Strawbridge, in the matter of Virgin Australia Holdings Ltd (administrators appointed) (No 2) [2020] FCA 717

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The Interlocutory Process filed on 11 May 2020 be made returnable at 10.15am on 13 May 2020.

Tiger International No. 1 Pty Ltd

Joinder

2. Pursuant to rule 9.05 of the Federal Court Rules 2011 (Cth) that Tiger International No. 1 Pty Ltd (Administrators Appointed) ACN 606 131 944 (Tiger 1) be added to this proceeding as Fortieth Plaintiff.

First meeting of creditors

3. Pursuant to section 1322(4)(a) of the Corporations Act the convening and holding of the first meeting of creditors of Tiger 1 in accordance with section 436E of the Corporations Act, pursuant to the notice sent to creditors in accordance with sections 75-225(1) and 75-15 of the Insolvency Practice Rules (Corporations) 2016 (Cth) (IPR), is not invalidated by reason of the notice having been issued on 7 May 2020 (resulting in less than five business days' notice of the meeting being given to the creditors of Tiger 1).

4. Pursuant to section 447A(1) of the Corporations Act and section 90-15 of the IPSC, that Part 5.3A of the Corporations Act is to operate, nunc pro tunc, in relation to Tiger 1, as if any notice (Notice) required to be given pursuant to sections 75-225(1) and 75-15 of the IPR is validly given to creditors of Tiger 1 by taking the following steps in accordance:

(a) where the First Plaintiffs:

(i) have an email address for a creditor, by sending the Notice by email to each such creditor;

(ii) where the First Plaintiffs do not have an email address for a creditor, but have a postal address for the creditor (or have received notification of non-delivery of a notice sent by email in accordance with (a)(i) above), by sending the Notice by posting a copy of it to the postal address for each such creditor;

(b) by publishing the Notice on the Australian Securities and Investments Commission (ASIC) published notices website at https://insolvencynotices.asic.gov.au/; and

(c) by publishing the Notice on the website maintained by the First Plaintiffs at https://www2.deloitte.com/au/en/pages/finance/articles/virgin-australia-holdings-limited-subsidiaries.html.

Other notices to creditors to be provided electronically

5. Pursuant to section 447A(1) of the Corporations Act and section 90-15 of the IPSC, that if, pursuant to any provision in any of Part 5.3A of the Corporations Act, Part 5.3A of the Corporations Regulations 2001 (Cth), the IPSC, or the IPR, the First Plaintiffs are required to provide any other notification to creditors during the administration of Tiger 1, the applicable notice requirements will be satisfied if the First Plaintiffs give such notice by taking the following steps:

(a) where the First Plaintiffs:

(i) have an email address for a creditor, by notifying each such creditor of the relevant matter via email;

(ii) do not have an email address for a creditor, but have a postal address for that creditor (or have received notification of non-delivery of a notice sent by email in accordance with (a)(i) above), by notifying each such creditor in writing of the relevant matter via post;

(b) by publishing notice of the relevant matter on the website maintained by the First Plaintiffs at https://www2.deloitte.com/au/en/pages/finance/articles/virgin-australia-holdings-limited-subsidiaries.html; and

(c) to the extent that the matter relates to a meeting that is the subject of section 75-40(4) of the IPR, by causing notice of the meeting to be published on the ASIC published notices website at https://insolvencynotices.asic.gov.au/.

Conducting meetings of creditors electronically

6. Pursuant to section 447A(1) of the Corporations Act and section 90-15 of the IPSC, that, to the extent not permitted specifically by sections 75-30, 75-35 and 75-75 of the IPR and the Corporations (Coronavirus Economic Response) Determination (No. 1) 2020 (Cth), the First Plaintiffs be permitted to hold meetings of creditors during the administration of Tiger 1 by telephone or audio-visual conference only at the place of the First Plaintiffs’ offices (without creditors of Tiger 1 being able to attend physically at that place), with such details of the arrangements for using the telephone or audio-visual conference facilities to be specified in each of the notices issued to creditors.

7. Pursuant to section 447A(1) of the Corporations Act and section 90-15 of the IPSC, that, to the extent not permitted specifically by section 75-35(2)(b) of the IPR and the Corporations (Coronavirus Economic Response) Determination (No. 1) 2020 (Cth), the creditors of Tiger 1 who wish to participate at any meeting of Tiger 1 by telephone or audio-visual conference only at the place of the First Plaintiffs’ offices (without creditors of Tiger 1 being able to attend physically at that place), must lodge with the First Plaintiffs, no later than the second last business day before the day on which the meeting is held, specific proxy forms containing the information in section 75-35(2)(b)(i)-(iii) of the IPR (with liberty to notify the First Plaintiffs of the withdrawal of that specific proxy and amended vote following any discussion at a meeting, in advance of a resolution being passed).

Committee of Inspection

8. Pursuant to section 447A(1) of the Corporations Act and 90-15 of the IPSC, that Divisions 75 and 80 of the IPSC, and Division 75 of the IPR are to operate as if the requirement in sections 80-10 and 80-15 of the IPSC for the creditors of a company to resolve that a committee of inspection be formed and to appoint members of the committee of inspection, be dispensed with.

9. Order 6(b) of the orders made on 24 April 2020 be varied by deleting the words “Thirty-Ninth Plaintiffs” and replacing them with the words “Fortieth Plaintiffs”, such that that order reads:

a single committee of inspection be formed in respect of the Second to Fortieth Plaintiffs.

10. Pursuant to section 447A(1) of the Corporations Act and 90-15 of the IPSC First Plaintiffs are not required to issue any further Proposal (as that term is defined in Order 6(d) of the orders made on 24 April 2020) to the creditors of the Second to Fortieth Plaintiffs.

Extension of Convening Period

11. Pursuant to section 439A(6) of the Corporations Act the convening period defined in section 439A(5)(b) of the Corporations Act in respect of each of the Second to Fortieth Plaintiffs (together, the Virgin Companies and each, a Virgin Company), be extended until 18 August 2020.

12. Pursuant to section 447A(1) of the Corporations Act, that Part 5.3A of the Corporations Act is to operate in relation to each of the Virgin Companies such that, notwithstanding section 439A(2) of the Corporations Act, the second meeting of the creditors of each of the Virgin Companies required under section 439A of the Corporations Act may be convened at any time before, or within, five (5) business days after, the end of the convening period as extended by order 12 above (provided the First Plaintiffs give notice of the meetings to eligible creditors of each of the Virgin Companies (including the persons claiming to be creditors of the Virgin Companies) at least five (5) business days before the meeting).

Limitation of Administrators’ Liability

Current Rio Tinto Agreement

13. Pursuant to sections 447A(1) and 443B(8) of the Corporations Act and section 90-15 of the IPSC, that Part 5.3A of the Corporations Act is to operate in relation to the Plaintiffs as if section 443A(1) of the Corporations Act provides that:

(a) the liabilities of the First Plaintiffs (in their capacity as administrators of the Twentieth Plaintiff) incurred with respect to any obligations arising out of, or in connection with, an agreement entered into with Rio Tinto Services Limited in respect of charter flights as described in paragraph 101 of the Strawbridge Affidavit (Rio Tinto Agreement), are in the nature of debts incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of the Twentieth Plaintiff; and

(b) notwithstanding that the liabilities in suborder (a) are debts incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of the Twentieth Plaintiff, the First Plaintiffs will not be personally liable to repay such debts or satisfy such liabilities to the extent that the proceeds of any applicable insurance policy held by or for the benefit of the First Plaintiffs or the Twentieth Plaintiff, or assets of the Twentieth Plaintiff are in aggregate insufficient to satisfy the debt and liabilities incurred by the First Plaintiffs arising out of, or in connection with, the Rio Tinto Agreement.

Conditional Credits

14. Pursuant to section 90-15 of the IPSC, the Court directs the First Plaintiffs would be justified in issuing conditional credits to customers of the Virgin Companies in accordance with the proposal set out in Schedule 2 to these orders (Conditional Credits).

15. Pursuant to section 447A(1) of the Corporations Act and section 90-15 of the IPSC, that Part 5.3A of the Corporations Act is to operate in relation to the Plaintiffs as if section 443A(1) of the Corporations Act provides that:

(a) the liabilities of the First Plaintiffs incurred with respect to any obligations arising out, of or in connection with, the issuing of Conditional Credits, including but not limited to taxes, airline surcharges and ancillary fees associated to the Conditional Credits Proposal, are in the nature of debts incurred by the Administrators in the performance and exercise of their functions as joint and several administrators of each of the Virgin Companies; and

(b) notwithstanding that the liabilities for the Conditional Credits are debts incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of each of the Virgin Companies, the First Plaintiffs shall not be personally liable to repay such debts or satisfy such liabilities to the extent that the assets of the particular Virgin Company or Virgin Companies that are the issuers of the Conditional Credits are insufficient to satisfy the debt and liabilities incurred by the First Plaintiffs arising out of, or in connection with, the issuance of the Conditional Credits.

Other ancillary orders

16. The First Plaintiffs must take all reasonable steps to cause notice of these orders to be given, within one (1) business day after the making of these orders, to:

(a) the creditors (including persons or entities claiming to be creditors) of each of the Virgin Companies, in the following manner:

(i) where the First Plaintiffs have an email address for a creditor, notifying each such creditor, via email, of the making of the orders and providing a link to a website where the creditor may download the orders and the Interlocutory Process;

(ii) where the First Plaintiffs do not have an email address for a creditor but have a postal address for that creditor (or have received notification of non-delivery of a notice sent by email in accordance with (a)(i) above), notifying each such creditor, via post, of the making of the orders and providing a link to a website where the creditor may download the orders and the Interlocutory Process; and

(iii) placing scanned, sealed copies of the orders and the Interlocutory Process on the website maintained by the First Plaintiffs at https://www2.deloitte.com/au/en/pages/finance/articles/virgin-australia-holdings-limited-subsidiaries.html.; and

(b) ASIC; and

(c) the Australian Competition and Consumer Commission (ACCC).

17. Any person who can demonstrate a sufficient interest has liberty to apply to vary or discharge any orders made pursuant to orders 2 to 16 above, on 1 business days' written notice being given to the Plaintiffs and to the Associate to Justice Middleton.

18. The First Plaintiffs have liberty to apply for any further extension of the convening period as extended by order 12 above at any time before 18 August 2020.

19. Order 12 of the orders made on 24 April 2020 be varied by deleting the words “Thirty-Ninth Plaintiffs” and replacing them with the words “Fortieth Plaintiffs” such that that order reads:

The Plaintiffs have liberty to apply on 1 business day’s written notice to the Court in relation to any variation of these orders or any other matter generally arising in the administrations of each of the Second to Fortieth Plaintiffs.

20. The Plaintiffs' costs of this application be costs in the administration of the Virgin Companies, jointly and severally.

21. These orders be entered forthwith.

22. The hearing be stood over until 10.15am on Friday, 15 May 2020 in respect of paragraphs 14, 15, 18, 20, 21, 22 of the Interlocutory Process.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

NSD 464 of 2020 | ||

IN THE MATTER OF VIRGIN AUSTRALIA HOLDINGS LTD (ADMINISTRATORS APPOINTED) ACN 100 686 226 & ORS | ||

VAUGHAN STRAWBRIDGE, SALVATORE ALGERI, JOHN GREIG AND RICHARD HUGHES, IN THEIR CAPACITY AS JOINT AND SEVERAL VOLUNTARY ADMINISTRATORS OF EACH OF VIRGIN AUSTRALIA HOLDINGS LTD (ADMINISTRATORS APPOINTED) First Plaintiffs VIRGIN AUSTRALIA HOLDINGS LTD (ADMINISTRATORS APPOINTED) ACN 100 686 226 Second Plaintiff VIRGIN AUSTRALIA INTERNATIONAL OPERATIONS PTY LTD (ADMINISTRATORS APPOINTED) ACN 155 859 608 (and others named in the Schedule) Third Plaintiff | ||

JUDGE: | MIDDLETON J |

DATE OF ORDER: | 15 MAY 2020 |

THE COURT ORDERS THAT:

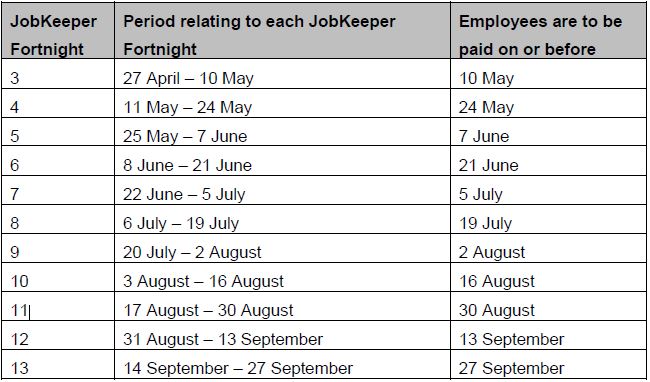

JobKeeper

1. By consent of the First Plaintiffs and the Deputy Commissioner of Taxation, the hearing of paragraph 18 of the Interlocutory Process be stood over until 10.15am on 20 May 2020, with liberty to the parties to provide the Associate to Middleton J any orders which are not opposed by the Deputy Commissioner of Taxation with respect to the relief sought in that paragraph.

Limitation of Administrators' Liability

Specified Categories of Future Agreements

2. Pursuant to section 447A(1) of the Corporations Act 2001 (Cth) (Corporations Act) and section 90-15 of the Insolvency Practice Schedule 2016 (Cth), being Schedule 2 to the Corporations Act (IPSC), Part 5.3A of the Corporations Act is to operate in relation to the Plaintiffs as if section 443A(1) of the Corporations Act provides that:

(a) the liabilities of the First Plaintiffs (in their capacity as administrators of each of the Virgin Companies) incurred with respect to any obligations arising out of, or in connection with, any future:

(i) agreement on the terms of, or substantially in accordance with, the Aircraft Protocols document in the form exhibited at Tab 12 of Exhibit VNS-2 to the Strawbridge Affidavit;

(ii) alliance agreements, being international arrangements established with various global airlines that provide the Virgin Companies with a long distance international network;

(iii) procurement contracts, including:

A. in-flight services agreements, being agreements entered into for the provision of food and beverages and other retail on-board services, catering, entertainment and internet wifi on flights operated by the Virgin Companies;

B. ground handling agreements, being agreements entered into for the provision of ground handling services for the Virgin Companies' flight arrivals and departures at national and international airports;

C. operational systems agreements, being agreements entered into for the provision of support and maintenance services in relation to licenced software, systems, platforms and network infrastructure;

D. fuel agreements, being agreements entered into for the supply and delivery of fuel to the Virgin Companies at various locations throughout Australia, New Zealand and the United States;

E. maintenance and parts agreements, being agreements entered into for the provision of maintenance, repair and modification services for aircraft operated by the Virgin Companies, including the provision of the relevant component parts;

F. IT agreements, being agreements entered into for the provision of core computer infrastructure and end user computing support services and business services to the Virgin Companies;

(iv) trade mark licence agreements;

(v) airport agreements, being agreements entered into with major airports across Australia, for the use of terminal gates, public spaces and facilities and for sub-leases in relation to each of the Virgin Companies' airport lounges;

(vi) charter agreements, being agreements entered into with various major companies for the supply of scheduled air transport services for personnel and freight to nominated destinations agreed between the parties to the agreement;

(vii) cargo agreements, being agreements entered into for the handling of cargo and the provision of management, administration and support services;

(viii) corporate sales agreements, being agreements entered into with major travel agents and other platforms, including with both government and private counterparties, which set out incentives offered by the Virgin Companies for the sale of Virgin flights by the relevant agents;

(ix) industry/agency agreements, being agreements entered into which provide for the preferred supply by the Virgin Companies of flight services to each of its clients, including with both government and private counterparties;

(x) insurance arrangements, including contracts to support the ongoing operation of the Virgin Companies' self-insurance scheme; and

(xi) training agreements, being agreements entered into to provide ongoing training to crew members.

(together, the Applicable Agreements and each, an Applicable Agreement) are in the nature of debts incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of each of the Virgin Companies; and

(b) notwithstanding that the liabilities in suborder (a) are debts incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of each of the Virgin Companies, the First Plaintiffs will not be personally liable to repay such debts or satisfy such liabilities to the extent that the assets of the particular Virgin Company or Virgin Companies that is or are a party to the particular Applicable Agreement are insufficient to satisfy the debt and liabilities incurred by the First Plaintiffs arising out of, or in connection with, the Applicable Agreements.

3. Pursuant to section 447A of the Corporations Act and section 90-15 of the IPSC, the First Plaintiffs are to provide notice, in the Applicable Agreement or otherwise, to any counterparty to an Applicable Agreement of order 2 above, prior to that counterparty entering into an Applicable Agreement.

4. Pursuant to section 447A of the Corporations Act and section 90-15 of the IPSC, the First Plaintiffs are to:

(a) keep a schedule noting each Applicable Agreement entered into by the First Plaintiffs on behalf of any of the Virgin Companies; and

(b) provide an update to the Committee of Inspection formed for the Second to Fortieth Plaintiffs (Committee), at each meeting of the Committee, as to each Applicable Agreement that the First Plaintiffs have entered into or proposed to be entered into together with estimated debts that may be incurred in respect of each Applicable Agreement, on behalf of any of the Virgin Companies.

Virgin Company Loan Monies

5. Pursuant to section 447A(1) of the Corporations Act and section 90-15 of the IPSC, Part 5.3A of the Corporations Act is to operate in relation to the Plaintiffs as if section 443A(1) of the Corporations Act provides that:

(a) any liability incurred by the First Plaintiffs arising out, of or in connection with, any loan or monies borrowed by a Virgin Company from another Virgin Company or Virgin Companies are in the nature of debts incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of each of the Virgin Companies; and

(b) notwithstanding that the liabilities in suborder (a) are debts incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of each of the Virgin Companies, the First Plaintiffs will not be personally liable to repay such debts or satisfy such liabilities to the extent that the assets of the particular Virgin Company that has borrowed monies from any other Virgin Company or Virgin Companies are insufficient to satisfy the debt and liabilities incurred by the First Plaintiffs.

Report on company activities and property

6. Pursuant to section 447A(1) of the Corporations Act and section 90-15 of the IPSC, Part 5.3A of the Corporations Act is to operate in relation to the Plaintiffs as if:

(a) a single report in the prescribed form about the business, property, affairs and financial circumstances of the Second, Third, Seventh to Tenth, Thirteenth, and Ninetieth to Twenty-Fourth Plaintiffs be prepared by each of the directors of the Second Plaintiff;

(b) the requirement in section 438B(2) that the directors of each of the Second, Third, Seventh to Tenth, Thirteenth, and Ninetieth to Twenty-Fourth Plaintiffs prepare a separate report about the business, property, affairs and financial circumstances of each of those companies, be dispensed with; and

(c) the requirement in section 438B(2) that the directors of each of the Fourth to Sixth, Eleventh to Twelfth, Fourteenth to Eighteenth, and Twenty-Fifth to Fortieth Plaintiffs prepare a separate report about the business, property, affairs and financial circumstances of each of those companies, be maintained.

Leave to members of the committee of inspection to derive profit

7. Subject to Orders 8 and 9 below, pursuant to sections 80-55(5)(b) and 90-15 of the IPSC, leave be granted to the members of the Committee to derive a profit or advantage from the external administration of each of the Virgin Companies.

8. No leave be granted for the members of the Committee to receive any gift or remuneration from the external administration of any of the Virgin Companies by reason of their position as a member of the Committee.

9. Pursuant to section 447A of the Corporations Act and section 90-15 of the IPSC, the First Plaintiffs are to:

(a) keep a schedule noting each agreement entered into by the First Plaintiffs on behalf of any of the Virgin Companies with a member of the Committee or any related entity of a member of the Committee (Agreements with Committee Members); and

(b) provide an update to the Committee, at each meeting of the Committee, as to each of the Agreements with Committee Members that the First Plaintiffs have entered into on behalf of any of the Virgin Companies;

(c) include, as a section in a report to creditors of the Virgin Companies pursuant to section 75-225 of the Insolvency Practice Rules (Corporations) 2016 (Cth), a list of the Agreements with Committee Members and a summary of the key terms of each such agreement.

Bank account

10. Pursuant to sections 65-45 and 90-15 of the IPSC, the First Plaintiffs (in their capacity as administrators of each of the Virgin Companies) are not required to maintain a separate administration account in relation to each of the Virgin Companies (as otherwise required by the operation of Division 65 of the IPS).

Other ancillary orders

11. The First Plaintiffs must take all reasonable steps to cause notice of these orders to be given, within one (1) business day after the making of these orders, to:

(a) the creditors (including persons or entities claiming to be creditors) of each of the Virgin Companies, in the following manner:

(i) where the First Plaintiffs have an email address for a creditor, notifying each such creditor, via email, of the making of the orders and providing a link to a website where the creditor may download the orders and the Interlocutory Process;

(ii) where the First Plaintiffs do not have an email address for a creditor but have a postal address for that creditor (or have received notification of non-delivery of a notice sent by email in accordance with (a)(i) above), notifying each such creditor, via post, of the making of the orders and providing a link to a website where the creditor may download the orders and the Interlocutory Process; and

(iii) placing scanned, sealed copies of the orders and the Interlocutory Process on the website maintained by the First Plaintiffs at https://www2.deloitte.com/au/en/pages/finance/articles/virgin-australia-holdings-limited-subsidiaries.html.; and

(b) the Australian Securities and Investments Commission;

(c) the Deputy Commissioner of Taxation; and

(d) the Attorney-General's Department (administering the Fair Entitlements Guarantee Scheme).

12. Any person who can demonstrate a sufficient interest has liberty to apply to vary or discharge any orders made pursuant to orders 2 to 10 above, on 1 business day's written notice being given to the Plaintiffs and to the Associate to Justice Middleton.

13. The Plaintiffs' costs of this application be costs in the administration of the Virgin Companies, jointly and severally.

14. The hearing be stood over until 10.15am on Wednesday 20 May 2020 in respect of paragraph 18 of the Interlocutory Process.

15. These orders be entered forthwith.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

NSD 464 of 2020 | ||

IN THE MATTER OF VIRGIN AUSTRALIA HOLDINGS LTD (ADMINISTRATORS APPOINTED) ACN 100 686 226 & ORS | ||

VAUGHAN STRAWBRIDGE, SALVATORE ALGERI, JOHN GREIG AND RICHARD HUGHES, IN THEIR CAPACITY AS JOINT AND SEVERAL VOLUNTARY ADMINISTRATORS OF EACH OF VIRGIN AUSTRALIA HOLDINGS LTD (ADMINISTRATORS APPOINTED) First Plaintiffs VIRGIN AUSTRALIA HOLDINGS LTD (ADMINISTRATORS APPOINTED) ACN 100 686 226 Second Plaintiff VIRGIN AUSTRALIA INTERNATIONAL OPERATIONS PTY LTD (ADMINISTRATORS APPOINTED) ACN 155 859 608 (and others named in the Schedule) Third Plaintiff | ||

JUDGE: | MIDDLETON J |

DATE OF ORDER: | 20 MAY 2020 |

THE COURT ORDERS THAT:

1. An order pursuant to section 447A(1) of the Corporations Act 2001 (Cth) (Corporations Act), that Part 5.3A of the Corporations Act is to operate in relation to the Plaintiffs as if section 443A(1) of the Corporations Act provides as follows:

(a) To the extent that:

(i) the First Plaintiffs incur any liability under section 443A(1) of the Corporations Act for debts to the Commonwealth as a result of any JobKeeper payment made during the period from 20 April 2020 to the earlier of 31 August 2020 and the end of the voluntary administration of the Ninth Plaintiff pursuant to the Coronavirus Economic Response Package (Payments and Benefits) Rules 2020 (Cth) (as amended) and Coronavirus Economic Response Package (Payments and Benefits) Act 2020 (Cth) (together, the Coronavirus legislation) arising out of, or in connection with, the employment of staff of the Ninth Plaintiff; and

(ii) those debts to the Commonwealth were incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of the Ninth Plaintiff; then

the First Plaintiffs shall not be personally liable for such debts to the extent that those debts exceed the assets of the Ninth Plaintiff.

(b) Order 1(a) does not apply to any liability for a debt incurred by the First Plaintiffs in consequence of the First Plaintiffs’ failure to act in good faith and without negligence in connection with the preparation or lodgement of the necessary documents or information for a JobKeeper payment.

(c) To the extent that:

(i) the First Plaintiffs incur any liability under section 443A(1) of the Corporations Act for debts to the Commonwealth as a result of any JobKeeper payment made during the period from 20 April 2020 to the earlier of 31 August 2020 and the end of the voluntary administration of the Tenth Plaintiff pursuant to the Coronavirus legislation arising out of, or in connection with, the employment of staff of the Tenth Plaintiff; and

(ii) those debts to the Commonwealth were incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of the Tenth Plaintiff; then

the First Plaintiffs shall not be personally liable for such debts to the extent that those debts exceed the assets of the Tenth Plaintiff.

(d) Order 1(c) does not apply to any liability for a debt incurred by the First Plaintiffs in consequence of the First Plaintiffs’ failure to act in good faith and without negligence in connection with the preparation or lodgement of the necessary documents or information for a JobKeeper payment.

(e) To the extent that:

(i) the First Plaintiffs incur any liability under section 443A(1) of the Corporations Act for debts to the Commonwealth as a result of any JobKeeper payment made during the period from 20 April 2020 to the earlier of 31 August 2020 and the end of the voluntary administration of the Thirteenth Plaintiff pursuant to the Coronavirus legislation arising out of, or in connection with, the employment of staff of the Thirteenth Plaintiff; and

(ii) those debts to the Commonwealth were incurred by the First Plaintiffs in the performance and exercise of their functions as joint and several administrators of the Thirteenth Plaintiff; then

the First Plaintiffs shall not be personally liable for such debts to the extent that those debts exceed the assets of the Thirteenth Plaintiff.

(f) Order 1(e) does not apply to any liability for a debt incurred by the First Plaintiffs in consequence of the First Plaintiffs’ failure to act in good faith and without negligence in connection with the preparation or lodgement of the necessary documents or information for a JobKeeper payment.

(g) Orders 1(a), 1(c) and 1(e) do not apply to any liability of the First Plaintiffs arising pursuant to section 11(2) and (3) of the Coronavirus Economic Response Package (Payments and Benefits) Act 2020 (Cth).

Other ancillary orders

2. The First Plaintiffs must take all reasonable steps to cause notice of these orders to be given, within one (1) business day after the making of these orders, to:

(a) the creditors (including persons or entities claiming to be creditors) of each of the Virgin Companies, in the following manner:

(i) where the First Plaintiffs have an email address for a creditor, notifying each such creditor, via email, of the making of the orders and providing a link to a website where the creditor may download the orders and the Interlocutory Process;

(ii) where the First Plaintiffs do not have an email address for a creditor but have a postal address for that creditor (or have received notification of non-delivery of a notice sent by email in accordance with (a)(i) above), notifying each such creditor, via post, of the making of the orders and providing a link to a website where the creditor may download the orders and the Interlocutory Process; and

(iii) placing scanned, sealed copies of the orders and the Interlocutory Process on the website maintained by the First Plaintiffs at https://www2.deloitte.com/au/en/pages/finance/articles/virgin-australia-holdings-limited-subsidiaries.html.; and

(b) the Australian Securities and Investments Commission; and

(c) the Deputy Commissioner of Taxation;

3. Any person who can demonstrate a sufficient interest has liberty to apply to vary or discharge any orders made pursuant to orders 1 above, on 1 business day’s written notice being given to the Plaintiffs and to the Associate to Justice Middleton.

4. The Plaintiffs' costs of this application be costs in the administration of the Virgin Companies, jointly and severally.

5. These orders be entered forthwith.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MIDDLETON J:

INTRODUCTION AND OVERVIEW

1 On 13, 15 and 20 May 2020 I made a number of orders on the application of the First Plaintiffs in this proceeding. These are the reasons for those orders.

2 The First Plaintiffs, Vaughan Strawbridge, Salvatore Algeri, John Greig and Richard Hughes of Deloitte (together, the ‘Administrators’), in their capacity as administrators of each of the Second Plaintiff, Virgin Australia Holdings Ltd (Administrators Appointed) (‘Virgin’), and the Third to Thirty-Ninth Plaintiffs and the prospective Fortieth Plaintiff, which are various subsidiaries of Virgin (together, the ‘Virgin Subsidiaries’), sought various orders in the Interlocutory Application filed on 11 May 2020. Virgin and the Virgin Subsidiaries are, together, referred to as the ‘Virgin Companies’. Each of the Virgin Companies is a company incorporated and operating in Australia. Each is part of a corporate group comprised of other companies incorporated and operating in Australia, New Zealand and Singapore known as the Virgin group of companies (the ‘Virgin Group’). The Virgin Group is an Australian-based corporate group that operates in the domestic and international passenger and cargo airline business. The Virgin Group also operates the ‘Velocity Loyalty Program’. However, entities related to the Velocity Loyalty Program are not in any form of external administration. The Virgin Group offers a variety of aviation products and services to the Australian aviation market, including corporate, government, leisure, low cost, regional and charter travellers and air freight customers (collectively, the ‘Business’).

3 Virgin is a public company whose shares are listed on the Australian Securities Exchange. On 20 April 2020, the Administrators were appointed as joint and several administrators of each of Virgin and the Virgin Subsidiaries other than the prospective Fortieth Plaintiff, Tiger International No. 1 Pty Ltd (Administrators Appointed) (‘Tiger 1’). On 28 April 2020, the Administrators were appointed as joint and several administrators of Tiger 1.

4 Collectively, before the appointment of Administrators, the Virgin Group employed approximately 10,000 employees nationally and operated a fleet of 144 aircraft. The Business operates under, amongst others, the ‘Virgin’ and ‘Tiger’ brand names.

5 The application primarily seeks the following relief:

(1) in respect of Tiger 1:

(a) curative orders having regard to the fact that the notice to creditors for the first meeting of creditors held on 11 May 2020 was sent to creditors less than the five business days required by s 436E(3) of the Corporations Act 2001 (Cth) (the ‘Corporations Act’);

(b) similar administrative-type orders to those sought in the first court application in this proceeding on 24 April 2020 (the ‘Initial Application’), including to hold meetings of creditors by video-link or telephone and to send notices to creditors electronically where email addresses are available to the Administrators; and

(c) orders varying those orders the Court made on 24 April 2020 so that the existing committee of inspection also encompasses Tiger 1;

(2) orders extending the period for the convening of the second meeting of creditors of each of the Virgin Companies (the ‘Second Meeting’), for approximately three months, to 18 August 2020 (the ‘Convening Period’);

(3) orders permitting the Second Meeting to be convened at any time within the Convening Period;

(4) orders limiting the Administrators’ personal liability with respect to obligations entered into after their appointment, including with respect to:

(a) specific charter flights provided to a particular customer, Rio Tinto Services Limited (‘Rio Tinto’);

(b) future arrangements to be entered into by the Administrators in connection with the operation of the Virgin Companies’ business;

(c) the Commonwealth’s JobKeeper programme (‘JobKeeper’); and

(d) intercompany loans between various entities within the Virgin Companies;

(5) directions that the Administrators would be justified in offering a conditional credit to customers of the Virgin Companies who have been unable to take flights booked with the Virgin Companies because those flights were cancelled in response to the COVID-19 pandemic (the ‘Conditional Credits Proposal’) (and an associated limitation of the Administrators’ personal liability in connection with the Conditional Credits Proposal);

(6) orders modifying the requirement in s 438B(2) of the Corporations Act that the directors of each of the Virgin Companies provide a report as to the company’s activities and property, and instead requiring that a single report be prepared for Virgin and various of the Virgin Subsidiaries (with the directors of the other Virgin Companies preparing reports in the usual manner);

(7) orders that the members of the committee of inspection be given leave to derive a profit or advantage from the external administration of each of the Virgin Companies (so as, for example, to permit the Administrators to cause the Virgin Companies to enter into arrangements to permit ongoing trading with members of the committee during the administration period); and

(8) orders dispensing with the requirement that the Administrators open and operate a separate bank account for each of the Virgin Companies.

6 In these circumstances I make the observation that the Court should support innovative measures that are considered appropriate by the Administrators as long as the interests of the relevant creditors are taken into account. It is important that there be an efficient progression of the administration and in a timely manner as far as the circumstances permit. Obviously, the role of the airline industry in Australia as a whole, of which Virgin is a part, is important to the whole community and to the national interests generally.

7 Before turning to the background to the application the subject of these reasons, I note that on 24 April 2020, following the Initial Application, I made orders (the ‘24 April Orders’), which:

(1) provided administrative-type relief to the Plaintiffs to permit them to hold meetings of creditors by video-link or telephone, to send notices to creditors electronically where email addresses were available to the Administrators, and for the formation of a single committee of inspection for the Second to Thirty-Ninth Plaintiffs; and

(2) granted the Administrators a four-week extension of the time in s 443B of the Corporations Act for the Administrators to give notice to lessors of property leased, used or occupied by the Second to Thirty-Ninth Plaintiffs as to whether to retain or give up possession of that property (together with a corresponding extension of the period in which the Administrators were not personally liable for obligations under those leases).

8 On 29 April 2020, the Court published reasons for judgment in respect of the 24 April Orders: Strawbridge, in the matter of Virgin Australia Holdings Ltd (administrators appointed) [2020] FCA 571 (the ‘First Judgment’).

FACTUAL BACKGROUND

9 The Administrators rely upon the affidavits of:

(1) Vaughan Neil Strawbridge dated:

(a) 15 May 2020 (the ‘Fourth Strawbridge Affidavit’);

(b) 11 May 2020 (the ‘Second Strawbridge Affidavit’), as amended by affidavit dated 15 May 2020, which corrects a minor error in the Second Strawbridge Affidavit;

(c) 11 May 2020, being the further affidavit of Mr Strawbridge (the ‘Supplementary Strawbridge Affidavit’);

(d) 23 April 2020, which was relied upon in the Initial Application;

(2) Kassandra Suzann Adams dated 15 May 2020 (the ‘Adams Affidavit’); and

(3) Elizma Bolt dated 19 May 2020 (the ‘Bolt Affidavit’).

10 The following statement of the factual background to these proceedings should be read in addition to the factual background in the First Judgment.

The Virgin Companies

11 The Administrators have currently identified that the Virgin Companies have approximately 12,808 known creditors in total (other than bondholders). The creditors identified thus far comprise the following:

(1) 26 lenders under secured corporate debt and aircraft financing facilities, who are together owed approximately $2,283,639,303;

(2) unsecured noteholders who are together owed approximately $1,988,250,000;

(3) 1,070 trade creditors, who are together owed approximately $166,704,085.69;

(4) 50 aircraft lessors, who are together owed approximately $1,883,914,848;

(5) 81 landlords, who are together owed approximately $71,209,929;

(6) 9,020 employees, who are together owed approximately $450,777,961; and

(7) in addition to the unsecured noteholders in respect of notes issued by Virgin Australia, Tiger 1 has the following creditors:

(a) the Ninth Plaintiff, Tiger Airways Australia Pty Ltd (Administrators Appointed), in the amount of approximately $38.5 million;

(b) the Tenth Plaintiff Virgin Australia Airlines Pty Ltd (Administrators Appointed) (‘VAA’), in the amount of approximately $11.9 million;

(c) the Fifth Plaintiff, Virgin Australia International Airlines Pty Ltd (Administrators Appointed), in the amount of approximately $3.5 million; and

(d) the Deputy Commissioner of Taxation (the ‘ATO’), the value of whose claim is not currently known.

12 The COVID-19 pandemic has led to a substantial downturn in the operations and revenue of the Virgin Companies. Between 18 March 2020 and 5 April 2020, the Commonwealth, State and Territory Governments took various steps that placed severe restrictions on overseas and inter-state travel; and similar restrictions were adopted worldwide to reduce the spread of COVID-19. Specifically, on 18 March 2020, the National Cabinet announced that the National Security Committee of Cabinet had issued ‘Level 4’ travel restrictions, being advice to Australians in relation to overseas travel of ‘do not travel’. Then, effective from 20 March 2020, the Commonwealth Government closed Australia’s borders to all non-citizens and non-residents. Effective from various times between 20 March 2020 and 5 April 2020, the Northern Territory, Tasmanian, Western Australian, Queensland and South Australian Governments imposed further travel restrictions for interstate travellers with some of these States and Territories closing their borders to all non-essential interstate travel for non-residents.

13 These actions have resulted in a significant reduction in the demand for international and domestic air travel, which is a significant part of the business operations of the Virgin Companies. It was Mr Strawbridge’s evidence that the COVID-19 pandemic has had a considerable adverse effect on the revenues of the Virgin Companies.

14 Since their appointment, the Administrators have sought to continue to trade the Virgin Companies on a ‘business as usual’ basis, albeit that, due to the travel restrictions arising from COVID-19:

(1) the airline is not operating any international passenger routes (with the exception of limited repatriation flights to and from Hong Kong and Los Angeles) and only limited domestic passenger routes (about 128 flights per week);

(2) the business is not being operated at full capacity; and

(3) it is likely that the Virgin Companies will continue to generate losses throughout the administration period whilst these restrictions are in place.

15 As the First Judgment noted at [14], the Virgin Companies comprise a very significant enterprise with substantial operations, complex affairs, considerable assets and a very large number and type of creditors; accordingly, the administrations are likely to be sophisticated and complex.

16 The Virgin Companies are, together, a very large commercial enterprise that carries on a very substantial aviation business. The administrations of the Virgin Companies are complex, involving both the operation of the business (where possible, due to constraints occasioned by the COVID-19) and an ongoing effort to sell the business as a going concern, or recapitalise it through a proposal for a deed of company arrangement (‘DOCA’).

Progress of the administrations

17 Since the Initial Application and the 24 April Orders, the Administrators have continued to progress the administration of the Virgin Companies, which include the following:

(1) General administration tasks, including:

(a) undertaking preliminary investigations into the financial position of the Virgin Companies and forensic imaging of the Virgin Companies’ electronic records;

(b) investigating the security held in relation to the assets and property of the Virgin Companies, including a review of the financing statements lodged against the Virgin Companies on the register established and maintained under the Personal Property Securities Register (‘PPSR’) and liaising with the relevant secured parties;

(c) undertaking preliminary calculations of the secured debt position of the Virgin Companies;

(d) locating and securing owned and leased assets, assessing the condition of those assets and ensuring that those assets are appropriately insured;

(e) taking steps to resolve retention of title claims, noting that many of these claims have taken (and may continue to take) some time to be resolved;

(f) dealing with the Virgin Companies’ banks and bank accounts;

(g) facilitating the ongoing trading of the Virgin Companies and the operation of the Business (subject to the restrictions imposed by the COVID-19 pandemic);

(h) reviewing various lease documentation and liaising with landlords in relation to rent relief;

(i) holding discussions with and requesting information from various key staff members and advisers in relation to the assets, liabilities and operations of the Virgin Companies;

(j) liaising with Government bodies and Government representatives at the State and Commonwealth level in relation to the administration of the Virgin Companies;

(k) liaising with employees and union representatives in relation to the administration of the Virgin Companies;

(l) continuing the employment of staff and facilitating the payment of employee wages, including assisting the Virgin Companies with accessing JobKeeper;

(m) undertaking calculations of employee entitlements;

(n) liaising with certain shareholders of the Virgin Companies in relation to the administration of the Virgin Companies;

(o) considering the books and records of the Virgin Companies to identify secured and unsecured creditors of the Companies;

(p) liaising with a large number of secured and unsecured creditors and various other stakeholders of the Virgin Companies in relation to the administration of the Virgin Companies;

(q) establishing, monitoring and managing six separate email addresses to deal with enquiries and correspondence in relation to the administration for:

(i) general enquiries: virginadmin@deloitte.com.au;

(ii) trade creditors and suppliers: virginsuppliers@deloitte.com.au;

(iii) employees: virginemployees@deloitte.com.au;

(iv) customer queries: virgincustomers@deloitte.com.au;

(v) aircraft lessors: virginaircraftlessor@deloitte.com.au; and

(vi) secured lenders: virginsecuredlenders@deloitte.com.au,

and together, these email addresses have received approximately 4,900 emails from creditors and other stakeholders of the Virgin Companies;

(r) establishing and maintaining a database to record the various creditor claims and assist with ongoing management of creditor claims; and

(s) conducting meetings with directors, senior management and staff of the Virgin Companies;

(2) tasks relevant to the Administrators’ statutory obligations, including:

(a) filing of requisite notices with ASIC in respect of the appointment of the Administrators, and the convening of the first meeting of creditors of the Second to Thirty-Ninth Plaintiffs on 30 April 2020 (the ‘First Meeting’) and the first meeting of creditors of Tiger 1 on 11 May 2020 (the ‘Tiger 1 First Meeting’);

(b) issuing the requisite statutory notices to creditors of the Virgin Companies; and

(c) notifying the ATO of the appointment of the Administrators;

(3) tasks relevant to the First Meeting, including:

(a) preparing the requisite notices and the circular to creditors;

(b) making an application to the Court for various orders including to permit the First Meeting to be held by electronic means;

(c) arranging for the use of a Microsoft Teams Live Event to be used to host the meeting;

(d) preparing for and attending the First Meeting;

(e) collecting and adjudicating proofs of debt and proxies lodged by secured and unsecured creditors before the First Meeting;

(f) conducting the First Meeting;

(g) preparing the minutes of the First Meeting; and

(h) preparing and issuing the proposal to creditors for their ratification of the

(i) proposed members of the committee of inspection selected by the Administrators;

(4) an application to the Court for orders with respect to, amongst other things, providing electronic notices to creditors and an extension of time to consider the position of leases entered into by the Virgin Companies;

(5) tasks relating to a process for a sale of the Business in respect of the Virgin Companies, including:

(a) commencing a short competitive process in respect of the recapitalisation of the Business and/or acquisition of the assets of the Virgin Companies including the entering into of non-disclosure agreements following receipt of expressions of interest (the ‘Sale Process’);

(b) engaging advisers Houlihan Lokey and Morgan Stanley to progress the Sale Process;

(c) instructing Houlihan Lokey to:

(i) issue a flyer (‘Flyer’) and non-disclosure agreement to interested parties on and from 21 April 2020 seeking binding offers to recapitalise or acquire the assets of Virgin Australia;

(ii) prepare an information memorandum and establish a secure data room containing documents regarding the Business and the financial position of the Virgin Companies (the ‘Data Room’); and

(iii) contact all known interested parties and potential buyers; and

(d) liaising with Houlihan Lokey and Morgan Stanley on the commencement of discussions with a number of interested parties.

18 On 30 April 2020, the Administrators held the First Meeting.

19 In accordance with the 24 April Orders, the First Meeting was held on 30 April 2020 at 11:30am via a Microsoft Teams Live Event.

20 Before the First Meeting, creditors and observers were required to pre-register through an online form hosted by Microsoft and were permitted to submit questions prior to the meeting.

21 At the First Meeting:

(1) there were approximately 898 creditors and 661 observers in attendance;

(2) creditors could submit questions via the live question and answer function within the Microsoft Teams Live Events virtual platform (‘Live Q&A Function’); and

(3) 137 questions were asked through the Live Q&A Function (with any questions asked in the Live Q&A Function that were not answered by the Chairperson having been answered by the Administrators FAQs on their website).

22 Following the First Meeting, on 5 May 2020, a circular to creditors was issued with a proposal as to the members of the committee of inspection (the ‘Proposed Committee of Inspection’) to be formed in accordance with the 24 April Orders (the ‘COI Proposal’). In accordance with the COI Proposal, the Proposed Committee of Inspection is to comprise the following members:

(1) 4 representatives of noteholder creditors;

(2) 11 representatives of employee creditors;

(3) 1 representative of other creditors;

(4) 6 representatives of secured creditors;

(5) 1 statutory representative;

(6) 6 representatives of trade creditors; and

(7) 1 statutory observer.

23 Creditors have until 12 May 2020 to vote on the COI Proposal. As at 11 May 2020, 99.47% of 4,541 votes that have been returned thus far have voted in favour of the Proposed Committee of Inspection. Thus, it is overwhelmingly likely that the members of the Proposed Committee of Inspection will be deemed to be the members of the committee by close of business on 12 May 2020 (the ‘Committee of Inspection’).

24 On 28 April 2020, Tiger 1, which is part of the ‘International Flying Rights Group’ of the Virgin Group, went into administration. Tiger 1 is an otherwise dormant entity (in that it does not carry out any business or operations). However, it is a guarantor in respect of various USD and AUD notes issued by Virgin Australia (and therefore has a contingent liability to the noteholders). Besides the noteholders (which I referred to earlier), the only external creditor of Tiger 1 is the ATO (the value of whose debt is uncertain). Thus, the external creditors of Tiger 1 are also creditors of certain other Virgin Companies.

25 As with the First Meeting, the Tiger 1 First Meeting was successfully conducted by electronic means. I note that at the Tiger 1 First Meeting:

(1) no proposal was sought for a committee of inspection to be formed solely for Tiger 1; and

(2) there were no objections raised in relation to inadequate notice being provided to creditors.

Sales process

26 I have already mentioned the tasks the Administrators have undertaken in terms of the selling of the Business.

27 As at 11 May 2020, a total of 19 commercial parties had been granted access to the Data Room.

28 The Sale Process’ indicative timeline is as follows:

(1) the Flyer and non-disclosure agreements were provided to parties on and from 21 April 2020;

(2) on and from 27 April 2020, the information memorandum was distributed to parties that had entered into a non-disclosure agreement and the Data Room was opened;

(3) non-binding indicative offers were due to be provided on 15 May 2020;

(4) binding offers are due to be provided on 12 June 2020;

(5) a binding implementation deed is proposed to be entered into by 21 June 2020, subject to any regulatory approvals that might be required;

(6) the terms of any DOCA are to be progressed leading up to the second meeting of creditors, to be in held in early August; and

(7) if applicable, a DOCA is to be executed shortly thereafter.

29 The Administrators are focused on seeking to achieve a successful outcome from the Sale Process, as a maximisation of the price paid for the business (through a DOCA or otherwise) is likely to provide the best result for creditors of the Virgin Companies.

TIGER 1 – MEETINGS BY ELECTRONIC MEANS, NOTICE BY EMAIL AND INCORPORATION INTO COMMITTEE OF INSPECTION

30 This matter is addressed in the Interlocutory Process at prayers 2-10 (which I will deal with in greater detail below), and in the Second Strawbridge Affidavit, which provides that:

Tiger 1

25. On 28 April 2020, the Administrators were appointed as joint and several administrators of Tiger 1 by resolution of the directors of that company pursuant to section 436A of the Corporations Act.

26. Tiger 1 is a wholly owned subsidiary of the Fifth Plaintiff. …

27. At the time of swearing this affidavit, the directors of Tiger 1 have not provided to the Administrators a ROCAP for any of the Virgin Companies.

28. Tiger 1 is part of the 'International Flying Rights Group' as described in paragraph 14 of my First Affidavit. While Tiger 1 is an otherwise dormant entity in the Virgin Group (in that it does not carry out any business or operations), it is a guarantor in respect of various USD and AUD notes issued by Virgin Australia. For that reason, the directors of Tiger 1 resolved to appoint administrators on the basis that it was insolvent or likely to become insolvent.

29. The Administrators understand that in addition to the noteholders (who are the creditors I referred to as unsecured bondholders in my First Affidavit) in respect of notes issued by Virgin Australia, Tiger 1 has the following creditors:

(a) the Ninth Plaintiff, Tiger Airways Australia Pty Ltd (Administrators Appointed), in the amount of approximately $38.5 million;

(b) the Tenth Plaintiff Virgin Australia Airlines Pty Ltd (Administrators Appointed) (VAA), in the amount of approximately $11.9 million;

(c) the Fifth Plaintiff, Virgin Australia International Airlines Pty Ltd (Administrators Appointed), in the amount of approximately $3.5 million; and

(d) the Deputy Commissioner of Taxation (ATO), the value of whose claim is not currently known.

30. On 30 April 2020, the Administrators published a combined notice of appointment and first meeting of creditors (Tiger 1 First Meeting) in respect of Tiger 1 (Tiger 1 Notice of Meeting) on the ASIC Insolvency Notices website … . The Tiger 1 Notice of Meeting provides details for the Tiger 1 First Meeting, which is scheduled to be held (at Deloitte’s offices) on 11 May 2020 at 2:00pm but with creditors being permitted to attend by electronic means only.

31. On 1 May 2020, the Administrators sent an initial notice of appointment and first meeting of creditors in respect of Tiger 1 dated 1 May 2020 to the ATO (Initial Tiger 1 Notice).

32. On 7 May 2020, the Initial Tiger 1 Notice was sent to each note trustee in relation to notes issued by Virgin Australia, being:

(a) Bank of New York Mellon at jeremy.hollingsworth@bnymellon.com;

(b) Sargon CT Pty Ltd at yvonne.kelaher@sargon.com;

(c) Computershare at wayne.hopkins@computershare.com.au; and

(d) DF King at mzheng@dfking.com,

(Note Trustees). …

33. The noteholders are contingent creditors as a result of guarantees provided by Tiger 1 in respect of the USD and AUD notes issued by Virgin Australia. The Administrators were delayed in providing the Initial Tiger 1 Notice to the Note Trustees as the Administrators were still ascertaining the nature of the claims that the noteholders had against the Virgin Companies (including ascertaining their status as contingent creditors).

34. Each of the noteholders, via the Note Trustees, was also provided with information about the affairs of the Virgin Companies and the impact of the administration of the Virgin Companies in the details provided in advance of, or at, the First Meeting. This information included that set out in:

(a) the Notice of Appointment and First Meeting of Creditors sent to the noteholders on or about 21 or 22 April 2020, … ; and

(b) Circular to Creditors dated 27 April 2020, sent to noteholders on the same date, … .

35. In addition, after the First Meeting, each of the noteholders was issued:

(a) the circular to creditors dated 5 May 2020 (sent to noteholders on the same date), as I referred to above, which included information on the proposed Committee of Inspection; and

(b) a notice to Virgin Australia’s noteholders dated 6 May 2020 (sent to noteholders on the same date), which contained information about the appointment of a Special Noteholder Liaison Counsel, … .

Attendance at Tiger 1 First Meeting

36. I refer to paragraphs 16-26 and 41-43 of the First Affidavit and paragraph 18 above. In light of those matters, in the opinion of the Administrators there was no practical impediment to holding the Tiger 1 First Meeting by electronic means only (other than conducting a poll of creditors).

37. I am aware that Mr Anthony Lowe, Director, Deloitte chaired the Tiger 1 First Meeting. I am informed by Mr Lowe and believe to be true that there were no technical issues with holding the first meeting electronically.

38. At the Tiger 1 First Meeting:

(a) there was no proposal for an alternative person or persons to be appointed as administrators and, accordingly, the appointment of the Administrators continues for Tiger 1;

(b) as set out below, no proposal was sought for a committee of inspection to be formed solely for Tiger 1; and

(c) there were no objections raised in relation to inadequate notice being provided to creditors.

Provision of electronic notices to creditors

39. I refer to paragraphs 56-61 of the First Affidavit. For the same reasons set out in those paragraphs, the Administrators consider that it is in the best interests of the creditors of Tiger 1 for the Administrators to be permitted to send notices by email to those creditors for whom an email address has been provided.

Committee of Inspection

40. As set out above, a single Committee of Inspection has been formed for the Second to Thirty-Ninth Plaintiffs.

41. At the Tiger 1 First Meeting, the Administrators informed the meeting that the Administrators did not propose to provide the creditors with an option to propose and vote on a resolution that a committee of inspection for Tiger 1 be formed. No objections were raised by any creditors at the meeting on this issue and no creditor sought to propose a resolution that a committee of inspection be formed solely for Tiger 1. Instead, the Administrators seek orders:

(a) that Tiger 1 form part of the entities to which the existing Committee of Inspection has been formed in respect of the Second to Thirty Ninth Plaintiffs; and

(b) confirming that the members of the Committee of Inspection be those selected by the Administrators and voted for by creditors in accordance with the COI Proposal as set out in paragraphs 20 to 22 above.

42. In the opinion of the Administrators, and based on our experience as insolvency practitioners, an order of this type will enable the Administrators to streamline the administrations rather than having separate committees of inspection. It will save costs in the administration by reducing the need to run duplicative processes (which I consider to be in the best interests of the creditors of the Virgin Companies as a whole).

43. Also, as detailed in paragraph 29 above, the only creditors of Tiger 1 (other than creditors within the Virgin Group) are also creditors of Virgin Australia in any event. Accordingly, the Administrators do not consider that there will be any prejudice to the creditors of Tiger 1 in the making of this order, as the Committee of Inspection proposed to include four members representative of the noteholders creditors.

31 As set out above, Tiger 1 appointed the Administrators as joint and several administrators to that entity on 28 April 2020. Accordingly, the Initial Application did not address Tiger 1 and the 24 April Orders do not presently apply to Tiger 1.

Joinder

32 The Administrators seek an order pursuant to r 9.05 of the Federal Court Rules 2011 (Cth) (the ‘Rules’) that Tiger 1 be added to this proceeding as Fortieth Plaintiff.

33 Rule 9.05(1)(b)(iii) of the Rules (which applies by reason of r 1.3(2)(a) of the Federal Court (Corporations) Rules 2000 (Cth)), permits the Court to join a person to existing proceedings if the person proposed to be joined ‘should be joined as a party in order to enable determination of a related dispute and, as a result, avoid multiplicity of proceedings’.

34 Tiger 1 should be joined to these proceedings as it is part of the group of Virgin Companies now in external administration and common issues have and will continue to arise in the course of the various administrations.

Curing insufficient notice of first meeting

35 The Administrators seek an order pursuant to s 1322(4)(a) of the Corporations Act that the convening and holding of the Tiger 1 First Meeting in accordance with s 436E of the Corporations Act, pursuant to the notice sent to creditors in accordance with rr 75-225(1) and 75-15 of the Insolvency Practice Rules (Corporations) 2016 (Cth) (the ‘IPR’), is not invalidated by reason of the notice having been issued on 7 May 2020 (resulting in less than five business days’ notice of the meeting being given to the creditors of Tiger 1).

36 The Tiger 1 First Meeting was convened on 30 April 2020 and was held on 11 May 2020.

37 Notice of the Tiger 1 First Meeting was given to the ATO (on behalf of the Deputy Commissioner of Taxation) on 30 April 2020. However, notice to the noteholders was not given until 7 May 2020, which is less than the five business days required by s 436E(3) of the Corporations Act.

38 Section 1322(4) of the Corporations Act is a remedial provision that is able to be used to cure a notice period that is less than that prescribed by the statute. The powers under that section are to be exercised liberally, so as not unreasonably to stifle corporate and financial activity merely on technical grounds: Winpar Holdings Ltd v Goldfields Kalgoorlie Ltd [2001] NSWCA 427 at [74]; Re Insurance Australia Group Ltd (2003) 128 FCR 581 at [27]; Re Wave Capital Ltd [2003] FCA 969 at [30].

39 Subject to the requirements of s 1322(6), the section confers an unfettered discretion on the Court: In the matter of National Roads and Motorists’ Association Ltd [2003] FCAFC 206 at [21]. Orders can be made under the section:

(1) with retrospective effect: Re Wood Parsons Pty Ltd (in liq) [2002] NSWSC 1058 at [52]; In the matter of Golden Gate Petroleum Ltd [2010] FCA 40 at [42]; and

(2) where there is a real question as to whether a contravention of a provision would even lead to invalidity, so as to avoid any uncertainty with respect to the matter: In the matter of Milgerd Nominees Pty Ltd [2019] NSWSC 311 at [13].

40 In the present case, s 1322(4)(a) may be used to confirm that the holding of (and passage of resolutions at) the Tiger 1 First Meeting is not invalidated by the notice of the meeting being provided to creditors being less than the prescribed statutory period.

41 As I noted earlier, Mr Strawbridge’s evidence is that Tiger 1 does not trade or carry out any business, but was placed into administration because it is a guarantor of the notes issued by Virgin Australia to the noteholders. Consequently, its creditors were already provided with details as to the administrations generally when the notice of the First Meeting was issued and sent to creditors. Those creditors of Tiger 1 were also able to attend the First Meeting on 30 April 2020.

42 Further, at the Tiger 1 First Meeting, no creditor raised any issue as to the inadequacy of any notice of the meeting.

43 In the circumstances, the order sought by the Administrators is appropriate and the requirements of s 1322(6) are satisfied.

Holding meetings by electronic means

44 The Administrators seek:

(1) An order pursuant to s 447A(1) of the Corporations Act and s 90-15 of the Insolvency Practice Schedule (Corporations) 2016, which is Sch 2 to the Corporations Act (the ‘IPSC’), that, to the extent not permitted specifically by rr 75-30, 75-35 and 75-75 of the IPR and the Corporations (Coronavirus Economic Response) Determination (No. 1) 2020 (Cth) (the ‘Determination’), the Administrators be permitted to hold meetings of creditors during the administration of Tiger 1 by telephone or audio-visual conference only at the place of the Administrators’ offices (without creditors of Tiger 1 being able to attend physically at that place), with such details of the arrangements for using the telephone or audio-visual conference facilities to be specified in each of the notices issued to creditors.

(2) An order pursuant to s 447A(1) of the Corporations Act and s 90-15 of the IPSC, that, to the extent not permitted specifically by r 75-35(2)(b) of the IPR and the Determination, the creditors of Tiger 1 who wish to participate at any meeting of Tiger 1 by telephone or audio-visual conference only at the place of the Administrators’ offices (without creditors of Tiger 1 being able to attend physically at that place), must lodge with the Administrators, no later than the second last business day before the day on which the meeting is held, specific proxy forms containing the information in r 75-35(2)(b)(i)-(iii) of the IPR (with liberty to notify the Administrators of the withdrawal of that specific proxy and amended vote following any discussion at a meeting, in advance of a resolution being passed).

45 In the First Judgment at [25] I said that there was no practical impediment to meetings of creditors being held by electronic means and it is appropriate (if not necessary) that this occur. I see no reason why the same observation should not apply with equal force to meetings of creditors of Tiger 1.

46 In addition, it was Mr Strawbridge’s evidence (which I referred to earlier), that the First Meeting was conducted successfully using electronic technology with creditors attending the meeting and participating without being physically present in the same location as the Administrators or one another.

47 For those reasons, the Administrators seek orders for Tiger 1 to the following effect, and in the same form as those made in the 24 April Orders with respect to the other Virgin Companies:

(1) confirming that the meetings of creditors of Tiger 1 (including the Tiger 1 First Meeting) may be held exclusively by electronic means; and

(2) requiring that, in respect of any creditor who wishes to participate in, and vote on, resolutions that are put to creditors at a meeting (to the extent that this may occur at meetings subsequent to the Tiger 1 First Meeting), special proxies must be provided to the Administrators no later than the second last business day before the meeting is held (although giving liberty to any creditor providing such a proxy to withdraw those voting instructions in advance of the resolution being passed).

48 It is appropriate to make those orders.

Electronic notice to creditors

49 The Administrators seek:

(1) An order pursuant to s 447A(1) of the Corporations Act and s 90-15 of the IPSC, that Pt 5.3A of the Corporations Act is to operate, nunc pro tunc, in relation to Tiger 1, as if any notice (‘Notice’) required to be given pursuant to rr 75-225(1) and 75-15 of the IPR will have been validly given to creditors of Tiger 1 by reason of the following steps having been taken before the date of the meeting:

(a) where the Administrators:

(i) have an email address for a creditor, by sending the Notice by email to each such creditor;

(ii) where the Administrators do not have an email address for a creditor, but have a postal address for the creditor (or have received notification of non-delivery of a notice sent by email in accordance with (a)(i) above), by sending the Notice by posting a copy of it to the postal address for each such creditor;

(b) by causing the Notice to be published on the Australian Securities and Investments Commission (‘ASIC’) published notices website at https://insolvencynotices.asic.gov.au/; and

(c) by publishing the Notice on the website maintained by the Administrators at https://www2.deloitte.com/au/en/pages/finance/articles/virgin-australia-holdings-limited-subsidiaries.html.

50 In the First Judgment, I observed at [27]-[29], by reference to the relevant authorities, that it is now commonplace for orders to be made, including at an early point in an administration, permitting external administrators to give notices to creditors by email and other electronic publication.

51 Because each of the noteholders is a creditor of Tiger 1, there are also a substantial number of creditors of that entity. In my view, as with the other Virgin Companies, notice to be given to creditors of Tiger 1 by email and publication on Deloitte’s website fulfils the objective of notifying as many creditors as quickly and cheaply as possible.

52 Accordingly, I will make orders permitting electronic notices to be given to creditors of Tiger 1 on a similar basis to the 24 April Orders with respect to the other Virgin Companies.

Incorporation into existing Committee of Inspection

53 The Administrators seek:

(1) An order pursuant to s 447A(1) of the Corporations Act and s 90-15 of the IPSC, that Divs 75 and 80 of the IPSC, and Div 75 of the IPR, are to operate as if the requirement in ss 80-10 and 80-15 of the IPSC for the creditors of a company to resolve that a committee of inspection be formed and to appoint members of the committee of inspection, be dispensed with.

(2) An order that Order 6(b) of the orders made on 24 April 2020 be varied by deleting the words ‘Thirty-Ninth Plaintiffs’ and replacing them with the words ‘Fortieth Plaintiffs’, such that that order reads:

… a single committee of inspection be formed in respect of the Second to Fortieth Plaintiffs.

(3) An order pursuant to s 447A(1) of the Corporations Act and s 90-15 of the IPSC that the Administrators are not required to issue any further Proposal (as that term is defined in Order 6(d) of the orders made on 24 April 2020) to the creditors of the Second to Fortieth Plaintiffs.

54 In Order 6(b) of the 24 April Orders, I ordered that there was to be a single committee of inspection for the Second to Thirty-Ninth Plaintiffs. At that time, Tiger 1 had yet to appoint administrators.

55 In the First Reasons, at [34(1)] and [38(1)], I accepted Mr Strawbridge’s evidence that, for administrations as large-scale and complex as those of the Virgin Companies, it would be appropriate and prudent for a committee of inspection to be formed and the Court concluded that it was in the best interests of creditors that a single committee be formed.

56 At the Tiger 1 First Meeting, the Administrators did not provide the creditors with an option to propose and vote on a resolution that a committee of inspection for Tiger 1 be formed; nor did any creditor at the Tiger 1 First Meeting request that a committee be formed.

57 Given that the external creditors of Tiger 1 are also creditors of other Virgin Companies, I accept the submissions of the Administrators that there is no reason for a separate committee of inspection to be formed. There will not be any prejudice to the creditors of Tiger 1 in the making of this order, as the Committee of Inspection is proposed to include four members representative of the noteholder creditors.

58 I accept the Administrators’ view that having the existing Committee of Inspection operate to include all of the Virgin Companies (that is, including Tiger 1) will streamline the administrations and save costs by reducing the need to run duplicative processes, which Mr Strawbridge considers to be in the best interests of the creditors of the Virgin Companies as a whole. In the circumstances, to achieve this result, I will vary Order 6(b) of the 24 April Orders to include Tiger 1.

59 Finally, in circumstances where:

(1) the COI Proposal has been issued to creditors;

(2) the creditors have had an opportunity to vote on the identity of members who are proposed to be on the Committee of Inspection;

(3) the proposed members come from a cross-section of the different categories of creditors of the Virgin Companies, including noteholders; and

(4) the votes on the COI Proposal are overwhelmingly in favour;

the Court will make an additional order confirming that no further proposal needs to be issued to creditors and that the members of the Committee of Inspection are those selected by the process set out in Orders 6(c)-(e) of the 24 April Orders.

EXTENSION OF THE CONVENING PERIOD

60 The Administrators seek:

(1) An order pursuant to s 439A(6) of the Corporations Act that the convening period defined in s 439A(5)(b) of the Corporations Act in respect of each of the Virgin Companies, be extended until 18 August 2020.

(2) An order, pursuant to s 447A(1) of the Corporations Act, that Pt 5.3A of the Corporations Act is to operate in relation to each of the Virgin Companies such that, notwithstanding s 439A(2) of the Corporations Act, the second meeting of the creditors of each of the Virgin Companies required under s 439A of the Corporations Act may be convened at any time before, or within, five business days after, the end of the convening period as extended by the order sought under (1) (provided that the Administrators give notice of the meetings to eligible creditors of each of the Virgin Companies (including the persons claiming to be creditors of the Virgin Companies) at least five business days before the meeting).

61 This matter is addressed in the Second Strawbridge Affidavit at [50]-[74], which provides that:

Background

50. Unless extended, the convening period for the second meeting of creditors of each of the Virgin Companies (other than Tiger 1) pursuant to section 439A(5) of the Corporations Act (Second Meetings) will end on 18 May 2020, requiring the Second Meetings to be held on or before 25 May 2020. In the case of Tiger 1, the convening period for the second meeting of creditors will end on 26 May 2020, requiring the meeting to be held on or before 2 June 2020. I refer to the convening period for the second meeting of creditors of each of the Virgin Companies as the Convening Period.

51. The administrations of the Virgin Companies are complex and the Administrators have received a number of expressions of interest in relation to the assets and business of the Virgin Companies. It is the current view of the Administrators that the continued trading of the Virgin Companies' business as a going concern during the administration period with a view to a sale of the business and assets of companies or the entering into of a DOCA maximises the chances of the Business continuing in existence or may result in a better return to creditors than an immediate winding up. On this basis, the Administrators believe that it is in the best interests of the Virgin Companies’ creditors that the Convening Period be extended for about 3 months, until 18 August 2020 noting that the Administrators will likely wish to convene the Second Meetings at the first opportunity following any sale of Business or the proposal for entry into a DOCA.

Creditors

52. I refer to paragraphs 65 and 66 of the First Affidavit.

53. As at 21 April 2020, searches of the PPSR disclosed that 3,463 registrations had been made against assets or property of the Virgin Companies (in total) on the PPSR. Given the number of registrations on the PPSR, the Administrators are continuing to review all available information in relation to the claims of the apparent secured creditors with security interests over the assets or property of the Virgin Companies registered on the PPSR.