FEDERAL COURT OF AUSTRALIA

Warner (Trustee), in the matter of McMillan (Bankrupt) v McMillan [2020] FCA 1759

ORDERS

ANTHONY JOHN WARNER IN HIS CAPACITY AS TRUSTEE IN BANKRUPTCY OF THE ESTATE OF BRIAN MCMILLAN Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The parties are to bring in Short Minutes of Orders to give effect to these reasons within fourteen days.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

FLICK J:

1 On 30 January 2020, the Applicant, Mr Anthony Warner, filed in this Court an Originating Application and a Statement of Claim. That Application was filed by Mr Warner in his capacity as the trustee of the bankrupt estate of Mr Brian McMillan (“the Trustee”), a sequestration order having been made on 6 November 2018. Mr Warner was also appointed the trustee on that date. The Respondent to the proceeding, Mrs Karin Elisabeth McMillan, is the wife of Mr McMillan.

2 The Trustee claims (inter alia) that a purported transfer of property by Mr McMillan to his wife in around May 2002 was void pursuant to either s 120 or s 121 of the Bankruptcy Act 1966 (Cth) (the “Bankruptcy Act”). Declaratory and other relief was sought.

3 It is concluded that the claims of the Trustee made pursuant to s 121 prevail.

THE BANKRUPTCY ACT – ss 120 & 121

4 The sections of the Bankruptcy Act of primary relevance to the present proceeding are ss 120 and 121 as they stood as at the time of the purported transfer in around May 2002.

5 Section 120 and its predecessors had a lineage dating back to the Fraudulent Conveyances Act 1571 (UK): Anscor Pty Ltd v Clout [2004] FCAFC 71 at [27], (2004) 135 FCR 469 at 477 per Lindgren J (“Anscor v Clout”). They are provisions designed to avoid dispositions of property to the prejudice of creditors.

6 Both sections were amended by the Bankruptcy Legislation Amendment Act 1996 (Cth). The amendments were intended “to make it easier for a trustee to succeed than was previously the case”: Sellers v One Step Plumbing and Concrete Pty Ltd [2002] FCA 478 at [98], (2002) 190 ALR 716 at 730 per Weinberg J (“Sellers”).

Section 120

7 Section 120(1) of the Bankruptcy Act provides as follows:

Undervalued transactions

Transfers that are void against trustee

A transfer of property by a person who later becomes a bankrupt (the transferor) to another person (the transferee) is void against the trustee in the transferor's bankruptcy if:

(a) the transfer took place in the period beginning 5 years before the commencement of the bankruptcy and ending on the date of the bankruptcy; and

(b) the transferee gave no consideration for the transfer or gave consideration of less value than the market value of the property.

…

Section 120(7) provides as follows:

Meaning of transfer of property and market value

For the purposes of this section:

(a) transfer of property includes a payment of money; and

(b) a person who does something that results in another person becoming the owner of property that did not previously exist is taken to have transferred the property to the other person; and

(c) the market value of property transferred is its market value at the time of the transfer.

8 In contrast to the present wording of s 120, a prior iteration of s 120 provided that a transaction was void if it was not made “in good faith and for valuable consideration”. When the section so provided, the High Court in 1986 concluded that a “purchaser … for valuable consideration” referred to a person “who has given a consideration for his purchase ‘which has a real and substantial value, and not one which is merely nominal or trivial or colourable’”: Barton v Official Receiver (1986) 161 CLR 75 at 86 per Gibbs CJ, Mason, Wilson and Dawson JJ (“Barton v Official Receiver”). See also: cf. Saba v Plumb [2018] NSWCA 60 at [99]-[100], (2018) 97 NSWLR 278 at 299 to 300 per Macfarlan JA.

9 But the relevant form of s 120, as amended in 1996, abandons reference to “valuable consideration” and, in lieu, refers to “consideration of less value than the market value of the property”: s 120(1)(b). The phrase “market value” is defined (in s 120(7)) as meaning the “market value at the time of the transfer”.

10 The reasons for the change in language are evident from the following extract from the Explanatory Memorandum to the Bankruptcy Legislation Amendment Bill 1996:

84.13 The consideration given by a person for the transfer of property must be an amount which is equal to at least the market value of the property at the time of the transfer (see proposed paragraph 120(7)(c)). This requirement is intended to overcome the decision of the High Court in Barton v Official Receiver (1986) 161 CLR 75 that a person who claims to be a purchaser of the property need not show that he or she had given fully adequate consideration for the transfer, but nevertheless must have given real and substantial consideration, and not consideration which is merely nominal, trivial or colourable. The expression ‘market value’ is intended to refer to the value of the property concerned if it were disposed of to an unrelated purchaser bidding in a market on an ordinary commercial basis for property of the kind disposed of, without any sort of discount or incentive for purchase being offered. The expression is not intended to include a situation where the property was being disposed of at a ‘fire sale’, at discounted prices because of some immediate need on the part of the owner to liquidate his or her assets. Of course, there may be differing opinions as to the precise market value of some property, for example house properties, where valuers or real estate agents may give kerbside valuations which spread over a range of monetary values. However, if the property was transferred for an amount less than the lowest amount in the range, the transfer would be a transfer at undervalue, for the purposes of the section.

The current form of s 120 was thus intended to overcome the decision in Barton v Official Receiver: Victorian Producers’ Co-Operative Co Ltd v Kenneth [1999] FCA 1488 at [11], (1999) 1 ABC (NS) 198 at 201 per Merkel J.

11 Section 120, as amended, requires the Court to consider the “value” of the consideration. “That is something to be determined on an objective basis”: Anscor v Clout [2004] FCAFC at [66], (2004) 135 FCR at 489 per Lindgren J. In explaining the significance of the 1996 amendments, his Honour there observed (at 478 to 479):

[32] The second change of present relevance is referable to the holding in Barton v Official Receiver (1986) 161 CLR 75 … that a person who claimed protection under the former s 120(7) as a person who had purchased from the disponee under the settlement “in good faith and for valuable consideration” needed to show, in relation to consideration, only that he had given “consideration for his purchase ‘which has a real and substantial value, and not one that is merely nominal or trivial or colourable’ …” (at 86). The new s 120(1), in contrast, is enlivened by nothing more than a transfer of property within the specified period under which “the transferee gave no consideration for the transfer or gave consideration of less value than the market value of the property” (emphasis added): see the Explanatory Memorandum relating to the Bankruptcy Legislation Amendment Bill 1995 (Cth) (the Explanatory Memorandum), para 84.13; Official Trustee in Bankruptcy v Lopatinsky (2003) 129 FCR 234.

[33] In considering the questions raised by the appeal, it is important to note the following matters.

[34] First, since s 120(1) is triggered by a transfer for less than full consideration, if the transferor (later the bankrupt) sells land having a market value of $1 million for $950,000 at any time in the period beginning five years before the commencement of the transferor’s bankruptcy and ending on the date of the bankruptcy, the provision is activated. It matters not that the transferee was a purchaser in good faith and for valuable consideration. However, if the transfer took place more than two years before the commencement of the transferor’s bankruptcy, the provision does not operate if the transferee proves that, at the time of the transfer, the transferor was solvent: s 120(3) (a person is insolvent if, and only if, the person is unable to pay all the person’s debts, as and when they become due and payable: s 5(2) and (3).

…

[36] Second, s 120(1) requires the Court to be satisfied only that the value of the consideration was less than the market value of the property transferred as at the date of the transfer. Unlike s 120(4), s 120(1) does not require the Court to assign any particular value to the consideration. …

“The focus is shifted from the motive for the transaction to whether or not full market value consideration has been given”: Verge v Devere Holdings Pty Ltd (No 4) [2010] FCA 653 at [224], (2010) 8 ABC (NS) 211 at 260 per McKerracher J. In Sellers, Weinberg J there observed in respect to the phrase “market value”:

[98] It is clear that s 120, in its present form, is intended to cover broadly the same area as the section it replaced. However, it is intended to make it easier for a trustee to succeed than was previously the case. The same has been said of s 121: Ashton v Prentice [1998] FCA 1464 ...

[99] In Spencer v Commonwealth (1907) 5 CLR 418, Griffiths CJ said (at 432):

In my judgment the test of value of land is to be determined, not by inquiring what price a man desiring to sell could actually have obtained for it on a given day, ie whether there was in fact on that day a willing buyer, but by inquiring “what would a man desiring to buy the land have had to pay for it on that day to a vendor willing to sell it for a fair price but not desirous to sell?”

[100] Issacs J said (at 441):

To arrive at the value of the land at that date, we have, as I conceive, to suppose it sold then, not by means of a forced sale, but by voluntary bargaining between the plaintiff and a purchaser, willing to trade, but neither of them so anxious to do so that he would overlook any ordinary business consideration.

[101] In James v Swan Hill Sewerage Authority [1978] VR 519, Harris J applied these formulations in determining the meaning to be accorded to the expression “market value” in a different legislative context. He concluded that the “market value” of land under s 11(b) of the Lands Compensation Act 1958 (Vic) was to be determined in accordance with the test laid down in Spencer.

[102] Harris J also referred to Commonwealth v Arklay (1952) 87 CLR 159 at 169–70 where it had been held that the term “value” in s 28(1)(a) of the Lands Acquisition Act 1906 (Cth) meant the value of the land to the owner. That in turn involved:

… simply an analysis of what in all the relevant circumstances would be the price that a willing purchaser would have to pay a vendor willing but not anxious to sell in order to obtain the land.

[103] Harris J concluded that this formulation, as well as that adopted in Spencer, was applicable to the determination of the “market value” of the land acquired. There is nothing in ss 120 or 121 of the Act to suggest that these formulations are not equally applicable to the determination of “market value” for the purpose of those provisions.

Section 121

12 Section 121(1) of the Bankruptcy Act provides as follows:

Transfers to defeat creditors

Transfers that are void

(1) A transfer of property by a person who later becomes a bankrupt (the transferor) to another person (the transferee) is void against the trustee in the transferor’s bankruptcy if:

(a) the property would probably have become part of the transferor’s estate or would probably have been available to creditors if the property had not been transferred; and

(b) the transferor’s main purpose in making the transfer was:

(i) to prevent the transferred property from becoming divisible among the transferor’s creditors; or

(ii) to hinder or delay the process of making property available for division among the transferor’s creditors.

Section 121(9) provides as follows:

Meaning of transfer of property and market value

For the purposes of this section:

(a) transfer of property includes a payment of money; and

(b) a person who does something that results in another person becoming the owner of property that did not previously exist is taken to have transferred the property to the other person; and

(c) the market value of property transferred is its market value at the time of the transfer.

13 In contrast to the current language of s 121(1), the predecessor provision to s 121(1) was expressed in terms of a “disposition of property … with intent to defraud creditors, not being a disposition for valuable consideration in favour of a person who acted in good faith…”. With reference to this provision, Brennan CJ and McHugh J in Cannane v J Cannane Pty Ltd (in Liq) [1998] HCA 26, (1998) 192 CLR 557 at 565-566 concluded:

[10] … The critical term for present purposes is “with intent to defraud creditors”. Provisions of this kind, based on 13 Eliz I c 5…, have been considered by courts in various jurisdictions and it is clearly established that the party seeking to avoid a disposition of property has the onus of proving an actual intent by the disponor at the time of the disposition to defraud creditors…. The creditors whom the fraudulent disponor of property might intend to defeat need not be existing creditors; they may be future creditors…. The intent prescribed by s 121(1) is an intent to defraud any present or future creditors…. But, as the intent must accompany the disposition…, it must relate to the effect of disposing of property then existing.

(footnotes omitted, emphasis in original).

Their Honours continued (at 567):

[13] If property be disposed of by sale and the sale price received by the disponor is equal to the true value of the property at the time of the disposition, the creditors have an undepleted fund against which to prove their debts. But if property is sold for an undervalue or is given away, that fact is relevant to the intent to be attributed to the disponor in disposing of the property…. The value of property at the time of disposition may reflect, of course, the prospect of its future increase or decrease in value. But disposition of property at an undervalue is only a fact from which, dependent on the surrounding circumstances, an inference of fraudulent intent may be drawn. …

[14] Section 121 is not enlivened merely by showing that the disposition has reduced the assets available to the creditors when the disponor is adjudicated bankrupt. It is the disponor’s intent to deprive creditors of assets against which (or against the proceeds of which) they would otherwise be entitled to prove their debts that enlivens the operation of s 121. …

(footnote omitted).

See also: [1998] HCA 26 at [37] to [39], (1998) 192 CLR at 573-574 per Gummow J. His Honour also observed (at 578):

[54] The expression “with intent to defraud” does not have any universal connotation applicable in all statutory contexts in which it is found…. However, the appellants properly relied upon a passage in the judgment of Dixon CJ in Hardie v Hanson ((1960) 105 CLR 451). This case arose under s 281 of the Companies Act 1943 (WA) and concerned the personal responsibility of a director for the debts or other liabilities of a company whose business had been carried on in the course of the winding-up “with intent to defraud creditors of the company or creditors of any other person”. Dixon CJ said…:

“The phrase ‘intent to defraud creditors of the company’ suggests that present or future creditors of the company will, if the intent is effectuated, be cheated of their rights. An intent to defraud creditors has been described, for the purposes of bankruptcy legislation, as an intent by deceit to deprive creditors of something to which they are entitled.”

In the same case, Kitto J said that the onus lay on the liquidator…:

“to prove affirmatively that the carrying on of the company’s business during the relevant fifteen months was characterized by an intent – which in the circumstances means an intent on the part of [the director] – to defraud creditors of the company. An actual purpose, consciously pursued, of swindling creditors out of their money had to be established against [the director] before a declaration under the section could be made.”

(footnotes omitted).

14 The 1996 amendments thus deleted the need to establish an “intent to defraud creditors” and substituted the need to establish the “main purpose” behind a transfer of property.

15 Section 121(1)(b) thus refers to the “transferor’s main purpose”, including preventing the transferred property from becoming divisible among creditors. Section 121(2) creates an irrebuttable presumption that such was the “main purpose”, “if it can reasonably be inferred from all the circumstances that, at the time of the transfer, the transferor was, or was about to become, insolvent”. In commenting upon this provision, Ryan, Heerey and Katz JJ in Re Jury; Ashton v Prentice [1999] FCA 671, (1999) 92 FCR 68 at 82 observed:

[57] Counsel for Mr Ashton did not attack his Honour’s finding that it could reasonably be inferred from all the circumstances that in August 1995 the bankrupt was insolvent. Rather, he argued that the presumption created by s 121(2) of the Act could be rebutted by direct proof that the transferor's main purpose was other than that described in s 121(1)(b). It was sought to derive support for that interpretation from the language of s 121(3).

[58] However, s 121(3) does not weaken or make rebuttable the presumption created by s 121(2). What s 121(3) does is acknowledge that the trustee may resort to modes of proving the transferor’s main purpose which are alternative to the presumption afforded by s 121(2). For example, the trustee may prove an admission by the transferee that the main purpose of the transfer was to prevent the property becoming divisible among the transferor's creditors, even though all of the circumstances at the time of the transfer did not permit, or positively contradicted, the inference that the transferor was, or was about to become, insolvent.

[59] We are supported in this conclusion that s 121(2) and (3) have independent spheres of operation by the reflection that the transferor’s evidence of his or her own subjective intention in making the transfer cannot usually affect the existence of circumstances giving rise to a reasonable inference of insolvency. In other words, even if the Court were to accept that the sole purpose of the transfer had been to effectuate a longstanding charitable or benevolent intention evidenced by a history of similar benefactions, that would not render unavailable the reasonable inference of insolvency required to support the conclusive presumption created by s 121(2).

[60] In the present case, as we have already mentioned, there was no attack on his Honour’s finding that insolvency, or imminent insolvency, could reasonably be inferred from all the circumstances. It must follow that, subject to s 121(4), s 121(1) operated to render the transfer to Mr Ashton void because the “main purpose” required by s 121(1)(b) (consisting of the two components in subpars (i) and (ii)) had been established by the operation of s 121(2).

[61] It would thus not be to the point if, contrary to his Honour’s findings, the bankrupt in fact had the purpose of selling the house to meet legal costs. Nor would it matter if, leaving s 121(2) aside, that might have been his main, or even only, purpose. Section 121(2) cannot be left aside. In its terms it operates to establish the s 121(1)(b) “main purpose” if the reasonable inference of insolvency is open.

Similarly, in Prentice v Cummins (No 5) [2002] FCA 1503 at [95], (2002) 124 FCR 67 at 90 (“Prentice v Cummins”), Sackville J observed that “if it can be reasonably inferred that the transferor was insolvent at the time of transfer, it will not matter if his or her subjective intention was not to prevent, hinder or delay the process of making property available for division among creditors…”. His Honour went on to further observe that if, on the other hand, “the trustee attacking a transfer does not rely on s 121(2), the trustee will need to establish that the transferor’s subjective purpose was that described in s 121(1)(b)”. See also: Lo Pilato v Kamy Saeedi Lawyers Pty Ltd [2017] FCA 34 at [158] to [162], (2017) 249 FCR 69 at 101-102 per Katzmann J.

16 Proof of a bankrupt’s “main purpose” requires evidence giving rise to a “reasonable and definite inference, and not merely to conflicting inferences of equal degree of probability”: The Trustees of the Property of Cummins v Cummins [2006] HCA 6 at [34], (2006) 227 CLR 278 at 292 (“Cummins v Cummins”). Gleeson CJ, Gummow, Hayne, Heydon and Crennan JJ there concluded:

Main purpose

[34] What had been required for the Trustees to succeed at trial was that the circumstances appearing in the evidence gave rise to a reasonable and definite inference, not merely to conflicting inferences of equal degree of probability, that, in making the August transactions, Mr Cummins had the “main purpose” required by the statute…. Further, counsel for the Trustees accepted that, in determining the inferences to be drawn from the primary facts, regard was to be had to the seriousness of the allegations made against Mr Cummins (although he was not a party) and the gravity of the consequences of findings adverse to him…. Reference was made to the well-known judgment of Dixon J in Briginshaw v Briginshaw….

(footnotes omitted).

The Bankruptcy Act & Jones v Dunkel

17 As a matter of general principle, the failure by a party to call an available witness may give rise to an inference that the evidence of that witness would not have assisted the case sought to be advanced by that party. An inference may thus be drawn where an available witness is not called: cf. Jones v Dunkel (1959) 101 CLR 298. Kitto J had there observed (at 308) that:

… any inference favourable to the plaintiff for which there was ground in the evidence might be more confidently drawn when a person presumably able to put the true complexion on the facts relied on as the ground for the inference has not been called as a witness by the defendant and the evidence provides no sufficient explanation of his absence. …

18 These observations, it may presently be noted, are equally applicable in bankruptcy proceedings as they are in other proceedings: Micheletto v El-Debel [2020] FCA 1031, (2020) 17 ABC (NS) 284 (“Micheletto”). Gleeson J had there observed (at 304 to 305):

Witnesses not called

[120] Neither the bankrupt nor Ms Ayad gave evidence to this Court.

[121] The unexplained failure by a party to call a witness may, in appropriate circumstances, support an inference that the uncalled evidence would not have assisted the party’s case: Jones v Dunkel (1959) 101 CLR 298 at 308 per Kitto J, 312 per Menzies J and 320-321 per Windeyer J.

[122] Further, the failure to call a witness may also permit the court to draw with greater confidence any inference that is unfavourable to the party that failed to call the witness, if that inference is open on the evidence and the uncalled witness appears to be in a position to cast light on whether the inference should be drawn: Kuhl v Zurich Financial Services Australia Ltd (2011) 243 CLR 361, 384–385 at [63].

[123] Where the absent witness is a party, an adverse inference may be more readily drawn against that party: …

Her Honour in that case had “no hesitation in drawing any inference adverse to the bankrupt or Ms Ayad that may be available by reason of their respective failures to give evidence…”. [2020] FCA at [125]; (2020) 17 ABC (NS) at 305.

THE BACKGROUND FACTS

19 The sequestration order was made against the estate of Mr McMillan on 6 November 2018 and, upon the making of such an order, the property of Mr McMillan (at least for present purposes) thereafter became vested in the Trustee and available for distribution amongst the creditors of his bankrupt estate: Bankruptcy Act, ss 115 and 116(1)(a).

20 The facts of central relevance to the present proceeding are within a comparatively narrow compass, although the detail of each of a series of financial transactions and other events assume relevance to the case sought to be advanced by the Trustee.

21 Those facts, for present purposes, commence in May 1995 when Mr and Mrs McMillan purchased as joint tenants a property at 23 Hedges Avenue, Strathfield, which is a suburb of Sydney (the “Strathfield property”). The purchase price was $320,000. That property was purportedly transferred from joint names into the sole name of Mrs McMillan in May 2002 for a stated consideration of $1. There was some doubt raised during Mr McMillan’s cross-examination as to the date of the transfer. The transfer itself is dated by hand as having been executed on 25 May 2002. On 22 May 2002, Mr and Mrs McMillan had obtained a valuation of the property from a firm of Property Consultants, G A Dwyer & Associates, in the sum of $800,000. Left unexplained was a letter from Aitken McLachlan & Thorpe (a firm of solicitors retained by Mr and Mrs McMillan) around a month after the purported transfer date, dated 19 June 2002, enclosing the transfer for Mr and Mrs McMillan’s execution. The transfer was stamped on 8 July 2002. Mr McMillan was unable to explain the discrepancy during his cross-examination.

22 Originally, Mr McMillan commenced his career as a spray painter and panel beater. But it was in around August 2001 that Mr McMillan commenced on a new career path, that of being the sole dealer for Rolls-Royce and Bentley motor cars in New South Wales and the Australian Capital Territory.

23 In very summary form, the case for the Trustee is that an analysis of the restructure of the McMillan group of companies and an analysis of the financial dealings which facilitated the development of Mr Millan’s business activities exposes – as the Trustee would have it – a very comfortable inference that the purpose of transferring the Strathfield property into his wife’s sole name was for the “main purpose” of either:

preventing that property from becoming divisible among his creditors; or

to hinder or delay the process of making the property available for division among his creditors.

Mr McMillan, as the Trustee would have it, was distancing the assets of his wife from any claims that could be made by creditors. His “main purpose” in transferring the Strathfield property was but part of this broader objective.

24 And again in very summary form, the case for Mrs McMillan as the Respondent to the proceeding was that the Strathfield property was transferred at a time when her father had just died and that she simply asked her husband – and he agreed without hesitation – to her request for the transfer. There was, moreover, on the Respondent’s case, no reason to question that account because there were, at the time of the purported transfer, no financial circumstances indicating any reason to be concerned about any claim by any creditor. The sequestration order made in November 2018, Senior Counsel for the Respondent stressed, was made some 16 years after the transfer.

25 Notwithstanding the superficial simplicity of the competing positions advanced on behalf of the Trustee and the Respondent wife, it is necessary to examine in a little detail:

the corporate structure of the McMillan group of companies and, in particular, the resignation of Mrs McMillan as a director of McMillan Prestige Car Repairs Pty Ltd in 2001; and

the replacement in June 2002 of the trustee of the McMillan Family Trust.

It is also necessary to examine in a little detail:

the Commonwealth Bank loan in 1995 which provided monies for the purchase of the Strathfield property, and the variation of those loan arrangements in 2001.

Placed in chronological context, it was in late 2000 that the proposal emerged for Mr McMillan to take on the Rolls-Royce and Bentley dealership, the “Dealer Agreement” being signed on 1 February 2001. Operations were to commence in August 2001, some eleven or so months prior to the transfer of the Strathfield property. It is in this context that it is necessary to consider:

the content of the Rolls-Royce Dealership agreement;

the provision of a temporary finance facility in 2001 by the St George Bank to enable (inter alia) the purchase of motor vehicles for sale; and

the provision of a finance facility by Volkswagen Financial Services Australia Ltd in April 2002.

It is the coincidence of the timing of these arrangements which forms a large part of the basis upon which the trustee invites the Court to draw an inference as to Mr McMillan’s “main purpose”. From the Respondent’s point of view, it is also necessary to consider:

the Volkswagen dealership, that being the occasion – so the Respondent maintains – some two years after the purported transfer of the Strathfield property to Mrs McMillan, for the financial downfall of Mr McMillan.

If inferences are to be drawn from one or other of these transactions (or cumulatively), and the evidence of Mr McMillan is presently left to one side, it is useful to at least start from an exposition of the objective facts themselves. It is also necessary to refer to the documentary chain recording the transfer of the Strathfield property from the joint names of Mr and Mrs McMillan to Mrs McMillan alone, which took place in about May 2002.

The corporate restructure & trusts

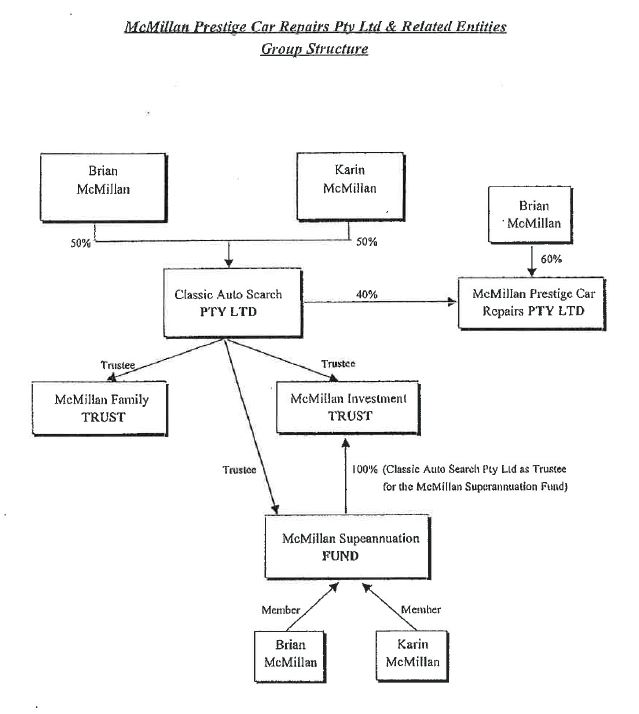

26 As at 2001, the corporate structure of the McMillan group of companies was depicted in a statement of accounts prepared by Mr McMillan’s accountant, Mr Geoffrey Vince, as follows:

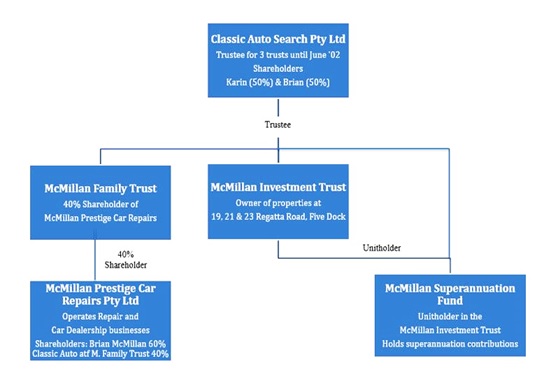

27 Prior to June 2002, a more detailed depiction of the role played by Classic Auto Search was as follows:

28 In May 2002, it may be noted that Mr and Mrs McMillan had retained the services of a firm of solicitors, Aitken McLachlan & Thorpe, in respect to their “General Personal Affairs” and “Estate Planning”. Part of the instructions given to that firm addressed what was referred to as “the change in Trustee”. The letter dated 3 May 2002 thus stated in part as follows (without alteration):

Geoff has asked us to assist by preparing documents to facilitate the change in Trustee of the McMillan Family Trust, from Classic Autosearch Pty Limited to another company which Geoff will incorporate. In order to do so, we will ask Geoff for a copy of the McMillan Family Trust Deed, together with a copy of your VW financing documents. At that time, we will advise further on what is necessary.

“Geoff” is a reference to Mr Geoffrey Vince, who was the accountant for the McMillan group of companies and close adviser to Mr and Mrs McMillan. A subsequent letter from the same firm of solicitors and dated 9 May 2002 concerning “Estate Planning” stated in part, albeit in expurgated form presumably to protect legal professional privilege, as follows:

I have requested Geoff Vince to let me have copies of the relevant Superannuation Fund Trust Deed and McMillan Family Trust Deed to ensure that any powers of appointment and the like are addressed. … I also note that a new trustee of the McMillan Family Trust is to be appointed, being a corporation in which Karin is no longer a director.

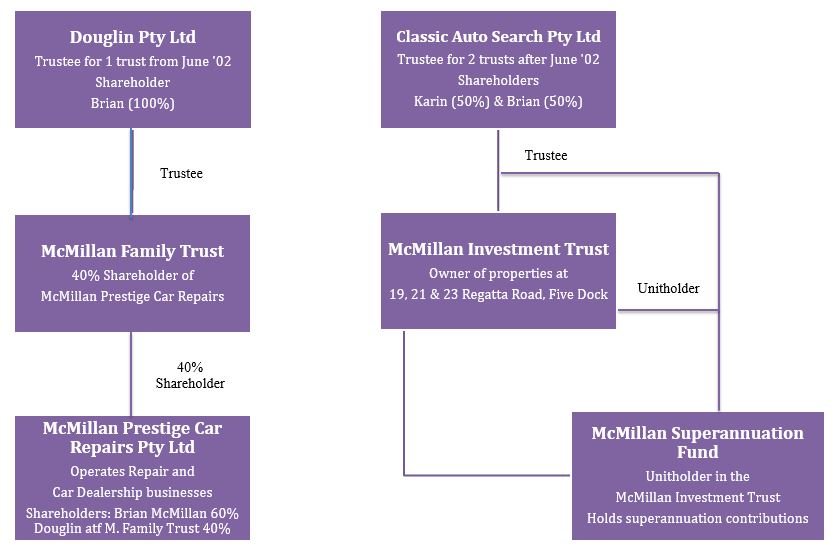

29 In June 2002, Classic Auto Search became the trustee of two trusts and Douglin Pty Ltd became the trustee of the McMillan Family trust, again depicted as follows:

The Deed of Appointment and Retirement of Trustee was executed on 26 June 2002. Pursuant to that Deed, Classic Auto Search Pty Ltd retired as trustee and Douglin Pty Ltd became the “new trustee”. After that date, the factual position accordingly was that:

Classic Auto Search, of which Mr and Mrs McMillan were equal shareholders, was no longer the trustee of the McMillan Family Trust, the trusteeship having been assumed by Douglin Pty Ltd; but

Classic Auto Search remained the trustee of the McMillan Investment Trust, being the entity which owned the Regatta Road properties, and also remained the trustee of McMillan Superannuation Fund.

Mrs McMillan had ceased to be a director of McMillan Prestige Car Repairs Pty Ltd in November 2001.

30 As at 30 June 2001 the Financial Statements prepared by Mr Vince recorded:

the McMillan Superannuation Fund as having “total members’ equity” of $438,158.22;

the McMillan Family Trust as having a “total equity” of $5,203.28;

McMillan Prestige Car Repairs Pty Ltd as having “total shareholders’ equity” of $734,678.74; and

the McMillan Investment Trust as having a “total equity” of $465,394.96.

The 1995 Commonwealth Bank loan & its variation in 2001

31 It was in March 1995 that Mr and Mrs McMillan obtained a bank loan from the Commonwealth Bank. That Bank had approved a loan of $103,000 to Mr McMillan and his wife to purchase the Strathfield property. The deposit for the property of $32,000 had been provided by Mrs McMillan, who had borrowed those monies from her mother. That deposit was repaid by McMillan Prestige Car Repairs between April 2002 and February 2003.

32 On 18 April 2001, the Commonwealth Bank approved a further facility in the sum of $520,000 to Mr and Mrs McMillan “to assist [them] with the purchase of two vehicles”. The security provided for the loan was stated to be (inter alia) a “Guarantee Joint and Several unlimited as to amount” by Mr and Mrs McMillan and a second registered mortgage over the Strathfield property.

33 On 21 September 2001, the Commonwealth Bank loan arrangement was varied. An “increase of $975,000” was then approved. The “previous approval” for $300,000 was increased to $1,275,000.

34 At the time of the increase it would appear that there was an outstanding loan of $300,000 in respect to 19 Regatta Road, Five Dock. That property had been acquired in April 1999 for a purchase price of $575,000. The increase in the facility being provided by the Commonwealth Bank enabled the purchase in October 2001 of the properties at 21 and 23 Regatta Road, Five Dock, each for a purchase price of $536,250. The properties were purchased by Classic Auto Search Pty Ltd as the trustee for the McMillan Investment Trust. The total purchase price paid for the three properties at Regatta Road, Five Dock was said by Senior Counsel for Mrs McMillan to be $1,647,500, comprised as follows:

19 Regatta Road | $575,000.00 |

21 Regatta Road | $536,250.00 |

23 Regatta Road | $536,250.00 |

Total | $1,647,500.00 |

35 Given that the increase in the Commonwealth Bank loan was to $1,275,000, Senior Counsel for Mrs McMillan suggests that Classic Auto Search Pty Ltd had an “equity” in these three properties of about $372,500 or about 22% as at October 2001. The 21 September 2001 letter from the Commonwealth Bank approving the increase in the facility being extended by the Bank “to assist [Mr and Mrs McMillan] in the purchase of commercial property at 21 and 23 Regatta Road …” enclosed a “Security Schedule”. That Schedule listed the securities as being:

“A Guarantee Joint and Several unlimited as to amount by BRIAN DOUGLAS MCMILLAN and KARIN ELISABETH MCMILLAN”;

a guarantee provided by McMillan Prestige Car Repairs supported by a first registered mortgage over its assets;

a second registered mortgage over the Strathfield property;

a first registered mortgage provided by Classic Auto Search Pty Ltd and the McMillan Investment Trust over the properties at 19, 21 and 23 Regatta Road; and

an equitable mortgage by Classic Auto Search Pty Ltd and the McMillan Investment Trust “over the whole of its assets”.

36 A subsequent letter from the Commonwealth Bank to Mr and Mrs McMillan dated 11 October 2001 itself attached a document dated 2 October 2001 signed by Mrs McMillan, in which she stated in part as follows:

…

I further acknowledge, as security provider for the Debtor, that my present maximum liability to the Bank under those documents is $1,275,000-00, plus all interest and amounts payable for discounts, costs, charges and expenses which the Bank may debit and charge to the account of the Debtor, or for which I am liable under my security(ies).

Schedule

Guarantee dated 23/4/1999, liabilities under which are secured by Mortgage dated 16/8/1999 over property at 23 Hedges Avenue, Strathfield NSW

The 23 April 1999 guarantee was not in evidence.

The emerging Rolls-Royce & Bentley dealership

37 The original business activities undertaken by Mr McMillan were that of a panel beater and spray painter. He repaired (inter alia) prestige motor vehicles. He conducted that business under the name of McMillan Prestige Car Repairs Pty Ltd from 1990.

38 In late 2000 through to the beginning of 2001, however, there emerged the proposal from Rolls Royce that Mr McMillan would operate a car dealership in addition to the business of repairing these vehicles.

39 Heads of Agreement were thus prepared on 19 December 2000 to which Mr Vince made some recommended changes on 25 January 2001.

40 The proposal itself may be found in a letter agreed to have a date of 31 January 2001 written by the Regional Manager, Australia & New Zealand, for Rolls-Royce & Bentley Motor Cars. The proposal was for the appointment of McMillan Prestige Car Repairs to be “Rolls-Royce & Bentley Motor Cars’ sole authorised Dealer for New South Wales and Australian Capital Territory”. A condition imposed included the redevelopment of premises at the corner of Queens Road and Regatta Road in Canada Bay. The redevelopment was to be completed by 1 August 2001. The “start date” was to be 1 February 2001. Rolls-Royce were to provide an interest free loan of AU$450,000 “to support the establishment of this new operation”.

41 On 1 February 2001, a “Dealer Agreement” was entered into between Rolls-Royce & Bentley Motor Cars Limited (RRBMC) and McMillan Prestige Car Repairs Pty Ltd. The Agreement was signed by Mr McMillan on behalf of McMillan Prestige Car Repairs. McMillan Prestige Car Repairs was identified as “The Dealer”. Part of the obligations assumed by McMillan Prestige Car Repairs pursuant to that Agreement included the following:

5. STOCK AND DEMONSTRATOR VEHICLES

5.1 The Dealer shall maintain a stock of new vehicles from the current delivery programme in accordance with the Brand Standards as amended from time to time.

5.2 The Dealer shall maintain a number of registered demonstrator vehicles in accordance with the Brand Standard and the agreed annual sales objectives.

5.3 The number of vehicles and the models to be kept in stock and used as demonstrator and showroom vehicles shall be agreed upon and recorded in writing when the sales target for the calendar year is agreed in accordance with Clause 4.1.

…

8. PARTS

8.1 In order to ensure sufficient supplies to meet customer needs in the Area of Responsibility, the Dealer shall constantly maintain a stock of parts in a quantity commensurate with needs, to be agreed in writing with RRBMC on an annual basis.

8.2 The Dealer shall comply with RRBMC’s requirements regarding the storage of the original parts to ensure appropriate safekeeping and processing.

8.3 The Dealer shall neither market nor use for the repair maintenance of the Contractual Products or corresponding goods parts which compete with and fail to meet the quality standard of the Contractual Products.

8.4 It is the Dealer’s obligation to obtain confirmation in writing of the quality and of the fitness for use from the part supplier in question. If the Dealer markets third-party parts, it shall store these separately from parts supplied by RRBMC.

Appendix 1 to the Agreement provided that the Showroom and Service Facilities were to be located at 19-27 Regatta Road, Five Dock. “Contractual Products” were defined in Appendix 2 as being “New ‘Bentley’ motor cars” and “Parts and Accessories for ‘Bentley’ Motor Cars supplied by RRBMC”. Appendix 5 contained the following terms and conditions:

Terms and Conditions for the sale of Contractual Products by RRBMC to the Dealer

…

8. RRBMC may make its acceptance of an order conditional upon part of the price being paid as a non-refundable deposit.

9. Unless otherwise agreed in writing between the parties, the full net price for Contractual Products shall be paid by the Dealer prior to delivery.

10. Payment shall be made by bank transfer to such account as RRBMC requests.

The temporary St George Bank facility

42 Condition 9 of Appendix 5 to the Dealer Agreement, it will be noted, provided that “the full net price for Contractual Products shall be paid by the Dealer prior to delivery”. There thus emerged the necessity for McMillan Prestige Car Repairs to secure finance to pay for the Contractual Products prior to delivery and until sold.

43 On 18 April 2001, the Commonwealth Bank approved a loan facility to McMillan Prestige Car Repairs Pty Ltd in the sum of $520,000 to facilitate the purchase of two vehicles.

44 By late June 2001, however, moves were on foot to arrange for a “temporary facility” until the new dealership was “up and running in Jan 2002”. Mr Vince had prepared a “Financial Package” at about that time. Included in that Package was a statement of the Operating Results for McMillan Prestige Car Repairs, disclosing the “operating results” for the three year period from 1998 through to 30 June 2000 being profits as follows:

1998 | $311,347 |

1999 | $119,939 |

2000 | $453,961 |

45 Part of the Financial Statement prepared by Mr Vince for the McMillan Family Trust separately recorded the “Total income” and “Expenses” and the resultant profit or loss for McMillan Prestige Car Repairs for the years ending 30 June 2000 and 2001 as being:

2000 | 2001 | |

Total income | $1,079,009.81 | $1,528,092.17 |

Expenses | $851,289.35 | $1,605,866.48 |

$227,720.46 | ($77,774.31) |

These accounts thus exposed a net loss for 2001 but a profit for 2000.

46 On 19 September 2001, the St George Bank forwarded to McMillan Prestige Car Repairs an “Indicative Finance Facilities Offer” which provided for:

a bailment facility of $2,000,000; and

an Import Letter of Credit Facility of $1,500,000.

The security to be provided was expressed as follows:

The securities for each facility are:

1. first ranking fixed and floating charge over all the assets and undertakings of McMillan Prestige Car Repairs Pty Limited.

2. first ranking real property mortgage from Brian McMillan over the property located at 23 Hedges Avenue Strathfield South NSW.

3. guarantees and indemnities by Classic Auto Search Pty Ltd, Brian McMillan and Karin McMillan.

Note: The amounts secured by the securities include the sum of the total amount owing for all facilities and other amounts. There are no limits on the amounts secured.

47 The offer was presumably accepted. On 19 November 2001, the St George Bank paid out the Commonwealth Bank for a total amount of $899,497.05. That amount was calculated as follows:

1. | payout of CBA business loan | $522,211.67 |

2. | payout CBA Home Loan | $162,120.14 |

3. | payout CBA Home Loan | $215,165.24 |

Total | $899,497.05 |

On the same date a Mortgage was executed by Mr McMillan in his own right and by Mr McMillan pursuant to a power of attorney on behalf of Mrs McMillan. The “fixed and floating charge”, as referred to in the Indicative facility offer dated 19 September 2001, was also executed by Mr McMillan and Mr Vince, both signing as directors of McMillan Prestige Car Repairs Pty Ltd on 19 November 2001. The “maximum prospective liability” in respect to the charge was expressed to be $7,000,000.

48 The facility offered by the St George Bank was itself thereafter replaced in April 2002 by an agreement between McMillan Prestige Car Repairs Pty Ltd and Volkswagen Financial Services Australia Limited.

The Volkswagen Financial Services facility

49 The Volkswagen Financial Services facility had its origins in a suggestion made by Mr Mark Tennant, the then Managing Director, Asia-Pacific for Rolls-Royce Motor cars and Bentley Motor cars. The suggestion was made in a letter to Mr McMillan dated 11 June 2001. That letter stated in part as follows:

Dear Brian,

I thought it would be useful ahead of my visit with Neil Morley in a couple of weeks, to give you some notice of the main areas we would like to discuss when we are with you. As you know, Neil’s role is, in broad terms, to ensure that our retail network develops the appropriate processes, practices and presentation for the Bentley marque – in short, to make sure our dealers are ready for MSB. In this context, Neil was the co-sponsor for Paul Evans’ recent visit to you, and much of our agenda is therefore derived from Paul’s findings.

FINANCE

This remains one of our biggest concerns, but in good part because we have absolutely no visibility of the financial state of your business.

It is of paramount importance that you establish the business on a solid financial footing. The impression we get at the moment is of an absence of financial separation between your personal situation and that of the business. Given the volumes we anticipate for NSW with MSB, you run the risk of being unable to make the best of the opportunity due to cash flow constrains. For example, you should anticipate a high volume of trade-ins against MSBs, both Rolls-Royce & Bentley product and other luxury marques. Our concern is that you will be unable to sustain the through-put of trade-ins, and thereby turn away MSB business.

As I hope you realize from our discussions on floor planning, and most recently the introduction to Volkswagen Financial Services, we are very keen to support you in this respect – but VWFS or any other finance company will require for greater transparency of your financial situation before agreeing terms.

Most immediately, therefore, I hope you have a good meeting with Oliver Schmitt and his colleague this week, and can come to some interim floor planning arrangements on your two landed cars to release funds for payment of the two units now at Crewe.

Mr McMillan responded on 2 July 2001 stating in part that he did “have [his] personal investment involved in the dealership” and that it was his “life, but [he had] no alternative to separate until a financial group is willing to support a floor plan – let’s hope VW come through”.

50 The agreement with Volkswagen did “come through” and was executed on 19 April 2002. It was an agreement between McMillan Prestige Car Repairs Pty Ltd and Volkswagen Financial Services Australia Limited, and was executed by Mr McMillan as sole director of McMillan Prestige Car Repairs Pty Ltd, Mrs McMillan having resigned as director in November 2001. The agreement was secured by a fixed and floating charge, the “Collateral Securities” there being described as follows:

Guarantee and Indemnity given by Brian Douglas McMillan, Classic Auto Search Pty Limited in its own right and as trustee for McMillan Family Trust in favour of VWFS dated on or about the date of this Charge.

The “maximum prospective liability” was stated to be $5,000,000. The exposure of Classic Auto Search, it may be noted, was exposure “in its own right and as trustee for McMillan Family Trust” – but not as trustee the McMillan Investment Trust. As a consequence of the Deed of Appointment and Retirement of Trustee executed on 26 June 2002, Classic Auto Search Pty Ltd retired as trustee of the McMillan Family Trust, and Douglin Pty Ltd became trustee.

The Transfer of the Strathfield property – May 2002

51 There was no contract in evidence of any sale by Mr McMillan of his interest in the Strathfield property to his wife.

52 That which was in evidence was:

an undated Discharge of Mortgage by the St George Bank, recording Mr and Mrs McMillan as Mortgagors;

the Transfer of the Strathfield property purportedly dated 25 May 2002, signed by Mr and Mrs McMillan as Transferors and Mrs McMillan as the Transferee and for a stated consideration of $1; and

a Mortgage dated 18 July 2002 over the Strathfield property to the St George Bank recording Mrs McMillan as the sole Mortgagor.

THE MAIN PURPOSE & SECTION 121(1)(b) – A MATTER OF INFERENCE

53 It was common ground that the principal question to be resolved in the present proceeding was whether, as a question of fact, Mr McMillan’s “main purpose” of transferring his half-share interest in the Strathfield property to his wife was either:

to prevent the transferred property from becoming divisible among his creditors; or

to hinder or delay the process of making property available for division among his creditors.

Expressed in this way, the claim made by the Trustee repeats the language of s 121(1)(b)(i) and (ii) of the Bankruptcy Act. It was not controversial that, as required by s 121(1)(a), the Strathfield property, the family home previously held by Mr and Mrs McMillan jointly, “would probably have become part of [Mr McMillan’s] estate or would probably have been available to creditors if the property had not been transferred”.

54 The onus was on the Trustee to prove that Mr McMillan’s “main purpose” was as claimed: Prentice v Cummins [2002] FCA 1503 at [97], (2002) 124 FCR at 90; Williams v Lloyd (1934) 50 CLR 341 at 372 per Dixon J (as his Honour then was). Proof of the “main purpose” required the Trustee to prove that the “purpose” was the “principal” or “leading” purpose or the “prevailing or most influential” purpose: Prentice v Cummins at [96]. Discharge of the onus required evidence of circumstances that give rise to “a reasonable and definite inference, not merely to conflicting inferences of equal degree of probability”: Cummins v Cummins [2006] HCA at [36], (2006) 227 CLR at 292 per Gleeson CJ, Gummow, Hayne, Heydon and Crennan JJ.

55 The Particulars set forth in the Trustee’s Statement of Claim as filed on 30 January 2020, in support of the central allegation as to Mr McMillan’s “main purpose”, were expressed as follows (without alteration):

Particulars

(i) The market value of the Strathfield property as at 25 May 2002 was well in excess of $1.

(ii) At the time of the Purported Transfer the Bankrupt had creditors which included a mortgage to the St George Bank dated 19 November 2001 (mortgage number 8367685L) with the respondent for a loan up to the amount of $1.5 million.

(iii) At the time of the Purported Transfer the Bankrupt had guaranteed the facility provided by VWFS to the trustee of the McMillan Family Trust.

(iv) The Purported Transfer took place at the same time as the trustee of the McMillan Family Trust was replaced so the transfer appears to be part of a reorganisation of the McMillan Prestige Group of companies.

(v) Following the Purported Transfer:

(A) The respondent was not a director of any trading companies in the McMillan Prestige Group of companies; and

(vi) The Bankrupt was the sole director of all trading companies in the McMillan Group; At the time of the transfer the Bankrupt had embarked on a risky venture as follows:

(A) the replacement of the trustee of the McMillan Family Trust;

(B) companies with McMillan Prestige Group of companies held the VW dealership for Five Dock and the Sydney dealerships for both Bentley and Rolls Royce);

(C) companies within the McMillan Prestige Group of companies had recently purchased in September 2001 new premises at 21 and 23 Regatta Rd Five Dock NSW for the Bentley and Rolls Royce Dealership.

56 Any evaluation of the evidence and the inferences to be drawn necessarily has to start from the fact that the Strathfield property was purchased in 1995 and transferred in mid-2002 for $1, in circumstances where the property had independently been valued at $800,000. But mid-2002 was some 16 years before the sequestration order was made against Mr McMillan. Viewed in isolation, those facts alone do not readily suggest the pursuit of some proscribed purpose – although the stated consideration of $1 certainly invites scrutiny. Hence the importance to the trustee of making good the inferences he invited the Court to now make.

57 In very summary form, it is concluded that:

although each of the individual Particulars if taken in isolation would only give rise to “conflicting inferences”, it is a consideration of the facts of relevance to each of those Particulars taken together which gives rise to the inference propounded by the Trustee.

The drawing of that inference is only further reinforced when a comparison is made between:

the facts prior to mid to late 2001; and

the prevailing facts in mid to late 2002.

Considerable reservations as to the reliability of Mr McMillan’s evidence and the failure to call witnesses have the consequence that his explanation for his reasons in transferring the property should be rejected.

58 Although each of the Particulars provided in support of the Trustee’s claims should be separately considered, it is the culmination of those Particulars which supports an inference as to Mr McMillan’s “main purpose”, an inference that is not adequately answered by the case sought to be advanced on behalf of the Respondent wife. Expressed differently, although none of the Particulars considered separately may lead to an inference adverse to Mr McMillan being drawn or an adverse inference as to his “main purpose” if taken in isolation, it is the “joining of the dots” exposed by those Particulars and the rejection of Mr McMillan’s evidence which dooms the Respondent wife’s case to failure.

59 It is thus concluded that the Trustee has discharged the onus resting upon him – the adverse inference the Court was invited to draw as to Mr McMillan’s “main purpose” being an inference which is a “reasonable and definite inference”: Cummins v Cummins [2006] HCA at [34], (2006) 227 CLR at 292 per Gleeson CJ, Gummow, Hayne, Heydon and Crennan JJ.

60 Mr McMillan’s evidence should thus be addressed, and thereafter:

each of the Particulars relied upon by the Trustee; and

the process of “joining the dots”.

Mr McMillan’s stated purpose – questions of credibility & reliability?

61 In his affidavit, Mr McMillan recounted the circumstances in which the property came to be transferred to his wife. It was in February 2002 that Mrs McMillan’s father had died. Prior to his death, and apparently as part of readying his affairs, the father had gifted his daughter a property at Stockton and given her a further $70,000 as a deposit for the adjoining property at Stockton. Stockton is a suburb of Newcastle in the State of New South Wales.

62 It was “shortly after” the father’s death that there was, on the account given by Mr McMillan, the following exchange:

Karin: I want the house to be in my name. It should have been anyway given I paid for Georges Hall and it was used to buy Strathfield.

[Mr McMillan]: I am happy with that.

The reference to Georges Hall was a reference to the former family home registered in the joint names of Mr and Mrs McMillan. This property had been purchased in March 1991 from the proceeds of the sale of two properties owned solely by Mrs McMillan. The request, according to Mr McMillan’s account in his affidavit, occasioned him no concern “because [he] always thought of it as her property anyway”.

63 This account was substantially repeated during his cross-examination where reference was made to the wife’s request and the following exchange then took place:

And I gather that your response to that was to accept what she asked and said, in effect, yes?––It took me a whole of a moment to answer yes. Whatever she asked, I said yes. It was done out of love. It was done out of her request. I put no reason behind it. I didn’t have any thinking behind it. I didn’t give it any consideration whatsoever.

So is this the position, then, that your wife expressed to you a belief that the home should be in her name because it was effectively hers anyway, is that how we understand it?––That’s how I always saw it.

…

So there was no issue between you and your wife as to your wife, as she would have it, effectively owning the home, is that right?––No issue whatsoever.

Mr McMillan, not unexpectedly, was challenged by Senior Counsel for the Trustee as to his reasons for the transfer. There was thus the following exchange between him and his cross-examiner:

But at the time, as you would have his Honour accept, the request was made you knew that VW had not asked for a personal guarantee from her in relation to the new facility and did not require a mortgage over Strathfield; correct?––Correct.

And the purpose of transferring the property into your wife’s name was simply to protect the family home for your wife and your children in case the expanding business did not succeed as planned; correct?––100 per cent incorrect.

You see, I want to suggest to you …?––Incorrect. I’m sorry.

… that having regard to what we know was occurring at the time, the real purpose of the transfer was to protect the property – screen assets in your wife’s name from risks that were perhaps then unknown in relation to your expanding business venture; correct?––Incorrect.

Do you accept that in April 2002 there was risk associated with your expanding business at all?––I accept every business has a risk. I’m a businessman. I accept every business has risk.

And the purpose, may I suggest to you, based on Mr Vince’s advice to transfer the family home into your wife’s name, was so that it would be put out of reach of your creditors?––Totally incorrect. I – I – if I could help you, I’ve only learnt about this terminology that you’re putting forward recently. At the time it was done out of integrity; it was done out of love. It was done – we didn’t have any thinking whatsoever – what you’re trying to frame, whatsoever, at all.

64 Without necessarily rejecting the evidence of Mr McMillan, reasons for reservation spring from a series of challenges made to his credit and the reliability of his evidence by Senior Counsel on behalf of the Trustee. Although other Particulars separately expose further reason to question the reliability of Mr McMillan’s evidence, for present purposes it is difficult to unquestioningly accept his account that the Strathfield property was “hers anyway” in circumstances where:

the finance provided by the Commonwealth Bank by way of mortgage to (inter alia) purchase the Strathfield property was a joint mortgage executed by both Mr and Mrs McMillan;

the deposit of $32,000 initially provided by Mrs McMillan pursuant to a loan provided by her mother was repaid by McMillan Prestige Car Repairs Pty Ltd; and

the mortgage repayments were paid by McMillan Prestige Car Repairs.

65 A residual reason for reservation also springs from the fact that Mr McMillan proved to be a person who was somewhat “loose with the truth”. He was thus a person who was prepared to present himself in a manner which best suited his purposes, with little regard for the factual accuracy of what was being said or represented. Thus, for example, in a “Personal Assets & Liabilities Statement” dated 7 September 2005 – obviously a date well after the May 2002 transfer of the Strathfield property – Mr McMillan was prepared to present his assets and liabilities as follows:

Assets | |

REAL ESTATE | |

159 Mitchell Avenue, Stockton | $925,000.00 |

161 Mitchell Avenue, Stockton | $2,250,000.00 |

23 Hedges Avenue, Strathfield NSW | $1,200,000.00 |

OTHER ASSET | |

Shares in McMillan Prestige Pty Limited | $5,000,000.00 |

Superannuation Fund | $1,350,000.00 |

Total Assets | $10,725,000.00 |

Liabilities | |

MORTGAGE | |

CBA Facilities | $3,500,000.00 |

Total Liabilities | $3,500,000.00 |

Net Value | $7,225,000.00 |

This statement concluded with the declaration signed by Mr McMillan that “the information given on this form is true and correct”. It was neither “true” nor “correct” for Mr McMillan to represent his assets as including the two Stockton properties, properties having a combined value in excess of $3 million and thus a little less than 50% of what was represented as his “Net Value”. Those two properties were in the sole name of his wife. The explanation provided by Mr McMillan for making this statement was said to be that he “had access to those assets to draw down against if [he] needed – that was all it was”. That explanation, with respect, is unsatisfactory.

66 Further reason to question the reliability of the account given by Mr McMillan as to why the Strathfield property was transferred into the sole name of his wife springs from the fact that Mrs McMillan was available to give evidence and had in fact filed an affidavit in the proceeding. The forensic choice made by Senior Counsel for Mrs McMillan, being the Respondent to the proceeding, was made at the conclusion of the evidence of her husband. Obviously the decision then made was, for whatever reason, not to call her. The onus of proof rested upon the Trustee and the central question of fact remained the “main purpose” sought to be pursued by Mr McMillan, a matter in respect to which he alone was perhaps the only relevant witness. It was his “main purpose” which had to be established by the Trustee and not any “purpose” or objective Mrs McMillan may have sought to achieve. Had the wife been called, however, she could have – and without being exhaustive – potentially given evidence going to such issues as:

the circumstances in which she had the conversation with her husband “shortly after” the death of her father and the request she then made to have the property transferred into her name; and

whether any advice had in fact been given by Mr Vince, whether the advice addressed any question as to asset protection from potential creditors and whether she had canvassed that advice with her husband.

Although recognising that such statements as have been made by Mrs McMillan may not throw much light (if any) upon an assessment as to what was motivating Mr McMillan at that point of time when he signed the transfer, it is perhaps not without some limited relevance to note that Mrs McMillan was being quite careful in accounting to her mother for the repayment of monies provided by way of loan. She was a person careful with accounting for debts that had been incurred. An undated letter from Mrs McMillan to her mother thus stated that “I have checked my paperwork and have summarised the monies we have received/paid”. That checking of the “paperwork” provided a careful account of the monies that had been advanced and stated that the “[t]otal amount of funds repaid including interest will be $102,820”. Repayment was to be by way of “12 instalments of $4,959.17”. The amounts repaid were “checked” by handwritten notations disclosing dates of repayment, the amounts repaid and the cheque numbers. Whatever may have been the attitude of her husband, Mrs McMillan was obviously a person astute in managing finances and ensuring debts – even to her mother – were fully repaid and accounted for. The letter, it must nevertheless be noted, was written in circumstances where the relationship between mother and daughter had apparently deteriorated – the letter cryptically stating that “[y]ou offered these monies in kind, now you are wishing them to be returned from anger”.

67 In the present case Mrs McMillan was, of course, a party. Notwithstanding a submission made by Senior Counsel on her behalf that an adverse inference should not be drawn, an inference is drawn that her evidence would not have assisted the submission that the transfer occurred, as Mr McMillan would have it, simply because his wife asked him to do it and it was “done out of love”: cf. Jones v Dunkel (1959) 101 CLR 298 at 308 per Kitto J; Micheletto [2020] FCA 1031 at [120] to [122], (2020) 17 ABC (NS) at 304 per Gleeson J.

68 Reservation is similarly expressed by reason of the failure on the part of the Respondent to call Mr Vince. Mr Vince could have potentially given evidence as to advice he had given regarding the transfer of the Strathfield property to possibly shed light on the reasons behind the transfer. Although no letter of advice was in evidence, it having been the subject of a subpoena but no production, it is nevertheless concluded that there was most probably a written advice or (at the very least) oral advice given by Mr Vince. So much follows from the reference in a Tax Invoice rendered by Aitken McLachlan & Thorpe in July 2002 to a “letter of advice”. Mr McMillan, moreover, when questioned as to advice given by Mr Vince, being to “screen” the family home from creditors, rejected that suggestion but accepted as follows that Mr Vince was available to give evidence as to the advice he had given:

… may I suggest to you that the letter of advice made quite clear that the purpose of the transfer of ownership of the family home was to screen or protect the family home from the unknown risks associated with the expanding business?––Totally incorrect.

And it explained that the purpose of the transaction was to put the family home out of the reach of your creditors, correct?––Incorrect. Didn’t have that thinking.

Can I just ask you, Mr Vince – he continues to practice as an accountant in Sydney, does he not?––I believe so.

Mmm?––Retired.

And he is someone who is able-bodied and able to speak and could potentially give evidence in a court case?––Yes.

And he – you would accept clearly provided advice in relation to the transfer of the interest of the family home to you and your wife and provided instructions to your solicitors in that regard?––After my wife asking to do it, yes.

An inability to produce a “letter of advice” some 18 years after it was given is, perhaps, understandable. But the failure to call Mr Vince, it is concluded, supports an inference that his evidence would not have corroborated the account being given by Mr McMillan or supported the case sought to be advanced by the Respondent wife. Mr McMillan, it may be noted, had little apparent difficulty in recalling at least the substance of the advice given so as to reject the proposition being put to him as “[t]otally incorrect”.

69 Given these reasons for reservation, Mr McMillan’s account as to the circumstances in which he transferred the Strathfield property to his wife cannot be accepted.

70 Such reasons for reservation in the acceptance of Mr McMillan’s evidence as to his purpose, however, do not necessarily lead to the acceptance of the Trustee’s claim. Reservation as to the reliability or credibility of Mr McMillan’s stated purpose for the transfer of the Strathfield property should not necessarily be translated into a total rejection of his evidence as being so implausible or unreliable that it should be rejected in its entirety. Reservation is simply a reason for caution in accepting (or not accepting) his evidence and a reason for testing his stated purpose against the inferences the Court was otherwise invited by the Trustee to draw from the available documents.

71 It forever remained a matter for the Trustee to prove that the “main purpose” in the transfer was for either of the purposes stated in s 121(1)(b)(i) or (ii) of the Bankruptcy Act. Reservation as to the acceptance of Mr McMillan’s evidence in this regard leaves open for resolution the question: if the transfer did not take place for the reasons set forth in his affidavit or for the reasons he expressed during cross-examination, what was his main purpose?

The St George indebtedness

72 The first two of the Particulars relied upon by the Trustee in support of his allegation as to the “main purpose” of Mr McMillan are expressed in the Statement of Claim as follows:

(i) The market value of the Strathfield property as at 25 May 2002 was well in excess of $1.

(ii) At the time of the Purported Transfer the Bankrupt had creditors which included a mortgage to the St George Bank dated 19 November 2001 (mortgage number 8367685L) with the respondent for a loan up to the amount of $1.5 million.

73 If (as has been expressed) reservations are held in respect to Mr McMillan’s explanation as to the circumstances in which the transfer of the Strathfield property occurred, the transfer of the property for a stated consideration of $1 certainly invites scrutiny. The more so is this the case when reference is made to the fact that the St George Mortgage dated 19 November 2001 was stamped, for duty purposes, at $1.5 million.

74 But nothing emerges, it is respectfully considered, from the St George Mortgage alone which supports any inference that the “main purpose” of the transfer was for either of the purposes relied upon by the Trustee.

75 The St George Mortgage replaced the earlier financial arrangement which had been entered into by Mr McMillan and his wife with the Commonwealth Bank in March 1995 and as varied in 2001. In addition to the repayment of the $32,000 loan and the mortgage repayments to the Commonwealth Bank being paid by McMillan Prestige Car Repairs undermining Mr McMillan’s assertion that the Strathfield property was “[Mrs McMillan’s] anyway”, the security provided to the Commonwealth Bank prior to its mortgage being discharged by the St George Bank raised further questions as to whether Mrs McMillan had in fact provided the guarantee for the Commonwealth Bank loan.

76 The Schedule to the Commonwealth Bank loan thus attracted attention during the cross-examination of Mr McMillan. On a list of securities, some were “ticked” by Mr McMillan and others were not. The suggestion advanced on behalf of the Trustee was that the absence of a “tick” adjacent to the reference to the guarantee meant that the guarantee had never in fact been provided. That suggestion is rejected. It is concluded that the guarantee was provided. So much, with respect, is apparent from the terms of the Commonwealth Bank letter dated 11 October 2001 and the enclosure of “a copy of the documentation that was executed and that forms part of the security position”. One of the documents enclosed was a document dated 2 October 2001 and signed by Mrs McMillan. It was in that document that Mrs McMillan acknowledged that her “present maximum liability to the Bank … is $1,275,000-00”. Although the 23 April 1999 guarantee was not in evidence, that which assumes present relevance is the acknowledgment in October 2001 on the part of Mrs McMillan as to her liability to the bank. And that amount extended not only to the home loan in respect to the Strathfield property but also the increase in the loan facility from $300,000 to $1,275,000 which had been approved on 21 September 2001.

77 A personal guarantee had thus been provided by Mrs McMillan to the Commonwealth Bank. And, contrary to a submission advanced on behalf of the Trustee, no inference can be drawn from the fact that the guarantee provided was limited to $1,275,000 in circumstances where the three Regatta Road properties had been purchased for about $1.65 million. As pointed out on behalf of Mrs McMillan, as at September/October 2001 it would appear that she and her husband had equity of about $372,500 in the properties. Nor can any inference be drawn from the fact that when the St George Bank financing replaced the earlier facility provided by the Commonwealth Bank, the Mortgage to the St George Bank was executed by Mr McMillan on behalf of his wife pursuant to a Power of Attorney. The Commonwealth Bank was paid out on 19 November 2001 and the Mortgage to the St George Bank was dated the same date. The security provided to the St George Bank also included a guarantee by Mrs McMillan. A Financial Statement prepared by Mr Vince recorded a profit of $227,720.46 for McMillan Prestige Car Repairs Pty Ltd for the year ending 30 June 2000 but a loss of $77,774.31 for the year ending 30 June 2001.

78 Just as Mrs McMillan had provided a guarantee to the Commonwealth Bank, she also provided a guarantee to the St George Bank. The provision of finance and the securities provided, obviously enough, preceded the May 2002 transfer of the Strathfield property.

79 But one of the recurring submissions made by Senior Counsel on behalf of the Respondent wife was that the personal guarantee being provided by the wife was inconsistent with the Trustee’s underlying proposition that the wife was trying to extricate herself from personal liability, and seeking to protect her assets from a claim being made in the future by potential creditors. Any “purpose” sought to be pursued by Mr McMillan in seeking to preclude creditors gaining access to the Strathfield property, so the submission ran, was inconsistent with the wife continuing to personally guarantee and thereby make her own personal assets available to creditors. This recurring submission, with respect, has considerable merit. Unanswered, it provides an obstacle to success on the part of the Trustee. Although the November 2001 St George Bank facility and securities provided preceded by some months the transfer of the Strathfield property in around May 2002, it nevertheless assumes considerable relevance in determining the “purpose” sought to be achieve by effecting the transfer.

80 Even though the personal guarantee given by Mrs McMillan may be but one of a number of other securities provided to the Commonwealth Bank, those other securities including mortgages over other assets, it nevertheless remains a security requested by both the Commonwealth and St George Banks and a guarantee in fact provided.

81 It is nevertheless the St George Bank Mortgage which is the subject of the Particulars provided by the Trustee in its Statement of Claim. This Mortgage was executed on 19 November 2001 and on that same day the St George Bank paid out the Commonwealth Bank for a total amount of $899,497.05. The mortgage incorporated a charge having a “maximum prospective liability” of $7,000,000.

82 No inference, it is concluded, can be drawn solely from the St George Bank Mortgage entered into on 19 November 2001 other than that the “purpose” being pursued by both Mr and Mrs McMillan was to pay out the Commonwealth Bank and to provide access to finance to fund the business activities of McMillan Prestige Car Repairs.

83 Had the Trustee sought an inference as to “main purposes” founded solely upon the first two of the Particulars provided, his claim for relief pursuant to s 120 of the Bankruptcy Act would in all likelihood have failed. But the relevance of those two Particulars was nevertheless to be evaluated not in isolation but as forming part of the “overall picture” to be gleaned from the Particulars in their entirety.

84 It is by reference to the subsequent Particulars that the picture sought to be painted by the Trustee started to take shape.

The guarantee of the VWFS Floorplan Facility

85 There was, of course, from the outset a need to provide finance for the acquisition of Rolls Royce and Bentley motor vehicles and spare parts for those vehicles, albeit perhaps for the unlikely event that those vehicles “failed to proceed”.

86 The third of the Particulars relied on by the Trustee in his Statement of Claim as a plank in the argument that the transfer of the Strathfield property was for either of the two main purposes relied on is that:

At the time of the purported Transfer the Bankrupt had guaranteed the facility provided by the VWFS to the trustee of the McMillan Family Trust.

The Volkswagen Financial Services Facility was executed on 19 April 2002, but had first been suggested by Mr Tennant on behalf of Rolls-Royce and Bentley in a letter to Mr McMillan on 11 June 2001. The agreement to provide finance pursuant to this facility, it is to be noted, nevertheless took place after the February 2002 exchange between Mr McMillan and his wife during which she requested him to transfer the Strathfield property but before the transfer of that property in around May 2002.

87 The 2002 facility had been preceded by:

the facility provided by the Commonwealth Bank and secured (at least in part) by a personal guarantee from both Mr and Mrs McMillan; and

the temporary facility provided by St George in November 2001, again secured (at least in part) by a personal guarantee from both Mr and Mrs McMillan.

The 2002 facility, by way of contrast, had been executed by Mr McMillan alone.

88 But no inference as to the “main purpose” of the kind pleaded by the Trustee should necessarily be drawn.

89 If attention is again confined to the period in about April/May 2002 and to the circumstances surrounding the Volkswagen Financial Services Facility being executed in April 2002, the fact is that at that point of time:

the primary security provided by Mr McMillan to Volkswagen included the Rolls-Royce and Bentley motor vehicles;

and that as at 30 June 2002:

the total amount owing under the facility was $2,188,070.06; and

the value of the “new vehicles” was $1,409,762.80 and the value of “Stock used vehicles” was $959,211, being a total of $2,368,973.80.

The amount then owing under the facility was thus less than the value of the motor vehicles which provided part of the security.

90 Those facts alone, however, do not deny the prospect that Mr McMillan may have envisaged at that point of time that the amount owing under the facility may well at some future date exceed the value in the vehicles themselves.

91 If attention is thus moved forward a year to determine the objective facts surrounding the security available, as at 30 June 2003:

the total amount owing under the facility was $3,111,948.06; and

the value of “new vehicles” was $1,122,585, the value of “vehicles in transit” was $605,070 and the value of “Stock used vehicles” was $1,273,221, being a total of $3,000,876.

As at 30 June 2003, the amount owing under the facility was slightly more than the security provided by the motor vehicles.