Federal Court of Australia

Tax Practitioners Board v Caolboy [2020] FCA 1559

ORDERS

Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

PENAL NOTICE TO: ARLENE CAOLBOY IF YOU (BEING THE PERSON BOUND BY ORDERS 1 AND 2 OF THESE ORDERS): (A) REFUSE OR NEGLECT TO DO ANY ACT WITHIN THE TIME SPECIFIED IN ORDERS 1 OR 2 OF THESE ORDERS FOR THE DOING OF THE ACT; OR (B) DISOBEY ORDERS 1 OR 2 BY DOING AN ACT WHICH THE ORDER REQUIRES YOU NOT TO DO, YOU WILL BE LIABLE TO IMPRISONMENT, SEQUESTRATION OF PROPERTY OR OTHER PUNISHMENT. ANY OTHER PERSON WHO KNOWS OF THIS ORDER AND DOES ANYTHING WHICH HELPS OR PERMITS YOU TO BREACH THE TERMS OF THIS ORDER MAY BE SIMILARLY PUNISHED. |

THE COURT ORDERS THAT:

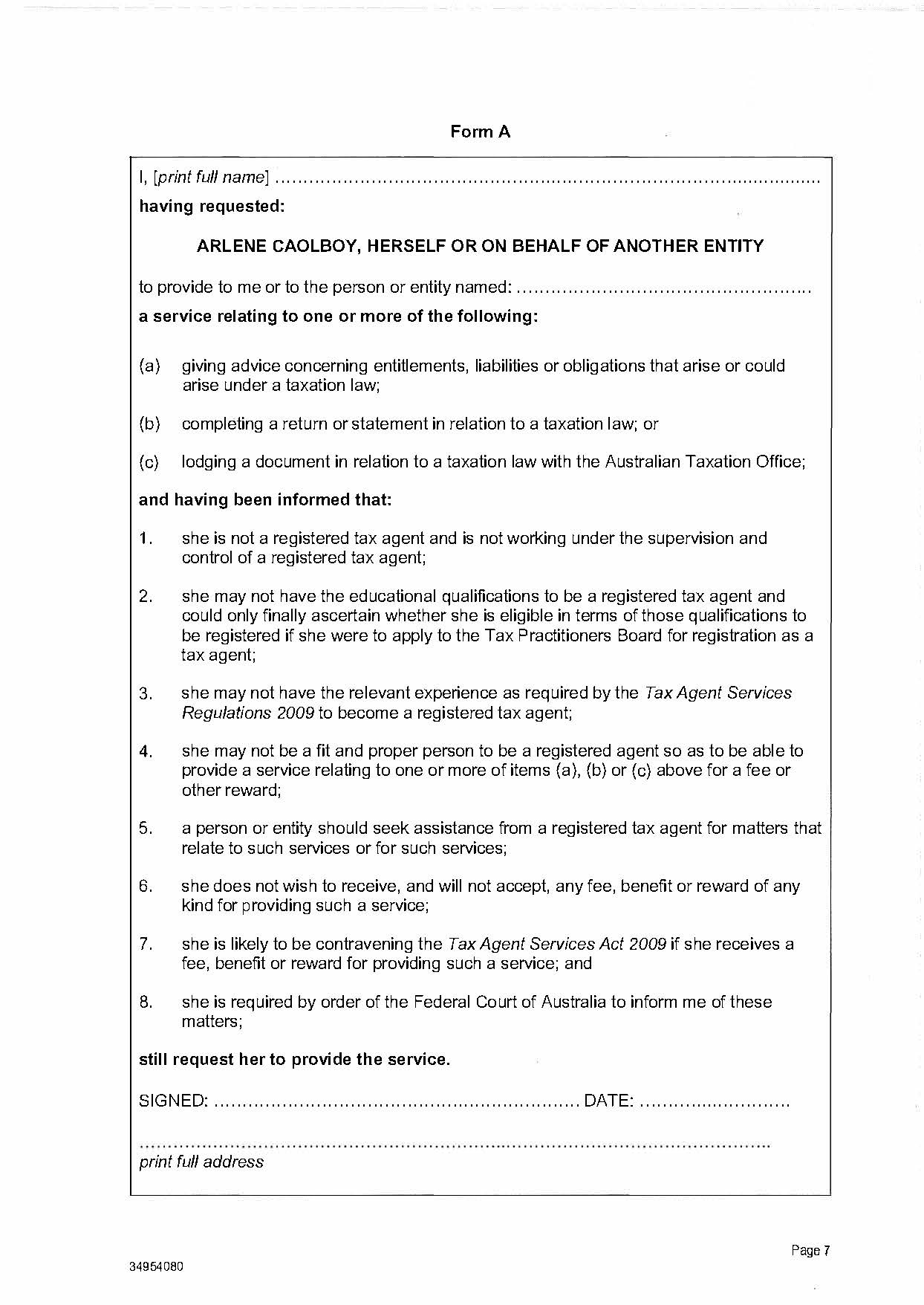

1. The respondent, for a period of three years from the date of this order, if requested to provide to another person or entity a service whether by her employees, agents or however otherwise, that relates to one or more of:

(a) advising another person or entity in relation to entitlements, liabilities or obligations in relation to an Australian taxation law;

(b) completing or lodging for another person or entity a return, statement or correspondence with the Commissioner in relation to an Australian taxation law; or

(c) representing another person or entity in their dealings with the Commissioner of Taxation,

must, before providing or agreeing to provide the said service, and unless then registered as a tax agent pursuant to the Tax Agent Services Act 2009 (Cth), inform the person of the matters referred to in paragraphs [1]-[8] of Form A annexed to these orders and, if the person or entity still requests the service be performed by the respondent:

(i) have the person or entity complete and sign a copy of Form A annexed to these orders;

(ii) retain a copy of the completed and signed form for a period of three years; and

(iii) provide any such completed and signed form to the applicant within 14 days of its request.

2. The respondent, for a period of three years from the date of this order, must not, unless then a registered tax agent pursuant to the Tax Agent Services Act, make any reference, in connection with the description or promotion of any services she offers to provide, to matters involving taxation or the Australian Tax Office unless that reference is a statement, or is closely accompanied by another statement, to the effect that she is not registered pursuant to the Tax Agent Services Act to provide tax agent services or BAS services.

3. The respondent pay penalties in the total amount of $40,000 to the Commissioner of Taxation, who is to receive those penalties on behalf of the Commonwealth. Those penalties are to be paid, as follows:

(a) $5,000 on or before 29 October 2023;

(b) $5,000 on or before 29 October 2024;

(c) $5,000 on or before 29 October 2025;

(d) $5,000 on or before 29 October 2026;

(e) $5,000 on or before 29 October 2027;

(f) $5,000 on or before 29 October 2028;

(g) $5,000 on or before 29 October 2029; and

(h) $5,000 on or before 29 October 2030.

4. There be no order as to costs.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

WHEELAHAN J:

Introduction

1 The Tax Practitioners Board is established by and has general administration of the Tax Agent Services Act 2009 (Cth) (Act). The object of the Act is to ensure that tax agent services are provided to the public in accordance with appropriate standards of professional and ethical conduct. The Act gives effect to that object by providing for the registration of tax agents. In order for an individual to be registered, the Board must be satisfied that the individual is a fit and proper person, that the individual meets certain requirements prescribed by the regulations relating to qualifications and experience, that the individual maintains professional indemnity insurance that meets the Board’s requirements, and in the case of the renewal of registration, that the individual meets the Board’s requirements in relation to continuing professional education. Upon registration, a registered tax agent must comply with several requirements, including the Code of Professional Conduct that is set out in Part 3 of the Act.

2 The Act provides for civil penalties for contravention of provisions that proscribe: (1) the provision of tax agent services without being registered under the Act; (2) the advertising of tax agent services when the person is not registered; and (3) a person falsely representing that he or she is a registered tax agent. The Board has standing to apply to the Court to seek civil penalties and injunctions in respect of contravening conduct.

3 By an originating application filed on 6 January 2020, the Board seeks pecuniary penalties, declarations, and injunctions against the respondent on the grounds that she advertised for and performed tax agent services without being registered under the Act, and on several occasions, she represented herself to individuals as being a registered tax agent, when she was not. The services that were provided by the respondent comprised work in connection with the preparation and lodgement of personal income tax returns for which she charged fees ranging between $100 and $455, with a typical fee of $165. The Board did not seek its costs of the proceeding.

4 The respondent, who was unrepresented in this proceeding, has co-operated with the Board and signed an amended statement of agreed facts, which was also signed by an Australian Government Solicitor lawyer who acts for the Board. At the hearing, the amended statement of agreed facts was tendered pursuant to s 191 of the Evidence Act 1995 (Cth). I shall refer to that document as the statement of agreed facts. By the statement of agreed facts, the respondent admitted the contraventions of the Act alleged in the Board’s statement of claim, except for some contraventions in relation to the unlawful advertising of tax agent services, which are no longer pressed. Further, the Board tendered a second statement of agreed facts in relation to the respondent’s health and financial circumstances, which is a topic to which I shall return.

5 In addition to the agreed facts, the Board tendered some correspondence from the Board to the respondent in June 2017, by which the Board notified the respondent of its concerns that she was advertising for, and providing tax agent services without being registered under the Act, together with the respondent’s reply.

6 For her part, the respondent prepared two affidavits, which due to COVID-19 restrictions were unsworn, but which the applicant tendered at the hearing. Those affidavits related to the respondent’s personal circumstances, which I shall address in due course.

The parties’ agreement as to penalties

7 Towards the conclusion of the hearing of the proceeding on 29 October 2020, I stood the matter down at the request of counsel for the Board so that instructions could be obtained in relation to submissions made by the respondent concerning her financial circumstances, and capacity to pay pecuniary penalties. Over the adjournment, the parties reached agreement to make a submission to the Court that penalties in the total sum of $40,000 should be ordered, payable in eight annual instalments of $5,000 each commencing on 29 October 2023.

8 While the parties’ agreement as to penalties does not fetter the Court’s discretion, it informs it: Tax Practitioners Board v Hogan [2012] FCA 642; 88 ATR 457. In the exercise of its discretion to fix penalties, the question before the Court is whether the parties’ proposal can be accepted as fixing an appropriate amount: Commonwealth v Director, Fair Work Building Industry Inspectorate (The Agreed Penalties Case) [2015] HCA 46; 258 CLR 482 at [48] (French CJ, Kiefel, Bell, Nettle, and Gordon JJ).

9 For the following reasons, I have determined that the penalty, and the mode of payment proposed by the parties, is appropriate, and I shall make orders accordingly.

The legislation

10 The following provisions of the Act are material.

11 Section 50-5 of the Act proscribes the provision of tax agent services for a fee –

50-5 Providing tax agent services if unregistered

(1) You contravene this subsection if:

(a) you provide a service that you know, or ought reasonably to know, is a *tax agent service; and

(b) the tax agent service is not a *BAS service or a *tax (financial) advice service; and

(c) you charge or receive a fee or other reward for providing the tax agent service; and

(d) you are not a *registered tax agent; and

(e) if you provide the tax agent service as a legal service—either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that tax agent service; or

(ii) subject to subsection (3), the service consists of preparing, or lodging, a return or a statement in the nature of a return.

Civil penalty:

(a) for an individual—250 penalty units; and

(b) for a body corporate—1,250 penalty units.

…

12 The terms tax agent service and BAS service are defined in the Act as follows –

90-5 Meaning of tax agent service

(1) A tax agent service is any service:

(a) that relates to:

(i) ascertaining liabilities, obligations or entitlements of an entity that arise, or could arise, under a *taxation law; or

(ii) advising an entity about liabilities, obligations or entitlements of the entity or another entity that arise, or could arise, under a taxation law; or

(iii) representing an entity in their dealings with the Commissioner; and

(b) that is provided in circumstances where the entity can reasonably be expected to rely on the service for either or both of the following purposes:

(i) to satisfy liabilities or obligations that arise, or could arise, under a taxation law;

(ii) to claim entitlements that arise, or could arise, under a taxation law.

(2) A service specified in the regulations for the purposes of this subsection is not a tax agent service.

…

90-10 Meaning of BAS service

(1) A BAS service is a *tax agent service:

(a) that relates to:

(i) ascertaining liabilities, obligations or entitlements of an entity that arise, or could arise, under a *BAS provision; or

(ii) advising an entity about liabilities, obligations or entitlements of the entity or another entity that arise, or could arise, under a BAS provision; or

(iii) representing an entity in their dealings with the Commissioner in relation to a BAS provision; and

(b) that is provided in circumstances where the entity can reasonably be expected to rely on the service for either or both of the following purposes:

(i) to satisfy liabilities or obligations that arise, or could arise, under a BAS provision;

(ii) to claim entitlements that arise, or could arise, under a BAS provision.

(1A) The Board may, by legislative instrument, specify that another service is a BAS service.

(2) A service specified in the regulations for the purposes of this subsection is not a BAS service.

13 In turn, by operation of s 3-5 of the Act, the term BAS provisions is defined by the Dictionary in s 995-1 of the Income Tax Assessment Act 1997 (Cth) as being referrable to a range of different provisions of taxation legislation which are described by reference to further layers of definitions such as indirect tax law, which includes the GST law, which itself is defined by s 195-1 of the A New Tax System (Goods and Services Tax) Act 1999 (Cth) as referring to other legislation, including regulations. There is a note to the definition of BAS provisions in s 995-1 of the Income Tax Assessment Act that BAS stands for Business Activity Statement. The parties’ agreement as to the facts and their characterisation relieves me from having to consider these provisions.

14 Section 50-10 of the Act proscribes the advertising of tax agent services by persons who are not registered tax agents –

50-10 Advertising tax agent services if unregistered

(1) You contravene this subsection if:

(a) you advertise that you will provide a *tax agent service; and

(b) the tax agent service is not a *BAS service or a *tax (financial) advice service; and

(c) you are not a *registered tax agent; and

(d) if the tax agent service would be provided as a legal service—either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that tax agent service; or

(ii) subject to subsection (3), the service would consist of preparing, or lodging, a return or a statement in the nature of a return; and

(e) if the tax agent service would be provided on a voluntary basis—you would not provide the service under a scheme approved by the Commissioner by notice published in the Gazette.

Civil penalty:

(a) for an individual—50 penalty units; and

(b) for a body corporate—250 penalty units.

(2) You contravene this subsection if:

(a) you advertise that you will provide a *BAS service; and

(b) you are not a *registered tax agent or BAS agent; and

(c) if the BAS service would be provided as a legal service—either:

(i) you are prohibited, under a *State law or *Territory law that regulates legal practice and the provision of legal services, from providing that BAS service; or

(ii) subject to subsection (4), the service would consist of preparing, or lodging, a return or a statement in the nature of a return; and

(d) if the BAS service relates to imports or exports to which an *indirect tax law applies—you are not a customs broker licensed under Part XI of the Customs Act 1901; and

(e) if the BAS service would be provided on a voluntary basis—you would not provide the service under a scheme approved by the Commissioner by notice published in the Gazette.

Civil penalty:

(a) for an individual—50 penalty units; and

(b) for a body corporate—250 penalty units.

…

15 Section 50-15 of the Act proscribes the making of an untrue representation that a person is a registered tax agent –

50-15 Representing that you are a registered tax agent, BAS agent or tax (financial) adviser if unregistered

You contravene this section if:

(a) you represent that you are a *registered tax agent, BAS agent or tax (financial) adviser; and

(b) that representation is untrue.

Civil penalty:

(a) for an individual—50 penalty units; and

(b) for a body corporate—250 penalty units.

…

16 Section 50-35 of the Act provides that the Board may apply on behalf of the Commonwealth to the Court for an order that a person who contravenes a civil penalty provision pay a pecuniary penalty to the Commonwealth. The power to apply for an order is conditioned on the application being made within four years of the contravention –

50-35 Federal Court may order you to pay a pecuniary penalty for contravening a civil penalty provision

Application for order

(1) Within 4 years after you contravene a civil penalty provision, the Board may apply on behalf of the Commonwealth to the *Federal Court for an order that you pay the Commonwealth a pecuniary penalty.

Court may order you to pay pecuniary penalty

(2) If the *Federal Court is satisfied that you have contravened a civil penalty provision, the Federal Court may order you to pay to the Commonwealth, for each contravention, the pecuniary penalty that the Federal Court determines is appropriate (but not more than the maximum amount specified for the provision).

Conduct contravening more than one civil penalty provision

(3) If conduct contravenes 2 or more civil penalty provisions of this Act, proceedings may be instituted against you in relation to the contravention of any one or more of those provisions. However, you are not liable to more than one pecuniary penalty in respect of the same conduct.

17 Section 70-5 of the Act empowers the Court to grant an injunction if it is satisfied that a person has engaged, or is proposing to engage in conduct that would constitute a contravention of a civil penalty provision –

70-5 Injunction to restrain or require certain conduct

(1) If, on the application of the Board, the *Federal Court is satisfied that you have engaged, or are proposing to engage, in conduct that would constitute a contravention of a civil penalty provision, the Federal Court may grant an injunction:

(a) restraining you from engaging in the conduct; or

(b) if in the Federal Court’s opinion it is desirable to do so, requiring you to do something.

(2) Before deciding the application, the *Federal Court may grant an interim injunction:

(a) restraining you from engaging in conduct; or

(b) requiring you to do something.

…

Agreed facts

18 The respondent has experience in bookkeeping, and some accounting. Over the years prior to the events the subject of this proceeding, she was employed by companies in bookkeeping roles.

19 At all times material to this proceeding, the respondent knew that persons and companies who wished lawfully to provide tax agent services or BAS services for a fee or other reward were required to be registered with the Board. She also knew that the Board had never assessed her as suitable for registration as a tax agent or a BAS agent, and that she was not a registered tax agent or BAS agent.

20 On 10 September 2013, the respondent had registered to her name the business name, “ABC Accounting Firm”. From at least about August 2015 until at least about August 2019, ABC Accounting Firm offered services in relation to, among other things, personal tax, company tax, Business Activity Statements, bookkeeping, and accounting. The services were offered by the respondent as a sole trader, although in some instances payments for the services were received into the bank account of a company, KMC Corporation Group Pty Ltd, of which the respondent was a director. The respondent offered her accounting services on internet sites, including LinkedIn, and Places to go in Melbourne.

Provision of tax agent services

21 Between about December 2015 and October 2018, the respondent provided services in relation to the preparation and lodgement of income tax returns, as set out in a schedule to the statement of agreed facts. It was agreed that the respondent knew and intended that the effect of providing the income tax services was to –

(a) ascertain the taxpayer’s liabilities, obligations or entitlements that arise, or could arise, under a taxation law; and/or

(b) advise the taxpayer about liabilities, obligations or entitlements that arise, or could arise, under a taxation law.

22 The respondent charged for, and in the usual course received a monetary payment as a reward for providing each agreed income tax service to each taxpayer. It was agreed that each taxpayer to whom the respondent provided services could reasonably have been expected to rely upon the income tax service provided to them for the purposes of satisfying liabilities or obligations, or claiming entitlements that arose, or could have arisen, under a taxation law. It was also agreed that there were no facts that would engage any of the criteria that would exclude the respondent from the proscription in s 50-5 of the Act.

23 The schedule to the statement of agreed facts showed that, in all, the respondent provided tax agent services to over 350 taxpayers, and the Board alleged 519 contraventions of the Act by the respondent in relation to the provision of those services. The schedule is not complete in relation to the fees that were charged for the individual services. While the fees varied, typical fees that were often charged were in the order of $110 and $165. Two fees of $440 each that appeared in the schedule were exceptional. The fees that were identified in the schedule totalled more than $38,000 but for most entries no fee was identified. In her affidavit dated 24 June 2020, the respondent stated that the fees that she received from her clients were around $12,000 in 2016, $49,000 in 2017, and $20,000 in 2018, which amounted to a total of $81,000.

Advertising

24 By its application, the Board alleged contraventions by the respondent advertising tax agent services and BAS services on her Facebook page. After the Court raised some issues as to whether on the agreed facts what was alleged constituted advertising, and if so, what service was advertised having regard to the separate treatment of the services in s 50-10(1) and (2) of the Act, the Board reasonably abandoned this claim.

25 The respondent maintained a publicly accessible LinkedIn page in her own name. In the period from 13 December 2016 to at least 17 July 2018, the respondent caused the following content to appear on her LinkedIn page –

36.1. ‘Summary

I have extensive experience in Accounting majoring in Bookkeeping, Management, Taxation and Auditing.

ABC Accounting Firm is been in business since 2013. Since then the business have acquired numerous of clients. Our business provides Accounting, Bookkeeping and Taxation Services.

Experience

Director

ABC Accounting Firm

July 2013 – Present (3 years 6 months)

…

Preparing and Lodging Company Tax Return

…

Preparing and Lodging Individual Tax Return

…

Registered Tax Agent:- GST, Tax Return’

26 It was agreed that by that content on her LinkedIn page, the respondent advertised and offered to the public services that related or could reasonably be understood to relate to one or more of the following tax services –

(a) ascertaining liabilities, obligations or entitlements of an entity that arise, or could arise, under a taxation law;

(b) advising an entity about liabilities, obligations or entitlements of the entity or another entity that arise, or could arise, under a taxation law; and

(c) representing an entity in their dealings with the Commissioner.

27 It was agreed that the services offered by the respondent on LinkedIn were offered to be provided for a fee, and were offered to be provided in such circumstances that a person or entity who acquired them could reasonably be expected to rely on the services for the purposes of satisfying their liabilities or obligations, or claiming their entitlements under a taxation law. It was agreed that the services offered on LinkedIn were tax agent services within the meaning of that expression in section 90-5 of the Act

28 The respondent also posted on the online event and business directory website, Places to go in Melbourne. In the period from about 8 November 2019 to at least 16 December 2019, the respondent caused the following content to appear on that website –

44.1. “ABC Accounting Firm

[Address and mobile phone number]

We offer the following services to our clients:

• Start up and set up new business

• Deal with Company tax return

• Deal with Individual tax return

• Prepare and lodge Tax liabilities such as GST, PAYG, Income tax and Payroll tax.

• Prepare and lodge superannuation

• Prepare Budget analysis

• Prepare Financial reports such as Cashflow Statements, Profit and Loss Balance Sheet

• Provide Bookkeeping services such as Accounts Payable, Accounts Receivable and Payroll.

ABC Accounting Firm will provide Accounting and Tax services. We will ensure that your accounts are prepared in accordance with Accounting Standards.

Our mission is simple and achievable and that’s by growing with our clients by giving them the right services they need.

29 It was agreed that the services offered by respondent on the Places to go in Melbourne website were offered to be provided for a fee, and were offered to be provided in such circumstances that a person or entity who acquired them could reasonably be expected to rely on the services for the purposes of satisfying their liabilities or obligations, or claiming their entitlements under a taxation law. It was agreed that the services offered on that website were tax agent services within the meaning of that expression in section 90-5 of the Act.

Untrue representations that the respondent was a registered tax agent

30 In about July 2016, about August 2017, and about July 2018, the respondent made untrue oral representations to three identified taxpayers that she was a registered tax agent.

Other matters

31 At [5] above, I referred to some correspondence between the Board and the respondent. On 5 June 2017, the Board sent a letter to the respondent informing her –

(a) of the requirement to be registered as a tax agent under the Act if she was charging or receiving a fee or other reward for providing a tax agent service;

(b) of the requirement to be registered as a BAS agent under the Act if she was charging or receiving a fee or other reward for providing a BAS service; and

(c) that it was concerned that she might have been providing tax agent services and BAS services while unregistered, and requesting that she provide a written acknowledgement that she would not provide tax agent services or BAS services for a fee while unregistered, or advertise the provision of tax agent services.

32 On 16 June 2017, the respondent in a letter to the Board confirmed that she would “not advertise, charge or receive fee or other reward for providing tax agent or BAS Services while unregistered.” The following day, on 17 June 2017, the Board notified the respondent that the Board would continue to monitor her activities, and that it may commence an investigation and apply to this Court for the imposition of penalties, and the respondent acknowledged receipt of that notification.

33 I infer from the agreed facts that following her receipt of the Board’s letter on 5 June 2017, and also following her commitment to the Board on 16 June 2017, the respondent continued to provide tax agent services, as evidenced by the services that post-date her letter that are itemised in the schedule to the statement of agreed facts, including many entries into 2018. The respondent did not dispute this inference when it was put to her during submissions.

34 On 16 November 2017, the respondent participated in a formal interview with the ATO during which she made relevant admissions, and on 23 February 2019, the respondent wrote to the Board relevantly admitting to all the contraventions that had been identified by the Board in correspondence sent to her, including contraventions that pre-dated those that are the subject of this application. Between March and May 2019, the respondent provided the Board with her complete client records, outlining to whom she had provided tax agent services, and participated in two meetings with the Board to discuss the admitted contraventions.

35 On 17 May 2019, the respondent made a voluntary disclosure to the ATO regarding the cash income that she received from her unauthorised tax agent services for the years 2014 to 2018.

The respondent’s circumstances

36 The respondent relied on evidence relating to her personal circumstances contained in the affidavits dated 24 June 2020 and 16 October 2020 and the statement of agreed facts dated 28 October 2020 in relation to the personal health and financial circumstances of the respondent, which was received on the basis that it did not supplant the other evidence on which the respondent relied: cf, Evidence Act, s 191(2)(b).

37 In her first affidavit, the respondent stated that she commenced acting as an unregistered tax agent in December 2015. She stated that she commenced with only a few taxpayers, and that her work gradually increased by word of mouth and advertising through Facebook. She stated that each year she charged taxpayers a set fee for preparing and lodging their tax returns. She stated that in the first year, she charged a fee of $110 per person, and then afterwards the fee increased to $165 in the year 2018. She stated that from 2015 to 2018, she had 534 clients. She stated that during this time, she was unemployed and not earning any income apart from a social security allowance, and that she was unable to pay her bills, rent and food.

38 The respondent stated that she suffers from diabetes, and has suffered a mild stroke. She takes medication for these illnesses. She is currently unemployed, stating that her unemployment was due to the ongoing treatments required for her health conditions.

39 The respondent took responsibility for her conduct, stating in one affidavit –

I’m aware that what I did was wrong and will not do it again. I’m not denying the allegations as I totally agree and will now face consequences of my wrong doing.

40 The respondent’s financial circumstances are difficult. The material before the Court indicates that she has little in the way of assets, the most significant being the balance of a bank account in the order of $11,777. Against that, the respondent is indebted to the ATO in the sum of $16,642, and Centrelink in the sum of $70,303, leaving a net position of debt over assets of $75,123. The respondent lives in a rented unit, and has regular liabilities for rent and utility accounts. She had recently been in receipt of some Jobseeker payments from Centrelink, but those payments have ceased.

The principles applicable to the fixing of civil penalties

41 The principles applicable to the imposition of civil penalties are well-known, and were recently considered by an enlarged Full Court in Pattinson v Australian Building and Construction Commissioner [2020] FCAFC 177. Those principles may be summarised as follows.

42 The authority that Parliament has invested in the Court to impose a penalty for contraventions of the Act is in aid of the statutory object of the Act, to which I referred at [1] above, namely to ensure that tax agent services are provided to the public in accordance with appropriate standards of professional and ethical conduct. The statutory object of the Act is directed to the protection of the public from unsuitable or unqualified persons giving advice, or assisting them in relation to their taxation affairs.

43 The principal, if not the only object of the imposition of a civil penalty for contravention of a civil penalty provision such as those appearing in the Act is deterrence. Penalties are imposed in an attempt to put a price on contravention that is sufficiently high to deter repetition by the contravener, and also by others who might be tempted to contravene the Act: Trade Practices Commission v CSR Limited [1990] FCA 762; 13 ATPR 41-076 at 52, 152 (French J), cited in Commonwealth v Director, Fair Work Building Industry Inspectorate (The Agreed Penalties Case) [2015] HCA 46; 258 CLR 482 at [55].

44 Relevant factors in the overall assessment of penalty include: the maximum penalties for the contraventions that are fixed by the Act; the nature, character and seriousness of the conduct; any loss and damage caused; the circumstances in which the conduct took place; the means of the contravener; the deliberateness of the conduct and the time over which it occurred; the attitude of the contravener as to compliance or contravention; any co-operation with the regulator; and contrition. The material considerations may pull in different directions, and the task of identifying and giving weight to those considerations involves questions of discretion, and of degree. There are four further considerations that are relevant.

45 First, the penalties imposed must be proportionate to the seriousness of the conduct giving rise to the contraventions.

46 Second, where multiple contraventions arise from a course of conduct, in imposing penalties care must be taken by the Court to avoid double punishment. This does not mean that there is a search for a single course of conduct. Rather, in the case of multiple contraventions it is necessary to examine all the conduct and to enquire how its course and its explanation factually and legally informs the imposition of penal orders so as to avoid double punishment: Transport Workers’ Union of Australia v Registered Organisations Commissioner [No 2] [2018] FCAFC 203; 267 FCR 203 at [91] (Allsop CJ, Collier and Rangiah JJ). This examination does not commence or end with an assumption that contraventions are part of a single course of conduct, or confine the maximum allowable penalty to that which would be applicable for one contravention: Australian Building and Construction Commissioner v Construction, Forestry, Maritime, Mining and Energy Union (The Nine Brisbane Sites Appeal) [2019] FCAFC 59; 269 FCR 262 at [12] (Allsop CJ, Griffiths J at [13] agreeing). This issue raises questions of fact and degree that may inform the exercise of the Court’s discretion in fixing penalties for the individual contraventions.

47 Third, there should in the case of multiple contraventions be a final check on the overall result to ensure that the total of the penalties that are imposed on a respondent for multiple contraventions is not excessive.

48 Fourth, while a contravener’s financial circumstances are relevant to determining appropriate penalties, it remains necessary to focus on deterrence as the principal purpose of the penalties, which includes general deterrence. In the case of both a corporation and an individual, penalties are not provable in a liquidation or a bankruptcy: Corporations Act 2001 (Cth), s 553B; Bankruptcy Act 1966 (Cth), ss 82(3) and 153(1); Mathers v Commonwealth [2004] FCA 217; 134 FCR 135 (Heerey J). Under s 50-45 of the Act, a penalty that the Court orders a person to pay is payable to the Commonwealth, and the Commissioner of Taxation may enforce the order as if it were a judgment of the Court. A judgment of this Court made in Victoria is enforceable as if it were a judgment or order of the Supreme Court of Victoria, in respect of which there is a 15 year limitation period from the date on which the judgment becomes enforceable: Federal Court of Australia Act 1976 (Cth), s 53(1); Federal Court Rules 2011 (Cth), r 41.10; Limitation of Actions Act 1958 (Vic), s 5(4); Commissioner of Taxation v Pavihi [2019] FCA 2056 at [25]-[27].

49 Nonetheless, it has been held that it may be appropriate to order a corporation that is in liquidation, or that faces insolvency, to pay an appropriate penalty as a deterrent to others: see Australian Competition and Consumer Commission v High Adventure Pty Ltd [2005] FCAFC 247 at [11] (Heerey, Finkelstein and Allsop JJ); Australian Securities and Investments Commission v AGM Markets Pty Ltd (in liq) (No 4) [2020] FCA 1499 at [34]-[35] (Beach J) and the cases cited therein. Corporations may be wound up and dissolved if their continued trading is frustrated by a liability to pay substantial civil penalties.

50 The position is different in relation to natural persons. The burden of a liability to pay a civil penalty may be inescapable. This has a human element to it, because the liability of an individual to pay a civil penalty that has no real prospect of being discharged may be crushing: cf, Tax Practitioners Board v Su [2014] FCA 731 at [25] (Jagot J); Tax Practitioners Board v Dedic [2014] FCA 511; 98 ATR 373 at [8] (Davies J). Thus, the deterrent quality of a penalty is to be balanced against the consideration that it should not be so high as to be oppressive, and that if deterrence is the object, the penalty should not be greater than what is required to achieve that object: NW Frozen Foods Pty Ltd v Australian Competition & Consumer Commission (1996) 71 FCR 285 at 293 (Burchett and Kiefel JJ), cited in Pattinson v Australian Building and Construction Commissioner at [100] and [102] (Allsop CJ, White and Wigney JJ, Besanko and Bromwich JJ at [226] agreeing).

51 The deterrent effect of a penalty is related to the sting or burden which the penalty imposes on the contravener. That is because, “[o]ther things being equal, it is assumed that the greater the sting or burden of the penalty, the more likely it will be that the contravener will seek to avoid the risk of subjection to further penalties and thus the more likely it will be that the contravener is deterred from further contraventions; likewise, the more potent will be the example that the penalty sets for other would-be contraveners and therefore the greater the penalty’s general deterrent effect.”: Australian Building and Construction Commissioner v Construction Forestry Mining and Energy Union [2018] HCA 3; 262 CLR 157 at [116] (Keane, Nettle and Gordon JJ). The implied power under s 546 of the Fair Work Act to make a personal payment order that was the subject of that case may be exercised in aid of ensuring that a penalty imposes an appropriate burden on the contravener. It is the imposition of the burden of the penalty that is directed to achieving the specific and general deterrent effect of the penalty. To give effect to the object of general deterrence, a penalty should be sufficiently high to put a price on contravention so that others are deterred from engaging in contraventions of a similar kind. The relative magnitude of the penalty, and the burden that it imposes on an individual may be related to the individual’s circumstances, so that in respect of objectively serious contraventions of the Act by an individual, if a penalty is seen to have serious consequences to that individual, it will further the object of both specific and general deterrence.

The parties’ submissions on the appropriate penalty

52 The Board’s submissions on the appropriate penalty addressed in turn each of the three categories of contraventions –

(1) the tax agent services contraventions of s 50-5 of the Act;

(2) the advertising contraventions of s 50-10 of the Act; and

(3) the representation contraventions of s 50-15 of the Act.

53 The Board’s submissions addressed the application of the totality principle in respect the Board’s proposed penalty for each of those categories separately.

54 The respondent’s submissions also addressed each of those categories, although beyond restating her admissions and other agreed facts, the material substance of the respondent’s submissions was limited to stating that while she understood and did not disagree with severe penalties being imposed, because of her circumstances, she would not be able to pay for more $100 per month, and she sought an instalment order.

The tax agent services contraventions

55 It was agreed that the respondent contravened s 50-5 of the Act by providing tax agent services while not being a registered tax agent on 519 occasions across the years 2016, 2017, and 2018. The maximum penalty for each individual contravention is 250 penalty units. In dollar terms, the maximum penalty amounts to $45,000 for each contravention up until 30 June 2017, and $52,500 for each contravention thereafter.

56 The Board submitted that where the respondent provided a bundle of tax services to the same taxpayer at around the same time, those services should be treated as within a single course of conduct and grouped as a single contravention, with the effect that the number of contraventions by the respondent should be reduced from 519 to 495, comprising 475 individual contraventions, and 20 courses of conduct. Nonetheless, the Board submitted that the Court could impose a maximum penalty for the total number of admitted contraventions, without taking account of that reduction.

57 The Board submitted that the nature and extent of the respondent’s conduct that gave rise to the tax agent services contraventions should be understood as occupying a position at the more serious end of the spectrum. The Board submitted that the respondent’s conduct was deliberate, organised, systematic, sustained, and protracted. The Board submitted that it involved a very significant number of contraventions and exposed a very significant number of individual taxpayers to a situation in which tax agent services were provided to them, without the protections offered by a person who is registered under the Act and subject to regulation by the Board. The Board submitted that the contraventions formed part of an enterprise designed to make a profit, that the respondent was motivated by commercial gain, and that she in fact derived a substantial financial advantage from the contraventions. The Board also submitted that the respondent’s contravening conduct was aggravated from at least 16 June 2017, when she committed to the Board that she would not charge for providing tax agent services while unregistered. The Board submitted that this provided a powerful justification for the imposition of a higher penalty in respect of contraventions that occurred after that date.

58 The Board made further submissions in relation to other matters that it said should inform the Court’s determination on the appropriate penalty for the respondent’s tax agent services contraventions. The Board submitted that considerations of general deterrence were much more significant than specific deterrence, and noted that the respondent had ceased providing tax agent services, had made full admissions and had shown appropriate contrition. The Board accepted that it was a substantial mitigating factor that the respondent admitted to each of the 519 contraventions at the earliest opportunity in this proceeding, and that a meaningful discount should be given to the respondent in recognition of her co-operation and acknowledgment of liability. The Board acknowledged that the respondent had not been found to have previously engaged in the same or similar conduct in the past. I pause to note that I do not give that consideration much weight because it is swamped by other factors such as the respondent’s persistence in her contraventions after the Board wrote to her in June 2017. In relation to the respondent’s financial circumstances and her medical conditions affecting her future earning capacity, the Board submitted that while those were relevant considerations, it remained necessary to ensure that the penalties imposed were at a level sufficient to satisfy the objective of general deterrence, and that giving effect to that object may often require the imposition of penalties that are beyond the financial means of the particular wrongdoer.

59 It is unnecessary that I set out the Board’s submissions as to the appropriate range of total penalties, as they were overtaken by the joint submission that penalties in the total sum of $40,000 should be imposed.

The advertising contraventions

60 It is agreed that the respondent contravened s 50-10 of the Act by advertising tax agent services while not a registered tax agent on two occasions. The maximum penalty for each individual contravention is 50 penalty units. In dollar terms, that maximum penalty amounts to $9,000 for each contravention up until 30 June 2017, and $10,500 thereafter.

61 In respect of the LinkedIn advertising contravention, the Board submitted that the LinkedIn advertisement was published for a sustained and substantial period in excess of three years, which was largely co-extensive with the period during which the respondent provided tax agent services while unregistered. The Board submitted that it was important that the LinkedIn advertisement was maintained for a period in excess of two years after the respondent committed to the Board that she would not charge for providing tax agent services while unregistered.

62 In respect of the Places to go in Melbourne advertising contravention, the Board submitted that there was a clear imperative for a substantial penalty to give effect to the need for specific deterrence, and to a lesser extent, general deterrence. The Board emphasised that this advertisement was displayed in November and December 2019, shortly before this proceeding was commenced on 6 January 2020, and after the respondent had made her commitment to the Board and she had been put on notice that the Board would continue to monitor her activities.

The representation contraventions

63 It was agreed that the respondent contravened s 50-15 of the Act on three occasions by representing that she was a registered tax agent, when that representation was untrue. In dollar terms, that maximum penalty amounts to $9,000 for each contravention up until 30 June 2017, and $10,500 thereafter.

Consideration of the appropriate penalty

64 Normally, in determining an appropriate penalty, careful attention should be given to the statutory maximum: Markarian v The Queen [2005] HCA 25; 228 CLR 357 at [31] (Gleeson CJ, Gummow, Hayne and Callinan JJ). Here, the statutory maximum is of limited utility, because if each contravention were to attract a maximum penalty, the total sum would exceed $26 million, which in the circumstances of this case, is not a useful starting point.

65 The respondent committed over 500 of contraventions of the Act spanning 2016, 2017, and 2018 which took the form of a consistent course of business activity. In this sense, all the contraventions are factually linked. In my view, it is appropriate in assessing a proportionate response to the respondent’s contraventions to stand back and to view the conduct in its totality as a means of properly informing the assessment of penalties. This approach takes the totality principle as a starting point. Taking a broad view of a contravener’s conduct in this way has been endorsed in other cases of numerically high contraventions of civil penalty provisions resulting from a course of business or conduct: see, Australian Competition and Consumer Commission v Coles Supermarkets [2015] FCA 330 at [17]-[18] (Allsop CJ); Australian Securities and Investments Commission v Commonwealth Bank of Australia [2020] FCA 790 at [65] (Beach J). And in an appropriate case, the Court may impose a single penalty for multiple contraventions where that course is agreed or accepted as being appropriate by the parties: Australian Building and Construction Commissioner v Construction Forestry Mining and Energy Union [2017] FCAFC 113; 254 FCR 68 at [149] (Dowsett, Greenwood and Wigney JJ).

66 I accept the Board’s submissions that are set out at [57] above about the seriousness of the respondent’s contravening conduct. I find that the respondent’s contraventions were calculated, and occurred for the purposes of achieving financial gain. Taken as a whole, the contraventions are towards the serious end of the spectrum. The factors that contribute to the seriousness of the conduct include the vulnerability of those members of the public to whom the respondent provided tax agent services. Those persons were vulnerable to the risk inherent in having their tax affairs managed by a person without the requisite qualifications to obtain registration by the Board. Further, the circumstances that the respondent continued to provide tax agent services and advertised for them after giving a commitment to the Board not to do so, and the admitted false representations that she was a registered tax agent that she made to three persons, reinforce the objective seriousness of her contraventions.

67 Counsel for the Board cited a number of first instance decisions involving other circumstances in support of submissions directed to parity. I have considered those decisions, but in the end I am drawn to the conclusion that no two cases are exactly alike, and that the present case is to be considered on its own terms. No useful conclusions are to be drawn from comparing the facts of this case with the facts of other cases.

68 The overriding consideration in the present case is general deterrence, although despite the respondent’s statement of acceptance of wrongdoing to which I referred at [39] above, some measure of specific deterrence also has a role to play.

69 I take particular account of the fact that the respondent’s co-operation and admissions have saved considerable costs and Court time, and I have given them substantial weight. Were it not for the respondent’s co-operation, an appropriate penalty would reasonably have to be much higher than the $40,000 proposed having regard to the objective seriousness of the contraventions.

70 I have been very mindful of the respondent’s personal and financial circumstances. I have evaluated the relevance of the respondent’s circumstances in the way I have indicated at [48]-[51] above. In my judgment, taking account of those circumstances a substantial penalty is warranted in order to give effect to the object of general deterrence. The imposition of penalties totalling $40,000 should be seen as a substantial burden on the respondent, and therefore a significant price to pay for the contraventions, but without being crushing. Against the context of the respondent’s personal circumstances, the burden of the proposed penalty on her is in my estimation sufficiently high that others will be liable to be deterred from engaging in contraventions of a similar kind.

The declarations sought by the Board

71 The Board also sought a series of declarations in terms set out in its originating application. The terms of the declarations sought were complex, in substance setting out all of the elements of proof of the admitted contraventions, including references to alternate bases of liability, and incorporating by reference a schedule to the statement of claim.

72 The Board submitted that as a public regulator charged with enforcing the Act, it had a real interest in seeking the declarations sought, which would serve the public purpose of marking the Court’s disapproval of the respondent’s serious misconduct in contravention of the Act. As a matter of principle, that submission should be accepted. However, I am not persuaded that the declarations sought by the Board should be made in this proceeding. By reason of their complexity, the terms of the declarations would not in a practical sense add to the utility of the imposition of penalties, and the reasons for their imposition, and I decline to make them. Instead, I shall summarise in the conclusions below the contravention for which penalties in the total sum of $40,000 are to be imposed.

Consideration of the injunctions sought

73 The Board sought injunctions against the respondent in terms similar to those granted by Logan J in Tax Practitioners Board v Hogan [2012] FCA 642; 88 ATR 457. The respondent did not oppose the injunctions sought.

74 The proposed injunctions operate for a period of three years, unless the respondent becomes a registered tax agent. The effect of the injunctions is twofold. First, if the respondent is requested to provide tax agent services, she must inform the person seeking her services that she is not a registered tax agent, and of other relevant matters including that if she receives a fee for providing those services, she is likely to be contravening the Act. If that person nonetheless wishes to proceed, the respondent must have that person sign a form attesting to having been informed of those matters, and the respondent must retain a copy of any such form to provide to the Board upon its request. Second, the respondent is restrained from making any reference to matters involving taxation or the ATO in connection with the promotion of any services that she may provide, unless she makes clear that she is not registered to provide tax agent services or BAS services.

75 I consider that the proposed injunctions are an appropriate means to further the protective object of the Act, and I shall grant those injunctions.

Conclusion

76 The respondent engaged in a consistent course of business activity over a sustained period of time, which involved serious contraventions of the Act. Those contraventions were –

(1) providing tax agent services while not a registered tax agent on 519 occasions across the years 2016, 2017, and 2018, in contravention of s 50-5 of the Act;

(2) advertising tax agent services while not a registered tax agent on two occasions, in contravention of s 50-10 of the Act; and

(3) representing that she was a registered tax agent, when she was not, on three occasions, in contravention of s 50-15 of the Act.

77 For all of the above contraventions, penalties in the agreed sum of $40,000 shall be imposed on the respondent, which shall be payable in eight annual instalments of $5,000 each, commencing in 2023 and continuing through until 2030.

78 I shall make orders accordingly.

I certify that the preceding seventy-eight (78) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Wheelahan. |

Associate: