FEDERAL COURT OF AUSTRALIA

Hutson (liquidator), in the matter of WDS Limited (in liq) (Receivers and Managers Appointed) [2020] FCA 299

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. Pursuant to s 90-15 of Sch 2 to the Corporations Act 2001 (Cth) (Act), being the Insolvency Practice Schedule (Corporations) (IPSC), on the condition that the joint and several receivers and managers of the property of the WDS Group transfer into the control of the first plaintiffs the assets held by them in the name of WDS Limited (Surplus), the first plaintiffs are justified in distributing the Surplus based upon the divisional asset allocation approach as described in paragraphs 96-98 of the affidavit of Robert William Hutson sworn on 18 July 2019.

2. Pursuant to s 579E(1) of the Act the second plaintiffs are a pooled group for the purposes of s 579E(1) of the Act.

3. Each first plaintiff (acting jointly or severally) has liberty to restore on two days’ notice.

4. Pursuant to s 43(3)(d) of the Federal Court of Australia Act 1976 (Cth) and s 90-15(3)(d) of the IPSC, the Commonwealth’s costs of and incidental to this proceeding be fixed at $50,768.41 and be paid out of the property of the second plaintiffs prior to the distribution of the property by the first plaintiffs.

5. Further to Order 4 of these Orders, the costs of this proceeding be costs in the windings up of the second plaintiffs.

THE COURT DIRECTS THAT:

6. Pursuant to s 579G(1)(e) of the Act:

(a) the first plaintiffs are justified in opening a new bank account to be treated by them as an “administration account” for the purposes of s 65-10 of the IPSC (New Account);

(b) the first plaintiffs are justified, upon receipt of the Surplus, in depositing the Surplus to the New Account; and

(c) the first plaintiffs are justified in undertaking all administrative steps necessary to give effect to Orders 6(a) and 6(b) of these Orders, including, but not limited to closing the existing bank accounts separately maintained and operated by the first plaintiffs for the second plaintiffs (Existing Accounts) and transferring the closing balances of the Existing Accounts to the New Account.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

Schedule

No: NSD 1160 of 2019

Federal Court of Australia

District Registry: New South Wales

Division: General

Name | ACN | |

1 | WDS (Mining) Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 113 284 263 |

2 | WDS (Energy & Infrastructure) Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 093 994 980 |

3 | WDS (Mining Engineering) Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 121 947 920 |

4 | Workforce Diversified Services Pty Ltd (in liquidation)(Receivers and Managers Appointed) | 121 947 911 |

5 | WDS (Engineering) Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 010 852 258 |

6 | WDS (Corporate) Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 121 715 482 |

7 | Advent Asia Pacific Pty Limited (in liquidation) (Receivers and Managers Appointed) | 127 536 921 |

8 | MacCormick Civil & Tunnelling Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 127 072 137 |

9 | Ackroyd Engineering Services Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 076 857 933 |

10 | WDS (Oil & Gas) Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 129 452 893 |

11 | WDS (Titeline) Pty Ltd (in liquidation) (Receivers and Managers Appointed) | 125 245 212 |

MARKOVIC J:

1 This is an application made under s 90-15 to Sch 2 to the Corporations Act 2001 (Cth) (Act), being the Insolvency Practice Schedule (Corporations) (IPSC), for a judicial direction and s 579E of the Act for a pooling order.

2 Robert Hutson, Martin Madden and Cassandra Mathews in their capacity as liquidators of WDS Limited (In Liquidation)(Receivers and Managers Appointed) (WDS) and, as applicable, as liquidators of 11 other named companies, each of which is a wholly owned subsidiary of WDS Limited (each a WDS Subsidiary and collectively the WDS Subsidiaries), are named as first plaintiffs (Liquidators) and WDS and the WDS Subsidiaries are named as second plaintiffs.

3 The orders sought by the plaintiffs in their amended originating process (Amended Application) relevantly include:

1 On the condition that the joint and several receivers and managers of the property of the WDS Group (Receivers) transfer into the control of the First Plaintiffs the assets held by them in the name of WDS Limited by 20 December 2019 (the Surplus), an order pursuant to section 90-15 of the IPSC that the First Plaintiffs are justified in distributing that Surplus based upon the divisional asset allocation approach as described in paragraphs 96-98 of the affidavit of Robert William Hutson dated 18 July 2019.

2 Further, or in the alternative, an order pursuant to section 579E(1) of the Act that the Second Plaintiffs are a pooled group for the purposes of section 579E(1) of the Act.

3 Orders pursuant to section 90-15 of the IPSC that:

a. Mr Martin Madden ceases to be a liquidator of each of the Second Plaintiffs;

b. Mr Robert Hutson be appointed as a joint and several liquidator of each of the companies named in the schedule (each being a wholly-owned subsidiary of WDS Limited (In Liquidation)(Receivers and Managers Appointed));

c. Ms Cassandra Mathews be removed as a liquidator of each of the Second Plaintiffs;

d. Mr Rahul Goyal be appointed as a joint and several liquidator of each of the Second Plaintiffs.

4. The costs of these proceedings be costs in the windings up of the Second Plaintiffs.

(Strikethrough and underlining omitted.)

4 On 25 October 2019 I granted leave to the Commonwealth of Australia (Commonwealth) pursuant to r 2.13 of the Federal Court (Corporations) Rules 2000 (Cth) to be heard on the application without becoming a party to the proceeding. On that day, upon being satisfied that it was appropriate to do so, I also made an order nunc pro tunc appointing Mr Hutson as a liquidator of each of the WDS Subsidiaries.

5 On 4 December 2019 I made orders removing Mr Madden and Ms Mathews as liquidators of each of WDS and the WDS Subsidiaries and appointed Rahul Goyal as joint and several liquidator of each of those companies.

Background

6 The following background facts are taken from a statement of facts provided by the plaintiffs, which was not contested by the Commonwealth, and the evidence relied on by the plaintiffs and the Commonwealth.

WDS and the WDS Subsidiaries

7 WDS was a public company listed on the Australian Securities Exchange (ASX).

8 WDS and the WDS Subsidiaries (together, the WDS Group) traded as a single entity and structured their operations between three principal divisions as follows:

(1) mining, which supplied skilled labour and specialist mining equipment to the underground mining industry;

(2) energy, which provided specialist design, construction and maintenance services in the oil, gas and water sectors; and

(3) corporate, which provided business support services to the mining and energy divisions.

9 WDS and the WDS Subsidiaries were centrally managed by WDS’s board and senior management team. Their administrative and financial reporting functions were also centrally managed.

10 In the circumstances described at [20]-[29] below, on 2 September 2015 the Liquidators were appointed as administrators (Administration Date) of WDS and, as applicable, the WDS Subsidiaries. As at that date:

(1) WDS and six of the WDS Subsidiaries, WDS (Mining) Pty Ltd, WDS (Energy & Infrastructure) Pty Ltd, Workforce Diversified Services Pty Ltd, WDS (Corporate) Pty Ltd, Ackroyd Engineering Services Pty Ltd (Ackroyd) and WDS (Titeline) Pty Ltd, were employing entities within the WDS Group (Employing Entities); and

(2) the WDS Group employed approximately 500 people.

11 On or about 30 May 2007 WDS and some of the WDS Subsidiaries entered into an Australian Securities and Investments Commission (ASIC) standard form deed of cross guarantee (Deed of Cross Guarantee). By the Deed of Cross Guarantee:

(1) each “Group Entity” covenanted with the “Trustee” for the benefit of each “Creditor” that the “Group Entity” guaranteed to each “Creditor” payment in full of any “Debt” in accordance with the Deed of Cross Guarantee;

(2) each “Group Entity” agreed with the “Trustee” that the Deed of Cross Guarantee would become enforceable in respect of a “Debt” of a “Group Entity” upon its winding up; and

(3) as a separate covenant by way of Deed Poll, each “Group Entity” agreed with each “Creditor” that the “Group Entity” would guarantee to each “Creditor” payment of any “Debt” due to the “Creditor” from any “Group Entity” in accordance with the Deed of Cross Guarantee.

12 Relevantly, the Deed of Cross Guarantee included the following definitions:

(1) “Group Entity” was defined to mean any one of the entities listed in Part 1 of the Schedule to the Deed of Cross Guarantee (Schedule) and any entity joined to the Deed of Cross Guarantee by the execution of an Assumption Deed;

(2) “Trustee” was named in Part 2 of the Schedule as I.T. Engineering (Qld) Pty Ltd;

(3) “Creditor” was defined to mean a person “who is not a Group Entity and to whom now or at any future time a Debt (whether now existing or not) is or may at any future time be or become payable”; and

(4) “Debt” was defined to mean “any debt or claim which is now or at any future time admissible to proof in the winding up of a Group Entity and no other claim”.

13 As at the Administration Date each WDS Subsidiary was party to the Deed of Cross Guarantee, either by signing or acceding to it.

14 On or about 31 May 2007 WDS lodged an application with ASIC for relief under ASIC Class Order 98/1418 “to enable grouping of the accounts for the subsidiaries in” the WDS Group. According to Mr Hutson the relief sought under the class order was granted and the WDS Subsidiaries were relieved from the requirement to prepare and lodge separate financial reports, directors’ reports and auditors’ reports for each entity in the WDS Group that was a party to the Deed of Cross Guarantee.

15 The WDS Group had two active bank accounts both of which were held by WDS with Australia and New Zealand Banking Group Limited. One of the accounts was used to collect receivables from customers of the WDS Group and the other account was the primary trading account of the WDS Group and appeared to have been used to pay employee payroll liabilities, vehicle and equipment lease payments, creditors, taxation payments and WorkCover payments. Despite attempts to do so, the Liquidators have been unable to locate any other accounts held by WDS or any other company in the WDS Group.

WDS Group’s reporting

16 WDS, as the holding company in the WDS Group, reported to the market on a consolidated basis.

17 The evidence before me establishes that:

(1) from at least 2008 the WDS Group prepared internal management accounting records on a consolidated basis;

(2) the consolidated financial statements of the WDS Group reported revenue, assets and liabilities by operating segment rather than by entity;

(3) according to Mr Hutson, based on the management accounts, transactions were categorised into the three divisions identified at [8] above which is consistent with the way the WDS Group reported on its revenue, primarily between the mining or energy divisions with ancillary allocation to the corporate support functions;

(4) from 2010 the WDS Group reported its revenue to its secured creditor Harrenvale Corporation (Australia) Pty Ltd (formerly GE Commercial Corporation (Australia) Pty Ltd) (GE) in financial reports which reconciled receipts and payments principally to its three divisions, namely mining, energy and corporate;

(5) from at least 1 July 2006 the WDS Group reported income to the Australian Taxation Office (ATO) as a tax consolidated group; and

(6) from around April 2008 each WDS entity was party to a tax funding agreement and tax sharing arrangement whereby each entity contributed to the income tax payable by the WDS Group in proportion to their contribution to the WDS Group’s taxable income and were entitled to refunds on the same basis.

The GE facility

18 On or about 29 April 2005 WDS and WDS (Mining) Pty Ltd entered into a secured debt facility with GE with a limit of $95 million (GE Facility). Each of the other WDS Subsidiaries acted as guarantors for the GE Facility.

19 As security for the GE Facility, WDS and each of the WDS Subsidiaries granted fixed and floating charges over all of their respective present and future assets and undertakings in favour of GE (each a GE Charge). Each GE Charge was executed by its respective chargor and lodged with ASIC. The registration of the GE Charges against WDS and each of the WDS Subsidiaries was transitioned to the Personal Property Securities Register on or about 30 January 2012.

Events leading to the administration and liquidation of the WDS Group

20 On or about 10 December 2013 WDS entered into a Major Works Construct Only Contract as contractor with Eagle Downs Coal Management Pty Ltd (EDCM) for the construction of specified works (EDCM Contract). Pursuant to the EDCM Contract:

(1) WDS was required to provide security to EDCM for 10% of the estimated contract sum;

(2) the security was required to be in the form of an unconditional and irrevocable undertaking given by an approved financial institution; and

(3) EDCM was entitled to convert the security into cash at any time and use the cash to pay for any costs, losses, expenses, or damages which it claimed it had incurred as a consequence of any act or omission or negligence or default of WDS.

21 On 22 January 2014, at the request of WDS, Assetinsure Pty Ltd (Assetinsure) as agent for Swiss Re International SE (Swiss Re) issued an unconditional undertaking to EDCM in the amount of $14,280,638 in respect of the EDCM Contract (Performance Bond).

22 On 7 August 2015 WDS announced to the ASX that on 30 July 2015 a “Friction Ignition” event had occurred on the Eagle Downs mine site and that “drift construction works” had been suspended.

23 On 11 August 2015 WDS notified GE and the ASX that it would breach its “fixed charge coverage ratio”. WDS’s announcement to the ASX also included the following:

WDS further advises that it has also now completed a major reforecast of both revenue and cost for the EDCM project, taking into account the production levels achieved to date and revised forecast rates of production to completion. This reforecast includes the delays caused by the recent “Friction Ignition” event. As a result WDS now expects to report, on 28 August 2015, a statutory NPAT loss for the year ended 30 June 2015 of $27-28 million, exceeding the guidance range of $14-15 million NPAT loss that was provided in June 2015.

The FY15 accounts included a write down of the energy sector goodwill due to a high level of uncertainty in securing contracts in line with the strategic plan.

24 On 24 August 2015 EDCM issued a demand to Assetinsure as agent of Swiss Re under the Performance Bond in the amount of $14,280,638 (EDCM Demand). The EDCM Demand gave rise to a corresponding obligation in WDS to indemnify Swiss Re in the amount the subject of the EDCM Demand.

25 On 25 August 2015 EDCM cashed the Performance Bond.

26 On 27 August 2015 WDS’s shares were suspended from trading on the ASX.

27 Between 25 August 2015 and 2 September 2015 WDS was in negotiations with GE, EDCM and Assetinsure on behalf of Swiss Re.

28 On 2 September 2015 Messrs Madden and Hutson and Ms Mathews were appointed as administrators of WDS and Mr Madden and Ms Mathews were appointed as administrators of the WDS Subsidiaries. WDS’s announcement to the ASX on that day includes:

… WDS Limited (ASX: WDS) Board announced that it has appointed Martin Madden, Cassandra Mathews and Robert Hutson of Korda Mentha as Voluntary Administrators to oversee the affairs of the WDS Group.

Further to our announcements of 25 and 27 August 2015, on the afternoon of 25 August 2015 the Company received advice that Eagle Downs Coal Management (EDCM) had cashed an insurance bond for $14.2m creating a new liability on the Company. This was a completely unexpected development and inconsistent with discussions that had been underway with EDCM about the future of the project.

…

Until today the Company, based on the information it had received and the progress with the negotiations that had occurred, believed that it would be able to continue to trade as a going concern and remain solvent.

Latest advice from the secured lender that it had decided against continuing to provide the Company with future drawdowns this week had diminished confidence that the Company’s obligations could be met. Coupled with the lack of viable and timely alternative funding, the Board is unable to reasonably form the view that the Company can remain solvent.

29 On 8 October 2015 the creditors of WDS resolved that it be wound up and that Messrs Madden and Hutson and Ms Mathews be appointed as liquidators. The creditors also resolved that the WDS Subsidiaries be wound up and that Mr Madden and Ms Mathews be appointed as their liquidators.

Appointment of receivers to the WDS Group

30 Following the appointment of administrators to the WDS Group, on 2 September 2015 GE appointed Quentin Olde and John Park of FTI Consulting as receivers and managers of WDS and the WDS Subsidiaries (Receivers).

31 Upon their appointment the Receivers assumed control of the WDS Group’s operations and assets, including all bank accounts, communicated with all stakeholders, including employees and major creditors, and undertook the task of realising all assets.

32 The sale of the WDS Group’s assets by the Receivers generated total realisations of $80,029,334.80 made up as follows:

(1) receivables from general debtors – $25,911,730.60;

(2) receivables associated with the “CPECC joint venture” – $20,602,722.80;

(3) payments associated with settlement with EDCM – $7,795,637.20;

(4) ATO refund – $5,095,176.60; and

(5) receipts from sales of fixed plant and equipment – $21,624,067.60.

33 As at 2 September 2015 the amount owing by WDS and the WDS Subsidiaries to GE was $43,909,324.60.

34 On or about 26 March 2018 the Receivers notified the Liquidators that they held a surplus fund of approximately $9.7 million (Surplus). The Receivers continue to hold the Surplus, the balance of which as at 30 September 2019 was $9,285,086.21. The Receivers have not retired and do not intend to do so until they are satisfied that no call will be made on their indemnity. Relevantly, a dispute has arisen between the Receivers and the Commonwealth which is described at [44] below.

35 The Liquidators expect to receive the Surplus after, or contemporaneously with, the Receivers’ retirement.

The ongoing liquidation of the WDS Group

36 The Liquidators have not had access to any live servers or information technology systems maintained and operated by the WDS Group. Thus the Liquidators’ review of the books and records kept by the WDS Group has been by way of an examination and search of a hard drive provided to the Liquidators by the Receivers in December 2018. The hard drive contains two terabytes of files relating to the affairs of the WDS Group.

37 Based on their searches the Liquidators have not located:

(1) any detailed asset register of the WDS Group’s plant and equipment that would enable them to determine with precision which company within the WDS Group was the legal owner of any particular asset;

(2) any contract, other than employment contracts, the Deed of Cross Guarantee and the GE Facility, with any WDS Subsidiary that would give rise to a trade liability as at the Administration Date. WDS was the primary legal counterparty to contracts by which the WDS Group generated revenue; or

(3) any financial statements prepared by any WDS Subsidiary which report revenue, assets or liabilities by entity.

38 The Liquidators have received, but not yet adjudicated on, proofs of debt for WDS and the WDS Subsidiaries. However, they believe that the total estimated debts for all companies in the WDS Group as at 30 April 2019 is $45,862,343 and of that amount the total estimated debts in respect of employee entitlements is $13,398,810.

The Commonwealth’s position

39 The Attorney-General’s Department (AGD) is currently responsible for the administration of the Fair Entitlements Guarantee Act 2012 (Cth) (FEG Act). Prior to 29 May 2019 the Department of Jobs and Small Business (Former Department) had that responsibility.

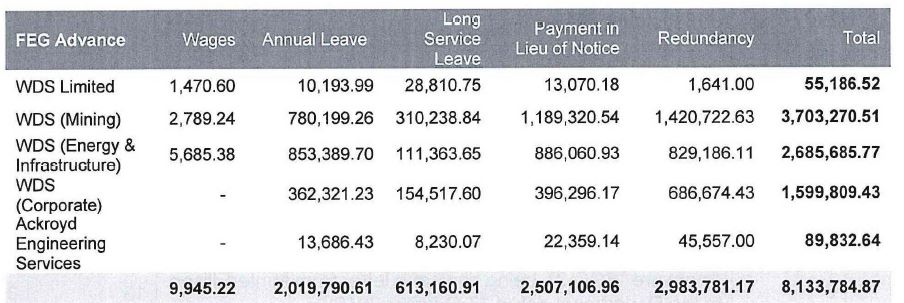

40 The Commonwealth has advanced $8,133,784.87 in employee entitlements to former employees of the WDS Group under the FEG Act made up as follows:

41 As explained by Benjamin Gregory Carmody, an acting senior executive lawyer and assistant secretary in the AGD, once the Commonwealth has advanced funds to eligible employees under the FEG Act it is subrogated to the position of those employees in, relevantly, the winding up to the extent of the advance.

42 A dispute has arisen between the Commonwealth and the Receivers about the Receivers’ obligations under s 433 of the Act. That section relevantly provides:

(2) This section applies where:

(a) a receiver is appointed on behalf of the holders of any debentures of a company or registered body that are secured by a circulating security interest, or possession is taken or control is assumed, by or on behalf of the holders of any debentures of a company or registered body, of any property comprised in or subject to a circulating security interest; and

(b) at the date of the appointment or of the taking of possession or assumption of control (in this section called the relevant date):

(i) the company or registered body has not commenced to be wound up voluntarily; and

(ii) the company or registered body has not been ordered to be wound up by the Court.

(3) In the case of a company, the receiver or other person taking possession or assuming control of property of the company must pay, out of the property coming into his, her or its hands, the following debts or amounts in priority to any claim for principal or interest in respect of the debentures:

(a) first, any amount that in a winding up is payable in priority to unsecured debts pursuant to section 562;

(b) next, if an auditor of the company had applied to ASIC under subsection 329(6) for consent to his, her or its resignation as auditor and ASIC had refused that consent before the relevant date—the reasonable fees and expenses of the auditor incurred during the period beginning on the day of the refusal and ending on the relevant date;

(c) subject to subsections (6) and (7), next, any debt or amount that in a winding up is payable in priority to other unsecured debts pursuant to paragraph 556(1)(e), (g) or (h) or section 560.

…

(5) The receiver or other person taking possession or assuming control of property must pay debts and amounts payable pursuant to paragraph (3)(c) or (4)(b) in the same order of priority as is prescribed by Division 6 of Part 5.6 in respect of those debts and amounts.

…

(9) For the purposes of this section, the references in Division 6 of Part 5.6 to the relevant date are to be read as references to the date of the appointment of the receiver, or of possession being taken or control being assumed, as the case may be.

43 As set out at [32] above, the Receivers collected and sold all of the WDS Group’s known assets and hold the proceeds of sale of those assets in an account opened in their name for the purposes of the receivership. According to Mr Hutson, based on his review, the Receivers’ records show that the Receivers treated all of the WDS Group’s assets as assets of WDS.

44 Mr Hutson has provided the following summary of the dispute, with which Mr Carmody agrees:

(1) Mr Hutson describes the position taken originally by the Former Department and I infer now by the AGD as follows:

a. certain assets realised by the Receivers comprised circulating assets; for example debtors, work in progress and stock;

b. there is no basis for the Receivers to draw an absolute conclusion that [WDS] owned all property of the WDS Group; and

c. where circulating assets owned by Employing Entities have been realised by the Receivers, they are required to pay priority employee entitlements out of those realisations prior to the repayment of the secured creditor’s debt.

(2) Mr Hutson summarises his understanding of the Receivers’ reasons for treating the WDS Group’s assets as those of WDS as follows:

a. the Receivers relied on the financial records of the WDS Group and statements by the Directors of the WDS Group as well as documentation of the WDS Group and the conduct of the WDS Group in matters such as its banking arrangements and contractual arrangements with customers of the WDS Group to form the view that all assets of the WDS Group were owned by [WDS];

b. the Receivers determined that where the books and records of the WDS Group did not identify the legal owner of the machinery and spare parts realised by the Receivers, and therefore that it was appropriate to proceed on that basis that these assets were assets of [WDS] which was the main trading entity of the WDS Group; and

c. that given the lack of financial or statutory accounts for each company in the WDS Group the Receivers consider their approach was not unreasonable.

45 The dispute between the Commonwealth and the Receivers is subject to a settlement, the terms of which are confidential but which, relevantly, is conditional upon the making of the pooling order sought in this application.

46 Mr Carmody explains that if a pooling order is not made then the arrangement between the Commonwealth and the Receivers will not take effect and the dispute about whether the Receivers have complied with s 433 of the Act will continue and may need to be resolved by litigation. There was evidence before me of the estimated cost of that litigation for all parties likely to be involved in it.

The Liquidators’ proposal as to the distribution of the Surplus and the effect of a pooling order

47 Based on their investigations into the affairs of the WDS Group the Liquidators found that:

(1) WDS was the entity that contracted with customers of the WDS Group and the principal entity that contracted with suppliers of the WDS Group;

(2) while they were able to identify some evidence of ownership of assets, including evidence that some assets may be owned by one or other of the WDS Subsidiaries, the position is not clear; and

(3) it is uncertain whether further investigation will result in reaching a definitive conclusion as to asset ownership.

48 Mr Hutson has considered the way in which to distribute the Surplus so that it will yield the best return for creditors as a whole while having regard to statutory priorities. In doing so, he has sought to understand the WDS Group’s divisional allocation of assets and liabilities prior to its insolvency with a view to understanding its pre-insolvency asset position. This required him to have regard to, among other things, the WDS Group’s management accounts, financial statements and the operation of the Deed of Cross Guarantee.

49 Mr Hutson’s evidence is that based on the work undertaken by him, the Liquidators are of the opinion that the Surplus should be distributed based on a divisional asset allocation within the WDS Group (Proposed Approach). The Liquidators are of the opinion that the Proposed Approach is consistent with the WDS Group’s management accounts and the reports as to affairs prepared by the directors of the WDS Group. In particular Mr Hutson, on behalf of the Liquidators, notes that:

(1) the segment reporting in the financial statements (applying International Financial Reporting Standards 8) is consistent with the divisional reporting of WDS;

(2) the operating segments were based on an aggregation of the operating assets and liabilities between two operating divisions, mining and energy; and

(3) the WDS Group did not itself separately report the asset and liability position of WDS as the parent entity or on a standalone basis.

50 Mr Hutson has had a summary of the estimated return to creditors prepared to illustrate how the Surplus may be allocated as a ratio based on the assets held in the mining, energy and corporate divisions. According to Mr Hutson, that analysis demonstrates that, after allocating the cash assets to WDS (based on the fact that WDS was the only entity in the WDS Group with a bank account as at the Administration Date) and excluding an initial allocation of funds for the Administrators’ fees and disbursements, the allocation of assets held in each of the relevant asset-holding entities immediately prior to the Administration Date was:

(1) WDS – 0.82%;

(2) WDS Corporate – 1.45%;

(3) WDS (Mining) – 51.29%; and

(4) WDS (Energy and Infrastructure) – 46.43%.

51 Mr Hutson has also had his staff undertake analyses of the returns from the Surplus to unsecured creditors based on different distributions of the WDS Group’s assets and liabilities. Those analyses are based on the following scenarios:

(1) scenario 1 is where all assets are allocated to WDS. Mr Hutson does not believe this is the most appropriate scenario because it is clear from WDS’s annual reports, interim financial reports, financial statements and management accounts that the WDS Group allocated revenue and liabilities to business centres formed within the mining and energy divisions of the WDS Group;

(2) scenario 2 models scenario 1 but adds in the cost of reconstruction of the books and records of each of WDS and the WDS Subsidiaries from the raw data used to generate the management accounts, estimated to be in excess of $1 million. For the same reasons as given in relation to scenario 1 Mr Hutson does not believe that this is the most appropriate scenario. In addition Mr Hutson does not think that the costs incurred to undertake a reconstruction of the books and records will ultimately benefit unsecured creditors as a whole (including priority creditors);

(3) scenario 3 is based on depreciation schedules and assumes they are a true reflection of the asset position of the WDS Group. Mr Hutson’s staff have not been able to locate any records based on which the depreciation schedules were calculated and he does not think that those schedules are the most reliable source of the WDS Group’s true asset position. They do not match the management accounts or the different corporate entities and refer only to fixed, and not intangible, assets;

(4) scenario 4 is modelled on the assumption that the assets sat in the Employing Entities in proportion to the number of employees in each entity. Mr Hutson says that he has seen no evidence in the WDS Group’s accounts to suggest that this was in fact how the assets were allocated and that it does not take account of assets other than machinery. Mr Hutson does not consider that this scenario reflects the reality of the WDS Group’s operations; and

(5) scenario 5 is modelled on a divisional asset allocation of the WDS Group’s assets and liabilities as recorded in the financial statements and management accounts. That is, it is modelled on the Proposed Approach. Mr Hutson is of the opinion that the WDS Group operated on a divisional basis and that this scenario is closest to the reality of the WDS Group’s operations.

52 According to Mr Hutson, the effect of applying the Proposed Approach without a pooling order would be that:

(1) the Commonwealth acting through the AGD as a priority creditor will receive a dividend of:

(a) 0c/dollar for claims made on WDS;

(b) 4.21c/dollar for claims made in respect of WDS (Corporate) Pty Ltd (being a company that falls within the corporate division);

(c) 100c/dollar for claims made in respect of WDS (Energy & Infrastructure) Pty Ltd (being a company that falls within the energy division);

(d) 65.23c/dollar for claims made in respect of WDS (Mining) Pty Ltd (being a company that falls within the mining division); and

(e) 0c/dollar for claims made on Ackroyd; and

(2) unsecured creditors will receive a dividend of 0.08c/dollar.

53 However, the Liquidators are of the opinion that a pooling order should be made because it is in the best interests of creditors of the WDS Group as a whole. In summary their reasons for reaching that conclusion are as follows:

(1) the books and records of the WDS Group demonstrate that the WDS Group was managed and traded as a single economic entity;

(2) the financial records of the WDS Group reveal that WDS used the WDS Subsidiaries to provide labour and services to it. The main source of revenue of the WDS Group, received by WDS, was from those services provided by the common pool of employees;

(3) the scenario 5 analysis, together with the pooling of the WDS Group, is an appropriate means to address the inequality that is caused to each of the Employing Entities that are liable for employee claims but did not benefit from the revenue actually generated by the employees. Allocating all of the Surplus to WDS does not reflect the actual asset position of the WDS Group prior to the Administration Date;

(4) each of the WDS Group’s companies’ affairs and books and records are intermingled and not easily separated. A pooling order would result in significant savings in time and costs associated with reconstruction of the WDS Group accounts and would enable the Liquidators to finalise the winding up of the WDS Group more efficiently;

(5) in the absence of a pooling order, there is unlikely to be sufficient funds in any of the liquidations of the WDS Subsidiaries to pay the costs of the winding up;

(6) some of the proceeds available for distribution arise from tax refunds received by WDS. Although WDS was the taxpayer, the refunds arise because of the collective trading effort of the whole of the WDS Group. Given the operation of the tax arrangements, any refund should be attributed across the WDS Group;

(7) if a pooling order is made, there will be no need to identify the owner of the machinery and spare parts sold by the Receivers, including obviating the need to reconstruct the books and records of the WDS Group;

(8) the cost of the Liquidators ascertaining the financial position of each company within the WDS Group (which may in any event not be possible from books and records) will be borne by the unsecured creditors as a whole; and

(9) a pooling order would avoid the administrative burden involved in conducting multiple liquidations, complying with statutory reporting requirements in respect of each company within the WDS Group and apportioning the Liquidators’ fees and expenses between them.

54 Mr Hutson further explains that based on his understanding of the WDS Group the effect of a pooling order would be that:

(1) all employee creditors of the WDS Group would receive 100c/dollar for all claims subject to s 556(1)(e) of the Act, being unpaid wages and superannuation contributions;

(2) all employee creditors of the WDS Group would receive 100c/dollar for all claims subject to s 556(1)(g) of the Act, being unpaid entitlements for annual leave, leave loading and long service leave;

(3) all employee creditors of the WDS Group would receive 28.32c/dollar for all claims subject to s 556(1)(h) of the Act, being unpaid entitlements for payments in lieu of notice and redundancy payments;

(4) non-employee trade creditors would receive 0c/dollar;

(5) the amounts advanced pursuant to the FEG Act and the unfunded employee entitlements would be reduced pari passu by the above payments in the order provided by the Act, by approximately $4.2 million for the amounts advanced pursuant to the FEG Act and $4.4 million for the unfunded employee entitlements;

(6) it is anticipated that the disagreement between the Receivers and the Commonwealth will be resolved without further delay;

(7) the Receivers will be able to transfer the Surplus and the Liquidators expect that the current available balance of the Surplus will be made available to creditors to be paid in accordance with the Liquidators’ current estimated returns;

(8) the Liquidators will be entitled to draw their remuneration and expenses, estimated in the amount of $509,766, plus any additional legal expenses from the Surplus. No remuneration has been drawn by the Liquidators since approximately November 2015, save for amounts advanced pursuant to the FEG Act in relation to the review conducted pursuant to that Act;

(9) the Liquidators will be able promptly to finalise the liquidation of the WDS Group, distribute a dividend to unsecured creditors and then attend to deregistering the entities in the WDS Group; and

(10) as already noted, a pooling order will avoid the administrative burden of conducting multiple liquidations and obviate the need for the Liquidators to reconstruct the books and records of the WDS Group, resulting in a saving of in excess of $1 million in their remuneration and expenses and making these funds available for distribution to creditors.

Legislative framework and relevant principles

Section 579E of the Act

55 Section 579E of the Act concerns pooling orders and relevantly provides:

Making of pooling order

(1) If it appears to the Court that the following conditions are satisfied in relation to a group of 2 or more companies:

(a) each company in the group is being wound up;

(b) any of the following subparagraphs applies:

(i) each company in the group is a related body corporate of each other company in the group;

(ii) apart from this section, the companies in the group are jointly liable for one or more debts or claims;

(iii) the companies in the group jointly own or operate particular property that is or was used, or for use, in connection with a business, a scheme, or an undertaking, carried on jointly by the companies in the group;

(iv) one or more companies in the group own particular property that is or was used, or for use, by any or all of the companies in the group in connection with a business, a scheme, or an undertaking, carried on jointly by the companies in the group;

the Court may, if the Court is satisfied that it is just and equitable to do so, by order, determine that the group is a pooled group for the purposes of this section.

Consequences of pooling order

(2) If a pooling order comes into force in relation to a group of 2 or more companies:

(a) each company in the group is taken to be jointly and severally liable for each debt payable by, and each claim against, each other company in the group; and

(b) each debt payable by a company or companies in the group to any other company or companies in the group is extinguished; and

(c) each claim that a company or companies in the group has against any other company or companies in the group is extinguished.

…

(10) The Court must not make a pooling order in relation to a group of 2 or more companies if:

(a) both:

(i) the Court is satisfied the order would materially disadvantage an eligible unsecured creditor of a company in the group; and

(ii) the eligible unsecured creditor has not consented to the making of the order; or

(b) all of the following conditions are satisfied:

(i) a company in the group is being wound up under a members’ voluntary winding up;

(ii) the Court is satisfied that the order would materially disadvantage a member of that company;

(iii) the member is not a company in the group;

(iv) the member has not consented to the making of the order.

(11) The Court may only make a pooling order on the application of the liquidator or liquidators of the companies in the group.

Just and equitable criteria

(12) In determining whether it is just and equitable to make a pooling order, the Court must have regard to all of the following matters:

(a) the extent to which:

(i) a company in the group; and

(ii) the officers or employees of a company in the group;

were involved in the management or operations of any of the other companies in the group;

(b) the conduct of:

(i) a company in the group; and

(ii) the officers or employees of a company in the group;

towards the creditors of any of the other companies in the group;

(c) the extent to which the circumstances that gave rise to the winding up of any of the companies in the group are directly or indirectly attributable to the acts or omissions of:

(i) any of the other companies in the group; or

(ii) the officers or employees of any of the other companies in the group;

(d) the extent to which the activities and business of the companies in the group have been intermingled;

(e) the extent to which creditors of any of the companies in the group may be advantaged or disadvantaged by the making of the order;

(f) any other relevant matters.

…

(Notes omitted.)

56 In Re Lombe (2011) 87 ACSR 84; [2011] NSWSC 1536 (Re Lombe) at [3] Barrett J described the effect of a pooling order, albeit at the risk of what his Honour described as “some oversimplification”, to be that several distinct windings up, as they affect creditors only, are administered as if they were a single winding up.

57 Barrett J considered whether a pooling order should be made by reference to the following six questions that his Honour posed at [7]:

(1) Is there “a group of 2 or more companies” (s 579E(1), introductory words)?

(2) Is each company in the group being wound up (s 579E(1)(a))?

(3) Is at least one of the conditions in subparas (i)–(iv) of s 579E(1)(b) satisfied?

(4) What does the evidence show with respect to the matters in s 579E(12) as they may affect the answer to the following question 5?

(5) Is it just and equitable that the order sought be made (s 579E(1)(b), concluding words)?

(6) Does s 579E(10) preclude the making of a pooling order?

58 The questions identified in Re Lombe have been accepted by subsequent authorities as a summary of the pre-conditions to the exercise of the power in s 579E: see for example Hathway, in the matter of Stacey Apartments Pty Ltd (in liq) v Southern Cross Estate Developers Pty Ltd (deregistered) [2019] FCA 1218 at [19]; Walker, in the matter of ZYX Learning Centres Limited (formerly A.B.C Learning Centres Limited) (Receivers and Managers Appointed)(in Liq) [2015] FCA 146 (Re Walker) at [32].

59 The extent to which a liquidator took steps to notify and explain to all known creditors an intention to seek a pooling order is also a relevant matter to be taken into account. In particular it assists the Court in determining whether making such an order would materially disadvantage unsecured creditors: Re Aboriginal Connections Aboriginal Corporation (in liq) (2012) 263 FLR 121; [2012] NSWSC 491 (Re Aboriginal Connections) at [42].

60 In Lofthouse v Environmental Consultants International Pty Ltd (in liq) [2012] VSC 416 at [18] Ferguson J said:

Section 579E(12) confers a wide discretion on the Court. However, the discretion must be exercised judicially having regard to the specific factors listed in paragraphs (a)-(e) of the legislation and, under paragraph (f), “any other relevant matters”. This requires the Court to consider the whole of the circumstances of the group of companies and their creditors.

(Footnote removed.)

61 If the Court finds “material disadvantage” exists for the purposes of s 579E(10) of the Act it cannot come to a positive conclusion that it is just and equitable to make a pooling order: Re Lombe at [82].

62 The determination of whether an eligible unsecured creditor would be materially disadvantaged by the making of a pooling order is a question to be determined in all of the circumstances of the case: Re Walker at [42], [50]. Relevant matters to take into account in determining that issue include the dividend payable to creditors in a pooled scenario versus a non-pooled scenario and whether any creditor has appeared to object to the making of the proposed pooling order: Re Walker at [40]; Re Aboriginal Connections at [42].

Section 90-15 of the IPSC

63 Section 90-15(1) of the IPSC empowers the Court to make such orders as it thinks fit in relation to the external administration of a company either on its own initiative or on application under s 90-20. The persons who may apply for an order under s 90-15 include an officer of the company: s 90-20(1) of the IPSC. An officer is defined in s 9 of the Act to include a liquidator.

64 Section 90-15(4) sets out a non-exhaustive list of the matters that the Court may take into account when making orders under subs (1) as follows:

(a) whether the liquidator has faithfully performed, or is faithfully performing, the liquidator’s duties; and

(b) whether an action or failure to act by the liquidator is in compliance with this Act and the Insolvency Practice Rules; and

(c) whether an action or failure to act by the liquidator is in compliance with an order of the Court; and

(d) whether the company or any other person has suffered, or is likely to suffer, loss or damage because of an action or failure to act by the liquidator; and

(e) the seriousness of the consequences of any action or failure to act by the liquidator, including the effect of that action or failure to act on public confidence in registered liquidators as a group.

65 The principles applicable to the exercise of the Court’s power under s 90-15 of the IPSC are the same as those that applied to the now repealed s 479(3) and s 511 of the Act: Warner (liquidator), in the matter of Sakr Bros Pty Ltd (in liq) [2019] FCA 547 at [18]. The following propositions emerge from the authorities on s 90-15 of the IPSC and its predecessor sections, s 479(3) and s 511 of the Act.

66 The Court’s power to make orders under s 90-15(1) is unconstrained: Deputy Commissioner of Taxation v Italian Prestige Jewellery Pty Ltd (in liq) (2018) 129 ACSR 115; [2018] FCA 983 at [36]. The subsection “contains no express words of limitation” and is “intended to facilitate the performance of a liquidator’s functions”: Re Octaviar Ltd (in liq) [2019] QSC 235 (Octaviar) at [10].

67 A liquidator may seek directions to obtain guidance as to the conduct of a liquidation and as a means to protect against allegations of breach of duty. However, it is generally not appropriate in an application for directions to make the liquidator’s commercial decisions where he or she has full power to act: Re Spedley Securities Ltd (in liq) (1992) 9 ACSR 83 at 85. In Re Ansett Australia Ltd (No 3) (2002) 115 FCR 409 at [65] Goldberg J summarised the circumstances in which a court will give directions as follows:

This review of the authorities satisfies me that the prevailing principle adopted by the courts, when asked by liquidators and administrators to give directions, is to refrain from doing so where the direction sought relates to the making and implementation of a business or commercial decision, either committed specifically to the liquidator or administrator or well within his or her discretion, in circumstances where there is no particular legal issue raised for consideration or attack on the propriety or reasonableness of the decision in respect of which the directions are sought. There must be something more than the making of a business or commercial decision before a court will give directions in relation to, or approving of, the decision. It may be a legal issue of substance or procedure, it may be an issue of power, propriety or reasonableness, but some issue of this nature is required to be raised. It is insufficient to attract an order giving directions that the liquidator or administrator has a feeling of apprehension or unease about the business decision made and wants reassurance. There must be some issue which arises in relation to the decision. A court should not give its imprimatur to a business decision simply to alleviate a liquidator’s or administrator’s unease. There must be an issue calling for the exercise of legal judgment.

68 The Court’s advice should be directed to whether the liquidator is justified in conducting a winding up in a particular way. Whether that is so should be determined by reference to a consideration of the liquidator’s reasons and the process by which the foreshadowed decision has been reached: Octaviar at [23].

Is this an appropriate case for a direction under s 90-15 of the IPSC?

69 The Liquidators submit that it is appropriate to seek the direction in para 1 of the Amended Application. They contend that the Surplus is approximately $9,285,086.21 and the total claims of unsecured creditors is $45,862,343 of which $13,398,810 represent priority creditor claims. The decision whether to allocate the Surplus on a divisional basis will have a significant impact on the rights of both priority and ordinary unsecured creditors. In the case of ordinary unsecured creditors, if the Liquidators proceed on the basis of a divisional asset allocation of the Surplus, ordinary unsecured creditors are likely to receive a dividend of 0.08c/dollar in respect of their provable debts.

70 Further, the Liquidators say that, as the true asset position of each of the WDS Subsidiaries is presently unknown without a detailed reconstruction of the books and records of those companies, it is conceivable that the Liquidators may come under scrutiny from unsecured creditors, including that they may face allegations of breach of duty, if they take a divisional asset allocation approach.

71 The Liquidators’ view is that without a pooling order the Surplus, once received, should be treated as assets of the mining, energy and corporate divisions and distributed in accordance with the divisional asset allocation approach i.e. the Proposed Approach. They have formed that view based on the following matters:

(1) the financial positions of each of WDS and the WDS Subsidiaries were intermingled. It is not possible based on the books and records to ascertain their respective asset positions but it is possible to ascertain the revenue generated by each division because those matters were reported in the segment reporting analysis provided with the financial statements;

(2) the WDS Group was centrally managed and the divisions treated as part of a diversified portfolio in respect of which collective strategic decisions were taken by a single board;

(3) it can be inferred from the documents available to the Liquidators that the benefits accrued to WDS under commercial contracts, the GE Facility and its tax consolidation were only achieved by virtue of the WDS Subsidiaries providing their support. For example, each of the WDS Subsidiaries were guarantors and gave fixed and floating charges over substantially all of their assets to secure the GE Facility which was used in the day to day operations of WDS and the WDS Group, and while WDS was the commercial counterparty to the majority of WDS Group contracts, it could not have fulfilled those contracts without employees provided by the Employing Entities;

(4) in the absence of evidence of an alternative asset position, the Surplus should be distributed in a way that reflects the relative revenue position of a division to other divisions in the WDS Group; and

(5) this is particularly so where the employees generated the bulk of the WDS Group’s revenue and are entitled to claim priority creditor status in their respective employer’s insolvency.

72 The Liquidators submit that their proposed distribution of the Surplus is not only justified based on the operating reality of the WDS Group but that it is also the fairest outcome because:

(1) by adopting a divisional asset allocation approach, the Liquidators will avoid having to undertake a reconstruction of the accounts to determine the true asset position of the WDS Group and thus avoid the need to incur the cost and delay which would be occasioned by that exercise. Given that the Liquidators have largely finished their work in the liquidations they do not consider that the delay is in the interests of creditors or that the cost will likely produce the clarity of the WDS Group’s asset position to justify the expense;

(2) it avoids the creditors of WDS receiving a windfall. If the Liquidators proceed on the basis that WDS owned all of the WDS Group’s assets, the creditors of WDS would receive a windfall in circumstances where the evidence suggests it acted only as the treasury and holding company of the WDS Group and did not positively generate revenue;

(3) if the WDS Group’s assets are treated as belonging to WDS, the Commonwealth would be denied its subrogated right of priority in respect of WDS (Mining) Pty Ltd, WDS (Energy & Infrastructure) Pty Ltd, WDS (Corporate) Pty Ltd and Ackroyd, amounting to $8,078,598.35. This is unfair because the statutory purpose of s 556(1)(e), (g) and (h) of the Act is to afford employees priority in windings up. Given the Employing Entities produced significant value for the WDS Group it would be unfair for the Commonwealth, which has paid employees’ claims and now wishes to exercise its rights of subrogation, to be denied its opportunity to recover a proportion of the monies outlaid;

(4) no creditor of any company in the WDS Group has sought to oppose the direction sought despite having been given an opportunity to do so; and

(5) it is fair with respect to the Liquidators’ remuneration. To date the Liquidators have apportioned their fees between WDS and the WDS Subsidiaries. If they are not entitled to treat the Surplus as an asset of the WDS Group, they will only be entitled to priority recovery of their fees in WDS which they contend is an unfair result in circumstances where the Receivers, by treating the assets of the WDS Group as pooled, were able to recover their fees in full from WDS. The Liquidators say that that they should not be prejudiced as to the recovery of their own fees by the Receivers’ approach to their appointment, particularly given that the Liquidators have been unfunded since their appointment on account of the Receivers asserting control over the WDS Group’s assets.

73 By para 1 of the Amended Application, the Liquidators seek a direction as to the distribution of the Surplus based upon the divisional asset allocation approach i.e. the Proposed Approach (see [49] above). They contend that the effect of making the direction in association with the pooling order sought by them is to justify the Proposed Approach as a method of allocation, as opposed to distribution, and to set up a counterfactual for the purposes of considering the pooling order and assisting in establishing the criteria that it is just and equitable that such an order be made.

74 Although the matter is not without doubt, on balance, I am satisfied that it is appropriate that a direction in the terms sought by the Liquidators should be made.

75 The issue that arises is whether there is any utility in making the direction in circumstances where the Liquidators have also sought, and I intend to make, a pooling order (addressed below). That is because the pooling order will, in effect, subsume any direction made pursuant to s 90-15 of the IPSC as it deals with the same subject matter. Once made, the Liquidators will proceed with the distribution of the Surplus in accordance with the pooling order.

76 That said, I am persuaded to make the direction sought by the Liquidators because an issue of the reasonableness or propriety of adopting the Proposed Approach arises in the liquidations of the companies in the WDS Group. This is not a mere commercial decision which the Liquidators face but a decision as to how to allocate the assets of the WDS Group, and thus the Surplus, in the face of claims by priority and ordinary unsecured creditors of the WDS Group and in circumstances where the books and records of the WDS Group as currently available do not present a conclusive picture. In that regard, I accept the Liquidators’ submissions as to the evidential basis for adopting the Proposed Approach and their views as to the fairness of adopting that approach as set out at [71]-[72] above. Further, the making of the direction will afford the Liquidators a level of protection to which, in the circumstances of this case, they are entitled.

Should a pooling order be made?

77 The Liquidators submit that it is appropriate that a pooling order be made. The Commonwealth supports the application for a pooling order but made submissions in relation to the issue of “material disadvantage”.

78 I will consider whether the order sought should be made by reference to the six questions identified in Re Lombe set out at [57] above.

Questions 1 to 3

79 The first and second questions are whether there is a group of two or more companies and whether each company in the group is being wound up. The evidence establishes that the WDS Group was made up of 12 companies, all of which are being wound up.

80 The third question concerns the satisfaction of one of the conditions in s 579E(1)(b) of the Act (see [55] above). In this case, among other things, by operation of the Deed of Cross Guarantee, each company in the WDS Group is jointly liable for one or more debts or claims. Thus s 579(1)(b)(ii) is satisfied.

Questions 4 and 5 – the just and equitable criteria

81 Question 4 concerns the factors set out in s 579E(12) of the Act to which the Court must have regard (see [55] above). As submitted by WDS, the following matters relevant to the criteria in s 579E(12) emerge from the evidence.

82 First, the business of the WDS Group was centrally managed. The board of WDS was responsible for the WDS Group’s business and strategic plans and corporate governance and the WDS Group had centralised senior management.

83 Secondly, the WDS Group essentially operated as a single business grouped into divisions. WDS, the listed holding company, was usually the counterparty that entered into commercial contracts on behalf of the WDS Group. However, WDS could not perform those contracts because it did not employ the necessary staff or likely hold the plant and equipment with which to do so. Staff were provided by the Employing Entities grouped within two operating divisions of the WDS Group, energy and mining, but were paid from a bank account held by WDS. There were no intercompany accounts reflecting balances owed between WDS and any of the Employing Entities for the use of those employees, nor is there any provisioning for employee entitlements.

84 Thirdly, WDS and WDS (Mining) Pty Ltd were the borrowers under the GE Facility with each of the WDS Subsidiaries acting as guarantors. In addition, each company in the WDS Group granted a fixed and floating charge over substantially all of its assets to secure the GE Facility. The Receivers were appointed by GE pursuant to its rights under the GE Facility and related security.

85 Fourthly, each of the companies in the WDS Group guaranteed the obligations of each other company pursuant to the Deed of Cross Guarantee.

86 Fifthly, since at least 2008 the WDS Group prepared consolidated accounts. None of the financial statements, interim financial reports or annual reports record revenue, assets or liabilities by entity. The Liquidators have located financial reports prepared by the WDS Group for GE which principally group revenue, assets and liabilities into the same categories as reported in the interim financial reports and annual reports, namely energy, mining and corporate. The management accounts also allocate transactions into those three categories.

87 Sixthly, since at least 1 July 2006 WDS and the WDS Subsidiaries were consolidated for tax purposes with WDS as the head company of the consolidated group.

88 Seventhly, WDS was the only company within the WDS Group which held bank accounts. It received and made payments for all of the WDS Group’s business from those accounts and, effectively, acted as the treasury company for the WDS Group.

89 Eighthly, the appointment of administrators to WDS and the WDS Subsidiaries was precipitated by the “Friction Ignition” event at the Eagle Downs mine site in August 2015 which, in turn, triggered EDCM’s call on the Performance Bond and ultimately caused GE to withdraw its support of the WDS Group and to refuse to provide future drawdowns under the GE Facility. The WDS Group did not have access to alternative funding. At that point the board of WDS concluded that it was unable to form a view that WDS could remain solvent. As all of WDS’s secured obligations were subject to security given by each of the WDS Subsidiaries and all of its other liabilities were assumed by the Deed of Cross Guarantee, any determination that WDS was not solvent was, in effect, a determination that applied to all the companies of the WDS Group.

90 Relevantly, while the Eagle Downs mine project was considered to be part of the mining division’s business, because of the way in which the WDS Group operated, the Liquidators submit that it is not possible to conclude that the failure of that project, which precipitated the administration of the WDS Group, is attributable only to the business of that division. I accept that submission. To do so would be to ignore the way in which the WDS Group in fact operated. As has been established its finances were intermingled and the Liquidators have been unable to identify any evidence that revenue from the mining division was segregated from that of the energy division. The businesses of the two divisions appeared to operate as parts of a diversified portfolio intended to offset downturns in the respective industries for the benefit of the WDS Group as a whole. For example WDS’s 2014 annual report includes the following under the heading “Note 29: Segment reporting”:

The Consolidated Group is managed primarily on the basis of product category and service offerings as the diversification of the Group’s operations inherently have notably different risk profiles and performance assessment criteria. Operating segments are therefore determined on the same basis. The Consolidated Group consists of two operating segments which operate in only one geographical segment – Australia:

Mining – The provision of skilled labour and specialist mining equipment to the underground mining industry.

Energy – The provision of specialist design, construction and maintenance services to the oil, gas and water sectors.

91 Finally, the Liquidators have been unable to uncover any evidence in the books and records of WDS or the WDS Subsidiaries that would enable them to assess the independent asset and liability position of each company in the WDS Group.

92 That then leaves for consideration s 579E(12)(e) which requires the Court to have regard to the extent to which creditors of any of the companies in the WDS Group may be advantaged or disadvantaged by the making of the pooling order. If the pooling order sought by the Liquidators is made the priority creditors, namely the employees, will be advantaged. They will have priority claims to the whole of the pooled surplus assets of the WDS Group irrespective of which entity previously owned which assets. In those circumstances the employees will receive 100% of their entitlements in respect of wages, superannuation contributions and leave (see s 556(1)(e) and (g) of the Act) and about 28% of their entitlements in respect of payments in lieu of notice and redundancy payments (see s 556(1)(h) of the Act). Those payments will exhaust the Surplus meaning that the remaining ordinary unsecured creditors will receive no dividend.

93 If a pooling order is not made the employees will be entitled to the statutory priority in ss 433, 556(1) and 561 of the Act in respect of assets held by the relevant Employing Entities. To the extent that employee entitlements are not satisfied from those assets the employees will have a claim in the liquidations of each other company in the WDS Group pursuant to the Deed of Cross Guarantee. Those claims will be contractual claims which will rank pari passu with the claims of ordinary unsecured creditors and will not attract the statutory priority. In that scenario, assuming the Surplus is distributed in accordance with the Proposed Approach it is estimated that as set out at [52] above:

(1) priority creditors will receive a dividend of:

(a) 0c/dollar for claims made on WDS;

(b) 4.21c/dollar for claims made in respect of WDS (Corporate) Pty Ltd;

(c) 100c/dollar for claims made in respect of WDS (Energy & Infrastructure) Pty Ltd;

(d) 65.23c/dollar for claims made in respect of WDS (Mining) Pty Ltd; and

(e) 0c/dollar for claims made on Ackroyd; and

(2) unsecured creditors will receive a dividend of 0.08c/dollar.

94 Given the insignificant return to ordinary unsecured creditors if a pooling order is not made it is difficult to see how making the order sought will disadvantage those creditors. By way of illustration, according to the Liquidators, the largest ordinary unsecured creditor by value is Assetinsure which lodged a proof of debt for approximately $14.8 million. It will receive a dividend of $11,854.10 if a pooling order is not made. The second largest ordinary unsecured creditor by value is Southern Cross Electrical which lodged a proof of debt for just over $2.3 million. It will receive a dividend of $1,853.89 if a pooling order is not made. In both cases, those creditors will receive no dividend if a pooling order is made. It is evident that the return to ordinary unsecured creditors is less than 1c/dollar and despite being given notice of the proceeding, no creditor in that class appeared to oppose the order sought. While ordinary unsecured creditors might suffer some disadvantage, that disadvantage is so small as to be insignificant given the likely returns: see Re Walker at [40].

95 Question 5 requires consideration of whether it is just and equitable that the pooling order sought should be made.

96 In considering that question I have had regard to the factors set out above and, given that I am satisfied that I should make a direction in the terms sought in para 1 of the Amended Application, to the fact that making a pooling order will minimise cost and delay and increase administrative efficiency in the winding up by obviating the need for the Liquidators to conduct multiple liquidations and comply with statutory requirements in respect of each company in the WDS Group. Based on those matters and subject to s 579E(10) of the Act (see below), I am satisfied that is it just and equitable to make a pooling order.

Question 6 – does s 579E(10) of the Act preclude the making of a pooling order?

97 Section 579E(10) of the Act is set out at [55] above. In Re Lombe at [82] Barrett J expressed the view that if “material disadvantage” is found the court could not be satisfied that it is just and equitable to make a pooling order.

98 Only s 579E(10)(a) of the Act is relevant to the present application because none of the companies in the WDS Group is being wound up under a members’ voluntary winding up. Section 579E(10)(a) precludes the court from making a pooling order if it is satisfied that it would materially disadvantage an eligible unsecured creditor of a company in the group and that eligible unsecured creditor has not consented to the making of the order.

99 Section 579Q of the Act provides that a creditor of a company in a group of two or more companies is an eligible unsecured creditor if the creditor’s debt or claim is unsecured and the creditor is not a company in the group or if the creditor is specified in the regulations. Regulation 5.6.73 of the Corporations Regulations 2001 (Cth) provides that:

Creditors that are eligible unsecured creditors

(1) For paragraph 579Q(1)(b) of the Act, the following creditors are specified:

(a) a creditor to which either of the following applies as a result of a modification of the Act made under paragraph 571(1)(d) of the Act:

(i) a debt payable by a company or companies in a group to any other company or companies in the group is not extinguished;

(ii) a claim that a company or companies in a group has against any other company or companies in the group is not extinguished;

(b) a creditor that is determined by a Court to be an eligible unsecured creditor.

Creditors that are not eligible unsecured creditors

(2) For subsection 579Q(2) of the Act, a creditor that is determined by a Court not to be an eligible unsecured creditor is specified.

100 Having regard to the definition of an eligible unsecured creditor in s 579Q and reg 5.6.73, the only relevant class of creditors for the purposes of s 579E(10)(a) in this case are unsecured creditors of one or more of the companies in the WDS Group who are neither WDS or a WDS Subsidiary.

101 The Liquidators raise as an issue whether they bear the onus of adducing evidence to establish whether the making of a pooling order would materially disadvantage an eligible unsecured creditor of a company in the WDS Group or whether a pooling order can be made on the evidence before the Court provided that the Court is not satisfied that the order would materially disadvantage an eligible unsecured creditor. The Liquidators describe the issue of statutory construction as finely balanced but consider that the better view is that they bear the onus of adducing sufficient evidence to allow the Court to conclude that no material disadvantage would arise to an eligible unsecured creditor by the making of an order under s 579E(1). However, in oral submissions senior counsel for the plaintiffs invited the Court not to resolve the issue and submitted that the scope and nature of the onus may well turn upon the particular circumstances of the case. In that regard, as I understood it, the position put was that in circumstances where the Court was minded to make the direction sought in para 1 of the Amended Application the issue of material disadvantage was straightforward and easily resolved in favour of making the pooling order.

102 It is on this issue that the Commonwealth wished to make submissions. The Commonwealth submits that contrary to the position posited by the Liquidators, s 579E(10)(a)(i) of the Act does not involve the imposition of an onus to prove the negative but means what it says. Namely, that if on all of the material before it the Court forms a state of satisfaction that an unsecured creditor would be materially disadvantaged by the making of a pooling order, the Court must not make the order.

103 Putting that to one side, the Commonwealth contends that one of the comparators in that exercise is the distribution to ordinary unsecured creditors if a pooling order is made, which in this case is nil. It says that the more difficult question is identifying and quantifying the other comparator, the position of ordinary unsecured creditors if no pooling order is made. The Commonwealth notes that in those circumstances, the position of ordinary unsecured creditors is completely unknown, as is the position of employees and, through them, the Commonwealth. The Commonwealth also notes that all the Court knows is the position of ordinary unsecured creditors at two extremes, namely:

(1) if WDS owns all assets of the WDS Group in which case, absent pooling, ordinary unsecured creditors, as well as employees under the Deed of Cross Guarantee, would receive 18c/dollar (which is scenario 1 referred to at [51(1)] above). The Commonwealth says that if this scenario was established there would be a serious issue about material disadvantage; and

(2) if the WDS Subsidiaries own all assets of the WDS Group in accordance with its operating divisions, absent pooling, ordinary unsecured creditors would receive about 0.08c/dollar (which is Scenario 5 referred to at [51(5)] above). The Commonwealth says that if this scenario was established a comparison of 0.08c/dollar to 0c/dollar would not result in material disadvantage.

104 The Commonwealth observes that an intermediate position is that the Employing Entities owned material assets with other assets being held in other entities including WDS. It contends that if that were the position then employee priority claims will exhaust the assets in the liquidations of the Employing Entities reducing the return to ordinary unsecured creditors.

105 The Commonwealth refers to the Liquidators’ evidence as to the cost and time that would be involved in establishing the true asset position of the WDS Group and submits that at the end of that process, if undertaken, there is no real prospect of a conclusion that WDS owned all of the assets of the WDS Group and that, consistent with the evidence, the more likely scenarios are divisional ownership, which is the Liquidators’ opinion to which weight should be afforded, or at least material asset ownership by the WDS Subsidiaries including the Employing Entities.

106 The Commonwealth also observes that there is a further layer of complexity to the extent that the Receivers realised property that was subject to a circulating security interest. In those circumstances the Commonwealth says that s 433 of the Act required the Receivers to pay out of that property amounts having priority under s 556(1)(e), (g) or (h), which did not occur. The Commonwealth notes that whether that was a breach of s 433 depends on the extent to which assets were owned by the Employing Entities and those assets were subject to a circulating security interest, a matter about which the Receivers and the Commonwealth are in dispute. The Commonwealth submits that if the Receivers breached s 433 of the Act, any monies the Commonwealth recovered would reduce the amount for which it would otherwise prove in the liquidations. It notes that while that dispute is on foot, the Receivers will not release the Surplus because they claim an entitlement to be indemnified and that the dispute will further delay and diminish any return to creditors. It says that if a pooling order is made, the Commonwealth has agreed to release the Receivers from any claims for breach of s 433 of the Act thereby freeing up the funds for immediate release to the Liquidators and distribution to creditors.

107 The Commonwealth thus submits that for the purposes of the comparison required by s 579E(10)(a)(i) the position of ordinary unsecured creditors absent pooling cannot be equated to an entitlement to 18c/dollar and rather, it is a far more contingent and uncertain position which is likely, if anything, to be at, or closer to, the divisional asset allocation scenario of 0.08c/dollar for ordinary unsecured creditors. It says that the Court would not reach a state of satisfaction that any ordinary unsecured creditor would be materially prejudiced by the pooling order.

108 The Commonwealth referred by way of analogy to Re Lombe where, in the context of considering s 579E(10)(a)(i), Barrett J referred at [90] to the fact that one creditor, who had lodged a proof of debt for $52,767, opposed pooling. Barrett J noted that upon inquiry the liquidator established that the objecting creditor was under the impression that, absent pooling, the whole of the net surplus from the sale of the business would be available for application to the debts of the company of which he was a creditor. Barrett J accepted the liquidator’s submission that the creditor’s objection proceeded on a mistaken premise and thus lacked substance. The Commonwealth submits that, although there are no creditors who oppose the making of a pooling order in this case, the same could be said here. That is, if a creditor did object on the basis that they thought they could get a higher return, arguably 18c/dollar based on the analysis in scenario 1 in which all assets were allocated to WDS (see [51(1)] above), they would similarly have proceeded on a mistaken premise for the reasons identified by the Liquidators.

109 Section 579E(10) of the Act acts as a constraint on the exercise of the Court’s power to make a pooling order. The Court must be satisfied that a pooling order if made would not materially disadvantage any eligible unsecured creditor. In circumstances where I am satisfied that a direction should be made that the Liquidators distribute the assets in accordance with the Proposed Approach, that conclusion is open to the Court. In those circumstances the relevant counterfactual is that ordinary unsecured creditors would receive 0.08c/dollar. On that basis, the analysis of the amount that would be received by the two largest creditors by value is set out at [94] above. In Re Walker at [40] Jagot J undertook a similar analysis to that undertaken by me in the context of s 579E(12)(e) based on a counterfactual where ordinary unsecured creditors would receive 0.23c/dollar. Her Honour concluded at [42] that while it is possible that there may be disadvantage, the extent of that possibility for disadvantage was not sufficient to weigh against the potential advantages of making the pooling order in the circumstances before her. Her Honour concluded at [53] that for the same reasons there was no material disadvantage in the context of s 579E(10) of the Act.

110 Having regard to the likely recovery to eligible unsecured creditors and the fact that despite being put on notice of the application no creditor has appeared to oppose the making of a pooling order, I am satisfied that a pooling order would not materially disadvantage any eligible unsecured creditors.

111 I should add that even if I were not minded to make the direction sought by the Liquidators in para 1 of the Amended Application I would, substantially for the reasons identified by the Commonwealth in its submission set out at [103]-[108] above, be satisfied that there would be no material disadvantage to any eligible unsecured creditor in making the pooling order.