Federal Court of Australia

Citadel Group Limited, in the matter of Citadel Group Limited [2020] FCA 1580

ORDERS

THE CITADEL GROUP LIMITED (ACN 127 151 026) Plaintiff | ||

DATE OF ORDER: |

OTHER MATTERS:

1. The Court notes that the Australian Securities and Investments Commission (ASIC) was provided with at least 14 days’ notice of the hearing of this application.

2. The Court is satisfied that ASIC has had a reasonable opportunity to:

(a) examine the terms of the proposed scheme of arrangement to which the application relates and a draft explanatory statement relating to that arrangement; and

(b) make submissions to the Court in relation to the proposed scheme of arrangement and the draft explanatory statement.

3. The Court notes the letter from ASIC to the Directors of The Citadel Group Limited dated 28 October 2020 at Annexure JPR-2 to the affidavit of Jolyon Percival Rogers dated 29 October 2020.

THE COURT ORDERS THAT:

1. Pursuant to s 411(1) of the Corporations Act 2001 (Cth) (Act), the Plaintiff convene and hold a meeting of its shareholders (Scheme Meeting):

(a) for the purpose of considering, and, if thought fit, agreeing (with or without modification), to the scheme of arrangement (Scheme) proposed to be made between the Plaintiff and its shareholders (Citadel Shareholders), the terms of which are set out in Annexure A to these orders; and

(b) to be held on Tuesday 1 December 2020 at 11.00 am (AEDT) and to be conducted electronically through an online platform (which is to be accessed in accordance with the instructions included in the Notice of Meeting to be sent to shareholders in accordance with order 2 below) in accordance with the provisions of Part 2 of the Corporations (Coronavirus Economic Response) Determination (No.3) 2020.

2. The Scheme Meeting be convened by sending on or before Friday 30 October 2020:

(a) an email to each Citadel Shareholder who has nominated an electronic address for the purposes of receiving notices of meeting and proxy forms from the Plaintiff (Email Shareholder) (or, in the case of joint holders, to the holder whose name appears first in the Plaintiff’s register), such email to be substantially in the form of pages 978-979 of Annexure PFL-1 to the affidavit of Peter Francis Leahy sworn on 28 October 2020 (Leahy Affidavit) which contains links to:

(i) an electronic copy of a document substantially in the form of the Scheme Booklet, a draft of which is at pages 293-756 of Annexure PFL-1 to the Leahy Affidavit (which contains among other things the proposed Scheme of Arrangement at Annexure D and Notice of Scheme Meeting at Annexure G) (Scheme Booklet); and

(ii) an online portal or website that is accessible by the Email Shareholder and which enables the Email Shareholder to:

A. lodge their proxy for the Scheme Meeting and voting instructions online; and

B. make an Election in relation to the Scrip Consideration online (as those terms are defined in the Scheme Booklet);

(b) the following hard-copy documents to each Citadel Shareholder who is not an Email Shareholder (or, in the case of joint holders, to the holder whose name appears first in the Plaintiff’s register):

(i) a letter substantially in the form of pages 980-982 of Annexure PFL-1 to the Leahy Affidavit (Letter) setting out the URL which provides access to a document substantially in the form of the Scheme Booklet (which contains among other things the proposed Scheme of Arrangement at Annexure D and the Notice of Scheme Meeting at Annexure G) and which sets out instructions about how to make an Election (as defined in the Scheme Booklet) and lodge a proxy for the Scheme Meeting and voting instructions;

(ii) an Election Form in relation to the Scrip Consideration (as those terms are defined in the Scheme Booklet) substantially in the form of pages 759-760 of Annexure PFL-1 to the Leahy Affidavit (Election Form) and a reply-paid envelope for the return of the completed Election Form; and

(iii) a proxy/voting form for the Scheme Meeting (Proxy Form), substantially in the form of pages 757-758 of Annexure PFL-1 to the Leahy Affidavit.

3. The documents referred to in order 2(b) be sent:

(a) in the case of Citadel Shareholders whose registered address is within Australia, by prepaid ordinary post addressed to the relevant addresses recorded in the Plaintiff’s register; and

(b) in the case of Citadel Shareholders whose registered address is outside Australia, by airmail or international courier service addressed to the relevant addresses recorded in the Plaintiff’s register.

4. Compliance with r 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) (Rules) be dispensed with, except in so far as that rule applies r 75-15(2) of the Insolvency Practice Rules (Corporations) 2016 (Cth).

5. Voting on the resolution to approve the Scheme is to be conducted by way of a poll.

6. A proxy in respect of the Scheme Meeting will be valid and effective if, and only if, a Proxy Form is completed and delivered in accordance with its terms or a proxy is lodged online in accordance with the instructions on the online portal or website referred to in order 2(a)(ii), and received by the Plaintiff by 11.00 am (AEDT, being Melbourne time) on 29 November 2020.

7. An Election (as defined in the Scheme Booklet) will be valid and effective if, and only if, an Election Form is completed, delivered and received by the Plaintiff in accordance with its terms or a valid election is made online in accordance with the instructions on the online portal or website referred to in order 2(a)(ii), by 5.00 pm (AEDT, being Melbourne time) on 24 November 2020.

8. Mr Peter Francis Leahy or failing him Mr Robert Ian Alexander, be Chair of the Scheme Meeting.

9. The Chair of the Scheme Meeting shall have the power to adjourn the meeting to such time, date and place as he considers appropriate.

10. Compliance with r 3.4 and Form 6 of the Rules is dispensed with.

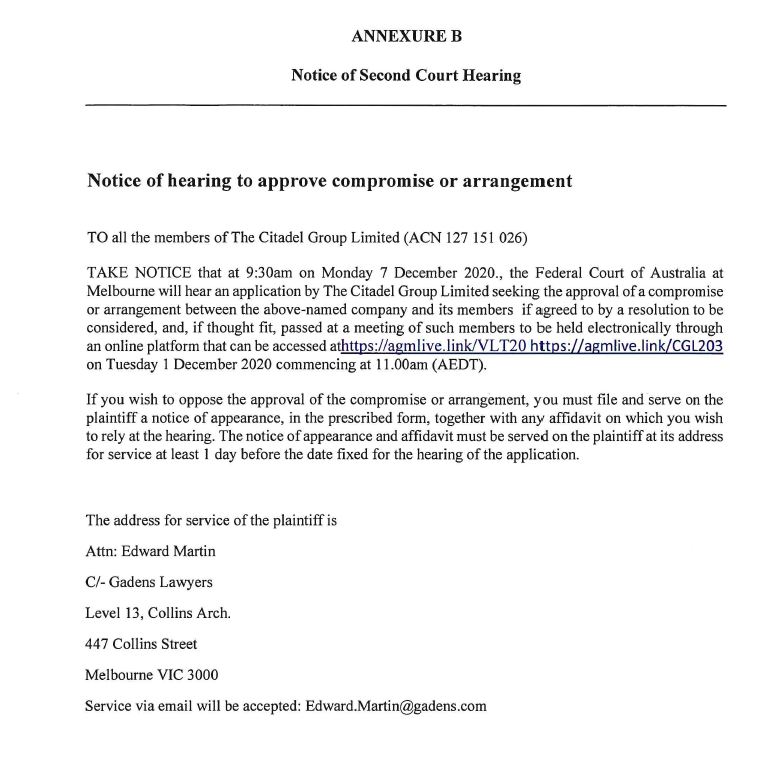

11. The Plaintiff publish a Notice of Hearing in The Australian newspaper, in substantially the form that appears at Annexure B hereto, not later than 5 days prior to the date fixed for the hearing of any application to approve the Scheme.

12. The further hearing of the Originating Process is adjourned to the Honourable Justice Beach at 9.30 am (AEDT, being Melbourne time) on Monday, 7 December 2020 or as soon thereafter as the business of the Court allows.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

[The order entered is available on the Commonwealth Courts Portal, which attaches the Scheme]

REASONS FOR JUDGMENT

BEACH J:

1 Citadel Group Limited applies for an order under s 411(1) of the Corporations Act 2001 (Cth) for a meeting of Citadel shareholders to be convened to consider a proposed scheme of arrangement (the Scheme).

2 Citadel is an Australian public company limited by shares. It is admitted to the official list of the ASX, and its shares are quoted for trading. It specialises in the development and delivery of technology solutions, including software platforms, digital services and managed services solutions. As at 11 September 2020, Citadel had a market capitalisation of approximately $313 million.

3 The commercial purpose of the Scheme is to provide for the acquisition of all the shares in Citadel by Pacific Group Bidco Pty Ltd (PEP BidCo). PEP BidCo is a special purpose company ultimately owned by funds managed or advised by Pacific Equity Partners Pty Limited (PEP). PEP is an Australian private equity firm which focuses on buyouts and late stage expansion capital in Australia and New Zealand.

4 If the Scheme is implemented, Citadel shareholders will receive $5.70 cash per Citadel share less a special dividend of up to $0.20 per Citadel share, unless a valid election is made to receive the scrip consideration in the form of Class B shares in Pacific Group Topco Limited (HoldCo). Foreign scheme shareholders will not be entitled to receive scrip consideration, but will receive the cash consideration for all of their scheme shares.

5 On 14 September 2020, Citadel entered into a Scheme Implementation Deed (SI Deed) with PEP BidCo. On 27 October 2020, Citadel and BidCo entered into a Deed of Amendment and Restatement in relation to the SI Deed, which provided for an increase to the maximum amount of any special dividend that may be declared by the board of directors of Citadel, to $0.20 per Citadel share. The SI Deed (as amended) provided for Citadel to propose the Scheme and that both Citadel and PEP BidCo would implement the Scheme on the terms of the SI Deed (as amended).

6 The Scheme provides for the acquisition by PEP BidCo of 100% of the shares in Citadel on issue on the scheme record date (the scheme shares). The scheme record date is anticipated to be 10 December 2020. Prior to PEP BidCo receiving a transfer of the scheme shares, the scheme consideration must be provided to the holders of the scheme shares as at the scheme record date (the scheme shareholders).

7 The scheme consideration will comprise the cash consideration, unless a shareholder other than a foreign scheme shareholder makes a valid election to receive the scrip consideration for all or some, but at least 50%, of their scheme shares. The availability of the scrip consideration is subject to valid elections being made by Citadel shareholders, other than foreign scheme shareholders, holding in aggregate at least 5% of Citadel shares, and is also subject to a scale back in certain circumstances. The cash consideration of $5.70 per scheme share less the amount of any special dividend is to be paid by PEP BidCo. The scrip consideration of 1 Class B share in HoldCo per scheme share the subject of a valid election is to be issued by HoldCo.

8 The obligations of PEP BidCo and HoldCo to provide the scheme consideration have been secured by their entry into a Deed Poll in favour of scheme shareholders.

9 Following provision of the scheme consideration to scheme shareholders, all scheme shares will be transferred to PEP BidCo.

10 It is anticipated that the above steps will occur on 17 December 2020.

11 Following the implementation of the Scheme, Citadel will be a wholly-owned subsidiary of PEP BidCo, and will be delisted from the ASX.

12 Now Citadel has prepared a Scheme Booklet, which includes the explanatory statement required by s 412 of the Act. A draft of the Scheme Booklet was lodged with ASIC on 12 October 2020. Amendments to that version of the draft Scheme Booklet were subsequently made and provided to ASIC.

13 The Scheme Booklet sets out a detailed description of the Scheme and its advantages and disadvantages. It also annexes an independent expert report of Mr Craig Edwards of Lonergan Edwards & Associates Limited.

14 In the independent expert report, Mr Edwards concludes that the Scheme is fair and reasonable and hence in the best interests of the scheme shareholders, in the absence of a superior alternative proposal emerging. In particular, Mr Edwards has assessed the value of Citadel shares on a 100% controlling interest basis to be between $5.24 and $5.75 per Citadel share. Mr Edwards notes that the cash consideration lies within his assessed valuation range for Citadel shares, and that accordingly the scheme consideration is fair to Citadel shareholders. Mr Edwards notes that Citadel shareholders who do not elect to receive the scrip consideration will receive $5.70 in cash per share if the Scheme is implemented, regardless of whether the special dividend is paid.

15 Mr Edwards has assessed the market value of HoldCo equity on a 100% controlling interest basis to be between $4.30 and $4.96 per share. Therefore he has concluded that the value of the scrip consideration is significantly less than the cash consideration. This valuation reflects a discount for minority interests and the lack of marketability of HoldCo shares.

16 Now the Citadel Board has unanimously recommended that Citadel shareholders vote in favour of the Scheme in the absence of a superior proposal and subject to Mr Edwards continuing to conclude that the Scheme is in the best interests of Citadel shareholders.

17 Let me say something further on the provision of the scheme consideration which will involve a number of entities:

(a) PEP BidCo will pay the cash consideration and receive a transfer of the scheme shares. PEP BidCo is a special purpose company that was incorporated on 4 September 2020 for the purpose of acquiring all of the scheme shares under the Scheme.

(b) All of the shares in PEP BidCo are owned by Pacific Group Midco Pty Ltd (MidCo). MidCo is a special purpose company that was incorporated on 4 September 2020 for the purpose of holding all of the shares in PEP BidCo.

(c) All of the shares in MidCo are owned by HoldCo. HoldCo will provide the scrip consideration, being 1 Class B share in HoldCo for every scheme share the subject of a valid election. HoldCo is a special purpose company that was incorporated on 14 September 2020 for the purposes of:

(i) directly holding all of the shares in MidCo and indirectly holding all of the shares in PEP BidCo; and

(ii) issuing HoldCo shares to eligible scheme shareholders who make a valid election to receive the scrip consideration.

(d) All of the shares in HoldCo are currently owned by Pacific Equity Partners Fund VI (Australia) Pty Ltd (PEP Fund VI Trust). The PEP Fund VI Trust is one of the entities that is part of a number of unit trusts and limited partnerships that are managed or advised by PEP.

18 Now under the terms of the SI Deed (as amended), the Citadel Board may declare a fully franked special dividend of up to $0.20 per Citadel share to be paid on or prior to the implementation of the Scheme. But whether a special dividend is ultimately declared and paid remains at the discretion of the Citadel Board. But if the special dividend is declared, it will be paid to all persons registered as Citadel shareholders as at the special dividend record date, which is expected to be 7.00 pm on Tuesday, 8 December 2020. The special dividend is expected to be fully franked.

19 If the special dividend is declared, then under the Scheme:

(a) the cash consideration of $5.70 per scheme share provided by PEP BidCo will be reduced to the extent of any special dividend;

(b) under the “mix-and-match option” of the scrip consideration, any cash consideration received by those Citadel shareholders will be reduced to the extent of any special dividend; and

(c) the paid up capital amount of the Class B shares to be issued as scrip consideration will be reduced to the extent of any special dividend, so that if Citadel declares a special dividend of $0.20 per Citadel share, the paid up capital amount of the Class B shares in HoldCo will be reduced from $5.70 to $5.50 per Class B share.

20 If the Scheme is to proceed, all conditions precedent other than Court approval must be either satisfied or waived by 8.00 am on the date of the second Court hearing, which will be 7 December 2020. If the Scheme is agreed to by shareholders and approved by me, it will become effective on 8 December 2020, and the scheme consideration will be issued to scheme shareholders on 17 December 2020. The scheme shares will subsequently be transferred to PEP BidCo on that date.

21 The mechanism for the transfer of the scheme shares to PEP BidCo and the issue of the scheme consideration to scheme shareholders is as follows. Prior to the implementation date and prior to the transfer of any scheme shares to PEP BidCo, PEP BidCo must deposit into a trust account in cleared funds an amount equal to the aggregate amount of cash comprised in the scheme consideration payable to scheme shareholders, with that amount to be held by Citadel on trust for the scheme shareholders for the purpose of Citadel dispatching the aggregate cash comprised in the scheme consideration to the scheme shareholders to which they are entitled. On the implementation date, subject to the deposit of funds by PEP BidCo, Citadel must pay or procure the payment of the cash consideration to each scheme shareholder from the trust account referred to. By no later than 12.00 pm (AEDT) on the implementation date, HoldCo must provide the scrip consideration to scheme shareholders in accordance with the Scheme. And on the implementation date but after BidCo and HoldCo have satisfied their respective obligations to provide the scheme consideration as outlined, the scheme shares held by scheme shareholders will be transferred to PEP BidCo.

22 Now whilst the scheme consideration is to be issued by PEP BidCo and HoldCo, those entities are not a party to the Scheme, and cannot be directly bound by it. So it has been necessary for the entities providing the scheme consideration to execute a Deed Poll in favour of scheme shareholders. In particular, as required by the SI Deed (as amended), PEP BidCo, MidCo and HoldCo have entered into the Deed Poll which contains a covenant by them in favour of the scheme shareholders to perform their respective obligations in relation to the scheme. This includes the obligation to provide or procure the provision of the scheme consideration to the scheme shareholders in accordance with the terms of the Scheme, including to issue all HoldCo shares which are the subject of valid elections by the scheme shareholders under the terms of the Scheme. And under the terms of the Scheme, Citadel undertakes in favour of each scheme shareholder to enforce the Deed Poll against PEP BidCo, MidCo and HoldCo on behalf of and as agent and attorney for the scheme shareholders.

23 Let me move to some more general matters.

24 Section 411(1) confers a discretion on the Court to make an order if certain requirements are satisfied, namely:

(a) a compromise or arrangement is proposed between a Part 5.1 body and its members or any class of them;

(b) application for the order is made in a summary way by the body;

(c) 14 days’ notice of the hearing of the application has been given to ASIC, or such lesser period as the Court or ASIC permits; and

(d) the Court is satisfied that ASIC has had a reasonable opportunity to:

(i) examine the terms of the proposed compromise or arrangement to which the application relates and a draft explanatory statement relating to the proposed compromise or arrangement; and

(ii) make submissions to the Court in relation to the proposed compromise or arrangement and the draft explanatory statement.

25 These requirements have been satisfied in the present case and accordingly my power has been enlivened. I am also satisfied that relevant provisions of the Corporations Regulations 2001 (Cth) (the Regulations) and the Federal Court (Corporations) Rules 2000 (Cth) have been satisfied. Let me turn then to the exercise of discretion.

26 My function on an application to order the convening of a meeting is supervisory. At this stage I should generally confine myself to ensuring that certain procedural and substantive requirements have been met including dealing with adequate disclosure, but with limited consideration of issues of fairness. But having said that, it is appropriate to consider the merits or fairness of a proposed scheme at the convening hearing if the issue is such as would unquestionably lead to a refusal to approve a proposed scheme at the approval hearing, that is, the proposed scheme appears now to be on its face “so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further” (Re Foundation Healthcare Ltd (2002) 42 ACSR 252 at [44] per French J). But in the present case, in my view there is no issue arising from the Scheme which would unquestionably lead to a refusal to approve the Scheme at the approval hearing. It cannot be said that the Scheme on its face is “so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further”. Put another way, the Scheme is not of such a nature and cast in such terms that if it receives the support of the statutory majorities at the meeting, nevertheless I would not be likely to approve it at the second court hearing.

27 In my view the Scheme is fit for consideration by Citadel shareholders at the proposed meeting, in the sense referred to. The question whether or not to accept particular consideration for shares is a commercial matter for the members of Citadel to assess, and they ought not be prevented from having the opportunity to do so provided that I am satisfied that they are acting on sufficient information and with time to consider what they are voting on. I am so satisfied. Further, it is relevant in this respect that the Scheme Booklet contains a recommendation from all directors that shareholders vote in favour of the Scheme, a statement that all directors intend to vote their Citadel shares in favour of the Scheme, and an independent expert report that the Scheme is fair and reasonable and in the best interests of Citadel shareholders.

28 Let me now discuss the following particular features of the Scheme that have been drawn to my attention, being:

(a) performance risk;

(b) shareholder warranties;

(c) the break fee;

(d) the exclusivity arrangements;

(e) the scheme consideration and class issues;

(f) whether there is any financial assistance in relation to the special dividend;

(g) employee share rights and short term incentives;

(h) foreign scheme shareholders and UK shareholders; and

(i) the purpose of the Scheme, and whether it is to avoid Chapter 6 of the Act.

Performance risk

29 Although PEP BidCo and HoldCo are to issue the scheme consideration, they are not parties to the Scheme and are not directly bound by it. As such, their obligations do not depend upon s 411 of the Act. But the Scheme before me effectively eliminates any performance risk. This is because Citadel has adopted safeguards to address the performance risk arising from the obligations of PEP BidCo and HoldCo to issue the scheme consideration. In particular, the terms of the Scheme supported by the SI Deed (as amended) prevent any transfer of the scheme shares to PEP BidCo unless and until the scheme consideration has been issued, and HoldCo, MidCo and PEP BidCo have executed a Deed Poll as I have said. It follows that there is no material performance risk which would justify me not ordering the convening of the scheme meeting.

Shareholder warranties

30 The Scheme provides that each scheme shareholder is taken to have warranted to PEP BidCo that, as at the implementation date, all of their scheme shares that are transferred under the Scheme will, at the date of transfer, be fully paid and free from all security interests and interests of third parties of any kind and from any restrictions on transfer of any kind, and that it has full power and capacity to sell and to transfer those shares together with any rights and entitlements attaching to such shares to PEP BidCo under the Scheme. The warranty is in the usual form, and such clauses have been held to be acceptable, as long as the warranty is sufficiently disclosed in the explanatory statement to shareholders, which it is. In my view, this deemed warranty clause is acceptable.

Break fee

31 If the Scheme does not become effective, a break fee of $4,486,473 may be payable by Citadel to PEP BidCo. The circumstances in which the break fee would be payable are set out in cl 12.2 of the SI Deed (as amended) and explained in the Scheme Booklet. They are in summary in circumstances where:

(a) a competing proposal is announced during the exclusivity period and, within 12 months of such announcement:

(i) the competing proposal is implemented or completed; or

(ii) the proponent of that competing proposal or any of its associates acquires a relevant interest in, an economic interest in or voting power of 50% or more of Citadel shares and that acquisition is unconditional or control of Citadel;

(b) during the exclusivity period, any Citadel director fails to recommend the Scheme or withdraws, adversely changes or adversely qualifies his or her recommendation or otherwise makes a public statement indicating that he or she no longer supports the Scheme, except where:

(i) the independent expert concludes in the independent expert report that the Scheme is not in the best interests of Citadel shareholders, other than where the reason for the independent expert’s conclusion is due wholly or partly to the existence of a competing proposal; or

(ii) Citadel is entitled to terminate the SI Deed as a result of PEP BidCo’s material breach and has given the appropriate termination notice to PEP BidCo; or

(c) PEP BidCo validly terminates the SI Deed where Citadel has materially breached any term of the SI Deed and, if the breach is capable of remedy, Citadel has not remedied the breach within the prescribed time.

32 But notwithstanding the occurrence of any event which would trigger a requirement to pay the break fee, the break fee is not payable if the Scheme becomes effective.

33 Further, the break fee is not payable merely because the Scheme does not proceed merely because Citadel shareholders do not agree to the Scheme at the scheme meeting in the requisite majorities required by the Act.

34 The value of the break fee represents approximately 1% of the total equity value of Citadel, having regard to the value of the scheme consideration.

35 In my view the terms of the break fee and the circumstances in which it was agreed are consistent with the requirements of the relevant authorities, and do not represent a barrier to the convening of a meeting to consider the Scheme.

Exclusivity arrangements

36 Clause 11 of the SI Deed (as amended) contains a number of exclusivity provisions, including “no shop”, “no due diligence” and “no talk” provisions. The exclusivity provisions apply during the “exclusivity period” which is defined in the SI Deed (as amended) as being the period from 14 September 2020, when the SI Deed was entered into, until the earlier of the termination of the SI Deed (as amended) or the end date of 14 March 2021.

37 But cl 11.7 of the SI Deed (as amended) provides the Citadel Board with a “fiduciary-out” in relation to the “no talk” and “no due diligence” restrictions. In particular, the obligations in relation to “no talk” and “no due diligence” do not prohibit Citadel or the Citadel Board from taking or refusing to take any action with respect to an actual, proposed or potential competing proposal, which was not solicited, invited, encouraged or initiated by Citadel in contravention of the “no-shop” obligation, provided that the Citadel Board has determined, in good faith and acting reasonably that after receiving advice from its financial adviser, the relevant competing proposal is, or is reasonably likely to become, a superior proposal and after receiving written legal advice from its external legal advisers, that compliance with the “no-talk” and “no-due diligence” obligations as applicable would constitute, or would be reasonably likely to constitute, a breach of any of the fiduciary or statutory duties of the Citadel directors.

38 In my view provisions such as those in the SI Deed are commonly found in merger implementation agreements. And in practice, it is well accepted that a “no-shop” clause need not be subject to a fiduciary carve-out.

39 In my view, the fiduciary carve-outs in the SI Deed (as amended) are appropriate. Further, the exclusivity period of 6 months is reasonable in light of the size, nature and complexity of the transaction. Moreover, the exclusivity provisions have been given adequate prominence in the Scheme Booklet.

40 For these reasons, the exclusivity arrangements do not prevent me from making an order to convene a meeting of members to vote on the Scheme.

Other matters

41 Let me deal with some other matters.

42 First, the potential availability of different forms of scheme consideration does not necessarily lead to the creation of more than a single class of shareholders. The question of classes and separate class meetings arises because of the reference in s 411(1) to an arrangement proposed between a company and its members “or any class of them”.

43 In Re Healthscope (2019) 139 ACSR 608; [2019] FCA 542 I engaged in a detailed review of the relevant authorities on classes at [105] to [120]. At [106], I said:

The well-established test for identifying a class for the purposes of a scheme of arrangement is that expressed by Bowen LJ in Sovereign Life Assurance Co v Dodd [1892] 2 QB 573 at 583. Sovereign Life Assurance concerned a creditors’ scheme of arrangement, but the test enunciated by Bowen LJ has been adopted ever since in members’ schemes (Re Foster’s Group Limited [2011] VSC 93 at [15] per Ferguson J). Bowen LJ expressed the class test in the following terms:

…The word “class” is vague, and to find out what is meant by it we must look at the scope of the section, which is a section enabling the Court to order a meeting of a class of creditors to be called. It seems plain that we must give such a meaning to the term “class” as will prevent the section being so worked as to result in confiscation and injustice, and that it must be confined to those persons whose rights are not so dissimilar as to make it impossible for them to consult together with a view to their common interest…

44 I also expressed the relevant question as being whether the rights of the relevant shareholders there under consideration were (at [107]):

so dissimilar from the rights of the other Healthscope shareholders as to make it impossible for them to consult together with a view to their common interest. Or put another way, do the differences in rights between NWH AssetCo (or its affiliates) and the other Healthscope shareholders mean that any community of interest between them has been displaced for the purposes of them considering and voting upon the proposed Scheme.

45 In relation to the specific question of whether different forms of scheme consideration give rise to the need for separate classes, it is appropriate to consider whether the existence of different proportional entitlements to different forms of consideration under a scheme of arrangement would necessitate the creation of separate classes of shareholders for the purpose of voting.

46 Now in the present case the potential availability of different forms of scheme consideration does not lead to the creation of more than a single class of shareholders. Relatedly, the fact that scheme shareholders who receive scrip consideration will be subject to the provisions of the Shareholders’ Deed in relation to those shares does not create any class issues. Citadel shareholders who receive Class B shares under the Scheme will only be able to sell or transfer their Class B shares in certain very limited circumstances as permitted under that Deed. However, in relation to the scheme consideration generally, this does not mean that the rights of scheme shareholders who elect to receive the scrip consideration are so dissimilar from the rights of the scheme shareholders who do not make an election as to make it impossible for them to consult together with a view to their common interest.

47 Second, if the special dividend is declared and paid by Citadel, there arises a question as to whether financial assistance is being given by Citadel to PEP BidCo to acquire the scheme shares. But in my view, the payment of the special dividend would not amount to financial assistance.

48 Section 260A of the Act provides that a company may financially assist a person to acquire shares in the company only if:

(a) giving the assistance does not materially prejudice (i) the interests of the company or its shareholders or (ii) the company’s ability to pay its creditors;

(b) the assistance is approved by shareholders under s 260B; or

(c) the assistance is exempt under s 260C.

49 The first question is whether the proposal in relation to the special dividend constitutes financial assistance at all within the meaning of the Act. The second question is whether, if it does, it is nevertheless permitted by s 260A.

50 As to the first question, it is well accepted that the term “financial assistance” has no technical meaning. The task is to examine the commercial realities of the transaction to determine whether it can properly be described as the giving of financial assistance by the company.

51 Now whilst there have been a number of decisions which have considered the issue of financial assistance in the context of dividends and schemes of arrangement, most of those decisions have considered whether the requirements of s 260A(a) have been met, without considering or deciding the threshold question as to whether the payment of a special dividend amounts to “financial assistance”. But in Re Legend Corporation Limited [2019] FCA 1249, O’Bryan J said (at [75]):

In my view, payment by Legend of the special dividend will not constitute financial assistance to acquire the Scheme shares. BidCo is not currently a shareholder of Legend and therefore will not receive the special dividend. The effect of the payment of the special dividend is merely to reduce the consideration payable for shares pursuant to the Scheme in a manner that reflects the cash outflow from the company and the consequential reduction in the net assets of Legend. While the Scheme Implementation Agreement anticipates the payment of the special dividend, the Scheme does not require the dividend to be paid (declaration of the dividend is at the election of Legend). The proper characterisation of these arrangements is that the consideration for the acquisition of the Scheme shares will be reduced to reflect the reduction in net assets of Legend resulting from payment of the dividend.

52 In my case, those observations apply equally to the Scheme. In particular, I would note that PEP BidCo is not currently a shareholder of Citadel and therefore will not receive the special dividend. Further, the effect of the payment of the special dividend is merely to reduce the consideration payable for the scheme shares in a manner that reflects the cash outflow from Citadel and the consequential reduction in its net assets. Further, whilst the SI Deed (as amended) anticipates the payment of the special dividend, the Scheme does not require the dividend to be paid. Declaration of the dividend is in the discretion of the Citadel Board.

53 Accordingly, the proper characterisation of these arrangements is that the consideration for the acquisition of the scheme shares will be reduced to reflect the reduction in net assets of Citadel resulting from any payment of the special dividend. This is not “financial assistance” within the meaning of the Act.

54 But in any event, in my view the payment of the special dividend will not prejudice Citadel, its shareholders or its ability to pay its creditors. In the present case, I accept the evidence of Citadel’s Chief Financial Officer, Ms Jennifer Martin, that in her view the financial position of Citadel generally and its asset and liability position in particular are such that Citadel’s net asset position is more than sufficient to meet the payment of the special dividend, and that the payment would not prejudice the interests of Citadel or its members or the ability of Citadel to pay its creditors.

55 Third, Citadel has on issue 388,308 employee share rights that remain outstanding. Citadel’s rules relating to its employee share rights plan gives the Citadel Board discretion to accelerate the vesting and lapsing of any or all employee share rights in the event of a proposed change of control of Citadel.

56 In accordance with the terms of this plan, Citadel’s Board has exercised its discretion and determined that, subject to the Scheme becoming effective, 179,120 employee share rights will lapse on the effective date, representing the employee share rights issued under Citadel’s FY21 long term incentive plan, other than those to be issued to Mr Mark McConnell, a director and the Chief Executive Officer of Citadel, subject to shareholder approval. Further, 209,188 employee share rights will vest on the effective date and will be cash settled in accordance with the terms of the employee share rights plan for an amount equal to $1,216,813.30, representing the employee share rights issued under Citadel’s FY19 LTI plan and FY20 LTI plan, other than those to be issued to Mr McConnell, subject to shareholder approval.

57 No Citadel directors have a relevant interest in employee share rights. However, subject to obtaining shareholder approval at its annual general meeting scheduled for 19 November 2020, Citadel proposes to issue Mr McConnell 61,551 employee share rights under the terms of Citadel’s FY20 LTI plan pursuant to his employment arrangements, the material terms of which were previously announced to the ASX on 13 November 2019, and 89,148 employee share rights under the terms of Citadel’s FY21 LTI plan.

58 If the issue of the employee share rights to Mr McConnell is approved by shareholders, then subject to the Scheme becoming effective, Citadel’s Board has exercised its discretion in accordance with the terms of the employee share rights plan and determined that the 61,551 employee share rights issued to Mr McConnell under the terms of Citadel’s FY20 LTI plan will vest on the effective date and will be cash settled in accordance with the terms of the employee share rights plan for an amount equal to $350,840.70, and the 89,148 employee share rights issued to Mr McConnell under Citadel’s FY21 LTI plan will lapse on the effective date.

59 In addition, Mr McConnell is eligible to participate in Citadel’s short term incentive plan for the financial year ending 30 June 2021. The STI plan provides executives with the opportunity to earn an annual incentive award which is delivered in cash subject to the satisfaction of annual performance against key performance conditions set and assessed by the Citadel Board. In accordance with the terms of the STI plan, in the event that a change of control of Citadel occurs during the relevant performance period, which will occur if the Scheme becomes effective, subject to him remaining employed by Citadel, Mr McConnell will be entitled to receive a proportionate amount of his annual incentive award having regard to service completed and performance up until the change of control event. Where such amount is payable, payment will not be made before the effective date, and will not exceed $440,000, being the maximum value of Mr McConnell’s annual incentive award under the STI plan for the current performance year. These matters are disclosed in the Scheme Booklet, where it is also stated that Citadel shareholders should have regard to these arrangements when considering Mr McConnell’s recommendation of the Scheme, which appears throughout the Scheme Booklet.

60 There are two issues which Citadel has raised for my consideration in relation to the proposed treatment of the employee share rights and short term incentives.

61 A question may arise as to whether those persons with the benefit of existing employee share rights who are also current shareholders should form a separate class from those shareholders who do not hold such rights because they will receive a benefit from the Scheme. In Re Skilled (2015) 113 ACSR 525 Robson J said (at [82]):

I am satisfied that the performance rights or options held by some employees do not give rise to a separate class of members. It is worth noting at the outset that the rights will not vest until after the meeting to approve the scheme is held. Accordingly, the issue of additional shares will not influence the voting at the meeting directly. The question is whether the rights and options themselves (and the prospect of additional shares upon their vesting) gives rise to a divergence of interests with other shareholders. I do not consider that it does. The shares to be issued if the rights or options vest are not of a different type than those of other shareholders. Moreover, it appears to me that the employees with performance rights or options are in no different position from any other employee of the company who would be impacted by the scheme’s implementation in different ways on the basis of various interests extraneous to their status as members.

62 These observations have been applied by me in other cases in relation to short term and long term performance rights and cash and equity rewards granted pursuant to employee incentive plans. In Re Amcor [2019] FCA 346, I noted (at [86]):

Accordingly, no separate class meetings are necessary or desirable. The holders of incentives who are also Amcor shareholders will participate in the Scheme on the same basis and receive the same consideration as Amcor shareholders who are not holders of incentives. That is, all shareholders are being treated equally under the Scheme. There is no additional benefit being offered by New Amcor to these shareholders under or in connection with the Scheme.

63 These observations apply with equal force to the Scheme proposed by Citadel, such that separate class meetings are not necessary or desirable as a result of the proposed treatment of the employee share rights.

64 Further, as noted above, if the Scheme becomes effective and Mr McConnell remains employed by Citadel, he may become entitled to receive a proportionate amount of his annual incentive award under the STI plan for the financial year ending 30 June 2021. In my view the nature and extent of any additional benefits that it might be said that Mr McConnell will become entitled to if the Scheme is implemented are not such as to make it inappropriate for him to make a voting recommendation to members. In any event, the arrangements are adequately disclosed in the Scheme Booklet, and shareholders are expressly told to have regard to these arrangements when considering Mr McConnell’s recommendation of the Scheme.

65 Fourth, the proposed treatment of foreign scheme shareholders and UK shareholders under the Scheme does not give rise to a requirement for separate class meetings.

66 Foreign scheme shareholders are not entitled to make an election to receive the scrip consideration. If the Scheme becomes effective, foreign scheme shareholders will receive the cash consideration in respect of all their scheme shares. A foreign scheme shareholder is a Citadel shareholder whose registered address as shown on the Citadel share register on the record date is a place outside of Australia, New Zealand or the United Kingdom. As at 23 October 2020 Citadel had 75 foreign scheme shareholders holding in aggregate approximately 1.06% of Citadel’s issued shares.

67 In my view, the proposed treatment of foreign scheme shareholders under the Scheme does not require those shareholders to meet together as a separate class for the purposes of considering the proposed scheme of arrangement.

68 It is common practice in schemes of arrangement where scrip comprises the proposed scheme consideration that identified foreign shareholders are not entitled to receive the scrip consideration but instead receive cash as consideration for their scheme shares. This is often achieved via the use of sale facility mechanism. In particular, the scrip to which foreign shareholders would otherwise have been entitled is instead issued to a sale agent on their behalf, who must subsequently sell those shares and remit the cash proceeds of the sale to the foreign shareholder. Such cases do not require the ineligible foreign shareholders to meet together as a separate class for the purposes of considering the proposed scheme of arrangement. The relevant authorities were discussed by me in Re Amcor at [42] to [44]. For present purposes, in my view there is no material difference between the outcome achieved via the sale agent facility just discussed and the payment of cash consideration directly to the foreign shareholders instead of issuing scrip that is contemplated by the Scheme. This is particularly so where, as here, the amount of the cash consideration is the same as the paid up capital amount of the scrip consideration. As such, in relation to the proposed treatment of foreign scheme shareholders under the Scheme, no separate class arises.

69 Further, under the Scheme, holders of scheme shares who are resident in the United Kingdom are not considered to be foreign scheme shareholders. But the Scheme provides an alternate mechanism for the issue of scrip consideration to UK shareholders from other scheme shareholders. This is to facilitate the availability of scrip-for-scrip rollover relief under the tax law of the United Kingdom. The particular mechanism is contained in the Scheme. It provides for UK shareholders who are to receive the scrip consideration to be “rolled up” the chain of holding companies by making a series of irrevocable directions. This will occur simultaneously such that UK shareholders will receive their Class B shares in HoldCo at the same time as other scheme shareholders who have elected to receive the scrip consideration. In my view the rights of UK shareholders are not so dissimilar to other scheme shareholders who will receive the scrip consideration as to require separate class meetings.

70 Fifth, schemes of arrangement are not required to be the subject of a report by an independent expert unless the parties have a common director, or the acquiring company controls 30% of the scheme company, neither of which is the case here.

71 Nevertheless, as I have indicated, Citadel has obtained a report from Mr Edwards as to whether, in his opinion, the Scheme is in the best interests of Citadel shareholders. And as I have said, Mr Edwards concludes that the Scheme is fair and reasonable and hence in the best interests of the scheme shareholders, in the absence of a superior alternative proposal emerging.

Section 411(17)

72 My power to approve a scheme is restricted by s 411(17). At the approval stage, I must be satisfied that there is no proscribed purpose as described in s 411(17)(a) or there must be provided to me a statement in writing by ASIC that it has no objection to the arrangement (s 411(17)(b)). But if such a statement is provided by ASIC, it will not be provided until the second court hearing.

73 In my view, s 411(17) does not present a bar to a meeting now being ordered to be convened as it seems likely that ASIC will produce the relevant statement at the second court hearing. Given that ASIC does not oppose the application for convening the meeting, it is appropriate for me to proceed at this stage on the basis that an application for approval would be unopposed by ASIC, and that ASIC will in due course provide a statement in the form contemplated by s 411(17)(b). I have taken comfort from ASIC’s letter dated 20 October 2020 to the directors of Citadel in this respect.

74 Accordingly, in circumstances where it is likely that ASIC will produce a statement under s 411(17)(b) and there are presently no matters supporting an inference that there is any proscribed purpose, the requirements of s 411(17) do not present a bar to me ordering that a meeting be now convened.

Adequacy of information

75 Relevant to the exercise of my discretion is the adequacy of the information to be provided to shareholders by way of explanation of the Scheme. This involves considering the adequacy of the disclosure in the Scheme Booklet.

76 There are three aspects to the explanatory statement required by s 412(1)(a) of the Act.

77 First, the explanatory statement must explain the effect of the arrangement, and in particular state any material interest of the directors, and the effect on those interests of the arrangement so far as it is different from the effect on the like interests of other persons. These matters are addressed in the Scheme Booklet.

78 Second, the explanatory statement must set out the prescribed information. Citadel has prepared a schedule which demonstrates compliance with these disclosure obligations, indicating where in the Scheme Booklet each of the requirements is met. I am satisfied with this.

79 Third, the explanatory statement must set out any other information that is material to the making of a decision whether or not to agree with the arrangement, being information which is within the knowledge of the directors and has not previously been disclosed. The Scheme Booklet is clear and comprehensive. In addition, the independent expert report contains a detailed evaluation of the Scheme, presented in a way that enables a shareholder to form a view of the merits of the Scheme.

80 Further, the verification procedures implemented to ensure that the Scheme Booklet does not contain any misleading or deceptive statements and satisfies the applicable disclosure requirements in relation to the information set out in the Scheme Booklet are, in my view, adequate.

81 Let me deal with another aspect.

82 As the Scheme is a members’ scheme only, it is necessary that the explanatory statement be registered by ASIC before the notice of meeting is sent to Citadel shareholders. Before registering the statement, ASIC must conclude that it appears to comply with the requirements of the Act, and must form the opinion that the statement does not contain any matter that is false in a material particular or materially misleading in the form and context where it appears.

83 Citadel has provided the proposed Scheme Booklet to ASIC, together with all amendments. There does not appear to be any unresolved matter of disagreement between ASIC and Citadel such as to impede registration. I do not see any difficulty concerning registration.

84 Now s 411(1) provides that if I have made an order convening a meeting of members, I may approve the explanatory statement. But I do not propose to formally do so. In view of the requirement for registration by ASIC and the criteria that ASIC must apply, it is more appropriate that the explanatory statement for a members’ scheme be dealt with in that fashion. But I should stress that not to so formally approve should not be seen as casting any doubt on the accuracy or adequacy of the Scheme Booklet which comprises the explanatory statement or that it is not suitable for registration by ASIC.

Scheme meeting

85 It is proposed that the scheme meeting will be held virtually at 11.00 am on Tuesday, 1 December 2020 via an online platform. Each Citadel shareholder who is registered on the Citadel share register at 7.00 pm (AEDT) on 29 November 2020 is entitled to attend and vote at the scheme meeting personally or by proxy.

86 As a result of the health risks associated with the COVID-19 pandemic, it is not appropriate to have a physical meeting. Instead, the meeting is to be held electronically through an online platform. Shareholders will be able to access the online platform by visiting a particular webpage address specified in the notice of meeting, which is annexed to the Scheme Booklet. The online platform will enable participants to view the scheme meeting live, vote on the relevant resolution in real time and ask questions online.

87 Such an arrangement is in accordance with the Federal and State government directions and restrictions and the Treasurer’s determination regarding electronic shareholder meetings. In particular, Pt 2 of the Corporations (Coronavirus Economic Response) Determination (No.3) 2020 (Cth) modifies the relevant provisions of the Act to permit shareholder meetings to be held electronically.

Conclusion

88 I am satisfied that the Scheme is of such a nature and cast in such terms that, if it achieves the statutory majorities at the scheme meeting, I would be likely to approve it, and that it is therefore appropriate to make the orders sought by Citadel.

89 In summary, the terms of the proposed Scheme are in a conventional form for an acquisition scheme. Further, there is no reason why the Scheme, if considered and adopted by the members, is not of such a nature as would be likely to be approved by me at the second hearing. Further, the Citadel shareholders are to be presented with an analysis of the proposed Scheme by an independent expert, including a detailed discussion of its advantages and disadvantages. Further, the Scheme Booklet meets the statutory requirements. Finally, it cannot be said that the Scheme appears on its face so blatantly unfair or otherwise inappropriate that it should be stopped in its tracks before going any further.

I certify that the preceding eighty-nine (89) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Beach. |

Associate: