FEDERAL COURT OF AUSTRALIA

Agnish Pty Limited v Folio Invest Pty Limited (No 4) [2020] FCA 120

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. The originating application filed on 12 June 2018 be dismissed.

2. The applicant pay the third respondent’s costs, as agreed or taxed.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

GRIFFITHS J:

Introduction

1 The applicant commenced these proceedings against three entities, namely Folio Invest Pty Limited (Folio Invest), Folio Property Pty Limited (Folio Property) and Mr Bradley Bilbie. After the proceedings were commenced and prior to the hearing, Folio Invest and Folio Property were both deregistered. Consequently, the applicant now proceeds against only Mr Bilbie, who was a director of both Folio Invest and Folio Property at all material times. Mr Bilbie represented himself in the proceeding.

2 The proceeding relates to an unsuccessful investment in a property development in August 2015 (Austral 1). The development was located at 95 Boyd Street and 1 Kelly St, Austral (Austral Project). The applicant’s investment in the Austral Project was by way of a loan agreement executed on 9 August 2015 (Loan Agreement). It will be necessary to say more about the Loan Agreement later but it is sufficient to note at this stage that the parties to that agreement did not include any of the three respondents.

3 In essence, the applicant contends that it entered into the Loan Agreement based upon representations made to it by Mr Bilbie on behalf of Folio Invest and/or Folio Property. The applicant complains that these representations regarding the Austral Project were misleading or deceptive in various respects. It complains that it relied upon those representations in entering into the Loan Agreement and that the representations were misleading or deceptive for the purposes of s 18 of the Australian Consumer Law (i.e. Sch 2 to the Competition and Consumer Act 2010 (Cth) (ACL)). In the alternative, the applicant contends that Folio Invest and/or Folio Property provided it with financial product advice which constituted a financial service for the purposes of s 12DA of the Australian Securities and Investment Commission 2001 (Cth) (ASIC Act) and s 1041H of the Corporations Act 2001 (Cth) (Corporations Act) and they engaged in misleading or deceptive conduct.

(a) Folio Invest representations

4 The representations which the applicant contends in its statement of claim were made by Mr Bilbie on behalf of Folio Invest were that, during the period 14 July 2015 to August 2015:

(a) the Austral 1 investment (to which the Loan Agreement related) would be “incredibly secure”;

(b) the Austral Project was significantly de-risked with a clear exit strategy;

(c) Folio Invest, Folio Property and/or Mr Bilbie were very capable; and

(d) the applicant would achieve a 40 percent return on the Austral 1 investment (Folio Invest Representations).

5 The applicant pleads that the Folio Invest Representations are partly oral and partly written. The oral part relates to the representation set out in [4(d)] above and was made by Mr Bilbie to Dr Arun Aggarwal on 30 July 2015. The written representations are said to have been recorded in an email from Mr Bilbie to Dr Aggarwal sent at 7:43 pm on 9 August 2015.

6 Dr Aggarwal is a director of the applicant and is a neurologist and chronic pain specialist. The applicant is the trustee of the self-managed superannuation fund known as Agni Super of which Dr Aggarwal is a member. He deposed that he is the person who is “solely responsible for making investment decisions for Agni Super and have done so on behalf of Agnish in the past”.

7 The Folio Invest Representations are said to have been misleading or deceptive or likely to mislead or deceive, in that:

(a) Agnish’s investment was not “incredibly secure”;

(b) the Austral Project was not significantly de-risked and did not have a clear exit strategy;

(c) Folio Invest, Folio Property and/or Mr Bilbie were not very capable; and

(d) the applicant would not achieve a 40 percent return on its investment.

8 In relation to its cause of action under the ASIC Act the applicant contends that, in making the Folio Invest Representations, Folio Invest provided financial product advice to the applicant and, accordingly, provided a financial service to it.

9 The applicant pleads that the making of the Folio Invest Representations contravened both s 12DA of the ASIC Act and s 1041H of the Corporations Act.

10 To the extent that the Folio Invest Representations were representations as to future matters, the applicant pleads that the representations were misleading or deceptive or likely to mislead or deceive as Folio Invest did not have reasonable grounds for making those representations.

(b) Folio Property representations

11 The applicant also contends that the following representations were made by or on behalf of Folio Property:

(a) Folio Property had an ability to guarantee a 30 percent annual return to investors;

(b) Folio Property had a proven system that enabled it to promise investors a 30 percent return;

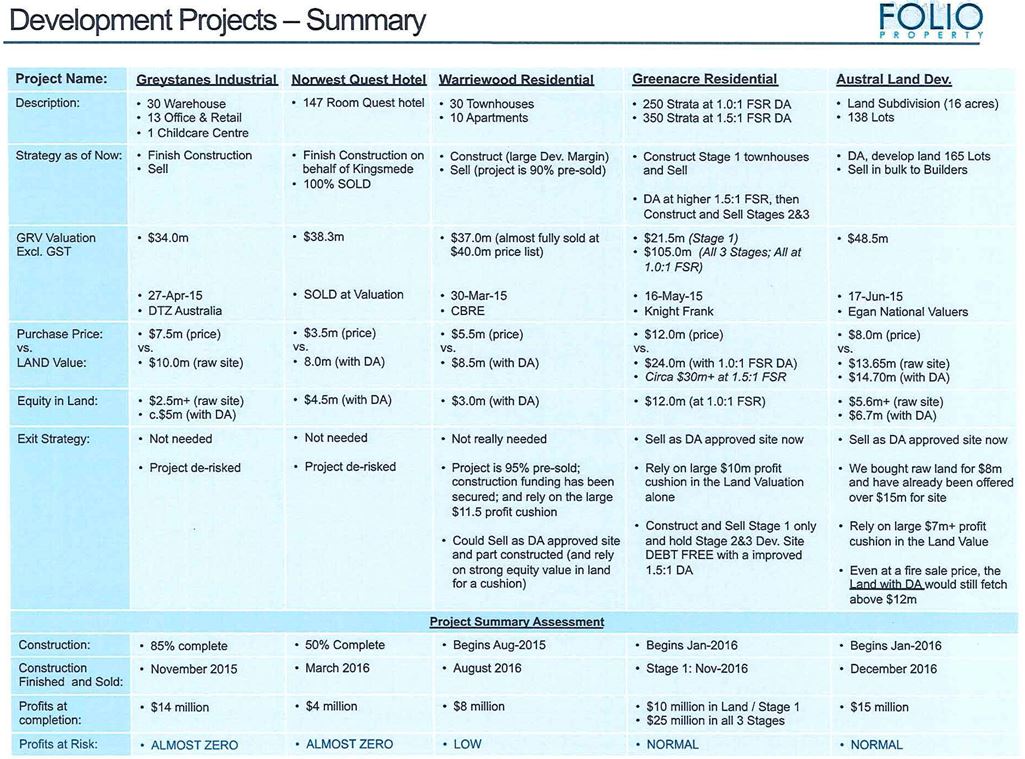

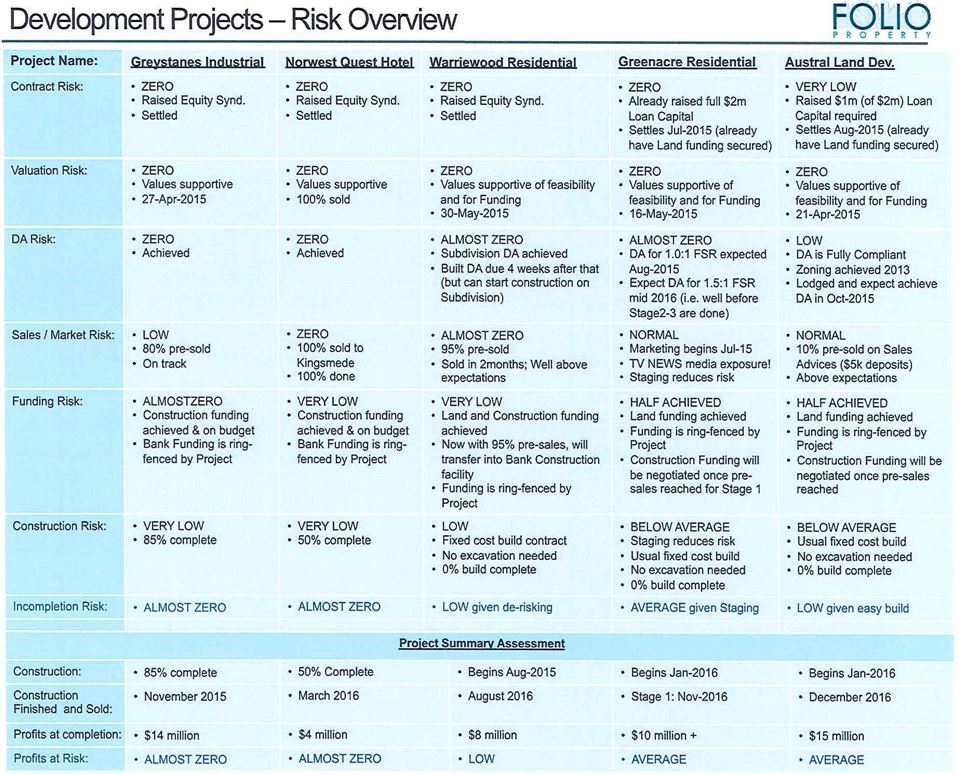

(c) the Austral Project would generate a profit of $18.5m;

(d) Folio Property was willing to offer security over assets in the form of developments which had an equity position of circa $40+ million; and

(e) Ms Jacqueline Anne Herps (Ms Herps) had a net asset position of circa $40m (Folio Property Representations).

12 The applicant contends that the Folio Property Representations are all contained in an undated brochure entitled “Folio Property”, and that Mr Bilbie was involved in the making of those representations. Moreover, it contends that the representations were misleading or deceptive, or likely to mislead or deceive, in that:

(a) Folio Property had no ability to guarantee a 30 percent annual return to investors;

(b) Folio Property had no proven system that enabled it to promise investors a 30 percent return;

(c) the Austral Project would not generate a profit of $18.5m;

(d) the assets over which the Folio Property was willing to offer security in the form of developments did not have an equity position of circa $40+ million; and

(e) Ms Herps did not have a net asset position of circa $40m.

13 The applicant contends that the making of the Folio Property Representations contravened s 18 of the ACL, s 12DA of the ASIC Act and s 1041H of the Corporations Act. To the extent that these representations were as to future matters, the applicant contends that they were misleading or deceptive or likely to mislead or deceive as Folio Property did not have reasonable grounds for those representations.

14 The applicant contends that it relied on the Folio Invest Representations and Folio Property Representations in proceeding with the Austral 1 investment and in entering into and performing its obligations under the Loan Agreement. It also contends that it has suffered loss and damage.

15 The applicant also initially pleaded a cause of action in negligence against Folio Invest alone. However, as the applicant now only presses the claims against the third respondent, Mr Bilbie, the claim in negligence has fallen away.

The applicant’s evidence

16 The applicant relied upon an affidavit dated 19 February 2019, affirmed by Dr Aggarwal.

17 Dr Aggarwal deposed that he received an email “out of the blue” from Mr Mogy of Folio Invest on 14 July 2015. Having regard to the content of the email, including the personal nature of its introduction, I think it more likely that it is a follow-up communication to earlier contact. The email stated that Folio Property worked “closely with an experienced developer who uses external funding for the early stages in a development funding opportunity” and that the “return is 30%p.a. on an 18-24 month term and is heavily securitised”. Under the heading “Returns & Structure” the email said that the structure was “as a loan agreement”, with a typical term of 18 months and with a fixed interest rate of 30 percent per annum. It stated that this “is a massive return which you will likely not find on the open market. You’d typically have to be a developer to make this much in a property”.

18 Under the heading “So, who are Folio Property?”, the email stated that “we have the deal structured via a loan agreement for simplicity, we have had the loan agreements independently vetted by lawyers for your protection”. With reference to the term “security”, the email stated “we love loan agreements allowing us to easily protect your position, we also secure you against our previous projects, all our development profit centres become guarantors for your loan”. At the end of the email was a section headed “Folio Invest Pty Ltd Disclaimer & Confidentiality Notice”. Relevantly, it stated:

The views of the author, either expressed or implied, may not represent the views of Folio Invest Pty Ltd… Every effort is made to ensure the accuracy of the information contained within this document. Folio have antivirus protection systems in place, however, no liability for any direct or indirect damage or losses, resulting from incorrect or misinterpreted information, or any form of virus activity contained herein will be accepted by any entity within the group…

19 There was a property brochure (Folio Property Brochure) attached to the email which Dr Aggarwal read and he said that it, along with the email itself, caused his interest in the Austral 1 investment. Key relevant features of the Folio Property Brochure may be summarised as follows:

(a) It was stated on page 3 that “[a]ll activity is structured as a loan agreement for your protection”.

(b) Also on page 3, Ms Herps was described as being a principal with Solstice Property Corporation, which is a property developer and development management specialist providing a wide range of services to facilitate the successful completion of a project.

(c) On page 4, it was stated: “We have confidence in our ability to guarantee a 30% annual return through our successful track record of developing our 5 step plan of property development”.

(d) On page 9, the Austral Project was described and the land value was specified as $8m and the profit was said to be $18.5m.

(e) On page 11, under the heading “Investment Opportunity”, it was stated that the investment needed was $1.5m, that the minimum investment was $100,000, and that the rate of return was 30 percent per annum over an investment period of 18 months.

(f) On page 12 of the Folio Property Brochure, the following information was provided under the heading “risk”:

RISK

Development Risks:

• There is a risk we do not get the approval done within the timeframe; however it is quite common to get extensions from the current land owner as typically both parties are motivated to settle the site as no one gets paid until it is settled. After the period if we weren't in a position to settle, the land owner probably wouldn't mind, for a small fee, to grant an extension. It is better to do that than take the property back to market and re-live another developer take (sic) another 12 months to do the same thing

• It will also be a fully compliant DA, meaning that the project will be built 100% within the rules of Council – therefore there are no reasons why it should not be a normal approval process. It is worth noting that Council's major source of revenue comes from when new dwellings are built.

• We can also settle without a Development Approval.

Construction Risks:

• Construction costs can blow out. A fixed price build contract will be put in place which will prevent this.

• Most of our sites don't have basement (sic). This is where complications and delays can occur.

• To ensure we get the best price for the build a tender process will be put to market

• Builders of this type of development must have a decent balance sheet, this will also be a pre-requisite from the funder.

Finance Risks:

• Always the key risk factor in any project. However due to the low LVR, obtaining funding should and has been relatively easy.

• We have funders that we have used in the past and there are others out there that will finance the land without a development approval (as long as it is lodged) up to 80% LVR.

Exit Risks:

• The current valuations are based off comparable sales that sold very quickly. We feel very confident that even if our DA was to get rejected (unlikely) that we could still sell the property within a speedy timeframe. We have an allocated amount of capital to spend on marketing.

(g) Under the heading “FAQ”, in response to Question 1: “It’s too good to be true, why is the return so high?”, it was stated that “We have a proven system that we have replicated many times and can thus promise our investors a 30%”, as well as stating that an investor:

… will sign a loan agreement with the development company that will state that you have a right to the agreed property and previous projects in the event of a default. The developer has a net asset position of $40 million but is looking for investors to help with cash flow to allow them to purchase more sites concurrently. The risk of default is mitigated as the developer only buys sites that are heavily undervalued.

(h) Question 5 of the FAQs was as follows:

Do I get a 2nd mortgage over the land?

A) You will sign a loan agreement with the development company that will state that you have a right to the agreed property and previous projects in the event of a default. The developer has a net asset position of $40 million but is looking for investors to help with cash flow to allow them to purchase more sites concurrently. The risk of default is mitigated as the developer only buys sites that are highly undervalued.

(i) Question 7 of the FAQs was as follows:

If the development were to go bust for some unforeseen reason am I liable for any losses?

A) Jacqueline Herps has a net asset position of circa $40 million, the funder will come after Jacqueline Herps not any of the individual lenders.

(j) Question 13 of the FAQs was as follows:

My lawyer and accountant say I shouldn’t do this. Who should I listen to?

A) Most lawyers and accountants have been trained to avoid any risk and consequently push away great opportunities that are presented to them. Many of them never reach financial freedom and continue to trade their time for money. We recommend you get advice from an accountant or lawyer that is also a wealthy investor. We believe this type of person will be able to give you a better perspective on the benefits and risks involved.

20 Dr Aggarwal described how on 14 and 15 July 2015 he had email exchanges with Mr Mogy in which he tested some of things Mr Mogy had mentioned. Dr Aggarwal said that he expressed his concern about such matters as the dwelling size in the Austral Project, to which Mr Mogy responded. Dr Aggarwal deposed that his preference in any investment was to take profit as a cash return instead of waiting for money. He deposed that, based on the further information and advice that he received from Mr Mogy in Mr Mogy’s email of 15 July 2015, he told Mr Mogy that he thought the Austral 1 investment sounded attractive and he was keen to have the applicant participate in it.

21 By an email dated 16 July 2015, Mr Mogy told Dr Aggarwal that the next step was for him to review the sample loan agreement, a copy of which was attached to the email. Mr Mogy told Dr Aggarwal that he “should take the time to review this and seek legal advice as appropriate”.

22 Dr Aggarwal described a telephone conversation he had with Mr Mogy on 21 July 2015 in which Dr Aggarwal provided him with the “proposed parameters of the extent of the Applicant’s potential involvement in the Austral 1 Investment”. They subsequently exchanged various emails in which Dr Aggarwal put forward different proposals to which Mr Mogy responded. The exchange included the following email which Dr Aggarwal sent to Mr Mogy on the evening of 21 July 2015 and which set out a revised investment proposal developed by Dr Aggarwal:

From: Dr Arun <… >

Sent: Tuesday, 21 July 2015 9:13:24 PM

To: Aitan Mogy

Cc: Arun Aggarwal

Subject: RE: Development Funding 30%p.a. Returns

Hi Aitan,

In consideration for a loan of $500,000 to the Austral land lot sub-division I request the following:

Proposal - $500,000 Loan

• Structured as a loan agreement

• Term - Typically 18 months (for the Austral site this will be up to 24 months paid pro-rata)

• Fixed interest rate of 20%p.a rather than 30%pa.

• Principal and interest is paid at the end of the loan term.

• Previous projects act as guarantors for your funds to secure your position

ie

• A cash return of 20%p.a (rather than 30%p.a) on the $500,000 to be paid at the end of the term (18 months fixed term+ optional 6xl monthly extensions)

ie 18 months = $ 660,000

Plus

• 2 x 300m2 land lots within the Austral subdivision (combined cost value of $240,000)

If this proposal is approved, I am in a position to sign the loan agreement and to transfer these funds on Monday 3rd August (when fixed deposit matures).

Hope you can get this done before your ski holiday.

Arun Aggarwal

23 Further emails were exchanged on 22 July 2015. Dr Aggarwal was attempting to change in his favour the terms and conditions of any investment, however, Mr Mogy responded by saying that the proposed changes either were not or would not be acceptable to the developer for the reasons he explained. Mr Mogy and Dr Aggarwal were plainly negotiating the terms upon which the applicant might make an investment in the Austral Project.

24 The two emails Mr Mogy sent to Dr Aggarwal on 22 July 2015 contained the following information and disclaimer (copied exactly):

… Want 9%p.a. returns paid monthly? – www.partnerlend.com.au

Want 30% p.a. returns paid at end of 18 month term? – www.folioproperty.com Folio Invest Pty Ltd Disclaimer & Confidentiality Notice The views of the author, either expressed or implied, may not represent the views of Folio Invest Pty Ltd “Folio” (ACN 150 171 252). Every effort is made to ensure the accuracy of the information contained within this document. Folio have antivirus protection systems in place, however no liability for any direct or indirect damages or losses, resulting from incorrect or misinterpreted information, or any form of virus activity contained herein will be accepted by any entity within the group. Recipients are urged to implement their own virus protection strategy. This email message contains information that is legally privileged and/or confidential. If you are not the intended recipient, you are notified that any unauthorized disclosure, copying, distribution or use of this information is strictly prohibited. If you have received this message in error please notify us by return email or phone...

25 Dr Aggarwal deposed that his first contact with Mr Bilbie was by way of an email he received from him on 29 July 2015. The email was sent by Mr Bilbie after Mr Mogy asked Mr Bilbie to call Dr Aggarwal in circumstances where, in an email to Mr Bilbie earlier that day, Mr Mogy had described Dr Aggarwal as having “unrealistic expectations of his return”.

26 This is a clear reference to Dr Aggarwal’s attempts to vary the terms of the proposed investment. Mr Bilbie emailed Dr Aggarwal and stated that he would call him later that day. He added:

I simply cannot include a block of land worth $330,000 on top of your interest. Often when you present someone with a good deal that doesn’t mean that we are desperate or that there is a huge amount of room to move. You will not find a return anywhere like what we are offering cause you are dealing direct and in this case with the boss…”.

27 Dr Aggarwal deposed that he had a telephone conversation with Mr Bilbie on 30 July 2015, in which words to the following effect were said:

Brad Bilbie: Arun, I've been involved in a number of development projects including the one in Warriewood. For Austral, the land valuation came back as $16.4 million. I'm buying this for only $4 million so $10 million has already been made. Once the development application goes through in 18 months, there will be another $4 to $5 million dollars in profit.

Arun Aggarwal: I would want to add a block of land as security to the deal just in case the deal goes bad. At least I will have title on the property.

Brad Bilbie: Arun, please understand that I cannot simply include a block of land worth $330,000.00 on top of the 30% interest. If you lent $500,000.00 you will get a 40% return in 18 months and what we would like to do is consider another development, Austral 2, which is 30% and has a profit share.

Arun Aggarwal: Brad, this is my first investment with you. I will go with the Austral 1 deal of $500,000.00 and we will look at the next deal in due course.

28 On 30 July 2015, after their telephone conversation earlier that day, Mr Bilbie sent Dr Aggarwal an email as follows:

From: Brad Bilbie

Sent: Thursday, 30 July 2015 1:54 AM

To: ‘agnish …’

Subject: Folio Property revised offering

Hi Arun,

Nice chatting with you earlier.

Further to our discussion I can do the following for you:

- Austral 1:

o $500,000 loan amount

o 40% p.a. interest rate

• Rate will increase to 50% if Austral 2 proceeds

o Return over 18 months $800,000 ($875,000 @ 50%)

- Austral 2:

o $2,000,000 loan amount

o 30% interest rate

o 10% profit share - please see 3rd attachment (conservative feasibility)

o Return over 18 months

• $2,900,000 principal and interest

• $1,000,000 profit. $1,500,000 if 80 units developed.

• Total circa $4,000,000+ return or 100%

See attached Agent Appraisal shows land value at $16.4 million, please note our buy price was $4 million. Expected profit without developing circa $10m, with developing the 80 units there is a further $4 - 5 million profit.

Please see 4th attached brochure and refer to our website www.partnerlend.com.au

- Background: Partner Lend is a private finance company that provides lenders with a high monthly cash flow and a secured position. This business specialises in providing fully secured loans to qualified businesses on a short term basis. Funds are lent strictly on a business to business basis and we only provide loans to borrowers with sufficient security. Money is lent out through our other lending company www.businesslend.com.au

- Return and term: Investors receive a 9% p.a. return paid monthly. Loan agreements are a minimum of 3 months and money can be withdrawn with 30 days' notice

• Example $1.000,000 = $90,000 profit p.a.= $7,500 paid monthly

• Security: Via the loan agreement we provide a head corporate guarantee on your funds, lender also becomes a registered secured creditor for each individual loan on the PPSR (personal property securities register). A typical loan might be $100,000 and the security for that loan would be – charge over company, personal guarantee, stat dec for appropriate use of funds and affordability, all of their personal assets (second mortgages, caveats), no security = no loan. We have set up this way to allow you to have a guarantee backed up with a tangible registered secured asset.

- Bonus: Upon lending/investing $500,000 or more in Folio property you will be awarded a 12% rate for Partner Lend on any amount lent

• Partner lend works extremely well for your line of credit as it pays monthly interest on the 1st of every month. If you can access funds at circa 4% you are then getting a 200% arbitrage position – very smart!

Best regards,

Brad

<image001.jpg> <image002.jpg>

Bradley Bilbie | Director Check out our latest video here

Folio Invest Pty Ltd

…

Want 9% p.a. returns paid monthly? - www.partnerlend.com.au

Want 30% p.a. returns paid at end of 18 month term? - www.folioproperty.com

Folio Invest Pty Ltd Disclaimer & Confidentiality Notice

Folio Invest are not Financial Advisers, nothing stated in any phone or email communications (including attachments) should ever be construed as such. The views of the author, either expressed or implied, may not represent the views of Folio Invest Pty Ltd (ACN 150 171 252). Every effort is made to ensure the accuracy of the information contained within this document. The information set out in this document has been prepared using information derived from a variety of external sources. Folio Invest does not warrant the accuracy of any of the information and does not accept any legal liability or responsibility for any injury, loss or damage incurred by the use of, or reliance on, or interpretation of the information contained herein. Folio have antivirus protection systems in place, however no liability for any direct or indirect damages or losses, resulting from incorrect or misinterpreted information, or any form of virus activity contained herein will be accepted by any entity within the group. Recipients are urged to implement their own virus protection strategy. This email message contains information that is legally privileged and/or confidential. If you are not the intended recipient, you are notified that any unauthorized disclosure, copying, distribution or use of this information is strictly prohibited. If you have received this message in error please notify us by return email or phone....

29 Dr Aggarwal deposed that he felt he could rely on Mr Bilbie’s assurances about the returns that would be achieved because it appeared to him that Mr Bilbie, and the Folio companies, “were experienced and knew the field”.

30 Dr Aggarwal referred to various other emails exchanged between he and Mr Bilbie in the period 1 to 10 August 2015. They included an email which Dr Aggarwal sent to Mr Bilbie on 1 August 2015, in which he said that he was happy to proceed and that he was “[j]ust waiting for final OK from legal”. He told Mr Bilbie that if he “want[ed] to start preparing necessary documents, that would be fine”. Mr Bilbie responded with an email dated 3 August 2015 in which he said that Dr Aggarwal should “make sure you get legal advice around the contract only, sometimes lawyers like to go outside their obligations and give generalised investment advice such as, I would be very cautious with anyone paying 30%, these types of things I have heard about being risky”. He told Dr Aggarwal that if his lawyer wanted to “go down that path they would need to spend at least 30 mins on the phone with me otherwise they will simply not have a clue what they are talking about”.

31 On 6 August 2015, Mr Bilbie sent a copy of the Loan Agreement signed by the counterparties. The next day, Dr Aggarwal wrote back seeking further information. In particular, Dr Aggarwal asked for documents stating the “value of the properties that are being used as security” and the “debt loaded against the companies/properties being used as security”, as well as balance sheets and profit/loss statements for the previous two years forall of the borrowers and guarantors.

32 On Sunday 9 August 2015 at 5:55 pm Mr Bilbie emailed Dr Aggarwal and attached a valuation of the properties at 95 Boyd Street and 1 Kelly Street which was described in Mr Bilbie’s email as the “property owned by Rein developments”. Mr Bilbie stated that the he properties were valued at $13.6m (in line with the $13.65m stated in the valuation document) and the purchase price was stated to be $8m. Mr Bilbie also provided Dr Aggarwal with a balance sheet for Ms Herps and stated that he had individual valuations which could be provided via dropbox for each of the properties associated with each of the corporate guarantors.

33 Mr Bilbie also attached to his email a document on Folio Property letterhead which provided information relating to the Austral 1 Project, as well as four other development projects relating to Greystanes Industrial, Norwest Quest Hotel, Warriewood Residential and Greenacre Residential (the Analysis). The summary section of the Analysis contained the following two pages (the information concerning the Austral 1 Project is in the last column):

34 It is to be noted that the Analysis was provided to Dr Aggarwal on 9 August 2015, being the same day on which the Loan Agreement was executed. It is clear from the further email correspondence of 9 August 2015 detailed immediately below at [35] to [37] that the execution of the Loan Agreement took place after Dr Aggarwal received the Analysis.

35 Dr Aggarwal responded to Mr Bilbie’s email attaching the Analysis on the same day with an email at 7:18 pm. After acknowledging the additional information he received from Mr Bilbie, he said:

As you can imagine, I am apprehensive when providing essentially a $500,000 “unsecured loan”.

As the money is coming out of my Super Fund, the investment decision will be audited.

In faith, I trust that you are an ethical businessman and will stand behind your return, given that you are the Boss and the person responsible.

36 Mr Bilbie replied shortly thereafter at 7:43 pm:

Thank you for your confidence in me and my team – you are in very capable hands and my moral and ethical obligations will always see you win.

Technically it can be argued the loan is unsecured only because you do not have a registered mortgage however is it (sic) incredibly secure, our equity position cannot be denied. All our projects are significantly de-risked and have clear exit strategies.

About half of our clients invest through superannuation – it’s a very wise move.

Will you be sending the signed agreement and completing the transfer tomorrow?

37 Mr Aggarwal responded at 9:38 pm as follows:

Loan agreement signed.

Money will be transferred as $400,000 from Super Fund and $100,000 from another account

38 Dr Aggarwal signed the Loan Agreement on behalf of the applicant with inter alia Rein Developments Pty Ltd. Other parties to the Loan Agreement were the Guarantor, which was defined as comprising five separate entities, including Ms Herps. Dr Aggarwal deposed that on 11 August 2015, the applicant transferred $500,000 under the Loan Agreement to Rein Developments.

39 The Loan Agreement did not contain any provision for securing the loan. Instead there was a clause entitled “Alternative Repayment” (clause 5.6), which provided as follows:

5.6 Alternative Repayment

(a) As an additional obligation of the Guarantor to the rest of this clause 5, in the event that the Company cannot repay the Outstanding Principal in full to the Financier on the Repayment Date then the Guarantor will ensure that the Financier is paid an amount equal to the Outstanding Principal, as a priority payment, from property development or investment projects to which the Guarantor or any Associate of the Guarantor is a party or investor namely;-

(i) development at Lot 6050 Norbrik Drive Bella Vista,

(ii) development at 53A & 53B Warriewood Road Warriewood,

(iii) development at 225 & 231-241A Hume Highway, 24 Hillcrest Avenue and 112 Northcote Road Greenacre,

(iv) development at 2-4 Picrite Close Pemulwuy, and

(v) any other property owned by the Company and/or the Guarantor.

(b) Neither the Guarantor nor any Associate of the Guarantor will take any profits or income out of any of those projects until such time as the Financier has been repaid the Outstanding Principal in full.

(c) The Guarantor represents, warrants and undertakes to the Financier that it or she (as the case may be) will not seek to assign, transfer or otherwise dispose of its or her (as the case may be) interest in any of the above developments and must ensure that all Associates of the Guarantor act in the same way.

(d) If an Event of Default has occurred, the Guarantor agrees that such default gives the Financier an interest in land under the Real Property Act 1900 (including an interest as chargee) by which the Financier may lodge a caveat against the title to the Relevant Property in order to further secure its rights under this document.

40 As the clause itself makes clear, the Loan Agreement did not provide for security in the traditional sense. Rather, there were separate guarantees provided by the various entities interested in the property developments and those entities were obliged to have recourse to their interests in the property developments in satisfaction of any obligations owed by them as guarantors. The only part of the clause that conferred anything resembling security was cl 5.6(d) which created an equitable charge on the occurrence of an event of default which could then be used to lodge a caveat against the relevant property. No similar obligation (i.e. to have recourse to any interest in property the subject of the Austral Project) was imposed on Rein Developments, the direct counterparty under the contract.

41 Another relevant feature is the term of the loan. Although the repayment date was specified as 18 months from the date of execution, the contract made provision for the lender to extend the repayment date by a further 6 months (i.e. up to a date two years after execution of the Loan Agreement). Extensions were in the lender’s sole discretion.

42 Payment of interest on the loan was to coincide with repayment of the principal on the repayment date.

43 Proceedings were brought by the applicant in 2017 in the Supreme Court of New South Wales against the “Guarantors” under the Loan Agreement. Although the company was successful in obtaining a judgment in February 2018 in the amount of approximately $1.2m in those proceedings, no steps were taken to enforce the judgment, evidently because searches indicated the Guarantor had no assets from which the judgment debt could be recovered.

44 Dr Aggarwal particularised the loss and damages suffered by the applicant in the total amount of $1,239,383.56 as comprising:

(a) $500,000 principal advanced under the Loan Agreement;

(b) $300,000 representing the accrued interest under the Loan Agreement and noting that no amount of that interest has been paid;

(c) $404,383.56 representing the accrued interest under the Loan Agreement between the period of 9 February 2017 to 18 February 2019 (calculated at $547.95 per day);

(d) $35,000 in respect of enforcement costs against the Guarantors of the Loan Agreement.

45 Paragraphs 29-40 of Dr Aggarwal’s affidavit were not read. Those paragraphs related to events which occurred after execution of the Loan Agreement. After the applicant’s counsel belatedly said that he wanted to withdraw the related documents from Exhibit 1 to which those unread paragraphs related, Mr Bilbie tendered those documents as Exhibit B (i.e. Tabs 21-29 to Dr Aggarwal’s affidavit).

Dr Aggarwal’s cross-examination summarised

46 Although I do not doubt Dr Aggarwal’s honesty, I did not find his evidence to be entirely reliable. He found it difficult to articulate the precise nature of the alleged misleading or deceptive conduct. When pressed in cross-examination, it emerged that his central grievance seemed to relate to what happened after he executed the Loan Agreement. In particular, he was upset that he had effectively been strung along by Mr Bilbie because it was not until mid-2017 that he learned that financing for the Austral Project had fallen over back in 2015. Dr Aggarwal also placed particular emphasis on the reliance he placed on what Mr Bilbie said due to his description of himself in the 29 July 2015 email as being the “boss” (extracted above at [26]), which again is not part of the pleaded case.

47 This presents a difficulty for the applicant as this particular conduct is not the pleaded conduct in the statement of claim. The pleaded case relates entirely to the Folio Invest Representations and Folio Property Representations which were made prior to Dr Aggarwal executing the Loan Agreement on 9 August 2015.

48 Another aspect of Dr Aggarwal’s evidence relates to [33] of his affidavit, which was not read. It was, however, tendered by Mr Bilbie and became Exhibit C. Dr Aggarwal stated there that on 27 September 2017 at 11:08 am he received an email from Mr Bilbie which provided a report in respect of various development projects, including the Austral Project. Dr Aggarwal’s original evidence was that he “read the report and formed the view that Agnish’s investment was at risk”. The difficulty is that Dr Aggarwal’s oral evidence was to the effect that he had no recollection that he had read the document. He stated he “I would have received this and I may or may not have even opened the attachment to read it, because there was so much in it.” Indeed, Dr Aggarwal stated that it was unlikely that he had done so given the way in which it was addressed as simply “Hello”. He said that it was not his habit to spend time reading such impersonal communications. This is at odds with his original affidavit as filed.

49 A further difficulty stems from [5] of Dr Aggarwal’s affidavit, where he described Folio Invest as “an advisory and brokerage firm offering financial resources, consultancy, and investment products”. When asked in cross-examination where he obtained that impression from, he said that these were the words of his lawyers. After the Court pointed out that it was his affidavit, not his lawyers’, Dr Aggarwal said that it is known that affidavits are prepared by lawyers. He did not seem to grasp the fact that by his affirmation of the affidavit he alone had accepted responsibility for its contents.

50 Another troubling part of Dr Aggarwal’s evidence related to the inadequacy of his answers to the question why he considered the Folio companies to be providing financial advice. He referred to Mr Bilbie’s email dated 3 August 2015 (see [30] above], where Mr Bilbie said that he would need to spend at least 30 minutes talking to Dr Aggarwal’s lawyer if the legal advice went beyond the strictly legal parts of the Loan Agreement. Dr Aggarwal said that he inferred from this offer that Mr Bilbie would provide financial advice to the lawyer. That is most unconvincing. Furthermore, the standard Folio Invest disclaimer which appeared at the end of Mr Bilbie’s emails explicitly stated that Folio Invest was not a financial advisor (see wording of the disclaimer at [28] above). Dr Aggarwal accepted that he did not provide any of his personal financial details to the Folio companies, as would be expected (and required) if they were providing financial advice. He also confirmed that he had never asked his lawyer to speak with Mr Bilbie and to take up the offer set out in Mr Bilbie’s email. It is true that the disclaimer in Mr Mogy’s emails is differently worded and does not explicitly state that Folio Invest is not a financial advisor.

51 I am satisfied that Dr Aggarwal should be viewed as a sophisticated investor. This is evident from his acceptance of the fact that he has an annual income of more than $250,000 and has assets worth more than $2.5m. It is also evident that his superannuation fund has been extensively involved in many investments, largely determined by him. He confirmed that the fund had one investment apartment as well as having investments in three different managed funds and a share portfolio. He confirmed that he did not have a financial advisor and that he personally had made all the investment decisions for the Super Fund.

52 Dr Aggarwal’s investor sophistication is also demonstrated by the pre Loan Agreement negotiations he conducted when he sought to address the lack of security on the loan by asking for two blocks of land.

53 Another troubling aspect of Dr Aggarwal’s evidence is that it only emerged during the course of cross-examination that he wrongly assumed that Mr Bilbie was a director of Rein Developments and/or some of the Guarantor companies. Dr Aggarwal plainly thought this was the case until the position was clarified in cross-examination. This serves to underline that Dr Aggarwal’s grievance arises in part from a deficient understanding of his investment and a desire to hold someone else responsible for his loss.

54 In cross-examination, Mr Bilbie tried to get Dr Aggarwal to accept that he (i.e. Mr Bilbie) had been moral and ethical and had sought to keep him informed of how the development progressed. Dr Aggarwal repeated that it was not until mid-2017 that he found out that the financing had not been secured for the Austral Project to proceed to settlement. It appeared that one of the financiers withdrew shortly after 9 August 2015 and this caused the development to fail. Dr Aggarwal did not learn of these developments until mid-2017 and he appeared angry that he was left in the dark.

55 When asked to identify the misleading or deceptive conduct the subject of his grievance, Dr Aggarwal said that it was not an email from Mr Bilbie dated 25 July 2017 that he first became aware that the other projects were not profitable and that the financier for the Austral Project had withdrawn. As noted, this is not the pleaded conduct.

56 In his cross-examination of Dr Aggarwal, Mr Bilbie emphasised the details of the Analysis extracted above at [33] where the risks were identified and information provided about the other projects. When asked in cross-examination whether Dr Aggarwal thought that there were any lies in that information, Dr Aggarwal said that it was all “conjecture”. He repeated that he was upset that it was not until mid-2017 that he found that the funding for the Austral Project had fallen over.

57 In re-examination, Dr Aggarwal was taken to Mr Bilbie’s email of 9 August 2015 at 7.43pm (see [36] above). Relying on this email he said that the particular statements alleged to be misleading or deceptive were that:

(a) the investment was “incredibly secure”;

(b) “our equity position cannot be denied” (saying he interpreted that as a representation there was “$40 million that was backing his company”);

(c) the other projects were “significantly derisked”; and

(d) there was a “clear exit strategy”.

58 Dr Aggarwal was also taken to [5] of his affidavit. He confirmed that the information referred to there regarding Folio Invest being an advisory firm came from what he viewed on the Folio Property website. When it was put to him that this was a different company, he simply said that they were interlinked.

59 Significantly, in re-examination Dr Aggarwal confirmed that he had carried out his own research into Austral. He said he had been looking at that area for a while and wanted to buy a property there because of its proximity to the Badgerys Creek airport and that it was an “up and coming area”. This further underlines his relative sophistication as an investor.

60 Although the Court extended the hours of sitting on the first day of the hearing (which had only been listed for one day), it was evident that if the hearing continued on that day the cross-examination of Mr Bilbie would take more than two hours and that Mr Bilbie wished to tender further material. After discussion, it was agreed that any further evidence to be tendered by Mr Bilbie should occur by 3 January 2020, the applicant had until 17 January 2020 to respond and any objections to further tendered material had to be filed and served by 31 January 2020. The hearing was adjourned to 11:30 am on 4 February 2020, with the cross-examination of Mr Bilbie limited to 90 minutes (i.e. 1 pm), with the respective closing addresses being no more than one hour and with 15 minutes for the applicant’s reply. These timelines were imposed in order to ensure that the matter finished within the second day in circumstances where Mr Bilbie was forced to defer his return to Sierra Leone.

The respondent’s evidence summarised

61 Mr Bilbie affirmed two affidavits, one dated 1 May 2019 and the other dated 17 January 2020. In his first affidavit, Mr Bilbie deposed that Folio Invest and Folio Property offered “residential real estate for sale under a Corporate Real Estate Licence”. He described how these companies expanded their operations to enable property development funding opportunities to occur by way of a loan. He said that this enabled the developer to pay soft costs, such as the cost of reports which were required to be lodged with a development approval application. It was evident that Mr Bilbie had a background in real estate.

62 Mr Bilbie said that neither of the companies offered “any financial products and do not operate under an Australian Financial Services Licence which is required to offer financial products to the market”.

63 Mr Bilbie submitted that the property development funding opportunity taken up by the applicant as not being a financial product, but rather a loan. Mr Bilbie submitted that Dr Aggarwal was “a sophisticated investor as determined by all of the relevant ASIC definitions in any event”. Mr Bilbie submitted that, on this basis, Dr Aggarwal was well aware of what he was getting into and that he “negotiated at every point trying to restructure the deal which clearly showed his experience”.

64 Mr Bilbie also submitted that Dr Aggarwal was encouraged to get legal advice and that he obtained such advice and was aware that it was an unsecured loan. He further submitted that Dr Aggarwal was evidently aware that a 40 percent per annum return contained an element of risk.

65 Mr Bilbie added that as at 9 August 2015, when the Loan Agreement was executed, the properties at 95 Boyd Street and 1 Kelly Street Austral were under contract for a total purchase price of $8m, that finance to complete the purchase of the Properties had been approved and mortgage documents signed and returned to the mortgagees’ solicitors in anticipation of the purchase of the properties being completed.

66 Mr Bilbie said that at the relevant time the loan was considered to be secure as the two properties had a valuation with a large equity increase exceeding $5m. He submitted that if the properties had secured development application approval and pre-sales had been achieved as was intended, with the development occurring in accordance with those approvals, “then the uplift in value of the Properties would have been even greater than that”.

67 Mr Bilbie submitted that it was likely that the applicant would have received the agreed return if completion of the purchase of the Properties had been effected and the development had been finalised.

68 Mr Bilbie submitted that when the Loan Agreement was entered into, the Guarantors either owned, or had entered into, legally binding arrangements to acquire the properties referred to in the alternative repayment clause of the Loan Agreement (being cl 5.6). There was no evidence to the contrary.

69 As mentioned, Mr Bilbie also relied upon an affidavit affirmed by him on 17 January 2020. Attached to it were various documents which he said provided a reasonable basis for some of the representations pleaded against him. One of the annexures was a statement dated 23 June 2014 from an accountant, Mr John Grego, who stated that an attached statement of assets and liabilities for Jacqueline Herps represented a true and fair value of her current financial position as at 23 June 2014. The attached one page document entitled “Jacqueline Herps assets and liabilities” stated that Ms Herps had net assets of $38m.

70 Mr Bilbie provided a statement dated 23 June 2016 on Solstice Property Corporation Pty Ltd letterhead, which was signed by Ms Herps, and which annexed a statement of her assets and liabilities as at 23 June 2016. Her net assets were stated to be $39,380,000.

71 Mr Bilbie relied upon a document entitled “Background Paper 6 (Part C)” and “Financial Products Available to Retail Investors” published by the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. He relied in particular on what that publication said concerning the definition of “Financial Product”.

72 In support of his submission that providing credit in the form of a loan is not a financial product, Mr Bilbie pointed to reg 7.1.06 of the Corporations Regulations 2001 (Cth).

Mr Bilbie’s cross-examination

73 Mr Bilbie was subjected to a lengthy cross-examination when the case resumed on 4 February 2020. It has to be said that the cross-examination appeared at times to be rather unfocussed and unproductive. It is also appropriate to say at this point that I found Mr Bilbie to be a truthful and responsive witness. He answered the questions asked of him frankly and responsively, notwithstanding that many of them were somewhat obtuse and understandably caused him some frustration.

74 The key relevant points to emerge from Mr Bilbie’s cross-examination may be summarised as follows. First, Mr Bilbie was taken to a series of emails which Mr Mogy sent to Dr Aggarwal in July 2015, as well as the Folio Property Brochure which was annexed to Mr Mogy’s email dated 14 July 2015. It was put to Mr Bilbie that the various representations made in that material were effectively adopted by him, because Mr Mogy forwarded that material to him on 29 July 2015. In response, Mr Bilbie emphasised that the information which had been provided to Dr Aggarwal prior to that date was given on the basis that it was not final and that a proposal was to be put to him after 14 July 2015, as was emphasised in Mr Mogy’s email of that day. In substance, Mr Bilbie said that the loan proposal which was put to Dr Aggarwal was not immutable as at 14 July 2015, but rather evolved thereafter, as is made plain from the terms of Mr Mogy’s email dated 14 July 2015 in which he foreshadowed that a proposal would subsequently be put to Dr Aggarwal. I accept that evidence.

75 Secondly, when it was put to Mr Bilbie that the Folio Property Brochure stated at page 9 that the Austral site had been exchanged in January 2015. Mr Bilbie agreed but added that it was not claimed that the site was owned as at the date of that Brochure. He pointed to the fact that on page 9 of that Brochure it was stated that “Site exchanged in January 2015”. I accept that evidence.

76 It might also be noted that the Court raised with Mr Tiliakos the relevance of any question about whether there had been a representation concerning the developer owning the site, because it was not one of the pleaded representations. In response, Mr Tiliakos said that the point was encompassed in all the matters raised in [6] and [15] of the statement of claim.

77 Thirdly, after Mr Bilbie’s attention was drawn to the relevant contracts for sale concerning the Austral land which indicated that the proposed settlement date was 30 June 2015, he was asked whether he told Dr Aggarwal prior to him entering into the Loan Agreement on 9 August 2015 that settlement had not in fact occurred at that date. In response, Mr Bilbie pointed to an email which he sent to Dr Aggarwal on 9 August 2015 at 5:55 pm, and shortly before Dr Aggarwal signed the Loan Agreement. In his email, which was sent on 9 August 2015 at 5:55 pm, Mr Bilbie provided Dr Aggarwal with a copy of a valuation for the Austral property and stated that it “settles on Wednesday”. He said that this showed that he had informed Dr Aggarwal that the property had not settled as planned, but was expected to settle on 12 August 2015. Mr Bilbie also said in that email that the valuation showed the property as valued at $13.6m and that the purchase price was $8m. Mr Bilbie provided Dr Aggarwal with a detailed analysis of various projects, including the Austral project (being the Analysis referred to at [33] above), as well as a balance sheet for Ms Herps (i.e. the balance sheet signed off by the accountant, Mr Grego). Part of the Analysis was headed “Development Projects – Risk Overview”. This section stated that it was expected that there would be a profit of $15m on completion of the Austral project.

78 Fourthly, when it was put to Mr Bilbie that he was supplying a financial product he firmly denied that proposition. He said that the Folio Property Brochure provided to Dr Aggarwal on 14 July 2015 was not investment advice, that he was not an investment advisor and he did not hold a financial services licence. Mr Bilbie drew attention to page 3 of that Brochure which described Folio Property as raising “funds for soft costs of property development and offers guaranteed high returns to investors… all activity is structured as a loan agreement for your protection”. He mentioned parts of the Folio Property Brochure which dealt with the subject of risk, including development risks, construction risks, finance and exit risks.

79 Mr Bilbie also drew attention to and was cross-examined on that section of the Folio Property Brochure which dealt with frequently asked questions. That section included statements that investors were asked “to loan us the funds for minimum of 18 months” and that “we recommend you get advice from an accountant or lawyer that is also a wealthy investor. We believe this type of person will be able to give you a better perspective on the benefits and risks involved”.

80 Fifthly, Mr Bilbie was asked questions regarding copies of emails which were forwarded to him by various third parties on 23 December 2019 in the course of the first day of the hearing and which ultimately led to the proceeding being adjourned because the applicant said it had insufficient time to respond to the material. This material was ultimately tendered as Exhibit 2. Mr Bilbie explained that he had not provided the material earlier because his computer which stored the material had been stolen in Africa and he was not aware until shortly before the hearing that the applicant contested the issues to which the material related.

81 It was put to Mr Bilbie in cross-examination that he was not previously aware of the contents of the various emails that were forwarded to him on 23 December 2019 and that he had no reasonable basis for making the relevant representations at the time they were made in 2015. Mr Bilbie firmly rejected that proposition. He said that he was aware of the entire finance process, including the fact that, at the time Dr Aggarwal executed the Loan Agreement, finance had been approved and that mortgage documents had been signed, which meant that it was “significantly de-risked in my eyes and in most people’s eyes”, not the least because the executed mortgage documents were binding legal agreements. I accept that evidence.

82 Mr Bilbie also said that, as at 9 August 2015, he believed that the project would proceed, relying in part on an email from Gadens Lawyers. In that email, a senior associate at Gadens sent a letter to the financier which said that “funds have been ordered and are being transferred in time for settlement which is being targeted for next Wednesday, 12 August 2015”. Mr Bilbie said that he was aware of this information at 9 August 2015. I accept that evidence. It is corroborated by the terms of his email dated 9 August 2015 at 5:55 pm which he sent to Dr Aggarwal.

83 Sixthly, when it was put to Mr Bilbie in cross-examination that he had no reasonable grounds to say in his email of 9 August 2015 at 7:43 pm that the loan was “incredibly secure, our equity position cannot be denied” and that all “our projects are significantly de-risked and have clear exit strategies”, Mr Bilbie disagreed. He said that the statements were “100 hundred percent accurate at the time”. Mr Bilbie explained that he relied upon the information contained in Gadens email dated 7 August 2015 and also on his belief at that time that the financing of the project had been finalised. He said that it was not until after 9 August 2015 that he learned that authorities had prevented a significant amount of funds which were intended for the project being brought to Australia. I accept that evidence.

84 Seventhly, it was put to Mr Bilbie that there was no reasonable basis for the statement in the Brochure that Folio Property had “confidence in our ability to guarantee a 30% annual return through our successful track record of implementing our 5 step plan of property development”. In response, Mr Bilbie said that he relied upon the valuation by Egan, as well as his own research, including accessing comparable sales on websites, and his experience as a former real estate agent in valuing the property. He said he had also taken into account other similar successfully completed projects. When Mr Bilbie’s attention was drawn to the disclaimer in the Egan valuation document, he said that he nevertheless took the valuation into account, including Egan’s solid business reputation, as well as his own research of comparative sales. In addition, he said that he took into account Mr Grego’s letter and attached balance sheet, together with his own knowledge of some of the previous projects in which Ms Herps had been involved. Mr Bilbie acknowledged that the financial information provided by Solstice Property Corporation was dated a year after the Loan Agreement was executed.

85 Eighthly, when Mr Bilbie was pressed on the basis of the statement in the Folio Property Brochure and elsewhere that the return on the loan is 30 percent per annum on an 18 to 24 month term and heavily securitised, he responded by saying that there was “a lot of equity in the existing project, and the current project, as we’ve already shown you, on an as is basis, before even the development approval before construction was $5.6m”. I accept this evidence.

86 Ninthly, when Mr Bilbie was challenged on the basis of the statement in the Folio Property Brochure that the loan was “heavily securitised”, he said that he believed that this was true and supported by the fact that there were multiple guarantors for the project and that other similar projects had proceeded to completion. Mr Bilbie further responded by referring to “the equity position across the principal company he lent to, and all the existing ones which had already settled, plus the personal guarantee from the Developer comprised a very large level of security”. I accept that that this was his honest opinion and that there was a reasonable basis for it.

Consideration and determination

87 In closing address, Mr Tiliakos correctly acknowledged that if the applicant failed to establish its cause of action under s 18 of the ACL, it could not succeed in its other cause of action. He also contended that if the applicant succeeded in its cause of action under the ASIC Act, s 18 of the ACL would not apply (see s 131A(2) of the Competition and Consumer Act 2010 (Cth)).

88 The central issue is whether the applicant has established its cause of action under s 18 of the ACL, to which I now turn.

(a) The applicant’s case under the ACL

(i) Some relevant legal principles

89 Section 18 of the ACL provides that a person must not, in trade or commerce, engage in conduct that is misleading or deceptive or likely to mislead or deceive.

90 There is no dispute that the conduct complained of was conduct in trade or commerce, noting that “trade or commerce” is defined in s 2(1) of the ACL as including any business or professional activity, whether or not carried on for profit. There can be no doubt that Mr Bilbie’s dealings with the applicant were undertaken in the course of his business activities.

91 Section 2(2)(a) ACL provides that a “reference to engaging in conduct is a reference to doing or refusing to do any act”. Relevant conduct can include representations such as statements made explicitly either orally or in writing or implicitly from words or conduct relating to a matter of fact (see Aqua-Marine Marketing Pty Ltd v Pacific Reef Fisheries (Australia) Pty Ltd (No 5) [2012] FCA 908 at [78] per Collier J).

92 It may also be accepted that silence may amount to misleading or deceptive conduct having regard to all the circumstances of the matter (see Miller & Associates Insurance Broking Pty Ltd v BMW Australia Finance Limited [2010] HCA 31; 241 CLR 357 at [16]-[23] per French CJ and Kiefel J). As their Honours noted there at [20], characterisation of conduct in the context of commercial dealings between individuals or individual entities needs to take account of the particular circumstances and context in which silence may be a circumstance to be considered. A practical approach is required in assessing whether there was a reasonable expectation of disclosure in characterising whether or not non-disclosure is misleading or deceptive from an objective viewpoint. Their Honours added at [22] that, as a general proposition, the relevant prohibition in what is now the ACL “does not require a party to commercial negotiations to volunteer information which will be of assistance to the decision-making of the other party”. Nor does it impose an obligation on a party to volunteer information in order to avoid the consequences of “the careless disregard, for its own interests, of another party of equal bargaining power and competence”.

93 As to whether conduct is misleading or deceptive, it is well settled that the relevant conduct must be viewed as a whole and in the light of all relevant surrounding facts and circumstances (see Campbell v Backoffice Investments Pty Ltd [2009] HCA 25; 238 CLR 304 at [102] per Gummow, Hayne, Heydon and Kiefel JJ). Moreover, conduct will only misleading or deceptive if it has a tendency to lead into error (Australian Competition and Consumer Commission v TPG Internet Pty Ltd [2013] HCA 54; 250 CLR 640 at [39] per French CJ, Crennan, Bell and Keane JJ).

94 It is equally uncontroversial that in determining whether particular conduct is misleading or deceptive, the particular facts must be considered in the light of the ordinary incidents and character of commercial behaviour. This means that a practical and pragmatic approach is required (see General Newspapers Pty Ltd v Telstra Corporation Ltd [1993] FCA 672; 45 FCR 164 at 177-178 per Davies and Einfeld JJ). It was recognised there that “in the ordinary course of commercial dealings, a certain degree of “puffing” or exaggeration is to be expected. Indeed, puffery is part of the ordinary stuff of commerce” (at 178). It may have been in the light of that observation that Mr Tiliakos in closing address abandoned that part of the applicant’s case concerning the representation that Mr Bilbie and the companies of which he was a director were “very capable”.

95 It is well settled that intention is not an essential element for a contravention of s 18 of the ACL. What is relevant is whether, tested objectively, the conduct complained of was misleading or deceptive or likely to mislead or deceive (see Parkdale Custom Built Furniture Pty Ltd v Puxu Pty Ltd [1982] HCA 44; 149 CLR 191 at 197 per Gibbs CJ).

96 Where the relevant representation is in the nature of a prediction or promise which does not come to fruition a central question is whether the prediction or promise had a reasonable or adequate foundation (see Global Sportsman Pty Ltd v Mirror Newspapers Pty Ltd [1984] FCA 180; 2 FCR 82 at [88]-[90]). There, the Court said:

The non-fulfilment of a promise when the time for performance arrives does not of itself establish that the promisor did not intend to perform it when it was made or that the promisor’s intention lacked any, or any adequate, foundation. Similarly, that a prediction proves inaccurate does not of itself establish that the maker of the prediction did not believe that it would eventuate or that the belief lacked any, or any adequate, foundation. Likewise, the incorrectness of an opinion (assuming that can be established) does not of itself establish that the opinion was not held by the person who expressed it or that it lacked any, or any adequate foundation.

… An expression of opinion which is identifiable as such conveys no more than that the opinion expressed is held and perhaps that there is basis for the opinion. At least if these conditions are met, an expression of opinion, however, erroneous, misrepresents nothing.

… Whether a statement is a statement of past or present fact, a promise, a prediction, or a expression of opinion, the making of it constitutes conduct which is misleading or deceptive or likely to mislead or deceive if the statement contains or conveys a misrepresentation…

97 Thus, where a representation is made with respect to a future matter (or the subject matter is a prediction or projection) and the person making the representation or prediction does not have reasonable grounds for making it, misleading or deceptive conduct may occur unless the representor can establish by evidence that the representation was made on reasonable grounds. Necessarily, therefore, each case must be determined on its own particular facts. Section 4 of the ACL provides an evidential burden on the respondent in relation to representations as to future matters to adduce evidence that there were reasonable grounds for the representation. Additionally, the person will not be taken to have reasonable grounds merely because such evidence is adduced. The fact that a person may honestly believe in a particular state of affairs does not necessarily mean that there are reasonable grounds for that belief (see Cummings v Lewis [1993] FCA 190; 41 FCR 559 at 565 per Sheppard and Neaves JJ).

98 Another relevant distinction is where the representation is a statement of opinion rather than a statement of fact. In determining whether or not a particular representation is merely the expression of the representor’s opinion, as opposed to being a statement of fact, primary focus must be on the recipient’s perception. Generally, the issue is resolved by directing attention to the person or persons to whom the representation was directed and asking whether any of those recipients reasonably understood the statement of one of fact or opinion (see Seafolly Pty Ltd v Madden [2012] FCA 1346; 297 ALR 337 at [65] per Tracey J). As Tracey J observed in that case at [65], it is often difficult to draw the line between statements of fact and of opinion, however, some general guidance is provided by the following observations in Tobacco Institute of Australia Ltd v Australian Federation of Consumer Organisations Inc [1992] FCA 962; (1992) 38 FCR 1 (from which Tracey J was citing) at 46-47:

No case will afford a guide to any other case, since it must essentially be a question of fact whether a particular formulation of words expresses merely an opinion or a statement of fact. However, two observations may be made. First, the subjective purpose or motivation of the maker of the statement will not be of much significance. It is the readers’ perception of the maker’s intention which will ordinarily be the significant matter. The question will generally be resolved by looking to the persons to whom the statement was directed and asking whether any members of that class of persons would reasonably understand the statement to be one of fact or opinion.

…

Secondly, a statement will most usually be seen as a statement of fact if it is one which can be measured against an objective criterion. Thus, generally, where no objective criterion exists, so that of necessity what is said must depend upon judgment or opinion, the statement will be seen not as a statement of fact but as one of opinion.

99 It is well settled that determining whether or not a representation is false or misleading is to be tested at the date of the making of the representation and not with the benefit of hindsight (see Bill Acceptance Corporation Ltd v GWA Ltd [1983] FCA 280; (1983) 50 ALR 242).

100 It is appropriate to now say something about the significance of a disclaimer clause in a cause of action under s 18 of the ACL, noting that there were disclaimer provisions in the emails sent by Mr Mogy about which the applicant complains, and in the email dated 30 July 2015 which Mr Bilbie sent to Dr Aggarwal, as well as statements of disclaimer in the Folio Property Brochure. Such provisions are relevant not because they operate to deny that there was any intention on the part of the representor (because intention is irrelevant), but rather because they form part of the overall circumstances which may need to be considered in determining whether particular conduct is misleading or deceptive or likely to mislead or deceive (see Butcher v Lachlan Elder Realty Pty Ltd [2004] HCA 60; 218 CLR 592 at [39] per Gleeson CJ, Hayne and Heydon JJ).

(ii) Application of relevant principles to the facts here

101 Against the background of these relevant general principles, it is convenient to now turn and address the case as presented by Mr Tiliakos on behalf of the applicant in closing address. That case, as succinctly expressed by Mr Tiliakos, was that the applicant “was duped into entering into a hopeless loan deal by the third respondent, that left it, and more importantly, its beneficiaries, severely out of pocket”. For the applicant to succeed, it is necessary for it to establish the relevant requirements in respect of each of the eight remaining pleaded representations which it contended gave rise to contravening conduct which contravened s 18 of the ACL.

102 I will address each of the pleaded representations in turn and explain why I reject the applicant’s claims. The focus will be on the applicant’s claims in relation to the s 18 ACL case, but the findings would also apply to the alternative causes of action if it had been necessary to determine them.

The Austral 1 investment would be incredibly secure

103 The representation that the Austral 1 investment would be “incredibly secure” was made in Mr Bilbie’s email dated 9 August 2015 which he sent to Dr Aggarwal at 7:43 pm. The statement is either an expression of opinion or, alternatively, a statement as to a future matter, bearing in mind that the investment did not occur until Dr Aggarwal executed the Loan Agreement later on 9 August 2015. In either case (and putting to one side who has the onus), the relevant issue is whether or not there is sufficient evidence before the Court to demonstrate that there was a reasonable basis for the representation at the time that it was made. For the following reasons, I consider that the evidence is sufficient for that purpose.

104 First, the representation cannot be read in isolation from the surrounding circumstances, which include (but are not limited) to all the contents of the 9 August 2015 email which is set out at [36] above. It is notable that the representation is made shortly after Mr Bilbie wrote that technically it was arguable that the loan is unsecured because there is no registered mortgage. It was in that context that he then added that the loan would be “incredibly secure”, and he added that the “equity position cannot be denied” and he also made other statements which the applicant complains involved separate representations to which I will return.

105 Secondly, I accept Mr Bilbie’s evidence that there was a reasonable basis for his description of the proposed loan being “incredibly secure” at the time the statement was made, even though circumstances changed thereafter. It is evident from the terms of Mr Bilbie’s email that part of the reason why he described the investment as “incredibly secure” was because of the equity position which he elaborated upon in his oral evidence. As at 9 August 2015, I accept that Mr Bilbie genuinely thought that finance had been finalised and that settlement of the two Austral properties, although deferred from 30 June 2015, was expected to settle on 12 August 2015 as confirmed in Gadens’ email to the financier. As noted above, Mr Bilbie was plainly aware of that fact because he conveyed it to Dr Aggarwal in his earlier email dated 9 August 2015 at 5:55 pm. I also accept that Mr Bilbie’s evidence that his opinion that the loan would be “incredibly secure” was based upon the information which he had at that time concerning Ms Herps’ asset position, the Egan valuation (see further below), the relevant information in the Analysis, his belief that approximately $11m funding had been offered to the developer by Mawson Flinders Cook, as confirmed by a letter of offer dated 26 June 2015 to that effect, which form part of Exhibit A, the success of previous projects in which his companies were involved and the fact there were several guarantors to the loan. I accept Mr Bilbie’s evidence that, up to 9 August 2015, he was kept informed by the developer of relevant matters relating to the Austral Project, including financing.

106 Thirdly, in determining whether the representation was misleading or deceptive or likely to mislead or deceive, account should also be taken of the fact that the statement was made to Dr Aggarwal who, in my opinion, was undoubtedly a sophisticated investor who was aware that the investment had risks. This is reflected in the nature of the negotiations conducted by Dr Aggarwal in seeking to obtain better terms for his investment, as well as the matters referred to at [51] and [59] above. Dr Aggarwal also gave evidence that he had undertaken his own research into the value of land near Badgerys Creek. There are numerous examples in the evidence of Dr Aggarwal testing the information which he was given by Mr Mogy and Mr Bilbie and trying to negotiate an investment on improved terms from his viewpoint. This is perhaps best illustrated by the email request which he made of Mr Bilbie on 7 August 2015 at 6:19 pm, where he asked Mr Bilbie to send him the value of the properties being used as security, the debt loaded against the companies/property being used as security and balance sheets and profit and loss statements for the last two years of all the borrowers and guarantors. It was in response to that request that Mr Bilbie forwarded Dr Aggarwal the information attached to his email dated 9 August 2015 at 5:55 pm (see [32] and [33] above), which contained information on risk.

107 For these reasons, even though as events transpired the loan proved not to be “incredibly secure”, I find that there was a reasonable basis for Mr Bilbie to make the representation which he did on 9 August 2015.

The Austral Project was significantly de-risked with a clear exit strategy

108 The source of this representation is again Mr Bilbie’s email dated 9 August 2015, which he sent to Dr Aggarwal at 7:43 pm, shortly before Dr Aggarwal signed the Loan Agreement. The representation was made a few hours after Mr Bilbie had sent Dr Aggarwal various information relating to the Austral Project, including the Egan valuation and the Analysis which Mr Bilbie had prepared of inter alia the Austral 1 Project.

109 In my view, the representation is in the nature of a statement of Mr Bilbie’s opinion. The relevant issue is whether, by reference to the evidence, he had reasonable grounds for expressing that opinion. I consider that he did.

110 First, I accept Mr Bilbie’s evidence that he relied upon the Egan valuation of $13.65m, as well as his understanding that the purchase price was $8m. I reject the applicant’s submission that Mr Bilbie was not entitled to rely upon the Egan valuation because of the express disclaimer in that document and, in particular, the statement that it was “not to be relied upon by any other party or for any other purpose” other than by the instructing party. That disclaimer clause may well have prevented Mr Bilbie from recovering any loss from Egan, but I do not view the disclaimer clause as preventing him from relying upon the report at his own risk.

111 Furthermore, the Analysis which Mr Bilbie provided to Dr Aggarwal contained the following information in respect of what was described as “Exit Strategy” (emphasis in original):

• Sell as DA Approved site now

• We bought raw land for $8m and have already been offered over $15m for site

• Rely on large $7m + profit cushion in the Land Value

• Even at fire sale price, the Land with DA would still fetch above $12m

This information provided a reasonable foundation for Mr Bilbie’s opinion at the time it was expressed. The applicant did not suggest that any of these matters were baseless.

112 Secondly, I also accept Mr Bilbie’s evidence that part of the basis for the statements he made in his email was the information from Mr Grego which he took into account relating to Ms Herps’ assets, together with his knowledge of the fact that other projects in which Ms Herps and his companies had been involved had been successfully completed and provided generous returns to investors.

113 Thirdly, it is important to note that Mr Bilbie did not tell Dr Aggarwal that the loan carried no risk at all. Plainly it did, as might be suggested by the unusually high interest rate return, together with the absence of any orthodox form of security, such as a mortgage. Dr Aggarwal was plainly aware of these matters, not only because he apparently read the relevant information provided to him in respect of the investment, but also because he himself attempted to negotiate a better deal which would have given him more orthodox security in the form of a block of land. Mr Bilbie told him that that would be unacceptable to the developer (see immediately below).

114 Finally, and more generally, I repeat what is said above regarding Dr Aggarwal being a sophisticated investor.

Agnish would achieve a 40% return on the Austral 1 investment

115 The source of this representation is what Mr Bilbie told Dr Aggarwal on 30 July 2015. This conversation occurred over the telephone and appears to have been the first direct contact between Dr Aggarwal and Mr Bilbie. According to Dr Aggarwal’s evidence, which I accept on this matter, he said that he told Mr Bilbie that he wanted to add a block of land as security to the investment just in case the deal went bad. I accept Dr Aggarwal’s evidence that Mr Bilbie responded by saying words to the effect that he simply could not include a block of land on top of the then proposed 30 percent interest return on the loan and that Mr Bilbie then added that if Dr Aggarwal lent $500,000 he “will get a 40% return in 18 months”. I also accept Dr Aggarwal’s evidence that Mr Bilbie then made reference to the possibility of him investing in another development, Austral 2, which would provide a 30% interest return and a profit share but Dr Aggarwal told Mr Bilbie in their conversation on 30 July 2015 that he would “go with the Austral 1 deal of $500,000 and we will look at the next deal in due course”.