Federal Court of Australia

The Colonial Mutual Life Assurance Society Limited, in the matter of The Colonial Mutual Life Assurance Society Limited [2020] FCA 1809

ORDERS

THE COLONIAL MUTUAL LIFE ASSURANCE SOCIETY LIMITED ACN 004 021 809 First Applicant AIA AUSTRALIA LIMITED ACN 004 837 861 Second Applicant | ||

THE COURT ORDERS THAT:

1. Pursuant to s 191(5) of the Life Insurance Act 1995 (Cth), the requirements of s 191(2)(c) of the Act be dispensed with insofar as it requires an approved summary to be given to each owner of a policy issued by the first applicant (CMLA), provided that the applicants comply with order 3 below.

2. Pursuant to s 191(5) of the Act, the requirements of s 191(2)(c) of the Act be dispensed with insofar as it requires an approved summary to be given to each owner of a policy issued by the second applicant (AIAA) referable to its Statutory Fund No. 1, provided that the applicants comply with order 3 below.

3. The applicants carry out the following steps:

Publication

(a) on or shortly after 18 January 2021, publish a notice of intention to make an application to the Court for confirmation of the scheme, in the form of annexure A to the originating application filed on 18 November 2020, in:

(i) the Commonwealth Government Notices Gazette; and

(ii) the newspapers approved by Australian Prudential Regulation Authority (APRA) as listed in annexure B to the originating application;

Webpages, email and scheme postal address

(b) from on or shortly after 18 January 2021 and up to and including the Scheme Effective Date as defined in the scheme document in the form of annexure D to the originating application, make a copy of the following documents available for viewing and download on the dedicated webpage specified in the notice of intention:

(i) the notice of intention;

(ii) the scheme document;

(iii) the scheme summary in the form of annexure A to these orders; and

(iv) the actuarial report of Mr Greg Della, the appointed actuary of CMLA dated 17 November 2020, the actuarial report of Mr Jeroen van Koert, the appointed actuary of AIAA dated 17 November 2020, and the actuarial report of Mr David Goodsall, the independent actuary dated 17 November 2020 (together, actuarial reports);

(c) from on or shortly after 18 January 2021 up to and including the Scheme Effective Date, include links to the webpage on:

(i) the help and support page on AIAA's website: www.aia.com.au; and

(ii) the Life Insurance, Annuities and Investment Growth Bond product information pages on the Commonwealth Bank of Australia's webpage: www.commbank.com.au.

(d) from on or shortly after 18 January 2021 up to and including the date of the confirmation hearing for the scheme, fixed pursuant to order 4 below, establish dedicated email addresses specified in the notice of intention to receive enquiries about the scheme; and

(e) from on or shortly after 18 January 2021 up to and including the date of the confirmation hearing, establish an online feedback form on the webpage to receive enquiries about the scheme;

Mail out

(f) as soon as reasonably practicable following the publication of the notice of intention, send, by regular pre-paid post a copy of the appropriate formal notification letter, being one of the letters in annexure B to these orders (and enclosing the scheme summary) to:

(i) policy owners of CMLA life policies;

(ii) previous policy owners of CMLA life policies which were cancelled as a result of a failure to pay the required premiums and which can still be reinstated at the time of the publication of the notice of intention;

(iii) owners of CMLA life policies which paid a trauma or total and permanent disability benefit in the period 12 months prior to the publication of the notice of intention, and who have an entitlement to “buy back” or reinstate an amount of life cover; and

(iv) previous policy owners of CMLA life policies which have been cancelled but which are the subject of an unresolved dispute or ongoing litigation or a remediation program,

except for such policy owners for whom CMLA has no record of a current mailing address;

(g) for persons who become CMLA policy owners on and from the date of the mail out in order 3(f) up to the Scheme Effective Date, provide the scheme summary in their Welcome Pack, by regular pre-paid post within 2 business days (or shortly after) of CMLA receiving the completed and signed application for cover or transfer form from the policy owner;

(h) in the event that the posted material referred to in order 3(f) is returned undelivered up to and including the confirmation hearing, to the extent reasonably practicable, follow CMLA’s returned mail procedure for that policy owner, as identified in the affidavit of Mark Jeffrey Moss filed 18 November 2020;

(i) for policy owners for whom CMLA has no record of a current mailing address as at the date of the mail out in order 3(f), CMLA will attempt to contact the policy owners to obtain a new mailing address in accordance with CMLA’s returned mail procedure;

Public Inspection

(j) from 20 January 2021 to 12 February 2021, make a copy of the scheme document, scheme summary, notice of intention and actuarial reports available for public inspection from 9.00am to 5.00pm at each location on weekdays (other than public holidays) in the locations provided in annexure C to the originating application;

Scheme Contact Centre

(k) from on or shortly after 18 January 2021 up to and including the date of the confirmation hearing, establish the Scheme Contact Centre to handle calls about the scheme made to the dedicated toll free phone numbers specified in the notice of intention;

(l) train the Scheme Contact Centre staff to handle calls relating to the scheme;

Other Notification

(m) on request, from on or shortly after 18 January 2021 until the date of the confirmation hearing, as soon as reasonably practicable, provide a copy of the scheme document, scheme summary, notice of intention and actuarial reports to any affected policy owners of AIAA or CMLA free of charge; and

(n) provide a general overview of the scheme to:

(i) financial advisers and financial advice licensees on a distribution list maintained by AIAA or CMLA, before or after the publication of the notice of intention;

(ii) group insurance administrators and brokers on a distribution list maintained by AIAA or CMLA, before or after the publication of the notice of intention; and

(iii) industry partners, including researchers, consultants and analysts with whom AIAA or CMLA has an existing relationship, by way of a media release published on AIAA's website as soon as reasonably practicable following the publication of the notice of intention,

including details of how affected policy owners can access further information about the scheme.

4. The confirmation hearing be fixed for hearing before Chief Justice Allsop on 8 March 2021 at 10.15 am.

5. The applicants pay the costs of the proceedings of APRA as agreed or, if agreement cannot be reached, as assessed.

6. The applicants file affidavits sworn or affirmed by the following deponents no later than 31 January 2021, in each case in the form of the affidavit filed on 18 November 2020:

(a) Jeroen Paulus van Koert;

(b) Gregory Joseph Della;

(c) David Millington Goodsall; and

(d) Mark Jeffrey Moss.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Schedule

No: NSD1245/2020

Federal Court of Australia

District Registry: New South Wales

Division: General

Second Applicant | AIA AUSTRALIA LIMITED 004 837 861 |

Annexure A to 16 December 2020 orders

Annexure B to 16 December 2020 orders

GLEESON J

1 The first applicant (CMLA) and the second applicant (AIAA) have commenced this proceeding for confirmation of a proposed scheme under Part 9 of the Life Insurance Act 1995 (Cth), pursuant to which the whole of the life insurance business of CMLA (apart from certain specific excluded assets and liabilities) would be transferred to AIAA. By s 190(1) of the Act, no part of a life insurance business of a life company may be transferred to another life company except under a scheme confirmed by the Court.

2 In advance of the hearing of the confirmation application, the applicants sought orders dispensing with the need to comply with s 191(2)(c) of the Act, which requires affected policy owners to be provided with information about the proposed scheme. After hearing the dispensation application, I made orders in accordance with the proposed orders. These are my reasons for making those orders.

3 Section 191(2)(c) provides that an application for confirmation of a scheme may not be made unless an “approved summary” of the scheme has been given to every “affected policy owner”. An “approved summary” means a summary approved by the Australian Prudential Regulation Authority (APRA) and “affected policy owner” means the owner of a policy that is referrable to a statutory fund affected by a scheme: s 191(1).

4 However, by s 191(5), the Court may dispense with the need for compliance with s 191(2)(c) in relation to a particular scheme if it is satisfied that, because of the nature of the scheme or the circumstances attending its preparation, it is not necessary that the paragraph be complied with.

5 In support of the orders sought, the applicants relied upon the following affidavits (all filed unsworn in accordance with the Court’s special measures in response to COVID-19 information note (SMIN-1)):

(1) affidavit of Jeronimus (Jeroen) Paulus van Koert, the appointed actuary of AIAA;

(2) affidavit of Gregory Joseph Della, appointed actuary of CMLA;

(3) affidavit of David Millington Goodsall, director of Synge & Noble, a consulting actuarial firm, and independent actuary for the scheme; and

(4) affidavit of Mark Jeffrey Moss, program manager at AIAA responsible for the management of the scheme.

APRA’s position

6 Mr Claxton appeared on behalf of APRA and informed the Court that APRA has no objection to the making of the orders proposed by the applicants, and is satisfied with the proposed steps for notifying affected policy owners of the proposed scheme: cf. Re National Mutual Life Association of Australasia Ltd [2016] FCA 1219 (National Mutual) at [4]. Mr Claxton proposed some minor amendments to the proposed formal notification letters referred to in the applicants’ draft orders, which were agreed by Mr Jackman SC, senior counsel for the applicants.

7 In particular, Mr Claxton confirmed that APRA does not consider it necessary for owners of policies referrable to the AIAA receiving fund, being AIAA’s Statutory Fund No. 1, to be given an approved summary of the scheme, having regard to the actuarial evidence that the scheme will have a positive impact on the Capital Adequacy Multiple for that statutory fund and the steps proposed to be taken by the applicants to publicise the proposed scheme.

Background to the proposed scheme

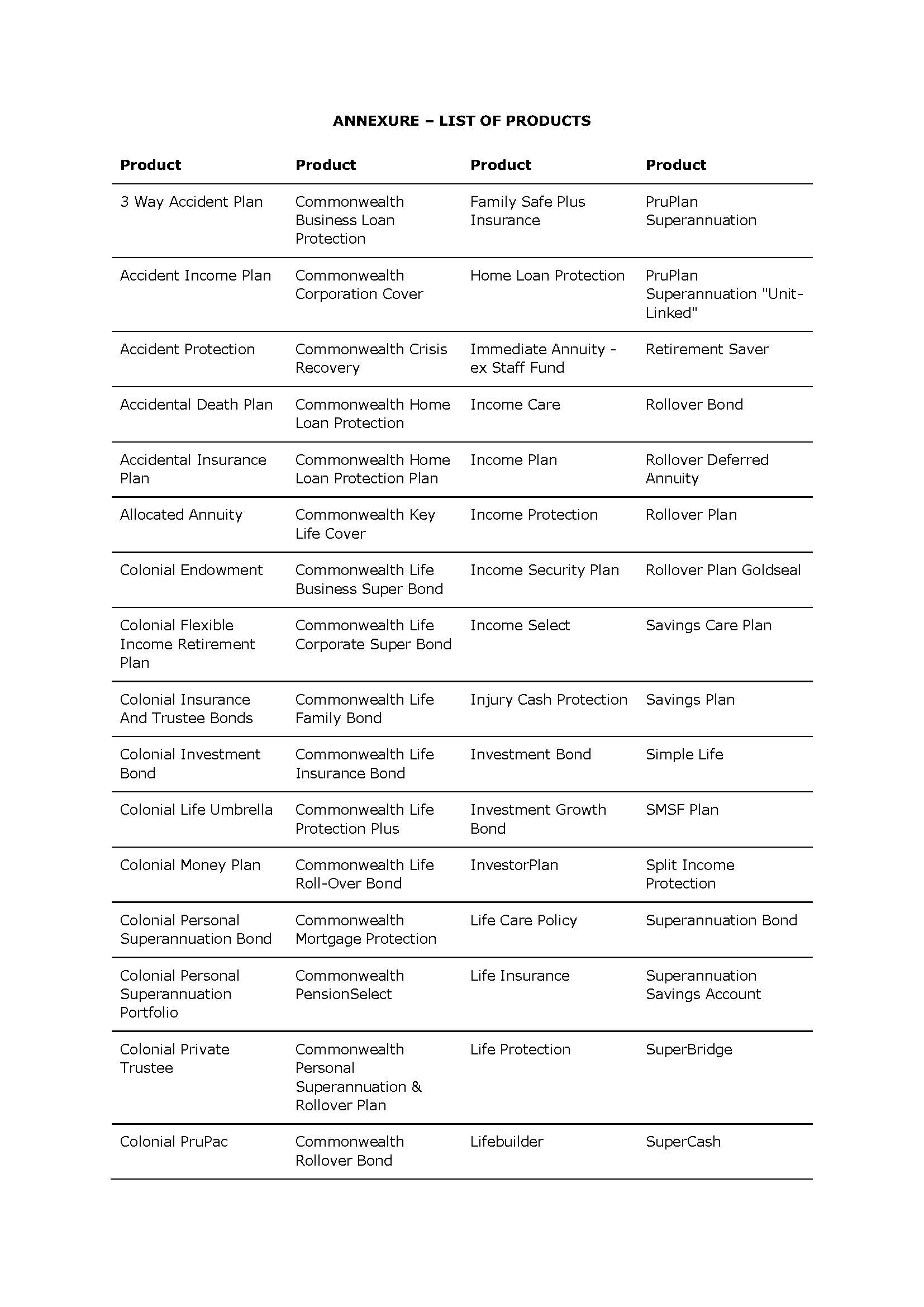

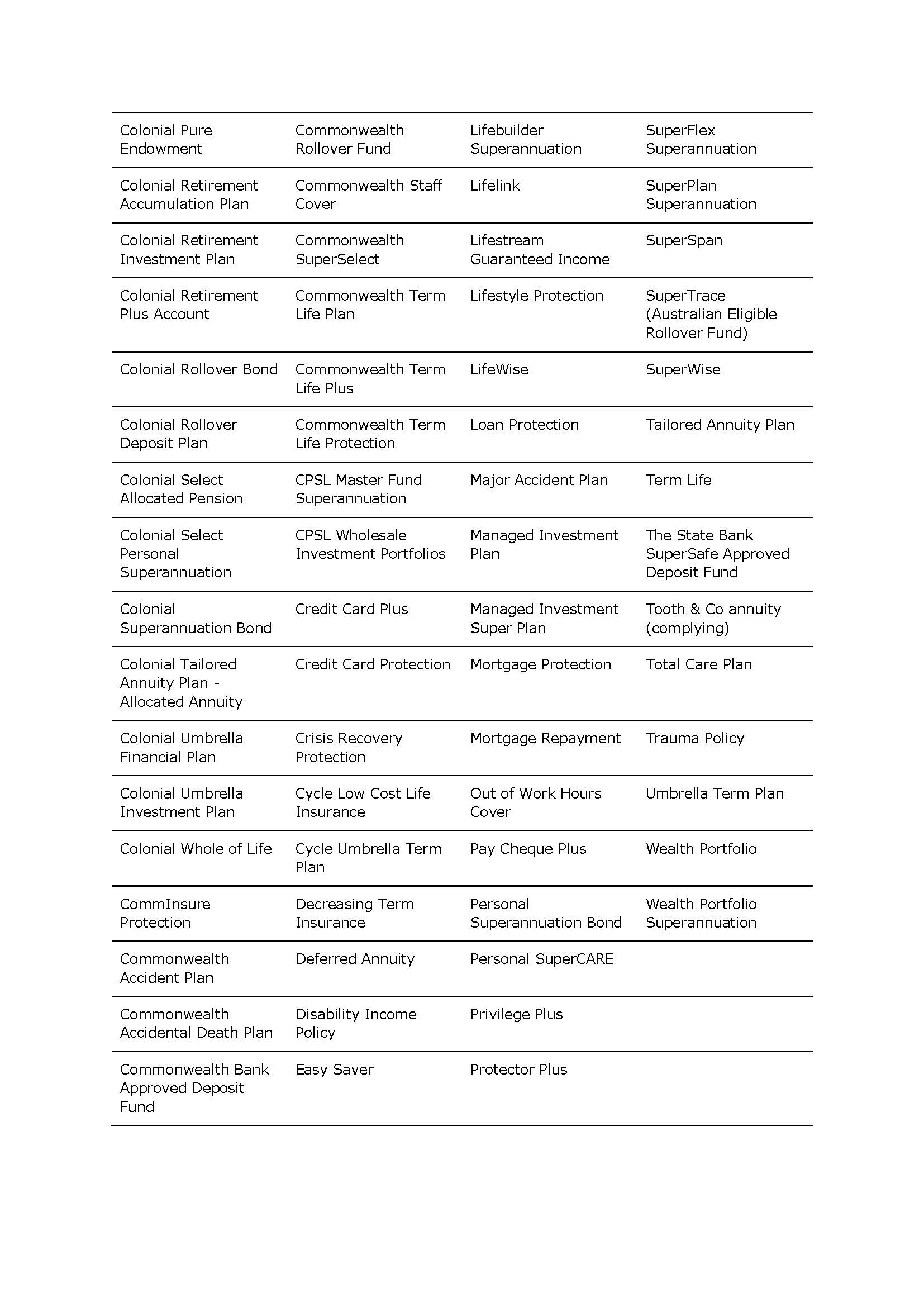

8 CMLA is currently ultimately wholly-owned by Commonwealth Bank of Australia (CBA), a company listed on the Australian Securities Exchange. CMLA is registered as a life company under s 21 of the Act. CMLA has six statutory funds in respect of its life insurance business within the meaning of the Act.

9 AIAA is ultimately wholly-owned by AIA Group Limited, a company listed on the Stock Exchange of Hong Kong. AIAA is also registered as a life company under s 21 of the Act. AIAA provides life insurance coverage to over 2.9 million people in Australia and employs approximately 1,200 people in Australia. AIAA currently has two statutory funds within the meaning of the Act.

10 On 21 September 2017, CBA announced the sale of its life insurance business in Australia, including CMLA, to AIA Group Limited. In parallel with a planned share sale of CMLA, which has been the subject of regulatory approval delays relating to the disposal by CMLA of its 37.5% stake in BoCommLife Insurance Company Limited, CBA and AIA Group Limited (through AIAA) have sought to implement an alternative approach to completing the divestment of CBA’s life insurance business. This has involved:

(a) the entry by CBA, AIAA and CMLA (among other entities) into a joint cooperation agreement to jointly manage AIAA’s and CBA’s life insurance businesses, including CMLA (Joint Cooperation Agreement). The Joint Cooperation Agreement became effective on 1 November 2019; and

(b) CBA, AIAA and CMLA working towards implementing the scheme.

11 Mr Moss’s evidence was that, under the terms of the Joint Cooperation Agreement, AIAA exercises an appropriate level of direct management and oversight of CBA’s life insurance business, including the ability to appoint a majority of the directors to CMLA. In practice, AIAA currently operates CMLA’s business jointly with its own life insurance business, and shares business functions, including actuarial teams, across the two businesses.

12 AIAA (along with CBA, CMLA and the other parties to the Joint Cooperation Agreement, where required) received approval to enter into the Joint Cooperation Agreement from the Commonwealth Treasurer on or around 30 October 2019 under the Financial Sector (Shareholdings) Act 1998 (Cth), the Insurance Acquisitions and Takeovers Act 1991 (Cth) (IATA), and s 74(2) of the Foreign Acquisitions and Takeovers Act 1975 (Cth) (FATA).

13 By decision dated 30 October 2020, the Treasurer made an unconditional decision pursuant to s 41 of the IATA that the Commonwealth Government has no objection to the proposed scheme.

14 By letter dated 2 November 2020, the Australian Government informed Ashurst that the Commonwealth has no objection to AIAA acquiring up to a 100% of the interest in the assets of the life insurance business conducted by CMLA, subject to certain conditions imposed under s 74(2) of the FATA.

Overview of proposed scheme

15 The proposed scheme is set out at annexure D to the originating application. The applicants summarised the effect of the scheme as follows.

(1) all policies of CMLA, as well as all assets of its statutory funds (other than the CMLA’s interest in BoCommLife and certain other assets specified in annexure D), will be transferred to AIAA;

(2) AIAA will assume all of the liabilities and obligations of CMLA in relation to its transferring business (other than liabilities relating to CMLA’s interest in BoCommLife and certain other liabilities specified in annexure D) and be entitled to all the rights and benefits of CMLA in relation to the transferring business;

(3) AIAA will become the issuer of CMLA life insurance policies and CMLA policy owners will become AIAA policy owners;

(4) the rights and liabilities of CMLA policy owners will be the same as they would have been if the applications on which their policies were based had been accepted by AIAA instead of CMLA and their policies had been issued by AIAA instead of CMLA; and

(5) any person having a claim or obligation to CMLA under or in respect of a CMLA policy will have the same claim on or obligation to AIAA irrespective of when the claim or obligation arose.

16 In summary, the applicants submitted:

(1) CMLA’s three statutory funds containing investment-linked policies (known as Statutory Fund No. 1L, Statutory Fund No. 2L and Statutory Fund No. 4) will be transferred as-is to AIAA – in other words, they will become new statutory funds in AIAA;

(2) the policies referable to CMLA’s other statutory funds (known as Statutory Fund No. 1, Statutory Fund No. 3 and Statutory Fund No. 5), as well as these funds’ underlying assets, will be transferred to AIAA’s Statutory Fund No. 1 (receiving fund).

17 As set out in cl 13.1 of annexure D, there will be no change to the terms and conditions of the policies of CMLA or AIAA as a result of the scheme, other than:

(1) references to “CMLA” will change to be references to “AIAA”; and

(2) references to a statutory fund of CMLA will change to be references to the relevant statutory fund of AIAA.

18 As set out in cl 15 of annexure D, all costs associated with the scheme will be paid for by AIAA and CMLA and not by the policy owners of AIAA or CMLA.

Actuarial reports

19 Three actuarial reports have been prepared in relation to the scheme, by Messrs van Koert, Della and Goodsall respectively. Mr van Koert has concluded that the proposed scheme will not materially prejudice existing AIAA policy owners. To illustrate the change to the financial position of AIAA’s statutory funds resulting from the proposed scheme, Mr van Koert set out the Capital Adequacy Multiples for the statutory funds as at 30 June 2020 and as at 30 June 2020 if the scheme had been implemented. For AIAA Statutory Fund No. 1, the multiple increased from 142% to 168%. According to Mr van Koert, this improvement is due mainly to improved diversification of risks under the Life and General Insurance Capital prodetnail standard set by APRA, generated by bringing the assets and liabilities of the relevant statutory funds together.

20 Mr Della has concluded that the proposed scheme will not materially prejudice existing CMLA policy owners. Mr Goodsall, the independent actuary, has formed the following opinions based on his review of the proposed scheme:

(1) the proposed scheme will not materially prejudice the interests of policy owners of CMLA and AIAA;

(2) the security of benefits for policy owners of CMLA and AIAA is maintained;

(3) the changes to the contractual references contained in the scheme are necessary to give effect to the scheme and will not adversely affect the contractual rights or benefits of policy owners of CMLA or AIAA; and

(4) there will not be any adverse impact on reasonable benefit expectations of policy owners of CMLA and AIAA.

Affected policy owners

21 As earlier noted, an “affected policy owner” is the owner of a policy that is referrable to a statutory fund affected by a scheme. As Allsop CJ explained in Re Macquarie Life Ltd [2016] FCA 973 (Macquarie Life) at [6], statutory funds of this kind separate and ring-fenced operational units of the overall life business of the company.

22 All six of CMLA’s statutory funds are affected by proposed scheme.

23 The applicants also accepted that AIAA’s Statutory Fund No. 1 is also affected by the proposed scheme, since it is receiving policies under the scheme: cf. Macquarie Life at [25]; Re St George Life Ltd [2018] FCA 1206 (St George Life) at [32].

24 As AIAA’s other statutory fund (Statutory Fund No. 3) is not receiving (or transferring) any policies under the proposed scheme, it will not be “affected” by the scheme within the meaning of the Act.

25 Thus, the relevant affected policy owners are the owners of policies referrable to CMLA’s statutory funds and AIAA’s Statutory Fund No. 1.

26 A “policy owner” is a person to whom a relevant policy has been issued, or an assignee or transferee of the rights of that person: cf. s 10 of the Act. A person who may have rights under the policy, but is not a person to whom a relevant policy has been issued, or an assignee or transferee of the rights of that person is not a “policy owner”: Macquarie Life at [22] and [27]; St George Life at [35].

27 The applicants have identified the following groups of persons to be “policy owners” for the purposes of the scheme:

(1) individuals who hold a current contract for life insurance in their own name;

(2) superannuation trustees or employers who enter into policies in their own name for the benefit of members of the funds or employees, respectively (but not the members of the funds or the employees themselves);

(3) policy owners who are currently “on claim”, that is, policy owners who are being paid a benefit following a claim on a policy they hold; and

(4) owners of certain categories of recently lapsed or cancelled policies, being:

(a) policies that have lapsed or been cancelled as a result of a failure to pay the required premiums, but that can be reinstated within a particular period if the policy owner resumes payment of their premiums;

(b) policies that have paid a trauma or total and permanent disability benefit within the last 12 months, but whose policy owner has an entitlement to 'buy back' or reinstate an amount of life cover; and

(c) policies that have lapsed but are the subject of an unresolved dispute or ongoing litigation or remediation program.

Request for dispensation orders

28 In substance, the applicants are seeking dispensation in respect of the requirement to contact the following groups of affected policy owners:

(1) owners of policies referable to AIAA’s receiving fund;

(2) any affected policy owners of CMLA for whom CMLA does not have a current mailing address, or ceases to have a current mailing address after despatch of the approved scheme summary; and

(3) any affected policy owners who become owners of CMLA policies after the date of the despatch of the approved scheme summary (new policy owners).

29 In substance, the grounds for the proposed dispensation in relation to these three groups was as follows:

(1) The cost of notifying owners of policies referable to AIAA’s receiving fund, of whom there are over 250,000, is not justified having regard to the expected positive impact of the scheme on the financial position of the receiving fund.

(2) Recent searches show that CMLA currently has mailing addresses for approximately 94.29% of affected policy owners of CMLA. The likely cost of further searches for addresses for the remaining policy owners is not justified having regard to the likely opportunity for similarly affected policy owners to raise any relevant objection.

(3) New policy owners are most appropriately informed of the proposed scheme when they receive their Welcome Pack, on entering into a new policy.

(4) The applicants propose to carry out other steps to advertise the scheme which, they submit, will be “likely to lead to notification of a very large number of affected policy owners, sufficient to bring forth, in all likelihood any objection to the scheme that is based on viable objective grounds”: cf. National Mutual at [42].

Consideration and conclusion

30 The policy underlying s 191(2)(c) is to give every affected policy owner a summary of the proposed scheme approved by APRA, and an opportunity to make submissions to the Court on the application for confirmation of the scheme: National Mutual at [31] and [32].

31 Matters that have been taken into account in the exercise of the discretion to dispense with this requirement include, relevantly (National Mutual at [34]):

(1) the nature of the scheme and whether it involves changes to the contractual benefits or entitlements and security of policy owners in respect of whom dispensation is sought;

(2) evidence from qualified actuaries as to whether policy owners in respect of whom dispensation is sought will be detrimentally affected by the scheme;

(3) practical difficulties and costs in providing an approved scheme summary to policy owners in respect of whom dispensation is sought;

(4) the extent to which the scheme may be brought to the attention of policy owners by means other than the approved scheme summary;

(5) the lack of material changes to policy terms and conditions;

(6) the involvement and attitude of APRA to the application.

32 However, by s 191(5), the Court may dispense with the need for compliance with s 191(2)(c) in relation to a particular scheme if it is satisfied that, because of the nature of the scheme or the circumstances attending its preparation, it is not necessary that s 191(2)(c) be complied with.

33 I am satisfied that it is not necessary that s 191(2)(c) be complied with, having regard to the evidence that affected policy owners will not be detrimentally affected by the scheme, the absence of any material changes to policy terms and conditions and APRA’s satisfaction with the proposed orders.

34 I accept it would be onerous for the applicants to give a copy of the approved scheme summary to AIAA affected policy owners, having regard to the evidence that they are not adversely affected by the proposed scheme.

35 I also accept that it would be onerous for the applicants to be required to give a copy of the approved scheme summary to CMLA affected policy owners for whom CMLA is unable to locate a mailing address through reasonable searches of its own records, where the applicants will give an approved scheme summary to approximately 94% of affected policy owners.

36 I also accept that the proposed orders make appropriate provision for informing new policy owners of the proposed scheme.

37 Finally, I was satisfied that the proposed orders make appropriate provision for drawing attention to the proposed scheme to affect policy owners who will not be given the approved summary in accordance with s 191(2)(c).

38 Accordingly, I made orders in accordance with the proposed orders.

I certify that the preceding thirty-eight (38) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |