Federal Court of Australia

Xplore Wealth Limited, in the matter of Xplore Wealth Limited [2020] FCA 1868

ORDERS

XPLORE WEALTH LIMITED ACN 128 316 441 Plaintiff | ||

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 411(1) and s 1319 of the Corporations Act 2001 (Cth) (Act), the plaintiff convene and hold:

(a) a meeting of its shareholders (Share Scheme Meeting) for the purpose of considering and, if thought fit, agreeing (with or without modification) to a scheme of arrangement (Share Scheme) proposed between the plaintiff and its shareholders (Scheme Shareholders), being the scheme substantially in the form contained at Annexure A to these Orders; and

(b) a meeting of its optionholders (Option Scheme Meeting) for the purpose of considering and, if thought fit, agreeing (with or without modification) to a scheme of arrangement (Option Scheme) proposed between the plaintiff and its optionholders (Scheme Optionholders), being the scheme substantially in the form contained at Annexure B to these Orders,

(together, the Scheme Meetings).

2. The Share Scheme Meeting be held on 12 February 2021, commencing at 10 am (Sydney time), and the Option Scheme Meeting be held on 12 February 2021, commencing at 11 am (Sydney time), to be conducted electronically through an online platform (which is to be accessed in accordance with the instructions included in the Scheme Booklet substantially in the form of Annexure DS-1 to the Affidavit of Donald Sharp sworn on 17 December 2020, and as modified in paragraphs 4.1(c) at page 37, and paragraph 7.2 at page 69 as indicated during the first court hearing on 18 December 2020 (Scheme Booklet) and the notices of meeting to be sent to shareholders and optionholders in accordance with Orders 3 and 4 below).

3. The Share Scheme Meeting be convened by sending on or before 12 January 2021:

(a) an email to each Scheme Shareholder who has nominated an electronic address for the purpose of receiving notices of meeting and proxy forms from the plaintiff (Email Shareholder) (or, in the case of joint holders, to the holder whose name appears first in the plaintiff’s register) which contains:

(i) an electronic copy of the Scheme Booklet (which contains among other things the proposed Share Scheme at Annexure D and Notice of Share Scheme Meeting at Annexure H);

(ii) an electronic copy of a personalised proxy/voting form for the Share Scheme Meeting; and

(iii) an electronic link to the online portal or website that is accessible by the Email Shareholder and which enables the Email Shareholder to lodge their proxy form for the Share Scheme Meeting and voting instructions online.

(b) by post to each Scheme Shareholder who is not an Email Shareholder (or, in the case of joint holders, to the holder whose name appears first in the plaintiff's register):

(i) a postcard setting out the electronic address to a website containing a copy of the Scheme Booklet;

(ii) a hard copy personalised proxy/voting form for the Share Scheme Meeting;

(iii) a reply-paid envelope for the return of completed proxy forms;

(iv) a hard copy election form (in respect of the Share Scheme Consideration election that is to be made by entitled Scheme Shareholders); and

(v) a separate reply-paid envelope for the return of the election form.

4. The Option Scheme Meeting be convened by sending on or before 12 January 2021:

(a) an email to each Scheme Optionholder who has nominated an electronic address for the purpose of receiving notices of meeting and proxy forms from the plaintiff (Email Optionholder) (or, in the case of joint holders, to the holder whose name appears first in the plaintiff’s register) which contains:

(i) an electronic copy of the Scheme Booklet (which contains among other things the proposed Option Scheme at Annexure E and Notice of Option Scheme Meeting at Annexure I); and

(ii) an electronic link to the online portal or website that is accessible by the Email Optionholder and which enables the Email Optionholder to lodge their proxy form for the Option Scheme Meeting and voting instructions online;

(b) by post to each Scheme Optionholder who is not an Email Optionholder (or, in the case of joint holders, to the holder whose name appears first in the plaintiff's register):

(i) a postcard setting out the electronic address to a website containing a copy of the Scheme Booklet;

(ii) a hard copy personalised proxy/voting form for the Option Scheme Meeting; and

(iii) a reply-paid envelope for the return of completed proxy forms.

5. The documents referred to in Orders 3(b) and 4(b) be sent:

(a) in the case of Scheme Shareholders and Scheme Optionholders whose registered address is within Australia, by prepaid ordinary post addressed to the relevant addresses recorded in the plaintiff’s register; and

(b) in the case of Scheme Shareholders and Scheme Optionholders whose registered address is outside Australia, by airmail or international courier service addressed to the relevant addresses recorded in the plaintiff’s register.

6. If the plaintiff receives an automatic, system generated notification that the documents were unable to be delivered to the nominated electronic address of any Scheme Shareholder or Scheme Optionholder to whom scheme documents were dispatched in accordance with orders 3(a) and 4(a) (Undelivered Email Recipients), the documents be dispatched by the plaintiff to Undelivered Email Recipients in accordance with Orders 3(b), 4(b) and 5.

7. Except to the extent addressed by these Orders, the Share Scheme Meeting and Option Scheme Meeting be:

(a) convened, held and conducted in accordance with the Corporations (Coronavirus Economic Response) Determination (No 3) 2020 (Cth) (Determination) and subject thereto, the provisions of Pt 2G.2 of the Act that apply to members of the company, and the provisions of the plaintiff’s Constitution that are not inconsistent with these Orders, the Determination and Pt 2G.2; and

(b) convened, held and conducted as if r 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) (Rules) does not apply.

8. Voting on the resolutions to approve the Share Scheme and the Option Scheme is to be conducted by way of poll.

9. A proxy form, appointment of a corporate representative, or power of attorney to act on behalf of the relevant Scheme Shareholder or Scheme Optionholder in respect of the Share Scheme Meeting and the Option Scheme Meeting respectively will be valid and effective if, and only if, it is completed and delivered in accordance with its terms and these Orders by 10 am 10 February 2021.

10. Alexander Hutchison, or failing him Donald Sharp, be Chair of the Scheme Meetings.

11. The Chair of the Scheme Meetings shall have the power to adjourn the meeting to such time, date and place he considers appropriate.

12. Compliance with r 3.4 and Form 6 of the Rules is dispensed with.

13. The plaintiff publish a notice of hearing in The Australian newspaper, in substantially the form that appears at Annexure C to these Orders, not later than five days prior to the date fixed for hearing of any application to approve the Share Scheme and the Option Scheme.

14. The originating process is adjourned for hearing before Markovic J on 18 February 2021 at 10.15 am (Sydney Time).

15. There be liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MARKOVIC J:

1 On 18 December 2020 I made orders pursuant to s 411(1) and s 1319 of the Corporations Act 2001 (Cth) (Act) convening:

(1) a meeting of Xplore Wealth Limited’s (Xplore Wealth) ordinary shareholders for the purpose of considering and, if thought fit, agreeing to a scheme of arrangement (Share Scheme) proposed between Xplore Wealth and its shareholders (Scheme Shareholders); and

(2) a meeting of Xplore Wealth’s optionholders for the purpose of considering and, if thought fit, agreeing to a scheme of arrangement (Option Scheme) proposed between Xplore Wealth and its optionholders (Scheme Optionholders).

2 These are my reasons for making those orders.

Background

3 Xplore Wealth is an Australian public company limited by shares and admitted to the list of the Australian Securities Exchange (ASX). It is in the business of providing wealth management platform services and generates revenue through three primary market offerings: retail investment platforms, institutional/wholesale platform services and a superannuation offering.

4 On 28 October 2020 Xplore Wealth announced to the market that it had entered into a binding scheme implementation agreement (SIA) with HUB24 Limited (HUB24) which proposed the Share Scheme and the Option Scheme (collectively, the Schemes) and pursuant to which it is proposed that HUB24 will acquire Xplore Wealth.

5 On 28 October 2020 prior to the announcement in relation to the Schemes, Xplore Wealth had a market capitalisation of approximately $20 million.

6 HUB24 is an Australian public company which was incorporated on 13 April 2007 and has been listed on the ASX since 5 July 2007. It is in the business of providing investment and superannuation platform services, including wealth management solutions, to the financial services industry. HUB24 has a market capitalisation of approximately $1.3 billion.

Share Scheme

7 If the Share Scheme is approved and implemented, all of the issued shares (Scheme Shares) in Xplore Wealth as at the scheme record date, being 23 February 2021, will be transferred to HUB24, Xplore Wealth will be delisted from the ASX and it will become a wholly owned subsidiary of HUB24.

8 Each Scheme Shareholder can elect to receive consideration for their shares in one of two forms: either cash consideration in the amount of $0.20 per Xplore Wealth share (Cash Consideration); or scrip consideration in the amount of 0.00926746 of HUB24 shares per Xplore Wealth share (Scrip Consideration) (collectively, Share Scheme Consideration). If no election is made by a Scheme Shareholder as to the preferred form of Share Scheme Consideration, that shareholder will receive the “Default Consideration”, namely 50% Cash Consideration and 50% Scrip Consideration.

9 Scheme Shareholders whose address in the share register is located outside of Australia or New Zealand (Foreign Scheme Shareholders) may only receive Cash Consideration. Similarly, Scheme Shareholders who are only entitled to less than a marketable parcel of HUB24 shares (being equal to a value of less than $500 under the Share Scheme) (Small Shareholders) may only receive Cash Consideration, regardless of whether or not they make an election.

10 There is an aggregate cap of Cash Consideration of $36 million and an aggregate cap of Scrip Consideration of $30 million worth of HUB24 shares. If the Scheme Shareholders elect to receive Cash Consideration or Scrip Consideration that exceeds those aggregate caps, then a scale-back mechanism will apply. Where Cash Consideration is scaled back, the shortfall will be made up of Scrip Consideration and vice versa.

11 The Share Scheme is not contingent on approval of the Option Scheme. If the Share Scheme is approved and the Option Scheme is not, then the Share Scheme will proceed. However, the Option Scheme will not.

Option Scheme

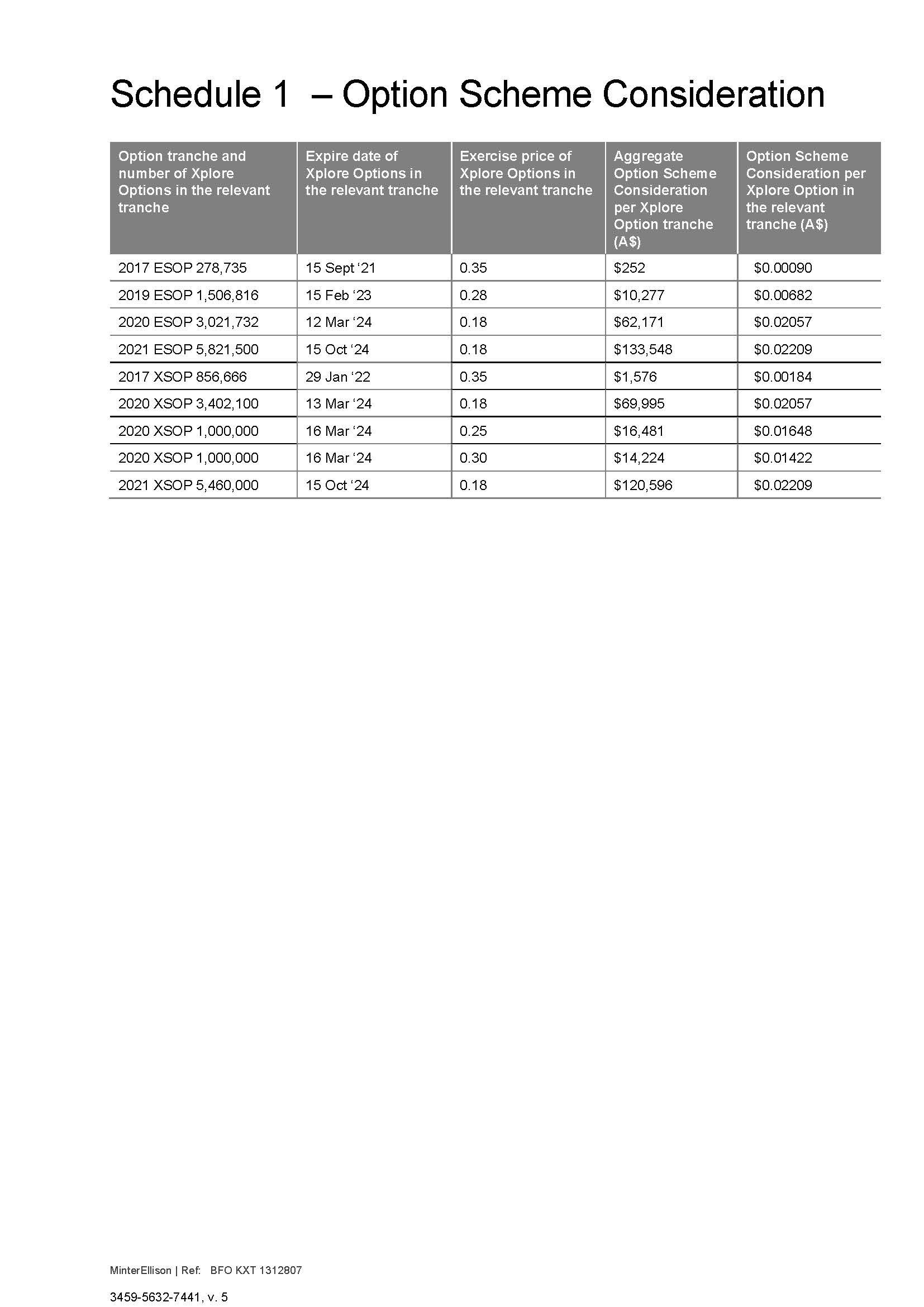

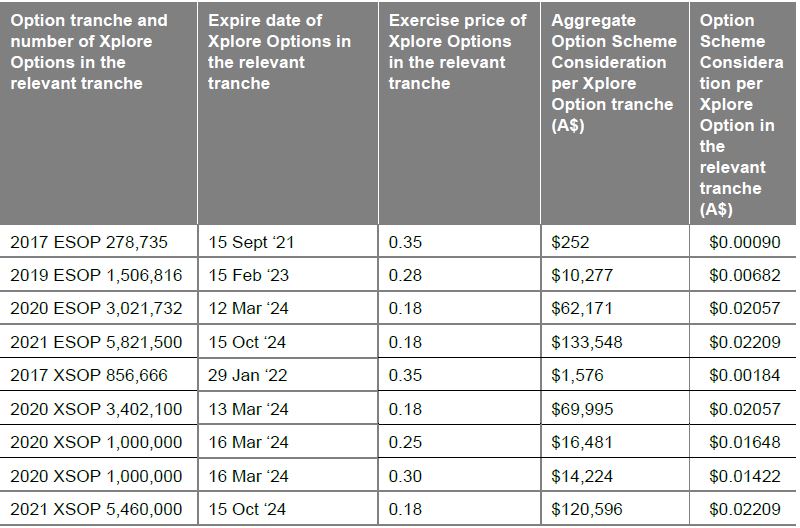

12 Xplore Wealth has issued 22,103,549 options under an employee share option plan (ESOP) and an executive share option plan (XSOP). There are approximately 83 optionholders. The options issued by Xplore Wealth were issued in tranches pursuant to the ESOP and XSOP.

13 Under the Option Scheme, persons holding options (Scheme Options) as at the scheme record date, being 23 February 2021, will have their options cancelled and will be paid consideration in the following amounts:

14 The Option Scheme is contingent on the Share Scheme being approved. If the Share Scheme is not approved, then the Option Scheme will not proceed and optionholders will continue to hold their shares and options respectively.

15 If the Share Scheme is approved and the Option Scheme is not approved, then the Option Scheme will not proceed. In those circumstances, the options held by optionholders will lapse unless they are exercised within one month of the “Implementation Date” (as defined) of the Share Scheme. Where the options are exercised, the resulting shares may be compulsorily acquired by HUB24 pursuant to Pt 6A.2 of the Act because HUB24 will hold more than 90% of the securities in Xplore Wealth.

Independent expert’s report

16 The directors of Xplore Wealth retained Leadenhall Corporate Advisory Pty Ltd (LCA) to provide an independent expert’s report (IER) in respect of the Schemes.

17 LCA has reached the following conclusions:

(1) the Share Scheme is fair and reasonable and it is in the best interests of shareholders; and

(2) the Option Scheme is not fair but is reasonable and it is in the best interests of optionholders.

18 The advantages and disadvantages for Scheme Shareholders referred to by LCA are as follows:

Advantages

The main advantages of the Proposed Transaction are:

• Share price: In the absence of the Proposed Transaction it is likely that the Xplore Wealth share price will fall below its recent trading range.

• Control premium: The Proposed Transaction offers a control premium of between 146% and 196% compared to the one-week VWAP for Xplore Wealth prior to its announcement. This is at the higher end of generally observed control premiums.

• Retained exposure to the sector: The scrip component of the Proposed Consideration allows for Xplore Wealth shareholders to retain exposure to the sector if they wish to do so.

• No superior alternative: We are not aware of any superior alternative proposals for Xplore Wealth.

Disadvantages

The main disadvantages of the Proposed Transaction are:

• Loss of upside: If Xplore Wealth is able to implement its strategy it is likely that its share price will increase. By accepting the Proposed Transaction Shareholders will have reduced exposure to this upside.

• Tax implications: The acceptance of the Proposed Transaction may result in tax leakage for shareholders that could otherwise be deferred.

19 Insofar as the Option Scheme is concerned, LCA concluded that it is not fair because the consideration being offered to the Scheme Optionholders for their options is less than its assessment of the value of those options. However, LCA concluded that the Option Scheme is nonetheless reasonable for the following reasons:

The advantages and disadvantages to Optionholders are similar to those listed above for Shareholders. However, an additional consideration for Optionholders is that if the share scheme is approved but the option scheme is not, Optionholders will have a one month window to exercise their options, otherwise the options will lapse. The shares that would be issued upon conversion of the options could then be compulsorily acquired by HUB24, therefore losing their time value. Compulsory acquisition at the offer price of $0.20 would lead to Optionholders receiving approximately $354,000 (net of the exercise price) as opposed to the proposed consideration under the option scheme of $429,000 as presented above. For this reason, we consider the Proposed Transaction is reasonable to Optionholders.

Directors’ recommendation

20 The board of Xplore Wealth unanimously recommends, in the absence of a superior proposal and subject to LCA continuing to conclude that the Share Scheme is in the best interests of shareholders and the Option Scheme is in the best interest of optionholders, that shareholders vote in favour of the Share Scheme and optionholders vote in favour of the Option Scheme. On the same basis, each director of Xplore Wealth intends to vote, or procure the voting of, any Scheme Shares and Scheme Options in which he or she has a relevant interest (as defined in the Act) in favour of the Share Scheme and the Option Scheme respectively.

Relevant principles

21 The principles applicable to whether the Court should order the convening of a meeting of a company’s members or creditors under s 411(1) of the Act are well settled.

22 There are three stages to an application under s 411 of the Act:

first, the application to the Court to approve the convening of a scheme meeting and the draft explanatory statement to be sent to scheme members;

secondly, the holding of the scheme meeting at which members vote on the proposed scheme; and

thirdly, the application to the Court to approve the proposed scheme,

see Re CSR Ltd (2010) 183 FCR 358 at [7]; EcoBiotics Limited, in the matter of EcoBiotics Limited [2017] FCA 643 at [19].

23 At the first court hearing, the Court will order the convening of a scheme meeting and approve a draft explanatory statement to be sent to scheme members if it is satisfied of the following matters:

(1) the plaintiff is a Pt 5.1 body;

(2) the proposed scheme is a compromise or (relevantly) an arrangement within the meaning of s 411(1) of the Act;

(3) the scheme booklet will provide proper disclosure to shareholders;

(4) the scheme is bona fide and properly proposed;

(5) the Australian Securities and Investments Commission (ASIC) has had a reasonable opportunity to examine the terms of the scheme and the scheme booklet and make submissions to the Court, and has had 14 days’ notice of the date of the first court hearing; and

(6) the procedural requirements of the Federal Court (Corporations) Rules 2000 (Cth) (Corporations Rules) have been met,

see Orion Telecommunications Ltd, re Orion Telecommunications Ltd [2007] FCA 1389 at [5].

24 In addition, “the court will not ordinarily summon a meeting unless the scheme is of such a nature and cast in such terms that, if it receives the statutory majority at the … meeting the court would be likely to approve it on the hearing of a petition which is unopposed”: F T Eastment & Sons Pty Ltd v Metal Roof Decking Supplies Pty Ltd (1977) 3 ACLR 69 at 72.

Consideration

25 Based on the evidence before me I was satisfied that:

(1) Xplore Wealth is a Pt 5.1 body under the Act. It is registered with ASIC and listed on the ASX;

(2) each of the Share Scheme and Option Scheme constitute an arrangement within s 411 of the Act. Insofar as the Option Scheme is concerned, the Scheme Optionholders, being persons holding options to acquire shares in Xplore Wealth, are considered creditors for the purpose of s 411: see MIA Group Ltd [2004] NSWSC 712; (2004) 50 ASCR 29 at [9];

(3) subject to the matters raised by counsel for Xplore Wealth in the course of the first court hearing and the amendments which arose therefrom, the Scheme Booklet will provide proper disclosure to Scheme Shareholders and Scheme Optionholders. Further, there has been a verification process undertaken in relation to the information contained in the draft Scheme Booklet by Xplore Wealth and HUB24;

(4) each of the Share Scheme and the Option Scheme is bona fide and properly proposed;

(5) ASIC was given more than 14 days’ notice of the first court hearing and has had an opportunity to examine the Schemes and the draft Scheme Booklet. By letter dated 17 December 2020, it informed Xplore Wealth that it had had a reasonable opportunity to examine the draft Scheme Booklet and that it did not intend to appear to make submissions or intervene to oppose the Schemes at the first court hearing under s 411(1) of the Act; and

(6) other procedural requirements have been met. There has been compliance with the applicable requirements of the Corporations Rules and consents to act as chair or alternate chair of the Scheme Meetings were in evidence before me.

26 Xplore Wealth brought a number of specific matters to my attention which I address below.

The Option Scheme

27 As set out above, LCA formed the view that the Option Scheme is not fair but is otherwise reasonable and in the best interests of Scheme Optionholders.

28 In AIRR Holdings Ltd, in the matter of AIRR Holdings Ltd [2019] FCA 2180 the independent expert also concluded that the proposed scheme the subject of that application was not fair but was reasonable and in the best interests of the members of the relevant company. In considering that issue at [76] Besanko J said:

AIRR referred me to Blackgold International Holdings Ltd, in the matter of Blackgold International Holdings Ltd [2017] FCA 601 (Blackgold). That case involved an independent expert report which concluded that the scheme consideration in question was not fair but was reasonable. Justice Siopis considered whether such a conclusion would preclude the Court from making final orders at the second court hearing. At [18]–[19], his Honour said:

18. The shareholders will make of the expert report what they make. However, in my view, this is a case where the observations of French J (as he then was) in Re Foundation Healthcare (2002) 42 ACSR 252 at 265 are pertinent. At [44], French J observed:

The court at the stage of ordering a meeting to approve a scheme does not ordinarily go very far into the question of whether the arrangement is one which warrants the approval of the court: Re NRMA Ltd at FLR 359; ACSR 605. That question is to be answered when the scheme returns to the court for final approval. That is not to exclude the possibility that a scheme may appear on its face so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further. The court is not required to be satisfied either at the convening or approval stage that no better scheme could have been devised. The scheme, on the face of it, is not obviously unfair or otherwise inappropriate. If there are interests adversely and unfairly affected then the probability is that the question will arise at either or both the scheme meetings or the final approval stage.

19. In my view, the expert report does not warrant the Court coming to the view that the scheme is so obviously unfair or unreasonable that it should not be allowed to go to a meeting. It will always be open to an objecting shareholder, or group of shareholders, to make submissions opposing the approval of the scheme at the second hearing.

29 At [78] his Honour concluded that while the independent expert’s opinion was an unusual feature of the proposed scheme in that case, it was not one which should preclude the Court from making an order under s 411(1) of the Act. His Honour found that the proposed scheme “was not so obviously unfair or unreasonable” that it should not be allowed to go to a scheme meeting for consideration by the company’s members.

30 The way in which the Option Scheme will operate is set out at [12]-[15] and LCA’s opinion in relation to that Option Scheme is set out at [19].

31 Xplore Wealth made the following submissions about the IER:

(1) the value attributed by LCA to the options for the purposes of the “fairness” opinion proceeds without reference to the option terms governing what occurs upon a “Predominant Control Event”. A Predominant Control Event is where an offer is made by a person for the whole of the issued ordinary share capital of Xplore Wealth (or any part that is not at the time owned by the offeror or any person acting in concert with the offeror) and, after announcement of the offer, the offeror acquires “Predominant Control” of Xplore Wealth. That is, the offeror owns at least 90% of the issued ordinary share capital of Xplore Wealth. However, LCA’s analysis shows that the occurrence of such an event will affect the value of the options. In particular, LCA has calculated the amounts per share (and therefore per option) which Scheme Optionholders will receive if the Option Scheme does not go ahead. Its calculations demonstrate that all Scheme Optionholders will receive less in that scenario than if the Schemes both proceed;

(2) as a result, notwithstanding LCA’s “mode of expression” it may be that the Option Scheme is fair and reasonable because in the circumstances of the Share Scheme, the option consideration exceeds the price the optionholders would receive if the Option Scheme was not proposed; and

(3) LCA’s reasoning in support of the opinion that the Option Scheme is reasonable, which is to the effect that the benefits to Scheme Optionholders are broadly similar to the benefits to Scheme Shareholders under the Share Scheme, does not appear to be a view shared by the directors of Xplore Wealth. Under the Option Scheme, Scheme Optionholders get the Cash Consideration identified. They do not, in that capacity, participate in the Share Scheme. Further, a vote in relation to the Option Scheme does not affect the Share Scheme because the Share Scheme is not dependent on the outcome of the Option Scheme. It is thus difficult to see how matters such as anticipated costs savings and no superior offer for the Share Scheme have any application to the Option Scheme. In addition, only a minority of optionholders are also shareholders and thus will not, even in a commercial sense, obtain any benefit from the Share Scheme.

32 Having regard to the Schemes and Xplore Wealth’s submissions, I was satisfied that the Option Scheme was not obviously unfair or otherwise inappropriate. The basis upon which the LCA has valued the Scheme Options for the purpose of reaching its conclusion that the Option Scheme is not fair is available to Scheme Optionholders in the IER. They will be able to consider that valuation and also the effect on them if the Option Scheme does not go ahead but the Share Scheme does. That latter issue, which led LCA to conclude that the Option Scheme is reasonable, is clearly explained to Scheme Optionholders, both in the Scheme Booklet and the IER.

33 The conclusion reached by LCA in relation to the Option Scheme did not warrant me coming to the view that the Option Scheme was so obviously unfair or unreasonable that it should not be allowed to go to a meeting. It will be open to a Scheme Optionholder to make submissions opposing the approval of the Option Scheme at the second court hearing if he or she desires to do so.

No separate classes

34 Xplore Wealth submitted, and I accepted, that there were no class issues in relation to the Schemes.

35 The test for whether separate classes are required involves three questions: what are the rights which existing members or creditors have against the company and to what extent are they different; to what extent are those rights differently affected by the proposed scheme; and does the difference in rights or different treatment of rights make it impossible for the members or creditors in question to consider the scheme as one class: see First Pacific Advisors LLC v Boart Longyear Ltd [2017] NSWCA 116; (2017) 121 ACSR 136 (Boart Longyear) at [80].

The Share Scheme

36 Here, the rights attaching to the Scheme Options are not affected by the Share Scheme. Rather, as Xplore Wealth submitted, the Share Scheme, as a Predominant Control Event, is a circumstance to which the rights attaching to the options are subject. Thus, the Share Scheme does not affect the rights of Scheme Shareholders who also hold Scheme Options any differently to the way in which it affects the rights of those shareholders who do not hold options.

37 Scheme Shareholders who also hold Scheme Options may have different commercial interests to those shareholders who do not. However, that circumstance is not class creating. The existence of different commercial interests which is likely to be the case for all Scheme Shareholders, each of whom will face their own unique commercial circumstances, does not of itself mean that the Scheme Shareholders are “so dissimilar as to make it impossible for them to consult together with a view to their common interest”: Sovereign Life Assurance Company v Dodd [1892] 2 QB 573 at 583; Re Nine Entertainment Group Ltd (No 1) (2012) 211 FCR 439 at [53]; see also Boart Longyear at [78]-[83].

The Option Scheme

38 The Option Scheme does not affect rights attaching to the Scheme Shares. The Share Scheme will proceed regardless of whether the Option Scheme proceeds. For that reason, Scheme Optionholders who also hold Scheme Shares are in the same position in relation to the Option Scheme as Scheme Optionholders who do not hold Scheme Shares.

39 As Xplore Wealth submitted, the benefits of the Share Scheme do not provide any additional incentive to Scheme Optionholders who also hold Scheme Shares. The circumstances and any incentive to vote in favour of the Option Scheme apply equally to all Scheme Optionholders, whether or not they are also Scheme Shareholders. That incentive is that the consideration under the Option Scheme exceeds the amounts to which Scheme Optionholders would be entitled without the Option Scheme if a Predominant Control Event were to occur.

40 The options in Xplore Wealth have been issued in tranches and thus have different expiry dates and exercise prices. In Talent2 International Limited, in the matter of Talent2 International Limited [2012] FCA 771 different classes were ordered for optionholders. The circumstances in which that was done were described by Yates J at [22] as follows:

It is proposed that there be separate meetings of scheme optionholders: one for those entitled to “out of the money” consideration and the other for those entitled to “in the money” consideration. Talent2 submits that the scheme optionholders fall into two classes for the purpose of considering the option scheme of arrangement by reason of the manner in which their options have been valued for the purpose of determining the consideration to which they will be entitled if the option scheme of arrangement is approved. Talent2 submits that the decision to hold separate meetings of scheme optionholders is supported by the observations of Lindgren J in Sino Gold at [57]. In that case the same division between “out of the money” and “in the money” consideration, involving the same valuation methods, was used.

(Emphasis added.)

41 Here, there is no difference in the manner in which the options have been valued. Rather, the same methodology has been used for all options, the “Black-Scholes option pricing model”, which takes into account the particular characteristics of each tranche of options. Accordingly, community of interest is not lost and separate classes are not required. The same conclusion was reached by Barker J in Coventry Resources Limited, in the matter of Coventry Resources Limited [2012] FCA 1252 at [23] where his Honour said:

Notwithstanding different characteristics of the options in terms of exercise price and expiry, the experts have used a consistent and indiscriminate application of the same pricing or valuation methodology for all the options. Consequently, notwithstanding the different characteristics of the options, there is sufficient community of interest between optionholders so that it is appropriate that a single meeting of all optionholders be convened: Re MIA Group at [14]; Warwick Resources Limited, in the matter of Warwick Resources Limited [2009] FCA 1231 (Re Warwick Resources Limited) at [9] (Siopis J); Re Sino Gold Mining Ltd (ACN 093 518 579) [2009] FCA 1277; (2009) 74 ACSR 647 at [40]-[58] (Lindgren J).

Break fee and exclusivity arrangements

42 Xplore Wealth also drew my attention to the provision for payment of a break fee included in the SIA and the exclusivity arrangements. Each of those matters is disclosed in the Scheme Booklet and I was satisfied, based on that disclosure and the evidence, that neither of them constituted a reason to decline to make an order under s 411(1) of the Act.

Conclusion

43 For those reasons, I was satisfied that the Schemes were of such a nature and cast in such terms that, if they were considered and agreed to by the requisite statutory majority in each case, the Court would be likely to approve them on a hearing of an unopposed application.

44 Accordingly, I made the orders sought by Xplore Wealth.

I certify that the preceding forty-four (44) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Markovic. |

Associate: