FEDERAL COURT OF AUSTRALIA

Brecher v Barrack Investments Pty Limited (No 2) [2020] FCA 911

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The application be dismissed.

2. The cross-claim be dismissed.

3. Unless any party applies within 7 days for a different order as to costs:

a. the applicants pay the respondents’ costs of the application, and

b. the cross-claimants pay the cross-respondents’ costs of the cross-claim.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

THAWLEY J:

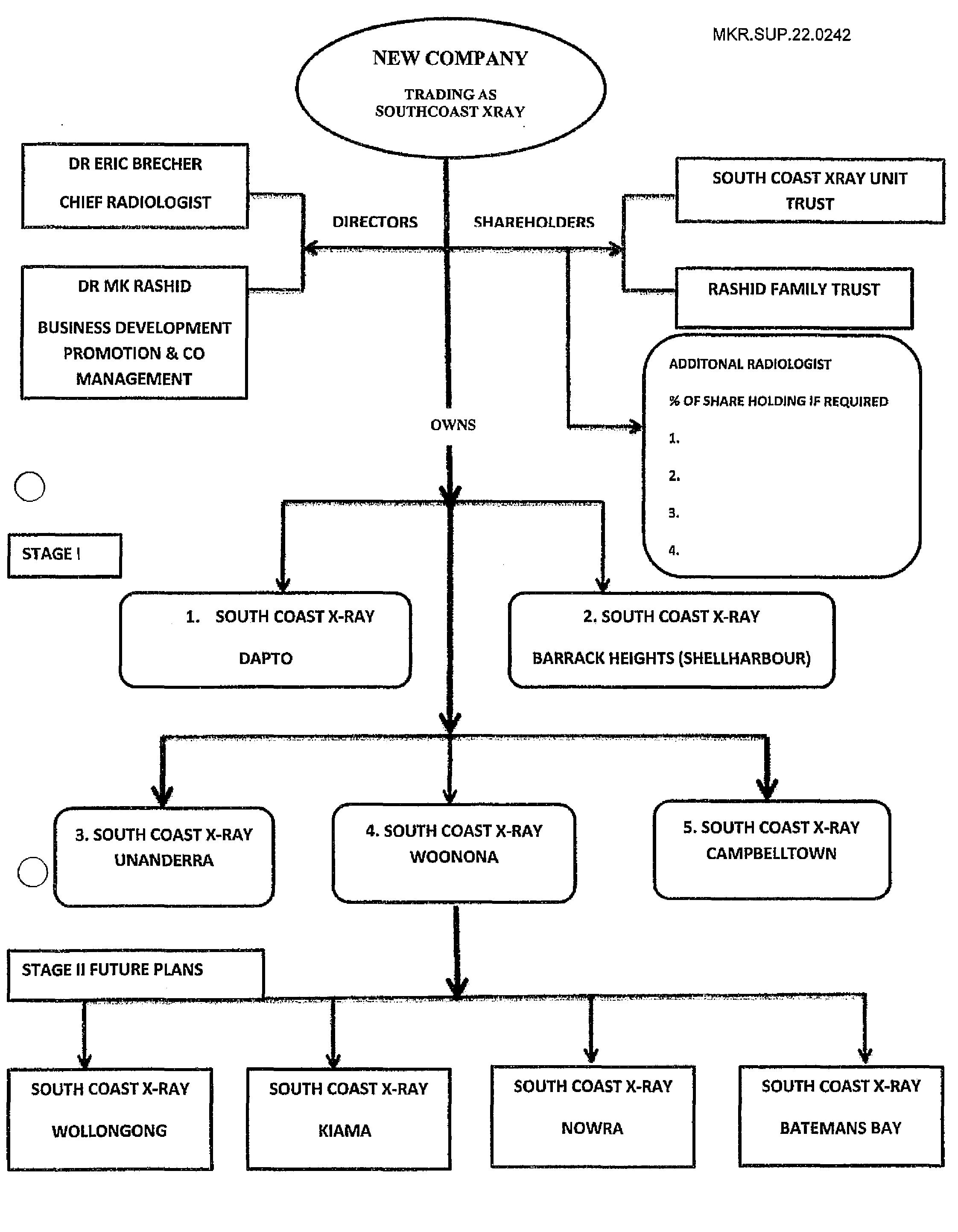

1 On 15 October 2015, Dr Brecher and Dr Rashid executed four documents at the offices of Acorn Lawyers (SCMI transaction documents, giving effect to the SCMI transaction). These four documents marked the commencement of an unsuccessful venture through the vehicle South Coast Medical Imaging Pty Ltd (in liquidation) (ACN 608 363 140) as trustee for the South Coast Medical Imaging Unit Trust (SCMI). The venture involved the merger of Dr Brecher’s existing radiology practice at Dapto (SCXR Dapto) with a new radiology practice (Barrack Heights practice) to be opened at Centre Health Complex Barrack Heights (Barrack Heights or CHC Barrack Heights) in a building which was owned by a company associated with Dr Rashid, Barrack Investments Pty Ltd.

2 SCMI’s new radiology practice at Barrack Heights commenced providing full services on or about 6 April 2016, having been handed over to SCMI on 15 February 2016. It was located in an area of CHC Barrack Heights which, after 15 October 2015, was fitted-out for the purpose by Delbest Pty Ltd, another company associated with Dr Rashid.

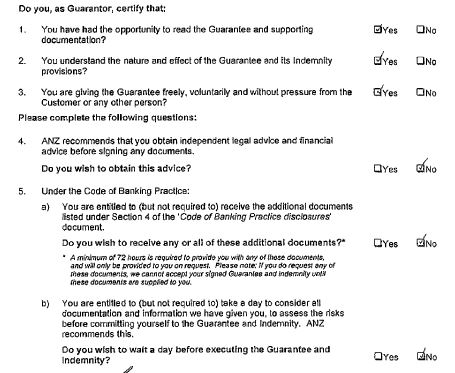

3 Funding for SCMI was sourced mainly from the Australia and New Zealand Banking Group Limited (ANZ) which advanced approximately $1.6 million. Dr Rashid and Dr Brecher executed guarantees and indemnities in favour of ANZ (ANZ Guarantee).

4 SCMI did not generate sufficient revenue. On 3 July 2017, an administrator was appointed. On 9 April 2018, it went into liquidation.

5 The witnesses’ accounts of what occurred at the meeting on 15 October 2015 were starkly at odds with each other.

6 On Dr Brecher’s case, Mr Ashutosh Agarwal of Acorn Lawyers, whom Dr Brecher had never met before, told him that: Acorn Lawyers acted for him and his company; the new business to be conducted by SCMI would generate $5,000,000 in the first year, $7,500,000 in the second year and $10,000,000 in the third year; Dr Rashid was a very important businessman in the region; and Dr Brecher should immediately execute the transaction documents, drafts of which had only just been completed, before Dr Rashid left overseas the next day.

7 Dr Rashid’s case was that Acorn Lawyers acted for SCMI only and that Mr Agarwal never represented otherwise. His case was that Mr Agarwal recommended that the SCMI transaction documents not be executed on the day and that Dr Brecher obtain independent legal advice. Dr Rashid denied that Mr Agarwal made any projections regarding SCMI’s revenue as asserted by Dr Brecher. Dr Rashid’s account was supported by the account given by Mr Agarwal.

8 The parties proceeded on the basis that someone was being untruthful about what was said at the meeting; the differing accounts were unlikely to be explained by faulty recollections.

9 By the SCMI transaction documents executed on 15 October 2015, SCXR Dapto was “rolled into” SCMI. Dr Brecher had purchased SCXR Dapto on 31 March 2014 for $2.5 million. Dr Brecher contended that he gave up his interest in SCXR Dapto for no or inadequate consideration. Dr Brecher also contended that he was unaware that the new radiology practice at Barrack Heights would be renting its premises from a company associated with Dr Rashid, Barrack Investments. He also contended that, when entering into the SCMI transaction, he did not know that the fit-out for the new premises was to be conducted by a second company associated with Dr Rashid, Delbest.

10 The events of 15 October 2015 must be examined in light of what occurred before that day. Dr Brecher and Dr Rashid had a number of discussions leading to them entering into the SCMI transaction. Dr Brecher contended that Dr Rashid made a number of misrepresentations in these discussions. He contended that he entered into the SCMI transaction in reliance on these misrepresentations.

11 By a cross-claim, Dr Rashid reciprocated by alleging that Dr Brecher had made a number of misrepresentations during discussions which occurred before 15 October 2015. The various alleged misrepresentations are addressed in more detail later in these reasons. Dr Rashid’s cross-claim also alleged that Dr Brecher had engaged in misleading or deceptive conduct in causing to be provided to Dr Rashid an inaccurate profit and loss statement and balance sheet concerning SCXR Dapto. Dr Rashid contended that he would not have entered into the SCMI transaction had he known the true financial position of SCXR Dapto. Amongst other losses claimed, Dr Rashid claimed that Barrack Investments would have leased an area at CHC Barrack Heights (Radiology Area) to a third party for the purpose of opening a radiology practice.

12 Dr Rashid also contended that, after the SCMI transaction had been entered into on 15 October 2015, Dr Brecher engaged in business and earned fees in breach of one of the SCMI transaction documents.

13 Dr Brecher had also made a series of claims against Acorn Lawyers. These claims were settled between the relevant parties during the hearing.

14 For the reasons which follow, each of the claims brought by Dr Brecher (and his interests) and each of the cross-claims brought by Dr Rashid (and his interests) are not made out and must be dismissed.

B.1 Dr Brecher and associated entities

15 The first applicant is Dr Eric Brecher (Dr Brecher). The second applicant is Eric Brecher Pty Ltd (EBPL). Dr Brecher is the sole director of, and shareholder in, EBPL. EBPL is the trustee of the South Coast X-Ray Unit Trust (SCXR Unit Trust) and the Eric Brecher Discretionary Trust.

16 EBPL, as trustee of the SCXR Unit Trust, owned and operated SCXR Dapto, a radiology practice conducted from leased premises at Dapto, trading as “South Coast X-Ray”. It purchased this business on 31 March 2014 for $2.5 million. In order to acquire and conduct this business, EBPL entered into certain leases and obtained finance on security. It borrowed money from Dr Brecher, Medfin Australia Pty Ltd (Medfin) and the Bank of Queensland (BOQ). The Medfin Facilities and BOQ Loans were secured, including by a guarantee given by Dr Brecher. EBPL also entered into leases with GE Commercial Pty Limited (later, Alleasing) for the lease of equipment and granted security over the leased equipment (Alleasing Securities).

17 Dr Brecher is a radiologist from the United States of America, specialising in the reading of images taken through medical imaging practices, including ultrasound, X-ray, CT (Computed Tomography) scan, MRI (Magnetic Resonance Imaging) scan, OPG (Orthopantomogram) scan and mammography machines. He has for some years worked in radiology in Australia and elsewhere. He described himself as a “prolific reader of radiology cases”. He explained what he meant by this, namely that, whereas a busy radiologist can read up to one hundred and fifty reports in a day, Dr Brecher can read three to four hundred in a day.

18 Dr Brecher was neither a reliable nor credible witness. He was cross-examined at length by counsel for Dr Rashid’s interests and counsel for Acorn Lawyers. I have taken the length and vigour of the cross-examination into account in making findings on credibility and reliability. The length of cross-examination was significantly contributed to by Dr Brecher’s often extensive responses to simple questions. These extensive answers were often argumentative, sometimes unresponsive, and occasionally perforated by statements that he was a “victim” and a credible witness.

19 Dr Brecher often provided answers to what he considered was being implied by questions rather than attempting a direct answer. He would accuse the cross-examiner of having no basis for asking questions and of speculating or even lying. Dr Brecher was also prone to asserting misconduct on the part of others with little or no established justification. Blame for events which he did not like, and allegations of misconduct, came easily to Dr Brecher, both as a witness and as revealed by the events which occurred. He was prone to angry outbursts. Examples are set out in the factual background below. Dr Brecher was quick to find fault in others and resilient to accepting responsibility. These characteristics, and those mentioned above, affected the manner in which Dr Brecher gave evidence as well as, importantly, the content and reliability of it.

20 More significantly, his oral evidence often sat uncomfortably at best with the contemporaneous documents and, at worst, in obvious conflict with them. His account as to the relevant events, usually put with great conviction, would change as documents were put to him and as he struggled to explain away the inconsistencies in his earlier evidence.

21 Dr Brecher did not give an accurate, frank or objective account of the relevant events. He was prepared to mislead whenever he perceived it would suit his interests.

22 Evidence was also given by Ms Renee Hyratt. She was Dr Brecher’s domestic partner and was the practice manager of SCXR Dapto. Ms Hyratt gave evidence which in some respects corroborated Dr Brecher’s evidence. In terms of demeanour, Ms Hyratt presented as generally credible. However, there were important aspects of her evidence which cannot be accepted as accurate. That may be a result of the ordinary process of reconstruction after the events, affected as it inevitably would be by the passage of time, the subconscious effect of interest in the result of the litigation, the effect of supporting Dr Brecher with his justifications and accounts of what occurred and the emotional strain that litigation brings.

B.2 Dr Rashid and associated entities

23 The first respondent is Barrack Investments. It has two issued shares one of which is registered in the name of Dr Mohamad Rashid (Dr Rashid), the third respondent. Barrack Investments is the registered proprietor of the land where the medical centre referred to as CHC Barrack Heights is located.

24 The second respondent is Delbest. It has two issued shares one of which is registered in the name of Dr Rashid.

25 Since around 2006, Barrack Investments and Delbest have conducted an integrated medical health business known as “Centre Health Barrack Heights” or “Centre Health Complex Barrack Heights”. Barrack Investments rents parts of the premises to third party health care providers. In addition, self-employed medical practitioners provide health care services to patients from CHC Barrack Heights and pay Delbest a fee for providing them with facilities and support services.

26 Dr Rashid is a medical doctor. Dr Rashid was a very softly spoken man. He was careful about giving his evidence. I found his evidence to be mostly reliable. His evidence generally sat comfortably with the contemporaneous documents. His recollection of all of the events and conversations was not perfect as is to be expected.

27 Dr Rashid is also a director and shareholder of Romore Pty Limited (Romore). Romore is the trustee of the Rashid Family Trust.

28 The fourth respondent was Mr Ashutosh Agarwal (sometimes referred to in evidence as Ash), who is a lawyer and director of the fifth respondent, Acorn Lawyers Pty Ltd (Acorn Lawyers). As mentioned, the proceedings against the fourth and fifth respondents settled during the hearing.

29 The employees of Acorn Lawyers included a solicitor, Mr Rocco Musumeci, who was present at parts of the meeting on 15 October 2015.

30 I found Mr Agarwal and Mr Musumeci to be generally credible witnesses. They were called to give evidence by Dr Rashid and his interests.

C SUMMARY OF THE APPLICANTS’ AND CROSS-CLAIMANTS’ CASES

C.1 Application to amend the amended statement of claim

31 On 5 December 2019, after the conclusion of the hearing, the applicants filed an interlocutory application seeking leave to amend further the amended statement of claim.

32 The amendments sought to engage the Australian Consumer Law, as adopted in New South Wales by s 28 of the Fair Trading Act 1987 (NSW) (ACL (NSW)), as an alternative to its claims relying upon the Australian Consumer Law in Sch 2 of the Competition and Consumer Act 2010 (Cth) (ACL (Cth)). The perceived advantage of this was apparently to facilitate an argument that the defence of contributory negligence pleaded by Dr Rashid and his interests was not available in respect of a claim under s 18 of the ACL (NSW). The argument was that s 137B of the Competition and Consumer Act 2010 (Cth) does not apply to the ACL (NSW) on the basis that it is not incorporated as a law of New South Wales by s 28 of the Fair Trading Act 1987 (NSW). The applicants referred in this respect to the decision of Campbell JA in Rennie Golledge Pty Ltd v Ballard (2012) 82 NSWLR 231 at [141]. Dr Rashid and his interests opposed the amendments on the basis that they were futile.

33 I allow the amendments. There is no prejudice to the respondents in allowing the amendments. It is not necessary to decide whether the amendments are futile because, for the reasons given below, the issue of contributory negligence does not arise on the conclusions ultimately reached. Nevertheless, the amendments should be allowed, as they may be relied upon in the event that a party decides to appeal.

34 At the conclusion of the hearing, the applicants and the remaining respondents, Dr Rashid and his interests, identified 40 issues to be determined in light of the way in which the case had been conducted. These are each dealt with below. There is benefit in also summarising some of the main allegations made by the applicants and the cross-claimants, as pleaded in the further amended statement of claim (FASOC) and the cross-claim.

C.2 The further amended statement of claim

35 A substantial number of the issues turned on whether Dr Rashid engaged in misleading or deceptive conduct, principally by making representations or adopting representations alleged to have been made by Mr Agarwal.

36 First, the applicants relied upon conduct said to have occurred before 15 October 2015: FASOC [14] to [18], [68]. It was asserted that:

(1) in late June or early July 2015, Dr Rashid represented to Dr Brecher that there would be a lot of work for a radiologist at CHC Barracks Height: FASOC [14];

(2) Dr Rashid represented that a previous tenant (PRP Diagnostic Imaging Pty Ltd) which had conducted a radiology practice at CHC Barrack Heights had left because of a dispute it had with Wollongong Nuclear Medicine, another tenant in CHC Barrack Heights: FASOC [15];

(3) in the first half of July 2015, Dr Rashid represented that:

(a) he had 20 full-time General Practitioners (GPs) working at CHC Barrack Heights and was expanding to 40;

(b) he was bringing in multiple specialists, including five obstetricians and gynaecologists;

(c) an additional floor was to be added to the medical centre; and

(d) as such, Dr Brecher did not have to be concerned about the profitability of the practice to be conducted at CHC Barrack Heights: FASOC [16];

(4) in about mid-July 2015, Dr Rashid:

(a) showed Dr Brecher plans for CHC Barrack Heights indicating where, inter alia, the 20 new GPs and the new specialists would practice;

(b) represented to Dr Brecher that the expansion would be completed by the end of 2019;

(c) undertook to find a neutral lawyer to represent both men and the business to be conducted by them from CHC Barracks Heights; and

(d) represented that the Barrack Heights practice would have enough work to justify the applicants’ involvement: FASOC [17]; and

(5) at various times, including in about September 2015, Dr Rashid undertook to Dr Brecher to find a lawyer to work for the two men and to draft the legal documents for the proposed Barrack Heights practice: FASOC [18].

37 Secondly, the applicants alleged that representations were made on 15 October 2015, when Dr Brecher and Dr Rashid executed the four agreements which implemented the SCMI transaction at Acorn Lawyers’ office. It was alleged that Mr Agarwal represented to Dr Brecher that:

(1) he and Acorn represented Dr Brecher, Dr Rashid and SCMI and would be performing work for Dr Brecher;

(2) the turnover of revenue of the Barrack Heights practice was expected to be $5 million for the first year, $7.5 million in the second year and $10 million in the third year;

(3) Dr Rashid would take out a loan in the sum of $2.5 million, of which up to $1.5 million would be used for the fit-out of the Barrack Heights practice and the balance would be spent on equipment;

(4) Dr Rashid would be negotiating the new lease for the Barrack Heights practice, and the rent would be about $25,000 per month;

(5) the Barrack Heights practice would be up and running by 15 January 2016;

(6) Dr Rashid would recruit new doctors and build up the number of doctors working at CHC Barrack Heights; and

(7) anything in EBPL’s bank account, as at the date of execution of the SCMI transaction documents, was Dr Brecher’s and Dr Brecher could take that money out at any time. This statement was allegedly made in response to a statement by Dr Brecher that he had put between $500,000 and $600,000 into SCXR Dapto and that he needed to get that loan back: FASOC [37].

38 It was alleged that Dr Rashid did not contradict or qualify what Mr Agarwal had said and that Mr Agarwal’s representations were adopted by Dr Rashid’s conduct, including by remaining silent: FASOC [38].

39 It was alleged that Mr Agarwal gave Dr Brecher a brief summary of the documents he and EBPL were to sign and did not advise Dr Brecher that the effect of the documents was to advantage the commercial interests of others over those of EBPL and Dr Brecher: FASOC [40].

40 It was alleged that Dr Rashid did not inform Dr Brecher that Dr Rashid had an interest in Barrack Investments or Delbest, the latter of which would or might undertake the fit-out works for the Barrack Heights practice: FASOC [41].

41 It was alleged that Dr Brecher and EBPL executed the documents in reliance, amongst other things, on the representations detailed in [37] above and on the basis of conduct engaged in by Dr Rashid: FASOC [42].

42 It was alleged that Dr Rashid and his interests engaged in unconscionable conduct within the meaning of s 21 of the ACL (Cth) and ACL (NSW): FASOC [83], [84].

43 It was alleged that Dr Brecher and EBPL suffered loss and damage, resulting from the alleged breaches of ss 18, 20 and 21 of the ACL (Cth) and ACL (NSW), as follows:

(1) In the case of EBPL:

(a) lost profits;

(b) its capital;

(c) the value of its business; and

(d) the lost opportunity to repay in whole the monies due under the Medfin Facilities, the BOQ Loans, and the Alleasing Securities, or to repay more than anything SCMI caused to pay over 2016 and 2017.

(2) In the case of Dr Brecher:

(a) as:

(i) EBPL ceased trading; and

(ii) SCMI did not pay out the Medfin Facilities and the BOQ Loans and the Alleasing Securities or cause them to be repaid as quickly as would have been the case had EBPL continued to trade,

he is under a greater financial liability under the guarantees given in support of those facilities;

(b) such liability as Dr Brecher has under the ANZ Guarantee; and

(c) Dr Brecher has lost income and the opportunity to recover his loans from EBPL.

44 It was alleged that Dr Rashid breached a fiduciary duty owed to Dr Brecher and EBPL: FASOC [89] to [93]. These breaches were said to given rise to the same loss and damage as identified above as having arisen from the breaches of the ACL (Cth) and ACL (NSW). There was no claim specifically made in the section of the pleading alleging breach of fiduciary duty on the part of Dr Rashid for disgorgement of profits made by Delbest in relation to the fit-out carried out for the new radiology practice to be opened at Barrack Heights. However, it was pleaded in [52] of the FASOC, which set out material facts after 15 October 2015, that the fit-out could have been carried out faster and at a lower cost.

45 It was alleged that the Deed of Acknowledgement executed on 15 October 2015 was void for uncertainty: FASOC [66]. However, this was not identified as an issue which needed to be determined at the conclusion of the hearing and was not the subject of any submission.

46 Dr Rashid, Barrack Investments and Delbest cross-claimed against Dr Brecher and EBPL. Their case, in summary, was that:

(1) Dr Brecher and EBPL agreed to purchase SCXR Dapto in the name of the SCXR Unit Trust for $2.5 million, which was substantially more than its value. The purchase was funded, amongst other things, through facilities provided by Medfin. EBPL, in some cases as trustee for the SCXR Unit Trust, also entered into operating lease agreements with GE Commercial and loan agreements with the BOQ.

(2) By 30 August 2015, Dr Brecher knew that Dr Rashid was considering:

(a) leasing a part of Barrack Heights to Primary Healthcare Limited, through its subsidiary Healthcare Imaging Services Pty Ltd, for the purpose of opening a radiology practice; or

(b) establishing a radiology practice at Barrack Heights himself or through associated entities.

(3) A new radiology practice at Barrack Heights would be a competitor of SCXR Dapto.

(4) By 30 August 2015, Dr Brecher knew or ought to have known that:

(a) SCXR Dapto could not repay its liabilities from operating cash flows;

(b) Dr Brecher had a contingent personal liability to repay those liabilities; and

(c) SCXR Dapto’s liabilities exceeded its assets and its debts exceeded its enterprise value and the business was making operating losses and was not able to pay its debts as and when they fell due.

(5) Dr Brecher made a series of representations to Dr Rashid on 30 August 2015 about his ability as a radiologist and the financial position of SCXR Dapto. The alleged representations, referred to as the “Restaurant Representations”, were:

(a) SCXR Dapto had been operating for 20 years or more;

(b) Dr Brecher could provide better radiology services to CHC Barrack Heights’s clients than Healthcare Imaging;

(c) SCXR Dapto was a substantial business having a gross income of $2.8 million per year and net profit of $350,000 per year;

(d) The SCXR Unit Trust was the owner and operator of SCXR Dapto;

(e) SCXR Dapto’s only debts were $2.2 million which it owed Medfin;

(f) SCXR Dapto had no liabilities other than the Medfin Facilities of $2.2 million;

(g) Dr Brecher worked six days a week, he did not take holidays and he did not have commitments to distract him from work;

(h) Dr Brecher could read and analyse 400 radiology reports a day;

(i) Dr Brecher could manage five or six other radiology practices without needing to hire another radiologist as Dr Brecher had the capabilities, skill and experience to manage the practices remotely;

(j) Dr Brecher owned real estate assets and a collection of expensive paintings in the United States; and

(k) Dr Brecher could not get finance in Australia because Australian banks did not lend against assets in the United States.

(6) Dr Brecher suggested, on 30 August 2015, that he and Dr Rashid set up a new company, involving a merger of SCXR Dapto with a new radiology practice at Barrack Heights.

(7) The representations were misleading or deceptive and made with the intention, amongst other things, of encouraging Barrack Investments, Delbest, Dr Rashid and Romore to go into business with Dr Brecher rather than leasing the radiology area at the Barack Heights Centre to Healthcare Imaging.

(8) On 31 August 2015, Dr Brecher caused a profit and loss statement of the SCXR Unit Trust’s income and expenses for the 2014-2015 financial year to be sent to Dr Rashid. This was given to Dr Rashid with the intention that it be relied upon in establishing the financial performance of SCXR Dapto and supporting its value and encouraging Dr Rashid to go into business with Dr Brecher. It conveyed representations or contained information which was misleading and deceptive.

(9) On 7 October 2015, Dr Brecher caused a balance sheet that purported to show the SCXR Unit Trust’s assets and liabilities as at 30 June 2015 to be given to Dr Rashid. This was given to Dr Rashid with the intention that it be relied upon in establishing the financial performance of SCXR Dapto and supporting its value and encouraging Dr Rashid to go into business with Dr Brecher. It conveyed representations or contained information which was misleading and deceptive.

(10) Dr Rashid relied on the Restaurant Representations, the profit and loss statement and the balance sheet in agreeing to Dr Brecher’s proposal and not entering into a lease with Healthcare Imaging.

47 Although the cross-claim pleaded that Dr Brecher made further representations on 2 September 2015, these were not identified as an issue at the conclusion of the hearing and were not the subject of any submission.

48 The cross-claimants also alleged that Dr Brecher earned fees performing work in breach of cl 6.1 of the Share Holders and Unit Holders Deed executed on 15 October 2015.

49 It is not practical to mention every piece of evidence adduced or event traversed in the course of the trial. I have considered all of the evidence as well as the lengthy written submissions advanced in respect of the evidence. The findings of fact set out below are based on the whole of the evidence, including close observation of witnesses when giving oral evidence about contested matters, particularly conversations, and the consistency of that evidence with the surrounding circumstances and contemporaneous documents.

D.1 Early 2014 to 31 March 2014: Purchase of SCXR Dapto

50 In early 2014, Dr Brecher commenced looking for a radiology practice to purchase. He found SCXR Dapto, a practice which was trading as “South Coast X-Ray”. He described it as a “small rundown practice in Dapto”. In the financial year ended 30 June 2013, SCXR Dapto generated revenue of $1,894,449. The profit was $191,370. Through EBPL, Dr Brecher purchased SCXR Dapto for $2.5 million. It was Dr Brecher’s case that he did not pay more than market value.

51 Dr Brecher engaged accountants from Crowe Horwath to provide advice in relation to the purchase. Dr Brecher had provided Mr Fintan Connolly of Crowe Horwath with “numbers provided by Dr Stanton”. Dr Arthur Stanton’s company had been the owner of SCXR Dapto. On 31 January 2014, Mr Connolly wrote an email to Dr Brecher which included:

While there is plenty of room for improvement for the South Coast XRay business my concern is that you should not overpay for a business with crap numbers and old equipment. Capacity to service borrowings will be critical.

52 In cross-examination, Dr Brecher said that Mr Connolly supported his purchase. Dr Brecher, when shown this email, gave the following evidence:

Yes. So already he’s cautioning you about overpaying for the business; do you agree with that?---Yes. But I had phone conversations with him where I discussed with him some of the other reasons why I was interested in purchasing South Coast X-Ray. And when I explained it to him he was quite in favour of why I was going ahead doing this.

And is it your evidence that he was supportive of you paying $2.5 million?---Yes. When I – when I went and explained to him my other reasons for wanting to purchase the business – remember, it was an independent valuation between two and to say it’s – I overpaid – so people could say that, you know, it was at the top of the range, you know, that I paid within the range. But when I explained to him other reasons why I was interested in purchasing the business, he became much more supportive.

53 Dr Brecher wrote an email to Mr Connolly on 3 February 2014 which included:

Maybe we should use an independent appraiser to value the equipment as the value is key if the practice fails. I would like to incentivise all the key people at the company to make sure they are working to their full capacity to build up this business. I’m a little concerned about the financial backing although Andrew Fraser from Medfin has told me he sees no problem with me getting the full loan.

There are important upgrades that need to be made to the practice. I believe that the entire office needs to be refurbished. Also it’s critical that they upgrade their PACS [Picture Archiving and Communication System] and RIS [Radiology Information System]. These costs can be in the 100-200K range.

54 Mr Connolly and Dr Brecher exchanged emails on 4 February 2014. Mr Connolly wrote to Dr Brecher stating:

I got a call from Michael [Mr Michael Gray was an employee of the Dapto practice] this morning, I presume further to your call with him last night. He is following up on getting information through.

I also received the profit and loss account for the last six months from Dr. Stanton. On the basis that the company made a net profit of $180k for six months, which seems less strong than you might have hoped for, I will continue to follow up on information and continue the review work as planned.

55 Dr Brecher responded on 4 February 2014:

I really would like to buy this practice so can you please try to negotiate another fair price for the practice if need be. I’m willing to overpay for it but not to an extent where I would lose more than 500K. Can you please make sure to give them the best offer possible for the practice but not one that I’m too exposed to financial ruin.

56 Mr Connolly replied to Mr Brecher later that day:

In terms of the price, I am doing homework around pricing and I am happy to deal with Dr. Stanton in structuring a deal. I will not be putting forward any offer/negotiation without your approval first. With a purchase of a $2.5m business the extent of your risk, if the bank lends you $2.5m is the full amount, you will need to get comfortable that the business will produce enough cash to service the debt and justify the price. While we can help in pulling information together, you ultimately will need to form a view as a practicing radiologist on the value and prospects of the business.

I have emailed Arthur Stanton, lets see what he comes back with.

57 Dr Brecher wrote an email to Dr Stanton on 4 February 2014, saying:

I hope you’re doing great. I really want to wrap this thing up in the next two weeks if possible. Could we please meet with the Accountant and Michael one of the next two upcoming Friday evenings? I’m pushing the accountant to go as fast as possible. I want him to be careful with his due diligence but at the same time I’m hoping to start working at the company in the next 3-4 weeks at [the] latest.

58 On 5 February 2014, Mr Gray and Dr Brecher exchanged emails. Dr Brecher wrote to Mr Gray at 2.39 pm, saying:

I hope you’re well. If it turns out that the practice is not worth 2.5 million, do you think Arthur would be willing to come down so that the bank will finance it completely?

59 Mr Gray responded at 2.51 pm as follows:

Not sure you would have to ask him but he was pretty set on that price. I just spoke to Medfin and they will call u. I will call after work

60 Dr Brecher replied at 3.10 pm:

Unfortunately, it’s not looking good. Looks like the business may be overpriced beyond my ability to get the financing.

61 Dr Brecher was unable to explain in cross-examination why he considered he would not be able to get the financing. His evidence was:

Does that suggest to you [that] you had information from Medfin that they were not going to be financing the full amount of the $2.5 million purchase price?---No. I don’t know what that means.

All right. Can you explain to the court why you said that:

It looks like the business may be overpriced beyond my ability to get the financing.

?---I don’t know why I said that.

62 Dr Brecher emailed Mr Connolly at 1.33 pm on 6 February 2014 as follows:

It looks like Stanton is unwilling to allow anyone to see the financials of the practice for the past two years. I feel duped by this guy and have no[w] expended money on an audit that he knew was going to go nowhere. I may take him to court to recover my expenses because he acted in bad faith.

63 On 11 February 2014, Mr Connolly and Dr Brecher exchanged further emails. Dr Brecher emailed Mr Connolly at 8.18 am stating:

Thanks so much Fintan! I really appreciate this. Depending on Andrew’s assessment of the practice (if he gives the thumbs up to a loan) would you please think about conducting a very extensive audit. I’m very concerned about losing a ton of money if the practice fails.

64 The reference to “Andrew’s assessment of the practice” was a reference to an assessment by Andrew Fraser of Medfin. Mr Connolly sent an email reply that day which included:

You are right to be concerned, the practice seems expensive and does not seem to make enough money to justify the price. I am happy to arrange for a review, get some expert input to conduct a review of the practice etc, but we need to get solid basic information.

Depending on what Andrew comes back with, it might make sense for me to go and see Dr. Stanton and try and get him to be more supportive with information. However, my guess is that he is not sharing numbers with you because they are terrible; but lets see.

65 On 13 February 2014 at 6.29 pm Mr Connolly sent an email to Dr Brecher which included:

[Andrew Fraser] has spoken to Michael and they are willing to provide two years of income and expense statements. Andrew is also arranging for an independent practice valuation which will take about a week to do. I have asked him to provide you and I with the accounts and valuation when he gets them. Lets see what they come back with.

In the meantime, I have been speaking with Ben Willis from the immigration law firm and he was to send you an email with some thoughts on the way to proceed. Has he been in touch with you?

66 Dr Brecher replied to Mr Connolly the next day at 9.39 am, stating:

It went great. Can you please get involved to make sure that the evaluation is proper and I’m not overpaying too much for the company? Can you also get into contact with Alan Pham the owner of the company I’m working for [Insight Radiology]. I’m hoping to work out a favorable deal with him in which he would get a piece of the company and I would hopefully get a portion of his company. He also knows the business extremely well and can tell you about what exactly to look at when buying a radiology practice. His email is: [email address].

67 In cross-examination, Dr Brecher explained that Mr Alan Pham had a few practices in 2014 which generated a turnover of many millions. He explained:

So this deal that you were considering pursuing, was that a partnership with Mr Pham?---No, I’m not sure. I mean, my feeling was – because I felt like a fish out of water and Alan Pham had a lot of experience in radiology – he had been running practices – and was looking for his advice in terms of making sure that I do everything properly in terms of what to look for when purchasing the business and setting it up. And I was interested in having him be sort of like a business manager for me where I would give him a percentage of my business and he would potentially give me a percentage of his business, as well as possibly even run my business.

When you say percentage of business, do you mean percentage of the company?---The company, yes.

Yes. And you’re saying here, “I’m hoping to work out a favourable deal with him”, does that suggest that you were initiating these discussions regarding a possible partnership?---Yes, it would probably be me – what I was looking for really was the – trying to get work from him and to give him some of – an interest in Dapto. Once again, I was trying to hedge so that if the company at Dapto didn’t do well, I would have money from my telereporting to help finance the Dapto practice.

But you were already doing telereporting for Dr Pham. You wouldn’t need to be working out a deal with him whereby he would get a piece of your company and he would hopefully – you would hopefully get a portion of his?---I think I – you know, to get more telereporting from him. So to get additional teleradiology as well as to get a interest in his company so that I was not only reporting from him but making a profit from his company that he was making, as well as for him to get profit from my company and to – so it was just a way doing what I was going to do later, and that is to try and increase the footprint so that I wasn’t exposed to just one site.

68 The fact that Dr Brecher had raised with Dr Pham the possibility of each of them owning a portion of each other’s companies lends some support to the fact that it was Dr Brecher who later raised a similar idea with Dr Rashid, rather than Dr Rashid raising the idea with Dr Brecher.

69 Dr Brecher and Mr Connolly exchanged a number of further emails between 18 and 24 February 2014. On 18 February 2014 at 12.06 pm Dr Brecher sent the following email to Mr Connolly:

I’ve resigned my position here at Insight Radiology and therefore have to purchase the Dapto practice. I have no alternative. I’ll have to sell my assets and purchase it if the bank doesn’t loan me the money.

Would you please help me structure a great contract for Luke Whitley who would be in charge of growing the practice. His email is: [email address]. I’m going to start working in Dapto in two weeks and would like him on board if at all possible. His role would be to go out and get as much business as possible and make me as productive as possible. I’d like to make his contract very incentive laden.

70 Dr Brecher sent a further email to Mr Connolly at 10.12 am on 24 February 2014, stating:

I hope you’re well. The evaluation came back at between 1.5-2 million due in part to Arthur Stanton not releasing all his financial information. I’m going to go ahead with the purchase since I have no choice. I have to give away around 500K in kickback money at this juncture so can inject all this money back into the company. I’d hope to get the price down to 2.25 million though because it needs 300K in upgrades asap.

71 When shown this email, Dr Brecher gave the following evidence:

So do you agree, first of all, that Medfin had done its own assessment of the value of the Dapto practice and that that assessment had indicated the practice was only worth between 1.5 to $2 million?---I don’t know if they did that. I don’t know who – who did that.

Well, Dr Brecher, I took you to the earlier emails where it indicated that Medfin was going to be doing its own evaluation of the practice based upon the financials it had. Do you recall that, or do you need me to take you to those emails?---No, because I know that they did it. There was another valuation for 2 to 2.5 million, so I’m not sure exactly who did this valuation, whether or not that was Medfin or someone else.

In the context of this email exchange between you and Mr Connolly, where Mr Connolly is following up Andrew Fraser of Medfin and asking if you’ve heard back, and your response being, “The evaluation came back at between 1.5 to 2 million”, does that suggest to you now, Dr Brecher, that Medfin had conducted an evaluation and it had come back at between 1.5 to 2 million dollars – of the business?---No, I’m not sure who did that evaluation. I assume, like you - - -

Who else did that evaluation, Dr Brecher?---I don’t know. I don’t know who did that.

If you go up the page - - -?---Because I don’t say, you know, Medfin did the evaluation.

Was anyone else interested in the value of the Dapto practice at this stage other than you and Medfin?---I’m not sure who did the valuation.

72 Dr Brecher was also asked about what he was referring to by the phrase “kickback money”:

What are you referring to when you talk about 500k in kickback money?---Yes. This is – I would like to explain this to his Honour. Could I please do that?

Sure?---Okay. So to me, because I was mentioning, you know, what other aspects that were interesting me about buying a company was the fact that I felt like, as a radiologist who had come from overseas as a physician, that people would take advantage of me through my visa – through my – you know, not letting me do work for other sites without permission, giving me – making me accept very low rates, and I believe by not only owning this company, South Coast X-ray, by getting a permanent visa I would be able to negotiate for myself very – higher teleradiology rates and – much higher than I was getting at that time, because I didn’t have this leverage. And I could also get as much work as I wanted to, because sometimes your employees would limit you and say, “Well, you can’t do as much unless, you know, you take some wage reduction”. So I just felt it was very unfair, the way the system was set up, and I felt that by going and purchasing my own company, it meant an extra – at least an extra $500,000 in my wallet from being able to negotiate better teleradiology deals.

So is that your best explanation of what you meant by “500k in kickback money”?---Yes, that’s exactly what I meant.

73 On 24 February 2014 Mr Connolly sent the following reply to Dr Brecher’s email:

Why don’t you have other choices? It sounds like a big gap in value?

Do you want me to do anything further?

If so give me a call to discuss.

74 Dr Brecher replied to Mr Connolly on 24 February 2014, stating:

Because I’m leaving work here and don’t have a sponsor. I would have to give up the lucrative deal i have with teleradiology which alone will earn me 60-70K a month (i had to give the radiologist I’m working with here about 30K a month in kickbacks to allow me to do teleradiology). My own company can sponsor me so i can continue to do teleradiology work.

75 In cross-examination by counsel for Acorn Lawyers, Dr Brecher explained:

First of all, what was the – where was the practice where you had to give 30k a month in kickbacks to allow you to do teleradiology?---

…

---Okay. Insight Radiology. And my sponsoring – the sponsoring doctor is named [person named], and he was saying – because for me to get – like, when I was sponsored, for example, at Insight Radiology, I would have to have a doctor sponsor me as well, a radiologist, and essentially, for me to get additional work, I would have to have his permission, and he was asking for about $30,000 a month to allow me to do work for this teleradiology company. So you could see that if I was able to earn $1 million a year – like, $100,000 a year, I would have to pay back to him about $30,000 a year, and that was just completely unacceptable to me. So that’s why I had this impetus to leave Insight Radiology. I loved working at Insight Radiology, but I felt the need to get away from it. Even though I didn’t have a sponsor and I may have to go back to the United States, the thought of having to pay kickbacks to me was just something I couldn’t bear.

76 Dr Brecher had earlier been asked questions by Dr Rashid’s counsel in relation to certain dealings with Dr Rashid and given evidence that he would not sign a “Promotional & Co-Management Services Agreement” in August 2015 (discussed below) because he thought it was illegal. He had given the following evidence in relation to that agreement:

I mean, I never once went to any medical practice when any doctor has ever asked for money that their doctors – that their doctors would send. The only time I’ve ever experienced this, in all my years of radiology, is with Dr Rashid. Every other medical practice you go to where you go and market to those places no one has ever asked for money to be repaid to them for patients that they send. To me, it sounded like he was asking for a bribe – a kickback.

77 Dr Brecher was taken by counsel for Acorn Lawyers to what he had said when cross-examined by counsel for Dr Rashid and then gave the following evidence:

Do you see that?---Yes, exactly, and I meant – I mean it, and what I was – meant by this was GPs. I never talked about radiologists, and this happened to me by a radiologist, not a GP, and I wasn’t - - -

So - - -?---And my – I didn’t take the – I didn’t want – I didn’t give the kickbacks and I stopped and I left Insight Radiology over it. So I would not go into anything where someone would take advantage of me – try to get me to get kickbacks or bribes. I don’t do that.

Dr Brecher, your evidence is “every other medical practice”; do you see that?---Yes, “medical practice”, not “radiology practice”. “Medical” means GPs.

And sitting there in that witness box you gave an oath or an undertaking to the court to tell the truth, the whole truth, and nothing but the truth, and do you agree that you have not done that in this case?---No, I definitely did that in this case, and what this says is that I never went to a GP – medical practice where anybody has ever asked me for a kickback or bribe. Okay. That has nothing to do with radiology practice. Radiology is different than GP practices and I was clearly referring to GP practices there.

Dr Brecher, do you agree that you gave that evidence to paint yourself as someone who was conscientious and moral and would not engage in something as nefarious as kickbacks?---I didn’t. I left Insight Radiology because of it, and then I didn’t have anything to do with this other contract. No matter what recital D [of the “Promotional & Co-Management Services Agreement”] has in it, I did not ask for this contract. I didn’t want anything to do with it, and I had it checked by my accountant [Ms Adams] to make sure that it wasn’t a kickback, and she didn’t think it was a kickback or a bribe, and so I signed it based upon her knowledge of cross-promotional agreements. But I left Insight Radiology because of the fact that I did not want to be subject to anything like a kickback or a bribe, and I felt like that was happening there and I left. I also told Medicare about it, so I informed Medicare of what happened. Okay.

Dr Brecher, you were earning between 60 and 70 thousand dollars a month in return for the work that you were doing for Insight?---And I – yes, and I – and I did – not at Insight. That was Global Radiology.

Global?---And I was going to give it up – give up all that money, because I would not be the subject of any crimes, any bribes or any kickbacks, so I gave it up. So when you say that I am moral, I am moral; believe me.

But in saying to this court and to his Honour that, every other medical practice that you go to, no one has ever asked for money to be paid for them – for patients that they send:

It sounded like he was asking for a bribe – a kickback.

?---Well, that - - -

You - - -?---I’m sorry.

- - - misled this court as to your experience with kickbacks, didn’t you?---No, I did not. I said medical practices that send radiology. There’s a difference. Okay. You’re wrong, and if – and if you – you know, I have my lawyers here. You are completely wrong. I said I had never been to a medical practice that sent their doctors to radiology that has asked for kickbacks. I never said anything here about radiologists doing it. This is completely different. This is going – and I’m talking about GPs, medical doctors, going and marketing and saying ..... “If I send you patients, you give me this money back.” What was happening at the radiology practice is completely different, because what was happening there was I was working as a radiologist and, because I wanted additional work, that happened. But this is a completely different situation to me – separate. This is going as a radiologist, marketing to GPs, and a GP, a general practitioner, asking for a kickback. This never happened to me before.

…

In the context of providing evidence in relation to the promotional and co-management services agreement, do you agree that it was misleading for you to suggest that you didn’t want to enter that agreement because you did not want to be involved in something like kickbacks?---No, it was not misleading at all.

78 Dr Brecher was then taken to some other evidence he had given in response to questions from Dr Rashid’s counsel. Dr Brecher had said in the context of that questioning:

Like I said, no other – no other medical practice has ever said that to me or any of our marketers. I never heard of anything like that. So I would have gone to the police had he come to me with this before we had made an agreement to go into business together.

79 The sentence “I never heard of anything like that” was drawn to his attention and Dr Brecher gave the following evidence:

Do you agree that a kickback from a radiology practice is similar to a kickback from – to a medical practice?---No. I said I had never seen anything – heard anything like that from medical practices, not, you know, referring work to a GP – I mean, I’m sorry, referring work to radiology groups. So the GP – I’ve never heard of a GP saying that, you know, “If we send you work we will get” – you know, “You give us a percentage of the money that we’re sending.” That’s what I was referring to. As far as the radiology, that was a different issue. That’s a visa issue, to me. That’s a flaw in the system, I believe, here, and I brought it up with Medicare. It has been reported to Medicare. You could look it up. You could go and ask them if I – you know, investigate that, but I did bring it up with Medicare.

80 Mr Connolly responded to Dr Brecher’s email at [74] above as follows:

I understand, but do you have to buy South Coast Radiology?

Did the immigration lawyer come up with alternative options?

As you have a valuation in hand for South Coast (which has the business being between $500k to $1m below the asking price) would it not make sense to try and get Dr. Stanton to improve his deal, or indeed offer to pay him on an earn out basis (i.e. borrow $1.5m from the bank then pay him the balance of consideration in a years time should the practice continue to do well?).

81 Dr Brecher replied and stated:

Yes, i’m going to try to [do] both but I’m sure I know what the answer will be. Fintan, I can promise you I can turn that practice into a cash cow. Do you know anyone who could negotiate on my behalf with Arthur?

82 Dr Brecher agreed that one of his responses to Mr Connolly’s email at [74] above was to say that “it will be a $5 million practice in a year or two”.

83 Mr Connolly sent an email at 2.09 pm which stated:

You are not buying what you can make of the practice, you are buying what’s there!

I would be happy to try and negotiate. Alternatively, happy to suggest a lawyer. I believe that any negotiation should be done face to face with Dr. Stanton.

84 Dr Brecher replied:

From what I understand Stanton is not willing to budge at all.

85 Mr Connolly replied:

You (or someone working on your behalf) needs to engage directly with Dr. Stanton. If he is unwilling to budge on price, then payment terms might be open to discussion. Also, if it’s a business and assets purchase, the allocation of purchase price needs to be considered.

Some ground for compromise needs to be found in order to try and do a deal.

86 I infer that, at least as at 24 February 2014, Dr Brecher had not retained a lawyer on the purchase of SCXR Dapto. Dr Brecher considered that Dr Stanton would not accept less than $2.5 million for the practice. The contemporaneous material indicates that Dr Brecher had not received the three years of financial material which he and Mr Connolly had sought. Medfin, to Dr Brecher’s knowledge, had valued the business at between $1.5 and $2 million. Dr Brecher’s accountants had not valued the business.

87 When he had earlier been cross-examined by Dr Rashid’s counsel, Dr Brecher had said:

You thought 2.5 million was too much to pay for the business?---Well, it was within the – the estimate. I had an estimate of – of an expert saying that it was between two million at its low end and $2.5 million at its high end …

88 Dr Brecher was taken to this by counsel for Acorn Lawyers and he confirmed that the estimate to which he was referring was not one provided by Crowe Howarth or Mr Connolly. He also agreed it was not provided by Medfin.

89 Dr Brecher was then shown an affidavit sworn in proceedings which had been in the Supreme Court of NSW concerning the administration of SCMI. Dr Rashid was also a party to those proceedings. In that affidavit Dr Brecher had described himself as a “medical practitioner, specialising in radiology”. This sits uneasily with his evidence that “‘medical’ means GPs” – see [77] above. Dr Brecher was taken to [16] of that affidavit where he stated:

I instructed my accountants to prepare a valuation for SCXR. At the time, my accountants were Crowe Howarth. At this time, SCXR was generating a revenue of approximately $1,200,000.00 per year. Of this, the profit was approximately $400,000.00 per year. My accountants valued the practice at between $2,000,000.00 and $2,500,000.00. At Tab 5 of the Exhibit is a true copy of the business valuation from Accounting Professionals (NSW) Pty Ltd, dated 16 April 2014.

90 Dr Brecher gave the following evidence:

And you were saying in your evidence on oath that Crowe Horwath had valued the practice at between 2 million and 2.5 million dollars, weren’t you?---Yes. If I’m incorrect about something, I don’t know if that constitutes perjury. I was just incorrect, but the fact is that there was a valuation of it for 2 to 2.5 million dollars. I was erroneous. I apologise for the mistake.

Well, it’s just plain wrong, isn’t it, Dr Brecher?---No, because I don’t see any reason – I wouldn’t lie about it, you know. I mean, there’s no benefit for me to lie about how [who] valuated it. I don’t care if Crowe Horwath evaluated it or anyone else evaluated it. Like I said, it has to be established evidence that, you know, the purchase price was based upon a valuation of 2 to 2.5 million dollars, and when I wrote this – or I swore this, I made an honest mistake, and honest mistakes I don’t believe are anything like perjury. But it’s up to his Honour to make that determination. I apologise.

Do you agree that you were careless as to the truth of the statements that you were making under oath?---No, I’m not careless at all. I try my best to make very accurate statements, and in this case, I agree with you that there’s an error. It was an honest error.

And do you agree that the statement that you made, whether honest or deliberate, was misleading?---It could be constituted as misleading, yes.

And it does matter, doesn’t it, Dr Brecher, who you say performed valuations when you’re trying to give credence to the valuation you’re putting forth for a practice that you’re suing in relation to, doesn’t it?---I don’t think so. I think that, you know, the – what I was saying was that it – there was an independent valuation, which I think is the best type of valuation, not one that’s done by – you know, has anyone who has conflicts of interest; someone who’s independent. And that was the valuation of 2 to 2.5 million dollars. I just made a mistake that it was done by my accountants. It wasn’t done by my accountants. And that’s all there is, I believe, to it, because it was just an honest mistake. It doesn’t favour me. It doesn’t – I don’t know why I would write this if I didn’t believe that it was true.

And do you say that that valuation of 2 to 2.5 million dollars was independent of you?---Yes. I didn’t have anything to do with the valuation.

Nothing to do with that valuation?---I don’t believe so. I asked for an independent, honest valuation of the company, and this is the valuation, I believe, that was given. I didn’t have any – I don’t ever lie or do any of that, you know, stuff. I want – when I bought that business, I wanted someone to give me an independent, thorough evaluation, and that’s all I asked for.

91 The independent valuation to which Dr Brecher referred in his evidence was one prepared by Garry Pinch of Accounting Professionals (NSW) Pty Ltd, which Mr Pinch sent to Mr Fraser of Medfin on 26 February 2014. It was prepared at the request of Dr Brecher. It will be recalled that Medfin was previously only satisfied that the value of SCXR Dapto was between $1.5 and $2 million. Mr Pinch’s valuation was a “calculation engagement” not a “valuation engagement” – cf: APES 225 Valuation Services, issued by the Accounting Professional & Ethical Standards Board. A “calculation engagement” is more confined than a “valuation engagement”. The valuation report included:

1. Scope and Purpose of the Valuation.

You have requested that we determine the indicative Fair Market Value of the business of South Coast X-Ray, as at the 26th February 2014. In accordance with the terms of our engagement letter and the requirements of the professional standard APES 225 “Valuation Services”, we have undertaken our work as a Calculation Engagement.

A Calculation Engagement means “an Engagement or Assignment to perform a Valuation and provide a Valuation Report where the Member and the Client or Employer agree on the Valuation Approaches, Valuation Methods and Valuation Procedures the Member will employ. A Calculation Engagement generally does not include all of the Valuation Procedures required for a Valuation Engagement or a Limited Scope Valuation Engagement”.

92 Under a “valuation engagement” the valuer is free to employ the valuation approaches, valuation methods, and valuation procedures that a reasonable and informed third party would perform taking into consideration all the specific facts and circumstances of the engagement or assignment available to the valuer at the time.

93 The valuation report stated that the valuation had been requested by Dr Brecher “to assist him in purchasing the [SCXR Dapto] business and to provide an independent opinion on the value of the business”.

94 The valuation contained extensive disclaimers. One reflected that it should not be relied upon for the purposes of obtaining funding for the business:

Specifically, this valuation must not be used to attract or induce other parties to purchase, invest in or lend funds to the business.

95 The valuation noted that it relied on unaudited information provided by the vendor and that the valuer did “not warrant that our enquiries have revealed all matters relevant to the valuation”. It stated:

The preparation of this report relies on a level of financial forecasting. Such forecasting requires an estimate of future financial performance and position. In doing so we do not in any way warrant the accuracy of this forecast or that actual results achieved by South Coast X-Ray will meet this forecast. By their very nature future forecasts can be impacted by a wide range of events, which cannot be identified in advance of their occurrence. Such financial forecasts are not capable of independent substantiation or verification. As such it is not possible to warrant the accuracy of the conclusions arrived at in the valuation opinion.

96 The valuation included a discounted cash flow analysis for the years 2014 to 2018 inclusive. It contained a number of assumptions. Dr Brecher stated that he assumed that the information for the assumptions came from him. I conclude it is more likely than not that the information did come from Dr Brecher, including information which was used to forecast future turnover. The assumptions included:

1. The business is to be valued on a going concern basis.

2. Assets are recorded at their fair market value.

3. The financial statements of the business and as provided to us reflect a full and complete disclosure of the financial operation and position of the business. No material events have occurred since the issue of the accounts to the 30th June 2013 that could impact business performance or considerations relevant in assessing business value and the books and records as maintained by the business up to 28th February 2014 reflect a full and complete disclosure of the financial operation and position of the business in the absence of the issue of formal accounts.

4. The business has made significant investment in establishment costs and the development of brand and market presence. The nature of this investment will be returned over future years and be reflected in the value of goodwill.

…

11. The business will not require any significant investment in replacement or new assets to achieve the required income forecasts, except for a new Ultrasound machine and replacement of the magnets for the MRI machine. These have been included at values of $120,000 and $200,000 respectively.

…

14. Revenue will increase on average by 5.2% per annum and overheads will increase on average by 2.9% throughout the forward forecast period. Operational expenditure and capital expenditure are not anticipated to increase above these percentage increases, except for the allowed capital acquisitions listed at assumption 11.

15. The business will continue to operate from the existing premises during the next five years without the need for any significant capital improvements to the premises.

…

19. If a Valuation Engagement had been performed under APES 225 rather than a Calculation Engagement, the results of this valuation calculation may have been different.

97 The nineteenth assumption is, of course, a statement of the obvious as opposed to an assumption. It necessarily follows that a valuer who is free to use such methods and make such inquiries as he or she considers appropriate might reach a different conclusion to a valuer retained under a “calculation engagement” of the kind Dr Brecher chose.

98 By 26 February 2014, Dr Brecher still had not obtained legal representation in relation to the potential purchase of SCXR Dapto. On 26 February 2014, he requested the contact details of a lawyer from Ms Maslanka, who was then the SCXR Dapto practice manager for Dr Stanton:

Can I please have the number of the lawyer Michael recommends? Also can you please send me the options I have in terms of the contract you discussed earlier on the phone with me?

99 Ms Maslanka responded at 9.14 pm on 26 February 2014, stating:

The company Michael recommends is Hanson Lawyers in Wollongong they are a well established local firm. The contact there who Michael has worked with previously is Anne Woods her contact number is [telephone number].

It would be good for you to get some advice on your options regarding the purchase as you need to chose [sic] the option that is best for you.

The option that would provide the smoothest transition would be for your company to buy 100% of the Southcoast Xray shares, taking over control of Southcoast Xray. Southcoast Xray would then just continue to operate as is now. That is what I have been led to believe.

The other option would be that you buy the company name? Then commence operation under that name?

As far as I am aware we don’t have any liabilities or problems that I can see arising that you would be liable for, though I’m not a lawyer so I don’t know how this all works.

Arthur is keen to move forward with a heads of agreement, confirming your intention to purchase Southcoast Xray, however he wants you to seek advise [sic] on what is best for you, he doesn’t want to influence your decision one way or the other on which option you would like to chose [sic]. Because in the long run the correct adjustments will be made for billings that are outstanding, staff entitlements etc.

Let me know your thoughts.

100 Dr Brecher forwarded this email to Mr Connolly on 26 February 2014, and requested his advice on the available options:

Can I please get your advice on which way you think I should go? I can’t definitively remember what advice you gave me in the past. So sorry.

101 On 27 February 2014 Mr Connolly wrote to Dr Brecher (emphasis in original):

While it is a question ultimately for your lawyer (and you need to ensure that you get a lawyer who is independent of the seller and has experience in acting for purchasers of businesses – happy to recommend one if you don’t have one), the general rule is that where you buy shares in a company, you take over all the assets as well as liabilities of that entity.

For a company such as South Coast XRay that has been around for many years, it could have significant/historic liabilities, tax problems, employee claims, patient claims etc.

However, it is difficult to form a clear view in terms of what risks might be there, as we never saw reliable financial information on this company. So in principal my personal view is that a “business and asset purchase” where you set up a new entity and acquire the business and assets of South Coast XRay would be preferred from a risk perspective. The issues with a “business and asset purchase” as against a share purchase are that the employees, registrations, immigration registrations, company name, bank account etc will all need to be transferred to set up again. I believe that the bank can work with either option, but should be consulted.

102 On 4 March 2014, Dr Brecher wrote an email to Mr Fraser stating:

I hope you’re well. I’ve been working at Dapto now for two days and have to say it’s the most inefficient practice I’ve ever worked at. It will take I believe a significant investment above the 2.5 million to get it running efficiently. I’m reconsidering purchasing the practice.

103 Dr Brecher indicated that “a significant investment” meant more than the additional expenditure that had been assumed on the basis of information provided by Dr Brecher in Mr Pinch’s valuation report.

104 Dr Brecher’s evidence as to his reliance on Mr Pinch’s valuation report was overstated:

And I suggest to you, Dr Brecher, that, in fact, you obtained that valuation purely for the purposes of obtaining a Medfin loan in the full amount of the purchase price?---No. That’s not true. I mean, I always – like – like I’ve said in my affidavit and my testimony, I always took a very pessimistic view, as well, of life, and that’s why I was rushing to open up a second radiology practice, but I was going in dumb. I looked at the worst case scenarios and that’s what I focused on. So this was a very important report for me. This is what I really based things on, an expert. I’m not an expert. I’ve never run my own radiology practice before. I had my – you know, I believed, you know, there were some things that I could do with it. I believed that I could get the revenue up, but I wasn’t certain of that. I had to rely on this report.

105 I make the following findings and draw the following inferences concerning the valuation and Dr Brecher’s evidence referred to above:

(1) I conclude that the predominant purpose of Dr Brecher obtaining Mr Pinch’s valuation was to secure finance for the purchase of SCXR Dapto from Medfin.

(2) Dr Brecher was involved in the valuation process to a greater extent than he was initially prepared to accept in cross-examination. Dr Brecher engaged the valuer under a “calculation engagement”. Under such an engagement, the valuer employed a methodology that was agreed upon by himself and Dr Brecher. Dr Brecher provided information which was the basis of many of the assumptions made in the valuation. It is more likely than not that Dr Brecher provided information to the valuer with respect to turnover, commencing with $2.55 million in 2014. SCXR Dapto’s actual turnover at the time was around $1.9 million.

(3) At the time of the report, Dr Brecher considered that one ultrasound machine required replacement and that it was desirable that the CT scanner be replaced. Dr Brecher wanted the practice to be refurbished. This involved more expenditure than was disclosed in the assumptions in the valuation.

(4) Dr Brecher engaged the valuer because Medfin was only satisfied that the business had a value of between $1.5 and $2 million and Dr Brecher wanted to convince Medfin otherwise in order to obtain a greater level of finance. I do not accept that Dr Brecher ever genuinely believed that the true value of SCXR Dapto as at the date of purchase was between $2 and $2.5 million. Although Dr Brecher denied that he did not rely on the valuation as indicating the true value, I do not accept that denial. Dr Brecher thought he could turn the practice into something of value; but that is very different to genuinely considering that the market value of the practice was in fact between $2 and $2.5 million.

(5) Dr Brecher knew he was paying too much for SCXR Dapto, but he did not care because he considered he would be able to turn the business into something better.

106 By 13 March 2014, Dr Brecher had retained Mr Roger Downs of Kells to act for him in relation to the purchase of SCXR Dapto. A draft of the contract for sale had already been prepared by this time and provided to Medfin.

107 On 24 March 2014 EBPL, as trustee of the SCXR Unit Trust, signed the contract for purchase of SCXR Dapto for $2.5 million, with a completion date of 31 March 2014. The contract was, however, not exchanged. Dr Brecher’s solicitor, Mr Roger Downs, advised Dr Brecher that formal lease transfers should be obtained before settlement of the contract. However, Dr Brecher spoke to Dr Stanton and agreed that he would accept letters from the relevant lessors about appropriate lease variations, with the formalities to be completed by the vendor’s solicitors, Access Law Group, or Mr Downs of Kells.

108 On 25 March 2014, Mr Fraser from Medfin wrote an email to Dr Brecher telling him that he had already started the process for extending the finance approval and to “take your time and get this done correctly”.

109 Mr Fraser and Dr Brecher met on 27 March 2014 and Dr Brecher executed the Medfin loan documentation. This included executing the Goodwill Loan for EBPL as trustee for the SCXR Unit Trust. Dr Brecher also executed the agreement as guarantor. Mr Fraser witnessed Dr Brecher’s execution of the document. Immediately above where he executed as guarantor, the agreement stated a number of matters under the heading “IMPORTANT”, including:

The guarantor should obtain independent legal and financial advice.

110 Dr Brecher was asked about providing this guarantee by Dr Rashid’s counsel and he stated that he had legal advice at the time. His evidence was:

You didn’t get legal advice, did you?---No, I did get legal advice.

About the guarantee?---Yes.

Who did you get the advice from?--- From Kells Lawyers.

You got no such advice, Doctor?---Why – why would you say that in - - -

I want to suggest to you, you got no such advice?---I had – Roger Downs was my lawyer when I was getting the Medfin loan, so I had legal representation, and he was helping me through the entire process, because, you know, this is the first purchase of a business that I’ve ever had, so I was unfamiliar with the entire process.

And he was, you say – I withdraw that. He was your lawyer?---Yes, Roger Downs from Kells Lawyers.

And that was important to you?---It was very important to me to have a lawyer.

You needed a lawyer to secure your interests?---Yes.

111 Dr Brecher’s evidence that he had advice from Kells Lawyers about the guarantee was not correct. He signed the relevant documents with Mr Fraser. There is no contemporaneous document which suggests he received any advice from Mr Downs in relation to the Goodwill Loan and associated guarantee.

112 Dr Brecher was referred to the evidence set out above by counsel for Acorn Lawyers. Dr Brecher then gave the following evidence:

And then there’s a reference to the guarantee. And then, at line 14, Mr George [counsel for Dr Rashid] said:

I want to suggest to you: you got no such advice?

And you responded:

I had – Roger Downs was my lawyer when I was getting the Medfin loan. So I had legal representation and he was helping me through the entire process because, you know, this was the first purchase of a business I’ve ever had.

Do you see that?---Yes.

Continuing:

And I was unfamiliar with the entire process.

?---Yes.

Now, that was wrong, that statement, wasn’t it?---No. Why is it wrong?

It was wrong in two respects: the first one being Mr Downs was not your lawyer advising you on the Medfin loan, was he?---I don’t know. I mean, I said to you I don’t recall whether or not he was.

And he was not helping you through the entire process, was he?---He helped me through the entire legal process.

Dr Brecher, he wasn’t even your lawyer when you signed the contract?---I meant legal process when I was talking about this – when I said that. When - - -

You don’t regard signing a contract as a legal process?---A contract is a legal process, yes.

And is it your evidence that you don’t regard signing a contract as a legal process?---A loan. I said that, you know, loans, I don’t regard as legal, but this I regarded as legal, and he did advise me during the entire – the legal process.

And I put to you that Mr Downs was not your lawyer helping you throughout the entire process because he wasn’t even your lawyer at the time that you signed the contract for sale, was he?---I can’t recall.

113 In the evening of 27 March 2014, Dr Brecher sent an email to Mr Fraser saying he was having a crisis. In cross-examination, Dr Brecher stated that he could not recall what the crisis was. I do not accept that he could not recall. The events, described below, are such that it is unlikely that they would not be recalled.

114 On 28 March 2014, Access Law Group (which acted for Dr Stanton) wrote an email directly to Dr Brecher noting that Dr Brecher was coming to see Mr Tom Ellicott, a lawyer who worked at the Wollongong office of Access Law Group, at 3.30 pm that day and attaching a copy of the contract. The email stated that Access Law Group was providing a copy of the contract from their file “as Kells have your signed copy”. The email then stated:

Tom Ellicott will go through the contract with you this afternoon to sign and exchange and go through the procedure for settlement.

115 Dr Brecher was asked, in cross-examination, whether this email was written because he no longer had a solicitor who was acting for him, namely Mr Downs of Kells. He stated that he could not recall. I do not accept that was truthful. He gave the following evidence:

Can you recall, Dr Brecher, why it was that you were not able to get the signed contract from Kells Lawyers?---No. I made – I’m not sure if I insulted Roger Downs or – I’m not sure. Maybe I was delinquent in my payments. I’m not sure why I wasn’t able to get it.

…

Do you see that?---Yes. It – yes, it seems like, you know, the contract I signed with Roger Downs will be re-signed with Tom Ellicott.

That’s correct?---Yes.

And why is it that Tom Ellicott would be going through the procedure for settlement and signing and exchanging the contract with you and not Roger Downs?---I don’t know.

Can I suggest a reason to you for why that might be the case?---Yes.

Dr Brecher, you sacked Roger Downs as your lawyer, didn’t you?---No.

…

Turning back to A70, Dr Brecher, can I put it to you that at 10.40 pm, when you called up or when you emailed Mr Fraser of Medfin saying that you have a crisis and thereafter had a conversation with him, which I assume from the email, you said to Andrew Fraser, “I want to proceed with exchange and completion of the sale as soon as possible, but my lawyer is holding me up”?---I can’t recall what I said to him. I have no recollection.

And you discussed with Mr Fraser at that time how it is that you could proceed without the interference of your lawyer, in terms of the two-week settlement period?---No. I can’t recall. That’s speculation.

And, having had that discussion with Mr Fraser from Medfin, you called up Access Lawyers and you informed them that Mr Downs was no longer your lawyer, didn’t you?---I can’t recall and it’s just speculation.

And further to that telephone call Ms Gabriella Virtu … sent you this email on 28 March with arrangements for you to come directly to their offices, didn’t she?---I can’t recall. I really haven’t reviewed these documents and on purpose. I don’t want to – I don’t even want to address these issues. I mean, I feel as if you’re – you’re blaming me for something, a victim, and everything here was done properly.

116 I do not accept Dr Brecher’s evidence that had forgotten why Mr Ellicott from Access Law Group and not Mr Downs would be going through the procedure for settlement and signing and exchanging the contract with Dr Brecher. Dr Brecher’s professed lack of recollection about this topic stood in stark contrast to his often adamantly expressed clear recollection of other events around this time.

117 Earlier in his cross-examination, Dr Brecher insisted that Mr Downs resigned because he had a pre-existing dispute with Dr Stanton. This evidence was misleading in light of the true facts. Dr Brecher was taken to the contract and it was pointed out that it did not identify a solicitor acting for him. Dr Brecher stated:

and there is nothing listed?---Yes, because what – what happened – and I can explain this to the judge – that Roger Downs had a long-standing dispute with the person who assigned their business to me, Arthur Stanton – and everything was complete. But because of this personal animus that the two had, Roger Downs didn’t want to deal with the – with Dr Stanton. They were having, you know, a tiff between them, so he resigned. And it was already done; the contract had been completed. So I just went to Access Law Group to sign what I had done with Dr – with Roger Downs. But Roger Downs did 100 per cent of the contract for me, and all that was missing was just the signature at the – at the bottom.