FEDERAL COURT OF AUSTRALIA

Avita Medical Limited, in the matter of Avita Medical Limited (No 2) [2020] FCA 674

ORDERS

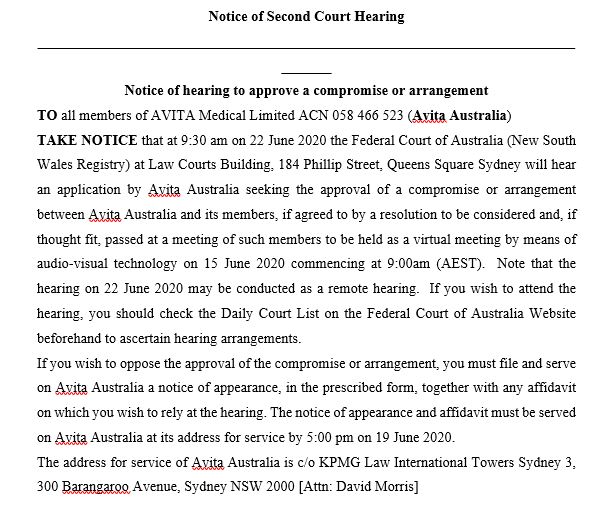

IN THE MATTER OF AVITA MEDICAL LIMITED ACN: 058 466 523 | ||

Plaintiff | ||

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 411(1) of the Corporations Act 2001 (Cth) (Act), the plaintiff convene and hold a meeting (Scheme Meeting) of the holders of ordinary shares in the plaintiff (Scheme Shareholders):

(a) to consider, and, if thought fit, to approve (with or without modification) the scheme of arrangement (Scheme) proposed to be made between the plaintiff and its shareholders, the terms of which are as set out in Annexure DM-7 to the Affidavit of David Morris affirmed 6 May 2020;

(b) to be held as a wholly virtual meeting by means of audio-visual technology, with no physical assembly, and otherwise in accordance with the orders of the Court made on 30 April 2020; and

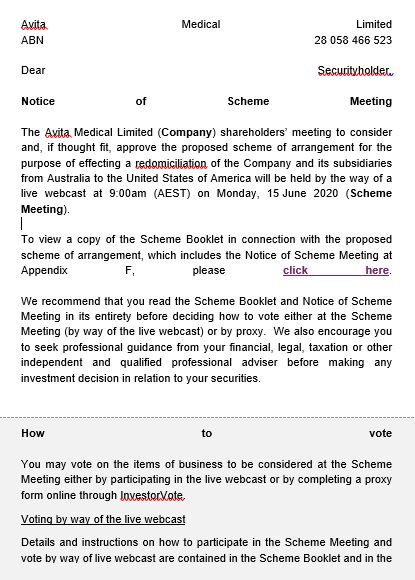

(c) to be held on 15 June 2020 commencing at 9:00am (AEST).

2. The scheme booklet, substantially in the form of Exhibit 2 (as amended by Exhibit 3), which comprises the explanatory statement as required by s 412(1)(a) of the Act, be and is hereby approved (subject to any minor amendments required by the Court or required and approved by ASIC for the purposes of registration thereof under s 412(6) of the Act).

3. The Scheme Meeting be convened by sending on or before 14 May 2020:

(a) in the case of Scheme Shareholders who have elected to receive shareholder communications electronically by way of email (Email Shareholders), an email substantially in the form contained at Annexure A to these orders which contains links to:

(i) a document substantially in the form of the scheme booklet (which contains, among other things, the Notice of Scheme Meeting at Appendix F to the scheme booklet); and

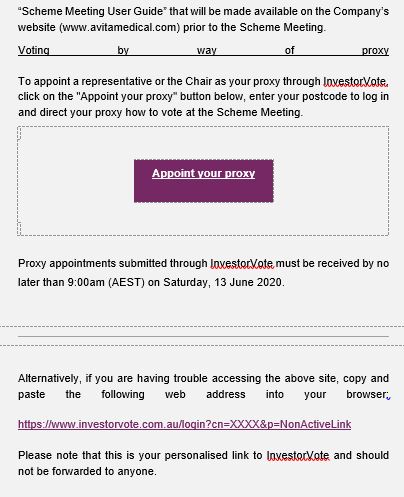

(ii) a personalised proxy form for the Scheme Meeting substantially in the form contained at Annexure “DM-9” to the third affidavit of David Morris sworn on 6 May 2020 (Proxy Form);

(b) in the case of Scheme Shareholders who are not Email Shareholders and whose registered address is in Australia, the following documents by pre-paid post addressed to the relevant addresses recorded in the plaintiff’s register:

(i) a document substantially in the form of the scheme booklet (which contains, among other things, the Notice of Scheme Meeting at Appendix F);

(ii) a personalised Proxy Form; and

(iii) a reply-paid envelope for the return of the Proxy Form; and

(c) in the case of Scheme Shareholders, other than Email Shareholders, whose registered address is outside Australia, the following documents by airmail or international courier service addressed to the relevant addresses recorded in the plaintiff’s register:

(i) a document substantially in the form of the scheme booklet (which contains, among other things, the Notice of Scheme Meeting at Appendix F);

(ii) a personalised Proxy Form; and

(iii) a return envelope for the return of the Proxy Form.

4. Subject to these Orders, the Scheme Meeting be convened, held, and conducted in accordance with the provisions of Pt 2G.2 of the Act (save for any applicable replaceable rule) that apply to a meeting of the plaintiff’s members.

5. Voting on the resolution to approve the Scheme is to be conducted by way of a poll.

6. A Proxy Form in respect of the Scheme Meeting will be valid and effective if, and only if, it is completed and delivered in accordance with its terms by 9.00 am (AEST) on 13 June 2020.

7. Mr Lou Panaccio, or failing him, Ms Suzanne Crowe, be Chair of the Scheme Meeting.

8. The Chair of the Scheme Meeting shall have the power to adjourn the meeting to such time, date and place as he or she considers appropriate.

9. Compliance with r 2.15 of the Federal Court (Corporations) Rules 2000 (Cth) (Rules) is dispensed with.

10. Compliance with r 3.4 and Form 6 of the Rules is dispensed with.

11. The plaintiff publish in The Australian newspaper once on or before 12 June 2020 an advertisement substantially in the form of Annexure B to these orders.

12. The further hearing of the originating process is adjourned to a hearing before Jagot J on 22 June 2020 at 9:30am (AEST).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

JAGOT J:

Background

1 As set out in the written submissions for the plaintiff, the plaintiff company, Avita Medical Limited (Avita Australia), entered into a scheme implementation agreement with Avita Therapeutics Inc, a company incorporated in the United States (Avita US), for the purpose of proposing a scheme of arrangement under Pt 5.1 of the Corporations Act 2001 (Cth) (the Act), by which Avita US will acquire all of the issued shares of Avita Australia in consideration for the shareholders of Avita Australia being provided with securities in Avita US (Proposed Scheme).

2 The Proposed Scheme was announced to ASX Limited on 20 April 2020.

3 By its originating process filed on 24 April 2020 Avita Australia seeks orders pursuant to s 411(1) of the Act to convene a meeting of its holders of ordinary shares (Scheme Shareholders) for the purpose of considering, and if thought fit, approving, the Proposed Scheme, and to approve the explanatory statement which is to accompany notice of the meeting (Scheme Booklet).

4 A useful description of the Proposed Scheme is set out in [10] of the affidavit of David Morris dated 24 April 2020, which describes that:

10. Under and in connection with the [Proposed Scheme]:

a. …[Avita US], a company incorporated in Delaware in the United States, which currently has no shares on issue, will acquire all of the shares in Avita Australia and become the new holding company of Avita Australia and the rest of [Avita Australia and its subsidiaries];

b. In consideration for this acquisition, shareholders in Avita Australia (other than the ADS Depositary) will exchange their shares in Avita Australia for CHESS Depository Interests (CDIs) in Avita US, which will be quoted for trading on the ASX market (which will be the secondary market for Avita US securities);

c. the ADS Depository will exchange its shares in Avita Australia for shares of common stock in Avita US, which will be quoted for trading on NASDAQ (which will be the primary market for Avita US securities);

d. some shareholders in Avita Australia will not be issued CDIs or shares of common stock in Avita US due to the legal or practical difficulties associated with offering CDIs or shares of common stock of Avita US into the jurisdictions in which they reside;

e. the ADS Depository will subsequently distribute the Avita US shares that it receives under the [Proposed] Scheme proportionally to the holders of the Avita Australia ADSs and the depositary instrument will be terminated; and

f. in consequence of becoming a wholly owned subsidiary of Avita US, Avita Australia will cease to be listed on the ASX and NASDAQ, and will subsequently be converted into an Australian proprietary company limited by shares.

5 The justification for the Proposed Scheme, which involves redomiciling the Avita Group to the United States, is set out in [9] and [10] of the affidavit of David McIntyre dated 6 May 2020 which state as follows:

9. First, by redomiciling the Avita Group to the United States, the Avita Group will better align its corporate structure with its operating structure. ln this regard I note that:

(a) nearly all of the Avita Group employees are located in the United States;

(b) the United States is Avita Australia’s largest market for its products, and Avita Australia derives nearly all of its revenue (over 90%) from the United States;

(c) there is the possibility of enhanced access to larger pools of capital that are available in the United States; and

(d) a majority of Avita Australia’s shares on issue (taking into account the American Depositary Shares (ADSs) that are deposited with The Bank of New York Mellon as ADS Depositary) are currently beneficially held by investors in the United States.

10. Secondly, since 31 December 2019 Avita Australia has been classified in the United States as a domestic public company for financial reporting purposes, whereas prior to this time it was only classified as such in Australia. From 1 July 2020, this will lead to increased risk, burden, resourcing and resultant costs associated with dual financial reporting and related compliance obligations in both the United States and Australia. By redomiciling the Avita Group to the United States, the Avita Group will substantially reduce its financial reporting and related compliance obligations and avoid significant costs in doing so.

Principles

First hearing matters

6 The written submissions and oral submissions for the plaintiff have identified the relevant issues. As set out in [48] of the written submissions for the plaintiff, there are six established matters that are generally required to be proven at the first hearing of a scheme of arrangement under s 411 of the Act: In the matter of OPUS Group Limited [2018] FCA 959 (OPUS Group) at [13]. The six matters are as follows:

(1) the plaintiff is a Pt 5.1 body;

(2) the proposed scheme is an “arrangement” within the meaning of s 411 of the Act;

(3) the explanatory statement will provide proper disclosure to members;

(4) the scheme is bona fide and properly proposed;

(5) the Australian Securities and Investments Commission (ASIC) has had a reasonable opportunity to examine the proposed scheme and the explanatory statement, has had a reasonable opportunity to make submissions and has had 14 [days’] notice of the hearing date of the first Court hearing; and

(6) any other procedural requirements have been met.

7 With respect to each of those criteria, I accept the submissions for Avita Australia as follows:

(1) The plaintiff is a Pt 5.1 body.

The evidence shows that Avita Australia is a company registered under the Act and is, therefore, a Pt 5.1 body within paragraph (a) of the definition of that expression in s 9 of the Act.

(2) The proposed scheme is an “arrangement” within the meaning of s 411.

As noted, the proposed scheme involves a redomiciliation of Avita Australia, and in this regard it constitutes an arrangement between Avita Australia and its members. In OPUS Group, Banks-Smith J observed that the Court had “approved schemes of arrangement used to effect a redomiciliation in a number of cases” (at [8]), and said at [7]:

Redomiciliation schemes may be used for a variety of reasons. It is not unusual for them to be used to allow a corporate group to seek a regime in another jurisdiction that may be more favourable to the nature of its business, or more conducive to raising equity capital.

(3) The explanatory statement will provide proper disclosure to members.

The evidence in this case includes evidence in respect of the due diligence and verification process which has been undertaken regarding the information contained in the Scheme Booklet. I have also been taken in detail to a letter from ASIC and the response to that letter, which resulted in some amendments to the Scheme Booklet after lodgement with ASIC. I am satisfied that the response from Avita Australia to ASIC adequately addressed all of the issues raised with ASIC, and also note that ASIC has provided its usual letter in relation to a first scheme hearing. I am satisfied that there is evidence that the Scheme Booklet will provide proper disclosure to the Scheme Shareholders.

(4) The scheme is bona fide and properly proposed.

As noted above, the reasons for the proposed redomiciliation scheme are provided in [9] and [10] of the affidavit of David McIntyre. The board of directors of Avita Australia has also unanimously resolved to recommend the Proposed Scheme and considers that it is in the best interest of shareholders. This evidence satisfies me that the Proposed Scheme is bona fide and has been properly proposed.

(5) ASIC has had a reasonable opportunity to examine the proposed scheme and the explanatory statement, and has had a reasonable opportunity to make submissions and has had 14 days’ notice of the hearing date of the first Court hearing.

The evidence that has been read and tendered satisfies all of these requirements.

(6) Any other procedural requirements have been met.

As set out in the written submissions for the plaintiff, the procedural requirements, including for the nomination of a chairperson and alternate chairperson, have been met.

8 The approach taken to a first court hearing under s 411 (1) of the Act for orders convening a meeting of shareholders to vote on the scheme, and approval of the distribution of the Scheme Booklet, are well-established.

9 In short, the court does not consider the business or commercial efficacy of the scheme of arrangement at the first stage and does not substitute its commercial judgment for that of the members. The role of the court is supervisory to the effect that the court must consider whether the scheme is “not inappropriate and is one that sensible businesspeople might consider to be of benefit to its members”: OPUS Group at [14].

Further issues

10 In the present case my attention has been drawn to a number of issues, only two of which require any further comment.

11 The first is the letter that was sent by ASIC relating to the disclosure in the Scheme Booklet. As I have said, I have also been taken to a detailed response from Avita Australia in relation to that matter, and am satisfied that the company has adequately dealt with all of ASIC’s concerns in an appropriate manner.

12 The second relates to various options also inclusive of warrants and restricted security units (RSUs). In the written submissions for the plaintiff, reference is made to the decision In the matter of Coventry Resources Limited [2012] FCA 1252 (Coventry Resources) at [18], where it was held that “[option holders] have generally been considered to be contingent creditors and that a scheme of arrangement that involves an adjustment of the rights of option holders, such as existing options being cancelled or new options being acquired, will require a separate creditor scheme of arrangement to adjust the option holders’ rights, in addition to a scheme for the members.

13 As set out in the written submissions for the plaintiff, however, Coventry Resources is premised on there being some adjustment to the rights of option holders. In the present case, the plaintiff is not asking the Court to approve an arrangement that will result in an adjustment of the rights of option holders. The holders of unlisted options, warrants and RSUs have no entitlement to attend the meeting to consider the Proposed Scheme on the basis of the securities. Rather, they have a prospective right to shares subject to satisfaction of the conditions of vesting and exercise attaching to their securities. The written submissions for the plaintiff also note that an issue which might arise for consideration is whether members who hold ordinary stock and who also hold additional unlisted options, warrants or RSUs should constitute a separate class from members who do not hold these securities. I accept the submissions for the plaintiff that these shareholders will not require voting in any separate class.

14 The principles applicable to the constitution of classes in the context of a scheme of arrangement have been outlined in In the matter of URB Investments Limited [2019] FCA 1977 at [44] to [48]. Reference is there made at [45] to the decision in Sovereign Life Assurance Company v Dodd [1892] 2QB 573 at 583, where Bowen LJ set out the test for identifying a class for a scheme of arrangement as follows:

It seems plain that we must give such a meaning to the term ‘class’ as will prevent the section being so worked as to result in confiscation and injustice, and that it must be confined to those persons whose rights are not so dissimilar as to make it impossible for them to consult together with a view to their common interest.

15 I am satisfied that the interests of members holding the additional securities are not so different as to make it impossible for them to consult with the other members of Avita Australia for the purposes of voting on the proposed scheme, and that no separate classes are required. In this regard, I refer to In the matter of Think Childcare Limited [2019] FCA 1862 at [33] to [34], in which Markovic J dealt with certain performance rights and stated as follows:

33 The regime set out in cl 4 of the scheme implementation deed is intended to effect an amendment to the [Think Childcare Limited (TNK)] performance rights with effect from the Scheme Record Date; on vesting TNK Performance Rights Holders are issued with Stapled securities rather than unstapled TNK shares. The proposed amendment to the terms of the TNK Performance Rights Plan involves a change to the securities to be issued on vesting and exercise of the TNK performance rights (from TNK shares to Stapled securities following implementation of the Stapling Proposal). It does not concern the removal or relaxation of any vesting conditions which TNK shareholders have previously approved.

34 As submitted by TNK these circumstances do not give rise to TNK Performance Rights Holders constituting a different class of shareholder as there is no relevant distinction between the rights of Scheme Shareholders. As Finkelstein J observed in Re Opes Prime Stockbroking Ltd (No 2) [2009] FCA 813; (2009) 179 FCR 20 at [64], it is ‘the difference in rights, not interests, that are relevant to determining whether or not separate classes exist’. See too [In the matter of Hills Motorway Ltd [2002] NSWSC 897 (2002); 43 ACSR 101].

16 Further, my attention has been drawn to In the matter of Skilled Group Limited (No 1) [2015] VSC 789 (2015) 113 ASCR 525 at [82] in which Robson J said:

I am satisfied that the performance rights or options held by some employees do not give rise to a separate class of members. It is worth noting at the outset that the rights will not vest until after the meeting to approve the scheme is held. Accordingly, the issue of additional shares will not influence the voting at the meeting directly. The question is whether the rights and options themselves (and the prospect of additional shares upon their vesting) gives rise to a divergence of interests with other shareholders. I do not consider that it does. The shares to be issued if the rights or options vest are not of a different type than those of other shareholders. Moreover, it appears to me that the employees with performance rights or options are in no different position from any other employee of the company who would be impacted by the scheme’s implementation in different ways on the basis of various interests extraneous to their status as members.

17 Having regard to these matters, I am satisfied that I should accept the submissions for the plaintiff, in particular that the explanatory statement in the form of the Scheme Booklet discloses all matters material to the decision of its members whether or not to approve the Proposed Scheme, noting that the Avita Australia directors have confirmed that all statements of fact contained in the Scheme Booklet in relation to the Avita Group are true and accurate in all material respects, and are not misleading or deceptive. I refer also to the existence of the report of the independent expert, Mark Whittaker, of BDO Australia, who has reached an opinion that the advantages of the Proposed Scheme outweigh its disadvantages, and, as such, the Proposed Scheme is in the best interests of shareholders of Avita Australia as a whole in the absence of an alternative proposal, or any further information.

18 In these circumstances, I am satisfied that I should make orders for the convening of the scheme meeting as set out in the proposed orders for the plaintiff. .

I certify that the preceding eighteen (18) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Jagot. |

Dated: 18 May 2020

Annexure A

Annexure B