FEDERAL COURT OF AUSTRALIA

Vodafone Hutchison Australia Pty Limited v Australian Competition and Consumer Commission [2020] FCA 117

ORDERS

VODAFONE HUTCHISON AUSTRALIA PTY LIMITED (ACN 096 304 620) Applicant | ||

AND: | AUSTRALIAN COMPETITION AND CONSUMER COMMISSION First Respondent TPG TELECOM LIMITED (ACN 093 058 069) Second Respondent | |

DATE OF ORDER: | 13 February 2020 |

THE COURT DECLARES THAT:

1. Pursuant to section 163A of the Competition and Consumer Act 2010 (Cth) and section 21 of the Federal Court of Australia Act 1976 (Cth), the acquisition by the Applicant of all of the ordinary shares in the Second Respondent by means of a scheme of arrangement under Part 5.1 of the Corporations Act 2001 (Cth), and implemented pursuant to the terms of the Scheme Implementation Deed dated 30 August 2018, would not have the effect, and would not be likely to have the effect, of substantially lessening competition in any market in contravention of section 50 of the Competition and Consumer Act 2010 (Cth).

THE COURT ORDERS THAT:

2. The parties confer, and on or before 12:00 noon on 27 February 2020, provide an agreed minute of order as to costs, or in the absence of agreement, short written submissions as to costs, which issue will be determined on the papers.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

MIDDLETON J:

1 The Applicant (‘Vodafone’, sometimes referred to as ‘VHA’) wishes to acquire all of the ordinary shares in the Second Respondent (‘TPG’) by means of a scheme of arrangement under Pt 5.1 of the Corporations Act 2001 (Cth). This would be implemented pursuant to a scheme implementation deed dated 30 August 2018 (‘Scheme Implementation Deed’).

2 It is a condition precedent to completion of the Scheme Implementation Deed that TPG and Vodafone have obtained informal merger clearance from the First Respondent (‘ACCC’). On 8 May 2019, the ACCC announced that it declined to give informal merger clearance on the expressed basis that the merger would be likely to have the effect of substantially lessening competition in the supply of retail mobile services in Australia, in contravention of s 50 of the Competition and Consumer Act 2010 (Cth) (‘CCA’).

3 By these proceedings, Vodafone seeks declaratory relief that the merger will not contravene s 50 of the CCA.

4 The Court has come to the view that the proposed merger would not have the effect, nor be likely to have the effect, of substantially lessening competition in the supply of retail mobile services in Australia. Accordingly, the declaratory relief sought by Vodafone will be granted so the merger can proceed as contemplated by the Scheme Implementation Deed.

5 The ACCC contended that the future state of competition without the merger is one where it is likely or there is a real chance that TPG will roll-out a mobile network, and will focus primarily on winning new customers through its aggressive pricing. In this way, TPG’s competitive constraint would prompt Vodafone, in particular, to respond by adjusting its prices, and the response of Vodafone would, in turn, lead to a competitive response by Optus and Telstra.

6 Then, the ACCC contended that with the merger there would be no competitive effect from any new entry. The new merged entity (called ‘MergeCo’) would not offer any substantially greater competitive constraint than that which Vodafone would offer without the merger. The ACCC contended that competition would not meaningfully be improved and the benefits of a new entry would be lost.

7 According to the ACCC, this comparison of the future state of competition with and without the merger, demonstrates that there is a real chance that the merger will substantially lessen competition by eliminating the prospect of TPG’s entry into the retail mobile market in Australia.

8 I have not accepted the above contentions of the ACCC, and have determined that Vodafone has discharged the burden of proof placed upon it to obtain the declaratory relief it sought in these proceedings.

9 Back in 2017, there was a moment in the affairs of TPG and Mr Teoh (the guiding force behind TPG) for a business opportunity to be taken to roll-out a retail mobile service. That moment has passed. To now leave TPG and Vodafone in their current state will not promote competition in the retail mobile market. A merger would not now, and would not likely in the relevant future, substantially lessen competition in the supply of retail mobile services in Australia.

10 It is extremely unlikely and there is no real chance that TPG will roll-out a retail mobile network or become an effective competitive fourth mobile network operator (‘MNO’) in Australia in the relevant future. When I refer to there being no real chance I mean that there is no commercially relevant or meaningful real chance that TPG will roll-out a retail mobile network or become an effective competitive fourth MNO. Then, Vodafone itself is facing, and will face, constraints in trying to compete with Telstra and Optus in the retail mobile market. The rational and business-like solution is for Vodafone and TPG to merge, with the result that both companies will be enhanced and will be a stronger competitive force against Telstra and Optus.

11 The alternative fact scenario in the future (if, as I find, it is extremely unlikely and there is no real chance that TPG will roll-out a retail mobile network) is that any potential for a third MNO to compete with Telstra and Optus will be gone. Then, even if TPG did attempt to enter the market as it did before, Vodafone would be left as it is and TPG would have a lack-lustre presence in the retail mobile market. This would not promote competition in this market. It is not necessarily the number of competitors that are in the relevant market, but the quality of competition that must be assessed. Further, it is not for the ACCC or this Court to engineer a competitive outcome. The only question for this Court is whether the merger would have the effect, or be likely to have the effect, of substantially lessening competition in the supply of retail mobile services in Australia.

12 Whether the earlier decisions of TPG to enter the Australian retail mobile market and then continue in that endeavour were sound, rational and commercial decisions is of historical interest, although of some relevance in these proceedings. Obviously, an analysis of this history will inform present market participants; rational market participants will act upon any lessons they might have gained from the previous TPG roll-out of a mobile network. To misquote Karl Marx, history repeats itself only when you ignore it. I do not imagine Mr Teoh will ignore the history. Mr Teoh will have learnt many lessons from his experience in rolling out a retail mobile network and its aftermath, including the lessons to be learnt as a consequence of these proceedings.

13 However, the true focus in these proceedings, as one part of the analysis, should be on the question of whether there is a likelihood, possibility or real chance (whatever phrase is adopted) that TPG will in the future (relevantly the next five years) roll-out a retail mobile network in the circumstances that can reasonably and sensibly be predicted based upon the evidence before the Court.

14 An important matter to keep in mind when considering individual factors that may impact upon the future likelihood, possibility or real chance of a roll-out by TPG is the cumulative effect of these factors, and how this cumulative effect would impact on the likelihood of making a rational commercial decision to roll-out a retail mobile network. Just because one factor is not ‘critical’ to achieving a roll-out (but is otherwise undesirable or difficult to implement) does not mean that that factor in conjunction with other factors, may not swing rational decision makers to a particular view against rolling out a retail mobile network. If sufficient factors that may favour a roll-out are either not likely to occur, or to a rational decision maker are undesirable or difficult to implement, this may indicate that a roll-out would be a decision no rational company in the position of TPG would take in the relevant future period. This is not to say that in looking at each factor that may be in favour of, or an impediment to, a roll-out of a retail mobile network, each factor will not need to be assessed in isolation. It is just that it will be necessary to look at the whole picture.

15 Then it must be recalled that the ultimate decision to proceed in the future with a roll-out of a mobile network will be that of TPG. It is abundantly clear that if Mr Teoh does not vote in favour of a roll-out it will not occur. If Mr Teoh votes in favour of a roll-out, then further processes at Board level will need to take place to assess a business plan in light of financial, technical and market conditions (all of which have been fully ventilated and analysed in these proceedings).

16 The assessment of Mr Teoh’s views and the reasons he has given for those views as to the future plans of TPG is critical to the Court’s assessment in these proceedings. It is always difficult to predict business decisions, which are subjective and depend upon the judgment of the persons making such business decisions. Then there is always the possibility that statements of business intentions made by interested parties or market participants may be made in the course of merger litigation to try and establish a more favourable counterfactual. I appreciate that both TPG and Vodafone before the Court sought to put their ‘best foot forward’ in support of the merger, and maybe what is put before a Court has a different complexion to that said outside the Court, where a company may seek to build itself up in the marketplace.

17 I have had the opportunity of assessing Mr Teoh as he gave his evidence; of assessing his views and opinions; and of assessing his capabilities and business approach. No attack was made upon his credibility, and none was warranted. Mr Teoh clearly had a tight grasp of the business affairs of TPG. Traditional good board governance would normally require careful documentation of analysis and decision making. Mr Teoh had a more informal and fluid approach, obviously with a capability to absorb and retain commercial information, and make sound commercial decisions. Mr Teoh did not base his decisions on rigorous financial modelling. Mr Teoh certainly portrayed as a market disruptor and as having an unconventional business style. Whilst he may do whatever it takes to progress his business, he is obviously not foolhardy. No one suggested he would act other than in a sound, rational and commercial way in deciding the future of TPG in the next five years (and beyond).

18 It would of course have been open for the Court to have rejected the evidence of Mr Teoh (and other witnesses called by Vodafone and TPG) as to their predictions of the future retail mobile market. This may have meant that the evidence supporting the merger was of little probative value, although normally the fact that a witness is not believed does not prove the opposite of what is asserted. However, this is not the position I have found myself in as I have accepted Mr Teoh’s evidence and his reasons for his views. Further, this is not a case where uncorroborated oral evidence is given by just one witness as to the future of the retail mobile market.

19 This leads me to another observation. The very nature of these proceedings, involving the consideration of extensive evidence and the public sworn statements made by personnel of both Vodafone and TPG as to their intentions, must be taken into account in my assessment of the future market. TPG has publicly disclosed in these proceedings its future intentions and limitations, and its senior executives have given sworn evidence that TPG has no business case for a roll-out. Both these factors create a serious disincentive for a listed public company later performing an about face and rolling out a retail mobile network. By exposing to its competitors its competitive strategy and business modelling, TPG would be under a serious competitive disadvantage if it were to roll-out a new network. This is not to say the Court process is self-fulfilling of the quest for a merger. However, where no objection is taken as to the credit of the major personnel involved in the industry (including, significantly, Mr Teoh), the Court will more readily be able to rely on industry participants’ evidence, subject to certain qualifications which I will later address.

20 Further, after the trial process, Vodafone and TPG will have become better informed of the various ways forward and various obstacles to be overcome. It is to be noted that where it is accepted by all parties that the guiding minds of Vodafone and TPG are rational business people, both Vodafone and TPG at the last day of the trial still considered the merger to be in their best interests and Mr Teoh has not resiled from his evidence that no roll-out of a retail mobile network will occur in the relevant future.

21 After all, an important issue I need to assess is whether Mr Teoh and the TPG Board will effectively change his and its mind. There currently stands a Board decision on 29 March 2019 that building a mobile network was not a feasible option, which has been acted upon and effectively re-affirmed in this proceeding. No party is attacking the bona fides of that decision taken in 29 March 2019. The assessment to be made is whether Mr Teoh and the TPG Board would change their mind (should the merger not proceed) keeping in mind that any change of mind will not be occurring until after the prospect of a successful merger is no longer possible.

22 Much of the case presented by the ACCC was that there are technical and financial ways in which TPG could roll-out its network in the future. To some degree, the options the ACCC put forward will be available. Further, in business, challenges are there to be met and overcome. Certainly, in 2017 TPG did not have all the various options (financial and technical) set in stone at the time it decided to enter the retail mobile market. Nevertheless, it is worthwhile to keep in mind that the ACCC will not be the entity rolling out the new retail mobile network the ACCC envisages in its detailing of various future options available to TPG. The risks of such a new venture will be upon TPG and its shareholders. It will be their business decision whether to start again or roll-out in the current and future circumstances that can be predicted.

23 Another very important consideration is to recall the significant difference in the position now and the position when TPG last rolled out its mobile network. One thing that TPG had previously was the will and incentive to enter the retail mobile market in Australia, led by the drive, influence and financial resources available to Mr Teoh. That will and incentive have now gone – that is not in dispute and was attested to by Mr Teoh. I cannot see that this state of affairs will alter in the next five years, even if there were options available or made available in that period of time in a financial and technical sense. The old saying comes to mind – ‘where there is a will there is a way’ – but without the will of Mr Teoh I cannot see TPG having another attempt to enter the retail mobile market in Australia.

24 I cannot conclude with absolute certainty that Mr Teoh and TPG will not change their minds, and attempt to re-start entry into the retail mobile market in Australia. However, it is extremely unlikely and there is no real chance of this happening in the next five years (or beyond). Putting aside expert testimony which talks of possibilities and opportunities for Mr Teoh in the future in the retail mobile market (which can only be based on certain assumptions), the general thrust of the evidence of the industry participants is that TPG’s ship has sailed in the retail mobile market in Australia. I stress I am very aware of the care that must be taken in accepting self-serving statements by interested parties and industry participants. The overall circumstances of the case will provide more reliable guidance than would oral evidence on the part of interested parties. However, the Court does not ignore that evidence, particularly when it is supported by reasons and otherwise credible. I am also aware that TPG and Vodafone in the past have been very pro-active in the promotion of their retail mobile services, and their approach now is more pessimistic. In that regard, out of court public statements of business people in connection with their enterprises come from a belief that their business is the greatest in the world, and without such a belief businesses would probably not prosper. Subject to the constraints of the law, public expressions of belief in one’s own business are to be expected and are part of marketing. In addition, care must be taken to put the past comments of market participants in context; as to timing, the market conditions, the level of generality, to what extent they were informed comments, and the circumstances in which they were made to the public. It is to be expected that opinions and views change, given new information or changes in market structure, or arising from market dynamics. This has been made evident by the emerging views of market participants in the retail mobile market over the period from 2017 to 2019.

25 The other point to stress at this stage of the Court’s reasons is this. There has been no attempt to discredit any of the lay witnesses head-on: by this I mean suggesting to them in the witness box that they are not telling the truth. Undoubtedly, there are more ways of taking a city in the course of battle other than by a direct attack. The attack in these proceedings has been more subtle; by reference to the likelihood of revisiting the past, the accumulation of other evidence suggesting what could happen in the future and what would be financially and technically feasible if Mr Teoh was in fact minded to roll-out a mobile network in Australia. As the ACCC stated in its closing written submission:

One of the fundamental issues for VHA and TPG to confront was why they said that TPG would not return to its pre-merger plan of rolling out a mobile network if the merger was no longer a possibility. Identifying the cogency of the reason for the change in strategy is important because expressions of opinion by executives about what they would do absent the merger when the merger remains on foot and they want the merger to occur are of limited value. That does not require the Court to conclude that those executives do not hold the views they say they have at the time they are expressed. But the likelihood that these would remain their views if the merger was no longer a possibility must be assessed against their past behaviour and conduct.

26 Whilst it is true that the views of participants in the marketplace should be assessed against ‘past behaviour and conduct’, as I have just indicated, there is limited utility in doing this unless such is viewed in the context of the time that behaviour and conduct took place.

27 However, I should make one matter clear relating to the earlier roll-out of the retail mobile network by TPG. I have not come to the conclusion that the earlier roll-out of the retail mobile network by TPG was considered at the outset by Mr Teoh or TPG to be doomed and destined to commercial failure. Mr Teoh considered that the roll-out of the retail mobile network would be competitive even though the network would be of a lower quality than that of Telstra and Optus. The analysis to be undertaken now in these proceedings must consider the quality of competition in the future. However, in doing this analysis and in assessing the evidence of various witnesses, I have considered the earlier roll-out as one way to assess the reasons given by witnesses for their predictions.

28 I make mention of the issue of efficiencies in the context of merger competition law. The Court is concerned with efficiencies and their effects on competitors. There is no doubt that the benefits of efficiencies, should a merger occur, should not be ignored: although the Court is not concerned just with an individual company’s efficiency, or whether the result of a merger is merely shown to improve the efficiencies between the merging companies themselves. The focus must be upon market efficiencies. Nevertheless, it should be recognised that there will be difficulties in proving and exactly quantifying benefits of efficiency with the coming into existence of a merged entity. Whilst efficiency gains must be proved to exist to the satisfaction of the Court, it needs to be recognised that requiring the merged parties to produce evidence where they are not operating as merged entities is difficult, and this difficulty needs to be recognised in assessing the evidence before the Court on the issue of efficiencies.

29 There was some reference in the course of these proceedings to mathematical probability and the assessment of future circumstances. It will be a rare case where mathematical techniques will make a decisive contribution to the resolution of forensic uncertainty. As observed by Mahoney JA in Jones and Another v Sutherland Shire Council [1979] 2 NSWLR 206 at 227-228:

the court is required to test its conclusion, not merely according to the subjective conviction of it, but also by reference to the reasonableness of its basis. Whether this involves a conceptual inconsistency in relation to probability is not of significance: in fact the conclusion is so tested. It may be tested, according to the case, against facts otherwise known or assumed to exist, and the inferences from them. The court may also look to the “probability” of the conclusion being correct according to a different meaning of probability. In this sense, it may test the conclusion by reference to the “chance” of its being so, in the sense of Pascal’s dice or Beanoulli’s “Large Numbers”. It may also test it according to what, if they are available, are the statistics (the human experience reduced to numbers) as to the existence of a particular fact in given circumstances. According to such matters, it may modify a view formed on other grounds. … But the probability of the correctness of a particular proposition of fact, at least of the present kind, cannot depend completely upon such a mechanical meaning of probability. There are, as the plaintiff’s argument in the present case emphasized, many cases in which Pascalian mathematics cannot be done, because there cannot be, or at least is not, information as to what are the number of “chances” or possibilities, and whether each of these is equally weighted. In such cases, and the present is one of them, the probabilities cannot be determined in that way. The existence of the fact is, subject to testing in such ways as may be appropriate, to be determined according to the court’s assessment of the facts, and its confidence that its assessment is correct. Testing aside, it may be that further explanation of this process is a matter for the experimental psychologist rather than for the lawyer or mathematician.

30 All courts in the course of their fact finding function must reach a sufficient level of persuasion depending on the nature of the fact finding they are undertaking.

31 The requisite standard of proof in a civil proceeding is expressed commonly as proof ‘on the balance of probabilities’. Expression of the standard of proof in a civil proceeding as satisfaction on the balance of probabilities is an acknowledgment that the judgment to be made by the tribunal of fact is inevitably to be made under conditions of uncertainty. However, whatever its underlying probability, a disputed historical fact once found is a fact which is taken to exist for the purpose of resolving the legal rights or liabilities that are in dispute. Of course, with an analysis involving the predication of the future, further complexities arise in the course of a court’s deliberations.

32 After referring to what Dixon J said in Briginshaw v Briginshaw and Another (1938) 60 CLR 336 (‘Briginshaw’), Gageler J in an article titled ‘Alternative Facts in the Court’ (2019) 93 Australian Law Journal 585 wrote:

The main thing Justice Dixon was saying, consistently with mainstream judicial and academic opinion in the United States, is that satisfaction on the balance of probabilities involves the formation under conditions of acknowledged uncertainty of a subjective belief. The requisite belief is an “actual persuasion” that the fact in issue actually exists – that a past event the occurrence of which is uncertain and is disputed did indeed occur. What he was emphasising is that belief, as Bentham put it, “is susceptible of different degrees of strength, or intensity”. The belief involved in having a state of satisfaction “beyond reasonable doubt”, the universally accepted expression of the requisite standard of proof for a fact asserted by the prosecution in a criminal proceeding, is similar to the belief involved in having a state of satisfaction “on the balance of probabilities” in that it is subjective belief and different only in that it is belief that must be held with a greater degree of intensity.

33 In these proceedings the Court has reached a sufficient level of persuasion on the relevant factual issues to reach the ultimate conclusion that the merger would not have the effect, and would not likely have the effect, of substantially lessening competition in the retail mobile market. The Court has been left in no relevant uncertainty, after reviewing the evidence, as to the future of the retail mobile market which will not involve Mr Teoh or TPG entering the Australian retail mobile market in the next five years.

34 Whilst there are a number of reasons leading to the conclusion I have reached, it was accepted by the parties that if I took the view I now have on there being no future likelihood, possibility or real chance of TPG entering into the retail mobile market, Vodafone would be entitled to the declaration sought in these proceedings.

35 As already indicated, Vodafone seeks a declaration that the merger would not have the effect, and would not be likely to have the effect, of substantially lessening competition in any market in contravention of sub-s 50(1) of the CCA. That sub-section relevantly provides that:

A corporation must not directly or indirectly:

(a) acquire shares in the capital of a body corporate; …

if the acquisition would have the effect, or be likely to have the effect, of substantially lessening competition in any market.

36 Subsection 50(3) of the CCA provides a list of non-exhaustive factors that must be taken into account when assessing whether an acquisition would have the effect, or be likely to have the effect, of substantially lessening competition in a market. These factors relevantly include ‘the height of barriers to entry to the market’ (sub-para (b)); ‘the level of concentration in the market’ (sub-para (c)); ‘the dynamic characteristics of the market, including growth, innovation and product differentiation’ (sub-para (g)); and ‘the likelihood that the acquisition would result in the removal from the market of a vigorous and effective competitor’ (sub-para (h)).

37 Because Vodafone seeks a declaration in the terms referred to above, it is necessary for it to establish, on the balance of probabilities, that the merger ‘would not be likely to have the effect of substantially lessening competition in the relevant market …’. In analogous circumstances in Australian Gas Light Company v Australian Competition and Consumer Commission and Others (2003) 137 FCR 317 (‘AGL’), French J held at 420 [355] that Australian Gas Light Company, the applicant in that case, was required to:

negative the existence of any real chance … of a commercially relevant or meaningful lessening of competition flowing from the acquisition.

38 Justice French emphasised at 420 [356] that if the Court was ‘left in a position of uncertainty’ about the existence of this ‘real chance’, then Australian Gas Light Company was not entitled to the relief that it sought.

39 It is convenient to set out the legal principles governing the interpretation of several terms which appear in sub-s 50(1) of the CCA, and which are relevant to the resolution of this proceeding.

40 Subsection 50(1) of the CCA focuses upon the effect of an acquisition ‘in any market’. The concept of a ‘market’ is given content by s 4E and sub-s 50(6) of the CCA. Section 4E of the CCA defines ‘market’ as meaning, unless the contrary intention appears:

a market in Australia and, when used in relation to any goods or services, includes a market for those goods or services and other goods or services that are substitutable for, or otherwise competitive with, the first-mentioned goods or services.

Subsection 50(6) of the CCA provides that, for the purposes of sub-s 50(1), ‘market’ means a market for goods or services in Australia, a State, a Territory or a region of Australia.

41 Several cases have considered the concept of a ‘market’: see, eg, Re Queensland Co-operative Milling Association Ltd (1976) 8 ALR 481 (‘Re QCMA’) at 512-519 (Trade Practices Tribunal); Queensland Wire Industries Proprietary Limited v Broken Hill Proprietary Company Limited and Another (1989) 167 CLR 177 at 195-196, 198 (Deane and Dawson JJ agreeing); Singapore Airlines Limited v Taprobane Tours WA Pty Ltd (1991) 33 FCR 158 at 174-178 (French J); Boral Besser Masonry Limited v Australian Competition and Consumer Commission (2003) 215 CLR 374 at 422-424 [133]-[138] (Gleeson CJ and Callinan J), 427 [155] (Gaudron, Gummow and Hayne JJ), and 456-458 [256]-[259] (McHugh J); Seven Network Ltd and Another v News Ltd and Others (2009) 182 FCR 160 (‘Seven Network’) at 239-240 [345]-[350] (Dowsett and Lander JJ); Australian Competition and Consumer Commission v Flight Centre Travel Group Limited (2016) 261 CLR 203 at 227 [66] (Kiefel and Gageler JJ); Air New Zealand Ltd v Australian Competition and Consumer Commission (2017) 262 CLR 207 at 221-223 [12]-[15] (Kiefel CJ, Bell and Keane JJ), 231 [44] (Nettle J) and 250-252 [119]-[122] (Gordon J).

42 The parties agree that for the purpose of these proceedings, there are only three pertinent markets, and only one in which there is controversy about competitive effects.

43 The first and most pertinent market is the national market in Australia for the supply of retail mobile services to retail customers. The character of this market has been the subject of a considerable amount of evidence. It is common ground that competition occurs across a number of factors, including price, data inclusions, geographic coverage, service quality, service add-on and retail support. Customers can readily switch from one provider to another.

44 There is no dispute between the parties as to the product and geographic dimensions of the retail mobile market. The product dimension of the centrally relevant market is properly defined as retail mobile services, and the market is Australia-wide. The parties essentially agree that the temporal dimension of the market does not extend beyond five years.

45 The second is the national wholesale market in Australia for the supply of wholesale mobile services to mobile virtual network operators (‘MVNO’) for the purpose of resupply to retail customers. The only suppliers in this market are Telstra, Optus and Vodafone. The customers are the 60 or so MVNOs operating in Australia.

46 The third is the national retail market in Australia for the supply of retail fixed broadband services to individual/household, small business, government and enterprise customers. As at June 2018, the major competitors and approximate market shares were as follows: Telstra 41%, TPG 25%, Optus 15% and Vocus 7%. Vodafone’s share has always been less than 1%.

47 The ACCC accepted in these proceedings that the merger would not have the effect, and would not be likely to have the effect, of substantially lessening competition in the wholesale mobile market or the retail fixed broadband market in contravention of s 50 of the CCA. However, the ACCC denied that the merger would not have the effect, and would not be likely to have the effect, of substantially lessening competition in the retail mobile market.

‘Substantially lessening competition’

48 The concept of ‘competition’ is not defined for the purposes of sub-s 50(1) of the CCA. However, in accordance with the reasons of the Trade Practices Tribunal in Re QCMA, competition is usually understood as ‘a dynamic process [which is] generated by market pressure from alternative sources of supply and the desire to keep ahead’. In short, ‘[c]ompetition expresses itself as rivalrous behaviour’.

49 As to the meaning of ‘substantial’ in the context of sub-s 50(1) of the CCA, Beach J held in Australian Competition and Consumer Commission v Pacific National Pty Limited (No 2) [2019] FCA 669 at [1262] (‘Pacific National’), synthesising a number of previous authorities, that:

[T]he concept of substantially lessening competition does not require a large or weighty lessening of competition, but only one that is meaningful and relevant to the competitive process. A short term effect readily corrected by market processes is not substantial in this respect. But a medium to long term effect not easily corrected may amount to a substantial lessening of competition.

50 When assessing the competitive detriment which is likely to result from the merger, it is generally considered useful to compare the future state of competition with the merger (often described as the ‘factual’) against the future state of competition without the merger (often described as the ‘counterfactual’): see, eg, AGL at 324 [9], 417-418 [352]-[353] (French J), and the authorities cited therein.

51 The Court’s task is not to assess whether, if TPG entered the retail mobile market as a fourth MNO, there would be some immediate price reaction from incumbent MNOs. The competitive impact created by new entry is often immediately obvious, but fleeting in its effect. An immediate but transitory increase in competition is not ‘substantial’ in the relevant sense – it is not meaningful to the competitive process. Therefore, a proposed merger that only forecloses the prospect of some short-term competition will not ‘substantially’ lessen competition. If, for instance, TPG would have been an unsuccessful and uncompetitive MNO in the medium to long term, the removal of the prospect of TPG entering as a fourth MNO could not ‘substantially’ lessen competition for purposes of s 50.

52 Since the judgment of French J in AGL (cf Australian Competition and Consumer Commission v Metcash Trading Ltd and Another (2011) 198 FCR at 305 [25] and 318 [89] (Buchanan J) (‘Metcash’)), it has been generally been accepted that, in the context of sub-s 50(1) of the CCA, the term ‘“likely” refers to a significant finite probability or “a real chance” rather than “more probable than not”’ (AGL at 415 [343])). Justice French reached this construction following an examination of the authorities (see, eg, Tillmanns Butcheries Pty Ltd v Australasian Meat Industry Employees’ Union and Others (1979) 42 FLR 331 at 347 (Deane J); Global Sportsman Pty v Mirror Newspapers Pty Ltd (1984) 2 FCR 82 at 87 (Bowen CJ, Lockhart and Fitzgerald JJ); News Ltd and Others v Australian Rugby Football League Ltd and Others (1996) 64 FCR 410 at 564-565 (Lockhart, von Doussa and Sackville JJ); and Monroe Topple & Associates Pty Ltd v Institute of Chartered Accountants in Australia (2002) 122 FCR 110), and ‘having regard to the statutory context provided by the other sections of Pt IV’ of the Trade Practices Act 1974 (Cth) (AGL at 415 [343]). Expanding upon the meaning of the term, French J said in AGL at 416-417 [348], citing, in respect of the final sentence, Rural Press Limited and Others v Australian Competition and Consumer Commission (2003) 216 CLR 53 at 71 [41] (Gummow, Hayne and Heydon JJ), that:

The meaning of “likely” reflecting a “real chance or possibility” does not encompass a mere possibility. The word can offer no quantitative guidance but requires a qualitative judgment about the effects of an acquisition or proposed acquisition. The judgment it requires must not set the bar so high as effectively to expose acquiring corporations to a finding of contravention simply on the basis of possibilities, however plausible they may seem, generated by economic theory alone. On the other hand it must not set the bar so low as effectively to allow all acquisitions to proceed save those with the most obvious, direct and dramatic effects upon competition. By the language it adopts and the function thereby cast upon the Court and the regulator in their consideration of acquisitions s 50 gives effect to a kind of competition risk management policy. The application of that policy, reflected in judgments about the application of the section, must operate in the real world. The assessment of the risk or real chance of a substantial lessening of competition cannot rest upon speculation or theory. To borrow the words of the Tribunal in the Howard Smith case, the Court is concerned with “commercial likelihoods relevant to the proposed merger”. The word “likely” has to be applied at a level which is commercially relevant or meaningful as must be the assessment of the substantial lessening of competition under consideration...

53 Subsequent decisions – including the judgment of Beach J in Pacific National – have treated the phrase ‘would … be likely to have the effect of substantially lessening competition’ as requiring the demonstration of a ‘real chance’ that the relevant acquisition would substantially lessen competition: see, eg, Universal Music Australia Pty Ltd and Others v Australian Competition and Consumer Commission (2003) 131 FCR 529 at 586 [247] (Wilcox, French and Gyles JJ); Seven Network at 330 [751] (Dowsett and Lander JJ); Australian Competition and Consumer Commission v Metcash Trading Ltd (2011) 282 ALR 464 at 492 [134]-[135] (Emmett J); Metcash at 341-342 [227]-[229] (Yates J); Pacific National at 263 [1266], 264 [1269], 265 [1274] and 266 [1279] (Beach J); Australian Competition and Consumer Commission v Cascade Coal Pty Ltd [2019] FCAFC 154 at 35 [148]; cf Metcash at 305 [25], 318-319 [89]-[90] (Buchanan J).

54 All parties encouraged me in these proceedings to follow the approach of French and Beach JJ.

55 This Court is not formally so bound to follow these earlier statements of principle. Nevertheless, while this Court may not formally be bound to interpret the term ‘likely’ as requiring the demonstration of a ‘real chance’, the weight of authority supports such an interpretation.

56 However, as recognised by Beach J in Pacific National at [1269], despite French J’s reasons in AGL in respect of the proper construction of s 50 and the endorsement of the ‘real chance’ construction in the subsequent case law, several later decisions have introduced a degree of uncertainty as to the application of that test.

57 The uncertainties that have arisen in the application of the test are illustrated by the reasons of Emmett J at first instance, and the separate reasons of Buchanan and Yates JJ sitting as part of the Full Court in Metcash. At first instance, Emmett J propounded a two-stage test with different legal thresholds for the counterfactual and the substantial lessening of competition assessments:

(1) first (at [145]), the ACCC, as the applicant in that case, was required to:

establish, on the balance of probabilities, what the future state of the market will be, both with and without the proposed acquisition.

(2) Secondly (at [146]), the ACCC, as the applicant in that case, was required to prove that:

there is a real chance that, if the proposed acquisition does proceed, that would result in a substantial lessening of competition compared to [the counterfactual].

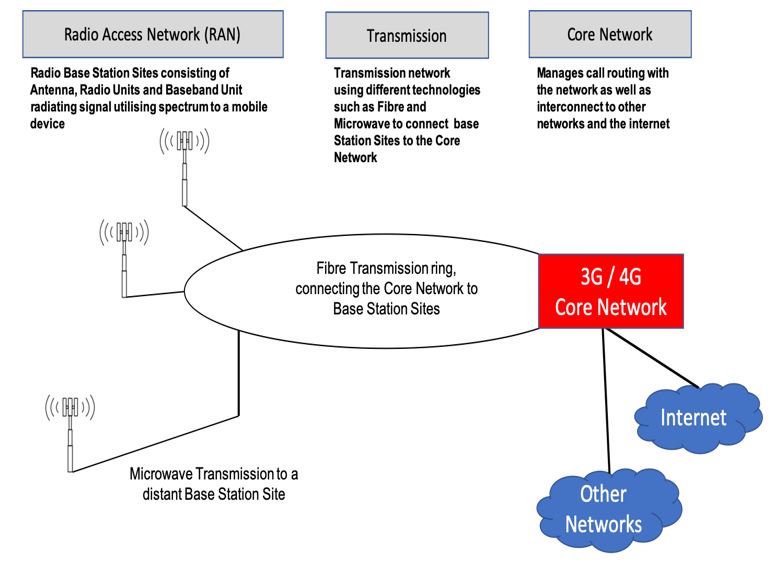

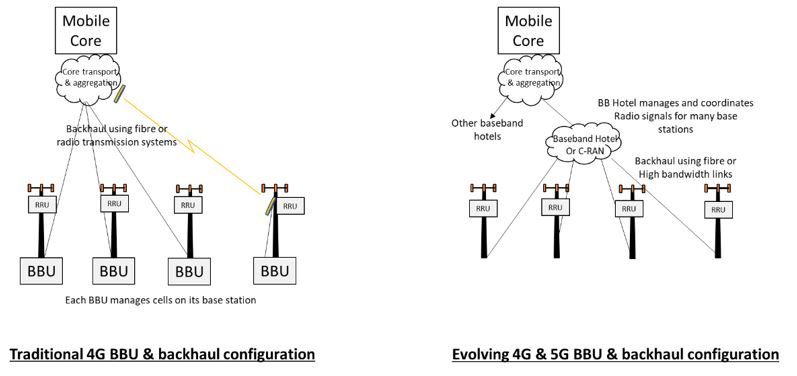

58 On appeal, Yates J held in Metcash at 342 [230] that it was not necessary for the Full Court to reach a concluded view as to which test ought be applied, because Emmett J had found that even:

if the Commission was only required to establish a real chance that its counterfactual case would come to pass in the event that the … acquisition did not proceed to completion, the Commission had not satisfied that standard.

Nonetheless, both Buchanan J (at 307-319 [37]-[90]) and Yates J (at 341-342 [215]-[230]), in obiter, considered the construction of the meaning of ‘likely’, and the appropriateness of separately analysing the counterfactual.

59 Departing from French J’s construction of ‘likely’ in AGL, Buchanan J (at 305 [25]), held that the real chance test should not be applied to s 50, and expressed concern that the test reflected ‘a departure from the ordinary civil standard of proof on the balance of probabilities’ (at 308 [401]). Justice Buchanan also held that if the counterfactual were to be separately proved, both the counterfactual and the substantial lessening of competition limbs ‘require the same standard of proof (balance of probabilities)’ (at 308 [40]). Justice Buchanan considered, however, that ‘they should probably be regarded as constituent elements of a compound conception’ (at 308 [40]).

60 While emphasising that it was not necessary to reach a final view on the matter, Yates J (at 342 [230]) preferred the view that a single-limbed test should be applied, ‘involving one evaluative judgment’, with the ‘real chance’ standard applying ‘to determine the existence and interrelationship of all of those facts, matters and circumstances’ which defined the future state of affairs (at 341 [227], [228]). His Honour explained (at 341-342 [227]-[229]):

If one accepts that the starting point is to draw a distinction between circumstances where an acquisition would have the effect of substantially lessening competition, established on the balance of probabilities, and circumstances where an acquisition would be likely to have that effect, established on the basis that there is a real chance that that would be so, it can be seen that s 50(1) itself imposes its own differential standards of proof, at least so far as the determination of competitive effect is concerned. The utility of imposing differential standards, as a matter of legislative policy, is not at all clear, given that contravention will always be established on the lowest threshold being satisfied. Nevertheless, if one is to proceed on that basis in the present case, then one question involving one evaluative judgment emerges: would the acquisition be likely to substantially lessen competition in the relevant market?

The answer to that question points to, and depends on, the interrelationship of all the facts, matters and circumstances which, in combination, define the future state of affairs that is characterised as being “likely”. If, for the purpose of satisfying the requisite legal standard, “likely” is taken to have the meaning of “a real chance”, then it is difficult to see why that standard should not apply to determine the existence and interrelationship of all those facts, matters and circumstances. If not, the possibility exists that different legal standards will intrude into inseparable elements of the calculus employed to detect change to the state of competition. As I have noted, a counterfactual is no more than an element of that calculus. Conceptually, it has no separate existence or purpose in the present context, other than as an aid to detect the existence and extent of change in the process of competition.

Moreover, in the continuum of fact-finding, there may not be a bright line between those facts that determine the future state of a market and those facts that determine the future state of competition in that market. Indeed, one can envision examples where the facts that show the likely future state of the market will be the very facts that are determinative of a finding about the likely future state of competition in that market. In those cases, can fact-finding be regulated by two different standards of proof? To require, in those cases, the adoption, if that be conceptually possible, of a higher standard for one purpose (to determine the state of the market) would be to obliterate the threshold to which the second limb of s 50(1) has subjected the impugned conduct.

61 As noted above, in Pacific National, Beach J followed the approach of French J in AGL and Yates J in Metcash in respect of the meaning of ‘likely’, holding that ‘in terms of the standard of proof overall, “likely” has been held to mean a real chance’, and that the ACCC, as the applicant in that case, did not ‘necessarily need to prove its counterfactual on the balance of probabilities’ (at [1266] and [1279]).

62 Furthermore, Beach J rejected the proposition that it was appropriate to assess the counterfactual as a discrete enquiry (at [1276]-[1279]). Rather, endorsing the approach taken by Yates J in Metcash (at [1276]-1279]), Beach J found that ‘the subject of the likelihood or real chance is singular in the sense that s 50 refers to the likely effect of substantially lessening competition and thus ultimately poses one question involving one evaluative judgment’ (at [1276]). Accordingly, in his Honour’s view, the application of s 50 in the case before him (at [1276]):

turn[ed] on [his] satisfaction in relation to this single evaluative judgment, even though the exercise of determining whether the competitive effects of a transaction amount to a substantial lessening of competition involves multiple constituent inquiries, namely, identifying the futures with and without the transaction, identifying the effect on competition of each, and then making the relevant comparison leading to answering the one question [above].

Understood in this way, and endorsing the concerns raised by Yates J in Metcash, Beach J considered it ‘a distraction to ask what standards of proof apply at each of the atomised constituent steps involved in assessing competitive effects’ (at [1277]).

63 Each of the parties to these proceedings accepted that the single evaluative judgment approach is to be adopted.

64 When addressing how, as a matter of practical reality, this single evaluative judgment was to be made, Beach J said at [1279] that:

the ACCC does not necessarily need to prove its counterfactual on the balance of probabilities. But the magnitude of any real chance that it demonstrates in respect of the alleged future states will practically and ultimately affect the magnitude of the real chance that it is able to demonstrate in respect of the alleged effects on competition and whether that rises to the requisite level of a likely effect of substantially lessening competition. …

65 Consistently with the analysis of French J in AGL, the reasoning of Yates J sitting as part of the Full Court in Metcash, and Beach J in Pacific National, it is appropriate for the Court in these proceedings to make a ‘single evaluative judgment’. In these proceedings, that ‘single evaluative judgment’ requires Vodafone to satisfy the Court that there is no ‘real chance’ that the merger would likely have the effect of substantially lessening competition (Pacific National at [1277] (Beach J); Metcash at 341-342 [227]-[229] (Yates J)). This is the approach I intend to take.

66 However, I note the submissions of Vodafone, which wished to reserve its position on this issue should the matter go on appeal.

67 Vodafone referred to the analysis of Buchanan J sitting in the Full Court in Metcash. As Buchanan J there explained, the ‘real chance’ standard appeared to slip into the jurisprudence in a series of cases where the construction of ‘likely’ was in no way dispositive. That same observation can equally be made of Beach J’s recent judgment in Pacific National. Vodafone submitted that the authorities in this Court are not a basis for adopting the ‘real chance’ construction, particularly given that that construction is at odds with the ordinary meaning of the word ‘likely’. Vodafone contended that the language of ‘real chance’ is a gloss on the language of the text of the statute, and a surer guide to the proper application of s 50 is to use the language of the statute.

68 I see some force in this approach. One must distinguish between the requirements of the substantive law (s 50) and the principles or rules of evidence. The content of s 50 is not addressing the evidentiary burden. It is addressing the present (‘would have the effect’) and the future (‘be likely to have the effect’) in the context of competition in the relevant market. The burden of proof is set out in s 140 of the Evidence Act 1995 (Cth), keeping in mind the principles referred to by Dixon J in Briginshaw and my discussion above. This does not take away from the evaluative or quantitative judgment a Court still needs to make, which will involve the concepts referred to by French J in AGL: ‘commercially relevant or meaningful’ (at 420 [355]), not ‘a mere possibility’ (at 416-417 [348]), and operating ‘in the real world’ (at 416-417 [348]). These concepts are relevant to the substantive requirement of s 50 to give effect to competition law and policy in the context of merger management. I intend to apply these concepts in these proceedings.

69 However, whatever test is adopted ultimately makes no difference to the outcome in these proceedings because of the conclusions I have reached on the issues presented to the Court.

What amounts to a ‘substantial lessening of competition’?

70 The concept of a ‘substantial’ lessening of competition refers to one that is ‘meaningful or relevant’ to the competitive process. As I have already alluded to, the concept of substantiality also has a temporal aspect. In Pacific National, Beach J observed at [1262]:

the concept of substantially lessening competition does not require a large or weighty lessening of competition, but only one that is meaningful and relevant to the competitive process. A short term effect readily corrected by market processes is not substantial in this respect. But a medium to long term effect not easily corrected may amount to a substantial lessening of competition.

71 I make an observation on the application in these proceedings to the evaluation process. The issue of whether TPG would enter as an MNO is one element of the counterfactual, although, as this issue has been presented to the Court, a significant element. However, it should not be taken for granted that a world with TPG as a fourth MNO is substantially more competitive than a world with Vodafone and TPG merged. In fact Vodafone contended that this will not be the case, and that a world with TPG as a fourth MNO will not be substantially more competitive (and indeed will be less competitive) than a world with the merger. This is a matter legally relevant to this Court’s enquiry in these proceedings.

72 Another matter to note is that s 50 does not require Vodafone to prove that MergeCo would impose an additional competitive constraint on Telstra and Optus beyond that which would be imposed in any event by Vodafone. Section 50 does not impose a positive duty on parties seeking to implement proper commercial arrangements to demonstrate that their mergers will increase competition. A party is entitled to a declaration of non-contravention of s 50 provided that the merger in question would not, and would not likely, substantially lessen competition.

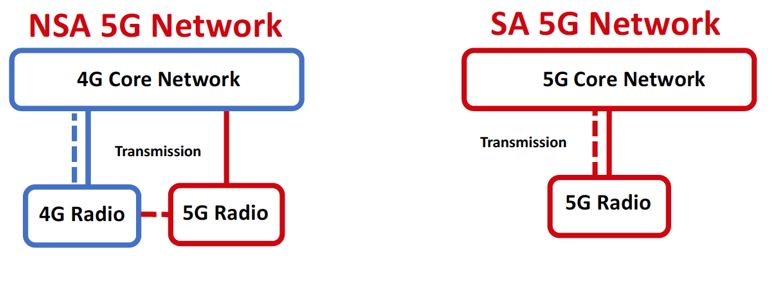

73 The parties provided to the Court chronologies which I have adopted and incorporated into one document which is attached to these reasons as Attachment ‘A’ and marked ‘Court Chronology’. It does not represent an agreed position between the parties, but is based upon documented evidence or unchallenged evidence, which I accept and forms a factual basis of my conclusions.

74 The lay witnesses were as follows:

75 Evidence type | Witness name | Witness description | Evidence relied upon by | Witness cross-examined (Y/N) |

Lay | Badrinath, Vivek | Chief Executive Officer – Rest of World Region, Vodafone Group Plc | VHA | Y |

Baker, Vaughan | Group Director, Government and Corporate Relations, MyRepublic Group Limited | ACCC | Y | |

Banfield, Stephen | Chief Financial Officer and Company Secretary, TPG | TPG | Y | |

Barlow, Todd | Managing Director, Washington H. Soul Pattinson & Company Limited | TPG | Y | |

Berroeta, Iñaki | Chief Executive Officer, VHA | VHA | Y | |

Bley, Yonatan | Head of Pricing and Product for Pre-paid, VHA | VHA | N | |

Bromhead, Nicholas | Leader, Telstra Wireless Solutions, Ericsson Australia Pty Limited | ACCC | Y | |

Chao, Zhang | Senior Product Manager, Huawei Technologies Malaysia | TPG | N | |

Davies, Michael | Head of Revenue, Macquarie Telecom Group Pty Ltd | ACCC | Y | |

Haigh, Adam | Senior wireless engineer / Radio Solutions Manager, Nokia Solutions and Networks Australia Proprietary Limited | ACCC | Y | |

Hanly, David | General Manager Networks, TPG | TPG | Y | |

Jiang, Yilin | Executive Product Manager, Huawei Technologies (Australia) Pty Ltd | TPG | N | |

Keane, Jonny | Data Analytics Manager, VHA | VHA | N | |

Levy, Craig | Chief Operating Officer, TPG | TPG | Y | |

Lopez, Yago | Head of Radio Access Network, VHA | VHA | Y | |

Naik, Dayandhan (Reggie) | General Manager, Fibre Operations & Mobile Deployment, TPG | TPG | Y | |

Pachos, Nick | General Manager, Product & Carrier Management, TPG | TPG | N | |

Pham, Philip | Head of Revenue Growth and Insights, VHA | VHA | N | |

Sivagnanam, Easwaren | General Manager Technology Strategy, VHA | VHA | Y | |

Sixt, Frank | Executive Director, CK Hutchison Holdings Limited | VHA | Y | |

Teoh, David | Executive Chairman of the Board and Chief Executive Officer, TPG | TPG | Y | |

Wang, Hong Wei | Principal Engineer, Wireless Network Product Line Department, Shanghai Huawei Technologies Co. Ltd | TPG | N | |

Ward, Desmond | Electromagnetic Energy Manager, VHA | VHA | Y | |

Ward, Glenn | Director – Sales and Carrier Relations, Exetel Pty Ltd | ACCC | Y | |

Willis, Jennifer | Lawyer, Allens Linklaters | VHA | N | |

Expert | Björnson, Emil | Massive MIMO expert, Associate Professor, Linköping University | TPG | Y |

Davis, Warwick | Economic expert, Frontier Economics | TPG | N | |

Foster, David | Economic expert, Director, Frontier Economics | TPG | Y | |

Gray, Dr Stephen | Valuation and corporate finance expert, Professor of Finance at the University of Queensland Business School / Frontier Economics | VHA | Y | |

Martin, Ian | Telecommunications sector investment expert, New Street Research / Ian Martin Advisory | TPG | N | |

Neal, Michael | Corporate finance expert, Director, Wylde Capital Pty Ltd | ACCC | Y | |

Padilla, Dr Jorge | Economic expert, Compass Lexecon Europe | VHA | Y | |

Smith, Patrick | Economic expert, Partner, RBB Economics | ACCC | Y | |

Wright, Michael | Mobile networks expert , Principal, Quadrature Pty Ltd | ACCC | Y |

76 The determination of these proceedings does not substantially turn on questions of credit in relation to any of the witnesses, including the lay witnesses. In relation to criticisms concerning individual expert witnesses I will consider these in other parts of my reasons.

77 However, I make these general observations on two expert witnesses.

78 Mr Smith was an expert economist called by the ACCC. Clearly Mr Smith is highly skilled and very thorough in his written and oral evidence, specialising as he does in the economics of competition and regulation. He applies economics, econometrics and industrial expertise to competition policy, litigation and arbitration. Mr Smith has acted as an expert witness in investigations of mergers, whether horizontal or vertical, and abuse of market power inquiries, covering excessive pricing, price discrimination, margin squeezing and predation, as well as in the assessment of pricing, profitability valuation and damages estimation in the context of dispute resolution and international arbitration. However, Mr Smith is not familiar with the telecommunications industry, which he readily accepted. Mr Smith necessarily had to rely upon a number of assumptions in reaching his conclusions, but himself recognised that the conclusions he reached would depend upon many factual matters to be determined by the Court in these proceedings.

79 A very important expert witness for the purposes of these proceedings, recognised as such by all parties, was Mr Wright. Mr Wright was an expert called by the ACCC to give evidence on retail mobile networks. Mr Wright had 37 years of experience in the telecommunications industry, and was well versed in the details of rolling out and operating a mobile network in Australia.

80 Mr Wright was a disinterested and objective witness – as lead Counsel for the ACCC put it, he had ‘no dog in this fight’. I have in the main accepted Mr Wright’s evidence: it provides significant objective evidence in a consideration of Mr Teoh’s position and in predicting the future of the retail mobile market.

SUMMARY OF THE RETAIL MOBILE MARKET

81 I now set out a summary of the retail mobile market. This has been taken from the primer prepared by the parties, the pleadings and substantially from Vodafone’s closing written submissions. I regard this summary as non-controversial. Where reference is made to the position of Vodafone, such as in relation to its current plan to roll-out 5G, the cost of a roaming agreement, market conditions and types of product (such as pre-paid and post-paid plans), I have relied upon the uncontested evidence presented by Vodafone or TPG.

82 The primer prepared by the parties is attached to these reasons as Attachment ‘B’, which also has incorporated the definitions of various terms or abbreviations used in these reasons where otherwise not indicated herein.

Characteristics of mobile networks in Australia

83 As a very general statement, the retail mobile market is a market characterised by relatively robust price competition which has only intensified since 2014.

84 Retail mobile services in Australia are supplied by MNOs and MVNOs. There are three MNO competitors in Australia, being Telstra, Optus and Vodafone. There are approximately 60 MVNO competitors in Australia. MVNOs acquire mobile services on a wholesale basis from MNOs.

85 Mobile networks have three primary components:

(1) a RAN, consisting of base stations that communicate with mobile devices over designated spectrum;

(2) a ‘backhaul’ transmission network, which connects the RAN sites to the core network; and

(3) a core network, which connects and manages the different parts of the network and connects to other networks (including the internet).

86 An MNO requires considerable funding to establish and maintain a mobile network. Operating a mobile network is a capital-intensive business driven by the need for constant investment. This is because competitive pressures demand constant improvements in capacity and quality:

(1) mobile technology is constantly evolving, with each new generation enabling new services and better quality. At present, the introduction of 5G is driving the requirement for MNOs to invest in upgrading their networks, with Telstra and Optus already offering 5G services;

(2) it is necessary to increase regularly the capacity of the network to ensure that a quality service can be delivered to consumers. This can only be done by acquiring additional spectrum if available, building new sites and/or upgrading equipment. At present, there is an urgent need to increase capacity because consumer data usage is increasing each year. Telstra and Optus have reported that data traffic on their networks is growing at 50% year-on-year. XXX XXXXXXX XXXXXX XXXX XX XXXX XXXXXX XX XXX XXXXXXXX XXXXXXX XX XXXXXXX XXX XXX XXXX;

(3) it is necessary to replace aged or superseded equipment; and

(4) it is necessary to maintain and upgrade networks between generational changes.

87 Given the high fixed cost involved in establishing and maintaining a mobile network, scale is very important for an MNO to compete effectively. By contrast, entry is relatively easy for MVNOs, which rely on wholesale access to an MNO’s network to supply services to customers.

Significance of network coverage and capacity

88 Two key aspects of the quality of a mobile network are:

(1) ‘coverage’ – the geographic locations that a customer’s mobile device is able to connect to a base station site in the mobile network; and

(2) ‘capacity’ – the amount of combined data bandwidth (usually measured in multiples of bps) a network has to support the volume of voice and data traffic generated by multiple simultaneous users on a network at defined performance standards.

89 Coverage can be measured either by geographic area or the proportion of the Australian population that the MNO can reach. Indoor coverage is also an important aspect of the quality of a network. While coverage is typically advertised on an outdoor basis, each MNO has sought to achieve good indoor coverage as consumers require coverage indoors, at work and at home. Achieving indoor coverage requires significantly higher RAN investment than that required to achieve outdoor coverage.

90 To offer the mobility that customers expect from mobile services, coverage needs to be provided in the areas where customers ‘work, live and play’, and the areas in-between. If an MNO does not have coverage in an area, its customers will be unable to use their mobile devices in that area. Coverage is important to consumers, corporates and enterprise customers – in other words, ‘coverage matters’ and is a significant aspect of competition between MNOs. It is for this reason that MNOs and MVNOs advertise and promote their network coverage.

91 The capacity of a mobile network is affected by:

(1) the nature and amount of spectrum to which the MNO has rights;

(2) the location, number and type of macro RAN sites and small cell sites;

(3) the capability and type of equipment used in the network, including spectral efficiency of the technology used; and

(4) the capacity of the transmission network.

Telstra currently holds more spectrum than Optus in regional and rural areas and more than Vodafone and TPG in all areas (ie metropolitan, regional and rural) while Optus holds more spectrum than Telstra, Vodafone or TPG in several major metro areas.

92 Network coverage and capacity contribute to customers’ perceptions of network quality, which refers to factors such as voice quality, ability to establish a call, ability to maintain a call, data speed and latency (ie time taken for data to travel to and from the customer). Lower network quality may, for example, manifest in slow download speed (which results in ‘buffering’, ie delays in service), an inability to use certain mobile applications or poor voice quality or drop outs. The maximum video resolution that can be streamed depends on the capacity that is made available by the network.

93 Poor network quality is a driver of customers switching from one MNO to another (referred to as ‘churn’). Total network capacity affects the number of customers an MNO network can sustain.

94 Inferior network quality was the cause of what has come to be known as ‘Vodafail’ (which I will discuss in detail later). From December 2010, Vodafone experienced serious network issues, which caused high rates of dropped calls and poor internet connectivity. Vodafone lost considerable market share which it has never recovered despite making significant network investment.

95 Given the importance of network quality to customers, Vodafone, Telstra and XXX XXXX XXXX XXXXX XXXX XXXXX XXXX XXXX XXXX XXXX. Vodafone uses Ookla data, and other measures, to report its network speeds internally. That data shows that Vodafone’s average download speeds have declined and are now considerably lower than Telstra and Optus’ average speeds.

96 XXXXX XXXXX XXX XXXXXXXX XXXX XXXXX XXXXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX XXXXXXXXX XXXX XXXXX XXXXX XXXXX XXXX.

Participants in the retail mobile market

97 Vodafone is the third largest supplier of mobile telecommunications services in Australia. Its business comprises the supply of retail mobile services, wholesale mobile services to MVNOs, and since December 2017, the supply of retail fixed line broadband services on the NBN in metropolitan areas. Vodafone supplies retail mobile services under the ‘Vodafone’, ‘Lebara’ and ‘Kogan Mobile’ brands. Vodafone’s mobile customer base comprises approximately six million customers. Vodafone uses the Lebara and Kogan brands as its second brands with a view to targeting value or price sensitive consumers at the low end of the market (XXXXXXXXX XXXXX XXXXXX XXXXX XXX).

98 Vodafone operates a 3G and 4G mobile network. As a result of the ‘Security Guidance’ (which I will return later to), to roll-out a 5G network, Vodafone must replace its existing Huawei 4G equipment with new equipment. This would also be the case for MergeCo. XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXX XXXXX XXXX XXXX XXXX XXXX XXXX XXXXXXX XXXXXX XXXXXX XXXXX XXXXX XXXX XXXX XXX XXXXXXX XXXXXX XXXXXX XXXXXX XXXXX XXXXXX XXXX XXXX XXXX.

99 Vodafone supplies mobile services to enterprise customers. Vodafone’s revenue from the sale of mobile services to enterprise customers in the 2018 financial year was around XXX XXXXXXX. This figure includes sales of mobile services to the small office/home office segment (‘SOHO’) as well as small businesses.

100 Other than retail fixed broadband services through the NBN to consumers and SOHO, Vodafone does not offer any fixed telecommunications services to businesses. Vodafone is not a relevant competitor in that segment as it does not provide services such as static IP, fibre transmission, fixed voice, cloud and colocation services that are provided by entities such as TPG and Macquarie Telecom.

101 The geographic coverage of Vodafone’s network is approximately 600,000 square kilometres and reaches around 96% of the population. Vodafone acquires roaming services from Optus under an agreement which came into effect in 2012. Under that agreement, Optus supplies roaming services to Vodafone, which extends Vodafone’s network coverage from 600,000 square kilometres (reaching 96% of the Australian population) to 900,000 square kilometres (reaching 97% of the Australian population).

102 The cost of roaming under this agreement is unsustainable for Vodafone: XXXX XXXX XXXX XXXX XXXXXX XXXXXX XXXXX XXXXX. This was largely due to the significant increases in mobile data traffic XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX. Vodafone has taken ‘demand management’ steps to try to curb the costs XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX.

103 TPG carries on business as:

(1) a supplier of retail fixed broadband services and retail fixed voice services to retail, small business, government, enterprise and wholesale customers;

(2) a supplier (as an MVNO) of retail mobile services to consumers; and

(3) a provider, through its subsidiaries AAPT and PIPE Networks Pty Ltd, of wholesale transmission services to other telecommunications service providers.

104 TPG has historically expanded through acquisitions. TPG acquired AAPT in 2014, which owned inter-capital fibre optic infrastructure, and diversified TPG’s revenue. In around September 2015, TPG acquired iiNet which gave it a larger retail customer base in retail fixed broadband services.

105 TPG’s key retail brands are TPG, iiNet and Internode. TPG has approximately 1.9 million fixed broadband subscribers. TPG owns and operates its own voice, data and internet network infrastructure.

106 TPG operates as an MVNO and has approximately 415,000 mobile subscribers in total. TPG has agreements with Vodafone and Optus to acquire wholesale mobile services.

107 In April 2017, TPG decided to acquire 700 megahertz (‘MHz’) spectrum and announced its intention to roll-out a mobile network.

108 Telstra supplies retail mobile services and retail fixed broadband services and has the largest number of subscribers for those services. It is the largest MNO by a considerable margin, with over 15 million subscribers. This market share does not include Telstra’s market share in the enterprise and government sectors, nor its second brands and MVNOs.

109 Telstra supplies retail mobile services under:

(1) the ‘Telstra’ brand. XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX XXXX XXXX XXXX XXXX XXXX XXXX;

(2) its second brand, ‘Belong’. Belong is a division of Telstra Corporation Limited. Belong commenced supplying retail mobile services in around October 2017 and by 30 June 2019, had around 248,000 subscribers. Telstra launched Belong to seek to improve Telstra’s ability to capture share in the price sensitive segment;

(3) the ‘Boost Mobile’ brand. Boost Mobile acts as a reseller for Telstra. Telstra’s focus for Boost has traditionally been the youth (16 to 34 years old) segment, and target customers such as school leavers, university students and young people starting their first job.

110 Telstra has 3G and 4G networks and is in the process of rolling out a 5G network. Telstra is advertising its 5G proposition heavily. Telstra has also already introduced Samsung and LG phones that are 5G compatible and engaged in significant marketing to promote its 5G roll-out. Telstra’s marketing is aimed at educating customers about 5G and its benefits.

111 The geographic network coverage of Telstra’s 3G and 4G networks greatly exceeds that of its competitors. Given that Telstra owns almost all of the network infrastructure in regional and rural Australia, other MNOs are required to pay Telstra, typically at a premium price, to access its infrastructure in order to provide services in these areas. For example, Vodafone must pay Telstra for use of its transmission infrastructure in certain regional areas where Telstra is the only supplier. Some transmission services are regulated but many services and elements of the charges are not.

112 Technology leadership is an important part of Telstra’s competitive strategy and it invests heavily in its mobile and fixed networks to achieve it.

113 Telstra is able to offer bundled products and services due to its position in the mobile and fixed services markets. Telstra also has a dominant position in the supply of both fixed and mobile telecommunication services to corporate and government sectors. In the 2018 financial year Telstra reported that its mobile services revenue for its small business and enterprise segments was $2.775 billion.

114 Telstra supplies mobile services by wholesale to MVNOs and, following Optus, has the second largest number of customers of wholesale mobile services. Currently, the MVNOs on Telstra’s network include: ALDI Mobile, Lycamobile, Pennytel, Southern Phone, Tangerine Telecom, TeleChoice, Think Mobile and Woolworths Mobile. As at December 2017, Telstra had 862,000 MVNO subscribers. By December 2018, that figure had grown to 1,098,000 subscribers.

115 Telstra owned and operated the legacy copper network, prior to its recent transfer in part to NBN Co. Telstra owns and operates an extensive transmission network and supplies wholesale transmission services to other service providers. Telstra acquires wholesale services from NBN Co, supplies NBN wholesale aggregation services to smaller retail service providers and has had the largest number of wholesale services in operation on the NBN.

116 Telstra is in a very strong financial position, with significant funds available for capital expenditure. Its financial position is in part due to its arrangements with government including NBN Co, under which Telstra received substantial payments from NBN Co for the transfer of its copper and hybrid fibre coaxial assets, duct rentals and in respect of each customer disconnected from Telstra’s access network.

117 Optus supplies mobile services in Australia and is the second largest MNO in Australia with a retail market share of approximately 28%. As at 31 March 2019, Optus had over 10 million wholesale and retail mobile subscribers. Optus has a 3G and 4G network and is also in the process of rolling out a 5G network. Optus supplies retail mobile services under the ‘Optus’ brand. It used the ‘Virgin Mobile’ brand until May 2018, but has been phasing it out since then. In February 2018, Optus entered into an agreement with Catch Group, which has a similar business to Kogan, to sell Optus mobile services under the brand ‘Catch Connect’.

118 Optus also supplies wholesale mobile services to MVNOs and has the highest number of customers for wholesale mobile services. Currently, the MVNOs/resellers on Optus’ network are: amaysim Australia Limited (‘amaysim’), Catch Connect, Coles Mobile, Dodo, Exetel, Hive Mobile, iiNet, Jeenee Mobile, Moose Mobile, OVO, Southern Phone, SpinTel, Vaya and Yomojo. amaysim is the largest MVNO in Australia. As at December 2018, amaysim reported having around 1.2 million subscribers.

119 Like Telstra and Vodafone, XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX. Optus’ strategy has also been to position its Optus branded business as comparable to Telstra’s ‘premium network’. To that end, Optus has invested considerable amounts of money to improve and market network performance. It has also sought to differentiate its offering by investing in acquiring content for broadcast to its subscribers.

120 Optus has the third largest number of customers for retail fixed broadband services, following Telstra and TPG. To supply these services, Optus acquires wholesale services from each of NBN Co and Telstra. Optus also supplies NBN wholesale aggregation services to smaller retail service providers and has had the third largest number of wholesale services in operation on the NBN.

121 Optus also supplies mobile and fixed telecommunication services to corporate and government customers. It is one of the key competitors in this space, although it is a long way behind Telstra. XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX. Optus also owns and operates its own transmission network and supplies wholesale transmission services to other service providers.

122 Optus is in a strong financial position and has significant funds available for capital expenditure.

Coverage and capacity of the three MNOs

123 The three mobile networks in Australia have different geographic footprints but are similar in terms of population coverage. Telstra’s network has the largest coverage footprint, at over 2.4 million square kilometres. Optus is the second largest, at around one million square kilometres. Vodafone’s network has the smallest geographic coverage at around 600,000 square kilometres, which increases to 900,000 square kilometres under Vodafone’s roaming agreement with Optus.

124 The differences appear smaller when expressed as population coverage due to population distribution. Telstra’s 3G network covers around 99.3% of the population, Optus’ 3G network covers around 98.5% of the population and Vodafone’s 3G network covers around 95.7% of the population, although this can extend to 97% under its Optus roaming agreement (which I referred to earlier). Geographic coverage remains important in areas of low population density – eg along highways and other transport routes in rural areas.

125 As noted above, there are approximately 60 MVNOs operating in Australia. There are low barriers to entry into the market for MVNOs.

126 While MVNOs set their retail prices independently, they are necessarily limited by the economics of their wholesale arrangements with the relevant MNO. Given this, MVNOs compete with each other and with the MNOs on price and customer support. There has been an increase of 30% in the market share of MVNOs since June 2016.

Segmentation and revealed preferences in the retail mobile market

127 XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXX XXXXX XXXXX XXXXX XXXX XXXX XXXX XXXX XXXX XX XXXX XXXX XXXX XXXX XXXX XXXX.

Market shares (current and historical)

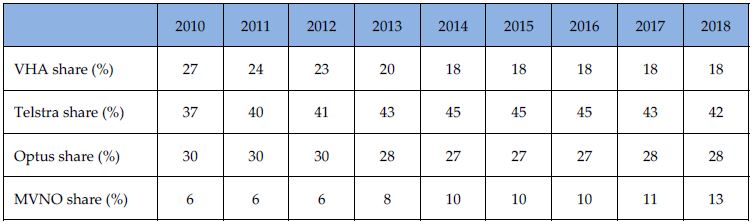

128 Based on figures taken from the ACCC Telecommunications Reports 2013-2014 and the ACCC Communications Market Report 2017-2018, the table below sets out market shares for the period 2010 to 2018. The market shares for the MVNOs in this table may include the second brands of the MNOs:

Types of mobile services offered (pre-paid and post-paid)

129 There are two main types of mobile products sold in Australia: pre-paid mobile products and post-paid mobile products. With a pre-paid mobile product, customers pay in advance for a particular voice and data allowance to be used within a particular period. Following that period, the subscriber must ‘recharge’. With a post-paid mobile product, customers are billed on a regular basis after a period (typically monthly) of usage pursuant to a customer’s contract (usually 12, 24 or 36 months). The customer does not lose access to mobile services if they exceed their plan allowances. However, they may be charged for any additional usage on their next bill.

130 Vodafone supplies both pre-paid and post-paid products under its primary ‘Vodafone’ brand, as do Telstra and Optus under their primary brands. Vodafone also supplies pre-paid products under the Kogan and Lebara brands. Vodafone’s post-paid products account for around XX% of Vodafone’s total retail mobile revenue. Post-paid plans may be offered as SIM only (‘SIMO’) plans or as handset plans. Under SIMO plans, customers purchase a mobile service but not a mobile handset for use in connection with that service. Under handset plans, customers purchase both a mobile service and a handset and pay for the cost of the handset over a specified period (12 to 36 months). While pre-paid mobile services may be bundled together with a handset, in many cases pre-paid mobile services are supplied without a handset.