FEDERAL COURT OF AUSTRALIA

Fuge v Commonwealth Bank of Australia [2019] FCA 1621

ORDERS

DATE OF ORDER: | 30 SEPTEMBER 2019 |

THE COURT ORDERS THAT:

1. By 4pm on 4 October 2019 the parties provide to the Court agreed minutes of order reflecting these reasons for judgment or, in the absence of agreement, competing minutes of order identifying the orders for which the parties contend.

2. In the event orders cannot be agreed, the proceeding is to be listed on a date to be notified by the Associate to Justice Lee for the purposes of the Court receiving the submissions of the parties as to the competing orders.

Note: Entry of orders is dealt with in Rule 39.32 of the Federal Court Rules 2011.

LEE J:

1 The applicants (Fuges) are a farming family. They feel a great affinity for the land they have toiled and feel a sense of injustice at the prospect of the connexion they have with that soil being severed. What follows is a tale of bad luck, miscalculation and wilfulness from which neither the Fuges nor the first respondent (Bank) emerges unscathed. The difference is that for the Fuges, their miscalculations have been life altering; for the Bank, it will presumably recover the money that is owed to it and move on.

2 This proceeding has several unfortunate characteristics which are recurringly seen by anyone experienced in banking litigation. One is that people experiencing a sense of grievance and in financial distress litigate at length over family property and incur costs which they cannot afford and are not well proportioned to the value of any claim. A second is that claims warranting relief are made on a less than compelling basis. A third is that sage advice encouraging a client to overcome their sense of grievance and salvage what they can from the wreckage, is either absent or not followed. A fourth is the making of a partly absurd claim by lawyers which can serve to distract attention away from other claims which may have merit, and entrenching the hostility of the opposing party. Justice Bryson said in the context of family equity suits in Turner v Windever [2005] NSWCA 73; (2005) ANZ Conv R 214 at 222 [104], a “Judge in Equity recurringly sees families destroy their economic positions and well-being in similar ways, and it is not in the Court’s power to stop it”. The same can be said for disputes of the present type.

3 The Fuges conducted their farming business on three properties near Forbes in the Central West region of New South Wales. One property (Kennedia West) was owned by Mr Anthony Fuge and the other two properties (Greenfields and Lenborough) were owned by both Anthony Fuge and Mr Matthew Fuge as tenants-in-common in equal shares (I will describe all three properties collectively as the Properties). The Fuges also owned water rights associated with each of the Properties (Water Rights). Until sometime around late 2008, the Fuges conducted a partnership (Partnership) which apparently operated the farming operations. The Partnership dissolved as a trading entity in 2008, from which time Anthony Fuge continued to conduct all farming operations in his own name.

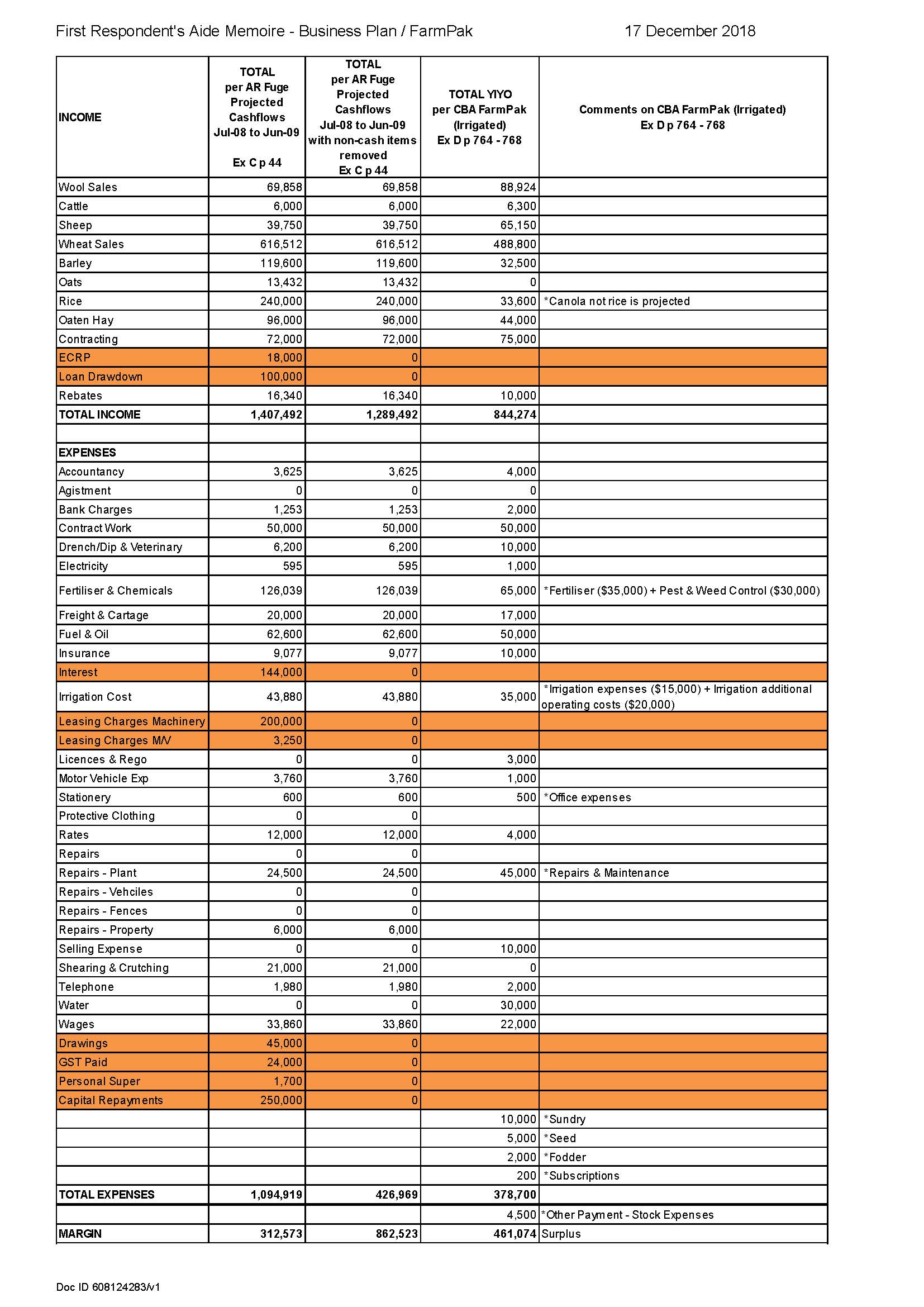

4 Prior to August 2008, the Fuges had various loans with Elders Rural Bank Ltd (Elders). By mid-2008, they used the services of a finance broker, Ms Sue Cohen, to seek to arrange alternative finance. Ms Cohen approached the Bank with a business plan prepared by Anthony Fuge in an effort to refinance with the Bank.

5 The Fuges advance a multitude of claims against the respondents. It is no longer necessary to detail the claims made as against the second and third respondents, as these were belatedly discontinued on the second day of the hearing. As against the Bank, for reasons which will become evident, it is not presently useful to attempt a detailed summary of the pleadings. It is best to begin by outlining in some detail the background to the dispute.

6 In late 2008, the Bank approved the Fuges’ application for finance and two “AgriAdvantage Plus” facilities were established, totalling $1.65 million, namely:

(a) $900,000 AgriAdvantage Plus facility for Anthony Fuge recorded in a letter of offer/facility agreement dated 7 August 2008 (signed by Anthony Fuge on 21 August 2008), comprising:

(i) $750,000 “better business loan” with a 5 year term (with the stated purpose being “refinance of existing finance”); and

(ii) $150,000 overdraft facility with an indefinite revolving term but repayable on demand (with the stated purpose being “working capital”);

(b) $750,000 AgriAdvantage Plus facility for Matthew Fuge recorded in a letter of offer/facility agreement dated 7 August 2008 (signed by Matthew Fuge on 12 September 2008); the facility comprised a better business loan for $750,000 with a 5 year term (with the stated purpose being “refinance of existing finance”).

7 These facility agreements required security to be provided by the Fuges, which comprised:

(a) three registered mortgages over the Properties, all dated 1 October 2008 (being the Kennedia West Mortgage; the Lenborough Mortgage; and the Greenfields Mortgage);

(b) first equitable charges over the three bundles of Water Rights;

(c) guarantee given by Anthony Fuge in respect of the borrowings of Matthew Fuge; and

(d) guarantee given by Matthew Fuge in respect of the borrowings of Anthony Fuge.

(collectively, the 2008 Original Securities)

8 Anthony Fuge executed his documents at Lenborough on 15 September 2008, in the presence of Mr Richard Hewitt, and Matthew Fuge executed his documents in Hong Kong. On 9 October 2008, the refinance of the Fuges’ Elders loans settled and the Bank paid Elders a sum of $1,423,046.90.

9 On 13 October 2008, the Bank wrote to both the Fuges confirming the establishment of the $750,000 better business loans with terms of five years. Over time, a series of changes were made to the original 2008 credit facilities with the 2008 Original Securities largely remaining in place. The changes were in the nature of advancing further funds, rolling-over loans and extending some liabilities. The changes are recorded in various letters of offer/facility agreements, signed by the Fuges as required.

10 In May 2009, the Bank extended a further AgriBusiness Line of Credit facility up to $130,000 to Anthony Fuge. This increase in the facilities required additional security in the form of a business and livestock mortgage to be given by both Fuges over all assets, including Merino sheep at Lenborough, Greenfields and Kennedia West (Business Mortgage). No additional funds were advanced or extended to Matthew Fuge, but the guarantee previously given by him in respect of Anthony Fuge’s liabilities was required to be extended to a new total of $1.03 million.

11 In February 2010, the Bank provided a further AgriAdvantage Plus better business loan in the amount of $100,000 to the Fuges. The security remained the same.

12 By February 2011, the one-year $100,000 better business loan had expired, and the Bank agreed to “roll over” that loan for a further one-year term. The security remained the same, other than the Business Mortgage previously given by both Fuges being replaced with a new mortgage to be given only by Anthony Fuge (Livestock Mortgage).

13 The evidence then discloses further letters of offer/facility agreements dated 22 February 2011, which record the Livestock Mortgage to be given by Anthony Fuge. The Livestock Mortgage appears to have been signed by Anthony Fuge on 25 February 2011, although the FASOC asserts this to be the product of forgery. The Livestock Mortgage was a mortgage over “all assets and uncalled capital including Merino Sheep depastured at” Lenborough, Greenfields and Kennedia West.

14 In March 2012, the $100,000 better business loan was rolled over for a further one-year term. In May 2012, the Bank extended and increased the $100,000 better business loan. The loan was extended to 27 March 2013 and the amount increased to $200,000. Again, the security did not change.

15 By 30 April 2012, the temporary extension of Anthony Fuge’s overdraft facility was required to be reduced back to $150,000. On 27 March 2013, the $200,000 better business loan (from May 2012) expired and was required to be repaid by the Fuges. On 9 October 2013, the $750,000 better business loans granted to each of Anthony and Matthew Fuge in 2008 were due to be repaid. The Fuges did not comply with any of these obligations.

B.3 Farm Debt Mediation and Settlement Recorded in “Heads of Agreement” Dated 17 July 2014

16 On or about 21 February 2014, the Bank issued a notice to the Fuges (s 8 Notice), pursuant to s 8 of the Farm Debt Mediation Act 1994 (NSW) (FDMA). The s 8 Notice identified that a total amount of $2,247,680.83 was then owing by the Fuges and that the Bank intended to take enforcement action. On 21 March 2014, Anthony Fuge sent an email to Mr Hewitt (which was then forwarded to Mr Matthew Maxwell) attaching a notice pursuant to s 9 of the FDMA, in which the Fuges requested a mediation. On the same day the Bank’s solicitors notified the Rural Assistance Authority that a mediation was required.

17 The Fuges engaged Mr Stephen Jay as their Rural Assistance Counsellor to assist them in relation to the mediation and their negotiations with the Bank. Mr Jay, on behalf of the Fuges, proposed that Mr David Bogan be appointed mediator and the Bank agreed.

18 A farm debt mediation took place on 17 July 2014 (Mediation). It was attended by Mr Maxwell and a solicitor from the Bank, as well as the Fuges and Mr Jay. Mr Bogan attended as mediator. The Mediation began at approximately 10am and concluded in the early afternoon. Precisely what occurred at this mediation will be considered in detail in Section E.4.3 below.

19 Unlike in many cases involving mediations, here we know some of what occurred by reason of evidence being adduced by the parties. It is necessary to explain why. The issue is one which I discussed in Dixon (Trustee) v Citiline Developments Pty Limited, in the matter of Nasr (Bankrupt) [2018] FCA 1446 in a different context; that being whether s 79 of the Judiciary Act 1903 (Cth) (JA) picks up s 304 of the Duties Act 1997 (NSW).

20 In the present case, the relevant section, s 18F (previously s 15) of the FDMA provides that:

18F Confidentiality of mediation sessions

(1) Evidence of anything said or admitted during a mediation session and a document prepared for the purposes of, in the course of or pursuant to, a mediation session are not admissible in any proceedings in a court or before a person or body authorised to hear and receive evidence.

(2) In this section, mediation session includes any steps taken in the course of making arrangements for a mediation session or in the course of the follow-up of a mediation session.

(3) This section does not apply to the following documents:

(a) a mediation agreement,

(b) a contract, deed, mortgage or other instrument entered into as a result of, or pursuant to, a mediation agreement,

(c) a summary of mediation under section 18O.

(4) This section does not apply to proceedings commenced with respect to any act or omission in connection with which the information has been disclosed on the basis of preventing or minimising the danger of injury to any person or damage to any property.

21 Of course in this justiciable controversy wholly within federal jurisdiction, the FDMA only applies by operation of s 79(1) of the JA, which provides:

The laws of each State or Territory, including the laws relating to procedure, evidence, and the competency of witnesses, shall, except as otherwise provided by the Constitution or the laws of the Commonwealth, be binding on all Courts exercising federal jurisdiction in that State or Territory in all cases to which they are applicable.

22 The FDMA therefore only operates as surrogate federal law to the extent that it is not inconsistent with either the Constitution or, relevantly here, a law of the Commonwealth. The evidence of what occurred during the mediation is unquestionably relevant to a fact in issue in this case, meaning it is relevant within the meaning of s 55 of the Evidence Act 1995 (Cth) (EA), being the law governing admissibility at this hearing. It follows that pursuant to s 56(1), except as otherwise provided by “this Act” (that is, the EA), evidence that is relevant in a proceeding, is admissible in the proceeding. The s 18F exception preventing admissibility of otherwise relevant evidence, is not “picked up” and applicable in the present circumstances (although it would have had applicability in the event a New South Wales court exercising federal jurisdiction was determining this matter, as another New South Wales Act – rather than a law of the Commonwealth – would be regulating issues of admissibility). When my preliminary view along these lines was drawn to the attention of the parties at the commencement of the hearing when dealing with objections, the objections previously maintained by the Bank as to the admissibility of evidence as to what occurred at the mediation were not pressed.

23 In any event, at the conclusion of the Mediation, a document entitled “Heads of Agreement” was signed by all parties (HOA).

24 The HOA included the following express terms which are of particular note in this proceeding:

(a) the [Fuges] acknowledge and agree that they are in default of the Transaction Documents … by virtue of the Defaults specified in the Section 8 Notice (cl 3.1.1);

(b) the [Fuges] acknowledge and agree that the Amount Owing [being, $2,247,680.83] is immediately due and payable by them to the [Bank] (cl 3.1.2);

(c) the [Fuges] are required to repay to the [Bank] the Amount Owing, together with accrued interest and costs by 30 November 2014 (c 5.1);

(d) the [Fuges] must make a payment of $50,000 to the [Bank] by 20 August 2014 (cl 5.2);

(e) the [Fuges] acknowledge and agree that their obligations to the [Bank] to repay the Amount Owing are secured by the Securities [set out in the s 8 Notice Notice] (cl 3.1.3);

(f) the [Fuges] release and discharge the [Bank] from all claims against the [Bank] arising from or in connection with the Transaction Documents (cl 4.2);

(g) by 31 July 2014, the [Fuges] must obtain market appraisals and sale methodology advice from 3 licensed agents as to the most appropriate method of sale for each of the Properties (on basis of the timeframes agreed within this Agreement) together with sales price guidance for each Property (cl 5.3);

(h) by 7 August 2014, the [Fuges] must provide to the [Bank] copies of the selling agents’ signed agency agreements for the sale of each of the Properties and details of the marketing campaign proposed for the sale of the Properties (cl 5.4);

(i) The [Fuges] must provide the [Bank] … with written fortnightly updates … as to the progress of the sale campaign for the Properties including a list of all interested parties, inspections conducted and any interim offers to purchase the Properties (cl 5.5);

(j) by 15 October 2014, the [Fuges] must provide to the [Bank] for its approval in writing, unconditional contracts for the sale of each of the Properties with a sale price sufficient to repay the Amount Owing, together with accrued interest and costs and a settlement date of not (sic) longer than 42 days from the date of exchange of a signed contract for sale (cl 5.6);

(k) in the event that the [Fuges] fail to comply with a term of this Agreement or commit any further defaults under the Facilities, they agree to:

(i) deliver up vacant possession of all of the Properties;

(ii) consent to judgment in favour of the [Bank] for the Amount Owing plus accrued interest and costs and possession of the Properties;

(iii) not do anything to interfere with the [Bank] taking possession of the Properties; and

(iv) a sale by the [Bank] in its capacity as mortgagee in possession (or by its appointed agents)

(cl 5.8)

(l) the [Fuges] may rescind this Agreement at any time before 5pm on the 14th day after the day on which this agreement is entered into (cl 8.1).

25 Despite the agreement reached at the mediation, the Fuges did not comply with cll 5.1, 5.2, 5.4 and 5.5. The Bank’s solicitors wrote to the Fuges on numerous occasions between August and December 2014 noting the alleged breaches of the HOA, as well as making certain offers.

26 By 19 January 2015, the Bank had not been paid the outstanding debt and issued a formal Notice of Demand to the Fuges, identifying their continuing breaches and demanding payment in the amount of $2,388,315.26 by 4.00pm on 23 January 2015. The Fuges did not make the payment by that deadline.

27 On or around 5 February 2015, the Bank served notices pursuant to s 57(2)(b) of the Real Property Act 1900 (NSW) (RPA) in respect of the Lenborough Mortgage, the Greenfields Mortgage and the Kennedia West Mortgage. On 9 February 2015, the Bank appointed Mr Robert Moodie and Mr Will Griffiths as receivers and managers. On 17 March 2015, the receivers and managers retired and they were instead appointed as agents for the Bank.

28 In August, purchasers were secured for Lenborough and Greenfields. During this period and up until 14 December 2015, the Fuges put various offers to the Bank in an effort to settle the dispute by selling Kennedia West and refinancing the debt owing to the Bank. These offers are detailed in Section H below. On 20 November 2015, Anthony Fuge exchanged a sale contract for Kennedia West with a purchaser. On 14 December 2015, the Bank exchanged contracts in relation to Lenborough and Greenfields and their respective Water Rights.

29 In July 2015, Mr Griffiths sold 214 Merino wether lambs and once the Properties were sold, the balance of the flock pursuant to the Livestock Mortgage.

30 The Bank applied these sale proceeds towards various facilities owing by the Fuges in the manner detailed in the affidavit of Mr Greentree at [169] with the result that the Bank calculated the amount owing by the Fuges as at 21 December 2017 to be $739,058.49. It will be necessary to resolve the dispute as to quantum below.

31 Regrettably, notwithstanding numerous amendments, the pleadings filed by the applicants were at best obscure and at worst incoherent. At the beginning of the hearing, I indicated to counsel for both sides that in order to obtain clarity in relation to those matters that I was required to determine, it was necessary that the real issues be identified with precision. My resolve to adopt such a course was fortified by the fact that the opening submissions filed in advance of the hearing by both parties demonstrated that there was an asymmetry between them as to precisely what was, and was not, part of the case to be advanced. Repeatedly during the course of the hearing, I made it crystal clear to counsel appearing for the Fuges that unless an issue appeared on the agreed list of issues which reflected the issues to be determined, then I did not propose to determine it. Accordingly, as matters emerged during the course of the hearing and it became clear that the list of issues was in some way incomplete, it was the subject of a specific order amending the list which became known as MFI 7.

32 The ultimate version of MFI 7 was in the following form:

MFI 7

ISSUES FOR DETERMINATION

1. Whether upon a proper construction of clause 4.2 of the Heads of Agreement dated 17 July 2014 (HOA), any causes of action by the applicants against the respondent (Bank) alleging: (a) improvident lending or unconscionable conduct or unjust contract relief or NCC relief in relation to facilities provided by the Bank prior to the HOA (Relevant Facilities); (b) breach of clauses 2.2, 25.1, 25.2, 26.2 and/or 28.5 of the [Code of Banking Practice] in relation to the provision of the Relevant Facilities; (c) negligent advice or omission of advice in relation to the provision of the Relevant Facilities; (d) misleading representations as to Special One Grain; or (e) as to invalidity or discharge by operation of law of any securities or guarantees existing as at 17 July 2014 (Pre-2014 Causes of Action) were released?

2. If one or more of the Pre-2014 Causes of Action would, on a proper construction of clause 4.2, have been released if the HOA was valid, is the HOA invalid because:

a. of some invalidity in the form of the notices pursuant to which the Farm Debt Mediation was convened by reason of the fact:

i. the Business and Livestock Mortgage by Anthony Fuge over all assets and uncalled capital including Merino Sheep purportedly dated 28 February 2011 (MFI 2, 351-355) (Livestock Mortgage) was forged or fraudulently made; or

ii. Anthony Fuge did not have authority to charge part of the Security the subject of the Livestock Mortgage?

b. the HOA was executed in circumstances where the conduct of the Bank in the mediation was contrary to the good faith requirement provided for in Part 2 of the Farm Debt Mediation Act 1994 (NSW) (for the reasons particularised in the schedule to this document)?

c. the HOA is a credit contract to which the National Credit Code applied that is unjust (for the reasons set out in the schedule to this document) and an order should be made that it is invalid?

d. the HOA was an unjust contract within the meaning of s 9 of the Contracts Review Act 1980 (NSW) (for the reasons set out in the schedule to this document) and an order should be made that it is invalid?

e. the HOA should be set aside because the entry into the HOA amounted to unconscionable conduct contrary to the provisions of s 12BC of the Australian Securities and Investments Commission Act 2001 (Cth) (for the reasons set out in the schedule to this document)?

3. In the light of the answers to questions 1 and 2, for such of the Pre-2014 Causes of Action that are able to be maintained, are the applicants entitled to any and, if so, what relief against the Bank?

4. Irrespective of the answers to questions 1 to 3, are the applicants entitled to common law damages or equitable relief by reason of the sale of any security property by the Bank after 17 July 2014 at an undervalue?

5. Irrespective of the answers to questions 1 to 4, are the applicants entitled to common law damages by reason of a breach by the Bank of the Code of Banking [Practice] arising by reason of the Bank's failure after 17 July 2014 to accept refinance offers made to the Bank on behalf of the applicants (being offers to discharge their indebtedness to the Bank)?

6. Whether the guarantee which appears at Exhibit C p 219 was discharged by operation of law by reason of the fact that the livestock mortgage (Exhibit C p 351) was entered into by the Bank and Anthony Fuge without the consent of Matthew Fuge.

7. Is the Bank entitled to the relief it seeks in the cross claim?

33 At the conclusion of the hearing, I directed that the parties make their final submissions in relation to the matters identified in MFI 7. In large part, the parties complied with this order and it is convenient to structure the balance of these reasons by reference to these issues. It should also be noted, however, that this case did not proceed with celerity, and by the time it came to finally reserve my judgment in this proceeding (six months subsequent to the hearing commencing), the parties had provided to the Court a total of no less than 19 different sets of submissions and aide-memoires. To the extent that any submissions of the parties have not been dealt with in this judgment, this is because they were either not substantiated beyond mere assertions or I do not consider that they relate relevantly to the issues specified in MFI 7.

D CONSTRUCTION OF THE HEADS OF AGREEMENT (Issue 1)

34 The first issue concerns the construction of cl 4.2 of the HOA.

35 The Bank contends that cl 4.2 is a complete release which operates to bar all of the Fuges’ Pre-2014 Causes of Action. Unsurprisingly, the Fuges contend that it does no such thing.

36 The general release in this proceeding was in the following terms:

From the date of this Agreement, the [Fuges] release and discharge the [Bank] from all Claims against the Creditor arising from or in connection with the Transaction Documents.

(emphasis added)

37 For the purpose of the HOA, Claim is defined in cl 1 to include: “a claim, demand, debt, action, proceeding, suit, cost, charge, expense, damage, loss and other liability”. Transaction Documents are defined to mean the “Facilities and the Securities” which in turn were defined as the Facilities and Securities referred to or set out in the s 8 Notice attached to the HOA. The s 8 Notice referred to those facilities and securities detailed in Section B above.

D.1 Whether cl 4.2 releases all claims arising from or in connexion with the Transaction Documents

38 The Fuges do not appear to cavil with the characterisation of the release as general, however, a number of arguments were advanced as to why the release would still not apply. Generally, it was contended that the words of a release are not determinative and the context of both the HOA and its formation must be considered. This is said to be a circumstance where the general release should be read as being constrained or qualified by the pre-existing dispute between the parties – being the repayment of the debts.

39 It is plain that as a general proposition, general words of release may from time to time be limited. At common law, the effect of a release accords with its likely ordinary and natural meaning. Where a release is expressed in general terms, however, principles of construction dictate that the operation of the exclusion will be limited to the subject or occasion to which the agreement, read as a whole, refers: Grant v John Grant & Sons Proprietary Limited (1954) 91 CLR 112 at 123 (Dixon CJ, Fullagar, Kitto and Taylor JJ). The Full Court of this Court recently explained in Sarina v Fairfax Media Publications Pty Ltd [2018] FCAFC 190 at [20]:

Thus, where, as often occurs, a deed recited that the parties have had a particular dispute, but the clause creating the release did not expressly confine its operation to the dispute mentioned in the recitals, the principles of construction at common law read down the wide words of the release to apply only to the dispute in the recitals.

40 As a matter of common law construction, the Fuges submit that: (a) the recital, acknowledgements and mediation agreement at Schedule 1 circumscribe the limits of the dispute; and (b) the s 8 Notice only refers to the Fuges’ defaults rather than the facilities themselves such that the release does not extend to issues as to the facilities. It is convenient to deal with these arguments sequentially.

41 First, the recital and acknowledgement clauses are said to confirm that the only dispute being resolved was the Bank’s claim against the Fuges for failure to repay their loans. The recital is in the following terms:

RECITALS

Whereas:

A. The Creditor provided the Facilities to the Farmers.

B. The Creditor holds the Securities to secure the repayment of the Amount Owing under the Facilities.

C. The parties have participated under the Act to address the issues in dispute among them and have reached an agreement on the terms set out below.

42 The Acknowledgement clause sets out a series of acknowledgements made by the Fuges. This includes:

The Farmers acknowledge and agree that:

3.1.1 they are in default of the Transaction Documents;

…

3.1.4 the Transaction Documents are valid and enforceable in accordance with their terms and continue in full force and effect;

43 It is difficult to see how, as a matter of construction, these clauses could assist the Fuges’ case given that the acknowledgement and recital expressly put the enforceability of the Transaction Documents in issue. The Fuges insist that the Acknowledgements clause is “absolutely silent” on the Bank’s wrongdoing. This is beside the point. The clause is not silent on the enforceability of the Transaction Documents. As to the Mediation Agreement, the submission made was that it describes the dispute by reference to the s 8 Notice. For that reason, this argument is sufficiently disposed of by my analysis as to the s 8 Notice below.

44 Secondly, it will be recalled that the Transaction Documents were defined in the HOA as the Facilities and Securities “referred to or set out in” the s 8 Notice. The Fuges argued that since the Transaction Documents were defined by reference to the s 8 Notice, and the s 8 Notice’s descriptions of “Facilities” and “Securities” only reference the Fuges’ failure to repay the Facilities, the only matter that “arises from” or “connects with” the Transaction Documents is a failure to pay. This argument does not withstand scrutiny. The only way in which the s 8 Notice feeds into the release clause is in a definitional sense, by giving content to the words “Transaction Documents”.

45 The s 8 Notice is a two-page document that outlines the Bank’s intention to take enforcement action. In detailing the defaults, the s 8 Notice names each of the various loans, and at the bottom of the first page there is a table which details all relevant facilities and their balance at the date of issue of the s 8 Notice. All Facilities outlined in Section B above, are clearly “referred to” in the s 8 Notice. The suggestion that the s 8 Notice should then operate so as to delimit the issues of the HOA to the Fuges’ obligation to repay the Bank, while excluding issues in relation to the enforceability or validity of those facilities and securities, merely needs to be stated to be rejected.

46 It is clear that as a matter of construction, issues 1(a)(b)(c) and (e) are all claims which in their terms explicitly “relate to” the facilities provided by the Bank, and therefore in turn, to the Transaction Documents. Issue 1(d) is slightly more complex and will be considered separately below.

47 In addition to the arguments of construction at common law, the Fuges seek to rely upon the High Court’s (Dixon CJ, Fullagar, Kitto and Taylor JJ) statement of equitable principle in Grant v John Grant at 129–130:

From the authorities which have already been cited it will be seen that equity proceeded upon the principle that a releasee must not use the general words of a release as a means of escaping the fulfilment of obligations falling outside the true purpose of the transaction as ascertained from the nature of the instrument and the surrounding circumstances including the state of knowledge of the respective parties concerning the existence, character and extent of the liability in question and the actual intention of the releasor.

48 In Sarina the Full Court explained at [21]:

[E]quity will restrain a party seeking to enforce a wide or general release where it would be unconscientious for that party to do so in all of the circumstances. In such a case, the court will examine the knowledge and intention of both releasor and releasee as to the subject matter on which the release would operate.

49 The Fuges contend that the equitable doctrine expressed in Grant v John Grant should apply to cl 4.2 because:

there is not an (sic) single iota of any evidence showing that the Fuges knew about, articulated, or complained to the Bank, prior to the Heads of Agreement, that they were dissatisfied with, entitled to, or were thinking about making a claim regarding asset lending, misleading or deceptive conduct, rights under the National Credit Code or Code of Banking Practice, and so on.

50 The difficulty for the Fuges is that it is not to the point whether they were aware of the specific legal claims potentially available to them at the time of signing the release. Equity will only intervene to prevent unconscientious reliance upon the general release. As demonstrated by the contents of the s 8 Notice and the agreement contained within the HOA as a whole, the Fuges were well aware of the fundamental factual bases out of which their Pre-2014 Causes of Action are said to have arisen. The HOA was entered into after the Mediation, which had taken place between the Fuges and the Bank as customers and banker, in relation to a number of loans, mortgages and other charges and guarantees which regulated their relationship.

51 The Fuges did not point to any inequality in knowledge between themselves and the Bank as to the circumstances or factual underpinnings of the facilities and securities, nor was any element of bad faith or disentitling conduct specifically alleged in relation to withholding information pertinent to the Pre-2014 Causes of Action. Equity will not intervene where an agreement was then struck and the Fuges agreed to release all claims against the Bank arising out of such a context. The parties are taken to have intended to resolve or reach a compromise in relation to all extant claims arising from the facilities and securities between them. Equity will not intervene to displace the position at law that issues 1(a)(b)(c) and (e) are released.

D.2 Whether Issue 1(d) was released by cl 4.2

52 In order to assess whether this claim was within the scope of the release, it is necessary to outline the details of the alleged misleading representation.

53 The representation is said to have occurred during a conversation between Anthony Fuge and Mr Hewitt. The contextual background being that Anthony Fuge and Mr Hewitt had a telephone conversation during which the issue of pooling grain arose. Anthony Fuge contends Mr Hewitt made a representation to the following effect: “If I had 10,000 tonnes I’d pool it with [Special One Grain] because they’re safe as houses and they’re a customer of ours”: FASOC at [9A(c)]. It is said that in reliance upon this representation, Anthony Fuge pooled a large amount of his harvest with Special One Grain. At [9E] it is alleged that the representation was erroneous in that the investment was an unreliable source of income “to meet his financial commitments including to the Bank”, and the Fuges suffered significant loss and damage in that Special One Grain underperformed.

54 Whether or not this representation was in fact made is not relevant to the present enquiry. The Bank accepts that a claim for misleading representation not associated with the Transaction Documents would not likely be covered by cl 4.2. The Bank provided four reasons as to why the claim was so associated.

55 First, the Bank relies upon the loss and damage element of the claim. The FASOC at [9J] particularises the loss suffered by reason of the misrepresentation as being loss of the Properties and associated Water Rights among other things. This is said to be enough to mean that the claim is “related to” the Transaction Documents, because presumably the Fuges’ claim is that the direct financial loss which occurred by reason of the misrepresentation prevented them from fulfilling their repayments.

56 Secondly, the Bank argues that in any event, the Fuges failed to advance any claim that they suffered loss that was not referable to the Transaction Documents. Thirdly, the alleged losses attributable to the representation were crystallised by the mediation and were therefore susceptible to being released.

57 Although the Fuges have sought to run any loss occasioned by the misrepresentation together with the broader claim, and have inadequately particularised the alleged loss directly referable to the Special One Grain representation, this does not mean, in and of itself, that the only potential loss that can be claimed is in relation to the facilities. To proceed otherwise would be to ignore the statutory words in s 82 of the Competition and Consumer Act 2010 (Cth), that a person is entitled to recover the amount of the loss or damage caused by the contravention. I am not persuaded that due to the wide-ranging particularisation of loss, the claim as to misrepresentation arises from or is in connexion with the Transaction Documents. The claim arises out of alleged advice given as to the investment of the Fuges’ grain harvest. How the Fuges were then planning to use that income is irrelevant.

58 Lastly, the Bank submitted that the FASOC alleges misleading or deceptive conduct “in relation to the provision of financial services”. This does not assist the Bank. The Fuges’ opening submissions make it clear that the financial service being relied upon is the provision of financial and business advice.

59 Notwithstanding the Bank’s submissions, the better view is that the claim as to misrepresentation does not fall within the release. The claim relates to alleged advice given as to the investment of the Fuges’ grain harvest. On an ordinary understanding of this claim and the release, this separate element of the dealings between the Bank and the Fuges was not within the contemplation of the parties at the time of entering into the HOA and was not released; however, for reasons I will explain, if I am wrong on this point, it does not matter as the claim is flawed in any event.

E VALIDITY OF THE HEADS OF AGREEMENT (ISSUE 2)

E.1 Alleged invalidity in the form of notices by which the Farm Debt Mediation was convened

60 This submission rests upon the alleged requirement that a s 8 Notice, such as that issued by the Bank on 21 February 2014, must identify, with respect to a mortgage, “the debt concerned”: Waller v Hargraves Secured Investments Limited [2012] HCA 4; (2012) 245 CLR 311. The Fuges rely upon the proposition that if a s 8 Notice is incorrect, then a valid notice must be re-issued, otherwise the farm debt mediation will be invalid. The s 8 Notice is said to have been invalid by reason of its reference to the Livestock Mortgage, which is said not to be enforceable.

61 Mr King, counsel for the Fuges, accepted during the course of argument, that an invalid s 8 Notice could not, by reason of this fact alone, invalidate an agreement reached at the end of the Mediation such as the HOA, but that the argument could still be relevant to either a larger unconscionability case, or as a defence to the cross-claim, in that the Bank would be statutorily prohibited from taking enforcement action.

62 Despite this concession by Mr King, it is useful to deal with the two substantive allegations made in relation to the form of the notice identified in MFI 7, as my findings in relation to these submissions go on to affect other issues raised in this proceeding.

E.1.1 Forged or Fraudulently Made

63 It is trite that allegations of forgery and fraud are not ones which are to be made lightly. As the Full Court (McKerracher, Robertson and Lee JJ) recently explained in CCL Secure Pty Ltd v Berry [2019] FCAFC 81 at [79]:

Under Rules 64 and 65 of the Legal Profession Uniform Conduct (Barristers) Rules 2015, no allegation of fact in any court document settled by the barrister could be made unless the barrister believed on reasonable grounds that the factual material already available provided a proper basis to do so. Moreover, as to allegations amounting to serious misconduct against any person, it was necessary for the barrister to believe on reasonable grounds that: (a) available material by which the allegation could be supported provided a proper basis for it; and (b) the client wished the allegation to be made, after having been advised of the seriousness of the allegation and of the possible consequences for the client and the case if it was not made out.

64 In the present case, serious allegations of deliberate fraud have been made from an early stage in the pleadings and in the sworn evidence. At [10(a)] of the FASOC, it is alleged that the Livestock Mortgage “is a forgery and was obtained by fraudulent means”. The issue of forgery was also raised at a case management hearing on 22 September 2017, which resulted in the original mortgage being taken into the custody of the Court. Mr King contended later that his basis for the allegation of forgery was that the date on the Livestock Mortgage document was not a date on which Anthony Fuge could have possibly signed it. A handwriting expert was then appointed as a referee, who produced a report which was adopted in February of 2018 (Report). The Report concluded that the signature on the document was likely that of Anthony Fuge. Despite the Fuges accepting the finding of the referee, no amendment was sought to be made to the pleadings and Mr King maintained the submission of forgery in opening submissions. During cross-examination on day three of the hearing, Anthony Fuge was shown an original copy of the Livestock Mortgage and agreed that the document bore his signature.

65 It is important here to divagate briefly, to explain the position taken by Mr King shortly before Mr Zahra, counsel for the Bank, reached the point of cross-examining Anthony Fuge as to the Livestock Mortgage documents. An exchange took place during which I expressed my concern as to his choice to maintain an allegation of fraud given his then instructions. It is worth setting it out briefly (T100-101):

MR KING: … Mr Hewitt brought a bundle of documents out and signed them on the kitchen table, I think, on the back of the truck. And it’s not clear – it hasn’t been made clear – or there is an assumption in my friend’s question that he knew what the documents were that he was signing. And I - - -

HIS HONOUR:… So your instructions, effectively, this was all done – he brought out a bundle of documents, then, on 25 February 2011, all signed over a kitchen table, so he wouldn’t have known one way or the other what he signed.

MR KING: Exactly.

HIS HONOUR: If those are you[r] instructions, how can you maintain that on 25 February 2011 there was a forgery, Mr King?

MR KING: Because the – well, two things: firstly, the document which my friend hasn’t yet taken him to was dated 28 February, not 25 February; and, secondly, he disputes that he did sign it.

HIS HONOUR: Yes, but you have already said to me that it was signed – on your instruction[s], it was signed in circumstances where a whole bundle was put out. There are documents here – I mean, it just seems to me, Mr King – this is a very serious allegation.

MR KING: Yes.

HIS HONOUR: It is an allegation which amounts to professional people engaging in criminal conduct. In the light of his answers in respect of signing other documents on 25 February and what you have just told me about how those documents are signed, I must say, I express no final views about it, but I’m concerned about the basis upon which there is currently in the possession of you and your solicitors [which allows you] to maintain an allegation of serious criminal misconduct against somebody.

MR KING: Yes. Well, your Honour, I refer to the authorities before the luncheon adjournment, and we do maintain it.

66 It was not until day six of the hearing that the following exchange took place (at T544-T545):

HIS HONOUR: Well, we know it’s not forged, don’t we? Are you seriously maintaining it’s forged, given what Mr Fuge said in cross-examination?

MR KING: No, I don’t, but we do say it was fraudulently made, having regard to the misrepresentations it contained and the fact that it was registered.

67 One would have thought that this would be the end of any such issue but on day 12, after closing submissions in reply had been filed, which somewhat remarkably included a submission which doubted the veracity of the second original mortgage not shown to the referee, Mr King finally acknowledged no forgery point was now taken (at T1050-1051):

HIS HONOUR: May I say, frankly, Mr King, I think you’re doing Mr Fuge a disservice by running this argument. Mr Fuge, to my mind, when he was dealing with these documents presented as someone who was genuinely trying to give a proper account. He didn’t obfuscate. He said, “That may well have been my signature”, etcetera.

MR KING: He did.

HIS HONOUR: Now, you for months and months and months had been running a case where there was deliberate fraud where someone had forged a signature, something Mr Fuge wasn’t prepared to come to, to his credit. Now, as far as I’m aware, that case still hasn’t been abandoned …

MR KING: we don’t press the contention, for the reasons your Honour has outlined, that this was a forgery by – of his signature on the document.

…

HIS HONOUR: So … I can take that that’s abandoned?

MR KING: That’s abandoned

68 Despite Mr King’s belated acknowledgment that the claim was abandoned, no application was made to amend the pleading. In any event, the allegation that the document was forged may now be put to one side.

69 Mr King did not, however, abandon any other claims as to fraud. At T1051, it was made clear that the case as to deliberate dishonesty was maintained, specifically, alleging that the Livestock Mortgage was fraudulently made. In closing submissions, it was asserted this was the case for two reasons. First, because the mortgage contains a misrepresentation which the Bank knew to be false at the time of registration. This misrepresentation is said to be that the mortgage is dated “28 February 2011”, when the evidence discloses that it was not signed on that date. It is alleged that the process is not in conformity with any authority that the mortgagor provided. Secondly, the mortgage is said to contain a further misrepresentation, being that Mrs Katrina Noble (née Westcott) witnessed the signature, when in fact, she did not.

70 The first argument is put in such a way that does not require me to make a finding as to whether Mrs Noble did in fact witness the signature. It is said that knowingly dating the mortgage on a date different to that on which Mr Fuge signed it is enough to amount to fraud. Fraud, however, requires actual dishonesty. Even on the Fuges’ case, other than asserting that the Bank knew the date to be incorrect, there is no actual element of dishonesty or malice alleged which can be brought home to the Bank. Beyond ensuring the document was dated prior to registration, there was no dishonest advantage or outcome that the Bank was attempting to achieve.

71 Having regard to the evidence of the witnesses, the most likely chain of events is that the document was signed at Kennedia West, the date was not filled in at that time and it was placed upon the document later by an employee of the Bank working in the securities area of the Bank – hardly a novel state of affairs as would be known to anyone with experience in routine conveyancing (including mortgage) transactions. In any event, how the date of 28 February 2011 came to be on the mortgage document is neither here nor there.

72 The Fuges were not able to provide any relevant authority which supported the proposition that the subsequent dating of the Mortgage was enough to set it aside. The submissions cited two authorities, which do not deal with the issue of incorrect dating: see National Commercial Banking Corp of Australia v Hedley [1986] ANZ ConvR 420; Australian Guarantee Corporation Ltd v De Jager [1984] VR 483. Apart from this, the cases concern the fraud exception to indefeasibility contained in s 42 of the RPA and Transfer of Land Act 1958 (Vic) respectively. Unsurprisingly, indefeasibility does not arise regarding the Livestock Mortgage as it is not governed by the RPA. The Livestock Mortgage was registered pursuant to the General Register of Deeds kept pursuant to the Registration of Deeds Act 1897 (NSW).

73 On no view of it can the subsequent dating of the Mortgage in this case, when the signature and witnessing were carried out according to law, operate as a fraudulent act to invalidate the Livestock Mortgage.

74 In any event, although it was not raised by the parties, it seems quite clear to me that this argument must fail for another reason, being that even if no mortgage could be said to have been validly entered into at common law, the Bank must have a claim for specific performance on the basis that an equitable mortgage exists. Here, the mortgage is in writing; signed by the mortgagor; and identifies the essential terms of the mortgage: see Performance Capital Mortgage Pty Ltd v Motive Finance & Leasing Pty Ltd [2010] NSWSC 429 at [17]-[18]. Moreover, and perhaps more importantly, there are at least two other documents that were signed by both the Fuges by which they agreed that in exchange for the Bank providing certain facilities there would be a suite of securities which included the replacement of a then existing business mortgage and the giving of a new business and livestock mortgage.

75 I now turn to the more serious allegation, that Mrs Noble was untruthful in her evidence and did not in fact witness Mr Fuge signing the document. It is necessary to begin with an assessment of the evidence given by Mrs Noble, Anthony Fuge and Mrs Melanie Fuge.

76 The affidavit evidence of Mrs Noble was that, to the best of her recollection, on at least one occasion she attended a meeting at the Fuges’ property in Forbes with Mr Hewitt. Despite admitting to no longer having an independent recollection of the time or date of that meeting, she did recall Anthony Fuge saying words to the effect of “my wife and I just got married in Eugowra”. She recalled thinking that it must have been uncomfortable weather for the wedding, as she had been in Eugowra at the same time, and it was “incredibly hot”. At the beginning of her evidence in chief, Mr Zahra asked whether Mrs Noble was able to point out Anthony Fuge in the court room, which she then did. Perhaps unsurprisingly, in light of the notorious difficulties with in-Court identification evidence, the Fuges argue that this evidence has very no probative value: see Alexander v The Queen (1981) 145 CLR 395 at 426-427; Festa v The Queen [2001] HCA 72; (2001) 208 CLR 593 at 601 [18]; however, this is neither here nor there, as I have not placed any weight upon this part of Mrs Noble’s evidence.

77 Mrs Noble gave evidence that the dates on the two letters of offer were written by her, and the witness signature on the Mortgage document belonged to her. In cross-examination, she gave evidence that it was always her practice to witness signatures immediately after the customer had signed the document. When asked to explain why the letter of offer was dated by her on 25 February 2011, but the mortgage was not, she replied that “[f]or some reason, things like mortgages and charges over particular assets, the business lending support team preferred for us to send them back undated and they would take care of that. It was something to do with the registration of the documents”: T587.12-15. I accept this evidence.

78 Anthony Fuge appeared to me to be a witness doing his best to tell the truth and, to his credit, was more circumspect in making allegations of wrongdoing than his Counsel. His oral evidence was consistent with the general assertion made in his affidavit evidence, that he had no recollection of Mrs Noble ever coming to the property in Forbes. Although at the beginning of cross-examination on this point he made an assertion that he positively denied Mrs Noble being at the property, this was later clarified. It became clear he had not understood there to be a difference between Mr Zahra’s question as to his not recollecting her being there, and whether he was able to deny positively that fact. Although Anthony Fuge did make an allegation of forgery as to his signature on the document in his affidavit, his oral evidence was delivered relatively thoughtfully, and he did not try to obfuscate when answering difficult questions. Importantly, as mentioned above, upon being shown the Livestock Mortgage, he accepted that the signature belonged to him.

79 The Fuges contend that Mrs Fuge gave powerful evidence denying that Mrs Noble had ever visited their home at Lenborough. Her evidence was, as best as she could remember, that Mr Hewitt always came to the house alone. If she had prior warning that Mr Hewitt was coming, she would usually bake a cake and they would have a cup of tea. In cross-examination, she told the Court that to the best of her recollection, Mr Hewitt was present at the farm on 25 February 2011, but she did not recall Mrs Noble being there. While Mrs Fuge explained she had no recollection of Mrs Noble ever coming to the farm, her evidence did not rise to a positive denial that Mrs Noble could have been there. I am satisfied that Mrs Fuge was trying her best to tell the truth.

80 Mrs Noble was a truthful witness. She did not present as someone with any interest in coming to Court and telling anything other than the truth. Mrs Noble’s oral evidence under cross-examination was consistent with the account given in her affidavit. At no point did Mrs Noble attempt to avoid the fact that her practice was to send mortgage documents to the Sydney office undated. The corroborative detail concerning her recollection of the weather at the time of the wedding also tends to provide some verisimilitude to her account. Further, in circumstances where the evidence of Anthony Fuge and Mrs Fuge is that they could not positively deny that Mrs Noble was present, there is simply no sound basis upon which to draw a conclusion that Mrs Noble did not in fact witness the signature. This would be the case for proof of any fact in similar circumstances, the proof falls so far short of making out an allegation of dishonesty to be risible. The allegation of forgery should not have been made, and once made, it should never have been maintained.

81 This submission rests on the proposition that despite the termination of the Partnership in late 2008, Matthew Fuge continued to own some of the sheep at the time of entry into the Livestock Mortgage. The Fuges submit that by reason of this, it was impossible for Anthony Fuge to commit his brother’s interest in the same property and it was never his intention to do so.

82 As the Bank notes in its submissions, the Fuges bear the onus of proving the state of affairs as to the ownership of the sheep for which they contend. The following evidence is relied upon by the Bank as demonstrating why that onus has not been discharged:

(a) Anthony Fuge’s financial statements which disclosed that he was the owner of the sheep at all relevant times after the termination of the Partnership;

(b) Matthew Fuge’s evidence that the sheep were never included in his financial statements;

(c) a Notice to Produce was issued to the Fuges calling for production of any documents recording Matthew Fuge as the owner of any sheep and the only documents produced was a record of the Partnership owning the livestock in 2009;

(d) the evidence of Matthew Fuge that he left the care and management of the sheep to Anthony Fuge;

(e) the evidence of Mr Griffiths that Anthony Fuge represented to him that he was the owner of the sheep; and

(f) the representations made by Anthony Fuge by virtue of his financial records that he was entitled to grant a mortgage over the livestock as the sole owner.

83 The Fuges submit that contrary to the Bank’s submissions, the actual state of affairs was that the brothers were joint owners of the sheep as they had contributed equally to the cost of the purchase of the flock. This position did not change after Anthony Fuge became a sole trader. These assets were made available by Matthew Fuge for Anthony Fuge to use as a sole trader, for which Matthew Fuge charged neither rent nor another fee. The evidence relied upon to disprove the correctness of the financial records was said to be: first, the publicly listed documents relating to the livestock ownership. When the livestock’s official NSW Property Identification Code was registered with the Local Land Services, both Fuges were registered as owners. This is also said to be the case when the registration was renewed in both 2009 and 2016.

84 Secondly, the Fuges rely upon their oral evidence in respect of the ownership. Anthony Fuge’s evidence was that he could not afford to pay his brother out for the livestock, and never did. As to the financial records, Anthony Fuge agreed that where livestock were accounted for in his Financial Report for the Year Ended 30 June 2013, this related to all of the livestock on the Properties for the period identified. Anthony Fuge agreed to the proposition that this financial report was not only supposed to set out the income of the Properties, but also provide details as to the true position concerning his assets and liabilities. He said that he did not inform the accountant who prepared the report that his brother jointly-owned the sheep, and that he just kept on breeding the sheep and running the business.

85 Matthew Fuge’s evidence was that he understood Anthony Fuge had included the sheep in his own personal financial statements because he was acting as a sole trader. When asked whether Anthony Fuge was the registered owner of the sheep, Matthew Fuge answered that he owned half the sheep, save for those bought by Anthony Fuge after the termination of the Partnership. Matthew Fuge was then taken to [115] of his affidavit, where it reads: “they were not the rightful owners of the livestock; my brother was the registered owner”. In response to this, Matthew Fuge acknowledged that his brother was the registered owner, as was the Partnership.

86 Thirdly, it was submitted that in any event, Anthony Fuge held the sheep on constructive trust for Matthew Fuge.

87 There are a series of cascading issues which pervade the Fuges’ submissions as to this point. The position as to the ownership of the livestock is somewhat obscure. Before considering the strength of the arguments summarised above, it is worth identifying the supposed consequences said to flow from a finding that Matthew Fuge jointly owned the livestock. Regrettably, this is another example of legal issues being floated for the Court to work out, without being fully developed in submissions or apparently being thought through.

88 The Fuges contend that Anthony Fuge would not have had the authority to mortgage his brother’s share. Two points should be made about this chain of reasoning. First, the high point of the Fuges’ evidence is the recording of the Partnership on the LPA Register. If that were to be taken as conclusive of ownership, the lawful owner would be the Partnership itself, not the two brothers individually in equal shares. Subject to an agreement to the contrary, it is trite that one partner, acting in that capacity, is entitled to deal with the property of the Partnership. This aspect was not explored at all in the Fuges’ submissions.

89 Secondly, even if I found that Anthony Fuge had no authority to offer security over Matthew Fuge’s portion of the livestock, the Fuges’ submissions do not endeavour to explain how this would legally affect the Livestock Mortgage. It appears to me that at best, Matthew Fuge would have a claim against Anthony Fuge for conversion. No submission was made or developed as to how the Bank’s title would be defeated or impeached. There is no suggestion that the Bank was on notice as to Anthony Fuge wrongfully representing his ownership status as to the livestock, and the proposition that the Bank had some form of obligation to go beyond Anthony Fuge’s representations and check a certificate of registration, cannot be accepted. Further, given the cross-guarantees, the Fuges were jointly and severally liable for the debts in any event. It is unnecessary to say anything further on this, since the Fuges do not even reach the stage of proving joint ownership of the livestock and so the possible consequences of such a finding fall away.

90 Turning now to the submissions, it is necessary to deal with the competing evidence as to ownership. The first and most obvious issue with taking the certificate of registration at face value, is the apparent ownership of the livestock by the Partnership, despite the Partnership having been dissolved in late 2008. Putting this to one side, the certificate cannot be taken as being definitive evidence of ownership in the presence of directly contradictory evidence, being the financial records of Anthony Fuge. Despite how the submissions may attempt to colour it, an LPA certificate of registration simply does not carry with it the legal status of registration pursuant to the RPA. This is not a case of title by registration.

91 As to the financial records, at the time the reports were prepared by the accountant, Anthony Fuge understood that the reports were to set out the true position of his assets, and at no point did he inform the accountant that the livestock was not owned by him alone. No explanation whatsoever was provided by the Fuges as to the discrepancy between the asserted position and the financial records. The Fuges have not established to my satisfaction that the livestock were co-owned and, I am inclined to think the financial records, prepared by a professional accountant, probably represented the true state of affairs. As to the Fuges’ oral evidence, reviewing their evidence fairly, the Fuges seem to believe that the livestock purchased prior to the dissolution of the Partnership was never “bought out” by Anthony Fuge, and as a consequence, remains property of the Partnership. I have already explained above why a finding that the Partnership owned the property would not assist in this claim.

92 For the many reasons I have outlined, this claim must fail.

93 For completeness, I will briefly discuss the final claim made connected to this point as to lack of authority. This being the issue of non est factum. This claim was not identified within MFI 7 and despite being mentioned at various points in the Fuges’ submissions, does not appear to have been pressed in the traditional sense.

94 This common law doctrine allows a mortgage to be set aside where the mortgagor has no understanding of what they are signing: Gibbons v Wright (1954) 91 CLR 423 at 443-444. To make out this defence, the mental incapacity must be such that the mortgagor through no fault of their own, is incapable of understanding the purpose of the document. The plea of non est factum will fail where the mortgagor was capable of understanding the general purport of what they were signing – regardless of whether it was actually explained: Gibbons at 438. The alleged sequence of events here was that Mr Hewitt attended Lenborough on 25 February 2011 and simply placed a pile of documents in front of Anthony Fuge for him to sign. It is said that Mr Hewitt did not take him through the documents, nor was any legal or other independent advice or assistance provided. Anthony Fuge gave evidence that he was unaware that he was signing the Livestock Mortgage on his own account and not conditionally. He explained that he understood the sheep to have been jointly owned by Matthew and himself and he would not have signed the Livestock Mortgage if he had known his brother was not also being asked to sign it.

95 The highest this claim was put in closing submissions was that Anthony Fuge did not understand or was unaware that he was signing the Livestock Mortgage solely on his own account, and not jointly or conditionally with his brother. The Fuges’ closing submissions accept that it is possible that Anthony Fuge understood another business mortgage was required. The argument run was that had Anthony Fuge known that his brother was not going to be asked to sign the document, he never would have. The problem is that this argument presumes that Anthony Fuge understood he was signing a mortgage over the livestock. If this was the case, then the potential liability of Matthew Fuge simply cannot rise to constitute a gap in understanding so significant as to make out a claim of non est factum.

E.2 Whether Bank acted contrary to its good faith obligations pursuant to the Farm Debt Mediation Act 1994 (NSW)

E.2.1 Existence of Statutory or Contractual Good Faith Obligation

96 Although the parties disagreed as to whether there was an obligation to mediate in good faith arising under the FDMA, there is no need to tarry to deal with this issue as it is common ground that obligations arising out of the Code of Banking Practice were incorporated into the agreement between the parties and the Bank accepted, as a matter of contract, it was obliged to act in good faith in relation to the mediation. What is hotly in dispute, however, is the content of such an obligation in circumstances such as the present. It is this issue to which I now turn.

E.2.2 Content of Good Faith Obligation

97 The content of a contractual obligation to mediate in good faith is not clearly defined. It is a concept which is often more easily considered by reference to examples of what constitutes a failure to comply with such an obligation. In Aiton Australia Pty Ltd v Transfield Pty Ltd [1999] NSWSC 996; (1999) 153 FLR 236 at 268 [156] Einstein J provided a non-exhaustive analysis of what constitutes compliance with or failure to comply with an obligation to mediate in good faith:

(1) to undertake to subject oneself to the process of negotiation or mediation (which must be sufficiently precisely defined by the agreement to be certain and hence enforceable).

(2) to undertake in subjecting oneself to that process, to have an open mind in the sense of:

(a) a willingness to consider such options for the resolution of the dispute as may be propounded by the opposing party or by the mediator, as appropriate.

(b) a willingness to give consideration to putting forward options for the resolution of the dispute.

Subject only to these undertakings, the obligations of a party who contracts to negotiate or mediate in good faith, do not oblige nor require the party:

(a) to act for or on behalf of or in the interests of the other party;

(b) to act otherwise than by having regard to self-interest.

98 Given the broad and somewhat amorphous nature of such an obligation, it is unsurprising that at 269 [159], Einstein J was conscious of the difficulties in attempting to prove a breach by a party of their obligation to mediate in good faith:

That there are in certain situations clear and even grave difficulties in being able to prove the breach by a party of an obligation to negotiate or mediate in good faith, is not to be taken as meaning that those obligations lack necessary identifiable content and are therefore so uncertain as to be unenforceable in law. Certainty or uncertainty of contractual obligation is not to be measured by difficulties of proving breach of contractual obligations. The two fields of discourse ought not be collapsed.

99 The challenge in determining the specific content of a good faith obligation is limited to the specific context of mediation; the difficulty in delineating what conduct would be inconsistent with the obligation can be seen in the context of contractual negotiations more generally: see Strzelecki Holdings Pty Ltd v Cable Sands Pty Ltd [2010] WASCA 222; (2010) 41 WAR 318 at 331-32 [35] per Pullin JA and Mineralogy Pty Ltd v Sino Iron Pty Ltd (No 6) [2015] FCA 825; (2016) 329 ALR 1 at 161 [1009] per Edelman J. Whatever else is unclear, one thing is pellucid: the difficulty of attempting to provide some sort of an exhaustive definition. The case of the Fuges is that they were “railroaded” into signing the HOA at the mediation and the Bank knowingly took advantage of the Fuges’ inequality in bargaining power by forcing them to accept an agreement they neither wanted nor understood. Whatever be the precise metes and bounds of the obligation to participate in a mediation in good faith, it is a necessarily contextual question, and it is unnecessary to dwell on the boundaries further here because if the Fuges make out their “railroading” contention as outlined above, this is not a case at the margins – it would demonstrate a want of participation in the mediation by the Bank in good faith.

E.2.2 Submissions and Consideration

100 As can be seen from MFI 7, the Fuges ran several arguments attacking the legitimacy of the HOA. Why the argument was put in such a hydra-headed way is difficult to fathom. Issues 2(b)-2(e) require consideration of whether the Bank mediated in bad faith; whether the HOA is an unjust contract pursuant to either the Contracts Review Act 1980 (NSW) (CRA) or the National Credit Code (NCC); and whether entry into the HOA amounted to unconscionable conduct. In the circumstances of this case, the allegation of a want of good faith is put in a way so that it forms a component part of the broader allegation that the contract was unjust in the circumstances in which it was made. The parties proceeded on the basis that the same arguments advanced as to why there was a breach of an obligation of good faith also applied to the issues of unjust contracts and unconscionability (in the sense that a breach of the obligation would necessarily be relevant to an assessment of unjustness or unconscionable conduct: see, for example, s 9(1) of the CRA). For reasons I will explain, it is most convenient to deal with the Fuges’ arguments in this part of their case by reference to the discussion as to the applicability of statutory relief under the CRA at E.4 below.

E.3 Whether the HOA is a credit contract to which the National Credit Code applied that is unjust and an order should be made that it is invalid

101 On day 14 of the hearing, at T1239, and after more than a few exasperations on my part as to the necessity of seeking relief under the CRA and also cognate relief under other statutes, including the NCC, the following exchange occurred:

HIS HONOUR: …it seems to me, Mr King, that the Contracts Review Act – you’re not going to get relief under the other statutes if you don’t get relief under the Contracts Review Act and if you get relief under the Contracts Review Act you don’t need relief on the other statutes.

MR KING: I think that’s the way Keane J put it in Paciocco, your Honour. Yes. And Allsop J in Paciocco in the Full court made the point, with respect, but a good one, that the greater learning about this whole area of unjust contracts is, in fact, bound up in the Contracts Review Act and that’s where much of the learning is to be found, and we respectfully adopt that, and so we respectfully adopt what has fallen from your Honour - - -

(emphasis added)

102 Prior to this exchange, Mr King had explained the pleading strategy as “abundant of caution”: T518. Although s 76 of the NCC is based on the unjust provisions of the CRA, it does not exclude the operation of that Act in relation to credit contracts regulated by the NCC. Given this, and the belated narrowing of issues by Mr King, it is unnecessary to deal with the far from straightforward issue of whether the HOA is a credit contract within the meaning of the NCC. I will instead turn to considering whether the HOA is an unjust contract within the meaning of the CRA.

E.4 Whether the HOA was an unjust contract within the meaning of s 9 of the Contracts Review Act 1980 (NSW) and an order should be made that it is invalid

103 The applicable principles of the CRA were not in dispute between the parties and it is common ground its provisions apply. The question of whether the HOA is an unjust contract requires an assessment of all of the circumstances leading up to the entry into the HOA.

104 The relevant enquiries to be undertaken by the Court have been summarised by Gleeson JA in Nemeth v Australian Litigation Funders Pty Ltd [2014] NSWCA 198 at [97] (with whom Meagher and Leeming JJA agreed):

In an application for relief under s 7 of the Act, the Court undertakes a three-stage process: Perpetual Trustee Co Ltd v Khoshaba at [99], per Handley JA; at [106], per Basten JA. The first stage is to make findings of primary fact. The second stage involves a finding that the contract is or is not unjust. The third stage is the exercise of the power to grant relief under the Act which may, but need not, follow from the conclusion that a contract is unjust.

(emphasis added)

105 In his detailed discussion on the then relatively new CRA in West v AGC (Advances) Ltd (1986) 5 NSWLR 610, McHugh JA at 621 explained the different ways in which a contract might be unjust. This being because it contains “substantive injustice”, which arises “because its terms, consequences or effects are unjust”; or because of “procedural injustice”, which arises “because of the unfairness of the methods used to make it” – or both. These labels were also adopted by the Full Court in Murphy v Overton Investments Pty Limited [2002] FCAFC 129, and more recently accepted as a correct statement of principle in Paciocco v Australia and New Zealand Banking Group Limited [2015] FCAFC 50; (2015) 236 FCR 199 at 284 [348]. In the same spirit in which the entire proceeding has been conducted, the Fuges’ contentions as to injustice (outlined in the Schedule) spanned both these possible avenues, with multiple contentions advanced in both groups.

106 As to the meaning of “unjust”, the CRA defines the term, non-exhaustively, in s 4, to include “unconscionable, harsh or oppressive”: Kowalczuk v Accom Finance Pty Ltd [2008] NSWCA 343; (2008) 77 NSWLR 205 at 221 [70] per Campbell JA with whom Hodgson and McColl JJA agreed; Perpetual Trustee Co Ltd v Khoshaba [2006] NSWCA 41; 14 BPR 26,639 at 26,658 [114] per Basten JA). Having noted this, it is important to bear in mind that “unjust” has a lower moral threshold than “unconscionable”: Paciocco at 286 [356] citing Attorney-General (NSW) v World Best Holdings Ltd [2005] NSWCA 261; (2005) 63 NSWLR 557 (Spigelman CJ).

107 Sub-section 9(1) provides that in determining whether a contract or a provision of a contract is unjust, the Court shall have regard to the public interest and to all the circumstances of the case, including such consequences or results as those arising in the event of: (a) compliance with any or all of the provisions of the contract; or (b) non-compliance with, or contravention of, any or all of the provisions of the contract. Sub-section 9(2) then outlines a number of specific matters which should be taken into account to the extent they are relevant. In effect, the court is required to undertake a “normative evaluation of the totality of relevant circumstances”: Nemeth at [96]. While Mason P referred to this exercise as “the unjustness calculus”: St George Bank Ltd v Trimarchi [2004] NSWCA 120 at [36], others have avoided this expression because it suggests that the exercise is mechanistic rather than being largely impressionistic and evaluative: see Khoshaba at [101] (Handley JA), [112] (Basten JA).

108 When it comes to determining whether the court should exercise its discretion to grant relief, regard may be had to the conduct of the parties to the proceedings in relation to the performance of the contract after it was made: s 9(5). Section 7 of the CRA then provides for the various ways in which the court may grant relief if it considers it just to do so.

109 Throughout the hearing, counsel for the Fuges raised a number of different reasons as to why the HOA was unjust. To ensure that I could be satisfied all of the Fuges’ various complaints as to the mediation and the HOA were taken into account, on day 12 of the hearing, the parties agreed to an exhaustive list of reasons as to why the Fuges say the mediation was conducted in bad faith, why the HOA is an unjust contract, and why entry into the HOA amounted to unconscionable conduct. This list became the Schedule to MFI 7, and issues 2(b), 2(c), 2(d) and 2(e) are to be considered with regard only to this schedule.

110 It is necessary to set the Schedule out in its entirety:

1. The substantive unfairness (CS [22]) comprises:

a. The Bank’s uncompromising irrefragable debt claim of $2,247,680.83.

b. The impossibly tight marketing schedule for the [Properties] imposed by the HOA.

c. The disproportionality inherent in the triggers for judgment, vacant possession and sale by the mortgagee imposed by the HOA.

2. The procedural unfairness (CS [23]) comprises:

a. bad faith conduct prior to and at the mediation by the Bank’s officers and legal representative comprising (CS [114]-[115]):

(i) in the lead-up to the mediation by:

I requiring Matthew Fuge to use an agent if he could not attend personally. This made him take desperate measures;

II communicating unilaterally with the Mediator on 16 July 2014 without copying in Stephen Jay or the Fuges. This meant that the Fuges had no opportunity to consider the 16 July 2014 version in advance.

III presenting a draft HOA the essence of which the Bank never compromised.

IV failing to postpone the Farm Debt Mediation upon Matthew Fuge telling it that he had not slept without verifying that he was impaired from participating.

(ii) at the mediation by:

I conducting the mediation with an incompetent and unqualified representative for the Fuges and knowing that one Fuge [Matthew] was impaired and the other [Anthony] did not have his glasses so could not read the Draft HOA.

II refusing to compromise a single cent.

III assuming, incorrectly, that no financier would facilitate a refinance, and killing off immediately any possibility of refinance.

IV imposing an impossible timetable to sell the [Properties], leading to inevitable default.

V imposing fortnightly notification conditions, which were impossible to meet.

b. The incompetence of Mr [Stephen Jay], the Fuges’ representative.

c. Fatal defects in the Sections 8 and 11 Notices.

d. In contravention of Farm Debt Mediation Act 1994 (NSW) s 11AA failing to conduct the required discussion and to personally prepare the heads of agreement, and instead permitting an amended version of a previous draft prepared by the Bank’s solicitors to be used as a final version.

111 It is clear from the closing submissions of both parties that they proceeded on the basis that the same arguments as to the Schedule applied in relation to all of issues 2(b)-2(d) of MFI 7 and for the reasons I have identified above it is therefore convenient to deal with all relevant arguments raised by reference to the CRA.

112 It is unnecessary for me to expand upon the Fuges’ submissions as to the points in the Schedule in any greater detail for present purposes. It is clear to me that the contentions as to substantive unfairness have more substance than those as to procedural unfairness. For that reason, I will begin by dealing briefly with the latter category.

E.4.3 Procedural Injustice – Stage One Findings