences of the conduct); but it can also describe objective recklessness, a concept which might otherwise be described as rash or imprudent conduct. Dr Stead submitted that the meaning pleaded was directed to the latter of these conceptions, and accepted that to avoid any ambiguity, the word “rashly” better captured what was conveyed.

21 The more substantive submission of Fairfax and Mr Aston was that the pleader had simply missed the mark. It was submitted that the ordinary reasonable reader would understand that the capital that is destroyed ([4]) is that of the VC unitholders ([6]), that is, the investors’ money, rather than the capital of the businesses with which Dr Stead is associated or with which she invests. The contention in the First Matter is that Dr Stead’s investments had caused the loss of investors’ money. It says nothing whatsoever, it was submitted, of Dr Stead’s management or involvement in any business invested in, or whether or not her conduct led to the loss of the capital of those businesses.

22 At first glance it might be thought that there is something in the difference between the focus on the destruction of the capital of the business ventures with which Dr Stead was associated and the destruction of the value of unitholders’ investments. For this reason, argument as to the Third Alleged Imputation transformed into debate as to whether an imputation with certain textual differences was substantively different in that it was comprehended in, or amounts to a shade or nuance of, the pleaded meaning.

23 When Dr Stead is introduced at [4], she is described as a “prodigious destroyer of capital”. The capital to which reference is being made is not specified. It is a somewhat loose expression to use in the context. In the abstract, a reader would most likely understand the term “capital” to mean the cash that comes into a business or conceptualise it as working capital, being an excess of current assets over current liabilities in a business. But colloquially, and leaving aside any accounting niceties, to an ordinary reasonable reader, the concept could no doubt also be conceived as the amount invested in a fund from which an investor sought to obtain a return.

24 We are not dealing with the abstract. It is trite that the matter must be read as a whole, and the imputations pleaded are to be construed in the context of the entire matter. When one attends to this task, the meaning conveyed to the hypothetical construct emerges tolerably clearly. After the reference to capital in [4] and the reference to Dr Stead’s Instagram posts in [5], reference is then made at [6] to the losses accrued by the “VC unitholders”. The whole thrust of the matter is the proffering of a “begging bowl” ([4]) by someone who has rashly destroyed the wealth of others, being the unitholders ([6]), and the ridicule conveyed as a consequence ([7]).

25 The ordinary reasonable reader does not engage in over-elaborate analysis and given the mocking tone, notwithstanding the AFR is a serious publication, it is less likely that the ordinary reasonable reader would read the First Matter with a high degree of analytical care.

26 The sting of rash destruction of capital causing enormous losses to unitholders was conveyed. The issue was whether allowing Dr Stead to rely on the recast imputation that “Elaine Stead rashly destroyed capital causing enormous losses to unitholders” is either: (a) sufficiently similar to be comprehended within the original pleaded meaning; or (b) a departure from the pleaded meaning, which nonetheless should be permitted when regard is had to considerations of fairness and practical justice.

27 When one has regard to the whole context of the article, the meaning that Dr Stead rashly destroyed capital causing enormous losses to unitholders is not substantively different in that it is comprehended within the terms of the pleaded meaning. As was explained by Mahoney ACJ in Crampton v Nugawela (1996) 41 NSWLR 176 (at 183), an applicant should not fail if the error is not pleading with complete accuracy the imputation that is in the published material. This is a case where the pleader, in attempting to respond to an ambiguous publication, has attempted to translate the imputation from the published material to the pleading (although it might have been done with more precision).

28 But even if I was wrong in this view, it would not matter. In contrast to the position in relation to the Second Matter to which I will come, if it is the case that the imputation that Dr Stead rashly destroyed capital causing enormous losses to unitholders is not comprehended within the original pleaded meaning, the supposed relevant unfairness articulated by Fairfax and Mr Aston had a high degree of unreality about it. It was not contended, nor could it be, that the cross-examination of Dr Stead would have been conducted differently in any specified way. Nor would I accept that any earlier recasting would have caused other or further enquiries to be made prior to trial. This is a case where a statutory truth defence was initially pleaded to this and other imputations. Over a score of subpoenas were issued and a vast array of material was inspected.

29 Fairfax and Mr Aston incorporated extensive particulars to justification (no less than 194 of them) of the imputation that there was a reckless destruction. Any fair reading of those particulars demonstrates that Fairfax and Mr Aston were prepared to run a truth defence which went beyond, but incorporated, losses to investors; moreover, and perhaps more relevantly, in the honest opinion defence maintained to the matter which was said to convey the Third Alleged Imputation, the particulars were, in part, directed to the role of Dr Stead in the management and deployment of funds of investors and her “overall responsibility” for exiting those investments realising gains or losses (particular 6), and particularisation was given of the losses in various funds by investors (see, eg, particulars 18, 30, 43, 44, 47).

30 Any notion that Fairfax and Mr Aston were labouring under the view that the capital of investors in the funds was somehow irrelevant to the issues to be determined must be rejected.

31 I find an imputation not substantially different to the imputation pleaded was conveyed in the terms identified. But in the event I am wrong to characterise the imputation in that way, no relevant unfairness or unjustness is occasioned to Fairfax and Mr Aston in allowing it to be relied upon.

Fourth Alleged Imputation

32 Finally, as to the First Matter, the imputation that Dr Stead “is a venture capitalist, who made stupid investments in two worthless companies, Shoes of Prey and Vinomofo, which had no business and no prospects of success” is said to be conveyed from the reference to “feminist cretin” in [4], the sentence commencing “[t]he losses accrued” in [6], and the overall tone of the First Matter in belittling Dr Stead. In the First Internet Matter, this meaning also is advanced by the by-line “a tax loss specialist” in [8].

33 Although conceding that the word “peanut” supports the notion “worthless” in the imputation, Fairfax and Mr Aston submit that nothing in the First Matter is addressed to whether the two companies had a business or prospects of success at the time of the investment.

34 This submission is without merit. A stupid investment in a worthless business would plainly be understood by the ordinary reader to be an investment that was misconceived at the time the decision was made by Dr Stead and others to invest. Although the businesses are identified as “start-ups” and are labelled as devoid of worth (that is, “peanut”), the notion they had “no business” might be thought to be subtly different to “no business of any worth”. The imputation conveyed to the ordinary reasonable reader was that “Elaine Stead is a venture capitalist, who made stupid investments in two worthless companies, Shoes of Prey and Vinomofo, which had no prospects of success”. This is not substantively different to what is pleaded.

Fifth Alleged Imputation

35 Turning to the Second Matter, it is said that the imputation was conveyed that Dr Stead “deliberately destroyed the capital of business ventures with which she was associated causing enormous losses to investors”.

36 Dr Stead submitted that this imputation arises from the entire Second Matter, including: the heading “Fox in Steven Marshall’s burning henhouse” in [2]; the phrase “venture capital pyromaniac” in [6]; the statement in [7] that Dr Stead “raised $9.1 million … to feed into Fox’s furnace”; the whole of [8], especially the statement “Stead set fire to other people’s money”; the answer “no” to the question “whether I did the right thing” in [9]; the suggestion that it was “scandalous” to allow Dr Stead to remain involved with the South Australian Venture Capital Fund (SAVCF) in [10]; the last sentence in [12], being “[i]n her case, it’s nothing Ventured, nothing lost”; and the overall tone of the Second Matter.

37 In a reprise of the arguments made in relation to the Second Alleged Imputation, Fairfax and Mr Aston contended the Second Matter would not convey that Dr Stead deliberately destroyed capital. The idea that a venture capitalist would deliberately destroy capital was said to be absurd, requiring such a meaning to be spelt out in plain terms and the pleaded meaning attributes a state of mind to Dr Stead that would simply not be understood by the ordinary reasonable reader. Considered as a whole, it was said that it does not reasonably convey that the loss of money was deliberate, as opposed to a result of bad decisions (see [9]). The use of the term “pyromaniac” does not, they submitted, convey an intention to destroy or cause damage.

38 As noted above, consideration must be given to tone and context. The tone was one of criticism but laden with an attempt to convey such criticism in what was intended to be a “clever” way. The criticism of Dr Stead was trenchant, but read as a whole it does not convey that she was engaged in a process of the deliberate destruction of the money of others. This can be seen in part by [7] which compares her actions to other venture capitalists that are described as “shrewder”; that is, better able to identify when the point had been reached that good money should not be thrown after bad. Similarly, in [9], the ordinary reasonable reader would discern that the article was conveying that although Dr Stead was an “arguably” good person who did the wrong thing, she did not take care of shareholders and investors, did not return capital in the way in which Blue Sky had targeted and failed to make good decisions. What was conveyed was that Dr Stead was behaving rashly or stupidly, not that she was intent on the seriously wrongful conduct of deliberately destroying money.

39 In addition to the necessity to consider context generally, specific reference should be made to two matters. The first is that in reaching my conclusion, the heading “Fox in Steven Marshall’s burning henhouse”, caused me some pause. The reference to a “fox” must be understood by a reader to refer to Dr Stead rather than Ms Jodie Fox, the other woman referred to in the article, because Ms Fox had nothing to do with the SAVCF or any activity or responsibility of the Premier of South Australia (as is made plain in [10]–[12]). The use of the descriptor “fox” is oft used to connote a cunning or sly person. Taking the word in isolation (used metaphorically to refer to a person), it does suggest some element of deceit or slyness. Read in context, however, such a reading would be strained. Reasonable people of ordinary intelligence, experience and education reading the whole article would not attach such significance into a play on words which, as the reader would understand, has its origin in the name of the other principal target of the article, Ms Fox.

40 The second is the danger in also reading too much into the term “pyromaniac”, or setting fire to money, or the notion of feeding cash into a furnace. A pyromaniac is, obviously enough, someone suffering from pyromania which, as would be known to the ordinary reasonable reader, is a type of mental disorder characterised by the impulse to set fire to things. Although the actions of a pyromaniac are intentional, pyromania is well understood as being a pathological or compulsive disorder. In this sense, the ordinary reasonable reader would distinguish it from arson, which is also an intentional act but well understood as being motivated by some non-pathological desire or purpose, such as material gain or revenge. Fire was used by the author as an extended metaphor (hence the references to setting fire to other people’s money or feeding cash into the furnace of Shoes of Prey), which references would all be understood as a fancy.

41 The Fifth Alleged Imputation was not conveyed.

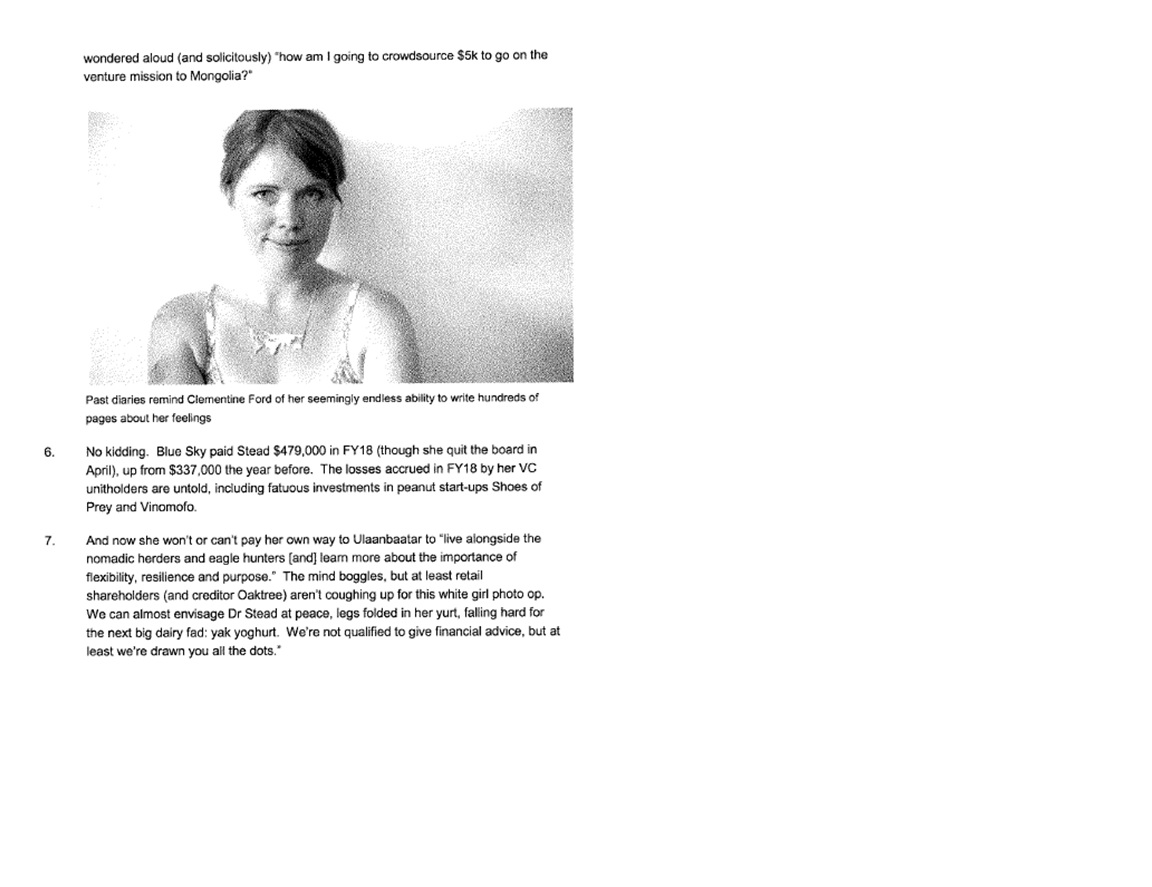

Sixth Alleged Imputation

42 This imputation, that Dr Stead, “a venture capitalist, wantonly lost millions of dollars entrusted to her by unsuspecting investors by channelling their funds into a string of hopeless investments” was the subject of extended debate, much of it focussed on the word “wantonly”.

43 Notably, in relation to the Second Matter, a cognate of the Third Alleged Imputation, which had made reference to Dr Stead acting “recklessly”, was avoided by the pleader.

44 The OED relevantly defines wanton as being: “without regard for right or consequences; in a way that betrays delight in wrongdoing or mischief, wilfully; recklessly; gratuitously”.

45 The Macquarie Dictionary Online relevantly defines wanton as:

adjective 1. done, shown, used, etc., maliciously or unjustifiably: *my father, appalled by the wanton destruction of the bird life he loved, brought in a bill for its protection – MARY DURACK, 1959.

2. deliberate and uncalled for: why ruin your career in this wanton way?

3. reckless or disregardful of right, justice, humanity, etc., as persons.

4. lawless or unbridled with respect to sexual behaviour; loose, lascivious, or lewd.

5. extravagantly luxurious or self-indulgent, as a person, way of life, etc.

…

– noun 9. a wanton or lascivious person, especially a woman.

– verb (i) 10. to act, grow, etc., in a wanton manner.

– verb (t) 11. to squander (away), as in pleasure.

[Middle English wantowen, literally, undisciplined, from wan- not + Old English togen disciplined]

–wantonly, adverb

–wantonness, noun

46 It was put by Dr Stead that wanton meant nothing more than reckless. Given the pleader’s apparently deliberate forensic decision not to use this latter adjective (as has been done in relation to the Second Alleged Imputation), understandably, oral argument revolved around the questions as to whether: (a) an imputation expressed in terms of objective recklessness did not differ in substance to the pleaded meaning; and (b) if it did so, whether it was a variant imputation that could be relied upon.

47 Why the word wantonly was used was never really explained save that it was said (at T449.3–5) “that wantonness carries with it a notion that it’s extensive or out of control which is carried by the references in the article to the burning and the pyromaniac”. But this was an incomplete answer because Dr Stead was explicit that the notion of investments being excessive or out of control could accurately be characterised as being reckless. Of course, the pleading of a meaning is, in the first instance, a matter for the applicant and the adequacy of that pleading cannot be determined by reference to other forensic choices that could have been made. But the consequence, as counsel for Dr Stead, Ms Chrysanthou SC, rightly accepted (at T452.1–2), was that “the term wantonness could give rise to some ambiguity”.

48 This ambiguity created challenges. Of course, in previous times in New South Wales it was not uncommon for the “form” of imputations to be attacked on the basis they were “ambiguous” or lacked sufficient certainty (cf Drummoyne Municipal Council v Australian Broadcasting Corporation (1990) 21 NSWLR 135 (at 137–8 per Gleeson CJ)). But given the real issue as to any alleged form deficiency is always whether there is likely to be confusion either at the pleading stage or at the trial, no strike out application relying on “ambiguity” was made (an entirely understandable and appropriate course since all issues were to be determined in this case by a judge). In any event, despite this admitted ambiguity, one must do the best one can while recognising that the meaning of the imputation must be seen in the entire context of the publication.

49 Without losing sight of the overall task, it is useful to consider initially whether the meaning that Dr Stead “wantonly lost millions of dollars entrusted to her by unsuspecting investors by channelling their funds into a string of hopeless investments” is substantively different to a meaning Senior Counsel for Dr Stead embraced as the pleader’s “intention”: that Dr Stead “recklessly (in the sense of rashly) lost millions of dollars entrusted to her by unsuspecting investors by channelling their funds into a string of hopeless investments”.

50 Despite Dr Stead’s submissions to the contrary, I think these meanings are quite different. Used in context and accompanied by the notion of “channelling”, the concept of Dr Stead operating wantonly is a meaning which conveys some form or aspect of deliberate conduct, not “mere” rashness or stupidity. As I have explained above, I do not consider that the Second Matter, taken as whole, conveys this former charge to the ordinary reader.

51 But this is not the end of the question as to whether a revised version of this imputation inserting a word which conveys objective recklessness or a want of due care can be relied upon. As explained above, whether and to what extent a departure from the pleaded meaning is permitted is to be resolved by considerations of fairness and practical justice.

52 In this regard, as noted above, it is relevant to bear in mind that when an applicant makes a forensic choice to plead a more serious or “higher” meaning than others that are available, a consequence of this forensic choice is to render more difficult the task of a respondent in proving the imputation is substantially true. It is fair to assume that rather than pleading an alternative of recklessness, the pleader chose the word wanton advisedly – and the consequence of this choice of the pleader was that it would (or at least may) be more difficult for truth to be proved in relation to this imputation. Obviously enough, the statutory defence of justification under s 25 of the Act would have required Fairfax and Mr Aston to prove that the imputations carried are substantially true.

53 Let us assume for a moment that I had found the “deliberateness imputations” and the Sixth Alleged Imputation had been conveyed and further assume that Fairfax and Mr Aston had run a justification defence and had proved, inter alia, that Dr Stead had negligently or rashly lost millions of dollars, but failed relevantly to prove that she had lost the money of investors deliberately. In that scenario one can see Senior Counsel for Dr Stead, with her customary skill and vigour, submitting that they had fallen short of the mark, including as to this imputation, because wantonly means more than mere negligence or rashness. For forensic reasons the pleader made a choice (and an understandable choice), but the result was to pitch the imputation too highly. In this regard, in response to a question directed by me, Senior Counsel for Dr Stead fairly conceded (at T466–7) that Fairfax and Mr Aston “may have” taken a different approach to whether or not they maintained the originally pleaded justification defence in respect of a variant of the Sixth Alleged Imputation being “the applicant, a venture capitalist, rashly or negligently lost millions of dollars entrusted to her by unsuspecting investors by channelling their funds into a string of hopeless investments”.

54 The pleaded Sixth Alleged Imputation was not only not conveyed, but considerations of fairness prevent reliance by Dr Stead upon the recast meaning proposed during argument.

Seventh Alleged Imputation

55 The notion of Dr Stead being untrustworthy and failing to deliver upon her promises is clearly conveyed by [7] and [9]. Mr Aston, after all, made plain that the answer to the question of whether Dr Stead “did the right thing” (which, given the context of the additional questions, must go beyond simply taking care of investors and delivering returns) was “no”. Although I have already explained that the heading, which refers to Dr Stead as a “fox”, was a play on words and does not go far enough contextually to impute deceit, it does reinforce a notion that Dr Stead is someone in whom one could not repose confidence. It would be clear to the ordinary reasonable reader that Dr Stead is described as somebody who acts in a way which is not “classy” and is somebody who did not do the right thing, did not take care of shareholders and investors, was not able to return capital in the way that had been hoped and did not make good decisions. It follows that the ordinary reasonable reader would have understood the matter in the way pleaded.

56 I do not consider there is any tension in accepting this imputation was conveyed with my rejection of the Fifth and Sixth Alleged Imputations (which connoted some form of behaviour which went further than objective recklessness or rashness). It must be borne in mind that one is required to consider the response of a non-legally trained audience of readers who were receiving the information in an impressionistic way and, at least in some respects, are prone to a degree of loose thinking.

57 I am satisfied that the imputation that Dr Stead is an untrustworthy venture capitalist who fails to deliver on her promises to shareholders and investors was conveyed.

Eighth Alleged Imputation

58 It is now necessary to turn to the Third Matter and the pleaded imputation is that “Dr Stead is not competent to hold the position of VC fund manager for South Australia because she deliberately and shamelessly lost other people’s money”.

59 The Third Matter has an important difference to the other publications. It is a tweet devoid of any context other than contained in the tweet is the “teaser” link to the Second Internet Matter. The tweet asserts in terms that Dr Stead has “an unenviable record setting fire to other people’s money”. Dr Stead’s submission was that it is difficult to see how the ordinary reasonable reader would not take this assertion as meaning anything other than that Dr Stead deliberately or wantonly destroyed the money. Further, unlike the Second Matter, there is no emollient reference to the fact that Dr Stead might arguably be a good person; nor is there reference to the fact that other venture capitalists did make similar investment decisions initially, but were sufficiently shrewd to have adopted another course when further information became available. Further, immediately juxtaposed to this assertion is the notion that the Premier of South Australia is insisting on imposing Dr Stead on South Australia’s “new VC fund manager”. This is followed by an expletive, the precise terms of which will be conveyed to the ordinary reasonable reader, demonstrating incredulity at the course adopted by the Premier. In this sense the tweet is a crude reduction of similar assertions made in the Second Matter.

60 The position of Fairfax and Mr Aston was that there is nothing in the tweet which suggests that the loss of money was the intended result of Dr Stead’s investments.

61 It is necessary to put out of mind the content of the Second Matter for the purpose of seeking to ascertain the meaning conveyed by the tweet. Considered solely on its own account, on balance, I do not believe it conveys the meaning that Dr Stead deliberately and shamelessly lost other people’s money. The sting of the tweet is obvious and the message is conveyed provocatively. The difficulty is that deliberately and shamelessly losing the money of others is conduct that would be considered by an ordinary reasonable reader as wicked, and not merely irresponsible or stupid conduct. The audience or readership of the tweet, composed of ordinary decent persons, of unexceptional intelligence, experience and education, would consider the tweet as conveying the notion that the Premier was making an inexplicable decision worthy of criticism by insisting on the continuing involvement with the SAVCF of someone said to be incompetent. The Eighth Alleged Imputation is pitched too highly, and given it is the only pleaded meaning of the publication, Dr Stead must fail in this aspect of her case.

B.4 Conclusions as to Meaning

62 It follows from the above, that on 7 December 2020, orders were made recording findings that the following imputations were conveyed:

(1) as to the First Matter, that:

(a) Elaine Stead is a cretin (Imputation 1A);

(b) Elaine Stead rashly destroyed capital causing enormous losses to unitholders (Imputation 1B);

(c) Elaine Stead is a venture capitalist, who made stupid investments in two worthless companies, Shoes of Prey and Vinomofo, which had no prospects of success (Imputation 1C);

(2) as to the Second Matter, that Elaine Stead is an untrustworthy venture capitalist who fails to deliver on her promises to shareholders and investors (Imputation 2).

63 Having found these imputations were conveyed in relation to Dr Stead and they were defamatory, it is necessary to examine the only defence that was pressed: the statutory defence of honest opinion. But before doing so in detail, it is convenient to deal with some aspects of the evidence.

C THE EVIDENCE OF DR STEAD AND MR ASTON GENERALLY

64 It will be necessary below to make specific findings when it comes to considering the defence and the question of damages. But it is well to commence by making some general findings about the credit and aspects of the evidence of the main protagonists, Dr Stead and Mr Aston; and also explain how it is necessary to deal with one aspect of the evidence.

C.1 Dr Stead

65 Dr Stead presented as a witness of the truth. Save for two aspects of her evidence which I will deal with below, I generally found her evidence to be impressive. She was responsive and presented as someone doing her best to give honest answers. Dr Stead obviously (and unsurprisingly) felt the weight of this litigation heavily and her testimony as to her subjective hurt was compelling. I will return to those specific aspects of her evidence when I deal with damages.

66 It is worth commencing by mentioning two (to an extent connected) aspects of Dr Stead’s personal and business life that received a good deal of attention during the course of the evidence. The first was that Dr Stead had been, well prior to 2019, an enthusiastic and, at least in some respects, indiscriminate user of social media. This had caused some disquiet within Blue Sky and some criticism in the AFR. For example, in a Rear Window article written by Mr Aston on 28 May 2018 (“For Blue Sky, plausibility remains illusive”), the following appeared:

Blue Sky’s VC boss Elaine Stead remains the worst (remaining) enemy of the company’s negligible plausibility …

To Future Fund chief executive David Neal’s comments last week that he wanted to put more capital into “global grade” Australian VC managers, Stead tweeted (to the headline, not the words in the article itself, naturally) that “no there’s not” any shortage of local VC capital. Gold, given Neal’s next line, that “it’s not in our interests or the interests of the taxpayer I don’t think for us to be investing in organisations that don’t meet that grade”.

Better still, though, were her thought bubbles on Sunday. “Lowest of lows today,” she admitted at 3:19pm.

“OMFG I just heard the best news but it’s a secret!” she tweeted at 6:54pm, turning on a dime, like a parody of a tween at a slumber party.

The only reassuring part of this unhinged drivel is just how late Blue Sky brings its VC chief into VC deals. Could there yet be financial redemption across the caravan parks of the Sunshine State?

Oh, and then she tweeted: “Yep, pretty sure I’ve lost my passport.”

(Emphasis in original).

67 Devoid of any context (a topic to which I will return), the sending of these tweets does seem unusual conduct for a public company director in the midst of an existential crisis for the company on whose board she sat. Perhaps unsurprisingly, the next day, a shareholder and Ord Minnett investment advisor communicated with Blue Sky’s then interim Chief Executive Officer, Mr Kim Morison in the following terms:

Someone kindly should perhaps take Dr Elaine Stead’s mobile off her to stop tweeting… see below… is this for real?

If this is real…this only damages Blue Sky credibility further… if not, take Mr Aston to court.

Cheers

68 Mr Morison showed Dr Stead this communication (which had been copied to others within both Ord Minnett and Blue Sky) and reprimanded her. Mr Morison then communicated with the shareholder:

Appreciate your concerns. Yes, we’ve done what we need to do. Elaine no longer has a twitter account.

Regards

Kim

69 The disciplining of Dr Stead arising from her tweeting was perceived by her to have been conducted by Mr Morison in “heated” terms and amounted to mistreatment. Indeed, she considered it sufficiently serious to cause her to engage solicitors to provide her with advice. Notwithstanding this, although she gave evidence she considered it was “fair enough” for Blue Sky management to have asked her to stop tweeting, she also said that prior to the meeting with Mr Morison, she believed the media would leave her tweeting alone and not report on it. This was surprising evidence, given that a few weeks earlier, on 7 May 2018, the following insulting comments had been published in a Rear Window article written by Mr Aston entitled “Blue Sky meltdown continues, untruths now official”:

Poor Elaine Stead, Blue Sky’s own Brick Tamlin, sure doesn’t sound happy. “So angry”, she tweeted on Sunday evening, before adding, an hour later, “today sucked dogs (sic) balls.” How fitting that on March 24 she tweeted that “your reputation and integrity is all you have.” Lord knows what she’ll do next – maybe go back and finish primary school?

(Emphasis in original).

70 That Dr Stead apparently held the view there was likely to be a lack of media interest in her tweeting was doubly peculiar given the issue had been previously raised with her by Mr Morison. This can be seen by her reference to a previous discussion in a draft email complaint she composed in relation to her upbraiding (the final version of which was not in evidence). The email records:

Although you did ask me to stay off Twitter until media interest dies down, I assumed that was in relation to Blue Sky related matters. The tweets you raised were personal tweets which were not related to Blue Sky and not inappropriate or unprofessional. I had also assumed the media focus had died down. When I resumed tweeting, it wasn’t to go against your request, it was because I believed it was safe and that the tweets were innocuous and of a personal nature … I had reasonably thought these tweets were not news worthy as they were not work related … However I understand that in the current environment, every piece of information can be twisted negatively by those with an agenda so I have deactivated my account as you have requested.

71 Although I do not go so far as rejecting Dr Stead’s evidence that prior to the meeting with Mr Morison she believed the general media would leave her tweeting alone and not report on it, given the contemporaneous intense media scrutiny of Blue Sky (arising from matters explained below) and her important role within Blue Sky as a public company director, it was, at best, a naïve view for Dr Stead to hold.

72 Before moving on, it is worth tarrying to observe a few matters including the distinction that Dr Stead drew in her complaint between “personal” and “professional” tweets. The supposed division raises interesting questions. What actually is personal in this context? To those of an age and cast of mind who have not embraced social media, the demarcation between what is private and public may be quite different to those more attuned to the contemporary zeitgeist. Speaking generally, to those accustomed to restricting one’s private musings to family and a circle of close friends, the inclination and apparent readiness of social media users to “share” their feelings and their views on everything from fascism to fish fingers seems decidedly odd. For some on social media, emoting or the recounting the mundane often seems to co-exist with commentary on issues of public significance or discussion of professional matters of moment. But to be too quick to stigmatise a tweet as banal is to fail to recognise that often seems the point of the exercise. Those forming the community of social media users, or a sub-set of them, might have quite a different conception from others as to what is noteworthy or inappropriate, silly, or even risible. Mr Aston was emphatic in denouncing what he perceived to be Dr Stead’s asinine posts, but anyone wishing to glance though the evidence of his tweets on foot massages or milkshakes might rationally form the view that they were without redeeming social importance.

73 Three points worth noting emerge from this: first, the context of a post on social media is important (which, as a habitué, Mr Aston would readily understand); secondly, it is unrealistic to assume that a mundane post by a newsworthy figure would necessarily stay within a community of social media users (something which Dr Stead should have understood); and thirdly, connected to the last point, given the nature of social media, characterising any post as being “private”, if made by a person who has a role of public interest, is problematical.

74 The notion of context is important when one considers the second aspect of Dr Stead’s evidence to which significant attention was directed: her connexion to, and communication with, her peers.

75 Dr Stead describes herself as a “Venture Capitalist”. She and her colleagues repeatedly referred in their evidence to being part of an “ecosystem”. This was not a reference to an ecosystem in the conventional sense, but rather, a buzzword used to describe the “open environment” where professionals with similar and different skills work collaboratively to assist one another in “raising new companies”. Dr Stead was evidently an enthusiastic participant in the “ecosystem”: she explained she was “a subscriber to the concept of ‘give first’” and that she “believe[s] wholeheartedly in being that person for others in our ecosystem”; she did this by “volunteering my time and expertise to mentoring entrepreneurs and start-ups”. Reciprocally, the evidence suggests her fellow participants within the “ecosystem” were a source of support to her. Part of this support and community, according to a fellow enthusiast and friend, Ms Monica Bradley (an investment advisor and company director), involved interactions on Twitter. Ms Bradley explained “all of us in the ecosystem, Australia wide, follow each other on Twitter”. When asked why, she responded:

I think it’s the nature of the Twitter technology, is the following kind of constitutes people of interest or what we would have called in the old days, communities of practice. So numbers of us follow each other, and that way then we share observations, learnings, information. But you know, I have – and everyone has very different interest groups. The ecosystem is one of mine, but I also have, you know, other people I follow on equality, or women’s rights or the Eurocarbon community. So I follow a variety of people, but ecosystem communicates a lot via Twitter, and direct messages on Twitter.

76 Like many other communities of like-minded individuals, it is apparent from the evidence that those within the “ecosystem” communicated in a singular way that was apparently understood and appreciated by those within this so-called “community of practice”. A good example has an especial relevance to this case, being a flyer from the Queensland Office of the Chief Entrepreneur’s so-called “Adventurer-in-Residence”, who entreated those “active in the Queensland entrepreneurial ecosystem” who wished to “improve their physical resilience and mental stamina” to travel to Mongolia to:

… summit a challenging local Khentii Mountain and learn about nomadic life - with interviews and hands-on experience with local families, along with progressing through introspective strategy and leadership workshops, all facilitated by The Nomadic School of Business team.

We will focus our immersion around the concepts of clarity, purpose and agility. Taking inspiration from our surroundings and the nomadic families we meet, the team will be guided through reflection on their own territory and season, the purpose of their team and organisation, and the qualities of agility needed to be truly responsive to your environment. We aim to help attendees see the world and themselves in a completely different way. We will also be meeting local entrepreneurs and Australians and other businessmen and women based in Ulaanbaatar.

77 To an outsider to the “ecosystem” and its interactions on social media, the public expression of private ruminations and the sometimes cloying expressions of support and mutual regard might seem easy to mock; but, as explained above, when considering the content and tone of Dr Stead’s social media posts, it is necessary to bear in mind the context of the communications: they are thoughts primarily shared with persons likely to have a similar “mind-set”.

78 From before her reprimand, Dr Stead had a “private” Twitter account. Mr Aston was aware of this from April 2018 when he received a message (“Elaine has gone private on Twitter! Say it ain’t so!!”: Ex 1, p 2990). But, as noted above, the label “private” is apt to mislead: the posts were still available to be viewed by her many “followers” (numbering about 5,000). Unlike Twitter, Dr Stead’s Instagram account had never been available to the general public; she gave thought to whom she “accepted” on Instagram and indeed Mr Aston’s request to follow her was rejected in April 2018. But it could hardly be said that the 500 to 600 followers she had on this medium amounted to a circle of intimacy.

79 As noted above, when the extent of her social media cohort is borne in mind, notwithstanding Dr Stead was directing her communications to the “ecosystem”, it must have been apparent by at least mid-May 2018, that her social media comments may, given the public interest in the travails of Blue Sky, be decontextualised and be the subject of critical media interest and comment. Indeed, as the extract from her complaint to Mr Morison belatedly recognised, in an environment where Blue Sky was the subject of focus, “every piece of information can be twisted negatively by those with an agenda”.

80 The reason why Dr Stead’s comments were likely to be of public interest leads me to an aspect of her evidence which did cause me concern, that is, the evidence relating to her activity as a director of Blue Sky. To explain why, it is necessary to go into a little detail.

81 Dr Stead originally joined Blue Sky as the Head of Venture Capital. Blue Sky was a listed alternative asset manager (ASX: BLA) operating as a holding company for fund managers that invested in four alternative asset classes: private equity and venture capital, real estate, hedge funds and agriculture and resources. Between September 2016 and April 2018, Dr Stead was a director of Blue Sky (although she continued as a senior executive until her employment ended on 30 September 2019). Regrettably, in the submissions of both parties there was a repeated tendency to elide distinctions between: (a) Blue Sky the listed entity; (b) Blue Sky Venture Capital, which was not a legal entity, and which was described in the Agreed Background Facts (ABF) as a “division of Blue Sky”, of which Dr Stead was “Investment Director” (defined as “BSVC”: ABF at [7]; Ex 2, p 383); (c) the entity BSVC Pty Ltd, in respect of which Dr Stead was apparently appointed an executive director in July 2013 (ABF at [9]); and (d) the entity Blue Sky Private Equity Pty Ltd (BSPE). BSPE was a wholly owned subsidiary of Blue Sky and operated as an investment manager.

82 The listed entity Blue Sky was, at one time, perceived by many participants in equity markets to be a spectacular success. By the first half of FY2014, revenue had reached $8.15 million with the company projecting more than $500 million in assets under management (AUM) by the end of that financial year. The details of further growth do not need recounting; it suffices to note that a succession of further capital raisings took place to fuel an ambitious and expansive investment strategy.

83 By contemporary accounts, many seemed to think the strategy had worked. In June 2017, an article was published written by Mr Anthony Boyd, of the AFR’s “Chanticleer” column. The column is prominent; indeed it self identifies as “Australia’s pre-eminent business column”. Among other things, the article (“Blue Sky Alternatives CEO Rob Stand fights back”) reported:

There is no better example of the surge in interest in alternative assets than Blue Sky Alternatives, a Brisbane manager which has shot the lights out for the past five years. This week it revealed that its total funds under management had hit $3 billion, which is up about $1 billion from a year ago. It lifted its funds under management by about $1 billion in the previous year.

Blue Sky has about $1 billion in private equity, $1 billion in real estate and about $1 billion in water and agriculture. It has a small amount in hedge funds.

Blue Sky is well on the way to meeting its target of having $10 billion in funds under management and being the home-grown version of Wall Street alternative asset giants Blackstone and KKR.

Any company with the words Blue Sky in its name will have its fair share of sceptics …

There is no suggestion that Blue Sky Alternatives has any [‘speccy’] features in its operations. First, it is not involved in mining. Second, its accounts are audited by respected firms and, third, its board includes respected Queensland business people.

But it has had its fair share of sceptics. In October and November last year, the short interest in the stock was equal to about 3.5 per cent of the issued capital.

Also, over the years Blue Sky has come under attack from bloggers and analysts claiming it is too reliant on asset revaluations and that its investment vehicles carry too much debt.

Chanticleer believes there is an element of the tall poppy syndrome wrapped up in the negativity towards Blue Sky. Many of the rumours have been proven to be wrong.

Chief executive Rob Shand is happy to deal with all the criticisms head-on. His arguments are quite persuasive, as shown by the fact that the level of institutional investment in Blue Sky’s range of funds has jumped from zero five years ago to 37 per cent in 2016.

In response to the claim that returns are driven by unrealistic valuations of assets, Shand says that 28 of the 31 asset realisations made by Blue Sky since 2006 have been at valuations higher than book value. He says this shows an inherent conservatism in the accounting for the value of assets.

In response to claims that valuations are too easily pumped up, Shand says each asset must go through four separate sets of eyes. It starts with KPMG as valuer, then EY as auditor, then the board of the fund and then the board of the head stock, Blue Sky Alternatives.

…

(Emphasis added).

84 There are a number of reasons why this article was significant. First (and perhaps explaining why there was some short interest in Blue Sky shares) was that aspects of the business of Blue Sky were opaque; it had apparently not provided, by way of periodic or continuous disclosure, either a breakdown between gross AUM and fee earning AUM, nor a breakdown as between various asset classes. Secondly, as a consequence, the communication of an aspect of this information (that Blue Sky “has about $1 billion in [the] private equity” asset class) in a prominent article, was arguably information of some moment. Thirdly, given its apparent source and publication in the AFR, it was information likely to come to the attention of investors or potential investors. Fourthly, it was information which might arguably be thought to be of significance to those investing, including in the VC funds (leaving aside anything else, it may matter to a potential investor in a venture capital fund to understand the quantum of total private equity assets under management, as compared to say, the real estate assets or agriculture and resources assets – even though they all may be generating upstream fee income).

85 Dr Stead gave evidence she was not happy about the article because “it was incorrect”; indeed, she believed it was an inaccurate estimate of AUM for any of the business units. The following evidence was then given:

MR DAWSON: It would be a bit of a worry, wouldn’t it, Dr Stead, if the financial world reading the [AFR] thought that that was the official company position when it wasn’t?---Yes.

Didn’t you think it was important to correct it if the company disagreed with it?---It was difficult to correct if we can’t actually say the number for each of the assets under management.

HIS HONOUR: Why couldn’t you say the number?---We had never disclosed the individual assets under management for each of our business units individually. We had only ever talked about it in its totality.

But that was a commercial decision - - -?---Yes.

- - - that was made?---Yes.

So up until the time … the information that the company had concerning the amount it had in private equity was information that was not generally available to the market?---Yes.

…

Did it concern you that given that in June [2017] it was – it had been conveyed inaccurately that Blue Sky had about 1 billion in private equity, that it may be appropriate for the communication to be made to the market to make it clear that the true position concerning the assets held in private equity were lower?---So the question was did it concern us, and the answer is yes.

Yes?---And there was much discussion about what to do, if anything.

Yes?---The consensus from the board in the end was to maintain our position, which was to not disclose assets under management by asset class, and because he hadn’t said anything materially different to what we had disclosed in totality of about three billion under management the decision was made to just let it go.

…

MR DAWSON: If Mr Shand was responsible for the breakdown in that Financial Review article I showed you, namely one billion in private equity, et cetera, if he had told the Australian Financial Review that it follows from what you’re saying that Mr Shand would have been misrepresenting the position, doesn’t it?---Yes.

And did you take up with Mr Shand as a director of Blue Sky the fact that this was inaccurate and information going into the public domain that was wrong? ---Yes.

Right. And your evidence is that there was a discussion at board level, was there, to let it lie?---Yes.

86 A curious aspect of this case is that although the business and ultimate demise of Blue Sky was the subject of voluminous evidence, according to the parties (as recorded in a document filed in advance of the trial), the limited factual findings that need to be made as to the underlying business of Blue Sky (and its failure) are related to the substantial truth of aspects of the alleged proper material relied upon by Mr Aston.

87 Consistently with this, in support of a submission that Fairfax and Mr Aston had failed to prove that Dr Stead had a “poor track record”, the following was said on behalf of Dr Stead:

The issue of why Blue Sky collapsed is not relevant to the facts in issue in this proceeding but … the March-April 2018 short-seller attack and related media coverage, including by Mr Aston and the AFR, affected the fundamentals of Blue Sky shortly thereafter.

88 The “attack” to which Dr Stead was referring was a report on Blue Sky by Glaucus Research Group California LLC (Glaucus), an activist short seller based in the United States, published on 28 March 2018 (Glaucus Report). The Glaucus Report was damning as to a range of matters, including the lack of transparency of Blue Sky. Dr Stead left the board shortly thereafter, but it was common ground that this was about redressing a deficiency of non-executive directors and had nothing to do with: (a) the publication of the Glaucus Report; (b) Blue Sky’s attempted rebuttal of it; nor (c) any disagreement she had with the Board as to inaccurate AUM information being in the public domain.

89 Just as it is beyond the scope of this case to make findings as to why Blue Sky collapsed or the accuracy of the Glaucus Report, given the way the case is pleaded, it is also beyond my role to make findings as to the legal or moral appropriateness of Dr Stead and the other directors letting misleading information as to the extent of fee earning AUM, and the breakdown of AUM as between various asset classes, to be left unaddressed – notwithstanding people were investing in funds managed by Blue Sky and were buying the listed entity’s shares.

90 During the course of the trial, at times, it seemed to be suggested that the failure of Blue Sky could be simply put down to the publication of the Glaucus Report and the consequent loss of investor confidence fuelled by the media (although, as noted above, Dr Stead’s evidence was somewhat more nuanced on close examination). In her evidence in chief, Dr Stead was highly critical of Glaucus in noting:

By publishing what I believe to be biased opinions in [the Glaucus Report] that are not based on facts, Glaucus’ aim was to panic Blue Sky investors and destroy their confidence in the company with a view to driving its share price down and exploiting the fall in the share price to make a significant profit. By doing so, it significantly improved its odds of being able to sell Blue Sky shares at a high price and buy at a low price …

I also believe Glaucus relies on the media to achieve its aim.

91 But when addressing why Blue Sky failed, in an article she wrote published on the website SmartCompany on 31 October 2019 (“The mainstream media sneers at success and revels in failure – and it feeds a culture of mediocrity”), to which she was taken in cross-examination, Dr Stead gave a somewhat more comprehensive response than simply blaming short sellers. She identified three main reasons for the debacle being:

[o]ur growth rate prior to the attack, combined with an activist short seller attack which was false, misleading and deceptive, and the board’s mistakes in the wake of the attack. I wear part responsibility for at least one of these reasons.

92 Dr Stead did not resile from this statement in cross-examination, and confirmed that the reason for which she wore “part responsibility” was the company’s growth rate. But to the extent it is relevant to credit, even this somewhat more complete account seems likely to miss the mark. Dr Stead accepted that Blue Sky’s shares traded efficiently. The so-called “efficient market hypothesis” in its “pure” (or even “semi-strong”) form has its persuasive critics, and no doubt distortions from fair market value can be caused by short sellers for a period (such as “short and distort” participants), but in the present case, Blue Sky ultimately responded to the Glaucus Report by placing further information into the market. Even assuming the Glaucus Report was inaccurate in material respects, ultimately one would expect investors acting rationally to have placed a fair value on Blue Sky shares based on the present value of projected future cash flows. The apparent problem for Blue Sky was that when additional information was revealed, the value placed by the market on the stock was very different than the heady days before, and immediately after, the “Chanticleer” column.

93 At this point it is convenient to identify and dismiss a submission made by Dr Stead connected to the activities of short sellers. It was suggested that it was somehow “improper” for Mr Aston to rely on information provided to him by anyone with a short position in Blue Sky. Speaking generally, market participants with long positions can be as biased as those holding short positions. Their perspective is different, but each perspective may be valid, provided one appreciates the respective partialities. It is unnecessary to go into the details, but it has been compellingly argued by financial economists that constraints on short selling can slow the dissemination of information into the market which, by impeding timely price responses to new information, undermines market efficiency. Leaving aside short term distortions, if the share price is seen as an equilibrium or fair value arrived at by all market participants, to exclude short sellers can systematically reduce the amount of information which should be reflected in the fair value share price. To submit, as Dr Stead did, that Mr Aston could not rely on any source or information to the degree he did, simply because it came or originated from a short seller is, with respect, jejune and I reject the notion that a journalist like Mr Aston was somehow obliged to ignore their views of the company or its officers in an a priori fashion.

94 The final matter to which preliminary comment should be made relates to the context of Dr Stead’s social media posts and, in particular, the context of one Instagram post that followed on from the efforts of the Chief Entrepreneur’s “Adventurer-in-Residence” to have members of Queensland entrepreneurial ecosystem gain “clarity” and “agility” by undergoing “immersion” in Mongolian nomadic life.

95 I referred earlier to the support Dr Stead perceived she received from those within her “community of practice”. Following the release of the Glaucus Report, which was discussed widely in the “ecosystem”, she attended a function and thereafter posted to Instagram a photo of herself with Ms Bradley, in which post she observed that Ms Bradley was a support to her, and explained:

When the chips were down, I was overwhelmed with love support and community. This woman is one of the awesome peeps [scil. people] in the Queensland ecosystem who has been a staunch sister.

96 She then went on to say that:

Along with many other sisters and brothers, many of whom I had the joy to see again tonight. You all know who you are. Thank you.

Now, given I’m currently broke, how am I going to crowd source $5k to go on the venture mission to Mongolia?

(Emphasis added).

97 As to the emphasised paragraph of her post, it was said by Fairfax and Mr Aston that Dr Stead did not give any direct evidence that this part of the post was a joke, despite having opportunities to do so. Moreover, the comments on the post in evidence do not appear to indicate that that was how it was understood by the two followers who responded to it (in fact they take issue with the fact that she referred to herself as “broke”) (Ex 1, p 3893). It followed, it was contended, the Court ought to be slow to conclude the emphasised remark was a joke.

98 But to the extent subjective intentions are actually relevant, it was made plain on behalf of Dr Stead throughout the case that this aspect of the post was not to be taken literally. This was put to Mr Aston (no doubt on instructions), and was asserted to be patent from any fair reading. I have little doubt, given the context of the post, that by her last paragraph Dr Stead was attempting to be light-hearted and was speaking in a jocular way to persons she considered colleagues and fellow enthusiasts of such “bonding” sessions. This was someone primarily conversing with “peeps” she considered her “brothers” and “sisters” in an emotional way. The joke might be perceived by some as being self-indulgent or injudicious (given that investors in Blue Sky and the funds she had managed had suffered financially), and two people may have taken issue with any assertion she was broke, but any want of tact did not mean this aspect of the post was not an attempt at levity. It follows, contrary to the complexion Mr Aston put on the post, I do not accept that Dr Stead’s post was an exercise in panhandling by a cadger trying to procure a free trip to East Asia.

C.2 Mr Aston

99 Mr Aston was an intelligent, self-possessed witness who sparred effectively with his cross-examiner.

100 Without objection, and without any limitation on its use, a 50-minute video went into evidence (Ex D) recording Mr Aston (together with two other journalists) being interviewed and taking questions at the Melbourne Press Club. It was both instructive and revealing. It provided a candid account of how Mr Aston regards his role, how he perceives his “inside Baseball” readership (at 30:20), and his modus operandi generally, including how he sometimes will (at 18:07):

… bite off a really big story and pursue it for months and months and stay on it and I think it’s important to do that, to own something and to pursue it to its ungainly end.

101 It is also evident that Mr Aston is conscious of the power of his position. In answer to a question posed by the interviewer (at 26:35) to identify someone the interviewees most enjoyed “tweaking, attacking or having fun with, just for the sheer and utter sport”, Mr Aston explained (at 29:22) he had “a lot of fun” with Mr Eddie McGuire, a prominent Melbourne identity. After telling a story, which he repeated in the witness box, about being “shirtfronted” by the Collingwood Football Club President in a corporate tent on Derby Day, he remarked that this was an “unwise decision” of Mr McGuire because “I’m the one with the column inches” (at 30:06).

102 Mr Aston also described how he perceived that Mr McGuire, by his actions, served him up a “slow full toss every time” (at 31:33). He later made another point about “how do you manage someone when they’re coming after you” (at 42:59), explaining that there are people “I went after” who confronted him but, by way of contrast, there are other persons who have reacted well and have since become sources or professional friends (at 43:39). He then explained (at 43:46):

… there are many slow deaths that have occurred on the page because people, through pride, or arrogance or wrongheadedness or whatever have chosen the former rather than the latter.

103 When cross-examined about this last comment, he dismissed its present relevance because Dr Stead never rang up and abused or confronted him. But the comment does seem to me to be material. Dr Stead did not act as some others had done, those “hail-fellow-well-met” types Mr Aston apparently considered good sports and who offered to take him out to lunch and tell a few yarns. When it was put to Mr Aston that his intention in relation to Dr Stead was to make her reputation suffer a “slow death”, and that she continued to defend her conduct at Blue Sky, he responded (T574.32–8):

Well, she continued to claim that Blue Sky collapsed through no wrongdoing of its own or through no fault of its own.

… I think her refusal to accept reality of what happened caused me … great surprise and it was … certainly a big part of what made me wonder what was going on in her head.

104 For reasons I will explain further below, Dr Stead was a target Mr Aston determined to “go after” because he perceived she was not taking responsibility for her alleged failures at Blue Sky and because of her insouciance, as he saw it, to the losses suffered by investors. The consequence of Dr Stead being targeted was that she did suffer a type of “slow death” as a consequence.