FEDERAL COURT OF AUSTRALIA

Auctus Resources Pty Ltd v Commissioner of Taxation [2020] FCA 1096

ORDERS

Applicant | ||

AND: | COMMISSIONER OF TAXATION OF THE COMMONWEALTH OF AUSTRALIA Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The parties are to confer and, if agreement can be reached, provide the Court with orders for final relief within 14 days hereof, or failing that, each party shall file written submissions on the issue of the form of final relief limited to four pages in length.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

STEWARD J.:

1 The applicant (the “taxpayer”) seeks relief against the respondent (the “Commissioner”) pursuant to s. 39B of the Judiciary Act 1903 (Cth.) (the “Judiciary Act”). In 2014 the Commissioner paid the taxpayer the sum of $2,269,336.05 as a result of a claim made by the taxpayer for a research and development, or “R & D”, tax offset refund in its tax return for the year of income ended 30 June 2013. The Commissioner says that this was a mistaken administrative overpayment for the purpose of s. 8AAZN of the Taxation Administration Act 1953 (Cth.) (the “T.A.A.”). As such it is a debt due to the Commonwealth. The taxpayer disagrees. It submits that it is entitled to keep the money paid to it, even though it now accepts that its R & D claim was incorrect.

Applicable Legislation and Extrinsic Material

2 Section 8AAZN is contained within Div. 4 of Pt. IIB of the T.A.A. That Part deals with running balance accounts (or “R.B.A.”s), the application of payments and credits and certain other related matters. Division 4 deals with “miscellaneous provisions about tax debts”. It contains provisions about when payments are treated as received; the electronic payment of tax debts; what are business days for tax debts; and about overpayments made by the Commissioner under taxation laws. Part IIB, including s. 8AAZN, was introduced into the T.A.A. in 1999 by the Taxation Laws Amendment Act (No. 3) 1999 (Cth.). Section 8AAZN provides:

Overpayments made by the Commissioner under taxation laws

(1) An administrative overpayment (the overpaid amount):

(a) is a debt due to the Commonwealth by the person to whom the overpayment was made (the recipient); and

(b) is payable to the Commissioner; and

(c) may be recovered in a court of competent jurisdiction by the Commissioner, or by a Deputy Commissioner, suing in his or her official name.

(2) If:

(a) the Commissioner has given a notice to the recipient in respect of the overpaid amount, specifying a due date for payment that is at least 30 days after the notice is given; and

(b) any of the overpaid amount remains unpaid at the end of that due date;

then the recipient is liable to pay the general interest charge on the unpaid amount for each day in the period that:

(c) started at the beginning of that due date; and

(d) finishes at the end of the last day on which, at the end of the day, any of the following remains unpaid:

(i) the overpaid amount;

(ii) general interest charge on any of the overpaid amount.

(3) In this section:

administrative overpayment means an amount that the Commissioner has paid to a person by mistake, being an amount to which the person is not entitled.

3 The effect of s. 8AAZN is to create a debt due to the Commonwealth to the extent of a mistaken administrative overpayment.

4 Division 355 of the Income Tax Assessment Act 1997 (Cth.) (the “1997 Act”) contains the rules for the allowance of R & D tax offsets. The entitlement to such an offset is created by s. 355-100. It is not necessary to set that provision out. Certain types of tax offsets are “refundable tax offsets” for the purposes of Div. 67 of Pt. 2-20 of the 1997 Act. Where a taxpayer’s refundable tax offsets exceed its tax liability, a refund may be payable to the taxpayer. For R & D tax offsets, the refund is payable pursuant to s. 67-30 and item 40 of s. 63-10(1) of the 1997 Act.

5 An R & D tax offset is available, amongst other things, for expenditure incurred on R & D activities which have been registered by Innovation and Science Australia (referred to as the “Board”) pursuant to s. 27A of the Industry Research and Development Act 1986 (Cth.) (the “I.R.D. Act”). That provision relevantly provides:

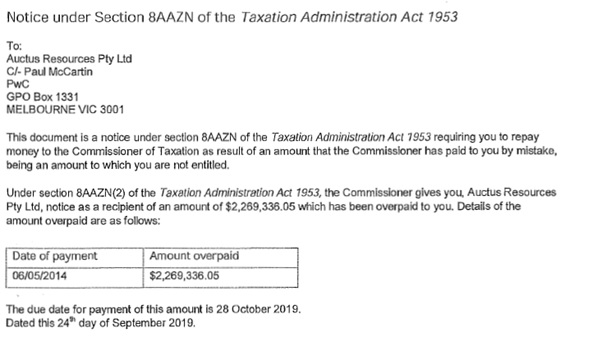

Registering R&D entities for R&D activities

(1) The Board must, on application by an R&D entity, decide whether to register or refuse to register the entity for either or both of the following for an income year:

(a) one or more specified activities as core R&D activities conducted during the income year;

(b) one or more specified activities as supporting R&D activities conducted during the income year.

6 Once an activity is registered, the scheme of the I.R.D. Act provides for the Board to conduct, if it so wishes, an examination of the activities undertaken by the taxpayer to determine whether they were core or supporting R & D activities. The Board is then authorised by s. 27J to make findings about that issue. That provision provides:

Findings about a registration

(1) The Board may make one or more findings to the following effect about an R&D entity’s registration under section 27A for an income year (the registration year):

(a) that all or part of a registered activity was a core R&D activity conducted during the registration year;

(b) that all or part of a registered activity was not an activity of a kind covered by paragraph (a);

(c) that all or part of a registered activity was a supporting R&D activity conducted during the registration year and in relation to:

(i) one or more specified registered core R&D activities; or

(ii) one or more specified core R&D activities for which the entity has been registered in an earlier income year; or

(iii) one or more specified core R&D activities yet to be conducted for which the entity could be registered in the registration year if those activities were conducted during the registration year; or

(iv) several specified core R&D activities, each covered by subparagraph (i), (ii) or (iii);

(d) that all or part of a registered activity was not an activity of a kind covered by paragraph (c).

Note 1: A finding is reviewable (see Division 5).

Note 2: The Board could make a finding under paragraph (b) if, for example, the Board has insufficient information to make a finding under paragraph (a). Similarly, the Board could make a finding under paragraph (d) if it has insufficient information to make a finding under paragraph (c).

(2) If the Board makes a finding under subsection (1) in relation to the R&D entity’s registration, the Board may specify in the finding the times to which the finding relates.

Example: A finding under paragraph (1)(a) could specify the times during the registration year that a registered activity was a core R&D activity.

(3) This section has effect subject to section 32B (findings cannot be inconsistent with any earlier findings).

7 Section 27L(1) should also be set out. It provides as follows:

Automatic variations so registration is consistent with findings

If an R&D entity is registered under section 27A for an income year, then while a finding is in force:

(a) under subsection 27B(1) in relation to the application for the registration; or

(b) under subsection 27J(1) in relation to the registration;

the registration is taken always to have existed in a form consistent with the finding.

8 The Commissioner is bound by a finding of the Board made under s. 27J (s. 355-705 of the 1997 Act) and has the power to issue an amended assessment to a taxpayer where the Board decides that an activity undertaken by a taxpayer was not a core or supporting R & D activity. The Commissioner has two years from the date of receiving the certificate setting out the Board’s finding to do this so long as that finding was made within four years after the end of the income year or the last of the income years (as appropriate) affected by the finding. That two year limitation only applies where issuing the amended assessment would increase the taxpayer’s liability. Section 355-710(1) and (2) of the 1997 Act provides:

Amendment of assessments

Dealing with findings of Innovation and Science Australia

(1) If:

(a) a certificate given to the Commissioner under the Industry Research and Development Act 1986 sets out:

(i) a finding under section 27B of that Act about an *R&D entity’s application for registration under section 27A of that Act for an income year; or

(ii) a finding under section 27J of that Act about an R&D entity’s registration under section 27A of that Act for an income year; or

(iii) a finding under section 28A or 28C of that Act made on application by an R&D entity during an income year; or

(iv) a finding under section 28E of that Act about an R&D entity and one or more R&D activities conducted or to be conducted during one or more income years; and

(b) the finding was made within 4 years after the end of the income year or the last of the income years (as appropriate);

despite section 170 of the Income Tax Assessment Act 1936, the Commissioner may amend the R&D entity’s assessment for an income year affected by the finding at any time for the purposes of giving effect to the finding.

(2) However, the Commissioner may only do so within 2 years after the Commissioner is given the certificate if giving effect to the finding would increase the R&D entity’s liability.

9 Section 355-710 is concerned with the assessment of a taxpayer. In the 2013 year of income, the Commissioner’s general assessing power in s. 166 of the Income Tax Assessment Act 1936 (Cth.) (the “1936 Act”) was in the following terms:

From the returns, and from any other information in the Commissioner’s possession, or from any one or more of these sources, the Commissioner shall make an assessment of the amount of the taxable income (or that there is no taxable income) of any taxpayer, and the tax payable thereon (or that no tax is payable).

10 The foregoing power makes no reference to an assessment of the amount of a taxpayer’s refundable tax offsets. Where a taxpayer has no taxable income and has instead received a refund arising from a refundable tax offset, which occurred in this case, it would appear that the Commissioner accepted (see below) that he had no power to issue an amended assessment pursuant to ss. 355-710 and 166 to reverse a refund paid which the taxpayer was not entitled to keep.

11 This position was resolved for the following year of income and the subsequent years of income, but on a prospective basis only. The Tax and Superannuation Laws Amendment (2013 Measures No.1) Act 2013 (Cth.) (the “2013 Amending Act”) introduced the following new s. 166 to replace former s. 166:

Assessment

From the returns, and from any other information in the Commissioner’s possession, or from any one or more of these sources, the Commissioner must make an assessment of:

(a) the amount of the taxable income (or that there is no taxable income) of any taxpayer; and

(b) the amount of the tax payable thereon (or that no tax is payable); and

(c) the total of the taxpayer’s tax offset refunds (or that the taxpayer can get no such refunds).

(Emphasis added.)

12 Section 172A of the 1936 Act was also introduced by the 2013 Amending Act. It also had effect from the 2014 year of income, and makes any overpaid refundable tax offsets due and payable within 21 days of the issue of an amended assessment disallowing those offsets. It is an express power to do what the Commissioner submits he has always been able to achieve by an application of s. 8AAZN. Section 172A provides:

Consequences of amendment of assessments of tax offset refunds

Amendment increases total of tax offset refunds

(1) If, by reason of an amendment of an assessment, the total of a person’s tax offset refunds is increased, the Commissioner must apply the amount of the increase in accordance with Divisions 3 and 3A of Part IIB of the Taxation Administration Act 1953.

Note: Interest on the amount of the increase may be payable under the Taxation (Interest on Overpayments and Early Payments) Act 1983.

Amendment reduces total of tax offset refunds

(2) If:

(a) by reason of an amendment of an assessment, the total of a person’s tax offset refunds is reduced; and

(b) as a result, an amount applied in accordance with Divisions 3 and 3A of Part IIB of the Taxation Administration Act 1953 before the amendment was excessive;

the person is liable to pay to the Commonwealth the amount of the excess. The amount is due 21 days after the Commissioner gives the person notice of the amended assessment.

Note: For provisions about collection and recovery of the amount, see Part 4-15 in Schedule 1 to the Taxation Administration Act 1953.

(3) If any of the amount (the overpayment) the person is liable to pay under subsection (2) remains unpaid after the time by which it is due to be paid, the person is liable to pay the general interest charge on the unpaid amount for each day in the period that:

(a) starts at the beginning of the day on which the overpayment was due to be paid; and

(b) finishes at the end of the last day on which, at the end of the day, any of the following remains unpaid:

(i) the overpayment;

(ii) general interest charge on any of the overpayment.

Note: The general interest charge is worked out under Part IIA of the Taxation Administration Act 1953.

13 I observe that the operation of s. 172A is dependent upon the Commissioner having issued the taxpayer with an amended assessment.

14 Neither party in their submissions that were filed before the hearing referred to Subdiv. 67-L of the Income Tax (Transitional Provisions) Act 1997 (Cth.) (the “Transitional Act”), although it was mentioned in passing by the Commissioner at the hearing before me. That was regrettable. The Subdivision should not have only been raised in this lackadaisical way. That is because Subdiv. 67-L contained a specific set of transitional provisions addressing a taxpayer’s tax offset refunds for the 2012-2013 year of income. They empowered the Commissioner to issue a notice to a taxpayer ascertaining that taxpayer’s tax offset refunds in that year of income or specifying that the taxpayer was to get no refund in that year of income. Subdivision 67-L was introduced precisely because new s. 166 had prospective effect only (i.e. from the 2014 year of income onwards). It also included, amongst other things, provisions concerning the evidentiary effect of such a notice; a taxpayer’s entitlement to object against a notice; and the Commissioner’s ability to amend a notice. Critically, there was also a provision that deemed, in the case of self-assessment taxpayers, the Commissioner to have given a Subdiv. 67-L notice specifying the taxpayer’s tax offset refunds “in accordance with what the entity specified in the return.”

15 Also regrettable is the fact that the submissions filed before the hearing did not inform the Court that Subdiv. 67-L was repealed in April 2019 by the Treasury Laws Amendment (2018 Measures No. 4) Act 2019 (Cth.). This took place with effect before the s. 8AAZN notice discussed below was sent by the Commissioner in September 2019. Self-evidently, the Commissioner, finding himself in a bind with this taxpayer, sought to invoke s. 8AAZN in the face of the removal of Subdiv. 67-L. He now does so, for the reasons set out below, by – in effect – trying to jam a square peg into a round hole.

16 I accept that the Counsel appearing before me may not have known about this statutory history at this level of detail or perhaps may not have appreciated its significance (although the Commissioner’s Senior Counsel did expressly raise its existence at the trial). But the Commissioner, I infer, knew about it and had a duty to tell, through his Counsel, the Court about it in plain terms.

17 The Revised Explanatory Memorandum which accompanied the Bill that became the 2013 Amending Act (the “2013 Revised Explanatory Memorandum”), described the need for Subdiv. 67-L by reference to the fact that a “system” for assessments of tax refundable offsets would take “some time” to implement. There was thus a need for transitional rules. At paras. 6.39 to 6.43 the following is recorded:

Delayed application of the assessment and objection amendments

Changes will need to be made to the Australian Taxation Office’s systems to bring the calculation of the amount of a taxpayer’s refunds arising from refundable tax offsets into the assessment regime. As this will take some time to implement, the amendments to the assessment provisions only apply to assessments for the 2013-14 and later income years made on or after 1 July 2013. [Schedule 5, items 24 and 27]

For the period before the assessment provisions apply, taxpayers will receive a notice of the amount of their refund from refundable tax offsets. The calculation of the amount in the notice is not an assessment. However, taxpayers can object to the notice separately from their right to object to their normal income tax assessment. [Schedule 5, item 10, subsections 67-115(2) and 67-135(1) of the IT(TP)A 1997]

The objection must be lodged within the same period that the taxpayer could lodge an objection to an assessment for the relevant income year. If there is no notice of assessment for the year, the objection period is as long as the period would have been if notice of an assessment had been given on the date of the notice. [Schedule 5, item 10, subsection 67-135(3) of the IT(TP)A 1997]

The amendments empower the Commissioner to:

• provide taxpayers with a notice of the amount of their refund arising from refundable tax offsets; and

• include the notice in some other notice the Commissioner is providing the taxpayer (it would usually be included in the notice of assessment).

The Commissioner can provide the notice electronically if the taxpayer’s return is lodged electronically. [Schedule 5, item 10, section 67-100 of the IT(TP)A 1997]

The Commissioner is deemed to provide a notice, if the taxpayer is a full self-assessment entity, when the taxpayer lodges its return for the 2012-13 income year. The notice is deemed to specify the amount of the entity’s tax offset refunds in accordance with the return. [Schedule 5, item 10, section 67-105 of the IT(TP)A 1997]

18 Several provisions of former Subdiv. 67-L should be set out. The key operational provision was former s. 67-100 which provided:

Notices of total of tax offset refunds

(1) The Commissioner may at any time give you a notice specifying:

(a) the amount the Commissioner has ascertained as being the total of your tax offset refunds for the 2012-13 income year; or

(b) that the Commissioner has ascertained that you can get no such refunds for the 2012-13 income year.

Note: The total of your tax offset refunds for later income years is included in your assessment for those years: see Part IV of the Income Tax Assessment Act 1936.

(2) The notice may be included in any notice the Commissioner gives to you, including a notice of assessment.

(3) The Commissioner may give you the notice electronically if you are required to lodge, or have lodged, your income tax return for the income year electronically.

19 Former s. 67-105 dealt with self-assessment taxpayers, such as the taxpayer here. It provided:

Deemed notices

(1) This section applies if:

(a) an entity is a self-assessment entity for the 2012-13 income year; and

(b) the entity lodges its income tax return for the 2012-13 income year at a particular time; and

(c) just before that time, the Commissioner has not already given the entity a notice under section 67-100.

(2) The Commissioner is taken:

(a) to have ascertained, in accordance with what the entity specified in the return:

(i) an amount as being the total of the entity’s tax offset refunds for the income year; or

(ii) that the entity can get no such refunds for the income year; and

(b) to have given the entity a notice to that effect under section 67-100 on the day on which the entity lodges the return.

20 The effect of this provision here, until the repeal of Subdiv. 67-L, was that the Commissioner was taken to have given the taxpayer (a self-assessment taxpayer) a notice stating that the taxpayer’s refundable tax offsets for the 2013 year of income were as claimed by it in its return (see below).

21 Former s. 67-115 is also important (for reasons set out below) and is re-produced as follows:

Effect of notices

(1) Your entitlement to a tax offset refund, and the time by which the refund must be applied in accordance with Divisions 3 and 3A of Part IIB of the Taxation Administration Act 1953, do not depend on, and are not in any way affected by, the giving of a notice under this Subdivision.

(2) An ascertainment mentioned in subsection 67-100(1) is not an assessment for the purposes of the income tax law.

22 Finally, I note former s. 67-130 which provided:

Evidence

(1) The production of:

(a) a notice given under this Subdivision; or

(b) a document under the hand of the Commissioner, a Second Commissioner, or a Deputy Commissioner, purporting to be a copy of a notice given under this Subdivision;

is, except in proceedings under Part IVC of the Taxation Administration Act 1953 on a review or appeal relating to the notice, conclusive evidence that the notice was given and of the particulars in it.

(2) The production of a document under the hand of the Commissioner, a Second Commissioner, or a Deputy Commissioner, purporting to be a copy of or extract from a notice given under this Subdivision is evidence of the matters set out in the document to the same extent as the original would have been evidence of those matters.

The Facts

23 The facts were not in dispute.

24 The taxpayer is the head company of a consolidated group for the purposes of Pt. 3-90 of the 1997 Act. It is a self-assessment entity that acquired a company called Mungana Goldmines Ltd (“Mungana”) in November 2015. Strictly speaking, the events set out below that occurred before this time happened in respect of Mungana, but I follow the practice adopted by the parties and refer to the relevant entity throughout as the taxpayer for convenience. On 13 March 2014, it made an application to the Board to register a certain project carried out over the 2013 and 2014 years of income as constituting an R & D activity for the purposes of s. 27A of the I.R.D. Act. The nature of that project – described in the application as one to “develop new processes to enable the extraction and processing of highly complex, variable ores located in heavily oxidised and geochemically depleted geologies” (the “purported R & D project”) – is not in issue.

25 On 14 March 2014, the Board registered the purported R & D project as an R & D activity. The notice of registration, however, informed the taxpayer that the act of registration did not constitute an indication that the project had complied with the requirements of the I.R.D. Act. It said:

Registration of activities does not, by itself, render the activities described in this registration as eligible core or supporting R&D activities, nor is it an indication of compliance with the requirements of the R&D Tax Incentive. Determining the eligibility of activities under the R&D Tax Incentive is the responsibility of the R&D entity, under self-assessment.

After registration, [the Board] may examine a registration in detail and this may lead to a formal finding about the eligibility of all or some of the registered activities. Should this be necessary, you will be contacted to discuss this registration.

26 On or about 2 April 2014, the taxpayer lodged its income tax return for the 2013 year of income. The return included a claim for an R & D tax offset refund in the sum of $2,269,336.05 (the “tax refund”). The return disclosed that in that year the taxpayer had a taxable loss in the sum of $6,615,895 and recorded the carrying forward of tax losses in the sum of $27,826,815. A further claim of this nature was apparently made by the taxpayer in the year of income ended 30 June 2014.

27 On or about 6 May 2014 the Commissioner paid the tax refund to the taxpayer. Ms. King, a senior officer in the Australian Taxation Office (the “A.T.O.”), gave unchallenged evidence that:

(a) in order to obtain a refundable tax offset an entity must “self-assess” whether they are eligible to make that claim. What is then disclosed in the entity’s tax return is initially accepted by the A.T.O. usually without query or checking;

(b) as part of that self-assessment regime, an R & D claim is automatically processed in the tax system, unless something arises to trigger an alert;

(c) the A.T.O. maintains a computer database which includes the A.T.O. Integrated System (the “A.I.S.”) and the Integrated Core Processing System (the “I.C.P.”). These were described by Ms. King in the following way:

(a) AIS contains records of credit and debit account postings for taxpayers’ Activity Statement and Franking Deficit Tax Accounts including payments that were posted to the accounts up to and including 23 December 2019.

(b) ICP contains records of all liabilities, payments and credits for taxpayers’ Income Tax accounts. As a matter of practice within the ATO, the information recorded on ICP is input into the system either manually by employees of the ATO, based on information furnished to the ATO by a taxpayer through tax returns, or automatically if the taxpayer lodged returns electronically. Since 24 December 2019, the Activity Statement and Franking Deficit Tax accounts in AIS have been transitioned into ICP, so that all account postings including credit and debit postings in AIS are now in ICP.

(d) the A.T.O.’s system contained no record that any of the taxpayer’s R & D claims for the 2013 year (or the 2014 year) of income had been queried by the Commissioner when the tax return for that year (or the 2014 year) was submitted the taxpayer.

28 On or about 8 December 2014, the Board commenced a review of the purported R & D project. Following the completion of that review, the Board issued to the taxpayer on around 7 October 2016 a “Certificate of Finding” made pursuant to s. 27J of the I.R.D. Act (noting for completeness that the taxpayer had acquired Mungana by this time). It informed the taxpayer that none of the activities that comprised the project constituted core or supporting R & D activities. The taxpayer then sought internal review of this decision. Following a review, on 12 April 2017, the Board confirmed that the activities comprising the purported R & D project were not core or supporting R & D activities. The taxpayer then sought further review of that decision in the Administrative Appeals Tribunal. That application for review was discontinued by the taxpayer on or about 19 July 2019.

29 On or about 12 September 2019, the Commissioner issued the taxpayer with reasons for:

(a) the issue to the taxpayer of a notice pursuant to s. 8AAZN requiring the taxpayer to repay the tax refund for the 2013 year of income; and

(b) the amendment of the taxpayer’s 2014 income tax assessment to reduce the claimed R & D refundable tax offset in the 2014 year of income to nil. The correctness of that assessment was not in issue before me.

30 The reasons, amongst other things, stated as follows:

The definition of ‘assessment’ under sections 6 and 166 of the Income Tax Assessment Act 1936 (ITAA 1936) did not include tax offset refunds for the 2013 and earlier income years. The law was amended to include tax offset refunds in the definition of ‘assessment’ for the 2014 and later income years.

Section 8AAZN of the TAA allows the Commissioner to collect a debt that is due as a result of an administrative overpayment being made to a taxpayer. An administrative overpayment means an amount the Commissioner has paid to a person by mistake, being an amount to which the person is not entitled.

31 A notice was issued by the Commissioner to the taxpayer on or about 25 September 2019 purportedly pursuant to s. 8AAZN of the T.A.A. seeking repayment of the tax refund (the “Notice”). It was in the following form:

32 Thereafter, the Commissioner purportedly offset certain GST and fuel tax credits it owed the taxpayer, as claimed by the taxpayer in its September to December 2019 Business Activity Statements (“B.A.S.”), against the tax debt said to have been created by the Notice set out above. In this way, the tax refund was repaid to the Commissioner. The Commissioner also imposed on the taxpayer general interest charge (“G.I.C.”) in the sum of $26,028.

The Present Proceeding

33 The taxpayer commenced its proceedings for relief against the Commissioner under s. 39B of the Judiciary Act in October 2019. By an amended application it sought the following orders:

A. An order setting aside the Notice.

B. Further or alternatively to A, an order prohibiting the [Commissioner] from acting pursuant to, relying on or otherwise taking action founded in reliance on, the Notice or its purported substance.

C. Further or alternatively to paragraphs A and B, a declaration that the [Commissioner] is not entitled pursuant to s 8AAZN of the Taxation Administration Act 1953 to issue a notice to the [taxpayer] purporting to require [it] to pay an amount to the [Commissioner].

D. Further or alternatively to paragraphs A to C, an order compelling the [Commissioner] to refund to the [taxpayer]:

a) the GST credit and a Fuel Tax Credit totalling $716,892.00 arising from the lodgement of the September 2019 BAS; and

b) the GST credit and a Fuel Tax Credit totalling $737,473.00 arising from the lodgement of the October 2019 BAS,

respectively, against the amount of $2,269,336.05: or

c) the GST credit and the Fuel Tax Credit totalling $918,931.00 arising from the lodgement of the November 2019 BAS; and

d) the GST credit and a portion of a Fuel Tax Credit totalling $643,260.55 arising from the lodgement of the December 2019 BAS;

e) general interest charge in respect of outstanding balances in the [taxpayer’s] income tax account in the amount of $26,028.

E. Further or alternatively to paragraph D, a declaration that the [Commissioner] is not entitled pursuant to s 8AAZLB of the Taxation Administration Act 1953 to offset:

a) the GST credit and a Fuel Tax Credit totalling $716,892.00 arising from the lodgement of the September 2019 BAS; and

b) the GST credit and a Fuel Tax Credit totalling $737,473.00 arising from the lodgement of the October 2019 BAS,

respectively, against the amount of $2,269,336.05; or

c) the GST credit and the Fuel Tax Credit totalling $918,931.00 arising from the lodgement of the November 2019 BAS against the amount of $1,561,426.15; and

d) the GST credit and a portion of a Fuel Tax Credit totalling $643,260.55 arising from the lodgement of the December 2019 BAS against the amount of $643,260.55; and

e) general interest charge in respect of outstanding balances in the [taxpayer’s] income tax account in the amount of $26,028.

F. An order that the [Commissioner] pay the [taxpayer’s] costs of the proceeding, to be taxed in default of agreement.

G. Such other or further orders as the Court considers just or expedient.

34 The Commissioner did not object to the form of proceeding commenced by the taxpayer.

35 Whilst the prayer for relief appears to be complex, in reality there was only one issue of substance before me, namely whether the Commissioner could use his power in s. 8AAZN of the T.A.A. to recover the tax refund.

Submissions of the Parties

36 The taxpayer’s argument was simple. It focused on the text of the definition of “administrative overpayment” and the phrase “an amount that the Commissioner has paid to a person by mistake”. It said that the word “mistake” should bear its ordinary meaning. It referenced the 3rd edition of the Macquarie Concise Dictionary where that word is described as meaning “an error in action, opinion or judgment; a misconception or misapprehension”. According to the taxpayer the issue before me could be distilled neatly as follows:

The definition of “administrative overpayment” thus directs an enquiry as to whether the payment was the result of (occasioned by) a mistake. That enquiry is a factual one.

(Footnote omitted.)

37 Here, it was submitted, the tax refund was not paid by mistake. Rather, it was paid correctly in accordance with the claim made by the taxpayer in its return for the 2013 year of income pursuant to the self-assessment regime. The only relevant impediment to the valid making of that claim was registration of the purported R & D project by the Board. But that had taken place in March 2014 and that registration remained in place when the Commissioner “automatically”, to use the language of Ms. King, paid the taxpayer.

38 The taxpayer also emphasised the word “by” in the definition of “administrative overpayment.” It submitted that the overpayment must have occurred “by mistake” in order to fall within that definition. In other words, the overpayment must have been caused by a mistake which was present when the overpayment was made. The taxpayer also submitted that the type of error which was causative of the overpayment needed to be administrative in nature. An example of such a mistake was said to be a payment to the wrong person.

39 The taxpayer submitted that it would be wrong to rely upon the events which had occurred after 2014 – namely, the Board’s findings made pursuant to s. 27J of the I.R.D. Act – as evidence of an earlier mistake. The Commissioner was not entitled, it was said, to reason post hoc ergo propter hoc from those events.

40 The taxpayer also contended that permitting the Commissioner to recover the tax refund in reliance upon s. 8AAZN would undermine the two-year time limit for the amendment of assessments to which the Commissioner is subject in s. 355-710(2), as set out above. It would also have the effect of ignoring the lack of any reference to refundable tax offsets in s. 166 as it was in 2013.

41 The Commissioner disagreed. He submitted that the payment had occurred by mistake because it has transpired that the taxpayer was not entitled in 2013 to the R & D tax offset. Registration pursuant to s. 27A of the I.R.D. Act did not mean that the taxpayer’s purported R & D project had complied with that Act. Rather, it has since been shown that its project did not comprise core or supporting R & D activities by the issue of the findings made by the Board pursuant to s. 27J of the I.R.D. Act. Those findings are no longer disputed by the taxpayer. It does not deny that it was not entitled to the tax offset. In that respect, the Commissioner emphasised the phrase “being an amount to which the person is not entitled” in the definition of “administrative overpayment.” He also submitted that the word mistake simply meant an “erroneous belief.” For that proposition he cited an English Court of Appeal decision about contractual mistake: Great Peace Shipping Ltd v. Tsavliris Salvage (International) Ltd [2003] Q.B. 679.

42 The Commissioner also submitted that even without s. 8AAZN he would in any event have been entitled to repayment of the tax refund in accordance with common law principles of restitution. He cited Commonwealth v. Davis Samuel Pty Ltd (No. 7) [2013] ACTSC 146; (2013) 95 A.C.S.R. 258 and Nurdin & Peacock Plc v. D B Ramsden & Co Ltd [1999] 1 W.L.R. 1249. He also referred to the following statement in the Explanatory Memorandum which accompanied the Bill which became the Taxation Laws Amendment Act (No.3) 1999 (Cth.) (the “1999 Explanatory Memorandum”):

Other consequential amendments are also necessary to support the above measures. For example, the new general interest charge will become tax deductible. Further, debts which currently arise as a result of administrative overpayments by the Commissioner of Taxation will become tax debts and will be subject to the new general interest charge. This amendment is necessary to ensure the new running balance accounts will register debts payable to the Commissioner of Taxation.

(Emphasis added.)

43 Relying on the foregoing passage, the Commissioner submitted that s. 8AAZN was simply a statutory re-enactment of his general common law right of recovery for mistaken payments. The section should, it was said, be read in conformity with that common law right.

44 The Commissioner also relied upon the headings to Pt. IIB of the T.A.A., the heading to Div. 4 of Pt. IIB and the heading to s. 8AAZN. For convenience they are as follows:

Running Balance Accounts, Application of Payments and Credits, and Related Matters

Miscellaneous provisions about tax debts

Overpayments made by the Commissioner under taxation laws

45 These headings were said to support the proposition that s. 8AAZN was not to be construed as limited to overpayments arising from the administration of an R.B.A.

46 The Commissioner also contended that his submission was supported by a decision of the Queensland Supreme Court. In Deputy Commissioner of Taxation v. Price [2010] QSC 196; (2010) 79 A.T.R. 137, the Commissioner sought to recover refunds arising from an incorrect claiming of certain input tax credits. The Commissioner had issued amended assessments to recover the amounts owing. For reasons which do not, with respect, appear clear to me, the Commissioner in Price also relied upon s. 8AAZN of the T.A.A. Lyons J. decided that this provision authorised the Commissioner to recover the overpaid refund. His Honour said at 142 [18]:

The result, therefore, is that the defendant was not entitled to the amounts paid to him on 23 May and 22 July 2005. The only sensible inference which can be drawn from the history which appears in the material relied on in the application is that the amounts then paid were paid on the mistaken basis that the defendant was entitled to them. That the basis was mistaken is demonstrated by the variation assessments. It is unnecessary to consider whether the mistake was a mistake of fact, or a mistake of law; a payment can be made by mistake in either case, and s 8AAZN does not limit its operation to either kind of mistake. It seems to me, therefore, that each of those payments was made by mistake, to a person not entitled to them; and each is an “administrative overpayment” for the purposes of s 8AAZN of the TAA.

(Footnote omitted.)

47 I note that Price was an application for summary judgment; there was no appearance by the taxpayer.

48 The Commissioner further submitted that the onus was on the taxpayer to show that it was entitled to the tax offset refund in the 2013 year of income. This it could not do. The Commissioner had paid the tax refund on the assumption, applicable under the self-assessment regime, that the taxpayer’s claim was correct. That assumption was mistaken. The taxpayer’s purported R & D project was not entitled to be registered under the I.R.D. Act. It followed that the taxpayer, it was said, could not show that the Commissioner’s assumption was correct or not erroneous.

49 In oral argument the taxpayer denied that the tax refund had been paid based upon a mistaken assumption. That was because the Commissioner had simply not made any assumption in making that payment. Rather, the payment had been made automatically pursuant to the self-assessment regime. The evidence of Ms. King, set out above, in my view supports that contention.

50 In that respect, in oral argument, the Commissioner’s Senior Counsel submitted that his client did not just rely upon the fact of the finding subsequently made by the Board in 2017 pursuant to s. 27J of the I.R.D. Act. He contended that the “mistake” which caused the overpayment was present when the tax refund was paid. That mistake was the taxpayer’s claim for an R & D refundable tax offset as set out in its tax return. The claim was mistaken because the taxpayer now concedes that it was not carrying out core or supporting R & D activities. The Commissioner again pointed out that the taxpayer had not shown that this claim was not mistaken.

51 The Commissioner also submitted, in oral argument, that his application of s. 8AAZN was not inconsistent with the temporal limitations imposed specifically by s. 355-710 of the 1997 Act and more generally by s. 170 of the 1936 Act. The Notice was not an assessment; it was a statement evidencing the taxpayer’s state of indebtedness to the Commissioner. There is no time limit, it was said, on the Commissioner’s lawful capacity to recover amounts owed to him. The Commissioner referred the Court to Deputy Commissioner of Taxation v. Moorebank Pty Ltd (1988) 165 C.L.R. 55.

52 In its reply submissions, the taxpayer observed that the availability of common law remedies was irrelevant to the task of construing the definition of “administrative overpayment.” It relied upon the description of s. 8AAZN as found in the 1999 Explanatory Memorandum where that provision was said to have introduced tax debts for “administrative errors” (at page 25). This was said to be the only explanation of the defined term “administrative overpayment” in that extrinsic material. It followed, it was submitted, that “administrative errors” were errors “of or pertaining to administration.”

53 The taxpayer also submitted in reply that the decision of Price was distinguishable because the “mistake” in that case arose from the conclusive effect of the assessments that had been issued. Further, the Commissioner’s case concerning the onus cast upon the taxpayer was misconceived. The taxpayer did not need to show that it was entitled to the R & D tax offset in the 2013 year of income. The sole question was whether at the time the tax refund was paid, it could be said that it had been paid by mistake. When the taxpayer’s tax return was lodged, it was contended, the Commissioner was relevantly taken, by reason of s. 166A(3), to have made an assessment that it had no taxable income and that no tax was payable “in accordance with what the taxpayer specified in the return.”

54 Reference was also made to s. 27L of the I.R.D. Act by both parties. As I understood it, the Commissioner relied upon this provision for the proposition that following the findings made in 2017 by the Board pursuant to s. 27J, it was always the case that the purported R & D project had never been properly registered, and had never been capable of being registered under s. 27A. In contrast, the taxpayer submitted that the application of this deeming provision from 2017, could not affect the answer to the factual question about whether the tax refund had been paid by mistake in 2014. That issue needed to be determined by reference to the facts applicable in that year.

55 Following the hearing of this matter, by direction of the Court, the parties filed written submissions concerning Subdiv. 67-L of the Transitional Act. The Court is grateful to both the taxpayer and the Commissioner for this assistance.

56 Both parties agreed that Subdiv. 67-L was a specific regime permitting the Commissioner to issue a notice specifying the total of a taxpayer’s tax offset refunds for the 2012-2013 year of income or which specified that the taxpayer was to get no such refund in that year. The parties also agreed that this Subdivision was repealed prior to the issue of the Notice sent to the taxpayer in this proceeding. The parties were otherwise in disagreement.

57 The taxpayer relied upon ss. 67-100 and 67-115, set out above, for the proposition that a notice sent by the Commissioner under Subdiv. 67-L was not an assessment and could not affect a taxpayer’s entitlement to a tax refund. Nor could such a notice create a liability to repay any refund. That is because no provision of Subdiv. 67-L is listed in s. 250-10 of Sch. 1 to the T.A.A. as a tax-related liability which the Commissioner may recover. Section 250-10 contains tables which comprise in each case an “index of each tax-related liability” under the 1936 Act and “other Acts.” The taxpayer also submitted that because it was a self-assessment taxpayer during the period in which Subdiv. 67-L operated, the Commissioner was taken to have issued a notice to it stating that it was entitled to a tax offset refund in the sum of $2,269,336.05. This deemed notice was otherwise said to have no significance for the purpose of a consideration of the Notice issued here.

58 The Commissioner submitted that the provisions of Subdiv. 67-L were irrelevant to the correct construction of s. 8AAZN and the word “mistake” as used in that provision. That is because Subdiv. 67-L was enacted well after the introduction of Pt. IIB of the T.A.A. Nor, during the period of its operation, would it have been correct to read down s. 8AAZN because of the presence of a specific regime for dealing with tax offsets. That is because Subdiv. 67-L conferred no specific power on the Commissioner: c.f. Anthony Hordern & Sons Ltd v. Amalgamated Clothing & Allied Trades Union of Australia (1932) 47 C.L.R. 1 at 7.

59 I finally observe that the parties agreed that the only issue the Court needed to determine was the application of s. 8AAZN. It did not need to consider further whether the Commissioner was also authorised to set off the various GST and fuel tax credits owed to the taxpayer. The parties informed the Court that if I were to decide that s. 8AAZN did not allow the Commissioner to recover the tax refund, the parties would seek to agree upon the form of final relief. I am grateful to the parties for their co-operation.

Disposition

60 This case, in substance, turns upon whether the Commissioner can properly use s. 8AAZN to resolve his problem of recovering refunds of tax paid pursuant to the claiming of refundable tax offsets prior to 1 July 2013 which have been subsequently found to have been excessive. In other words, can it be used in addition to the specific power of recovery now conferred by s. 172A of the 1936 Act? That problem exists only in respect of the period following the repeal of Subdiv. 67-L of the Transitional Act. It also exists here because the taxpayer had substantial losses in the 2013 year of income; the Commissioner could not recover the tax refund by the issue of an amended assessment.

61 A number of observations should be made.

62 First, the taxpayer expressly conceded that it was not entitled, as a matter of the application of the I.R.D. Act and Div. 355 of the 1997 Act to the facts as they existed in the 2013 year of income, to the R & D refundable tax offset it claimed in its return for that year. It nonetheless seeks to keep the tax refund. It does so, not because of some underlying principle or policy which might support that outcome. Rather, it simply seeks to take advantage of the drafting deficiencies in s. 166 before it was amended. In my view, a taxpayer is entitled to take such a point against the state and thereby reap a windfall gain, if the provisions permit it to do so.

63 Secondly, at least during the 2013 year of income, the ordinary way in which the Commissioner might seek to recover a tax debt was to sue on the basis of the issue of an assessment or amended assessment which created that liability (although see also s. 8AAZH below). The presence of s. 350-10 in Sch. 1 of the T.A.A. (formerly expressed in s. 177 of the 1936 Act) facilitated that means of recovery. For reasons already given, it was not possible here for the Commissioner to amend the taxpayer’s assessment in the 2013 year of income to recover the tax refund.

64 Thirdly, the inability to recover the tax refund paid here to the taxpayer through the process of assessment or amended assessment was more generally resolved by Parliament passing the 2013 Amending Act, which did two things:

(a) it substituted s. 166 with a new provision which permits the Commissioner to make an assessment of the total of a taxpayer’s tax offset refunds (or that the taxpayer can get no such refunds). This change, however, had only prospective effect from the 2014 year of income. According to the 2013 Revised Explanatory Memorandum, this was due to the need to make changes to the A.T.O.’s “systems”; and

(b) it introduced Subdiv. 67-L into the Transitional Act to deal specifically with the claiming of refundable tax offsets for the 2012-13 year of income. The Commissioner never exercised the powers conferred upon him by this Subdivision prior to its repeal in 2019.

The Commissioner’s reliance upon s. 8AAZN should be considered in that statutory context.

65 Fourthly, I respectfully accept the taxpayer’s submission that the presence of the phrase “by mistake” requires the presence of a mistake which is the activating cause of the overpayment for it to be an “administrative overpayment” as defined by s. 8AAZN. Inferentially, it must be a mistake made by or imputed to the Commissioner. That is because he is the person who has made the relevant overpayment.

66 Fifthly, s. 8AAZN is found within Pt. IIB of the T.A.A. Whilst perhaps not exclusively devoted to the creation and maintenance of R.B.A.s, in substance, that is the context in which s. 8AAZN is to be construed. Indeed, at para. 1.122 of the 1999 Explanatory Memorandum, s. 8AAZN is described as a consequential amendment which was “necessary to support the introduction of RBAs”. In that respect, it is noteworthy that Pt. IIB creates a power of recovery which is additional to the process of assessment and amended assessment. It is contained in s. 8AAZH which is in the following terms:

Liability for RBA deficit debt

(1) If there is an RBA deficit debt on an RBA at the end of a day, the tax debtor is liable to pay to the Commonwealth the amount of the debt. The amount is due and payable at the end of that day.

Note: For provisions about collection and recovery of the amount, see Part 4-15 in Schedule 1.

(2) If there are several tax debtors, their liability for the debt is of the same kind as their liability for the tax debts that were allocated to the RBA.

Example: If the tax debtors are jointly and severally liable for the tax debts that were allocated to the RBA, they will also be jointly and severally liable for the RBA deficit debt.

67 Where a taxpayer makes an incorrect claim for a deduction or offset, or fails to include an amount of assessable income in its return, the error is capable of correction by assessment and the Commissioner may collect the tax thereby arising by suing on that assessment or by relying upon s. 8AAZH. In the case of an incorrectly paid refund arising from an excessive claim for a tax offset, there is now an express power conferred on the Commissioner to amend the taxpayer’s assessment and an express power, conferred by s. 172A of the 1936 Act, to recover the overpayment as a debt due to the Commonwealth. In that specific statutory context, and in my view, the type of “mistake” which s. 8AAZN is directed at, is not an incorrect claim made in a return about a deduction, offset or amount of assessable income.

68 More particularly here, s. 8AAZN is not apt to permit the Commissioner to recover the tax refund paid to the taxpayer, given the existence of former Subdiv. 67-L of the Transitional Act and current s. 172A of the 1936 Act. The Commissioner should have used the mechanism created by that former Subdivision to recover the tax refund. No explanation was given to the Court as to why he had not done so. In that respect, during the period of its operation I do not, with great respect, accept that the principle from Anthony Horden would not have applied to read down s. 8AAZN if it had been necessary to do so. The Commissioner conceded that it was a “specific regime”. In that respect, whether that regime did or did not confer a “power” on the Commissioner, the principle that specific positive words used in a provision may justify a field of exclusive operation is well known: Minister for Immigration and Multicultural and Indigenous Affairs v. Nystrom (2006) 228 C.L.R. 566.

69 I also do not, with great respect, accept the taxpayer’s proposition that a notice issued pursuant to Subdiv. 67-L would have done no more than specify the amount of a tax offset refund and would not have authorised recovery of an incorrectly claimed refund. It is true that such a notice is not an assessment; it is also true that it is not listed as a tax-related liability in s. 250-10 of Sch. 1 to the T.A.A. But the presence of a conclusive evidence provision in s. 67-130 would have no work to do, if the Commissioner could not recover an overpaid refund in accordance with the issue of a notice pursuant to s. 67-100. If it were necessary to do so, in such circumstances, the existence of a statutory power of recovery would be implied.

70 There is otherwise strength in the Commissioner’s contention that the ambit of s. 8AAZN should not be affected by the temporary presence of Subdiv. 67-L, which was enacted years after Pt. IIB of the T.A.A. In Prebble v. Commissioner of Taxation (2003) 131 F.C.R. 130 both parties sought to interpret a provision of the 1936 Act, which had been introduced in 1964, by reference to other provisions and amendments enacted subsequently. Hill and Hely JJ. decided that these other provisions and amendments were of no assistance. At 142 [52] their Honours said:

It is impossible to see that these amendments could affect the interpretation of sections which were unaffected by the amendments. … At most they might indicate Parliament’s understanding of the law as at the time of the amendments, which could be right or wrong.

71 However, in 2013 Parliament plainly considered that it needed to enact Subdiv. 67-L to permit, amongst other things, the recovery of incorrectly claimed refundable tax offsets. On this occasion, for the reasons contained in this judgment, Parliament’s understanding of the law was correct.

72 Finally, if the Commissioner is correct in his broad interpretation of s. 8AAZN, current s. 172A(2) would be rendered otiose – a result which would directly conflict with the well-established principle of statutory construction articulated in Project Blue Sky Inc v. Australian Broadcasting Authority (1998) 194 C.L.R. 355 at 382 [71].

73 It follows that, in my view, the type of “mistake” s. 8AAZN is directed at are mistakes made in the administration of an R.B.A. They would include, for example, a payment to the wrong person; a payment arising from a misallocation of tax debts; or a payment arising from computer error. Such errors, essentially administrative or procedural in nature, may be corrected by the Commissioner issuing a notice under s. 8AAZN. Whether it is, or is not, open now for the Commissioner to recover the tax refund using common law restitutionary principles is not a matter about which I need to express any view.

74 Sixthly, in reaching that conclusion, I have not been influenced by the choice of the word “administrative” in the defined term “administrative overpayment”. In Esso Australia Resources Pty Ltd v. Federal Commissioner of Taxation (2011) 199 F.C.R. 226, the Full Court of this Court considered whether the use of the word “marketable” in the defined term “marketable petroleum commodity”, as found in the Petroleum Resource Rent Tax Assessment Act 1987 (Cth.), could influence the meaning of that definition. The taxpayer contended that it could not. That contention was summarised at 256 [100] as follows:

The burden of the co-venturers’ argument is that the manner in which the expression “marketable petroleum commodity” had been defined means that the petroleum products in question did not need to be “marketable”, that is, readily saleable. Because the definition has this consequence, it is illegitimate to have regard to the word “marketable” in construing the definition.

75 The Full Court accepted that contention at 257 [102]-[103] as follows:

The principle contended for by the co-venturers does, however, appear to be the established law of this country. “It would be quite circular to construe the words of a definition by reference to the term defined”: Owners of Shin Kobe Maru v Empire Shipping Co Inc (1994) 181 CLR 404 at 419 (Shin Kobe Maru). For that proposition the High Court cited Wacal Developments Pty Ltd v Realty Developments Pty Ltd (1978) 140 CLR 503 (Wacal). It is true that in Wacal Gibbs J declined to allow the term defined in that case – “instalment contract” – to be used as aid to the construction of the associated definition (“[w]ith all respect it is impermissible to construe a definition by reference to the term defined” (at 507)). But it may be doubted whether Wacal established anything so broad as the larger proposition that the term defined may not be used to resolve antecedent ambiguity in the definition. At least two members of the bench in Wacal thought that there was no ambiguity in the definition at all which required resolution. Stephen J thought that “[n]o doctrine of interpretation justifies, in the present circumstances, any departure from what I regard as the ordinary meaning of the legislature’s words” (at 513) and Murphy J thought that there “hardly seems to be any room for ambiguity” (at 522). It is difficult to discern from Wacal a ratio decidendi that requires abstention from the reference to the term defined as a device for resolving ambiguity in a definition for the case did not present that issue.

Nevertheless, Shin Kobe Maru does seem to establish that principle. There the question was whether the expression “a claim … relating to … ownership” in s 4(2)(a) of the Admiralty Act 1988 (Cth) extended to a claim to enforce an agreement that ownership in a vessel be transferred to a third party. The term defined was “proprietary maritime claim”. The passage already cited from Shin Kobe Maru shows that the Court held that the word “proprietary” could not be used as an interpretative aid in construing the definition (at 419). That would seem to close the question in Australia.

76 Nonetheless, given the statutory context, and given the passages I have referred to from the 1999 Explanatory Memorandum, the type of mistake covered by s. 8AAZN is likely to be procedural in nature arising out of some error in the maintenance of a taxpayer’s R.B.A.

77 Seventhly, I am unable, very respectfully, to agree with the Commissioner’s submission that the “mistake” which activated the overpayment was the wrong claim made by the taxpayer for a refundable tax offset. For the reasons I have already expressed, that is not the type of “mistake” with which s. 8AAZN is concerned. Nor is it a mistake made by the Commissioner.

78 Eighthly, my conclusion is, to some extent, supported by the temporal limitations on the Commissioner’s power of assessment in s. 355-710. Leaving aside the law applicable to the 2013 year of income, presently the Commissioner’s power to recover a refund arising from an incorrectly claimed tax offset would appear to be premised on the issue by him of an assessment or amended assessment which reduces that claimed tax offset. This is the effect of s. 172A (set out above). If the Commissioner’s submission here concerning the scope of operation of s. 8AAZN were to be accepted, the temporal limitation contained in s. 355-710, and engaged by s. 172A, could be entirely avoided.

79 Ninthly, I do not very respectfully think that Lyons J.’s observations in Price compel any contrary conclusion. As I have already pointed out, that was a case where the Commissioner sought summary judgment and where the taxpayer had failed to make any appearance. Moreover, his Honour did not have the benefit of the submissions made to me by Counsel for the taxpayer.

80 Tenthly, I do not think that s. 27L of the I.R.D. Act justifies a different conclusion. Section 27L is a deeming provision. It operates concordantly with s. 355-705 of the 1997 Act to effect, amongst other things, a conclusion about the operation of Div. 355 to a taxpayer. But it cannot alter the taxable facts as they existed at the time the tax refund was paid in 2014. If at that time the taxpayer, as a fact, was not paid the tax refund by mistake, s. 27L cannot operate to reverse that reality.

Conclusion

81 For the foregoing reasons, in my respectful view, the Commissioner was not authorised to apply s. 8AAZN to recover the tax refund. I will give the parties 14 days within which to agree upon the form of final relief, or failing that, to supply short submissions on that issue to the Court.

Postscript

82 Following the hearing of this matter, the parties drew to the Court’s attention a contention made by the Commissioner in written correspondence between him and the taxpayer that post-dated the hearing. Most regrettably, that contention was not pleaded by the Commissioner, nor was it made in his submissions or otherwise raised by him at the hearing before me. The contention was that, if I were to find in favour of the taxpayer, the Commissioner would nevertheless refuse to recognise that the taxpayer was entitled to keep the tax refund because he was also authorised by s. 15C of T.A.A. to recover it. Section 15C provides:

Recoverable Payments

(1) If, apart from this subsection, the Commissioner does not have power under a taxation law to pay an amount (the relevant amount) to a person (the recipient) purportedly as an amount to which the recipient is entitled to under a taxation law, then the Commissioner may pay the relevant amount to the recipient.

Recovery

(2) If a payment is made under subsection (1) to the recipient, the relevant amount:

(a) is a debt due to the Commonwealth by the recipient; and

(b) is payable to the Commissioner; and

(c) may be recovered in a court of competent jurisdiction by the Commissioner, or by a Deputy Commissioner, suing in his or her official name.

(3) If:

(a) a payment is made under subsection (1) to the recipient; and

(b) an amount is payable to the recipient by the Commonwealth under a taxation law (the Commonwealth liability);

then:

(c) the relevant amount; or

(d) such part of the relevant amount as the Commissioner determines;

may, if the Commissioner so directs, be recovered by deduction from the Commonwealth liability.

(4) For the purposes of a designated recovery provision, in determining whether an amount is payable, disregard subsection (1) of this section.

(5) If the relevant amount is recovered under a designated recovery provision, the relevant amount cannot be recovered under subsection (2) or (3) of this section.

(6) If the relevant amount is recovered under subsection (2) or (3) of this section, the relevant amount cannot be recovered under a designated recovery provision.

(7) Except as provided by subsection (6), subsection (3) does not limit Part IIB.

Designated recovery provisions

(8) For the purposes of this section, each of the following provisions is a designated recovery provision:

(a) section 8AAZN of this Act;

(b) section 70 of the Superannuation Guarantee (Administration) Act 1992;

(d) section 24 of the Superannuation (Government Co-contribution for Low Income Earners) Act 2003;

(e) a similar provision of a taxation law.

(9) For the purposes of a designated recovery provision, in determining:

(a) whether a person is entitled to an amount; or

(b) whether an amount is payable;

disregard subsection (1).

83 Except in the most exceptional circumstances, the policy in favour of finality of litigation does not permit a party to raise new points following the hearing. In this regard I rely on the well-known remarks of McHugh J. in Eastman v. Director of Public Prosecutions (A.C.T.) (2003) 214 C.L.R. 318 at 330 [29]-[31]:

Parties to matters before the Court need to understand that, once a hearing in the Court has concluded, only in very exceptional circumstances, if at all, will the Court later give leave to a party to supplement submissions. Parties have a legal right to present their arguments at the hearing. If a new point arises at the hearing, the Court will usually give leave to the parties to file further written submissions within a short period of the hearing — ordinarily seven to fourteen days. But a party has no legal right to continue to put submissions to the Court after the hearing. In so far as the rules of natural justice require that a party be given an opportunity to put his or her case, that opportunity is given at the hearing.

This is not the first time that this Court has had to emphasise that the hearing is the time and place to present arguments. In Carr v Finance Corporation of Australia Ltd [No 1], Mason J said:

“The material was submitted without leave having been given by the Court. The impression, unfortunately abroad, that parties may file supplementary written material after the conclusion of oral argument, without leave having been given beforehand, is quite misconceived. We have to say once again, firmly and clearly, that the hearing is the time and place to present argument, whether it be wholly oral or oral argument supplemented by written submissions.”

Once the hearing has concluded, the workload of the Court makes it impossible for the Court to give leave to file further submissions — with all the attendant delay in the Court's business by a fresh round of submissions. Efficiency requires that the despatch of the Court’s business not be delayed by further submissions reflecting the afterthoughts of a party or — as perhaps is the case in this appeal — some dissatisfaction with the arguments of the party's counsel.

(Footnote omitted.)

84 In my view, even though the tax legislation of the Commonwealth is oppressively complex, and parties can make mistakes, they nonetheless should not be permitted to continue to raise further argument once a final hearing has taken place, save in exceptional circumstances. Those circumstances do not exist here. The Commissioner had a full opportunity to present his case, and he was represented by leading Counsel and junior Counsel. He should not now be permitted to raise s. 15C to defeat the benefit of the taxpayer’s win. Nor can he, once final relief has been entered, avoid the consequences of that relief as between himself and the taxpayer here. Save for his right of appeal, he has no lawful capacity to re-open the subject matter of this litigation simply because he has found a new section he had overlooked. It is clear that the doctrine of res judicata applies to him: Chamberlain v. Deputy Commissioner of Taxation (1988) 164 C.L.R. 502.

85 If the Commissioner wishes now to rely on s. 15C, he should be limited to seeking leave to do so on any appeal from this decision. It will be a matter for a Full Court to determine whether to grant such leave. In my view, based on the case before me, the taxpayer has established an entitlement to keep the tax refund, and the form of final relief agreed on by the parties should reflect this fact. The form of final relief should not reflect any additional points on which the Commissioner now wishes to rely afresh, such as s. 15C, to deny the taxpayer’s entitlement to the tax refund.

I certify that the preceding eighty-five (85) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Steward. |

Associate: