Federal Court of Australia

Court v Spotless Group Holdings Limited [2020] FCA 1730

Table of Corrections | |

2 December 2020 | In paragraph 51, “not” has been added as the fourth word. |

ORDERS

Applicant | ||

AND: | SPOTLESS GROUP HOLDINGS LIMITED Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to sections 33V and 33ZF of the Federal Court of Australia Act 1976 (the Act), settlement of the proceeding upon the terms set out in the Deed of Settlement and the Settlement Distribution Scheme (and any annexures therein) filed by the Applicant (together, the Settlement) be approved.

2. Pursuant to sections 33V and 33ZF of the Act, the Applicant is authorised nunc pro tunc for and on behalf of Group Members to enter into and give effect to the Settlement and the transactions contemplated for and on behalf of Group Members.

3. Pursuant to section 33ZB of the Act, the persons affected and bound by the Settlement are the Applicant, the Respondent and Group Members.

4. Pursuant to sections 33V and 33ZF of the Act, Slater and Gordon Ltd be appointed nunc pro tunc from 18 June 2020 as Administrator of the Settlement Distribution Scheme and is to act in accordance with the Court approved Settlement Distribution Scheme.

5. Pursuant to sections 33V(2), 22 and/or 23 of the Act and the Funding Terms approved by the Court on 8 May 2019:

(a) “Legal Costs and Disbursements”, being legal costs and disbursements of the Applicant on a solicitor and own client basis, including those incurred in connection with the proceeding on her own behalf and on behalf of all Group Members in the proceeding, be approved in the amount $7,856,318;

(b) “Project Costs”, further to the proportion of the Applicant’s Legal Costs and Disbursements paid by the Funders, are approved in the amount of $340,345;

(c) “Funders’ Remuneration”, be approved in the amount $19,500,324, being 22.5% of the settlement sum (net of costs);

(d) the “Applicant’s Reimbursement Payment”, being the Applicant’s reasonable claim for compensation for the time and/or expenses incurred in the interests of prosecuting on behalf of Group Members as a whole be approved in the amount $25,000; and

(e) the “Administration Project Costs”, being costs and disbursements incurred by the Applicant in connection with the administration of the Settlement Distribution Scheme be approved in the amount $211,165, without prejudice to the right of the Administrator to make application to the Court for approval of further “Administration Project Costs”.

6. Pursuant to rule 28.67 of the Federal Court Rules 2011 (the Rules):

(a) the report of Catherine May Dealehr dated 21 August 2020; and

(b) the supplementary report of Catherine May Dealehr dated 26 August 2020;

be adopted as varied to allow an uplift of 15% on Slater and Gordon’s conditionally incurred professional fees.

7. Pursuant to section 33ZF of the Act or otherwise, upon the coming into effect of orders 1, 2, 4 and 5 above, each of the undertakings given by:

(a) the Applicant;

(b) Slater and Gordon;

(c) Investor Claim Partner Pty Ltd;

(d) ICP Capital Pty Ltd;

(e) Therium Australia Limited; and

(f) Therium Litigation Finance AF IC,

to each other and to the Court to comply with their obligations under the Funding Terms attached as Annexure A to the orders of the Honourable Justice Murphy made 8 May 2019 be discharged.

8. Pursuant to rule 2.43(1) of the Rules, all amounts paid into Court by or on behalf of the Applicant as security for the Respondent’s costs of the proceeding, and any interest accrued on those amounts, be repaid to the solicitors for the Applicant.

Confidentiality

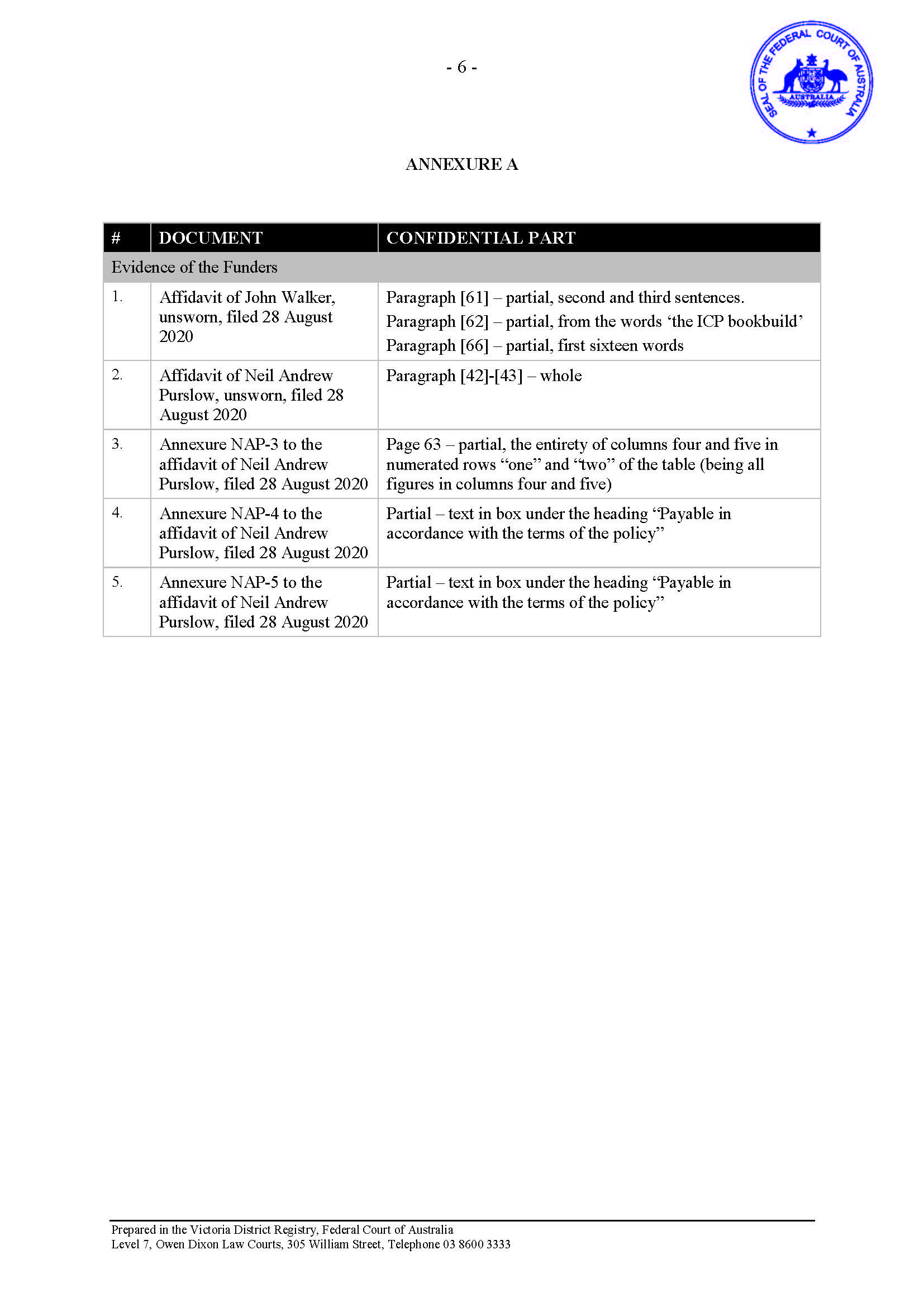

9. Until further order, pursuant to section 37AG(1)(a) of the Act, on the ground that the order is necessary to prevent prejudice in the proper administration of justice:

(a) the confidential annexures MGC-21 and MGC-33 to the affidavit of Mathew Glen Chuk dated 28 August 2020;

(b) the unredacted confidential annexures MGC-34 and MGC-35 to the affidavit of Mathew Glen Chuk dated 28 August 2020;

(c) the unredacted affidavit of John Walker dated 28 August 2020, and its annexures (Walker Affidavit);

(d) the unredacted affidavit of Neil Andrew Purslow dated 28 August 2020, and its annexures (Purslow Affidavit); and

(e) the passages set out in Annexure A to these orders, being redactions to mask commercially sensitive information in the Walker Affidavit and Purslow Affidavit,

be:

(i) confidential and not be published or made available to any person;

(ii) marked or designated as confidential; and

(iii) held on the Court file in accordance with (i) and (ii) hereof until further order of the Court.

10. The Funders will file forthwith versions of the Walker Affidavit and the Purslow Affidavit in which the passages set out in Annexure A and Annexure B to these orders have been redacted.

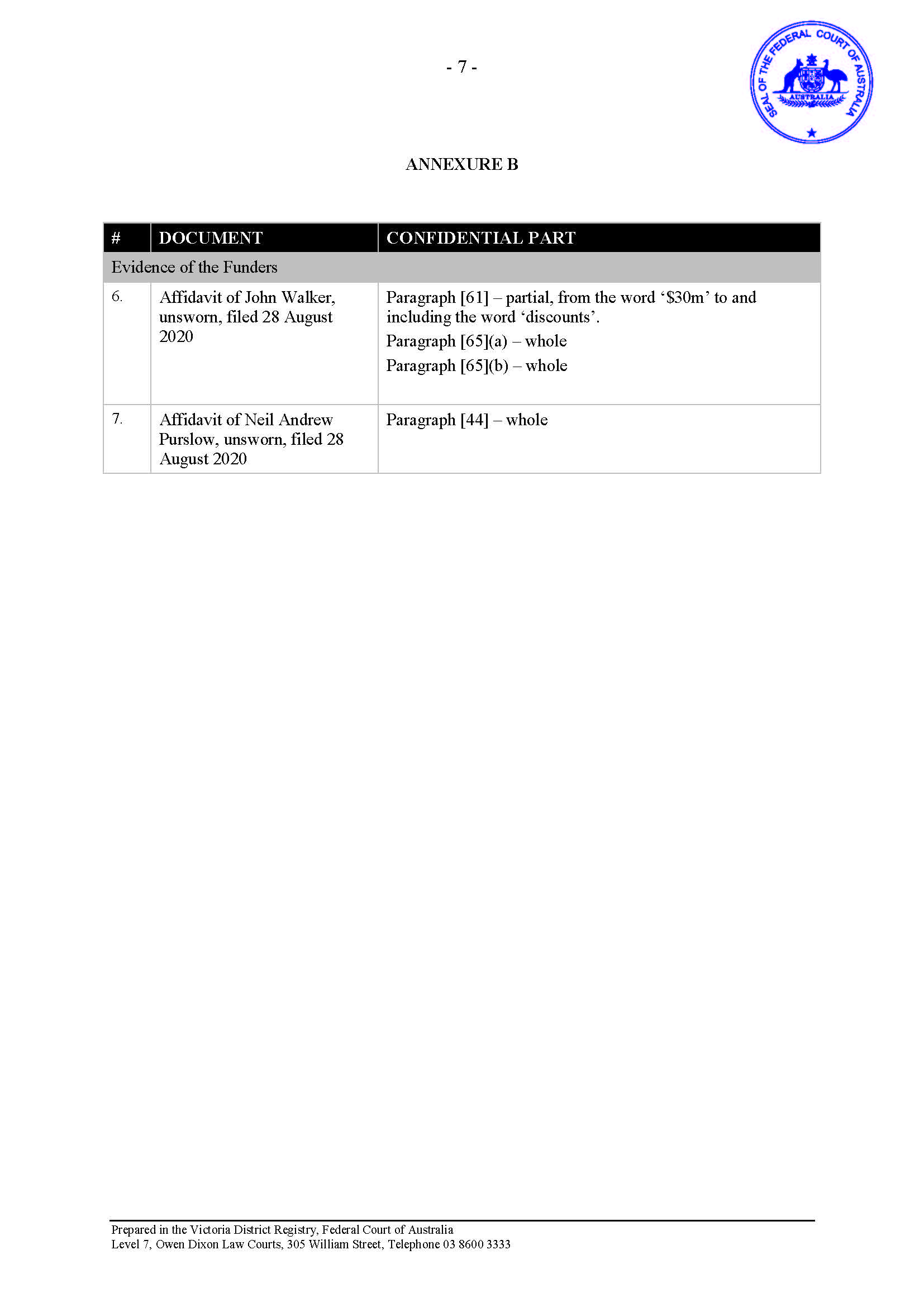

11. Pursuant to section 37AG(1)(a) of the Act, on the ground that the order is necessary to prevent prejudice in the proper administration of justice:

(a) the confidential annexures MGC-32, MGC-36, MGC-37 and MGC-39 to the affidavit of Mathew Glen Chuk dated 28 August 2020;

(b) the report of Catherine May Dealehr dated 21 August 2020; and

(c) the supplementary report of Catherine May Dealehr dated 26 August 2020; and

(d) the passages set out in Annexure B to these orders, being redactions to mask information which is sensitive if the litigation is to continue, in the Walker Affidavit and Purslow Affidavit,

be, until the expiry of the appeal period in respect of these Orders or determination of any appeal if filed, or further order:

(i) confidential and not be published or made available to any person;

(ii) marked or designated as confidential;

(iii) held on the Court file in accordance with (i) and (ii) hereof.

12. Upon the expiry of the appeal period in respect of these Orders or determination of any appeal if filed, the Funders will forthwith file versions of the Walker Affidavit and the Purslow Affidavit in which the passages set out in Annexure A to these orders have been redacted.

Late registrants

13. Pursuant to section 33ZF of the Act, the following Group Members are deemed to be Registered Group Members for the purposes of the Deed of Settlement and the Settlement Distribution Scheme and will be treated as if they complied with paragraph 8 of the orders made on 21 February 2020:

(a) L&J Stagoll ATF the Stagoll Super Fund A/C; and

(b) Deborah Jane Evans and James Robert Newton Morey in their capacity as executors of the estates of Daryl Garfield Ritchie, deceased.

Further listing

14. The Applicant has liberty to apply to re-list the proceeding as soon as practicable after completion of the distribution of the Settlement Sum (and must in any event do so no later than thirty days after such completion) so that final orders can be made, including orders that:

(a) the proceeding be dismissed on the basis that the dismissal is a defence and absolute bar to any claim (either directly or indirectly) or proceeding by the Applicant or any Group Member in respect of, or relating to, the subject matter of the proceeding, without prejudice to:

(i) the right of any party to the Deed of Settlement to make an application to enforce the Deed of Settlement in a new proceeding; or

(ii) the right of any Registered Group Member to make application to the Court in accordance with the terms of the Settlement Distribution Scheme; or

(iii) the right of the Administrator of the Settlement Distribution Scheme to refer any issues relating to the Settlement Distribution Scheme to the Court for direction or determination in accordance with the terms of the Settlement Distribution Scheme; and

(b) there be no order as to costs as between the Applicant and the Respondent.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A

ANNEXURE B

MURPHY J:

1 This is an application for Court approval of the settlement of a securities class action pursuant to s 33V of the Federal Court of Australia Act 1976 (Cth) (the FCA). The applicant, Alison Court, brought the class action against the respondent, Spotless Group Holdings Ltd (Spotless), alleging misleading or deceptive conduct and contraventions of the continuous disclosure regime in s 674 of the Corporations Act 2001 (Cth) (Corporations Act), doing so on her own behalf and on behalf of all persons who acquired an interest in fully paid ordinary shares in Spotless between 25 August 2015 and 1 December 2015. The applicant subsequently added as group members persons who acquired an interest in long exposure to Spotless’ shares by entering into equity swap confirmations in respect of such shares.

2 The proceeding was commenced on 25 May 2017 as an “open class” representative proceeding. Then, pursuant to orders made on 26 November 2018 and 21 February 2020 (the Class Closure Orders), the group members entitled to share in the settlement became 721 registered group members (Registered Group Members), of which 453 have entered into litigation funding agreements (Funded Group Members) with the litigation funders that jointly funded the proceeding. The litigation funders are Investor Claim Partner Pty Ltd (ICP) and ICP Capital Pty Ltd (ICP Capital) (together the ICP Entities), and Therium Australia Ltd and Therium Litigation Finance AF IC (Therium), collectively the Funders. The balance of the Registered Group Members have not entered into a litigation funding agreement (Unfunded Group Members).

3 The parties reached an in-principle settlement of the proceeding pursuant to which Spotless agreed to pay the applicant and group members the sum of $95 million inclusive of costs in full and final settlement of their claims, subject to Court approval (the proposed settlement). Under the proposed settlement the settlement sum, together with any interest that has accrued on it pending distribution to Registered Group Members, is proposed to be distributed in accordance with a proposed Settlement Distribution Scheme, following the deduction of Court-approved amounts for the applicant’s legal costs and disbursements, litigation funding charges, a reimbursement payment to the applicant and settlement administration costs.

4 I heard the settlement approval application on 2 September 2020. I was well-satisfied that the proposed settlement is fair and reasonable in the interests of group members to bound to it, including as between group members, and I made orders on 9 September 2020 to approve the settlement pursuant to s 33V of the FCA. Some questions arose in relation to:

(a) whether it was appropriate for the Funders to have been as closely involved in the settlement negotiations as they were;

(b) whether the settlement is fair and reasonable having regard to the fact that only Registered Group Members are permitted to share in the compensation achieved in the settlement but all group members are bound by the release and their rights will thereby be extinguished;

(c) whether the Court has power under s 33V(2) of the FCA to order a payment to the Funders in return for the costs and risks they took on in funding the proceeding, so that all group members who benefit from the settlement pay the Funders the same pro rata share of the litigation funding expenses incurred to achieve the settlement; and

(d) if the Court does have such power, whether the proposed funding commission is fair and reasonable.

I now provide reasons for the orders made.

THE EVIDENCE

5 The parties rely upon the following material:

(a) two affidavits with annexures of Mathew Glen Chuk, a practice group leader in the class actions practice of Slater & Gordon, the solicitors for the applicant, made 5 June 2020 and 28 August 2020. The relevant annexures include:

(i) a confidential joint opinion of counsel dated 28 August 2020 provided by Peter Collinson QC and Melanie Szydzik, senior and junior counsel briefed for the applicant in the proceeding, in relation to the reasonableness of the proposed settlement (Counsel’s Opinion);

(ii) a copy of the Slater & Gordon Conditional Legal Costs Agreement offered to group members as at 30 January 2017 (First CLCA);

(iii) a copy of the litigation funding agreement offered to group members by Therium Australia as at 30 January 2017 (Initial Therium LFA);

(iv) a copy of the Notice of Disclosure to the Federal Court made 12 October 2017 in relation to the Spotless Umbrella Co-Funding Agreement dated 20 July 2017 between the ICP Entities and Therium Australia, to which the applicant and Slater & Gordon are also parties (the Co-Funding Agreement), including a copy of:

(A) the amended Slater & Gordon Conditional Costs Agreement (Second CLCA) relating to the co-funded proceeding; and

(B) the amended litigation funding agreements offered by Therium Australia and the ICP Entities from approximately July 2017 (Amended Therium LFA and Amended ICP LFA), both of which include as a schedule the Terms of Engagement between Slater & Gordon and the Funders respectively (Terms of Engagement);

(v) a copy of the executed Deed of Settlement dated 29 May 2020 (Settlement Deed);

(vi) the proposed Settlement Distribution Scheme (SDS), including the confidential Loss Assessment Formula and confidential schedules relevant to the loss assessment formula;

(vii) a copy of the after the event Adverse Costs Insurance Policy (ATE Policy) entered into by the Funders with AmTrust Europe (AmTrust) to insure against any adverse costs liability up to a confidential limit;

(viii) copies of the invoices for the premiums in relation to the ATE Policy;

(ix) copies of invoices from AmTrust for deeds of indemnity provided by AmTrust in favour of Spotless as security for costs in 2018 and 2019; and

(x) a copy of the estimates of claim value modelling prepared by Slater and Gordon;

(b) an affidavit with an annexure of Michael Edward Russell, a partner of Colin Biggers & Paisley Pty Ltd, the solicitors for the respondent, made 28 August 2020;

(c) an affidavit with annexures of Neil Andrew Purslow, Chief Investment Officer of Therium, made 31 August 2020. The relevant annexures include:

(xi) a copy of the Terms of Engagement between Slater & Gordon and Therium Australia entered into on or about 30 January 2017;

(xii) a copy of the Initial Therium LFA offered by Therium Australia to potential claimants between January and May 2017;

(xiii) a copy of the Assignment and Assumption Deed dated 17 April 2019 by which Therium Australia assigned all of its rights and obligations under the Initial Therium LFAs and the Amended Therium LFAs to Therium Litigation Finance AF IC (Assignment Deed); and

(xiv) copies of the invoices for the premiums in relation to the ATE Policy;

(d) an affidavit with annexures of John Walker, Chief Executive Officer of Investor Claim Partner Pty Ltd and Managing Director of ICP Capital Pty Ltd and ICP Funding Pty Ltd, made 31 August 2020. The relevant annexures include:

(xv) a copy of the Co-Funding Agreement dated 20 July 2017;

(xvi) a copy of the litigation funding agreement offered by ICP and ICP Capital to potential claimants in the initial book building process (Initial ICP LFA); and

(xvii) copies of invoices paid by ICP Capital in respect of third party costs associated with the case.

6 In relation to the reasonableness of the applicant’s legal costs and disbursements two reports by an independent legal costs expert, Catherine Mary Dealehr, who was appointed as a referee pursuant to s 54A of the FCA (the Costs Referee), are before the Court.

THE KEY TERMS OF THE PROPOSED SETTLEMENT

7 The Settlement Deed is straightforward. Its key terms are as follows:

(a) Spotless agrees to pay $95 million inclusive of costs (Settlement Sum) in full and final settlement of the proceeding, with no admission as to liability;

(b) the Settlement Sum is to be paid within 35 days into a fund (the Settlement Fund) where it will be held by Slater & Gordon:

(xviii) on trust for Spotless until Final Settlement Approval (meaning either the expiry of the appeal period in respect of settlement approval orders without any appeal or application for leave to appeal being filed, or the disposition of any appeals from the settlement approval orders, whichever is the earlier); and thereafter

(xix) on trust for the applicant and group members;

(c) the applicant on her own behalf and on behalf of group members releases and discharges Spotless and its Related Parties jointly and severally from the Claims (as defined);

(d) Slater & Gordon covenants on behalf of itself and on behalf of its Related Parties not to bring or otherwise aid, abet, counsel or procure the bringing of any Claim by any person against Spotless or its Related Parties;

(e) the Funders’ covenant on behalf of themselves and on behalf of their Related Parties not to fund or otherwise aid, abet, counsel or procure the bringing of any Claim by any person against Spotless or its Related Parties; and

(f) Slater & Gordon and the Funders’ covenant on behalf of themselves and on behalf of their respective Related Parties, subject to their professional obligations, not to take any step to encourage any class member to cease to be the applicant or a class member, to opt out, to object to settlement approval or to appeal the settlement approval.

THE RELEVANT PRINCIPLES

8 The principles to be applied in a settlement approval application under s 33V are uncontentious. Fundamentally, the Court’s task is to decide whether the proposed settlement including the proposed distribution of the settlement is fair and reasonable having regard to the interests of the group members who will be bound by it, including as between group members. The Court assumes an onerous and protective role in relation to group members’ interests which is not unlike the role the Court assumes when approving settlements on behalf of persons with a legal disability: see Australian Securities and Investments Commission v Richards [2013] FCAFC 89 at [7]-[8]; Kelly v Willmott Forests Ltd (in liquidation) (No 4) [2016] FCA 323; (2016) 335 ALR 439 at [62]-[77]; Blairgowrie Trading Ltd v Allco Finance Group Ltd (Recs & Mgrs Apptd) (In Liq) (No 3) [2017] FCA 330; (2017) 343 ALR 476 at [81]-[85]; Caason Investments Pty Ltd v Cao (No 2) [2018] FCA 527 at [12]-[13]; Camilleri v The Trust Company (Nominees) Ltd [2015] FCA 1468 at [5].

9 The factors adopted in Williams v FAI (No 4) (2000) 180 ALR 459 at [19], as reflected in the Class Actions Practice Note (GPN-CA) (Practice Note) at 15.5, are a useful guide to the considerations relevant in deciding whether a proposed settlement is fair and reasonable. They include:

(a) the complexity and likely duration of the litigation;

(b) the reaction of the class to the settlement;

(c) the stage of the proceedings;

(d) the risks of establishing liability;

(e) the risks of establishing loss or damage;

(f) the risks of maintaining a class action;

(g) the ability of the respondent to withstand a greater judgment;

(h) the range of reasonableness of the settlement in light of the best recovery;

(i) the range of reasonableness of the settlement in light of all the attendant risks of litigation; and

(j) the terms of any advice received from counsel and/or from any independent expert in relation to the issues which arise in the proceeding.

WHETHER THE PROPOSED SETTLEMENT IS FAIR AND REASONABLE

10 I now turn to consider various relevant considerations.

Counsel’s Opinion

11 The relevant factors set out in Williams and the Practice Note are addressed in detail in a confidential Counsel’s Opinion prepared by the senior and junior counsel briefed for the applicant. Mr Collinson QC has been briefed as senior counsel in the proceeding since its inception and Ms Szydzik has been briefed since July 2017. Counsel’s Opinion is provided on the basis that it candidly and frankly discloses the factors which are material to the decision to accept a settlement and decide upon the SDS. The Counsel’s Opinion is both comprehensive and considered and it opines on the proposed settlement against the criteria set out in Williams and the Practice Note. Counsel recommend approval of the proposed settlement as being fair and reasonable in the interests of group members, and as between group members. I have relied heavily on Counsel’s Opinion in concluding that the proposed settlement is fair and reasonable, and its quality and the careful attention given to the relevant criteria gave me confidence in doing so.

12 I cannot go into the detail of the confidential Counsel’s Opinion, and it is unnecessary to go deep into the detail of the case. But it is worth briefly noting some matters which are material. In summary, the claim pleaded in the Third Further Amended Statement of Claim alleges that at the time that Spotless represented to the market on 25 August 2015 that it expected its 2016 financial year (FY16) results to materially exceed its 2015 financial year (FY15) results, and that it was confident that its FY16 net profit after tax (NPAT) of between 161 million and 161.5 million would be achieved (together the FY16 Guidance), Spotless did not have reasonable grounds for giving that guidance and it ought to have informed the market of the true position concerning the profitability of its business. Causes of action were pleaded for misleading or deceptive conduct in contravention of s 1041H of the Corporations Act, s 12DA of the Australian Securities and Investments Commission Act 2001 (Cth) (ASIC Act), s 18 of the Australian Consumer Law, being Schedule 2 to the Competition and Consumer Act 2010 (Cth) (ACL) and continuous disclosure contraventions of s 674(2) of the Corporations Act. Relief was sought in the form of declarations of the pleaded contraventions and damages pursuant to ss 1041I and 1317HA of the Corporations Act, s 12GF of the ASIC Act and s 236 of the ACL.

13 There were four main pillars to the applicant’s case:

(a) that one of the key representations made by Spotless on 25 August 2015 concerning its FY16 NPAT meant that there was an immediate and sizeable gap between the FY16 Guidance and Spotless’ internal forecast FY16 NPAT;

(b) that Spotless had failed to properly account for a number of FY15 one-off financial adjustments in its budget for FY16 which had the result of distorting the baseline earnings for FY16, creating a gap between the FY16 Guidance and Spotless’ internal budget or forecast;

(c) that Spotless’ ‘new business’ budget was overly aggressive and would not be achieved; and

(d) that acquisitions made by Spotless in FY15 in its Laundry and Linen Division and the acquisition of the AE Smith business were suffering integration issues that were unlikely to be resolved in FY16. The Laundry and Linen Division was also unlikely to achieve forecasted earnings as a result of other aspects of its business.

14 The case is factually and legally complex and it was strenuously contested. The proceeding did not settle in principle until the eve of trial, following two formal mediations which were held a long time apart. By the time of settlement, both parties had served all their lay and expert evidence, including the applicant’s reply expert evidence, and the expert conclave concerning materiality and loss had occurred. The expert evidence for the plaintiff comprises two industry expert reports, an accounting report, a materiality report, a loss report, and reply reports. The parties were therefore in a position to make a well-informed assessment of the strengths and weaknesses of their respective cases.

15 While the applicant’s case had reasonable prospects of success, it nevertheless faced a number of significant risks on liability, which are discussed in detail in Counsel’s Opinion. In relation to the risks of establishing loss and damage, the expert witnesses took quite different views. Having regard to Counsel’s Opinion and the discussion and analysis of the relevant considerations, I am satisfied that the proposed settlement falls comfortably within the range of reasonable settlements having regard to the attendant risks of the litigation. It is fair and reasonable and in the interests of class members to be bound to it, including as between class members.

The scope of the release

16 Clause 8.1 of the Settlement Deed provides that upon the later of (i) payment of the Settlement Sum into the Settlement Fund or (ii) Final Settlement Approval being obtained, the applicant on or own behalf and on behalf of all group members releases and discharges Spotless and its Related Parties jointly and severally from the Claims.

17 “Claim” is defined in cl 1.1 as follows:

Claim means:

(a) all claims made by the Applicant and Group Members against Spotless in the Proceeding;

(b) any claims the Applicant and Group Members may have against Spotless and/or their Related Parties:

(i) which are raised in the Proceeding;

(ii) which were at any time the subject of the Proceeding or any part of the Proceeding; or

(iii) which relate to the matters or issues the subject of the Proceeding or any part of the Proceeding, whether arising at common law, in equity or under statute.

18 “Related Parties” is defined to mean “the related bodies corporate of a Party as defined in the Corporations Act and the present or former directors, officers, partners, principals, employees, servants, contractors and agents of a Party and its related bodies corporate.”

19 The applicant submits that while, as in most settlements, the release is expansively drafted, in practical terms it does not extend beyond the matters the subject of the proceeding, so as to purportedly effect releases of unconnected claims. The applicant also notes that group members were advised of the fact of and the scope of the release in the Notice of Proposed Settlement and no group members objected on that basis.

20 The meaning of “relate to” is broad and I held a concern in relation to whether cl 1.1(b)(iii) of the Settlement Deed might purport to effect a release of group members’ individual non-common claims. The applicant has no representative authority under the FCA beyond the scope of the common claims that were or could have been the subject of the proceeding : see Timbercorp Finance Pty Ltd (in liquidation) v Collins; Timbercorp Finance Pty Ltd (in liquidation) v Tomes [2016] HCA 44; (2016) 259 CLR 212 at [53]-[54]. In the course of the approval hearing, senior counsel for Spotless informed the Court that, having regard to the reference in the opening words of cl 1.1(b) to “the claims of the Applicant and group members”, Spotless understood the release in (b)(iii) to mean “any common claims that the applicant and group members may have against Spotless, which relate to the matters or issues the subject of the proceeding or any part of the proceeding, whether arising in common law, in equity or under statute”; such that the release captures the common claims as pleaded and which could have been pleaded based on the same factual substratum. On the basis of senior counsel’s concession in open Court I am satisfied that the release does not go beyond the scope of the applicant’s representative authority.

21 The other terms of the Settlement Deed are unremarkable and of the kind commonly seen in settlement agreements in litigation of this type. In my view they are fair and reasonable in the circumstances of the case.

The preclusion of Unregistered Group Members

22 On 26 November 2018, I made orders, by consent, for class member registration and class closure pursuant to s 33ZF of the FCA. Order 12 provides that any class member who wished to participate in any distribution of any amount agreed in settlement of the proceeding was obliged to register their claim by 28 January 2019 (the Class Deadline). Pursuant to Order 12, registration could be accomplished:

(a) where a class member had already entered into a funding agreement with one of the Funders - by providing or taking all reasonable steps to provide specified share trading information to Slater & Gordon;

(b) where a class member had not entered into a funding agreement with one of the Funders - by executing a funding agreement with one of the Funders and providing or taking all reasonable steps to provide specified share trading information to Slater & Gordon; or

(c) by completing or taking reasonable steps to complete and return a Class Member Registration Form either online or in hard copy.

23 The orders provided for a regime under which notice of the requirement to register was provided to group members by:

(a) sending a notice to all persons who acquired a legal interest in ordinary shares in Spotless during the relevant period by use of the information in the share register;

(b) the applicant sending a notice to each class member who has entered into a funding agreement with one of the Funders; and

(c) Slater & Gordon posting a copy of the notice on its website.

24 Order 14 provides that, subject to any further order of the Court, any class member that neither opted out nor registered as a class member in accordance with Order 12 on or before the Class Deadline (Unregistered Class Member):

(a) shall remain a class member for all purposes, including for the purpose of being bound by any judgment in the proceeding and being entitled to participate in any award of damages by the Court if the proceeding does not settle; but

(b) will not be entitled to receive a distribution from any settlement of the proceeding, subject to Court approval, reached at or within 90 days after the conclusion of a mediation then set to occur by no later than 29 March 2019, but will be bound by the terms of any settlement agreement approved by the Court in respect of such settlement.

25 On 21 February 2020, I made further Class Closure Orders pursuant to s 33ZF of the FCA, again by consent. The orders fixed 16 March 2020 as an extended Class Deadline by which any class member who wished to share in the proceeds of any settlement of the proceeding must register their claim. The orders included a further regime for giving notice to group members by the same methods as the earlier notice. The effect of the orders was to again notify group members of the requirement to register and to extend the period within which they could do so.

26 Order 10 of those orders provides that, subject to any further order, any class member who failed to register by 16 March 2020 and had previously failed to register:

(a) shall remain a class member for all purposes, including for the purpose of being bound by any judgment in the proceeding and being entitled to participate in any award of damages by the Court if the proceeding does not settle; but

(b) will not be entitled to receive a distribution from any settlement of the proceeding, subject to Court approval, but will be bound by the terms of any settlement agreement approved by the Court in respect of such settlement.

27 Mr Russell deposes, and I accept, that the notices to be sent to group members pursuant to the Class Closure Orders were distributed by email and/or post consistently with those orders. The effect of the Class Closure Orders, coupled with the release in the Settlement Deed, means that group members who neither opted out nor registered by 16 March 2020 continue to be group members; are therefore bound by the release in the Settlement Deed, but precluded by the orders from sharing in the compensation achieved through the settlement.

28 On 22 April 2020, the NSW Supreme Court of Appeal handed down Haselhurst v Toyota Motor Corporation Australia Ltd t/as Toyota Australia [2020] NSWCA 66 (Payne JA with whom Bell P, Macfarlan, Leeming JJA and Emmett AJA agreed). The Court held that the class closure order made in in the early stages of that proceeding was beyond the power of s 183 of the Civil Procedure Act 2005 (NSW) (CPA), the counterpart to s 33ZF of the FCA. The Court concluded (at [99]), that the construction of Part 10 of the CPA (and by implication Part IVA of the FCA) preferred by the majority in BMW Australia Ltd v Brewster [2019] HCA 45; (2019) 374 ALR 627 was inconsistent with acceptance of dicta in Melbourne City Investments Pty Ltd v Treasury Wine Estates Limited [2017] FCAFC 98; (2017) 252 FCR 1 at [74]-[75] (Jagot, Yates and Murphy JJ) that the Court had power under s 33ZF to make certain types of class closure orders.

29 In Haselhurst the Court expressly contemplated the possibility that class closure orders could be made upon settlement approval or judgment under ss 173, 177 and 179 of the CPA, those sections being the counterparts of ss 33V, 33Z and 33ZB of the FCA: Haselhurst at [53], [87], [105] and [108]. The Court recognised (at [108]) that Part 10 of the CPA specifically envisaged that group members’ rights could be extinguished upon approval of a settlement under s 173 or following judgment under s 177.

30 Following Haselhurst, different judges of this Court continued to affirm that this Court has power under s 33V and 33ZB of the FCA to make orders binding on all group members to approve a settlement which disentitled unregistered group members from sharing in proceeds of settlement yet extinguished their claims: see Inabu Pty Ltd as trustee for the Alidas Superannuation Fund v CIMIC Group Limited [2020] FCA 510 at [8] (Jagot J); Fisher (as trustee for the Tramik Super Fund Trust) v Vocus Group Ltd (No 2) [2020] FCA 579 at [61] (Moshinsky J); Cantor v Audi Australia Pty Ltd (No 5) [2020] FCA 637 at [431] (Foster J) and Uren v RMBL Investments Ltd (No 2) [2020] FCA 647 at [26] and Webster (Trustee) v Murray Goldman Co-operative Co Limited (No 4) [2020] FCA 1053 at [24] (Murphy J).

31 Subsequently, on 4 June 2020, the NSW Supreme Court of Appeal handed down Wigmans v AMP Ltd [2020] NSWCA 104 (Macfarlan, Leeming and White JJA). The Court held that Part 10 of the CPA did not authorise the giving of a notice to group members before mediation which stated that group members who did not register may not be entitled to receive a distribution from any settlement that might be agreed at or within a specified period after the mediation, and foreshadowed that the parties intended to apply for an order that such group members be excluded from receiving a benefit from such a settlement: Wigmans at [25]-[26], [32], [34] and [132].

32 In Wigmans, which included two members of the Court in Haselhurst, the Court expressed a somewhat different view to that in Haselhurst as to the power of the Court to extinguish group members’ rights without their receiving any compensation upon settlement approval under s 173 of the CPA or following judgment under s 177. The Court said that a settlement under which group members who have not registered receive nothing and in which their rights against the respondent are extinguished, is “contrary to the essence of the opt out regime” (at [95]), at least unless unregistered group members are notified and given an opportunity to participate after settlement: at [128]. The Court considered that a settlement which extinguished the rights of group members without payment to be contrary to a “fundamental precept” of Part 10 of the CPA, inherent in the legislative choice of an opt out regime, that group members need take no positive step before settlement (at [79], [131]-[132]), and involved an “insoluble” conflict of interest between registered and unregistered group members: at [79], at [118], [120], [129] and [132]. The Court said that the decisions in Inabu and Vocus, which sought to distinguish Haselhurst and followed the approach of Beach J in Newstart 123 Pty Ltd v Billabong International Ltd [2016] FCA 1194 at [68], to be of no assistance being settlement approvals by consent: at [113]-[117].

33 The decisions in Haselhurst and Wigmans cast doubt on the validity of the Class Closure Orders made in the present case, but I am nevertheless satisfied that the proposed settlement is fair and reasonable in the interests of group members and as between group members.

34 This is so, first, because the Class Closure Orders were not challenged by either party or any class member. Consequently, as orders of a superior court of record they remain valid until set aside: State of New South Wales v Kable [2013] HCA 26; (2013) 252 CLR 118 at [32]. It is the Class Closure Orders which provide that Unregistered Group Members are not permitted to share in any distribution of the Settlement Sum; that condition does not directly arise from the Settlement Deed. It is also relevant that the Class Closure Orders were made before Haselhurst and Wigmans were handed down and the parties, including the applicant acting as the group members’ representative, proceeded on the basis that the orders were valid and of legal effect.

35 Second, it is plain that the Class Closure Orders were important to the parties in achieving the settlement. Mr Russell deposed that the orders, together with the releases provided by the applicant on behalf of herself and group members, were “extremely important” and “essential” in giving Spotless the finality and certainty needed to agree to the $95 million settlement.

36 Third, the settlement benefits the substantial body of group members who took the time to register their claims and are now able to share in a substantial settlement which avoids the further expense, inconvenience, uncertainty and risk of ongoing litigation. Group members were given notice, by use of the share register, on two separate occasions more than one year apart, of the requirement to register if they wished to share in the proceeds of any settlement which was achieved. The notices informed them that should they neither register nor opt out before the Class Deadline they would be bound by any settlement achieved and thus lose their right to claim damages but be precluded from sharing in the settlement monies.

37 Fourth, Unregistered Group Members were expressly informed in the Notice of Proposed Settlement that if they had not registered the applicant intended to seek orders confirming that they are not entitled to a distribution of money from the settlement, and would nevertheless be bound by the terms of the settlement. They were informed that if they wished to object to the proposed settlement or any aspect of it they were required to complete and return a Notice of Objection. This is not the same as the post-settlement registration process contemplated in Wignams (at [128]), but it is worth noting that only two Unregistered Group Members objected to the settlement. The settlement approval orders provide for both of those group members to be treated as having registered.

38 I am not aware of any group member who asserts that he or she has been disadvantaged by this aspect of the proposed settlement. I consider the preclusion of Unregistered Group Members from sharing in the proceeds of settlement in circumstances where their rights are extinguished by the release is not a reason to decline to approve the settlement.

The reaction of the class to the proposed settlement

39 There were two objections to settlement approval filed by class members in the proceeding being:

(a) L&J Stagoll as trustee for The Stagoll Super Fund A/C; and

(b) Deborah Jane Evans and James Robert Morey in their capacity as executors of the estate of Daryl Garfield Ritchie deceased.

40 The notice of objection filed by Mr and Mrs Stagoll said that the only communication they had received in relation to the proceeding was the Notice of Proposed Settlement, which had been forwarded to them by their previous share broker. Their previous broker had ceased to act for them from November 2018. The notice of objection filed by Ms Evans and Mr Morey said that the deceased died in early 2017 and that the estate had been administered by one of the deceased’s daughters, Gail Harrison. Ms Harrison however became unwell with cancer and required regular hospital admissions, and she was away from home, away from the post, and had many things on her mind. Then there was a challenge to the will of the deceased, which was also very stressful for Ms Harrison. Ms Harrison died in November 2019, age 66. Ms Evans and Mr Morey said that they could not say whether Ms Harrison ever received a class member registration and class closure notice, but they could say that such notices were never brought to their attention and they had no knowledge of the requirement to register.

41 I was satisfied that it would be unjust to exclude the two objectors, including having regard to the decision in Wigmans: see Money Max Int Pty Ltd v QBE Insurance Group Ltd [2018] FCA 1030; (2018) 358 ALR 384 at [44]. The orders provide that they be treated as if they had registered their claim pursuant to the Class Closure Orders made on 21 February 2020.

THE FUNDERS’ INVOLVEMENT IN SETTLEMENT NEGOTIATIONS

42 Mr Walker deposes that he knows Jeffrey Gray, Spotless’ representative in the settlement negotiations, having met him in relation to other litigation he had been involved in. He said the following about his interaction with Mr Gray in relation to settlement of this proceeding:

On 30 January 2019, Mr Gray called me and commenced without prejudice discussions aimed at settlement of the claims in these proceedings. With approval of Slater & Gordon I commenced discussions which culminated in the unsuccessful mediation on 22 March 2019.

On 27 February 2020, Mr Gray again contacted me on a without prejudice basis to prepare for the mediation convened on 17 April 2020. That mediation was unsuccessful in the day but provided a base for subsequent without prejudice discussions between him and me directly, and then between the law firms, culminating in an in-principle settlement of the claims advanced in the proceeding on 18 May 2020.

43 As I have said, I am satisfied that the proposed settlement is comfortably within the range of reasonable settlements of the proceeding having regard to the attendant risks of the litigation and it is in the group members’ interests. Very little information is provided in relation to the negotiations, and there is no basis to conclude that Mr Walker’s involvement in the settlement negotiations adversely affected group members’ interests. I accept that his involvement may have benefited group members. Even so, in my view it was inappropriate for the Funders, through Mr Walker, to have direct negotiations with Spotless as they did. In my view such a practice is to be deprecated.

44 In Fostif Pty Ltd v Campbells Cash & Carry Pty Ltd [2005] NSWCA 83; (2005) 63 NSWLR 203 at [137] Mason P accepted that in funded proceedings it is essential for the litigation funder to have some control over the proceeding for it “to protect its legitimate interests”. On appeal, in Campbell’s Cash & Carry Pty Ltd v Fostif Pty Ltd [2006] HCA 41; (2006) 229 CLR 386 at [89], Gummow, Hayne and Crennan JJ said that it was “hardly surprising” that a person who invests in a proceeding wishes to control it. Here my concern is not so much one of ‘control’, although that may lie behind Mr Walker taking a lead role in settlement negotiations, rather than the applicant’s lawyers. My concern is that the Funders’ involvement in negotiations occurred in circumstances of a potential conflict of interest.

45 Good faith and knowledgeable bargaining leading to the maximisation of a possible settlement is particularly important in the context of a class action since the interests of absent class members must be adequately represented and protected by the applicant’s lawyers: see A Conte, H Newberg, Newberg on Class Actions, Thomson West, Fourth edition, 2002, at 15.26. Not all the Registered Group Members have entered into funding agreements with the Funders, or signed retainers with Slater & Gordon.

46 That a funder may suffer from a conflict of interest in relation to settlement negotiations is plain. As the ALRC report , Integrity, Fairness and Efficiency - An Inquiry into Class Action Proceedings and Third-Party Litigation Funders, December 2018 (ALRC Report) notes (at 6.94):

Litigation funders are in a unique position. They fund litigation and can give directions to the plaintiff’s solicitors, but they are not the client. This can create numerous situations of conflicts not addressed by the regulatory mechanisms that aim to manage conflicts…

Such conflicts were, at the relevant time, largely regulated by Regulatory Guide 248 - Litigation Schemes and Proof of Debt Schemes: Managing Conflict of Interest (2013) (Regulatory Guide 248) which notes that “[t]he nature of the arrangements between the parties involved in a litigation scheme…has the potential to lead to a divergence between the interests of the members and the interests of the funder...”: at 248.11. It requires that funders have in place and follow continual “robust arrangements for addressing potential, actual or perceived conflicts of interest”: at 248.13. Doubts have been expressed as to the effectiveness of Regulatory Guide 248 in regulating a funder’s conflicts of interest: ALRC Report at 6.106-6.107, 6.109-6.114

47 Those with experience of settlement negotiations in representative proceedings understand that it is sometimes the position that a funder’s interests in relation to settlement do not coincide with the interests of the applicant and group members. Some different economic drivers operate in relation to a funder as compared to the applicant and group members, and it is not uncommon for there to be a real disparity in the views of the applicant’s lawyers and the funder as to the appropriate settlement range. It is common too that the likelihood of there being such a difference in view is recognised by the respondent. In Perera v GetSwift Limited [2018] FCA 732; (2018) 263 FCR 1 at [32] Lee J observed, and I respectfully agree:

…By reason of the very nature of the commercial model I have described, a desire exists on behalf of the funders to not only obtain a return, but to obtain that return with celerity. To those acting for applicants, there is a need to be alive to the possibility arising of a conflict between the commercial imperatives and demands of the funder, and the interests of the applicants and group members in maximising the recovery of their claims. To suggest simplistically that there is always an alignment between the funder and group members (because each have an interest in maximising relevant claims) is to fail to appreciate the difference between a commercial enterprise seeking consistent and predictable returns (and management of risk spanning a number of projects), with the position of a group member involved in one action who has a relatively small amount at stake which the group member may be willing to wager on the possibility of a greater return…

48 Amongst other things, a funder may see settlement for a particular amount or at a particular stage as desirable having regard to its financial position and exposure to risk, whereas the applicant and group members having contracted to receive the benefit of the funder’s financial resources may take a different view. Or a funder may take a portfolio-based view of the risks and potential damages, whereas for the applicant and group members the particular case may be their only shot and they do not take into account any other exposure faced by the funder. The authors D Grave, K Adams and J Betts, themselves experienced class action litigators on the defence side, noted in Class Actions in Australia (Lawbook Co, Second edition, 2012 at p 858):

Circumstances might arise in which the funder wishes to settle the proceeding for what the funder regards as a reasonable offer of settlement, whereas group members wish to advance the proceeding to trial, hoping for a better outcome. If the proceedings are continued, the funder’s investment may be at risk. For example, if the matter proceeds to a judgment which falls below the amount of the settlement offer, the funder may receive a lower commission or the funder’s overall return may be diminished by an adverse costs order.

49 The potential for such conflicts of interest does not however mean that it is inappropriate for a funder to have input into settlement negotiations. Regulatory Guide 248 requires funders to have in place and follow robust arrangements for addressing potential, actual or perceived conflicts of interest” and compliance with such arrangements may ameliorate the risk. Further, the Practice Note requires that any funding agreement includes provisions for managing conflicts of interest, and provides that “the applicant’s legal representatives have a continuing obligation to recognise and manage properly any conflicts of interest”: Practice Note at 5.9 and 5.10. The Funding Terms in the present case include a mechanism whereby, if the Funders and the applicant disagree as to whether or on what terms a settlement offer should be made or rejected, it is to be resolved by obtaining the opinion of senior counsel, which opinion shall be final and binding. Compliance with that requirement may also ameliorate the risk.

50 I consider that in the present case it was appropriate to give the Funders real input in relation to settlement given that they are paying the applicant’s legal costs, meeting security for costs and obliged to pay any adverse costs order, and are authorised to provide day-to-day instructions to the applicant’s solicitors. The Funders could be expected to bring to the settlement negotiations an understanding of the costs of failure in the case, as opposed to the applicant who is not exposed to any risk other than the risk of not obtaining any damages if the case is lost. It is appropriate that the risks the Funders face be reflected in settlement discussions.

51 But that does not mean that it is appropriate for a funder to be directly involved in settlement negotiations, particularly in the absence of the applicant’s lawyers, as occurred in the present case. As the ALRC Report recognises, misconduct by a funder “might consist of almost undetectable behaviours, such as subtle (but inappropriate) pressure to settle”: ALRC Report at 6.114. In settlement negotiations subtle indications can carry substantial import. The funder may suffer from a conflict of interest and where the funder is directly involved in settlement negotiations, the indications it gives might move a case towards the funder’s preferred settlement outcome.

52 It is important to keep in mind that, unlike the applicant’s and group members’ lawyers, litigation funders are not officers of the Court; they do not owe ethical obligations to the Court or to the applicant and group members; and they do not owe fiduciary obligations to the applicant and group members. They are commercial parties funding litigation for profit and, particularly in a large and expensive class proceedings involving substantial risk, it is likely that their commercial interests will be front of mind.

53 Given the potential for conflicts of interest I do not consider it to have been appropriate in the present case for the Funders to have been directly involved in the settlement discussions, nor appropriate for the applicant’s lawyers to have allowed that direct involvement. The applicant’s lawyers, both solicitors and counsel, have fiduciary obligations to seek to advance the interests of the applicant and group members, including by bargaining for the largest possible settlement. One might ask how they can satisfy that obligation if they allow the negotiations to be conducted through a funder which may suffer from a conflict of interests or if they do not control the settlement negotiations.

54 I accept that there may be circumstances where there is an identifiable advantage for the applicant and group members in having negotiations conducted through a funder, but that will be the exception rather than the rule, and great care must be taken to manage any potential conflict of interest. In the present case, which has a potential claim value in excess of $100 million, it is difficult to understand why the settlement negotiations were not conducted by experienced senior counsel and senior solicitors. If the Funders wanted substantial input into those negotiations that could readily have been facilitated.

55 In my view the Court should give consideration to amending the Practice Note so as to provide guidelines in relation to the appropriate lines of demarcation between the applicant’s lawyers and the funder in relation to settlement negotiations.

THE PROPOSED SDS

56 For the proposed settlement to be fair and reasonable in the interests of group members, including as between group members, the SDS must achieve a fair division of the proceeds of the settlement, doing so at a cost which is reasonable and proportionate. Putting to one side for the moment the quantum of the various proposed deductions from the settlement sum for which the SDS provides, I am satisfied that the SDS is fair and reasonable.

57 It is worth noting that prior to the settlement approval hearing Slater & Gordon provided each group member with an individualised estimate of his or her recovery under the proposed settlement. That is an improvement to the standard practice in shareholder and investor class actions as it meant that group members were provided with an understanding of their approximate recovery if the settlement was approved. That allowed group members to make a more informed decision as to whether they wished to object to the proposed settlement.

58 The SDS adopts a different approach to the claims of group members who acquired fully paid ordinary shares in the relevant period and those who acquired equity swaps. The value of group members’ claims:

(a) based in equity swaps were reduced by a modest percentage to reflect the uncertainty about how the Court would treat those claims given their derivative nature; and

(b) based in short sale transactions were discounted by a further amount because of the increased difficulty in establishing causation. Arguably, it is less clear that the assumptions underpinning market-based causation apply to such transactions, and it might be expected that direct reliance would be more difficult to establish than for persons who acquired ordinary shares.

In my view that differential in the treatment of group members’ claims does not show that the settlement is not fair and reasonable inter se. The proposed pro rata settlement distribution will lead to Registered Group Members receiving an equal return relative to their claims after deduction of all costs allowed to be deducted from the Settlement Fund.

59 The SDS provides for the following:

(a) Slater & Gordon to be appointed as the Administrator of the SDS. Slater & Gordon has substantial experience in acting as the administrator of settlement distribution schemes, and that experience should assist in the efficient administration of the SDS. I deal with the question of the reasonableness of the proposed settlement administration costs separately;

(b) Registered Group Members have already been provided with a Notice of Estimated Distribution and a Trade Confirmation Summary Report which provides them with a record of the Claim Data. Registered Group Members can seek a review of the Trade Confirmation Summary Report by filing a Review Request. If no Review Request is filed by the specified deadline, then the Registered Group Member is deemed to have confirmed that the Trade Confirmation Summary Report is correct;

(c) the Notice of Estimated Distribution is an individualised estimate of the amount of compensation to be received by the group member based on the SDS. That distribution is calculated by applying the Loss Assessment Formula in a confidential schedule to the SDS to the share trades made by the group member;

(d) Unregistered Group Members can seek a review of the Notice of Estimated Distribution by filing a Review Request. If no Review Request is filed by the specified deadline then the Registered Group Member is deemed to have accepted the Estimated Distribution;

(e) if a Registered Group Member does not file a notice of objection with the Court, the Registered Group Member is deemed to have accepted the outcome of the review;

(f) the Administrator is permitted to rely on information relating to group members’ claims and to verify that the information is sufficient. No amendment is permitted to group members’ claim data after the deadline for any Review Request to be filed, unless by reason of error, slip or omission by the Administrator, a review determination or order of the Court. The Administrator is required to use reasonable endeavours to ensure the accuracy of the database containing the data for group members’ claims;

(g) a dispute resolution process whereby a Registered Group Member may refer a dispute to independent counsel of not less than five years post-admission experience;

(h) after deduction of various amounts from the Settlement Fund, with which I later deal, distribution of the settlement monies is to be made on a pro rata basis to all Registered Group Members;

(i) after 60 days following distribution, if any payments have been rejected or remain unpresented, distribution shall be deemed to have been made such that the Registered Group Members have no claim against the Administrator;

(j) interest accruing on the Settlement Fund will form part of the Settlement Fund and be available for distribution to Registered Group Members;

(k) the completion of distributions made under the SDS satisfies all rights, claims or entitlements of all group members, and the liability of the Administrator and delegates is limited. The SDS provides for an indemnity from the Settlement Fund for tax or other liabilities; and

(l) the SDS is subject to the supervision of the Court.

60 There is a balance to be struck between fine-tuning settlement allocations and the costs of undertaking an exercise which is designed to ensure that each group member receives such proportion of the settlement sum as reflects his or her own claim and the likelihood of success. In Camilleri at [43](d) Moshinsky J said, and I respectfully agree, that it is relevant to whether a settlement should be approved “whether the costs of a more perfect assessment procedure would erode the notional benefit of a more exact distribution.” I am satisfied that the SDS is fair and reasonable in the interests of group members and as between group members.

61 The SDS provides for the following Court-approved amounts to be deducted from the Settlement Fund prior to distribution to group members:

(a) for the applicant’s reasonable legal costs incurred in the conduct of the proceedings (the applicant’s costs);

(b) the litigation funding commission proposed to be charged by the Funders pursuant to the Court-approved Funding Terms;

(c) a payment paid to the applicant in reimbursement for the time, inconvenience and burden of acting as the representative party for the benefit of group members (the reimbursement payment);

(d) an amount to reimburse the Funder for disbursements it incurred which are recoverable as Project Costs under the Funding Terms (the Project Costs); and

(e) the Administrator’s estimated costs incurred in the administration of the settlement (settlement administration costs).

62 I now turn to deal with those proposed deductions.

THE PROPOSED APPLICANT’S COSTS

63 Reflecting the Funding Terms, the SDS provides that the applicant’s costs, as approved by the Court, be deducted from the Settlement Fund prior to any distribution to class members. The question is whether those costs are fair, reasonable and proportionate.

64 I appointed Ms Dealehr as an independent Costs Referee pursuant to s 54A of the FCA to inquire and report in relation to the reasonableness of the legal costs charged and proposed to be charged to the applicant and group members. She provided a detailed, thorough and considered report on 21 August 2020 and a supplementary report on 26 August 2020. Ms Dealehr concluded that, save for some relatively minor amounts that ought not be allowed, the applicant’s costs and disbursements satisfied both limbs of the test in s 172(1) of the Legal Profession Uniform Law which is Schedule 1 to the Legal Profession Uniform Law Application Act 2014 (Vic) (Uniform Law); that is, in the circumstances of the case the costs were proportionately and reasonably incurred and proportionate and reasonable in amount. It is appropriate to adopt the Costs Referee’s reports save for one matter in relation to the uplift fee sought in relation to the conditional part of Slater & Gordon’s fees.

65 The Funding Terms approved under the common fund order made on 8 May 2019, and the LFAs which preceded those terms, set a “Funding Limit” of $6.65 million on the costs and disbursements that the Funders were obligated to pay, unless varied by agreement in writing. Under the First CLCA and the Second CLCA entered into between the applicant and Slater & Gordon, the firm was retained to act for the applicant in the proceeding on the basis that its fees were paid by the Funders up to the Funding Limit, and thereafter it would conduct the case on a conditional or No Win-No Fee basis. The First and Second CLCAs provide that upon a successful outcome in the case Slater & Gordon is entitled to an uplift fee of “up to 25%” on any unpaid professional fees.

66 At a point which is not clear on the materials but which I infer is approximately 9 months before the trial date, the legal fees and disbursements run up by Slater & Gordon exceeded the Funding Limit and the Funders’ obligation to pay Slater & Gordon’s invoices ceased. Thereafter Slater & Gordon conducted the case on a No Win-No Fee basis. At the time of settlement approval the firm had incurred and had not been paid professional fees of approximately $700,000. There is a difference in the evidence before the Court as to whether the Funders were still obligated to pay disbursements incurred in the case, but that is not relevant for present purposes.

67 In Ms Dealehr’s opinion, the specification in the First and Second CLCAs that the uplift fee that might be payable was “up to 25%” failed to inform the applicant and group members in plain language of the obligation to pay an uplift fee and the applicable percentage of that fee. She concluded that meant that the costs agreements were therefore void pursuant to s 185 of the Uniform Law. Although Ms Dealehr considered the unpaid professional fees to have been proportionately and reasonably incurred, and proportionate and reasonable in amount, she recommended that no uplift fee be approved.

68 I take a different view. The relevant clause in the First and Second CLCAs said:

In the event that We have conducted part of Your case on a Win-Fee basis and Your case is Successful, We are entitled, pursuant to the terms of this LCA and the LPUL, to charge you a success fee of up to 25% of the Professional Fees incurred on a No Win-No Fee basis.

In a case of this size and complexity, where it could not be known whether or at what stage of the proceeding the Funding Limit might be exceeded, it is impossible to state with precision, at the outset, whether it is likely to be appropriate for the applicant’s solicitors to be paid all of the allowable 25% uplift fee under s 182(2) of the Uniform Law, or some lesser percentage. In my view the phrase “up to” acts as a qualifier to the maximum allowable 25% uplift rate and it is understandable and in plain language. It provides a means by which the “uplift” or “success” fee can be ratcheted, and thus the fee may be less than the allowable 25% maximum if the circumstances of the case justify an uplift fee but not to the extent of 25%. The applicant and Funded Group Members did not say that they had any difficulty understanding the meaning of the clause, and I doubt that any did so.

69 In the circumstances of the case, having regard to the substantial success achieved and also to the fact that the Costs Referee found the conditional legal fees incurred to be reasonable and proportionate, it is appropriate to allow an uplift fee for the substantial work which was conducted on No Win-No Fee basis. There are though some reasons why an uplift of less than 25% ought to be applied, including because the unpaid fees were not outstanding for a lengthy period and for the reasons provided by Ms Dealehr at paragraphs 40 and 41 of her first report. In my view it is appropriate to allow a 15% uplift on the professional fees incurred on a conditional basis.

70 Taking into account that change, which will increase the approved applicant’s costs by about $105,000, I consider it appropriate to allow the deduction of $7,856,318 for the applicant’s costs and disbursements on a solicitor and own client basis.

The proposed settlement administration costs

71 The orders appointing the Costs Referee also required Ms Dealehr to report as to the reasonableness of the sum proposed for settlement administration costs. With one exception I considered it appropriate to adopt the Costs Referee’s report which said that $220,651 (inclusive of GST) was a reasonable and proportionate amount for settlement administration costs. I reduced the amount by $10,423 to reflect my view that it was unlikely that group members would seek review in relation to the distributions under the SDS as most had already been provided with a Notice of Estimated Distribution and had not done so. I approved settlement administration costs to $211,165 but gave liberty to apply to the Administrator in the event that such an amount was insufficient to meet the costs incurred.

THE PROPOSED LITIGATION FUNDING COMMISSION

The background

72 By orders made on 18 June 2020, the Funders were granted leave to be represented in the application for settlement approval. They filed an interlocutory application dated 28 August 2020 seeking an order that they receive equitable remuneration for their provision of litigation funding, at the rate of 22.5% of the settlement sum net of approved legal costs.

73 The Funders rely on the affidavits of Mr Purslow and Mr Walker which show that:

(a) in early 2016 ICP commenced investigating a proceeding against Spotless in relation to the events giving rise to the present case and they subsequently sought legal, accounting and econometric advice regarding the merits of the claim, which investigation was largely complete by late 2016. Thereafter the ICP Entities entered into litigation funding agreements with a number of shareholders who had expressed interest in participating in a class action, and a retainer with a firm of solicitors, and had consulted with counsel in anticipation of litigation, but no proceeding was yet commenced; and

(b) in August 2016 Therium Australia, along with Slater & Gordon, commenced their own investigation. Between January and May 2017, Therium Australia entered into engagement terms with Slater & Gordon and in conjunction with that firm undertook “book building” of clients, following which it unconditionally agreed to fund the claim against Spotless.

74 Mrs Court, represented by Slater & Gordon and funded by Therium, then commenced the proceeding on 25 May 2017. The day after the applicant commenced the proceeding, Mr Walker contacted Slater & Gordon and Mr Purslow inviting discussion as to arrangements by which the Funders could jointly fund the proceeding. Ultimately, those negotiations culminated in the applicant, her solicitors and the Funders entering into the Co-Funding Agreement which provides for the Funders to fund the action and also that:

(a) the applicant will consider extending the claim period to include an earlier period and include an equity swap claim contemplated in the ICP Entities’ proposed claim;

(b) Slater & Gordon is to remain as solicitors on the record;

(c) each of the Funders retain their respective contractual rights to recover, as commission from those group members who had signed a funding agreement with that funder prior to the execution of the Co-Funding Agreement, a proportion of their recovery sums;

(d) the Funders are together required to enter into an after the event insurance policy to pay any adverse costs order that is made, which policy is to cover costs in an amount representing a substantial part of the budgeted costs. The Funders would each bear 50% of the costs of such a policy; and

(e) the applicant is to apply for a common fund order, that would entitle the Funders to a proportion of any damages that would otherwise be paid to those group members who had not signed a funding agreement with either of the Funders.

75 On 8 May 2019, the Court made a common fund order (CFO) which, subject to certain undertakings from the Funders, provides:

Subject to further order, pursuant to sections 23 and 33ZF of the Federal Court of Australia Act 1976 (Cth) and rule 1.32 of the Federal Court Rules 2011, the Funding Terms attached as Annexure A (Funding Terms) be approved and be binding upon the Applicant, the group members…[the Funders] and [Slater & Gordon].

(Emphasis in original).

76 Relevantly, cll 8 and 9 of the Court-approved Funding Terms provides for “Funders’ Remuneration” as follows:

As consideration for performing the obligations under these Funding Terms, the Funders’ Remuneration shall be such amount as determined by the Court at the time the Recoveries is [sic] agreed or determined, which shall not exceed 25% of Net Recoveries, shared among the Funders in accordance with agreements between them.

For the avoidance of doubt, these Funding Terms displace any obligation of a Group Member to pay more than 25% of Net Recoveries to a Funder under the terms of a Group Member Funding Agreement.

“Net Recoveries” is defined in the Funding Terms to mean, in effect, the cash recoveries payable to all group members pursuant to the settlement of the proceeding, less the costs and expenses incurred in the prosecution of the proceeding.

Power

77 In Brewster the High Court held that s 33ZF of the FCA is not a source of power to make a CFO. Unlike the CFO in Pearson v State of Queensland (No 2) [2020] FCA 619 at [268], the CFO in the present case it is not capable of operating without a further order of the Court. Accordingly, in the circumstances of the present case, the doctrine in Kable at [32] does not apply and if the order the Funders seek is to be made it must be made afresh, and under a power other than s 33ZF.

78 As I said in Uren at [47]-[73] I do not consider that the ratio of Brewster, or the considered dicta of the majority, stand for the proposition that the Court has no power to make an order under s 33V(2) of the FCA to require all group members to pay a pro rata contribution from a settlement to a litigation funder, so that the litigation funding expenses incurred to achieve a settlement are shared fairly and equitably between those who will benefit from the settlement. Since the decision in Brewster, a number of judges of this Court have concluded that the Court has power to make a CFO at the point of settlement approval, pursuant to the power in s 33V(2), including in McKay Super Solutions Pty Ltd (Trustee) v Bellamy’s Australia Ltd (No 3) [2020] FCA 461 at [31] (Beach J); Vocus at [72] (Moshinsky J); Uren at [51]-[54]; Clime Capital Limited v UGL Pty Limited [2020] FCA 66 (Anastassiou J); Lenthall v Westpac Banking Corporation (No 2) [2020] FCA 423 at [12] (Lee J); Webster at [111]. In Cantor at [405]-[421], Foster J took a different view.

79 Most recently, the Full Court in Davaria Pty Ltd v 7-Eleven Stores Pty Ltd [2020] FCAFC 183 at [42] (Lee J, with whom Middleton and Moshinsky JJ agreed), and the NSW Court of Appeal in Brewster v BMW Australia Ltd [2020] NSWCA 272 at [28](iv)-(v), [30] and [41]-[43] (Brewster (CA)) (Bell P with whom Bathurst CJ and Payne JA agreed) confirmed that the High Court decision in Brewster is not authority for the proposition that there is no power under s 33V of the FCA or s 173 of the CPA to make a common fund order at the point of settlement approval. In Brewster (CA) Bell P observed at [38]-[40]:

The factual context of a settlement being presented to the Court for approval is very different to the situation, at the commencement or an early stage of litigation, where the Court is asked to approve an order nominating a particular percentage or commission which a funder may extract from any settlement ultimately reached or judgment ultimately given, when that sum is not known and the attitude of group members towards the settlement is also unknown. Moreover, at the point of settlement, ex hypothesi, the Court making the order will not be concerned with whether the litigation will be funded going forward or the risks which may be entailed in providing funding. Those risks will have been taken and be spent. The Court will be armed with “hard” information rather than speculative possibilities as to key integers, by reference to which its discretion may be exercised to approve a settlement and make any orders with respect to distribution (including to third parties such as solicitors administering any settlement fund): cf BMW (HC) at [68].

In these circumstances, one can well understand an argument that it is just in all the circumstances for a funder to receive a measure of recompense out of the overall settlement sum for its contribution to the realisation of the settlement pool beyond that which may result from a FEO, as that term was described in the plurality judgment in BMW (HC) at [86]. A conclusion to that effect may be influenced by the size of the overall settlement sum, the amount proposed to be paid to group members, the number of group members who signed up to the funding agreement, the amount that would be required to be paid to the funder if a FEO were made, the degree of risk involved in funding the action, and the length and complexity of the proceedings.

Without knowing any of these matters, and absent clear statutory language requiring such a conclusion, it would be unusual, to say the least, for a superior court to conclude, in an a priori way, that a settlement could not be approved or that it would not be just that an order be made for an amount to be paid out of the overall settlement sum to a funder, even if the amount so ordered exceeded that which would have been contractually payable by those group members who had signed up to a funding agreement.

80 The applicant and the Funders seeks an Equitable Remuneration Order in the exercise of the Court’s powers under s 33V(2) of the FCA, alternatively s 23 of the FCA, and in equity. For the reasons I explained in Uren, I consider the Court has power to make such an order, and the real question is one of discretion; that is, whether in the circumstances of the case it is ‘just’ under s 33V to do so.

The exercise of the discretion

81 It matters little whether an order under s 33V of the type sought is styled as an “Equitable Remuneration Order” as the Funders do, a “Common Fund Order” as such orders as have historically been called, or as an “Expense Sharing Order” as Lee J made in Lenthall at [3]. As Lee J observed in Davaria at [8], the use of labels such as “Common Fund Order” can operate to obscure important differences between the forms of orders, and the different statutory contexts in which such orders have been made, and such orders sometimes deal with different concepts. But keeping that in mind, and for the convenience of having a shorthand description, I prefer the name “Expense Sharing Order”, based as it is in the words of the Practice Note at 15.4.

82 In Money Max Int Pty Ltd (Trustee) v QBE Insurance Group Limited [2016] FCAFC 148; (2016) 338 ALR 188 at [80] (Murphy, Gleeson and Beach JJ), although in a different context, the Full Court set out a non-exhaustive list of factors relevant to assessing the reasonableness of a proposed funding commission. I have had regard to those factors. After having taken all relevant factors into account the Full Court said (at [82]) that it expected that the courts:

…will approve funding commission rates that avoid excessive or disproportionate charges to class members but which recognise the important role of litigation funding in providing access to justice, are commercially realistic and properly reflect the costs and risks taken by the funder, and which avoid hindsight bias.

In Kuterba v Sirtex Medical Limited (No 3) [2019] FCA 1374 at [12] Beach J said, and I respectfully agree, that the approval of funding commission rates should not become a “race to the bottom” and funding rates should provide an appropriate reward for the risk undertaken by a litigation funder.

The costs and risks assumed by the Funders

83 In class action litigation the fundamental obligations of a commercial third-party litigation funder (usually) include paying the applicant’s legal costs and disbursements, putting up security for costs, and indemnifying the applicant and group members in relation to any adverse costs order. In return the funder is entitled, upon success in the proceeding, to: (a) reimbursement of the legal costs and disbursements it has paid; (b) the return of the security for costs it has advanced; and (c) a funding commission in consideration of the costs and risks it took on.

84 The arrangement under the Funding Terms in the present case is no exception. Clause 3 of the Funding Terms is headed “Funders’ Obligations”. It provides:

[The Funders] must fund the Project Costs of the Applicant and Group Members, by:

(a) paying the Lawyers the Legal Costs and Disbursements charged by the Lawyers for all Legal Work (whether incurred before or during the Funding Period) up to the Funding Limit;

(b) paying the costs of any insurance covering an Adverse Costs Order;

(c) paying and indemnifying the Applicant and any Group Member against any Costs Order which the Court makes in the Proceeding against the Applicant or a Group Member in favour of the Respondent, in so far as the costs the subject of the Costs Order were incurred either before or during the Funding Period; and

(d) providing any security for costs in the Proceeding, in the form that the Court orders, or in the absence of any order, in such form as the Applicant and the Funders agree and the Respondent accepts.