FEDERAL COURT OF AUSTRALIA

Oceanview Developments Pty Ltd trading as Darwin River Tavern & Darwin River Supermarket v Allianz Australia Insurance Ltd trading as Territory Insurance Office [2020] FCA 852

ORDERS

DATE OF ORDER: | 19 June 2020 |

THE COURT ORDERS THAT:

1. Within 14 days the parties file an agreed minute of order, or competing minutes of order, together with any submissions on the proposed orders and on the future conduct of the proceeding.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ALLSOP CJ:

Introduction

1 The proceedings concern a claim for indemnity for property damage under an Industrial Special Risks policy issued by the respondent (Allianz) to the applicant (Oceanview). The property is in Darwin.

2 Oceanview conducts hotel, supermarket, post office and service station businesses on Lot 2333, 195 Darwin River Road, Darwin River. The land (two lots: 2333 and 2334) was purchased in October 2015 from the National Australia Bank exercising a power of sale; and at the same time the businesses were acquired from the receiver of the debtor (Litchfield), which had also conducted a nursery business on Lot 2334. Oceanview did not buy the nursery business.

3 By agreement with the parties issues of policy construction and indemnity were ordered to be heard first and separately. The issues that have been referred for the purposes of the separate hearing have been reduced by the applicant to a claim for declarations as follows:

1.1. “the Property Insured” under Section 1 of Industrial Special Risks (ISR Mark IV) Insurance Policy number 796694023ISC between the Applicant as insured and the Respondent as insurer (Policy) is not confined or limited to:

1.1.1. the property described in the Schedule of Declared Assets at Court Book vol. 1 page 88;

1.1.2. the property or categories of property which is or are used in or related to the Business of the Applicant as described in the Schedule to the Policy at Court Book vol. 1 pages 84 to 87 and/or in the Schedule of Declared Assets Court Bok vol. 1 page 88;

1.2. the words “Orchid House” in the exclusion on page 3 of the Schedule to the Policy do not refer to the shade sails shown on pp. 170 and 183 of exhibit PW-1 to the affidavit of Paul Winter of 2 September 2019.

4 Declaration 1.2 appears to be the subject of agreement.

5 To understand the nature of the claim for the declarations it is necessary to understand something more in detail about the property, the terms and conditions of the policy and the circumstances of the writing (being a renewal) of the policy.

6 The current policy period was, as reflected in the Closing (Endorsement) dated 12 June 2018, 12 June 2018 to 5 April 2019 4pm local time.

7 On 29 September 2018, a fire caused damage to property being pipes, tanks, drains, cables, switches, sockets, conduits and other infrastructure for water and power, pots, stands, uprights and other equipment and property that had been used in the nursery.

8 The policy had two sections: material loss or damage, and consequential loss. Some of the property that was damaged was used in or in connection with the conduct of the relevant businesses; some was not. Some had been used in the conduct of the nursery business. The dispute concerns whether the material damage section of the policy covers the damaged property, not whether the section concerned with business interruption and consequential loss applies to any loss. For reasons that follow, the proper construction of the policy is that the material damage indemnity is not limited in the way contended for by the insurer.

The property and the layout of the premises

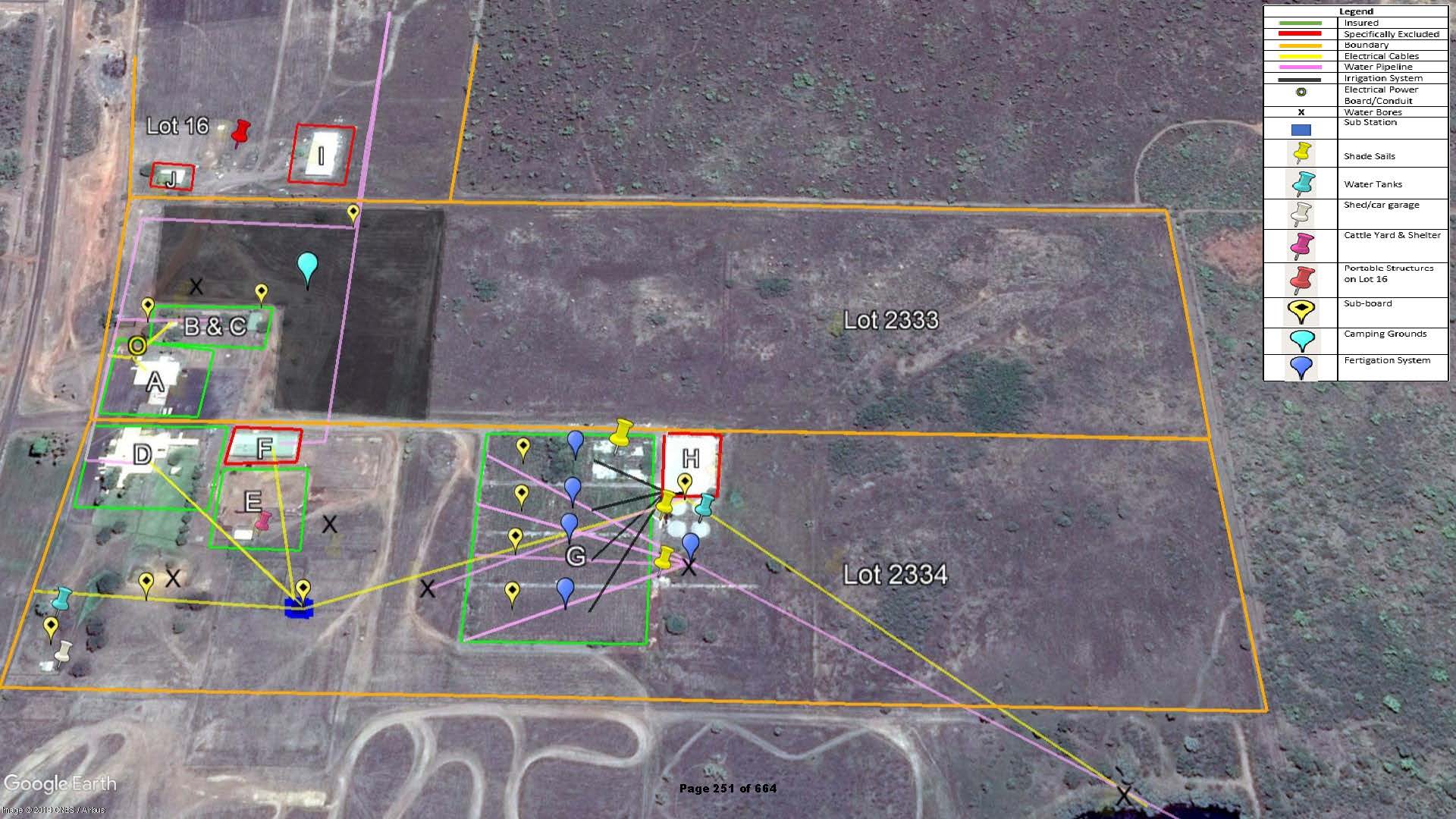

9 Attached to these reasons is a copy of p 251 of the Court Book being a photograph showing Lots 2333 and 2334 and surrounding areas, with various signs and markings to identify relevant parts of the premises.

10 The photograph (to which I will refer as photograph A) is to be read with parts of the affidavit of Mr Winter, a director of Oceanview. Together with a six page extract from the affidavit of Mr Winter (referred to below) it was marked Exhibit C in the proceeding. Photograph A, when examined by landscape view has north at the top of the page so held, in the direction of Lot 16 and south at the bottom of the page thus held. The fire came from the east and reached where E and F are marked, burning through the old nursery in area G. It did not damage the building at H. Damage was done to infrastructure between H and D, F and E. The damage, along with relevant improvements on the land, was described in [12] of Mr Winter’s affidavit. I will refer to the alphabetical markings on photograph A.

11 A on the left centre in the south west corner of Lot 2333 is the site of the supermarket, post office and petrol station. None of this property was damaged by the fire.

12 B immediately to the north of A is the site of eight demountable cabins used in temporary accommodation for visitors. One was damaged by the fire. This hearing is not concerned with indemnity for this damage.

13 C adjacent to B is the site of an ablution block for the cabins. This was not damaged.

14 D to the south of A and in the northwest corner of Lot 2334 is the site of the tavern and bottle shop. This was not damaged by fire.

15 E to the south east of D is the site of a rodeo arena and cattle yard used to hold rodeos. The cattle yard and shelter is marked with a red pin on photograph A. This was not damaged by fire.

16 F to the immediate north of E is the site of the Shed Bar being a metal framed steel clad shed. This was not damaged by the fire. As will be seen, this property was expressly excluded from the material damage insurance in the policy.

17 H at the centre of the northern boundary of Lot 2334 is the site of a large shed containing a two-storey office and flat known as the Orchid House. This was not damaged by fire. This was also property expressly excluded from the material damage insurance in the policy. (Marking H was, somewhat confusingly referred to as “G” in the list of property at [12] of Mr Winter’s affidavit.)

18 There is the site of a small steel shed at the south west corner of Lot 2334 marked with a white pin which shed was used as a garage. It was damaged by fire.

19 The table at [12] of Mr Winter’s affidavit then describes features of electrical and water infrastructure said to service both Lots 2333 and 2334.

(a) There is a 240-volt electrical distribution system marked with yellow markers with a black diamond inside and the yellow lines, being a power distribution board, surge protection devices, power cables and sub-boards. These were damaged by fire.

(b) There is a high voltage substation marked as a blue rectangle below the south east corner of the green square marked E. This was damaged by fire.

(c) There are above and below ground water pipelines being pink lines in Lots 2333 and 2334 servicing these lots and neighbouring properties. These were damaged by fire.

(d) There are five water bores marked with an ‘X’ on Lots 2333 and 2334 all of which were damaged, as was the bore south of Lot 2334 also marked with an ‘X’. Each of these bores had a water pump adjacent. All were damaged by the fire.

(e) There is irrigation and plumbing equipment, being pipes, pumps and sprinklers used to service the camping area. This was damaged by fire. It is unclear where this equipment is. The irrigation system that is marked in black lines in G appears to service the camping ground on Lot 2334, though it is not clear if this is the equipment referred to at [20(d)] below. This equipment was damaged by fire.

20 The table at [12] of Mr Winter’s affidavit then describes infrastructure servicing the nursery on Lot 2334. The nursery is at the site marked G.

(a) There were shade sails on or adjacent to the nursery marked with a yellow pin. They were attached to freestanding steelwork. At the time of the fire they had been removed and were in storage. The table in [12] does not refer to any damage.

(b) There were four water tanks, filtration tanks and associated pipes that are marked on photograph A to the east of G and south of H and identified with a blue pin. They were damaged beyond repair by the fire.

(c) There was a so-called fertigation system consisting of tanks, pumps, electrical cables and other equipment that distributed dissolved fertiliser to the nursery. It was at the site of a blue marker near the bore, south of the four water tanks and Orchid House (H). This was destroyed by the fire.

(d) There was other water distribution and irrigation system equipment that was destroyed by fire. It is not clear where this precisely is located, but it must be on or near the nursery. It was destroyed by the fire.

(e) There were racks and steel uprights in the nursery (G) that were destroyed by fire.

(f) There was high tensile cabling and associated bolts, clamps and turnbuckles that was and were attached to the steel uprights that held the shade sails. These were damaged by the fire.

(g) There was electrical distribution equipment: junction boxes, a conduit, power cables and lights that were destroyed by the fire.

21 Above Lot 2333 on its north western boundary is Lot 16 which has on it a large steel shed, the Machinery Shed marked I on photograph A and a Manager’s House marked J on photograph A. Both were specifically excluded from insurance cover under the policy. Also on Lot 16 is a portable steel structure marked with an orange pin. There were other improvements on Lot 16, being shed coverings to provide shade for animals, water tanks, bores, pumps and electrical equipment.

22 The applicant in address stressed three points about the evidence of the infrastructure described in [12] of Mr Winter’s affidavit, photograph A and the various photographs exhibited to Mr Winter’s affidavits that showed aspects and features of various parts of the property: first, the variety of structures and improvements on the very large blocks of land being Lots 2333 and 2334; secondly, the variety of ways that these structures and improvements could be used in business, whether so used now or in the future (that is, in particular, not limited to the now defunct nursery); and, thirdly, the complexity of the power, water and other infrastructure that services and connects the improvements on both Lots 2333 and 2334, and the adjacent lots.

23 To the extent that there appears to be electrical equipment and cabling in the vicinity of the nursery that assists with the business of the tavern or bottle shop the insurer agrees that damage, to some degree, falls within the indemnity. The applicant claims, however, that under the terms of the policy it is entitled to be indemnified for all damaged property owned by it under the wide words of “Property Insured” under section 1 of the policy, whether or not that property is used in or in connection with any business currently carried on on the land.

The policy

24 The indemnity under the material loss or damage section of the policy (section 1) was in the following terms in cl 1.1:

In the event of any physical loss, destruction or damage (hereinafter in Section 1 referred to as “damage” with “damaged” having a corresponding meaning) not otherwise excluded happening during the Period of Insurance at the Situation to the Property Insured described in Section 1, the Insurer(s) will, subject to the provisions of this Policy including the limitation on the Insurer(s) liability, indemnify the Insured in accordance with the applicable Basis of Settlement.

25 Under the heading “Property Insured” in cl 1.2 the following appeared:

All real and personal property of every kind and description (except as hereinafter excluded) belonging to the Insured or for which the Insured is responsible, or has assumed responsibility to insure prior to the occurrence of any damage, including all such property in which the Insured may acquire an insurable interest, or for damage to which the Insured becomes responsible or assumes responsibility to insure, after the commencement of the Period of Insurance.

26 The phrase “hereinafter excluded” in cl 1.2 is a reference to exclusions applicable. Clause 3.1 dealt with exclusions under section 2 and cl 3.2 dealt with exclusions under sections 1 and/or 2.

27 There was no other clause in section 1 of the policy which could define the phrase “Property Insured”.

28 In cl 3.4.16 in a part of the policy dealing with “all sections” of the policy (material damage (section 1) and consequential loss (section 2)), the following appears concerning the status of headings (such as “Property Insured”):

Headings have been included for ease of reference and it is understood and agreed that the terms and Conditions of this Policy are not to be construed or interpreted by reference to such headings.

29 The difficulty that arises from a literal application of cl 3.4.16 to cl 1.2 is that whilst other provisions under other headings are expressed in self-contained and fully explanatory sentences, here, in order that full meaning can be given to the clause, if the heading of cl 1.2 is ignored, one does not know (at least literally) what the clause concerns, although its text makes it amenable to an understanding that it is a definition of property. Further, not to read the clause as a definition of “Property Insured” would be absurd. Such an error can be corrected in the process of construction by the principle expressed by Dixon CJ and Fullagar J in Fitzgerald v Masters [1956] HCA 53; 95 CLR 420 at 426–427:

Words may generally be supplied, omitted or corrected, in an instrument, where it is clearly necessary in order to avoid absurdity or inconsistency.

See also in the same case McTiernan, Webb and Taylor JJ at 95 CLR 437; and see the helpful part of the judgment of Lord Bingham of Cornhill on the interpretation of business documents and the interpolation of words in Homburg Houtimport BV v Agrosin Private Ltd (The ‘Starsin’) [2003] UKHL 12; [2004] 1 AC 715 at 737–742 [9]–[24] and especially 741 [22]–[23].

30 What appears in cl 1.2 should be read as a definition of the phrase “Property Insured” in cl 1.1.

31 The terms of the policy must be read with the Closing (Endorsement) document dated 12 June 2018 (Exhibit A2 in the proceeding). The Closing (Endorsement) contained a document headed “The Schedule” which contained the following for the period from 12 June 2018 to 5 April 2019 4pm local time at the Insured’s head office:

THE INSURED | Oceanview Developments Pty Ltd T/As Darwin River Tavern & Darwin River Supermarket and/or subsidiary and/or related Corporations as defined under Australian Corporations Law, for their respective rights, interests, inter-relationships and liabilities. |

THE BUSINESS | Principally General Store consisting of Post Office and Fuel Stop, Tavern, Drive thru bottle shop and all other activities incidental thereto. |

THE SITUATION | Principally Lots 2333 & 2334, 195 Darwin River Road, Darwin River and any other situation in Australia owned or occupied by the Insured for the purposes of the Business or elsewhere in Australia where used by the Insured or where the Insured is undertaking work or has goods or property (including where goods or property are stored, or undergoing processing, repairs maintenance, overhaul or improvements). |

...

THE PREMIUM | Premium | As Agreed | ||

Fire Services Levy | As Agreed | |||

Goods & Services Tax | As Agreed | |||

Stamp Duty | As Agreed | |||

which amounts are provisional and shall be adjusted in accordance with the Provisions of this Policy. | ||||

DECLARED VALUES | (In accordance with the Basis of Settlement 1.3 and 2.2) | $ | ||

Section 1 | All Property Insured | 7,300,000 | ||

Section 2 | Gross Profit | 1,200,000 | ||

Increased Cost of Working | 100,000 | |||

Fees | 50,000 | |||

32 There was a combined limit of liability of sections 1 and 2 of $10 million. Sub-limits applied to various types of property under section 1. These included the following:

$ | |

Personal Property, Tools & Effects of | |

Directors, Employees and Visitors | |

Limit per person; and | 5,000 |

In the aggregate for all Directors, Employees and Visitors | 20,000 |

… | |

Paintings, Works of Art, Antiques and Curios | 50,000 |

33 The applicant referred to these particular sub-limits because of the existence of cll 1.3.8 and 1.3.12 in the combined policy wording in cl 1.3 dealing with the Basis of Settlement that related to them:

1.3.8 On Personal Property of the Insured’s Directors and employees and of visitors to the Insured’s premises: The replacement cost at the time and place of replacement.

…

1.3.12 PAINTINGS, WORKS OF ART ANTIQUES AND CURIOS

On paintings, works of art, antiques and curios, none of which form part of the stock in trade or merchandise of the Business:

The cost of restoring and repairing to a condition substantially the same as before the damage plus any reduction in market value caused by the damage. If restoration or repair is not possible, the market value immediately before the damage.

Provided that the liability of the Insurer(s) under this Basis of Settlement shall not exceed the amount of the Sub-Limit stated in the Schedule under the heading “Paintings, Works of Art, Antiques and Curios”.

34 The importance of cll 1.3.8 and 1.3.12 was said by the applicant to be that they provide for the basis of settlement of aspects of cover granted; rather than, as submitted by the respondent, that they provide for an expansion of cover beyond cover otherwise given by the definition of the Property Insured and the terms of the Closing (Endorsement).

35 The Basis of Settlement under cl 1.3 also contains a clause for obsolete property in cl 1.3.2 and “empty premises awaiting demolition” in cl 1.3.9. as follows:

1.3.2 On raw materials, supplies and other merchandise not manufactured by the Insured:

The replacement cost at the time and place of replacement provided that replacement shall have been carried out with reasonable despatch, or if such property is not replaced, the original cost to the Insured of such property or the indemnity value, whichever is the lesser. If such property is obsolete, the Basis of Settlement, whether or not such property is replaced, shall be the original cost to the Insured of such property or the indemnity value, whichever is the lesser.

...

1.3.9 On empty premises awaiting demolition:

The salvage value of the building materials and/or landlord’s fixtures and fittings, net of demolition costs.

36 The Schedule to the policy excluded certain matters from cover. These were identified as: “Manager’s House, sheds etc” – these were the house marked J, and sheds; “Shed Bar” which was marked F; “Orchid House” which was marked H; “Machinery shed” which was marked I; and “Fencing”.

37 On a separate page after the three page Schedule, was a document entitled “Schedule of Declared Assets” as follows:

SCHEDULE OF DECLARED ASSETS

Situation | State | Building $ | Cnts/Stock $ | R.O.D. $ | Plant & Contents $ | Stock $ | Other 3 $ | Total $ |

Lot 2334 Darwin River Road Tavern | NT | 5,000,000 | 150,000 | 5,150,000 | ||||

Lot 2333 Darwin River Road General Store & Post Office | NT | 2,000,000 | 150,000 | 2,150,000 | ||||

Total | 7,300,000 |

THIS TABLE DOES NOT FORM PART OF THE POLICY

38 The applicant stressed the words at the foot of the document that the schedule was not contractual in its fundamental submission that the generality of the phrase “Property Insured” in cl 1.2 when read into cl 1.1 is not limited or constrained by the Schedule of Declared Assets or by what appears adjacent to “Section 1” next to “Declared Values” on the first page of the Schedule (see [31] above). Further, the applicant identified the purposes of this schedule as related to the calculation of co-insurance under cl 1.4.14 and adjustment of premium under cl 3.3.4, which clauses were, relevantly, as follows:

1.4.14 CO-INSURANCE

The Insured is required to insure for full value calculated in accordance with the appropriate Basis of Settlement Clauses, as at the commencement of the Period of Insurance and, in relation to any Property Insured acquired after the commencement of the Period of Insurance, as at the time of acquisition of that property.

In the event of a claim, the moneys otherwise payable under Section 1 of this Policy shall be the proportion that the Insured’s declaration at the time of the commencement of the Period of Insurance of the value of all property insured at the Situation to which the damaged item or items belong bears to 80% of the value of all such property as at the time of commencement of the Period of Insurance calculated in accordance with the appropriate Basis of Settlement Clauses.

Provided that this Clause shall not apply if the amount of the damage does not exceed 10% of the amount of the Insured’s declaration of value for that Situation.

For the purposes of the application of this Clause, the Insured’s Declared Values at any Situation shall not include any allowance for Extra Cost of Reinstatement provided under Clause 1.4.5, or for the costs and expenses referred to in the additional cover provided in Sub-Clauses 1.1.2 to 1.1.7 The Indemnity inclusive.

Provided further that this Clause 1.4.14 shall not apply to property forming part of the property insured, which has been insured under this Policy for the full value stated in a Valuation prepared by an Approved Valuer not less than three years before the commencement of the Period of Insurance, and which an Approved Valuer has updated not more than twelve months prior to the commencement of the Period of Insurance.

Approved Valuer means a Certified Practising Valuer registered with The Australian Property Institute within the relevant property discipline.”

…

3.3.4 ADJUSTMENT OF PREMIUM

(a) The Premium shown is provisional and is calculated on the Declared Values of:

(i) Property Insured;

(ii) Gross Profit and Insured Pay-Roll;

on the day of commencement of each Period of Insurance.

39 Section 2 of the policy deals with consequential loss. Plainly such indemnity is concerned with an ongoing business. The indemnity in cl 2.1 reflects this:

In the event of any building or any other property or any part thereof used by the Insured at the Premises for the purpose of the Business being physically lost, destroyed or damaged during the Period of Insurance by any cause or event not hereinafter excluded (loss, destruction or damage so caused being hereinafter termed “Damage”) and the Business carried out by the Insured being in consequence thereof interrupted or interfered with, the Insurer(s) will, subject to the provisions of this Policy including the limitation on the Insurer(s) liability, pay to the Insured the amount of loss resulting from such interruption or interference in accordance with the applicable Basis of Settlement.

40 It is to be noted that the necessary physical damage that interrupts or interferes with the Business is not defined by “Property Insured” in cl 1.2 of section 1, but is “any building or… property or any part thereof used by the Insured at the Premises for the purpose of the Business”.

41 Further, under cl 3.4.13 cover under section 2 of the policy ceases upon discontinuance of business, as follows:

If during the currency of this Policy the Insured:

(a) permanently discontinues or ceases to carry on the Business or if the Insured’s proprietary interest in the Business ceases otherwise than by death, or

(b) (being a corporation) is placed in liquidation, provisional liquidation under official management, under the control of a receiver and manager or if control over its assets is assumed by a receiver, or

(c) (being a natural person) becomes bankrupt.

then the insurance under Section 2 shall cease unless its continuance is admitted in writing by the Insurer(s).

Such termination of cover shall not apply if any of the events stated in Sub-Clauses (a), (b) or (c) are caused by loss, insured by Section 2 of this Policy, resulting from interruption of or interference with the Business in consequence of damage to property used by the Insured at the Premises.

42 No such clauses exists in section 1 of the policy, noting also at [35] above the obsolete property and premises awaiting demolition provisions in the Basis of Settlement.

The circumstances and context of the taking out of the policy

43 In its submissions, the respondent emphasised aspects of the circumstances and context of the policy. This extrinsic material identifies, it was submitted, the subject matter of the insurance. The applicant contested the relevance of such evidence.

44 The respondent first issued an ISR policy in substantially these terms to the applicant in April 2016. The form of the policy wording was that of the broker (Arthur J Gallagher). The broker also prepared the Closing in each year that contained the Schedule to the policy and the Schedule of Declared Values.

45 Whilst the policy wording remained unchanged, the two schedules did change from the 2016/2017 and 2017/2018 years to the 2018/2019 policy year (the last being the year in which the fire occurred). In these two earlier years the Insured and the Business had been described in the same terms as [31] above, but the Situation had been described as follows:

THE SITUATION Principally As per Schedule of Assets and any other situation in Australia owned or occupied by the Insured for the purposes of the Business or elsewhere in Australia where used by the Insured for the purposes of the Business or elsewhere in Australia where used by the Insured or where the Insured is undertaking work or has goods or property (including where goods or property are stored or undergoing processing, repairs maintenance, overhaul or improvements).

46 The Schedule of Declared Assets in the schedules for these two earlier policy years had included Lot 16, the Manager’s house ($450,000) and removal of debris at “all locations” ($1 million). The 2017/2018 Schedule of Declared Assets read as follows, the only differences in the earlier year being as to slightly lesser amounts:

SCHEDULE OF DECLARED ASSETS

Situation | State | Building $ | Cnts/ Stock $ | R.O.D. $ | Plant & Contents $ | Stock $ | Other 3 $ | Total $ |

Lot 2334 Darwin River Road Tavern | NT | 3,000,000 | 811,370 | 120,000 | 3,931,370 | |||

Lot 2333 Darwin River Road General Store & Post Office | NT | 1,000,000 | 191,000 | 150,000 | 1,341,000 | |||

Lot 16 Darwin River Road Manager’s House | NT | 400,000 | 50,000 | 450,000 | ||||

All Locations (Removal of Debris) | NT | 1,000,000 | ||||||

Total | 6,722, 370 |

THIS TABLE DOES NOT FORM PART OF THE POLICY

Both Schedules of Declared Assets contained the clear statement (in capitals, as set out above) to the effect that the schedule was not contractual.

47 The sub-limits listing in each earlier year contained the same matters set out at [32] above. The premium and declared values were in the same form as at [31] above, except that values were different (lower in the earlier years (2016/2017 and 2017/2018) as to section 1 and significantly lower as to each of the three components of section 2 in the later year (2018/2019)).

48 There had been claims under the 2016/2017 and 2017/2018 policies for damage to an oven, to a bore pump motor, to fencing caused by fire from a controlled burn-off by the bushfire authority, and for loss of stock and damage to a refrigerator.

49 The renewal of the policy in 2018 was handled between Mr Penning and Mr Morrow, underwriters of the respondent, and Ms Dixon, an account underwriter working under Mr Penning’s supervision, on the one hand, and the applicant’s broker, Ms Smyth of Arthur J Gallagher, on the other. The communications between them were not in contest.

50 In January 2018 Ms Smyth, the broker, asked for and was given the claims history for the policy.

51 On 9 February 2018, Ms Smyth asked Mr Morrow by email whether there was any particular information required for renewal and whether a survey would be conducted. He responded by email of the same day that a “revised asset schedule and your coverage summary for the ISR” was needed. This exchange was said by the respondent to reflect the reality that the asset schedule was central to the underwriting process.

52 On 1 March 2018, Ms Smyth sent an email to Mr Morrow attaching an “ISR Slip based on same assets” requesting that terms be worked out on this basis. The ISR Slip identified the Business and the Situation as:

THE BUSINESS: Principally tavern and general store including service station and post office and all other activities incidental thereto

THE SITUATION: Principally Lots 16, 2333, 2334, 2335, 2336 (165 Darwin River Road) Darwin River Road, Darwin River NT and any other situation in Australia owned or occupied by the Insured for the purposes of the Business or elsewhere in Australia where used by the Insured or where the Insured is undertaking work or has goods or property (including where goods or property are stored, or undergoing processing, repairs maintenance, overhaul or improvements).

The Slip set out the Declared Values as:

DECLARED VALUES: | Section 1 | |

(in accordance with | [All property insured] | $6,722,370 |

Clause 1.3 (Basis of | ||

Settlement) | ||

Section 2 | ||

(in accordance with | Gross Profit | $3,207,000 |

Clause 2.2 (Basis of | Increased Cost of Working | $1,000,000 |

Settlement) | Claim Preparation Fees | $100,000 |

The Schedule of Declared Assets attached to the Slip was in the identical form as the Schedule of Declared Assets for the previous year (see [46] above) with one exception: the form provided on 1 March 2018 did not contain the statement in capitals at the bottom as to non-contractual status.

53 At this unpropitious moment a claim was made for fire damage to fencing caused by back-burning being undertaken by Bushfires NT. Ms Smyth notified it on 5 March 2018.

54 On 22 March 2018, Ms Dixon sent an email with a renewal invitation with alternative options with the fire claim paid and the fire claim withdrawn. Mr Penning said in his affidavit that in formulating the offers he had regard to information obtained from the broker “on the assets to be covered, set out in a Schedule of Declared Assets attached to an Insurance Program Summary – Oceanview Developments”. This document (as exhibited to Mr Penning’s affidavit) was in the same form on the Schedule of Declared Assets for the 2017/2018 policy year, but without the broker’s name at the top, and without the statement in capitals set out at [37] above. These documents were the documents sent by Ms Smyth on 1 March 2018 – see [52] above.

55 The Renewal Invitation sent by Ms Dixon to Ms Smyth on 22 March 2018 set out the Business, Situation and/or Premises and Declared Values as follows, noting that under Declared Values there was a statement as to what is the “Property Insured”:

Business | Principally General Store consisting of Post Office and Fuel Stop, Tavern, Drive thru bottle shop and property owners and any other activity incidental thereto. | ||

Situation and/or Premises | Principally LOT 2334 DARWIN RIVER ROAD DARWIN RIVER NT 0841 and any other situation/premises in Australia owned or occupied by the Insured for the purposes of the Business or elsewhere in Australia where used by the Insured or where the Insured is undertaking work or has goods or property (including where goods or property are stored, or undergoing processing, repairs, maintenance, overhaul or improvements). | ||

Declared Values | In accordance with the Basis of Settlement | ||

Section 1 – Material Damage | |||

The following is Property Insured: | |||

Building(s) | $4,400,000 | ||

Contents other than Stock | $1,052,370 | ||

Stock | $270,000 | ||

Total | $5,722,370 | ||

Section 2 – Consequential Loss of Profits | |||

Gross Profit | $3,207,000 | ||

Gross Revenue | Not Insured | ||

Gross Rentals | Not Insured | ||

Insured Pay-roll | Not Insured | ||

Increased Cost of Working | $1,000,000 | ||

Claims Preparation Costs | $100,000 | ||

Loss of Rent | Not Insured | ||

Total | $4,307,000 | ||

56 On 22 March 2018, Ms Smyth responded by email with an ISR slip with two options for asset values. She summarised the approach in the email as follows:

As discussed, sorry to be a pain but they have decided to remove Section 2 completely.

I have attached an ISR slip with:

1. 2 options for Asset Values

A. Current Asset Values including Manager?s House

B. Increased Asset Values but excluding Manager?s House

2. Both Options EXCLUDE any Section 2 cover so TAV is reduced.

3. Deductible Options

A. Current Deductibles

B. Plus 4 x Options with a Major Perils Excess and an All other Losses excess

Can you run these options based on the current Fire Claim proceeding and NOT proceeding?

Please confirm Fire Excess if the bushfire claim does not proceed.

(I take “TAV” to mean Total Asset Value.)

57 The Insurance Program Summary contained the following as to declared values:

DECLARED VALUES: | Section 1 | |

(in accordance with | [All property insured] | As attached |

Clause 1.3 (Basis of | ||

Settlement) |

58 Attached was a Schedule of Declared Assets (without a statement as to the non-contractual status of the document as set out at [37] above) which contained the two options:

SCHEDULE OF DECLARED ASSETS

DARWIN RIVER TAVERN COMPLEX

Situation | Building, P&E, Fixtures $ | Stock $ | Content $ | TAV $ | LAOL $ |

Section 1 Assets | |||||

OPTION A (Current insured Assets) | |||||

Lot 2334 Darwin River Road (Tavern, Bottlemart & associated buildings) | 3,811,370 | 120,000 | |||

Lot 2333 Darwin River Road (General Store, Post Office, Fuel Station & associated buildings) | 1,191,000 | 150,000 | |||

Manager’s House | 400,000 | 50,000 | |||

Total Asset Value | 5,402,370 | 270,000 | 50,000 | 5,722,370 | 6,300,000 |

OPTION B | |||||

Lot 2334 Darwin River Road (Tavern, Bottlemart & associated buildings) | 5,000,000 | 150,000 | |||

Lot 2333 Darwin River Road (General Store, Post Office, Fuel Station & associated buildings) | 2,000,000 | 150,000 | |||

7,000,000 | 300,000 | 7,300,000 | 8,000,000 | ||

Section 2

Gross Profit – DELETED FOR RENEWAL QUOTES

Excluded Buildings & Contents

Manager’s House

Shed Bar

Orchid House

Machinery Shed

Any other buildings not specified

Fencing

59 One sees here higher values for the two main properties (option B), while lesser values are given if the Manager’s House is included. The asset values were given and the identification of assets was made in a context where no business interruption cover (section 2) was sought.

60 On 23 March 2018 Ms Dixon responded setting out additional options for Ms Smyth to consider.

61 On 26 March 2018, Ms Smyth came back to Mr Penning with another proposal:

Hi Travis

Thanks for listening.

If you can please review terms based on the following I would greatly appreciate it. With and without Bushfire claim proceeding.

TAV OPTION 1:

Sec 1: $7,300,000

Sec 2: Nil

TAV $7,300,000

Can you get this rate down to around 0.55% inc Terr (without bushfire claim)?

TAV OPTION 2:

Sec 1: $7,300,000

Sec 2: $1,200,000

AICW $100,000

Claims Prep $50,000

TAV $8,650,000

And this one down to 0.47% inc Terr (without bushfire claim)?

Both above rates would produce a base premium a bit over $40k which would clear the other losses.

And give me rates with the claim proceeding both of the above TAVs please.

Excess: $1,000 all other

Cyclone $20,000

Flood $10,000

Remove Fire excess on the “without bushfire claim” quotes. I will have them confirm in writing that they have Maintained Firebreaks within their boundaries for this to be removed.

If they do pull the fire claim, the original rate quoted of 0.4716% based on a TAV $10m is still a 52% increase from 0.31% which seems extreme.

Thanks again for reviewing it. Talk to you tomorrow.

62 Ms Dixon (not Mr Penning) dealt with this. She had a conversation with Ms Smyth, and then sent the following further options:

As per our conversation please find attached the Options as per your email below;

Option 1a: (Including Claim)

TAV $7,300,000

Combined Limit $8,000,000

Rate incl terror: 1.8342%

Premium: $133,897.47 incl terror

Option 1b: (Excluding Claim)

TAV $7,300,000

Combined Limit $8,000,000

Rate incl terror: 5809%

Premium: $42,404.13 incl terror

Option 2a: (Including Claim)

TAV $8,650,000

Combined Limit $10,000,000

Rate incl terror: 5642%

Premium: $135,306.56 incl terror

Option 2b: (Excluding Claim)

TAV $8,650,000

Combined Limit $10,000,000

Rate incl terror: 0.5065%

Premium: $43,808.79 incl terror

Deductibles:

Flood $10,000

Cyclone $20,000

All Other $1,000

Regarding the Fire excess as per your conversation with Travis.

63 On 5 April 2018, Ms Smyth sent an email to Ms Dixon enclosing a Closing (Renewal) dated 5 April 2018. The email stated:

Hi Travis & Kirsty

Thanks for all the effort on this one, finally nailed it.

It was under attack from AFA the whole time.

Closing attached now and I have used the Net rate you provided.

Can I have a CofC?

Thanks

(“C of C” referred to Certificate of Currency.)

64 The Closing (Renewal) dated 5 April 2018 (Exhibit A1) contained in the Schedule, the Insured, the Business and the Situation, which were in the form of the previous year’s closing (see [45] and [31] above) (the Situation was amended in the 12 June Closing (Endorsement), see [31] above), and the Premium and Declared Values were as in the 12 June Closing (Endorsement) ([31] above). The Schedule of Declared Values was as set out at [37] above, with the statement in capitals as to the non-contractual status of the document there set out.

65 On the same day, 5 April 2018, Ms Dixon sent the Certificate of Currency. The document was also stated not to be contractual. It stated:

This Certificate of Currency is issued as a matter of information only and confers no rights upon its holder. This Certificate of Currency does not form part of the terms and conditions of the Policy and does not amend, extend, replace or alter the terms, conditions, definitions, limitations and exclusions noted therein.

This Certificate of Currency is provided as a summary only of the cover provided and is current only at the Date of Issue. The Policy may be subsequently altered or cancelled in accordance with its terms after the Date of Issue of this notice without further notice to the holder of this notice.

Certain words used in this document and the Policy have special meanings. Please read the Policy Wording, the Schedule and any other document that forms part of the Policy for the terms and conditions of cover.

…

TOTAL DECLARED VALUE: | Section 1: | $7,300,000 |

Section 2: | $1,350,000 |

…

COMBINED LIMIT OF LIABILITY | $10,000,000 |

PROPERTY INSURED | As per the asset schedule & noting the following |

• Lot 2334 Darwin River Rd, Darwin River NT 0841 | |

POLICY WORDING: | Arthur J. Gallagher Industrial Special Risks ISR Mark IV Version 2.0 12.14 |

COVERING: | Physical loss and/or damage to the insured property including loss of profits as per policy wording. |

66 On 12 June 2018, Ms Smyth set an email to Mr Morrow and Ms Dixon as follows:

Morning

Can you please update the address to Lots 2333 & 2334, 195 Darwin River Road, Darwin River and note National Australia Bank as interested Party on this policy and send an updated CofC urgently?

Thanks

Deb

Thus, the changes to the Closing (Renewal) of 5 April 2018 in the Closing (Endorsement) of 12 June 2018 were administrative. The updated certificate of currency was sent the same day (12 June) by Mr Morrow.

67 The Certificate of Currency was amended and the section “Property Insured” was changed from that as set out at [65] above, to:

PROPERTY INSURED | As per the asset schedule & noting the following |

• Lot 2334 195 Darwin River Road Building $5,000,000 | |

• Lot 2333 195 Darwin River Road Building $2,000,000 | |

68 In her affidavit, Ms Dixon referred to the written communications and said (as could be taken from Mr Penning’s affidavit) that there was no mention of a nursery business or any assets or infrastructure associated with a nursery business. Ms Smyth did not depose to any such conversation.

69 Mr Morrow also gave evidence by affidavit. He attached his email communications with Ms Smyth. He said he had no communications with her about an Orchid House, a Shed Bar or a Machinery Shed. That was not disputed.

70 The respondent also read an affidavit of a surveyor Mr Molyneux. He carried out a survey in May 2017. He described his task as the request for “a survey … on two businesses and properties associated with those businesses carried on at [a property at 195 Darwin River Road, Darwin River] by [Oceanview]”: see paras 3 and 4 of his affidavit. He was shown around the operating businesss by the manager. There was no discussion of a nursery business or equipment or infrastructure. He saw, but did not inspect, a large shed (the Shed Bar) and a rodeo area.

71 I admitted into evidence the whole of volumes 1 and 2 of the Court Book. Volume 1 contained an affidavit of the broker Ms Smyth. It was not read. It is contained in Volume 1 at pp 296–330. Her deposed evidence is at pp 296–300, the balance at pp 301–330 were relevant documents. The pages of her deposed evidence should be taken not to be in evidence.

72 Mr Penning said that he had discussions with Ms Smyth. He recalled that the Manager’s House was to be excluded because the occupants were obtaining separate insurance; that the Shed Bar would be excluded because it was not operational; that fencing would not be covered because of previous claims; and he recalled that there was no discussion about the Orchid House or the Machinery Shed (being excluded assets). None of this was disputed. He was unaware in 2017 and 2018 of any nursery business or assets.

73 None of the deponents was cross-examined.

The submissions of the parties

The principal submissions of the applicant insured in chief

74 The applicant identified the governing principles of construction derived fundamentally from authoritative decisions of the High Court as set out in Onley v Catlin Syndicate Ltd as the Underwriting Member of Lloyd’s Syndicate 2003 [2018] FCAFC 119; 360 ALR 92; 20 ANZ Insurance Cases 62-182 at [33]; AIG Australia Limited v Kaboko Mining Limited [2019] FCAFC 96; 20 ANZ Insurance Cases 62-205 at [42]–[43]; Dalby Bio-Refinery Ltd v Allianz Australia Insurance Limited [2019] FCAFC 85; 20 ANZ Insurance Cases 62-203 at [18]. (Reference could also be made to Todd v Alterra at Lloyd’s Ltd [2016] FCAFC 15; 19 ANZ Insurance Cases 62-093 at [42]–[44].)

75 The applicant stressed the clear difference in terms and structure of an ISR policy into material damage and business interruption sections, recognised by Pagone AJA writing for the Victorian Court of Appeal (Buchanan and Dodds-Streeton JJA concurring) in Allstate Exploration NL v QBE Insurance (Australia) Ltd [2008] VSCA 148; 15 ANZ Insurance Cases 61-773 at [8]. It can be accepted that this distinction is of importance. The first (material damage) section is concerned with physical loss and damage to property; the second (consequential loss) section is concerned with interruption to business (by increased cost of working or lower profit or turnover). There will sometimes be a connection between the two covers, or a requirement to take both covers. The consequential loss insurer has an obvious interest in the insured being properly in funds to repair material damage that may affect the on-going consequential loss. The nature of what property must be damaged if the second section is to be engaged does not, however, necessarily conform with the commercial object of the property cover in the first section.

76 The applicant insured focused on the wide and plain words of cll 1.1 and 1.2 of section 1: see [24]–[25] above. Further the Schedule of Declared Assets was not contractual. The specific exclusion of certain property would have been unnecessary if the insurance was limited to the declared assets. The property in the sub-limits and the context of the basis of settlement provisions demonstrate that other property is included in the cover that is not listed in the asset declaration.

77 The declaration of values relates to co-insurance or underinsurance and calculation of premium.

78 The applicant referred to and relied upon CIC Insurance Ltd v Barwon Region Water Authority [1998] VSCA 77; 147 FLR 353; (1999) 10 ANZ Insurance Cases 61-425.

79 The applicant also submitted that the policy was not confined by reference to its use in or in connection with the operation of any of the businesses conducted by the applicant insured. Clause 2.1, the indemnity provision in section 2 reveals such connection (see [39] above). That is naturally so, it was submitted, because of the purpose of section 2 as concerned with business interruption. The different forms of cl 1.1 (read with cl 1.2) and cl 2.1 were, it was submitted, deliberate, reflecting different types, and widths, of cover.

80 Further, it was submitted that the cover for obsolete property (cl 1.3.2), personal property of directors, employees and visitors (cl 1.3.8), empty premises awaiting demolition (cl 1.3.9) and paintings, works of art, antiques and curios (cl 1.3.12) is inconsistent with such a narrowing of the policy.

81 Further, it was submitted that the termination of cover when a business ceases in section 2 (cl 3.4.13 – see [41] above) but not section 1, stands against a restriction based on connection with an existing business.

82 It was submitted by the applicant insured that the restriction sought by the insurer led to an uncertain, inconvenient and uncommercial construction. The precise extent of cover would depend upon, and might move from time to time depending on, the mode of operation of the business. The nature of the relational association for property insurance would be unclear. The nature of the relation in cl 2.1 is caused and related to the nature of business interruption cover.

The principal submissions of the respondent insurer

83 The respondent insurer contended that section 1 only covered property relating to the businesses conducted by the applicant, not the nursery.

84 The argument proceeded as follows: The words of cl 1.2 are a definition which must be construed in the context of the operative provisions and in the commercial setting of the policy. The question is the proper construction of the operative clause, which should be read with the definition inserted. When one reads the indemnity provision (cl 1.1) with cl 1.2 inserted in the context of the Insured, the Business and the Situation in the Schedule in the Closing (Endorsement) it is clear, it was submitted, that the policy was intended to cover property related to the Business identified in the Schedule: being the described “General Store consisting of Post Office and Fuel Stop, Tavern, Drive thru bottle shop and all other activities incidental thereto”. The co-insurance clause (cl 1.4.14 – see [38] above) required, it was submitted, the applicant to insure all property for full value. The Schedule of Declared Assets, though not part of the policy, is essential contextual background. The broad terms of the indemnity are directed to the proper subject matter of the insurance.

85 The fact that the subject matter of the policy is that identified in the Schedule of Declared Assets is reinforced, it was submitted, by the uncontested events of renewal. The negotiation and making of the policy was by reference to the assets and asset values declared.

86 The respondent referred to general principles of construction that are not in doubt: The process requires attention to the language used, the commercial circumstances addressed by the document and the intended objects. The meaning of words must be determined in the light of the instrument as a whole and definitions are to be construed within the operative provisions to which they relate. Recourse to matters external to the contract may be necessary to identify the commercial purpose or object of the contract where that is facilitated by understanding its genesis and market: reference being made to McCann v Switzerland Insurance Australia Ltd [2000] HCA 65; 203 CLR 579 at 589; Mount Bruce Mining Pty Limited v Wright Prospecting Pty Limited [2015] HCA 37; 256 CLR 104 at 117 [49]; Electricity Generation Corporation v Woodside Energy Ltd [2014] HCA 7; 251 CLR 640 at 657; Onley v Catlin Syndicate 360 ALR 92 at [33]; AIG v Kaboko 20 ANZ Insurance Cases 62-205 at [43]; and Charter Reinsurance Co Ltd v Fagan [1997] AC 313 at 384.

87 The respondent also stressed aspects of the judgments in Barwon and referred to the decision of the New South Wales Court of Appeal in Caine v Lumley General Insurance Limited [2008] NSWCA 4; 15 ANZ Insurance Cases 61-756 as of some guiding assistance. A proper reading of these cases and of Independent Publishers Pty Ltd v Royal Insurance Australia Limited (1985) 3 ANZ Insurance Cases 60-679, it was submitted, assists in the conclusion that the wide words of the indemnity are directed to the proper subject matter of the policy: property relating to the business of the applicant.

88 There was nothing problematic, it was submitted, about cover depending on whether property is owned or used in the business: see the extension of cover in the definition of the Situation. It was submitted that the definition of the Situation requires the applicant to demonstrate that property at such other locations (away from Lots 2333 and 2334) is owned for the purpose of the business. Further, there was nothing factually or practically difficult about identifying the property related to the business.

89 Clause 1.1 is to be read with the Schedule, the definitions of the Business and the Situation, in the context of the Schedule of Declared Assets and of the negotiation of renewal.

90 It was submitted that the coverage for obsolete property (cl 1.3.2), personal property (cl 1.3.8), empty premises property (cl 1.3.9) and artworks (cl 1.3.12) were extensions and would not be necessary on the applicant’s construction.

91 Whilst the Schedule of Declared Assets was not a contractual document and whilst it had a purpose in calculating co-insurance and adjusting premium (cll 1.4.14 and 3.3.4), the respondent submitted that it was an important contextual circumstance as the document through which the applicant satisfied its obligation in the co-insurance clause to insure the “Property Insured” for full value at inception.

92 The respondent submitted that the result of the applicant’s submission was uncommercial, denying to the insurer an opportunity to note the risk of redundant and exposed property said to be valuable in a bushfire prone area.

The applicant’s submissions in reply

93 The applicant stressed here the importance of the unambiguous text of the policy especially in cll 1.1 and 1.2: Cherry v Steele-Park [2017] NSWCA 295; 96 NSWLR 548 at [72], [1] and [119]; Mount Bruce Mining v Wright Prospecting 256 CLR at 116 [48]; Australian Broadcasting Commission v Australasian Performing Right Association Ltd [1973] HCA 36; 129 CLR 99 at 109. It also stressed the standard form character of such a policy and the need for a stable meaning by reference to the plain and ordinary meaning of the words used: CIC Insurance Ltd v Bankstown Football Club [1997] HCA 2; 187 CLR 384 at 389; and McCann v Switzerland Insurance Australia 203 CLR at 601.

94 The applicant submitted that the approach of the respondent is to limit the words of cll 1.1 and 1.2 by a form of impermissible implication.

95 The Business in the Schedule is “principally” that set out. The Schedule of Declared Assets does not describe any business, but two situations. The description of the Business is contractual, but general and indefinite and does not limit “Property Insured”.

96 The applicant accepted that it was required by the co-insurance clause (cl 1.4.14) to insure the “Property Insured” for “full value calculated in accordance with the appropriate Basis of Settlement Clauses…”. This does not, it was submitted, define the Property Insured; rather the clause sets out the consequences in terms of indemnity for the Property Insured, if there has been a failure to do so.

97 The applicant submitted that Caine could be distinguished.

Consideration

98 The task of construction of a commercial contract is governed by principles that are not in doubt, subject to some aspects of the legitimacy of examination of mutually known objective circumstances as part of the context of the entry into a written contract. None of the submissions put require any exegesis at first instance of the principles. I simply refer to Electricity Generation Corporation v Woodside Energy 251 CLR at 656–657 [35], and the cases there cited; Mount Bruce Mining v Wright Prospecting 256 CLR at 116–117 [48]–[52] and the cases there cited; Wilkie v Gordian Runoff Limited [2005] HCA 17; 221 CLR 522 at 529 [16]; and Australian Broadcasting Commission v Australasian Performing Right Association 129 CLR at 109–110.

99 At the level of expression of generality none of the applicable principles provides the answer to the problem at hand: see also the remarks of Bell ACJ in Wiggins Island Coal Export Terminal Pty Ltd v New Hope Corporation Ltd [2019] NSWCA 316 at [8]–[9]. Nonetheless, it assists to recognise that competing constructions may be open, but that a choice (of one, necessarily) must be made by reference to text, context and purpose, preference being given to a construction supplying a congruent operation to the various components of the whole: Australian Broadcasting Commission v Australasian Performing Right Association 129 CLR at 109; and Wilkie v Gordian Runoff 221 CLR at 529 [16].

100 The task is one of construction of a wording of a commercial ISR policy, together with the Closing (Endorsement) document with its contents tailored specifically to the circumstances of the Insured. Thus, to the extent that object and purpose of the wording are to be obtained from the specific contractual documents, the Closing (Endorsement) and the Schedule provided the parties with the opportunity to identify and tailor the specific individual features of the policy that the general words of the policy wording may not be able to achieve.

101 Before turning to the text and structure of the policy documents, it can be stated and accepted at the outset that the negotiation of the renewal focused upon the assets and their values that were declared in the documents provided by the broker, that there was no discussion of any property to be insured other than the matters set out in the Schedule of Declared Assets as sent on 1 March 2018 being in the same form as the previous year’s schedule (set out at [46] above), though when sent on 1 and 22 March 2018 it did not contain the non-contractual statement.

102 It is clear that the renewal was rated and priced on the assets and asset values that were provided. Further, the Schedule to the Closing (Endorsement) of 12 June 2018 made clear that the Declared Values in accordance with the Basis of Settlement in cl 1.3 for “All Property Insured” was $7.3 million. An examination of the Schedule of Declared Assets gives content to that figure of $7.3 million – as referable to the value of the “Tavern, General Store & Post Office” plus stock. That, however, is not to say that the only property insured is what is under “Situation” in the Schedule of Declared Assets that did not form part of the policy.

103 What the declared values of all property insured are is one thing, what was the property the subject of the indemnity is quite another.

104 That question is to be answered by construing cll 1.1 and 1.2 in the context of the Closing (Endorsement), the Schedule and the policy provisions otherwise, as a whole.

105 Reading cl 1.2 into cl 1.1 and adjusting the wording and the Closing (Endorsement) for relevance and brevity, the indemnity under the wording was for damage, not otherwise excluded, happening at Lots 2333 and 2334 (the Situation), to (all) real and personal property of every kind and description, except as excluded, belonging to Oceanview, or for which it was responsible or had assumed responsibility to insure.

106 Whilst the definition of the Situation in the Schedule to the Closing refers to the purposes of the Business such does not expressly qualify “Lot[s] 2333 and 2334”. Those lots are “principally” the Situation. The Situation is, however, not so limited; it extended to: “and any other situation in Australia owned or occupied by [Oceanview] for the purposes of the Business” and, further, “elsewhere in Australia where used by [Oceanview] or where [it] is undertaking work [etc.]”. Lots 2333 and 2334 are plainly owned and occupied for the purposes of the Business. That is clear from the context. But the significance of the Situation in cl 1.1 is that that is where the damage happens. It does not provide any relational definitional connection between the Business and the Property Insured. There is no restriction on the extent of the Property Insured by reference to some connection with the Business as defined in the Schedule. Property belonging to Oceanview which is damaged at Lots 2333 and 2334 is covered by the indemnity. The Business as defined in the Schedule is not part of the definition of indemnity for Property Insured under section 1 (as it is in section 2). The damage must happen at the Situation. The Property Insured is all real and personal property of every kind and description belonging to the Insured or for which the Insured is responsible or has assumed responsibility to insure.

107 The setting out of Declared Values in the Schedule and the reference to “All Property Insured 7,300,000” does not form a basis for reading cll 1.1 and 1.2 as all real and personal property etc insofar as such property relates to or is used in connection with the defined Business. The Declared Values section of the Schedule does not concern the identification of what is the Property Insured, rather it deals with the declared value of all that property. The indemnity is for all the real and personal property of Oceanview at the Situation, relevantly Lots 2333 and 2334.

108 The provisions of the Basis of Settlement (cl 1.3) show how certain types of property will be treated for the purpose of indemnity. It is not an apt place to see an endorsement by way of extension of indemnity not provided for under cll 1.1 and 1.2, as argued by the respondent. It includes property that may clearly not have a relational connection with the businesses: see cl 1.3.8 and cl 1.3.12. Further, cll 1.3.9 and 1.3.12 are inapt for inclusion if only the property concerned with the operation of the Business is covered.

109 It can be accepted that cl 1.4.14 requires the Insured “to insure for full value”. But that is not part of the definition of Property Insured. Rather, a failure to do so leads to the co-insurance or averaging consequences otherwise set out in cl 1.4.14. Further, there will be an effect on the adjustment of premium under cl 3.3.4.

110 The respondent’s submission that the definition of the Situation in the Closing (Endorsement) requires a limitation on Property Insured by some express connection between that property and the carrying on of the Business does not withstand textual analysis. The Situation is where the property must be damaged: where the damage “happens”. It is a Situation expressed to be (other than Lots 2333 and 2334) which is owned or occupied by the insured for the purpose of the Business. In respect of Lots 2333 and 2334 there was no doubt but that the Business was being carried on. But, at such situations, the policy covers all property defined in cll 1.1 and 1.2 in section 1.

111 This construction is not uncommercial, though, given the nature of the rating of such a policy, especially for section 1, it is not difficult to understand why the insurer feels aggrieved that it was not informed of the property that would fall within the coverage. That may be a question of non-disclosure and its consequence; or one for the co-insurance provisions, or both.

The decisions of Barwon and Caine

Barwon

112 There was striking similarity between both the policy and terms, and the controversy here and in Barwon 147 FLR 353. The policy in Barwon was an ISR policy with a material damage section that had a definition of “Property Insured” in similarly wide and substantially the same terms to cl 1.1 and 1.2 here. A bridge had not been disclosed as part of the property to be insured. A reading of the whole of the judgment of Ormiston JA is (as one would expect of such a learned and experienced commercial judge) valuable. In particular, at 365–366 his Honour discusses the co-insurance clauses in the policy and, perhaps importantly for any later issues to be resolved here, the relationship between the existence of the co-insurance clause and the obligation of disclosure; and at 366 as to the adjustment of premium. In discussing the width of the coverage Ormiston JA said the following at 364 in respect of the very similar indemnity clause as here:

That the subject matter of the policy is not meant to be confined to items of property specified in the policy or set out in any "schedule" or "declaration" is made clear from the extensive range of items covered in the "Basis of Settlement" clause and by the specific inclusion in the definition clause of all property in which the insured "may acquire an insurable interest during the period of insurance", thereby bringing within its scope property which could not have been declared up to or on the day of the commencement of the relevant period of insurance. Notwithstanding that the argument of the appellant might appear to have suggested the contrary, I would conclude that the policy covered all the Authority's property regardless of the making of declarations for the various purposes for which they are required under the policy. This conclusion, as I would see it, is fundamental to an understanding of the manner in which the policy was intended to operate.

113 Justice Phillips, who agreed with the judgment of Ormiston JA said (at 375) that he was “troubled” that:

the Authority can claim successfully for damage to property which was never included in any of the recurrent declarations of value, required under the policy for the purpose of calculating premium.

114 His Honour then noted (at 376) that there was an argument not presented that:

the three items of property for damage to which the Authority was now claiming were not insured under the policy because of the Authority's failure to include them, either directly or indirectly, in a relevant declaration of value.

115 Justice Kenny agreed in unqualified terms with Ormiston JA.

116 It is to be noted that the policy in Barwon contained a provision that the Schedule of Declared Values attached to and formed part of the policy for the purpose of co-insurance. Here, of course, the same schedule was expressly not part of the contractual documents.

117 One can also see a similarity in the form of the Schedule, including, importantly, the definition of “the Situation and/or Premises”: at 147 FLR 355.

118 Whilst not determinative, Barwon gives support to the structure of the policy here contended for by the applicant. It is a structure that the plain words of the policy support.

119 Before turning to Caine, one matter should be reinforced about the words of the policy. It can be accepted, without reservation, that wide words of any indemnity provision may retain their width, but only be referable to a certain and limited subject matter that the objective context reveals to be intended to be indemnified. That is why the Closing (Endorsement) and its wording are so important. If “Property Insured” was to be given a meaning only by reference to what was declared in a schedule or by reference only to property connected in some (prepositional) way with the Business, rather than damage happening at the Situation to any real and personal property of the Insured, the Closing (Endorsement) was the place to draw that limitation of subject matter. The respondent submitted that such limitation is to be found in the definition of “Situation”. I do not agree. The role of a relationship between the Business and the Situation there is to identify expressly places, other than Lots 2333 and 2334, where there is a business, and so a place where property of the Insured is covered if damage happens at that Situation. It does not qualify damage happening at the Situation to “all real and personal property of every kind and description… belonging to the Insured or for which the Insured is responsible or has assumed responsibility” in cl 1.2, which is what is covered at that Situation, where the Insured carries on the Business.

120 The difficulty here with the argument that the use of the extrinsic circumstances is only to identify the subject matter of the indemnity, is that the terms of the Closing (Endorsement) and the policy wording, must be adjusted or rewritten for the argument to succeed.

Caine v Lumley General

121 The respondent insurer placed reliance on Caine v Lumley General 15 ANZ Insurance Cases 61-756. There, the Court found that a declaration of the value of property insured in a schedule, in the context of a policy that required that the appellants declare the value of all Property Insured, was a statement of the Property Insured. The case concerned a caravan park and the insurance of caravans thereat and, in particular, whether the valuable annexes to the caravans were separately insured, they not being listed as declared assets.

122 The Court (McColl JA, with whom Mason P and McClellan CJ at CL agreed) expressed the view (importantly, in relation to a schedule of assets that was part of the policy) that the annexes were not separately insured, saying at 15 ANZ Insurance Cases 61-756 at p 76,525 [62]:

Accordingly, in my view an objective interpretation compels the conclusion that the list of “declared assets” in the Schedule was intended to comprehend all the major items of property at the caravan park and that the reference to “caravans” both in the Schedule and E15 was intended to encompass the entire structure.

123 The extent of cover was identified by a clause (Clause B) that is set out at 15 ANZ Insurance Cases 61-756 at p 76,515 [20] that made the conclusion of the Court plainly open (indeed, with respect, correct) that the Schedule of assets was to be understood as integral to the identification of the subject matter of the indemnity: the Property Insured. In reasoning to the conclusion at [62] that it set out above, McColl JA said the following at [60] and [61]:

60 The extent of cover clause in Section 1 provided that the respondent would, inter alia, indemnify the appellants “up to the value of the Limit(s) and Sub-Limit(s) of Liability referred to in the Schedule”. The Schedule both set out the details of the appellants’ cover (see definition of “Schedule” in the General Definitions) and represented the appellant’s declaration of the value of the “Property Insured”. Although the definition of the latter concept was broad, it was refined in relation to the particular risk by the requirement that the appellants declare the value of the “Property Insured” at each Situation, calculated in accordance with the Basis of Settlement clause.

61 Thus the enumeration of property and values in the Schedule under the heading “Material Damage Declared Assets” represented, in my view, the appellants’ identification of the property at the caravan park which they had insured for material damage. The identification of “caravans” in the Schedule without reference to the tropical roofs or annexes demonstrated objectively that those three structures were regarded as constituting a “caravan” for the purposes of the listing “Caravans Indemnity”. This conclusion is reinforced by the enumeration of other items of property in the Schedule such as machinery (including hose reels), barbecues, pergolas, washers and dryers. A Schedule which descends to that level of particularity cannot sensibly be understood to have excluded what on the appellants’ case were the most substantial items of property at the caravan park.

124 The definition of the word “Schedule” to which McColl JA referred made it clear not only that it was contractual but that it related to the extent of cover, saying (set out at p 76,514 [17]):

‘Schedule’ means the attachment which forms part of the Policy and shows Your Policy number, together with the details of Your cover including the Sections of the Policy which apply

125 Here the policy terms are different. The Schedule of Declared Assets is non-contractual; and it was not defined as in Caine. There is no extent of cover clause in like terms that directs one to the (contractual) Schedule. The indemnity and the Property Insured here is found in cll 1.1 and 1.2 and linked to the definition of Situation by reference to where the damage happens.

126 Neither Barwon nor Caine is determinative. Both are decisions on particular wording, though the wording in Barwon is much closer to the facts here.

Conclusion

127 For the above reasons, I would answer the questions to this point in the manner contended for by the applicant insured.

128 It is not clear to me the extent to which there may now be a debate about the property covered by the policy. In effect my conclusion is that the applicant is entitled, subject to the operation of the policy and any question of non-disclosure to indemnity under section 1 for damage to all Property Insured as described in cl 1.2 other than excluded property happening at the Situation defined in the Closing (Endorsement) that is, relevantly, principally Lots 2333 and 2334.

129 I will give the parties an opportunity to consider whether the suggested declarations sought set out at [3] above are the most appropriate way to resolve the case to this point and to consider the question of costs. At the moment, I consider that it may be premature to award costs to date; but I will hear the parties.

Orders

130 I will direct the parties to bring in short minutes and short written submissions about appropriate orders and the conduct of the balance of the proceeding.

131 By way of postscript, I had intended to deliver this judgment in February or at the latest by the first half of March. The difficulties, delays and calls on my time in connection with the Court caused by COVID-19 have delayed the resolution of the issues for decision, a matter which I regret given the aims of this list.

I certify that the preceding one hundred and thirty-one (131) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Chief Justice Allsop. |

Photograph A