FEDERAL COURT OF AUSTRALIA

Lloyd v Belconnen Lakeview Pty Ltd [2019] FCA 2177

File numbers: | NSD 1417 of 2017 NSD 1555 of 2018 |

Judge: | LEE J |

Date of judgment: | 20 December 2019 |

Catchwords: | CONTRACT – money had and received – failure of consideration and mistake – contract between vendors and purchasers – price included an amount payable referable to GST – GST component a distinct part of consideration paid by purchasers – vendors not liable to pay GST – purchasers sought repayment of money as a result of failure of consideration and mistake – whether vendors had title to retain the money in whole or part – whether failure a distinct and severable part of the consideration RESTITUTION – recovery – unjust enrichment – relevance of contract – whether vendors had a duty to make restitution to the purchasers in whole or part –whether defence applies to obligation to repay in whole or part TAXATION AND REVENUE LAW – A New Tax System (Goods and Services Tax) Act 1999 (Cth) – consequences of decision in Federal Commissioner of Taxation v Gloxinia Investments Ltd [2010] FCAFC 46; (2010) 183 FCR 420 – operation of transitional arrangements and sale of residential premises by developers an input taxed supply REPRESENTATIVE PROCEEDINGS – representative proceedings – complex class action – Merck orders concerning initial trial – adjudication of individual claims, common issues and ‘issues of commonality’ TRADE PRACTICES – consumer protection – misleading and deceptive conduct and unconscionable conduct –– whether respondents’ conduct towards applicants amounted to contravening conduct TRADE PRACTICES – consumer protection – whether respondents’ conduct unconscionable DAMAGES – measure of damages – respondent a willing vendor – if properly informed an applicant would have sought reduction in purchase price for unit – causation – loss of a chance – standard of proof – calculation of loss |

Legislation: | Australian Consumer Law ss 18, 21 Australian Securities and Investments Commission Act 2001 (Cth) s 12CB A New Tax System (Goods and Services Tax) Act 1999 (Cth) ss 9-5, 9-10, 9-70, 11-5, 19-10(1)(c), 29-70, 38-325, 75-5, 75-10, 75-20, 75-30 Civil Law (Sale of Residential Property) Act 2003 (ACT) Competition and Consumer Act 2010 (Cth) Pt XI Constitution s 90 Evidence Act 1995 (Cth) s 136 Federal Court of Australia Act 1976 (Cth) ss 33ZB Land Titles Act 1925 (ACT) s 48 Tax Laws Amendment (2011 Measures No. 9) Act 2012 (Cth) Trade Practices Act 1974 (Cth) |

Cases cited: | A & A Property Developers Pty Ltd v MCCA Asset Management Ltd [2017] VSCA 365 Abigroup Contractors Pty Ltd v Sydney Catchment Authority (No 3) [2006] NSWCA 282; (2006) 67 NSWLR 341 ABN AMRO Bank NV v Bathurst Regional Council [2014] FCAFC 65; (2014) 224 FCR 1 Australia and New Zealand Banking Group Limited v Westpac Banking Corporation (1988) 164 CLR 662 Australian Competition and Consumer Commission v Universal Music Australia Pty Ltd [2001] FCA 1800; (2001) 115 FCR 442 Australian Financial Services and Leasing Pty Limited v Hills Industries Limited [2014] HCA 14; (2014) 253 CLR 560 Australian Securities and Investments Commission v Hellicar [2012] HCA 17; (2012) 247 CLR 345 Australian Securities and Investments Commission v Kobelt [2019] HCA 18; (2019) 93 ALJR 743 Avon Products Pty Limited v Commissioner of Taxation [2006] HCA 29; (2006) 230 CLR 356 Badenach v Calvert [2016] HCA 18; (2016) 257 CLR 440 Baltic Shipping Company v Dillon (1993) 176 CLR 344 Bowler v Hilda Pty Ltd [2000] FCA 899 Brady King Pty Ltd v Commissioner of Taxation [2008] FCAFC 118; (2008) 168 FCR 558 Bullabidgee Pty Ltd v McCleary [2011] NSWCA 259 Butcher v Lachlan Elder Realty Pty Limited [2004] HCA 60; (2004) 218 CLR 592 Campbell v Backoffice Investments Pty Ltd [2009] HCA 25; (2009) 238 CLR 304 Chowder Bay Pty Ltd v Paganin [2018] FCAFC 25 Commercial Union Assurance Company of Australia Limited v Ferrcom Pty Ltd (1991) 22 NSWLR 389 Commissioner of State Revenue (Vic) v Royal Insurance Australia Limited (1994) 182 CLR 51 Commissioner of Taxation v DB Rreef Funds Management Limited [2006] FCAFC 89; (2006) 152 FCR 437 Coshott v Lenin [2007] NSWCA 153 Darvall McCutcheon v H K Frost Holdings Pty Ltd [2002] VSCA 85; (2002) 4 VR 570 David Securities Pty Limited v Commonwealth Bank of Australia (1992) 175 CLR 353 Demagogue Pty Ltd v Ramensky (1992) 39 FCR 31 Dillon v RBS Group (Australia) Pty Limited [2017] FCA 896; (2017) 252 FCR 150 Dovuro Pty Limited v Wilkins [2003] HCA 51; (2003) 215 CLR 317 Duoedge Pty Ltd v Leong [2013] VSC 36 Equuscorp Pty Ltd v Haxton [2012] HCA 7; (2012) 246 CLR 498 Falkingham v Hoffmans (a firm) [2014] WASCA 140; (2014) 46 WAR 510 Farah Constructions Pty Limited v Say-Dee Pty Limited [2007] HCA 22; (2007) 230 CLR 89 Federal Commissioner of Taxation v Gloxinia Investments Ltd [2010] FCAFC 46; (2010) 183 FCR 420 Gill v Ethicon Sàrl (No 3) [2019] FCA 587 Graham & Linda Huddy Nominees Pty Ltd v Byrne [2016] QSC 221 Graham Barclay Oysters Pty Limited v Ryan [2002] HCA 54; (2002) 211 CLR 540 Ha v New South Wales (1997) 189 CLR 465 Hanave Pty Ltd v LFOT Pty Ltd (formerly Jagar Projects Pty Ltd) [1999] FCA 357; (1997) 43 IPR 545 Hodgson, D H, “The Scales of Justice: Probability and Proof in Legal Fact-finding” (1995) 69 ALJ 731 HTW Valuers (Central Qld) Pty Ltd v Astonland Pty Ltd [2004] HCA 54; (2004) 217 CLR 640 Jones v Dunkel (1959) 101 CLR 298 Klemweb Nominees Pty Ltd (as trustee for the Klemweb Superannuation Fund) v BHP Group Limited [2019] FCAFC 107; (2019) 369 ALR 583 Kovan Engineering (Aust) Pty Ltd v Gold Peg International Pty Ltd [2006] FCAFC 117; (2006) 234 ALR 241 La Trobe Capital & Mortgage Corporation Ltd v Hay Property Consultants Pty Ltd [2011] FCAFC 4; (2011) 190 FCR 299 Lipkin Gorman v Karpnale Ltd [1991] 2 AC 548 Mann v Paterson Constructions Pty Ltd [2019] HCA 32; (2019) 373 ALR 1 Masters Home Improvement Australia Pty Ltd v North East Solutions Pty Ltd [2017] VSCA 88 Merck Sharp & Dohme (Australia) Pty Ltd v Peterson [2009] FCAFC 26; (2009) 355 ALR 20 Miller & Associates Insurance Broking Pty Ltd v BMW Australia Finance Limited [2010] HCA 31; (2010) 241 CLR 357 Mount Bruce Mining Pty Limited v Wright Prospecting Pty Limited [2015] HCA 37; (2015) 256 CLR 104 Nikolic v Oladaily Pty Ltd [2007] NSWCA 252 Niru Battery Manufacturing Co v Milestone Trading Ltd [2002] EWHC 1425 (Comm); 2 All ER (Comm) 705 Nunin Holdings Pty Ltd v Tullamarine Estates Pty Ltd [1994] 1 VR 74 Paciocco v Australia and New Zealand Banking Group Ltd [2015] FCAFC 50; (2015) 236 FCR 199 Parkdale Custom Built Furniture Proprietary Limited v Puxu Proprietary Limited (1982) 149 CLR 191 Pavey & Matthews Proprietary Limited v Paul (1987) 162 CLR 221 Pereira v Director of Public Prosecutions (1988) 82 ALR 217 Prasad v Sangha [2012] NSWCA 92 Regent Holdings Pty Ltd v State of Victoria [2012] VSCA 221; (2012) 36 VR 424 Rinbridge Marketing Pty Ltd v Walsh [2000] FCA 1738 Roxborough v Rothmans of Pall Mall Australia Limited [2001] HCA 68; (2001) 208 CLR 516 Sellars v Adelaide Petroleum NL (1994) 179 CLR 332 Sindel v Georgiou (1984) 154 CLR 661 Smith v Moloney [2005] SASC 305; (2005) 92 SASR 498 Sterling Guardian Pty Ltd v Commissioner of Taxation [2006] FCAFC 12; (2006) 149 FCR 255 Taco Company of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 Ted Brown Quarries Pty Ltd v General Quarries (Gilston) Pty Ltd (1977) 16 ALR 23 Thomas v SMP (International) Pty Ltd [2010] NSWSC 822 Waribay Pty Ltd v Minter Ellison [1991] 2 VR 391 WesTrac Pty Ltd v Eastcoast OTR Tyres Pty Ltd [2009] NSWSC 728 Wilkie v Gordian Runoff Limited [2005] HCA 17; (2005) 221 CLR 522 Wyzenbeek v Australasian Marine Imports Pty Ltd (in Liq) [2019] FCAFC 167 Yorke v Lucas (1985) 158 CLR 661 Woolf, H, Access to Justice Report, Final Report (London, HMSO), 1996 Allsop, J, “Restitution: Some historical remarks” (FCA) [2015] FedJSchol 22 Birks, P, “Failure of Consideration and its Place on the Map” (2002) 2 OUCLJ 1 Edelman, J and Bant, E, Unjust Enrichment (Oxford, 2nd ed, 2016) Heydon, JD, Heydon on Contract (2019, Thomson Reuters) Jackman, I, The Varieties of Restitution (Federation Press, 2nd ed, 2017) Mason K, Carter J W, and Tolhurst G J, Restitution Law in Australia (LexisNexis, 3rd ed, 2016) |

Date of hearing: | 1, 2, 3, 9, 22 May, 3, 24, 25, 26 June, 5 October 2019 |

Date of last submission: | 23 October 2019 |

Registry: | New South Wales |

Division: | General Division |

Nation practice area: | Commercial and Corporations |

Sub-Area: | Commercial Contracts, Banking, Finance and Insurance |

Category: | Catchwords |

Number of paragraphs: | 392 |

Counsel for the Applicants | Mr A J L Bannon SC, Mr C Colquhoun, Mr C McMeniman |

Solicitor for the Applicants | Corrs Chambers Westgarth |

Counsel for the First Respondent in NSD1417/2017 | Mr N C Hutley SC, Mr A J McInerney SC, Mr A R R Vincent |

Counsel for the Second and Third Respondents in NSD1417/2017 | Mr N Hutley SC, Mr A R R Vincent |

Solicitor for the Respondents in NSD1417/2017 | HWL Ebsworth Lawyers |

Counsel for the Respondents in NSD1555/2018 | Mr N Hutley SC, Mr J Hewitt |

Solicitor for the Respondents in NSD1555/2018 | K & L Gates |

ORDERS

NSD 1417 of 2017 | ||

| ||

BETWEEN: | SUSAN MARGARET LLOYD Applicant | |

AND: | BELCONNEN LAKE VIEW PTY LTD ACN 127 550 029 First Respondent JOHN KINLOCH HINDMARSH Second Respondent GERALD JOHN RYAN Third Respondent | |

JUDGE: | LEE J |

DATE OF ORDER: | 20 DECEMber 2019 |

THE COURT ORDERS THAT:

1. By 3pm on 24 December 2019 the parties are to provide to the Associate to Justice Lee agreed or competing Short Minutes of Order which provide a timetable for the exchange of further submissions and proposed orders, including orders pursuant to s 33ZB of the Federal Court of Australia Act 1976 (Cth).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

ORDERS

DATE OF ORDER: |

THE COURT ORDERS THAT:

1. By 3pm on 24 December 2019 the parties are to provide to the Associate to Justice Lee agreed or competing Short Minutes of Order which provide a timetable for the exchange of further evidence in relation to the case of the first and second applicants and further submissions and proposed orders, including orders pursuant to s 33ZB of the Federal Court of Australia Act 1976 (Cth).

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011

LEE J:

[1] | |

[17] | |

[17] | |

[21] | |

B.3 The Centrality of the Contracts to the Resolution of all Issues | [24] |

[31] | |

[31] | |

[45] | |

[49] | |

[52] | |

[69] | |

[71] | |

[86] | |

[86] | |

[97] | |

[97] | |

[99] | |

[116] | |

[132] | |

[140] | |

[140] | |

[166] | |

[166] | |

[176] | |

[178] | |

[178] | |

[181] | |

[182] | |

[197] | |

[210] | |

[210] | |

[212] | |

[217] | |

[222] | |

[222] | |

[228] | |

[235] | |

[235] | |

[237] | |

[254] | |

[260] | |

[261] | |

[268] | |

[288] | |

[289] | |

[289] | |

[293] | |

[294] | |

[295] | |

[301] | |

[304] | |

[305] | |

[311] | |

[311] | |

[312] | |

[313] | |

[313] | |

[318] | |

[325] | |

[333] | |

[337] | |

[370] | |

[372] | |

[373] | |

[374] | |

[387] |

A INTRODUCTION & FACTUAL BACKGROUND

1 These two class actions give rise to a number of legal complexities, but their genesis is easily understood.

2 As is generally known, even by those with no detailed knowledge of the entrails of the A New Tax System (Goods and Services Tax) Act 1999 (Cth) (GST Act), a supply of residential premises is generally an input taxed supply, and hence not subject to goods and services tax (GST). As a result, ordinary property owners need not pay an amount representing GST on their homes, nor on their investment properties. Despite this, generally, a supply of new residential premises is not input taxed and will be subject to GST. The apparent rationale being that GST is levied on the value added to the property by the developer.

3 Speaking generally, “new residential premises” is a term defined in the GST Act to include residential premises which have not previously been sold as residential premises and have not been the subject of a long-term lease. It is often the case that development of flats occurs where a developer enters into a development lease, the terms of which require the developer to undertake the development and, once completed, the development lease is surrendered and the land upon which the flats are built is supplied to the developer by way of sale or grant of a long-term lease. For some time, it was thought that when developers later sold the flats, there was a sale of “new residential premises” and GST was payable. But as it turned out, things were not quite so simple.

4 In Federal Commissioner of Taxation v Gloxinia Investments Ltd [2010] FCAFC 46; (2010) 183 FCR 420, the Full Court, by majority, held that in the circumstances described above, the sale of residential premises by the developer was an input taxed supply. The flats or home units were no longer “new” because they had been the subject of a long-term lease. Given that this was a departure from the then prevailing understanding of the Australian Taxation Office (ATO), unsurprisingly and promptly thereafter, legislation was passed (Tax Laws Amendment (2011 Measures No. 9) Act 2012 (Cth) (Amending Act)), which meant, subject to transitional arrangements, sales of newly constructed residential premises, which were the subject of a development lease arrangement, are subject to GST.

5 For the developers sued in these class actions, this presented an opportunity. Spurred on by an entrepreneurial accounting firm, Maxim Chartered Accountants (Maxim), the respondents engaged Maxim to apply for a private ruling from the ATO to the effect that sales to be made to purchasers were not taxable supplies, by reason of the operation of the transitional provisions contained in the Amending Act.

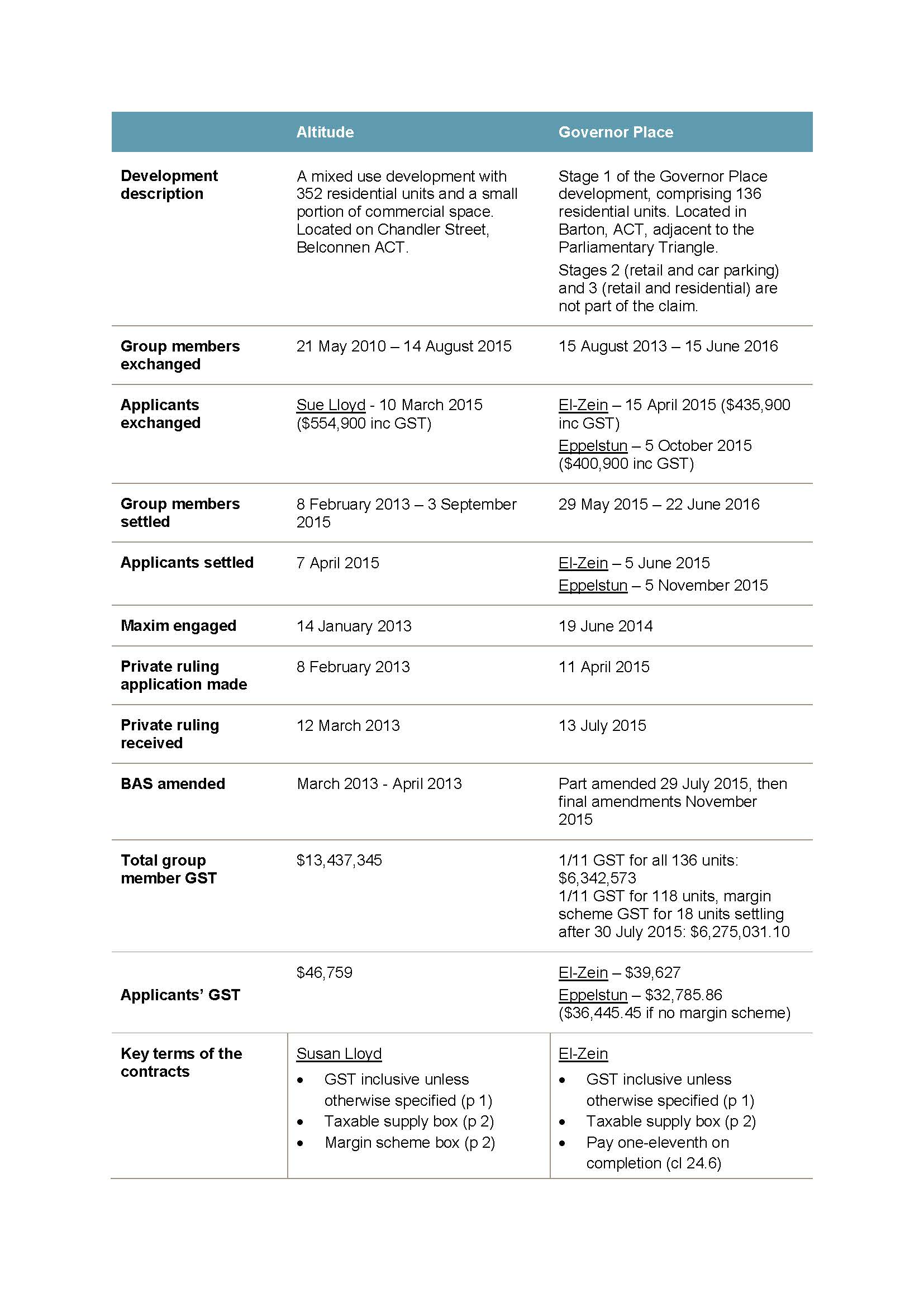

6 The first developer was Belconnen Lakeview Pty Limited (the trustee of the Belconnen Lakeview Unit Trust) (Belconnen). It was the developer of the “Altitude Apartments” (Altitude), located on land in the suburb Belconnen, in the Australian Capital Territory. In 2007, Belconnen purchased the unexpired term of the relevant Crown Lease and was granted development approval in 2009. From about 2010, Belconnen offered to enter into, and entered into, contracts to sell the unexpired term of the then unregistered unit leases for the flats to be developed in Altitude (the building of which commenced in mid-2011). Eventually, in February 2013, the units plan was registered and upon registration, the Crown Lease ended and Belconnen became the holder of an estate in leasehold in each of the unit leases and Belconnen was entitled to sell the flats (strictly speaking, the unexpired term of the unit leases for the units) (Altitude Units). The contracts for the Altitude Units (Altitude Contracts) started settling from 8 February 2013 and did not finish settling until 3 September 2015.

7 Discussions with Maxim had started around the middle of 2012 and Maxim was engaged in January 2013. A private ruling request was lodged on behalf of Belconnen with the ATO on 8 February 2013. Shortly thereafter, on 12 March 2013, the Commissioner of Taxation (Commissioner) issued a private ruling to Belconnen to the effect that the sales of the Altitude Units were input taxed and not taxable supplies, subject to Belconnen amending any GST returns that had been lodged to ensure that all acquisitions were treated as not being creditable acquisitions (Altitude Private Ruling). GST returns were subsequently amended in March and April 2013.

8 Despite this, all the Altitude Contracts were prepared on the basis that the sales of the Altitude Units would be taxable supplies. The price of the Altitude Units (Price) was described in the Altitude Contracts as being inclusive of GST.

9 The second developers were Barton Nine Pty Limited as trustee of the Barton Nine Settlement and 13.9 Barton Pty Limited as the trustee of the 13.9 Barton Commercial Property Trust (Barton Developers). The history of this development is broadly similar to that of Altitude, although there are differences, which will become evident.

10 The Barton Developers were the developers of the “Governor Place Apartments” (Governor Place), on land in Barton, ACT (Governor Place Property). In June 2010, the Barton Developers were granted a holding lease of the Governor Place Property and commenced development. From about August 2013, the Barton Developers entered into contracts to sell the unexpired term of the then unregistered unit leases for the flats to be developed in Governor Place. Eventually, in May 2015, the Governor Place units plan was registered, and the Barton Developers were entitled to proceed to settle the units in Stage 1 of Governor Place (Governor Place Units). Contracts for sale were entered into between 15 August 2013 and 15 June 2016.

11 Following the retention of Maxim in June 2014, that firm lodged on behalf of the Barton Developers a private ruling request on 11 April 2015 and obtained it on 13 July 2015. As with the Altitude Private Ruling, the private ruling was to the effect that the sales of the Governor Place Units were input taxed and not taxable supplies, subject to Belconnen amending GST returns (Governor Place Private Ruling). Again, GST returns were then amended, partly in July 2015 and finally in November 2015.

12 Although at least two types of contracts were entered into with purchasers of the Governor Place Units, for reasons I will explain, they were both prepared on the basis that the sales of the Governor Place Units would be taxable supplies, and that the sale price was inclusive of GST.

13 As will also become evident, the precise chronology and interrelationship of the events summarised above have significance in both proceedings. Conveniently, the parties in each proceeding have agreed on the details of relevant events. This has allowed me to set out, as an annexure to this judgment (Annexure A), a table which identifies the relevant events and records my findings as to when they occurred. In understanding these reasons, it will be necessary to make reference to Annexure A at various times.

14 The allegation of the applicants in these two separate Part IVA representative proceedings is that both the Belconnen and the Barton Developers implemented essentially similar schemes, both motivated by profit and driven by self-interest. These schemes, it was contended in final submissions, allowed Belconnen and the Barton Developers to retain amounts which purchasers believed would be required to have been paid over by the respondents to the ATO to discharge the GST liability arising upon the taxable supply. Although, as will be explained below, the factual contest is relatively limited, the respondents contend the applicants’ characterisation of their actions is unpleaded, ahistorical and inapt and, more significantly, all the applicants’ claims for relief are misconceived.

15 As would be by now obvious, there are some common factual threads running through the two proceedings and both cases give rise to similar legal issues. Although the initial trials of both proceedings were heard together, there are, however, some differences of real significance, and evidence in one proceeding is not evidence in the other.

16 It is convenient to commence by identifying the two proceedings and the issues that are the subject of this judgment following concurrent hearing of the initial trials.

B PROCEEDINGS AND SCOPE OF THE INITIAL TRIALS

17 The applicant in the proceeding NSD 1417 of 2017 (Altitude proceeding), Mrs Susan Lloyd, and each of the represented persons in the Altitude proceeding (Altitude group members) purchased an Altitude Unit pursuant to an Altitude Contract.

18 Mrs Lloyd brings the Altitude proceeding on her behalf and on behalf of the Altitude group members, to recover the component of the purchase price payable pursuant to the Altitude Contract said to be referable to GST. She pleaded an array of causes of action, including for money had and received, breach of contract, misleading or deceptive conduct and unconscionable conduct (contrary to the provisions of the Australian Consumer Law, as applied by Pt XI of the Competition and Consumer Act 2010 (Cth) (ACL) and the Trade Practices Act 1974 (Cth) (TP Act)).

19 Accessorial claims are also brought against two officers of Belconnen, Mr John Hindmarsh and Mr Gerald Ryan, on the basis that they were knowingly involved in the statutory contraventions.

20 On 30 April 2019, an order was made in the Altitude proceeding that the following matters would be determined at the initial trial, being: the whole of the claim of Mrs Lloyd; and various agreed common issues of law or fact set out in Schedule 1 to those orders. The issues of law and fact identified (cross referenced to the then extant pleadings) were as follows:

Issue | Pleadings |

GST | |

1. Was GST payable by [Belconnen] in respect of the sale of the unexpired term of a Unit Lease for [an Altitude Unit]? | SOC [26]-[29] D [9]-[10] |

Restitution | |

2. Did the price paid by the [Altitude group members] to [Belconnen] under the [Altitude Contracts] include a distinct and severable component which was referable to GST? | SOC [30] S [11] |

3. Is [Belconnen] liable to pay to the [Altitude group members] an amount equivalent to the component of the price paid under the [Altitude Contracts] which was referable to GST (if any)? | SOC [31]-[35] D [12]-[14] |

Breach of contract | |

4. Was there an express or implied term of the [Altitude] Contracts that [Belconnen] warranted that: a. GST was payable in respect of the sale of the unexpired term of a Unit Lease for [an Altitude Unit]; and/or b. GST would be paid to the [ATO]? | SOC [36] D [15] |

5. If so, did [Belconnen] breach such term? | SOC [37] D [16] |

6. Did the [Altitude group members] suffer loss and damage by reason of any breach of the pleaded term? | SOC [38] D [17] |

7. Was there an implied term of the [Altitude] Contracts that if GST was not payable in respect of the sale of the unexpired term of a Unit Lease for [an Altitude] Unit, [Belconnen] would pay to the [Altitude group members] an amount equivalent to the component of the price paid under the [Altitude] Contracts which was referable to GST? | SOC [39] D [18] |

8. If so, did [Belconnen] breach the implied term? | SOC [40] D [19] |

9. Did the [Altitude group members] suffer loss and damage by reason of any breaches of the implied term of the [Altitude] Contracts? | SOC [41] D [17] |

False, misleading or deceptive conduct | |

10. Did the Altitude Contracts proffered by [Belconnen] to the [Altitude group members] represent that: a. GST was payable in respect of the sale of the unexpired term of a Unit Lease for [an Altitude] Unit; and/or b. GST would be paid to the Australian Taxation Office? | SOC [42]-[43] D [21]-[22] |

11. Did [Belconnen’s] conduct as pleaded in paragraphs 42 and 44 of the SOC constitute false, misleading or deceptive conduct in respect of the [Altitude group members] in contravention of ss 52 and/or 53A(b) of the TP Act and/or ss 18(1) and/or 30(1)(c) of the ACL? | SOC [46]-[49] D [24]-[26] |

12. Did the [Altitude group members] suffer no loss and damage because of conduct of [Belconnen] as pleaded in paragraphs 42 and 44 of the SOC in contravention of ss 18(1) and/or 30(1)(c) of the ACL (if any) by reason that: a. the market value of the Unit Lease was the price paid for it by the [Altitude group members]; and/or b. the market value of the Unit Lease was equal to or exceeded the price paid for it by the [Altitude group members]; and/or c. the market value of the Unit Lease is unaffected by whether the sale of the Unit Lease was a taxable supply or input taxed? | SOC [51] D [28], [37] |

Unconscionable conduct | |

13. Did [Belconnen] engage in the following system of conduct or pattern of behavior in respect of the [Altitude group members]: a. As pleaded in paragraphs 16 to 22 of the SOC, offering to enter into, enter into and settle on [Altitude] Contracts containing terms to the effect that the sale of the unexpired term of a Unit Lease for [an Altitude] Unit was a taxable supply and the Price was inclusive of GST; b. From at least November 2012, taking the position that the sale of the unexpired term of a Unit Lease for [an Altitude] Unit was (or was likely to be) input taxed and that GST was not (or was unlikely to be) payable; c. At all material times prior to the settlement of the [Altitude] Contracts, failing to inform the applicants and the [Altitude] group members that GST was not (or was unlikely to be) payable in respect of the sale of the unexpired term of a Unit Lease for [an Altitude] Unit; and d. Retaining for its own benefit an amount equivalent to the component of the Price paid by the [Altitude group members] referable to GST? | SOC [51DA] D [29], [32] |

14. Were the [Altitude group members] in a position of special disadvantage with [Belconnen] by virtue of the factual matters pleaded at paragraph 51A of the SOC and did [Belconnen] take advantage of the [Altitude group members]? | SOC [51A]-[51D] D [30]-[32] |

15. Did [Belconnen’s] conduct as pleaded in paragraph 51A-51E of the SOC constitute unconscionable conduct in respect of the [Altitude group members] in contravention of ss 51AA and/or 51AB of the TP Act and/or ss 20-21 of the ACL? | SOC [51F] D [32] |

16. Did the [Altitude group members] suffer no loss and damage because of alleged unconscionable conduct of [Belconnen] in contravention of ss 20 and 21 of the ACL (if any) by reason that: a. the market value of the Unit Lease was the price paid for it; and/or b. the market value of the Unit Lease was equal to or exceeded the price paid for it; and/or c. the market value of the Unit Lease is unaffected by whether the sale of the Unit Lease was a taxable supply or input taxed? | SOC [51G] D [32], [37] |

Knowing involvement | |

17. Were [Mr Hindmarsh or Mr Ryan] knowingly involved, as pleaded in paragraphs 52 and 53 of the SOC, in contraventions of [Belconnen] for the purposes of s 75B of the TP Act and/or s 2 of the ACL? | SOC [52]-[53] D [33]-[34] |

B.2 The Governor Place Proceeding

21 The first and second applicants in proceeding NSD 1555 of 2018 (Governor Place proceeding), Mr Hassan El-Zein and Mrs Deborah El-Zein, and the third and fourth applicants, Mr Glenn Eppelstun and Mrs Atsuko Eppelstun and each of the represented persons in the Governor Place proceeding (Governor Place group members) purchased a Governor Place Unit pursuant to a contract. As will be explained further below, there were different contracts entered into (Governor Place Contracts): Mr and Mrs El-Zein and the Taxable Supply Group Members (from about 15 August 2013 to about 23 June 2015) entered into the Taxable Supply Contracts; while it appears other group members (from about 30 July 2015) entered into the Margin Scheme Contracts. Mr and Mrs Eppelstun themselves entered into a form of Margin Scheme Contract which had peculiarities (Eppelstun Contract), which I will examine below. Importantly, no other claim of a group member who executed a Margin Scheme Contract was brought forward for determination. Although some comments were made from the bar table as to group members signing a different form of Margin Scheme Contract from Mr and Mrs Eppelstun, I do not have a secure foundation to ascertain the precise form or prevalence of Margin Scheme Contracts that differ from the express terms of the Eppelstun Contract.

22 Mr and Mrs El-Zein and Mr and Mrs Eppelstun seek to recover the component of the purchase price payable said to be referable to GST. The applicants in the Governor Place proceeding plead a similar miscellany of causes of action as those in the Altitude proceeding. On 30 April 2019, a consent order was made in the Governor Place proceeding that at the initial trial the whole of the claims of Mr and Mrs El-Zein and Mr and Mrs Eppelstun would be determined, together with issues of law and fact, which were identified as follows:

Issue | Pleadings |

GST | |

1. Was GST payable by the [Barton] Developers in respect of the sale of the unexpired term of a Unit Lease for a [Governor Place] Unit? | SOC [30]-[34] D [30]-[34] |

Restitution | |

2. Did the price paid by the [Governor Place group members] to the [Barton] Developers under the [Governor Place] Contracts include a distinct and severable component which was referable to GST? | SOC [37] D [37] |

3. Are the [Barton] Developers liable to pay to the [Governor Place group members] an amount equivalent to the component of the price paid under the [Governor Place] Contracts which was referable to GST (if any)? | SOC [38]-[42] D [39]-[42] |

Breach of contract | |

4. Was there an express or implied term of the [Governor Place] Contracts that the [Barton] Developers warranted that: a. GST was payable in respect of the sale of the unexpired term of a Unit Lease for a [Governor Place] Unit; and/or b. GST would be paid to the Australian Taxation Office? | SOC [51] D [51] |

5. Was there: a. in the [Taxable Supply Contracts], an express term that if the sale of the unexpired term of a Unit Lease for a [Governor Place] Unit was not in fact a taxable supply the Barton Developers would pay to the [Governor Place group members] an amount equal to one-eleventh of the Price; or b. in the [Governor Place] Contracts, an implied term that if the sale of the unexpired term of a Unit Lease for a [Governor Place Unit] was not in fact a taxable supply the [Barton] Developers would pay to the [Governor Place group members] an amount equivalent to the component of the Price referable to GST? | SOC [43], [47] D [43], [47] |

6. Did the [Barton] Developers breach the express or implied terms of the [Governor Place] Contracts referred to in Questions 4 or 5 above? | SOC [44]-[45], [48]-[49], [52] D [44]-[45], [48]-[49], [52] |

7. Did the [Governor Place group members] suffer loss and damage by reason of any breaches of the express or implied terms of the [Governor Place] Contracts? | SOC [46], [50], [53] D [46], [50], [53] |

8. Were the rights of the [Governor Place group members] to sue on the terms of the [Governor Place] Contracts extinguished by merger? | D [45], [49], [52] |

9. Should relief be withheld from the [Governor Place group members] on the grounds that the terms of the [Governor Place] Contracts referred to in Question 5 above were a penalty? | D [45], [49] |

10. In the [Margin Scheme Contracts], should relief be withheld from the [Governor Place group members] on the grounds of mistake? | D [49] |

False, misleading or deceptive conduct | |

11. Did the [Governor Place] Contracts proffered by the [Barton] Developers to the [Governor Place group members] represent that: a. GST was payable in respect of the sale of the unexpired term of a Unit Lease for a [Governor Place] Unit; and/or b. GST would be paid to the [ATO]? | SOC [54]-[55] D [54]-[55] |

12. If the answer to Question 11 is yes, did the [Barton] Developers have reasonable grounds for making the representations? | SOC [58] D [58] |

13. Did the Barton Developers’ conduct as pleaded constitute false, misleading or deceptive conduct in respect of the [Governor Place group members] in contravention of ss 18 and/or 30(1)(c) of the ACL? | SOC [58]-[61] D [58]-[61] |

14. Did the [Governor Place group members] suffer no loss and damage because of conduct of the [Barton] Developers in contravention of ss 18 and/or 30(1)(c) of the ACL (if any) by reason that: a. the value of the Unit Lease equals or exceeds the amount paid for it; and/or b. the value of the Unit Lease is unaffected by whether the sale of the Unit Lease was a taxable supply or input taxed? | SOC [63] D [63] |

Unconscionable conduct | |

15. Did the [Barton] Developers: a. Offer to enter into, enter into and settle on [Governor Place] Contracts containing terms to the effect that the sale of the unexpired term of a Unit Lease for a [Governor Place] Unit was a taxable supply and the Price was inclusive of GST; b. Take the position that the sale of the unexpired term of a Unit Lease for a [Governor Place] Unit was (or was likely to be) input taxed and that GST was not (or was unlikely to be) payable; c. Fail to inform the Applicants and the [Governor Place group members] that GST was not (or was unlikely to be) payable in respect of the sale of the unexpired term of a Unit Lease for a [Governor Place] Unit; and d. Retain an amount equivalent to the component of the Price referable to GST. | SOC [63A]-[63C], [63F]-[63G] D [63A]-[63C], [63F]-[63G] |

16. Were the [Governor Place group members] in a position of special disadvantage and did the [Barton] Developers take advantage of the Purchasers? | SOC [63D]-[63F] D [63D]-[63F] |

17. Did the [Barton] Developers’ conduct as pleaded constitute unconscionable conduct in respect of the [Governor Place group members] in contravention of ss 20-21 of the ACL? | SOC [63I] D [32] |

18. Did the [Governor Place group members] suffer no loss and damage because of conduct of the [Barton] Developers in contravention of ss 20-21 of the ACL (if any) by reason of either of the matters referred to in Question 14 above? | SOC [63J] D [63J] |

23 After the evidence and prior to submissions, all claims for breach of contract in both proceedings were abandoned (save for a claim for damages for breach of cl 24.6 made by Mr and Mrs El-Zein on behalf of themselves and the Taxable Supply Group Members). Additionally, it became apparent that a number of the questions identified in the consent orders are not truly common and there are difficulties in the wording of some of the common questions. I mention this because although I will identify my conclusions as to the cases of the applicants, there will be a need for caution and close attention in preparing appropriate orders pursuant to s 33ZB of the Federal Court of Australia Act 1976 (Cth) (FC Act) reflecting those conclusions (and which serve to identify the precise metes and bounds of the “statutory estoppel” binding group members who have not opted out). These orders will also need to take into account any substantive difference between the Eppelstun Contract, and any other types of Margin Scheme Contracts, which were not only not the subject of claims advanced at the initial trial, but were not in evidence before me.

B.3 The Centrality of the Contracts to the Resolution of all Issues

24 Reference has already been made to the fact that the applicants in both proceedings advanced various causes of action, including for breach of contract. Notwithstanding that claims in contract have been largely abandoned, this does not diminish the importance of the proper construction of the Altitude Contracts, the Taxable Supply Contracts and the Eppelstun Contract (collectively, Contracts) as being the logical starting point of any analysis of the legal issues.

25 The reasons why this is so, are important.

26 First, although the main thrust of the case advanced in final submissions was one based on application of restitutionary principles, restitution cannot impose a liability that would subvert or undermine an existing allocation of risk established by contract. Reference has often been made to the “gap-filling role” of restitution. As the authors (Professor J W Carter, K Mason QC and G J Tolhurst) of Restitution Law in Australia (LexisNexis, 3rd ed, 2016) explain at 95 [215], it is fundamental that as a general rule “restitutionary issues arise in respect of ineffective rather than effective contracts”. It will be necessary to deal with the role of restitutionary remedies in far more detail below, but by way of introduction, very recently, in Mann v Paterson Constructions Pty Ltd [2019] HCA 32; (2019) 373 ALR 1, Kiefel CJ, Bell and Keane JJ (although in the minority in the result), conveniently collected statements from a number of authorities under the heading “Contract and the subsidiarity of restitutionary claims” (at 7-8 [14]–[18]):

Restitutionary claims must respect contractual regimes and the allocations of risk made under those regimes. In Pavey & Matthews Pty Ltd v Paul, in a passage cited with approval by French CJ, Crennan and Kiefel JJ in Equuscorp Pty Ltd v Haxton, Deane J said:

“The quasi-contractual obligation to pay fair and just compensation for a benefit which has been accepted will only arise in a case where there is no applicable genuine agreement or where such an agreement is frustrated, avoided or unenforceable. In such a case, it is the very fact that there is no genuine agreement or that the genuine agreement is frustrated, avoided or unenforceable that provides the occasion for (and part of the circumstances giving rise to) the imposition by the law of the obligation to make restitution.”

In Pan Ocean Shipping Co Ltd v Creditcorp Ltd (“The Trident Beauty”), Lord Goff of Chieveley spoke to similar effect:

“[A]s a general rule, the law of restitution has no part to play in the matter; the existence of the agreed regime renders the imposition by the law of a remedy in restitution both unnecessary and inappropriate.”

In Lumbers v W Cook Builders Pty Ltd (In liq), Gleeson CJ noted that the contractual arrangements in that case “effected a certain allocation of risk” and that there was “no occasion to disturb or interfere with that allocation” and “every reason to respect it”. Gummow, Hayne, Crennan and Kiefel JJ spoke of taking “proper account” of the contractual rights and obligations that existed…

Their Honours noted that it is essential to consider how the claim fits with contracts the parties have made because, as Lord Goff “rightly warned” in The Trident Beauty, “serious difficulties arise if the law seeks to expand the law of restitution to redistribute risks for which provision has been made under an applicable contract”.

In MacDonald Dickens & Macklin (a firm) v Costello in the Court of Appeal of England and Wales, Etherton LJ, with whom Pill and Patten LJJ agreed, in rejecting a restitutionary claim, said:

“The general rule should be to uphold contractual arrangements by which parties have defined and allocated and, to that extent, restricted their mutual obligations, and, in so doing, have similarly allocated and circumscribed the consequences of non-performance. That general rule reflects a sound legal policy which acknowledges the parties’ autonomy to configure the legal relations between them and provides certainty, and so limits disputes and litigation.”

(endnotes and internal citations omitted)

27 It follows that in the individual Contracts with which we are presently concerned, the starting point is to ascertain whether a relevant agreed regime is absent (as the applicants contend) or whether (as the respondents would have it) there is no sphere of operation of restitutionary principles because the bargains reflected in the Contracts provided for an effective “contractual allocation of risk”: Coshott v Lenin [2007] NSWCA 153 per Mason P at [10]; see also Nikolic v Oladaily Pty Ltd [2007] NSWCA 252 per Mason P at [101] (Campbell JA and Handley AJA agreeing).

28 Secondly, the assessment as to whether conduct is misleading and deceptive is a question of fact to be determined in the context of the evidence as to the alleged conduct and all relevant surrounding facts and circumstances: Taco Company of Australia Inc v Taco Bell Pty Ltd (1982) 42 ALR 177 at 199 per Deane and Fitzgerald JJ. A fundamental requirement is that, in the circumstances, the impugned conduct induces or is capable of inducing error: Parkdale Custom Built Furniture Proprietary Limited v Puxu Proprietary Limited (1982) 149 CLR 191 at 198 per Gibbs CJ. It necessarily follows that context, including the contractual context, is critical – a fortiori, in a case where impugned representations are said, at least in part, to have been conveyed by the express terms of a contract.

29 Thirdly, the primary pleaded norm prohibiting unconscionable conduct (s 21 of the ACL) is directed to prohibiting conduct that is, “in all the circumstances”, unconscionable, including, of course, the circumstances of the paction between the parties.

30 Accordingly, it is necessary to turn initially to the terms and proper construction of the Contracts, being the contract representative of the Altitude Contracts (Lloyd Contract), the contract representative of the Taxable Supply Contracts (El-Zein Contract) and the bespoke Margin Scheme Contract before tghe Court (Eppelstun Contract).

C AN ANALYSIS OF THE CONTRACTS

C.1 Relevant Principles, the Printed Terms and GST

31 Unsurprisingly, the relevant principles were not in contest and do not require excursus in this judgment other than to note that the rights and liabilities of parties under a contract are determined objectively, by reference to its text (being the entire text of the contract as well as any document or statutory provision referred to in the text), context and purpose: Mount Bruce Mining Pty Limited v Wright Prospecting Pty Limited [2015] HCA 37; (2015) 256 CLR 104 at 116 [46].

32 As is routine with contracts for the sale of land, each of the Contracts were adapted from a standard form; in these cases, the Law Society of the Australian Capital Territory (ACT) Contract for Sale forms. The Altitude Contracts were adapted from the 2013 Edition, while the Governor Place contracts were adapted from the 2008 Edition. Given that there were no material differences in the provisions between these two editions for the purpose of these proceedings, I will refer to the printed terms compendiously (Printed Terms). The Printed Terms provided for a two page schedule of details to be populated (Schedule) and provided, by way of identification in the Schedule, for various documents to be attached which were to form part of the Contracts and were augmented by special conditions drafted by the solicitors for the vendor, or to use the contractual term, the “Seller” (Special Conditions). The first of the substantive terms provided for by the Printed Terms provided that “[t]he Seller agrees to sell and the Buyer agrees to buy the Property for the Price on these terms”.

33 The Schedule, as one would expect, set out, on page one, the conventional particulars of the conveyance identifying a number of what became defined terms including the: Land, Seller, Seller Solicitor, Stakeholder, Seller Agent, Goods (that is, inclusions), Date for Completion, Buyer, Buyer Solicitor and Date of this Contract. Importantly, as noted above, the defined term “Price” was specified, as being a total amount, followed by the words:

(GST inclusive unless otherwise specified).

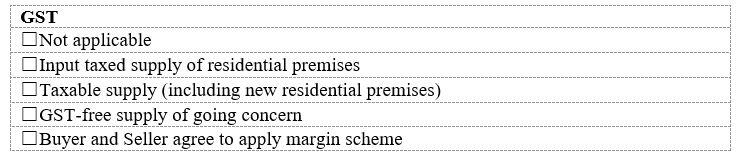

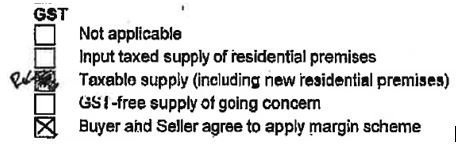

34 After referring to any details of co-ownership, page one also provided space for execution. The following page, again conventionally, identified documents included in, and forming part of the Contracts, and then identified further particulars, including the following boxes relating to GST:

35 I will return to the significance of these boxes relating to GST contained in the Schedule (GST Schedule) below.

36 It is common ground that the Printed Terms are drafted so as to be applicable to all conveyances of land in the ACT, which, like elsewhere in Australia, is a type of property transfer closely regulated by statute. Accordingly, the Printed Terms may or may not be applicable depending upon the peculiar circumstances of the conveyance. Similarly, the Schedule includes space for including individual details which may or may not be relevant depending upon the circumstances.

37 One of those individual circumstances is, of course, the nature of the supply. A sale of real property can be taxable, input taxed or GST free. Only taxable supplies, of course, are subject to GST (as a supply is not a taxable supply to the extent that it is GST free or input taxed: see s 9-5 of the GST Act). A consequence of the supply being input taxed, is that there is no entitlement to any input tax credits in relation to anything acquired to make the supply.

38 Notwithstanding that “supply” is defined very broadly in s 9-10(1), and includes “a grant, assignment or surrender of real property”, s 9-10(2)(d) makes it clear that there is no “supply” within the meaning of the GST Act upon exchange of contracts for the sale of land. It is therefore conceivable that after exchange, and prior to settlement (which in the case of “off the plan” sales could be a very considerable period), the characterisation of the anticipated supply could change from a taxable supply to a supply which is not taxable or vice versa.

39 It necessarily follows that the Printed Terms must accommodate four matters relevant to GST. The first has already been remarked upon: the Printed Terms must express the fact that on the information then available, the sale will, upon settlement, be a supply that is taxable, input taxed or GST free.

40 The second matter the Printed Terms accommodate relevant to GST, is that this classification of the supply may change between the time of exchange and later settlement.

41 The third matter the Printed Terms accommodate relevant to GST, is the possible operation of the “margin scheme” which, by definition, can only apply when the supply is a taxable supply. It is necessary to pause to explain this briefly. Ordinarily, of course, the amount of GST payable on a taxable supply is 10% of the value of the taxable supply (GST Act s 9-70), but the GST Act contains a margin scheme provision which, when it applies to a taxable supply, means the amount of GST payable is one-eleventh of the “margin”, that is, speaking generally, the difference between the price for which the supplier supplied the property, and the price for which it was initially purchased by that supplier (GST Act s 75-10). The reason for this is obvious: it was designed to correct what would otherwise be an anomaly arising where GST is attracted on the supply of land, but no input tax credit is available: see Brady King Pty Ltd v Commissioner of Taxation [2008] FCAFC 118; (2008) 168 FCR 558 at 560 [8]. What is of further significance is that the margin scheme may apply to the sale of the type of property with which we are concerned, but it will only do so if both the supplier and the recipient of the supply have agreed in writing that the margin scheme is to apply: GST Act s 75-5(1). To anticipate matters, it is worth noting that prior to the Altitude Private Ruling, Belconnen were treating the sale of an Altitude Unit as a taxable supply and intended to apply the margin scheme (because no input tax credit was available to Belconnen); whereas despite indications in some Governor Place Contracts to the contrary, the Barton Developers could not make use of the margin scheme (because the relevant land was initially acquired as a taxable supply and an input tax credit was available).

42 The fourth matter the Printed Terms accommodate relevant to GST, is how the standard form regulates the rights of the Seller and Buyer substantively depending upon whether the sale of the property was taxable (and whether or not the Buyer and Seller agreed to apply the margin scheme), or was input taxed, or was GST free. Depending upon the relevant box ticked in the GST Schedule (see [34] above), the Printed Terms had a section (cl 24 headed “GST”) which had subclauses that would operate in different ways depending upon the nature of the supply ascertained upon settlement. Clause 24 is as follows:

24 GST

24.1 If a party must pay the Price or provide any other consideration to another party under this Contract, GST is not to be added to the Price or amount, unless this Contract provides otherwise.

24.2 If the Price is stated in the Schedule to exclude GST and the sale of the Property is a taxable supply, the Buyer must pay to the Seller on Completion an amount equal to the GST payable by the Seller in relation to the supply.

24.3 If under this Contract a party (Relevant Party) must make an adjustment, pay an amount to another party (excluding the Price but including the Deposit if it is released or forfeited to the Seller) or pay an amount payable by or to a third party:

24.3.1 the Relevant Party must adjust or pay at that time any GST added to or included in the amount; but

24.3.2 if this Contract says this sale is a taxable supply, and payment would entitle the Relevant Party to claim an input tax credit, the adjustment or payment is to be worked out by deducting any input tax credit to which the party receiving the adjustment or payment is or was entitled multiplied by the GST Rate.

24.4 If this Contract says this sale is the supply of a going concern:

24.4.1 the parties agree the supply of the Property is the supply of a going concern;

24.4.2 the Seller must on Completion supply to the Buyer all of the things that are necessary for the continued operation of the enterprise;

24.4.3 the Seller must carry on the enterprise until Completion;

24.4.4 The Buyer warrants to the Seller that on Completion the Buyer will be registered or required to be registered;

24.4.5 If for any reason (and despite cl. 24.1 and 24.4.1) the sale of the Property is not the supply of a going concern but is a taxable supply:

(a) the Buyer must pay to the Seller on demand the amount of any GST payable by the Seller in respect of the sale of the Property; and

(b) the Buyer indemnifies the Seller against any loss or expense incurred by the Seller in respect of that GST and any breach of cl 24.4.5(a).

24.5 If this Contract says that the Buyer and Seller agree that the margin scheme applies to the supply of the Property, the Seller warrants that it can use the margin scheme and promises that it will.

24.6 If this Contract says the sale is a taxable supply, does not say the margin scheme applies to the sale of the Property, and the sale is in fact not a taxable supply, then the Seller must pay the Buyer on Completion an amount of one-eleventh of the Price.

24.7 On Completion the Seller must give the Buyer a tax invoice for any taxable supply by the Seller by or under this Contract.

43 In addition to the GST Schedule and the reference to the Price being GST inclusive, the terms of cl 24 reflect the bargain relating to the imposition of GST. For this reason, it is worth examining how the various aspects of the clause operate in the different circumstances contemplated by the standard contract:

(1) Clause 24.1: Consistently with the Schedule, this subclause confirms that the Price is, in the case of taxable supplies, GST inclusive.

(2) Clause 24.2: Although not presently relevant to the Contracts because they are all GST inclusive, this “GST gross up” provision provides, where the Price in the Schedule excludes GST, for an increase in the consideration for GST in the event the sale on completion is a taxable supply. It operates together with cl 24.7, which provides for the provision by the Seller to the Buyer of a tax invoice on settlement.

(3) Clause 24.3: Again not directly relevant here, this subclause is aimed at circumstances where: (a) an adjustment is made on settlement; or (b) a payment is made as reimbursement for an agreed cost; or (c) a purchaser forfeits the deposit, thus triggering GST for the Seller on the amount of the deposit amount. The subclause operates to provide that the party making the adjustment or payment must include any applicable GST (cl 24.3.1), except to the extent an input tax credit is available (cl 24.3.2).

(4) Clause 24.4: This “going concern” provision applies where the Property is sold as part of an operating enterprise, for example, where the realty forms part of a business sale or involves the sale of leased commercial premises. The going concern requirements are set out in s 38-325 of the GST Act and (mercifully) are unnecessary to recount here. It is only noteworthy because, as explained above, it contemplates a change in the position between exchange and settlement. If it is determined that the sale was not GST-free as a going concern, the Buyer must pay the Seller an additional amount for GST (notwithstanding the Price may have been expressed to be GST inclusive (cl 24.1) and the sale was agreed to be GST-free as a going concern (cl 24.4.1)).

(5) Clause 24.5: This clause is of importance. If there is agreement (by crossing the box in the GST Schedule or otherwise in the contract) that the margin scheme applies to the future supply, the “Seller warrants that it can use the margin scheme and promises that it will”. This warranty safeguards the position of the Buyer if the position changes between the time of exchange and settlement. Sometimes a breach of this warranty could result in nominal damages, and sometimes in compensatory damages. For example, a developer Buyer may want to acquire a residential development site from another developer Seller under the margin scheme, so that it is eligible to apply the margin scheme on its own future taxable supplies of “new residential premises”. As explained above, the developer Buyer will not be entitled to any input tax credits for GST paid on the purchase under the margin scheme (s 75-20), but the developer Buyer will suffer a loss if the margin scheme is not applied as promised by the Seller (being the increased GST on the future sales). However, for ordinary residential Buyers, there is no similar loss because they are not entitled to an input tax credit for their purchase nor liable for GST on any future sale, thus only nominal damages would be payable upon any breach of warranty by the Seller.

(6) Clause 24.6: This only applies where the taxable supply box is crossed (or the Contract otherwise provides that the sale is a taxable supply) but the margin scheme does not apply and yet the sale, as it turns out, is not a taxable supply. Obviously enough, if the Seller is making a taxable supply of a commercial premises, and the Price is GST inclusive, the Buyer may be entitled to an input tax credit if the purchase is a “creditable acquisition” (s 11-5). This would usually be the case for a sale of commercial property as one would expect the Buyer to be GST registered and the acquisition to be for a creditable purpose. If the sale changed from being a taxable supply prior to settlement, the Buyer would not be entitled to an input tax credit (such as where the Seller ceases to carry on any enterprise and cancels its GST registration prior to settlement). Subclause 24.6 would then operate to provide the Seller an abatement on settlement of one-eleventh of the GST inclusive price to reflect the inability of the Buyer to claim an input tax credit. Importantly, this is an abatement operating as an adjustment on completion, and does not operate so as to provide for an adjustment of the Price for the conveyance. Obviously enough, the same issues requiring an abatement do not arise for domestic residential Buyers because they do not make a “creditable acquisition” and, even leaving aside registration, they cannot claim any credits. Clause 24.6 does not apply to contracts which apply the margin scheme because, as noted above, cl 24.5 provides that the Seller warrants that it can use the margin scheme and promises that it will.

(7) Clause 24.7: This requires the Seller to give a tax invoice for any taxable supply to the Buyer on settlement. Section 29-70(1)(c)(vi) of the GST Act requires such an invoice to identify the amount of GST payable in relation to the taxable supply. The GST Act provides that there is no obligation on a supplier to provide a tax invoice except where the supply is a taxable supply (s 75-30); and the purchaser has requested that the supplier provide a tax invoice (s 29-70(2)). Subclause 24.7 constituted such a request.

44 In the context of evaluating the applicants’ arguments, I will examine below the relationship between the crosses made in the boxes in the GST Schedule and cl 24. But having identified and explained the Printed Terms common to all the Contracts, it is now appropriate to go to the circumstances and Standard Conditions of each of the three types of Contracts that, in each case, incorporated these Printed Terms.

C.2 The Terms of the Lloyd Contract

45 Each of the Altitude Contracts, including the Lloyd Contract, provided that the Price was “GST inclusive”. In the case of Mrs Lloyd, the Price was “$554,900.00 (GST inclusive unless otherwise specified)”.

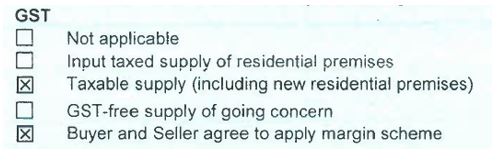

46 In the GST Schedule (see [34] above), the following appeared:

47 In addition to cl 24 of the Printed Terms, three Special Conditions in the Lloyd Contract (and the other Altitude Contracts) have relevance. They are as follows:

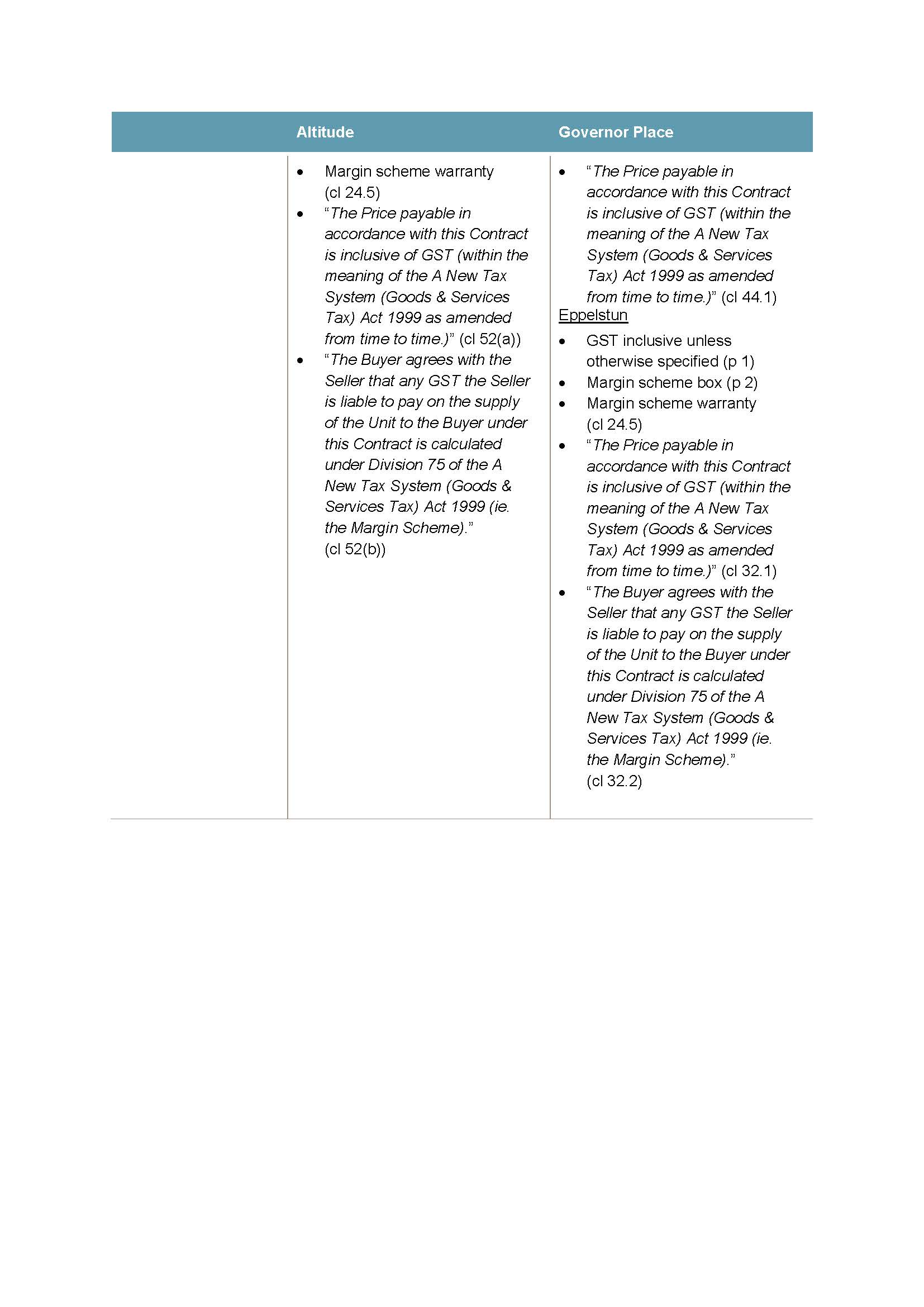

(1) Clause 52 of the Special Conditions:

52. Price inclusive of GST

(a) The Price payable in accordance with this Contract is inclusive of GST (within the meaning of the A New Tax System (Goods & Services Tax) Act 1999 (sic) as amended from time to time.)

(b) The Buyer agrees with the Seller that any GST the Seller is liable to pay on the supply of the Unit to the Buyer under this Contract is calculated under Division 75 of the A New Tax System (Goods & Services Tax) Act 1999 (sic) (ie. the Margin Scheme).

(2) Clause 56 of the Special Conditions:

56. Representations

56.1 Entire agreement

The Buyer agrees that this Contract sets out the entire agreement of the parties on the subject matter of this Contract and supersedes any prior agreement, advice, material supplied to the Buyer or understanding on anything connected with the subject matter of this Contract.

56.2 No reliance

Each party has entered into this Contract without reliance upon any representation, statement or warranty (including sales and marketing material and preliminary art work), except as set out in this Contract.

(3) Clause 60 of the Special Conditions:

60. Definitions

60.1 Definitions

In these Special Conditions the following words have the following meanings:

“Contract” means this contract for sale including the Printed Terms and these Special Conditions and any annexure or schedules to it.

…

“Printed Terms” means the printed terms of the standard ACT Law Society Contract 2013 Edition.

60.2 Same meanings

For the avoidance of any doubt, unless otherwise stated, the terms that are defined in the Printed Terms of the Contract have the same meanings in these Special Conditions.

48 At present I need only comment upon cl 52 which serves to reinforce the fact that the Lloyd Contract was GST inclusive and that the Special Conditions in the Lloyd Contract (which had paramountcy) did not provide “to the contrary” of the Printed Terms. Additionally, cl 52(b) contemplated that Belconnen may not be liable for GST on the supply (“any GST the Seller is liable to pay on the supply …”) and that only Belconnen could have a liability for GST, if applicable on settlement, as Belconnen, as Seller, was the entity making the supply.

C.3 The Terms of the El-Zein Contract

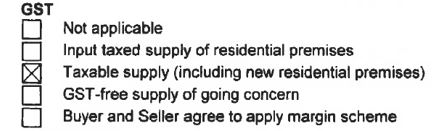

49 The El-Zein Contract also provided that the Price was “GST inclusive” and the Price for the relevant Governor Place Unit was “$435,900.00 (GST inclusive unless otherwise specified)”.

50 In the GST Schedule (see [34] above), the following appeared:

51 In addition to cl 24 of the Printed Terms, there were Special Conditions in the El-Zein Contract, in substantively the same terms as the Lloyd Contract, as to confirmation that the Price was inclusive of GST (cl 44.1) and as to an “entire agreement” and “representations” (cl 47). Apart from the fact that the margin scheme did not apply, the contractual position as between the Barton Developers and Mr and Mrs El-Zein was similar to that applying as between Belconnen and Mrs Lloyd.

C.4 The Terms of the Eppelstun Contract

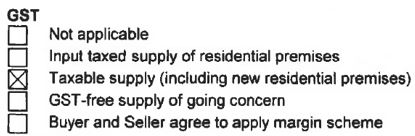

52 The position as to the Eppelstun Contract was somewhat different and the source of some contention (although the Special Conditions identified above as to the Price being GST inclusive (cl 32.1) and as to an “entire agreement” and “representations” (cl 35) were also present).

53 Mr and Mrs Eppelstun agreed to purchase their relevant Governor Place Unit for a Price specified as being “$400,900.00 (GST inclusive unless otherwise specified)”. As is common with conveyancing contracts, the Eppelstun Contract was executed in counterpart. The counterpart signed by Mr and Mrs Eppelstun and provided by their solicitors on exchange to the Barton Developers (Buyer Counterpart) was, like the El-Zein Contract, as follows:

54 However, the counterpart signed on behalf of the Barton Developers and provided on exchange to the solicitors for Mr and Mrs Eppelstun (Seller Counterpart) was different and as follows:

55 The evidence does not allow a definitive conclusion to be reached as to who crossed, rubbed out and then initialled next to the “Taxable supply (including new residential premises)” box on the Seller Counterpart. The Barton Developers did not call their solicitor, Mr Archie Tsirimokos, of Meyer Vandenberg, who executed the Seller Counterpart. It is possible to conclude, however, that the changes were placed on the Seller Counterpart prior to exchange and were on the Seller Counterpart when it was received by the solicitors for Mr and Mrs Eppelstun. In any event, the disconformity, such as it was, was either overlooked by the solicitors or regarded as being sufficiently insignificant not to stand in the way of exchange having been effected and the ultimate settlement of the conveyance.

56 It is necessary to resolve the competing contentions of the parties as to the contractual significance of the difference between the counterparts. The Barton Developers assert that the margin scheme box was “ticked by mistake” on the Seller Counterpart. The evidence discloses that in July 2013 a conveyancer at Meyer Vandenberg enquired as to whether the margin scheme applied to the sale of the Governor Place Units and was then informed by a development manager at Morris Property Group that the “[m]argin scheme is not able to be applied”. Later in July 2013, Meyer Vandenberg prepared a revised version of the master contract with the relevant margin scheme special condition (cl 45.2) deleted. A marked up draft of the Special Conditions to the master contract included a comment that “[a]s this land was sold to us as a taxable supply, we cannot nominate the margin scheme” and an instruction was given to Meyer Vandenberg to “ensure the front page reflects same”.

57 After registration of the Governor Place units plan, Meyer Vandenberg was asked to update the contracts and it is evident that this revision of the Special Conditions reintroduced the margin scheme in a special condition (cl 32.2). Clause 32 is of importance (and is essentially the same as cl 52 of the Altitude Contracts) and merits setting out in full:

32. PRICE INCLUSIVE OF GST

32.1 Price Inclusive

The Price payable in accordance with this Contract is inclusive of GST (within the meaning of the A New Tax System (Goods & Services Tax) Act 1999 (Cth) (sic) as amended from time to time.)

32.2 Margin Scheme

The Buyer and the Seller agree that any GST that the Seller is liable to pay on the supply of the Unit to the Buyer under this Contract is to be calculated under Division 75 of the A New Tax System (Goods & Services Tax) Act 1999 (Cth) (sic) ie. the Margin Scheme.

58 In any event, as noted above, at some time around when the Seller Counterpart was executed by Mr Tsirimokos on or about 6 October 2015 under the power of attorney, the margin scheme box was ticked and both the Seller Counterpart and the Buyer Counterpart included the margin scheme Special Condition cl 32.2 set out above.

59 Senior Counsel for the Barton Developers submitted that “if one put it in terms of offer and acceptance” there was “no meeting of minds about the relevant topic of engagement”; this is because “it’s not just the tick… It’s the tick plus the promises attached to the tick which is the offer. The ticks are there to engage [cl] 24” (T.85 24.6.19). In effect, it was contended, “[a]ll that has happened is there is no relevant ticking at all under GST. None” (T.86 24.6.19).

60 Mr and Mrs Eppelstun submit that the submission of the Barton Developers is both incomplete and misconceived. Whatever the position as to the ticking of the box in the GST Schedule and the inclusion of special condition cl 32.2, the evidence relied on by the Barton Developers is said to fall short of establishing any mistake because, apart from anything else, it is left unsatisfactorily unclear why the person who made the amendments did what they did.

61 Ultimately, however, the issue comes down to one of construction. Contractual construction, of course, depends on finding the meaning of the language of the Eppelstun Contract. I think notions of offer and acceptance in the present context can be a distraction. The Eppelstun Contract was, of course, comprised by two counterparts and although it may sometimes be possible to regard the party who signs first as being the offeror, where a contract for the sale of land is formed by an exchange of counterparts, to attempt to analyse the formation of agreement in terms of a succession of offer and acceptance is somewhat artificial: see Nunin Holdings Pty Ltd v Tullamarine Estates Pty Ltd [1994] 1 VR 74 at 81 (Hedigan J). Nor is the issue one that involves consideration of rectification, as Mr and Mrs Eppelstun say the proper construction is clear and rectification is unnecessary; and the Barton Developers say there was no common intention as to the nature of the proposed supply and hence the instruments cannot be rectified to bring them into conformity with the common intention of the parties: see Sindel v Georgiou (1984) 154 CLR 661 at 667.

62 Hence the issue is simply whether, as a matter of interpretation, the Eppelstun Contract records a consensus on the relevant terms. This involves reading the Eppelstun Contract as a whole giving weight to all clauses in an endeavour to give effect to the intention of the parties as reflected in the language which they have used. In doing so, of course, the court will try to ensure the congruent operation of its various components as a whole (Wilkie v Gordian Runoff Limited [2005] HCA 17; (2005) 221 CLR 522 at 529 [16]) and a court is entitled to approach the task on the assumption “that the parties ... intended to produce a commercial result” and to avoid the Eppelstun Contract “making commercial nonsense or working commercial inconvenience”: Mount Bruce at 117 [51] (French CJ, Nettle and Gordon JJ).

63 If one is to approach the examination of the text in the context of the surrounding circumstances known to both the parties, including the purpose and object of the transaction and by assessing how a reasonable person would have understood the language in that context, then the objectively ascertained answer to what the parties intended relating to GST emerges.

64 Clause 32.2 provided, in terms, that Mr and Mrs Eppelstun agreed with the Barton Developers that “any GST” would be calculated under the margin scheme. This provision can be read together with the Buyer Counterpart (which simply noted that the supply was taxable). In truth there is no real inconsistency between them, this is because one supplements the other and in accordance with s 75-5(1) of the GST Act, an agreement between the parties to apply the margin scheme to the taxable supply (see [41] above) is found upon consideration of the instruments as a whole. Moreover, cl 32.2 is consistent with all other terms of the Seller Counterpart (which noted the agreement that the margin scheme was to apply, and hence the supply was necessarily taxable). Moreover, the mere fact that the agreement to apply the margin scheme might be found in the Special Conditions where the relevant box is not ticked in the GST Schedule, does not undermine the operation of cl 24.5 of the Printed Terms, which contemplates the agreement to apply the margin scheme being found anywhere in “this Contract”.

65 When read as a whole, including by reference to how a reasonable person would have understood the language in context, it seems to me that in addition to Mr and Mrs Eppelstun agreeing with the Barton Developers on exchange that the Price was GST inclusive, the Eppelstun Contract says that Mr and Mrs Eppelstun and the Barton Developers agreed that the margin scheme applies to the supply and hence the Barton Developers warranted by cl 24.5 (incorrectly as it turns out) that it could use the margin scheme and promised that it would.

66 For the sake of completeness, I note I do consider the answer to this construction issue is found by reference to the “override” clause (cl 38) (which conventionally, like many conveyancing contracts, gives paramountcy to the Special Conditions over the Printed Terms). This is for two reasons: first, properly understood, there is not, in truth, an inconsistency between the Special Conditions and the Schedule if the contract is read as a whole; and secondly, in any event, the better view is that the particulars and markings in the Schedule do not form part of the Printed Terms as that term is defined (see cl 27.1(c) of the Special Conditions).

67 It may be accepted that given the history of the Governor Place development recounted at [10]-[11] above, the Barton Developers did not intend to apply the margin scheme (a matter unknown to Mr and Mr Eppelstun), but the subjective intentions of the Barton Developers are, of course, not to the point. Of course, the actual state of one party’s mind is generally irrelevant for the purposes of construction including in circumstances where the other contracting party does not know the other is labouring under a “mistake”: see J D Heydon QC, Heydon on Contract (2019, Thomson Reuters) at [8.170], [8.180] and [9.330]. Here, even if one was to accept that there was a “mistake” as alleged, it was entirely unilateral and it was not suggested that Mr and Mrs Eppelstun were in any way aware of it.

68 Determining this issue of construction brings into focus the relationship between the Schedule and cl 24 of each of the Contracts; this is an issue that is fundamental in: (a) ascertaining whether there is a relevant “gap” in the Contracts as alleged; and (b) ascertaining what was represented by the Seller to the Buyer by placing crosses in the GST Schedule in the draft contract for exchange, a matter central to the way the express representation case advanced by the applicants is pleaded.

69 Having dealt with the terms of the Contracts and prior to considering how the Printed Terms deal with the rights and obligations of the parties relating to GST inter se, it is useful to set out from Annexure A, in tabular form, the relevant dates and also what each Contract said about the nature of the anticipated supply and what, in truth, the positon was on completion:

CONTRACT | EXCHANGE | WHAT THE CONTRACT “SAYS” ON EXCHANGE | COMPLETION | NATURE OF SUPPLY ON COMPLETION |

Lloyd Contract | 10 March 2015 | Taxable supply – agreement to apply margin scheme | 7 April 2015 | Input taxed |

El-Zein Contract | 15 April 2015 | Taxable supply – no agreement to apply margin scheme | 5 June 2015 | Taxable Supply |

Eppelstun Contract | 5 October 2015 | Taxable supply – agreement to apply margin scheme | 5 November 2015 | Input taxed |

70 As can be from the above table, it is important to note that no claim has been brought forward in either case in which: (a) the relevant contract said on exchange there was to be a taxable supply; (b) there was an agreement to apply the margin scheme; and (c) the supply was a taxable supply upon settlement.

C.6 The Relationship between the GST Schedule & Clause 24

71 The GST Schedule and cl 24 cannot be considered otherwise than in the context of each of the Contracts as a whole. Obviously enough, when one considers how the Contracts deal with the rights and obligations of the parties relating to GST, the starting point (page 1 of the Schedule) is that the Price is “GST inclusive unless otherwise specified” and the contractual choice of the parties was not to otherwise specify.

72 As noted above, however, the fact that the Price was GST inclusive is not the same as saying that the supply on completion would necessarily be a taxable supply, or that GST would necessarily be payable following the supply. As explained above, the Contracts necessarily contemplated that the characterisation of the supply could change between exchange and settlement. Subject to further qualification by other terms, what “GST inclusive” means in the standard contract for the sale of real property in the ACT is that irrespective of what happens between exchange and settlement or prior to GST becoming payable, the Buyer will have no liability for payment of GST. In this sense, the “risk” of liability for GST lies with the Seller.

73 This is neither novel nor surprising. In Duoedge Pty Ltd v Leong [2013] VSC 36, a purchase was made in accordance with the standard Real Estate Institute of Victoria contract for sale of real estate, which included a condition:

13 GST

13.1 The Purchaser does not have to pay the Vendor any GST payable by the Vendor in respect of a taxable supply made under this Contract in addition to the price unless the Particulars of Sale specify that the Price is ‘plus GST’…

74 The parties filled in the purchase price but added a handwritten annotation so that it read “$916,000 GST inclusive”. A special condition required the vendor to provide the purchaser with a tax invoice and, prior to settlement, the vendor provided a tax invoice. Having subsequently developed and sold off the developed land, the purchaser claimed an input tax credit, but this was rejected by the ATO and the purchaser commenced proceedings in the Magistrate’s Court against the vendor seeking a refund of an amount representing the GST amount identified in the tax invoice. In the course of allowing an appeal against the findings of a Magistrate that a term could be implied that if the supply was not taxable, the vendor would refund the GST amount identified in the tax invoice and curiously (in the light of the foregoing conclusion) that rectification of the contract was appropriate, John Dixon J at [23] explained:

The plain meaning of this contract is that the GST risk lay with the vendor … The parties have expressed the intention that the purchaser has no obligation to make a further payment in respect of any GST assessment that might later follow. In other words, the parties plainly intended that the risk that GST might need to be remitted to the Tax Office lay with the vendor. If the transaction did not involve a taxable supply, that risk was abated to the benefit of the vendor, who retains the full price that it contracted to receive for the property. Objectively assessed, this is what the terms relating to GST show to be the intention of the contracting parties. This construction is neither uncertain, nor ambiguous.

75 It seems to me the argument of the applicants that “GST inclusive” as used in the context of these Contracts means something different to its use in the contract considered by John Dixon J, does not withstand scrutiny. Like with the Victorian contract, the “default” position under the Printed Terms was that the Price was inclusive of GST. The Contracts necessarily accommodated the possibility, irrespective of the crossing or crossings in the GST Schedule, that the nature of the supply could change when it later came time, upon completion, to make the supply. As explained above, this possibility is reflected in parts of cl 24 (see [43] above) and also in cl 52(b) of the Altitude Special Conditions (see [48] above) and cl 32.2 of the Eppelstun Contract (see [57] above).

76 What follows from this are two matters of importance in understanding the operation of the Contracts: first, as a general proposition, to the extent that there is a risk of the supply being taxable on settlement, subject to any terms to the contrary, such a risk is allocated to the Seller as the party liable to remit any GST payable to the ATO; secondly, as noted above, there is an identifiable risk to be allocated, because the time of the relevant supply is at completion and not exchange, which, in the case of at least some of the “off-the-plan” sales, might be years in the future.

77 What then does the crossing of a box in the GST Schedule signify?

78 The first function is that crossing a box in the GST Schedule serves to engage cl 24 of the Printed Terms. Contrary to the argument initially advanced by the applicants (later not seriously pressed), the ticking of the box itself does not constitute a promise or a warranty about what would happen upon settlement. The primary role of placing a cross or crosses in the boxes is to signify which subclauses within cl 24 apply, subject to any Special Conditions. For example (like any other provision of the Contracts which noted an agreement the margin scheme would apply, such as cl 52(b) of the Altitude Contracts or cl 32.2 of the Eppelstun Contract), the ticking of the box notifying that the parties agreed the margin scheme would apply, operates to engage cl 24.5. Similarly, the ticking of the box that says the sale is a taxable supply (without the parties agreeing the margin scheme would apply), engages cl 24.6. Of course, cll 24.3.2 and 24.7 could also be engaged depending upon the circumstances. If the sale was GST exclusive and the taxable supply box is crossed, subject to any change of the nature of the supply on settlement, cl 24.2 would then operate.

79 A second function, when properly analysed, is connected to the first. It is not in contest that the crossing of the boxes on the Contracts was performed on behalf of the Seller in a version of the relevant Contract provided to the Purchaser. The respondents contested the notion that the crossing of the boxes constituted any statement or representation by the Seller, but submitted that to the extent it did so, the representation that was conveyed was not as alleged by the applicants: see Final Submissions of Belconnen (SB) at [395], [499], [502], [511]; Final Submissions of Barton Developers (SBD) at [13], [83], [166].