Tiger Resources Limited, in the matter of Tiger Resources Limited (No 2) [2020] FCA 266

ORDERS

TIGER RESOURCES LIMITED (ACN 077 110 304) Plaintiff | ||

AND | INTERNATIONAL FINANCE CORPORATION Defendant | |

DATE OF ORDER: |

THE COURT ORDERS THAT:

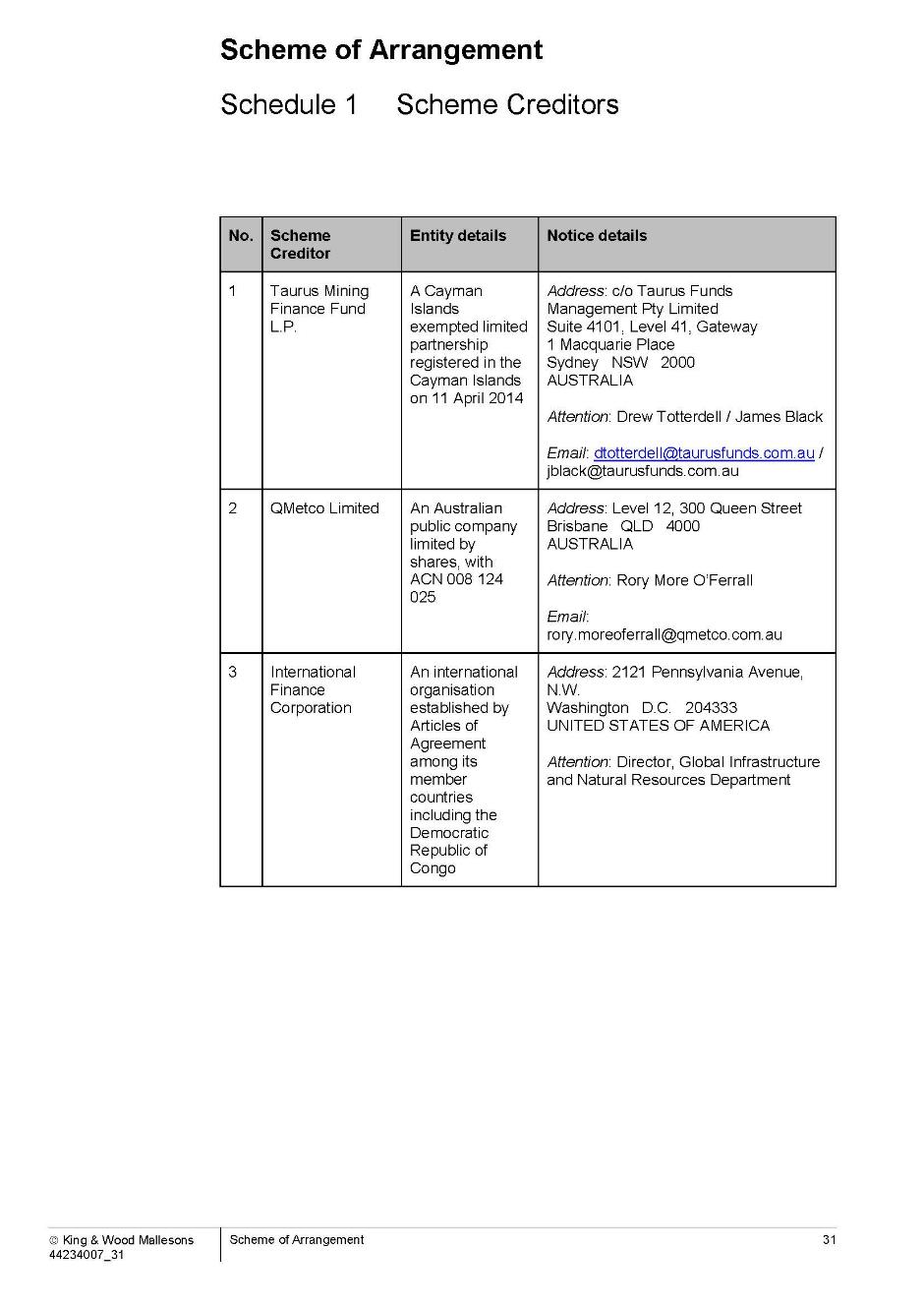

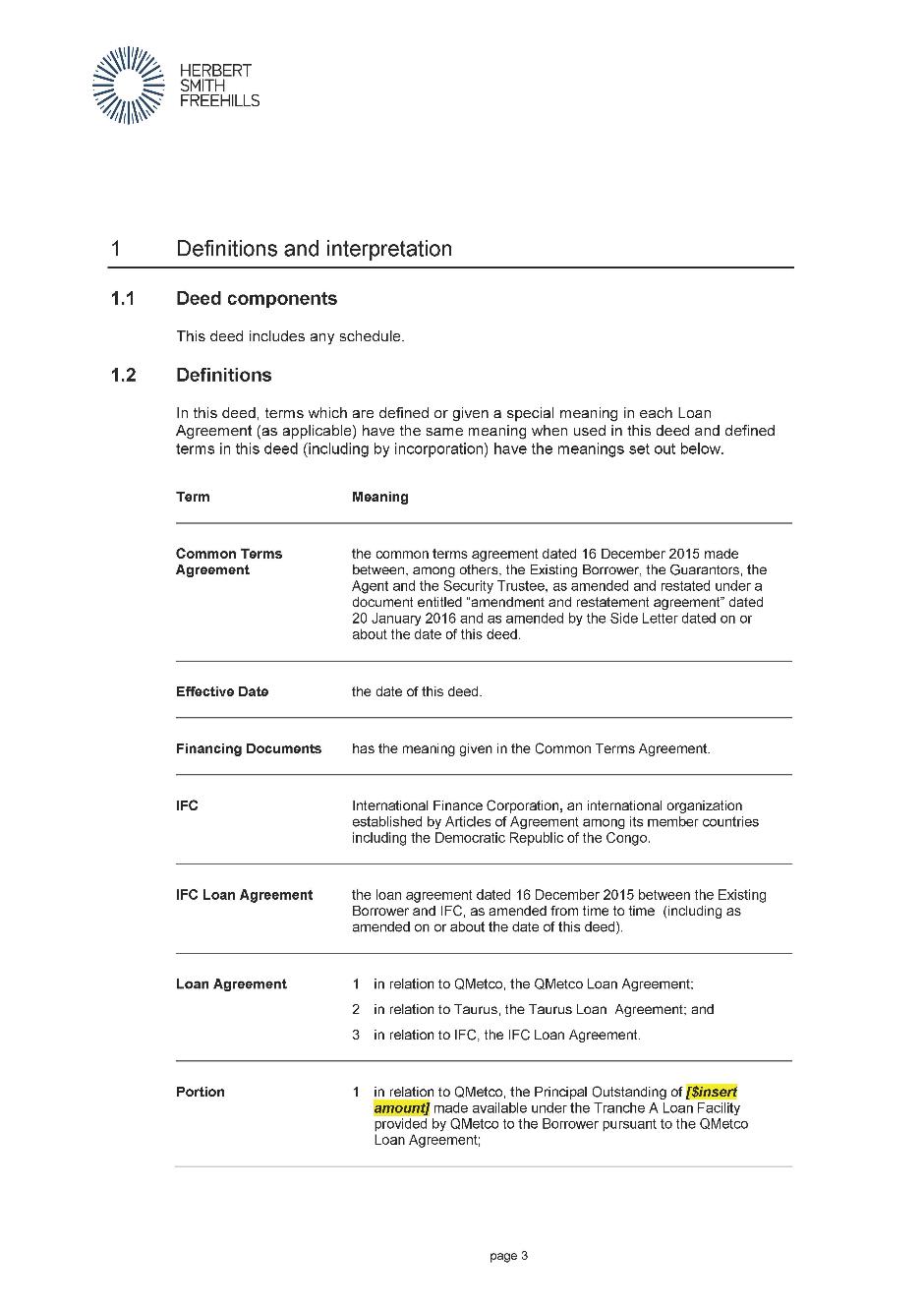

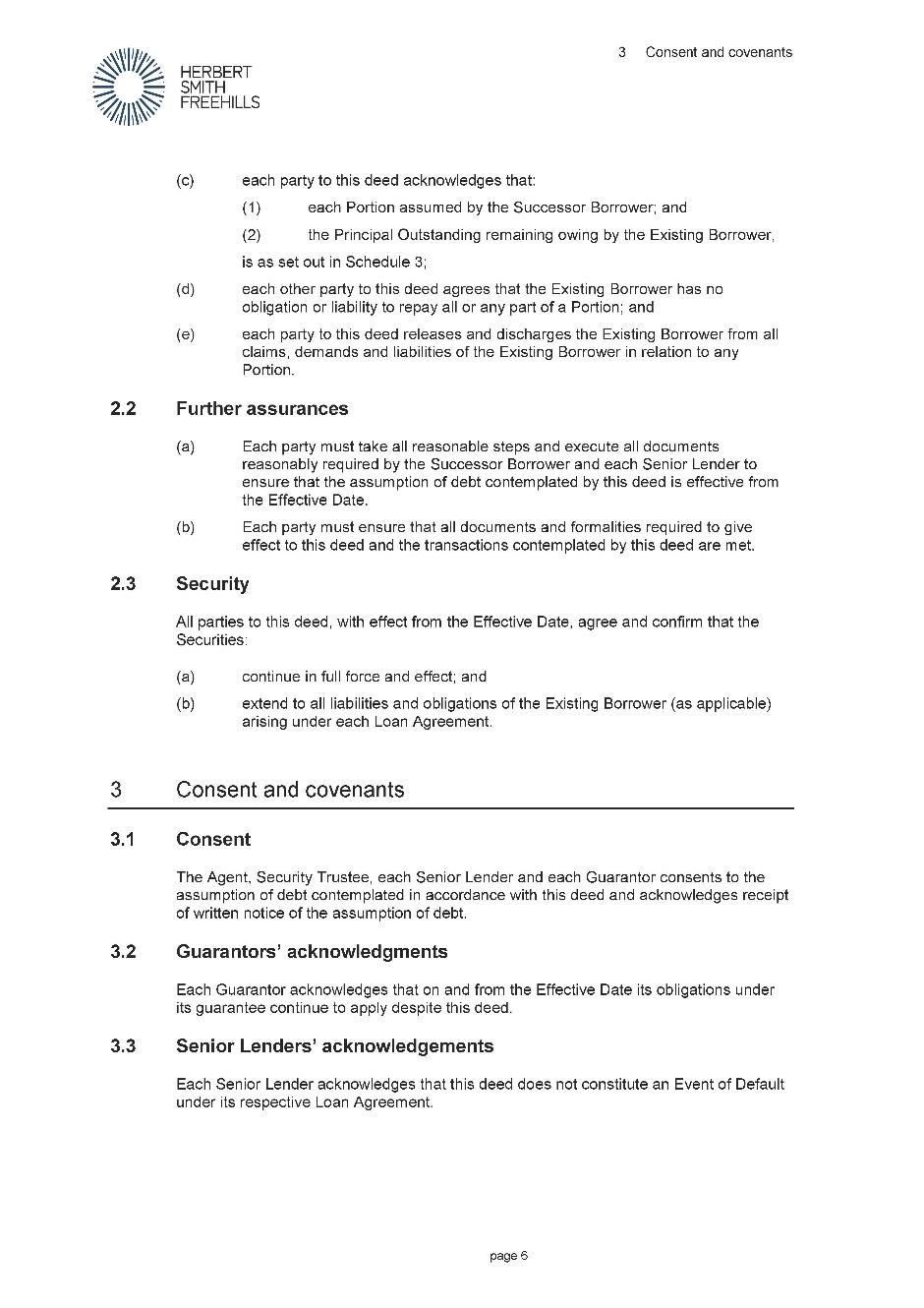

1. Pursuant to s 411(4)(b) and s 411(6) of the Corporations Act 2011 (Cth) (Act), the Scheme of Arrangement (Scheme) between the plaintiff and Taurus Mining Finance Fund, L.P., QMetco Limited and International Finance Corporation, being the Scheme in the form contained in Annexure A to these orders, be and is hereby approved.

2. Pursuant to s 411(2) of the Act, the plaintiff be exempted from compliance with s 411(11) of the Act.

3. Pursuant to r 1.10 of the Federal Court (Corporations) Rules 2000 (Cth), the time for publication specified in rule 3.4 of those rules be abridged nunc pro tunc to 19 February 2020.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ANNEXURE A

GLEESON J:

1 On 21 February 2020, I conducted the second court hearing concerning a scheme of arrangement proposed to be made between the plaintiff (Tiger) and Taurus Mining Finance Fund LP (Taurus), QMetco Limited (QMetco) and International Finance Corporation (IFC) (collectively, scheme creditors) (scheme). At the conclusion of the hearing, I made orders, including an order pursuant to s 411(4)(b) and s 411(6) of the Corporations Act 2001 (Cth) (Act) approving the scheme, for the following reasons.

2 In support of the application for approval of the scheme, senior counsel for Tiger, Mr Jackman SC, read the following affidavits:

(1) affidavit of Caroline Denise Keats, Managing Director and Chief Executive Officer of Tiger, sworn 17 December 2019;

(2) affidavit of Ian Goldberg, Chief Financial Officer and Company Secretary of Tiger, affirmed 20 February 2010;

(3) affidavits of Timothy Michael Klineberg, solicitor, sworn 19 and 20 February 2020; and

(4) affidavit of Natasha Ann Rodricks, solicitor, affirmed 19 and 20 February 2020.

3 IFC appeared at the second hearing and opposed the orders sought on grounds that were addressed on the application for orders in connection with the convening of the scheme meeting: Tiger Resources Limited, in the matter of Tiger Resources Limited [2019] FCA 2186 (earlier judgment). IFC acknowledged that its opposition must fail based on the reasoning in the earlier judgment, including concerning the meaning of “compromise or arrangement” in s 411(1) which applies equally to the meaning of that expression in s 411(4).

4 IFC did not submit that there was any other reason why the Court should not exercise its discretion to approve the scheme.

5 Otherwise, no one appeared to oppose the scheme.

BACKGROUND

6 I adopt the following statement of the background to the scheme from the written submissions provided by Tiger:

5. On 23 December 2019, the Court made orders for Tiger to convene a scheme meeting at which certain of its creditors could consider, and if thought fit agree to (with or without modification) the terms of the Scheme. On 10 February 2020, the Court made further orders permitting the dispatch of supplementary material to certain creditors of Tiger. The effect of that additional material was to allow the creditors to consider whether to vary the Scheme as originally propounded and, if thought fit, approve that Scheme.

6. In summary terms, the Scheme (in its varied form) proposes a compromise between Tiger and three of its creditors: Taurus Mining Finance Fund LP (Taurus), QMetco Limited (QMetco) and IFC (together Scheme Creditors). In effect, these creditors will swap part of their debt for equity in Tiger. In the absence of the proposed Scheme and without additional funding, the independent expert has opined that Tiger will be insolvent.

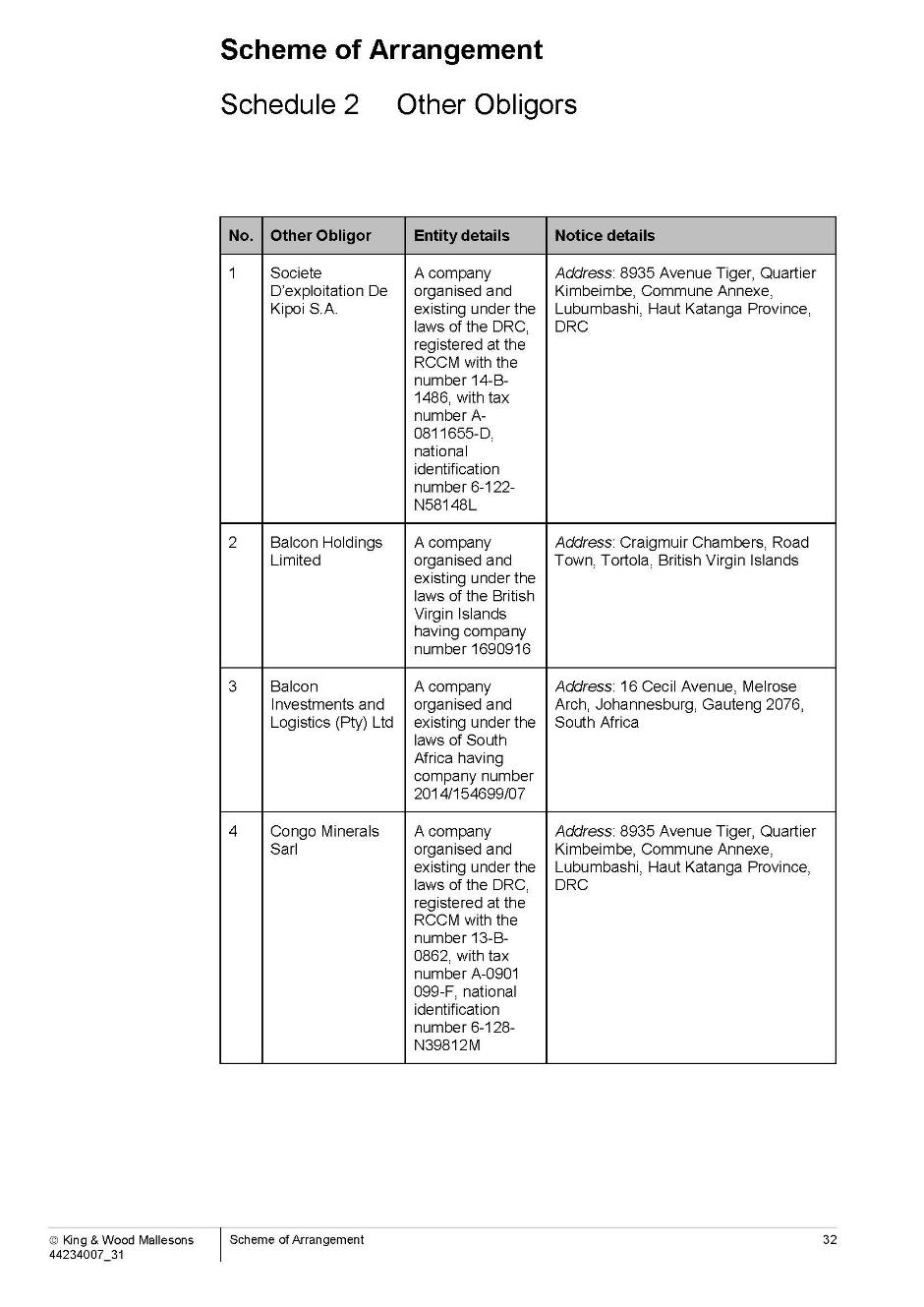

7. Tiger is an Australian public company that is listed on ASX Limited [earlier judgment at [6]]. Tiger is the holding company of a number of other companies incorporated in foreign jurisdictions, which together form the Tiger group. The main operating company within the Tiger group is Societe d’Exploitation de Kipoi S.A (SEK), which conducts mining activities in the Democratic Republic of Congo [earlier judgment at [7]].

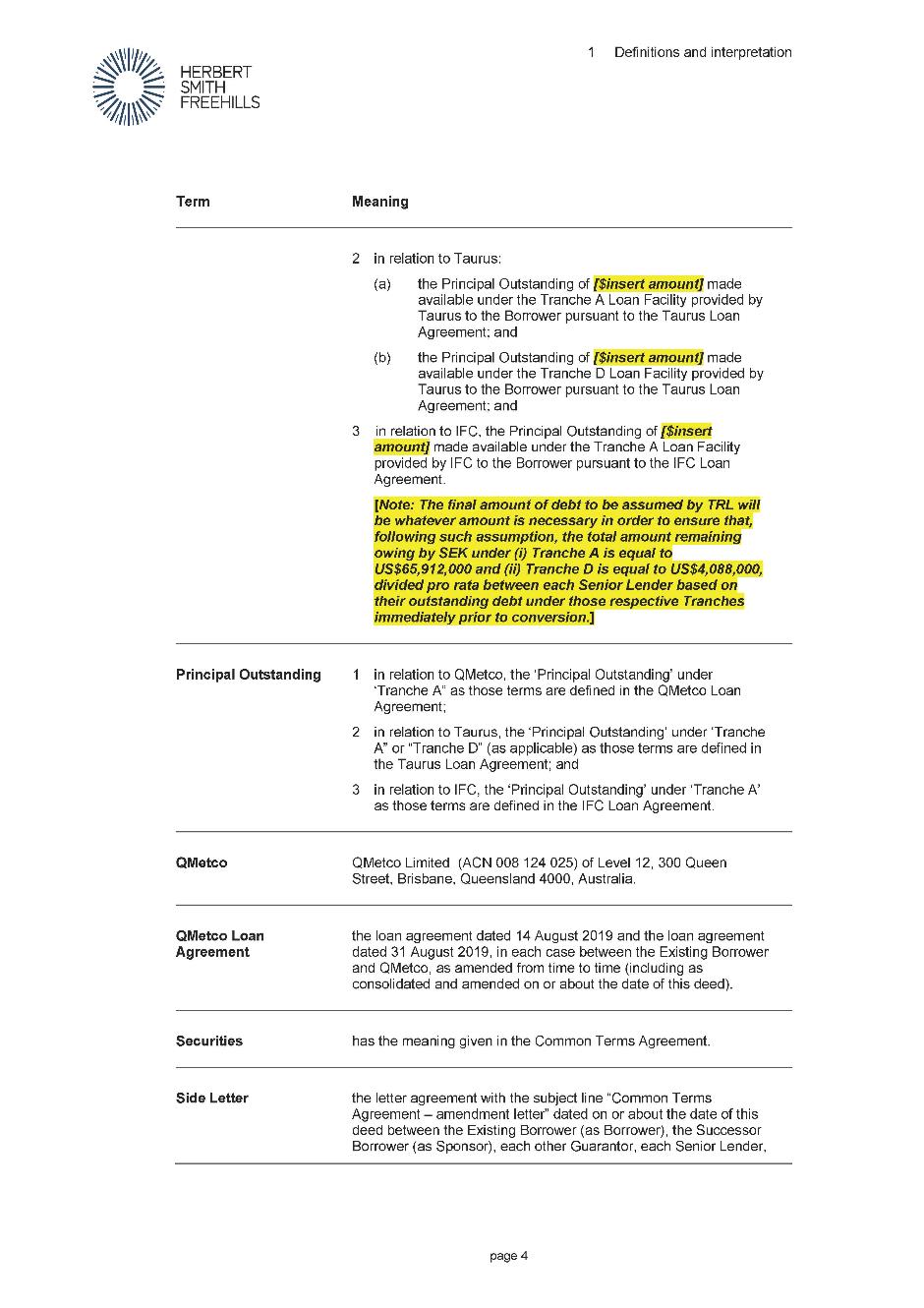

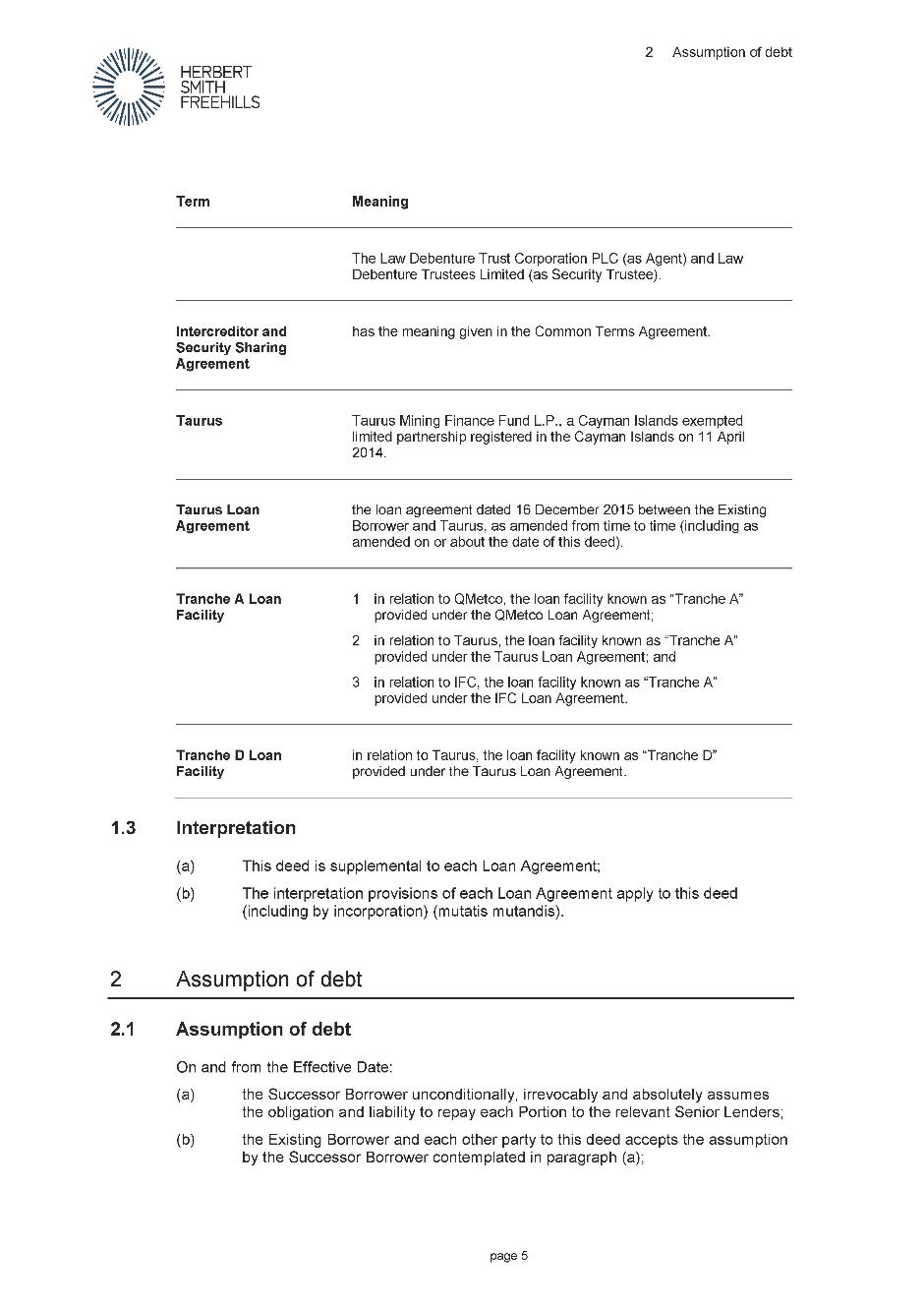

8. SEK has secured borrowings from three creditors: Taurus, QMetco and IFC [earlier judgment at [13]]. Tiger and other members of the Tiger group guarantee those borrowings [earlier judgment at [13]. Those borrowings are on a senior basis (Senior Facility) and super senior basis (Super Senior Facility) [earlier judgment at [13]]. Tranche A of SEK’s debt comprises the Senior Facility and Tranches D and E of SEK’s debt comprises the Super Senior Facility [earlier judgment at [13]]. Tranches D and E have priority over Tranche A [earlier judgment at [13]].

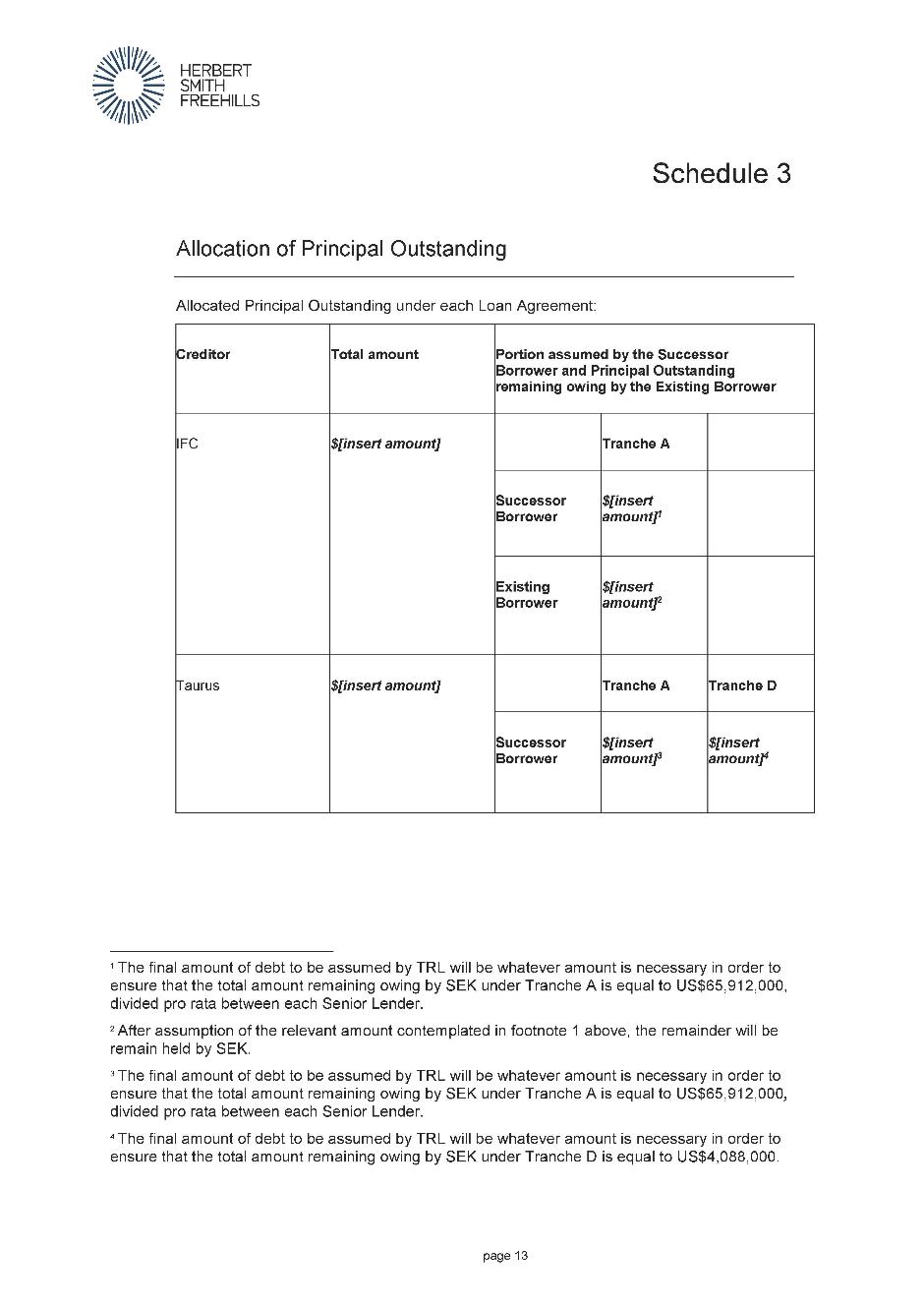

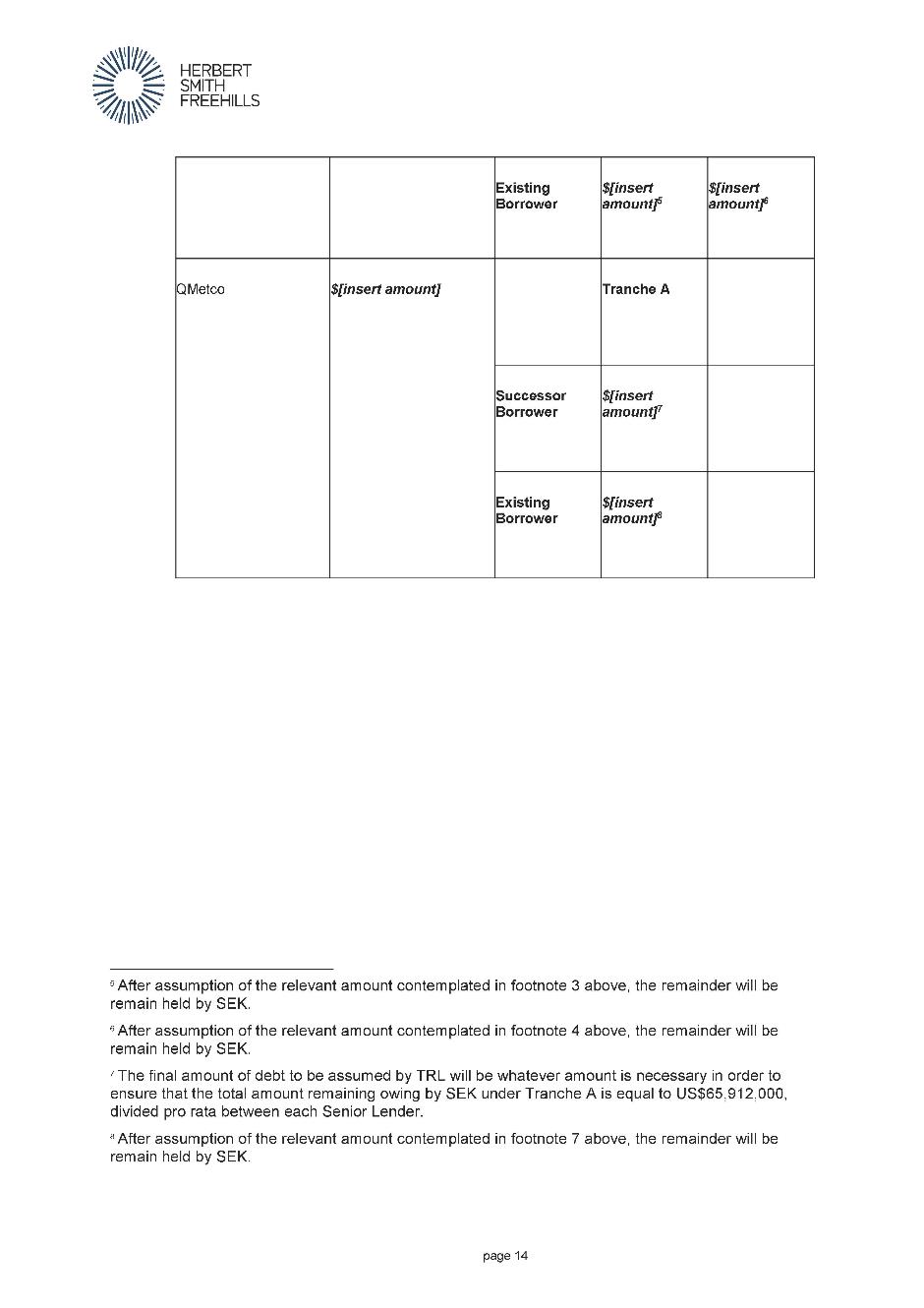

9. Under the Scheme, it is proposed that the debt in respect of Tranches A and D will be compromised. It is proposed that the Tranche A and Tranche D debt will be converted to equity in Tiger at the same rate. The terms on which the compromise will operate are set out pg 6 of the Supplementary Explanatory Statement. In summary:

a. Tranche A (which is held by Taurus, QMetco and IFC) amounted to approximately US$222.9 million prior to implementation of the Scheme (as at 31 December 2019) and will amount to approximately US$65.9 million after the implementation of the Scheme.

b. Tranche D (which is held by Taurus) amounted to approximately US$13.8 million prior to implementation of the Scheme (as at 31 December 2019) and will amount to approximately US$4.1 million after the implementation of the Scheme.

c. Tranche E (which is held by QMetco) and will not be compromised under the Scheme. QMetco will not vote in respect of Tranche E debt.

10. Prior to the implementation of the Scheme, the Scheme Creditors hold 25.02% of the issued shares in Tiger. After implementation of the Scheme, the Scheme Creditors will hold 99.33% of the issued shares in Tiger.

SCHEME MEETING

7 Mr Klineberg chaired the scheme meeting on 17 February 2020. QMetco and Taurus each appointed Mr Klineberg as its proxy to vote on its behalf “for” both resolutions proposed.

8 IFC did not submit a proxy form and did not attend the scheme meeting.

9 The following two resolutions were therefore passed unanimously:

(1) That the scheme of arrangement proposed between the Scheme Company and the Scheme Creditors, as contained and described in the Explanatory Statement dated 23 December 2019, is amended in the manner described in the form of the scheme of arrangement set out in Annexure A to the Supplementary Explanatory Statement, of which the notice convening this meeting forms part.

(2) That, pursuant to and in accordance with section 411 of the Corporations Act 2001 (Cth), the scheme of arrangement proposed between the Scheme Company and the Scheme Creditors, as contained and described in the Explanatory Statement dated 23 December 2019 and as amended pursuant to resolution 1 (Preliminary Resolution), is agreed to (with or without any alterations or conditions made or required by the Court, provided that such alterations or conditions do not change the substance of the Scheme, including the Steps, in any material respect).

PROPOSED AMENDMENTS TO THE SCHEME

10 Section 411(6) of the Act provides that the Court may grant its approval to a compromise or arrangement “subject to such alterations or conditions as it thinks just”.

11 In Independent Practitioner Network Ltd, in the matter of Independent Practitioner Network (No 2) [2008] FCA 1593, Lindgren J explained the scope of the power conferred by s 411(6) as follows (at [16]-[17]):

[16] I do not purport to define or circumscribe the circumstances in which the Court may properly exercise the discretion to approve subject to alterations. The circumstances in which the Court may be asked to exercise the power vary. For example, the purpose may be to overcome minor technical errors or oversights present in the scheme as agreed to by the shareholders (see, for example, Re H Craig Pty Ltd); to bring the scheme as agreed to by them into line with the explanatory statement that was sent to them (see, for example, Re Permanent Trustee Co Ltd); or to protect creditors (see, for example, Re Evandale Estates Ltd). The alterations may be suggested by the plaintiff or by the Court. Apparently, however, the plaintiff would be entitled, if faced with alterations on which the Court insisted but to which it did not agree, to withdraw its application for approval.

[17] At least one thing is clear: the Court will not approve subject to alterations unless it is satisfied that the scheme as proposed to be altered would still have been agreed to by the requisite statutory majorities.

12 In Australian Co-operative Foods Ltd [2008] NSWSC 1221 at [50], Barrett J concluded that a “minor adjustment of a non-prejudicial kind” was clearly within the power to approve subject to alteration. His Honour concluded that the members would still have approved the scheme by precisely the same majority had the alteration been included.

13 In In the matter of Boart Longyear Limited (No 2) [2017] NSWSC 1105; 122 ACSR 437 at [108], Black J concluded that the proposed alterations to the schemes were within the scope of s 411(6) for several reasons, saying:

… I proceed on the basis that s 411(6) of the Corporations Act confers a discretion on the Court, to be exercised judicially, having regard to its statutory purpose and in the light of the whole of the circumstances surrounding the matter. It seems to me that the Court could, in principle, think it “fit” to approve the schemes in this case with material alterations where the schemes and those alterations provide a proper mechanism to implement a complex compromise or arrangement; substantial costs and resources have plainly been devoted to developing them; the Plaintiffs are insolvent or near insolvency and would likely not have the luxury of restarting their restructuring again from the beginning; the Plaintiffs and all voting secured creditors and substantially all voting unsecured creditors affected by the alterations support them; and there would be no utility in ordering further creditors’ meetings where it is already clear that an overwhelming majority of the voting secured creditors and voting unsecured creditors support the alterations. I am satisfied that the proposed alterations are within the scope of the alteration power under s 411(6) of the Corporations Act for those reasons, although the alterations involve a novel application of the section.

14 IFC did not contend that any of the proposed amendments changed the substance of the scheme in any material respect.

15 The proposed amendments were:

(1) An amendment to the definition of “Final Escrow Date” from “[13 March 2020]” to “the first Business Day after the Calculation Date”. Clause 8.3(a) (“Entitlement to Scheme Shares”) provides that each “Trustee” will ask each “Recipient” (being each of the scheme creditors) to confirm certain items (such as it is a sophisticated or professional investor and its instructions to transfer or sell the Scheme Shares) (Requested Confirmations) and to execute a share transfer form, to which the relevant scheme creditor must respond prior to the “Final Escrow Date”. The Trustees are not expected to ask for the Requested Confirmations until the “Effective Date” for the scheme (the day when all of the conditions precedent under the scheme are satisfied). If the Effective Date occurs after 13 March 2020, then it would not be possible for the scheme creditors to comply with cl 8.3(a) because the time would already have expired. If the Recipients do not comply with cl 8.3(a), and cl 8 applies to them (because they require FIRB Approval and have not yet obtained FIRB Approval prior to the Calculation Date: cl 8.1(a)), then they may not be entitled to the “Scheme Shares”.

(2) The effect of this alteration is to provide the scheme creditors with additional time to complete the steps necessary for them to obtain the Scheme Shares. In this sense, it is a minor amendment that could not work any prejudice to the scheme creditors and, I accept, is likely to avoid such prejudice. It is not an alteration to the scheme that would have affected the vote in favour of the scheme had it been included.

(3) It is proposed to insert a new cl 7.5(f)(vi) into the Scheme, which deals with an exemption from US securities laws. The effect of this clause will be to make clear that Tiger will be relying on a particular exemption under US securities laws to issue Scheme Shares to the scheme creditors. This is said to be a matter is of significance where IFC’s address for service is in the United States. IFC did not dispute that similar disclosure wording to cl 7.5(f)(v) was already included in the Explanatory Statement provided to scheme creditors (at section 1.11). In these circumstances, I accepted that this is again a minor amendment that does not work any prejudice and is not an alteration to the scheme that would have affected the vote in favour of the scheme had it been included.

(4) Clause 4.1(b) sets out a regulatory approval condition precedent that is expressed by reference to 8 am on the date of the second court hearing. As matters have transpired, there has been a delay in obtaining the relevant regulatory approval in the Democratic Republic of Congo. That has meant that it is unlikely that satisfaction of that condition precedent will be obtained by the relevant time. In order to adjust for this circumstance, Tiger proposed to remove the time limitation in this clause, such that may be fulfilled at a later point. That later point will be constrained by the “End Date” under the scheme, which is six months after the Court makes any order approving the scheme. Again, in the absence of any opposition from IFC, I accepted that this was a matter capable of modification under s 411(6).

UPDATED EVIDENCE OF TIGER’S FINANCIAL POSITION

16 In the earlier judgment, I recorded the following concerning Tiger’s solvency:

[19] Tiger’s independent expert evidence is that it will be insolvent if the scheme does not proceed.

[20] Tiger noted the evidence of Chief Financial Officer, Ian Goldberg, as to Tiger’s cash flow position in the period to the week commencing 30 March 2020. In particular, Tiger presently forecasts material negative cash balances in the week commencing 17 February 2020 (approximately US$5.5 million), increasing in subsequent weeks commencing 2 March 2020 (approximately US$8.4 million), 13 March 2020 (approximately US$13 million) and 30 March 2020 (approximately US$22.3 million).

[21] Mr Goldberg also gave evidence of the endeavours that Tiger is making and will continue to make during the interim period up to mid-February 2020 to seek to attract further finance. Mr Goldberg’s evidence is that the approval and implementation of the scheme during that period of time is key to Tiger’s ability to attract further finance. New finance is necessary to fund working capital, the “Capital Works Program” and the “Further Exploration”, outlined in further detail in the draft explanatory statement. Mr Goldberg stated that he is not confident of attracting any further finance without the reduction of the secured debt owed by Tiger and its subsidiaries.

17 Mr Goldberg’s 20 February 2020 affidavit included updated cashflow projections which forecast that, if the scheme is not implemented, Tiger will be cashflow negative from the week beginning 22 March 2020, that is, about one month later than had been previously forecast. Mr Goldberg’s affidavit sets out the reasons that he considers to have led to this change.

18 As to Tiger’s efforts to obtain additional funding, Mr Goldberg’s evidence included that none of the potential financiers were willing to advance further funding until the scheme had been approved and implemented on its current terms. Mr Goldberg’s view was that, in order to avoid insolvency, Tiger would require bridging finance from its incumbent financiers pending implementation of the scheme and completion of discussions with the potential financiers.

19 IFC did not take issue with Mr Goldberg’s evidence in any respect.

LEGAL FRAMEWORK FOR CONSIDERING WHETHER TO APPROVE SCHEME

20 The Court has a discretion whether to approve a scheme, and is not bound to approve it merely because it has previously made orders for the convening of meetings or because the statutory majorities have been achieved: Seven Network Limited (ACN 052 816 789), in the matter of Seven Network Limited (ACN 052 816 789) (No 3) [2010] FCA 400; (2010) 267 ALR 583 (Re Seven Network) at [31].

21 The matters the Court was required to take into account in deciding whether to approve the scheme include:

(1) whether the orders of the Court convening the scheme meeting were complied with;

(2) whether the resolution to approve the scheme was passed by the requisite majority;

(3) whether other statutory requirements have been satisfied;

(4) whether all conditions to which the scheme is subject (other than Court approval and lodgement of the Court’s orders with ASIC) have been met or waived;

(5) whether the scheme is fair and reasonable so that an intelligent and honest member of the relevant class, properly informed and acting alone, might approve it. In considering this question, it is not the role of the Court to usurp the decision of the relevant class by imposing its own commercial judgement on the scheme or to consider whether a better scheme might have been proposed;

(6) whether Tiger has brought to the attention of the Court all matters that could be considered relevant to the exercise of the Court’s discretion; and

(7) whether there was full and fair disclosure to the scheme creditors of all information material to the decision whether to vote for or against the scheme.

See Signature Capital Investments Limited, in the matter of Signature Capital Investments Limited (No 2) [2016] FCA 385 at [4] referring to Solutions 6 Holdings Limited ACN 003 264 006, in the matter of Solution 6 Holdings Limited ACN 003 264 006 [2004] FCA 1049; (2004) 50 ACSR 113 at [18]-[21]; Permanent Trustee Company Limited [2002] NSWSC 1177; (2002) 43 ACSR 601 at [8]-[10]; Central Pacific Minerals NL [2002] FCA 239 at [12]- [14]; Re Seven Network at [35]-[39].

CONSIDERATION

22 In this case, two of the three scheme creditors voted in favour of the scheme, exceeding the voting thresholds set by s 411(4)(a)(i). The third scheme creditor, IFC, declined to vote.

23 The evidence demonstrates compliance with the Court’s orders.

24 As to statutory requirements, based on the evidence of Ms Keats, I am satisfied that the scheme has not been proposed for the purpose of enabling any person to avoid the operation of any of the provisions of Ch 6 of the Act, and accordingly, approval of the scheme is not precluded by s 411(17) of the Act. Ms Keats’ evidence was that the scheme was “the transaction which will enable the restructuring of [Tiger’s] secured facilities and will put the balance sheet of [Tiger] and its subsidiaries in a position to enable them to obtain the additional financing they require to avoid insolvency proceedings”. The scheme was proposed to enable Tiger and its related entities in the Democratic Republic of Congo, British Virgin Islands and South Africa to reduce their current unsustainable debt position, through a debt-for-equity swap, in a manner that will allow Tiger to continue operating into the future. Ms Keats affirmed that the scheme was not proposed to avoid the operation of any provision of Ch 6 of the Act. As Tiger’s lawyers, King & Wood Mallesons, put it to ASIC, by letter dated 16 December 2019:

The Scheme Company’s situation can be stated shortly as follows: it is expected that it will be insolvent in the very short term unless drastic measures are taken to reduce its debt burden and restructure its debt more generally. This is not just a company in need of funds. It is a company which would be likely in administration right now if not for the forbearance of the majority of its Senior Lenders in anticipation of the debt restructure being proposed under the Scheme. More importantly for the purposes of this letter, the Scheme Company’s equity has no value – current shareholders no longer have any real economic interest in the Scheme Company.

25 The updated evidence about Tiger’s financial position did not suggest that the position as to the value of shares in the company has changed materially.

26 Tiger noted that the 3 February 2020 order for publication of notice of the hearing for an order approving the scheme did not provide for publication at least 5 days before the date fixed for the hearing of the application, as required by r 3.4 of the Federal Court (Corporations) Rules 2000 (Cth) (Rules). In circumstances where all relevant creditors were notified of the scheme meeting and the evidence was that shareholders did not have any real economic interest in whether the scheme was implemented, I accepted that it was appropriate to abridge the time for service specified in r 3.4 to 19 February 2020.

27 Mr Goldberg certified that all conditions precedent had been satisfied other than those relating to the Court’s approval of the scheme; recognition of the scheme by the High Court of England; the orders of this Court approving the scheme or giving effect to the scheme becoming effective; and the provision of all necessary or desirable regulatory approvals.

28 As to the last matter, Mr Goldberg gave evidence of a delay in obtaining approval from the Democratic Republic of Congo to an indirect change of control of the “Borrower” as defined in the scheme. It was proposed that the scheme be amended so that satisfaction of this condition be a condition subsequent. Although it is usual for schemes to qualify for approval only after all conditions are satisfied, a condition which prevents the scheme coming into operation unless it is satisfied may be acceptable: In the matter of Wollongong Coal Limited [2020] NSWSC 73 at [47] to [49].

29 In the absence of any submission to the contrary from IFC, I accepted that the scheme (amended in the manner proposed including by the inclusion of the condition subsequent) is fair and reasonable and that full and fair disclosure has been made to the scheme creditors. I had no reason to doubt that Tiger has brought to the Court’s attention all matters that could be considered relevant.

30 It was appropriate that Tiger be exempted from compliance with s 411(11) of the Act where there was no proposed amendment to Tiger’s constitution.

CONCLUSION

31 For those reasons, I was satisfied that I should approve the scheme, subject to the alterations proposed by Tiger and make the other orders that I made on 21 February 2020.

I certify that the preceding thirty-one (31) numbered paragraphs are a true copy of the Reasons for Judgment herein of the Honourable Justice Gleeson. |

Associate: