FEDERAL COURT OF AUSTRALIA

Australian Competition and Consumer Commission v Quantum Housing Group Pty Ltd (No 2) [2020] FCA 802

ORDERS

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION Applicant | ||

AND: | QUANTUM HOUSING GROUP PTY LTD (ACN 141 554 798) First Respondent CHERYL ANNE HOWE Second Respondent | |

DATE OF ORDER: |

THE COURT DECLARES THAT:

1. Between February 2017 and July 2018, the first respondent (QHG) made representations to owners of rental properties (Investors) which were not true to the effect that:

(a) the real estate agents contracted to manage their properties (Property Managers) must enter into an agreement with QHG (Portfolio Management Agreement) in order to manage a QHG National Rental Affordability Scheme (NRAS) property for the Investor;

(b) a Property Manager must meet the requirements of the 'Guidelines for the Approval of Property Managers' (Accreditation Guidelines) to manage QHG NRAS properties;

(c) the existing Property Managers will not be able to continue to manage the QHG NRAS properties and one of QHG's 'approved' Property Managers (Approved Property Managers) should take their place;

(d) the Accreditation Guidelines protect the Investor against a loss of their incentive, and protect QHG if they have to indemnify the Investor for this loss;

(e) the Investor's Property Manager has decided not to, or was unable to, meet all of QHG's requirements for managing the property;

(f) the Investor must appoint a new Property Manager, and should use a QHG Approved Property Manager, because if they do so they will be protected financially;

(g) the Investor has failed to appoint an Approved Property Manager and as a result the Investor is in default of the NRAS Agreement; or

(h) as a consequence of the Investor failing to appoint an Approved Property Manager, QHG had a right to and would terminate the NRAS Agreement.

(together, the Misleading Representations).

2. QHG also made a representation to some Investors which was not true that the Investor's Property Manager had not properly managed the compliance of their property (the Additional Misleading Representation).

3. By making the Misleading Representations and the Additional Misleading Representation, QHG in trade or commerce:

(a) engaged in conduct that was misleading or deceptive or likely to mislead or deceive in contravention of s 18(1) of the Australian Consumer Law (ACL); and

(b) as to the Misleading Representations in paragraph 1(a), (c) and (f), in connection with the supply or possible supply of services, made false or misleading representations concerning the existence, exclusion or effect of any condition, warranty, guarantee, right or remedy in contravention of s 29(1)(m) of the ACL.

4. Further, by making the Misleading Representations referred to in paragraphs 1(a), (b), (c), (d), (e), (f), (g) and the Additional Misleading Representations, in connection with the supply or possible supply of services, QHG made false or misleading representations with respect to the need for services in contravention of s 29(1)(l) of the ACL.

5. The second respondent (Ms Howe) was a person knowingly concerned in QHG's contraventions, as declared in paragraphs 1 to 4.

THE COURT ORDERS THAT:

Pecuniary Penalties

6. QHG must pay to the Commonwealth of Australia a penalty of $700,000.

7. Ms Howe must pay to the Commonwealth of Australia a penalty of $50,000 with payment to be made as follows:

(a) $20,000 within 30 days of the date of the order; and

(b) $2,000 per month for a period of 15 months after the first payment has been made.

Costs

8. QHG must pay the applicant's costs, to be taxed if not agreed.

9. Ms Howe must pay the applicant's costs, fixed at the sum of $10,000 with payment to be made in monthly instalments of $2,000 with the first payment commencing 16 months after the first payment amount is made of the pecuniary penalty amount, as set out in paragraph 7 above.

Publication orders

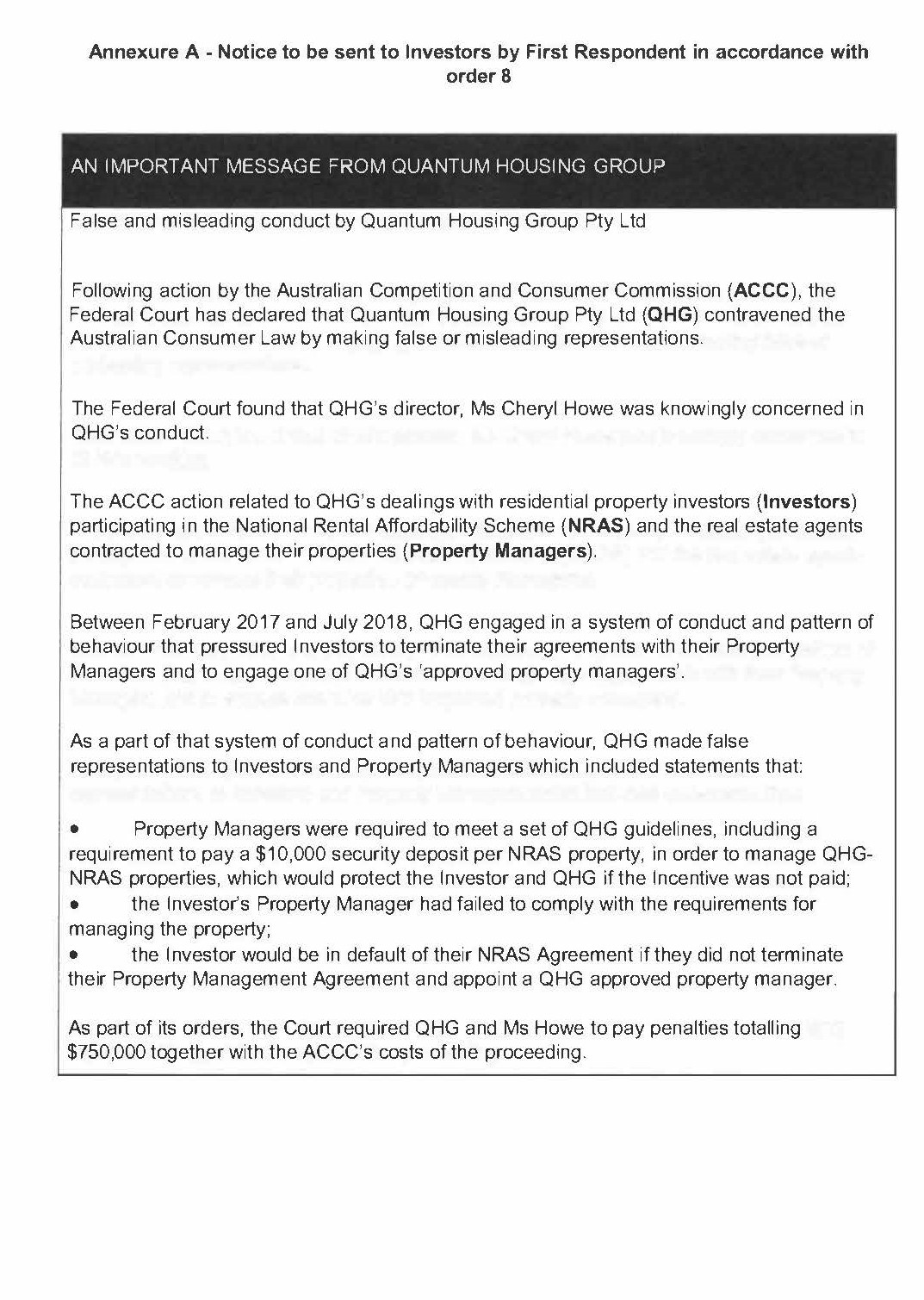

10. Within 21 days of the date of this order, QHG must email each of the 1215 Investors it held allocations for as at 19 December 2019, with the content of the notice set out in Annexure A of this order.

Other orders

11. From the date of this order, Ms Howe is disqualified from managing a corporation for a period of three years, pursuant to s 248 of the ACL.

12. The reasons for judgment delivered at the time of the making of these orders are to be affixed with the Court's seal and retained on the Court's file for the purposes of s 137H of the Competition and Consumer Act 2010 (Cth).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

COLVIN J:

1 Quantum Housing Group Pty Ltd (QHG), now in liquidation, was in the business of arranging investments in properties that qualified for incentives under the National Rental Affordability Scheme (NRAS) established by the Commonwealth Government in 2008. QHG was an Approved Participant in the NRAS and by 2017 held at least 1,200 allocations of funding for properties subsidised by the scheme.

2 The NRAS provided for subsidies to be paid in accordance with a system of approved allocations. QHG obtained approved allocations. QHG then entered into agreements with individual investors who purchased rental dwellings the subject of each allocation. It was a matter for agreement between QHG and the investor as to how the incentives would be paid in respect of each allocation of funding under the NRAS. Generally speaking, the agreements between QHG and each investor were in a standard form and allowed for the appointment of a property manager to manage the property in a manner that ensured ongoing qualification for the NRAS incentive.

3 Mr Ashley Richard Fenn controlled another company that had been an Approved Participant for the purposes of the NRAS. He also controlled entities that provided management services to investors who had purchased properties that received allocations under the NRAS.

4 In 2017, an agreement was entered into for the sale of the business operated by QHG (and other companies) to a company associated with Mr Fenn. QHG's management then devised a plan, described as the Roll Up Plan, to encourage investors to transfer the management of properties that qualified for incentives under the NRAS to property managers who were related to, or preferred by, Mr Fenn. Ms Cheryl Ann Howe was the sole director and secretary of QHG at the time. She was involved in the implementation and execution of the Roll Up Plan which was evidently intended to benefit the financial interests of Mr Fenn and others. Ms Howe's involvement was, in effect, as a management employee.

5 In proceedings commenced in this Court, the Australian Competition and Consumer Commission (ACCC) claimed that QHG contravened the Australian Consumer Law (ACL) (being Schedule 2 to the Competition and Consumer Act 2010 (Cth)) by engaging in systemic unconscionable conduct and misleading conduct and that Ms Howe was involved in that contravening conduct. A detailed statement of facts has been filed by which QHG agrees that it engaged in conduct of the character alleged by the ACCC and Ms Howe agrees to having been involved in the conduct.

6 The parties have submitted a minute of orders which sets out the terms of proposed declarations of contraventions, a disqualification order for Ms Howe, pecuniary penalties, publication orders and orders as to costs. All orders are agreed by the parties to be appropriate in the circumstances, save that the liquidator of QHG makes no submission as to the appropriateness of the proposed pecuniary penalty to be imposed upon the company.

7 For the following reasons, I am satisfied that there should be orders in terms of the minute of orders save that there should not be orders declaring that there was unconscionable conduct by QHG or that certain of the representations made contravened s 29(1)(m) of the ACL or that Ms Howe was involved in conduct of that particular character.

Summary of the agreed factual position

8 Between February 2017 and July 2018, QHG engaged in a system of conduct and pattern of behaviour by which it implemented the Roll Up Plan. Its conduct had the following overall characteristics:

(1) QHG was in a superior bargaining positioning in dealing with investors by reason that it was the Approved Participant in the NRAS and received the incentives;

(2) under the arrangements for the NRAS, investors were dependent on QHG in order to receive their incentive because if QHG did not lodge a statement of compliance for their property it would be in breach under the NRAS and the incentive would not be paid;

(3) the bargaining position of QHG was enhanced by the fact that under the arrangements for the NRAS at the relevant time, investors could not change to another Approved Participant;

(4) QHG took advantage of the fact that investors relied upon QHG in order to participate in the NRAS in order to continue to receive their incentive under the terms of their agreements with QHG by formulating and implementing the Roll Up Plan;

(5) the aim of the Roll Up Plan as formulated and implemented by QHG was to pressure all of the investors who had agreements with QHG to arrange to obtain property management services from property managers identified as approved by QHG;

(6) QHG did not disclose to investors its commercial associations with the approved property managers;

(7) QHG issued rounds of misleading correspondence to at least 450 investors that were designed to interfere with the contractual relationships between the investors and their property managers by unduly pressuring investors to terminate their relationships with the property managers and change to a property manager approved by QHG;

(8) as the rounds of correspondence progressed, the pressure on investors increased;

(9) as part of the implementation of the Roll Up Plan, QHG unilaterally imposed accreditation guidelines on its investors;

(10) amongst other things, the accreditation guidelines required the property manager of an investor to pay a security deposit of $10,000 if the investor did not transfer the management of their property to a QHG approved property manager;

(11) the imposition of the security deposit was directed to excluding property managers who were not approved by QHG;

(12) the security deposit was without any commercial justification or purpose. It only protected QHG in circumstances where QHG required no further protection because it had the benefit of an indemnity in the agreements with investors as well as insurance maintained by the property managers;

(13) in its communications with investors, QHG justified the requirement for the security deposit on the basis that QHG would suffer loss and damage if an investor did not receive its incentive under the NRAS because it had provided assurances to investors that would require full reimbursement from the property manager when that was not true;

(14) QHG also maintained that the security deposit would protect investors when that was not true;

(15) eventually investors who had not changed to a QHG preferred property manager were issued with notices stating that they were in default under their agreement with QHG which governed their entitlement to the incentive under the NRAS;

(16) a number of the property managers who managed properties for the investors who were not QHG approved property managers objected to providing the required security deposits;

(17) when there was a refusal by a property manager to pay the security deposit, QHG used that refusal as a basis to refuse to renew agreements and then to pressure investors to appoint a QHG approved property manager;

(18) during the period of the conduct, the management of at least 260 properties was transferred by individual investors to a QHG approved property manager; and

(19) the fact that the conduct by which the Roll Up Plan was implemented caused a number of investors to change the management of their property to a QHG preferred property manager (being the aim of the conduct) is not disputed.

9 Ms Howe was the sole director of QHG during the above conduct. She was in control of the employees who sent out the rounds of correspondence and involved in the dealings to arrange for the correspondence to be sent. However, the agreed facts show that the conduct was being driven by Mr Fenn and it was he and others who benefitted from the conduct.

Contraventions

10 I am satisfied that the facts as agreed establish that each of the following representations were made to investors and that those representations were false in the respects described below, namely:

(1) Property managers contracted to manage an investor's property must enter into an agreement with QHG in order to manage the investor's property when there was no such requirement under terms of the agreements between QHG and the investors.

(2) Property managers must meet the requirements of the accreditation guidelines issued by QHG when a property manager could manage an investor's property without complying with the guidelines including without providing the security deposit required by the guidelines.

(3) Existing property managers would not be able to continue to manage the investor's property and one of QHG's approved property managers should take their place when the existing property managers were able to continue and there was no need for an approved property manager to take their place.

(4) The accreditation guidelines protect the investor against a loss of their incentive and protect QHG if they have to indemnify the investor for the loss when that was not the case.

(5) The investor's property manager had decided not to, or was unable to, meet all of QHG's requirements when the property managers were able to meet reasonable requirements for managing the properties.

(6) The investor must appoint a new property manager and should use a QHG approved property manager because if they did so the investor would be protected financially when QHG could not require the investors to appoint a new property manager and such an appointment was not necessary for the financial protection of the investor whether by payment of the security deposit under the accreditation guidelines or otherwise.

(7) The investor had failed to appoint an approved property manager and as a result was in default under the agreement with QHG when there was no obligation under the agreement to appoint an approved property manager.

(8) As a consequence of the investor failing to appoint an approved property manager QHG had a right to and would terminate its agreement with the investor when QHG had no such right.

Misleading conduct

11 The making of the representations to investors was misleading conduct in trade or commerce and contravened s 18(1) of the ACL. The conduct was targeted at investors for the purpose of securing their agreement to change their property manager. It was conduct that was part of a plan directed to that outcome. The false statements were of a kind that was likely to induce error on the part of an investor as to the matters the subject of the representations. Therefore, the requisite causal connection to establish the contravention is demonstrated: Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2013] HCA 54; (2013) 250 CLR 640 at [39].

False representations

12 In addition, the agreed facts establish that the representations at (1), (3) and (6) of [10] above were false representations concerning the need for services, namely the need for a replacement property manager, and the making of those representations contravened s 29(1)(l) of the ACL.

13 The ACCC also submitted that the making of each of the representations contravened s 29(1)(m) of the ACL because they were false statements concerning 'the existence, exclusion or effect of [a] right'. Precisely what is meant by the term 'right' for the purposes of the provision was not addressed by the ACCC in its submissions.

14 Section 29(1)(m) of the ACL provides:

A person must not, in trade or commerce, in connection with the supply or possible supply of goods or services or in connection with the promotion by any means of the supply or use of goods or services … make a false or misleading representation concerning the existence, exclusion or effect of any condition, warranty, guarantee, right or remedy (including a guarantee under Division 1 of Part 3-2).

15 I find that for the following reasons each of the representations made to investors (described at [10] above) were representations as to the exclusion, existence or effect of a right:

(1) The representation to the effect that a property manager must enter into an agreement with QHG in order to manage the investor's property was a representation as to whether the investor had a right unconstrained by the terms of the NRAS and the investor's agreement with QHG to enter into an agreement with a property manager of the investor's own choosing.

(2) The representation to the effect that property managers must meet the requirements of the accreditation guidelines was a representation that the right to appoint a property manager of the investor's own choosing was excluded by the guidelines.

(3) The representation to the effect that investors needed an approved property manager was a representation that the right to appoint a property manager of the investor's own choosing was excluded or did not exist.

(4) The representation to the effect that the investor's property manager had decided not to, or was unable to, meet all of QHG's requirements was a representation to the effect that QHG could impose requirements of a kind that denied the existence of the investor's right to appoint a property manager of the investor's own choosing.

(5) The representation to the effect that investors must appoint a new property manager and should use a QHG approved property manager because if they do so they will be protected financially, was a representation to the effect that QHG could impose requirements of a kind that denied the existence of the investor's right to appoint a property manager of the investor's own choosing.

(6) The representation to the effect that the investor had failed to appoint an approved property manager and as a result the investor was in default under the investor's agreement with QHG was a representation as to the rights of the investor under the agreement and the rights of the investor to receive incentives under the NRAS.

(7) The representation to the effect that if the investor failed to appoint an approved property manager, QHG had a right to and would terminate its agreement with the investor was a representation as to the rights of the investor under the agreement and the rights of the investor to receive incentives under the NRAS.

16 However, the representation to the effect that the accreditation guidelines protected the investor against loss of their incentive and protected QHG was not a representation as to the exclusion, existence or effect of a right. It was a representation as to the purpose for the accreditation guidelines.

17 I am also satisfied that the agreed facts establish that a representation was made to some investors to the effect that the investor's property manager had not properly managed compliance which was not the case. I do not accept that the representation was also one to which s 29(1)(m) applied.

Unconscionable conduct

18 The parties have agreed that between February 2017 and July 2018, QHG engaged in unconscionable conduct by engaging in a system of conduct and pattern of behaviour which they describe in the following terms:

(1) QHG took advantage of its superior bargaining position relative to investors as a result of the investors' reliance on QHG to participate in the NRAS and receive their incentive;

(2) QHG formulated and implemented the Roll Up Plan, which had as its aim to unduly pressure all of QHG's investors to accept property management services from an approved (QHG-related) property manager;

(3) to that end, QHG unilaterally imposed the accreditation guidelines;

(4) the imposition of the security deposit in particular was directed to excluding property managers who were not approved by (related to) QHG;

(5) the security deposit was not otherwise required as it only protected QHG and QHG was otherwise protected from loss by an indemnity in its agreements with the investors and by insurance maintained by the property managers; and

(6) in furthering the Roll Up Plan, QHG also made the misleading representations to investors, in order to unduly pressure them to terminate their relationships with existing property managers and change to a property manager from a small panel including one or more QHG-related property managers.

19 In Australian Securities and Investments Commission v Kobelt [2019] HCA 18, the High Court considered whether the conduct in that case contravened the statutory prohibition against unconscionable conduct expressed in s 12CB(1) of the Australian Securities and Investments Commission Act 2001 (Cth). It is a provision of the same character and has the same origins as that contained within s 21 of the ACL. In Kobelt it was claimed that a system of commercial dealing by which people who were socially and economically vulnerable were allowed to book-up credit mostly to fund the supply of second-hand motor vehicles (but also for the supply of groceries and fuel) was unconscionable. The Court was split as to the principles to be applied and the outcome.

20 Kiefel CJ and Bell J at [14] stated that the term unconscionable is to be understood as bearing its ordinary meaning and proscribes conduct 'that objectively answers the description of being against conscience'. Their Honours then cited the following values as informing the standard of conscience fixed by the statute (quoted from the reasons of Allsop CJ in Paciocco v Australia and New Zealand Banking Group Ltd [2015] FCAFC 50; (2015) 236 FCR 199 at [296]):

… certainty in commercial transactions, honesty, the absence of trickery or sharp practice, fairness when dealing with customers, the faithful performance of bargains and promises freely made, and:

'the protection of those whose vulnerability as to the protection of their own interests places them in a position that calls for a just legal system to respond for their protection, especially from those who would victimise, predate or take advantage'.

21 Their Honours then referred to unconscionable conduct as requiring 'not only that the innocent party be subject to special disadvantage, but that the other party must also unconscientiously take advantage of that special disadvantage' and observing that this 'has variously been described as requiring victimisation, unconscientious conduct or exploitation': at [15]. Therefore, in the view of their Honours an essential part of the provision was the protection of the vulnerable and the conduct had to involve taking advantage of that vulnerability in a manner that might be characterised as predatory or exploitative.

22 Gageler J described the statute as operating to prescribe a normative standard of conduct to be administered in the totality of circumstances: at [87]. His Honour emphasised 'the gravity of the conduct necessary to be found by a court in order to be satisfied of a breach of that standard': at [88]. The 'conduct proscribed by the section as unconscionable is conduct that is so far outside societal norms of acceptable commercial behaviour as to warrant condemnation as conduct that is offensive to conscience': at [92]. Further, '[f]or a court to pronounce conduct unconscionable is for the court to denounce that conduct as offensive to a conscience informed by a sense of what is right and proper according to values which can be recognised by the court to prevail within contemporary Australian society': at [93]. Of significance is his Honour's description of unconscionable conduct as being worthy of condemnation because of its gravity in the sense that it was far outside what was acceptable.

23 Keane J required a scrutiny of the exact relations established between the parties: at [115]. His Honour found that in the particular case, it had not been established that the book-up system conducted by Mr Kobelt 'exploited his customers' socio-economic vulnerability in order to extract financial advantage from them'. His Honour declined to find that Mr Kobelt actually took advantage of any increased vulnerability of his customers or acted with predatory intent with a view to do so: at [116]. His Honour found that unconscionable conduct required an element of exploitation, variously described as exploitation, victimisation, unconscientious conduct or a predatory state of mind: at [118]. This was said to follow from the choice of the legislature to use the 'morally freighted' term of unconscionability: at [119].

24 As to the statutory standard, Nettle and Gordon JJ said at [234]:

The assessment of whether conduct is unconscionable … involves the evaluation of facts by reference to the values and norms recognised by the statute, and thus, as it has been said, a normative standard of conscience which is permeated with accepted and acceptable community standards. It is by reference to those generally accepted standards and community values that each matter must be judged.

25 Like Kiefel CJ and Bell J, their Honours identified the need for there to be vulnerability or special disadvantage and conduct by which advantage was taken of that vulnerability or special disadvantage. As to voluntariness, their Honours said at [157]:

… considerations of voluntariness need to be assessed in the context of the system of conduct in issue. Conduct can be unconscionable even where the innocent party is a willing participant; the question is how that willingness or intention was produced. An innocent party may be capable of making an independent or rational judgment about an advantage in an otherwise bad bargain. However, an advantage, and the capacity of the innocent party to identify that advantage and make a rational choice, cannot operate to transform what is, in all the circumstances, an exploitative arrangement. Nor can the existence of that advantage absolve from liability the stronger party who unconscientiously takes advantage of the weaker party.

(original emphasis)

26 Therefore, Nettle and Gordon JJ appear to describe a standard that may not have the characteristics of predation or victimisation described by Kiefel CJ, Bell and Keane JJ or of the gravity described by Gageler J. However, their Honours did describe unconscionability in terms that required that there be vulnerability and an exploitation of that vulnerability.

27 Edelman J agreed with the reasons of Nettle and Gordon JJ. Therefore, his Honour must also be taken to accept that unconscionable conduct requires that there be a taking advantage or exploitation of a vulnerability of another party. His Honour also dealt with the context in which the statutory language came to be expressed and concluded that it was intended to lower the bar on the moral standard for measuring inappropriate behaviour and concluded at [295]:

… the history of development of [the] statutory proscription demonstrates a clear legislative intention that the bar over which conduct will be unconscionable must be lower than that developed in equity even if the bar might not have been lowered to the 'unreasonableness' and 'unfairness' assessments in the various categories in nineteenth century equity.

28 The members of the Court who were in the minority in finding that the conduct of Mr Kobelt was unconscionable (Nettle, Gordon and Edelman JJ), did not favour an interpretation of the standard that required a high degree of moral disapprobation. Kiefel CJ, Bell and Keane JJ emphasised the need for victimisation, exploitation or a predatory state of mind. Kiefel CJ and Bell J referred, with apparent approval, to the view of the Full Court of this Court that moral obloquy had a role to play but was not a substitute for the statutory words: at [60]. Keane J found that the statute 'imports the "high level of moral obloquy" associated with the victimisation of the vulnerable': at [118]. Gageler J recanted the use of the term moral obloquy for the reason that it 'has the potential to be misleading to the extent that it might be taken to suggest a requirement for conscious wrongdoing': at [91]. However, as noted above, his Honour expressed the view that for conduct to be unconscionable it must be so far outside societal norms of acceptable commercial behaviour as to warrant condemnation as conduct that is offensive to conscience.

29 Therefore, the majority view supports the adoption of a standard that requires exploitation of disadvantage by a party in a stronger position by conduct that is well outside the bounds of what is generally seen to be moral, right or acceptable commercial behaviour. It is not every instance where a person in a stronger commercial position gains an advantage by reason of that position over a person in a weaker or disadvantaged position that is unconscionable. It is not enough that the dealing might be described as unfair or unreasonable. Rather, unconscionable conduct involves dealing with those who are vulnerable in a manner that exploits that vulnerability by engaging in conduct that may be plainly or obviously criticised when viewed through the lens of an understanding of proper commercial behaviour according to prevailing norms and standards.

30 In making the evaluation as to whether conduct is unconscionable, there must be regard to the non-exhaustive and non-prescriptive list in s 22 of the ACL, although the presence of one or more of those matters will not be determinative. However, the statutory list is to be considered for the purpose of determining whether the conduct was unconscionable. The nature of the list is such that it describes aspects that may be present in many types of commercial dealings. Ultimately, the statutory prescription is against engaging in unconscionable conduct not against conduct which takes places in circumstances of the kind described in the list.

31 For the following reasons, I am not satisfied that the admitted description of the conduct of QHG falls within the statutory notion of unconscionable conduct.

32 The conduct as described concerns dealings by QHG with its investors. There is no description of the financial or other circumstances of the investors that would enable them to be characterised as being vulnerable or in a position of disadvantage of a kind that might expose them to being exploited or victimised. It may be inferred from the facts as admitted that they are each of sufficient financial standing and sophistication to be undertaking an investment in a residential property of a kind that qualifies for the incentives provided for by the NRAS. There is no indication that any of the investors were incapable of looking after their own interests or understanding the nature of their dealings with QHG.

33 The consequence of the conduct of QHG is that investors were persuaded to switch to a QHG preferred provider of management services. There is no suggestion that there was any financial disadvantage suffered by an investor as a result. The financial burden of the conduct appears to have fallen on the property managers whose services were terminated. That consequence is not one which is relevant to whether the dealings by QHG with the investors were unconscionable.

34 It may be accepted that the nature of the NRAS and the position of QHG as the Approved Provider who was required to certify compliance in order for investors to be entitled to ongoing incentives meant that QHG had a degree of power in its dealings with individual investors.

35 However, the operative conduct by which the Roll Up Plan was implemented was the making of false representations about the nature of the arrangements for the NRAS and the imposition of the accreditation guidelines requiring the security deposit. The conduct did not depend upon being able to exploit identified vulnerability or disadvantage on the part of the investors. Rather, it involved taking advantage of the power conferred by the nature of the NRAS. The conduct of QHG did not depend for its success on the vulnerability of the investors. It depended upon leveraging the power afforded by the control that QHG had over the continuation of the flow of incentives under the NRAS to investors.

36 Therefore, to the extent that proposed orders depend upon the claim of unconscionable conduct by QHG I am not satisfied that the orders should be made.

Declarations

37 The Court has a wide discretion whether to grant declaratory relief: Ainsworth v Criminal Justice Commission [1992] HCA 10; (1992) 175 CLR 564 at 581-582. Declarations should deal with a real controversy, not hypothetical or theoretical questions. If a declaration of a contravention of a statutory provision is made then the terms of the declaration should be expressed in a manner that indicates how and why the conduct amounts to a contravention: Australian Securities & Investments Commission v Westpac Banking Corporation [2018] FCA 1733 at [29].

38 I am satisfied that it is appropriate for declaratory relief to be ordered in the terms sought by the ACCC, save as to unconscionable conduct. The principles to be applied were summarised in Australian Building and Construction Commissioner v Construction, Forestry, Mining and Energy Union [2017] FCAFC 113; (2017) 254 FCR 68 at [90]-[93]. For reasons I have given, and to the extent I have identified, the proposed declaratory orders reflect contraventions that have been demonstrated by the facts as agreed. They identify the nature of the contravening conduct. They will serve to record the Court's disapproval of the conduct, inform others of the nature of the contravening conduct and assist in deterring others from engaging in similar conduct.

Disqualification order

39 I recently summarised the principles to be applied in deciding whether to make a disqualification order in Australian Competition and Consumer Commission v Geowash Pty Ltd (Subject to a Deed of Company Arrangement) (No 4) [2020] FCA 23 at [65]-[69].

40 Ms Howe was the sole director and secretary of QHG for the whole of the period of the contravening conduct. She controlled QHG at that time and directed its staff who assisted her in implementing the Roll Up Plan. The contravening conduct is properly characterised as serious and ongoing. It was the role of a director such as Ms Howe to ensure that a strategy such as the Roll Up Plan conformed to the law and the prevailing standards of appropriate commercial behaviour. On the facts as agreed her conduct fell well below meeting that obligation.

41 The proposed disqualification period of three years will protect the public, particularly as Ms Howe continues to be employed in a similar role to that which she performed for QHG. Ms Howe accepts that the disqualification order is appropriate. No undue prejudice is advanced as a reason why the order should not be made. The order is justified on the basis of specific and general deterrence.

Pecuniary penalties

42 The quantum of an appropriate penalty is to be determined by synthesising all relevant factors into an overall figure: Singtel Optus Pty Ltd v Australian Competition and Consumer Commission [2012] FCAFC 20 at [54]. The process is undertaken instinctively, not mathematically: Director of Consumer Affairs Victoria v Alpha Flight Services Pty Ltd [2015] FCAFC 118. It requires an identification of the significant factors relevant to assessing penalty in the particular case and then the assessment of an amount that will deter conduct of that kind in the future, both in the community generally and by the parties involved.

43 Pecuniary penalties put a price on contravention in order to deter repetition: Commonwealth of Australia v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; (2015) 258 CLR 482 at [55] applying the reasoning of French J in Trade Practices Commission v CSR Ltd [1990] FCA 762. The civil penalty is to be set to deter those engaged in trade and commerce 'from the cynical calculation involved in weighing up the risk of penalty against the profits to be made from contravention': Singtel Optus cited with approval in ACCC v TPG Internet at [66].

44 Section 224(2) of the ACL provides that in determining the appropriate penalty the Court must have regard to all relevant matters including:

(a) the nature and extent of the act or omission and of any loss or damage suffered as a result of the act or omission; and

(b) the circumstances in which the act or omission took place; and

(c) whether the person has previously been found by a court in proceedings under Chapter 4 or [Part 5‑2] to have engaged in any similar conduct.

45 Factors that may be relevant were set out in NW Frozen Foods Pty Ltd v Australian Competition and Consumer Commission [1996] FCA 1134; (1996) 71 FCR 285. Those factors are not a checklist: Australian Competition and Consumer Commission v Coles Supermarkets Australia Pty Ltd [2015] FCA 330 at [9]. The task is to consider what is of particular relevance in each case.

46 There is express provision to the effect that where conduct constitutes a contravention of two or more provisions that attract civil penalties under the ACL, a person is not liable to more than one penalty in respect of the same conduct: s 224(4)(b).

47 Where there are a number of contraventions that are considered to form part of a single course of conduct then an overall penalty may be assessed on that basis: Construction, Forestry, Mining and Energy Union v Cahill [2010] FCAFC 39 at [39]. The extent to which that may be appropriate depends on the circumstances of the case.

48 As to cases where a regulator such as the ACCC has reached agreement with a party as to an appropriate penalty for contravening conduct, in Commonwealth of Australia v Director, Fair Work Building Industry Inspectorate [2015] HCA 46; (2015) 258 CLR 482, the High Court approved of the following propositions in Minister for Industry, Tourism and Resources v Mobil Oil Australia Pty Ltd [2004] FCAFC 72 at [51]:

(i) It is the responsibility of the Court to determine the appropriate penalty to be imposed under s 76 of the TP Act in respect of a contravention of the TP Act.

(ii) Determining the quantum of a penalty is not an exact science. Within a permissible range, the courts have acknowledged that a particular figure cannot necessarily be said to be more appropriate than another.

(iii) There is a public interest in promoting settlement of litigation, particularly where it is likely to be lengthy. Accordingly, when the regulator and contravenor have reached agreement, they may present to the Court a statement of facts and opinions as to the effect of those facts, together with joint submissions as to the appropriate penalty to be imposed.

(iv) The view of the regulator, as a specialist body, is a relevant, but not determinative consideration on the question of penalty. In particular, the views of the regulator on matters within its expertise (such as the ACCC's views as to the deterrent effect of a proposed penalty in a given market) will usually be given greater weight than its views on more 'subjective' matters.

(v) In determining whether the proposed penalty is appropriate, the Court examines all the circumstances of the case. Where the parties have put forward an agreed statement of facts, the Court may act on that statement if it is appropriate to do so.

(vi) Where the parties have jointly proposed a penalty, it will not be useful to investigate whether the Court would have arrived at that precise figure in the absence of agreement. The question is whether that figure is, in the Court's view, appropriate in the circumstances of the case. In answering that question, the Court will not reject the agreed figure simply because it would have been disposed to select some other figure. It will be appropriate if within the permissible range.

49 The maximum penalty for a contravention of s 29 of the ACL at the relevant time was $1,100,000 for a body corporate and $220,000 for a natural person. The maximums applied for 'each act or omission': s 224 of the ACL.

50 The penalty proposed by the ACCC for QHG is $700,000. QHG does not agree the quantum of the penalty, but makes no submissions opposing the quantum sought by the ACCC. The agreed penalty in the case of Ms Howe is $50,000.

51 I consider the following factors to be of significance for assessing the appropriate penalty for QHG in the present case:

(1) The conduct was planned, deliberate and sustained over a considerable period.

(2) The conduct was blatant and involved a concerted effort to trick investors into switching property managers to a QHG approved property manager. It was conduct about which there could not be any reasonable uncertainty as to its propriety.

(3) The conduct escalated and involved the implementation of further strategies and in that sense it is not accurate to view the conduct as a single course of conduct. There was a single overall plan that was implemented by a strategy that developed over time and deployed different representational conduct that was false and misleading in order to secure the outcome of investors switching to a QHG approved property manager.

(4) The conduct exploited the circumstances of the NRAS, a government scheme designed to provide affordable rental properties, not the conferral of economic power to secure control of the appointment of property managers.

(5) The conduct involved misleading and false representations being made to at least 450 investors.

(6) The property manager for at least 260 properties was changed during the period of the contraventions.

(7) It may be inferred that the conduct caused a number of investors to switch property managers, but there is no evidence, by admission or otherwise, that enables a conclusion to be reached as to the full extent to which this was the case.

(8) The parties agree that the transfer by investors of their property management services resulted in loss for the property manager in the form of lost fees that varied because the extent of the loss was dependent upon the rent paid for the property.

(9) The extent of the loss suffered is difficult to estimate.

(10) Loss suffered may include a loss of the investor's ability to freely choose a property manager and loss of convenience and service quality, but no evidence was led as to whether this was the case.

(11) There is no evidence of the nature or extent of the financial advantage secured by the conduct.

(12) QHG has not previously been found to have engaged in any similar contravening conduct.

(13) In the financial year ending 30 June 2019, QHG earned an income of $1,150,000 and reported a profit of $50,729.

(14) QHG's allocations under the NRAS have been transferred to other Approved Applicants and QHG received no consideration for the transfers.

(15) The conduct has not been demonstrated to be unconscionable conduct and the penalty was proposed by the ACCC on the basis that the conduct also contravened that statutory standard.

(16) QHG did not have a compliance programme in place.

(17) QHG has cooperated with the ACCC during the course of its investigations and has admitted the contravening conduct after investigation by the ACCC.

(18) The initial investigation by the ACCC concerned a related allegation of third line forcing conduct and QHG wrote to certain investors advising that the ACCC had confirmed that it would not be continuing with any investigation which statement was false.

(19) QHG did not cease the contravening conduct immediately upon the ACCC undertaking its investigation and denied any wrongdoing until agreed facts were prepared more than six months after proceedings were commenced by the ACCC.

(20) In breach of an undertaking to the ACCC, QHG continued issuing correspondence to investors as part of the Roll Up Plan.

(21) The admissions have avoided the costs of a complex hearing.

(22) The subsequent insolvency of QHG is to be taken into account but must be balanced with the need for deterrence.

52 It may be inferred from the nature and extent of the admitted conduct, the effort that went into the conduct and its sustained nature that there was thought to be a considerable financial advantage to be gained from securing investors to switch property managers. A significant financial penalty is required to deter conduct of that kind. This is not a case where there is an absence of any evidence of suggested harm: cf Australian Competition and Consumer Commission v MSY Technology Pty Ltd (No 2) [2011] FCA 382 at [79] (Perram J). Here, the parties agree that there was harm caused by the conduct. However, the nature and extent of that harm is not quantified (and it is agreed that it would be difficult to quantify).

53 Had I been persuaded that the conduct of QHG was also properly to be characterised as unconscionable and therefore exploitative of hundreds of investors for a sustained period of time, I would have considered the proposed penalty to have been inadequate for conduct of that kind. The prescription against unconscionable conduct protects those who are unlikely to be able to raise complaint or otherwise advocate in their own interests. Therefore, appropriate financial penalties are required to deter the insidious and unscrupulous who seek to profit from exploiting their vulnerability. Section 21 of the ACL is a law that applies only in instances where the failure to adhere to recognised community standards of commercial behaviour is blatant. For those reasons, it is conduct of a kind which requires significant penalties in order to ensure general and specific deterrence.

54 However, in view of the fact that the ACCC has not established that the admitted conduct amounts to unconscionable conduct I am satisfied that the penalty proposed by the ACCC is appropriate. In forming that view I have taken account of the totality principle and am satisfied that the penalty is in proportion to the conduct of QHG viewed as a whole. The representational conduct was blatantly wrong, it was serious and sustained and it was directed at a large number of investors.

55 In the case of Ms Howe, the penalty amount is agreed. In those circumstances, I need to be satisfied that the penalty is within the appropriate range. As to Ms Howe's involvement in the contravening conduct of QHG, in addition to the matters that I have already described concerning the nature and extent of that conduct, the following further matters are significant:

(1) Ms Howe has agreed to the disqualification order which will apply for three years.

(2) There is no evidence that Ms Howe benefitted personally from the conduct. Her role was an employee who did not have a financial interest in QHG.

(3) Ms Howe's annual salary between 2017 and 2019 has been between about $100,000 and $130,000.

(4) Ms Howe is currently employed in a similar role and receives an annual salary of $122,500.

56 Having regard to the above factors and the rest of the circumstances I have described, I am satisfied that the agreed penalty is within the permissible range, albeit that the penalty for Ms Howe is at the low end of that range.

Publication orders

57 The agreed orders provide for an email to be sent to each of the 1,215 investors for whom QHG held allocations under the NRAS. I am satisfied that the proposed notice will serve a corrective purpose and is directed to ensuring that all investors, so far as possible, are informed as to the correct position. The proposed notice should be amended to delete references to unconscionable conduct.

Orders for findings to be evidence in other proceedings

58 It is agreed that an order should be made for a copy of these reasons for judgment with the seal of the Court affixed to be retained for the purposes of s 137H of the Competition and Consumer Act. Those provisions facilitate proof of findings made in proceedings of the present kind in certain other proceedings and I am satisfied that the order should be made.

Costs and time for Ms Howe to pay

59 The parties propose orders as to time for Ms Howe to pay her pecuniary penalty and orders as to costs and those orders should be made on the basis that they agreed.

I certify that the preceding fifty-nine (59) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Colvin. |

Associate: