Federal Court of Australia

Lee v Parker [2020] FCA 1453

ORDERS

First Plaintiff KIA SILVERBROOK Second Plaintiff | ||

AND: | First Defendant AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Second Defendant | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

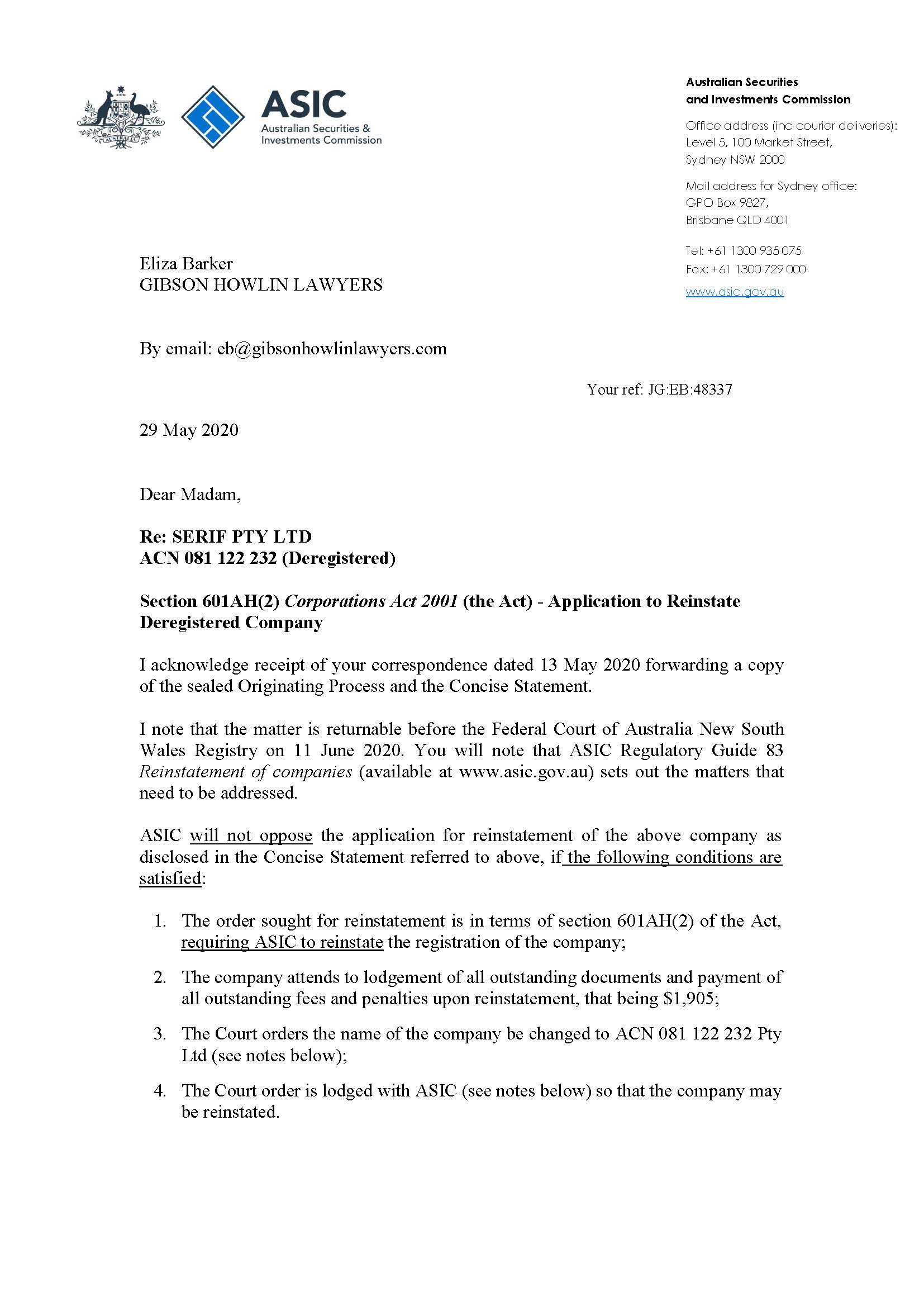

1. Pursuant to s 601AH(2) of the Corporations Act 2001 (Cth), the second defendant reinstate the registration of Serif Pty Ltd ACN 081 122 232 (Deregistered) subject to compliance with the conditions set out in the second defendant’s letter dated 29 May 2020.

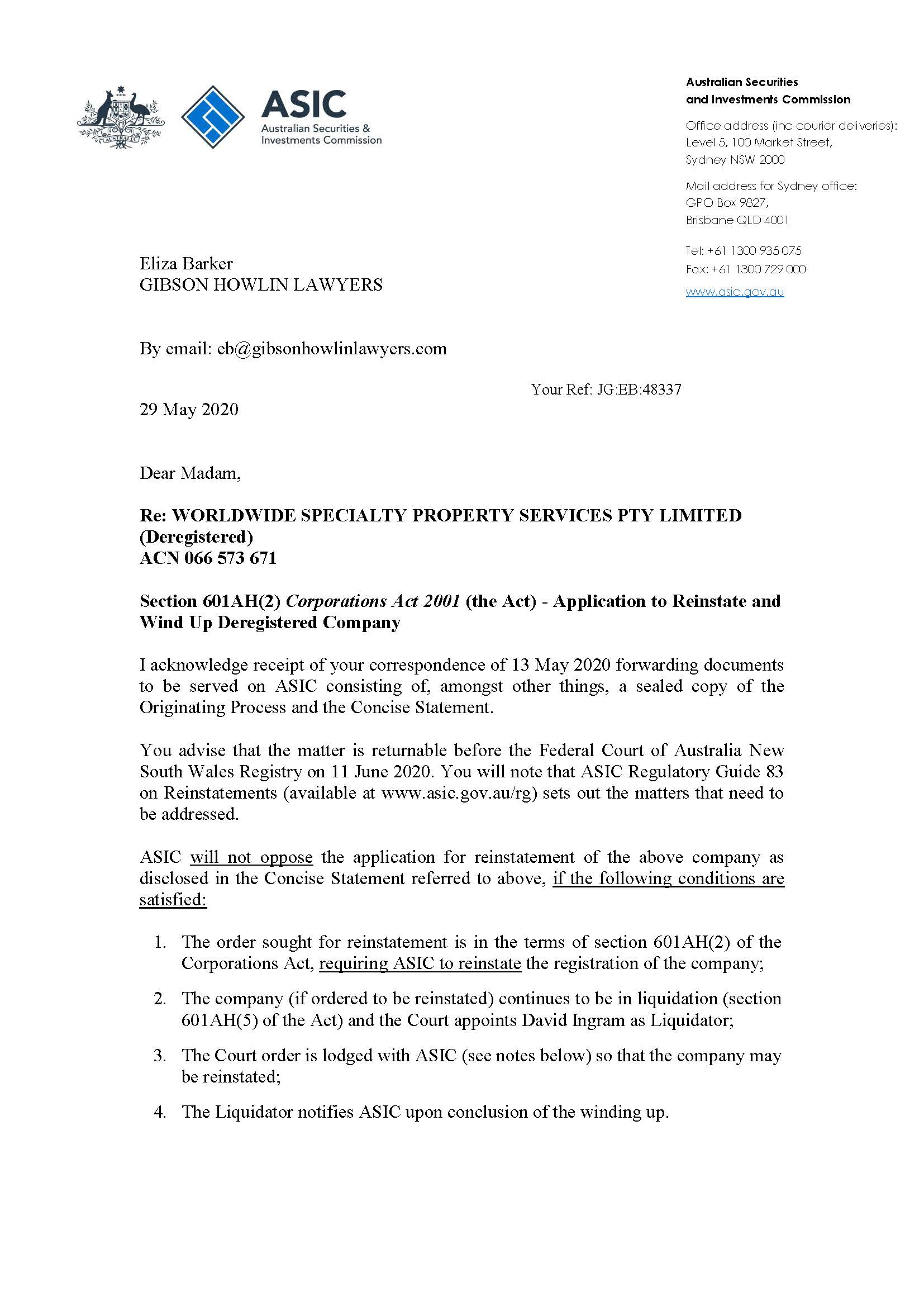

2. Pursuant to s 601AH(2) of the Corporations Act 2001 (Cth), the second defendant reinstate the registration of Worldwide Speciality Property Services Pty Ltd ACN 066 573 671 (In liq) (Deregistered) (WSPS) subject to compliance with the conditions set out in the second defendant’s letter dated 29 May 2020.

3. Upon reinstatement of WSPS, and pursuant to ss 601AH(3)(b) and (d) of the Corporations Act 2001 (Cth), Mr David Ingram be appointed as liquidator of WSPS.

4. The plaintiffs notify the second defendant within seven days of these orders.

5. The parties have liberty to apply to the docket judge for the further conduct of the substantive proceeding.

6. The costs of the plaintiffs’ applications be their costs in the cause.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GRIFFITHS J:

1 The plaintiffs seek reinstatement of two companies (Worldwide Speciality Property Services Pty Ltd (WSPS) and Serif Pty Ltd (Serif)) under s 601AH of the Corporations Act 2001 (Cth). WSPS was deregistered on 20 June 2019. Serif was deregistered on 15 May 2016. If the companies are reinstated, the plaintiffs seek the appointment of a new liquidator to WSPS.

2 In the originating process dated on 11 May 2020, the plaintiffs seek additional relief. By orders dated 11 June 2020, the matters summarised in [1] above were allocated for a preliminary and separate determination.

3 The first defendant (Mr Gregory Parker) was the liquidator of WSPS between 16 April 2014 and 20 March 2019. If reinstated, it is proposed to commence proceedings against Mr Parker for alleged breaches of fiduciary duties and statutory duties owed by him under ss 180 and 181 of the Corporations Act as an officer of WSPS. The claims relate to what are said to be 140 United States patent or patent registration applications (Patents) in the name of WSPS which Mr Parker is alleged to have failed to preserve and realise during the liquidation of that company. Mr Parker denies the plaintiffs’ claims.

4 The second defendant is the Australian Securities and Investments Commission (ASIC). It did not object to the reinstatement of the companies as long as certain specified conditions are satisfied as set out in two letters with regard to Serif and WSPS respectively dated 29 May 2020.

5 Serif was the legal and beneficial owner of the two issued ordinary shares in WSPS. The plaintiffs were:

(a) directors of WSPS between 16 September 1994 and 20 June 2019, with the first plaintiff being the secretary of that company during that time;

(b) directors and secretaries of Serif from 22 December 1997 to 15 May 2016; and

(c) each the legal and beneficial owner of 50% of the ordinary shares issued by Serif.

The evidence and summary of background facts

6 The plaintiffs relied upon three affidavits by the first plaintiff and an expert report by Mr Peter Haley, who provided an “indicative valuation” of the Patents. Mr Haley was cross-examined. Mr Parker relied upon two affidavits by his solicitor and an expert report by Mr Yves Hazan (primarily concerning US patent law) in response to Mr Haley’s report. Mr Parker also relied upon an expert report by Mr Grant Kepler, who responded to various questions regarding Mr Haley’s report.

7 The Australian Taxation Office (ATO) has a judgment debt in the form of director penalties against the plaintiffs in the amount of $13,961,633.90, in respect of WSPS’s unpaid taxation liabilities (see Lee v Deputy Commissioner of Taxation; Silverbrook v Deputy Commissioner of Taxation [2020] NSWCA 95). It appears that the plaintiffs have sought special leave to appeal from that decision.

8 The second plaintiff provided Mr Parker with a certified Report as to Affairs dated 29 April 2014 concerning WSPS. He estimated the value of the Patents as $18,848,613.00. The Report was accompanied by a document headed “WSPS Patent inventory 16 April 2014” which identified the Patents.

9 There is a strong dispute regarding the value of the Patents. Mr Haley has given them an “indicative valuation” of approximately $20m based on a cost-based valuation methodology or $37,297.977.00 on a market-based methodology. Mr Parker objected to all of Mr Haley’s report on the basis it relied on factual assumptions which have not been made good by lay evidence. Mr Parker drew attention to the fact that the balance sheets for WSPS as at 30 June 2013 and 30 June 2014 contain no reference to the Patents being an intangible asset beneficially owned by WSPS. He also relied upon the criticisms levelled at Mr Haley’s report by both Mr Hazan and Mr Kepler.

Consideration and determination

10 Sub-sections 601AH(2), (3) and (5) are as follows:

601AH Reinstatement

…

Reinstatement by Court

(2) The Court may make an order that ASIC reinstate the registration of a company if:

(a) an application for reinstatement is made to the Court by:

(i) a person aggrieved by the deregistration; or

(ii) a former liquidator of the company; and

(b) the Court is satisfied that it is just that the company’s registration be reinstated.

(3) If:

(a) ASIC reinstates the registration of a company under subsection (1) or (1A); or

(b) the Court makes an order under subsection (2);

the Court may:

(c) validate anything done during the period:

(i) beginning when the company was deregistered; and

(ii) ending when the company’s registration was reinstated; and

(d) make any other order it considers appropriate.

Note: For example, the Court may direct ASIC to transfer to another person property vested in ASIC under subsection 601AD(2).

…

Effect of reinstatement

(5) If a company is reinstated, the company is taken to have continued in existence as if it had not been deregistered. A person who was a director of the company immediately before deregistration becomes a director again as from the time when ASIC or the Court reinstates the company. Any property of the company that is still vested in the Commonwealth or ASIC revests in the company. If the company held particular property subject to a security or other interest or claim, the company takes the property subject to that interest or claim.

11 The relevant legal principles are discussed in cases such as Pilarinos v Australian Securities and Investments Commission [2006] VSC 301 per Gillard J; Deputy Commissioner of Taxation v Australian Securities and Investments Commission; in the matter of Civic Finance Pty Limited (Deregistered) [2010] FCA 1411 per Jagot J; The Bell Group Limited v Australian Securities and Investments Commission [2018] FCA 884; 358 ALR 624 per McKerracher J; In the matter of European Metal Recyclers Pty Ltd (in liq) (deregistered) [2018] NSWSC 946 per Gleeson JA and Perera v Australian Securities and Investments Commission, in the matter of Hodder Rook & Associates Pty Limited [2019] FCA 2015 per Markovic J and the cases referred to therein.

12 The relevant principles may be summarised as follows.

(a) On an application for reinstatement, the focus is the justice of reinstating the company, not the justice of any proceedings which it is proposed that the reinstated company might institute.

(b) It is important not to lose sight of the fact that a company’s registration is not reinstated for a particular purpose; rather, the reinstatement is for all purposes.

(c) It is generally not appropriate in a reinstatement application to go into factual matters which are the subject of dispute. This is particularly so where the question arises whether a proposed action is doomed to fail and that question involves complex factual and legal matters. I see no reason why a similar approach should not be taken to contested opinions on a subject such as valuation. As Gillard J said in Pilarinos at [106] (emphasis added):

106. The question of whether the proposed action was doomed to fail is a question which involves complex factual matters, and inferences that are to be drawn from the factual matters. Some of the facts and some of the inferences are very much disputed between the parties and involve reasonably complex questions of law. It is not appropriate in those circumstances for this Court to attempt to determine the likely outcome of any proceeding. That is best left to a Court hearing. Some of the matters raised are “fact sensitive” and it is inappropriate to attempt to resolve those on affidavit material. Mr Garde also raised the question of the proceeding being statute barred and also precluded by laches. The interest claimed is an equitable one. This involves interesting questions relating to limitations and, further, laches is a matter that is fact sensitive.

(d) Without derogating from sub-paragraph (c) above, it is generally sufficient for the Court to determine on the material before it whether any proposed proceeding have a prima facie basis and are not futile because, for example, it is hopeless.

(e) The expression “person aggrieved” is a broad one, which should be construed liberally. It includes a person who has been damaged or injured in a legal sense. It excludes, however, a person who is a mere busybody, who has no genuine interest in the outcome of a decision. A person aggrieved includes a person who has a genuine grievance as a result of a decision which prejudices his or her interest, which must be real and direct and can result from a person being subject to legal burden by a decision. A person aggrieved could include a shareholder who can demonstrate that he or she is a creditor of the company, or that there will be a surplus of assets and rights to dividends if the company were to be reinstated.

(f) However, a shareholder (or a director), by that status alone, will not necessarily be a person aggrieved. For example, where a company is insolvent, neither a shareholder nor a director is aggrieved by the deregistration simply because, as a consequence of the insolvency, the shareholder has no asset of any value and the director’s office was displaced by the liquidator.

(g) There is no temporal restriction in the expression “person aggrieved” as long as there is a causal link between the grievance and the deregistration. Consequently, a person can become aggrieved after the time of deregistration.

(h) As to the requirement that reinstatement be “just”, the legislation does not provide any list of criteria, but relevant matters can include:

(i) the circumstances in which a company came to be deregistered and the reasons for seeking the reinstatement order;

(ii) the future activities of the company, if an order for reinstatement were made, and whether good use would be made of the reinstatement;

(iii) whether any particular person is likely to be prejudiced by the reinstatement;

(iv) any relevant public policy consideration; and

(v) whether there has been unwarranted delay.

(i) On an application for reinstatement the Court is concerned with the justice of reinstating the company, not the justice of any proceedings which the reinstated company might institute and/or prosecute.

(j) It is also well settled that the Court has a residual discretion whether or not to order reinstatement.

13 It is convenient to address these issues under discrete headings.

(a) Are the plaintiffs persons aggrieved?

14 Mr Parker contended that neither of the plaintiffs is a person aggrieved. His submissions may be summarised as follows.

15 First, the plaintiffs’ claim that they are unsecured creditors of WSPS by operation of s 269-45 of Sch 1 to the Taxation Administration Act 1953 (Cth) is unsustainable. That is because any rights which they may have under that provision only accrue on payment of the judgment debt owing to the Australian Taxation Office (ATO). There is no evidence that the plaintiffs would be able to satisfy that judgment debt.

16 Secondly, as to the plaintiffs’ reliance on their status as indirect beneficiaries of any liquidation dividend paid in the future by the reinstated WSPS, this assumes that the claims against Mr Parker will succeed and produce an economic return. This invites the question whether the Patents have been shown to have any value which would justify the reinstatement of WSPS and the prosecution of the claims against Mr Parker. In this context, as mentioned, Mr Parker objected to all of Mr Haley’s valuation report. As also mentioned, Mr Parker submitted that the available evidence indicated that the Patents had no value at all. This was said to be reflected in the omission of any relevant entry in WSPS’s balance sheets for 30 June 2013 and 30 June 2014 respectively in relation to the Patents.

17 In circumstances where the plaintiffs have not demonstrated, even on a prima facie basis, that the Patents had any value during the liquidation of WSPS, Mr Parker submitted that there was no prospect of the plaintiffs obtaining any economic return so as to render them “aggrieved persons”.

18 For the following reasons, I do not accept those contentions. First, as to Mr Parker’s challenge to the admissibility of all of Mr Haley’s report, I do not accept that the report is inadmissible in the light of what Heydon JA said in Makita (Australia) Pty Ltd v Sprowles [2001] NSWCA 305; 52 NSWLR 705 at [85] regarding reliance on factual assumptions which have not been proven. As Weinberg and Dowsett JJ said in Sydneywide Distributors Pty Ltd v Red Bull Australia Pty Ltd [2002] FCAFC 157; 234 FCR 549 at [87] with reference to that paragraph of Heydon JA’s reasons for judgment:

The use of the phrase “strictly speaking” in the last sentence should not be overlooked. It may well be correct to say that such evidence is not strictly admissible unless it is shown to have all of the qualities discussed by Heydon JA. However many of those qualities involve questions of degree, requiring the exercise of judgment. For this reason it would be very rare indeed for a court at first instance to reach a decision as to whether tendered expert evidence satisfied all of his Honour’s requirements before receiving it as evidence in the proceedings. More commonly, once the witness’s claim to expertise is made out and the relevance and admissibility of opinion evidence demonstrated, such evidence is received. The various qualities described by Heydon JA are then assessed in the course of determining the weight to be given to the evidence. There will be cases in which it would be technically correct to rule, at the end of the trial, that the evidence in question was not admissible because it lacked one or other of those qualities, but there would be little utility in so doing. It would probably lead to further difficulties in the appellate process.

19 In rejecting Mr Parker’s objection, I took the view that the absence of proof of factual assumptions made by Mr Haley went to the weight to be given to his evidence and not to its admissibility. In determining that weight I also took into account the interlocutory nature of the current proceeding and noting that further inquiries are likely to be made in the course of preparing for the substantive hearing (see Makrypodis v Eleisawy [2014] NSWSC 1429 at [44] per Lindsay J). For reasons which will be further developed below, and for the purposes of this stage of the proceeding above, I accept Mr Haley’s evidence that, on an indicative valuation basis, the Patents have an approximate value of $20m or $38m, depending upon the valuation methodology.

20 Secondly, I am satisfied that the plaintiffs have lost rights where they could otherwise have caused Serif to commence the proceedings reflected in the originating application.

21 Thirdly, given that Serif was the holding company of WSPS and the plaintiffs were the sole shareholders of Serif, they are aggrieved because they have lost the ability potentially to recover damages as sought in the originating process if there is a surplus of assets.

22 Fourthly, if the proceedings against Mr Parker are ultimately successful, this could have the effect of reducing the plaintiffs’ personal director liabilities to the ATO.

23 Fifthly, the absence of any reference to the Patents as assets of value in the balance sheets may simply reflect that the Patents were not for sale at that time.

(b) Is it just to reinstate the companies?

24 I am satisfied that it is just to reinstate WSPS. First, there is a good use to be made of the reinstatement with reference to the proposed action against Mr Parker. Secondly, there are other reasons why it would be just to reinstate WSPS, including matters of public interest, where Mr Parker’s alleged failures occurred as an official liquidator.

25 On the basis of the material before me, I am not satisfied that there are no prospects of recovery if WSPS is reinstated and the substantive proceedings are further prosecuted against Mr Parker. It is not appropriate at this stage to seek to resolve disputed factual matters, disputed opinions or complex legal questions. The basis for the claims against Mr Parker is sufficiently supported by the evidence filed in the proceedings to date. The existing evidence indicates the following:

(a) WSPS was the owner of the Patents.

(b) Upon WSPS being placed into liquidation, Mr Parker was told by the second plaintiff about the Patents.

(c) He also told Mr Parker that he valued the Patents at $18,848,613.

(d) Mr Parker did not take steps to realise the Patents apparently because he had received information that WSPS was in fact not the owner of those Patents, when it appears, on the basis of the existing evidence, that no such information was ever received.

(e) Mr Parker had sufficient funds in the liquidation to enable him to seek to sell the Patents or otherwise extend their expiration dates.

(f) The Patents have all expired.

(g) While again noting that it is inappropriate to seek to resolve disputed evidence, including evidence relating to the value of the Patents and the extent and timing of information provided to Mr Parker by the plaintiffs relating to the Patents, I am satisfied that Mr Haley’s report indicates that the Patents have an indicative value which, if recovered, would not render the proceedings against Mr Parker futile.

26 As to Mr Haley’s evidence, it is important to appreciate that he made clear that his expert opinion focussed on the “indicative valuation” of the Patents. Quite properly, Mr Haley expressly acknowledged that he was provided with limited information, had to make certain stated assumptions and also relied upon information he obtained from the plaintiffs. He frankly stated that his Report constituted a limited scope valuation. These matters all go to weight. At this stage of the proceeding, and notwithstanding the cross-examination, I consider that Mr Haley’s report deserves some weight. The substantive proceeding cannot be characterised at this stage as futile or hopeless. It can also be assumed that the valuation evidence in the substantive proceeding may be different from that which is currently before the Court, given that additional relevant information is likely to come to hand, including possibly by way of discovery, other forensic processes or by inquiry.

27 I am prepared at this stage of the proceeding to act upon Mr Haley’s evidence notwithstanding the force of some of Mr Kepler’s criticisms of Mr Haley’s report. Those criticisms include the following:

(a) Mr Haley’s valuations were performed without information as to the commercial viability of the Patents and the likely revenues they would generate;

(b) Mr Haley’s market-based valuation methodology inappropriately incorporated “success bias” notwithstanding that there was no evidence as to their commercial viability;

(c) if the Patents were worth $37m it is difficult to understand why the plaintiffs, as former directors, did not sell the Patents in the face of the financial difficulties which ultimately led to WSPS being liquidated; and

(d) Mr Haley relied extensively on information provided to him by the second plaintiff and also made several unsubstantiated assumptions, with the consequence that there was an increased risk that Mr Haley’s valuation opinions were not reliable.

28 I respond to each of those criticisms in turn as follows:

(a) Mr Haley himself acknowledged that he did not have the information described in [27(a)] above and that is part of the reason why he gave only an “indicative valuation” of the Patents;

(b) even if this criticism is accepted, it does not affect Mr Haley’s cost-based methodology;

(c) this is a matter which may well be explored in the substantive proceeding and there may be a range of possible explanations for why the directors acted as they did; and

(d) these matters were all candidly acknowledged by Mr Haley, who gave only an “indicative valuation”.

29 For the following additional reasons, I do not accept Mr Parker’s reasons for opposing reinstatement.

30 First, he says that WSPS would come back into existence with liabilities of $18,353,007 and would be insolvent. This is not determinative as it is not proposed that WSPS will be returned to the control of its former directors, or that it will trade. Instead, a new liquidator will be appointed. That liquidator will be an officer of the Court, and presumably would not allow any proceedings to continue in the name of WSPS without suitable assurances of the merit of the case, and funding for the litigation.

31 Secondly, Mr Parker says that any claim against him is speculative and there is little if any chance of any material financial return to the Company where the value of the Patents may not eclipse the total amount outstanding to creditors. Having regard to Mr Haley’s evidence, which I generally accept, there is a prospect of a judgment in favour of WSPS of an amount in the range of $18m-$37m. Even if the amount is only $18m or less, it is still appropriate to reinstate and allow the proceedings to continue in the interests of the creditors, and in particular the ATO. It would be the primary beneficiary of the proceedings up to a judgment in the amount of $18m. The plaintiffs would also benefit personally from any reduction in WSPS’s taxation liabilities to that same extent.

32 Thirdly, Mr Parker says that there is no evidence of funding of the prospective litigation against him, nor of security for his costs. Again, as noted above, if the registration of WSPS is reinstated, a new liquidator will be appointed over WSPS and that will be a relevant matter for his or her consideration. An amount of $20,020.00 has been deposited by the first plaintiff into a trust account to enable the proposed liquidator, Mr Ingram, to undertake preliminary investigations of WSPS’s affairs. If it is the case that the plaintiffs maintain the proceedings on WSPS’s and Serif’s behalf (which would require leave), questions of security would need to take into account that they are natural persons. Finally, I consider that issues concerning security for costs are appropriately left to be raised and determined in the substantive proceeding (see Pilarinos at [109] per Gillard J).

33 The following aspects of the two expert reports relied on by Mr Parker are also relevant.

(a) Mr Hazan confirms that WSPS owned the Patents. Critically, Mr Hazan also opines at [14.3]: “… Given the unique business model of the patent owner Mr Haley identifies at [3.5] and [3.6], the information about previous achievements under that business model as a proportion of the 4,747 patents registered in the US in my opinion may be the most reliable information for comparative purposes that I would provide to a valuer”. This provides another basis for the reinstatement of WSPS – once reinstated, the liquidator could access the historical tax returns of WSPS that would demonstrate the income derived from the Patents and allow a more precise valuation.

(b) The expert report of Mr Kepler, at its highest, seeks to undermine Mr Haley’s conclusions, but at no point does Mr Kepler suggest that the Patents lack any value.

34 It is acknowledged that the plaintiffs have not in this proceeding to date established the precise value of the Patents for the purposes of this restatement application. I do not think that they had to. It is sufficient for the plaintiffs to demonstrate on a prima facie basis that the Patents are assets of real value that were not realised by Mr Parker. I did not understand Mr Marksell, who appeared for Mr Parker, to challenge that this is the correct test.

35 There is another important matter which points to it being just to reinstate the companies. It relates to public policy considerations which favour a liquidator being held to account for the discharge of his or her legal duties. If reinstatement is ordered and the substantive proceedings are prosecuted, there will be some prejudice to Mr Parker, who will need to defend the proceeding. It is likely that even if his defence is successful his legal costs will not be fully recovered on a party-party basis.

36 Mr Parker’s opposition to the application for reinstatement places him in a difficult personal position. That is because his opposition is primarily directed to protecting himself from being sued in respect of the discharge of his duties as liquidator. That is not to say that someone in Mr Parker’s position cannot oppose reinstatement on the basis that a proposed proceeding affecting them is hopeless or otherwise doomed to fail having regard to the material before the Court at this time. For reasons I have explained, however, that is not the case here.

(c) The residual discretion

37 I see no reason why the Court would decline the reinstatement in the exercise of its residual discretion.

Conclusion

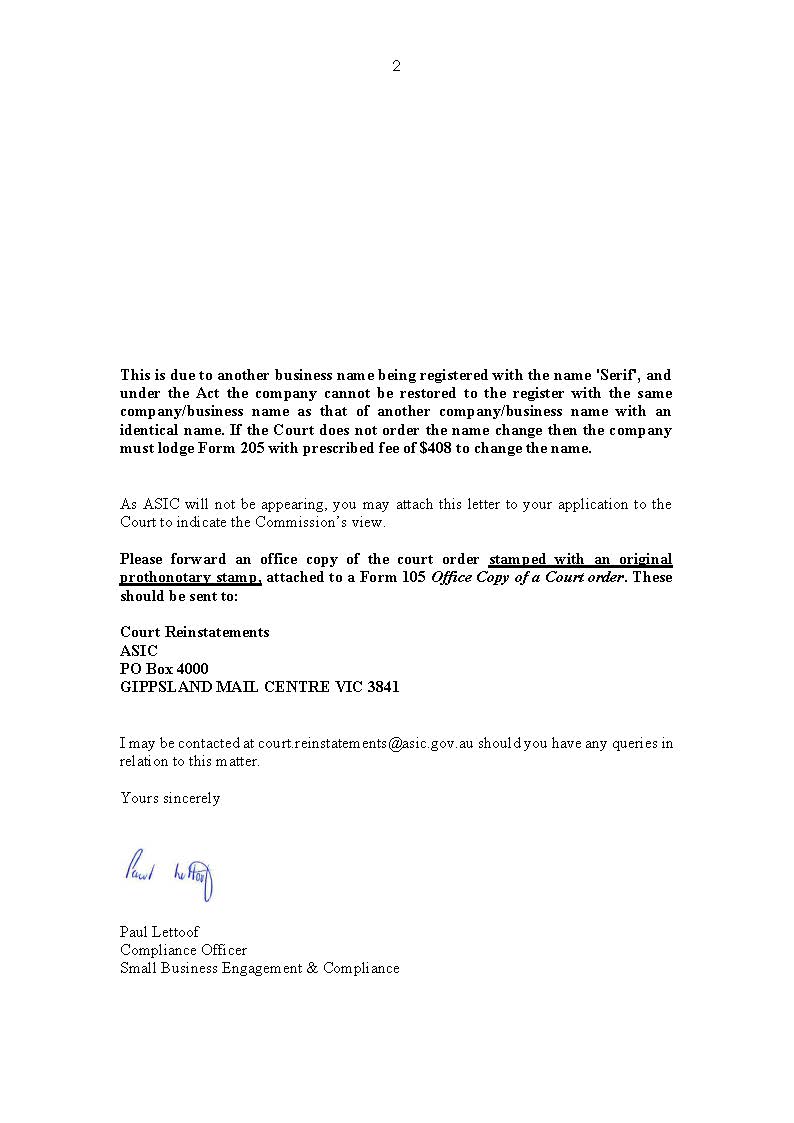

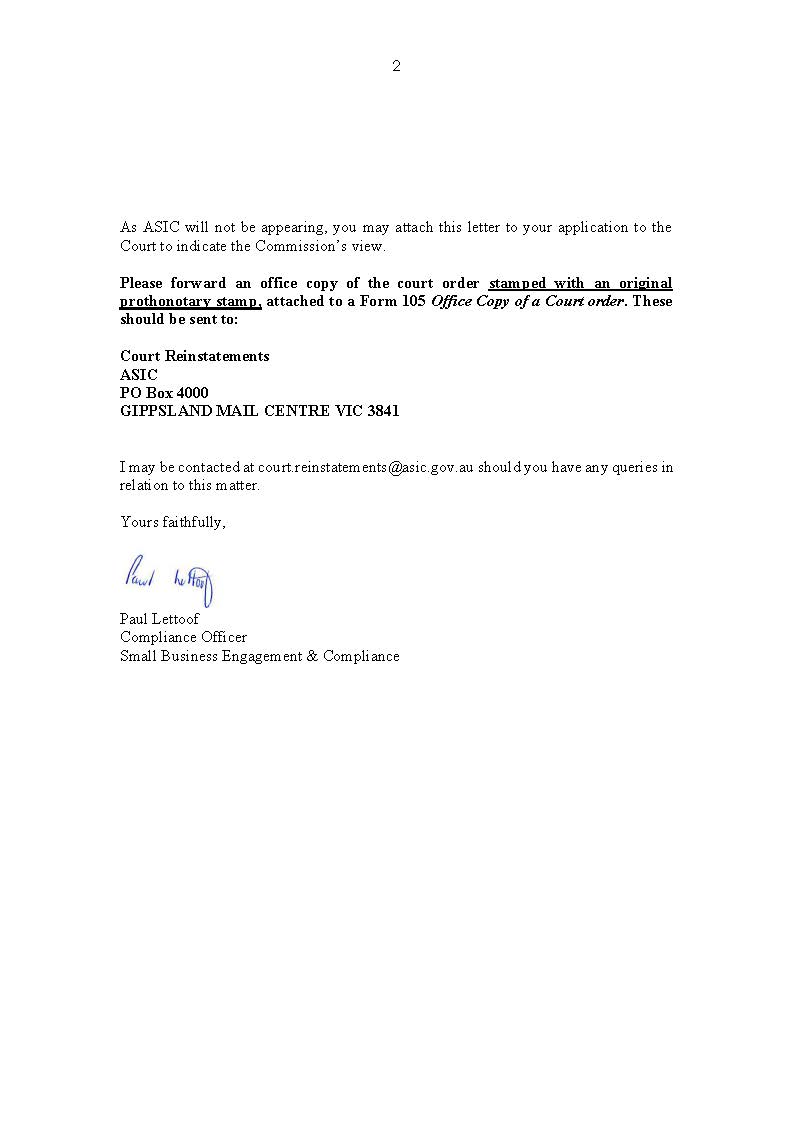

38 For these reasons, both companies will be reinstated, subject to compliance with certain conditions set out in two letters dated 29 May 2020 from the second defendant, which are attached at Annexure A to these reasons for judgment. Mr David Ingram will be appointed liquidator of WSPS. ASIC should be notified of these matters. Having regard to the interlocutory character of the matter, I consider that it is appropriate to order that costs of the current part of the proceeding be the plaintiffs’ costs in the cause.

39 The parties have liberty to apply to the docket judge for the future conduct of the proceeding.

I certify that the preceding thirty-nine (39) numbered paragraphs are a true copy of the Reasons for Judgment of the Honourable Justice Griffiths. |

ANNEXURE A