Federal Court of Australia

Binqld Finances Pty Ltd (In Liq) v Israel Discount Bank Limited; In the Matter of Binqld Finances Pty Ltd (In Liq) (No 2) [2020] FCA 1208

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The Interlocutory Application filed by the defendant, Israel Discount Bank Limited (IDB) (formerly the thirteenth defendant) on 10 February 2017 be dismissed.

2. IDB pay the plaintiffs’ costs of and incidental to that Interlocutory Application.

3. The Interlocutory Application filed by the plaintiffs on 28 October 2019 be dismissed.

4. There be no orders as to the costs of that Interlocutory Application.

5. The fourth plaintiff, BCI Finances Pty Limited (ACN 055 988 531) (In Liquidation) (BCI) be removed as a party to this proceeding.

6. The joinder of John Sheahan, Ian Russell Lock and the Commissioner of Taxation (Cth) as additional plaintiffs in this proceeding effected by Order 5 made by Foster J in this proceeding on 12 November 2019 be confirmed.

7. The leave granted to the plaintiffs to amend their Second Further Amended Originating Application by Order 6 made by Foster J on 12 November 2019 be confirmed.

8. The leave granted to the plaintiffs to amend their Third Further Amended Statement of Claim by Order 7 made by Foster J on 12 November 2019 be confirmed.

9. By 28 August 2020, the plaintiffs file clean copies of their Third Further Amended Originating Application and Fourth Further Amended Statement of Claim with the following alterations to the parties:

(a) The removal of BCI as the fourth plaintiff herein; and

(b) The consequential alteration in the identification of Messrs Sheahan and Lock and the Commissioner of Taxation (Cth) from being the fifth, sixth and seventh plaintiffs respectively to being the fourth, fifth and sixth plaintiffs respectively.

10. The costs of and incidental to the Interlocutory Application filed by the plaintiffs on 2 October 2019 concerning the joinder of Messrs Sheahan and Lock and the Commissioner of Taxation (Cth) as additional plaintiffs and the consequential amendments to the pleadings herein be costs in the proceeding.

11. The proceeding be fixed for case management before the Docket Judge on a date and at a time to be fixed by the Docket Judge.

12. The parties have liberty to apply on seven (7) days’ notice.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

FOSTER J:

1 The principal application presently before the Court with which this judgment is concerned involves the question of whether the service in Israel of Originating Process upon the sole defendant remaining in this proceeding, Israel Discount Bank Limited (IDB) (a foreign corporation incorporated in Israel which apparently has no presence in Australia), should stand and, in the alternative, whether the whole of this proceeding should be permanently stayed. IDB contends that service upon it should be discharged or set aside and, in the alternative, that the whole of this proceeding should be permanently stayed. IDB was originally the thirteenth defendant in this proceeding. It is now the only defendant.

Background

2 Binqld Finances Pty Ltd (In Liquidation) (Binqld), Ligon 268 Pty Ltd (In Liquidation) (Ligon 268) and E.G.L. Development (Canberra) Pty Limited (In Liquidation) (EGL) are the first three plaintiffs in this proceeding. Each of those corporations is in liquidation. The appointed liquidators are John Sheahan and Ian Russell Lock, the fifth and sixth plaintiffs respectively. In these Reasons for Judgment, I shall refer to Messrs Sheahan and Lock together as “the liquidators”. The seventh plaintiff is the Commonwealth Commissioner of Taxation (Commissioner). The liquidators and the Commissioner were added as plaintiffs only recently (on 12 November 2019). Their joinder was permitted conditionally and is subject to challenge by IDB.

3 The fourthnamed plaintiff in this proceeding is B.C.I. Finances Pty Limited (In Liquidation) (BCI). BCI makes no current claims in this proceeding. By Notice of Discontinuance filed on 30 September 2016 pursuant to leave granted by me on the same day, BCI discontinued all claims which it had previously made in this proceeding. In those circumstances, it is appropriate that I now order that BCI’s name be removed as a plaintiff.

4 In the period from the respective dates of incorporation of Binqld, Ligon 268 and EGL (the corporate plaintiffs) to the dates upon which each of those corporations was wound up, the affairs of those corporations were controlled by one or more of Emil Binetter, Erwin Binetter, Andrew Binetter and Michael Binetter. Erwin Binetter was the brother of Emil Binetter and the father of Andrew Binetter and Michael Binetter.

5 In this proceeding, it is alleged by the corporate plaintiffs that, from time to time in the period from the mid to late 1980s, the controllers of the corporate plaintiffs caused those companies to enter into a number of transactions, some of which involved IDB, the purpose of all of which was to fraudulently enable the corporate plaintiffs and other corporations controlled by the Binetter family to avoid their taxation obligations in Australia and thereby to benefit members of the Binetter family.

6 Commencing in December 2009, the Commissioner issued a number of amended taxation assessments, shortfall interest assessments and penalty assessments against the corporate plaintiffs. Those assessments constituted the liabilities upon which each of those corporations was later wound up.

7 When this proceeding was commenced, there were four plaintiffs and thirteen defendants. The four plaintiffs were Binqld, Ligon 268, EGL and BCI. The first ten defendants were corporations controlled by members of the Binetter family, the eleventh defendant was Bank Hapoalim B.M. and the twelfth defendant was Bank Hapoalim (Switzerland) Limited. As I have already said, IDB was named as the thirteenth defendant.

8 The version of the plaintiffs’ Originating Application and Statement of Claim which was current in September and December 2016 contained claims and causes of action made variously on behalf of the corporate plaintiffs and BCI against one or more of the defendants. The claims against the defendants were all ancillary claims. The primary contraventions were alleged to be breaches by the directors of the plaintiffs of the fiduciary obligations and statutory duties owed by them to the plaintiffs by, in some cases, knowingly receiving moneys transferred in breach of such obligations, and, in all cases, by knowingly assisting in breaches of such fiduciary obligations and by being involved in breaches of the relevant statutory duties (as to which, see s 181(1) and s 182(1) of the Corporations Act 2001 (Cth) (Corps Act). At the heart of the plaintiffs’ claims were the transactions to which I have referred at [5] above.

9 In late September 2016, BCI settled its claims against Bank Hapoalim B.M. and Bank Hapoalim (Switzerland) Limited. As those claims were the only claims made by it in this proceeding, it has, since that time, taken no further part in this proceeding.

10 On 30 September 2016, on the same occasion as I granted leave to BCI to discontinue all the claims made by it in this proceeding, I granted leave to the corporate plaintiffs and BCI to serve IDB outside Australia in Israel with the Originating Application, Genuine Steps Statement and Amended Statement of Claim which had, by then, been filed in this proceeding. The plaintiffs’ application for that leave was made ex parte. Pursuant to that leave, service of those documents was effected on IDB on 4 December 2016 in Israel in accordance with the Hague Convention as to the service of process.

11 By Interlocutory Application filed on 10 February 2017 (IDB’s Discharge Application), IDB applied for the following relief:

1. The Thirteenth Defendant seeks an order under r 13.01(1)(d) of the Rules to discharge the orders of Foster J made on 30 September 2016 giving leave to the First, Second and Third Plaintiffs to serve the Originating Application dated and filed 3 December 2015 in this proceeding (NSD 1600 of 2015) on Israel Discount Bank Limited, in Israel in accordance with the Hague Convention.

2. Further or alternatively, the Thirteenth Defendant seeks an order under r 13.01(1)(b) of the Rules to set aside service of the Originating Application dated and filed 3 December 2015 in this proceeding (NSD 1600 of 2015) on Israel Discount Bank Limited, in Israel in accordance with the Hague Convention.

3. Further or alternatively, the Thirteenth Defendant seeks an order for a permanent stay of the proceedings against it.

12 On the same day, IDB filed a Notice of Address for Service in which the following statement appeared:

For the avoidance of doubt, the Thirteenth Defendant intends this document to be treated as entering a conditional “appearance in the proceeding”, within the meaning of r 10.70 of the Federal Court Rules (2011) (Cth).

13 Rule 13.01 of the Federal Court Rules 2011 (FCR) provides:

13.01 Setting aside originating application etc

(1) A respondent may apply to the Court for an order:

(a) setting aside an originating application; or

(b) setting aside the service of an originating application on the respondent; or

(c) declaring that an originating application has not been duly served on the respondent; or

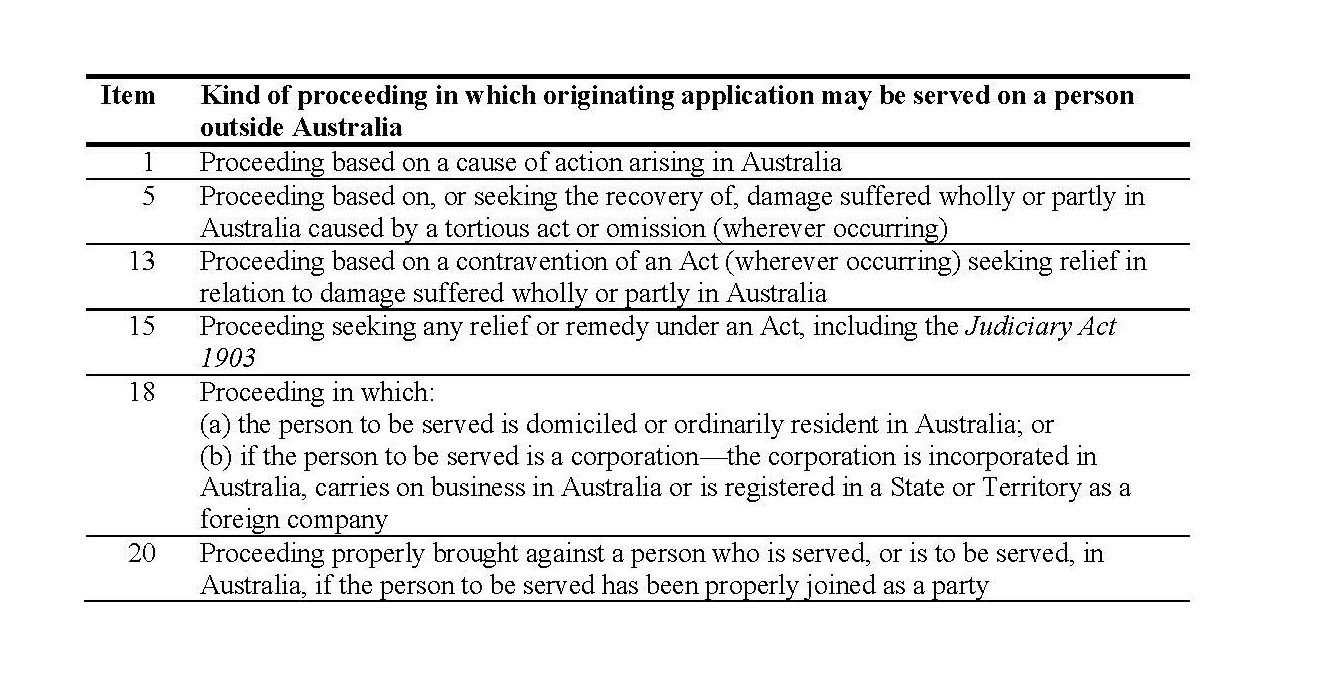

(d) discharging any order giving leave to serve an originating application outside Australia or confirming service of an originating application outside Australia.

Note: Rule 10.43 deals with the procedures for serving originating applications outside of Australia.

(2) If an order under paragraph (1)(b) or (c) is sought, the application must be accompanied by an affidavit stating:

(a) the date on which the originating application was served on the respondent; and

(b) details of the service.

(3) A respondent applying for an order under subrule (1) must file the interlocutory application and affidavit at the same time that the respondent files a notice of address for service.

14 IDB relies upon r 13.01(1)(b) and (d) FCR in its Discharge Application.

15 On 29 September 2017, I heard the claims for relief made by IDB in pars 1 and 2 of its Discharge Application. At that time, the parties had agreed to defer the hearing of IDB’s claim for a permanent stay of this proceeding to a later date.

16 After I reserved my decision in respect of those matters, in late 2018, the corporate plaintiffs settled all of the claims made by them in this proceeding except those against IDB. That settlement also dealt with certain other claims made by the corporate plaintiffs against persons and entities who were not parties to this proceeding, as well as other matters. In these Reasons, I shall refer to this overall settlement as “the settlement”.

17 Although, pursuant to the settlement, on 11 October 2018, the plaintiffs discontinued their claims in this proceeding against the Binetter companies (the first to tenth defendants), in their extant pleadings against IDB, they nonetheless continue to rely upon many of the allegations against those companies which they had formerly made in those pleadings. Those allegations are said to be an integral part of the case which the corporate plaintiffs seek to press against IDB.

18 The case currently pleaded and maintained by the corporate plaintiffs against IDB based upon the principles in Barnes v Addy (1874) LR 9 Ch App 244 (Barnes v Addy) and ss 79, 181 and 182 of the Corps Act is, therefore, essentially the same case as was pleaded against IDB in the original Statement of Claim filed in this proceeding on 3 December 2015. In addition, in early 2019, pursuant to leave granted by me, the corporate plaintiffs added a new case against IDB which is based upon s 37A of the Conveyancing Act 1919 (NSW) (s 37A). IDB did not oppose the addition of the s 37A case at that time.

19 In late 2018, in light of the settlement, IDB applied to reopen its case in support of the claims for relief made by it in its Discharge Application. It made that application upon the ground (inter alia) that it was entitled to have access to the settlement documentation in order to investigate whether or not the terms of the settlement had any impact upon the case which it had sought to advance in support of the claims for relief made by it in its Discharge Application and, if so, the nature and extent of that impact. In particular, IDB wished to investigate whether the corporate plaintiffs’ claims for compensation in this proceeding had been fatally damaged by the circumstance that the corporate plaintiffs had recovered substantial compensation under the settlement. Had IDB been able to prove that contention, it is likely that it would have wished to argue that the plaintiffs have not established the requisite prima facie case for the purposes of the FCR dealing with service out of the jurisdiction (as to which, see r 10.43(4)(c) FCR).

20 On 1 November 2018, I granted leave to IDB to reopen its case in support of its Discharge Application. On the same day, I also made orders requiring the plaintiffs to produce to IDB the settlement documentation. Those orders spawned satellite litigation involving the Commissioner which has not yet been resolved (see Binqld Finances Pty Ltd (In Liq) v Israel Discount Bank Limited; In the Matter of Binqld Finances Pty Ltd (In Liq) [2019] FCA 1186 and Commissioner of Taxation v Israel Discount Bank Limited [2020] FCAFC 71). To date, the settlement documentation has not yet been produced to the Court or to IDB.

21 At the same time, I required the plaintiffs to amend their Originating Application and Amended Statement of Claim so as to remove therefrom all matter that was not relevant to their sole remaining case, that is to say, their case against IDB.

22 On 12 November 2019, I conducted a further hearing of IDB’s Discharge Application. That hearing was a full rehearing of that Application although the evidence and submissions relied upon at the earlier hearing on 29 September 2017 were also relied upon at the hearing on 12 November 2019.

The Plaintiffs’ Pleaded Cases

23 The current pleadings filed by the plaintiffs are the Third Further Amended Originating Application filed on 14 November 2019 (3FAOA) and the Fourth Further Amended Statement of Claim (4FASOC) filed on the same day. Those pleadings were filed pursuant to leave granted by me to the plaintiffs on 12 November 2019. At the hearing which took place on that day, IDB objected to leave being granted to the plaintiffs to join the liquidators and the Commissioner as additional plaintiffs and to make consequential amendments to the versions of those pleadings current as at 12 November 2019. Because the plaintiffs raised concerns that any delay in the grant of leave to join those parties and amend those pleadings might give rise to limitation problems, upon the basis that the leave was subject to my consideration of IDB’s contentions and arguments in support of its Discharge Application and without prejudice to those contentions and arguments, I indicated to the parties at the hearing on 12 November 2019 that I would grant the leave sought pro tem and revisit in this judgment the questions of whether the liquidators and the Commissioner should be joined as additional plaintiffs and whether the consequential amendments sought by the plaintiffs should be allowed.

24 In the current iteration of their pleadings, the corporate plaintiffs claim equitable compensation and an order for relief under s 37A. In the alternative, they claim an account of profits. They also claim interest and costs. In addition, Binqld claims compensation pursuant to s 1317H of the Corps Act in respect of alleged involvement on the part of IDB in the breaches of s 181(1) and s 182(1) of that Act alleged against Binqld’s directors. That claim for compensation is based upon ss 79, 181(2) and 182(2) of the Corps Act.

25 The liquidators and the Commissioner claim s 37A relief in the alternative to claims for such relief made by the corporate plaintiffs. The joinder of the liquidators and the Commissioner as additional plaintiffs was sought by the corporate plaintiffs on 12 November 2019 in order to meet a submission made by IDB to the effect that the corporate plaintiffs have no standing to invoke s 37A.

26 In the 3FAOA and 4FASOC, each of Binqld, Ligon 268 and EGL relies upon causes of action against IDB which are, in each case, possessed by each individual corporation. The claims which each of the corporate plaintiffs makes are not joint claims. All of the claims have been joined in the one proceeding pursuant to r 9.02 FCR. It has never been suggested by IDB (or any other defendant) that the individual claims made by each of the three corporate plaintiffs had been improperly or inappropriately included in this one proceeding.

27 Central to the claims made by each of the corporate plaintiffs against IDB are the matters pleaded in pars 23 to 27 of the 4FASOC in which the corporate plaintiffs describe “the IDB Banking Service”. Those paragraphs are in the following terms:

(1) The IDB Banking Service

23. IDB offered a banking service to persons in Australia and elsewhere (the IDB Banking Service) which had some or all of the following elements:

(a) There was a primary customer, a deposit customer and a borrowing customer, of which the primary customer and the deposit customer could be the same person or entity.

(b) IDB created a deposit account and a borrowing account (or accounts) and could also create a balancing account to record the difference between the credit balance of the deposit account and the sum of the debit balance(s) of the borrowing account (or accounts).

(c) The primary customer caused the deposit customer to deposit funds in the deposit account.

(d) IDB permitted the primary customer and/or the deposit customer to nominate and authorise other persons, who became borrowing customers, to be entitled to draw advances from the borrowing account(s).

(e) IDB permitted drawing of advances from the borrowing account(s) provided the total amount of outstanding advances drawn from the borrowing account(s) did not come to exceed the total amount in the deposit account (that is, the deposit account was “back to back” with the borrowing account(s)).

(f) IDB would not permit the debit balance of the borrowing account(s) to exceed the credit balance of the deposit account (which difference may have been recorded in a balancing account).

(g) When IDB advanced funds to the borrowing customers who had been nominated by the primary customer, the advance of funds would be styled as a loan.

(h) From time to time, funds were transferred to the borrowing account(s) with IDB as and when determined by the primary, deposit or borrowing customers and styled as repayments of loans made by IDB at interest rates nominated by the primary, deposit or borrowing customers, not by IDB.

(i) IDB would pay interest on the positive difference between the debit balance of the borrowing account(s) and the credit balance of the deposit account (which difference may have been recorded in a balancing account).

(j) IDB received a benefit from the provision of the IDB Banking Service through charging a margin on any funds received into the borrowing accounts.

(k) IDB may have received other commercial benefits not known to the applicants.

Particulars of the period IDB Banking Service offered

(i) The period during which the IDB Banking Service was offered is not known to the applicants but from a letter from EGL to IDB dated December 1988 appears to have been offered from at least that time and, in any event, was offered in the period from 1992 to 2009.

Particulars of the existence and terms of the IDB Banking Service

(i) The proforma documents issued to Civic and/or Advance, two companies related to the Binetter family, on or around 19 March 2004.

(ii) The proforma documents issued to EGL on or around 12 April 2000.

(iii) A set of bank statements issued by IDB to Ligon 268 on or around 23 July 2012.

(iv) The existence of and terms of the IDB Banking Service are to be inferred from the existence of and terms of a similar banking service provided by BH Israel and BH Switzerland and supplied to BCI and the Binetter family in the circumstances described in Schedule F. [Schedule F repeats the pleadings previously included in the Statement of Claim which articulate BCI’s case against Bank Hapoalim B.M. and Bank Hapoalim (Switzerland) Limited]

24. The IDB Banking Service provided the following benefits to the primary customer and/or the deposit customer:

(a) it created the appearance of a loan between IDB and the persons nominated (ie the borrowing customers), when in fact the source of the funds was controlled by the primary customer and/or the deposit customer; and/or

(b) it allowed the primary customer to deploy funds under its control by deposit of those funds with IDB and the subsequent advance of those funds (or funds in equal amount) by IDB to borrowing customers as if, and with the appearance, that money was debt funded by IDB from IDB’s capital, with the taxation benefits that that would justify; and/or

(c) it made payments made by borrowing customers to IDB appear to be repayments to IDB of principal and interest on loans advanced by IDB, and thereby concealed the offshore income ultimately received by the primary customer by reason of the use of the IDB Banking Service; and/or

(d) by this means, the primary customer was able to use money on deposit with IDB to earn offshore income in a way which:

(i) concealed the existence of the funds held in the deposit account and the true nature of the IDB Banking Service;

(ii) concealed the existence of the offshore income earned in the deposit account and/or through the use of the IDB Banking Service;

(iii) allowed the primary customer to avoid declaring, and therefore paying tax on, the offshore income in the primary customer’s home jurisdiction.

25. At all relevant times, IDB knew that:

(a) the IDB Banking Service provided the benefits to the primary customers who obtained the service set out in paragraph 23;

(b) primary customers obtained the IDB Banking Service to obtain the benefits set out in paragraph 24;

(c) the primary customers and/or borrowing customers who utilised the IDB Banking Service would, or were likely to, claim in their tax returns submitted in their home jurisdictions that:

(i) the advances of funds from the borrowing account to the borrowing customers were the proceeds of loans advanced by IDB;

(ii) the transfer of funds back to the borrowing account was to repay principal and interest on loans advanced by IDB;

(d) the primary customers and/or borrowing customers would not disclose the existence of the deposit account or the true nature of the IDB Banking Service to the revenue authorities in their home jurisdiction;

(e) the income earned on the deposit account would not be declared by the primary customer or the deposit customer as income in tax returns submitted in their home jurisdiction;

(f) the IDB Banking Service was, and could be, utilised by primary customers to seek to avoid or evade tax in the home jurisdiction of the primary or borrowing customers;

(g) IDB had devised and provided the IDB Banking Service as a means of facilitating the ability of primary customers who sought to avoid or evade tax in the home jurisdiction of the primary or borrowing customer.

Particulars

(i) IDB’s knowledge is to be inferred from the fact that:

A. there would be no commercial rationale for a bank to offer a banking service like the IDB Banking Service, in particular, one which involved two separate but back-to-back accounts and the facilitation of transfers to persons styled as loans but where the primary or deposit customer nominates the interest rate and payment frequency to apply, other than to create a mechanism to obtain the custom of customers seeking to obtain benefits of the type set out in paragraph 24;

B. there would be no commercial rationale for a primary customer to acquire the IDB Banking Service and structure their affairs in the manner contemplated by its use unless the primary customer was seeking to obtain benefits of the type set out in paragraph 24.

26. In the alternative, at all relevant times, IDB ought reasonably have known the matters alleged in paragraph 25.

Particulars

(i) By reason of the matters alleged in paragraph 24 and IDB’s awareness of the commercial circumstances and taxation arrangements in the customer’s home jurisdiction.

27. Further in the alternative, at all relevant times IDB knew circumstances which would have disclosed the matters alleged in paragraph 25 to an honest and reasonable person.

Particulars

(i) By reason of the matters alleged in paragraph 24 and IDB’s awareness of the commercial circumstances and taxation arrangements in the customer’s home jurisdiction.

28 In these Reasons for Judgment, I shall also adopt the expression “the IDB Banking Service” to describe the service which is described in pars 23 to 27 of the 4FASOC.

29 Paragraphs 23 to 27 of the 4FASOC were relied upon against the Binetter corporate defendants in earlier iterations of the plaintiffs’ Statement of Claim. Those paragraphs are also repeated and relied upon by each of the corporate plaintiffs as part of the causes of action now relied upon against IDB in the 4FASOC (as to which, see par 105 (Binqld), par 137 (Ligon 268) and par 172 (EGL)).

30 I shall now address the claims made by the corporate plaintiffs against IDB based upon its alleged knowing assistance in the breaches of the general law fiduciary obligations owed by the directors of Binqld to it and its alleged involvement in the breaches by the directors of Binqld of their statutory duties owed to it. I will then look at the Binqld s 37A claims.

31 Binqld’s claims against IDB are pleaded in pars 105 to 136 of the 4FASOC.

32 Those claims may be summarised as follows:

(a) At all relevant times, Andrew Binetter and Michael Binetter controlled the affairs of Binqld (pars 108, 108A, 109 and 110);

(b) Those two men devised a scheme involving Binqld to assist them, or persons and entities comprising the Binetter family and its associates, in evading Australian tax (par 107);

(c) The Binqld scheme described in par 107 was implemented from April 2006 onwards as follows:

(i) The IDB Banking Service was acquired;

(ii) Funds under the control of the Binetter family were placed on deposit with IDB in a deposit account pursuant to the IDB Banking Service;

(iii) In accordance with the IDB Banking Service, instructions were sent to IDB to make advances to bank accounts in Australia held by Binqld;

(iv) On receipt of funds from IDB, Binqld transferred those funds to other entities related to the Binetter family; and

(v) Binqld lodged tax returns for FY2007 and FY2008 which treated the advances from IDB as loans and claimed as deductible expenses an amount equivalent to the amount paid or payable by Binqld to IDB characterised as interest under the transactions with IDB, thereby reducing income tax which would otherwise have been payable by Binqld under provisions of Australian income tax legislation

(par 111);

(d) Pursuant to the Binqld scheme, Binqld advanced various amounts from tranches of funds received from IDB by Binqld to entities in the Nudie Juices group and other Binetter companies (pars 111A, 111B, 111C and 111D); and

(e) Subsequently, in respect of FY2007 and FY2008, Binqld claimed significant sums as deductible expenses for overseas interest in circumstances where, to the knowledge of Andrew Binetter and Michael Binetter, Binqld was not entitled to claim such deductible expenses (pars 114–124B).

33 In pars 117A to 123, Binqld pleads that, as the directors and controllers of Binqld, each of Andrew Binetter and Michael Binetter owed general law fiduciary obligations to Binqld:

(a) To refrain from any act that involved a conflict of interest between the performance of his function as a director of Binqld and his performance of any other function or his personal affairs;

(b) Not to use his position improperly to gain an advantage for himself or someone else or to cause detriment to Binqld;

(c) To exercise the powers that he possessed and the duties that he had as a director of Binqld for a proper purpose;

(d) To exercise the powers that he possessed and the duties that he had as a director of Binqld in good faith, in the interests of Binqld; and

(e) To exercise reasonable care and skill in the exercise of his duties as a director, so as not to expose Binqld to a risk of loss.

34 At par 121, Binqld pleads the statutory duties owed by Andrew Binetter and Michael Binetter to Binqld pursuant to s 181(1) and s 182(1) of the Corps Act.

35 At pars 122 and 123 of the 4FASOC, Binqld pleads:

122 The involvement and continuing involvement of Binqld in the Binqld scheme was a course of conduct engaged in from the time of Binqld’s incorporation until at least on or around 2 March 2015 when it entered external administration that:

(a) was engaged in in order to assist persons or entities comprising the Binetter family to evade Australian tax;

(b) was pursued for reasons extraneous to the interests of Binqld and in order to further the interests of the Binetter family in evading Australian tax;

(c) was not in the best interests of Binqld because it exposed Binqld to:

(i) a risk that the Commissioner would commence a tax audit of the affairs of Binqld;

(ii) a risk that the Commissioner, acting rationally, would issue Binqld an assessment or amended assessment which disallowed any interest expenses claimed as deductible expenses including pursuant to ss 167 or 170 of the ITAA;

(iii) a risk that the Commissioner, acting rationally, would issue Binqld an assessment or amended assessment which treated the amounts it had received from IDB as income including pursuant to ss 167 or 170 of the ITAA;

(iv) the likelihood that if any of the risks in (i) to (iii) arose, that the Binqld directors would act in their own self-interest or in the interests of the Binetter family, and not the interests of Binqld, by:

A. continuing to conceal the existence of the deposit account from the Commissioner;

B. continuing to conceal the offshore income earned on and in the deposit account from the Commissioner; and

C. failing to provide the necessary documents or disclosures to avoid or minimise the risks manifesting to Binqld;

(d) was pursued by the Binqld directors to benefit themselves or persons or entities comprising the Binetter family by evading the Australian tax payable by those persons or entities through the concealment pleaded in paragraph 119 above;

(e) gave rise to a conflict of interest between the interests of Binqld and the interests of the Binqld directors in that:

(i) the Binqld scheme was entered into and continued in order to assist persons other than Binqld to evade Australian tax (being Andrew and/or Michael and/or other persons or entities comprising the Binetter family); and

(ii) the Binqld scheme was to the detriment of Binqld because it exposed it to the risks identified in subparagraph (c) and did not provide it any benefit at all;

(f) alternatively, negligently exposed Binqld to the risk of loss.

123. In the premises, each of Andrew and Michael breached the fiduciary obligations they owed to Binqld set out in paragraph 120 above and/or the statutory duties they owed to Binqld set out in paragraph 121 above:

(a) by being in a position of conflict of interest with Binqld as long as:

(i) Binqld was involved in the Binqld scheme; and

(ii) he continued to be a director of Binqld; and/or

(b) by involving Binqld in the Binqld scheme; and/or

(c) by continuing to involve Binqld in the Binqld scheme through each of the acts of:

(i) directing IDB to advance funds to Binqld; and/or

(ii) advancing the amounts received to the Nudie companies, Ligon 237, Winmar, Dunba and/or Dunmaf; and/or

(iii) submitting the tax returns set out in paragraphs 112 to 117 above which claimed as deductible expenses, an amount equivalent to the amount paid or payable by Binqld to IDB under the transactions with IDB, thereby reducing income tax which would otherwise have been payable by Binqld under provisions of Australian income tax legislation; and/or

(iv) continuing to conceal the existence of:

A. the Binqld scheme;

B. the deposit account;

C. the offshore income earned on and in the deposit account;

from the Commissioner at all times; and/or

(v) failing to provide the necessary documents or disclosures to explain the Binqld scheme and the existence of the deposit account and offshore income to the Commissioner at any time before the issuing of the assessments, shortfall interest assessments and penalty assessments set out in paragraph 131 below.

(d) alternatively, by negligently exposing Binqld to the risk of loss.

36 At pars 124 to 127, Binqld pleads the facts and matters relied upon as founding its ultimate contention that IDB is liable to it pursuant to the principles explained by Lord Selborne LC in Barnes v Addy and pursuant to s 181 and s 182 of the Corps Act. Those paragraphs of the 4FASOC are in the following terms:

(4) Knowing assistance and involvement by IDB

124. At all relevant times, IDB knew that:

(a) a purpose of the Binetters in acquiring the IDB Banking Service and using it with respect to Binqld by advancing funds to it which were styled as loans was:

(i) to conceal the deposit account from the Commissioner;

(ii) to conceal the offshore income from the Commissioner; and

(iii) to assist persons or entities comprising the Binetter family to evade Australian tax, including on the offshore income earned on the deposit account;

(b) this purpose was not for the benefit or in the best interests of the borrowing customer (being Binqld); and

(c) the use of the borrowing customer was for the benefit of those who controlled it including the primary customer (being a person or entity related to the Binetter family).

Particulars

(i) Paragraphs 25 to 27 above are repeated.

(ii) IDB’s knowledge is to be inferred from the fact that there was no commercial rationale for a bank to offer a banking service like the IDB Banking Service which:

A. allowed the primary customer to advance its funds to borrowing customers of its choosing;

B. allowed the primary customer to choose the interest rate and payment terms that would apply to the transfers to borrowing customers which were styled as loans; and

C. allowed the primary customer to conceal the deposit account through a structure which used multiple accounts,

other than to obtain the custom of customers seeking to obtain benefits of the type set out in paragraph 24 above in circumstances where the IDB Banking Service, included the benefit of evading tax in the primary customer’s home jurisdiction.

(iii) IDB’s knowledge is to be inferred from the fact that:

A. the borrowing customer (being Binqld) made no regular payments purporting to be interest to IDB;

B. the borrowing customer (being Binqld) made no regular payments purporting to be loan repayments or partial loan repayments;

C. IDB made no formal demands to the borrowing customer (being Binqld) for regular payments of the type referred to above; and

D. IDB took no steps to ensure repayment of any amounts purporting to be loans; and

E. in lieu of the above, IDB was content to process payments to it as and when they were made and allocate the payments as “principal” and “interest” as directed by Andrew and/or Michael.

(iv) IDB’s knowledge is to be inferred from its conduct in willingly assisting the concealment of the scheme by providing the letter dated 2 March 2009 which omitted to disclose the true nature of the arrangements between EGL and IDB, including the existence of and [sic] amount contained in the deposit account.

(v) IDB’s knowledge is to be inferred also from the facts in relation to Ligon 268 set out in particular (iii) to paragraph 161 below and in relation to EGL set out in particular (iii) to paragraph 204 below.

124A. In the alternative, at all relevant times, IDB ought reasonably have known the matters alleged in paragraph 124.

Particulars

(i) The particulars to paragraph 124 are repeated.

124B. Further in the alternative, at all relevant times, IDB knew circumstances which would have disclosed the matters alleged in paragraph 124 to an honest and reasonable person.

Particulars

(i) The particulars to paragraph 124 are repeated.

125. IDB benefited from the Binqld scheme because it received the benefit of:

(a) holding the positive difference between the debit balance of the borrowing account and the credit balance of the deposit account from [sic] to time pursuant to the terms of the IDB Banking Service;

(b) receiving a margin on the payments made into the borrowing account or accounts from time to time or otherwise receiving fees and commissions for supplying the IDB Banking Service; and

(c) an increased customer base.

126. The use of the IDB Banking Service was an important element of the Binqld scheme because:

(a) it allowed the transfer to and from IDB of substantial sums of money to be styled as loans from IDB and loan repayments and interest repayments to IDB when the true position was that the funds came from and were under the control at all times of the person or entity related to the Binetter family who was the primary customer pursuant to the IDB Banking Service;

(b) it provided Binqld and the Binqld directors with a means to attempt to justify aspects of the Binqld scheme if questioned by the Commissioner;

(c) it provided Binqld and the Binqld directors with a means to give aspects of the Binqld Scheme seeming legitimacy; and

(d) it allowed persons or entities comprising the Binetter family to access a larger amount of funds than would have been the case if the Binqld scheme had not existed and Australian tax had been paid on the funds.

127. With the general knowledge set out in paragraphs 25 to 27 and the specific knowledge set out in paragraphs 124 to 124B and through its conduct in:

(a) making available and providing the IDB Banking Service to Binqld and/or persons or entities comprising the Binetter family; and/or

(b) advancing funds to Binqld from the borrowing account provided through the IDB Banking Service; and/or

(c) receiving funds into the borrowing account from Binqld and/or persons or entities comprising the Binetter family;

IDB:

(d) knowingly assisted the breaches of the fiduciary obligations owed to Binqld by the Binqld directors set out in paragraph 123;

(e) was involved within the meaning of ss 181(2) and 182(2) of the Corporations Act in the breaches of the statutory obligations owed to Binqld by the Binqld directors set out in paragraph 123 by assisting in, and benefiting from, the implementation of the Binqld scheme in the manner set out in paragraph 125 above;

(f) thereby contravened ss 181(2) and 182(2) of the Corporations Act and remained in contravention each day until Binqld’s involvement in the Binqld scheme was terminated by the appointment of the liquidators on 2 March 2015.

37 Binqld claims compensation for the losses it contends it suffered by reason of the breaches of directors’ duties alleged against Andrew Binetter and Michael Binetter. The amount claimed is $29,075,504.19 being the amount of the unpaid assessments for income tax, penalties and interest incurred by Binqld as a result of those breaches.

38 The claims made by Ligon 268 against IDB are structured in the same way as the claims made by Binqld against IDB. The persons who are alleged to have breached their fiduciary duties owed to Ligon 268 are Erwin Binetter, Andrew Binetter and Michael Binetter. No allegation is made against those persons that they also contravened the Corps Act. As a consequence, no claim is made against IDB in respect of Ligon 268 based upon the Corps Act. The total amount claimed by Ligon 268 is $32,458,486.64.

39 The claims made by EGL against IDB are also similarly structured as the claims made by Binqld. As was the case with Ligon 268, EGL does not make any claim against IDB based upon involvement in breaches of any statutory duties owed to EGL by Erwin Binetter, Andrew Binetter or Michael Binetter. The total amount claimed by EGL is $40,767,456.58.

40 At pars 351 to 374 of the 4FASOC, the plaintiffs plead their cases based upon s 37A. In those paragraphs, the corporate plaintiffs allege that approximately $59 million was transferred by Binqld, Ligon 268 and EGL, at the instigation of Andrew Binetter and Michael Binetter, in circumstances where each of those companies was, or was about to become, insolvent. It is then alleged that the transfers were made with the intent to defraud the creditors of each of those companies and are voidable upon application by each of those companies, upon application by the liquidators and upon application by the Commissioner.

The Relevant Rules of Court

The Text of the Rules

41 Part 10, Div 10.4—Service outside Australia FCR prescribes the circumstances in which a party is permitted to serve Court documents in places outside Australia.

42 Rule 10.41 FCR provides as follows:

10.41 Definitions for Division 10.4

In this Division:

convention, for a foreign country, means a convention (other than the Hague Convention), agreement, arrangement or treaty about service abroad of judicial documents to which the Crown in right of the Commonwealth or, if appropriate, in right of a State, and a foreign country are parties.

foreign country means a country other than Australia.

Hague Convention means the Convention on the Service Abroad of Judicial and Extrajudicial Documents in Civil or Commercial Matters done at the Hague on 15 November 1965.

Note 1: Originating application is defined in the Dictionary.

Note 2 to r 10.41 FCR is not presently relevant.

43 The chapeau to r 10.42 FCR is in the following terms:

10.42 When originating application may be served outside Australia

Subject to rule 10.43, an originating application, or an application under Part 7 of these Rules, may be served on a person in a foreign country in a proceeding that consists of, or includes, any one or more of the kinds of proceeding mentioned in the following table.

44 In the present case, the plaintiffs rely upon Items 1, 5, 13, 15, 18 and 20 in the table referred to in r 10.42 FCR. Those Items in that table are in the following terms:

45 Rule 10.43 FCR provides as follows:

10.43 Application for leave to serve originating application outside Australia

(1) Service of an originating application on a person in a foreign country is effective for the purpose of a proceeding only if:

(a) the Court has given leave under subrule (2) before the application is served; or

(b) the Court confirms the service under subrule (6); or

(c) the person served waives any objection to the service by filing a notice of address for service without also making an application under rule 13.01.

Note: A respondent may apply to set aside an originating application or service of that application—see rule 13.01.

(2) A party may apply to the Court for leave to serve an originating application on a person in a foreign country in accordance with a convention, the Hague Convention or the law of the foreign country.

(3) The application under subrule (2) must be accompanied by an affidavit stating:

(a) the name of the foreign country where the person to be served is or is likely to be; and

(b) the proposed method of service; and

(c) that the proposed method of service is permitted by:

(i) if a convention applies—the convention; or

(ii) if the Hague Convention applies—the Hague Convention; or

(iii) in any other case—the law of the foreign country.

(4) For subrule (2), the party must satisfy the Court that:

(a) the Court has jurisdiction in the proceeding; and

(b) the proceeding is of a kind mentioned in rule 10.42; and

(c) the party has a prima facie case for all or any of the relief claimed in the proceeding.

Note 1: The law of a foreign country may permit service through the diplomatic channel or service by a private agent—see Division 10.5.

Note 2: Rules 10.63 to 10.68 deal with service of local judicial documents in a country, other than Australia, that is a party to the Hague Convention.

Note 3: The Court may give permission under subrule (4) on conditions—see rule 1.33.

(5) A party may apply to the Court for leave to give notice, in a foreign country, of a proceeding in the Court, if giving the notice takes the place of serving the originating application.

(6) If an originating application was served on a person in a foreign country without the leave of the Court, a party may apply to the Court for an order confirming the service.

(7) For subrule (6), the party must satisfy the Court that:

(a) paragraphs (4)(a) to (c) apply to the proceeding; and

(b) the service was permitted by:

(i) if a convention applies—the convention; or

(ii) if the Hague Convention applies—the Hague Convention; or

(iii) in any other case—the law of the foreign country; and

(c) there is a sufficient explanation for the failure to apply for leave.

46 In the present case, service upon IDB in Israel was effective for the purpose of this proceeding because I granted leave under r 10.43(2) FCR before the relevant documents were served (r 10.43(1)(a)). At the time I granted that leave (30 September 2016), I was satisfied that the Court had jurisdiction in this proceeding, that the proceeding was of a kind mentioned in r 10.42 FCR and that the corporate plaintiffs and BCI had a prima facie case for at least some of the relief then claimed in the proceeding.

47 This Court has jurisdiction in respect of the causes of action under the Corps Act relied upon by Binqld as against IDB. In addition, given the common substratum of facts between those causes of action and the causes of action brought by Binqld based upon the principles in Barnes v Addy, the Court also has jurisdiction in respect of those causes of action. For similar reasons, in the circumstances of this case, the Court also has jurisdiction in respect of s 37A cases brought by Binqld. Given that the claims brought by Ligon 268 and EGL have been appropriately included in this proceeding, the Court also has jurisdiction in respect of those claims. IDB conceded that, as at the date of service of the pleadings upon it in Israel and as at 29 September 2017, the date of the first hearing, the Court had jurisdiction in this proceeding within the meaning of r 10.43(4)(a) (see Transcript, 29/09/2017 at p 32 ll 24–37).

48 The plaintiffs rely upon the Items which I have specified at [44] above as the bases upon which they have met the requirement set out in r 10.43(4)(b) FCR.

The Prima Face Case Requirement (Rule 10.43(4)(c) FCR)

49 In ACN 078 272 867 Pty Ltd (In Liq) (formerly Advance Finances Pty Ltd) v Binetter; In the Matter of ACN 078 272 867 Pty Ltd (In Liq) (formerly Advances Finances Pty Ltd) [2018] FCA 952 (Advance Finances) at first instance, at [8]–[12], Lee J summarised the relevant principles in the following terms:

The principles are well established and have been very recently summarised by Rares J in Morris v McConaghy Australia Pty Ltd [2018] FCA 435 at [29]-[30] as follows:

In Ho v Akai Pty Ltd (In Liq) (2006) 247 FCR 205 at 208 [10], Finn, Weinberg and Rares JJ said:

As has been observed on many occasions, the prima facie case requirement has to be met at the outset, usually on an ex parte basis, and without the advantage of discovery and other procedural aids to the making out of a case: see eg Merpro Montassa Ltd v Conoco Specialty Products Inc (1991) 28 FCR 387 at 390. It “should not call for a substantial inquiry”: WSGAL Pty Ltd v Trade Practices Commission (1992) 39 FCR 472 at 476; see also Sydbank Soenderjylland A/S v Bannerton Holdings Pty Ltd (1996) 68 FCR 539 at 549. For present purposes it is sufficient to say that a prima facie case for relief is made out if, on the material before the court, inferences are open which, if translated into findings of fact, would support the relief claimed: Western Australia v Vetter Trittler Pty Ltd (in liq) (1991) 30 FCR 102 at 110. Or, to put the matter more prosaically as Lee J did in Century Insurance Ltd (in prov liq) v New Zealand Guardian Trust Ltd [1996] FCA 376:

What the Court must determine is whether the case made out on the material presented shows that a controversy exists between the parties that warrants the use of the Court’s processes to resolve it and whether causing a proposed respondent to be involved in litigation in the Court in Australia is justified.

The requirement of r 10.43(4)(c), that there be a prima facie case for all or any of the relief sought, will be satisfied if the applicant makes out a prima facie case, to the standard referred to above, in respect of any one of the causes of action for which relief is sought: Ho 247 FCR at 215 to 216 [45] applying Bray v F Hoffman-La Roche Ltd (2003) 130 FCR 317 in respect of an analogue of r 10.43(4)(c).

The requirement has been described as “not particularly onerous”: see Australian Competition and Consumer Commission v Yellow Page Marketing BV [2010] FCA 1218 at [25] per Gordon J. It was observed of a predecessor provision by Bennett J in Australian Competition and Consumer Commission v April International Marketing Services Australia Pty Ltd (No 6) [2010] FCA 704; (2010) 270 ALR 504 at 507 [8]:

Establishing a prima facie case for the relief claimed…should not call for a substantial inquiry. A prima facie case is made out where, upon a broad examination rather than an intense scrutiny of the material before the court, inferences are shown to be open which, if translated into findings of fact, would support the relief claimed: Western Australia v Vetter Trittler Pty Ltd (in liq) (rec and mgr apptd) (1991) 30 FCR 102 at 110; 4 ACSR 795 at 802–3 per French J; Sydbank Soenderjylland (A/S) v Bannerton Holdings Pty Ltd (1996) 68 FCR 539 at 549; 149 ALR 134 at 142–3; the Full Court in F Hoffman-La Roche at [17] and [96]–[97] per Carr J.

Like the former rule (O 9, r 7), it was common ground that FCR 13.01 requires the conduct of a rehearing of the original decision to grant leave, taking into account any additional material put to the Court on the later application: Tycoon Holdings Ltd v Trencor Jetco Inc (1992) 34 FCR 31 at 33; Bray v F Hoffman-La Roche Ltd [2003] FCAFC 153; (2003) 130 FCR 317 at 332 [53]; Australian Competition and Consumer Commission v Prysmian Cavi E Sistemi Energia SRL (formerly Pirelli Cavi E Sistemi Energia SPA) (No 4) [2012] FCA 1323; (2012) 298 ALR 251 at 258 [40]. In this regard, it was uncontroversial that it was open to the plaintiffs, on the hearing of the Bank’s inter partes application to set aside service, to adduce additional evidence to that put before Foster J on the ex parte application: WSGAL Pty Limited v Trade Practices Commission (1992) 39 FCR 472; Costa Vraca Pty Ltd v Bell Regal Pty Ltd [2003] FCAFC 305.

Further, in the context of applications under FCR 13.01, where a prima facie case for relief is established, it was accepted that the Court would not set aside service merely because the case for relief did not conform precisely to the words of the statement of claim. This makes sense, because in this way, applications such as the present do not provide a mechanism for some form of collateral attack on the pleadings: Cell Tech Communications Pty Ltd v Nokia Mobile Phones (UK) Ltd (1995) 58 FCR 365 at 373-374.

It follows in the present circumstances that a sufficient prima facie case will be established if such a case is made out in relation to either the Conveyancing Act Claim or the Corporations Act Claim: see Bell Group Ltd (in liq) v Westpac Banking Corporation (1996) 20 ACSR 760; Cell Tech at 373.

50 In its judgment dismissing IDB’s Application for Leave to Appeal from the judgment of Lee J (Israel Discount Bank Ltd v ACN 078 272 867 Pty Ltd (In Liq) (formerly Advance Finances Pty Ltd) (2019) 367 ALR 71 (Advance Finances, FC)), at 77 [22], the Full Court (Yates, Beach and Moshinsky JJ) said:

The primary judge set out the applicable principles regarding the prima facie case requirement in r 10.43(4)(c) of the Federal Court Rules at [8]–[12] of the Reasons, referring to cases including Morris v McConaghy Australia Pty Ltd [2018] FCA 435 (Morris) at [29]–[30] per Rares J; Australian Competition and Consumer Commission v Yellow Page Marketing BV [2010] FCA 1218 at [25] per Gordon J; and Australian Competition and Consumer Commission v April International Marketing Services Australia Pty Ltd (No 6) (2010) 270 ALR 504; [2010] FCA 704 at [8] per Bennett J. In Morris, Rares J quoted from the judgment of the Full Court of this Court in Ho v Akai Pty Ltd (in liq) (2006) 247 FCR 205; [2006] FCAFC 159 (Ho v Akai) at [10], where the Full Court said that “a prima facie case for relief is made out if, on the material before the court, inferences are open which, if translated into findings of fact, would support the relief claimed”. It was sufficient for the plaintiffs to establish a prima facie case in relation to either the Conveyancing Act claim or the Corporations Act claim: Reasons at [12], citing Bell Group Ltd (in liq) v Westpac Banking Corporation (1996) 20 ACSR 760; Cell Tech Communications Pty Ltd v Nokia Mobile Phones (UK) Ltd (1995) 58 FCR 365 at 373; 136 ALR 733 at 741 (Cell Tech).

51 I propose to apply these principles when considering the question of whether the corporate plaintiffs have established a prima facie case for some or all of the relief claimed by them in their pleadings, as required by r 10.43(4)(c) FCR.

52 The onus of establishing that they have a prima facie case to the requisite standard rests upon the plaintiffs as the claimants for final relief. What may be required in any particular case to discharge that onus will depend upon (inter alia) the nature of the claims for final relief made by the applicant and the requirements of the substantive law underpinning the causes of action relied upon in support of those claims for relief.

53 If an applicant ultimately fails to establish that it has a prima facie case for some or all of the relief claimed by it in the proceeding, then leave to serve the Originating Process outside Australia must be refused, or, if leave has already been granted but is subsequently being challenged by the party served, the order granting leave to serve the relevant process outside Australia should be discharged and/or service of that process on that party should be set aside. This would be so whether or not the method of service chosen by the plaintiff was permitted by and in accordance with the law of the foreign country where service is to be effected. That is, if an applicant fails to establish that it has a prima facie case to the requisite standard, the challenged service will not be valid.

54 The content of the law of a foreign country for the purposes of proceedings in this Court is a question of fact. Commonly, parties adduce evidence before the Court from a suitably qualified expert as to the content of the relevant foreign law. This was the approach taken in the present case, although the weight to be accorded to the expert testimony of the witnesses called by the parties here will be influenced by the circumstance that neither party cross-examined the other party’s expert witnesses.

Setting Aside Service or Discharge of the Order for Service

The Requirements of r 10.42 FCR and r 10.43(4)(b) FCR

55 I shall address the requirements of r 10.42 FCR by reference to the Items in the r 10.42 table relied upon by the plaintiffs (ie Items 1, 5, 13, 15, 18 and 20).

Item 1

56 The corporate plaintiffs are all companies incorporated in Australia and carrying on business in Australia. The fiduciary and statutory duties alleged by those plaintiffs as owed to them by their directors were obligations and duties owed in Australia. At all relevant times, each of the defaulting directors was generally domiciled in Australia. Much of the conduct of the delinquent directors took place in Australia. It is tolerably clear that the causes of action constituting the alleged contraventions by the directors of the corporate plaintiffs were all causes of action which arose in Australia. The corporate plaintiffs submitted that IDB provided the IDB Banking Service in Australia. They submitted that IDB received funds from Australian residents into the deposit account and then allowed drawdowns to each of the corporate plaintiffs in Australia from the borrowing accounts. The corporate plaintiffs also submitted that IDB provided clean documents for use in Australia. Those clean documents provided assistance to the directors in effecting the frauds which they are alleged to have committed.

57 IDB, on the other hand, submitted that the conduct alleged to constitute the relevant knowing assistance and involvement in the contraventions on the part of the directors of the corporate plaintiffs took place entirely outside Australia and in Israel. For this reason, IDB submitted that the corporate plaintiffs could not rely upon Item 1.

58 The corporate plaintiffs’ causes of action against IDB for knowing assistance based upon the principles enunciated in Barnes v Addy and Binqld’s cause of action for knowing involvement in the Corps Act contraventions alleged against the directors of Binqld were not complete, it seems to me, until the directors put into effect their fraudulent scheme. The effectuation of that scheme took place in Australia. For this reason, I think that the better view is that the causes of action relied upon by the corporate plaintiffs against IDB arose in Australia.

59 In the 4FASOC, there are three separate claims brought against IDB based upon s 37A. First, there are the claims made by the corporate plaintiffs. Second, there are the claims made by the liquidators. Third, there are the claims made by the Commissioner. The s 37A claims made by the corporate plaintiffs were included in the pleadings in this proceeding in February 2019. The s 37A claims made by the liquidators and the Commissioner were conditionally included in the pleadings on 12 November 2019.

60 In its Written Submissions dated 20 September 2019 (at pars 36 to 42), IDB argued that none of the s 37A claims arose in Australia. Its submissions may be summarised as follows:

(a) An action will arise in Australia if the substance of the action arose here. The usual approach is to ask where the place of “the act on the part of the defendant which gives the plaintiff his cause to complain” took place.

(b) Here, the complaint made against IDB is that it received, in Israel, payment of money from the corporate plaintiffs in circumstances which rendered that payment of money subject to refund.

(c) A necessary element of the s 37A claims is the requirement for the plaintiffs to establish that IDB lacked good faith in receiving the funds in Israel. Because that requirement focuses on IDB’s state of mind at the time it received the payments, as ascertained from relevant officers and employees located in Israel, that element did not involve conduct in Australia but rather involved conduct in Israel.

(d) Taking the above matters together, in the result, none of the claims based upon s 37A fall within Item 1 because all of those claims arose in Israel.

61 The plaintiffs took issue with this analysis. At pars 104 to 113 of their Written Submissions dated 31 October 2019, the plaintiffs made detailed submissions as to why IDB’s contentions in this respect are incorrect.

62 The plaintiffs made the following submissions:

(a) The s 37A claims focus on alienations of property and the intent with which those alienations were made. In this case, the s 37A claims attack the conduct of the persons who previously controlled and administered the plaintiffs (Erwin, Andrew and Michael Binetter);

(b) The prejudice at which the s 37A claims are aimed is prejudice that occurred in Australia viz loss of control of the funds the subject of the transfers under attack;

(c) It does not matter where the funds ended up; and

(d) The prejudice suffered by the corporate plaintiffs and the Commissioner occurred in Australia.

63 I think that the better view is that the s 37A causes of action also arose in Australia for the reasons submitted by the plaintiffs. It follows that all of the causes of action relied upon by the plaintiffs arose in Australia and that Item 1 was and is satisfied in the present case.

Item 5

64 The corporate plaintiffs maintained their reliance upon Item 5 and referred to two cases in support of their submissions (OJSC Oil Company Yugraneft (In Liq) v Abramovich [2008] EWHC 2613 (Comm) (OJSC) and Commonwealth Bank of Australia v White [1999] 2 VR 681 at 698–699 [63]–[64] per Byrne J). The corporate plaintiffs also referred me to a decision which was to the contrary effect (Nicholls v Michael Wilson & Partners Ltd (2010) 243 FLR 177 at 240 [339] per Lindgren AJA).

65 I do not think that any of the claims made by the plaintiffs in the present case are torts within the meaning of Item 5.

66 In OJSC, Clarke J (at [223]) regarded the claims for dishonest assistance made in the case before him as being “so closely analogous to a claim in tort (as characterised for purely domestic purposes) that it should, I would have thought, be so characterised for private international law purposes”.

67 With respect to his Lordship, I do not find that reasoning persuasive. The concept of “tort” in Australian domestic law is well understood and does not, in my view, encompass such a claim. I see no reason to interpret the concept differently for Private International Law purposes.

68 Nor do I think that the Corps Act claims against IDB or the s 37A claims against IDB can be characterised as torts.

69 Accordingly, I reject the plaintiffs’ proposition that Item 5 is engaged at all in the present case.

Items 13 and 15

70 Items 13 and 15 relate to proceedings based upon the contravention of an “Act” or seeking relief or remedy under an “Act”.

71 In the Dictionary forming part of the FCR (Schedule 1), “Act” is defined to mean the “Federal Court of Australia Act 1976”. No other definition of “Act” is to be found in the FCR.

72 IDB submitted that the word “Act” in Items 13 and 15 should be interpreted as meaning “Commonwealth Statutes”. In support of that proposition, it relied upon Perdaman Chemicals & Fertilisers v Griffin Coal Mining Company Pty Ltd [2011] FCA 1425 at [11] per Siopis J and Fletcher v Capstone Aluminium SDN BHD; In the Matter of McLay Industries Pty Ltd (In Liq) [2016] FCA 1459 at [11] per Greenwood J. However, neither of those cases directly decides the point nor is either of those cases of any real assistance in resolving the point. In the paragraphs cited, Siopis J and Greenwood J merely observe that, in the case before each of them, the relevant claim was based upon a Commonwealth Act. Neither of their Honours said that “Act” in Items 13 and 15 means “Commonwealth Act”.

73 IDB also relied upon s 38 of the Acts Interpretation Act 1901 (Cth). However, that section merely speaks to the permissive identification of statutes and does not mandate any particular or specific descriptor. It certainly does not go so far as to suggest that a reference to the word “Act” in rules of court (and, in particular, in the FCR) should be taken to be a reference to statutes passed by the Commonwealth Parliament in contradistinction to statutes passed by State and Territory Parliaments.

74 IDB also relied upon s 21(b) of the Acts Interpretation Act. However, I do not regard that section as being relevant.

75 The only authority cited by the parties which is directly in point is Bray v F Hoffman-La Roche Ltd (2003) 130 FCR 317 at 350 [152] per Branson J. There, her Honour said (in passing, it has to be said) that an “Act” within the meaning of the Rules is an Act passed by the Parliament of the Commonwealth. Justice Branson referred to s 38(1) of the Acts Interpretation Act to support that statement. The other members of the Full Court did not adopt her Honour’s views on this point.

76 At pars 119 to 121 of their Written Submissions dated 31 October 2019, the plaintiffs made the following submissions in relation to Items 13 and 15:

The purpose of the items in r 10.42 is to ensure that the proceeding in question has a sufficient connection with “the country asserting jurisdiction”, ie, Australia: cf Tiger Yacht at [50]. Rule 10.42 “describes a number of different kinds of proceedings which have a sufficient connection with Australia to justify the invocation of Australian jurisdiction in relation to the dispute”: International Maritime Services Pty Ltd v Marina Towage Pte Ltd [2014] FCA 416 at [8].

It is significant that r 10.42 focusses on the proceeding’s connection with Australia. Where the connecting factor between a proceeding and Australia is that the proceeding seeks “any relief or remedy under an Act” (r 10.42, item 15), the strength of that connection does not depend upon whether the Act in question is a State Act or a Commonwealth Act. The same may be said in respect of the use of “Act” in items 12, 13, 14 and 16.

Considering the purpose of the rule, there is no reason why the drafters of r 10.42 would have intended to distinguish between the two types of Act. That purpose would be undermined if the narrow reading of “Act” applied, as the result would be that cases with a stronger connection to Australia than many cases within r 10.42 might nevertheless fall outside the rule. This suggests that the drafters did not intend the narrow meaning of “Act” to apply. A “contrary intention” for the purposes of s 2(2) of the Acts Interpretation Act exists. The word “Act” should be read as any Australian statute.

77 I think that these submissions are correct and I accept them. Therefore, I am of the opinion that the plaintiffs’ s 37A claims fall within Items 13 and 15.

78 Clearly enough, the plaintiffs’ claims based upon the Corps Act fall within Items 13 and 15.

79 IDB submitted that the causes of action relied upon by Binqld based upon the Corps Act were not sufficient to satisfy Items 13 and 15, as contended by the corporate plaintiffs, because Binqld has not established that the Corps Act applies to the alleged conduct of IDB. This submission was not developed. Nonetheless, as I understand this submission, IDB contends that the relevant provisions of the Corps Act founding the allegation of knowing involvement on its part do not have any extraterritorial effect.

80 However, the Corps Act contraventions alleged by Binqld against IDB are contraventions in respect of which relief is sought in relation to damage suffered in Australia. In that event, it does not matter where the relevant contravention occurred. Accordingly, even if IDB’s submission that the relevant conduct with which IDB stands charged occurred in Israel, and not in Australia, that is not sufficient to take the present proceeding outside Item 13.

81 Item 15 applies because Binqld seeks relief and a remedy under the Corps Act against IDB.

82 For all of the above reasons, I think that the requirements of Items 13 and 15 are satisfied in the present case.

Item 18

83 The corporate plaintiffs submitted that IDB carried on business in Australia at all relevant times because:

(a) It supplied banking services to Australian residents;

(b) It transferred funds into Australia from time to time and received funds from Australia from time to time; and

(c) It was involved in a scheme or schemes which had as its purpose the evasion of Australian tax. IDB was involved in that scheme for the purpose of profit on a continuous and repetitive basis.

84 These circumstances justify the conclusion that IDB was undertaking activities in Australia as a commercial enterprise in the nature of a going concern, that is, activities engaged in for the purpose of profit on a continuous and repetitive basis.

85 IDB submitted that the evidence did not support a conclusion that it was relevantly carrying on business in Australia. The mere fact that its customers happened to be Australian was not sufficient. IDB also submitted that the services which it provided to the corporate plaintiffs and their directors were provided in Israel, not in Australia.

86 It seems to me that IDB did provide some of its banking services in Australia because it received funds from time to time remitted from Australia and repatriated funds to Australia all at the behest of the corporate plaintiffs who were based in Australia. I do not consider that the mere fact that IDB did not have an office in Australia and generally did not have employees based in Australia necessarily leads to the conclusion that it was not relevantly carrying on business in Australia. For these reasons, I am of the opinion that Item 18 was and is also satisfied.

Item 20

87 Item 20 allows an applicant to serve any person who is outside the jurisdiction if that person is a necessary or proper party to an action that is brought against another party who has already been served in Australia. The correct approach to determining whether the proceeding is of a kind referred to in Item 20 is to ask whether a local respondent has been properly joined and then to determine whether the proposed foreign party would have been a proper party to the proceeding if it had been within the jurisdiction (see Costa Vraca Pty Ltd v Bell Regal Pty Ltd [2003] FCAFC 305 (Costa Vraca) at [17] per Ryan, Kiefel and Gyles JJ). A person may be considered to be a proper or necessary party where the claims against that person arise from a common substratum of facts (Costa Vraca at [25]).

88 When this proceeding was commenced and also at the time when service was effected upon IDB, there were twelve other defendants joined as parties to the proceeding. The first ten of those defendants were Binetter-controlled corporations, all of which were incorporated in Australia. They had been served with the Originating Process long before service was effected on IDB. The eleventh and twelfth defendants were the Bank Hapoalim parties.

89 The joinder of all of those defendants at the suit of the corporate plaintiffs and BCI at each of those times was legitimate because all of those defendants were appropriately joined as defendants pursuant to r 9.02 FCR.

90 IDB submitted that it was not a necessary or proper party within the meaning of Item 20. IDB submitted that the case against the Binetter corporations could have been determined by the Court without reference to the matter against IDB. It submitted that it would not have impeded the Court’s ability to determine the corporate plaintiffs’ claims against those defendants if IDB had not been a party to the proceeding. These submissions made on behalf of IDB ignore the fact that Item 20 is not confined to the joinder of foreign parties who are necessary parties but also encompasses foreign entities which are considered to have been “properly joined as a party”.

91 IDB also submitted that, given that the settlement was effected in late 2018, before the resumed hearing of its Discharge Application on 12 November 2019, Item 20 no longer applies because, by then, there were no longer any local defendants in the proceeding. I do not think that this submission is correct. The matter must be judged as at the date service was effected (4 December 2016). The Binetter-related defendants were still parties to this proceeding with the consequence that Item 20 was satisfied then.

92 For the above reasons, I consider that Item 20 was and is clearly satisfied in the present case. This proceeding was properly brought against the twelve defendants with whom the plaintiffs have now settled. IDB was properly joined as a party to this proceeding.

Conclusions (Rule 10.42 FCR)

93 For all of the above reasons, I consider that r 10.42 FCR is satisfied in respect of all of the claims currently made in the 3FAOA and the 4FASOC because this proceeding “… includes … one or more of the kinds of proceeding” mentioned in the Table forming part of r 10.42 FCR. It necessarily follows from this conclusion that the requirement specified in r 10.43(4)(b) has also been satisfied in the present case.

The Plaintiffs’ Prima Facie Case

94 When the plaintiffs’ ex parte application for leave to serve the Originating Process on IDB in Israel was before me, the plaintiffs relied (inter alia) upon the affidavit of John Sheahan affirmed on 24 May 2016. There were voluminous exhibits to that affidavit. Those exhibits included most of the Tender Bundle documents tendered by the plaintiffs at the trial before Gleeson J of proceeding SAD5 of 2015 (SAD5). That trial took place in August and September 2015. Justice Gleeson delivered judgment in that matter (BCI Finances Pty Ltd (In Liq) v Binetter (No 4) (2016) 348 ALR 227 (BCI Finances (No 4))) on 18 November 2016.

95 Instead of formally tendering all of that material, the plaintiffs relied upon a “mini bundle” of documents or “supplementary tender bundle” (STB).

96 This approach was adopted in order to avoid unnecessarily burdening the Court with documentary tenders.

97 At the hearing before me, on 29 September 2017, the plaintiffs adopted the same approach. IDB did not object to this course.

98 The STB was tendered in evidence before me on 29 September 2017. It became Exhibit A.

99 Exhibit A was largely, if not entirely, directed to the role played by IDB in this saga. It was not intended to address the position of the delinquent directors (Erwin, Andrew and Michael Binetter) to any degree. It is fair to say that, on 29 September 2017, and indeed at the second hearing on 12 November 2019, the parties proceeded upon the basis that the plaintiffs had at least a prima facie case against those directors and their associated corporate entities who were the first to tenth defendants in this proceeding. The hearings before me were conducted upon the basis that, for present purposes, the plaintiffs did not need to prove that case. In particular, at Transcript 29/09/17, p 7 ll 15–28, the following exchange took place:

HIS HONOUR: Do you accept that there’s enough evidence here to a requisite prima facie level to establish the liability of the principal actors in the so-called fraudulent and dishonest design?

MR CLELLAND: Can we put it slightly differently and say that we don’t want to be heard to argue that there isn’t.

HIS HONOUR: All right. So you’re concentrating very much on the position of your own client - - -

MR CLELLAND: Yes.

HIS HONOUR: - - - and on the absence of enough evidence to justify the case put against your client.

See also the observations which I made at Transcript 29/09/17, p 27 ll 5–10.

100 The prima facie case requirement does not call for a substantial enquiry. It is sufficiently satisfied if, on the material before the Court, inferences are open which, if translated into findings of fact, would support the relief claimed (Ho v Akai Pty Ltd (In Liq) (2006) 247 FCR 205 (Ho) at 208 [10] per Finn, Weinberg and Rares JJ).

101 To recap, before they were wound up, the corporate plaintiffs were under the control of their directors, Erwin, Andrew and Michael Binetter. The plaintiffs allege that the directors of each of the corporate plaintiffs breached the duties owed to them by involving and continuing to involve the plaintiffs in a scheme or schemes implemented to assist persons within, and entities connected with, the Binetter family in evading Australian tax. Involving the plaintiffs in that scheme or schemes provided no benefit to the plaintiffs, while exposing them to the risk of unfavourable tax assessments.

102 The scheme or schemes involved using the IDB Banking Service in order to bring substantial funds into Australia styled as loans to the plaintiffs, while at the same time concealing from the Commissioner the existence of offshore funds held in accounts with IDB for the purposes of evading Australian tax.

103 SAD5 was a proceeding brought by the corporate plaintiffs and BCI against members of the Binetter family and a number of their associated corporate entities. That is to say the plaintiffs in SAD5 were the same corporations as comprise the first three plaintiffs in this proceeding together with BCI. The subject matter of that proceeding was essentially the same subject matter as this proceeding. The scheme described in the pleadings in this proceeding is the same scheme as the scheme relied upon in SAD5. The tax assessments resulting from the fraudulent conduct of the Binetters referred to in this proceeding are the same tax assessments as were in play in SAD5. In truth, the only difference between the two sets of proceedings is the identity of the defendants. For this reason, observations made by Gleeson J in Binetter (No 4) are relevant to the present application. Although that judgment was the subject of an appeal, the settlement was agreed before the Full Court had delivered judgment in that appeal. The settlement resolved all matters under consideration in the appeal with the exception of the appeal concerning the position of Gary Binetter. For that reason, it was necessary for the Full Court to deliver a judgment dealing with that part of the appeal concerning Gary Binetter (BCI Finances Pty Ltd (In Liq) v Binetter (2018) 362 ALR 597 (BCI Finances v Binetter, FC). That Full Court judgment did not interfere with the findings and orders made by Gleeson J in Binetter (No 4). The appeal involving Gary Binetter was dismissed and the orders made by Gleeson J against the other parties in SAD5 remained in full force and effect after the settlement was agreed.