Federal Court of Australia

Hanna v Deputy Commissioner of Taxation [2020] FCA 1467

ORDERS

Applicant | ||

AND: | DEPUTY COMMISSIONER OF TAXATION Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The Application for an extension of time is granted, with time being extended to 20 August 2020.

2. The Application for leave to appeal is refused.

3. The proceeding is dismissed.

4. The Applicant is to pay the costs of the Respondent.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

FLICK J

1 Now before the Court is an Application for an extension of time and an application for leave to appeal from the decision of Jagot J in Hanna v Deputy Commission of Taxation [2020] FCA 1021.

2 In that decision reasons were published and orders were made by her Honour dismissing an application for an extension of time in which to seek judicial review pursuant to the Administrative Decisions (Judicial Review) Act 1977 (Cth) (the “Judicial Review Act”). Review was sought of decisions communicated to the Applicant by way of letters dated 8 August 2019. Those letters also advised the Applicant that any application for judicial review was required to be filed within 28 days, namely by 5 September 2019. On 13 September 2019 the Applicant filed an application for an extension of time. In dismissing that application, her Honour concluded that the Applicant was, at the time of making that application, an undischarged bankrupt and was, accordingly, not a “person aggrieved” for the purposes of the Judicial Review Act: [2020] FCA 1021 at [31]. In so concluding, her Honour reviewed authorities going to the status of an undischarged bankrupt and the submission advanced by the Respondent that the Applicant lacked standing. Her Honour concluded:

[31] I accept these submissions. The authority referred to above clearly supports the proposition that a person such as the applicant has no proprietary interest in the bankrupt estate, and is therefore not a “person aggrieved” by the remission decisions for the purposes of the ADJR Act. Although the cases referred to by the respondent qualify that an undischarged bankrupt may have standing where the relevant decision affects some future interest that exists after he or she has been discharged from bankruptcy, no submissions to this effect were put by the applicant.

[32] It necessarily follows that the application is without merit, leading to the conclusion that the application for an extension of time should be dismissed.

3 A decision dismissing an application for an extension of time, such as the decision of her Honour, is an interlocutory decision: Ferdinands v Chief of Army [2009] FCA 22 at [4] to [8] per Mansfield J. There is no right of appeal from such decisions. Leave to appeal is required: Federal Court of Australia Act 1976 (Cth), s 24(1A). And any application for leave to appeal is required to be filed within 14 days: Federal Court Rules 2011 (Cth), r 35.13. But that time can be extended and may be extended where it is necessary to do justice as between the parties: Gallo v Dawson (1990) 64 ALJR 458 at 459 per McHugh J.

4 On the facts of the present case, it was on 20 August 2020 that the Applicant filed his Application for an extension of time and leave to appeal. In doing so, he sought to challenge the decision of the primary Judge. The application came before the Court for directions on 16 September 2020. It was nevertheless considered appropriate that the Application itself could be then heard and determined. In addition to oral submissions then made by both Mr Hanna and Counsel for the Respondent, both parties were granted a further opportunity to file further written submissions. The Respondent availed itself of that opportunity, but Mr Hanna did not.

5 It is concluded that:

an extension of time should be granted to seek leave to appeal;

but that:

leave to appeal should be refused.

6 The extension of time should be granted because:

there was, at the very least, uncertainty on the part of Mr Hanna as to the time within which he was required to file any application;

there was an absence of prejudice to the Respondent in the event of an extension being granted; and

the period of time for which the extension was required was comparatively short.

The Respondent, moreover, did not oppose an extension of time other than by reference to the absence of merit in any appeal.

7 Of relevance to an application for leave to appeal is (inter alia) “whether in all the circumstances the judgment of the primary Judge is attended by sufficient doubt to warrant it being reconsidered by the Full Court”: Rawson Finances Pty Limited v Commissioner of Taxation [2010] FCAFC 139 at [4], (2010) 81 ATR 36 at 38 per Ryan, Stone and Jagot JJ. On the facts of the present case, her Honour was clearly correct in concluding that the bankruptcy of the Applicant precluded him from commencing any proceeding. That conclusion is not “attended by sufficient doubt”. Concurrence is expressed with the reasoning and conclusions of her Honour.

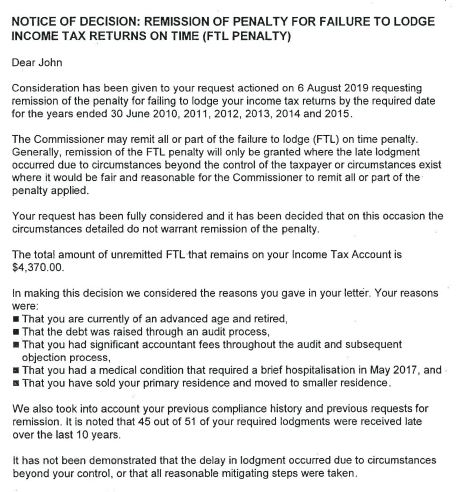

8 Separate from that basis upon which her Honour proceeded, consideration was also given to the form of relief sought by the Applicant. In issue were the 8 August 2019 decisions. In part, those letters provided as follows:

(formal parts omitted)

The letters went on to state the “review rights” available to the Applicant.

9 If recourse is had to the affidavit evidence filed in the proceeding before Jagot J, it emerges that factual matters were sought to be canvassed by Mr Hanna going beyond matters of any apparent relevance to the decision refusing to remit penalties for failure to lodge tax returns. The relevance of this factual material, with respect to Mr Hanna, remained elusive. It was partly for this reason that liberty was granted to the parties to file further written submissions after the conclusion of the hearing on 16 September 2020. Whether it was by reference to these further factual matters which Mr Hanna sought to place before the Court or otherwise, another matter of concern to Jagot J was the form of relief which he sought. That relief included orders which, her Honour concluded, could not be granted by the Court: [2020] FCA 1021 at [34]. Concurrence is again expressed with respect to this further conclusion of her Honour.

CONCLUSIONS

10 Although an extension of time is granted, leave to appeal is refused.

11 No error has been exposed in the reasoning of the primary Judge. Any appeal would be without merit.

THE ORDERS OF THE COURT ARE:

1. The Application for an extension of time is granted, with time being extended to 20 August 2020.

2. The Application for leave to appeal is refused.

3. The proceeding is dismissed.

4. The Applicant is to pay the costs of the Respondent.

I certify that the preceding eleven (11) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Flick. |