FEDERAL COURT OF AUSTRALIA

Brown v Commissioner of Taxation [2020] FCA 817

ORDERS

Applicant | ||

AND: | Respondent | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Having regard to sections 5(1)(f) and 5(2)(b) of the Administrative Decisions (Judicial Review) Act 1977 (Cth) (ADJR Act), the decision of the delegate of the Commissioner of Taxation dated 5 March 2019 under s 269-35(4A) of Schedule 1 to the Taxation Administration Act 1953 (Cth) is set aside pursuant to s 16 of the ADJR Act, and the matter remitted to the Commissioner for determination according to law.

2. The Respondent pay the Applicant’s costs, as agreed or assessed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

(REVISED FROM THE TRANSCRIPT)

KERR J:

1 This is an application pursuant the Administrative Decisions (Judicial Review) Act 1977 (Cth) (ADJR Act) for judicial review of a decision by the Commissioner of Taxation.

2 The decision in respect of which the Applicant seeks judicial review is described in the application as the:

decision of the Respondent dated 5 March 2019 under section 269-35(4A) of Schedule 1 to the Taxation Administration Act 1953 (C’th) (TAA) (Decision) that the Applicant had not satisfied the Respondent of the matters under subsection 269-35(2) of Schedule 1 to the TAA, namely that he is not liable to a penalty under Division 269 of Schedule 1 to the TAA because the Applicant took all reasonable steps, or there were no reasonable steps he could have taken, to ensure that the following happened:

(i) cause Trojan Security (AU/NZ) Pty Ltd formerly known as Agile Security (AU/NZ) Pty Ltd (the Company) to comply with its obligations;

(ii) cause an administrator of the Company to be appointed under section 436A, 436B or 436C of the Corporations Act 2001 (C’th) (CA); or

(iii) cause the Company to begin to be wound up within the meaning of the CA.

3 It is useful to identify at the outset what is, and what is not, in issue in this proceeding.

4 Section 269-35(4A) falls within Division 269 of Schedule 1 to the Taxation Administration Act 1953 (Cth). Section 269-5 explains the rationale of that Division as follows:

The object of this Division is to ensure that a company either:

(a) meets its obligations under:

(i) Subdivision 16-B (obligation to pay withheld amounts to the Commissioner); and

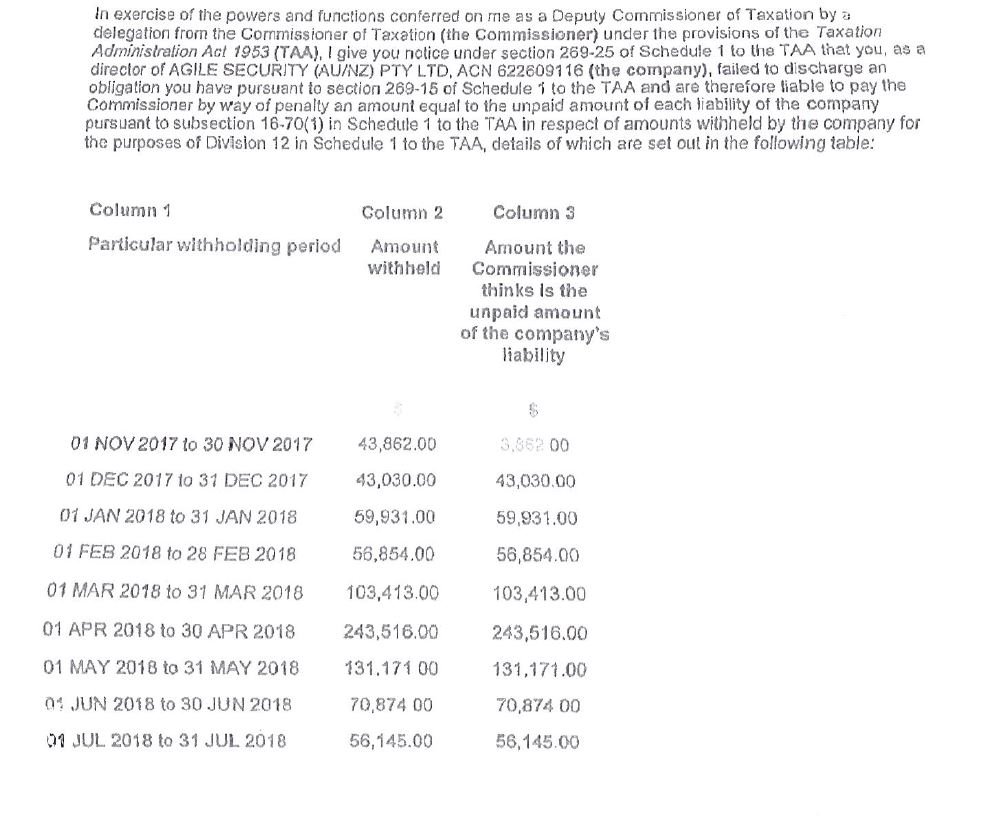

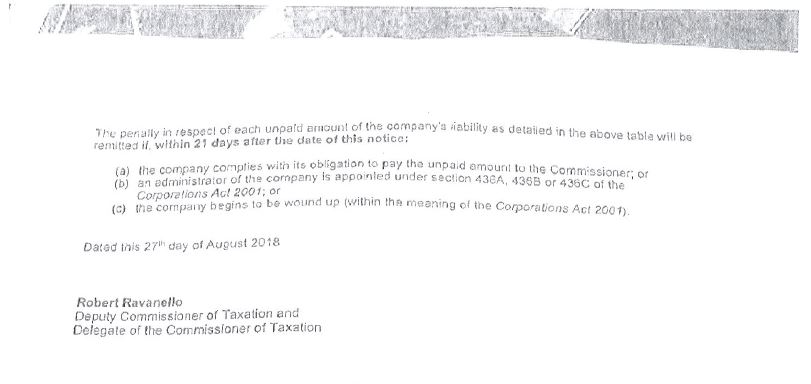

(ii) Division 268 (estimates of PAYG withholding liabilities and superannuation guarantee charge); and

(iii) Part 3 of the Superannuation Guarantee (Administration) Act 1992 (obligation to pay superannuation guarantee charge); and

(iv) Divisions 33 and 35 of the * GST Act in respect of * assessed net amounts; and

(v) Division 162 of the GST Act in respect of GST instalments (within the meaning of the GST Act); or

(b) goes promptly into voluntary administration under the Corporations Act 2001 or into liquidation.

Note: The directors' duties are enforced by penalties on the directors. A penalty recovered under this Division is applied towards meeting the company's obligation.

5 The obligations with which directors of a company are obliged to cause the company to comply are set out in s 269-10. In very crude summary, the relevant obligations of the company are, inter-alia, to pay to the Commissioner when due any sums the company has withheld as pay as you go taxation (PAYG) and amounts due in respect of the superannuation guarantee charge (SGC).

6 The legislative architecture as implements the objective of the Division then provides:

269-15 Directors' obligations

Directors' obligations

(1) The directors (within the meaning of the Corporations Act 2001) of the company (from time to time) on or after the initial day must cause the company to comply with its obligation.

(2) The directors of the company (from time to time) continue to be under their obligation until:

(a) the company complies with its obligation; or

(b) an administrator of the company is appointed under section 436A, 436B or 436C of the Corporations Act 2001; or

(c) the company begins to be wound up (within the meaning of that Act).

7 Directors who fail to meet their obligation in one of those manners become, in the circumstances provided for by s 269-20, liable to pay the Commissioner a penalty. The penalty for which a director becomes liable at the end of the due day is equal to the unpaid amount of the company’s liability to the Commissioner (s 269-20(5)).

8 However, while the liability to pay that penalty is then incurred the Commissioner is prohibited from commencing proceedings to recover it until the expiry of 21 days from the date on which the director has been given a written notice: s 269-25(1).

9 For that purpose, the notice must:

(a) set out what the Commissioner thinks is the unpaid amount of the company's liability under its obligation; and

(b) state that you are liable to pay to the Commissioner, by way of penalty, an amount equal to that unpaid amount because of an obligation you have or had under this Division; and

(c) explain the main circumstances in which the penalty will be remitted.

10 By way of explanation of what is meant by the “main circumstances” in which a penalty is remitted, s 260-30(1) provides:

(1) Subject to subsection (2), a penalty of yours under this Division is remitted if the directors of the company stop being under the relevant obligation under section 269-15:

(a) before the Commissioner gives you notice of the penalty under section 269-25; or

(b) within 21 days after the Commissioner gives you notice of the penalty under that section.

11 However, as has been noted, a director of a company that has not made the payments required of it remains subject to the obligation provided for by s 269-15 until:

(a) the company complies with its obligation; or

(b) an administrator of the company is appointed under section 436A, 436B or 436C of the Corporations Act 2001; or

(c) the company begins to be wound up (within the meaning of that Act).

12 Assuming the penalty is not remitted, s 269-35 then provides for three potential defences a director can advance to avoid liability for a penalty. The defences available are stated in the following terms:

269-35 Defences

Illness

(1) You are not liable to a penalty under this Division if, because of illness or for some other good reason, it would have been unreasonable to expect you to take part, and you did not take part, in the management of the company at any time when:

(a) you were a director of the company; and

(b) the directors were under the relevant obligations under subsection 269-15(1).

All reasonable steps

(2) You are not liable to a penalty under this Division if:

(a) you took all reasonable steps to ensure that one of the following happened:

(i) the directors caused the company to comply with its obligation;

(ii) the directors caused an administrator of the company to be appointed under section 436A, 436B or 436C of the Corporations Act 2001;

(iii) the directors caused the company to begin to be wound up (within the meaning of that Act); or

(b) there were no reasonable steps you could have taken to ensure that any of those things happened.

(3) In determining what are reasonable steps for the purposes of subsection (2), have regard to:

(a) when, and for how long, you were a director and took part in the management of the company; and

(b) all other relevant circumstances.

(3AA) If the obligation referred to in subparagraph (2)(a)(i) is an obligation to pay an amount of an estimate of an underlying liability under Division 268, that reference to an obligation includes a reference to the obligation to pay the underlying liability.

(3AB) For the purposes of subsection (3AA), assume that the underlying liability exists as identified in the notice of the estimate under section 268-15.

Superannuation guarantee charge and assessed net amounts--reasonably arguable position

(3A) You are not liable to a penalty under this Division to the extent that the penalty resulted from the company treating the Superannuation Guarantee (Administration) Act 1992 or the * GST Act as applying to a matter or identical matters in a particular way that was * reasonably arguable, if the company took reasonable care in connection with applying that Act to the matter or matters.

When you can rely on this section

(4) For the purposes of:

(a) proceedings in a court to recover from you a penalty payable under this Division; or

(b) proceedings in a court against you in relation to a right referred to in paragraph 269-45(2)(b) (directors jointly and severally liable as guarantors);

subsection (1) or (2) of this section does not apply unless you prove the matters mentioned in that subsection.

(4A) For the purpose of the Commissioner recovering from you a penalty payable under this Division (other than as mentioned in subsection (4)), subsection (1) or (2) does not apply unless:

(a) you provide information to the Commissioner during the period of 60 days starting on the day the Commissioner:

(i) in the case of the Commissioner recovering the penalty under section 260-5 (Commissioner may collect amounts from third party)--gives you a notice under subsection 260-5(6) in relation to the penalty; or

(ii) otherwise--notifies you in writing that he or she has recovered any of the penalty; and

(b) the Commissioner is satisfied of the matters mentioned in subsection (1) or (2) of this section on the basis of that information.

13 That - regrettably long - introductory discussion provides the context required to identify what is, and is not, in issue in this application. That question has greater than usual significance in this proceeding. That is because it is uncontentious that the Commissioner has commenced proceedings in the Supreme Court of Queensland for the recovery of the balance of the claimed penalty amounts. It is also uncontentious that in those proceedings the Applicant (the respondent to those proceedings) has advanced a defence in reliance on the provisions of s 269-35(2) and (3) as are also in issue in this matter.

The basic facts

14 The Applicant, Mr Brown, served as a director of ACN 622 609 116 Pty Ltd trading as Trojan Security (AU/NZ) Pty Ltd (formerly known as Agile Security (AU/NZ) Pty Ltd) from 31 May 2018 until his resignation on 1 September 2018.

15 For the period 31 May 2018 until 15 June 2018, both he and Mr Brinkies were its directors.

16 On 15 June 2018, Mr Brown became the company’s sole director. He remained so until he resigned on 1 September 2018.

17 Mr Brinkies thereupon resumed office as the company’s sole director until it was wound up in insolvency on 28 February 2019 by order of the Supreme Court of Western Australia on the application of a third party creditor, National Security Services Australia Pty Ltd.

18 When the Applicant became a director of ACN 622 609 116 Pty Ltd, that company was already in significant default of its obligations to pay withheld sums of PAYG to the Commissioner. It does not appear to be contentious that those amounts were already in excess of $600,000.00. In an affidavit filed in these proceedings on 10 October 2019, the Applicant deposes that he only became aware of that circumstance in August 2018. He had at that time been surprised at the size of the amounts owing. He deposes that he instructed Mr Brinkies (who had continued in a management and operations role within the company, and who had advised him of the outstanding liabilities) to immediately contact the Australian Taxation Office to negotiate a payment arrangement.

19 I will return to what the Applicant later submitted to the Commissioner as his reasons for contending that he had taken all reasonable steps to ensure that one of the events provided for in s 269-35(2)(a) happened or, alternatively, there were not reasonable steps he could have taken to ensure they did. For present purposes however it is sufficient to note that, after requesting further information, the Commissioner ultimately was unpersuaded that the instalment arrangements the company had proposed should be entered into.

20 It is important to note that as at August 2018 when the Applicant became aware of the company’s outstanding withheld PAYG amounts, he had been already a director of the company for a period in excess of 30 days. That is significant only insofar as s 269-20(3) provides a 30 day safe-haven provision for new directors before they will become personally liable for penalties for outstanding company liabilities. Mr Kaskani, counsel for the Commissioner, did not accept that the Applicant could have avoided such liability simply by resigning and ceasing to hold office within that period. I note however the observations of Heydon JA in Deputy Commissioner of Taxation v Saunig [2002] NSWCA 390; 55 NSWLR 722 at [23] (albeit in obiter, and in respect of repealed and re-enacted provisions with a shorter time frame) that the only course open to a director who cannot secure the cooperation of his fellow directors is “to resign and thus escape any continuing liability”. However, that question does not arise in the facts of this case. It need not be determined.

21 Having regard to the statutory architecture of Div 269, whatever may have been his earlier options the Applicant’s counsel Mr Frenkel does not dispute that by the time the Applicant became aware that the company of which he had become a director had withheld PAYG he had become personally liable to pay as a penalty to the Commissioner (subject possibly to remission and to any available defence pursuant to s 269-35) an amount equal to the unpaid amounts due on account of PAYG the company should have, but had not, paid.

22 However, until the Commissioner issued the Applicant with a s 269-25 notice the Commissioner could not commence recovery proceedings in respect of that penalty.

23 On 27 August 2018 the Commissioner issued the Applicant with such a notice. The Applicant received it on 29 August 2018. The notice was in the following terms:

24 While his underlying liability does not turn on the point, it may be seen that of the total, only the last two amounts were in respect of sums withheld by the company after the Applicant’s appointment as director.

25 Subsequently, the Commissioner issued the Applicant with two further s 269-25 Notices.

26 On 22 October 2018 (after the Applicant had resigned as a director) he was issued with a notice for a further amount of $89,866.00. That was the amount that the Commissioner had estimated as PAYG withheld by the company for the withholding period of 1 August 2018 to 31 August 2018. It will be recalled that the Applicant had been the sole director of the company in August 2018.

27 Pursuant to s 269-10(4), the Commissioner’s estimate can operate to render a director personally liable to a penalty in the relevant amount. That is subject to any available defence provided for by s 269-35. Mr Frenkel does not suggest that the estimate did not have that effect in the present instance: subject to any defence.

28 On 6 February 2019, the Commissioner issued the Applicant with a third notice: on this occasion in respect of amounts that the company had withheld from the Commissioner in respect of superannuation guarantee charges. That notice was in respect of three periods: 01 April 2018 to 30 June 2018 where the amount advised as remaining unpaid was $42,293.82; 01 Jan 2018 to 31 March 2018 where the amount advised as remaining unpaid was 44,249.99; and 01 October 2017 to 31 December 2017 where the amount advised as remaining unpaid was $31,559.30.

29 As in the case of the two Director Penalty Notices (DPNs) issued in respect of PAYG, that notice did not create any new liabilities. It was simply the case that, until that notice was given, the Commissioner had been precluded from commencing proceedings to recover those sums as a penalty.

The issue to be decided

30 In this proceeding, brought pursuant to the ADJR Act, the Applicant takes no point that that the third notice omitted any reference to the recipient’s capacity to have the relevant penalties remitted if an administrator were appointed or the company began to be wound up within 21 days.

31 The sole issue is the validity (or otherwise) of the subsequent decision of the Commissioner made pursuant to s 269-35(4A) with respect to the defence the Applicant later advanced. The application therefore requires close attention to be given to how s 269-35(4A) fits within the scheme provided for in the Act with respect to the relevant defence.

32 The defence on which the Applicant sought to rely in his communications, via his legal representatives, with the Commissioner was that provided for in s 269-35(2). It is that defence which the Commissioner later rejected, or purportedly rejected, and which is the subject of the present proceeding. His legal representatives made submissions to the Commissioner that determining what are “reasonable steps” for the purposes of that defence required the Commissioner to give attention to the factors identified in s 269-35(3).

33 Neither party submits that the defence provided for by s 269-35(1) is material. Both are agreed that s 269-35 subss (3AA), (3AB) and (3A) are also immaterial.

34 The defences of “illness” and “all reasonable steps” as are provided for in s 269-35(1) and (2)-(3) then bifurcate into two distinct and separate decisional streams:

(4) For the purposes of:

(a) proceedings in a court to recover from you a penalty payable under this Division; or

(b) proceedings in a court against you in relation to a right referred to in paragraph 269-45(2)(b) (directors jointly and severally liable as guarantors);

subsection (1) or (2) of this section does not apply unless you prove the matters mentioned in that subsection.

(4A) For the purpose of the Commissioner recovering from you a penalty payable under this Division (other than as mentioned in subsection (4)), subsection (1) or (2) does not apply unless:

(a) you provide information to the Commissioner during the period of 60 days starting on the day the Commissioner:

(i) in the case of the Commissioner recovering the penalty under section 260-5 (Commissioner may collect amounts from third party)--gives you a notice under subsection 260-5(6) in relation to the penalty; or

(ii) otherwise - notifies you in writing that he or she has recovered any of the penalty; and

(b) the Commissioner is satisfied of the matters mentioned in subsection (1) or (2) of this section on the basis of that information.

35 The Commissioner thus may bring proceedings in a court, in which case s 369-35(4) casts the burden of proving the facts going to the defence on the director or former director of the relevant company.

36 Alternatively, the Commissioner potentially has available certain “self-help” remedies as would to permit him or her to recover in whole or in part a penalty that is due. The provision that regulates how the defence relevant to these proceedings can be relied upon against the Commissioner when recovery is sought by means of such a “self-help” remedy – i.e. other than by taking proceedings in a court - is provided for in s 269-35(4A).

37 The language of s 269-35(4A), while addressed to the entitlement of a person who may seek to rely on the defence, nevertheless assumes that the Commissioner must give the notice provided for in s 269-35(4A)(a)(i), or otherwise notify the director (or former director) in writing if he or she seeks to enforce the penalty provisions other than in a court.

38 It is the giving of such notice or information in writing that triggers a right in the director or former director to provide, within 60 days, any information on which he or she may wish to rely as might satisfy the Commissioner of the existence of a sound defence.

39 The Commissioner must then make his or her decision under s 269-35(4A) “on the basis of that information” (being the information provided by the director or former director) within 60 days of his or her having been so notified: s 269-35(4A)(b). That element of the statute has two important aspects. The first is that the director or former director must be provided an opportunity to advance a potential defence if the Commissioner wishes to rely upon non-curial self-help measures. Absent such notice being given, the processes of procedural fairness required by the Act are incapable of being engaged. The consequence, necessarily implied as matter of statutory construction, is that if the Commissioner does not give such a notice he or she cannot lawfully rely on the provisions of Div 269 to authorise his or her use of self-help provisions for the recovery of a penalty.

40 Second, as Mr Kaskani submits, the provision necessarily implies that if notice is given and responded to the Commissioner is required to make his or her decision on a limited basis. The decision must be made on the basis of the information the director or former director provides to the Commissioner. That, of course, does not require the Commissioner to accept that information as credible. However, it does imply that the information provided and the representations advanced on behalf of a director or former director defines the scope of what is put in issue as a defence in those circumstances.

Background facts and decision

41 In respect of the penalties identified in the first DPN, the Commissioner gave notice on 9 October advising that the amount of $758,796.00 remained unpaid and that enforcement proceedings - including those against third parties - would follow.

42 Within the following 60 days, the Applicant’s legal advisors wrote three letters to the Commissioner on his behalf dated respectively 20 November 2018, 12 February 2019 and 27 February 2019.

43 Neither party submits that the 12 February letter is material. I will not discuss it further.

44 The 20 November letter made the following representations:

Background

We are instructed that:

1. on 1 November 2017, the Company was registered, with Mr Justin Brinkies appointed as the director of the Company;

2. on 31 May 2018, Mr Brown was appointed as a director of the Company;

3. on 15 June 2018, Mr Brinkies was removed as a director of the Company;

4. in or around late August 2018, the Company became aware that it had accumulated a debt to the ATO in respect of its taxation obligations;

5. on 24 August 2018, Mr Brinkies on behalf of the Company contacted the ATO and proposed a payment arrangement to satisfy the debt in weekly instalments of $10,000, with a larger instalment of $20,000 every third week;

6. by email on 24 August 2018, the ATO requested that the Company provide copies of its profit and loss statement, balance sheet, and current aged creditors and debtors listing by close of business on 28 August 2018 in order to consider the payment proposal;

7. by email on 24 August 2018, the Company complied with the ATO's request for additional information and documents. In addition to the requested documents, the Company also provided the ATO with its budget for the period July 2018 to June 2019 (First Payment Proposal);

8. on 27 August 2018, being three (3) days after the Company contacted the ATO to discuss the debt and negotiate a payment arrangement, Mr Brown was issued with the First DPN;

9. having received no response to the First Payment Proposal, on 29 August 2018 the Company made a payment of $10,000 to the ATO in accordance with the First Payment Proposal. A copy of the payment receipt was emailed to the ATO on the same day;

10. on 1 September 2018, Mr Brown resigned and was removed as a director of the Company, and Mr Brinkies was reappointed;

11. the Company thereafter continued its efforts to negotiate a payment arrangement until 4 October 2018, when it applied to have the Statutory Demand issued to the Company on 12 September 2018 set aside;

12. on 9 October 2018, the ATO issued a notice of legal action to Mr Brown; and

13. on 22 October 2018, Mr Brown was issued with the Second DPN.

Application of the Defence

We consider that during his time as a director of the Company, Mr Brown, together with Mr Brinkies took all reasonable steps to ensure that the Company complied with its taxation obligations including by having a representative of the Company immediately seek to negotiate a payment arrangement with the ATO for payment of the debt in full.

Our client considers the ATO's rejections of the Company's First Payment Proposal and subsequent payment proposals to be unreasonable in the circumstances.

We note that:

1. Mr Brown was a director of the company for only ninety-three (93) days. Having regard to the date the Company became aware of its debt (on or around 24 August 2018), Mr Brown had only eight (8) days within which to ensure that the Company complied with its taxation obligations;

2. upon becoming aware of the debt, the Company contacted the ATO for the purposes of negotiating a payment arrangement to satisfy its debt and made the First Payment Proposal;

3. notwithstanding that the ATO gave the Company until 28 August 2018 to provide the requested information and documents in order to consider the First Payment Proposal, on 27 August 2018 the ATO issued the First DPN;

4. having received no response from the ATO regarding the First Payment Proposal, on 29 August 2018, the Company made a payment of $10,000 to the ATO in accordance with the First Payment Proposal;

5. the ATO did not respond to the First Payment Proposal until 10 September 2018, after Mr Brown had been removed as a director.

We consider that the defence set out in section 269-35(2)(a)(i) of Schedule 1 of the TAA is made out, and as such, Mr Brown is not liable for the sums claimed in the First DPN and Second DPN.

45 The 27 February 2019 letter refers to the Commissioner not having acknowledged the Applicant’s earlier correspondence of 20 November. It then repeats verbatim much of what had been advanced on his behalf in the earlier letter. There is however some significant additional text, identified in bold:

8. on 27 August 2018, being three (3) days after the Company contacted the ATO to discuss the debt and negotiate a payment arrangement, Mr Brown was issued with the First DPN. We note that the First DPN was issued in respect of the Company's unpaid monthly PAYG withholding liabilities for the period 1 November 2017 to 31 July 2018. The Commissioner's estimate of the unpaid amount of the Company's liability for that period was $768,796.00;

9. having received no response to the First Payment Proposal, on 29 August 2018 the Company made a payment of $10,000 to the ATO in accordance with the First Payment Proposal. A copy of the payment receipt was emailed to the ATO on the same day;

10. on 1 September 2018, Mr Brown resigned and was removed as a director of the Company, and Mr Brinkies was reappointed;

11. on 10 September 2017 the ATO issued a garnishee notice (Garnishee Notice) to Cashflow Finance Australia Pty Ltd in respect of funds held on the company’s behalf;

12. the Company thereafter continued its efforts to negotiate a pay arrangement until 4 October 2018, when it applied to have the statutory demand issued to the Company on 12 September 2018 (Statutory Demand) set aside;

13. on 9 October 2018, the ATO issued a notice of legal action to Mr Brown;

14. on 22 October 2018, Mr Brown was issued with the Second DPN. The Second DPN was issued in respect of the Company’s unpaid PAYG withholding liability for the period 1 August 2018 to 31 August 2018. The Commissioner’s estimate of the unpaid amount of the Company’s liability in respect of that period was $89,866.00.

(Emphasis added).

46 The 27 February 2019 letter also updated the Applicant’s representation with new information, responsive to events since transpiring:

15. by email on 20 November 2018, we sent a letter to the ATO setting out our client's defences in respect of the DPNs. We did not receive a response to that letter;

16. on 23 November 2018, the Company was successful in having the Statutory Demand set aside.

17. in or around late January 2019, Mr Brown became aware through his accountant that the ATO had withheld his Income Tax refunds;

18. on 6 February 2019, Mr Brown was issued with the Third DPN. The Third DPN was issued in respect of the Company's superannuation guarantee charge amounts for the period 1 October 2017 to 1 June 2018. The Commissioner's estimate of the unpaid amount of the Company's liability for that period was $118,103.11;

19. by email on 12 February 2019, we wrote to you requesting a copy of a garnishee notice if any, and details such as when Mr Brown was informed, and the method by which Mr Brown was informed that his Income Tax refund was withheld by the ATO;

20. by email on 12 February 2019, you responded by letter noting recent contact with Mr Brown's accountant, and stated that the Commissioner had recovered a portion of the penalty by automatically offsetting Mr Brown's Income Tax refund amounts against his director penalty liabilities (specifically relating to PAYG withholding).

47 The 27 February 2019 letter then addresses what the Applicant advanced to the Commissioner as the basis of his defence as follows:

Defences to Director Penalty Notices

We note that the First DPN, Second DPN and Third DPN were issued by the ATO pursuant to section 269·25 of Schedule 1 of the Taxation Administration Act 1953 (Cth) (TAA).

As you are no doubt aware, section 269-35(2) of Schedule 1 of the TAA states that a person is not liable to a penalty under section 269-25 if:

a) the person took all reasonable steps to ensure that one of the following happened:

(i) the directors caused the company to comply with its obligation:

(ii) the directors caused an administrator of the company to be appointed under section 436A, 436B or 436C of the Corporations Act 2001;

(iii) the directors caused the company to begin to be wound up (within the meaning of that Act); or

b) there were no reasonable steps the person could have taken to ensure that any of those things happened.

We note that section 269-35(3) of Schedule 1 of the TAA states that in determining what are considered reasonable steps for the purposes of section 269-35(2), the ATO must have regard to when, and for how long, a person was a director and all other relevant circumstances.

For the purposes of section 269-35(4A)(a)(ii) of Schedule 1 of the TAA, we note that Mr Brown was only informed in writing by the Commissioner that a portion of the penalty had been recovered on 12 February 2019 following our enquiry.

Application of the Defence

We consider that during his time as a director of the Company, Mr Brown, together with Mr Brinkies, took all reasonable steps to ensure that the Company complied with its taxation obligations. These steps included having a representative of the Company immediately seek to negotiate a payment arrangement with the ATO for payment of the debt in full, and making payments towards the debt in good faith during the period in which the ATO was purportedly considering the Company's payment proposal.

We note that:

1. Mr Brown was a director of the company for only ninety-three (93) days, from 31 May 2018 to 1 September 2018. Having regard to the date the Company became aware of its debt (on or around 24 August 2018), Mr Brown had only eight (8) days within which to ensure that the Company complied with its taxation obligations;

2. upon becoming aware of the debt, the Company contacted the ATO for the purposes of negotiating a payment arrangement to satisfy its debt and made the First Payment Proposal;

3. notwithstanding that the ATO gave the Company until 28 August 2018 to provide the requested information and documents in order to consider the First Payment Proposal, on 27 August 2018 the ATO issued the First DPN;

4. having received no response from the ATO regarding the First Payment Proposal, on 29 August 2018 the Company made a payment of $10,000 to the ATO in accordance with the First Payment Proposal;

5. the ATO did not respond to the First Payment Proposal until 10 September 2018, after Mr Brown had been removed as a director:

6. in addition to issuing the Garnishee Notice and a Statutory Demand two days apart, circumstances which the court has already found to be an abuse of process, we note that the First DPN had already been issued, and the Second DPN was issued shortly thereafter. That is, the ATO has employed three debt collection enforcement methods contemporaneously; and

7. the First DPN was issued to Mr Brown before the ATO had considered or responded to the First Payment Proposal, attempted to recover the debt from the Company, or even determined whether the Company had the capacity to pay the debt.

Having regard to the foregoing, we consider that the defence set out in section 269-35(2)(a)(i) of Schedule 1 of the TAA is made out, and as such, Mr Brown is not liable for the sums claimed in the First DPN, Second DPN and Third DPN.

In the circumstances, our client demands that the ATO remit the amounts set out in the First DPN, Second DPN and Third DPN in respect of Mr Brown, and to refund the amount recovered by the Commissioner pursuant to the DPNs.

48 The information in bold was not included in the text of the original (20 November 2018) letter.

49 On 5 March 2019, the Commissioner wrote to the Applicant advising that the Commissioner had declined to accept that he had a valid defence. The Applicant sought a statement of reasons. That statement was provided on 4 April 2019.

50 Omitting non-contentious introductory paragraphs, the Commissioner’s reasons were as follows:

FINDINGS ON MATERIAL QUESTIONS OF FACT

5. I made the following findings of fact which were material:

a. Michael James Brown was a director of the Company and was appointed a director from 31 May 2018 to 01 September 2018;

b. Michael James Brown was given a notice pursuant to section 269-25 of Schedule 1 to the TAA 1953 with respect to a director’s liability to pay a penalty pursuant to section 269-20 of Schedule 1 to the TAA 1953 with respect to:

i. Pay As You Go - Withholding (PAYGW) amounts for 01 November 2017 to 31 July 2018 on 27 August 2018;

ii. PAYGW estimates for the period 01 August 2018 to 31 August 2018 on 22 October 2018; and

iii. Superannuation Guarantee Charge for 01 October 2017 to 30 June 2018 on 6 February 20194 (DPNs).

c. On 24 August 2018, the Company requested a payment arrangement in relation to its integrated client account liabilities.

d. The Company had a director prior to Michael James Brown's appointment as director, who was removed as director on 15 June 2018. The previous director remained an employee of the Company, and was reinstated as director upon Michael James Brown ceasing to be director. On 24 August 2018, Michael James Brown authorised the employee to discuss the Company's liability With the ATO, and to ensure that the Company meets its PAYG withholding and SGC obligations under the CA 2001.

e. Based on the financial information of the Company, its poor compliance history and inability to address its current obligation, the ATO did not grant a payment arrangement.

EVIDENCE AND OTHER MATERIAL UPON WHICH THE DECISION WAS BASED

6. I based my foregoing findings on:

a. Mirrored Australian Securities on Time (MASCOT) search for the Company dated 22 October 2018;

b. DPNs given to Michael James Brown dated 27 August 2018, 22 October 2018 and 06 February 2019;

c. Letter from Atticus Lawyers & Advisors dated 20 November 2018;

d. ATO Siebel Notes with respect to the Company from 21 December 2017 to 7 March 2019, being the relevant periods the Company's liabilities and the DPN debt arose.

THE REASONS FOR THE DECISION

7. The decision was made under section 269-35(4A) of Schedule 1 to the TAA 1953, which provides as follows:

269-35(4A)

For the purpose of the Commissioner recovering from you a penalty payable under this Division (other than as mentioned in subsection (4)), subsection (1) or (2) does not apply unless:

(a) you provide information to the Commissioner during the period of 60 days starting on the day the Commissioner.

(i) in the case of the Commissioner recovering the penalty under section 260-5 (Commissioner may collect amounts from third party) - gives you a notice under subsection 260-5(6) in relation to the penalty;

or

(ii) otherwise - notifies you in writing that he or she has recovered any of the penalty; and

(b) the Commissioner is satisfied of the matters mentioned in subsection (1) or (2) of this section on the basis of that information.

8. Michael James Brown was a director of the Company from 31 May 2018 to 01 September 2018 and was given the following DPNs:

a. 27 August 2018 in respect of unpaid PAYGW liabilities incurred by the company for the monthly periods 01 November 2017 to 31 July 2018.

b. 22 October 2018 in respect of unpaid PAYGW estimate liabilities incurred by the company for the period 01 August 2018 to 31 August 2018.

c. 01 February2 019 in respect of unpaid Superannuation Guarantee Charge (SGC) liabilities incurred by the company for the quarterly periods between 01 October 2017 to 30 June 2018.

9. As a director, Michael James Brown, has statutory defences to penalties notified in the DPN as follows:

All reasonable steps

269-35(2)

You are not liable to a penalty under this Division if:

(a) you took all reasonable steps to ensure that one of the following happened:

(i) the directors caused the company to comply with its obligation;

(ii) the directors caused an administrator of the company to be appointed under section 436A, 436B or 436C of the Corporations Act 2001;

(iii) the directors caused the company to begin to be wound up (within the meaning of that Act); or

(b) there were no reasonable steps you could have taken to ensure that any of those things happened

10. The relevant obligations under subsection 269-15(1) of Schedule 1 to the TAA 1953 are as follows:

Directors' obligations

269-15(1)

The directors (within the meaning of the Corporations Act 2001) of the company (from time to time) on or after the initial day must cause the company to comply with its obligation.

11. The company's obligations are as follows:

269-10(1)

This Division applies as set out in the following table:

Obligations that directors must cause company to comply with | ||

Item | Column 1 This Division applies if, on a particular day (the initial day), a company is a company registered under the Corporations Act 2001 , and on the initial day ... | Column 2 and the company is obliged to pay to the Commissioner on or before a particular day (the due day ) ... |

1 | that amount in accordance with Subdivision 16-B. | |

4 | The company is given notice of an estimate under division 268 | the amount of the estimate. |

5 | a *quarter ends | Superannuation guarantee charge for the quarter in accordance with the Superannuation Guarantee (Administration) Act 1992 |

12. Liability to penalty for new directors is provided for in section 269-20(3) of Schedule 1 to the TAA 1953, which provides:

269-20(3)

You are also liable to pay to the Commissioner a penalty if:

(a) After the due day, you became a director of the company and began to be under an obligation under section 269-15; and

(b) 30 days later, you are still under that obligation.

13. The 30 day period in section 269-20(3) applies to all of a Company's outstanding PAYGW liabilities, and all unpaid SGC liabilities from 1 April 2012.

14. On 24 August 2018, Michael James Brown authorised an employee of the Company to discuss the Company's obligations with the ATO, and make a request for a payment arrangement.

15. It is unclear from the facts provided what steps Michael James Brown himself actually took to have the PAYGW and SGC liabilities paid, particularly between the date of his appointment and at least until 24 August 2018.

16. In light of the above, I decided that Michael James Brown has not satisfied the Commissioner of Taxation of the Commonwealth of Australia that he is not liable to a penalty under Division 269 of Schedule 1 to the TAA 1953 because:

a. Michael James Brown took all reasonable steps, or there were no reasonable steps he could have taken to ensure the following happened:

i. cause the Company to comply with its obligations;

ii. cause an administrator of The Company to be appointed under section 436A, 4368 or 436C of the CA 2001; or

iii. cause the Company to begin to be wound up within the meaning of the CA 2001.

(Footnotes omitted).

Consideration

51 Mr Frenkel’s written submissions are critical of the decision for many reasons. However, in oral argument two matters stood out.

52 First, there is no mention of the Applicant’s letter of 27 February 2019 as falling within the materials upon which the decision was based.

53 It will be recalled that that letter not only conveyed further information. It also again specifically drew the Commissioner’s attention to the Applicant’s submission that in determining what are considered reasonable steps for the purposes of s 269-35(2), the Commissioner must have regard to when and for how long the relevant person was a director and all other relevant circumstances. That submission reflected the terms of s 269-35(3), which had been specifically referred to earlier in the paragraph.

54 The second matter that stood out is that the decision maker does not make any mention of s 269-35(3); notwithstanding her purporting to set out the terms of the defence at paragraph [9] of the statement of reasons.

55 In oral submissions Mr Kaskani submitted that, although it is not mentioned, it may be inferred that the decision maker had taken s 269-35(3) into account. He submits that when the decision maker referred in her findings at paragraph [5(a)] to the dates on which the Applicant had commenced as a director and had ceased to be a director, she had impliedly fulfilled her duty to engage with his case that he had been appointed as a director at a time when the company already had large withholdings of PAYG owed to the Commissioner; that he was a director for only a short period and so on. Also implicit within that reference to the dates of the Applicant’s directorship was a rejection of the relevance of those circumstances to the Commissioner’s determination of what should be considered to have been “reasonable steps” on the facts of the Applicant’s case.

56 I reject that submission.

57 The way that a decision-maker sets out his or her findings of fact may reveal that he or she has misconceived his or her statutory function. As Gleeson CJ, McHugh, Gummow and Hayne JJ held in Minister for Immigration and Multicultural Affairs v Yusuf [2001] HCA 30; 206 CLR 323 (Yusuf) at [69] (applied by the Full Court of the Federal Court of Australia in Soliman v University of Technology, Sydney [2012] FCAFC 146; 207 FCR 277 (Marshall, North and Flick JJ) at [54]):

The Tribunal's identification of what it considered to be the material questions of fact may demonstrate that it took into account some irrelevant consideration or did not take into account some relevant consideration …

(Emphasis in original).

58 The same principle applies where a decision maker supplies reasons requested pursuant to the ADJR Act. An omission in the reasons so supplied may reveal that the decision maker has made a reviewable error of law: Yusuf at [10]. Scrutiny of this kind enables the courts to supervise the work of tribunals and other decision makers, and ensure that they act according to law. As Rares J observed in Minister for Immigration and Citizenship v SZLSP [2010] FCAFC 108; 187 FCR 362 at [86]:

Hence, the importance the courts have placed on the absence from the written statement… of some matter that would have demonstrated that the decision was made according to law or not affected by jurisdictional error. A written statement ensures transparency in the tribunal's exercise of a power conferred on it by the Parliament. This transparency is essential … to enable the Court to exercise the judicial power of the Commonwealth in reviewing whether the decision was made according to law or affected by a jurisdictional error.

59 In Yusuf, the plurality held (at [69]) that where a decision maker has a duty to give reasons a reviewing court is entitled to infer “that any matter not mentioned …was not considered … to be material”. It is well established that a party seeking, on judicial review of a such a decision, to contend that a decision maker’s stated reasons should be augmented by one or more unstated findings faces a difficult task: see Spruill v Minister for Immigration and Citizenship [2012] FCA 1401 per Robertson J at [18] and Tauariki v Minister for Immigration and Citizenship [2012] FCA 1408 per Cowdroy J at [43]-[44].

60 That is not to construe what the High Court said in Yusuf as elevating, to a fixed rule of law, the proposition that a reviewing court must always conclude that any matter not mentioned by a decision maker was not considered to be material. The way a decision is expressed, read fairly and in context, will sometimes show that a decision maker has made a particular finding: despite there being no mention of it in his or her reasons.

61 Mr Kaskani is correct that the relevant decision is entitled to be read fairly, in the context in which it appears, and not parsed cynically to expose error. However, I am unpersuaded that the decision, even beneficially read, permits the construction for which he contends. In my view, the reasons provided reveal nothing as would suggest that the decision maker identified the provisions of s 269-35(3) as a potentially relevant component of the statutory defence. Nor is there anything to suggest that the decision maker gave attention to applying the information supplied to her on behalf of the Applicant to the defence provided for in s 269-35(2) having regard to that statutory text.

62 In my opinion, the Applicant has established reviewable error in the relevant decision involving either an error of law (ADJR Act s 5(1)(f)) or a failure to take a relevant consideration into account in the exercise of the decision maker’s power (ADJR Act s 5(2)(b)).

63 In reaching that conclusion, I reject Mr Kaskani’s responsive oral submission:

….our reading of the provision is one that subsection (3) is only enlivened when one has regard to what is contained in subsection (2). So if we work backwards, we start with subsection (4A) where the applicant is given an opportunity to provide information in order to substantiate his or her defence under subsection (2). And the provision specifically says:

The Commissioner must be satisfied of the matters mentioned in subsection (1) or (2) of this section, on the basis of that information.

…. Subsection (2) is, the all reasonable steps. So one says, “Okay, the information that the applicant must provide must deal with all reasonable steps for the entire period, or that there were on reasonable steps that could have been taken for that entire period,” and they are matters that the courts have made clear. And your Honour’s point is but before you do that, (3) also says in determining what are reasonable steps for the purposes of subsection (2), have regard to when and for how long around directorship and management, and all other relevant circumstances. I say that in – I read it out in that way, or I address it in that way, your Honour, because we don’t see (3) as limiting the decisions or the way in which the decisions approach the obligations on the taxpayer to deal with information that addresses all relevant steps, all reasonable steps for the entire period.

64 I reject that submission because the text of s 269-35(3) makes it plain that that provision has operation “in determining” what are reasonable steps for the purposes of s 269-35(2). It has no further operation after that has been determined.

The futility contention

65 Section 16(1) of the ADJR Act relevantly provides:

Powers of the Federal Court and the Federal Circuit Court in respect of applications for order of review

(1) On an application for an order of review in respect of a decision, the Federal Court or the Federal Circuit Court may, in its discretion, make all or any of the following orders:

(a) an order quashing or setting aside the decision, or a part of the decision, with effect from the date of the order or from such earlier or later date as the court specifies;

(b) an order referring the matter to which the decision relates to the person who made the decision for further consideration, subject to such directions as the court thinks fit;

(c) an order declaring the rights of the parties in respect of any matter to which the decision relates;

(d) an order directing any of the parties to do, or to refrain from doing, any act or thing the doing, or the refraining from the doing, of which the court considers necessary to do justice between the parties.

66 For the Commissioner, Mr Kaskani correctly observes that remedies under the ADJR Act are not as of right. They are discretionary. One reason for which a remedy may be refused is futility.

Provision of information

67 Mr Kaskani submits that having regard to the observations of the decision maker at paragraph [15] and the absence of any information submitted on the Applicant’s behalf to explain what action he took prior to 24 August 2019 to have the company’s PAYG and SGC liabilities met, it would be futile to remit the decision to the Commissioner.

68 Mr Kaskani submits that the reasoning of the New South Wales Court of Appeal in Canty v Deputy Commissioner of Taxation [2005] NSWCA 84; 63 NSWLR 152 (Canty) per Handley JA at [45]-[46] (Beazley and Santow JJA concurring) applies so that the defence advanced must be rejected in that circumstance. The paragraphs to which Mr Kaskani referred the Court were as follows:

45. Under s 222AOJ(3) it is a defence if the defendant proves that he or she “took all reasonable steps to ensure that the directors complied with” the obligation, or that “there were no such steps that the person could have taken” (emphasis added). The natural meaning is that the combined defences must cover the whole of the period between the breach of the obligation on the due date and the expiry of the notice.

46. Proof that nothing could have been done at various times during this period would not establish that nothing could have been done at other times. Proof that the person took all reasonable steps at various times would not establish that he or she took all reasonable steps.

69 Mr Kaskani submits:

There are no facts here in relation to the period from 31 May to 24 August and I apprehend, well, other than the fact that he was a director, obviously, during that period. And let’s say, your Honour, for argument’s sake, that it’s Mr Brown’s case that he did not take part in any management of the company. That he was completely sidelined, and he did nothing and he relied on accountants and bookkeepers and he relied on other professionals to do the work. Then of course subsection (3) would be highly relevant because that would be something that when he presents the information that he does in respect of the entire period, the decision-maker is directed to, “Well, you need to look at the extent to which he took part in management or failed to take part in management.” Perversely, not taking part in management assists him, rather than understanding all of his obligations. The difficulty we have here - - -

70 However, that submission proceeded on the premise that I have rejected above at [63]-[64]. I am satisfied that, where relevant, s 269-35(3) operates at the threshold when a decision maker is determining what are to be understood as “reasonable steps”.

71 The important qualification I express in the above is “where relevant”. In Canty, s 269-35(3) (or more precisely its predecessor provision as similarly expressed) was not relevant. In that case, the appeal turned on whether the provisions of then Subdiv B of Div 9 of Pt VI of the Income Tax Assessment Act 1936 (Cth) applied to a former director after his resignation. It was held that it did. No point is taken in that regard in these proceedings.

72 In the facts that applied in Canty, the equivalent of s 269-35(3) was not relevant.

73 That s 269-35(3) went unmentioned in Canty is unsurprising, because the former director in that case had been one of two directors of the company from 1996 until his resignation on 31 August 1999 (see Canty at [2]-[3]). No issue of his only having assumed that role recently was relevant. Handley JA’s observations as set out above and as to what objectively the former director ought to have known about the company’s liabilities are to be understood in light of the Court’s finding that the former director had actual knowledge of the company’s financial difficulties, its arrears and past defaults (see Canty at [58]).

74 For those reasons I reject the proposition that Canty can be applied as if it determines the outcome where s 269-35(3) is (not implausibly) called in aid to determine what “reasonable steps” are required of a director who has held office for only a short period, in circumstances where that question is specifically relevant.

75 In compliance with leave granted, after oral submissions the Commissioner also drew the Court’s attention to the decision in Roche v Deputy Commissioner of Taxation [2015] WASCA 196 (Roche) in which the Western Australia Court of Appeal dismissed an appeal from a decision of the Master that summary judgment be entered in the Commissioner’s favour on the basis that the appellant had no arguable defence to the Commissioner’s claim. The Court of Appeal - Buss, Newnes and Murphy JJA - applied Canty. However, the facts in Roche similarly did not plausibly engage with the potential application of s 269-35(3). I am accordingly satisfied that that case is, for the same reason, equally distinguishable.

76 In addition, I note that the premise for the defence advanced by the former director in Canty was entirely different to the circumstances of the present case. The premise advanced in Canty was as follows:

Defence of reasonable steps

31. The appellant’s defence under s 222AOJ(3) (see at 155 [10] supra) as pleaded was that he had taken all reasonable steps to ensure that the directors had complied with s 222AOB(1), or there were no such steps that could have been taken. The trial judge held that the defence failed because there was no evidence that the appellant had taken any steps to cause the company to comply with s 222AOB(1)(b) by making an agreement with the Commissioner under s 222ALA. This is factually correct but the appellant argued that it was legally incorrect.

(Emphasis added).

77 By contrast, in the Applicant’s instance it is not contentious that on becoming aware of his company’s indebtedness to the Commissioner he had voluntarily ensured that the Commissioner was provided with all relevant company records. He then had arranged for the company on 24 August 2018 to offer to make an agreement with the Commissioner for payment by instalments. He had subsequently authorised the company to make an initial payment of $10,000 in earnest of that proposal. The Commissioner’s decision to reject that proposal was not communicated to the company until 10 September 2018: over a fortnight later, and nine days after the Applicant had resigned as a director.

78 Mr Kaskani accepts that the period over which the Applicant was required to explain his conduct to make good a defence with respect to the first DPN was from the date on which he became liable, to 17 September 2018.

79 In Canty, Handley JA reasoned:

37. The defence under par (a) is that the person “took all reasonable steps to ensure that the directors complied with subsection 222AOB(1)”. Compliance would be achieved if any one of those events were to occur. Thus if payment was made there is no need for an agreement, an administrator, or a liquidator. If payment was being pursued the other courses would for the time being be unnecessary and counterproductive. If payment is out of the question or cannot be achieved the person bound must address the other steps. If winding up then becomes the preferred option there will be no need for the time being to seek the appointment of an administrator.

38. The defences under par (a) and par (b) are cumulative not mutually exclusive. A defendant may establish that there was nothing that could reasonably be done to achieve payment. He or she may also establish that there was no point in attempting to negotiate an agreement with the Commissioner. In such a case the defence under par (b) would succeed pro tanto leaving the defence under par (a) to address the remaining options.

39. In other cases the defence under par (b) may succeed in relation to all options, so that the defence under par (a) need not be considered. If the only feasible options are the appointment of an administrator or a liquidator a person under the duty, acting reasonably, may decide to seek a winding up. If so, he or she will not be acting unreasonably by doing nothing to secure the appointment of an administrator at that stage. The converse will also be true.

80 Although it is not necessary to decide the point in these proceedings, what his Honour appears to be suggesting in those paragraphs is that where an instalment proposal remains in prospect, no other step (administration or winding up) is reasonably required (see also Canty at [41]).

81 It is not necessary to decide that issue because it is not open to this Court to substitute the decision of the New South Wales Court of Appeal in Canty for the text of the statute, where the facts of that case are relevantly distinguishable.

82 Mr Kaskani accepts that this Court should not refuse relief on the ground of futility unless it is established to be inevitable that on remittal relief would be refused. If a decision has been established to be legally flawed and a different outcome sought on remittal is arguably legally open, the merits are exclusively a question for the Commissioner. That is as I find the position to be in the present circumstances.

Concurrent proceedings

83 Finally, I turn to the Commissioner’s submission that there would be no utility in the relief sought because the issue of whether the relevant defence can be made good will be determined finally in the judicial proceedings pending in the Supreme Court of Queensland.

84 On first blush, there is much force in that submission.

85 The Applicant in the present proceedings, being the respondent in the proceedings before the Supreme Court of Queensland, has in that forum also asserted a defence based on s 269-35(2).

86 However, that is where the position bifurcates. Having regard to s 269-35(4), the defence provided for in s 269-25(2) “does not apply” unless the respondent proves the relevant matters. It will thus be open to Mr Brown in those curial proceedings to adduce such evidence as he sees fit in that regard. He will not be confined to the evidence or submissions advanced to the Commissioner as are material to these proceedings.

87 Mr Kaskani and Mr Frenkel agree that if this Court sets aside the decision under review and remits it for the Commissioner’s reconsideration then no issue of inconsistency (in the legal sense) will arise. That is because the Commissioner’s decision was required to be based on the information provided to him within the relevant 60 days. It will remain limited to the same information, even if remitted. By contrast, the proceedings in the Supreme Court of Queensland will potentially take into account other evidence.

88 The parties have not reached any agreement as between themselves as would avoid parallel administrative and judicial proceedings. It can be accepted to be unusual that Div 269 proceeds on the basis that the evidence or information available in each review can differ. It is nonetheless entirely possible that the Commissioner may uphold a defence applying s 269-35(4A), while a Court having regard to different evidence adduced pursuant to s 269-35(4) might come to the contrary conclusion (and vice-versa). As the parties submit, I accept that any difference in outcome would not indicate that one finding was in error.

89 In those circumstances, Mr Frenkel submits that it cannot be concluded that there will be no utility in a remission. While the curial proceedings will determine whether the defence sought to be relied upon by the Applicant in that proceeding succeeds, that determination will not affect the outcome of self-help remedies pursued or liable to be pursued by the Commissioner.

90 In that regard, Mr Frenkel points out that the Commissioner has withheld the Applicant’s personal tax refund for the 2018 financial year and has applied those funds to the debt the subject of the DPNs. Mr Kaskani accepts that the way in which s 269-35(4A) is intended to operate is that if the Applicant makes good his defence on remittal, then that amount would be required to be returned to the Applicant.

91 Having regard to the parties’ respective submissions, it is thus clear that the existence of parallel judicial proceedings do not deprive the relief sought of legal utility.

Orders and disposition

92 These reasons have focused on the first DPN notice. Mr Frenkel took no point that there may not have been technical compliance with the obligation to give notice of pending enforcement of the other penalties sought, such that the Applicant would have 60 days to advance any defence in respect of the sums due under those two further DPNs. He was content to proceed on the basis that the Applicant had received informal notice and had relied on the same defence in respect of those further two notices. In the circumstance that the Applicant has established that his grounds of review are made out in respect of the first notice, there is no reason why that the decision, expressed in terms of all of the three DPNs, should not be remitted for reconsideration on that basis. Mr Kaskani does not submit otherwise. I accept that to be the case.

93 I will order that the matter, as embraces all three DPNs, be remitted to the Commissioner for determination according to law.

94 Having heard the parties on the question of costs, the Respondent does not resist the proposition that costs should follow the event. I will so order.

I certify that the preceding ninety-four (94) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Kerr. |

Associate: