FEDERAL COURT OF AUSTRALIA

CellOS Software Ltd v Huber (No 2) [2020] FCA 505

ORDERS

CELLOS SOFTWARE LTD ACN 114 670 094 Applicant | ||

AND: | First Respondent BIRINC TRADE CORP Second Respondent SKY WEALTH INTERNATIONAL LTD (and others named in the Schedule) Third Respondent | |

DATE OF ORDER: |

THE COURT DECLARES THAT:

1. The First Respondent breached his statutory duties to the Applicant in contravention of ss 181(1) and 182(1) of the Corporations Act 2001 (Cth) (the Act) and breached his fiduciary duties to the Applicant as the chief executive officer and the director responsible for fundraising by:

(a) procuring the purchase of a substantial number of shares in the Applicant, and the sale of a substantial number of shares in the Applicant for profit, thereby diverting investors from taking up shares in the Applicant;

(b) causing the Applicant to enter into a loan agreement with LGA Energy Investments Limited which contained an option to convert past and future loans to the Applicant to shares in the Applicant at SG$1.80 per share, at a time when the market price for shares in the Applicant was at least US$2 per share;

(c) causing LGA Energy Investments Limited to exercise the option at SG$1.80 per share under the said loan agreement, in circumstances where:

(i) he was selling shares in the Applicant at US$2 per share to raise funds that could be advanced under the loan agreement;

(ii) shares could be placed in the market at more than US$2 per share, including, between December 2013 and March 2014, at US$5 per share.

(d) from September 2013 to July 2014, procuring the sale of shares in the Applicant

at US$2 to fund the Applicant, instead of at the going price of up to US$5 per share;

(e) causing the Applicant to enter into a loan agreement with the Fourteenth Respondent which contained an option to convert loans to the Applicant to shares in the Applicant at 80 per cent of the share price reported in the last audited accounts, then SG$1.80 per share, at a time when there was a market for shares at US$10 per share.

2. The First Respondent was involved in LGA Energy Investments Limited’s contravention of s 208 of the Act by causing the entry into and extension of the loan agreement with the Applicant, and exercises of the option therein.

3. The Second to Fifteenth Respondents:

(a) were involved in the First Respondent’s contraventions of ss 181(1) and 182(1) of the Act; and

(b) knowingly assisted in the First Respondent’s breaches of his fiduciary duties under the second limb of Barnes v Addy.

4. The First to Fifteenth Respondents are jointly and severally liable to account to the Applicant for the profit obtained by each of them by reason of the First Respondent’s fiduciary breaches.

5. 2,800,000 shares in the Applicant held by the Second Respondent comprise the traceable proceeds of profit obtained by reason of the First Respondent’s fiduciary breaches, and are held on a constructive trust for the Applicant.

6. 2,350,000 shares in the Applicant held by the Fifth Respondent comprise the traceable proceeds of profit obtained by reason of the First Respondent’s fiduciary breaches, and are held on a constructive trust for the Applicant.

7. 2,800,000 shares in the Applicant held by the Sixth Respondent comprise the traceable proceeds of profit obtained by reason of the First Respondent’s fiduciary breaches, and are held on a constructive trust for the Applicant.

8. 2,583,641 shares in the Applicant held by the Seventh Respondent comprise the traceable proceeds of profit obtained by reason of the First Respondent’s fiduciary breaches, and are held on a constructive trust for the Applicant.

9. 2,300,000 shares in the Applicant held by the Eighth Respondent comprise the traceable proceeds of profit obtained by reason of the First Respondent’s fiduciary breaches, and are held on a constructive trust for the Applicant.

10. That the payments totalling US$8.3 million and SG$2,570,707 paid to the Applicant and attributed to the loan agreement with the Fourteenth Respondent comprise profit (or the traceable proceeds thereof) obtained by reason of the First Respondent’s fiduciary breaches.

AND THE COURT ORDERS THAT:

11. The First to Fifteenth Respondents account to the Plaintiff in the sum of AU$42,000,000.00.

12. The First to Fifteenth Respondents pay the Applicant’s costs of and incidental to this proceeding.

13. Liberty to apply.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

BEACH J:

1 I have previously delivered judgment in this matter making findings on liability against the first respondent, Mr Huber, and the second to fifteenth respondents (the Huber controlled entities); see CellOS Software Ltd v Huber (2018) 132 ACSR 468: [2018] FCA 2069.

2 In summary I found that Mr Huber, although the chief executive officer of CellOS at the relevant time and with responsibility for raising funds to run CellOS’ business, instead of procuring potential investors to buy shares issued by CellOS, diverted potential investors to buying shares from him through the Huber controlled entities, which shares he had purchased in a grey market at a substantial discount to the price that CellOS could have issued them for. Further, in order to fund CellOS, Mr Huber caused LGA and Pized to enter into uncommercial loan agreements with CellOS, without disclosing his interest in these lending entities. For convenience and unless I stipulate otherwise, terms used in these reasons have the same meanings as I defined in my principal reasons. What I have just described in terms of Mr Huber’s pattern of behaviour may be defined as “the Scheme”.

3 I found that Mr Huber had breached ss 181(1) and 181(2) of the Corporations Act 2001 (Cth) (the Act) and his fiduciary duties to CellOS. I also found that the Huber controlled entities were knowingly involved in these contraventions and also knowingly assisted Mr Huber’s breaches of his fiduciary duties as reflected in the second limb of Barnes v Addy.

4 Late last year a further trial was conducted on the question of equitable remedies. On the basis of my principal findings and the further evidence adduced, CellOS is entitled to an account of profits, with a constructive trust to be ordered in aid of that account which will apply to the shares in CellOS held by the Huber controlled entities.

5 Now at the start of the trial on quantum, CellOS sought an account of the profits made by Mr Huber and the Huber controlled entities on the sale of shares purchased by them at a discount and subsequently sold for between US$2 and US$10 per share, together with a constructive trust over the CellOS shares still held by the Huber controlled entities and obtained through the Scheme. Alternatively, CellOS sought equitable compensation for:

(a) the loss of the opportunity to issue new shares to investors due to the diversion of investors by the Scheme; and

(b) the loss occasioned by the issuing of shares under the LGA loan agreement at SG$1.80 in circumstances where the prevailing price for the sale of CellOS shares was at least US$2, and by late 2013 not less than US$5 per share.

6 But as matters developed, an account of profits seemed to me to be the most suitable remedy, and this was ultimately CellOS’ preference as Dr Charles Parkinson telegraphed during his meticulous presentation.

7 Let me say something about the evidence adduced at this second stage. By orders that I made after the trial on liability, Mr Huber was ordered to file and serve an affidavit setting out details of all profits made by him and the Huber controlled entities as a result of the Scheme. Pursuant to that order, Mr Huber filed an affidavit dated 14 March 2019, CellOS filed an additional expert report of Ms Siobhan Hennessy, a partner of PWC Australia, dated 21 May 2019 (the further Hennessy report). Mr Huber then filed a second affidavit dated 2 July 2019 responding to the further Hennessy report. Further, Mr Huber filed other material being two sets of extensive written submissions dated 21 October 2019 and 20 December 2019 together with additional documentary material by way of further evidence. I should also note that CellOS was given leave to file a supplementary report of Ms Hennessy as a result of issues that arose during this second stage, which report was provided on 2 December 2019 (the supplementary Hennessy report).

8 Before getting into the detail, let me briefly say something about equity. No elaborate disquisition is necessary.

Some equitable principles

9 A secure starting point is Mason J’s observations in Hospital Products Ltd v United States Surgical Corporation (1984) 156 CLR 41 at 107 to 110.

10 First, a fiduciary is liable to account for a profit or benefit obtained:

(a) in circumstances where there is a conflict or possible conflict of interest or duty; or

(b) by reason of the fiduciary taking advantage of any opportunity or knowledge which he derived in consequence of his occupation of the fiduciary position.

11 In Ancient Order of Foresters in Victoria Friendly Society Ltd v Lifeplan Australia Friendly Society Ltd (2018) 360 ALR 1 at [68] and [69], Gageler J elaborated on these two bases, and then went on to observe three matters that are relevant to my context, namely:

(a) it is not necessary for the fiduciary to be liable to account that the benefit or gain to the fiduciary be at the expense of the principal;

(b) it is not necessary to show that the fiduciary acted dishonestly, fraudulently or otherwise than in good faith;

(c) but contrastingly to (b), if a knowing participant in someone else’s breach of fiduciary duty is to be held liable to account, the conduct of the fiduciary must be shown to be of a dishonest and fraudulent character.

12 Second, as Mason J said, to be liable to account it is not necessary to show and it makes no difference that it was not the fiduciary’s duty to obtain the profit or benefit for the person to whom the duty was owed as an incident of his fiduciary duty.

13 Mason J then took forward some of these themes as a participant in the joint reasons in Warman International Limited v Dwyer (1995) 182 CLR 544 at 557 to 562. Let me continue adding to the list of propositions that can be synthesised from Warman as further expounded in Ancient Order.

14 Third, liability to account does not depend upon establishing that the person to whom the duty was owed had suffered injury or loss. But when accounting for profits, “the amount of what has been lost by the plaintiff may in some situations be relevant to what has been gained by the errant fiduciary or knowing assistant” (Ancient Order at [190] per Nettle J). There is of course no contradiction here. Liability to account is not so contingent. But if there is injury or loss to the person to whom the duty is owed, then such injury or loss is not necessarily irrelevant in a forensic sense in the account context.

15 Fourth, in practice the assessment of the profit may be difficult. Now given the nature of the task, no arithmetical exactness is required. But what is required is to be as accurate as one can, albeit that this may in context not rise higher than reasonable approximation because of forensic limitations or imprecision inherent in the evaluative exercise of determining the causally connected profit or gain. I will elaborate on this causation question in a moment.

16 Fifth, “[it] is necessary to keep steadily in mind the cardinal principle of equity that the remedy must be fashioned to fit the nature of the case and the particular facts” (Warman at 559).

17 Sixth, in terms of determining the liability to account for and disgorge any profits, one is not confined to looking only at the direct result of particular acts of wrongful knowing assistance. One is entitled to look at the overall effect of the wrongful conduct (Ancient Order at [4] and [5] per Kiefel CJ, Keane and Edelman JJ).

18 Seventh, what an errant fiduciary or knowing participant is required in equity to account for in terms of any gain or benefit is surely to be informed by the nature of the equitable duty or obligation found to have been breached, as well as the state of mind of the fiduciary or both the fiduciary and the knowing participant.

19 Eighth, it is for the respondent “to establish that it is inequitable to order an account of the entire profits” (Warman at 561). So, if there has been a mingling of the profits attributable to the respondent’s breach of fiduciary duty with the profits attributable to the respondent’s efforts and investment not connected to the opportunity gained by being a fiduciary, the respondent bears the onus of justifying the disentanglement.

20 Relatedly, “[w]hether it is appropriate to allow an errant fiduciary a proportion of profits or to make an allowance in respect of skill, expertise and other expenses is a matter of judgment which will depend on the facts of the given case” (Warman at 562).

21 Let me now elaborate further on causation and quantification by reference to Ancient Order.

22 First, if one is dealing with the liability of a knowing participant, the relevant causal connection is not between the benefit or gain and the conduct which constitutes knowing participation. Knowing participation is not a “free-standing head of liability divorced from the fiduciary obligations” (Gageler J at [85]). Rather, the benefit or gain for which a knowing participant may be liable to account is required to have a causal connection with the fiduciary’s breach of his equitable obligations.

23 Second, it may be sufficient to establish a causal connection if the benefit or gain to the fiduciary or knowing participant would not have been obtained “but for” the breach (plurality at [9] and Gageler J at [88]), but that is not the only way to establish causation; for example, a test of material contribution may suffice and even where a “but for” test is not satisfied.

24 Now as I have indicated, where a causal connection is shown to exist, the onus shifts to the respondent to establish that it is inequitable to require an accounting of the total value of the benefit or gain received. So, the plurality said (at [13]):

While it is true that equity will not require an errant fiduciary or a participant in a breach of fiduciary duty to account for an advantage which the breach of fiduciary duty has not caused or to which it has not sufficiently contributed, where causation is sufficiently established the onus is upon the errant fiduciary or participant to show that he or she should not account for the full value of the advantage. That onus is not discharged by mere conjecture or supposition giving the benefit of the doubt to a proven wrongdoer. The requirement of proof conforms with the obligation of a party charged with a breach of fiduciary duty to show why the full value of an advantage obtained in a situation of conflict of duty should not be disgorged.

(Citations omitted.)

25 There are various ways that such an onus might be discharged. Relevantly to my context, the plurality explained (at [15] and [16]):

The second way, which was the focus of this appeal, is by demonstrating that the benefit or advantage is beyond the scope of the liability for which the wrongdoer should account for profits. A wrongdoer might prove that some profit or benefit is beyond the scope of liability for which he or she should account if the profit or benefit has no reasonable connection with the wrongdoing.

…

No precise test has been prescribed for determining when it will be inequitable to account for a benefit on the basis that it has no reasonable connection with wrongdoing. Nor is there any need for such a test. All of the circumstances must be considered, including the nature of the conduct. It is pertinent here that the profits were from deliberate and dishonest conduct, and were those desired to be achieved.

…

26 Gageler J also explained (at [92]):

Putting aside those cases in which equitable relief might be withheld on established discretionary grounds by reference to disentitling conduct of the plaintiff, the defendant needs to demonstrate, in order to establish that it is inequitable to order an account of the value of the whole of the identified benefit or gain, either that the benefit or gain is attributable in part to one or more other contributing causes by reference to which it is “practically just” that the benefit or gain be apportioned or that some allowance be made in favour of the defendant, or that there is some other reason why accounting for the whole of the gain would amount to a windfall to the plaintiff of such a nature or to such a degree that the accounting would fail to vindicate the purposes underlying equity’s imposition of the fiduciary obligation that has been breached.

(Citations omitted.)

27 And as he said (at [94]):

Factors which might bear on the judgment to be made in an individual case cannot be catalogued exhaustively in advance. They will include the relative extent to which other causes which might include the skill and industry of the defendant can be assessed as having contributed to the benefit or gain that is causally connected to the breach of fiduciary obligation. They will also include whether, and if so to what extent, the defendant’s gain reflects uncompensated loss on the part of the plaintiff. And although the purpose of the remedy is not to punish, consideration of what is just in the context of the equitable obligation to be vindicated by the remedy cannot exclude consideration of the severity of the breach of the fiduciary obligation and the extent of the defendant’s own involvement and culpability in it.

28 Ultimately, one is engaged in both a factual and evaluative exercise in determining the true measure of the benefit or gain for which the respondent must account, requiring an analysis of both causation and the points just made.

29 To this point I have only dealt with an account of profits. Let me now deal with a question relating to equitable compensation concerning CellOS’ loss. CellOS says that it lost the right to issue shares at a particular price. But in such a scenario, what is the loss? Is it the full subscription moneys constituting the essence of the loss of capital? Or is it the loss of opportunity to raise capital? On one view it might be said that what would have been lost were shareholders’ funds. On another view it might be said that there is not a real loss because the asset created (share proceeds received) would be matched by a corresponding “liability” reflected in the share capital account, with the capital ultimately being returnable to shareholders. On yet another view it might be said that such a capital sum is not irrevocably lost because CellOS could always raise that capital at another time. Further, should the focus not be on the loss of capital or the lost opportunity to raise capital, but rather the loss of use of any money that would have been received if the capital in the counterfactual scenario had been raised?

30 On the question of share capital, it is worth repeating what was said in Cable & Wireless Australia & Pacific Holding BV (in liq) v Federal Commissioner of Taxation (2017) 251 FCR 483 at [94] and [95] per Allsop CJ, Middleton and Beach JJ:

… [B]efore proceeding further it is necessary to be clear about what is meant by “capital” or “shareholders’ capital”. In the present context, we are concerned with share capital rather than other commercial contexts such as working capital. As explained by Gower and Davies’ Principles of Modern Company Law (9th edition by Paul Davies and Sarah Worthington) at [11-1], in the present context, “capital” connotes the value of the assets contributed to the company by those who subscribe for its shares; we are not, of course, here dealing with the market value of shares. We have emphasised the “value” of what is contributed, as it is this concept rather than the assets themselves (say subscription money) that is being referred to; it may also be appropriate to describe this in terms of the “amount of the share(s)” so contributed (see for example, Archibald Howie Pty Ltd v Commissioner of Stamp Duties (NSW) (1948) 77 CLR 143 at 153 per Dixon J). The assets will change their form, indeed may be disposed of or lost. But this is not a reduction of capital as such. Likewise, the company may create or acquire new or enhanced assets through, for example, trading profitably, borrowing money from a third party or asset revaluation. But this is not share capital as such in that form. Moreover, a share capital account is not as such an asset account.

The concept of “capital” as used in the present context is also to be distinguished from “equity”. The concept of “equity” usually describes a surplus of assets over liabilities. It is not the same as capital. So, in the present case, for Optus in the year ending 31 March 2002, total equity equalled net assets. Total equity itself can be divided into components. So, for Optus for the year in question, it was divided into “contributed equity”, “reserves” and “retained profits (accumulated losses)”. But the only component of total equity referable to “capital” or “shareholders’ capital” was “contributed equity”. And, as we have indicated earlier, the debit on the buy-back reserve account was not in form or in substance a charge on contributed equity. It was never seen as such commercially or economically by any of the highly sophisticated relevant participants (the complete opposite to the scenario in Consolidated Media).

31 In my view, rather than talking about share capital, it is better to focus on the subscription moneys that would otherwise have been payable to CellOS. What is the loss then? Prima facie, it may be said that the loss would be the lost opportunity to use the subscription moneys, rather than the face value of the subscription moneys. On the value of a lost opportunity, it is useful to recall what was said in Generic Health Pty Ltd v Bayer Pharma Aktiengesellschaft (2018) 267 FCR 428 at [181] to [184] per Allsop CJ, Yates and Beach JJ:

We are dealing with a hypothetical situation of the past, namely, whether if a sale of Isabelle had not been made, then an equivalent sale of Yasmin would have been made. Accordingly, we must form an estimate of the likelihood that the hypothetical situation would have occurred: see Malec v JC Hutton Pty Ltd (1990) 169 CLR 638 at 639 per Brennan and Dawson JJ. In that respect, we must assess the degree of probability that such an event would have occurred and adjust any award of damages to reflect that degree of probability: Malec at 643 per Deane, Gaudron and McHugh JJ.

In another sense, the question can be looked at through the lens of the value of a lost opportunity. The lost opportunity was to make a sale of Yasmin if the sale of Isabelle had not been made. In our view, it is not in doubt that it was established before the primary judge that, on the balance of probabilities, for all sales of Isabelle there was a loss of an opportunity to make a sale of Yasmin. The question then is: what is the value of the lost opportunity? On that question, the value is to be “ascertained by reference to the degree of probabilities or possibilities” involved in the hypothetical counterfactual: Sellars v Adelaide Petroleum NL (1994) 179 CLR 332 at 355 per the plurality.

Another way to express the same point is as Brennan J described it in Sellars at 368:

Although the issue of a loss caused by the defendant’s conduct must be established on the balance of probabilities, hypotheses and possibilities the fulfilment of which cannot be proved must be evaluated to determine the amount or value of the loss suffered. Proof on the balance of probabilities has no part to play in the evaluation of such hypotheses or possibilities: evaluation is a matter of informed estimation.

This theme of informed estimation resonates with some observations made by Hayne J in Placer (Granny Smith) Pty Ltd v Thiess Contractors Pty Ltd (2003) 77 ALJR 768; 196 ALR 257 at [37] and [38]. Any estimation must be done “with as much precision as the subject matter reasonably [permits]”. Mere difficulty in estimating damages does not relieve a court “from the responsibility of estimating them as best it can”.

32 There is authority for the notion that in one sense one is looking at the revenue element of the loss, rather than a loss of capital. So the question is: what was the loss of revenue which might have been obtained by the use of the money or at least the lost opportunity in that respect? Support for such a measure is provided by Adelaide Petroleum NL v Poseidon Ltd (1990) 98 ALR 431 at 530 to 531 per French J, Poseidon Ltd v Adelaide Petroleum NL (1991) 105 ALR 25 at 42 per Burchett J and at 51 per Lee J, Strategic Minerals Corp NL v Basham (1997) 25 ACSR 470 at 506 to 507 per White J and Ramsay v BigTinCan Pty Ltd (2014) 101 ACSR 415 at [69] to [72] per Macfarlan JA. So, on these authorities it is the loss of use of the funds rather than the loss of the capital per se which is the appropriate measure in terms of looking at the matter through the lens of a loss of opportunity.

33 But I do not think that this is a comprehensive answer in all cases. What if the market appetite for the issue at the time it should have occurred was $10 per share? Now assume that the opportunity to issue was lost at that price. But assume later that the market appetite was only $1 per share. Has the company lost $9 per share? In one sense, yes. But in another sense, no. The company may be able to get in the same overall dollars by reducing the issue price but issuing more shares. But then there would be consequential damage to its capital raising ability including detriment to existing shareholders who would suffer an unnecessary diminution in their holdings which would have flow on consequences. But that would be a different type of loss. But what if the opportunity was lost altogether because it would seemingly be unrealistic to issue shares below a particular price? Even then, the lost subscription moneys might not be recoverable as a capital loss. The company may be able to procure other forms of finance, albeit more expensive. In such a scenario, the loss might be the additional costs incurred flowing from the company having to obtain a less desirable and more expensive form of finance.

34 I do not need to elaborate further as I propose to order an account of profits rather than equitable compensation.

Analysis

35 In my view, by diverting Cellos’ opportunity for it to issue new shares into the market, Mr Huber improperly gained profits. The Scheme’s essential elements as found by me were as follows. Between 20 September 2011 and 12 August 2015, at least 47,529,484 shares in CellOS were transferred to the Huber controlled entities from third party investors; my earlier reasons had a figure of 47,872,063 although this has now been revised down in the light of Ms Hennessy’s further evidence. Mr Huber then promoted CellOS shares to investors, ostensibly to raise capital directly for CellOS by the issue of new shares. Between 20 September 2011 and 11 August 2015, Mr Huber sold via the Huber controlled entities at least 51,945,132 shares he had acquired from early investors to 355 third party investors. Those sales generated significant profits, which were in part directed to CellOS and attributed to LGA under the LGA loan agreement and later to Pized under the Pized loan agreement. Mr Huber’s position is that he made no profit from the Scheme. Further details of the Scheme are set out in my principal reasons.

36 Let me first deal with Ms Hennessy’s evidence as set out in the further Hennessy report and as debated at the hearing of this second stage.

37 Ms Hennessy was instructed by reference to my principal reasons to calculate the profit made by the respondents. She did so after making some revisions to some of the figures referred to in my reasons that the parties now accept. In the further Hennessy report, Ms Hennessy estimated that the profit made by the respondents on the sale of the shares was between AU$52,515,488 (the low scenario) and AU$114,196,498 (the high scenario), with a mid-point estimate of AU$105,477,847 (the mid scenario). These figures have been more recently updated, a matter which I will discuss later.

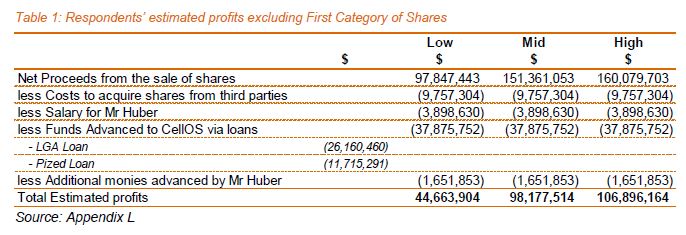

38 The difference between the two assessments of gross share sale proceeds caused the ultimate difference between the low scenario and mid scenario assessments of net profit. The difference was as a result of the assumptions adopted by Ms Hennessy as to the price paid to the respondents for the share sales where the sale price was not known. In both scenarios, Ms Hennessy relied upon the actual price paid for the shares where it was known. But in the low scenario in relation to the balance of share sales where the consideration was not known, Ms Hennessy assumed that the shares were sold at AU$2.23 per share, which was the weighted average AUD equivalent per share purchase price paid by the respondents for CellOS shares where the consideration was known. In the mid scenario, Ms Hennessy assumed that the shares were sold at AU$3.36 per share, which was in turn based on an assumed market for CellOS shares of US$2 per share pre-30 May 2014, and US$10 per share post-30 May 2014. The latter assessment was based on an analysis of the market price paid for CellOS shares, which showed that the typical price for CellOS shares was US$2 up to 30 May 2014, and US$10 thereafter. I found that in the period from September 2013 to July 2014, there were willing buyers of CellOS shares at US$5 and up to US$10. There was additional evidence before me that the market price for CellOS shares from mid-2014 was between US$5 and US$10. In the high scenario, further to the mid scenario, Ms Hennessy relied on a market price of US$5 for CellOS shares from 16 December 2013 to 30 May 2014.

39 It is worth stating now that adopting a conservative approach, which is in favour of the respondents, my final calculations rely upon relevant low scenario assumptions.

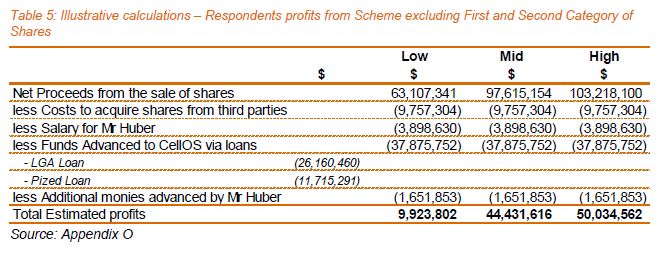

40 More generally, in my view, subject to some matters that I will discuss later, Ms Hennessy’s methodological approach to the calculation of profit was appropriate.

41 Ms Hennessy also made an allowance for a substantial AU$1 million a year salary for Mr Huber, notwithstanding that it was for Mr Huber to make out any appropriate allowances in light of his conduct.

42 Now although Mr Huber was directed to file an affidavit disclosing the profits made by him, Mr Huber’s affidavits in the main simply seek to challenge my principal reasons. Much remains unexplained and undisclosed, including Mr Huber’s failure to disclose additional bank accounts which may show the flow of funds to him, the source of the payment of US$900,000 for the balance of his personal property purchase in Dubai or much in the way of corroborating documentation for the assertions contained in his affidavits.

43 In such circumstances, I am entitled to draw inferences about the respondents’ profits extrapolating out from the known purchase and sales consideration, and upon making the assumption that shares were sold at market price. Indeed, it was for Mr Huber to prove that the consideration actually paid in respect of any of those share transfers was less than the market price, and to make out any appropriate deductable allowances.

44 Further, even if I do not accept Ms Hennessy’s approach to the calculation of profit, my findings would support an order that the respondents profited by at least AU$30 million on an alternate basis. Let me explain.

45 AU$26,160,460 was paid to CellOS and attributed to the LGA loan agreement. I found that SG$16.8 million of that amount was derived from the sale of shares held by Basalt, which purchased its shares from early investors, and that “it [was] likely that the remainder derived from the sale of shares listed in sch 1 to the 5FASOC” (at [683] and [740]). I found that Mr Huber was not selling his personal shares in Blue Delorite, and had no other way of personally generating funds. To the extent there is any doubt, I accept that all funds attributable to the LGA loan agreement were net profits earned by Mr Huber from the sale of CellOS shares in the grey market. But on any view, at the least half the funds going into the LGA loan were derived from the Scheme.

46 Mr Huber then caused the conversion of the entire LGA loan agreement “debt” into 17,477,204 CellOS shares at SG$1.80 per share of which 16,815,157 were transferred on 9 May 2014 to Birinc (2,800,000), Sky Wealth (2,300,000), Rex Investors (1,681,516), Sun Way (2,350,000), Aura Finance (2,800,000), Harvest Sky (2,583,641) and Rich Max (2,300,000).

47 Further, as any profits improperly earned by Mr Huber were held on constructive trust for CellOS, the CellOS shares issued to LGA and their subsequent sale proceeds comprised the traceable property of CellOS. But on any view, over half of these shares were held on constructive trust for CellOS. Of the LGA shares, only 4,265,157 were sold for valuable consideration. On any view, these were held on trust for CellOS. Of these 4,265,157 shares, I made findings that 2,000,000 shares were sold to the Pecks for US$2 per share for a total consideration of US$4 million, 399,000 shares were sold to other investors for US$10 per share for a total consideration of US$3,990,000, and the consideration paid for the balance of the 1,866,157 shares was unknown.

48 Mr Huber stated that in the latter half of 2014, he sold about 1 million CellOS shares at US$10 per share. This is consistent with the evidence about the market price of CellOS shares at that time. If the balance of 1,866,157 shares where the consideration was unknown were sold at US$10 per share, then the total consideration for those shares was US$18,661,570. The total consideration, together with the known consideration paid for the LGA shares, would be US$26,651,570. Allowing a deduction for 10% brokerage fees would make a profit of US$23,986,413, or approximately AU$35,499,891.25 at exchange rates at the relevant time. Allowing a further deduction for salary for Mr Huber at AU$3,898,630, would mean a profit of AU$31,601,261.25.

49 I do not propose to elaborate further on this alternative basis as I have accepted Ms Hennessy’s final calculations based upon her central methodology which I will explain later, albeit on the low scenario basis.

50 Let me at this point say something on the question of loss from the perspective of CellOS, even though I do not propose to award equitable compensation.

51 Ms Hennessy also estimated CellOS’ loss at between AU$58,491,271 and AU$120,172,281, with a mid scenario assessment of AU$111,453,630.

52 By the Scheme, Mr Huber caused CellOS detriment by denying it the opportunity to raise funds by directly issuing shares to investors. Ms Hennessy’s calculation of CellOS’ loss differs only from her calculation of Mr Huber’s profit in the sense that CellOS would not have had to acquire CellOS shares from early investors to resell. Accordingly there is no deduction for the estimated AU$9,874,413 paid by Mr Huber to acquire shares from early investors, nor any deduction for 10% in brokerage fees in relation to the purchase of those shares. Rather, Ms Hennessy assumed a AU$1 million per annum (AU$3,898,630 in total) cost to CellOS to issue the shares directly to investors.

53 The relevant but for analysis assumes that CellOS would have been able to issue the same quantum of shares for the same amount it is estimated that Huber sold them for, less the additional cost to CellOS to issue new shares instead of trading extant stocks.

54 Further, I found that Mr Huber caused detriment to CellOS, being the difference between the amount actually raised (reflected in SG$1.80 per share under the LGA loan agreement and option) and the amount CellOS would have raised if the shares had been issued by CellOS to investors (at least US$2, and possibly US$5 per share). I found that by exercising the option to convert debt to equity at SG$1.80 per share, Mr Huber caused relative detriment to CellOS’ shareholders by diluting their shareholdings in disadvantageous circumstances.

55 It would seem for the evidence that the loss suffered from those uncommercial share issues (excluding sales commissions) was in excess of US$10,179,489.26, using the market price of US$2 per share, that is, AU$15,065,644.10 using an appropriate exchange rate, calculated as follows:

Date | Shares issued | Issue price SG$ | SG$: US$ at issue | Issue price US$ | MP at US$2 | Loss at MP of US$2 | MP at US$5 | Loss at MP of US$5 | |

a) | 28.06.13 | 6,453,773 | 11,616,791 | 0.78375 | 9,104,659.95 | 12,907,546 | 3,802,886.05 | 32,268,865 | 23,164,205.05 |

b) | 2.10.13 | 3,467,877 | 6,242,179 | 0.7966 | 4,972,519.79 | 6,935,754 | 1,963,234.21 | 17,339,385 | 12,366,865.21 |

c) | 10.12.13 | 333,333 | 600,000 | 0.80037 | 480,222 | 666,666 | 186,444.00 | 1,666,665 | 1,186,443.00 |

d) | 6.02.14 | 1,666,666 | 3,000,000 | 0.78413 | 2,352,390 | 3,333,332 | 980,942.00 | 8,333,330 | 5,980,940.00 |

e) | 19.02.14 | 1,388,888 | 2,500,000 | 0.79084 | 1,977,100 | 2,777,776 | 800,676.00 | 6,944,440 | 4,967,340.00 |

f) | 27.03.14 | 4,166,666 | 7,500,000 | 0.78507 | 5,888,025 | 8,333,332 | 2,445,307.00 | 20,833,330 | 14,945,305.00 |

Total: | 17,477,203 | 31,458,970 | 24,774,916.74 | 34,954,406 | 10,179,489.26 | 87,386,015 | 62,611,098.26 |

56 I do not need to reflect further on these loss questions as I propose to order an account of profits. And as I say, there are conceptual difficulties with measuring loss in this way concerning loss of opportunity where a company has lost the opportunity to issue new capital at a particular price. But I do not need to discuss these matters further.

Eight issues

57 As I have indicated, the remedy in the frame is an order for an account of profits against Mr Huber and the Huber controlled entities, calculated in accordance with the methodology set out in the further Hennessy report although with some modifications arising from the following matters.

58 There were eight substantive matters raised before me in addition to Mr Huber’s more general point that he made no profit. Further, as I have said, the onus fell upon Mr Huber to identify why and to what extent it would be inequitable to order that he and the Huber controlled entities should not have to account for the entire profit derived from the Scheme.

59 The first issue was whether it was open to Mr Huber to contend that the 20,800,000 shares detailed in the table following [59] of his affidavit dated 2 July 2019 were transfers of his personal shares, in the face of my findings that they were not. I note that CellOS accepted that the 15th transfer detailed in the list of the 20,800,000 shares, that is, the 3,000,000 shares transferred by Blue Delorite to Maitreya Mandala on 10 September 2012, was a transfer on Mr Huber’s behalf. Otherwise CellOS made no other concession.

60 The second issue was whether the further Hennessy report erroneously included a sale of 1,500,000 shares of the 20,800,000 shares to Woon Shung Toon on 10 October 2012 as a sale by a Huber controlled entity to a third party. I note that CellOS accepted that 1,100,000 of the 1,500,000 shares transferred by Maitreya Mandala to Woon Shung Toon on 10 October 2012 involved a transfer of Mr Huber’s shares. They have now been removed from the calculation of profit in the supplementary Hennessy report. No other concession has been made.

61 The third issue was whether the further Hennessy report erroneously included transfers of 12,700,000 of the 20,800,000 shares to Mr Narulla associated persons, as purchases from third parties. CellOS did not make any concession as to any of these share transfers.

62 As to issues one to three, Mr Huber says that he transferred 20,800,000 shares (more accurately 20,846,978 shares) to Mr Narulla and persons associated with him to hold and sell on his behalf to fund CellOS (issue one). He says that these shares were not part of the Scheme, and he identified what he said was the subsequent transfer of these shares, erroneously included in the further Hennessy report as transfers as part of the Scheme (issues two and three). CellOS says that, inter alia, issue one is contrary to my findings made at the trial on liability, although CellOS makes a limited concession in relation to a single share transfer, which traces into the shares the subject of issue two.

63 The fourth issue was whether the further Hennessy report erroneously included 1,100,000 shares transferred by Blue Delorite to CellOS staff on 27 November 2013 as sales by a Huber controlled entity to third parties, and 400,000 shares transferred from CellOS staff to Blue Delorite (on 1, 2, 13 and 24 April 2015) as purchases by a Huber controlled entity from third parties. But CellOS has now conceded that Mr Huber should be given credit for these share transfers. They have been removed from the calculation of profit in the supplementary Hennessy report.

64 The fifth issue was whether the further Hennessy report erroneously included the transfer of 950,000 shares from Blue Delorite to Tay Teck Huat on 18 April 2013, as a sale by a Huber controlled entity. CellOS has now also conceded that Mr Huber should be given credit for these share transfers and they have been removed from the profit calculation in the supplementary Hennessy report.

65 The sixth issue was whether the further Hennessy report erroneously included 8,106,500 shares transferred by “Narulla companies” to Melvin Tan and his wife Seah Chye Tin, as sales by Huber controlled entities to third parties. CellOS has not made any concession in respect of any of these share transfers.

66 The seventh issue was whether the further Hennessy report erroneously included 2,540,000 shares transferred by “Narulla companies” to other “Narulla companies”, as sales by Huber controlled entities to third parties. Again, CellOS has not made any concessions in respect of any of these share transfers.

67 As to issues six and seven, Mr Huber says that CellOS shares were sold by Mr Narulla and Mr Min Wee without his knowledge, and that these shares should be excluded from Ms Hennessy’s calculations. He identified 10,600,000 such shares. CellOS says that Mr Huber knew about and received a benefit in respect of these sales.

68 The eighth issue was whether Mr Huber was entitled to a credit for any further amounts paid to CellOS and not attributed to the LGA or Pized loans in the further Hennessy report or the initial Hennessy report of 27 July 2017. Now CellOS has conceded that Mr Huber should be given credit for the following additional payments of SG$2,098,000 made to CellOS: SG$500,000 on 4 March 2013; SG$70,000 on 21 January 2013; SG$1,220,000 less SG$122,000 (SG$1,098,000) on 3 October 2012; and SG$430,000 on 3 August 2012. But CellOS says that these payments do not result in any extant liability owed by CellOS to LGA. I also note that Mr Huber has been given a credit for these amounts in the supplementary Hennessy report.

69 Let me go into some of the issues in a little more detail. For this purpose, let me begin with issues one to three involving the 20,800,000 shares.

Issue one

70 As I have indicated, this issue was raised in Mr Huber’s defence to the liability case. The list of the 20,800,000 shares contained in the second Huber affidavit is relevantly the same as the list contained at annexure five of Mr Huber’s witness statement dated 18 August 2017. In the Huber witness statement, Mr Huber claimed that between 2008 and 2010, he had transferred 4,500,000 shares to Mr Narulla to hold for him and later sell. He said further that those shares were transferred to Child and Family Foundation and sold by mid-2012, at which point he transferred another 16,300,000 shares to Mr Narulla to sell to raise more funds for CellOS.

71 Mr Huber was cross-examined about these matters at length at the trial on liability, and his evidence was shown to be unreliable to say the least. A share adjustment prepared for PWC in the course of conducting CellOS’ audit recorded that some of Mr Huber’s transfers of shares from Blue Delorite to Mr Narulla and others were for services rendered by Mr Narulla. Blue Delorite was reimbursed for these shares on the basis that they were really being transferred on behalf of CellOS. The auditors acknowledged these transfers and Blue Delorite was reimbursed 5,700,000 shares on that basis. Mr Huber told the board of CellOS that these shares were being transferred to Blue Delorite as a reimbursement.

72 Mr Huber ultimately conceded that the shares he said that he had transferred to Mr Narulla to be sold through Child and Family Foundation were in fact provided for services rendered, that he was reimbursed for these, and that none of the 4,500,000 early shares Mr Huber identified as being transferred were being held by Mr Narulla on trust for him. Further, there was no subsequent transfer of 16,300,000 shares from Blue Delorite and/or Mr Huber to Mr Narulla and others that Mr Huber could identify as being part of the Scheme. Further, when asked why he bothered to transfer his shares to Mr Narulla in order that the shares be sold by Child and Family Foundation or other companies rather than Mr Huber retaining control of his shares himself, Mr Huber could offer no explanation. Mr Huber also acknowledged that Mr Jaspal Narulla (Mr Narulla’s uncle), the recipient of 1,500,000 of the 20,800,000 shares, had provided assistance to CellOS. Further, Mr Jaspal Narulla claimed that he was still owed 8,500,000 shares. Mr Huber conceded that Mr Jaspal Narulla’s claims were inconsistent with Mr Huber having transferred shares to Mr Jaspal Narulla to hold on Mr Huber’s behalf. He was unable to provide any explanation for the discrepancy.

73 In my view, Mr Huber’s evidence was unreliable to say the least, and none of the 20,800,000 shares were transferred to Mr Narulla and others to be held on Mr Huber’s behalf.

74 Further, Mr Huber conceded on the second day of the trial on quantum that he had received a reimbursement in respect of 2,500,000 of the 20,800,000 shares. Accordingly, he now claims that only approximately 18,300,000 shares were transferred to Mr Narulla and others to be held on his behalf. Although Mr Huber did not specifically identify the shares in respect of which he accepted he had received refunds, CellOS has now identified, which I accept, those 2,500,000 shares (in reality, 2,437,510 shares) as being:

(a) 500,000 shares transferred by Blue Delorite to “JASPAL NARULLA FAM INVTS P/L” on 7 January 2008;

(b) 500,000 shares transferred by Blue Delorite to “WETWATERS 8 (S) PTE LTD” on 7 January 2008;

(c) 500,000 shares transferred by Blue Delorite to “BARAMUL SIGPAORE PTE LTD” on 7 January 2008; and

(d) 937,510 shares transferred by Blue Delorite to Harveen Narulla on 11 July 2008.

75 Now CellOS accepts that the 15th transfer detailed in the list of the 20,800,000 shares, that is, the 3,000,000 shares transferred by Blue Delorite to Maitreya Mandala on 10 September 2012, were not transferred to Mr Narulla (or for his benefit) for consideration (whether by remuneration or otherwise), given that Maitreya Mandala was a Huber controlled entity. This was an internal transfer between Huber controlled entities. But save as regarding issue two, little follows for the purpose of assessing quantum. Ms Hennessy did not rely in her calculation of profit on the transfer of 3,000,000 shares from Blue Delorite to Maitreya Mandala as a purchase of shares by a Huber controlled entity from a third party, nor as a sale by a Huber controlled entity to a third party. Further, Maitreya Mandala purchased more shares from third parties than it sold to third parties. Save for the transfer identified in issue two, Mr Huber has not established that any of the sales by Maitreya Mandala to third parties were sales of those same 3,000,000 shares.

76 Accordingly, even if Mr Huber’s contention were to be accepted, only around 17,300,000 shares would need to be removed from the Scheme for the purposes of calculating profit.

Issue two

77 CellOS has now accepted that 1,100,000 of the 1,500,000 shares transferred by Maitreya Mandala to Woon Shung Toon on 10 October 2012 are traceable to the 3,000,000 shares transferred from Blue Delorite on 10 September 2012, discussed immediately above. But CellOS does not accept that the balance of 400,000 shares were traceable to Mr Huber’s shares.

78 The share transaction statement for Maitreya Mandala shows that the only other CellOS shares acquired by Maitreya Mandala prior to that transfer were 400,000 shares from Mark and Sandra Evers (in one tranche of 300,000, and another of 100,000) on 10 September 2012. Now at the trial on liability, although Mr Huber denied knowledge of Maitreya Mandala’s purchases from the Evers, I found that he knew the Evers. Further, Mr Huber signed the Maitreya Mandala share transaction statement showing the transfer from them. In my view Maitreya Mandala’s purchase of shares from the Evers was part of the Scheme.

Issue three

79 Mr Huber says that he should be permitted an allowance for these 12,700,000 shares, as they are traceable to the 20,800,000 shares. CellOS submits that no allowance should be permitted for these shares. I accept the position advanced by CellOS on this aspect.

80 First, as set out earlier in relation to issue one, save for the 3,000,000 shares transferred to Maitreya Mandala, the 20,800,000 shares were not Mr Huber’s personal shares.

81 Second, as also set out earlier, at least 4,500,000 of the 20,800,000 shares were transferred to Mr Narulla and others as consideration for services rendered. Once it is accepted that these shares were transferred for consideration, it is appropriate that they be included in Ms Hennessy’s analysis as purchases by Huber controlled entities from third parties. But even if they were not to be so included, ascribing a consideration for them is in Mr Huber’s favour. It increases the cost base in Ms Hennessy’s profit calculation.

82 Third, Ms Hennessy identified that proceeds of AU$335,586 were received into CellOS from Mr Narulla between 18 December 2012 to 25 February 2013, around the dates that shares were transferred to Mr Narulla by Blue Delorite. As CellOS correctly submits, to the extent that these payments are traceable or attributable to these share transfers, then they provide further evidence that these share transfers were for consideration. Mr Huber has received a credit for these payments in Ms Hennessy’s calculations of profit.

83 Fourth, Ms Hennessy was unable to trace any shares that entered the Scheme from Mr Narulla and others through the Scheme to any sales of CellOS shares by Huber controlled entities.

84 In my view Mr Huber bears the onus of disentangling any profits obtained from his property from the profits obtained by reason of his fiduciary breaches. Accordingly, even if the 20,800,000 shares were transferred to Mr Narulla and others to hold on Mr Huber’s behalf, he has failed to prove that any of his shares, save for CellOS’ concession as to 1,100,000 of these shares, were sold as part of the Scheme and erroneously included in Ms Hennessy’s assessment of profit.

85 Let me now say something about issues six and seven being the shares allegedly sold by Mr Narulla and Mr Min Wee without Mr Huber’s knowledge.

Issue six

86 I agree with CellOS that no allowance should be permitted for these shares.

87 First, the transfers were not from “Narulla companies”. Rather, such transfers were all from the following entities which I found were Huber controlled entities:

(a) Gambier: 2,591,500 shares to Seah Chye Tin from 7 October 2013 to 18 July 2014;

(b) Maitreya Mandala: 110,000 shares to Seah Chye Tin 5 from March 2013 to 18 March 2013, and 200,000 shares to Melvin Tan on 20 March 2014;

(c) Marsh Commercial: 3,264,000 to Seah Chye Tin from 20 August 2013 to 26 June 2014, and 100,000 shares to Melvin Tan on 30 August 2013;

(d) Nesterland: 499,000 shares to Seah Chye Tin from 10 January 2013 to 5 December 2013; and

(e) Rex Investors: 492 shares to Seah Chye Tin from 25 November 2013 to 17 March 2014, and 715,000 shares to Melvin Tan on 7 July 2014.

88 Second, these transfers were not made for nil consideration. I found that they were sales.

89 Third, at the trial on liability Mr Huber said that these sales were made without his knowledge. Now whilst I was prepared to accept that there were some dealings engaged in by Mr Narulla which were unknown to Mr Huber, I rejected the contention for the most part. Relevantly, I also found that after January 2013 Mr Huber was personally signing letters to Computershare approving transactions from or to Maitreya Mandala, Nesterland and Rex Investors.

90 Fourth, irrespective of whether Mr Huber knew about the transactions, he profited from the transactions. Generally speaking, Mr Huber used the profits of the Scheme to fund CellOS through the LGA loan and the Pized loan. He also used such profits in connection with the discharge of his bankruptcy, paying other personal expenses, and in the purchase of properties in Melbourne and Dubai. I found that the proceeds of share sales were paid into Nesterland’s bank account, and Mr Huber’s personal expenses were paid out of the Nesterland bank account.

91 Fifth, in any event and for the most part, Mr Narulla and Mr Min Wee were acting as Mr Huber’s agents. Mr Huber is thereby not only bound by the acts of his agents, but is estopped from denying them.

Issue seven

92 No allowance should be made for these transfers for the reasons given regarding issue six.

93 Further, the only evidence relied upon by Mr Huber to establish that Haskins Corporation and Tsibello Pte Ltd were “Narulla companies”, and Access Asia Management Inc a “Min Wee Company”, is the email and schedules appearing in the second Huber affidavit. But I have not admitted these documents into evidence. Mr Huber conceded at the first day of trial on quantum that he had a copy of these documents at the trial on liability, but decided not to deploy them. Moreover, he now seeks to deploy the documents to undermine my findings in respect of those matters. Further, the documents, at least to the extent and in the manner relied upon by Mr Huber, comprise inadmissible hearsay. But in any event, even if I were to admit the documents, the content of the documents is so ambiguous and uncertain that they do not establish that Haskins Corporation and Tsibello Pte Ltd are “Narulla companies”, or that Access Asia Management Inc is a “Min Wee company”.

94 At this point it is convenient to say something more on the evidence. As I have said, at this second stage the parties sought to rely upon further evidence as I have described earlier. They also relied on a Schedule of Additional Documents. Given that CellOS does not object to the tender of the further documents, not otherwise tendered, listed in Part A of the Schedule of Additional Documents, being documents Mr Huber sought to rely upon, I will accept and treat them as having been tendered. Further, CellOS has also sought to tender the documents, not otherwise tendered, listed in Part B of the Schedule of Additional Documents. Documents 1, 2, and 5 to 9 in Part B are documents which were before me at the trial on liability in the court book but which were not tendered. These are the certificates issued by LGA to CellOS under the LGA loan quantifying the total outstanding debt and exercising the option over that total amount. These documents were relied upon by CellOS to support its submission that the whole of the LGA loan was converted to shares, and none remains on CellOS’ books. Documents 13 to 16 in Part B are documents provided to Ms Hennessy for the purpose of her preparing the supplementary Hennessy report, in order to undertake the tracing exercise. Given that Mr Huber has not objected to this material, I will accept such documents and treat them as tendered.

The new quantification

95 After the hearing on quantum and other relief, Ms Hennessy prepared a supplementary report which has calculated the profit made by Mr Huber and the Huber controlled entities, allowing for these concessions. She has calculated the profit as between AU$44,663,904 and AU$106,896,164.

96 CellOS submits that Mr Huber has failed to demonstrate that Ms Hennessy’s calculations of profit should be reduced beyond the concessions that I have described above. Further, in considering issues one to three and six and seven, CellOS says that I should resolve any doubtful questions against Mr Huber. I agree.

97 Further, CellOS asked Ms Hennessy to remove from her calculation of profit any of the 20,800,000 shares, being those identified by Mr Huber as his shares. Ms Hennessy was unable to trace any of these shares through the Scheme. But in any event, for illustrative purposes, she carried out a calculation on the basis that 17,309,468 shares were traceable into the Scheme, reflecting that Mr Huber had conceded that 2,500,000 of the 20,800,000 shares were not transferred to Mr Narulla on trust for him and that CellOS had already conceded 1,100,000 of the 20,800,000 shares in issue two. She calculated the profit from the Scheme absent those shares as between AU$9,923,802 and AU$50,034,562.

98 Further, CellOS asked Ms Hennessy whether the proceeds from the sale of any of the 20,800,000 shares, being those identified by Mr Huber as his shares, could be traced into either the LGA loan or the Pized loan. Ms Hennessy expressed the view that none of the proceeds from the sale of those shares could be traced into either loan.

99 But more generally, I accept though that on any view, the funds going into CellOS as part of the LGA loan and the Pized loan can be treated as funds derived from the Scheme, even if not sourced to these 20,800,000 shares specifically.

100 Let me go into more detail concerning the supplementary Hennessy report. The supplementary Hennessy report set out Ms Hennessy’s opinion as to:

(a) The total profit and loss made by the respondents from the Scheme if:

(i) certain shares did not form part of the Scheme (see appendix one to her 6 November 2019 instructions) (the first category of shares); and

(ii) certain payments were treated as a “cash inflow” for the purposes of her calculation of loss and “funds advanced to CellOS via loans” for the purposes of her calculation of profit; CellOS accepted that Mr Huber was entitled to a credit for these amounts.

(b) The total profit and loss made by the respondents from the Scheme if the following were excluded from her calculations:

(i) the first category of shares (save for line item 5 of appendix one, except to the extent it comprises any of the second category of shares as identified in appendix two of her instructions); and

(ii) the second category of shares excluding the reimbursement shares (as identified in appendix three of her instructions); the second category of shares encompasses shares transferred by him and Blue Delorite to certain recipients and covers substantially the 20,800,000 shares that I have discussed earlier.

101 In her opinion, the estimated total profit made by the respondents from the Scheme was AU$44,663,904 to AU$106,896,164 when:

(a) the first category of shares were excluded from the Scheme; and

(b) the payments set out in [100(a)(ii)] were treated as a “cash inflow” for the purposes of her calculation of loss and “funds advanced to CellOS via loans” for the purposes of her calculation of profit.

102 The estimated profits made by the respondents from the Scheme after excluding the first category of shares and including the additional moneys advanced by Mr Huber were summarised by Ms Hennessy as follows:

103 Ms Hennessy also calculated interest. But as I will explain later, I do not propose to award interest on this basis.

104 In the further Hennessy report, Ms Hennessy estimated the profits made by the respondents from the Scheme to be AU$52,515,488 to AU$114,196,498.

105 But the exclusion of the first category of shares reduced the amount of shares purchased by Huber controlled entities from third parties and reduced the amount of shares sold by Huber controlled entities to third parties. Reducing the amount of shares involved in the Scheme had the impact of reducing the estimated total profit made by the respondents.

106 Further, the inclusion of the payments which CellOS conceded were received from Mr Huber as referred to in [100(a)(ii)] also had the impact of reducing the amount of the respondents’ profits.

107 Ms Hennessy also gave up to date loss calculations. But as I propose to order an account of profits I do not need to set out any updated loss calculations. In any event, the order of magnitude thereof is comparable.

108 Further, Ms Hennessy was instructed to provide her opinion as to the estimated total profit made by the respondents from the Scheme if the additional moneys advanced by Mr Huber were included and the following were excluded from the calculations:

(a) the first category of shares; and

(b) the second category of shares excluding the reimbursement shares.

109 In order to exclude the second category of shares from the estimated total profit made by the respondents from the Scheme, Ms Hennessy needed to be able to trace the second category of shares through the Scheme to determine which Huber controlled entities purchased the shares and in what quantities, and which Huber controlled entities ultimately sold the shares to third parties and in what quantities.

110 The second category of shares totalled 20,849,978. Ms Hennessy was instructed to exclude the reimbursement shares which total 2,437,510. Further, she was instructed to exclude any overlap between the first category of shares and the second category of shares, of which she identified an overlap of 1,100,000. After excluding these categories of shares, the remaining shares in the second category of shares totalled 17,309,468.

111 But based on the available information she was unable to trace the remaining shares of 17,309,468 from the second category of shares through the Scheme.

112 Given that she was unable to trace the second category of shares through the Scheme, she was unable to determine the impact that the second category of shares would have on her assessment of the estimated total profit made by the respondents from the Scheme. Therefore, she could not exclude the shares from the Scheme transactions upon which her assessment of the respondents’ profits was based if she could not identify them in the Scheme transactions.

113 But to assist me, she prepared illustrative calculations to demonstrate the impact on her estimated profit calculations if all 17,309,468 remaining shares were excluded.

114 The illustrative calculations of the estimated total profit made by the respondents from the Scheme including the additional funds advanced by Mr Huber and excluding the first category of shares and the second category of shares was between AU$9,923,802 to AU$50,034,562 as summarised by her as follows:

115 She also calculated interest. But as I say, I do not propose to use her interest calculations.

116 Ms Hennessy again also detailed various loss calculations, but I do not need to include these.

Traceable payments

117 Ms Hennessy was instructed to consider whether and to what extent the proceeds from the sale of any of the shares referred to below were traceable to payments made to CellOS and attributed to the LGA loan and Pized loan:

(a) the first category of shares (save for line item 5 of appendix one, except to the extent it comprised any of the second category of shares); and

(b) the second category of shares excluding the reimbursement shares.

118 Ms Hennessy attempted to trace the proceeds using two methodologies. First, she started with the shares in the first category of shares and second category of shares and attempted to trace any share sale proceeds forward through the Scheme. Second, she started with the loan proceeds attributed to the LGA loan and Pized loan and attempted to trace the proceeds back through the Scheme to the shares in the first category of shares and second category of shares.

119 But because of the tracing difficulties that she encountered, she was unable to specifically identify whether any of the proceeds from the sale of either of the first category of shares or second category of shares were traceable to the proceeds received by CellOS from the LGA loan or Pized loan.

120 But notwithstanding these difficulties, I am satisfied that the source of the moneys advanced under the LGA loan and the Pized loan were profits from the Scheme.

Other matters

121 I have considered Mr Huber’s further written submissions and attached materials (some 54 pages) filed on 23 December 2019, which he was given leave to file so that he could respond to the supplementary Hennessy report. Let me make the following points.

122 First, Mr Huber requested that I re-open and review my main findings in my principal reasons. I reject that request. There is no substance to it. Mr Huber has any relevant appeal rights.

123 Second, Mr Huber asserted that he made losses on the LGA and Pized loans. He has also asserted that he made no profit from the secret trading of others. Now I have looked at appendix one to his submissions of some 20 pages which seems to be a cobbled together version of bits and pieces which constitute in a sense Mr Huber’s case thesis that I largely rejected at the trial on liability. Moreover, I found that the proceeds of the Scheme were used to provide the funds that were then advanced as part of the LGA loan and the Pized loan. I do not accept any of his analysis including assertions about losses at the relevant time. Moreover, his detailed analysis in appendix one seems more focused, in the case of LGA, on shares in and out, and shares “owed” to him by CellOS (see p 28). But none of this is to deny the appropriateness of the profit calculations or methodology used by Ms Hennessy flowing from the Scheme. Further, as to his assertion that he is down 705,000 shares concerning Pized, again this does not take him anywhere. The fact is that the proceeds of the Scheme were used to fund the Pized loan.

124 I should say that I do accept that there may be losses now in terms of the value of the shares currently held by the Huber controlled entities. But of course for an account of profits, one is looking at the profits made from and at the time of the breaches of fiduciary duty.

125 Third, what has been asserted by Mr Huber from [5] to [13] of his latest submissions is a composite of a stream of consciousness and wishful thinking. The opportunity given to Mr Huber was to respond to the supplementary Hennessy report in terms of its up to date calculations flowing from the hearing on quantum. It was not an opportunity for Mr Huber to have another go as to how he would have wished the trial on liability to have proceeded and been determined.

126 Fourth, I have considered the miscellany of points at [14] to [25] of his latest submissions. To the extent, which are few in number, that they engage with Ms Hennessy’s analysis they are unconvincing. Nevertheless I am going to discount Ms Hennessy’s overall figures in order to cover any contingencies or points that I might have overlooked. Further, to the extent that these points seek to re-open my liability findings, I reject them.

127 Fifth, Mr Huber has made submissions on topics such as “Alleged leakage” (including appendix three) and “Secret Share Trading” (including appendix four), but again much of this seems to engage more with my liability findings and not with the supplementary Hennessy report although there are some rare exceptions (see for example [111] on p 53). The same can be said for matters concerning Mr Patel (appendix two). In this context, I have also considered the summary of points at [19] to [25], [41] to [43], [44] to [46] and [47] to [53], but the same points can be made.

128 Let me now address two final topics concerning the status of the Pized loan and the status of the LGA loan.

The Pized loan

129 I found that the payments into CellOS attributable to the Pized loan were derived from the sale of shares in CellOS as a result of the Scheme.

130 Further, Ms Hennessy confirms that she was unable to trace any of the funds paid to CellOS and attributed to the Pized loan to the share transfers CellOS has conceded in favour of Mr Huber or the 20,800,000 shares referred to by Mr Huber. As noted above, Mr Huber bears the onus of disentangling any profits obtained from his property from the profits obtained by reason of his fiduciary breaches. He has failed to do so.

131 In my view, the funds paid to CellOS and attributed to the Pized loan comprise profit derived in breach of Mr Huber’s fiduciary duty, which was at all times until its receipt by CellOS impressed with a constructive trust in favour of CellOS. Thus, the payments to CellOS did not give rise to a liability to Pized, or anyone else, despite what is recorded in CellOS’ financial records. None of the funds traceable to the Pized loans are traceable to any of the share transfers conceded by CellOS or the 20,800,000 shares. It follows that CellOS is not indebted, and does not have any liability, to Pized in respect of the Pized loan.

LGA loan

132 CellOS accepts that SG$2,098,000 of net payments made by Mr Huber to CellOS in the period 3 August 2012 to 4 March 2013 were not identified in the initial Hennessy report or the further Hennessy report. Mr Huber contends that these payments were part of the LGA loan. But in my view, any amount owing to LGA in respect of these amounts has been satisfied by the conversion of the debt to equity conversion option under the LGA loan agreement.

133 The LGA loan agreement provided the following. First, LGA could at any time before 31 December 2013, at its election and in its absolute discretion, exercise an option to convert any part or all of the “Outstanding Loan” into equity in CellOS. Second, should LGA so elect to exercise that option it would give written notice to CellOS of the “Option Amount”, supported by a certificate showing the then “Outstanding Loan”. “Outstanding Loan” meant the amount certified by LGA to be outstanding at any time, under a certificate signed by its officer, which would be conclusive evidence of the same. Moreover, “Option Amount” meant the amount of the “Outstanding Loan” that LGA elected to convert into equity in CellOS pursuant to any exercise of the option.

134 On 27 June 2013, and after each of the relevant payments were made, Mr Narulla sent an email to Mr Mark Rodrigues of CellOS, the text of which is set out in my principal reasons (at [259]), but the relevant extracts of which are repeated again for ease of reference:

Heads up:

All the funds that have been loaned to Indoaust over the past couple of years to keep the business funded will be converted on Friday 28 June 2013 into shares.

Mei Lan is finalising the amount of the loan (she’s using SGD for this). It will be about SGD 12 million.

The Option Price is SGD 1.80 per share. The amount of shares will be determined once Mei Lan finalises the amount...

135 On 28 June 2013, LGA gave notice under the LGA loan agreement that it wished to exercise the option to convert “the presently Outstanding Loan … into fully paid ordinary shares ...” of CellOS. The notice was accompanied by a certificate, as required, certifying that the “Outstanding Loan” as at 28 June 2013 was SG$11,676,791.

136 In the audited financial accounts for the financial year ended 30 June 2013 signed by Mr Huber, the auditors noted this conversion event. Accordingly, they did not record any liability outstanding in respect of the LGA loan as at 30 June 2013. Contrastingly, the amount of the Pized loan was recorded as outstanding at the end of the 2015 and 2016 financial years.

137 I note that a further five conversion notices were issued by LGA under the LGA loan agreement in similar terms, each effecting a conversion of the total “Outstanding Loan” owing to LGA at each relevant date into shares in CellOS.

138 In summary, any liability owing by CellOS to LGA in relation to the relevant payments was converted to equity each time, with the outstanding loan balance of the LGA loan reduced to nil on each occasion. Mr Huber’s submissions on this aspect do not take him anywhere.

Conclusion

139 I accept Ms Hennessy’s methodology in the supplementary Hennessy report. Accordingly I will order an account of profits based upon her low scenario estimate of AU$44,663,904. I will further discount this for contingencies giving a figure of AU$42,000,000.

140 Mr Huber has failed to discharge his onus of establishing that it would be inequitable to order him to account for the entirety of the profit made by him and the Huber controlled entities as a result of his fiduciary breaches.

141 Let me make some final observations.

142 First, at this stage I have not allowed for any interest component. I have not awarded equitable compensation and so one dimension for any loss of use claim simply does not arise. As to the other dimension concerning the respondents’ use of any of the profits received from the Scheme, I am not satisfied that I should add any use component, particularly in light of subsequent events concerning CellOS’ share price.

143 Second, as the shares held by the Huber controlled entities were sourced from the operation of the Scheme and its profits, it is appropriate that I declare that such shares be held on a constructive trust in favour of CellOS.

144 Third, even if I had accepted Mr Huber’s submissions concerning a substantial proportion of the relevant 20,800,000 shares, nevertheless one could still justify an account applying to a quantum in the order of AU$42,000,000. I say that because on one view I could have taken the mid scenario used by Ms Hennessy and her illustrative calculations excluding both the first category of shares and the second category of shares which would have given a figure of AU$44,431,616. Now I accept that I have chosen the low scenario generally as a conservative measure in favour of Mr Huber. But another equally open choice would have been for me to have taken the mid scenario. There is imprecision, of course, in this whole exercise. But overall I am satisfied that AU$42,000,000 is the appropriate figure with no interest. Moreover, as participants, the Huber controlled entities should also be jointly and severally liable with Mr Huber for accounting for such an amount.

145 Fourth, as the moneys used to advance the Pized loan were sourced from the implementation of the Scheme, it is appropriate to declare that CellOS has no outstanding indebtedness to Pized. What CellOS is purported to owe is in substance owed to itself. Any such loan should be expunged from CellOS’ balance sheet and past balance sheets reconstructed with such a purported loan removed. The tenth declaration that I propose to make, followed through to its logical consequence, should achieve this result.

146 Finally, I appreciate Mr Huber’s intuitive thought that he has not made any profit, but rather suffered significant losses. But such a perspective is partly informed by what happened to the share price of CellOS well after the relevant events. That hindsight analysis does not deny that at the time of the breaches of fiduciary duty, significant profits were made for which there should be an accounting. But as I say, I have not awarded interest.

147 I will make declarations and orders to reflect these reasons.

I certify that the preceding one hundred and forty-seven (147) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Beach. |

Associate:

VID 951 of 2015 | |

REX INVESTORS LTD | |

Fifth Respondent: | SUN WAY GLOBAL GROUP LIMITED |

Sixth Respondent: | AURA FINANCE LIMITED |

Seventh Respondent: | HARVEST SKY HOLDINGS LIMITED |

Eighth Respondent: | RICH MAX INVESTMENTS LIMITED |

Ninth Respondent: | NESTERLAND SERVICES LTD |

Tenth Respondent: | WILLOW FINANCIAL LTD |

Eleventh Respondent: | LIGHTHOUSE INVESTMENTS LTD |

Twelfth Respondent: | LEARIO OVERSEAS CORP |

Thirteenth Respondent: | STARDUST FINANCIAL CORP |

Fourteenth Respondent: | PIZED MANAGEMENT LTD |

Fifteenth Respondent: | BLUE DELORITE PTY LTD ACN 116 976 151 |

Seventeenth Respondent: | CONSTANCE EMILY PECK |

Eighteenth Respondent: | ALAN PECK |

Nineteenth Respondent: | MELVIN TAN |